Solventum: From 3M's Healthcare Crown Jewel to Independent Innovator

I. Introduction & Setting the Stage

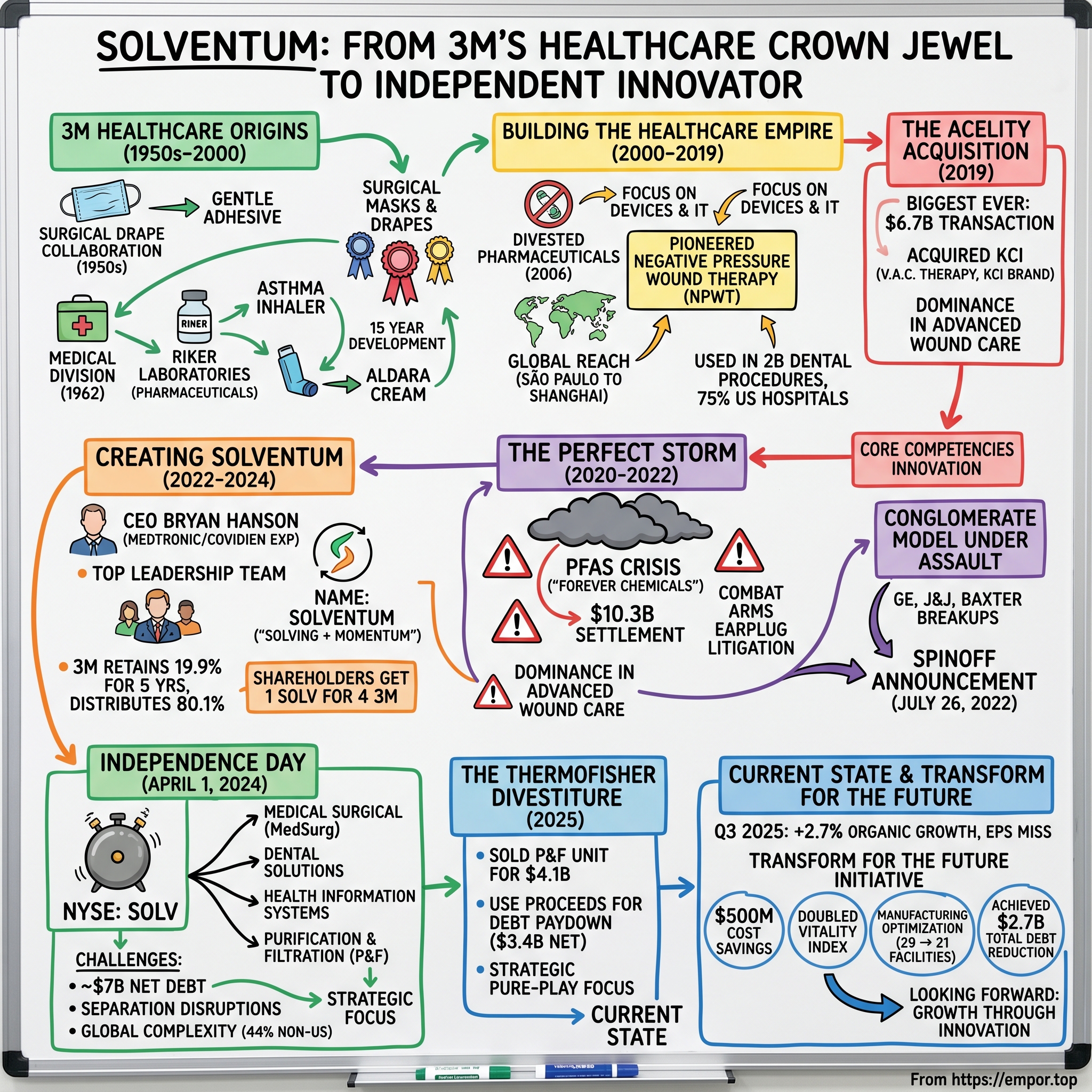

The rain-soaked streets of South Carolina's federal courthouse gleamed under the March sun as lawyers filed out, briefcases heavy with settlement papers. Inside, 3M had just agreed to write a check that would make headlines worldwide: $10.3 billion to settle claims over "forever chemicals" contaminating America's drinking water. For the 122-year-old industrial conglomerate, it was a moment that crystallized years of mounting pressures—legal, financial, and existential.

Four days later, on April 1, 2024, a new company called Solventum Corporation began trading on the New York Stock Exchange under the ticker symbol "SOLV". The spinoff represented more than just corporate restructuring; it was the liberation of a business that had sales of $8.2 billion in 2023 and employed 22,000 employees worldwide.

This wasn't just another healthcare spinoff in an era of conglomerate breakups. Solventum emerged as one of the largest medical device separations in history, joining the ranks of Covidien's split from Tyco and Abbott's creation of Abbvie. Yet paradoxically, this "new" company brought with it seven decades of healthcare innovation heritage—from the first surgical drapes to breakthrough wound care technologies.

The story of Solventum is really three intertwined narratives: how a tape company became a healthcare powerhouse, why 3M had to let its crown jewel go, and what happens when $8 billion in revenue and decades of innovation suddenly stand alone. As Bryan Hanson, who joined 3M on September 1 as CEO of the Health Care Business Group, coming from Zimmer Biomet where he served as President and Chief Executive Officer since 2017, would later say at the company's inaugural investor day: "We're a new company with a long legacy of creating breakthrough solutions."

The timing was no accident. Healthcare spinoffs had become the strategy du jour—General Electric, Johnson & Johnson, Baxter, and Medtronic all announced similar moves. But Solventum's path would prove uniquely challenging, emerging debt-laden into independence while simultaneously executing one of the most complex operational separations in recent corporate history.

II. The 3M Healthcare Origins Story (1950s-2000)

The genesis of 3M's healthcare empire began not in a laboratory, but in a conversation. After World War II, three physicians approached 3M with the idea to create a surgical drape using a plastic sheet that could stick to skin. The doctors knew about 3M tapes so they wanted to collaborate with 3M scientists to create a gentle adhesive that would stick to skin. At the time, surgeons were still using sterilized cloth attached with painful pincers—a medieval solution in the atomic age.

3M established a Medical Division in 1962, the same year the company moved to its new global headquarters in Maplewood, Minnesota. But the healthcare ambitions had been percolating for over a decade. The company's culture, famously described by technical director Ken Hanley, was distinctive: "We lead with a focus on science and technology, unlike most companies which lead by focusing on a specific market. Our culture is to be curious and explore. We have an appetite for solutions. We have relevant technologies and science that can be applied to improving lives, and health care is the perfect fit".

The pharmaceutical chapter began when 3M retained the Riker Laboratories name for the subsidiary until at least 1985 after acquiring the California-based company in the mid-1960s. This wasn't a dabbling—it was serious science. By the late 1950s, 3M had produced its first asthma inhaler, and in the mid-1990s, 3M Pharmaceuticals produced the first CFC-free asthma inhaler in response to adoption of the Montreal Protocol.

Perhaps the most striking example of 3M's patience and persistence came with Aldara. In the 1980s and 1990s, the company spent fifteen years developing a topical cream delivery technology which led in 1997 to health authority approval and marketing of a symptomatic treatment for genital warts, Aldara. Fifteen years for a single product—that's the kind of long-term thinking that would become increasingly rare in the quarterly-earnings-obsessed pharmaceutical industry.

The innovation wasn't limited to drugs. The decorative ribbons had been developed from the innovative non-woven fibers process, which also led to many other successful products including surgical masks and drapes. From tape to surgical drapes to pharmaceuticals—each innovation built on the last, creating what 3M called "technology platforms" that could spawn entire product families.

By 2000, 3M's healthcare business had grown from a single surgical drape idea into a diversified portfolio spanning wound care, dental products, drug delivery systems, and health information technology. The division was generating billions in revenue and had become central to 3M's identity as an innovation company. Yet even as the new millennium dawned, forces were gathering that would ultimately force 3M to choose between its industrial heritage and its healthcare future.

III. Building the Healthcare Empire (2000-2019)

Mike Roman stood before Wall Street analysts in 2006, explaining what many saw as heresy: 3M was walking away from pharmaceuticals. 3M divested its pharmaceutical unit through three deals in 2006, netting more than US$2 billion. At the time, 3M Pharmaceuticals comprised about 20% of 3M's healthcare business and employed just over a thousand people.

The divestiture marked a pivotal strategic shift—3M would focus on medical devices and healthcare IT, not drug development. It was a bet that material science, not molecular science, would drive the company's healthcare future.

That bet would soon be validated spectacularly. 3M pioneered Negative Pressure Wound Therapy (NPWT), becoming first-to-market with a technology that would revolutionize wound care. The company's scientists had figured out how to use controlled negative pressure to promote healing in complex wounds—turning physics into medicine.

Geographic expansion accelerated through the 2010s. 3M's healthcare products found their way into hospitals from São Paulo to Shanghai. The company claimed its products were used in over two billion dental procedures worldwide, while its software ran in more than 75% of U.S. hospitals. These weren't just sales statistics; they represented deep entrenchment in global healthcare infrastructure.

The innovation engine kept humming, leveraging what the company called its core competencies: innovating at the intersection of health, material, and data science. Adhesives technology from the tape division improved surgical dressings. Filtration expertise from industrial applications enhanced biopharmaceutical manufacturing. Data analytics capabilities transformed hospital coding and billing systems.

By 2018, 3M Healthcare had become a $7 billion enterprise within an enterprise, contributing roughly 20% of the company's total revenue. The division operated almost autonomously, with its own R&D centers, manufacturing facilities, and go-to-market strategies. It had, in many ways, outgrown its parent—a fact that would soon become impossible to ignore when acquisition fever struck in 2019.

IV. The Acelity Acquisition: Biggest Healthcare Bet (2019)

3M agreed to buy medical-products maker Acelity Inc. for about $4.4 billion, its biggest acquisition ever, with the company valuing the transaction at $6.7 billion including Acelity's debt. The October 2019 completion transformed 3M Healthcare overnight.

The Acelity business was well known for creating and growing new segments based on the ability to identify and address unmet clinical needs with KCI-branded products that advance the practice of medicine, beginning with the introduction of V.A.C.® Therapy - groundbreaking Negative Pressure Wound Therapy. Today, KCI product offerings also include advanced wound dressings and negative pressure surgical solutions. KCI's solutions contribute to better patient outcomes by enhancing wound healing. The business has annual revenue of approximately $1.5 billion with year-to-date organic growth of 5 percent through September 30, 2019.

The strategic logic seemed impeccable. As CEO Mike Roman explained on the investor call: "Health care for us has been a strong growth marketplace and portfolio, so we've been investing in a broader range of technologies". Acelity's KCI division would become part of 3M's Medical Solutions business, creating critical mass in advanced wound care—a market growing faster than overall healthcare spending.

Integration began immediately, with 3M deploying its vaunted operational excellence to streamline Acelity's supply chain and expand its global reach. The combined wound care portfolio now treated 1.6 million hard-to-heal wounds annually, establishing 3M as a dominant force in a $10 billion global market.

Yet even as champagne corks popped in St. Paul, storm clouds were gathering. The Acelity acquisition added significant debt to 3M's balance sheet just as the company faced mounting legal challenges. What looked like strategic boldness in 2019 would soon seem like unfortunate timing. The acquisition that was meant to secure 3M Healthcare's future would instead become one of the catalysts for its independence.

V. The Perfect Storm: Why 3M Had to Split (2020-2022)

The PFAS crisis erupted like a slow-motion avalanche. These "forever chemicals," once prized for their versatility, had become 3M's forever nightmare. 3M produced about 70% of PFOA and PFOS that was used historically in the US. The company stopped making the chemicals in the early 2000s, but decades of use in firefighting foam and other products led to widespread contamination of drinking water sources. The chemicals are slow to break down in the environment. Facing thousands of lawsuits over PFAS contamination and growing liabilities, 3M announced in late 2022 that it will cease production of all PFAS, including fluoropolymers, by the end of 2025.

The settlement negotiations were staggering in scope. 3M agreed to contribute up to a present value of $10.3 billion, payable over 13 years. 3M expected to record a pre-tax charge of approximately $10.3 billion in the second quarter of 2023. This wasn't just about money—it was about 3M's very identity as a responsible corporate citizen being called into question.

Simultaneously, military veterans were suing over allegedly defective Combat Arms earplugs, claiming hearing damage from products meant to protect them. The litigation tsunami was overwhelming 3M's legal department and dominating management attention.

The conglomerate model itself was under assault from Wall Street. Investors increasingly valued focused pure-plays over diversified industrials. General Electric announced that it would spin off its health care, aerospace, and energy businesses. Johnson & Johnson announced that it would spin off its consumer health division. Comparisons were also made to the decisions by Kellogg's and Toshiba to split into multiple entities, as well as United Technologies's spin-off of Otis Worldwide and Carrier Global.

On July 26, 2022, 3M announced that it would spin off its healthcare division as a separate company to streamline operations. CEO Mike Roman said that the split would "position 3M for the future, to create more opportunity and greater certainty". The announcement came the same day that 3M's Aearo Technologies subsidiary filed for Chapter 11 bankruptcy over the earplug litigation—a stark juxtaposition of crisis and opportunity.

The healthcare division, generating a quarter of 3M's revenue, had become too valuable to remain tethered to a company drowning in industrial-era liabilities. The spinoff wasn't just strategic repositioning; it was a life raft for one of 3M's most promising businesses.

VI. The Spinoff Process: Creating Solventum (2022-2024)

The search for leadership began immediately. 3M needed someone who understood both the complexity of medical device markets and the intricacies of corporate separations. Bryan Hanson fit the bill perfectly. Prior to joining Zimmer Biomet, Hanson was Executive Vice President and President of Medtronic's Minimally Invasive Therapies Group, where he oversaw and provided strategic direction to an approximately $9 billion business. Prior to Medtronic, he served in a number of executive roles of increasing responsibility at Covidien.

His experience was particularly relevant: In 2011, as Surgical Solutions Group President, Hanson transformed two of Covidien's largest divisions—Energy-based Devices and Surgical Devices—into one global business unit. He had lived through Covidien's spin from Tyco, participated in its sale to Medtronic, and led a major divestiture to Cardinal Health. Few executives had his depth of experience in healthcare transformations.

Building the leadership team became Hanson's first priority. He recruited Wayde McMillan, another Covidien/Medtronic veteran, as CFO. Chris Barry, former CEO of NuVasive, joined as Executive Vice President. The team was deliberately constructed from executives who had navigated similar transitions.

On November 16, 2023, 3M unveiled that the new company would be called Solventum, a portmanteau of the words "solving" and "momentum". The name was more than branding—it was a statement of intent. "Solving" captured the company's problem-solving DNA inherited from 3M, while "momentum" signaled the urgency of independent growth.

The financial engineering was complex. 3M's Board of Directors approved the distribution to 3M shareholders of 80.1% of the outstanding shares of Solventum. 3M will retain 19.9% of the outstanding shares of Solventum common stock, which will be monetized within five years following the spin-off. The structure provided 3M with future monetization options while giving Solventum immediate independence.

Holders of 3M common stock received one share of Solventum common stock for every four shares of 3M common stock held at the close of business on March 18, 2024. The mechanics were straightforward, but the operational separation was anything but. Systems, contracts, employees, and facilities all needed to be carved out or replicated. It was like performing surgery on conjoined twins who shared vital organs.

VII. Independence Day: Solventum as Standalone (April 1, 2024)

Bryan Hanson rang the opening bell at the New York Stock Exchange on April 3, 2024, two days after Solventum officially began trading. The company emerged with four distinct business segments: Medical Surgical (MedSurg), Dental Solutions, Health Information Systems, and Purification & Filtration. Each represented a different facet of 3M's healthcare legacy, now united under a single, focused management team.

The numbers painted a picture of instant scale: products used in over two billion dental procedures, treatments for 1.6 million hard-to-heal wounds annually, software in more than 75% of U.S. hospitals, and membrane technology enabling 25 million dialysis treatments per year. This wasn't a startup—it was a fully formed healthcare giant freed from its industrial parent.

Yet freedom came with burdens. Wall Street expected Solventum to shoulder approximately $7 billion in net debt, with interest servicing immediately eating into free cash flow. The company's initial guidance reflected these realities: flat to slightly negative revenue growth for 2024 as it dealt with separation disruptions and built standalone infrastructure.

The challenges were immediate and multifaceted. Solventum needed to establish its own IT systems, having relied on 3M's infrastructure for everything from enterprise resource planning to email. Supply chains required reconfiguration—many products were manufactured in shared 3M facilities. Customer contracts needed to be transferred, regulatory approvals updated, and employee benefits restructured.

Geographic complexity added another layer. With 44% of sales coming from outside the U.S., Solventum had to establish legal entities, tax structures, and operational capabilities across dozens of countries simultaneously. Each market had its own regulatory requirements, distribution partnerships, and competitive dynamics.

The market's initial reception was cautiously optimistic. Solventum was immediately added to the S&P 500 index, providing automatic inclusion in index funds and institutional portfolios. But analysts worried about the debt burden, questioning whether the company could simultaneously deleverage, invest in growth, and maintain competitive R&D spending.

VIII. The Thermo Fisher Divestiture: Strategic Focus (2025)

Eight months into independence, Solventum made its boldest move yet. On February 25, 2025, the company announced it would sell its Purification & Filtration business to Thermo Fisher Scientific for $4.1 billion. The transaction closed on September 2, 2025, for $4.0 billion in cash before customary adjustments, with Solventum using the net proceeds of $3.4 billion primarily to pay down outstanding debt.

The divestiture represented more than financial engineering—it was strategic focus in action. P&F had been a solid business, serving bioprocessing, healthcare, and industrial filtration markets. But it didn't fit Solventum's vision of becoming a pure-play medical device and healthcare IT company. As CEO Bryan Hanson explained: "Completing the transaction is an important milestone in Solventum's three-phased transformation plan and positions us well to advance our capital allocation strategy as we reduce leverage and strengthen our balance sheet with enhanced flexibility to invest in organic and inorganic growth opportunities. Looking ahead, we remain focused on strategic execution, ensuring we deliver even greater value to our customers, team members and investors".

The operational complexity of the divestiture rivaled the original 3M separation. Seven manufacturing facilities transferred to Thermo Fisher, along with 1,700 employees. Nearly 200 transition service agreements ensured continuity for customers during the handover. Following the transaction close, Solventum will provide transitional services and perform certain manufacturing and distribution activities on behalf of Thermo Fisher.

Financially, the impact was transformative. The debt reduction fundamentally altered Solventum's trajectory, reducing interest expense and freeing up cash flow for growth investments. Solventum's updated full year 2025 guidance reflects the expected reduction of net interest expense, which will more than offset the financial impact of the divestiture of the P&F business.

Updated 2025 guidance reflected newfound confidence: organic sales growth of 2-3% and adjusted earnings per share of $5.88-$6.03. The company had successfully executed its first major strategic move as an independent entity, proving it could actively manage its portfolio rather than simply operate inherited assets.

IX. Current State & Transform for the Future Initiative

The third quarter 2025 earnings call on November 6 brought mixed news. Sales of $2.1 billion increased 2.7% on an organic basis compared to the prior year and increased 0.7% on a reported basis. But earnings per share of $1.50 missed analyst forecasts of $1.77—a 15.25% shortfall that sent shares down 2% in after-hours trading.

Behind the headlines, a transformation was underway. The "Transform for the Future" initiative, announced earlier in 2025, targeted $500 million in cost savings through operational improvements and portfolio optimization. This wasn't typical corporate cost-cutting—it was systematic reimagination of how Solventum operated.

The vitality index, measuring revenue from products launched in recent years, had nearly doubled since independence. New product launches accelerated across all segments: innovative wound dressings in MedSurg, next-generation dental composites, AI-powered coding solutions in HIS. The innovation pipeline that had been constrained within 3M was now unleashed.

Segment performance told divergent stories. MedSurg continued steady growth driven by wound care innovation and surgical solutions. Dental Solutions gained momentum through focused portfolio management and improved service levels. HIS benefited from healthcare's digital transformation, with hospitals desperately needing efficiency tools amid staffing shortages.

Manufacturing optimization progressed rapidly. The company consolidated from 29 facilities at separation to 21 by November 2025, while actually improving product availability. Supply chain simplification reduced complexity and cost while enhancing reliability—critical for hospital customers who couldn't afford stockouts.

Most significantly, the September 2025 P&F divestiture generated $3.4 billion in net proceeds used primarily to pay down debt, achieving $2.7 billion in total debt reduction. This dramatic deleveraging transformed Solventum's financial flexibility, positioning the company for its next phase: growth through innovation and strategic acquisitions.

X. Playbook: Key Business Lessons

The Solventum story offers a masterclass in corporate transformation, with lessons extending far beyond healthcare. First, timing the spinoff proved crucial—waiting until after the Acelity integration but before legal liabilities overwhelmed the parent. Too early, and Solventum would have lacked scale; too late, and it might have been dragged down by 3M's challenges.

Leadership composition emerged as perhaps the most critical factor. Hanson's decision to recruit executives with spinoff experience—particularly from Covidien/Medtronic—created a management team that understood both the operational complexities and emotional challenges of separation. They had lived through similar transitions and knew which battles to fight and which to defer.

Portfolio optimization couldn't wait for perfect conditions. The P&F divestiture, executed while still separating from 3M, demonstrated that new companies can't afford to be passive. Despite operational strain, Solventum chose to reshape its portfolio immediately rather than wait for stability that might never come.

The balance between continuity and change proved delicate. Solventum needed to maintain customer relationships and product quality during massive operational changes. The company achieved this through phased transitions—keeping some 3M systems temporarily while building new capabilities, ensuring no disruption to customer service.

Debt management dominated early strategy, but not at the expense of innovation. While aggressively paying down debt, Solventum actually increased R&D intensity, recognizing that falling behind technologically would be fatal in competitive medical device markets. The company learned to be disciplined but not austere.

Building corporate identity from conglomerate heritage required deliberate culture work. Solventum couldn't simply be "former 3M Healthcare"—it needed its own mission, values, and employee value proposition. The company invested heavily in internal communications and culture-building, recognizing that employee engagement would determine success.

Perhaps most importantly, Solventum demonstrated that focus beats diversification in modern healthcare. By shedding P&F and concentrating on core medical devices and healthcare IT, the company could allocate resources more effectively and respond more quickly to market changes. The era of healthcare conglomerates was ending; the age of specialized innovators had begun.

XI. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's 5 Forces:

Supplier Power: Moderate - Solventum sources raw materials from diverse suppliers, limiting individual bargaining power. However, specialized components for medical devices and stringent quality requirements give certain suppliers leverage. The company's scale provides negotiating power, but switching costs for validated medical-grade materials remain significant.

Buyer Power: High - Hospital systems have consolidated dramatically, with group purchasing organizations (GPOs) controlling vast purchasing decisions. These buyers demand continuous price concessions, value-based contracts, and bundled solutions. Solventum's broad portfolio provides some negotiating leverage, but pricing pressure remains intense, particularly for commodity products.

Threat of Substitutes: Moderate - While surgical supplies and wound care have limited direct substitutes, alternative treatment modalities constantly emerge. Digital health solutions threaten traditional products, and minimally invasive procedures reduce demand for certain surgical supplies. Innovation remains critical to staying ahead of substitution threats.

New Entrants: Low - Regulatory barriers create formidable entry obstacles. FDA approval processes, clinical trial requirements, and quality system regulations require years and millions in investment. Established customer relationships and hospital formulary positions further protect incumbents. However, digital health segments face lower barriers.

Competitive Rivalry: High - Solventum competes against both diversified giants like Johnson & Johnson and specialized players in each segment. Price competition is fierce in mature categories, while innovation races characterize growth segments. Market share battles intensify as organic growth slows industry-wide.

Hamilton's 7 Powers:

Scale Economies: Present - Manufacturing scale drives unit cost advantages, particularly in high-volume products like surgical drapes and wound dressings. Shared R&D platforms across product lines amplify innovation ROI. Global distribution infrastructure spreads fixed costs across geographies.

Network Effects: Limited - HIS software creates modest network effects as more hospitals adopt standardized coding practices. However, most medical device segments lack true network dynamics. Clinician training and familiarity create some switching costs but not classical network effects.

Counter-positioning: Not Primary - Solventum largely competes with traditional business models rather than disrupting them. The company emphasizes superior execution and innovation within established categories rather than fundamentally different approaches.

Switching Costs: High in HIS, Moderate in Devices - Hospital IT systems create significant switching costs through integration complexity, staff training, and workflow disruption. Medical devices have moderate switching costs from clinician familiarity and supply chain integration, though less than software.

Branding: Strong Heritage - Seven decades of 3M healthcare innovation created trusted brands like Littmann stethoscopes. However, building independent Solventum brand awareness remains a work in progress. Professional healthcare buyers focus more on clinical evidence than consumer-style branding.

Cornered Resource: Significant - Patents protect key innovations, particularly in advanced wound care and dental materials. Regulatory approvals and clinical data represent irreplaceable assets. The company's 70-year knowledge base in medical-grade adhesives and materials science is difficult to replicate.

Process Power: Substantial - Decades of experience have created sophisticated manufacturing processes, quality systems, and regulatory expertise. The ability to consistently produce medical-grade products at scale while maintaining quality represents embedded organizational knowledge that new entrants struggle to match.

XII. Bear vs. Bull Case

Bear Case:

The debt burden looms large despite recent reductions. Even after the P&F divestiture, Solventum carries significant leverage that constrains financial flexibility. Interest expense consumes cash that could fund R&D or acquisitions, potentially causing the company to fall behind in innovation races.

Growth remains uninspiring. Organic revenue growth of just 2-3% barely outpaces inflation, suggesting limited pricing power or volume growth. The company's mature markets face structural headwinds from hospital budget constraints and procedure volume pressures. Historical performance offers little encouragement—revenue was essentially flat from 2021-2023 during 3M ownership.

Commoditization threatens margins across multiple segments. Basic wound care, surgical supplies, and dental materials increasingly compete on price rather than differentiation. GPOs continuously pressure pricing, while private-label competitors chip away at market share in commodity categories.

Operational complexity persists despite separation progress. Remaining entanglements with 3M through transition service agreements create execution risk. Building standalone capabilities while maintaining business performance stretches management attention and resources thin.

Competition intensifies from every direction. Large diversified players leverage portfolio breadth for bundled contracts. Specialized competitors out-innovate in narrow segments. Digital health startups threaten traditional products with software solutions. Chinese manufacturers increasingly compete on price in international markets.

Bull Case:

Pure-play focus unlocks value that was hidden within 3M's conglomerate structure. Independent Solventum can allocate resources optimally, pursue targeted M&A, and respond quickly to market opportunities without competing for attention against industrial businesses.

Market positions remain strong despite competitive pressures. Leading shares in advanced wound care, dental restoratives, and hospital coding software provide defensive moats. These positions generate steady cash flow to fund growth initiatives and debt reduction.

The $93 billion addressable market continues expanding at 4-6% annually, driven by aging populations, rising chronic disease prevalence, and emerging market healthcare development. Even maintaining share in growing markets drives organic revenue growth.

Transformation initiatives show early traction. Nearly doubled vitality index demonstrates innovation acceleration. Cost savings on track to deliver $500 million benefit. Debt reduction ahead of schedule, creating flexibility for growth investments and acquisitions.

Management team expertise in healthcare transformations reduces execution risk. Leadership's experience navigating similar situations at Covidien and Medtronic provides playbook for value creation. Early wins in operations and portfolio management build confidence in long-term execution.

Strategic flexibility improves dramatically post-deleveraging. Reduced debt service frees cash for R&D and tuck-in acquisitions. Clean balance sheet enables larger transformational deals when opportunities arise. Financial flexibility allows countercyclical investments during downturns.

XIII. Looking Forward: The Next Chapter

The path forward centers on three phases of transformation. Phase one—stabilization and deleveraging—nears completion with the P&F sale. Phase two—operational optimization and organic growth acceleration—is underway through the Transform for the Future initiative. Phase three—value creation through innovation and M&A—awaits in 2026 and beyond.

Debt reduction remains paramount near-term, with management targeting investment-grade metrics by year-end 2026. This financial flexibility will unlock strategic options currently constrained by leverage. Once achieved, capital allocation can shift toward growth investments rather than debt service.

M&A opportunities will multiply as the balance sheet strengthens. Tuck-in acquisitions in wound care, dental, and healthcare IT can accelerate growth and expand margins. Management has signaled discipline—no transformational deals until organic growth stabilizes and integration capabilities mature.

Innovation priorities focus on convergence opportunities at the intersection of devices, materials, and software. AI-powered surgical planning tools, smart wound dressings with embedded sensors, and predictive analytics for hospital operations represent next-generation solutions that leverage Solventum's unique capabilities.

Geographic expansion, particularly in Asia-Pacific and Latin America, offers significant growth potential. Rising middle classes, expanding healthcare access, and increasing surgical volumes in emerging markets provide long-term tailwinds. Localization strategies will be crucial to compete against regional players.

Digital transformation accelerates across all segments. Connected devices, cloud analytics, and AI-driven insights transform traditional products into comprehensive solutions. The HIS segment leads this transition, but opportunities exist across the portfolio to embed intelligence into physical products.

Competition will intensify as industry consolidation continues. Solventum must maintain innovation momentum while defending market share against larger rivals and disrupting startups. Success requires balancing efficiency with investment, focus with flexibility.

XIV. Epilogue & Key Takeaways

Solventum's journey from captive division to independent company illuminates broader themes reshaping industrial America. The age of conglomerates, built on portfolio theory and financial engineering, yields to an era demanding focus, agility, and specialization. What worked for 3M in the 20th century—diversification across unrelated businesses—became a liability in capital markets that value pure plays.

The spinoff represents both liberation and burden. Freedom from 3M's legal liabilities and capital allocation constraints enables strategic focus, but independence brings new challenges. Solventum must build capabilities that 3M provided while simultaneously transforming its business model. It's akin to rebuilding a plane while flying it.

For healthcare industry consolidation, Solventum offers a contrarian example. While medtech giants grow through mega-mergers, Solventum demonstrates that focus and execution can compete against scale. The company's success or failure will influence how other conglomerates approach healthcare assets.

Three critical metrics will determine Solventum's trajectory. First, organic revenue growth must accelerate beyond the current 2-3% to justify premium valuations. Second, EBITDA margins need expansion through mix improvement and operational efficiency. Third, return on invested capital must exceed the cost of capital consistently—the ultimate measure of value creation.

The lessons extend beyond Solventum. Corporate transformations require more than financial engineering; they demand operational excellence, cultural change, and strategic clarity. Leadership matters enormously—experience navigating similar transitions provides invaluable pattern recognition. Timing is everything—acting too early or too late can doom even well-conceived strategies.

For investors, Solventum presents a classic special situation. The company trades at a discount to pure-play medtech peers, offering potential multiple expansion as execution improves. Yet significant risks remain from leverage, competition, and execution complexity. Success requires patience—transformations take years, not quarters.

The next 18-24 months will prove pivotal. Can Solventum accelerate organic growth while maintaining margins? Will management deploy capital wisely as debt constraints ease? Can the company build an independent identity that attracts talent and customers? These questions will determine whether Solventum becomes a successful standalone company or merely a way station to eventual consolidation.

What's certain is that Solventum's story has only just begun. Born from one of America's most iconic companies, carrying decades of innovation heritage but also significant debt, the company stands at an inflection point. The transformation from 3M Healthcare to Solventum Corporation represents more than a name change—it's a bet that focused expertise beats diversified scale in modern healthcare. Time will tell if that bet pays off.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube