Teledyne Technologies: From Singleton's Conglomerate to Modern Sensor Empire

I. Introduction & Episode Roadmap

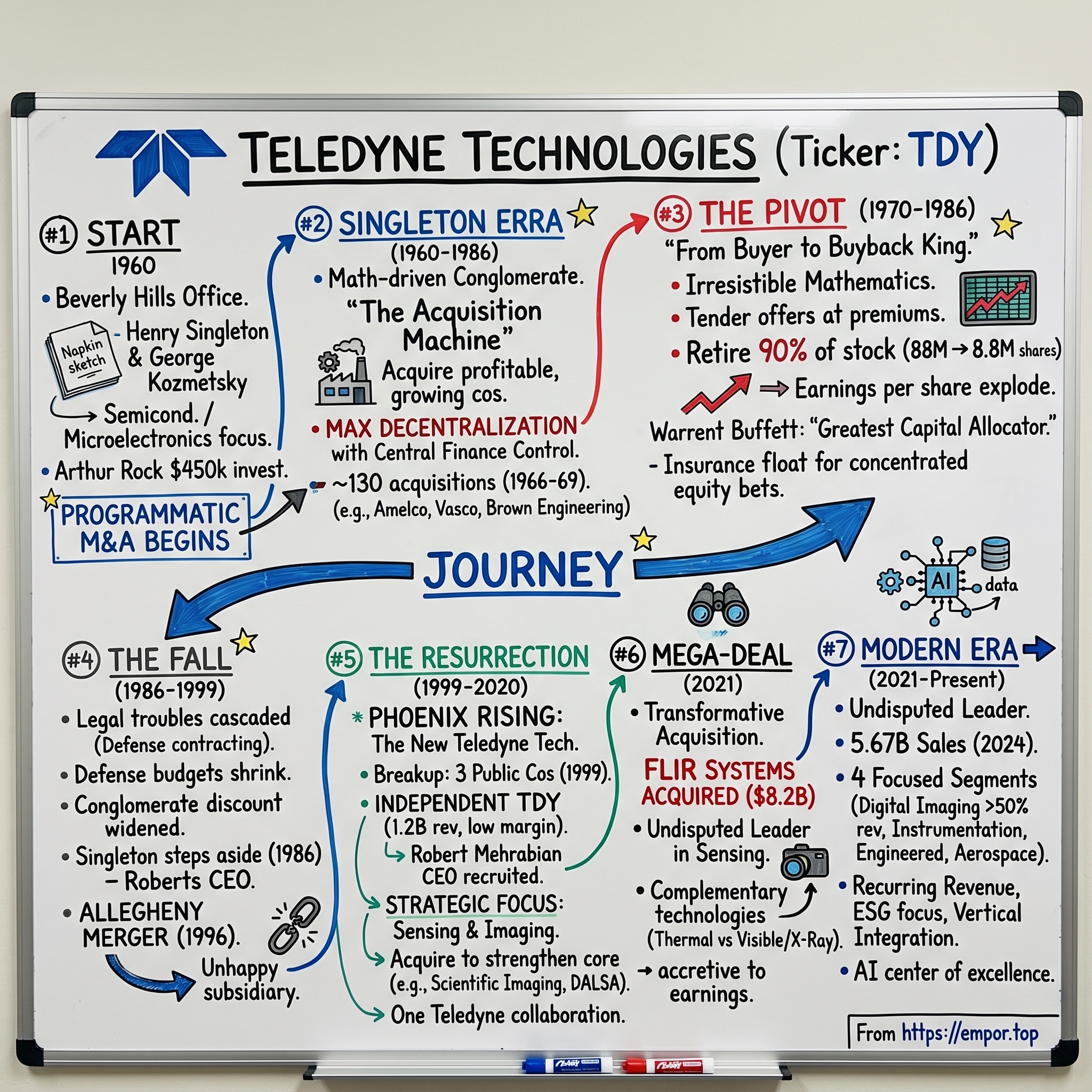

Picture this: A brilliant PhD electrical engineer sits in a sparse Beverly Hills office in 1960, sketching out plans for what he believes will be a semiconductor powerhouse. Fast forward six decades, and that company—after being built into one of history's most legendary conglomerates, dismantled into pieces, and reassembled as something entirely new—commands a $20 billion market capitalization as the undisputed leader in sensing and imaging technologies.

This is the Teledyne story—a corporate odyssey that defies conventional business wisdom at every turn.

The central question that drives this narrative isn't just how Henry Singleton built one of history's greatest conglomerates through 130 acquisitions and then bought back 90% of his own company's stock. It's how a company can completely reinvent itself, shedding its conglomerate skin to emerge as a focused technology leader that's more valuable than ever. It's a masterclass in capital allocation, corporate strategy, and the art of knowing when to zig while everyone else zags.

Why does this matter now? In an era where industrial consolidation is accelerating, where sensors and AI are converging to create entirely new markets, and where the ghosts of 1960s conglomerates still haunt boardrooms from GE to United Technologies, Teledyne offers a playbook that's both cautionary tale and inspiration. The company that once epitomized financial engineering has transformed into the picks-and-shovels provider for the sensor revolution—from autonomous vehicles to climate monitoring, from deep-sea exploration to deep-space imaging.

This story unfolds in three acts: the Singleton era of legendary capital allocation (1960-1986), the painful dismemberment and wandering years (1986-1999), and the phoenix-like resurrection as Teledyne Technologies (1999-present). Along the way, we'll explore how a company can maintain its DNA through radical transformation, why Warren Buffett called Singleton "the greatest capital allocator of all time," and how current CEO Robert Mehrabian orchestrated one of the most successful corporate reinventions in American business history.

The themes that emerge—disciplined capital allocation, the power of decentralized operations with centralized financial control, and the ability to see value where others see only fragments—offer lessons that transcend industries and eras. This isn't just a business story; it's a meditation on corporate evolution, the nature of value creation, and what it really means to build something that lasts.

II. The Singleton Genesis: Founding & Philosophy (1960-1966)

The Beverly Hills restaurant was elegant but not ostentatious—exactly the kind of place where serious men made serious deals in 1960. Henry Singleton, fresh from his bitter departure from Litton Industries, sat across from George Kozmetsky, mapping out their future on a napkin. Both men had watched Tex Thornton promote Roy Ash over Singleton at Litton, a slight that would fuel one of the greatest entrepreneurial stories in American business. "We're not building another Litton," Singleton said quietly. "We're building something better."

Singleton was no ordinary engineer. He'd graduated first in his class at the Naval Academy, earned his PhD in electrical engineering from MIT, and held patents that would revolutionize inertial navigation. But what set him apart wasn't his technical brilliance—it was his ability to see business as a mathematical optimization problem. Where others saw chaos, Singleton saw patterns. Where others chased growth, he chased value.

Their initial company, Instrument Systems, formed in June 1960 with Arthur Rock's $450,000 investment, had a deceptively simple plan: build a major firm centered on microelectronics and control system development. But here's where Singleton's genius first revealed itself—rather than building from scratch, they would acquire. Not the sprawling, ego-driven acquisitions that characterized the conglomerate era, but surgical strikes on undervalued companies with strong cash flows.

The first move came in October 1960 with Amelco, a small electronics manufacturing plant. It wasn't glamorous—Amelco made semiconductor devices for military applications—but it generated cash and gave them a foothold in the fast-growing defense electronics sector. This set the template: acquire profitable, growing companies at reasonable multiples, give their management autonomy, but maintain iron-fisted financial control from headquarters.

By 1961, when the company went public under its new name Teledyne (from the Greek words for "distant" and "force"), Singleton had already articulated his philosophy: "I believe in maximum decentralization. I don't believe in presidents coming to headquarters with their hats in their hands. All we ask is that they perform." This wasn't just management speak—Teledyne's headquarters would never exceed 50 people, even when the company employed over 40,000.

The early financial performance validated the approach. Revenue grew from $4.5 million in 1961 to $89 million by 1965, with net margins consistently above industry averages. But here's what most observers missed: while everyone focused on Teledyne's semiconductor ambitions, Singleton was quietly assembling something far more ambitious. He wasn't building a semiconductor company that happened to make acquisitions; he was building an acquisition machine that happened to start in semiconductors.

The distinction mattered. By 1966, Teledyne had acquired 16 companies across electronics, aviation, and specialty metals. Each acquisition followed Singleton's rigid criteria: the company had to be profitable, growing, available at less than 12 times earnings, and run by management willing to stay on. He turned down ten deals for every one he made, a discipline that would define Teledyne's culture.

What made this period remarkable wasn't just the pace of acquisitions but the method. Singleton pioneered what would later be called "programmatic M&A"—using Teledyne's high-multiple stock (often trading at 30-50 times earnings) to acquire companies trading at 10-12 times earnings. It was arbitrage in its purest form, creating value simply through the transaction itself. Every acquisition was immediately accretive to earnings per share, creating a virtuous cycle that pushed Teledyne's stock ever higher.

But Singleton understood something his imitators didn't: this game had an expiration date. Even as Teledyne's stock soared and acquisition opportunities multiplied, he was already planning for the day when the music would stop. That foresight would soon prove invaluable, setting the stage for one of the most aggressive acquisition sprees in corporate history.

III. The Acquisition Machine: Building an Empire (1966-1969)

George Roberts remembered the exact moment he knew Teledyne had transformed into something unprecedented. Standing in the newly acquired Vanadium-Alloy Steel Company (Vasco) facility in July 1966, watching molten metal pour into molds that would become jet engine components, he turned to Singleton: "Henry, we're not a semiconductor company anymore, are we?" Singleton's response was characteristic: "We never were. We're a capital allocation company."

The Vasco acquisition marked Teledyne's metamorphosis from focused electronics player to full-blown conglomerate. But unlike the ego-driven empire building at ITT or Gulf + Western, every move followed Singleton's mathematical logic. Vasco brought specialty metals expertise, geographic expansion into the Eastern U.S., and most importantly, predictable cash flows from long-term aerospace contracts. Singleton immediately made Roberts president, demonstrating his belief that operational expertise should run operations while he focused on capital allocation.

What followed was perhaps the most disciplined acquisition binge in corporate history. Between 1966 and 1969, Singleton acquired 130 companies—roughly one every ten days. Yet he maintained his strict criteria: no hostile takeovers, no turnarounds, no betting on synergies. Just profitable, growing businesses available at reasonable prices, run by managers who wanted to stay.

The 1967 acquisition of Brown Engineering exemplified the strategy. With 3,500 employees in Huntsville, Alabama, Brown was deeply embedded in NASA's Apollo program and held critical DoD contracts. The price—$23 million in stock—seemed steep, but Singleton saw what others missed: Brown's contracts stretched years into the future, providing the predictable cash flows that would fund further expansion. Within two years, Brown's contributions exceeded the entire purchase price.

By 1969, Singleton had organized Teledyne into 16 Groups managing 94 profit centers across 120 locations. The structure was revolutionary in its simplicity: complete operational autonomy for division presidents, but absolute financial control from Beverly Hills. Division presidents could hire, fire, set strategy, and allocate capital up to certain limits. But they submitted detailed financial reports weekly, and any significant capital expenditure required Singleton's personal approval.

This wasn't the bloated bureaucracy that would doom other conglomerates. Teledyne's headquarters remained lean—fewer than 50 people managing a company generating $1.3 billion in revenue. No human resources department. No investor relations. No business development team. Just Singleton, a handful of financial analysts, and an iron discipline that turned conventional management wisdom on its head.

The numbers from this period remain staggering: sales grew from $89 million in 1965 to $1.3 billion in 1969, while net income soared from $3 million to $60 million. Return on equity consistently exceeded 20%. But the real magic was in the financial engineering. Using stock trading at 40-50 times earnings to buy companies at 10-12 times earnings, every acquisition immediately boosted earnings per share, justifying an even higher stock price, enabling more acquisitions—a perpetual motion machine of value creation.

Wall Street was mesmerized. Analysts struggled to categorize Teledyne—was it an electronics company? An aerospace contractor? A specialty materials producer? Singleton's answer was elegantly simple: "We're in the business of generating returns for shareholders." This wasn't corporate speak; it was mathematical truth. While competitors chased revenue growth or market share, Singleton optimized for one variable: long-term per-share value.

The operational philosophy was equally distinctive. Division presidents never came to Beverly Hills for strategy sessions or budget reviews. Instead, Singleton visited them, usually unannounced, spending days on factory floors and in engineering labs. He could discuss metallurgy with Vasco's engineers, semiconductor physics with Amelco's scientists, and orbital mechanics with Brown's aerospace team. This wasn't micromanagement—it was pattern recognition, gathering data points that would inform future capital allocation decisions.

But even as Teledyne's empire expanded and its stock price soared, storm clouds gathered. The conglomerate boom had attracted scrutiny from regulators and skepticism from a new generation of analysts who questioned whether these sprawling empires could sustain their growth. By late 1969, Teledyne's P/E ratio began to compress, falling from 50 to 30, then 20. Lesser executives might have doubled down on acquisitions, trying to grow their way out of trouble.

Singleton saw opportunity where others saw crisis. If the market would no longer value Teledyne as a growth story, he would transform it into something else entirely. The acquisition machine that had consumed 130 companies was about to reverse direction in one of the most audacious pivots in corporate history.

IV. The Great Pivot: From Buyer to Buyback King (1970-1986)

The Teledyne boardroom in early 1970 was silent as Singleton unveiled his new strategy. "Gentlemen," he said, pulling down a chart showing Teledyne's stock price versus intrinsic value, "we've been sellers of equity at 50 times earnings. Now we have the opportunity to be buyers at 10 times. The mathematics are irresistible." Board members exchanged glances—share buybacks were virtually unheard of in 1970. Companies issued stock; they didn't retire it. But Singleton wasn't interested in convention.

What followed was the most aggressive share repurchase program in corporate history. Over the next 12 years, Teledyne would buy back an astounding 90% of its outstanding shares—from 88 million shares to just 8.8 million. The mechanism was elegant: tender offers at slight premiums to market price, funded by the cash flows from those 130 acquisitions. Every share retired meant remaining shareholders owned a larger piece of an increasingly valuable pie.

The numbers tell a staggering story. Despite minimal revenue growth—sales increased from $1.3 billion in 1970 to just $1.5 billion in 1980—earnings per share exploded from $0.68 to $27.40, a 40-fold increase. Return on equity soared above 30%. The stock price, which had languished around $10 in 1970, would reach $400 by 1986. Shareholders who held through the buyback period earned returns exceeding 20% annually for 15 years.

But Singleton wasn't content with just buybacks. In 1972, he made another contrarian move: building a massive insurance operation. Starting with the acquisition of United Insurance Company of America, Teledyne would eventually amass over $1 billion in insurance float. While Warren Buffett was quietly doing the same at Berkshire Hathaway, Singleton saw insurance differently—not just as a source of cheap capital, but as a option on market volatility.

The insurance portfolio became Singleton's second weapon. Rather than investing float in bonds like traditional insurers, he built concentrated equity positions in undervalued companies. By 1975, Teledyne owned significant stakes in Litton Industries (sweet irony), Curtis-Wright, and Federal Signal. These weren't passive investments—Singleton served on boards, influenced strategy, and occasionally engineered profitable exits. The insurance operation alone generated returns exceeding 20% annually through the 1970s.

The operational discipline during this period was remarkable. While revenue barely grew, margins expanded relentlessly. Division presidents, knowing growth capital wouldn't be forthcoming, focused on efficiency and cash generation. The specialty metals division pioneered new alloys for jet engines. The electronics units developed cutting-edge submarine communications systems. The instruments group created sensors that would fly on the Space Shuttle. Innovation continued, but every dollar of investment had to meet Singleton's hurdle rate: 20% annual returns or higher.

This was when Warren Buffett famously declared Singleton "the greatest capital allocator of all time." In his 1980 letter to Berkshire shareholders, Buffett wrote: "Henry Singleton has the best operating and capital deployment record in American business... if one took the 100 top business school graduates and made a composite of their triumphs, their record would not be as good as Singleton's."

The financial engineering reached its apotheosis in the early 1980s. Teledyne's balance sheet had become a work of art: minimal debt, massive cash generation, and a book value growing at 20%+ annually despite returning enormous amounts of capital to shareholders through buybacks. When hostile takeover artists circled other conglomerates, they avoided Teledyne—Singleton had made it mathematically impossible to acquire at anything approaching a reasonable price.

But the very success created new challenges. By 1985, with only 8.8 million shares outstanding and a stock price approaching $400, Teledyne had become almost too successful. The stock was illiquid, institutional ownership was minimal, and the company that had once been a Wall Street darling was now largely ignored by analysts who couldn't understand its sprawling complexity.

More troubling were operational issues. The defense contracting scandals of the mid-1980s ensnared several Teledyne divisions. The insurance operations, so profitable in rising markets, struggled when interest rates fell. And Singleton himself, now in his 70s, showed signs of stepping back. The company needed fresh leadership and a new strategic direction.

In 1986, Singleton made his final major decision as CEO: stepping aside in favor of George Roberts while remaining chairman. It seemed like a graceful transition, but the Teledyne that Singleton built—a reflection of one man's singular genius—would prove impossible to maintain without him. The empire built on mathematical logic was about to confront the messy realities of corporate succession.

V. The Fall & Dismemberment: Legal Troubles to Allegheny (1986-1999)

The federal investigators arrived at Teledyne Electronic Systems in California on a gray morning in March 1989, armed with subpoenas and questions about billing irregularities on classified Navy contracts. George Roberts, now CEO, watched from his Beverly Hills office as news trucks gathered outside facilities across the country. The mathematical precision of the Singleton era had given way to something messier—the grinding reality of running a defense contractor in the post-Cold War world.

Roberts faced challenges Singleton never had to confront. The defense budget was shrinking. The insurance operations that had generated spectacular returns in the 1970s were bleeding cash as interest rates plummeted. Most critically, the very structure that made Teledyne successful—radical decentralization with minimal oversight—had created pockets of ethical lapses that prosecutors eagerly pursued.

The legal troubles cascaded through the early 1990s. Teledyne pleaded guilty to conspiracy charges related to false testing of electronic components, paying $17.5 million in fines. Another division paid $85 million to settle allegations of improper billing on government contracts. Each revelation eroded the company's carefully cultivated reputation for operational excellence. The stock price, which had reached $400 under Singleton, drifted lower, settling in the $200 range by 1995.

Wall Street's perception had shifted dramatically. The conglomerate structure that Singleton had optimized for tax efficiency and capital allocation flexibility was now seen as an anachronism. Analysts openly questioned the logic of keeping insurance operations, specialty metals, and advanced electronics under one roof. The "conglomerate discount"—the market's tendency to value diversified companies at less than the sum of their parts—widened to 30-40%.

Roberts tried to adapt, initiating modest restructuring efforts and improving compliance systems. But he lacked Singleton's mathematical ruthlessness and capital allocation genius. Where Singleton would have seen opportunity in the depressed stock price and initiated another massive buyback, Roberts pursued a middle path that satisfied no one. The board, increasingly populated by outside directors with little connection to the Singleton era, began pushing for more dramatic action.

The endgame began in 1996 when Allegheny Ludlum Corporation, a specialty steel producer, approached Teledyne about a merger. The logic seemed compelling: combine Allegheny's steel operations with Teledyne's specialty metals division to create a materials powerhouse. But the deal represented something Singleton would have never contemplated—a merger of equals where Teledyne shareholders would own only 60% of the combined entity.

From August 1996 to November 1999, Teledyne existed as an unhappy subsidiary of Allegheny Teledyne Incorporated, a $4 billion amalgamation employing 24,000 people. The cultures never meshed. Allegheny's executives, accustomed to the commodity steel business, couldn't understand Teledyne's defense electronics operations. Teledyne's division presidents, used to radical autonomy, chafed under Allegheny's more traditional corporate structure.

The inevitable breakup came on November 29, 1999, when Allegheny Teledyne split into three separate public companies: Teledyne Technologies (inheriting the electronics and aerospace businesses), Allegheny Technologies (keeping the metals operations), and Water Pik Technologies (a grab bag of consumer products that somehow ended up in the portfolio). Each piece was worth more separately than the whole had been together—a final vindication of the conglomerate discount.

The newly independent Teledyne Technologies was a shadow of Singleton's empire. Annual revenue of $1.2 billion was less than Teledyne had generated in 1969. The company retained 19 of the original Teledyne operations, mostly in aerospace and defense electronics, but lacked strategic coherence. The stock opened at $13 per share, giving the company a market capitalization of just $500 million—roughly what Singleton had paid for individual acquisitions in the 1960s.

Yet hidden within this diminished enterprise were the seeds of resurrection. The electronic systems, instruments, and aerospace operations that survived the dismemberment weren't random leftovers—they were businesses with common threads: advanced sensors, imaging systems, and electronic instruments. These technologies, considered mature and unexciting in 1999, were about to become critical enablers of the digital revolution.

The board's masterstroke was recruiting Robert Mehrabian as CEO. An Armenian immigrant with a PhD in engineering from Oxford, Mehrabian had spent his career in aerospace, most recently as president of Hughes Electronics. He possessed both the technical depth to understand Teledyne's products and the strategic vision to see their potential. More importantly, he understood Singleton's philosophy even if he would apply it differently.

Standing before employees at his first town hall in January 2000, Mehrabian made a promise: "We're going to rebuild Teledyne, not as a conglomerate, but as a focused technology leader. We'll grow organically and through acquisition, but every move will strengthen our core competencies in sensing and imaging." The path forward required abandoning Singleton's pure capital allocation focus for something more operational, more strategic. The phoenix was ready to rise.

VI. Phoenix Rising: The New Teledyne Technologies (1999-2020)

Robert Mehrabian's first strategic planning session as CEO in early 2000 was deliberately held not in a Beverly Hills boardroom but at Teledyne's imaging sensor facility in California. Surrounded by engineers developing infrared detectors for the Mars rovers, he made his vision tangible: "Every acquisition, every R&D dollar, every strategic decision will build toward one goal—becoming the world's premier provider of sophisticated sensing and imaging systems."

The new Teledyne Technologies initially comprised 19 legacy operations generating $1.2 billion in revenue with margins barely reaching 5%. But Mehrabian saw what others missed: these weren't random businesses but complementary pieces of a sensing technology puzzle. The infrared sensors from one division could combine with the signal processing from another and the packaging expertise from a third to create solutions no competitor could match.

His first moves focused on operational excellence rather than financial engineering. Mehrabian instituted what he called "One Teledyne"—breaking down the radical autonomy of the Singleton era to encourage collaboration between divisions. Engineers from the marine instruments group began working with aerospace electronics teams. The digital imaging division shared technology with industrial sensors. This wasn't the suffocating centralization that doomed other conglomerates but targeted integration where it created value.

The acquisition strategy that emerged was radically different from Singleton's approach yet oddly faithful to its spirit. Where Singleton bought anything that met his financial criteria, Mehrabian acquired only companies that strengthened Teledyne's sensing and imaging capabilities. Between 2000 and 2011, Teledyne acquired nearly 80 companies, transforming from 19 operations to almost 100. But every acquisition fit the strategic framework.

The 2006 acquisition of Scientific Imaging Technologies for $27 million exemplified the new approach. The company made specialized CCD sensors for astronomy and life sciences—markets too small for larger competitors but perfect for Teledyne's focused strategy. Within three years, Teledyne had integrated the technology across multiple divisions, selling enhanced sensors for everything from semiconductor inspection to pharmaceutical research. The acquisition paid for itself in 18 months.

By 2011, Mehrabian had organized Teledyne into four focused segments that would define its future: Digital Imaging (from X-ray to infrared sensors), Instrumentation (test and measurement equipment), Engineered Systems (aerospace and defense electronics), and Aerospace and Defense Electronics (communications and avionics). Each segment had clear strategic rationale and compelling growth drivers.

The financial transformation was remarkable. Revenue grew from $1.2 billion in 2000 to $2.4 billion in 2011, but more importantly, operating margins expanded from 5% to 15%. Return on invested capital exceeded 12%. The stock price, which started at $13 in 1999, reached $60 by 2011. This wasn't the explosive multiple expansion of the Singleton era but steady, compound growth built on operational excellence.

The 2014 acquisition of DALSA Corporation for $341 million marked Teledyne's evolution into a true platform company. DALSA brought machine vision technology crucial for factory automation and medical imaging. But more than products, it brought capabilities in CMOS sensor design that Teledyne could leverage across its entire portfolio. Within two years, DALSA technology appeared in products throughout Teledyne's segments, from industrial inspection to defense applications.

Mehrabian also understood something crucial about modern technology markets: recurring revenue matters more than one-time sales. He pushed divisions to develop software, services, and consumables that generated predictable cash flows. By 2015, over 30% of revenue came from recurring sources—service contracts, software subscriptions, and replacement parts. This wasn't as dramatic as Singleton's insurance float, but it provided the stable cash generation needed for continued investment.

The digital imaging segment became Teledyne's crown jewel, growing to over $1 billion in revenue by 2018. The company's sensors flew on the Mars Curiosity rover, enabled the first images from the James Webb Space Telescope, and powered machine vision systems in thousands of factories. Teledyne had quietly become indispensable to multiple industries, holding dominant positions in niche markets too specialized for larger competitors but too technical for smaller ones.

Environmental monitoring emerged as an unexpected growth driver. Teledyne's marine instruments monitored ocean acidification for climate research. Its gas analyzers measured emissions at refineries and power plants. Its spectrometers detected pollutants in water supplies. As environmental regulations tightened globally, demand for Teledyne's monitoring systems soared. By 2020, environmental applications generated over $500 million in annual revenue.

The competitive moat that emerged was different from Singleton's financial engineering but equally powerful. Teledyne's advantage lay in what Mehrabian called "technology fusion"—the ability to combine sensing technologies across wavelengths and applications that competitors with narrower focus couldn't match. A customer needing to inspect semiconductor wafers could get X-ray, infrared, and visible light inspection systems from a single vendor, with software that integrated all three.

By 2020, Teledyne Technologies had achieved what seemed impossible after the 1999 breakup: revenue of $3.1 billion, operating margins of 17%, and a market capitalization exceeding $14 billion. The company that had been written off as conglomerate debris had transformed into a focused technology leader. But Mehrabian wasn't finished. He was about to make his boldest move yet—one that would have made even Henry Singleton take notice.

VII. The FLIR Mega-Deal: Transformative Acquisition (2021)

The video call on January 4, 2021, started like dozens of others during the pandemic—pixelated faces in home offices, muted microphones, the awkward dance of remote dealmaking. But when Robert Mehrabian and FLIR Systems CEO Jim Cannon finally connected, they were about to negotiate the defining transaction of modern Teledyne: an $8.2 billion acquisition that would create the undisputed leader in sensing and imaging technology.

FLIR Systems wasn't just another acquisition target—it was Teledyne's mirror image and perfect complement. Founded in 1978, FLIR had built the world's leading position in thermal imaging, with cameras detecting everything from fever in airports during COVID to gas leaks at chemical plants. With $1.9 billion in revenue and 3,500 employees, FLIR was nearly as large as Teledyne's entire digital imaging segment. This wasn't a bolt-on acquisition; it was a transformation. The strategic rationale was compelling on multiple levels. "At the core of both our companies is proprietary sensor technologies. Our business models are also similar: we each provide sensors, cameras and sensor systems to our customers. However, our technologies and products are uniquely complementary with minimal overlap, having imaging sensors based on different semiconductor technologies for different wavelengths," Mehrabian explained to investors. This wasn't corporate speak—it was technical reality. Teledyne's strength in visible light and X-ray imaging perfectly complemented FLIR's dominance in thermal infrared.

The deal structure reflected lessons learned from both companies' histories. FLIR stockholders would receive $28.00 per share in cash and 0.0718 shares of Teledyne common stock for each FLIR share, implying a total purchase price of $56.00 per FLIR share—a 40% premium based on FLIR's 30-day volume weighted average price. The mix of cash and stock was deliberately calibrated: enough cash to provide certainty and liquidity, enough stock to align interests and share in future upside.

The financing strategy channeled Singleton's discipline while adapting to modern markets. Rather than relying solely on cash or stock, Mehrabian orchestrated a complex but optimal capital structure: $4.5 billion in new debt at historically low interest rates, $2 billion in cash on hand, and $1.7 billion in Teledyne stock. The debt-to-EBITDA ratio would peak at 4.2x—aggressive but manageable given the combined company's cash generation. Within 24 months, Mehrabian projected deleveraging to below 3x through operational cash flow alone.

What made the FLIR acquisition transformative wasn't just size but strategic fit. The combined company would offer what Mehrabian called "a full spectrum of imaging technologies and products spanning X-ray through infrared and from components to complete imaging systems" plus "a complete range of unmanned systems and imaging payload across all domains ranging from deep sea to deep space." No competitor could match this breadth—not Honeywell, not L3Harris, not even larger conglomerates like General Electric.

The integration planning revealed the acquisition's true elegance. FLIR's thermal cameras for industrial inspection complemented Teledyne's X-ray systems for the same applications. FLIR's unmanned systems business—including drone manufacturers Aeryon and Altavian—added platforms for Teledyne's sensors. FLIR's consumer products, while non-core, generated cash that could fund R&D in strategic areas. Even the customer bases were complementary: FLIR was stronger in state and local government, Teledyne in federal; FLIR dominated in Europe, Teledyne in Asia.

Teledyne expected the acquisition to be immediately accretive to earnings, excluding transaction costs and intangible asset amortization, and accretive to GAAP earnings in the first full calendar year following the acquisition. But the real value lay in revenue synergies—opportunities to sell Teledyne products to FLIR customers and vice versa, to combine technologies into new solutions, to leverage combined R&D budgets for breakthrough innovations.

The market reaction was initially mixed. Some investors worried about integration risk, debt levels, and the premium paid. Short sellers circled, betting that Teledyne had overpaid for a company facing its own challenges. FLIR's government business had been declining, its automotive thermal imaging hadn't achieved expected penetration, and COVID had disrupted several end markets.

But Mehrabian had answers for every concern. The integration would follow Teledyne's proven playbook: maintain operational continuity while gradually implementing best practices. The debt would be manageable given combined EBITDA approaching $1.5 billion annually. And the premium? "We're not buying FLIR for what it is today," Mehrabian told analysts, "but for what the combined company can become."

The acquisition closed on May 14, 2021, with Mehrabian noting: "We appreciate the support from our stockholders, and I am delighted to welcome FLIR to the Teledyne family." Edwin Roks, Vice President of Teledyne and President of Teledyne's Digital Imaging Segment, was promoted to Executive Vice President and would continue to serve as President of the Digital Imaging Segment, which now included Teledyne FLIR.

The first year post-acquisition validated Mehrabian's vision. Revenue synergies emerged faster than projected as customers embraced integrated solutions. Operating margins expanded as Teledyne implemented its operational excellence programs across FLIR's facilities. Most importantly, the combined R&D capabilities began producing innovations neither company could have achieved alone—multi-spectral imaging systems that could see through smoke, fog, and darkness; AI-powered threat detection combining thermal and visible imaging; miniaturized sensors for next-generation autonomous systems.

By late 2021, even skeptics acknowledged the acquisition's brilliance. Teledyne had created a sensing and imaging powerhouse with leading positions across multiple spectrums, applications, and end markets. The company that Henry Singleton built through financial engineering had been reborn through technological integration. The transformation was complete, but the story was far from over.

VIII. Modern Era: Market Position & Competitive Dynamics (2021-Present)

The modern Teledyne Technologies headquarters in Thousand Oaks, California, buzzes with an energy unimaginable in Singleton's sparse Beverly Hills office. Engineers collaborate on quantum cascade lasers for detecting chemical weapons. Data scientists develop AI algorithms for autonomous underwater vehicles. Yet the company maintains its disciplined heritage—still lean by corporate standards, still focused on returns over revenue.

Full year net sales for 2024 were $5,670.0 million, compared with $5,635.5 million for 2023, an increase of 0.6%. This modest top-line growth masks a more complex story. The primary driver behind last 12 months revenue was the Digital Imaging segment contributing a total revenue of US$3.07b (54% of total revenue). The FLIR integration has fundamentally transformed Teledyne's revenue mix, with imaging now representing over half of total sales.

The competitive landscape in 2024 looks nothing like the conglomerate battles of the 1960s. Teledyne's primary rivals—Honeywell, Thermo Fisher Scientific, Danaher—are themselves focused technology companies that emerged from their own conglomerate transformations. Each competes in specific niches: Honeywell in industrial automation sensors, Thermo Fisher in life sciences instrumentation, Danaher in environmental monitoring. But none matches Teledyne's breadth across the electromagnetic spectrum or its unique position bridging defense and commercial markets.

Defense and space markets remain Teledyne's bedrock, generating approximately 40% of revenue. The company's sensors fly on virtually every U.S. military satellite, its electronic warfare systems protect fighter jets, and its underwater vehicles map the ocean floor for the Navy. We continue to see robust demand in our longer cycle defense, space, and energy businesses. The return of great power competition has driven defense budgets higher, with particular emphasis on the sensing and intelligence capabilities where Teledyne excels.

But it's the commercial and industrial markets that offer the most compelling growth story. Factory automation drives demand for machine vision systems. Environmental regulations require continuous emissions monitoring. Semiconductor manufacturing needs ever-more-precise inspection systems. Medical device companies integrate Teledyne's imaging sensors into everything from dental X-rays to surgical robots. These markets are less cyclical than defense, offer higher margins, and present opportunities for recurring revenue through service contracts and software subscriptions.

The company's approach to ESG (Environmental, Social, and Governance) reflects its evolution from Singleton's pure capitalism to Mehrabian's stakeholder awareness. Teledyne's environmental monitoring systems help enforce pollution regulations worldwide—a profitable irony for a company with roots in specialty metals and defense contracting. The company has committed to reducing its own carbon footprint by 50% by 2030, while its products enable customers to do the same.

Supply chain management has emerged as a critical capability in the post-COVID era. Unlike companies that offshored production seeking lower costs, Teledyne maintained most manufacturing in the U.S., Canada, and Western Europe. This decision, initially seen as inefficient, proved prescient when semiconductor shortages and logistics disruptions crippled competitors. Teledyne's vertical integration—designing chips, building sensors, and assembling systems—provides resilience that pure-play competitors lack.

The integration of artificial intelligence and machine learning across Teledyne's products represents both opportunity and challenge. AI enhances threat detection in defense systems, enables predictive maintenance in industrial sensors, and improves image analysis in medical devices. But it also requires massive R&D investment and new talent. Teledyne has responded by establishing AI centers of excellence within each business segment and partnering with universities for advanced research.

"In the fourth quarter, we achieved all-time record sales and non-GAAP earnings per share," said Robert Mehrabian, Executive Chairman. "Year-over-year growth accelerated, as our shorter-cycle businesses improved throughout 2024 coupled with strong demand in our longer cycle defense, space, and energy businesses."

The financial metrics tell a story of operational excellence. Operating margin was 18.8% for both the third quarter of 2024 and 2023. Excluding pretax acquired intangible asset amortization expense and pretax FLIR integration costs, non-GAAP operating margin for the third quarter of 2024 was 22.5%, compared with 22.8% for the third quarter of 2023. These margins exceed most industrial competitors and approach software-like levels in some segments.

Capital allocation remains disciplined but different from the Singleton era. During the third quarter of 2024, the Company repurchased approximately 0.3 million shares for $138.8 million, bringing the year-to-date repurchases to $332.6 million through the end of September 2024. Given our record free cash flow in 2024, we ended the year with very low leverage despite $1.1 billion of capital deployment. The company balances growth investment, debt reduction, opportunistic buybacks, and strategic acquisitions—a more nuanced approach than Singleton's binary strategy.

Looking ahead, the company's management believes that first quarter 2025 GAAP diluted earnings per share will be in the range of $3.90 to $4.04 and full year 2025 GAAP diluted earnings per share will be in the range of $17.70 to $18.20. The company's management further believes that first quarter 2025 non-GAAP diluted earnings per share will be in the range of $4.80 to $4.90 and full year 2025 non-GAAP diluted earnings per share will be in the range of $21.10 to $21.50. This guidance reflects confidence in continued operational improvement despite macroeconomic uncertainties.

The modern Teledyne has achieved something remarkable: maintaining the disciplined capital allocation culture of its founder while building genuine technological differentiation. It's no longer just a financial engineering story but a tale of innovation, integration, and strategic focus that positions it uniquely for the sensor-driven future.

IX. Playbook: Capital Allocation & Business Lessons

The conference room at Harvard Business School was packed for the case study discussion on Teledyne—a rare examination spanning two distinct eras of capitalism. The professor posed the central question: "How do you evaluate capital allocation excellence across radically different business environments?" The answer, as students would discover, lay not in copying specific tactics but understanding timeless principles.

Henry Singleton's capital allocation philosophy was deceptively simple: treat corporate finance as a mathematical optimization problem. When your stock trades at 50 times earnings, issue equity aggressively. When it falls to 10 times, buy it back with equal aggression. This wasn't market timing—it was arbitrage. Between 1960 and 1969, Singleton issued shares worth billions in today's dollars. Between 1970 and 1986, he retired 90% of those same shares at a fraction of the price. The math was irresistible: selling high and buying low, applied to your own equity.

But the genius went deeper than simple P/E arbitrage. Singleton understood that capital allocation is fundamentally about opportunity cost. Every dollar retained in the business must earn its keep against alternative uses: acquisitions, buybacks, dividends, or debt reduction. He established a hurdle rate—20% annual returns—and ruthlessly enforced it. Projects that couldn't meet this threshold didn't get funded, no matter how strategic they seemed.

The decentralization model that Singleton pioneered prefigured modern platform companies by decades. Division presidents operated like CEOs of independent companies, with complete operational autonomy. But financial reporting was sacrosanct—detailed weekly reports flowed to Beverly Hills, where Singleton and his small team could spot trends, problems, and opportunities faster than any centralized bureaucracy. This wasn't the fake decentralization of matrix organizations but genuine entrepreneurial freedom coupled with financial accountability.

Singleton's approach to debt was equally sophisticated. While other conglomerates leveraged themselves to the hilt, Teledyne maintained a fortress balance sheet. Debt was a tool, not a strategy—used opportunistically when rates were attractive but never allowed to constrain strategic flexibility. This discipline proved crucial during the 1970s stagflation and 1980s recession, when overleveraged competitors collapsed while Teledyne continued buying back stock.

The insurance operation strategy deserves special attention. By acquiring insurance companies, Singleton gained access to float—premiums collected today but not paid out until future claims. This float could be invested for Teledyne's benefit, providing what Buffett would later call "free money." But unlike traditional insurers who invested conservatively in bonds, Singleton built concentrated equity positions in undervalued companies, generating returns that transformed insurance from a side business into a profit center.

Robert Mehrabian's modern playbook adapts these principles to a different era. Where Singleton optimized for financial returns, Mehrabian optimizes for strategic position. Acquisitions must strengthen core competencies in sensing and imaging, not just meet financial hurdles. The discipline remains—Mehrabian has walked away from dozens of deals over valuation concerns—but the criteria have evolved.

The modern approach to capital deployment is more balanced but equally disciplined. Organic R&D investment, historically minimal under Singleton, now consumes 5-6% of revenue—necessary for maintaining technological leadership. Acquisitions focus on capability enhancement rather than P/E arbitrage. Share buybacks occur opportunistically when the stock is undervalued, but not at the expense of strategic investments. Debt is managed to maintain flexibility while optimizing the cost of capital.

The operational excellence that Mehrabian instituted would have seemed foreign to Singleton but proves essential in modern markets. Lean manufacturing, Six Sigma quality programs, and integrated supply chain management drive margin expansion. Cross-selling between divisions, discouraged in Singleton's era, now generates significant revenue synergies. The company that once had no marketing department now employs sophisticated go-to-market strategies tailored to each end market.

The lessons for modern executives are nuanced but powerful:

First, capital allocation remains the CEO's most important job. Whether you're issuing stock for acquisitions or buying it back, the math must be compelling. Market sentiment is noise; intrinsic value is signal.

Second, decentralization with accountability beats centralization every time. Give operators freedom to run their businesses but maintain absolute discipline on financial reporting and capital allocation. Trust but verify, delegate but measure.

Third, strategic focus eventually matters more than financial engineering. Singleton could build a conglomerate through P/E arbitrage because markets were inefficient. Today's markets are less forgiving of complexity. Mehrabian's focused approach—building depth in sensing and imaging—creates value through operational and technological synergies that pure financial engineering cannot match.

Fourth, patient opportunism beats aggressive action. Both Singleton and Mehrabian waited years for the right acquisitions, the right moment to buy back stock, the right time to issue debt. In a world obsessed with quarterly earnings, this long-term orientation remains a sustainable competitive advantage.

Fifth, maintain financial flexibility at all costs. Both eras of Teledyne leadership prioritized balance sheet strength over aggressive growth. This conservatism enabled opportunistic moves when competitors were constrained—buying back stock in downturns, acquiring distressed assets, investing in R&D when others cut back.

The measurement systems tell the story. Singleton focused on one metric above all: long-term per-share value creation. Revenue growth, market share, employee satisfaction—all were secondary to this prime directive. Mehrabian tracks a broader dashboard—organic growth, margin expansion, return on invested capital, customer satisfaction—but the north star remains shareholder value creation over the long term.

For modern conglomerates and industrial consolidators, Teledyne offers both inspiration and warning. The Singleton-era success proves that exceptional capital allocation can create enormous value. The 1990s dismemberment shows that conglomerate structures require exceptional leadership to maintain. The Mehrabian resurrection demonstrates that focused strategy and operational excellence can revive even the most challenged franchises.

The ultimate lesson may be that there's no permanent formula for business success. Singleton's financial engineering worked brilliantly in the conglomerate era but became obsolete as markets evolved. Mehrabian's focused technology strategy works today but may require adaptation as sensing markets mature. The constant is not the strategy but the discipline—rigorous analysis, patient execution, and the courage to zig when others zag.

X. Analysis & Investment Case

The sell-side analyst's model was a work of art—dozens of tabs, thousands of formulas, projections stretching to 2030. But the senior portfolio manager pushed it aside and asked the only question that mattered: "Is Teledyne a Singleton-style value play hiding in a Mehrabian growth story, or is it actually what it claims to be—a secular winner in sensing and imaging?" The answer would determine whether this was a compelling investment or an expensive trap.

The bear case starts with valuation. Trading at roughly 22-25 times forward earnings, Teledyne commands a premium to industrial peers and even some pure-play technology companies. Bears argue this multiple assumes perfect execution: successful integration of FLIR and future acquisitions, continued margin expansion despite inflation, and sustained defense spending despite fiscal pressures. Any stumble—a botched acquisition, margin compression, or defense budget cuts—could trigger multiple compression that overwhelms operational progress.

Defense exposure presents another concern. With approximately 40% of revenue tied to U.S. government contracts, Teledyne faces political and budgetary risks beyond its control. The debt ceiling debates, continuing resolutions, and shifting defense priorities create uncertainty. Moreover, the company's classified work makes it difficult for investors to fully understand the business. Bears worry that defense spending could plateau or decline as focus shifts from hardware to software and cyber capabilities.

Integration challenges loom large. While the FLIR acquisition appears successful so far, Teledyne has announced additional deals including Micropac Industries and select aerospace and defense electronics businesses from Excelitas. Each acquisition brings integration risk—cultural clashes, customer defections, key employee departures. The company that grew through 130 acquisitions under Singleton had his singular genius guiding integration. Can Mehrabian's team maintain the same discipline?

The competitive landscape is intensifying. Chinese companies are aggressively entering sensing markets with lower-cost alternatives. Software-defined sensors could commoditize hardware. Large tech companies like Apple and Google are developing their own imaging technologies. Traditional competitors like Honeywell and Thermo Fisher have their own acquisition war chests. Teledyne's technological moats, while substantial, are not impregnable.

Environmental and regulatory risks deserve consideration. Many of Teledyne's products enable surveillance and military applications, raising ESG concerns for some investors. The company's environmental monitoring business, while growing, depends on regulatory enforcement that could weaken under business-friendly administrations. Export controls and technology transfer restrictions could limit international growth.

But the bull case is equally compelling, starting with secular growth drivers. The proliferation of sensors in everything from vehicles to factories to medical devices is still in early innings. Autonomous systems require multiple sensing modalities—exactly Teledyne's sweet spot. Environmental monitoring will only grow as climate change accelerates. Space commercialization needs the specialized sensors Teledyne provides. These are decade-long trends with compound growth potential.

Teledyne's competitive moats run deeper than most appreciate. The company doesn't just make sensors—it makes the specialized semiconductors that go into sensors, the packaging that protects them, the software that processes their output, and the systems that integrate multiple sensors. This vertical integration creates barriers that pure-play competitors can't match. Moreover, many products are designed into customer systems for 10-20 year lifecycles, creating switching costs and recurring revenue streams.

The pricing power evidence is compelling. Despite inflation and supply chain challenges, Teledyne has expanded margins through price increases that customers accept because alternatives don't exist. When you're the only company that makes a sensor capable of detecting certain chemical weapons or imaging through specific atmospheric conditions, price becomes secondary to capability. This pricing power should persist as products become more specialized and mission-critical.

Financial metrics support the bull case. Return on invested capital consistently exceeds 12%, well above the cost of capital. Free cash flow conversion exceeds 100% of net income. The balance sheet has strengthened despite massive acquisitions, with net debt-to-EBITDA below 2x. These aren't the metrics of an overleveraged roll-up but a disciplined operator generating real economic value.

The revenue mix evolution is particularly attractive. Recurring revenue from service contracts, software subscriptions, and consumables has grown from 15% in 2010 to over 30% today. This provides stability through cycles and supports premium valuations. Moreover, commercial and industrial exposure has increased from 40% to 60%, reducing government dependency and expanding addressable markets.

Management quality and alignment deserve recognition. Mehrabian owns significant stock and has delivered 15%+ annual returns since becoming CEO. The executive team combines long Teledyne tenure with fresh outside perspective. Capital allocation remains disciplined—the company walked away from several large deals in 2023 over valuation concerns. This isn't a management team chasing growth at any price.

Comparing Teledyne to relevant peers illuminates its unique position:

| Metric | Teledyne | Honeywell | Thermo Fisher | Danaher |

|---|---|---|---|---|

| Market Cap | ~$20B | ~$140B | ~$200B | ~$170B |

| Revenue Growth (5yr CAGR) | 8% | 3% | 12% | 10% |

| Operating Margin | 18% | 21% | 18% | 23% |

| ROIC | 12% | 15% | 9% | 11% |

| Net Debt/EBITDA | 1.8x | 2.5x | 3.2x | 2.1x |

Teledyne trades at a discount to best-in-class operators like Danaher despite similar margins and returns, suggesting potential multiple expansion as the FLIR integration proves successful.

Future acquisition targets could further strengthen the investment case. Companies specializing in LiDAR for autonomous vehicles, quantum sensors for navigation, or AI-powered image analysis would fit Teledyne's framework. With $1+ billion in annual free cash flow and modest leverage, the company has firepower for transformative deals without stressing the balance sheet.

The scenario analysis reveals asymmetric risk-reward:

Bull case (30% probability): Multiple expansion to 28x earnings as FLIR synergies exceed expectations and secular growth accelerates. Stock reaches $650 (+40% upside).

Base case (50% probability): Current multiple maintained as company delivers mid-single-digit organic growth plus accretive acquisitions. Stock reaches $550 (+18% upside).

Bear case (20% probability): Multiple compression to 18x on integration challenges or defense cuts. Stock falls to $400 (-14% downside).

The probability-weighted return of approximately 20% over 18-24 months compares favorably to market alternatives, especially considering Teledyne's defensive characteristics.

For long-term investors, Teledyne represents a rare combination: a company with conglomerate-era capital allocation discipline, modern technology differentiation, and exposure to secular growth themes. It's neither a pure value play nor a growth story but something more interesting—a quality compounder with optionality. The company that Henry Singleton built on financial engineering has been reborn as a technology leader, but the DNA of disciplined capital allocation remains.

The investment decision ultimately depends on time horizon and risk tolerance. Short-term investors might struggle with the stock's volatility and integration uncertainties. But for those with multi-year perspectives, Teledyne offers exposure to sensing megatrends through a proven operator with exceptional capital allocation capabilities. In a market starved for quality growth at reasonable prices, that's an increasingly rare combination.

XI. Epilogue & "If We Were CEOs"

The view from Teledyne's headquarters in Thousand Oaks stretches to the Pacific Ocean on clear days—a fitting metaphor for the company's expanding horizons. As we contemplate what we'd do as CEO in 2025, we must balance respect for what Mehrabian has built with recognition that the next chapter requires new thinking.

First priority: accelerate the shift from hardware to integrated solutions. Teledyne's individual sensors are world-class, but customers increasingly want complete answers, not components. We'd create a "Solutions Architecture" group, staffed with domain experts who can combine sensors, software, and AI into packages that solve specific problems—automated quality inspection for semiconductor fabs, comprehensive environmental monitoring for smart cities, or integrated threat detection for military bases. This isn't just bundling products; it's creating new value propositions that competitors selling individual sensors cannot match.

Geographic expansion represents untapped potential. Teledyne generates roughly 70% of revenue in North America, yet the fastest-growing markets for sensing technology are in Asia. We'd establish innovation centers in Singapore, Seoul, and Tel Aviv—not just sales offices but real R&D facilities that can develop products for local markets while tapping regional talent. The goal isn't just selling Western products in Eastern markets but creating solutions that could only come from understanding local needs.

The next platform acquisition should be in AI and machine learning—not the large language models capturing headlines but specialized AI for sensor fusion and image analysis. Companies like Percipient.AI or Reality AI have developed algorithms that can extract insights from sensor data that humans cannot see. Acquiring and integrating these capabilities across Teledyne's sensor portfolio would create a competitive moat that hardware-only competitors couldn't cross.

We'd also pursue an aggressive "sensor as a service" strategy. Instead of selling a $100,000 inspection system, offer it for $3,000 per month with continuous updates, remote monitoring, and guaranteed uptime. This transforms capital expenditures into operating expenses for customers while creating predictable, high-margin recurring revenue for Teledyne. The installed base of thousands of systems becomes an annuity stream worth billions.

On the operational side, we'd push vertical integration even further. Teledyne already makes many of its own semiconductors, but we'd invest in advanced packaging capabilities—the ability to integrate multiple sensing modalities on a single chip. This "more than Moore" approach would enable new products impossible with current technology while reducing costs and improving reliability.

Cultural evolution needs attention. The company that thrived under radical decentralization must now excel at collaboration. We'd institute "innovation sprints" where teams from different divisions work together on customer challenges. The marine instruments team might combine with aerospace sensors and AI experts to create autonomous ocean monitoring systems. These cross-pollination efforts, impossible in Singleton's era, are essential for modern innovation.

The balance between growth and profitability would tilt slightly toward growth, but with Singleton-style discipline. We'd set a simple rule: every growth investment must have a clear path to 20% returns within three years. This isn't the "growth at any cost" mentality that destroyed WeWork or the conservative "margin above all" approach that caused GE to miss technology transitions. It's disciplined growth—expanding aggressively where we have competitive advantage while maintaining the financial strength to weather downturns.

Environmental and sustainability leadership could differentiate Teledyne beyond current efforts. We'd commit to making our environmental monitoring division carbon-negative—actually removing more carbon through our monitoring and compliance services than our operations produce. This isn't just ESG window dressing; it's recognizing that the companies helping solve climate change will capture enormous value over coming decades.

For the capital structure, we'd maintain Mehrabian's balanced approach but with one modification: establish a venture capital arm with $500 million to invest in early-stage sensing and imaging startups. This would provide windows into emerging technologies, potential acquisition pipelines, and cultural vitalization as Teledyne engineers interact with startup founders. Think of it as R&D with upside—exactly the kind of optionality Singleton would appreciate.

The biggest risk facing Teledyne isn't competition or technology disruption—it's complacency. The company has executed brilliantly for over a decade, but success breeds conservatism. We'd institute "disruption workshops" where teams must design products that would obsolete our current offerings. Better to disrupt ourselves than let others do it.

Finally, we'd prepare for the inevitable CEO succession. Mehrabian has been brilliant, but he won't lead forever. The next CEO should combine technical depth with financial acumen—someone who understands both quantum cascade lasers and discounted cash flows. We'd identify and develop internal candidates while maintaining openness to external talent. The transition from Singleton to Roberts was painful partly because it was reactive; the next transition should be proactive.

Looking back at Teledyne's journey—from Singleton's financial engineering masterpiece through painful dismemberment to Mehrabian's focused technology leader—the thread that connects success across eras is discipline. Disciplined capital allocation. Disciplined operations. Disciplined strategy. The specific tactics change with times, but the underlying commitment to value creation through discipline endures.

If we were CEO, we'd honor that discipline while pushing Teledyne toward its next transformation: from product company to solution provider, from North American leader to global force, from hardware manufacturer to AI-enabled insight generator. The sensing revolution is just beginning. Autonomous vehicles, personalized medicine, climate monitoring, space exploration—all depend on the technologies Teledyne provides.

The company Henry Singleton founded in a Beverly Hills office has become indispensable to modern civilization. The company Robert Mehrabian rescued from conglomerate purgatory has emerged as a focused technology leader. The next chapter—whether written by us or another—will determine whether Teledyne becomes the defining sensing and imaging company of the 21st century or merely another successful industrial firm.

The potential is there. The foundation is solid. The opportunity is massive. What's needed is the courage to pursue it with the same contrarian conviction that led Singleton to buy back 90% of his stock and Mehrabian to bet $8 billion on FLIR. In the end, that's the true Teledyne way: seeing value where others see risk, acting when others hesitate, and maintaining discipline when others lose their heads.

The view from Thousand Oaks stretches to the horizon. The only question is how far Teledyne is willing to reach.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube