IPCA Laboratories: The Antimalarial Giant That Rode the Hydroxychloroquine Wave

I. Introduction & Episode Hook

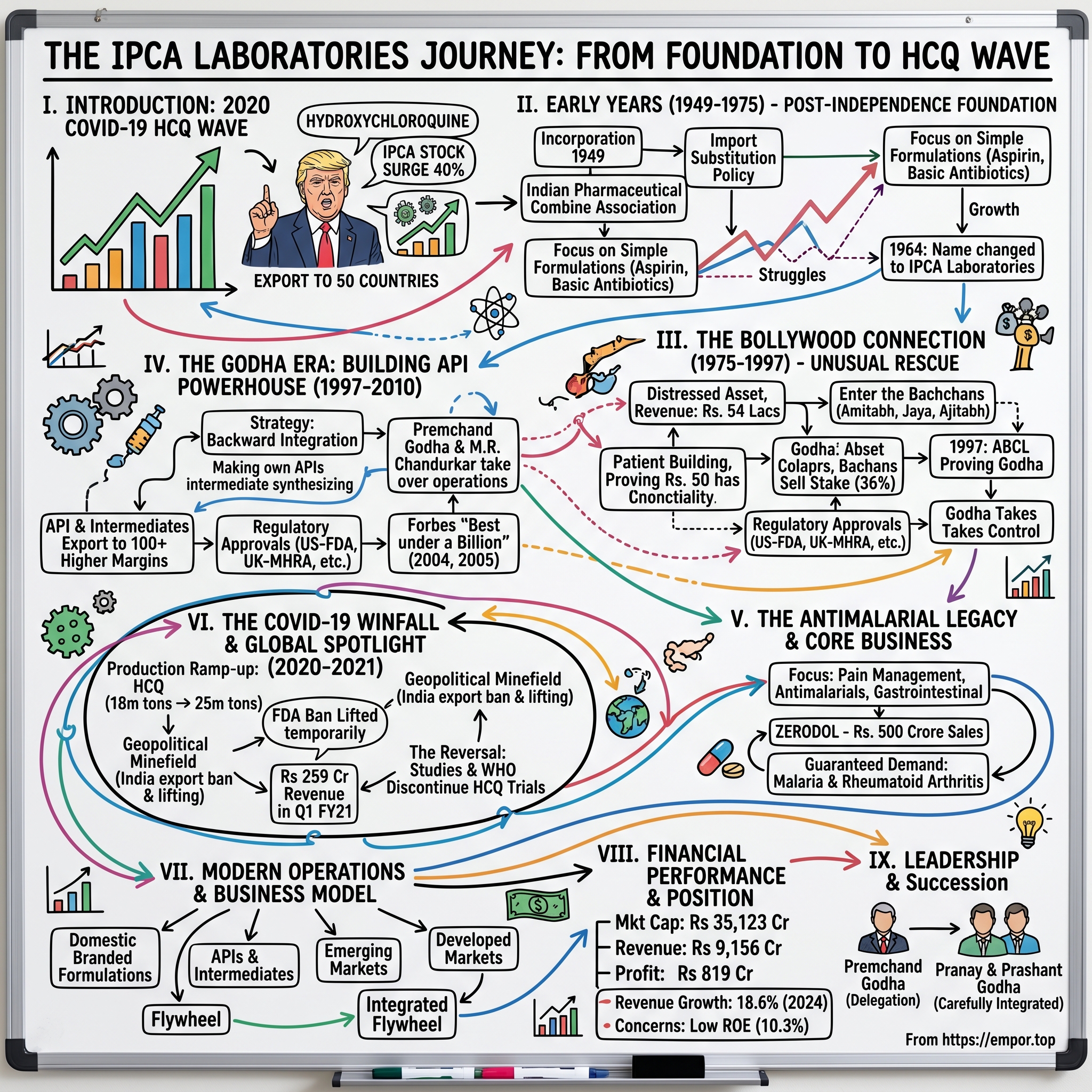

March 21, 2020. As pandemic panic gripped global markets and pharma stocks gyrated wildly, Donald Trump stepped to the White House podium and uttered two words that would send shockwaves through an obscure corner of the pharmaceutical world: "hydroxychloroquine sulfate."

In a nondescript industrial complex in Mumbai's Kandivali suburb, executives at IPCA Laboratories watched their phones explode with messages. The company—one of the world's largest manufacturers of hydroxychloroquine—had just been thrust into the global spotlight. Within days, their stock would surge 40%, export inquiries would flood in from 50 countries, and a 71-year-old antimalarial drug would become the world's most controversial molecule.

But here's what makes this story truly remarkable: IPCA wasn't some Silicon Valley biotech riding a speculative wave. This was a company founded in 1949, just two years after Indian independence, that had quietly built itself into a ₹35,000 crore pharmaceutical powerhouse through decidedly unglamorous means—making generic painkillers and antimalarials that most investors had never heard of.

The IPCA story reads like three distinct acts in Indian corporate history. Act One: A post-independence struggle to build credibility in a nascent industry. Act Two: An unlikely Bollywood detour when the Bachchan family—yes, that Bachchan family—took control in 1975. Act Three: The transformation under chartered accountant Premchand Godha into one of India's most efficient API manufacturers.

How does a company go from ₹54 lakh in revenue when Amitabh Bachchan was chairman to ₹9,156 crore today? How did a farmer's son from Rajasthan who managed Bollywood finances end up building one of the world's most important antimalarial supply chains? And what can the IPCA playbook teach us about building value through operational excellence rather than innovation?

This is that story—of backward integration, Bollywood connections, and how sometimes the most boring businesses create the most extraordinary value.

II. The Early Years & Foundation (1949-1975)

October 19, 1949. The Indian subcontinent was still reeling from partition's wounds when a group of Mumbai businessmen and medical professionals gathered to incorporate a company with an ambitious name: The Indian Pharmaceutical Combine Association Limited. India had been independent for barely two years, and these founders were betting that a nation of 350 million people couldn't forever depend on imported medicines from British and American companies.

The timing was both terrible and perfect. Terrible because India's pharmaceutical infrastructure was essentially non-existent—the country imported 85% of its medicines, local manufacturing meant repackaging imported bulk drugs, and Indian companies were seen as inferior copycats. Perfect because Prime Minister Nehru's government was about to launch an aggressive import substitution policy that would protect domestic manufacturers.

The company's early years read like a chronicle of post-independence industrial struggle. Operating from a small facility in Mumbai, they initially focused on simple formulations—aspirin tablets, basic antibiotics, vitamin supplements. Nothing sophisticated, nothing that required complex chemistry. Just the pharmaceutical equivalent of rice and dal—essential, unglamorous, but desperately needed.

In 1964, fifteen years after incorporation, the company simplified its name to IPCA Laboratories Ltd., dropping the verbose original title. It was a small change that signaled bigger ambitions. By the early 1970s, IPCA had expanded its product line to include antimalarials—a prescient move given India's massive malaria burden. The WHO estimated that India accounted for nearly 80% of Southeast Asia's malaria cases in the 1970s.

But by 1975, IPCA was struggling. Revenue had stagnated, competition from larger players like Glaxo and Pfizer's Indian operations was intensifying, and the company needed both capital and credibility. The founders began searching for new investors who could provide both. What happened next would become one of Indian pharma's most unusual chapters.

The company was about to be saved by India's biggest movie star—though not in the way anyone expected.

III. The Bollywood Connection: Enter the Bachchans (1975-1997)

The meeting took place in a South Mumbai office building in early 1975. On one side sat IPCA's exhausted founders, their company bleeding cash and market share. On the other sat an unlikely rescue team: Amitabh Bachchan, already emerging as Bollywood's "angry young man"; his brother Ajitabh; his wife Jaya, herself a major star; and two men who would prove far more important to IPCA's future—M.R. Chandurkar and Premchand Godha. Premchand Godha's story begins in Village Zeerota in Rajasthan, where he was born into a farming family. After completing his commerce graduation from Ajmer in 1966, he came to Mumbai to pursue chartered accountancy, qualifying in 1971. The young CA from rural Rajasthan had started a practice managing finances for various clients, including an emerging Bollywood star who would soon become India's most famous actor.

Godha had been managing the financial affairs of Amitabh Bachchan and his family, gaining valuable expertise in financial management. It was this connection that brought him to the IPCA opportunity. The Bachchans weren't looking to run a pharmaceutical company—they needed investment diversification. But Godha and his partner M.R. Chandurkar saw something different: a chance to build.

When they acquired IPCA in 1975, the company's turnover was a meager Rs. 50 lacs, with a single formulations manufacturing unit at Mumbai. To put that in perspective, a decent flat in South Mumbai cost about Rs. 2 lacs at the time. This wasn't a trophy acquisition—it was a distressed asset.

The arrangement was unusual even by 1970s standards. Amitabh Bachchan became chairman, bringing celebrity credibility to a company desperately needing it. His brother Ajitabh handled administration. Jaya Bachchan joined the board. But the real work—the unglamorous grind of fixing supply chains, negotiating with suppliers, managing working capital—fell to Godha and Chandurkar.

Godha joined as Director on October 31, 1975, and became Managing Director in March 1983. Those eight years between director and MD tell their own story—of patient building, of proving himself while the Bachchans held the spotlight.

The company began its transformation slowly. They expanded the product portfolio beyond basic formulations to include more complex molecules. They negotiated technology transfer agreements with European companies. They invested in quality control—a radical idea when most Indian pharma companies were content with "good enough."

By the mid-1980s, IPCA had grown to Rs. 5 crore in revenue. Not spectacular, but steady. The Bachchans remained supportive but increasingly distant shareholders as Amitabh's film career exploded with hits like "Deewar" and "Sholay." The real operators were Godha and Chandurkar, methodically building what would become one of India's most efficient pharmaceutical operations. The exit saga unfolded gradually through the late 1990s. In 1997, the Bachchan family sold their 36% stake in IPCA Labs to the company's directors. But the timing tells a deeper story. This was the same year that Amitabh Bachchan Corporation Limited (ABCL)—Big B's ambitious foray into entertainment conglomeration—spectacularly collapsed. The successive failures led to ABCL eventually collapsing in 1997.

ABCL had brought the Miss World pageant to India in 1996, but the event was a financial disaster. The company's film "Mrityudata" flopped. Creditors were circling. "Without a doubt that was one of the darkest moments in my 44-year professional career," Amitabh later recalled. "I looked at the options before me and evaluated different scenarios. The answer came pat - I know how to act. I got up and walked to Yashji (Chopra, filmmaker), who stayed behind my house. I implored him to give me work".

When the Bachchan family hit tough financial times around 1999, they sold their stake in IPCA and ended the association. The family needed liquidity, and their IPCA shares were among the few unencumbered assets. For Godha and Chandurkar, it was the opportunity they'd been waiting for—to finally take full control of the company they'd been effectively running for years.

The irony wasn't lost on industry observers. While Amitabh Bachchan was rebuilding his career through "Kaun Banega Crorepati" and "Mohabbatein," his former chartered accountant was quietly building one of India's most successful pharmaceutical companies. The Bollywood chapter of IPCA was over, but the real transformation was just beginning.

IV. The Godha Era: Building an API Powerhouse (1997-2010)

With the Bachchans gone and full control in their hands, Premchand Godha faced a strategic inflection point. The easy path would have been to continue as a formulations company, importing active pharmaceutical ingredients (APIs) from China and Europe, pressing them into tablets, and selling them with reasonable margins. That's what 90% of Indian pharma companies did in the late 1990s.

But Godha saw what others missed: the entire Indian pharmaceutical industry was built on quicksand. If China decided to restrict API exports, or if currency fluctuations made imports expensive, hundreds of Indian companies would be crippled overnight. The solution was backward integration—making your own APIs, controlling your own destiny.

"Unless we are technologically good, it is better not to make," became Godha's mantra. It sounds simple, almost banal. But in practice, it meant saying no to dozens of lucrative opportunities in favor of building deep expertise in a handful of molecules.

The company began with what it knew best—antimalarials. Chloroquine phosphate and hydroxychloroquine sulfate weren't glamorous molecules. They'd been around since the 1940s, patents had long expired, and margins were thin. But here's what Godha understood: these were essential medicines that would always have demand, and if you could make them cheaper and purer than anyone else, you'd have a defensible business.

By 2000, IPCA had invested heavily in API manufacturing capabilities. They weren't just making the final API—they were synthesizing the intermediates, the precursors to the precursors. Each step backward in the supply chain meant lower costs and higher margins. When competitors were buying 4,7-dichloroquinoline from China at $50 per kilogram, IPCA was making it in-house for $15.

The numbers tell the story. IPCA became a fully-integrated Indian pharmaceutical company manufacturing over 350 formulations and 80 APIs for various therapeutic segments. By the mid-2000s, 79% of APIs and Intermediates business came from exports, serving over 100 countries

The recognition came early in Godha's tenure. In 2004, Forbes selected Ipca, for the second consecutive year as one among the first 200 'Best under a billion company' in Asia. This wasn't just a vanity award—Forbes Asia screened over 20,000 publicly listed companies to identify those with consistent profitability, low debt, and strong governance. For a company that had been struggling just a decade earlier, it was validation that the backward integration strategy was working.

The regulatory certifications told another story of methodical capability building. It also got certification from US Food and Drug Administration (FDA), UK-Medicines and Healthcare products Regulatory Agency (MHRA), South Africa-Medicines Control Council (MCC), Brazil-Brazilian National Health Vigilance Agency (ANVISA) and Australia-Therapeutic Goods Administration (TGA). Each approval meant months of inspections, documentation, and quality system upgrades. But each also opened new markets—the US FDA approval alone meant access to the world's largest pharmaceutical market.

By 2010, IPCA had transformed from a simple formulations company into one of the world's most important antimalarial API suppliers. The foundation was set for what would become the company's defining decade.

V. The Antimalarial Legacy & Core Business

In the pharmaceutical world, there's a saying: "The money is in chronic, not cure." IPCA understood this better than most. While competitors chased blockbuster drugs with billion-dollar price tags and decade-long development cycles, IPCA focused on molecules that had been around since World War II.

Hydroxychloroquine sulfate, first synthesized in 1946, wasn't glamorous. It was introduced as a medicine for malaria 70 years ago, but is now used to treat rheumatoid arthritis. Chloroquine phosphate was even older. But these antimalarials had something invaluable: guaranteed demand. Malaria still killed 400,000 people annually, mostly in Africa and Southeast Asia. Rheumatoid arthritis affected 1% of the global population. These weren't diseases that would disappear with better sanitation or lifestyle changes.

IPCA's approach to antimalarials exemplified their philosophy. They didn't just make the final drug—they controlled the entire value chain. When competitors bought intermediates from China, IPCA synthesized them in-house. This backward integration meant that when China restricted exports during environmental crackdowns, IPCA kept producing while competitors scrambled for supply.

But the real genius was in pain management. "There are several combinations under this brand, which has already achieved the Rs 500-crore sales landmark. We have given a target to make it Rs 1,000 crore", Godha explained about Zerodol. The math was simple: India had 100 million arthritis patients. Each needed daily pain relief. A pill that cost pennies to produce could be sold for rupees. Multiply that by 365 days and millions of patients, and you had a blockbuster without the blockbuster investment.

IPCA's focus area is pain management. "In India we are leaders in anti-malarial and rheumatoid arthritis drugs. The portfolio wasn't random—antimalarials, pain management, gastrointestinal drugs. These were therapeutic areas where patients needed daily medication for years, sometimes decades. No cure meant continuous revenue. No patent meant no expiry date on profits.

By 2019, IPCA's domestic formulation business had grown to over ₹2,500 crore, with 4 of our branded formulations being ranked amongst the top 300 brands of Indian Pharma Market as per IQVIA May 2020. We are also leaders in Pain, Rheumatology, Antimalarials and Haircare therapies. The company employed 6000+ sales & marketing professionals and serve these formulations to more than 2,00,000 doctors across India. With 25 depots and 3200 stockists across the country we are present in every corner of India. Our finished formulations is available at over 5,00,000 retail shops across India.

VI. The COVID-19 Windfall & Global Spotlight (2020-2021)

March 19, 2020. On March 21 President Trump touted hydroxychloroquine – and its biochemical cousin, chloroquine – as potential "game changers" in the battle against COVID-19. Within hours, IPCA's phones started ringing. Export inquiries flooded in from 50 countries. Stock traders in Mumbai bid up the shares 10% at opening. A molecule that had been selling for Rs. 3 per tablet was suddenly the world's most wanted drug.

The timing was extraordinary. HCQ, the drug Trump referred to, has not been sold anywhere in the world as an anti-malarial medicine for decades. It was introduced as a medicine for malaria 70 years ago, but is now used to treat rheumatoid arthritis. Yet here was the American president, the world's most powerful man, essentially giving IPCA free global advertising.

Trump's endorsement of HCQ gave a shot in the arm to IPCA, one of the leading global manufacturers of the time-tested, patent-expired drug. IPCA saw demand soar globally for a month or two. As Covid-19 was pulling down earnings of businesses in the first quarter of FY21, IPCA's business and margin growth was rising, driven by the opportunities on account of chloroquine and hydroxychloroquine API (active pharmaceutical ingredient or bulk drug) and formulations.

The production ramp-up was immediate and dramatic. IPCA increased its HCQ production from 17-18 million tonnes pre-Covid-19 to 25 million tonnes. But this wasn't just about manufacturing capacity—it was about navigating a geopolitical minefield.

India initially banned hydroxychloroquine exports on March 25, wanting to secure domestic supply. Trump's response was swift and threatening—he hinted at retaliation if India didn't release the drug. Within days, India partially lifted the ban. IPCA and Zydus Cadila received orders to produce 10 crore tablets for the Indian government while simultaneously ramping up for export.

The FDA, which had banned IPCA's products from three facilities in 2015 due to quality issues, suddenly granted an exception. Ipca Laboratories says the FDA is lifting a ban on products from two plants so it can ship hydroxychloroquine sulphate and chloroquine phosphate APls along with hydroxychloroquine sulphate tablets to the U.S. Desperate times called for desperate measures.

The numbers were staggering. In an earnings call in August, A.K. Jain, Joint MD, IPCA said overall sales of hydroxychloroquine and chloroquine in relation to Covid-19 in the April-June quarter was around Rs 259 crore and that contributed significantly to the margins of the company. In three months, IPCA had generated what would normally be a year's worth of antimalarial revenue.

During the 10-week period between Feb. 17 and April 27 doctors wrote approximately 483,000 more prescriptions for hydroxychloroquine than in the same time period in 2019. The week after President Trump mentioned the drug during a press conference, prescriptions were up more than 200% compared to the previous year.

But the boom was built on sand. By May, studies were showing hydroxychloroquine didn't work against COVID-19. Some suggested it might even be harmful. The U.S. Food and Drug Administration (FDA) today revoked its emergency use authorization (EUA) for hydroxychloroquine sulfate (HCQ) and chloroquine phosphate (CQ) to treat COVID-19. The two antimalaria drugs, touted by President Donald Trump and others as potential game-changers in tackling the new coronavirus that causes COVID-19, have failed in recent randomized controlled clinical trials to prevent disease in newly infected people or treat those with symptoms.

The reversal was as swift as the rise. By July, the WHO had discontinued hydroxychloroquine trials. Countries that had stockpiled millions of tablets quietly shelved them. IPCA's hydroxychloroquine revenues normalized. The windfall was over.

But here's what separated IPCA from companies that chased every COVID opportunity: they never bet the farm on hydroxychloroquine. They ramped up production when demand spiked, captured the profits when they could, and smoothly transitioned back to normal operations when the bubble burst. No new facilities built, no long-term contracts signed, no stranded assets.

Annual turnover has risen to Rs 4,422 crore, with three-year compounded annual growth rate (CAGR) of 11.87 per cent. During the three-year period, profit after tax (PAT) grew 51.32 per cent. The companys market cap grew 71.16 per cent during October 2019-September 2020. The hydroxychloroquine windfall had accelerated IPCA's growth trajectory, but it hadn't defined it.

VII. Modern Operations & Business Model

Walk through any of IPCA's 18 manufacturing units in India and you'll notice something unusual for an Indian pharmaceutical company: the absence of chaos. No frantic activity, no last-minute scrambles, no heroic firefighting. Just methodical, almost boring, efficiency.

This operational philosophy reflects Godha's worldview. IPCA is a fully-integrated Indian pharmaceutical company manufacturing over 350 formulations and 80 APIs for various therapeutic segments. But unlike competitors who chase every opportunity, IPCA's expansion has been deliberate, almost conservative.

The manufacturing footprint tells the story. Since 1949, Ipca's wide network of manufacturing units has expanded to 15 locations across the globe, including our API manufacturing facility in North Carolina, USA. Each facility specializes in specific molecules or formulations, building deep expertise rather than broad capabilities.

The business model revolves around four distinct segments, each with its own dynamics:

Domestic Branded Formulations: The cash cow. 4 of our branded formulations being ranked amongst the top 300 brands of Indian Pharma Market as per IQVIA May 2020. We are also leaders in Pain, Rheumatology, Antimalarials and Haircare therapies with a steadily growing portfolio. We have a strong team of 6000+ sales & marketing professionals and serve these formulations to more than 2,00,000 doctors across India. With 25 depots and 3200 stockists across the country we are present in every corner of India. Our finished formulations is available at over 5,00,000 retail shops across India.

APIs and Intermediates: The moat. Ipcas APIs and Formulations produced at world class manufacturing facilities are approved by leading drug regulatory authorities including the US-Food and Drug Administration (FDA), UK-Medicines and Healthcare products Regulatory Agency (MHRA), South Africa-Medicines Control Council (MCC), Brazil-Brazilian National Health Vigilance Agency (ANVISA) and Australia-Therapeutic Goods Administration (TGA) with operations in over 100 countries.

Emerging Markets: The growth engine. It is present in over 36 countries of Asia, Africa, CIS, and South America, including Cambodia, Kazakhstan, Kenya, Lagos, Madagascar, Mauritius, Myanmar, New-Zealand, Nigeria, Oman, Russia, Sri Lanka, Sudan, Tanzania, Ukraine, Vietnam and Yemen. These markets offer higher margins than developed countries but require local relationships and regulatory navigation.

Developed Markets: The validation. Selling generics in the US, Europe, and Australia doesn't generate spectacular margins, but it validates quality standards and opens doors in other markets.

The genius is in how these segments reinforce each other. APIs provide cost advantages for formulations. Domestic success funds international expansion. Regulatory approvals in developed markets ease entry into emerging ones. It's a flywheel that gains momentum with each rotation.

VIII. Financial Performance & Market Position

The numbers tell a story of remarkable consistency in an industry known for volatility. Mkt Cap: 35,123 Crore | Revenue: 9,156 Cr | Profit: 819 Cr. These aren't the explosive multiples of a software company or the razor-thin margins of commodity chemicals. They're the steady, predictable returns of a business that has found its sweet spot.

In 2024 the company made a revenue of $1.02 Billion USD an increase over the revenue in the year 2023 that were of $0.86 Billion USD. The 18.6% growth might not grab headlines, but it's been remarkably consistent year after year. No boom-bust cycles, no dramatic pivots, just steady expansion.

The recent quarterly results show this consistency in action. Ipca Laboratories Ltd's revenue jumped 10.8% since last year same period to ₹2,341.51Cr in the Q1 2025-2026. Ipca Laboratories Ltd's net profit jumped 21.31% since last year same period to ₹233.21Cr in the Q1 2025-2026. Note how profit growth outpaces revenue growth—a sign of improving operational efficiency.

But here's the concern that keeps coming up in analyst reports: Company has a low return on equity of 10.3% over last 3 years. In a sector where peers like Sun Pharma and Dr. Reddy's deliver ROEs above 15%, IPCA's returns look pedestrian. The company is trading at 5.05 times its book value, suggesting the market values something beyond just the assets on the balance sheet.

The ownership structure provides stability. Promoter Holding: 44.7%—high enough to maintain control, low enough to avoid minority shareholder concerns. The Godha family has never diluted below 40%, even during expansion phases, preferring internal accruals over equity dilution.

What's most interesting is comparing IPCA to its peers. Sun Pharma, with revenues of ₹50,000+ crore, trades at 65 times earnings. Cipla, at ₹25,000 crore revenue, trades at 35 times. IPCA, at ₹9,156 crore, trades at around 42 times earnings. The market is pricing IPCA between generic commodity players and specialty pharma innovators—exactly where its business model sits.

The geographic revenue mix reveals the strategy. Domestic formulations contribute about 35%, APIs and intermediates 25%, with the rest from international markets. This isn't accidental—it's designed to balance growth (emerging markets), stability (domestic business), and validation (developed markets).

IX. Leadership & Management Philosophy

In the conference room of IPCA's Mumbai headquarters, there's a peculiar tradition. Every Monday morning, the executive team meets—but Premchand Godha rarely attends. Godha's management mantra is complete delegation of power. No presidents report to him. "Everyone reports to the three directors, two of whom are my sons. One is a deputy MD. They coordinate with me for guidance", he explains.

This isn't negligence—it's philosophy. In fact, Godha claims that in the last 45 years, he has never met a single doctor to write his company's product. "My policy is that if you are hired for that work, you do it. I believe in you", he says. In an industry where CEOs often micromanage every detail, Godha's approach seems almost reckless. Yet As testimony of the success of this strategy he points out is the number of people who have continued with IPCA for 30, 40 years.

The second generation has been carefully integrated into the business. Mr. Pranay Godha has done his B.Sc. from University of Bombay and has also obtained a degree in M.B.A from the New York Institute of Technology, USA. He has nearly 12 years experience in the field of Marketing and General Management. Mr. Godha was appointed as the Executive Director of the Company with effect from 11th November, 2008.

Pranay Godha has been appointed as Managing Director and Chief Executive Officer (MD & CEO) of Ipca Laboratories Limited with effect from April 1, 2023. The elevation to CEO wasn't sudden—Pranay had spent 15 years learning every aspect of the business, from API manufacturing to international marketing.

His brother Prashant took a different path. Mr. Prashant Godha, is a graduate in commerce and has done Post Graduate Diploma in Business Management and has experience of over 13 years in pharmaceutical Marketing and General Management. He was appointed as an Additional Director on the Board of the Company with effect from July, 2011 and was appointed as Executive Director of the company with effect from 16th August, 2011.

The division of responsibilities is clear. Pranay focuses on operations and strategy as CEO. Prashant handles marketing and new business development. Ajit Kumar Jain, the long-serving Joint Managing Director who joined when revenue was in crores, provides institutional memory and financial oversight as CFO.

But what's most interesting is what hasn't changed with the generational transition. The company still avoids patent litigation. Still focuses on backward integration. Still prioritizes operational excellence over innovation. The younger Godhas haven't tried to transform IPCA into something it's not—they've doubled down on what it does well.

The management team below the board level tells another story. Presidents head each function—R&D (APIs), R&D (Formulations), Operations, Quality Assurance, International Marketing. Many have been with the company for decades. There's Dr. N.A. Vekariya heading API R&D, Shailesh Laul managing formulation operations, Dr. Sanjay Kapadia ensuring quality. Each is an expert in their domain, given complete autonomy within defined parameters.

This structure—strong family control at the board level, professional management at operational level, complete delegation within defined boundaries—has created an unusual culture. It's neither the chaotic entrepreneurialism of a family business nor the bureaucratic rigidity of a professional corporation. It's something uniquely IPCA.

X. Playbook: Strategic Lessons

The IPCA playbook isn't taught in business schools because it violates most conventional wisdom. Don't innovate, integrate backward. Don't chase growth, chase consistency. Don't maximize margins, maximize predictability. Yet it's created one of India's most valuable pharmaceutical companies.

Lesson 1: The Power of Boring "I can keep continuing this company for 100 years with one product," Godha once said about Zerodol. This isn't hyperbole—it's strategy. While competitors chase the next blockbuster, IPCA focuses on drugs that will be needed forever. Malaria isn't going away. Arthritis isn't getting cured. Pain will always need management.

Lesson 2: Backward Integration as Competitive Advantage Nearly 79% of the APIs and Intermediates business is from exports making them one of India's top exporters of APIs, serving over 100 countries around the globe. The core strategic focus has been on backward integration, resulting in superior supply chain reliability and cost competitiveness. When you control your supply chain from basic chemicals to finished tablets, you're insulated from both supply shocks and price volatility.

Lesson 3: Technology Without Romance "Litigation is not part of our company policy. We are doing old, gold standard products. We don't do any new product research. We have a completely different R&D set up meant to develop new generic products - intermediates, API s and formulations. IPCA's R&D isn't about discovering new molecules—it's about making old molecules cheaper and purer.

Lesson 4: Geographic Arbitrage Sell the same product in 100 countries at 100 different prices. What costs $100 in the US might cost $10 in Kenya and $1 in India. The molecule is identical, but the margins vary by geography. IPCA's global footprint allows it to maximize value extraction from each molecule.

Lesson 5: The Family-Professional Balance Family provides vision and values. Professionals provide execution. The Godhas set strategy but don't meddle in operations. Presidents run their divisions like independent businesses. This balance between control and autonomy has created remarkable stability.

Lesson 6: Crisis as Opportunity (But Don't Bet on It) The hydroxychloroquine windfall showed IPCA's ability to capitalize on unexpected demand. But crucially, they didn't restructure the company around it. They ramped up, captured profits, and returned to normal. Windfalls are bonuses, not strategies.

XI. Bear vs. Bull Case & Future Outlook

The Bull Case:

The optimists see IPCA as a coiled spring. India's pharmaceutical market is growing at 10-12% annually, driven by an aging population and expanding health insurance. IPCA's domestic brands, especially in pain management, are perfectly positioned to capture this growth.

Globally, the generic drug market is expected to reach $650 billion by 2030. As patents expire on blockbuster drugs, companies with strong manufacturing capabilities and regulatory approvals will capture value. IPCA's 80+ APIs and approvals across major markets position it well.

The backward integration strategy becomes more valuable as supply chains fragment. Recent geopolitical tensions have made pharmaceutical supply chain security a national priority. Governments are willing to pay premiums for supply security—exactly what IPCA offers.

Biosimilars represent the next frontier. Five years ago, we started research on biosimilars, too, and expect some products to be ready in the next five years, says Godha. If IPCA can replicate its small molecule success in biologics, it could unlock another decade of growth.

The valuation remains reasonable compared to peers. At 42 times earnings, IPCA trades at a discount to specialty pharma companies while offering more predictability than pure generic players.

The Bear Case:

The skeptics point to structural challenges. Company has a low return on equity of 10.3% over last 3 years. In a capital-scarce country like India, this is suboptimal capital allocation. Why invest in a business generating 10% returns when government bonds yield 7% risk-free?

The lack of innovation is a long-term risk. As AI and precision medicine transform drug discovery, companies focused on 70-year-old molecules may find themselves obsolete. IPCA's entire business model assumes the future looks like the past.

China remains a threat. Chinese companies are moving up the value chain from basic chemicals to finished formulations. They have scale advantages IPCA can never match. If China decides to dominate generic pharmaceuticals like it did solar panels, IPCA has no defense.

Regulatory risks are mounting. The FDA's 2015 ban on IPCA facilities (later lifted) shows how quickly fortunes can change. As regulatory standards tighten globally, compliance costs will pressure margins.

The succession question looms. While Pranay and Prashant Godha are capable, they haven't been tested by a real crisis. The transition from founder to second generation is where many family businesses falter.

The Likely Path:

Reality will probably split the difference. IPCA will continue growing at GDP-plus rates, generating steady if unspectacular returns. The domestic business will remain a cash cow. International expansion will provide growth but at lower margins. Biosimilars might work but won't transform the company.

The real question is whether steady competence is enough in a world demanding exponential growth. IPCA's answer, demonstrated over 75 years, is yes. Not every business needs to disrupt or be disrupted. Sometimes, the most radical thing you can do is stay boring.

XII. Epilogue: Lessons for Founders

The conference room in IPCA's Mumbai office has witnessed a remarkable transformation. From ₹54 lakh in revenue when the Bachchans were involved to ₹9,156 crore today. From a struggling manufacturer of basic drugs to one of the world's largest antimalarial suppliers. From Bollywood glamour to pharmaceutical respectability.

But perhaps the most remarkable thing about IPCA's story is how unremarkable it seems. No breakthrough drugs. No patent victories. No massive acquisitions. Just decades of patient building, brick by brick, molecule by molecule.

This is the lesson IPCA offers to founders: not every business needs to change the world. Sometimes the best strategy is to find something the world will always need and become boringly good at providing it. While others chase revolution, you can build wealth through repetition.

Premchand Godha, the farmer's son from Rajasthan who started as Amitabh Bachchan's accountant, understood something profound: in pharmaceuticals, as in life, consistency beats brilliance. You don't need to cure cancer to build a ₹35,000 crore company. You just need to reliably make painkillers cheaper than anyone else.

The great businesses aren't always the ones that make headlines. Sometimes they're the ones making the same tablet they've made for 70 years, just a little better and a little cheaper each time. IPCA proves that in a world obsessed with disruption, there's still value in persistence.

For founders reading this, the message is clear: find your hydroxychloroquine. Not a miracle drug that might change the world, but a boring molecule that the world will always need. Then spend the next 50 years becoming the best at making it. The results might not be exciting, but they'll be profitable.

And in the end, as Premchand Godha knows, boring profits spend just as well as exciting ones.

Final Analysis

IPCA Laboratories represents a fascinating paradox in modern capitalism—a company that has created enormous value by explicitly avoiding value creation as Silicon Valley defines it. No disruption, no innovation, no transformation. Just relentless operational excellence applied to commoditized products.

The company's trajectory from ₹54 lakh to ₹9,156 crore in revenue isn't a hockey stick—it's a steady climb, year after year, quarter after quarter. This consistency, rather than despite it, is the source of IPCA's value. In a volatile industry in a volatile country in a volatile world, IPCA offers something precious: predictability.

The business model—backward integration, geographic diversification, focus on chronic therapies—creates multiple reinforcing moats. None are individually insurmountable, but together they create a formidable competitive position. It would take a competitor years and billions of rupees to replicate IPCA's infrastructure and regulatory approvals.

Yet the company's greatest strength might also be its greatest weakness. The same conservatism that protected IPCA from pharmaceutical boom-bust cycles might blind it to fundamental industry shifts. As personalized medicine, AI-driven drug discovery, and biological therapies transform healthcare, IPCA's focus on 70-year-old molecules looks increasingly antiquated.

The generational transition adds another layer of complexity. Pranay and Prashant Godha are competent operators, but they're inheriting a business built for a different era. Their challenge isn't just maintaining what their father built—it's evolving it without destroying what makes it valuable.

For investors, IPCA offers a clear trade-off: lower returns for lower risk. Company has a low return on equity of 10.3% over last 3 years, but it's unlikely to surprise on the downside. This isn't a lottery ticket—it's a bond with equity upside.

The hydroxychloroquine episode of 2020-2021 perfectly encapsulated IPCA's opportunity and limitation. When the world needed massive quantities of a generic drug immediately, IPCA delivered. But when the world moved on, so did IPCA's windfall. The company can capture temporary dislocations but can't create sustained premium pricing.

Perhaps the most important lesson from IPCA's story is that there are multiple paths to building value. Not every company needs to pursue monopolistic profits through innovation. Sometimes, accepting commodity returns while executing better than competitors is enough. IPCA has built a ₹35,000 crore business on margins that technology companies would find unacceptable.

As India's pharmaceutical industry evolves, IPCA faces a strategic inflection point. Does it continue its conservative approach, accepting steady but unspectacular returns? Or does it use its cash flows to fund more ambitious ventures, risking its hard-won stability for potentially higher rewards?

The answer, knowing IPCA's history, will probably be characteristically boring: a bit of both, but not too much of either. Some investment in biosimilars, but not betting the company. Some geographic expansion, but only to markets they understand. Some product innovation, but nothing that requires real research.

And that might be exactly the right strategy. In a world of black swans and tail risks, being boring has never been more valuable. IPCA Laboratories might never cure cancer or colonize Mars, but it will be there, quarter after quarter, making the pills that help millions of people get through their day with a little less pain.

Sometimes, that's enough.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube