Alivus Life Sciences: India's API Powerhouse Goes Independent

I. Introduction & Episode Roadmap

Picture this: September 2023, a boardroom in Ahmedabad. Karsanbhai Patel's Nirma Limited—the soap-to-cement conglomerate that built an empire on disrupting Hindustan Unilever—writes a ₹5,652 crore check to acquire 75% of Glenmark Life Sciences. It's one of the largest pharmaceutical deals in India that year, yet it barely makes headlines outside industry circles. Why would a company known for detergents and cement suddenly bet big on active pharmaceutical ingredients?

The answer lies in a transformation story that's quintessentially Indian: a captive supplier breaking free, a spin-off finding its wings, and ultimately, a strategic acquisition that promises to reshape India's position in the global pharmaceutical supply chain. Today, Alivus Life Sciences—as it was rechristened in December 2024—stands at ₹2,400 crore in revenue with a market capitalization hovering around ₹11,463 crore.

But here's what makes this story compelling for students of business strategy: Alivus represents a new breed of Indian pharmaceutical companies. Not the generic drug makers that dominated the 1990s and 2000s. Not the branded formulations players chasing doctor prescriptions. This is about the unsexy, highly technical, deeply moated business of making the actual drug substances—the APIs—that go into medicines worldwide. And not just any APIs, but the non-commoditized, high-value molecules where India can compete on quality, not just cost.

The journey from Glenmark's internal API division to Nirma-backed independent powerhouse touches every major theme in modern Indian business: the art of the corporate spin-off, the challenge of transitioning from captive to third-party sales, the strategic importance of backward integration, and the global shift toward supply chain resilience post-COVID. It's a story about how an API division, once seen as merely supporting infrastructure for a parent company's formulations business, became valuable enough to command a ₹5,600+ crore valuation.

What we're about to unpack is how a business unit that started with a single manufacturing facility evolved into a multi-site operation spanning Maharashtra and Gujarat, serving customers across India, Europe, North America, Latin America, and Japan. We'll explore why Nirma—yes, the washing powder Nirma—saw strategic gold in pharmaceutical intermediates. And we'll dissect whether this newly independent entity can fulfill its ambition of becoming a global Contract Development and Manufacturing Organization (CDMO) player, competing with the likes of Lonza and Catalent.

The timing couldn't be more critical. As global pharmaceutical companies scramble to diversify supply chains away from China, as biosimilars and complex generics demand sophisticated manufacturing capabilities, and as regulatory standards tighten worldwide, companies like Alivus find themselves at the intersection of capability and opportunity. But can they execute?

II. The Glenmark Origins & API Business Genesis

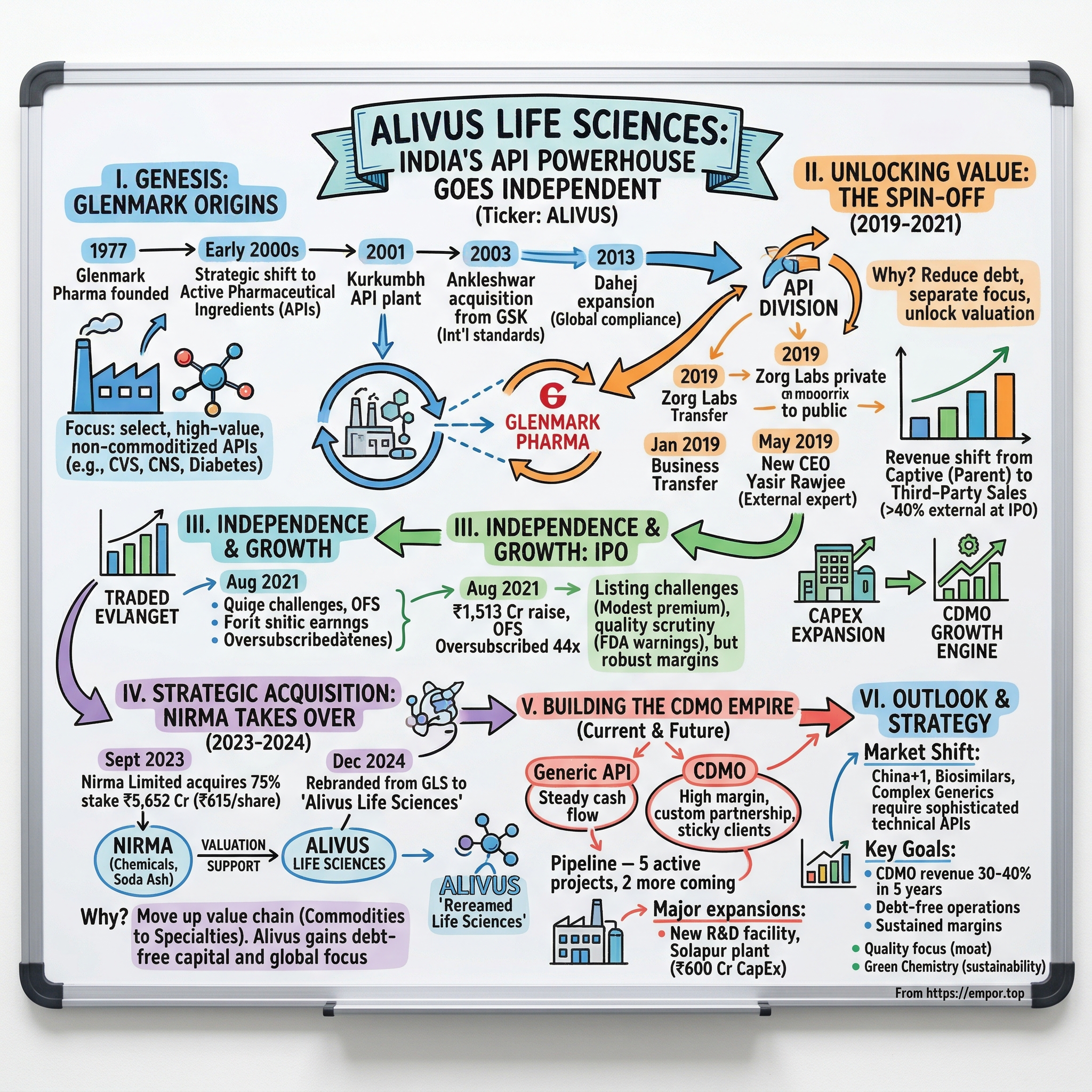

The year was 1977 when Gracias Saldanha, a former Boots India executive, founded Glenmark Pharmaceuticals in a modest setup in Mumbai. But our story really begins decades later, in the early 2000s, when Glenmark's second-generation leader Glenn Saldanha (Gracias's son) made a strategic decision that would plant the seeds for today's Alivus. Glenn Saldanha understood something fundamental about the pharmaceutical value chain in the early 2000s: whoever controls the raw materials controls the pricing power. In 2001, Glenmark diversified into API manufacturing, starting operations at its Kurkumbh facility in Maharashtra. This wasn't just backward integration—it was strategic positioning for what would become one of India's most successful pharmaceutical spin-offs two decades later.

The genesis of what would become Alivus actually traces back to a corporate structure maneuver in 2011. The business was incorporated as Zorg Laboratories Private Limited—a name that sounds more like a villain's corporation from a B-movie than a future API powerhouse. Before 2019, the API business was an integral part of Glenmark Pharma (GPL), separated from GPL into GLS through a Business Transfer Agreement in Jan 2019, and subsequently listed on NSE & BSE in FY22.

But let's rewind to understand the strategic logic. In 2003, the company acquired the Glaxo SmithKline (GSK) API manufacturing plant in Ankleshwar, Gujarat. Think about the audacity—a relatively young Indian pharma company acquiring a facility from one of the world's pharmaceutical giants. This Ankleshwar acquisition wasn't just about capacity; it brought with it international regulatory compliance standards and established customer relationships.

In 2004, Glenmark Life Science commenced manufacturing facility at Mohol, Maharashtra. By now, a pattern was emerging: multiple facilities across different states, each with distinct capabilities, creating both operational redundancy and specialized competencies. The Mohol facility would later become crucial for regulated market supplies, eventually earning USFDA approval.

The real transformation began accelerating around 2013. Glenmark Life Science commenced the third manufacturing plant at Dahej, Gujarat, and in the same year, the Ankleshwar plant was inspected by COFEPRIS. This Dahej facility represented a major leap—not just in capacity but in sophistication. It was designed from the ground up to meet the stringent requirements of global regulatory authorities.

What's fascinating is how the API business evolved from a cost center supporting Glenmark's formulations to a profit center in its own right. By 2018, the writing was on the wall. Glenmark Pharmaceuticals, like many Indian pharma companies of that era, found itself in a debt trap—the result of ambitious R&D spending on novel drug discovery that hadn't paid off as expected. The API business, meanwhile, was generating steady cash flows with EBITDA margins north of 25%.

Glenmark Pharmaceuticals transferred its Active Pharmaceuticals Ingredient (API) business to Glenmark Life Sciences, a wholly owned subsidiary of the company. This transfer was completed on December 31, 2018. The timing was deliberate—closing the transfer on the last day of the calendar year allowed for clean accounting separation heading into 2019.

But here's where the story gets interesting from a strategic perspective. Facing a debt problem in 2019, Glenmark considered selling off its active pharmaceutical ingredient (API) business before opting instead for a spinoff. The decision to spin off rather than sell outright was crucial. A direct sale might have fetched immediate cash but would have completely severed Glenmark from a business it had nurtured for nearly two decades. The spin-off allowed them to retain majority control while creating an independent entity that could be valued separately by the market.

The transformation from captive supplier to independent entity required a fundamental shift in mindset. For years, the API division's primary customer was its parent company. Sales teams didn't need to hustle for new business; R&D priorities were dictated by Glenmark's formulation pipeline; pricing was essentially internal transfer pricing. Now, suddenly, they needed to compete in the open market against established players like Divi's Laboratories, Laurus Labs, and global giants like Teva API and Sandoz.

By the time of separation, the business had evolved into something substantial: As of 31 December 2020, it had a portfolio of 120 molecules globally and sold its APIs in India and exported its APIs to multiple countries in Europe, North America, Latin America, Japan and the rest of the world. The portfolio wasn't just broad—it was strategically curated. Glenmark Life Sciences is a developer and manufacturer of select high value, non-commoditized active pharmaceutical ingredients (APIs) in chronic therapeutic areas, including cardiovascular disease (CVS), central nervous system disease (CNS), pain management and diabetes.

The focus on "non-commoditized" APIs is crucial to understanding the business model. While companies like Aurobindo and Dr. Reddy's were fighting price wars in commoditized molecules like paracetamol and ibuprofen, Glenmark Life Sciences positioned itself in complex molecules with higher barriers to entry. These required sophisticated chemistry capabilities, specialized equipment, and deep regulatory expertise—moats that couldn't be easily replicated by new entrants.

The company works with 16 of the 20 largest generic companies globally. This customer concentration might seem like a risk, but it actually validated the quality and reliability of their operations. When Mylan (now Viatris), Teva, or Sandoz sources APIs from you, it's a stamp of approval that opens doors globally.

The regulatory track record built over these years was perhaps the most valuable intangible asset. In 2012, its Ankleshwar manufacturing facility was inspected by the Japanese regulatory agencies PMDA and AFSSAPS. In 2018, the company Dahej manufacturing plant was inspected by EDQM, ANSM, US FDA, and the Mohol plant was inspected by the US FDA. The Ankleshwar manufacturing plant was inspected by US FDA, Health Canada and PMDA, Japan agency. Each successful inspection was like adding another badge to their credibility armor.

The evolution from Glenmark's internal API division to an independent entity ready for public markets represents a masterclass in corporate strategy. It shows how sometimes the most valuable assets aren't the ones getting the headlines but the unglamorous workhorses generating consistent returns. As we'll see in the next section, the journey to IPO would test whether this business could truly stand on its own feet.

III. The Spin-off Journey & IPO (2019–2021)

The boardroom at Glenmark House in Mumbai must have been tense in early 2019. Glenn Saldanha faced a classic founder's dilemma: how to unlock value from a cash-generating asset without losing control of a strategic resource. In 2019, Glenmark nearly sold off the unit to address its debt issues but opted for a spinoff. The debt burden—accumulated from years of ambitious but largely unsuccessful novel drug discovery programs—had become an albatross around Glenmark Pharmaceuticals' neck.

The spin-off wasn't just a financial engineering exercise; it required surgical precision in separating two deeply intertwined businesses. Think about it: for nearly two decades, the API business had operated as Glenmark's internal supplier. Shared services, from HR to IT systems, quality control to regulatory filings, all needed to be untangled. Transfer pricing agreements that were once internal paperwork suddenly became arm's length commercial contracts.

The mechanics of the separation revealed the complexity. First came the Business Transfer Agreement in January 2019, which formally carved out the API business from the parent company. But the corporate structure had an interesting twist—the business wasn't entirely new. It had been quietly restructured years earlier as Zorg Laboratories, which Glenmark had acquired through a Share Purchase Agreement in July 2018, then converted to a public limited company in August 2018. This wasn't last-minute planning; it was methodical preparation for eventual independence.

In May 2019, Yasir Rawjee became CEO of Glenmark Life Sciences. Rawjee's appointment was strategic—he wasn't a Glenmark insider but came with deep API industry experience. His mandate was clear: transform a captive supplier into a competitive, customer-focused organization. Under his leadership, the company had to build capabilities it never needed before: independent sales and marketing, customer relationship management, and most critically, the ability to compete for business against established API players.

The cultural transformation was perhaps harder than the operational one. Employees who had spent careers in the comfortable embrace of a captive relationship suddenly faced market realities. Sales teams had to learn to pitch against competitors. R&D had to prioritize projects based on market demand, not parent company needs. Manufacturing had to become cost-competitive, not just quality-compliant.

Then came the pandemic—simultaneously the worst and best timing for a pharmaceutical IPO. On one hand, COVID-19 disrupted supply chains, made factory inspections impossible, and created massive uncertainty. On the other, it highlighted the critical importance of pharmaceutical supply chain resilience and the dangers of over-dependence on Chinese APIs. Suddenly, investors were paying attention to API manufacturers like never before.

The IPO prospectus, filed in July 2021, told a compelling story. In 2001-2002, Glenmark launched the API manufacturing business by setting up a manufacturing facility in Kurkumbh in the state of Maharashtra. In 2019, the API manufacturing business of Glenmark was sold and spun off into Glenmark Life Sciences. The company positioned itself not as Glenmark's castoff but as India's answer to the global need for supply chain diversification.

The numbers in the IPO documents revealed the transformation's success. Revenue from external customers (non-Glenmark) had grown from less than 20% pre-separation to over 40% by the time of IPO. The company was no longer just Glenmark's API division; it was becoming a standalone force. EBITDA margins remained robust at around 30%, proving the business model's resilience even without the cushion of captive sales.

August 2021 arrived with fanfare. The IPO comprised 21,022,222 equity shares aggregating to ₹1,513.6 crores—a mix of fresh capital raise and offer for sale by Glenmark Pharmaceuticals. The pricing band of ₹695-720 per share valued the company at roughly ₹8,000 crores at the upper end. For context, this was higher than several established pharmaceutical companies' valuations, reflecting investor optimism about the API sector's prospects.

The IPO was oversubscribed 44.17 times on 27 July 2021 but it disappointed all investors. The overwhelming subscription came primarily from institutional investors who saw the China+1 opportunity clearly. Retail investors, perhaps less familiar with the B2B API business model, were more cautious. The listing day performance was modest—the stock opened at ₹760 on NSE, a premium of just 5.6% over the issue price of ₹720.

Post-IPO, Glenmark Pharmaceuticals retained an 82.06% stake, maintaining firm control while achieving the deleveraging objective. The fresh capital from the IPO—approximately ₹500 crores—went toward capacity expansion and working capital, giving Glenmark Life Sciences the financial muscle to compete independently.

But independence brought new challenges. This IPO may not have come at a particularly good time, in light of Glenmark Life's financial obligation to its parent. The company still relied heavily on Glenmark Pharmaceuticals for a significant portion of revenue. Related party transactions remained substantial, raising questions about true independence. Could Glenmark Life Sciences survive and thrive if the parent company reduced its purchases?

The first year as a listed entity tested this question. Management had to balance multiple stakeholders' interests—minority shareholders wanting aggressive growth, Glenmark Pharmaceuticals needing reliable supply, and customers questioning whether the company would prioritize parent company orders over theirs. Quarterly earnings calls became exercises in reassurance, with management repeatedly emphasizing their commitment to all customers equally.

The regulatory scrutiny also intensified post-listing. In October 2019, following an inspection by the US Food and Drug Administration (FDA) of Glenmark's plant in Himachal Pradesh, the FDA sent Glenmark a warning letter in which it detailed "significant violations of current good manufacturing practice." While this was for a Glenmark facility, not Glenmark Life Sciences, such news created nervousness about the entire Glenmark ecosystem's quality standards.

Yet the company pressed forward with its growth strategy. New customer acquisitions accelerated. The CDMO (Contract Development and Manufacturing Organization) business, barely a footnote pre-IPO, began showing promise. The company started positioning itself not just as an API supplier but as a development partner for complex molecules—a higher-margin, stickier business model.

By early 2023, two years post-IPO, Glenmark Life Sciences had proven it could stand independently. External customer revenue had crossed 60%. The company had successfully commercialized several new molecules. Most importantly, it had established its own identity in the market, separate from the Glenmark brand. But the biggest transformation was yet to come—one that would completely redefine its ownership, strategy, and even its name.

IV. Building the API & CDMO Empire

Walk through the production floors at Dahej, and you'll witness pharmaceutical chemistry at industrial scale—500-kiloliter reactors churning out complex molecules, automated systems maintaining temperatures within fractions of a degree, and quality control labs running 24/7 to ensure every batch meets specifications that would make a Swiss watchmaker envious. This is the empire Glenmark Life Sciences built, one reactor at a time.

By 2021, the company's manufacturing footprint had evolved into something formidable. Alivus Life Sciences Limited, formerly Glenmark Life Sciences, is a leading developer and manufacturer of select high value, non-commoditized Active Pharmaceutical Ingredients (APIs) in chronic therapeutic areas. But what does "non-commoditized" really mean in the API world? It's the difference between making aspirin—where dozens of suppliers fight over pennies—and manufacturing complex cardiovascular molecules where only a handful of companies globally have the expertise.

The portfolio strategy was deliberate and sophisticated. The company had assembled around 151 molecules across therapeutic areas, but not randomly. Each molecule was chosen for specific characteristics: complexity of synthesis, regulatory barriers, market size, and competitive dynamics. Cardiovascular drugs formed the backbone—accounting for over 34% of revenue. These weren't simple blood pressure medications but complex molecules like sacubitril, a key component of heart failure treatment that requires multiple synthesis steps and sophisticated purification techniques.

Central nervous system (CNS) molecules presented different challenges. These drugs, treating everything from depression to epilepsy, often require handling controlled substances, navigating complex regulatory frameworks, and maintaining chain-of-custody documentation that would satisfy both DEA and international narcotics control boards. The company's ability to handle these molecules gave them access to a market segment many competitors avoided.

The diabetes portfolio—contributing about 15% of revenue—capitalized on the global diabetes epidemic. But again, these weren't simple metformin generics. The focus was on newer anti-diabetic molecules coming off patent, where early entry could capture significant market share before commoditization set in. The company's scientists had developed proprietary processes for several DPP-4 inhibitors and SGLT-2 inhibitors, the newer classes of diabetes drugs that commanded premium pricing.

In 2013, Glenmark Life Sciences expanded its operations to Dahej, Gujarat, a strategic location for API manufacturing. In recent years, the company has further expanded its manufacturing capacities, particularly in 2023, with significant investments in its Ankleshwar and Dahej facilities. These expansions included a new Oncology Plant at Dahej and the commissioning of several new production modules at the Ankleshwar facility. As a result of these brownfield expansion projects, Glenmark Life Sciences has seen an increase in its total installed capacity, reaching an impressive 640 KL in FY 2023, with a further 240 KL expansion at the Dahej facility.

The oncology expansion deserves special attention. One of the key areas where Glenmark Life Sciences has made a significant impact is in the oncology segment. The company has invested heavily in developing APIs for oncology treatments, which are often more complex and require highly specialized manufacturing processes. The Oncology Plant at Dahej was developed as part of a brownfield expansion project, with one module being fully commissioned in 2023, and the second module set to follow soon after. This wasn't just adding capacity; it was entering an entirely different league. Oncology APIs require containment facilities to protect workers from exposure, specialized waste treatment systems, and quality standards that make regular pharma manufacturing look casual.

The global footprint told another story of transformation. While many Indian API companies focused primarily on the US market, Glenmark Life Sciences had deliberately diversified. Europe accounted for nearly 30% of sales, Japan another 15%, and emerging markets the rest. This wasn't accidental—each geography required different regulatory filings, quality standards, and customer relationships. The company had systematically built these capabilities over two decades.

The Ankleshwar, Dahej and Mohol facilities are approved by the USFDA, MHRA(UK), FIMEA (Finland), Romania (Europe), PMDA (Japan), COFEPRIS (Mexico), Health Canada, KFDA (South Korea), EDQM (Europe), KFDA, WHO-GMP and Gujarat FDCA authorities and cater to the regulated markets of the US, Europe and Japan. Each approval represented months of preparation, detailed inspections, and ongoing compliance costs. But they also represented moats—barriers that new entrants couldn't easily cross.

The CDMO business emerged as the growth engine for the future. The company is also increasingly providing contract development and manufacturing operations (CDMO) services to multinational and specialty pharmaceutical companies. This wasn't just contract manufacturing—any company with reactors could do that. CDMO meant partnering with innovator companies from the development stage, optimizing synthesis routes, scaling up from lab to commercial production, and often developing second-generation processes that improved yields or reduced environmental impact.

The CDMO model fundamentally changed the customer relationship. Instead of transactional API sales, these were multi-year partnerships with milestone payments, development fees, and long-term supply agreements. A successful CDMO project could generate revenue for a decade or more, with margins significantly higher than generic API sales. By 2023, the company had five active CDMO projects in various stages, with two more in the pipeline.

What made Glenmark Life Sciences particularly attractive to CDMO customers was its integrated capabilities. The company could handle projects from gram-scale synthesis in R&D labs to multi-ton commercial production. The Dahej facility, in particular, was designed with flexibility in mind—reactors that could handle different chemistries, modular clean rooms that could be reconfigured for different products, and analytical capabilities that could support regulatory filings in any major market.

The quality infrastructure underpinning all this was staggering. Over 400 quality control professionals, multiple quality assurance teams for different markets, and computerized systems that tracked every gram of material through the production process. The company maintained separate quality units for different facilities to prevent systemic issues from spreading. Post the various FDA warnings to parent company Glenmark, maintaining pristine quality records became even more critical.

Environmental and safety considerations had evolved from compliance requirements to competitive advantages. The Dahej facility featured zero liquid discharge systems, solvent recovery units that recycled over 80% of solvents, and energy-efficient processes that reduced carbon footprint. These weren't just good corporate citizenship—many customers, especially European ones, now demanded environmental sustainability from their suppliers.

The human capital driving this empire was equally impressive. Over 1,400 employees, including more than 200 with advanced degrees in chemistry or chemical engineering. The R&D team alone numbered over 150, working on everything from new synthesis routes to process optimization. The company had established partnerships with academic institutions, funding research projects and recruiting top talent directly from universities.

By 2023, Glenmark Life Sciences had transformed from a captive API supplier into a formidable player in the global pharmaceutical supply chain. Revenue had crossed ₹2,000 crores, with external customers accounting for the majority. EBITDA margins remained robust at around 30%, proving the business model's sustainability. The company supplied APIs to 16 of the top 20 global generic companies—a customer list that would be the envy of any API manufacturer.

But challenges remained. Chinese competition was intensifying as their manufacturers improved quality standards. Pricing pressure in generic APIs was constant. Customer concentration risk persisted—the top 10 customers still accounted for over 60% of revenue. Environmental regulations were becoming stricter, requiring continuous investment in pollution control. And always lurking was the reputational risk from any quality lapses, which could destroy years of trust-building in days.

Yet the foundation was solid. The combination of manufacturing scale, regulatory expertise, customer relationships, and technical capabilities positioned Glenmark Life Sciences as one of India's premier API companies. The question now wasn't whether the company could compete independently—it had proven that. The question was whether it could take the next leap from successful API manufacturer to global CDMO leader. That transformation would require not just capital and capabilities, but perhaps a new owner with deeper pockets and broader ambitions.

V. The Nirma Acquisition: New Chapter Begins (2023–2024)

September 2023, Nirma House, Ahmedabad. Karsanbhai Patel, the octogenarian founder who built a detergent empire from his backyard, sat across from his senior leadership team. At 78, most industrialists would be planning succession, not ₹5,600 crore acquisitions. But Patel had always defied convention—from taking on Hindustan Unilever in the 1980s to building one of India's largest soda ash plants in Gujarat's salt deserts. Now, he was about to make his biggest pharmaceutical bet yet.

By divesting 75% of its API business, Glenmark has resolved its debt problem. The buyer is Nirma, which will pay 615 Indian rupees per share ($681 million). The price—₹615 per share—represented a premium to the prevailing market price, but more importantly, it valued Glenmark Life Sciences at over ₹7,500 crores, a testament to the value creation since the IPO just two years earlier.

For outsiders, Nirma buying an API company seemed incongruous. This was a company known for washing powder, soap, and soda ash—what did they know about complex pharmaceutical manufacturing? But dig deeper into Nirma's history, and the logic emerges. The company had quietly built a substantial chemicals business over the decades, including caustic soda, chlorine derivatives, and specialty chemicals. Many of these are precursors or intermediates in pharmaceutical manufacturing. Nirma already understood complex chemistry, regulatory compliance, and B2B sales—all critical for API success.

Last year, Glenmark Pharma agreed to sell a 75% stake in the life sciences unit, spun off in 2019 to focus on the API business, to Nirma to pay off some of its debt of about 46 billion rupees. For Glenmark Pharmaceuticals, this was liberation. The debt burden that had constrained strategic options for years could finally be addressed. Glenn Saldanha could refocus on the formulations business and innovation pipeline without the distraction of debt servicing.

The transaction structure was elegant. The sale leaves the company with a 7.8% share in the API subsidiary, named Glenmark Life Sciences, which will continue to operate as an independent firm under the ownership of Nirma, according to GLS CEO Yasir Rawjee, Ph.D. Glenmark retained a small stake—enough to benefit from future upside but not enough to influence operations. This was crucial for customer confidence; a complete exit might have signaled abandonment, potentially triggering customer defections.

But why would Nirma, with no prior pharmaceutical experience, make such a massive bet? The answer lay in Karsanbhai Patel's long-term vision for the group. Nirma had been systematically moving up the value chain—from commodities to specialty chemicals, from B2C to B2B. The pharmaceutical sector represented the apex of this evolution: high margins, deep moats, and global markets. Moreover, Patel understood something fundamental: India's pharmaceutical industry was at an inflection point, transitioning from generic formulations to complex APIs and innovative drugs.

The cultural fit, surprisingly, was better than many expected. Both companies shared DNA of frugal innovation, operational excellence, and competing against multinationals. Nirma's culture of cost leadership and efficiency could benefit an API business where every percentage point of yield improvement translated to millions in profit. Meanwhile, Glenmark Life Sciences brought technical sophistication and regulatory expertise that could elevate Nirma's entire chemicals portfolio.

"I see this as an opportunity to further strengthen our position in the API industry and continue the growth trajectory," Rawjee said. Yasir Rawjee's continuation as CEO was crucial for continuity. He had navigated the company through spin-off, IPO, and now acquisition—institutional knowledge that couldn't be easily replaced. His endorsement of Nirma as the new owner sent a powerful signal to employees, customers, and investors.

The integration process revealed Nirma's sophistication. Rather than imposing their systems wholesale, they took a selective approach. Financial controls and procurement processes were standardized to leverage Nirma's scale—imagine the negotiating power when buying solvents for both detergent and pharmaceutical production. But technical operations, quality systems, and customer relationships remained autonomous, recognizing the specialized nature of pharmaceutical manufacturing.

December 2024 brought the most visible change: rebranding to Alivus Life Sciences. The name change was more than cosmetic. "Alivus"—suggesting life and vitality—signaled a break from the Glenmark legacy and the beginning of an independent identity. It also addressed a practical problem: customer confusion about whether the company was still part of Glenmark, especially important given the parent company's occasional regulatory issues.

The strategic shifts under Nirma ownership became apparent quickly. First, capital allocation became more aggressive. Where Glenmark had been constrained by debt, Nirma could fund expansion from its substantial cash flows. Plans for a new R&D facility, dormant for years, were revived with an 18-month completion target. The Solapur facility, a long-discussed project, moved from planning to execution.

Second, the customer diversification strategy accelerated. Under Glenmark, there was always tension about competing too aggressively for business that might conflict with the parent's interests. Now, freed from these constraints, Alivus could pursue any opportunity. The sales team was reorganized by geography and therapeutic area rather than by relationship to Glenmark.

Third, the CDMO business received renewed focus and investment. Nirma understood that commoditization was the enemy of margins—they had seen it in detergents. CDMO represented a way to escape the commodity trap in APIs, building sticky customer relationships and value-added services that went beyond simple manufacturing.

The financial impact was swift. Revenue from its contract development and manufacturing (CDMO) unit rose 27.2%, said Glenmark Life Sciences, which counts companies such as Aurobindo Pharma and Torrent Pharmaceuticals among its customers. "Looking ahead, a strong orderbook for external business, coupled with improved visibility of CDMO business gives me confidence of delivering steady growth in FY24 and in the coming years," Rawjee said.

Market reaction to the acquisition was initially mixed. Some investors worried about Nirma's lack of pharmaceutical experience. Others questioned whether the cultural integration would work. The stock price volatility in the months following the announcement reflected this uncertainty. But operational performance began winning over skeptics. Customer retention remained high, new business wins accelerated, and margins stayed robust.

The regulatory strategy under Nirma showed sophisticated understanding. Rather than cutting corners to reduce costs—a temptation for any cost-focused acquirer—Nirma actually increased quality spending. They understood that in pharmaceuticals, one FDA warning letter could destroy years of reputation building. Additional quality personnel were hired, systems were upgraded, and a culture of "quality first" was reinforced.

Nirma's distribution and logistics capabilities brought unexpected benefits. Their nationwide network, built for consumer products, could be leveraged for domestic API distribution. Their relationships with shipping companies and freight forwarders, negotiated at group level, reduced logistics costs. Even simple things like insurance, purchased at group level, delivered savings.

The HR integration revealed another strength. Nirma had experience managing technical talent from their chemicals business. They understood the importance of retaining key personnel, especially in R&D and regulatory affairs. Retention bonuses, career development programs, and in some cases, better compensation packages than under Glenmark, helped maintain stability during the transition.

By mid-2024, the transformation was largely complete. Alivus Life Sciences had emerged as a stronger entity—backed by a debt-free parent, freed from historical constraints, and positioned to capitalize on global opportunities. The company now had the financial firepower to compete for large CDMO contracts, the independence to pursue any customer, and the strategic clarity that comes from having an owner aligned with long-term value creation.

Post the deal, it would hold only a 7.84% stake in the unit. For Glenmark, watching from the sidelines with their residual stake, it must have been bittersweet. They had nurtured this business for two decades, only to sell it when its best days might be ahead. But such is the nature of corporate finance—sometimes you have to sell your jewelry to save the house.

The Nirma acquisition represented more than just a change in ownership. It was a validation of the API business model, a vote of confidence in India's pharmaceutical manufacturing capabilities, and most importantly, a new chapter in the continuing consolidation of India's pharmaceutical industry. As 2024 drew to a close, Alivus Life Sciences stood ready to write its next chapter—no longer as Glenmark's offspring or Nirma's acquisition, but as an independent force in the global pharmaceutical supply chain.

VI. Current Operations & Financial Performance

The numbers tell a story of transformation amid turbulence. Sales rose 21.05% to Rs 649.55 crore in the quarter ended March 2025 as against Rs 536.60 crore during the previous quarter ended March 2024. For the full year, sales rose 4.54% to Rs 2386.88 crore in the year ended March 2025 as against Rs 2283.21 crore during the previous year ended March 2024. These aren't explosive growth figures, but in the context of a major ownership transition and global supply chain disruptions, they represent remarkable stability.

Walk into any quarterly earnings call, and you'll hear Yasir Rawjee strike a careful balance between optimism and realism. "The start of the new year marks a notable shift for us as we transition to Alivus Life Sciences. I am pleased to report that our Q3 performance reflects this renewed energy, with growth across both GPL and Non-GPL segments. Geographically, regions like India, Europe, ROW and Japan contributed to the growth." The diplomatic language masks a more complex reality—managing the delicate transition from captive supplier to independent player while maintaining relationships on all sides.

The Q3 FY25 performance showcased the business's underlying strength. Net profit of Alivus Life Sciences rose 15.32% to Rs 136.96 crore in the quarter ended December 2024 as against Rs 118.77 crore during the previous quarter ended December 2023. Sales rose 12.05% to Rs 641.84 crore in the quarter ended December 2024 as against Rs 572.80 crore during the previous quarter ended December 2023. But here's what the headline numbers don't capture: the composition of this growth was shifting fundamentally.

The segmental breakdown reveals the strategic challenge. On segmental front, the revenue from Generic API grew by 16.9% YoY to Rs 596.6 crore in Q3 FY25 while revenue from CDMO declined 14.29% YoY to Rs 30 crore in Q3 FY25. The CDMO decline wasn't a failure of execution but rather the lumpy nature of the business—projects move from development to commercial phases unpredictably, creating quarterly volatility that tests investor patience.

What's remarkable is the margin resilience. For Q3FY25, EBITDA was at Rs 200.8 crore, a growth of 15.2% YoY. EBITDA margin stood at 31.3%, up 90 bps YoY. In an industry where Chinese competitors routinely undercut prices by 20-30%, maintaining margins above 30% requires either exceptional operational efficiency or product differentiation—Alivus had both.

The cash position tells another story—one of financial prudence in an capital-intensive industry. During 9MFY25, the company generated a strong free cash flow of Rs 1,838 million leading to Cash and Cash Equivalents (including short term investments) of Rs 4,993 million as of 31 December 2024. This wasn't just about having a war chest; it was about having the flexibility to pursue opportunities without diluting shareholders or taking on debt.

The company has delivered a poor sales growth of 9.20% over past five years. Company is almost debt free. This five-year CAGR might seem disappointing at first glance, but it encompasses the spin-off period, COVID disruptions, and the ownership transition. More importantly, being debt-free in a capital-intensive industry is like being the only person with an umbrella in a rainstorm—when credit markets tighten, you're the one still standing.

The geographic diversification strategy was paying dividends. While many Indian API companies remained overly dependent on the US market, Alivus had built a more balanced portfolio. Geographically, regions like India, Europe, ROW and Japan contributed to the growth. Each geography brought different dynamics—Europe valued environmental compliance, Japan prioritized quality consistency, emerging markets focused on cost-effectiveness.

But challenges lurked beneath the surface. The relationship with Glenmark Pharmaceuticals—still a major customer—created an ongoing balancing act. When GPL business declined 22% year-over-year in certain quarters, it directly impacted Alivus's top line. This customer concentration risk was the elephant in every investor call, addressed but never fully resolved.

The PLI (Production Linked Incentive) scheme impact added another layer of complexity. "Our overall performance has remained consistent with past years, with sustained margins, despite facing external challenges, most notably the loss in PLI revenue. One of the most encouraging outcomes this year was our ability to maintain EBITDA margins at 30%, even in the absence of PLI benefits and amid market headwinds." The government incentive had provided a cushion that was now gone, forcing the company to prove its economics without subsidies.

CFO Tushar Mistry's commentary revealed the operational philosophy: "Our emphasis on achieving quality growth has delivered encouraging outcomes with highest ever quarterly revenue at Rs 6,418 million. This translated to steady gross margins at ~56%, while our EBITDA grew by 15.2% YoY, underscoring our ability to cater a diversified product range while maintaining stringent cost efficiency." The focus on "quality growth" over volume growth was crucial—better to grow slowly with good margins than chase revenue at any cost.

The working capital management deserved special attention. In an industry notorious for stretched receivables and bloated inventories, Alivus maintained disciplined capital turnover. Raw material sourcing—often from the same Chinese suppliers they competed against in finished APIs—required careful inventory management to balance cost and supply security.

Product portfolio evolution continued quietly in the background. While the company maintained its stronghold in cardiovascular and CNS molecules, new additions focused on complex generics coming off patent. The sweet spot was molecules with $50-200 million global market size—large enough to matter, small enough to avoid commodity competition.

The R&D spending, though not separately disclosed in recent quarters, remained substantial. But unlike the parent Glenmark's ambitious novel drug discovery programs, Alivus focused on process innovation—finding better ways to make existing molecules. Less glamorous perhaps, but far more predictable in returns.

Environmental compliance costs were rising but manageable. New effluent treatment requirements, particularly for the oncology facility, required continuous investment. But this too became a competitive advantage—as regulations tightened, smaller competitors struggled to keep up, effectively raising barriers to entry.

The human resources situation reflected broader industry trends. Attracting talent to manufacturing facilities in Mohol or Dahej—far from the urban centers where young professionals preferred to live—required creative compensation and career development strategies. The company's investment in automation wasn't just about efficiency; it was about reducing dependence on hard-to-find skilled operators.

During FY25, the company generated a strong free cash flow of Rs 2,328 million leading to Cash and Cash Equivalents (including short term investments) of Rs 5,487 million as of 31 March 2025. This cash generation, even while investing in capacity expansion, validated the business model's fundamental soundness. It also provided the flexibility for the ambitious capital expenditure plans ahead.

The market's response remained mixed. The 52-week high of Alivus Life Sciences Ltd (ALIVUS) is ₹1335.10 and the 52-week low is ₹819.05. The P/E (price-to-earnings) ratio of Alivus Life Sciences Ltd (ALIVUS) is 25.12. The P/B (price-to-book) ratio is 5.23. These valuations—neither cheap nor expensive—reflected the market's wait-and-see attitude toward the company's transformation under Nirma ownership.

As fiscal 2025 drew to a close, Alivus Life Sciences stood at an inflection point. The operational performance was solid, the balance sheet was strong, and the strategic direction was clear. But execution would determine whether this became another successful Indian API company or something more ambitious—a global CDMO player competing with the best in the world.

VII. The CDMO Strategy & Future Growth

In a nondescript conference room in Dahej, the CDMO team huddles over a molecule structure that looks like modern art—benzene rings connected by elaborate bridges, functional groups jutting out at precise angles. This isn't just chemistry; it's a puzzle worth potentially ₹200 crores in revenue over the next five years. The client, a mid-sized European specialty pharma company, needs someone to scale up production from 10 kilograms to 10 tons while maintaining 99.9% purity. This is the future Alivus is betting on.

The CDMO opportunity represents a fundamental shift in business model. Think of generic APIs as selling commodities—you make what everyone else makes, compete on price and delivery. CDMO is bespoke tailoring—you develop custom processes for specific clients, often for patented molecules, creating relationships that can last decades. The margins tell the story: generic APIs might yield 25-30% EBITDA margins; successful CDMO projects can deliver 40%+.

By early 2025, Alivus had five CDMO projects in various stages, with two more in the pipeline. The pipeline diversity was strategic—some projects were for innovator companies developing new chemical entities, others for specialty generic companies needing complex synthesis capabilities, and a few for large pharma companies outsourcing non-core molecules. Each project type brought different risk-reward profiles and timeline expectations.

The real competitive advantage in CDMO isn't just manufacturing capability—it's the ability to navigate the intersection of chemistry, regulatory requirements, and commercial viability. Take their project with a Japanese innovator: the molecule required a key intermediate that was available only from a single Chinese supplier. Alivus's team developed an alternative synthesis route that bypassed this bottleneck, turning a supply chain vulnerability into a competitive advantage. This kind of problem-solving creates customer stickiness that transcends price competition.

The investment required for CDMO success is substantial but different from traditional API capacity expansion. Instead of large reactors for bulk production, you need flexible, smaller-scale equipment that can handle diverse chemistries. Instead of operators trained on standard processes, you need PhD chemists who can troubleshoot novel synthesis routes. Instead of selling to procurement departments, you're partnering with R&D heads and chief scientific officers.

CapEx plans reflected this strategic shift: ₹600 crore earmarked for expansion, including a state-of-the-art R&D facility and the new Solapur plant. But look closer at the allocation—nearly 40% was for analytical equipment, pilot plants, and R&D infrastructure rather than pure manufacturing capacity. This wasn't about making more of the same; it was about capability building for making anything.

The R&D facility, slated for completion within 18 months, deserved special attention. Designed in collaboration with European CDMO consultants, it would feature kilo labs for early-stage development, pilot plants for scale-up studies, and analytical labs that could support regulatory filings globally. The location—strategically placed between Mumbai and Pune—would help attract talent from India's pharmaceutical research hubs.

Global pharmaceutical trends provided tailwind for the CDMO strategy. Big Pharma's continued focus on biologics and cell therapies meant they were increasingly outsourcing small molecule manufacturing. The patent cliff of 2025-2030 would see over $200 billion in drugs losing exclusivity, creating opportunities for complex generic development. Most importantly, the China+1 strategy wasn't just about supply security anymore; it was about intellectual property protection and regulatory compliance.

Competition in the CDMO space was fierce but fragmented. Global leaders like Lonza and Catalent commanded premium valuations but were expensive. Chinese CDMOs like WuXi AppTec offered cost advantages but faced increasing scrutiny from Western clients over IP concerns. Indian players like Syngene and Piramal Pharma Solutions were credible but focused on different segments. Alivus's sweet spot—complex chemistry for mid-sized molecules—had room for a focused player.

The commercial strategy for CDMO was fundamentally different from generic APIs. Instead of responding to RFQs (Request for Quotations), success required proactive business development. The company hired senior executives from established CDMOs, people who brought not just expertise but relationships with decision-makers at pharmaceutical companies. They attended specialized conferences like CPhI and Informex, not to sell products but to understand emerging needs.

Risk management in CDMO required sophisticated thinking. Unlike generic APIs where demand is predictable, CDMO projects could fail in clinical trials, face regulatory delays, or see commercial plans change. The company's approach was portfolio diversification—never let any single project exceed 15% of CDMO revenue, balance early-stage and commercial projects, mix innovator and generic clients.

The regulatory strategy for CDMO was particularly complex. Each project might require different regulatory filings—DMFs for the US, CEPs for Europe, technical dossiers for emerging markets. The company invested in dedicated regulatory teams for CDMO projects, professionals who understood not just compliance but could advise clients on regulatory strategy. This consultative approach transformed Alivus from vendor to partner.

Technology integration accelerated under the CDMO push. Digital twin technology allowed simulation of scale-up before actual production. Process Analytical Technology (PAT) enabled real-time monitoring of critical parameters. Quality by Design (QbD) principles were embedded from development stage, reducing scale-up risks. These weren't just buzzwords but practical tools that reduced development timelines and improved success rates.

The talent challenge for CDMO was acute. India produced thousands of chemistry graduates, but few with the specific skills needed for complex synthesis and scale-up. Alivus partnered with institutes like ICT Mumbai and NCL Pune, sponsoring research projects and creating a pipeline of specialized talent. They also established a "reverse mentoring" program where young scientists worked with experienced production managers, combining fresh thinking with practical knowledge.

Environmental considerations in CDMO went beyond compliance. Many projects involved hazardous chemistries—organometallics, high-pressure hydrogenations, cryogenic reactions. The company invested in specialized containment equipment and safety systems. But they also developed "green chemistry" capabilities, offering clients environmentally friendly alternatives to traditional synthesis routes—a differentiator particularly valued by European customers.

The financial model for CDMO created interesting dynamics. Development projects might generate limited revenue initially but create annuities during commercial production. The company's approach was to share risk and reward—lower development fees in exchange for better commercial terms. This aligned incentives and created longer-term partnerships rather than transactional relationships.

Customer testimonials, though not publicly disclosed for confidentiality reasons, revealed the value proposition. A European specialty pharma executive privately shared: "They're not the cheapest, but they deliver what they promise. More importantly, when we hit problems—and we always do—they find solutions rather than excuses." This reputation for reliability was worth more than any marketing campaign.

By mid-2025, the CDMO strategy was showing early results. The two projects moving to commercialization were expected to generate ₹50 crores per quarter—meaningful contribution to the top line with superior margins. More importantly, the pipeline was building, with several projects in phase II/III trials that could commercialize in 2026-2027.

The long-term vision was ambitious but achievable: CDMO contributing 30-40% of revenue within five years, relationships with top 20 pharma companies globally, and recognition as the partner of choice for complex small molecule development. This wasn't about abandoning the generic API business—that provided stable cash flows and manufacturing scale. It was about adding a higher-margin, higher-growth layer on top.

The risks were real. CDMO required patient capital—projects could take 3-5 years from initiation to commercial revenues. Customer concentration could increase as successful projects scaled. Technical failures, while rare, could damage reputation disproportionately. Competition from Chinese CDMOs with state backing could intensify pricing pressure.

Yet the opportunity was compelling. The global CDMO market for small molecules was expected to grow at 7-8% annually, reaching $50 billion by 2030. India's share was less than 5%, suggesting substantial room for growth. Alivus's combination of chemistry capabilities, manufacturing scale, and now Nirma's financial backing positioned them to capture a meaningful share of this opportunity.

As the CDMO team in Dahej finalizes the process for that complex molecule, they're not just solving a chemistry problem. They're building the foundation for Alivus's transformation from a successful API manufacturer to a global pharmaceutical services leader. The journey from ₹2,400 crores in revenue to potentially ₹5,000 crores lies through this CDMO corridor—complex, risky, but ultimately rewarding for those who can navigate it successfully.

VIII. Playbook: Business & Investing Lessons

The Art of the Spin-off: When Separation Creates Value

The Glenmark-Alivus separation offers a masterclass in value creation through division. The paradox is compelling: the combined entity was worth less than the sum of its parts. Why? Because investors couldn't properly value an innovative pharma company with a stable API business hidden inside, nor could they appreciate an API business constrained by its parent's priorities.

The timing mattered enormously. Had Glenmark attempted this separation five years earlier, the API business wouldn't have had sufficient scale or customer diversification. Five years later, and the debt situation might have forced a distressed sale. The 2019-2021 window—with COVID highlighting supply chain resilience and markets hungry for pharmaceutical IPOs—was optimal.

The execution playbook is worth studying. First, operational separation preceded legal separation by years. Separate management teams, distinct P&Ls, and independent customer relationships were established well before the spin-off. Second, the IPO route rather than direct sale allowed price discovery while maintaining control. Third, retaining majority stake post-IPO provided continuity comfort to customers while allowing future monetization at better valuations.

For investors, the lesson is to look for similar situations: divisions that serve different customers, require different capabilities, and trade at different multiples when independent. The red flags to avoid: excessive interdependence, unclear separation costs, and management teams unprepared for independence.

Building Trust in Regulated Markets: Quality as Competitive Advantage

In APIs, regulatory compliance isn't just a cost center—it's the moat. Every successful FDA inspection, every clean EIR (Establishment Inspection Report), every approved DMF adds another brick to the trust wall. Alivus understood this deeply, maintaining separate quality units for different facilities to prevent systemic issues from spreading.

The investment in quality seems excessive until you consider the alternative. One FDA warning letter can destroy years of relationship building. Customers might tolerate slightly higher prices or longer lead times, but they won't tolerate quality uncertainty. In this business, trust is earned in decades and lost in days.

The playbook extends beyond mere compliance. Proactive communication with regulators, voluntary upgrades beyond minimum requirements, and transparent disclosure of issues before they become problems—these build regulatory capital that pays dividends during inspections. When FDA inspectors know you as the company that self-reports and fixes problems, they approach inspections differently than with companies known for hiding issues.

Debt-free Operations in Capital-intensive Industry

Operating without debt in an industry that typically leverages 2-3x EBITDA requires discipline that borders on paranoia. But Alivus's debt-free status wasn't just conservative financial management—it was strategic positioning. In a cyclical industry with volatile input costs and pricing pressure, leverage amplifies both upside and downside.

The debt-free advantage manifests in multiple ways. Negotiating power with suppliers improves when they know you can pay cash. Customer confidence increases when they know financial distress won't disrupt supply. Most importantly, strategic flexibility—the ability to pursue opportunities or weather downturns without banker approval—has option value that doesn't appear on financial statements.

The capital allocation framework that enables debt-free operation is instructive. First, match investment timing with cash generation, not market opportunity—better to be late to capacity expansion than early with borrowed money. Second, maintain higher working capital buffers than leveraged competitors—the cost of carrying extra inventory is less than the cost of supply disruption. Third, return excess capital to shareholders rather than pursuing empire building—discipline in good times provides flexibility in bad times.

Transitioning from Captive to Third-party Business Model

The psychological shift from captive supplier to market competitor might be the hardest transformation in business. Employees comfortable with internal transfer pricing must learn market pricing. Sales teams accustomed to guaranteed orders must learn to compete. R&D familiar with parent company priorities must learn market needs.

The successful transition requires deliberate culture change. Hiring outsiders for key positions brings market perspective but risks losing institutional knowledge. The balance Alivus struck—keeping operational leadership while bringing in commercial expertise—offers a template. Yasir Rawjee's external hiring as CEO, while retaining technical teams, exemplified this approach.

The customer diversification strategy proceeded in waves. First, sell to other Indian companies who understood the quality heritage. Then, expand to regulated markets leveraging existing certifications. Finally, pursue innovator companies with CDMO offerings. Each wave built on the previous, reducing parent company dependence gradually rather than abruptly.

The metrics evolution tells the story. Initially, success was measured by capacity utilization and cost per kilogram. Post-independence, metrics shifted to customer acquisition, wallet share, and margin expansion. This wasn't just reporting change but fundamental reimagining of what constituted success.

The Conglomerate Advantage: Strategic Buyers vs. Financial Buyers

Nirma's acquisition reveals an underappreciated truth: in certain situations, strategic buyers from adjacent industries create more value than industry consolidators or financial buyers. Nirma brought chemical expertise, procurement scale, and patient capital without the baggage of competing priorities or portfolio optimization that plague industry buyers.

The synergy realization followed unexpected patterns. Cost synergies came not from headcount reduction but from procurement leverage and shared infrastructure. Revenue synergies emerged not from cross-selling but from Nirma's credibility opening doors in new geographies. Most surprisingly, cultural synergies—both companies' DNA of competing against multinationals—proved more valuable than financial synergies.

For sellers, the lesson is to think broadly about potential acquirers. The obvious buyer—industry leader looking for consolidation—might not be the best buyer. For acquirers, the lesson is that adjacency can be an advantage. You bring fresh perspective, avoid antitrust issues, and can often pay more because you're not duplicating existing operations.

Building Competitive Advantage Through Complexity

Alivus's focus on "non-commoditized" APIs wasn't just marketing speak—it was systematic selection of molecules where complexity created barriers. Complex doesn't just mean difficult synthesis; it means regulatory complexity, supply chain complexity, customer requirement complexity. Each layer of complexity that you can manage but competitors cannot becomes a moat component.

The framework for evaluating complexity is multidimensional. Technical complexity: how many synthetic steps, what specialized equipment needed, what purity requirements? Regulatory complexity: how many markets need approval, what documentation required, what inspection history needed? Commercial complexity: how many customers, what service levels, what payment terms? The sweet spot is high enough complexity to deter competition but not so high that it becomes uneconomical.

The capability building followed a logical sequence. Start with moderate complexity to build competence. Use profits from established products to fund capability expansion. Move up the complexity curve gradually, ensuring each new level builds on previous capabilities. This patient approach contrasts with the "big bang" transformation attempts that often fail.

The Information Asymmetry Advantage

One underappreciated aspect of the API business is the information asymmetry between manufacturers and customers. Pharmaceutical companies know their formulation needs but often don't understand API manufacturing intricacies. This knowledge gap creates opportunity for value creation through consultation, not just supply.

Alivus leveraged this by becoming educators, not just vendors. Technical seminars for customer R&D teams, regulatory workshops for quality departments, supply chain consultations for procurement teams—these built relationships beyond commercial transactions. When customers see you as a knowledge partner, price becomes secondary to value.

The information advantage compounds over time. Each customer interaction provides market intelligence about upcoming needs, competitive dynamics, and regulatory changes. This mosaic of information, properly synthesized, provides strategic advantage no amount of market research can replicate.

Managing the Innovation Paradox

The API business faces an innovation paradox: you must continuously innovate to stay competitive, but most innovation has limited appropriability—process improvements can be reverse-engineered, cost reductions get passed to customers. Alivus's approach to this paradox offers lessons.

First, focus innovation on customer problems, not just internal efficiency. A process that reduces customer's regulatory burden creates value you can capture. Second, bundle innovations rather than monetize individually—a suite of improvements is harder to replicate than individual advances. Third, use innovation to move into higher-value segments rather than just improve existing operations.

The R&D allocation strategy reflected this thinking. Rather than pursuing breakthrough innovation (high risk, long timeline) or purely incremental improvement (low return), they focused on "application innovation"—novel ways to apply existing knowledge to customer problems. This middle path balanced risk and return while building cumulative advantage.

The Platform Economics Hidden in Plain Sight

While not a technology platform in the traditional sense, Alivus exhibits platform characteristics that create value. The manufacturing infrastructure serves multiple products, spreading fixed costs. The regulatory certifications enable multiple market entries, amortizing compliance costs. The customer relationships support multiple molecule sales, reducing selling costs.

Understanding these platform dynamics changes strategic thinking. Adding a new molecule to existing infrastructure has different economics than building dedicated capacity. Entering a new geography with existing products differs from simultaneous market and product development. Cross-selling to existing customers beats acquiring new customers for single products.

The operational implications are profound. Invest in flexible rather than dedicated assets. Build capabilities that serve multiple purposes. Maintain excess capacity that appears inefficient but enables opportunity capture. These principles contradict traditional manufacturing efficiency metrics but create strategic optionality.

The Trust Equation in B2B Relationships

In B2B pharmaceuticals, trust has specific components: technical competence (can you make it?), regulatory reliability (will it pass inspection?), supply security (will you deliver?), and relationship stability (will you be here tomorrow?). Alivus systematically built each component, understanding that weakness in any dimension undermines the others.

The trust-building playbook is replicable. Start with smaller, less critical orders to demonstrate capability. Graduate to strategic products as trust builds. Never compromise quality for short-term gain—reputation damage exceeds any immediate benefit. Most importantly, communicate problems proactively—customers forgive mistakes but not surprises.

The returns to trust compound wonderfully. Trusted suppliers get early visibility into customer needs, allowing better planning. They receive higher prices because switching costs include rebuilding trust elsewhere. They weather occasional problems because relationship value exceeds incident cost. In industries where trust takes years to build, it becomes the ultimate competitive advantage.

IX. Analysis & Bear vs. Bull Case

Bull Case: The Aligned Stars

Begin with the macroeconomic tailwinds that feel almost too perfect. The global pharmaceutical industry stands at $1.6 trillion and growing, with the API segment capturing an increasing share as drug complexity rises. More critically, the China+1 narrative has evolved from supply chain nice-to-have to boardroom imperative. When the U.S. BIOSECURE Act discussions explicitly name Chinese pharmaceutical companies as security risks, Indian API manufacturers don't just benefit from sentiment—they benefit from policy.

Alivus's positioning within this context appears almost prescient. The focus on non-commoditized APIs means they're not competing with hundreds of Chinese manufacturers churning out acetaminophen. It is a leading developer and manufacturer of select, high-value, non-commoditized, active pharmaceutical ingredients (APIs) in chronic therapeutic areas. These chronic therapy areas—cardiovascular, CNS, diabetes—represent growing segments as global populations age and lifestyle diseases proliferate.

The Nirma backing transforms the financial equation. Company is almost debt free. In an industry where competitors typically leverage 2-3x EBITDA, Alivus can pursue opportunities others cannot afford. Want to build that $100 million R&D facility? No banker approval needed. See an acquisition opportunity? Move fast without financing contingencies. This financial flexibility has strategic value beyond the balance sheet numbers.

The regulatory track record provides another bull pillar. With approvals from USFDA, PMDA, EDQM, and others, Alivus has demonstrated ability to meet the world's strictest standards. Each successful inspection adds to the trust bank, creating switching costs for customers who might otherwise be tempted by cheaper alternatives. In pharmaceuticals, regulatory excellence isn't just compliance—it's competitive advantage.

The CDMO opportunity could be transformative. If even three of the five projects in pipeline achieve commercial success, we're looking at potential revenue addition of ₹600-800 crores annually at margins significantly above the corporate average. The global CDMO market grows at 7-8% annually, and India's penetration remains under 5%. Alivus doesn't need to dominate—just capturing incremental share creates substantial value.

Management quality, often overlooked in technical discussions, deserves emphasis. Yasir Rawjee navigated the company through spin-off, IPO, and acquisition while maintaining operational performance. "FY25 was our first full year under the Nirma ownership. Our overall performance has remained consistent with past years, with sustained margins, despite facing external challenges, most notably the loss in PLI revenue." This steady hand through transformation suggests capability to handle future challenges.

The valuation argument has merit. Trading at 25x earnings might seem full, but compare to global CDMO players at 35-40x or innovative pharma at 30-35x. As Alivus transitions toward higher-value services, multiple expansion seems plausible. The market capitalization of ₹11,463 crores could double if the company successfully executes its CDMO strategy and achieves peer multiples.

Bear Case: The Uncomfortable Questions

Start with the elephant: The company has delivered a poor sales growth of 9.20% over past five years. Yes, this period included COVID, spin-off, and ownership change. But five years is long enough to smooth disruptions. If management couldn't deliver double-digit growth during a period of pharmaceutical industry expansion, why expect acceleration now?

Customer concentration remains troubling despite diversification efforts. Glenmark might be declining as a percentage of revenue, but the top 10 customers likely still represent 60%+ of sales. Lose one major customer—entirely possible in the brutal generic drug industry—and the growth story evaporates. The CDMO strategy might actually increase concentration as successful projects scale.

The CDMO transition itself carries execution risk that bulls underestimate. Moving from transactional API supply to collaborative development partnerships requires different capabilities—technical, commercial, cultural. Many Indian pharmaceutical companies have attempted this transition; few have succeeded at scale. What makes Alivus different?

Competition intensifies from every direction. Chinese manufacturers are moving upmarket, improving quality while maintaining cost advantages. Other Indian players like Laurus Labs and Neuland Laboratories are pursuing similar strategies with deeper pockets or longer track records. Global CDMOs are establishing Indian operations to access talent while maintaining international brand premium. Where's the sustainable differentiation?

The Nirma ownership, while providing capital, raises strategic questions. Does a conglomerate focused on chemicals and consumer products have the pharmaceutical expertise to guide strategic decisions? Will they have patience for CDMO investments that might take 5-7 years to fully pay off? The cultural integration between a Gujarati conglomerate and a Mumbai-based pharmaceutical company might prove harder than anticipated.

Regulatory risks never disappear in pharmaceuticals. One FDA warning letter—even for minor issues—could disrupt customer relationships and delay new business. The parent company Glenmark's history of regulatory issues, while technically separate, creates reputational overhang. Customers might wonder: are the quality systems truly independent?

The margin sustainability deserves scrutiny. EBITDA margin stood at 31.3%, up 90 bps YoY. Impressive, but how sustainable as Chinese competition returns post-COVID and input costs normalize? The loss of PLI benefits already pressures margins. Price erosion in generic APIs continues relentlessly. Can CDMO revenue scale fast enough to offset margin pressure in the base business?

The Decisive Factors

Three critical variables will determine which case prevails:

CDMO Execution: If Alivus successfully commercializes even half the pipeline projects and wins 2-3 new projects annually, the bull case gains credibility. But if projects face delays, technical failures, or customer defections, the growth story unravels. Watch quarterly updates on project progression and new win announcements.

Customer Diversification: The trajectory of non-Glenmark revenue tells the independence story. If external revenue reaches 75%+ with no customer exceeding 15%, concentration risk diminishes substantially. But if Glenmark dependence persists or new concentration emerges, the risk profile remains elevated.

Margin Evolution: The ability to maintain 30%+ EBITDA margins while transitioning the business model would validate the strategy. But if margins compress below 25%, it suggests commoditization pressures overwhelming mix improvement benefits.

Scenario Analysis

Best Case (20% probability): CDMO strategy succeeds spectacularly. Revenue reaches ₹4,000 crores by FY28 with CDMO contributing 40%. Margins expand to 35% on mix improvement. The stock re-rates to 35x earnings, implying market cap of ₹25,000 crores. Returns: 120% over three years.

Base Case (50% probability): Steady execution with modest CDMO success. Revenue grows at 12-15% annually reaching ₹3,200 crores by FY28. Margins stable around 30%. Modest multiple expansion to 28x. Market cap of ₹16,000 crores. Returns: 40% over three years.

Bear Case (30% probability): CDMO struggles, competition intensifies. Revenue growth slows to 5-7% annually. Margins compress to 25%. Multiple contracts to 20x. Market cap of ₹10,000 crores. Returns: -13% over three years.

The Investment Decision Framework

For growth investors, Alivus offers exposure to structural themes—supply chain diversification, CDMO growth, Indian pharmaceutical evolution—with reasonable valuation. The Nirma backing provides downside protection while CDMO optionality offers upside. Position sizing should reflect execution uncertainty.

For value investors, the current valuation appears full unless you believe in dramatic business model transformation. Wait for better entry points during market corrections or operational disappointments. The debt-free balance sheet limits distress scenarios, making patience affordable.

For income investors, the dividend policy remains uncertain under new ownership. The current dividend yield of Alivus Life Sciences Ltd (ALIVUS) is 0.50. This suggests capital appreciation, not income, drives returns. Look elsewhere for yield.

The Verdict

The bull-bear debate ultimately reduces to a single question: Can Alivus transform from a successful API manufacturer to a value-added pharmaceutical services company? The pieces are in place—technical capability, regulatory credentials, financial resources, market opportunity. But execution in pharmaceuticals is notoriously difficult, with long timelines and binary outcomes.

The risk-reward appears balanced at current valuations. Bulls betting on successful transformation could see substantial returns. Bears worried about execution challenges won't lose catastrophically given the solid base business and strong balance sheet. Like many investment decisions, this one depends on your tolerance for transformation risk and patience for long-term execution.

For those choosing to invest, three guideposts for monitoring: 1. CDMO revenue run-rate reaching ₹50 crores per quarter by FY26 2. Customer concentration metrics improving with top 10 customers below 50% of revenue 3. Margins holding above 28% despite mix shift and competition

If these metrics trend positively, add on weakness. If they deteriorate, respect the message and reassess. In the complex world of pharmaceutical manufacturing, execution excellence separates winners from also-rans.

X. Epilogue & Future Outlook

The Rebranding as Metaphor

December 2024. The nameplate outside the Mumbai corporate office changes from "Glenmark Life Sciences" to "Alivus Life Sciences." On the surface, it's just rebranding—new logo, new website, updated business cards. But symbolically, it represents something profound: the final cutting of the umbilical cord, the emergence of a fully independent identity after years of living in a parent's shadow.

The name "Alivus" itself tells a story. Derived from roots suggesting life and vitality, it signals ambition beyond just manufacturing white powders for other companies' tablets. This is about being alive to possibilities, vital to the global pharmaceutical supply chain. It's a declaration that the company's best chapters lie ahead, not behind.

The R&D Facility: Building for Tomorrow

Eighteen months from now, if plans hold, a new R&D facility will rise between Mumbai and Pune. This isn't just another building—it's a statement of intent. Designed with input from European CDMO consultants, featuring kilo labs that wouldn't look out of place in Basel or Boston, equipped with analytical instruments that can detect impurities at parts-per-billion levels.

But buildings don't innovate—people do. The real investment is in the 200+ scientists who will work there, the partnerships with academic institutions that will feed talent, the culture of innovation that must be carefully cultivated. Can a company that spent two decades as a cost-efficient manufacturer build the innovation muscle needed for CDMO leadership? The R&D facility will be the crucible where this transformation is tested.

India's Pharmaceutical Destiny

Alivus's story cannot be separated from India's larger pharmaceutical narrative. The country that became the "pharmacy of the world" through generic drugs now aspires to move up the value chain—from copying molecules to creating them, from supplying ingredients to developing drugs. This transition isn't just about economics; it's about national pride, strategic autonomy, and global standing.

The geopolitical context adds urgency. As U.S.-China tensions reshape global supply chains, as Europe seeks to reduce dependency on single sources, as Japan emphasizes supply security, India has a generational opportunity to become the trusted alternative. But trust in pharmaceuticals isn't granted by geography—it's earned through consistent quality, reliable supply, and regulatory excellence.

Alivus embodies both the opportunity and challenge. They have the technical capability, regulatory approvals, and now financial backing to compete globally. But so do dozens of other Indian companies. The winners will be those who can execute consistently, innovate purposefully, and build relationships that transcend transactions.

The Five-Year Vision