Aurobindo Pharma: From Pondicherry to Global Generics Giant

I. Introduction & Episode Roadmap

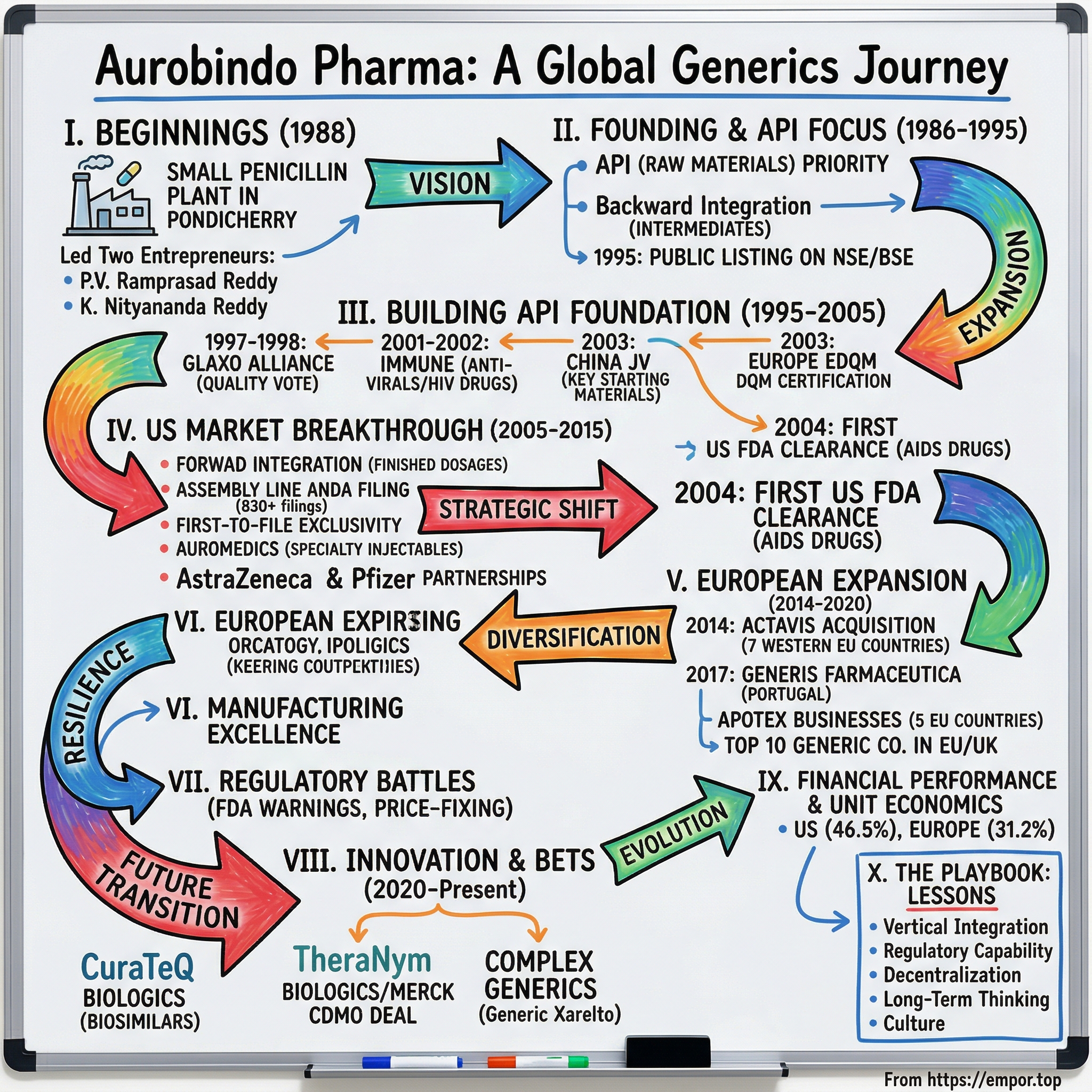

Picture this: A small penicillin plant in Pondicherry, 1988. The air thick with the smell of fermentation cultures, machinery humming in the tropical heat. Two entrepreneurs, P.V. Ramprasad Reddy and K. Nityananda Reddy, stand in what would become the first manufacturing facility of Aurobindo Pharma. They had a vision that seemed almost naive at the time—to build a pharmaceutical company that could compete with global giants from this modest beginning in South India.

Fast forward to 2025: Aurobindo Pharma stands as India's second-largest listed pharmaceutical company by revenue, commanding a market capitalization of $8.77 billion. The company exports to over 150 countries, holds the crown as the largest generics player in the United States market, and operates 29 manufacturing facilities across the globe. How did two entrepreneurs transform a single penicillin plant into one of the world's top 10 generic pharmaceutical companies?

This is a story of relentless vertical integration, regulatory chess moves, strategic acquisitions, and the unglamorous but essential work of making medicines affordable. It's about building trust after violations, navigating the cutthroat world of generic drug pricing, and betting big on biosimilars when others hesitated. Along the way, we'll explore how Aurobindo mastered the art of turning distressed pharmaceutical assets into profit centers, why vertical integration became their superpower, and what it really takes to compete in an industry where your product becomes a commodity the moment your patent expires.

The pharmaceutical industry isn't Silicon Valley—there's no "move fast and break things" here. One contaminated batch, one failed FDA inspection, one manufacturing deviation can destroy years of reputation building. Yet Aurobindo navigated this minefield to generate $3.62 billion in trailing twelve-month revenue, with operations spanning from Hyderabad to New Jersey, from Portugal to China.

What makes Aurobindo particularly fascinating is how they've played the long game in an industry obsessed with quarterly earnings. While competitors chased blockbuster drugs, Aurobindo quietly built the infrastructure to manufacture everything from the raw materials to the finished tablets. They turned regulatory compliance—usually seen as a cost center—into a competitive moat. And they've shown that in the generic drug business, the real money isn't in being first; it's in being reliable, scalable, and vertically integrated.

Over the next several hours, we'll dissect how Aurobindo built this empire, examining their playbook move by move. We'll explore their early struggles in the liberalizing Indian economy of the 1980s, their calculated entry into the US market, their European shopping spree during market downturns, and their current pivot toward complex generics and biosimilars. We'll also confront the darker chapters—the price-fixing allegations, FDA warning letters, and environmental controversies that nearly derailed their ambitions.

This isn't just a business story; it's a masterclass in building a global enterprise from an emerging market, competing on quality rather than just cost, and creating value in an industry where your best products inevitably become commodities. Whether you're an investor trying to understand the pharmaceutical value chain, an entrepreneur navigating regulated industries, or simply curious about how essential medicines actually get made and distributed globally, this deep dive into Aurobindo's journey offers lessons that extend far beyond pharma.

So let's start where all great business stories begin—with two ambitious founders, a big vision, and barely enough capital to get started.

II. The Founding Story & Early Vision (1986–1995)

The year was 1986. India's pharmaceutical landscape looked nothing like today's powerhouse industry. The Bhopal gas tragedy was barely two years old, casting a shadow over chemical manufacturing. Patent laws still favored process innovation over product patents—a quirk of Indian policy that would prove crucial. And in this environment of cautious optimism and regulatory flux, two men decided to start a pharmaceutical company with a vision that seemed audacious: making medicines accessible and affordable to patients across the globe.

P.V. Ramprasad Reddy wasn't your typical pharmaceutical entrepreneur. Unlike many founders who came from medical or chemistry backgrounds, Reddy brought a commercial mindset shaped by years in the trading business. His co-founder, K. Nityananda Reddy, complemented this with deep technical knowledge of pharmaceutical manufacturing. Together with a small group of committed professionals, they incorporated Aurobindo Pharma in Hyderabad, choosing a name that evoked both Indian heritage (Sri Aurobindo was a renowned philosopher) and global ambitions.

But vision without execution is just hallucination. The founders needed a strategy that could work within India's unique pharmaceutical ecosystem of the 1980s. India's Patent Act of 1970 had created an unusual opportunity—while product patents weren't recognized, process patents were. This meant Indian companies could reverse-engineer patented drugs using different manufacturing processes. It was perfectly legal, economically vital for a developing nation, and would become the foundation of India's generic drug industry.

The founders made their first crucial decision: instead of starting with formulations (finished drugs) like most Indian pharma companies, they would begin with Active Pharmaceutical Ingredients (APIs)—the actual chemical compounds that give medicines their therapeutic effect. It was a contrarian move. APIs required significant capital investment, complex chemistry, and stringent quality control. But Ramprasad Reddy saw what others missed: whoever controlled the raw materials would eventually control the supply chain. In 1988-89, their vision became concrete with the commencement of operations with a single-unit manufacturing Semi-Synthetic Penicillin (SSP) at Pondicherry. The choice of semi-synthetic penicillins wasn't random. SSPs represented a sweet spot in pharmaceutical manufacturing—technically complex enough to deter casual competition, but not so cutting-edge as to require unaffordable technology. The Pondicherry plant was modest by today's standards, but it represented everything the founders had—their savings, borrowed capital, and most importantly, their reputations.

The early days were brutal. Competition from established players like Ranbaxy and Cipla was fierce. Customers were skeptical of a new entrant. Banks were reluctant to lend to an unproven pharmaceutical startup. The founders often worked 18-hour days, with Ramprasad Reddy handling commercial negotiations while Nityananda Reddy supervised production. They couldn't afford specialized departments—everyone did everything. Quality control technicians helped with packaging when orders surged. Managers swept floors. The founders personally drove trucks to ensure timely delivery.

But something remarkable happened in 1992. Aurobindo Pharma became a public company, a bold move for a four-year-old company with a single product line. The decision to go public so early revealed the founders' ambition and confidence. They weren't building a family business to pass down through generations—they were building an institution that would outlast them. In 1992-1993, Aurobindo expanded by establishing another unit in Pashamylaram, Hyderabad. This unit was dedicated to manufacturing CMIC chloride, a key bulk drug intermediate. This wasn't just geographic expansion—it was the beginning of backward integration, manufacturing the very chemicals needed to produce their antibiotics. The facility later merged with the parent company in 1994-95, consolidating operations and strengthening the balance sheet.

The real test came with the listing on Indian stock exchanges in 1995. The markets were skeptical. Here was a company less than a decade old, competing against giants like Ranbaxy (founded in 1961) and Cipla (founded in 1935). The IPO pricing reflected this skepticism, but the founders saw it differently. Public listing meant access to capital markets, transparency requirements that would force operational discipline, and most importantly, the credibility needed to approach international customers.

What set Aurobindo apart in these early years wasn't revolutionary technology or blockbuster products. It was something more fundamental: the founders' conviction that Indian pharmaceutical companies could compete globally not just on cost, but on quality. While others were content serving the domestic market with its relaxed regulatory standards, Ramprasad Reddy was already thinking about FDA approvals and European certifications.

The company's early culture reflected this ambition. Engineers were sent to conferences in Europe to learn about Good Manufacturing Practices (GMP). Quality control wasn't an afterthought—it was built into the process from day one. The founders instituted a policy that seems obvious now but was radical then: every batch would be tested as if it was going to the most stringent regulator, even if it was destined for a market with minimal oversight.

By 1995, as Aurobindo's shares began trading on Indian stock exchanges, the company had established three critical foundations that would define its future: a focus on APIs rather than just formulations, a commitment to vertical integration starting with intermediates, and an unwavering belief that quality—not just cost—would be their competitive advantage. The small penicillin plant in Pondicherry had evolved into something more ambitious: a platform for global pharmaceutical manufacturing. The stage was set for the next phase of growth—building the API foundation that would make Aurobindo a force in global generics.

III. Building the API Foundation (1995–2005)

The late 1990s found Aurobindo at a crossroads. They had proven they could manufacture quality penicillins and intermediates, but the global pharmaceutical landscape was shifting. The Uruguay Round of GATT negotiations meant India would eventually have to recognize product patents. The window for reverse-engineering patented drugs was closing. Ramprasad Reddy saw this not as a threat but as an opportunity to pivot toward becoming an essential supplier to the world's pharmaceutical companies.

The strategy was audacious in its simplicity: become so good at making Active Pharmaceutical Ingredients that even Big Pharma would come knocking. But executing this strategy required capital, technology, and most crucially, international regulatory approvals that no Indian API manufacturer had systematically pursued at scale.

In 1997-1998, validation came from an unexpected source. Glaxo (India), the Indian subsidiary of the UK-based multinational, formed an alliance with Aurobindo to meet its global bulk drug requirements. This wasn't just another supply contract—it was a vote of confidence from one of the world's largest pharmaceutical companies. The message to the market was clear: Aurobindo's quality was good enough for Big Pharma.

The Glaxo partnership taught Aurobindo invaluable lessons about international pharmaceutical standards. Glaxo's auditors scrutinized everything—from raw material sourcing to waste disposal, from documentation practices to worker training programs. Each audit was a masterclass in pharmaceutical manufacturing excellence. Nityananda Reddy later recalled how Glaxo's team would spend days examining a single production line, questioning every decision, every parameter, every deviation. It was exhausting but transformative.

By 1999-2000, Aurobindo was ready to expand beyond penicillins. The company diversified its portfolio, introducing a wide range of Cephalosporins (both oral and sterile) and anti-virals. This wasn't random diversification—each product was chosen for strategic reasons. Cephalosporins were the next generation of beta-lactam antibiotics, commanding higher prices than penicillins. Anti-virals were becoming critical as the HIV/AIDS epidemic peaked globally.

The anti-viral decision proved particularly prescient. In 2001-2002, Aurobindo launched an exclusive anti-viral division named Immune, focusing on HIV/AIDS treatment. This wasn't just about business—it was about purpose. The HIV/AIDS crisis was devastating sub-Saharan Africa, and treatment costs were prohibitive. Aurobindo saw an opportunity to fulfill its founding mission of making medicines accessible while building a profitable business line.

The technical challenges of manufacturing anti-retrovirals were immense. These weren't simple antibiotics—they required complex chemistry, stringent purity standards, and absolute consistency. A single impurity could render the drug ineffective or worse, contribute to viral resistance. Aurobindo's chemists worked around the clock, developing new synthesis routes that could deliver the required purity at a fraction of the cost of originator processes.

But the real breakthrough came from an unexpected direction: China. In 2003-2004, Aurobindo launched a joint venture with Shanxi Tongling Pharmaceuticals in China, with commercial production commencing in its 100% subsidiary in China the same year. This wasn't about manufacturing in China for the Chinese market—it was about securing access to key starting materials and intermediates at competitive costs. While other Indian companies were wary of Chinese partnerships, fearing intellectual property theft, Aurobindo structured the venture carefully, keeping critical technology in India while leveraging China's chemical manufacturing capabilities.

The year 2003 also marked a regulatory milestone: Aurobindo received its first Certificate of Suitability (CoS) from the European Directorate for Quality Medicines (EDQM). This certification was more than a piece of paper—it was a passport to the European market. The CoS confirmed that Aurobindo's API met European Pharmacopoeia standards, opening doors to supply pharmaceutical companies across the EU.

The EDQM certification process was grueling. European inspectors didn't just check if the product met specifications—they examined the entire manufacturing process, from raw material qualification to finished product testing. They wanted to see not just what Aurobindo did, but why they did it. Every decision needed scientific justification. Every deviation needed root cause analysis. The discipline required for EDQM certification would prove invaluable when Aurobindo later pursued US FDA approvals.

By 2004, Aurobindo's API division was firing on all cylinders. The company acquired a sterile plant from Dee Pharma and received recognition from the State Labour Department of Andhra Pradesh with the 'Best Management Award'. Most significantly, it received US FDA clearance for AIDS drugs at its Unit VIII facility. This FDA approval was a watershed moment—it meant Aurobindo could now supply anti-retrovirals for the US President's Emergency Plan for AIDS Relief (PEPFAR), one of the largest pharmaceutical procurement programs in history.

The numbers told the story of transformation. From a single product (semi-synthetic penicillin) in 1995, Aurobindo now manufactured over 50 APIs across multiple therapeutic categories. Revenue had grown from a few million dollars to hundreds of millions. More importantly, the company had built something intangible but invaluable: a reputation for reliable quality at competitive prices.

The vertical integration strategy was also paying dividends. By controlling the entire value chain from basic chemicals to finished APIs, Aurobindo could ensure quality at every step while maintaining cost competitiveness. When competitors faced raw material shortages or price spikes, Aurobindo's integrated operations provided stability. This operational resilience would prove crucial in the next phase of growth.

The foundation was now complete. Aurobindo had the manufacturing capabilities, regulatory approvals, and market credibility to take on the next challenge: entering the US generics market, the world's largest and most profitable, but also most demanding pharmaceutical market. The lessons learned from building the API business—the importance of quality systems, regulatory compliance, and vertical integration—would guide this ambitious expansion.

IV. The US Market Breakthrough (2005–2015)

The conference room in Hyderabad was tense. It was late 2004, and Ramprasad Reddy had just proposed something that seemed like corporate suicide: Aurobindo would shift focus from being primarily an API supplier to becoming a finished dosage manufacturer for the US market. The CFO's concerns were valid—this meant competing directly with their own customers, companies that bought Aurobindo's APIs to make their own generics. "We'll lose our biggest buyers," one executive warned. Reddy's response was prescient: "If we don't forward integrate, we'll eventually lose them anyway."

The timing seemed perfect. In 2005-2006, Aurobindo made its strategic entry into the premium markets of the USA and Europe with generic formulations. But entering the US generics market in the mid-2000s was like trying to board a moving train. Teva, Mylan, and Sandoz dominated the landscape. Indian companies like Dr. Reddy's and Ranbaxy had already established beachheads. The FDA's requirements were becoming more stringent following several high-profile quality failures. Yet Aurobindo saw opportunity where others saw obstacles.

The US strategy was built on three pillars: vertical integration as a competitive advantage, a high-volume ANDA filing strategy, and strategic partnerships with established players. Unlike competitors who relied on third-party API suppliers, Aurobindo could control quality and costs from raw materials to finished tablets. This wasn't just about margins—it was about supply security. When Ranbaxy faced FDA import bans due to quality issues, Aurobindo's integrated model looked increasingly attractive to US buyers seeking reliable suppliers.

The ANDA (Abbreviated New Drug Application) operation Aurobindo built was unlike anything the Indian pharmaceutical industry had seen. While competitors celebrated filing 20-30 ANDAs per year, Aurobindo built an assembly line approach to regulatory filings. Scientists in Hyderabad would identify products coming off patent, develop formulations, conduct bioequivalence studies, and prepare regulatory dossiers with military precision. By 2015, the company had filed 830 ANDAs with over 600 approvals—a filing intensity that rivaled much larger companies.

But volume alone doesn't win in US generics. The real game is being first-to-file on valuable products, earning 180-day exclusivity periods where you're the only generic on the market. Aurobindo's scientists became forensic patent analysts, identifying weaknesses in originator patents, developing non-infringing processes, and filing ANDAs the moment patents became challengeable. They didn't always win these races, but when they did, a single product with 180-day exclusivity could generate more profit than dozens of commodity generics. The creation of AuroMedics marked Aurobindo's entry into specialty injectables. Aurobindo commenced marketing specialty injectables to fund the development in USA through AuroMedics. This wasn't just another product line—it was a strategic masterstroke. Injectable generics are harder to manufacture than oral solids, require specialized facilities, and face less competition. While everyone was fighting over generic Lipitor tablets, Aurobindo was quietly building capabilities in sterile manufacturing that would generate higher margins with less pricing pressure.

The partnerships Aurobindo forged during this period read like a who's who of Big Pharma. AstraZeneca and Pfizer weren't just buying Aurobindo's products—they were essentially endorsing the company's quality standards to the world. These weren't charity deals. Big Pharma companies were under pressure to reduce costs while maintaining quality. Aurobindo offered them a solution: the same molecule, same quality, at 30-50% lower cost through Indian manufacturing efficiency.

But the real validation came from market performance. Since its first US ANDA approval in 2004, Aurobindo has expanded its portfolio to include more than 150 product families, representing a wide range of therapeutic categories. Aurobindo has been recognized as the fastest growing pharmaceutical company in 2012, and in early 2013, thanks to the ongoing support of our customers, became one of the top 10 pharmaceutical companies, brand or generic, in terms of total prescriptions dispensed.

The 2014 acquisition of Actavis's generic operations in seven Western European countries for $41 million was perfectly timed. Actavis was divesting non-core assets ahead of its merger with Allergan. Aurobindo picked up established products, customer relationships, and most importantly, local market knowledge at a fraction of replacement cost. This wasn't just an acquisition—it was Aurobindo's entry ticket to the European generics party.

The US operations weren't without challenges. FDA inspections became increasingly rigorous. Competition from other Indian players intensified. Price erosion accelerated as pharmacy benefit managers consolidated buying power. Yet Aurobindo's integrated model provided resilience. When competitors struggled with API supply disruptions, Aurobindo's captive production ensured continuity. When pricing pressures squeezed margins on simple generics, Aurobindo's pipeline of complex products provided relief.

By 2015, Aurobindo had transformed from an API supplier trying to enter finished dosages to one of the most formidable players in US generics. The company was now the largest generics company in the US market by prescriptions dispensed—an astonishing achievement for a company that had entered the market just a decade earlier. The foundation was set for the next phase: geographic diversification beyond the US, because in pharmaceuticals, concentration risk is existential risk.

V. European Expansion & Geographic Diversification (2014–2020)

The boardroom in Hyderabad was unusually quiet as the M&A team presented their findings. It was early 2014, and Actavis was shopping its European generic operations—seven countries, established products, but declining revenues. The asking price of $41 million seemed reasonable, perhaps too reasonable. "What's wrong with these assets?" a board member asked. The answer revealed Aurobindo's emerging superpower: they saw opportunity where others saw operational headaches.

The Actavis assets in Western Europe—operations in France, Italy, Spain, Portugal, Belgium, Netherlands, and Germany—were underperforming not because of fundamental flaws but due to neglect. Actavis, focused on higher-margin branded drugs, had starved these generic operations of investment. Products weren't being renewed, sales forces were demoralized, and manufacturing was subscale. For most buyers, this spelled trouble. For Aurobindo, it spelled opportunity.

The integration playbook Aurobindo developed for the Actavis acquisition would become their template for European expansion. First, leverage Indian manufacturing to improve product costs by 30-40%. Second, revitalize the product portfolio by filing new dossiers using Aurobindo's extensive ANDA library adapted for European requirements. Third, maintain local commercial presence—Europeans preferred buying from European entities, even if the products came from India. Fourth, achieve economies of scale by consolidating back-office functions while keeping customer-facing operations local.

The transformation was swift. Within 18 months, the acquired operations went from loss-making to profitable. Revenue per product increased as Aurobindo's supply chain reliability won back customers who had defected due to Actavis's inconsistent service. The European pharmaceutical establishment took notice—here was an Indian company that understood that success in Europe required more than just low prices; it required local presence, regulatory excellence, and cultural sensitivity. Emboldened by the Actavis success, Aurobindo embarked on an acquisition spree that would transform its European presence. In 2017, Aurobindo Pharma inked a pact to acquire Portugal's Generis Farmaceutica SA from Magnum Capital Partners for €135 million. This wasn't just another bolt-on acquisition—it made Aurobindo the largest generic pharmaceutical company in Portugal, with 271 products and a state-of-the-art manufacturing facility in Amadora capable of producing 1.2 billion tablets annually.

The Generis acquisition revealed Aurobindo's evolving M&A philosophy. They weren't looking for perfect assets—they were looking for strategic fits with improvement potential. Generis had strong brand recognition in Portugal but was struggling with growth. Aurobindo saw an opportunity to leverage Generis's local market knowledge while injecting their product pipeline and manufacturing efficiency. The projected synergies—€2 million in 2018 and €5 million in 2019—were conservative, and Aurobindo typically exceeded such targets.

But the real masterstroke came with the Apotex acquisitions. Aurobindo Pharma Ltd. signed a definitive agreement to purchase the Apotex businesses in Poland, the Czech Republic, the Netherlands, Spain and Belgium. Apotex, the Canadian generic giant, was divesting these operations under regulatory pressure. The assets were quality operations with established products, but Apotex's legal troubles had created uncertainty among customers and employees.

Aurobindo's integration of the Apotex assets showcased their operational sophistication. They retained key personnel to maintain continuity, immediately addressed supply chain concerns to reassure customers, and leveraged their Indian manufacturing base to improve product margins. Within two years, these previously struggling operations were contributing positively to EBITDA.

The geographic diversification strategy wasn't just about risk mitigation—it was about regulatory arbitrage. Different European countries had different pricing mechanisms, tender processes, and reimbursement systems. By having a presence across multiple markets, Aurobindo could optimize where to launch products first, how to price across borders, and when to participate in government tenders. A product that was commoditized in Germany might still command premium pricing in Poland. By 2020, the transformation was complete. Aurobindo ranked among the top 10 generic companies in EU/UK and had become the largest Indian Pharma company in terms of revenue from Europe. The company had operations across 10 European countries with over 550 marketed products. Europe now contributed 31.2% of total revenues, providing crucial geographic balance to the 46.5% coming from the United States.

The COVID-19 pandemic tested Aurobindo's operational resilience like never before. Border closures, supply chain disruptions, panic buying—every aspect of pharmaceutical distribution was stressed. Yet Aurobindo's distributed manufacturing footprint and integrated supply chain proved their worth. When competitors struggled to source APIs from locked-down regions, Aurobindo's multiple manufacturing sites ensured continuity. The company emerged from the pandemic stronger, with enhanced reputation among European health authorities for reliability during crisis.

The European expansion wasn't just about acquiring assets—it was about building a platform for the next phase of growth. Each acquisition brought not just products and facilities, but regulatory knowledge, customer relationships, and local market intelligence that would be impossible to build organically. By 2020, Aurobindo wasn't an Indian company selling in Europe; it was a European pharmaceutical company that happened to be headquartered in India.

VI. Manufacturing Excellence & Vertical Integration

The manufacturing floor at Aurobindo's Unit VII in Hyderabad operates with the precision of a Swiss watch. Robots handle materials that human hands never touch. Environmental monitoring systems track particle counts in real-time. Quality control stations dot the production line like sentinels. This isn't just automation—it's a philosophy that every tablet produced must meet the standards of the most demanding regulator in the world, regardless of its destination.

Operating across more than 29 commercial manufacturing and packaging facilities worldwide, Aurobindo Pharma holds approvals from esteemed regulatory agencies such as USFDA, UK MHRA, EDQM, PMDA Japan, Health Canada, MCC South Africa, and ANVISA Brazil. This global manufacturing footprint isn't just about scale—it's about strategic redundancy. Each facility can potentially back up others, ensuring that a regulatory issue at one site doesn't cripple the entire operation.

The numbers are staggering: manufacturing capacities of 50+ billion formulation units and 19,000+ MT APIs annually. To put this in perspective, Aurobindo produces enough tablets each year to give every person on Earth six doses. But scale without efficiency is just expensive overhead. Aurobindo's genius lies in how they've optimized this vast network.

The vertical integration strategy that began in the 1990s with backward integration into intermediates had evolved into something far more sophisticated. Aurobindo doesn't just make the API and the finished drug—they often control the entire value chain from basic chemicals to the packaging material. When a customer orders a generic drug from Aurobindo, they're buying from a company that probably manufactured the active ingredient, formulated the tablet, produced the bottle, and printed the label.

This integration provides three critical advantages. First, quality control: when you control every step, you can ensure consistency that's impossible when relying on third-party suppliers. Second, cost efficiency: eliminating middleman margins at every step compounds into significant cost advantages. Third, supply security: when global supply chains seize up, as they did during COVID-19, integrated manufacturers keep running while others scramble for materials.

The economics of vertical integration in generics are compelling but require massive capital investment and operational expertise. Consider a simple antibiotic tablet. A non-integrated manufacturer might buy the API at $100 per kilogram, formulate it into tablets, and sell the finished product with a 30% margin. Aurobindo manufactures that same API for $40 per kilogram (including allocated overheads), formulates it in their own facilities, and can either pocket the additional margin or use it to win price-sensitive tenders.

But vertical integration isn't universally beneficial. For low-volume, high-complexity products, the investment in dedicated manufacturing might never pay off. Aurobindo's solution was selective integration—own the manufacturing for high-volume, strategic products while sourcing niche ingredients from specialists. This hybrid model provides flexibility without sacrificing the core advantages of integration.

The COVID-19 pandemic became an unexpected validation of Aurobindo's manufacturing strategy. When China locked down in early 2020, global pharmaceutical supply chains panicked. Companies dependent on Chinese APIs faced potential stockouts. Aurobindo, with its integrated facilities and strategic inventory buffers, not only maintained supply but actually gained market share as competitors faltered. The company's ability to rapidly scale production of essential medicines during the pandemic earned recognition from health authorities globally.

Quality control at Aurobindo transcends regulatory compliance—it's embedded in the company culture. Each facility operates under the principle of "Right First Time," a methodology that emphasizes prevention over correction. Operators are trained not just to follow procedures but to understand the science behind them. This deep technical competence proved crucial when regulators began conducting remote inspections during the pandemic—Aurobindo's teams could explain and demonstrate their processes virtually with the same confidence as in-person.

The investment in manufacturing excellence shows in the numbers. Despite producing billions of units annually, Aurobindo maintains batch failure rates below industry averages. Their on-time-in-full (OTIF) delivery metrics consistently exceed 95%, crucial for maintaining customer relationships in the cutthroat generics market. When Walmart or CVS places an order, they need certainty that the products will arrive on schedule—Aurobindo's manufacturing reliability has made them a preferred supplier.

The next frontier in manufacturing excellence is digitalization. Aurobindo has begun implementing AI-driven predictive maintenance, IoT-enabled supply chain tracking, and blockchain-based verification systems. These aren't buzzword initiatives—they're practical applications that reduce downtime, improve traceability, and enhance security. A tablet produced in Hyderabad can be tracked through every step of its journey to a pharmacy shelf in Hamburg.

VII. Regulatory Battles & Quality Challenges

The email arrived on a Friday afternoon in December 2016, the kind of timing that ruins weekends for pharmaceutical executives. Twenty American attorneys general had filed a civil complaint accusing Aurobindo Pharma of participating in a coordinated scheme to artificially maintain high prices for a generic antibiotic and diabetes drug. The allegations were explosive: price collusion through informal gatherings, telephone calls, and text messages among six pharmaceutical firms. For a company that had built its reputation on providing affordable medicines, the irony was painful.

The price-fixing allegations weren't unique to Aurobindo—they engulfed much of the generic drug industry. But for a company trying to establish itself as a trusted supplier to the US market, the reputational damage was severe. Stock price tumbled. Customers questioned contracts. Competitors smelled blood. The response from Aurobindo's leadership was swift but measured: cooperate fully with investigations, strengthen compliance procedures, and most importantly, ensure such allegations could never surface again.

The price-fixing case was still winding through courts when another crisis hit. On June 20, 2019, Aurobindo received a warning letter from the USFDA after an inspection of its drug manufacturing facility in Pydibhimavaram, Srikakulam District, Andhra Pradesh. The warning letter summarized significant deviations from current good manufacturing practices (cGMP) for active pharmaceutical ingredients. FDA warning letters are the regulatory equivalent of a red card in football—they stop new product approvals and can lead to import bans.

The Pydibhimavaram warning letter detailed failures that seemed almost elementary: inadequate investigation of batch failures, insufficient evaluation of process changes, incomplete documentation. For a company of Aurobindo's sophistication, these weren't capability failures—they were systemic breakdowns in quality culture at that specific facility. The root cause analysis revealed an uncomfortable truth: rapid expansion had outpaced the development of quality systems and personnel training.

But the regulatory challenges weren't limited to the FDA. In April 2018, Aurobindo was featured in the Dutch documentary television program Zembla, which detailed accusations of environmental damage and poor working conditions at their Hyderabad facilities. The footage was damaging—waste water discharge, workers without proper protective equipment, local communities complaining of pollution. For European customers increasingly focused on ESG criteria, this was a crisis that transcended regulatory compliance.

The product recalls of 2018 and 2019 added another layer of complexity. Aurobindo Pharma USA recalled tablets containing valsartan due to the detection of N-Nitrosodiethylamine (NDEA), a probable human carcinogen. In November 2019, they recalled ranitidine tablets, capsules, and syrup due to unacceptable levels of N-nitrosodimethylamine (NDMA). These weren't manufacturing failures unique to Aurobindo—the entire industry was grappling with nitrosamine impurities. But each recall eroded trust and reinforced the perception of quality problems.

The October 2019 observations from the USFDA for the Unit-7 formulation plant in Telangana regarding potentially misleading documentation caused share prices to drop over 20%. Investors were losing patience. The cumulative effect of regulatory actions was threatening to undo years of reputation building. Something had to change, and it had to change dramatically.

Aurobindo's response to these challenges revealed organizational maturity. Instead of treating each issue in isolation, they initiated a comprehensive quality transformation program. External consultants were brought in—not to window-dress for regulators but to fundamentally redesign quality systems. The company invested over $100 million in upgrading facilities, implementing electronic batch records, and establishing a centralized quality command center that monitors all global operations in real-time.

The human element was equally important. Aurobindo instituted a "Quality First" program that went beyond training to change mindsets. Quality metrics became part of performance evaluations at all levels. A confidential whistleblower system was established, allowing employees to report concerns without fear of retaliation. Most significantly, quality leaders were given veto power over commercial decisions—if quality said no, the product didn't ship, regardless of commercial implications.

The environmental and labor concerns raised by the Zembla documentary prompted a separate but parallel transformation. Aurobindo invested in zero-liquid discharge systems, upgraded worker safety equipment, and began publishing detailed sustainability reports. They engaged with local communities, establishing health clinics and education programs. This wasn't just corporate social responsibility theater—it was recognition that sustainable operations require social license, especially in densely populated areas like Hyderabad.

The remediation efforts began showing results by 2020. FDA inspections, while still finding observations, no longer resulted in warning letters. The frequency and severity of product recalls decreased. Customer audit scores improved. Most tellingly, new product approvals resumed at pre-crisis levels. Aurobindo had learned a painful lesson: in pharmaceuticals, quality isn't just about compliance—it's about survival.

The legal resolution of the price-fixing allegations remains ongoing, but Aurobindo has implemented robust antitrust compliance programs. All customer interactions are documented. Price discussions require legal review. Training on antitrust law is mandatory for all commercial personnel. The message from leadership is clear: better to lose a deal than violate antitrust law.

What's remarkable about Aurobindo's navigation of these challenges is how they've emerged stronger. The quality improvements made under regulatory pressure have actually enhanced operational efficiency. The environmental investments have reduced long-term costs. The enhanced compliance programs have made the company a more attractive partner for Big Pharma collaborations. Sometimes, crisis catalyzes transformation in ways that comfortable success never could.

VIII. Innovation & Future Bets: Biosimilars, Specialty, and Beyond (2020–Present)

The conference room in Hyderabad's genome valley was buzzing with nervous energy. It was early 2020, and Aurobindo's board was about to make their biggest strategic bet since entering the US market. The proposal on the table: invest over $500 million in biosimilar development, entering a field dominated by giants like Samsung Biologics and Amgen. For a company built on small-molecule generics, this was venturing into uncharted territory. "We're either five years too late or perfectly timed," Ramprasad Reddy remarked. History would prove it was the latter.

Aurobindo Pharma plans to expand its product portfolio with high-value products in oncology, hormones, biosimilars and novel drug delivery solutions like depot injections, inhalers, patches and films. This wasn't diversification for its own sake—it was recognition that the traditional generics market was maturing. Price erosion in simple generics was accelerating. Biosimilars, complex generics, and specialty products offered better margins and longer competitive windows.

The biosimilar strategy crystallized around CuraTeQ Biologics, Aurobindo's dedicated biologics subsidiary. Unlike small molecules that can be perfectly copied, biologics—proteins produced in living cells—can only be approximated. This complexity creates significant barriers to entry: development costs of $100-200 million per product, development timelines of 6-8 years, and regulatory requirements that approach those of new drugs. But the rewards match the risks—biosimilar markets face less competition and command higher prices than traditional generics. The validation of Aurobindo's biosimilar strategy came in May 2024 when TheraNym Biologics, a wholly owned subsidiary of Aurobindo Pharma Ltd, signed a pact with Merck & Co. for expanding its biologics manufacturing facilities and exploring contract manufacturing operations for biologics. The deal involved TheraNym investing approximately ₹1,000 crore in establishing a state-of-the-art facility in Borapatla, Telangana, featuring large-scale bioreactors for mammalian cell culture products and a vial-filling isolator line capable of producing 25-30 million vials annually.

This wasn't just a contract manufacturing deal—it was Aurobindo's entry ticket to the elite club of global biologics manufacturers. The CEO of CuraTeQ described it as India's potential "WuXi moment," referencing how WuXi Biologics had transformed China into a biologics manufacturing powerhouse. The facility would be unique in offering both drug substance and finished product capabilities under one roof, a rare proposition in the biologics CDMO space. But biosimilars weren't the only frontier. The approval of Rivaroxaban Tablets USP (generic Xarelto) to be launched in Q1 FY26 represented Aurobindo's push into complex generics. With an estimated US market size of $447 million for the 2.5mg strength alone and $8.5 billion for all strengths, this single product could significantly impact revenues. The approval came after years of development and patent challenges, showcasing Aurobindo's ability to navigate the complex landscape of paragraph IV litigation.

The innovation strategy extended beyond products to delivery systems. Depot injections, inhalers, patches, and films weren't just line extensions—they were attempts to create differentiation in commoditized markets. A depot injection that reduces dosing frequency from daily to monthly commands premium pricing. An inhaler with superior delivery characteristics can capture market share even in generic markets. These weren't moonshots; they were calculated bets on incremental innovation that could generate outsized returns.

R&D expenditure at ₹450 crore, representing 5.6% of total revenue, might seem modest compared to Big Pharma's double-digit R&D spending. But Aurobindo's R&D is laser-focused on commercial outcomes. Every project has a clear path to market, defined revenue potential, and identified customers. This isn't blue-sky research—it's targeted development aimed at specific market opportunities.

The organizational structure for innovation reflects this pragmatism. Rather than a centralized R&D organization, Aurobindo operates multiple focused units: CuraTeQ for biosimilars, Eugia for specialty injectables, separate teams for complex generics and novel delivery systems. Each unit operates with entrepreneurial autonomy while leveraging the parent company's infrastructure. It's Silicon Valley's subsidiary model applied to pharmaceutical development.

What's particularly impressive about Aurobindo's innovation strategy is its timing. They're entering biosimilars just as the first wave of blockbuster biologics loses patent protection. They're developing complex generics as pricing pressure makes simple generics uneconomical. They're building CDMO capabilities as Big Pharma increasingly outsources manufacturing. This isn't coincidence—it's strategic positioning for the next decade of pharmaceutical industry evolution.

The risks are substantial. Biosimilar development can fail at any stage. Complex generics face the same pricing pressures as simple generics once multiple competitors enter. CDMO relationships depend on maintaining quality standards that one slip-up can destroy. But Aurobindo has shown they can manage complexity and risk. Their journey from a single penicillin plant to a global pharmaceutical company suggests they have the operational discipline to execute this ambitious innovation agenda.

IX. Financial Performance & Unit Economics

The numbers tell a story of transformation, but you have to know how to read them. Aurobindo's current revenue (TTM) of $3.62 billion USD, up from $3.33 billion in 2023, might seem like modest growth for a company with such ambitious plans. But in the generic pharmaceutical industry, where price erosion of 5-10% annually is normal, any revenue growth represents significant volume gains and successful product mix management.

The geographic revenue mix reveals the strategic choices: United States (46.5%), Europe (31.2%), India (12%), and others (10.3%). This isn't accidental distribution—it's deliberate portfolio construction. The US provides high margins but concentrated risk. Europe offers stability but lower margins. India and other markets provide growth but require local presence. The mix has shifted over the years as Aurobindo consciously reduced US concentration from over 60% five years ago. The Q3FY25 results tell a more nuanced story. Aurobindo reported an 8.5% YoY increase in revenue from operations, reaching ₹7,979 crore, marking its highest-ever quarterly revenue. Yet net profit declined 10% YoY to ₹846 crore, primarily due to weaker sales in the US market. This divergence between revenue growth and profit decline illustrates the fundamental challenge of generic pharmaceuticals: volume growth being offset by price erosion.

The margin dynamics reveal the complexity of Aurobindo's business model. Gross margins at 58.4% seem healthy, but this includes high-margin specialty products offsetting commodity generics. The EBITDA margin of 20.4% is respectable but has compressed from 21.8% a year earlier. R&D expenditure at ₹450 crore represents 5.6% of total revenue—a delicate balance between investing for the future and maintaining current profitability.

The unit economics vary dramatically by product category. A simple generic antibiotic might generate gross margins of 30-40%, while a complex injectable could yield 70-80%. Biosimilars, still in development, promise margins above 60% but require upfront investments that won't pay off for years. The API business, facing pricing pressure from Chinese competition, operates on razor-thin margins but provides strategic value through vertical integration.

Capital allocation has been disciplined but aggressive. Net debt reduction of $84 million in Q3FY25 while maintaining capital expenditure of $106 million shows financial prudence. The company generates sufficient cash flow to fund both growth investments and debt reduction—a balance many pharmaceutical companies struggle to achieve. The 400% interim dividend announced in FY25 signals confidence in cash generation capacity.

The working capital management deserves special attention. In an industry where payment terms can stretch to 180 days, Aurobindo maintains a cash conversion cycle of approximately 120 days. This efficiency in converting sales to cash provides the liquidity needed for opportunistic acquisitions and rapid scaling of new products.

Competition impacts the financial model in complex ways. When Aurobindo is first-to-market with a generic, they might capture 60-70% market share at premium pricing. As competitors enter, market share drops to 20-30% and prices collapse by 70-80%. The financial model depends on having enough product launches to offset the natural decay of existing products—a pharmaceutical treadmill that never stops.

The 10% year-on-year decline in net profit despite revenue growth isn't necessarily alarming—it's the reality of generic pharmaceuticals. What matters is whether Aurobindo can maintain this delicate balance while transitioning to higher-margin products. The investments in biosimilars, complex generics, and CDMO capabilities suggest management understands that the current model, while generating substantial cash, needs evolution to sustain long-term value creation.

Currency dynamics add another layer of complexity. With 88% of revenues from international markets but significant costs in Indian rupees, Aurobindo benefits from rupee depreciation. A 5% weakening of the rupee against the dollar can add 200-300 basis points to margins. This natural hedge has been a tailwind, but it's not a strategy—it's luck that can reverse.

Looking forward, the financial trajectory depends on three factors: successful biosimilar launches that can command premium pricing, maintaining discipline in the US generics market despite pricing pressure, and leveraging the European platform for stable, if unspectacular, returns. The numbers suggest Aurobindo has the financial strength to navigate this transition, but execution will determine whether they emerge as a differentiated pharmaceutical company or remain trapped in the commodity generics treadmill.

X. Playbook: Business & Investing Lessons

If you were to distill Aurobindo's journey from a single penicillin plant to a $8.77 billion global pharmaceutical company into actionable lessons, what would they be? The playbook isn't about pharmaceutical manufacturing—it's about building a global business from an emerging market, creating value in commoditized industries, and managing complexity at scale.

Lesson 1: Vertical Integration as Competitive Moat Aurobindo's decision to backward integrate into APIs when everyone else was focusing on formulations seemed contrarian in the 1990s. Today, it's their superpower. When supply chains break, when raw material prices spike, when quality issues emerge at suppliers—Aurobindo keeps running. The lesson isn't just about owning your supply chain; it's about controlling the variables that determine your destiny. In commoditized industries, the company that controls the most variables wins.

Lesson 2: Regulatory Capability as Strategic Asset Most companies view regulatory compliance as a cost center. Aurobindo turned it into a competitive advantage. Their ability to navigate FDA, EDQM, PMDA, and dozens of other regulatory bodies isn't just about following rules—it's about understanding that in pharmaceuticals, regulatory approval is the product. The actual tablet is a commodity; the approval to sell it is the asset. Companies that master regulatory complexity can enter markets others can't, charge premiums others can't justify, and build relationships others can't replicate.

Lesson 3: Geographic Diversification Beyond Risk Mitigation The conventional wisdom says geographic diversification reduces risk. Aurobindo proved it can also create value through regulatory arbitrage, pricing optimization, and portfolio management. A product that's commoditized in the US might still command premiums in Portugal. A regulatory approval in one country can accelerate approval in another. Geographic diversification isn't just about spreading risk—it's about creating options.

Lesson 4: Acquiring Distressed Assets and Turning Them Around Aurobindo's acquisition strategy—buying underperforming assets from distracted sellers—requires operational excellence, not financial engineering. The Actavis European assets, Generis in Portugal, Apotex operations—all were struggling when acquired. Aurobindo's playbook: maintain local commercial presence, upgrade manufacturing through Indian operations, expand product portfolio, achieve profitability within 18-24 months. This isn't venture capital-style betting on potential; it's operational transformation of existing assets.

Lesson 5: Managing Complexity Through Decentralization With 29 facilities, 150+ countries, thousands of products, and multiple regulatory regimes, Aurobindo should be drowning in complexity. Instead, they manage it through radical decentralization. Each major unit—APIs, US formulations, Europe, specialty—operates with significant autonomy. Central control focuses on capital allocation, regulatory strategy, and technology transfer. The lesson: at scale, command-and-control breaks down. Federated structures with clear accountability work.

Lesson 6: Long-term Thinking in Short-term Industries Generic pharmaceuticals is a brutally short-term industry. Quarterly pricing pressure, annual tender cycles, constant competitive threats. Yet Aurobindo makes decade-long bets: building biosimilar capabilities, establishing CDMO relationships, creating regulatory infrastructure. They accept short-term margin pressure for long-term positioning. In commoditized industries, the companies thinking in decades beat those thinking in quarters.

Lesson 7: Building Trust After Violations The price-fixing allegations, FDA warning letters, environmental controversies—any one could have been fatal. Aurobindo's response playbook: acknowledge quickly, fix comprehensively, communicate transparently, and emerge stronger. They didn't just address the specific violations; they rebuilt entire quality systems. The lesson: in regulated industries, trust once broken is hard to rebuild, but companies that genuinely transform can emerge with enhanced credibility.

Lesson 8: The Power of Boring Businesses Aurobindo doesn't make breakthrough drugs that cure cancer or reverse aging. They make generic antibiotics, blood pressure medications, and diabetes drugs—boring, essential medicines that millions need daily. There's no pricing power, no brand loyalty, no technological moat. Yet they've built a multi-billion dollar business by executing better than competitors in these "boring" categories. The lesson: in boring businesses, operational excellence is the only differentiator, and it's enough.

Lesson 9: Capital Allocation in Capital-Intensive Industries Pharmaceutical manufacturing requires massive capital investment with long payback periods. Aurobindo's capital allocation framework is instructive: prioritize investments with multiple use cases (facilities that can make various products), stage investments to match market development, maintain financial flexibility for opportunistic acquisitions, and never bet the company on a single product or market. This isn't about avoiding risk—it's about taking calculated risks with capped downside.

Lesson 10: Culture as Competitive Advantage The most underappreciated aspect of Aurobindo's success might be culture. The company maintains an entrepreneurial, cost-conscious culture despite its scale. Engineers still think like owners, questioning every expense. Scientists celebrate regulatory approvals like sports victories. This isn't manufactured corporate culture—it's the authentic DNA from when survival was uncertain. The lesson: culture formed in adversity, if preserved through prosperity, becomes a lasting competitive advantage.

These lessons extend beyond pharmaceuticals. Whether you're building a manufacturing business in Vietnam, a software company in Nigeria, or a consumer brand in Brazil, the principles apply: control your critical inputs, master the complexities others avoid, think in decades while executing in quarters, and build trust through consistent delivery. Aurobindo's playbook isn't about making medicines—it's about building a global business from the periphery, and that's a playbook worth studying.

XI. Analysis & Bear vs. Bull Case

The investment case for Aurobindo Pharma presents a fascinating study in contradictions. Here's a company that has delivered remarkable growth over decades yet trades at valuations suggesting modest expectations. It operates in a commoditized industry yet generates substantial cash flows. It faces constant regulatory scrutiny yet maintains operational resilience. Understanding Aurobindo requires weighing these contradictions carefully.

Bull Case: The Transformation Story

The bulls see Aurobindo at an inflection point. With five hundred and twenty-two approved drugs and twenty-two tentative approvals in the US alone, the company has built one of the industry's most robust generic pipelines. Each approval represents years of development, regulatory navigation, and investment—barriers that new entrants can't easily replicate.

The biosimilar opportunity alone could transform Aurobindo's economics. The global biosimilar market is expected to reach $100 billion by 2030, growing at 15-20% annually compared to low single-digit growth for traditional generics. Aurobindo's early investments, particularly the Merck CDMO deal, position them to capture disproportionate value. If even two or three biosimilars achieve commercial success, they could add $500 million in high-margin revenue.

Vertical integration advantages compound over time. While competitors scramble for API supplies or face quality issues with third-party manufacturers, Aurobindo controls its destiny. This integration becomes more valuable as supply chains fragment and regulatory scrutiny intensifies. The company that can guarantee supply with consistent quality commands premium valuations.

The European platform is undervalued by markets focused on US dynamics. Europe offers stable, predictable returns with less dramatic price erosion than the US. Aurobindo's position as a top-10 generic player across eight European countries provides ballast against US market volatility. As European governments push for greater generic penetration to control healthcare costs, Aurobindo is positioned to benefit.

Complex generics and specialty products offer escape velocity from commodity pricing. Products like injectables, inhalers, and depot formulations face less competition and command higher margins. Aurobindo's investments in these capabilities, while expensive upfront, create differentiation in an otherwise undifferentiated market.

The valuation disconnect is striking. At current levels, Aurobindo trades at roughly 15x earnings despite generating consistent cash flows, maintaining strong returns on capital, and investing for future growth. Compare this to branded pharmaceutical companies trading at 25-30x earnings with similar growth rates but higher risk profiles.

Bear Case: The Structural Challenges

The bears see intractable industry dynamics. US pricing pressure isn't cyclical—it's structural. Pharmacy benefit managers consolidate buying power, FDA accelerates generic approvals, and competition from Indian and Chinese manufacturers intensifies. Aurobindo's 46.5% revenue exposure to the US market makes them vulnerable to these dynamics. A 10% price decline in the US requires 15-20% volume growth just to maintain revenues—an increasingly difficult equation.

Regulatory risks remain elevated despite remediation efforts. The history of warning letters, product recalls, and compliance issues suggests systemic challenges that aren't fully resolved. One major regulatory action could shut down a facility, halt new approvals, and destroy years of reputation building. With 29 manufacturing facilities, the surface area for regulatory problems is vast.

The dependence on commoditized products limits pricing power. Despite portfolio expansion, most of Aurobindo's revenue comes from generic drugs where the only differentiation is price. When your product is chemically identical to competitors', you're always one aggressive competitor away from margin compression.

Biosimilar success is far from guaranteed. The development costs are enormous, regulatory pathways remain uncertain, and commercial success requires capabilities Aurobindo hasn't demonstrated. Unlike small molecules, biosimilars require significant marketing effort, physician education, and patient support programs. Big Pharma has advantages in these areas that Aurobindo can't easily replicate.

Management bandwidth is stretched. Running operations across 29 facilities, 150 countries, and thousands of products while simultaneously pursuing biosimilars, complex generics, and CDMO opportunities risks losing focus. The history of pharmaceutical companies suggests that those trying to do everything often excel at nothing.

Competition from Chinese manufacturers intensifies. As Chinese companies improve quality and gain regulatory approvals, they'll pressure pricing across all markets. Aurobindo's cost advantages versus Western competitors disappear when competing against Chinese scale and government support.

ESG concerns could limit institutional investment. The environmental controversies, labor concerns, and governance questions raised by price-fixing allegations make Aurobindo uninvestable for ESG-focused funds. As ESG considerations become mandatory rather than optional, this could structurally limit demand for the stock.

The Synthesis

The reality likely lies between these extremes. Aurobindo is neither the transformed specialty pharmaceutical company bulls envision nor the declining commodity manufacturer bears fear. It's a transition story—a company using cash flows from mature businesses to fund evolution toward higher-value opportunities.

The key variables to watch: biosimilar launch success, US pricing stability, European market dynamics, and regulatory compliance. If two of these four turn positive, the bull case gains credibility. If two turn negative, the bear case dominates.

For investors, Aurobindo represents a classic value-with-options situation. You're buying a cash-generative business at reasonable valuations with free options on biosimilars, complex generics, and CDMO opportunities. The downside is probably limited by cash generation and breakup value. The upside depends on execution of the transformation strategy.

The investment decision ultimately comes down to time horizon and risk tolerance. Short-term investors should probably avoid Aurobindo—too many quarterly variables can disappoint. Long-term investors willing to wait for the transformation might find an asymmetric opportunity. The company that successfully navigates from commodity generics to specialty pharmaceuticals could see multiple expansion that more than offsets any operational challenges.

XII. Epilogue & "If We Were CEOs"

Standing at the helm of Aurobindo Pharma in 2025 would be like captaining a cargo ship while rebuilding it into a speedboat—at sea, in choppy waters, with passengers aboard. The fundamental challenge isn't strategic—the direction toward biosimilars, complex generics, and specialty products is clear. The challenge is execution while maintaining the existing business that funds the transformation.

If we were CEOs, the first priority would be portfolio rationalization. Aurobindo currently manufactures thousands of products across dozens of markets. Many generate marginal returns and consume disproportionate management attention. A ruthless SKU rationalization—cutting the bottom 30% of products by profitability—would free resources for higher-value opportunities. Yes, revenue might decline short-term, but margins and return on capital would improve.

The second move would be doubling down on the CDMO opportunity. The Merck deal validates Aurobindo's biologics capabilities, but it's just the beginning. Big Pharma increasingly wants to outsource manufacturing while retaining intellectual property. Aurobindo should position itself as the trusted manufacturing partner for complex products—the TSMC of pharmaceuticals. This requires different capabilities than generic manufacturing: project management, confidentiality protocols, and customer service excellence.

Geographic focus needs sharpening. Rather than maintaining presence in 150 countries, concentrate on 30-40 markets that offer the best risk-adjusted returns. Deep presence in fewer markets beats shallow presence everywhere. This might mean exiting certain emerging markets where regulatory costs exceed profit potential.

The innovation model needs restructuring. Rather than trying to develop everything internally, create a venture arm that invests in early-stage pharmaceutical companies developing complex generics and specialty products. Provide them manufacturing expertise and regulatory support in exchange for commercial rights. This leverages Aurobindo's strengths while accessing external innovation.

Regulatory compliance should become a source of competitive advantage, not just risk mitigation. Implement real-time quality monitoring using IoT sensors and AI-driven anomaly detection. Make Aurobindo's facilities the most transparent, most inspected, most trusted in the industry. When regulators need a benchmark for good manufacturing practices, they should think of Aurobindo first.

The talent strategy needs upgrading. Generic pharmaceutical manufacturing doesn't attract top talent the way biotech or tech companies do. Create differentiated career paths, equity participation programs, and innovation challenges that make Aurobindo a destination employer. The transformation to specialty pharmaceuticals requires different talent than commodity manufacturing.

Capital allocation should follow a barbell strategy: return excess cash to shareholders while making concentrated bets on transformational opportunities. The current approach of spreading investments across multiple initiatives dilutes impact. Better to make three big bets that could each move the needle than thirty small bets that won't matter even if successful.

Environmental and social initiatives shouldn't be compliance exercises but strategic differentiators. Become the first major pharmaceutical manufacturer to achieve carbon neutrality. Create apprenticeship programs that lift entire communities. Make Aurobindo synonymous with sustainable pharmaceuticals. This isn't just corporate responsibility—it's building a moat that financial engineering can't replicate.

The communication strategy needs overhaul. Aurobindo's story is poorly understood by investors who see just another generic pharmaceutical company. Regular capital markets days, detailed segment reporting, and clear metrics for transformation progress would help markets properly value the evolution underway.

Most importantly, cultural evolution must accompany strategic transformation. The scrappy, cost-conscious culture that built Aurobindo remains valuable, but it needs complementing with capabilities in innovation, customer service, and brand building. This isn't about replacing the old culture but expanding it to embrace new competencies.

The path forward for Aurobindo isn't easy, but it's clear. The company that successfully navigates from commodity generics to specialty pharmaceuticals, from product manufacturer to solution provider, from emerging market challenger to global partner, will create enormous value. The assets are in place, the market opportunities exist, and the management team has proven execution capability.

The next decade will determine whether Aurobindo becomes India's first truly global pharmaceutical champion or remains a successful but ultimately limited generic manufacturer. The difference lies not in strategy but in execution, not in vision but in daily decisions, not in ambition but in operational excellence.

For investors, employees, and other stakeholders, Aurobindo represents both the promise and peril of transformation. Success would validate the thesis that emerging market companies can compete globally not just on cost but on capability. Failure would reinforce the barriers that keep developing world companies trapped in commodity businesses.

The story of Aurobindo Pharma is far from over. In many ways, it's just beginning. The small penicillin plant in Pondicherry has grown into a global pharmaceutical enterprise, but the real test lies ahead: Can a company built on manufacturing excellence evolve into one defined by innovation? Can operational efficiency coexist with creative exploration? Can an Indian company become a global pharmaceutical leader not by copying Western models but by creating its own?

These questions won't be answered in quarterly earnings calls or annual reports. They'll be answered in laboratories where scientists work on next-generation biosimilars, in boardrooms where executives make bet-the-company decisions, and in manufacturing facilities where quality becomes culture rather than compliance.

The journey from Pondicherry to global pharmaceutical leadership isn't complete. In fact, the hardest part—transformation from commodity to specialty, from follower to leader, from emerging to established—has just begun. Whether Aurobindo successfully navigates this transformation will determine not just its own fate but will influence how we think about emerging market companies competing in global industries.

The next chapter of the Aurobindo story remains unwritten. But if the past is any guide, it will be characterized by ambitious goals, operational discipline, strategic opportunism, and the relentless pursuit of making medicines accessible and affordable to patients across the globe. That mission, articulated by two entrepreneurs in 1986, remains as relevant today as it was then. The methods may evolve, the markets may change, the products may advance, but the purpose endures.

And perhaps that's the ultimate lesson from Aurobindo's journey: In industries where products become commodities and advantages erode, purpose provides permanence. The company that remembers why it exists, not just how it makes money, has a north star that survives market cycles, regulatory challenges, and competitive threats. For Aurobindo, that purpose—making medicines accessible and affordable—isn't just corporate rhetoric. It's the reason a small penicillin plant in Pondicherry became a global pharmaceutical force, and it's the reason the best chapters of this story may still lie ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube