Bajaj Finance: India's Lending Machine

I. Introduction & Episode Roadmap

Picture this: A company that started as a small two-wheeler financing arm in 1987 now touches the financial lives of over 100 million Indians—nearly one in every fourteen citizens. It has a customer base of 101.82 million and holds assets under management worth ₹416,743 crore (US$49 billion), as of March 2025. This is Bajaj Finance Limited, India's most valuable non-banking financial company (NBFC), a lending juggernaut that has fundamentally reshaped how Indians consume, borrow, and dream.

The numbers tell a remarkable story: Mkt Cap: 5,44,775 Crore (up 32.1% in 1 year), making it more valuable than several established banks. But here's the fascinating question that drives our exploration today: How did a captive finance unit of a scooter manufacturer become India's most formidable consumer lending machine, competing head-to-head with century-old banks while navigating regulatory minefields and fintech disruption?

This is a story of transformation at multiple levels—from product company to financial powerhouse, from physical branches to digital dominance, from single-product lender to lifestyle financier. It's about how Bajaj Finance cracked the code of lending to India's aspirational middle class, built a data moat that rivals tech giants, and created a cross-selling engine that would make any Silicon Valley company envious.

We'll trace the journey from Jamnalal Bajaj's founding vision through the scooter empire that defined middle-class mobility, to today's omnichannel financial services behemoth. We'll examine how Rajeev Jain's strategic playbook transformed a sleepy auto finance company into a fintech before fintech was cool. We'll dissect the NBFC model's advantages and vulnerabilities, analyze how the company survived multiple crises from IL&FS to COVID, and understand why it trades at premium valuations despite regulatory headwinds.

Most importantly, we'll extract timeless lessons about building in regulated industries, creating network effects in financial services, and the art of risk management at scale. Whether you're a founder, investor, or simply curious about India's financial transformation, this deep dive into Bajaj Finance offers insights into building enduring value in one of the world's most complex markets.

II. The Bajaj Empire & Origins

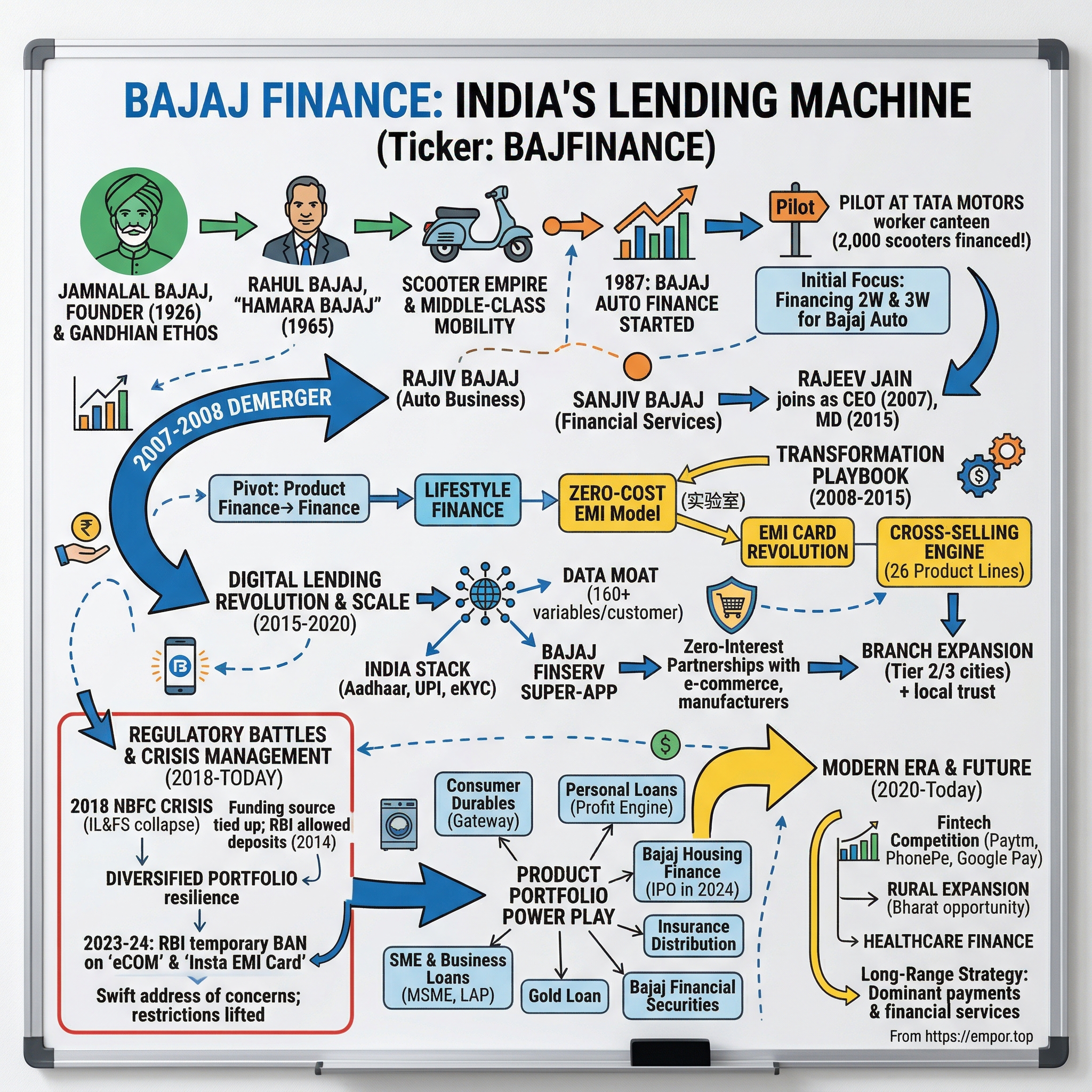

The Bajaj story begins not in boardrooms or factories, but in the crucible of India's independence movement. A rich merchant of Wardha, Seth Bachhraj and his wife later adopted him as their grandson. Under the guidance of Seth Bachhraj, Jamnalal Bajaj got involved in the family business and acquired the know-how of being a tradesman- keeping strict accounts and buying and selling commodities- excelling in his work. In 1926 he founded what would become the Bajaj group of industries.

Jamnalal Bajaj wasn't just a businessman—he was Gandhi's fifth son, as the Mahatma himself called him. This connection to India's freedom struggle would embed a certain ethos in the Bajaj DNA: business as nation-building, capitalism with conscience. When Jamnalal established Bajaj Auto in 1945, just two years before independence, it was with the vision of putting India on wheels—affordable, reliable wheels that could navigate both urban streets and rural paths.

The real transformation came under Rahul Bajaj, who took the reins in 1965 at age 27. This was License Raj India, where producing a scooter required government permission, importing technology needed bureaucratic approval, and waiting lists for Bajaj scooters stretched to years. Rahul Bajaj didn't just navigate this system—he conquered it. The Bajaj Chetak became more than a scooter; it became a symbol of middle-class arrival. "Hamara Bajaj" wasn't just an advertising tagline—it was a cultural phenomenon that captured the aspirations of a nation finding its economic feet.

By the 1990s, Bajaj Auto was synonymous with two-wheelers in India. The company had mastered the art of producing reliable, affordable vehicles for the masses. But Rahul Bajaj saw the writing on the wall: liberalization was opening India to global competition, consumer finance was becoming crucial for growth, and the future belonged to those who could facilitate consumption, not just production.

The strategic seeds of financial services were planted early. Rahul Bajaj liked the idea and needed some validation before making an important decision that could disrupt the NBFC space in India. Like a startup, a pilot was run to test the idea. A three-day financing camp was set up at Tata Motors' worker canteen, where they sold 2,000 scooters on auto finance from Citibank! There could not be a better validation of a product market fit. Rahul Bajaj was not going to miss this. So, in 1987, he decided to start Bajaj Auto Finance to provide financial services and lending solutions. Initially, it focused on financing the purchase of 2W and 3W manufactured by Bajaj Auto. This move aimed to make it easier for customers to purchase Bajaj vehicles, thereby boosting sales and customer loyalty.

The 2007-2008 demerger was a watershed moment, orchestrated with the precision of a master chess player thinking several moves ahead. Luckily, the demerger at Bajaj had just happened with Rahul Bajaj carving out the group's businesses among his two sons - older son Rajiv got the auto business, while younger son Sanjiv was handed over the financial services division. The new holding company Bajaj Holdings and Investment Ltd has 31.49 per cent in auto major Bajaj Auto Ltd and 39.16 percent in financial services arm Bajaj Finserv Ltd, which in turn has 74 per cent each in two insurance ventures and 57.53 per cent in Jain managed Bajaj Finance Ltd.

This wasn't just corporate restructuring—it was strategic positioning for different futures. Rajiv would focus on competing globally in automobiles, while Sanjiv would build the financial services empire. The split recognized a fundamental truth: manufacturing and financial services require different DNAs, different risk appetites, and different growth strategies.

Sanjiv Bajaj, armed with an MBA from Harvard Business School, brought a different vision. Where his father had built physical products, Sanjiv would build financial products. Where Bajaj Auto had provided mobility, Bajaj Finance would provide liquidity. The transition from making scooters to making loans might seem like a leap, but it was actually a natural evolution—both businesses were fundamentally about enabling Indian aspirations.

The genius of the demerger became apparent over time. While Bajaj Auto battled global giants like Honda and faced the commoditization of two-wheelers, Bajaj Finance had the freedom to innovate in financial services without the baggage of manufacturing legacy. It could be agile, digital-first, and customer-obsessed in ways that a traditional manufacturing company couldn't.

The cultural DNA transfer was crucial. From Bajaj Auto, the financial services arm inherited deep distribution knowledge, understanding of middle-class India, and most importantly, brand trust built over generations. When a Bajaj Finance representative knocked on doors in small-town India, they carried sixty years of goodwill. This trust, impossible to buy or build quickly, would prove invaluable in the lending business where credibility is currency.

By 2008, the stage was set. The old Bajaj—maker of scooters, symbol of socialist India—had split into focused entities ready for capitalist India's consumption boom. Bajaj Finance, freed from its manufacturing parent, was ready to reimagine itself not as a captive finance company but as India's lending machine. The empire had divided to conquer.

III. The Captive Finance Beginning (1987–2007)

The early years of Bajaj Auto Finance were unglamorous, almost deliberately so. Originally incorporated as Bajaj Auto Finance Limited on 25 March 1987, as a non-banking financial company, primarily focused on providing two and three-wheeler finance. After 11 years in the auto finance market, Bajaj Auto Finance Ltd launched its initial public issue of equity share and was listed on the Bombay Stock Exchange and National Stock Exchange of India.

This wasn't Silicon Valley-style disruption—it was patient, methodical foundation-building in the unsexy world of hire-purchase agreements and hypothecation documents.

In 1987, when Bajaj Auto Finance was born, India's financial landscape was radically different. Banks were government-owned behemoths focused on priority sector lending. Credit cards were for the ultra-elite. Personal loans required knowing someone who knew someone. The vast middle class—teachers, small businessmen, government employees—were essentially unbanked for consumption needs. They could save in banks but couldn't borrow for aspirations.

The initial model was simple: sit inside Bajaj Auto dealerships, finance Bajaj vehicles, collect EMIs. The company was essentially a facilitator, greasing the wheels of Bajaj Auto's sales machine. But this simplicity masked sophisticated execution. Building a collections infrastructure in pre-digital India meant feet on streets, relationships with local strongmen, and deep understanding of cash flow patterns in different occupations and geographies.

At the turn of the 20th century, the company ventured into the consumer durables finance sector and started offering small-size loans. This was the first strategic expansion beyond captive auto finance. The insight was profound: Indians would buy refrigerators, televisions, and washing machines on EMI just like they bought scooters, if someone made it easy enough.

The consumer durables financing business became Bajaj Finance's laboratory for innovation. They pioneered what would later become the "zero-cost EMI" model—though technically no EMI is zero-cost, the perception mattered. By working with manufacturers and retailers to subsidize interest costs, they made the monthly payment the only number that mattered to consumers. A ₹30,000 television became ₹2,500 per month for twelve months. Middle-class Indians could finally afford to aspire.

Building the dealer network was painstaking work. Each electronics retailer, each mobile phone shop, each furniture store had to be evangelized. The Bajaj Finance representative became a fixture at these stores, processing applications, explaining terms, collecting documents. This wasn't tech-enabled disruption—this was old-fashioned relationship building, trust creation through repetition and reliability.

The risk management in these early years was primitive by today's standards but effective for its time. Credit decisions were based on simple heuristics: stable employment, local residence, family guarantors. The company learned through trial and error which occupations defaulted more, which cities had better payment culture, which products saw higher delinquencies. Every default was a data point, every successful collection a validation of method.

Pre-2008 India offered unique opportunities for NBFCs. The Non-Banking Financial Companies (NBFCs) are quasi-banking institutions in India. They are allowed to make loans just like banks do. However, they are not allowed to take deposits from people in order to make these loans. Hence, these Non-Banking Financial Companies (NBFCs) borrow money from the bond market in order to make loans. Banks were constrained by priority sector requirements, government mandates, and bureaucratic decision-making. NBFCs could move fast, take risks, and serve segments banks wouldn't touch.

The business that Jain inherited was nothing but a captive kind of finance company with 85 per cent of the revenues coming from auto financing - the balance 15 per cent was consumer durables and personal computers. The asset quality was very poor at 10 per cent gross NPAs. This was the reality of the business in 2007—successful by some metrics but fundamentally limited, a captive finance company that hadn't yet discovered its true potential.

The decision to go beyond auto financing wasn't sudden but evolutionary. Each new product category—two-wheelers to consumer electronics to personal computers—taught valuable lessons. How to assess risk in different asset classes. How to collect in different geographies. How to partner with different types of merchants. The company was unknowingly building capabilities that would prove crucial in its transformation phase.

By 2007, Bajaj Auto Finance had achieved modest success: a loan book in the thousands of crores, presence across India, profitable operations. But it was still fundamentally a single-product company in a multi-product world, a physical company in an increasingly digital age, a facilitator when it could be a principal. The stage was set for radical transformation, waiting for a leader who could see beyond the constraints of captive finance to the possibilities of lifestyle finance.

The unglamorous years weren't wasted years. They were the foundation, the patient accumulation of trust, knowledge, and capability that would enable explosive growth. Every loan officer trained, every collection process refined, every dealer relationship built—these would compound when the company found its true calling. The captive finance beginning was ending, but its lessons would echo through everything that came next.

IV. The Transformation: Rajeev Jain's Playbook (2008–2015)

Rajeev joined the Bajaj Finserv Group in 2007 as the Chief Executive Officer of Bajaj Finance Ltd and became the Managing Director in 2015. His leadership has enabled Bajaj Finance to transform itself from a captive single-product auto finance company to an omnipresent and technology-driven agile financial powerhouse, offering the entire spectrum of loan products, payments and investments to consumers and businesses.

The transformation of Bajaj Finance under Rajeev Jain wasn't just a business turnaround—it was a complete reimagination of what an NBFC could be in India.

Jain didn't come from traditional banking. Prior to that, Rajeev worked as Business Development Manager with GE Capital for about 4.5 years and was amongst the first 10 employees at GE Money, India. He started his career in 1993 with Eicher as a management trainee. His experience at GE Capital and AIG had taught him that consumer finance in India was ripe for disruption. Prior to Bajaj Finance, Rajeev worked with GE, American Express and the American International Group (AIG), serving in various senior leadership roles. As Deputy CEO of the consumer lending business at AIG, Rajeev built the strategic framework for AIG Consumer business's foray into India.

When Jain took charge, he inherited a business with serious problems but also hidden strengths. The problems were obvious: concentrated revenue streams, poor asset quality, limited product portfolio. The strengths were less visible but more valuable: the Bajaj brand, distribution relationships, and two decades of lending experience. Jain's genius was seeing how to leverage the strengths while fixing the problems.

The strategic pivot from product finance to lifestyle finance was profound. Instead of thinking "what products can we finance?", Jain asked "what lifestyle needs can we fulfill?" This reframing changed everything. Suddenly, Bajaj Finance wasn't competing with other auto financiers—it was competing with banks, credit card companies, even informal moneylenders. The addressable market expanded from millions to hundreds of millions.

Jain, who generally starts his day at 7 am, has played a key role in making the company's zero-interest, consumer durables financing product—now known as 'Buy now, pay later'—a big hit, so big that it was instantly replicated by competitors, including high street banks. The EMI card revolution was Jain's masterstroke, launched before anyone truly understood its potential. This wasn't just a credit card—it was a consumption enabler designed for an India that didn't trust credit cards but understood EMIs.

The EMI card solved multiple problems elegantly. For consumers, it provided credit without the fear of spiraling debt that credit cards carried. For merchants, it increased ticket sizes and conversion rates. For Bajaj Finance, it created a recurring relationship with customers rather than one-time transactions. EMI Network Card comes with a pre-approved loan of up to Rs.4 lakh that customers can use across any of Bajaj Finserv's 60,000+ partner stores in more than 1,300 cities. It comes with features like flexible tenors ranging from 3 – 24 months, nil foreclosure charges, and one time document submission to allow shopping favourite products on EMI from top e-commerce platforms.

The cross-selling engine that Jain built was unprecedented in Indian finance. Since inception, the Company has leveraged technology to launch 26 product lines and 51 product variants for retail, MSME and commercial consumers, with major product innovations such as the EMI card and Flexi. The goal wasn't just to acquire customers but to own their financial lives. Start with financing a mobile phone, then offer a personal loan, then a credit card, then insurance. The metrics became religious: products per customer, lifetime value, cross-sell ratios.

Under his leadership, Bajaj Finance Limited has delivered a 14-year 51% CAGR growth of Profit and an asset growth of 37% CAGR. Barring the pandemic year 2021, Return on Equity has been averaging over 20% in last 10 years. These aren't just good numbers—they're exceptional by any global standard, sustained over a period when India saw demonetization, GST implementation, IL&FS crisis, and COVID.

The branch expansion strategy was counterintuitive in an increasingly digital world. While fintech startups preached digital-only models, Jain was opening physical branches in Tier 2 and Tier 3 cities. But these weren't traditional bank branches—they were customer acquisition machines, local trust centers, problem resolution hubs. The physical presence created comfort for customers taking their first formal loans, while digital channels handled the volume transactions.

Technology investment during this period was massive but pragmatic. Jain didn't try to build a technology company—he built a lending company powered by technology. Every process was digitized not for the sake of digitization but for speed, scale, and risk management. Loan approvals that took days now took hours, then minutes. Document collection went from physical to digital. Risk models evolved from simple scorecards to sophisticated algorithms.

On the second, the leadership understood that Indian banking's lending was guided by biased reasons and perceived flaws. Notably, there was a significant trust deficit towards self-employed borrowers, with a strong preference for the salaried class. Moreover, retail underwriting decisions primarily relied on CIBIL data as the metric of creditworthiness. Bajaj Finance realised the need for a nuanced approach to identify high-quality borrower classes that had previously been overlooked.

The risk management philosophy Jain instituted was sophisticated yet practical. Instead of avoiding risk, the company priced for it. Higher risk segments got loans but at higher rates. The portfolio was diversified across products, geographies, and customer segments. No single segment could bring down the company. This diversification would prove crucial during crisis periods.

Partly, the experience and wisdom of two stalwarts— the late Rahul Bajaj and ex-Citibanker Nanoo Pamnani—helped the company, but it was Jain's execution skills, which he honed in multinational firms like GE, American Express and AIG, that drove the product's strategy. "Once a broader strategy is in place, he rolls up his sleeves to do the job," says a professional who worked with Jain earlier.

The cultural transformation was as important as strategic changes. Jain built a performance-driven culture unusual in traditional Indian companies. Promotions were merit-based, compensation was competitive, and entrepreneurship was encouraged. The company began attracting talent from banks, consulting firms, and technology companies—people who wouldn't have considered an NBFC career earlier.

Customer obsession became religion. Every product launch, every process change, every technology investment was evaluated on customer impact. The company pioneered doorstep service for documentation, instant approvals for existing customers, and flexible repayment options. These might seem standard now, but they were revolutionary in Indian lending circa 2010.

By 2015, the transformation was complete. Bajaj Finance Limited Transformed the company from 2500 Crores to a 21000 Crores high growth company in a span of 6.5 years. The company is a diversified financial services company with presence across consumer, SME and Commerical business with a market capitalisation of USD 1.1 Billion currently. The company was no longer a captive auto financier but India's leading consumption financier. The playbook was proven: customer acquisition through easy entry products, cross-selling through data and relationships, risk management through diversification and pricing, growth through technology and distribution.

V. The Digital Lending Revolution & Scale (2015–2020)

The period from 2015 to 2020 marked Bajaj Finance's transition from a traditional NBFC with digital capabilities to a digital-first lender with physical presence. This wasn't just digitization—it was complete reimagination of lending in the age of smartphones and India Stack.

India Stack—the combination of Aadhaar, UPI, and eKYC—was a game-changer that Bajaj Finance embraced faster and more comprehensively than competitors. While banks struggled with legacy systems and startups lacked lending experience, Bajaj Finance had the perfect combination: lending expertise, risk management capability, and agility to adopt new technology.

The Aadhaar opportunity was transformative. Additionally, by 2020, it had started using data analytics and big data tools. Customer onboarding that once took days with physical document verification could now happen in minutes. KYC became eKYC. Physical signatures became digital signatures. The friction in customer acquisition dropped dramatically, enabling scale previously impossible.

Building the app ecosystem wasn't just about having a mobile app—it was about reimagining the entire customer journey for mobile-first India. The Bajaj Finserv app became a super-app before super-apps were trendy, combining lending, insurance, investments, and shopping in one interface. By 2020, 60% of Bajaj Finance's workload was on cloud and originally, they aimed to create a super-app for existing customers, but due to COVID-19 pandemic in India, they expanded the plan to encompass various services by integrating five proprietary marketplaces within their ecosystem—EMI store, insurance,

The data moat Bajaj Finance built during this period was extraordinary. With millions of customers across multiple products, the company accumulated unprecedented insights into Indian consumer behavior. 160+ variables per customer wasn't just a number—it represented deep understanding of spending patterns, repayment behavior, life events, and credit needs. This data advantage created a virtuous cycle: better data led to better risk assessment, which led to better pricing, which led to more customers, which led to more data.

Risk management through economic cycles became sophisticated. The company had survived demonetization in 2016—a sudden shock that temporarily disrupted cash-based repayments. The learnings were invaluable: how to quickly adapt collection strategies, how to provide customer relief without destroying portfolio quality, how to maintain growth while managing risk. These lessons would prove crucial during COVID.

The zero-interest EMI partnerships expanded aggressively during this period. E-commerce: : Bajaj Finserv has partnered with the leading e-commerce platforms to offer all products on EMIs. EMI Network Card allows purchasing products and get benefits such as loans with zero down payment, convenient repayment tenor of up to 12 months By partnering with e-commerce platforms, smartphone manufacturers, and consumer brands, Bajaj Finance embedded itself into the purchase journey. The company wasn't just a lender—it was a sales enabler, marketing partner, and conversion optimizer for merchants.

The merchant ecosystem became a moat. With tens of thousands of merchant partners, Bajaj Finance had distribution that no digital-only player could match quickly. Each merchant relationship was carefully cultivated—training their staff, integrating with their systems, solving their working capital needs. This wasn't just B2C lending—it was B2B2C, where the B2B relationship enabled the B2C opportunity.

Competing with banks while being an NBFC required strategic positioning. Banks had cheaper funding costs and regulatory advantages. But Bajaj Finance had speed, flexibility, and customer focus. Where banks took weeks for loan approval, Bajaj Finance took minutes. Where banks required branch visits, Bajaj Finance came to doorsteps. Where banks had rigid products, Bajaj Finance offered customization.

The scale achieved during this period was staggering. Customer base grew from millions to tens of millions. Product lines expanded from basic loans to sophisticated financial solutions. Geographic presence extended from urban centers to rural markets. Over 17 years, Bajaj Finance has enabled India's growing mass affluent and middle-class population to fulfil aspirations by providing access to an extensive range of financial solutions.

Digital acquisition engines became increasingly sophisticated. The company mastered performance marketing, SEO, app store optimization, and social media marketing. But digital acquisition was married with physical activation—customers acquired online were serviced offline when needed, creating an omnichannel experience before omnichannel became buzzword.

The innovation in products continued relentlessly. Flexi loans that allowed borrowers to pay only interest initially. Doctor loans tailored for medical professionals. Business loans based on GST returns. Each product was designed for specific segments with specific needs, moving away from one-size-fits-all lending that characterized traditional banking.

Under his strategic direction, Bajaj Finance has brought millions of new-to-credit consumers into the formal financial system, empowering them with finance for life's everyday needs. This wasn't just business growth—it was financial inclusion at scale. Millions of Indians got their first formal loans from Bajaj Finance, building credit histories that would enable future financial access.

Technology infrastructure investments during this period were massive. Cloud adoption, API-first architecture, microservices, real-time decisioning engines—the company was building technology infrastructure that could handle not just current scale but 10x future scale. By 2015, BFL had set up a series of Disaster Recovery (DR) data centers for business continuity.

The regulatory navigation during this period was masterful. As NBFCs came under increased scrutiny post IL&FS crisis, Bajaj Finance proactively strengthened compliance, improved disclosures, and maintained conservative leverage ratios. The company understood that regulatory trust was as important as customer trust for long-term success.

By 2020, Bajaj Finance had achieved what seemed impossible five years earlier: it had become India's most valuable NBFC, competing effectively with banks many times its size, while maintaining growth rates typical of startups. The digital revolution wasn't just adopted—it was mastered and integrated into a unique model that combined digital efficiency with human touch, scale with personalization, growth with risk management.

VI. Regulatory Battles & Crisis Management

The true test of a financial institution isn't how it performs in good times but how it survives crises. Between 2018 and 2024, Bajaj Finance faced a series of existential challenges that would have destroyed weaker companies. The navigation through these crises revealed both the strength of the business model and the sophistication of management.

The 2018 NBFC crisis began with IL&FS but threatened to engulf the entire sector. It all began in September 2018, when financing behemoth Infrastructure Leasing & Financial Services (IL&FS) collapsed. Here's a timeline of what went wrong for India's NBFCs: IL&FS, a leading NBFC in India, defaulted around September 2018, followed by the DHFL crisis in less than a year. These twin shocks to the banking system dried up the funding opportunities for NBFCs.

The IL&FS collapse wasn't just another corporate failure—it was a systemic shock that questioned the entire NBFC model. The demise of IL&FS four years ago was one of the most significant financial crises that impacted a major conglomerate, seizing the financial system and exhausting liquidity. The debt involved was over Rs 1 lakh crore, of which only Rs 55,000 crore was addressed, leaving approximately 62% unresolved.

For most NBFCs, the crisis was existential. They have been borrowing money short term and have been lending it out long term. This asset liability timing mismatch is obviously a recipe for disaster. However, the NBFCs have been able to roll it over and pay their debts when due. This is the reason the Non-Banking Financial Companies (NBFCs) were able to function without too many problems.

But Bajaj Finance had built differently. However, Bajaj Finance had no issues during this period as its funding source was already tied up. In 2014, RBI allowed Bajaj Finance to take deposits from the public. This meant that Bajaj Fin already had access to public deposits at a significantly lower interest cost. This deposit-taking capability, rare among NBFCs, provided funding stability when wholesale markets froze.

Between Sept. 21 and 24, large NBFCs like Housing Development and Finance Corporation (HDFC) and Bajaj Finance's market cap erodes by around Rs18,600 crore and Rs13,800 crore, respectively. The market panic was real, but Bajaj Finance's response was measured. Instead of retrenching, the company used the crisis to gain market share from weaker competitors who were forced to stop lending.

Additionally, the organisational structure ensured Bajaj Finance had limited exposure to high risk. The diversified portfolio across products and segments meant no single asset class could bring down the company. While real estate-focused NBFCs collapsed, Bajaj Finance's consumer-focused portfolio remained resilient.

The RBI's evolving stance on NBFCs created both challenges and opportunities. In September 2022, the RBI included Bajaj Finance as one of the 16 NBFCs that are part of the NBFC-Upper Layer list. This means that the RBI has requested that the company must develop and implement a board-approved policy for the adoption of the more stringent regulatory framework that is applicable to it. Being classified in the upper layer meant bank-like regulations but also signaled systemic importance.

The personal loan caps and regulatory tightening of 2023-24 were particularly challenging. In November 2023, RBI banned the company from approving or distributing loans through two of its lending services, namely 'eCOM' and 'Insta EMI Card'. The ban was a shock—Bajaj Finance had never faced such direct regulatory action.

This action was taken because Bajaj Finance allegedly violated the RBI's digital lending guidelines. The central bank's digital lending guidelines, enforced last year, require that a lender disclose all fees and charges to borrowers upfront and also detail its recovery practices in the event of a default. The issue wasn't predatory lending but technical compliance—the company hadn't provided adequate Key Fact Statements (KFS) to borrowers.

The response was swift and comprehensive. On May 2nd, 2024, Bajaj Finance announced that the RBI had lifted the restrictions on their Insta EMI Card and eCOM platform. This suggests that Bajaj Finance has addressed the concerns raised by the RBI. Within six months, the company had revamped its disclosure processes, enhanced customer communication, and satisfied regulatory requirements.

Managing NPAs through demonetization and COVID required different strategies. Demonetization in 2016 was a temporary liquidity shock—customers had intent to pay but not means. The company provided short-term relief while maintaining collection intensity. COVID was different—both intent and means were affected. The response was nuanced: moratoriums for genuinely affected customers, restructuring for viable but stressed accounts, aggressive collection for willful defaulters.

Bajaj Finance in a statement said net loan losses and provisions for Q2FY25 were Rs 1,909 crore, up from Rs 1,077 crore in Q2FY24. Loan losses and provisions remained elevated in Q2. This increase was across all retail and SME lines of businesses. Company continues to take risk actions by cutting segments and pruning exposures. The recent increase in provisions shows the company's conservative approach—recognizing problems early and providing adequately rather than hiding stress.

The regulatory tightening around digital lending created new compliance burdens. On May 8, 2025, the Reserve Bank of India ("RBI") issued the RBI (Digital Lending) Directions, 2025, ("2025 Directions") which consolidate and replace earlier frameworks, including the 2022 Guidelines on Digital Lending ("2022 Guidelines") and the 2023 Guidelines on Default Loss Guarantee ("2023 DLG Guidelines"). The 2025 Directions introduce key clarifications and significant changes to strengthen India's the digital lending framework.

The management of regulatory relationships became as important as customer relationships. Regular engagement with RBI, proactive compliance, transparent reporting—these became organizational priorities. The company learned that regulatory trust, once lost, is harder to rebuild than customer trust.

The Reserve Bank of India (RBI) has taken some steps to prevent the conversion of this Non-Banking Financial Companies (NBFCs) crisis into a full-fledged financial crisis. The RBI has changed its rules in order to make it easier for Non-Banking Financial Companies (NBFCs) to obtain capital. Banks were earlier restricted in the number of loans they could make to NBFCs. Banks were earlier allowed to lend a maximum of 10% of their loans to NBFCs. This limit has been temporarily raised to 15% for a few months. The immediate effect of this step has been to release close to $10 billion worth of liquidity to the cash-starved NBFC sector.

Through each crisis, Bajaj Finance demonstrated antifragility—getting stronger through stress rather than just surviving. Market share increased during industry downturns. Customer trust deepened through transparent communication during difficult times. Regulatory relationships strengthened through proactive engagement. The company emerged from each crisis not just intact but improved—with better risk management, stronger compliance, deeper customer relationships.

VII. The Product Portfolio Power Play

The evolution of Bajaj Finance's product portfolio is a masterclass in market expansion, customer lifecycle management, and cross-selling excellence. Each product wasn't just a revenue line—it was a customer acquisition tool, a cross-selling opportunity, and a data collection mechanism.

Consumer durables financing remained the gateway drug into the Bajaj Finance ecosystem. Retail EMI: Retail EMI option offers easy financing on electronics & home appliances like smartphone, tv, washing machine, air conditioner, laptop, air cooler etc, furniture, lifecare service, groceries, clothes, accessories and more. No hidden charges, simply divide the cost of the purchase into easy instalments. This can be availed through across the retail network of Bajaj Finance Ltd. The brilliance wasn't in the product itself but in its role as customer acquisition tool. Finance a ₹30,000 phone for a 25-year-old, and you've potentially acquired a customer for life.

Personal loans became the profit engine. Personal Loan: Borrow up to Rs 25 lakh collateral free Personal Loan by just meeting simple eligibility criteria and submitting basic documents. Once customers experienced the ease of Bajaj Finance's consumer durable loans, personal loans were natural next step. No collateral, minimal documentation, instant approval for existing customers—the friction was systematically removed.

The expansion into SME and business loans marked strategic evolution. In January 2023, Bajaj Finance launched its loan against property (LAP) business for micro, small, and medium-sized enterprise (MSME) customers. As of December 2024, mortgages currently make up 31% of its consolidated AUM, while SME lending accounts for 14% and commercial lending for 13%. This wasn't just portfolio diversification—it was recognition that small businesses and self-employed individuals were underserved by traditional banks.

The credit card business represented direct competition with banks. In the past, Bajaj Finance had been working with RBL Bank and DBS Bank to issue co-branded credit cards. But, in early December 2024, the company ended its partnerships due to new Reserve Bank of India rules restricting the role of non-banking partners in such agreements. However, in early 2025, the company re-entered the same space by partnering with Bharti Airtel to launch a co-branded insta EMI card. The regulatory challenges didn't deter the company—it found new ways to participate in the lucrative credit card market.

Insurance distribution became a significant fee income generator. By leveraging its customer base and distribution network, Bajaj Finance became one of India's largest insurance distributors without taking insurance risk. Every loan customer was potential insurance customer. Every branch was insurance sales point. Every customer interaction was insurance opportunity.

Bajaj Housing Finance, as a wholly owned subsidiary of Bajaj Finance, provides various housing finance products, including home loans, loans against property, and lease rental discounting, among others. In June 2024, it has filed its DRHP with Securities and Exchange Board of India for a ₹7,000 crore (US$830 million) initial public offering, including a ₹4,000 crore (US$470 million) crore fresh share sale and a ₹3,000 crore (US$350 million) offer-for-sale by parent company, Bajaj Finance. The housing finance subsidiary represented long-term strategic positioning in India's under-penetrated mortgage market.

Gold Loan: A loan offered against the gold customers own, gold loan helps customers meet their financial needs with a high loan limit of Rs. 2 crs, at attractive interest rates, with flexible repayment option and no charges on part-prepayment or foreclosure to make the loan affordable. Gold loans tapped into India's cultural affinity for gold while providing secured lending opportunities with lower risk.

The art of cross-selling at Bajaj Finance was scientific. To grow BFL share of customer's wallet by offering all products and services in a frictionless manner and deliver highest Customer Satisfaction (CSAT) score and Products Per Customer (PPC). Customer data was analyzed to identify next best product. Life events triggered loan offers. Repayment behavior determined credit line increases. The goal was simple: own the customer's financial life.

Product innovation continued relentlessly. Flexi loans for businesses allowing interest-only payments initially. Education loans with moratorium periods. Doctor loans with higher limits recognizing earning potential. Each product was designed for specific segments with specific needs, moving away from generic lending products.

Retailer Finance: An exclusive finance option for the retail partners, it will help them avail finance for acquiring inventory from the manufacturers. The retailers are assigned a pre-approved credit line which they can use any time they want and are the first time ever that non-collateral based financing option has been introduced for the retailers. B2B lending products created ecosystem lock-in—retailers dependent on Bajaj Finance for inventory funding were natural partners for consumer financing.

The fee income streams from insurance, mutual fund distribution, and payment services reduced dependence on interest income. This wasn't just revenue diversification—it was margin expansion, as fee income had minimal capital requirements compared to lending.

Bajaj Financial Securities Ltd. ('BFinsec'), which is registered with the Securities and Exchange Board of India (SEBI) as a Stock Broker and Depository Participants. The securities business represented adjacency expansion—wealthy customers needed investment services beyond lending products.

Customer lifecycle management became sophisticated. Young professionals started with consumer durable loans, graduated to personal loans, took home loans when married, business loans when entrepreneurial, and eventually wealth management services. Each life stage had corresponding products, creating 20-30 year customer relationships.

The power of the portfolio wasn't just in individual products but in their interconnection. Data from one product informed risk assessment for another. Relationship from one product enabled cross-selling another. Trust built through one product facilitated adoption of another. The portfolio became a system, not just a collection.

Risk diversification through portfolio construction was masterful. When personal loans faced stress, secured loans compensated. When urban markets slowed, rural markets grew. When consumer lending faced regulatory scrutiny, business lending expanded. No single product, segment, or geography could destabilize the company.

By 2024, Bajaj Finance had built India's most comprehensive lending portfolio outside of banks. But unlike banks constrained by regulation and legacy, Bajaj Finance could innovate rapidly, launch products quickly, and shut unsuccessful experiments without bureaucracy. The product portfolio wasn't just business lines—it was competitive moat, customer lock-in, and growth engine combined.

VIII. Modern Era: Competition & New Frontiers (2020–Today)

The post-2020 era brought unprecedented challenges and opportunities. COVID-19 accelerated digital adoption by years. Fintech disruption intensified with new players backed by billions in venture capital. Regulatory scrutiny increased with RBI determined to prevent excesses. In this environment, Bajaj Finance had to evolve from disruptor to incumbent while maintaining growth momentum.

The fintech disruption came from multiple directions. Paytm pioneered payments and attempted lending. PhonePe and Google Pay dominated UPI but eyed financial services. New-age lenders like Slice, Uni, and Jupiter targeted young consumers with slick apps and instant credit. Each claimed to be building the future of finance, dismissing traditional players as dinosaurs.

But Bajaj Finance's response was nuanced. Instead of competing head-on with fintechs on their terms, the company leveraged its advantages: risk management experience through cycles, profitable unit economics, regulatory relationships, and physical distribution. While fintechs burned cash acquiring customers, Bajaj Finance acquired profitably. While fintechs faced regulatory crackdowns, Bajaj Finance maintained compliance.

The board didn't take much time to give its stamp of approval to build a one-stop shop financial services super app with a shopping and e-commerce ecosystem. The Bajaj Pay super-app ambitions represented recognition that financial services were becoming platform businesses. The app wasn't just for transactions—it was for engagement, combining payments, loans, insurance, investments, and shopping.

Healthcare finance emerged as major opportunity. Medical inflation, inadequate insurance coverage, and increasing health consciousness created demand for healthcare loans. Bajaj Finance partnered with hospitals, diagnostic chains, and pharmacies to embed financing at point of care. This wasn't just another loan product—it was participation in India's healthcare transformation.

Rural expansion accelerated as urban markets saturated. And, across 3800 towns, it has 294 consumer branches and 497 rural locations with over 33,000+ distribution points and 1,50,000+ stores. But rural didn't mean simple replication of urban model. Products were redesigned for agricultural cash flows. Distribution partnered with local institutions. Risk assessment incorporated local knowledge. Rural wasn't just geography—it was entirely different business requiring different capabilities.

The Bharat opportunity—India beyond metros—became strategic priority. This wasn't corporate social responsibility but hard business logic. Bharat was where consumption growth would come from, where credit penetration was lowest, where competition was manageable. But serving Bharat required patience, investment, and deep understanding of local dynamics.

Managing through RBI's digital lending guidelines required fundamental changes. The 2025 Directions significantly enhance the regulatory framework for digital lending by addressing key areas such as scope, DLG framework, multi-lender LSP arrangements, reporting infrastructure, cooling-off period, customer protection and data privacy: Customer Protection: The 2025 Directions increases its protection to the customers in digital lending by structuring grievance redressal mechanisms and mandating comprehensive website disclosures.

The competitive dynamics shifted fundamentally. Banks, traditionally slow, were digitizing rapidly. Fintechs, initially disruptive, were discovering that lending was harder than payments. Foreign players were entering through partnerships and acquisitions. The competitive moat had to be continuously reinforced through innovation, execution, and customer service.

Its assets under management (AUM) grew by 29 per cent to Rs 3.73 trillion as of September 30, 2024, from Rs 2.9 trillion as of September 30, 2023. New lines of businesses have started contributing 2-3 per cent of AUM growth, it said. The growth trajectory remained impressive despite size—growing 29% at ₹3.73 trillion AUM is harder than growing 29% at ₹100 crore.

Technology transformation accelerated. Cloud adoption reached majority of workloads. API-first architecture enabled rapid integration with partners. Machine learning models improved risk assessment. But technology was enabler, not strategy—the focus remained on customer needs and business outcomes.

The partnership ecosystem expanded beyond traditional merchants. E-commerce platforms, travel aggregators, education technology companies, health tech startups—each became distribution partner. The strategy was simple: be present wherever customers made purchase decisions. Embedded finance became reality before it became buzzword.

Regulatory relationships evolved from compliance to collaboration. Bajaj Finance engaged proactively with RBI on policy formation, shared data for financial inclusion initiatives, and participated in regulatory sandboxes. The company understood that in regulated industries, regulatory capital was as important as financial capital.

The NBFC has been grappling with elevated losses in the last few quarters, especially in the personal loan segment in rural regions. It reported lower-than-expected profit in the first quarter as well, hurt by higher funds set aside to cover potential bad loans. The challenges were real—asset quality stress in certain segments, regulatory restrictions on growth, competitive intensity in profitable products. But these were managed actively through portfolio rebalancing, underwriting tightening, and strategic patience.

The talent war intensified as technology companies, startups, and global firms competed for same pool. Bajaj Finance responded by building strong culture, offering entrepreneurial opportunities within large company framework, and investing heavily in training and development. The company became talent factory for Indian financial services, with alumni founding or leading numerous startups.

We have crafted a visionary blueprint (Long-Range Strategy) for the next decade that reshapes our ambition, strategy, approach, and goals of customer share, market share and profit share. The blueprint envisages your Company to become a dominant payments and financial services company in India over the medium term.

International expansion remained conspicuously absent from strategy. Unlike banks seeking global presence, Bajaj Finance focused entirely on India. The logic was compelling: India offered decades of growth, international expansion would distract from core market, and regulatory complexities weren't worth potential returns.

By 2024, Bajaj Finance stood at interesting inflection point. It was simultaneously incumbent and challenger, traditional and digital, mass and premium. The company had to defend against nimble startups while attacking conservative banks, maintain growth while managing risk, innovate while ensuring compliance. The modern era wasn't about choosing sides but transcending traditional boundaries.

IX. Playbook: Business & Investing Lessons

The Bajaj Finance story offers profound lessons for building enduring value in regulated industries, creating competitive advantages through execution, and managing growth with risk. These aren't theoretical frameworks but practical insights extracted from real-world execution over decades.

The NBFC advantage versus banks is structural and enduring. Considering most NBFCs are non-deposit taking, they are not subject to the stringent RBI regulations and this has allowed them to grow at a blistering pace over the course of the past few years. NBFCs can move faster, experiment more, and serve segments banks won't touch. But this advantage comes with funding disadvantages that must be managed carefully.

Customer acquisition cost (CAC) and lifetime value (LTV) mastery is fundamental to Bajaj Finance's model. The company understood early that CAC must be evaluated not for single products but entire customer lifecycle. Losing money on first product was acceptable if customer generated profits through subsequent products. This LTV thinking enabled aggressive customer acquisition while maintaining profitability.

Most of Bajaj Finance's revenue is generated from suppliers who pay for access to their larger customer base. This business model insight is profound—customers aren't the only revenue source. Merchants pay for access to customers, manufacturers subsidize interest costs for sales enablement, insurance companies pay distribution fees. The platform model in financial services predated platform thinking in technology.

Risk-adjusted pricing sophistication separates winners from losers in lending. Bajaj Finance doesn't avoid risk—it prices for it. Higher risk segments get loans at higher rates. The portfolio mathematics work because pricing compensates for losses. This requires sophisticated risk models, continuous monitoring, and courage to walk away from underpriced business.

Data advantages compound over time. Each customer interaction generates data. Each product provides different perspective on customer behavior. Each repayment cycle refines risk models. After millions of customers and billions of transactions, the data advantage becomes insurmountable for new entrants. But data without analytics is worthless—the investment in analytics capabilities is as important as data collection.

Distribution moats in India are physical and digital. Since its inception, it has leveraged technology to launch 26 product lines and 51 product variants for retail, MSME, and commercial consumers, with major product innovations like the EMI card and Flexi with a significant presence in both urban and rural India. The 3,800 towns presence isn't just about reach—it's about trust, service, and local knowledge. Digital can acquire customers, but physical presence retains them during stress periods.

The cross-selling flywheel is elegant: acquire customers through simple products, build trust through service, expand relationship through relevant offers, deepen engagement through multiple products, create switching costs through convenience. Each product makes next product easier to sell. Each interaction provides opportunity for expansion.

Culture and execution matter more in lending than strategy. Everyone knows lending opportunity in India is massive. The differentiation is in execution—speed of approval, quality of service, collection effectiveness, risk management discipline. Bajaj Finance's culture of customer obsession, performance orientation, and continuous improvement drives superior execution.

Capital efficiency and ROE optimization require balancing growth with profitability. To build businesses with a long-term view anchored on prudence and risk management to deliver 'through the cycle' return on equity of 21-23%. The 21-23% ROE target isn't arbitrary—it represents optimal balance between growth investment and shareholder returns. Higher ROE might mean underinvesting in growth; lower ROE might mean destroying value.

Regulatory navigation in financial services is continuous, not episodic. Compliance isn't cost center but competitive advantage. Companies that engage proactively with regulators, exceed minimum requirements, and help shape policy have structural advantages over those that view regulation as burden.

Brand trust in financial services takes decades to build, moments to destroy. The Bajaj brand, built over 75 years, provides trust that no amount of advertising can buy. But trust must be continuously earned through fair practices, transparent communication, and customer-first decisions, especially during crisis periods.

Technology is enabler, not strategy. Bajaj Finance succeeded not because it had best technology but because it used technology to serve customers better, assess risk more accurately, and operate more efficiently. Technology investments were always evaluated on business impact, not technical elegance.

Diversification across products, segments, and geographies provides resilience. When personal loans face stress, secured loans compensate. When urban markets slow, rural markets grow. When consumer lending faces scrutiny, business lending expands. This portfolio approach reduces volatility and enables consistent growth.

Timing matters enormously. Bajaj Finance rode multiple waves perfectly—India's consumption boom, financial inclusion expansion, digital adoption acceleration. But timing isn't luck—it's about positioning for inevitable trends and having patience for them to materialize.

Talent density drives outcomes. The concentration of high-performers at Bajaj Finance creates virtuous cycle—good people attract good people, high standards become self-reinforcing, success breeds confidence for bigger bets. Investment in talent development pays exponential returns.

The balance between entrepreneurship and process is delicate. Too much process kills innovation; too little process creates chaos. Bajaj Finance maintains entrepreneurial energy within professional framework—encouraging experimentation while maintaining risk discipline.

Patient capital enables long-term thinking. The Bajaj family's controlling stake provided stability for long-term investments that might not pay off immediately. This patient capital advantage is underappreciated in financial services where quarterly earnings pressure can drive short-term decisions.

X. Analysis & Bear vs. Bull Case

The investment case for Bajaj Finance polarizes opinions. Bulls see India's best-in-class lender with decades of growth ahead. Bears see overvaluation, regulatory risks, and competitive threats. The truth, as always, is nuanced.

The Bull Case:

India's credit penetration remains extraordinarily low. Household debt to GDP is around 40% versus 75% in China and over 100% in developed markets. As India grows from $3.7 trillion to $10 trillion economy, credit growth will outpace GDP growth. Bajaj Finance, with its distribution, brand, and execution capabilities, will capture disproportionate share.

During the pandemic, Rajeev successfully carried out Zero based budgeting exercise, reimagining all the processes across businesses and functions in the Company. The execution track record through multiple crises—demonetization, IL&FS, COVID—demonstrates resilience. Management has consistently delivered 20%+ ROE while growing at 30%+ CAGR. This isn't luck but systematic capability in risk management, customer acquisition, and operational excellence.

The data moat is real and growing. With 100+ million customers and 160+ variables per customer, Bajaj Finance has insights no competitor can replicate quickly. This data advantage improves risk assessment, enables personalized marketing, and creates switching costs. In lending, better data means better outcomes—lower losses, higher margins, faster growth.

To be a leading payments and financial services company in India with acustomer franchise of over 150 million, market share of 3% of payments Gross erchandise Value (GMV), 3%-4% of total The transformation from lender to financial services platform expands addressable market exponentially. Payments, insurance, investments, healthcare finance—each represents massive opportunity. The customer base and distribution provide launch advantages in each new category.

Management quality and depth are exceptional. An industry veteran with nearly 3 decades of stellar experience in managing diverse consumer lending businesses, viz., auto loans, durable loans, personal loans and credit cards, Rajeev has spent 18 years with Bajaj Finance, driving sustainable businesses and large-scale digital transformations to create long-term value for stakeholders. The leadership team combines experience with innovation, Indian market knowledge with global best practices.

The Bear Case:

Regulatory overhang is permanent in financial services. As per the 2023 list of NBFCs issued by the Reserve Bank of India, Bajaj Finance Limited holds the second position in the upper layer based on scale-based regulation guidelines. Being systemically important means bank-like regulation without bank-like advantages. Future regulatory changes could constrain growth, increase costs, or reduce profitability.

Asset quality cycles are inevitable in lending. Bajaj Finance's loan losses and provisions grew 77% on-year to Rs 1,909 crore. Its gross non-performing asset ratio - the ratio of bad loans to total lending - deteriorated to 1.06% at the end of September, from 0.91% a year earlier. Current stress in personal loans could be early indicator of broader problems. High growth often masks deteriorating underwriting standards that become visible only during downturns.

Fintech competition is intensifying. New players backed by billions in venture capital are targeting same customers with better user experience, lower costs, and higher risk appetite. While Bajaj Finance has defended successfully so far, competitive intensity will pressure margins and growth.

Valuation premium leaves no room for error. Stock is trading at 5.63 times its book value Trading at 5.6x book value implies perfect execution forever. Any disappointment—regulatory action, asset quality stress, growth slowdown—could trigger significant multiple compression.

Concentration risk in unsecured lending is concerning. Large portion of portfolio is unsecured consumer loans dependent on individual repayment capability. Economic downturn affecting employment could trigger systemic stress. Unlike secured loans with collateral, recovery in unsecured loans depends entirely on collection effectiveness.

Technology disruption could obsolesce traditional advantages. If lending becomes purely algorithmic, Bajaj Finance's physical distribution and relationship model become liabilities, not assets. Pure digital players with lower costs could undercut pricing while maintaining profitability.

Comparison with Peers:

Versus HDFC Bank: Bajaj Finance grows faster but with higher risk. HDFC Bank's deposit franchise provides funding advantage and stability. Bajaj Finance's agility and focus provide growth advantage. Market values growth over stability, hence premium valuation.

Versus Kotak Mahindra Bank: Both command premium valuations for quality. Kotak is more conservative, Bajaj Finance more aggressive. Kotak's banking license provides long-term advantages, Bajaj Finance's NBFC status provides near-term flexibility.

Versus New-Age Fintechs: Bajaj Finance has profitability and scale, fintechs have innovation and venture capital. The convergence is inevitable—Bajaj Finance becoming more digital, fintechs becoming more regulated. Winners will combine both capabilities.

The Next Decade Outlook:

Can they become a bank? Technically possible but strategically questionable. Banking license would provide deposit access but reduce flexibility. The NBFC model's advantages might outweigh banking license benefits, especially if digital public infrastructure reduces funding disadvantages.

Should they become a bank? The strategic logic isn't compelling. Bajaj Finance can achieve banking scale and scope without banking constraints. Partnership models, co-lending arrangements, and platform approach might provide better risk-adjusted returns than traditional banking.

The transformation into financial services platform is more promising than banking aspiration. Payments, insurance, investments—each leverages existing capabilities while expanding addressable market. The super-app strategy could create ecosystem lock-in that transcends traditional lending.

International expansion remains unlikely but not impossible. The India opportunity is far from saturated. But Indian diaspora markets, Southeast Asian expansion, or strategic partnerships could provide growth optionality in next decade.

The balance of probabilities favors continued outperformance, but with higher volatility. Bajaj Finance will likely remain India's premier consumption financier, but journey will include regulatory speedbumps, competitive challenges, and cycle management. The premium valuation reflects this quality but also embeds execution risk.

XI. Epilogue & Future Scenarios

What would success look like in 2035? Bajaj Finance serving 200 million customers, managing ₹20 trillion in assets, operating as India's private financial utility. Not just lending but orchestrating financial lives—savings, payments, investments, insurance, healthcare, education. The transformation from lender to platform complete, from product company to ecosystem orchestrator.

The optimistic scenario sees India's per capita income doubling, financial inclusion reaching universal coverage, and digital infrastructure enabling seamless services. In this world, Bajaj Finance becomes India's Ant Financial—dominant platform intermediating large portion of financial transactions. The company successfully navigates regulatory evolution, manages credit cycles, and fends off competitive threats through continuous innovation.

The realistic scenario acknowledges challenges. Growth moderates from 30% to 15-20% as base expands. Regulations tighten, reducing profitability but improving stability. Competition intensifies, compressing margins but expanding markets. Bajaj Finance remains highly successful but not dominant, one of several large players in competitive market. ROE normalizes to 15-18%, still attractive but not exceptional.

The pessimistic scenario involves systemic shocks. Deep recession triggers widespread defaults in unsecured portfolio. Regulatory backlash against NBFCs forces dramatic business model changes. Technology disruption obsolesces traditional advantages. New players backed by global capital and superior technology capture next generation of customers. Bajaj Finance survives but as diminished force, struggling to maintain relevance.

Biggest Risks Ahead:

Regulatory risk remains paramount. RBI's increasing focus on consumer protection, digital lending guidelines, and systemic stability could constrain growth models that worked historically. The pendulum between growth enablement and stability could swing decisively toward stability.

Credit cycle risk is inherent in lending. India hasn't experienced deep recession since 1991. Young population, high growth, and fiscal stimulus have prevented serious downturns. When inevitable recession arrives, leveraged consumers and aggressive lenders will face reckoning. Bajaj Finance's portfolio quality will be tested severely.

Technology disruption accelerates. Central bank digital currency, open banking regulations, account aggregators, and digital public infrastructure could fundamentally reshape financial services. Traditional advantages of distribution and relationships might evaporate if financial services become purely digital and interoperable.

Competitive dynamics intensify. Global giants like Amazon, Google, and Walmart are entering Indian financial services. Chinese players might return through partnerships. Domestic conglomerates like Reliance and Adani are building financial services ambitions. The competitive landscape in 2035 will be unrecognizable from today.

Biggest Opportunities Ahead:

Financial inclusion remains massive opportunity. Hundreds of millions of Indians still lack access to formal credit. As India urbanizes, formalizes, and digitizes, addressable market expands continuously. Bajaj Finance's capabilities in serving mass market position it perfectly for this opportunity.

New categories beyond traditional lending beckon. Healthcare finance, education finance, supply chain finance, sustainability finance—each represents billion-dollar opportunity. Bajaj Finance's brand, distribution, and execution capabilities provide launch advantages in adjacent categories.

Platform economics could drive exponential value creation. As Bajaj Finance aggregates customers, merchants, and financial service providers, network effects strengthen. The company could become toll collector on large portion of India's financial transactions, earning fees without taking risk.

Data monetization possibilities expand with scale. Insights from 100+ million customers have value beyond lending—market research, targeted advertising, economic forecasting. Privacy-compliant data monetization could create high-margin revenue streams.

Lessons for Founders Building in Regulated Industries:

Regulatory relationship is strategic asset. Invest in compliance, engage proactively with regulators, and help shape policy. View regulation as moat, not burden. Companies that master regulatory navigation have structural advantages.

Patient capital enables long-term thinking. Quarterly earnings pressure drives short-term decisions that destroy long-term value. Find patient investors who understand regulated industries require investment cycles measured in years, not quarters.

Culture eats strategy in execution businesses. Financial services is ultimately execution business—thousands of daily decisions, millions of customer interactions. Building execution culture is harder but more valuable than crafting strategy.

Trust takes decades to build, moments to destroy. Every customer interaction, every crisis response, every regulatory engagement either builds or depletes trust. In financial services, trust is ultimate currency.

Technology enables but doesn't replace business judgment. Invest heavily in technology but remember that lending is ultimately about understanding human behavior, economic cycles, and risk management. Technology amplifies capabilities but doesn't replace wisdom.

Diversification provides resilience. Single product companies are vulnerable to regulatory changes, competitive threats, and cycle risks. Building portfolio of products, segments, and geographies creates anti-fragility.

Final Reflections:

The Bajaj Finance story is ultimately about transformation—of company, industry, and country. From scooters to loans, from products to platform, from physical to digital, from India to Bharat. Each transformation required courage to abandon successful models for uncertain futures.

That's the learning for us to exploit the new opportunities emerging in a [Covid-19] crisis situation," explains Jain, 51, who has played a key role in transforming a small Bajaj Finance into one of India's fastest-growing NBFCs. The journey from captive auto financier to India's lending machine wasn't predetermined but constructed through thousands of decisions, experiments, and iterations.

Building a lending juggernaut requires paradoxical capabilities: patience and urgency, innovation and discipline, growth and risk management, technology and humanity. Bajaj Finance's success comes from resolving these paradoxes, not choosing sides.

The next decade will test everything Bajaj Finance has built. Success isn't guaranteed—regulated industries are graveyards of former champions who couldn't adapt. But the capabilities, culture, and ambition position Bajaj Finance to shape India's financial future rather than just participate in it.

For entrepreneurs, investors, and observers, Bajaj Finance offers masterclass in building enduring value in complex markets. The lessons transcend financial services—how to transform legacy businesses, build in regulated industries, create platforms from products, and serve aspirational populations.

The story continues to unfold. Whether Bajaj Finance becomes India's defining financial institution or cautionary tale of hubris depends on decisions being made today in Pune headquarters, RBI offices, and millions of customer interactions. The machine has been built—its ultimate destination remains unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube