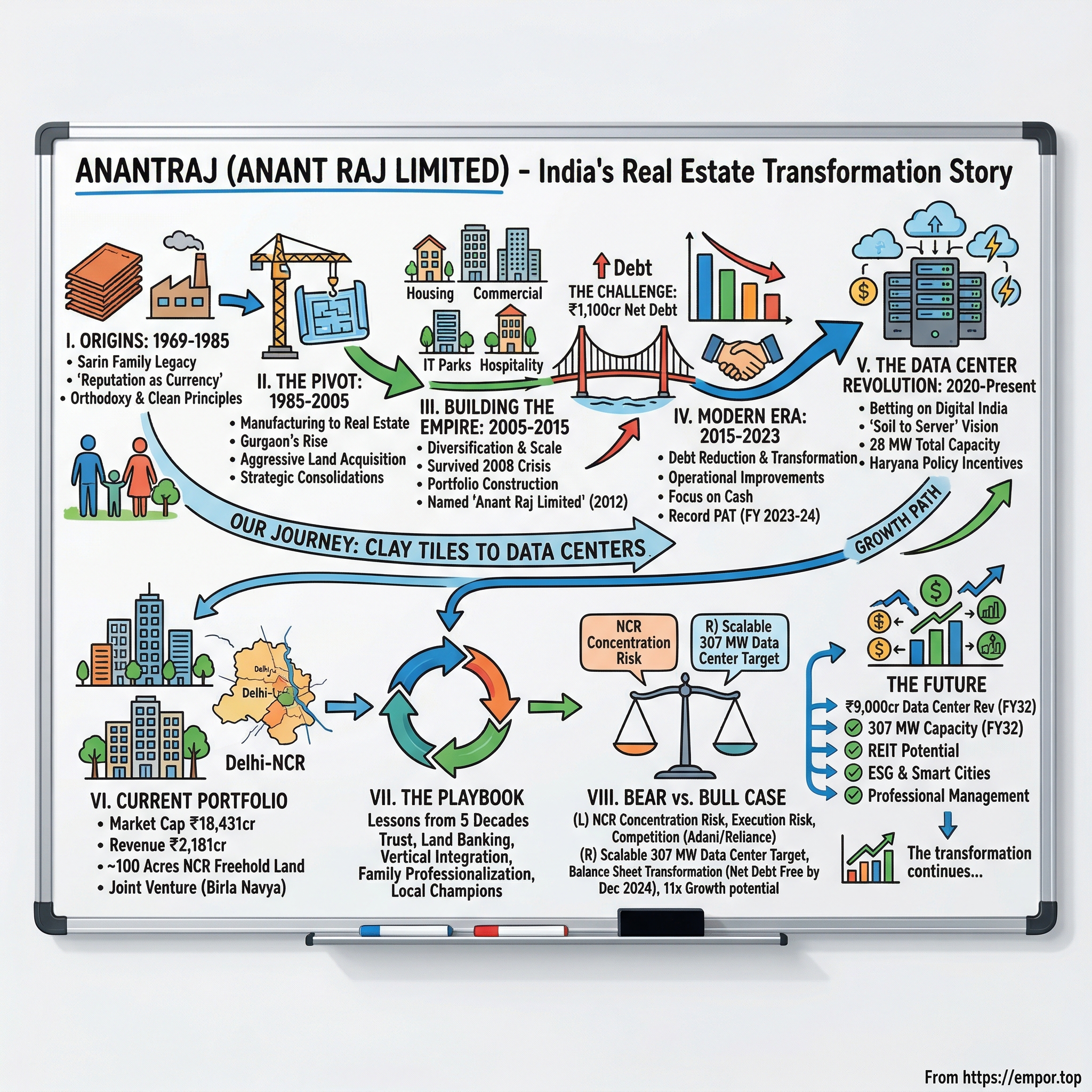

Anant Raj Limited: From Clay Tiles to Data Centers - India's Real Estate Transformation Story

I. Cold Open & The Hook

Picture this: It's 2024, and in the gleaming boardrooms of Gurugram, a 39-year-old company that once manufactured ceramic tiles is fielding calls from global hyperscalers about data center capacity. The transformation is so complete, so audacious, that even seasoned real estate analysts do a double-take. This is Anant Raj Limited—a company that has quietly built a ₹18,000+ crore market capitalization while most investors weren't looking.

The numbers tell a story of metamorphosis: From clay products to controlling 100 acres of prime Delhi-NCR land. From carrying ₹1,180 crore in net debt just three years ago to targeting net-debt-free status by December 2024. From traditional real estate development to projecting ₹9,000 crore in revenue from data centers by FY32.

But here's what makes this story truly remarkable: While DLF and Godrej Properties captured headlines and foreign capital, Anant Raj was methodically acquiring land parcels, building without fanfare, and somehow maintaining what they claim is a litigation-free track record—an almost mythical achievement in Indian real estate. The Sarin family, led by founder Ashok Sarin, built this empire on what they call "orthodox and clean principles," a phrase that sounds quaint until you realize they've actually pulled it off.

This isn't just another Indian real estate story. It's a masterclass in patient capital allocation, strategic pivots, and the power of controlling the entire value chain—from soil to server, as their new tagline goes. How did a ceramic tile manufacturer become one of NCR's largest landowners? Why is a traditional real estate developer now betting its future on data centers? And most intriguingly, how has a family-run business in one of India's most opaque sectors maintained 60% promoter holding while scaling to institutional size?

The answer lies in understanding not just what Anant Raj built, but how they built it—through five decades of India's economic transformation, from the License Raj through liberalization, from the 2008 crisis through demonetization, and now into the digital infrastructure boom. This is that story.

II. Origins: The Sarin Family Legacy (1969-1985)

The year was 1969. Man had just landed on the moon, but in India, the economy was still earthbound, shackled by the License Raj. It was into this environment that Shri Ashok Sarin, armed with little more than ambition and his parents' blessings, laid the foundation of what would become the Anant Raj Group. His parents—Lala Anant Ram Sarin and Smt. Raj Kumari Sarin—weren't wealthy industrialists or political powerbrokers. They were middle-class Delhi residents who understood one fundamental truth: in a capital-scarce economy, reputation was currency. Ashok Sarin wasn't building in Delhi's established real estate corridors. He was working the peripheries, taking on small construction contracts, building relationships with landowners, and most importantly, establishing a reputation for something almost unheard of in Indian construction: completing projects without litigation—a principle he adhered to from scratch, making the company a rarity in the real estate sector.

The pre-incorporation years from 1969 to 1985 were Sarin's apprenticeship in India's byzantine construction industry. This was an era when getting cement required government permits, steel was allocated through quotas, and every project involved navigating a labyrinth of bureaucracy. While others sought shortcuts through political connections or creative accounting, Sarin emphasized nurturing strong relationships with stakeholders, including investors, government authorities, and business partners, focusing on transparency, corporate governance, and ethical practices.

Think about the audacity of this approach. In 1970s India, "orthodox and clean principles" wasn't just a moral stance—it was a competitive disadvantage. Projects took longer. Costs were higher. Growth was slower. But Sarin was playing a different game. He understood that in a trust-deficit market, reputation compounds like interest. Every completed project without a court case, every payment made on time, every promise kept—these weren't just business transactions. They were deposits in a reputational bank account that would pay dividends for decades.

The decision to formalize as Anant Raj Clay Products in 1985 seems puzzling at first glance. Why ceramic tiles? Why manufacturing? The answer reveals Sarin's strategic thinking. In pre-liberalization India, manufacturing offered something construction couldn't: predictable cash flows, easier access to institutional credit, and most importantly, a legitimate platform for land acquisition. Factories needed land. Land could be developed. The ceramic tile business wasn't the end goal—it was the trojan horse.

By 1985, when Anant Raj Clay Products was officially incorporated, Sarin had spent 16 years learning every corner of Delhi's real estate market. He knew which villages would be acquired for development, which farmers were ready to sell, which bureaucrats could be trusted. This wasn't insider information—it was ethnographic knowledge, accumulated through thousands of cups of tea, countless site visits, and relentless relationship building.

The India that Anant Raj was born into was about to change dramatically. Economic liberalization was still six years away, but the seeds were already being planted. The government was beginning to recognize that India's cities needed to grow, that infrastructure needed investment, that the License Raj was strangling entrepreneurship. Sarin, with his clean balance sheet and litigation-free track record, was perfectly positioned for what was coming. The foundation wasn't just built on land and concrete—it was built on trust, patience, and an almost religious commitment to doing business the hard way. As we'll see, this would become Anant Raj's greatest competitive advantage.

III. The Pivot: From Manufacturing to Real Estate (1985-2005)

The ceramic tile factory in Bahadurgarh was humming along nicely by the late 1990s. Orders were steady, margins were respectable, and Anant Raj Clay Products had carved out a decent niche in North India's construction materials market. Any reasonable businessman would have been content. But Ashok Sarin was watching something extraordinary unfold around him: the birth of Gurgaon.

What's now a gleaming symbol of India's economic transformation was, in 1990, little more than agricultural land punctuated by the occasional farmhouse. But Sarin saw what others missed. The Maruti Suzuki factory had been operational since 1983. The Delhi-Jaipur highway was being upgraded. Most critically, Haryana's government had just notified massive land acquisition for what would become the Millennium City. The writing wasn't just on the wall—it was in the gazette notifications that most businessmen never bothered to read. In 2005, the company entered into the new emerging business opportunities in real estate development, marking the beginning of one of Indian real estate's most aggressive acquisition sprees. But this wasn't random empire-building. Sarin had a thesis: consolidate fragmented land holdings in areas about to witness infrastructure development, then leverage that land bank for multiple revenue streams.

The acquisition strategy was surgical. In the first phase, five group companies engaged in development of Hospitality, IT Parks and Service Apartments merged with the company effective from April 1, 2005—Kalinga Meadows Ltd, Sarvodya Builders Pvt Ltd, B T Estates Pvt Ltd, Camation Buildcon Pvt Ltd and Elegant Buildtech Pvt Ltd. In the second phase, three companies were amalgamated in 2006, followed by twelve more group companies including Greenwood Promoters, Jasmine Promoters, Sunrise Buildtech, and Victor Promoters.

Each acquisition brought something specific: land parcels in strategic locations, existing development licenses, or relationships with local authorities. This wasn't just about scale—it was about creating an integrated platform that controlled the entire value chain from land acquisition to project delivery.

Consider the timing. In 2005, India's real estate sector was still largely unorganized. RERA wouldn't exist for another decade. Private equity was just discovering Indian real estate. Most developers were still family operations working on one or two projects at a time. Sarin saw an opportunity to institutionalize before institutions arrived.

The NCR was transforming at breakneck speed. The Delhi Metro's Yellow Line had just opened, connecting Gurgaon to central Delhi. IT companies were setting up massive campuses. Shopping malls were sprouting like mushrooms after monsoon rain. And critically, the Haryana government was liberalizing its licensing policies, allowing private developers to acquire and develop large townships.

Sarin's visionary approach positioned Anant Raj Limited as a key player in the rapidly evolving National Capital Region (NCR). His ability to foresee emerging trends and strategically navigate the market ensured the company's continued expansion and diversification. While competitors fought over prime locations in established areas, Anant Raj was quietly accumulating land in what would become Gurgaon's commercial corridors.

The transformation from Anant Raj Clay Products to Anant Raj Limited wasn't just a name change—it was a complete reimagining of the business model. The ceramic tile operations continued, providing steady cash flow, but they were now a sideshow. The main event was real estate development, and Sarin was positioning his company to be not just a participant but a market maker.

What made this pivot remarkable wasn't just its scale but its execution. Between 2005 and 2010, while navigating the global financial crisis, Anant Raj would go from a tile manufacturer with real estate ambitions to one of NCR's largest landowners. They weren't the biggest—DLF held that crown—but they had something arguably more valuable: a debt-free land bank acquired at historical costs, setting the stage for the next phase of growth.

IV. Building the Empire: Diversification & Scale (2005-2015)

The Lehman Brothers collapse in September 2008 should have been catastrophic for Anant Raj. Global credit markets froze. Indian real estate prices crashed 40% in six months. Developers with aggressive leverage were filing for bankruptcy. DLF's stock fell 90% from its peak. Yet when the dust settled, Anant Raj had not only survived—it had thrived. The secret? They had been conservative when everyone else was euphoric.

The Company successfully developed more than 20 msf of real estate projects in the Housing, Commercial, IT Parks, Shopping Malls, Hospitality, Residential and Affordable Housing sub-segments. This wasn't random diversification—it was calculated portfolio construction. While competitors bet everything on luxury residential, Sarin spread his bets across asset classes, creating natural hedges against market cycles.

The IT park developments were particularly prescient. In 2007, when most developers were chasing residential buyers, Anant Raj was building technology infrastructure. They signed joint ventures with private hotel chains in Delhi, including partnerships with Alstoff Hotels and Atkiens Spence. They even entered into a joint-venture agreement with the Reliance Group for developing two hotels in an SEZ project—a move that seemed contrarian at the time but would prove brilliant as business travel to NCR exploded.

The 2008 crisis became Anant Raj's opportunity. While overleveraged developers were forced to sell assets at distressed prices, Anant Raj was buying. Land prices in Gurgaon fell 50-60% from their 2007 peaks. Construction costs plummeted as contractors desperate for work accepted lower margins. Most importantly, the crisis separated serious developers from speculators. Anant Raj emerged on the other side with an enhanced reputation and a significantly larger land bank.

The Company changed its name from 'Anant Raj Industries Limited' to 'Anant Raj Limited' in October 2012. This wasn't mere rebranding—it signaled the complete transformation from a manufacturing company that did real estate to a pure-play property developer. The ceramic tile business, once the core, was now almost an afterthought.

The period from 2010 to 2015 saw Anant Raj execute what can only be described as a masterclass in capital allocation. They developed commercial properties for lease income, providing steady cash flows. They built residential projects for sale, generating large one-time profits. They held strategic land parcels for appreciation. Each asset class served a specific purpose in the portfolio, creating a self-reinforcing cycle of growth.

But success brought its own challenges. By 2015, Anant Raj had accumulated significant debt—over ₹1,100 crore in net debt. The company had grown rapidly, but it had also become unwieldy. Multiple subsidiaries, complex holding structures, and ambitious projects across segments had created operational complexity. The real estate market was also changing. The government was talking about RERA. Buyers were becoming more sophisticated. Competition was intensifying.

What happened next would define Anant Raj's trajectory for the next decade. The company needed to transform again—from a traditional real estate developer to something more modern, more focused, and critically, less leveraged. The seeds of this transformation were already being planted, though few could see it at the time.

V. Modern Era Transformation: Debt Reduction & Digital Pivot (2015-2023)

The boardroom at Anant Raj's Gurgaon headquarters in early 2016 must have been tense. Net debt stood at over ₹1,100 crore. RERA was about to fundamentally change how real estate worked in India. Demonetization would hit in November, sucking liquidity out of the property market. And most ominously, a new generation of Sarins—Amit, Amar, and Ashim—were pushing for radical changes to how the family business operated.

The transformation that followed was nothing short of remarkable. Net debt at the end of fiscal year 2023-24 stands at ₹267.66 Crore, down from ₹967.27 Crore in FY 2022-23 and ₹1,179.68 Crore in FY 2021-22. This wasn't achieved through financial engineering or asset sales at distressed prices. It was systematic, disciplined deleveraging combined with operational improvements that would make any private equity firm proud.

The strategy had three pillars. First, focus on cash-generating assets. The company shifted from speculative development to projects with clear visibility on sales. Second, improve operational efficiency. This meant rationalizing subsidiaries, streamlining decision-making, and implementing professional management practices. Third, and most importantly, prepare for the digital transformation of real estate.

The company achieved a record turnover of ₹1,520.74 Crore and a Profit After Tax (PAT) of ₹265.93 Crore – the highest in the company's history during FY 2023-24. These weren't just good numbers—they represented a fundamental shift in how Anant Raj operated. The company had learned to generate profits not through leverage and speculation, but through operational excellence and strategic focus.

The leadership transition was equally important. While Ashok Sarin remained the guiding force, the next generation brought fresh perspectives. Amar Sarin and Amit Sarin became CEOs, while Anil Sarin served as Co-Founder & Managing Director. This wasn't the typical Indian family business succession drama. It was a carefully orchestrated transition that preserved institutional knowledge while injecting new energy.

The digital pivot started quietly. While the market focused on Anant Raj's traditional real estate projects, the company was laying the groundwork for something much bigger. They began studying data center economics, understanding cooling technologies, learning about power infrastructure. This wasn't a random diversification—it was a calculated bet on India's digital future.

By 2020, when COVID-19 forced the world online, Anant Raj was ready. They had the land in the right locations—near power grids, with fiber connectivity, away from flood zones. They had the capital, having dramatically reduced debt. Most importantly, they had the conviction that data centers weren't just another real estate vertical—they were the future of real estate itself.

The operational improvements during this period were staggering. The company managed to reduce its overall borrowing cost to below 10%—remarkable for an Indian real estate company. Cash flows improved consistently. The balance sheet strengthened quarter after quarter. This wasn't the Anant Raj of 2015—it was a leaner, more focused, more ambitious company. The stage was set for the next act: the transformation from a real estate developer to a digital infrastructure player.

VI. The Data Center Revolution: Betting on Digital India (2020-Present)

In March 2021, as India was battling the second wave of COVID-19, Anant Raj made an announcement that seemed to come from left field: they were entering the data center business. The real estate community was skeptical. Data centers? Wasn't that for IT companies? The skeptics didn't understand what the Sarins had figured out: data centers are real estate—just with servers instead of residents. Anant Raj has reported the operationalisation of an additional 22 MW of IT load capacity across its data centre campuses in Manesar and Panchkula, Haryana, bringing the company's total capacity to 28 MW, including its cloud services infrastructure. This wasn't incremental progress—it was exponential scaling in an industry where every megawatt counts.

The "Bharat Built: Soil to Server" vision announced at their Technology Day event wasn't just marketing fluff. It captured something profound: Anant Raj wasn't abandoning real estate for technology—they were recognizing that in the 21st century, real estate IS technology infrastructure. Every WhatsApp message, every UPI transaction, every Netflix stream needs physical space, power, cooling, and connectivity. Data centers are the new townships.

The company has projected revenue from its data centre and cloud services business to reach approximately Rs 1,200 crore by FY27, and scale further to nearly Rs 9,000 crore by FY32. The company aims to achieve a total capacity of 63 MW by FY27 and 307 MW by FY32 across key locations including Panchkula, Manesar, and Rai.

What made Anant Raj's data center strategy brilliant wasn't just timing—it was execution. They already owned the land in strategic locations. They had existing structures that could be retrofitted. They understood construction, power management, and cooling systems from decades of building IT parks. Most importantly, they had patient capital and a clean balance sheet to fund the transformation.

The company's data centre and cloud operations are managed through its wholly owned subsidiary, Anant Raj Cloud, focused on building advanced digital and cloud infrastructure in line with India's broader digital economy goals. This wasn't a side project—it was a full-scale commitment with dedicated management and resources.

The locations weren't random either. Manesar, Panchkula, and Rai weren't chosen for their scenic beauty. These sites offered proximity to power grids, fiber optic networks, and crucially, they were far enough from Delhi to avoid pollution and flooding risks but close enough to serve the capital's massive data needs. Haryana has positioned itself as a favourable destination for data centre development through policies such as the Haryana State Data Centre Policy, offering incentives including subsidised power tariffs, single-window clearances, and support for green infrastructure development.

The numbers tell a story of aggressive but calculated expansion. Starting from 6 MW of operational capacity, scaling to 28 MW, targeting 63 MW by FY27, and ultimately 307 MW by FY32—this isn't organic growth. It's a land grab in the digital infrastructure space, executed with the same methodical approach the Sarins used to accumulate physical land in NCR decades ago.

But here's what makes this pivot truly strategic: Anant Raj isn't competing with Adani or Reliance on their terms. They're leveraging their unique advantages—owned land, construction expertise, local relationships—to build a differentiated position in the data center market. While others are buying land at current prices, Anant Raj is converting land bought decades ago. While others are hiring construction firms, Anant Raj is its own construction firm.

The cloud services angle through "Ashok Cloud" adds another dimension. This isn't just about leasing space to hyperscalers—it's about moving up the value chain, offering managed services, capturing more wallet share from enterprise customers. The partnership with Orange Business signals serious intent to compete not just in infrastructure but in services.

As India's data consumption explodes—from 20 GB per user per month today to potentially 100 GB by 2030—the demand for data center capacity isn't linear, it's exponential. Anant Raj's bet is that this demand will overwhelm supply, that location will matter more than ever, and that having ready-to-deploy capacity will command premium pricing. Based on early indicators, they might be right.

VII. Current Portfolio & Market Position

Standing in Sector 63A, Gurugram, you can see the full scope of Anant Raj's ambition. What was once farmland is now a 200-acre integrated township under development, with towers rising against the Aravalli skyline. But the real asset isn't what's being built—it's what lies beneath: a vast, fully-paid, freehold land bank of approx. 100 acres in most prominent locations in Delhi and the National Capital Region earmarked for diverse projects including residential developments, warehousing, and hospitality.

The market has finally noticed. With a market cap of ₹18,431 crore, revenue of ₹2,181 crore, and profit of ₹461 crore, Anant Raj has emerged from the shadows of DLF and Godrej Properties to claim its place among NCR's real estate elite. But unlike its peers who chase pan-India expansion, Anant Raj remains laser-focused on its core geography—a strategy that looks increasingly prescient as NCR's premium real estate market explodes.

The company anticipates an estimated revenue potential of ₹15,000 Crore from residential sales, integrated development in Sector 63A, Gurugram, over the next 4 to 5 years. This isn't speculative inventory hoping for buyers. The Birla Navya project, a joint venture with Birla Estates spread over 43 acres, has seen its first two phases completely sold out, with the third phase 60% sold. The market is voting with its wallets.

The residential portfolio reads like a playbook for capturing every segment of the housing market. Luxury villas for HNIs. Plotted developments for investors. Group housing for young professionals. Affordable housing in Neemrana and Tirupati for the mass market. Each project serves a specific customer segment, but they all leverage the same core advantages: prime locations, clear titles, and the Anant Raj brand that now carries weight in NCR.

Promoter Holding stands at 60.1%—a number that tells its own story. While other developers diluted aggressively during growth phases or distress periods, the Sarin family maintained control. This isn't just about wealth preservation—it's about maintaining the ability to make long-term decisions without quarterly pressure from institutional investors.

The commercial portfolio, often overlooked by analysts focused on residential sales and data centers, generates the steady cash flows that fund everything else. IT parks leased to technology companies, shopping malls serving suburban populations, office complexes housing everything from startups to multinational corporations—these aren't glamorous assets, but they're the bedrock of Anant Raj's financial stability.

What's remarkable about Anant Raj's current position is how they've managed to be both conservative and aggressive simultaneously. Conservative in maintaining low debt, focusing on one geography, keeping promoter control. Aggressive in scaling data centers, launching massive townships, projecting revolutionary growth. It's a balance few Indian real estate companies have managed to strike.

The competitive positioning is unique. DLF is bigger but also more expensive and arguably more exposed to luxury market cycles. Godrej Properties has national presence but lacks Anant Raj's concentrated land bank in NCR. Brigade and Prestige are strong in South India but have limited NCR presence. Anant Raj occupies a sweet spot—large enough to execute massive projects, focused enough to maintain operational excellence, ambitious enough to capture the digital infrastructure opportunity.

Looking at the portfolio today, you see a company in transition. The old Anant Raj—traditional real estate developer, family-run, NCR-focused—still exists. But overlaid on this foundation is the new Anant Raj—data center operator, cloud services provider, technology infrastructure player. The market capitalization suggests investors are betting the new will eventually overshadow the old, but for now, both coexist, creating multiple engines of growth.

VIII. Financial Deep Dive & Turnaround Story

The numbers from Q4 2024-2025 would make any CFO smile: Revenue jumped 21.58% year-over-year to ₹550.90 crore, while net profit jumped 51.46% year-over-year to ₹118.64 crore. But these headline figures only hint at the remarkable financial transformation unfolding at Anant Raj.

The deleveraging journey reads like a Harvard Business School case study in financial discipline. Net debt at the end of fiscal year 2023-24 stands at ₹267.66 Crore, down from ₹967.27 Crore in FY 2022-23 and ₹1,179.68 Crore in FY 2021-22. This wasn't achieved through financial engineering or asset fire sales. It was systematic debt reduction funded by operational cash flows—the hardest but most sustainable path to balance sheet strength.

The company is focused on deleveraging its balance sheet to become a net debt free company by December 2024, reflecting commitment to financial health and operational efficiency. In an industry where leverage is often seen as a sign of aggression and growth, Anant Raj's march toward debt-free status is contrarian—and brilliant. Every rupee not paid in interest is a rupee available for growth capex or distributions.

The cost of capital transformation is equally impressive. The company managed to reduce its overall borrowing cost to below 10%—a remarkable achievement for an Indian real estate company. To put this in context, many developers pay 12-15% for debt, and some stressed developers pay 18% or more. This 200-500 basis point advantage translates directly to the bottom line and provides a sustainable competitive advantage.

The company achieved a record turnover of ₹1,520.74 Crore and a Profit After Tax (PAT) of ₹265.93 Crore – the highest in the company's history, with total income increased by 51.34% and EBITDA grew by 51.54% to ₹371.25 Crore. These aren't just good numbers—they represent a fundamental shift in the quality of earnings. The growth is coming from operations, not financial leverage or one-time gains.

The return on equity improvement tells the real story. When you strip away the leverage and focus on operational returns, Anant Raj is generating ROEs competitive with the best in the industry. But unlike peers who juice returns with debt, Anant Raj's returns are sustainable and growing.

The working capital management deserves special mention. In real estate, working capital is often where profits go to die—money tied up in unsold inventory, delayed collections, extended payment terms. Anant Raj has systematically improved its working capital cycle, accelerating collections, reducing inventory holding periods, and negotiating better payment terms with suppliers.

The capital allocation framework going forward is clear: First, complete the deleveraging to achieve net-debt-free status. Second, fund the data center expansion primarily through internal accruals. Third, maintain sufficient liquidity for opportunistic land acquisitions. Fourth, consider returning capital to shareholders through dividends or buybacks once the growth capex phase moderates.

What's remarkable about this financial transformation is its timing. Anant Raj cleaned up its balance sheet just before the next growth supercycle in Indian real estate and digital infrastructure. While competitors are still dealing with legacy debt from the previous cycle, Anant Raj enters the new cycle with a clean balance sheet, improved credit rating, and access to capital at competitive rates.

The quarterly progression shows accelerating momentum. Each quarter isn't just better than the previous year—it's building on the previous quarter, suggesting operational improvements are compounding. The quality of revenue is also improving, with a higher proportion coming from sales of ready inventory rather than under-construction projects, reducing execution risk and accelerating cash conversion.

Looking at the numbers holistically, you see a company that has learned from the mistakes of the past cycle. The aggressive leverage of 2010-2015 has been replaced by financial conservatism. The scattered approach to development has been replaced by focused execution. The family-run governance has evolved to include professional management. This isn't just a turnaround—it's a transformation into a fundamentally different, better company.

IX. The Playbook: Lessons from Five Decades

The Anant Raj playbook isn't taught in business schools, but perhaps it should be. Over five decades, the Sarins have developed a set of principles that have allowed them to survive and thrive through India's economic liberalization, multiple real estate cycles, regulatory upheavals, and now, digital transformation.

Lesson 1: Trust Compounds Faster Than Capital Shri Ashok Sarin emphasised the importance of nurturing strong relationships with stakeholders, including investors, government authorities, and business partners, with his focus on transparency, corporate governance, and ethical practices earning the company widespread respect and goodwill. In Indian real estate, where trust is scarce and litigation common, Anant Raj's claim of being litigation-free isn't just a legal achievement—it's a competitive moat.

Lesson 2: Land Banking at Historical Cost is the Ultimate Edge While others were flipping land for quick profits, Anant Raj was accumulating and holding. Land bought in the 1990s at ₹10 lakh per acre is now worth ₹10 crore. This patient approach to land banking created a balance sheet advantage that no amount of financial engineering can replicate. When you own land at 1% of current market value, every project is profitable.

Lesson 3: Vertical Integration Reduces Risk Anant Raj's integrated model—owning the land and managing the entire project lifecycle—helps them stay fast, cost-efficient, and reliable in delivery. When you control every step from land acquisition to construction to sales, you eliminate coordination failures, reduce transaction costs, and capture value at every stage.

Lesson 4: Diversification Within Focus Anant Raj diversified across asset classes—residential, commercial, retail, hospitality, data centers—but stayed focused on NCR. This "diversified specialist" approach provided multiple revenue streams while maintaining operational focus and local market expertise. You can be everything to someone or something to everyone, but not everything to everyone.

Lesson 5: Family Businesses Can Professionalize Without Losing Soul The transition from Ashok Sarin to the next generation wasn't a dramatic succession battle but a gradual evolution. The family maintained control while bringing in professional management, modern systems, and institutional practices. They proved that family businesses can modernize without losing their entrepreneurial spirit or long-term orientation.

Lesson 6: Timing Matters, But Time in Market Matters More Anant Raj didn't time the real estate cycle perfectly. They faced challenges in 2008, struggled with debt in 2015, navigated demonetization in 2016. But by staying in the market through cycles, they accumulated knowledge, relationships, and assets that compound over time. Survival is the prerequisite for success.

Lesson 7: Regulatory Complexity Can Be a Moat India's real estate regulations are byzantine—multiple approvals, changing rules, complex compliance. While others see this as a burden, Anant Raj turned it into an advantage. Their ability to navigate this complexity, built over decades, creates barriers to entry for new players and advantages in execution speed.

Lesson 8: Technology Adoption Must Be Strategic, Not Cosmetic The move into data centers wasn't about following a trend—it was recognizing that real estate and technology infrastructure are converging. Instead of building a prop-tech app or virtual reality showrooms, Anant Raj went deep into actual technology infrastructure. Substance over style.

Lesson 9: Conservative Finance Enables Aggressive Growth The paradox of Anant Raj's strategy is that financial conservatism—low debt, high promoter holding, focus on cash flows—enabled aggressive business expansion. When you're not worried about the next interest payment, you can make long-term bets that others can't afford.

Lesson 10: Local Champions Can Win Against National Giants While DLF, Godrej, and others pursued pan-India strategies, Anant Raj doubled down on NCR. They proved that deep local knowledge, relationships, and focus can triumph over scale and geographic diversification. In real estate, all business is local.

These lessons weren't learned in classrooms or consulting presentations. They were forged in the crucible of Indian business, where relationships matter more than contracts, where patience pays more than aggression, where survival is success. The Anant Raj playbook may be specific to their context, but the principles—trust, patience, focus, integration, evolution—are universal.

X. Bear Case vs. Bull Case

Bear Case: The Skeptic's View

The bears have legitimate concerns. Real estate is cyclical, and Anant Raj's concentration in NCR makes them vulnerable to regional downturns. If Gurugram's premium real estate market corrects—as it did in 2008 and 2014—Anant Raj's revenues could face significant pressure. Unlike diversified players with exposure across geographies, they can't offset weakness in one market with strength in another.

The data center ambitions, while exciting, face execution risks. Building and operating data centers requires expertise in power management, cooling systems, network operations—competencies vastly different from traditional real estate development. The projection of 307 MW by FY32 requires flawless execution and massive capital investment. Any delays, cost overruns, or technology challenges could derail these ambitious plans.

Competition is intensifying from multiple directions. In traditional real estate, DLF remains the 800-pound gorilla in NCR with superior brand equity and institutional relationships. Godrej Properties is entering NCR aggressively with its national brand and execution capabilities. In data centers, giants like Adani and Reliance have deeper pockets and potentially better access to global hyperscalers.

Regulatory changes remain a constant threat. The real estate sector faces continuous regulatory evolution—RERA compliance, GST changes, land acquisition laws, environmental regulations. Any adverse regulatory change could impact profitability or delay projects. The data center business faces its own regulatory uncertainties around data localization, power tariffs, and environmental norms.

The concentrated promoter holding of 60.1%, while providing stability, also limits institutional ownership and potentially impacts valuations. Many global funds have maximum exposure limits to companies with high promoter holdings, potentially limiting Anant Raj's access to international capital markets.

Interest rate sensitivity remains high despite deleveraging. Real estate demand is significantly impacted by mortgage rates, and any sustained increase in interest rates could dampen buyer sentiment. Even as Anant Raj reduces its own debt, its customers remain dependent on mortgage financing.

Bull Case: The Believer's Thesis

The bulls see a transformation story just beginning to unfold. The target to scale up to 63 MW by FY27 and 307 MW by FY32 isn't just ambitious—it's backed by concrete assets and execution capabilities. With land already owned and partial infrastructure in place, Anant Raj has significant cost advantages over new entrants who must acquire land at current prices.

The NCR concentration, rather than a weakness, is a strength. NCR represents 30% of India's real estate market by value, contributes significantly to India's GDP, and continues to attract corporate headquarters, embassies, and high-net-worth individuals. Anant Raj's deep local knowledge and relationships in this market create sustainable competitive advantages.

The balance sheet transformation is complete. Achieving net-debt-free status by December 2024 provides enormous financial flexibility. The company can fund growth through internal accruals, access debt markets at competitive rates when needed, and weather any potential downturns without distress.

The ₹15,000 crore residential revenue pipeline over the next 4-5 years provides clear visibility on near-term growth. With projects already launched and partially sold, execution risk is lower than greenfield developments. The strong sales velocity in projects like Birla Navya validates market demand.

Digital infrastructure is a multi-decade megatrend. India's data consumption is growing at 30%+ annually, AI adoption is accelerating, and data localization requirements are expanding. The demand for data center capacity will likely exceed supply for years, supporting strong pricing and returns for early movers like Anant Raj.

The land bank at historical cost is an unmatched advantage. With 100 acres of prime NCR land fully paid for, Anant Raj can generate superior returns on any development. This land bank would cost thousands of crores to replicate at current prices—value not fully reflected in the current market capitalization.

Strong promoter commitment with 60% holding ensures long-term thinking and alignment with minority shareholders. The successful generational transition with second-generation leaders actively involved provides continuity and fresh perspectives.

The integrated business model—from land ownership to development to operations—provides multiple profit pools and competitive advantages. While pure-play developers face margin pressure from land costs and construction inflation, Anant Raj's integrated model provides natural hedges.

The Verdict

Both bears and bulls have valid points. The truth likely lies somewhere in between—Anant Raj is neither a risk-free growth story nor a value trap. It's a complex transformation story with significant opportunities and real challenges. The key question for investors isn't whether Anant Raj will face challenges—they will. It's whether the opportunities, particularly in digital infrastructure, outweigh the risks, and whether management can execute on their ambitious vision while maintaining the financial discipline they've demonstrated over the past five years.

XI. Looking Forward: The Next Chapter

India stands at an inflection point. By 2030, 600 million Indians will live in cities. Data consumption will increase 5x. The economy will double to $7 trillion. In this transformation, companies that provide critical infrastructure—physical and digital—will capture disproportionate value. Anant Raj is positioning itself to be one of these companies.

The NCR opportunity alone is staggering. As India's political capital, corporate hub, and startup ecosystem, NCR will continue to attract talent, capital, and development. The infrastructure investments—new airports, metro expansion, highway development—will further enhance NCR's attractiveness. Anant Raj's concentrated bet on this geography looks increasingly prescient.

The data center expansion roadmap is aggressive but achievable. The shift from 28 MW current capacity to 307 MW by FY32 represents 11x growth—ambitious by any standard. But with hyperscalers signing 10-20 year contracts for capacity, established locations with power and connectivity, and proven execution capabilities, Anant Raj has the ingredients for success.

The potential for a REIT structure adds another dimension to the story. With commercial assets generating stable rental income and data centers coming online with long-term contracts, Anant Raj could potentially launch one of India's first diversified REITs combining traditional real estate and digital infrastructure. This would provide capital recycling opportunities while maintaining operational control.

ESG initiatives, often an afterthought in Indian real estate, are becoming central to Anant Raj's strategy. Data centers consume enormous amounts of power—making renewable energy adoption not just environmentally responsible but economically essential. The company's focus on green building certifications, water conservation, and sustainable development positions them well for ESG-conscious investors.

The next generation's vision extends beyond traditional boundaries. While Ashok Sarin built a real estate company, the second generation is building an infrastructure platform. This isn't just semantic—it represents a fundamental reimagining of what Anant Raj can become. From residential townships that are smart cities to data centers that power India's digital economy, the vision is expansive yet grounded in execution capabilities.

The technology integration goes deeper than data centers. Anant Raj is exploring proptech applications for sales and customer service, IoT integration in commercial properties, and AI-driven project management. This isn't technology for technology's sake—it's about improving operational efficiency and customer experience.

International partnerships are likely as Anant Raj scales. Data center operations require global best practices, hyperscaler relationships, and potentially foreign capital. The company's clean reputation and professional management make them an attractive partner for international players looking for Indian exposure.

The capital allocation framework for the next decade is becoming clear: 40% of capital toward data center expansion, 40% toward residential development, 20% toward opportunistic investments. This balanced approach provides growth while maintaining flexibility.

The human capital transformation is equally important. Anant Raj is hiring from technology companies, consulting firms, and international real estate firms. The culture is evolving from a traditional family business to a professional organization while maintaining entrepreneurial agility.

Looking ahead, the biggest risk might be execution bandwidth. With ambitious plans across multiple verticals, ensuring quality and timely delivery will be challenging. The company's track record suggests they understand this—growth has been measured, not reckless.

The next decade will determine whether Anant Raj becomes a regional champion or a national infrastructure giant. The pieces are in place—prime land bank, clean balance sheet, ambitious vision, execution capabilities. The market opportunity is clear—urbanization, digitalization, infrastructure development. What remains is execution—the daily blocking and tackling of building projects, signing customers, managing costs, and delivering returns.

XII. Conclusion: The Transformation Continues

Anant Raj's story is far from over. What started as a construction business in 1969, evolved into a real estate developer in 2005, and is now transforming into a digital infrastructure player represents not just corporate evolution but adaptation to India's changing economy. The company that once made ceramic tiles now aims to power India's digital transformation—a journey that captures the broader story of Indian business over the past five decades.

The transformation from ₹1,180 crore in net debt to near debt-free status while simultaneously scaling operations and entering new verticals defies conventional wisdom about corporate turnarounds. This wasn't financial engineering—it was operational excellence combined with strategic vision and disciplined execution.

The data center pivot, initially met with skepticism, now looks prescient. As AI drives exponential growth in computing demand, as India enforces data localization, as enterprises move to the cloud, the demand for data center capacity will only accelerate. Anant Raj's early mover advantage, combined with owned land and execution capabilities, positions them to capture significant value from this megatrend.

The family business that professionalized without losing its soul offers lessons for Indian enterprises navigating generational transitions. The Sarins proved that family ownership can coexist with professional management, that long-term thinking can drive short-term performance, that ethical business practices can be a competitive advantage.

The focus on NCR, criticized by some as lack of ambition, emerges as strategic brilliance. While others spread themselves thin across India's diverse and challenging real estate markets, Anant Raj built depth in India's most important economic region. Local expertise, accumulated over decades, cannot be replicated by national players parachuting in with capital and ambition.

The numbers tell a story of transformation: From struggling with debt to generating record profits. From traditional development to digital infrastructure. From family operation to professional organization. From regional player to potential national champion. Each metric—revenue growth, margin expansion, debt reduction, capacity addition—points to a company hitting its stride.

Yet challenges remain real and substantial. Competition intensifies daily. Execution risks multiply with scale. Regulatory uncertainties persist. Technology evolution accelerates. The path from current position to stated ambition requires flawless execution in an imperfect world.

What makes Anant Raj compelling isn't perfection—it's the combination of ambition and capability, vision and execution, innovation and tradition. This is a company that understands both clay tiles and cloud computing, both land acquisition and data center cooling, both relationship building and financial engineering.

The investment thesis ultimately rests on a simple but powerful idea: India's transformation from a $3.5 trillion to $7 trillion economy requires massive infrastructure investment—physical and digital. Companies that can provide this infrastructure efficiently, ethically, and profitably will create enormous value. Anant Raj, with its unique combination of assets, capabilities, and ambition, is positioned to be one of these companies.

As we watch Anant Raj's next chapter unfold, we're not just observing a corporate story—we're witnessing India's economic transformation through the lens of a single company. From clay to cloud, from tiles to terabytes, from Ashok Sarin's vision to the next generation's ambition, Anant Raj embodies the journey of Indian business itself: complex, challenging, occasionally chaotic, but ultimately, full of possibility.

The story that began in 1969 with a young entrepreneur seeking his parents' blessings has evolved into one of Indian real estate's most intriguing transformation stories. Whether Anant Raj achieves its ambitious targets—₹9,000 crore from data centers, 307 MW capacity, net-debt-free status—remains to be seen. But what's clear is that this is a company that has consistently defied expectations, overcome challenges, and emerged stronger from every crisis.

For investors, customers, competitors, and observers, Anant Raj represents something rare in Indian business: a company simultaneously rooted in tradition and reaching for the future, conservative in finance but aggressive in ambition, local in focus but potentially national in impact. The transformation continues, and the best chapters may still be unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube