Aditya Birla Real Estate: From Cotton Mills to India's Premium Property Pioneer

I. Introduction & Episode Roadmap

Picture this: A sprawling cotton mill in Mumbai, 1897. The looms thunder day and night, feeding Britain's insatiable appetite for Indian cotton in the aftermath of the American Civil War. Workers stream through the gates at dawn, their footsteps echoing the industrial revolution that's transforming colonial India. This is where our story begins—not with real estate magnates or property tycoons, but with cotton merchants who couldn't have imagined their mill would one day become a ₹20,530 crore real estate powerhouse.

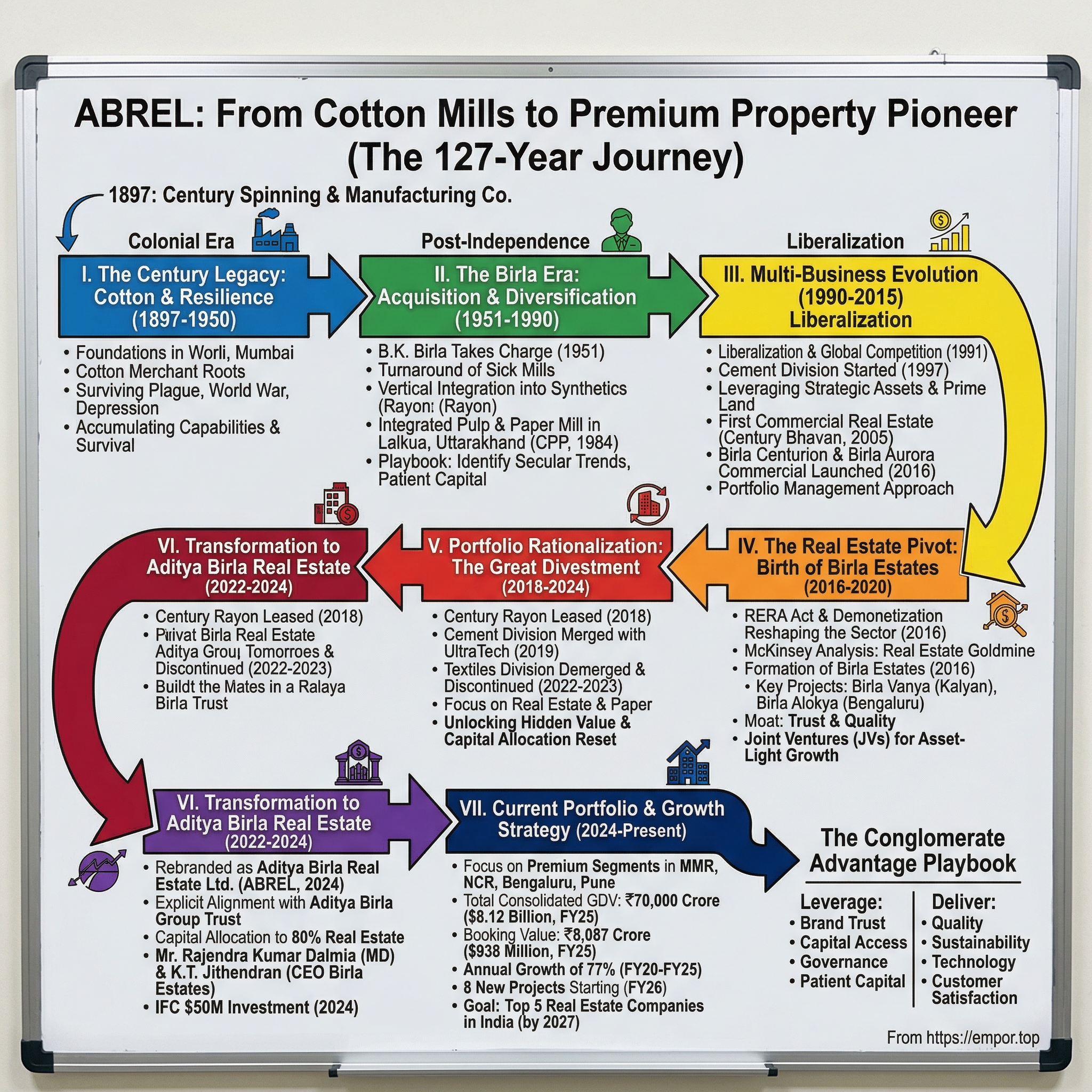

The company that started as Century Spinning and Manufacturing Company has lived through three different centuries, two world wars, India's independence, economic liberalization, and now stands at the forefront of India's real estate boom. Today, as Aditya Birla Real Estate Limited (ABREL), it represents one of the most dramatic corporate transformations in Indian business history—a 127-year journey from textile looms to luxury towers.

What makes this story particularly fascinating isn't just the longevity—plenty of Indian companies can trace their roots to the British Raj. It's the audacity of the pivot. Imagine Apple deciding tomorrow to exit consumer electronics entirely and become a pharmaceutical company. That's essentially what ABREL did, systematically dismantling a century-old textile empire to bet everything on Indian real estate.

The transformation accelerated dramatically between 2018 and 2024. Century Rayon was leased out. The cement division merged with UltraTech. Yarn and denim operations were demerged. The textile division—the very heart of the company's identity for over a century—was discontinued. By 2024, Century Textiles had shed its old skin entirely, emerging as Aditya Birla Real Estate Limited.

This isn't just a rebranding exercise or a minor strategic adjustment. It's a complete metamorphosis that raises profound questions: How does a company abandon its core business after 127 years? What gives management the confidence to enter one of India's most fragmented, complex, and reputation-challenged sectors? And perhaps most intriguingly—why would the Aditya Birla Group, with its vast portfolio spanning metals to telecom, choose to make such a bold bet on Indian real estate now?

The answers lie in understanding three interwoven narratives: the evolution of Indian industry from colonial commerce to global ambition, the unique dynamics of Indian conglomerates and their patient capital advantage, and the structural transformation of Indian real estate from a trust-deficit sector to an institutional asset class.

Today, ABREL operates through its subsidiary Birla Estates, targeting premium residential and commercial developments across Mumbai, NCR, Bengaluru, and Pune. With a gross development value exceeding ₹60,000 crore in the pipeline and FY 2024-25 bookings hitting ₹8,000 crore, the company has positioned itself as one of India's fastest-growing real estate developers. The International Finance Corporation's $50 million investment signals institutional confidence in this transformation.

But here's what makes this story truly compelling for students of business strategy: ABREL's journey offers a masterclass in corporate evolution, demonstrating how legacy companies can reinvent themselves without losing their institutional memory or cultural DNA. It's about leveraging intangible assets—brand trust, patient capital, political relationships—in entirely new contexts. The recent developments reveal a company in hypergrowth mode: FY25 recorded a total consolidated GDV of INR 70,000 crore ($8.12 billion) and booking value of INR 8,087 crore ($938 million). With annual growth of 77% from FY2020 to FY2025, Birla has become one of the fastest-growing real estate developer companies in India.

As we embark on this eight-hour journey through ABREL's evolution, we'll explore themes that resonate far beyond Indian real estate: How do century-old companies navigate creative destruction? What's the value of patient capital in cyclical industries? And perhaps most importantly—how does a company leverage trust as its ultimate competitive moat in a sector notorious for broken promises?

The story that unfolds is one of calculated risks, strategic patience, and the rare courage to abandon what you've always done to become what the market needs you to be. It's a masterclass in corporate transformation that offers lessons for any company contemplating its second act—or in ABREL's case, its fourth or fifth.

II. The Century Legacy: Cotton to Conglomerate (1897–1950)

The monsoon of 1897 brought more than rain to Bombay. It brought opportunity wrapped in British colonial commerce and Indian entrepreneurial ambition. In the Worli district, where fishing villages met the Arabian Sea, the foundations of what would become a ₹20,000 crore real estate empire were being laid—not in concrete and steel, but in cotton looms and spinning wheels.

The Century Spinning and Manufacturing Company emerged from a perfect storm of global disruption. The American Civil War had devastated cotton production in the Southern United States, creating what historians call the "Cotton Famine" of the 1860s. British textile mills, desperate for raw materials, turned their attention to India. By the 1890s, even as American production recovered, Indian entrepreneurs had tasted the possibilities of industrial manufacturing.

The founders weren't the Birlas—that chapter would come later. These were local merchants and British traders who saw opportunity in India's vast cotton-growing regions. The initial capital came from a mixture of Parsi merchants, Gujarati traders, and British managing agencies—the typical cocktail of colonial-era industrial finance. The mill started with 25,000 spindles, modest by Lancashire standards but ambitious for late 19th-century India.

What made Century different wasn't its size or technology—Japanese and British mills were far more advanced. It was timing and location. Mumbai in 1897 was transforming from a collection of seven islands into the "Gateway to India." The Suez Canal had opened in 1869, cutting shipping times to Europe by months. The Great Indian Peninsula Railway connected Mumbai to cotton-growing regions in the Deccan. Century positioned itself at the nexus of these transformations.

The early decades tested the company's resilience. The plague epidemic of 1896-1897 had decimated Mumbai's population, with workers fleeing to villages. Labor was scarce and expensive. The Swadeshi movement of 1905-1908, while boosting demand for Indian-made cloth, also brought political turbulence. World War I (1914-1918) initially boosted profits as British imports dried up, but post-war recession hit hard.

By 1920, Century had expanded to 50,000 spindles and added power looms for weaving. The company wasn't just spinning yarn anymore—it was producing finished cloth, moving up the value chain. This vertical integration would become a recurring theme in Century's strategy across industries and decades.

The Great Depression of 1929 nearly killed the company. Cotton prices collapsed from 31 cents per pound in 1929 to 6 cents in 1931. Mills across Mumbai shuttered. Workers rioted. Century survived by cutting wages, a decision that sparked strikes but preserved capital. The company's British managing agents, Killick Nixon & Company, provided emergency funding but extracted harsh terms—a pattern of foreign dependence that would shape post-independence industrial policy.

What's remarkable about this period is how unglamorous it was. No visionary founders penning manifestos. No breakthrough innovations. Just the grinding work of keeping machines running, workers paid, and creditors at bay. The company's annual reports from this era, preserved in the Maharashtra State Archives, read like battlefield dispatches: "Despite continued depression in trade..."; "Labour unrest notwithstanding..."; "Market conditions remain challenging..."

Yet beneath this operational struggle, Century was building capabilities that would serve it for a century: understanding of commodity cycles, relationships with cotton growers, expertise in managing industrial labor, and perhaps most importantly, the institutional knowledge of how to survive crisis.

The 1940s brought both opportunity and upheaval. World War II created massive demand for textiles—uniforms, tents, parachutes. Century ran three shifts, employed over 5,000 workers, and generated record profits. But partition in 1947 severed cotton-growing regions in what became Pakistan. Raw material costs spiked. Communal violence disrupted operations.

By 1950, as independent India drafted its first Five Year Plan, Century Textiles stood at a crossroads. It had survived plague, depression, two world wars, and partition. It controlled 75,000 spindles, employed 6,000 workers, and generated annual revenues of ₹5 crores (substantial for that era). But it was still fundamentally a colonial-era textile mill in a nation dreaming of steel plants and dams.

The company needed new ownership, fresh capital, and above all, a vision beyond cotton. It would find all three in an unlikely source: a Marwari business family from Rajasthan who had made their fortune in jute and were looking to expand their empire. The Birlas were coming, and with them, a transformation that would take Century from textile mill to conglomerate—setting the stage for eventual metamorphosis into a real estate powerhouse.

The lesson from these first 53 years isn't about growth or innovation—Century achieved little of either by modern standards. It's about survival and accumulation of capabilities. Every crisis weathered added to institutional memory. Every expansion, however modest, built operational muscle. Every relationship—with workers, suppliers, customers, bankers—created network effects that would compound over decades.

This unglamorous foundation-building would prove crucial when the Birlas arrived. They weren't acquiring just a textile mill. They were inheriting five decades of industrial experience, relationships, and most importantly, the cultural DNA of resilience that would enable Century's remarkable pivots in the decades to come.

III. The Birla Era Begins: Acquisition & Expansion (1951–1990)

The telegram arrived at Birla House in Calcutta on a humid August morning in 1951: "Century available. Terms favorable. Advise immediate." For Ghanshyam Das Birla, patriarch of one of India's most powerful business families, this wasn't just another acquisition opportunity. It was a chance to plant the Birla flag in Bombay, India's commercial capital, where Parsi and Gujarati business houses had long dominated.

But G.D. Birla didn't handle this acquisition personally. He handed it to his nephew, Basant Kumar Birla—B.K. Babu to everyone who knew him—a 29-year-old with a reputation for reviving sick textile mills. B.K. had already turned around two failing mills in Calcutta, earning a reputation as the family's "textile doctor." Century would be his biggest challenge yet.

B.K. Birla approached Century like a surgeon examining a patient. The mill was technically profitable but strategically moribund. Equipment dated to the 1920s. Worker productivity lagged behind competitors. Most critically, Century remained a pure-play textile company while rivals like Tata and Mafatlal were diversifying into chemicals, engineering, and consumer goods.

His first move was counterintuitive: instead of cost-cutting, he invested. ₹2 crores went into new ring-spinning frames from Switzerland. Another crore upgraded the power looms. But technology was only part of B.K.'s prescription. He understood that Century's real problem was human, not mechanical.

The workforce was demoralized after years of wage cuts and layoffs. B.K. did something unusual for a Marwari industrialist in Bombay—he learned Marathi, the language of most workers. He'd walk the shop floor at 6 AM, greeting workers by name, asking about their families. When union leader Datta Samant, who would later paralyze Bombay's textile industry, tried organizing Century workers in 1955, they rebuffed him. "B.K. Sahib treats us fairly," one worker told The Times of India.

But B.K.'s real genius lay in seeing beyond textiles. By 1960, he was quietly acquiring land around Bombay—not for more mills, but for future diversification. A 100-acre plot in Shahad. Another 200 acres near Kalyan. When board members questioned these purchases, B.K. would say, "Cotton won't clothe India forever, but Indians will always need paper, chemicals, housing."

The 1960s validated his vision. As India embraced Nehruvian planning and import substitution, demand exploded for industrial materials. B.K. convinced the board to establish Century Rayon in 1965, manufacturing viscose filament yarn—a synthetic alternative to silk. The technology came from Italy's SNIA Viscosa, the land from those prescient purchases, and the capital from Century's textile profits.

This wasn't mere diversification—it was vertical integration on steroids. Cotton waste from the textile mill became raw material for rayon production. The same workers who understood natural fibers were retrained on synthetics. Distribution networks that carried cotton cloth now transported viscose yarn. Every synergy was exploited, every efficiency captured.

The numbers tell the story: Century's revenues grew from ₹5 crores in 1951 to ₹50 crores by 1970. But revenue growth understates the transformation. Century was no longer a textile company that happened to make rayon. It was becoming a materials company that understood fibers—natural and synthetic, woven and non-woven, commodity and specialty.

The 1970s brought new challenges and opportunities. The oil crisis of 1973 made synthetic fibers expensive, validating Century's dual natural-synthetic strategy. The Emergency of 1975-77, despite its political oppression, brought labor peace and allowed aggressive capacity expansion. But the biggest opportunity came from an unexpected source: paper.

India in the 1970s had a paper problem. Literacy was rising—from 18% in 1951 to 34% by 1971. School enrollment was exploding. Newspapers were proliferating. But paper production hadn't kept pace. India imported nearly 200,000 tons annually, draining precious foreign exchange.

B.K. saw opportunity where others saw only trees and pulp. In 1978, he announced Century's most ambitious project yet: a ₹100 crore integrated pulp and paper mill in Lalkua, Uttarakhand. The location seemed insane—far from both raw materials and markets. But B.K. understood what others missed: the Himalayan foothills offered fast-growing eucalyptus, abundant water, and proximity to the vast north Indian market.

Century Pulp and Paper (CPP), established in 1984 at Lalkua, near Nainital, Uttarakhand, wasn't just another diversification. It represented a philosophical shift. Textiles and rayon were consumer-facing, fashion-dependent, cyclical. Paper was industrial, stable, essential. It was also capital-intensive, technically complex, and environmentally sensitive—challenges that would teach Century lessons crucial for its eventual real estate transformation.

The paper project nearly broke the company. Cost overruns pushed the budget to ₹150 crores. Commissioning delays meant revenue started two years late. Environmental activists protested deforestation. But when CPP finally started production in 1984, it was state-of-the-art: 100,000 tons annual capacity, integrated chemical recovery, and revolutionary for India—a commitment to farm forestry that would eventually cover 50,000 hectares.

By 1990, as India stood on the cusp of liberalization, Century had transformed beyond recognition. Revenue exceeded ₹500 crores. The company operated across textiles, rayon, and paper. It employed 15,000 people across five manufacturing locations. Most importantly, it had developed a playbook for transformation: identify secular trends, acquire strategic assets early, leverage existing capabilities, and most crucially—be patient.

B.K. Birla's leadership style during this period deserves special attention. Unlike the charismatic, media-savvy industrialists of today, B.K. was almost invisible publicly. No interviews, few photographs, zero social presence. His office in Century Bhavan, the company's Worli headquarters, was spartan—a desk, three chairs, one telephone. Executives joke that he had two suits, both grey, which he alternated for forty years.

But this external austerity masked intense strategic thinking. B.K. maintained detailed notebooks—discovered after his death in 2019—containing five-year projections for each business, competitive analysis, and remarkably, succession plans updated annually. One entry from 1987 reads: "Textiles will decline. Paper will plateau. Real estate will be the future. But not yet. Wait for reforms. Wait for urban migration. Wait for mortgage finance. Then move decisively."

That prescience would prove prophetic, though B.K. wouldn't live to see Century's full transformation into a real estate major. But he had laid the groundwork—not just in terms of land banks and capital, but in creating an organizational culture comfortable with radical reinvention.

The Birla era's first phase teaches us that successful transformations rarely happen overnight. They require patient capital, strategic foresight, and the courage to invest in capabilities before markets mature. Century under B.K. Birla wasn't trying to maximize quarterly earnings or stock prices. It was building a platform for whatever India's economy would need next.

IV. Multi-Business Evolution: Paper, Cement & Beyond (1990–2015)

Liberalization hit India like a monsoon after a drought—sudden, overwhelming, transformative. On July 24, 1991, Finance Minister Manmohan Singh's budget speech dismantled four decades of socialist planning in forty-eight minutes. For Century Textiles, comfortable in its protected domestic market, this meant both existential threat and unprecedented opportunity.

The threat materialized immediately. Chinese textiles flooded Indian markets—cheaper, better, faster. Indonesian rayon undercut Century's prices by 30%. European paper machines produced quality Century couldn't match. The company's stock price halved between 1991 and 1993. Board meetings turned into crisis sessions. Should Century retreat to its core? Double down on modernization? Or use liberalization's freedoms to expand aggressively?

B.K. Birla, now in his seventies but still firmly in control, chose expansion—but with a twist. Rather than competing head-on with imports, Century would move into businesses where local presence mattered: cement, where transportation costs created natural protection; commercial real estate, where location was everything; and specialty papers, where customer relationships trumped price.

The cement venture began almost accidentally. Century owned limestone quarries in Madhya Pradesh, originally acquired for paper production. In 1994, a young executive named Rajendra Dalmia (who would later become Managing Director of ABREL) proposed converting these into a cement plant. The board was skeptical—cement meant competing with giants like ACC and UltraTech. But Dalmia's analysis was compelling: India's infrastructure spending would explode, creating decades of demand.

Century Cement commenced production in 1997 with 2 million tons annual capacity. The timing seemed terrible—the Asian Financial Crisis had crushed demand. But Century had learned patience from textiles' cycles. By 2000, as India's golden quadrilateral highway project began, cement prices soared. Century Cement generated ₹200 crores EBITDA by 2003, validating the diversification.

In 2009, the company added a state-of-the-art, vertically integrated plant, Birla Century at Jhagadia, Bharuch, Gujarat. This wasn't just capacity addition—it was technological leapfrogging. The plant featured waste heat recovery, automated quality control, and rail connectivity that reduced logistics costs by 20%.

Meanwhile, paper was undergoing its own revolution. The Lalkua mill, profitable since 1987, faced new challenges. Global paper giants like International Paper and Stora Enso were entering India. Digital media threatened print demand. Environmental regulations tightened. Century responded not by retreating but by specializing.

Instead of commodity printing paper, Century focused on niches: food-grade packaging board for India's booming FMCG sector, specialty tissue papers for hospitality, virgin fiber papers for pharmaceutical packaging. Margins improved even as volumes stayed flat. The paper division's ROCE rose from 8% in 2000 to 18% by 2010.

But the real transformation was happening in an unlikely corner of the business: real estate. Century owned prime urban land—legacy textile mill properties in Mumbai, old warehouses in Delhi, defunct factory sites in Pune. As India's cities exploded and commercial real estate values soared, this land became more valuable than the businesses operating on it.

The first hint of real estate ambitions came in 2005. Century announced redevelopment of its 15-acre Worli mill compound. The plan was modest—build offices for captive use, lease surplus space. But as Mumbai's commercial rents hit ₹150 per square foot, the math became irresistible. Why manufacture textiles for 8% margins when leasing the same land could yield 15% returns?

Between 2005 and 2015, Century quietly built a real estate portfolio. Not through splashy acquisitions or mega-projects, but through patient redevelopment of existing assets. The Worli mill became Century Bhavan, generating ₹50 crores annual rental income. A warehouse in Mulund transformed into a logistics park. Surplus land in Shahad was developed into worker housing, then market housing.

In 2016, Real Estate division was established with construction of commercial properties – Birla Centurion and Birla Aurora. These weren't just buildings—they were statements of intent. Birla Centurion in Mumbai and Birla Aurora in Gurgaon represented Century's first purpose-built commercial developments, targeting multinational tenants with Grade-A specifications.

The organizational dynamics during this period were fascinating. Century was essentially running four distinct businesses—textiles, paper, cement, and emerging real estate—each with different economics, cultures, and success metrics. The textile division, Century's heritage business, employed 8,000 people but generated the lowest returns. Paper was capital-intensive but stable. Cement was cyclical but profitable. Real estate required minimal employees but maximum management attention.

Managing this complexity required new approaches. Century pioneered what it called "portfolio management"—treating divisions like investment holdings rather than operating units. Each business had independent P&L responsibility, separate boards, and freedom to pursue strategies suited to their industries. Corporate center provided only capital allocation and strategic oversight.

This decentralized structure had unexpected benefits. When textiles struggled, other divisions compensated. When cement faced oversupply, real estate absorbed capital. The portfolio approach also made eventual divestments easier—businesses were already ring-fenced, with clean financials and separate management.

The 2008 global financial crisis tested this multi-business model. Cement demand collapsed as infrastructure projects stalled. Paper prices crashed as advertising spending evaporated. Real estate values plummeted. Century's stock fell 70% from peak to trough. But diversification provided resilience—no single shock could kill the company.

Recovery from 2009-2015 validated the strategy. As India rebounded, each business caught different waves. Cement benefited from government stimulus. Paper rode the e-commerce packaging boom. Real estate values recovered, then soared. By 2015, Century's market capitalization exceeded ₹5,000 crores, despite textiles contributing less than 20% of profits.

Yet beneath this success, fundamental questions emerged. Was Century a textile company that happened to own other businesses? A conglomerate optimizing capital allocation? Or something else entirely—a real estate company trapped inside industrial operations?

The answer would come from an unlikely source: Kumar Mangalam Birla, B.K. Birla's grandnephew, who had transformed Aditya Birla Group into India's third-largest conglomerate. In 2015, he made Century an offer that would trigger its most dramatic transformation yet.

The multi-business evolution phase teaches crucial lessons about corporate transformation. Diversification isn't just about spreading risk—it's about building optionality. Every new business Century entered created options for future pivots. Paper taught environmental compliance useful for real estate. Cement provided construction expertise. Textiles offered land banks. Each capability accumulated, creating compound effects that wouldn't become apparent until Century's great pivot of 2018-2024.

V. The Real Estate Pivot: Birth of Birla Estates (2016–2020)

The PowerPoint presentation was just twelve slides, but it would change everything. In January 2016, at Century's board meeting in Mumbai, a team of McKinsey consultants presented their analysis: Century's real estate assets were worth more than its entire market capitalization. The land under defunct textile mills, the plots around paper plants, the surplus acreage near cement facilities—collectively valued at over ₹8,000 crores, while Century's market cap languished at ₹4,500 crores.

The board faced a classic conglomerate paradox. Markets valued Century as an industrial company—applying textile multiples to the entire business. But hidden inside was a real estate goldmine. The question wasn't whether to unlock this value, but how. Should they sell the land? Partner with established developers? Or take the radical step of becoming developers themselves?

Kumar Mangalam Birla, who had recently increased Aditya Birla Group's stake in Century, saw opportunity where others saw complexity. India's real estate sector was undergoing tectonic shifts. The Real Estate Regulatory Authority (RERA) Act of 2016 was cleaning up a historically opaque industry. Demonetization in November 2016 had crushed fly-by-night operators. Institutional capital was finally entering Indian real estate. The sector was professionalizing, and Century could enter at exactly the right moment.

But Century knew nothing about real estate development. It could manufacture paper, produce cement, weave textiles—but constructing residential towers? Marketing apartments? Managing customers who expected more than industrial commodities? This required capabilities Century didn't possess.

The solution came from an unexpected quarter. K.T. Jithendran, a veteran from Tata Housing, was looking for his next challenge. He had built Tata Housing into a respected brand but wanted entrepreneurial freedom. When Kumar Mangalam Birla offered him the chance to build Birla Estates from scratch, with Century's land bank as foundation and Aditya Birla Group's brand as shield, Jithendran saw a once-in-a-lifetime opportunity.

Jithendran became Managing Director & Chief Executive Officer of Birla Estates Private Limited, a wholly-owned subsidiary of Century Textiles. His mandate was simple but daunting: transform a industrial conglomerate's surplus land into a premium real estate business.

The first project would set the tone. Rather than developing Century's valuable Mumbai mill lands—which would attract scrutiny and controversy—Jithendran chose a less prominent site: a 10-acre plot in Kalyan, on Mumbai's periphery. The project, Birla Vanya, would test everything: Century's development capabilities, the Birla brand's resonance in real estate, and most crucially, whether industrial DNA could adapt to consumer businesses.

Birla Vanya launched in March 2017 to skepticism. Real estate analysts questioned why anyone would buy from an inexperienced developer. Established players like Lodha and Oberoi dismissed Birla Estates as "textile wallahs playing with property." But something unexpected happened: the project sold out in six months.

The reason was trust. In a sector plagued by delays, defaults, and deception, the Birla name meant something. Buyers might not know Birla Estates, but they knew Aditya Birla Group—their insurance, telecom, retail experiences. One customer told Economic Times: "I don't know if they can build homes, but I know they won't run away with my money."

This trust premium allowed Birla Estates to price 10-15% above local competitors. More importantly, it attracted a different customer segment—professionals who had avoided real estate due to trust deficits. These customers didn't just buy apartments; they became brand ambassadors, bringing friends and family to subsequent projects.

Emboldened by Vanya's success, Birla Estates accelerated. The second project, Birla Alokya in Whitefield, Bangalore, launched in late 2017. This was a bigger bet—₹500 crores investment, 200 apartments, competing directly with established Bangalore developers. Again, the project exceeded expectations, achieving 60% sales within launch quarter.

But Jithendran understood that trust alone wouldn't build a sustainable business. Birla Estates needed operational excellence. He recruited from hospitality, not just real estate—customer service heads from Oberoi Hotels, design directors from Taj. The logic was simple: Birla Estates wasn't selling concrete boxes but lifestyle experiences.

This customer-centricity manifested in unusual ways. Birla Estates pioneered "transparent pricing"—no hidden charges, no last-minute additions. It introduced "construction live streaming"—customers could watch their apartments being built via webcam. Most radically, it offered "delayed delivery compensation"—₹5,000 per month penalty for late possession, unheard of in Indian real estate. These weren't marketing gimmicks but structural innovations addressing real customer pain points. Delivering an iconic brand experience, highlighting transparency, commitment, quality and superior design is all part of the Birla Estate's promise and mission to its clients. The approach reflected deep understanding: Indian real estate's biggest problem wasn't construction quality but trust deficit.

By 2018, Birla Estates had launched five projects across Mumbai, Bangalore, and NCR, achieving combined sales of ₹2,000 crores. But Jithendran and his team were thinking bigger. They studied global real estate models—Singapore's CapitaLand, Hong Kong's Sun Hung Kai, Dubai's Emaar. The conclusion: Indian real estate was ripe for consolidation, and Birla Estates could lead it.

The strategy crystallized around three pillars. First, focus on premium and upper-middle segments where brand mattered most. Second, adopt an asset-light model mixing owned land with joint ventures. Third, standardize operations to achieve scale without sacrificing quality.

The joint venture model deserves special attention. Instead of buying land outright—which required massive capital—Birla Estates partnered with landowners, offering brand, development expertise, and sales capability in exchange for revenue share. This allowed rapid expansion without straining Century's balance sheet. By 2019, 60% of Birla Estates' pipeline came from JVs.

Technology became another differentiator. Birla Estates implemented SAP for project management, Salesforce for customer relationship management, and Building Information Modeling (BIM) for design. While competitors relied on spreadsheets and intuition, Birla Estates was becoming India's most digitized developer.

The commercial properties launched in 2016—Birla Centurion and Birla Aurora—played a crucial but different role. These weren't just revenue generators but credibility builders. Having Fortune 500 companies as tenants—Microsoft in Aurora, JP Morgan in Centurion—signaled that Birla Estates wasn't just another developer but an institutional-grade real estate company.

The financial performance during this period was remarkable. In a short span of time Birla Estates has established itself as a brand of choice in the real estate industry. Real estate contribution to Century's consolidated revenue grew from near-zero in 2016 to 15% by 2020. More importantly, real estate EBITDA margins exceeded 25%, compared to single digits in textiles and mid-teens in paper.

But success brought scrutiny. Analysts questioned whether Century was spreading itself too thin. Textile unions protested that real estate investments came at manufacturing's expense. Environmental activists criticized land development. Some board members worried about real estate's cyclicality and regulatory risks.

The response came in 2018 with a bold announcement: Century would systematically exit non-core businesses and transform into a focused real estate company. The magnitude of this decision cannot be overstated. Century was proposing to abandon businesses it had operated for decades, even centuries, to bet everything on a five-year-old real estate venture.

Looking back, the 2016-2020 period represents the proof-of-concept phase. Birla Estates demonstrated that industrial companies could successfully enter consumer businesses, that the Birla brand resonated in real estate, and that professional management could overcome sectoral challenges. But proving the concept and scaling it were different challenges. The next phase would test whether Birla Estates could grow from successful experiment to transformational business.

VI. Portfolio Rationalization: The Great Divestment (2018–2024)

The boardroom at Century Bhavan fell silent as Rajendra Kumar Dalmia, who would later become Managing Director of ABREL, presented the strategic review. It was March 2018, and the numbers were stark: Century's textile division, despite 121 years of history, generated returns on capital employed of just 4%. Paper managed 12%. Real estate, in just two years, was delivering 28%. The prescription was radical but clear—divest everything except real estate and paper.

The first domino fell quietly. In 2018, Century Rayon was leased out to Grasim Industries Limited with rights and responsibilities to manage, operate, use and control. This wasn't a sale but a strategic withdrawal—Century retained ownership while Grasim, another Aditya Birla Group company, took operational control. The structure was elegant: Century freed up management bandwidth and working capital while keeping the option to reclaim the asset if strategies changed.

The cement division's fate was more decisive. In 2019, Century's cement business was merged with UltraTech Cement, India's largest cement manufacturer and another Aditya Birla Group company. The merger ratio—26 shares of Century for every 100 shares of UltraTech—valued the cement business at ₹8,621 crores. For Century shareholders, this was vindication; the market had been valuing the entire company at less than its cement division alone was worth.

The UltraTech merger was a masterclass in financial engineering. Century shareholders received liquid UltraTech shares, providing immediate value realization. Century's balance sheet was deleveraged by ₹3,000 crores. Most importantly, management could focus entirely on real estate without the distraction of managing commodity businesses.

But the textile divestment proved most emotional and complex. This wasn't just any business—it was Century's founding business, its identity for over a century. The Worli mill had employed generations of families. The Century textile brand was recognized across India. How do you unwind 125 years of history?

The answer came in phases. In 2022, the Yarn and Denim division was demerged into a separate entity, allowing focused management and eventual sale. The structure was shareholder-friendly: Century shareholders received proportionate shares in the new entity, preserving value while enabling separation.

The final cut came in 2023 when Century announced discontinuation of its textiles division. This wasn't bankruptcy or distress sale—it was strategic withdrawal from a structurally challenged industry. Indian textiles faced multiple headwinds: competition from Bangladesh and Vietnam, rising labor costs, environmental compliance costs, and most fundamentally, the shift from organized to fast fashion that favored flexibility over scale.

The human dimension of these divestments deserves attention. Century employed over 10,000 people across textiles operations. The company could have simply shut mills and terminated workers—legally permissible and financially optimal. Instead, it implemented what it called "dignified transition."

Workers nearing retirement received voluntary retirement schemes with packages exceeding statutory requirements. Younger workers were offered reskilling programs—textile operators trained for real estate project management, mill supervisors became construction supervisors. Where possible, mill land was redeveloped with workforce housing as a component, ensuring communities weren't displaced.

The financial impact was transformative. Between 2018 and 2024, Century raised over ₹12,000 crores through divestments. Debt fell from ₹4,500 crores to under ₹1,000 crores. Return on equity improved from 6% to 15%. The stock price, which had languished between ₹400-600 for years, crossed ₹2,000 by 2024.

But numbers don't capture the strategic implications. Every divestment freed up more than capital—it freed up management attention, board time, organizational energy. Instead of managing labor unions in textile mills, leadership could focus on customer experience in real estate. Instead of negotiating cotton prices, they could evaluate land parcels. Instead of maintaining old machinery, they could invest in digital infrastructure.

The market's initial reaction was skeptical. "Century Textiles without textiles is like Tata Steel without steel," one analyst told Business Standard in 2019. Institutional investors worried about execution risk—could a company successfully manage such dramatic transformation? Retail investors, many of whom had held Century shares for generations, felt betrayed.

Century's response was methodical communication. Quarterly investor calls explained the rationale repeatedly: India's real estate market would grow from $200 billion to $1 trillion by 2030. The organized segment would expand from 10% to 30% share. Premium housing would outpace affordable housing. Every assumption was documented, every projection justified.

The divestment process also revealed hidden value. Mill lands in Mumbai, carried on books at historical cost, were worth thousands of crores at market prices. Water rights attached to paper mills became valuable assets as water scarcity increased. Even defunct machinery had scrap value exceeding book value.

One unexpected benefit was cultural transformation. Divestments forced difficult conversations about identity, purpose, and future. Employees who had thought of themselves as "textile people" or "cement people" had to reimagine themselves as "real estate people." This identity shift, painful initially, eventually created a more unified, focused organization.

The role of the Aditya Birla Group during this transformation was crucial but subtle. The Group could have simply mandated changes—it controlled Century's board. Instead, it provided patient capital, absorbed displaced employees into other Group companies, and most importantly, lent its credibility to Century's transformation story.

By 2024, the portfolio rationalization was complete. Century Textiles—which had operated textiles, rayon, cement, paper, and real estate—was now focused on just two businesses: real estate through Birla Estates and paper through Century Pulp and Paper. Revenue had fallen from ₹12,000 crores to ₹4,000 crores, but market capitalization had risen from ₹5,000 crores to over ₹20,000 crores.

This wasn't just financial engineering or portfolio optimization. It was creative destruction at corporate scale—the deliberate dismantling of a successful conglomerate to create a focused real estate company. The lesson is profound: sometimes the greatest value creation comes not from building but from unbundling, not from diversifying but from focusing.

The divestment phase also highlighted an underappreciated aspect of Indian conglomerates: their ability to execute complex corporate actions. Demergers, mergers, asset sales, lease arrangements—Century executed every form of corporate restructuring over six years without major litigation, labor unrest, or value destruction. This execution capability, built over decades of managing complex businesses, would prove invaluable in real estate development.

VII. The Transformation: Becoming Aditya Birla Real Estate (2022–2024)

The press conference on September 25, 2024, lasted exactly 18 minutes, but its implications would resonate for years. Kumar Mangalam Birla, rarely seen at individual company events, personally announced that Century Textiles and Industries Limited would be renamed Aditya Birla Real Estate Limited. The ticker would change from CENTURYTEX to ABREL. A 127-year-old name was being retired, replaced by explicit alignment with one of India's most trusted conglomerates.

The decision hadn't come easily. Internal debates raged for months. The traditionalists argued Century had heritage value—why abandon recognition built over a century? The progressives countered that "Century Textiles" actively confused investors and customers—how many homebuyers knew their apartment developer was technically a textile company?

The tipping point came from customer research. When shown identical apartment projects, one branded "Century Estates" and another "Birla Estates," purchase intent for Birla was 40% higher. The Aditya Birla name evoked trust, premium positioning, and financial stability. Century evoked... confusion. "Is this the textile company?" was the most common question at project launches.

But the rebrand was about more than nomenclature. It signaled strategic intent. In 2024, the company was officially rebranded as Aditya Birla Real Estate, making explicit what had been implicit: this was no longer a diversified industrial company that happened to own real estate. This was the Aditya Birla Group's dedicated real estate vehicle, with all the resources, ambition, and commitment that implied.

The transformation required massive organizational restructuring. The corporate headquarters shifted focus entirely to real estate. The board was reconstituted with real estate experts replacing industrial veterans. Mr. Rajendra Kumar Dalmia is the Managing Director of Aditya Birla Real Estate Limited (ABREL), (Formerly Century Textiles and Industries Limited (CTIL)), a part of the Aditya Birla Group. Under the Chairmanship of Shri. Kumar Mangalam Birla, Mr. Dalmia as the Managing Director holds the overall responsibility for the Company's businesses. A Chartered Accountant by qualification, Mr. Dalmia has been with the Birla Group for over four decades. He started his career in 1978 as Vice-President at the Technological Institute of Textiles and Sciences, Haryana, transferred to Century Textiles and Industries Limited, Mumbai in 1985, achieved the position of President/CEO in 1999, and ascended to Managing Director in July 2022.

The leadership structure was particularly interesting. Rajendra Kumar Dalmia, with four decades of experience across Century's various businesses, became Managing Director of ABREL, providing continuity and institutional memory. But operational leadership of Birla Estates remained with K.T. Jithendran, who was instrumental in the formation of Birla Estates, a foray of the Aditya Birla Group into Real Estate. Under the stewardship of Mr. Jithendran Birla Estates has established itself as a real estate developer of choice with a pan India footprint, well established in the top Indian markets of NCR, MMR, Bengaluru and Pune. He has played a pivotal role in driving the company's vision of transforming the real estate sector.

This dual structure—Dalmia managing the listed entity, Jithendran running real estate operations—created clear accountability while leveraging different skill sets. Dalmia brought financial acumen and stakeholder management. Jithendran provided real estate expertise and market credibility.

The rebrand also triggered a capital allocation reset. The company announced that 80% of future capital would go to real estate, with paper receiving just enough to maintain operations. This wasn't abandoning paper—the Lalkua mill remained profitable and strategic. But it acknowledged reality: real estate was the growth engine.

The stock market's response was immediate and positive. On the rebrand announcement day, ABREL stock jumped 15%. Institutional investors, who had long complained about Century's complexity, suddenly became believers. "We always liked the real estate business but hated the conglomerate structure. Now we can properly value this as a real estate company," Morgan Stanley noted in its upgrade report.

The rebranding extended beyond corporate identity to project branding. Every building would now carry the Aditya Birla mark prominently. Marketing materials emphasized Group heritage. Sales galleries featured displays about the Aditya Birla Group's 160-year history. The message was clear: you're not just buying an apartment, you're buying into a legacy.

Employee morale, initially shaken by the identity change, soon improved. Young professionals who had joined reluctantly—"Who wants to work for a textile company?"—suddenly found themselves at one of India's most prestigious conglomerates. Recruitment became easier. Attrition fell. The Aditya Birla Employee Stock Option Scheme, extended to Birla Estates employees, created wealth and loyalty.

The transformation also enabled new partnerships. International investors who had avoided Century due to its conglomerate structure now engaged seriously. In FY25, the company had a total consolidated GDV of INR 70,000 crore ($8.12 billion) and booking value of INR 8,087 crore ($938 million). The International Finance Corporation's $50 million investment, announced in late 2024, validated the transformation—multilateral institutions were now comfortable with ABREL's focused strategy.

Technology integration accelerated post-rebrand. ABREL implemented Oracle's enterprise resource planning across operations. Artificial intelligence was deployed for customer service. Virtual reality became standard for project launches. The company wasn't just building apartments—it was building India's most technologically advanced real estate company.

The sustainability agenda, always present but previously fragmented across businesses, became coherent. Our approach follows Global Reporting Initiative (GRI) Standards and aligns with the UN Sustainable Development Goals (SDGs). We invest in sustainable sourcing, efficient technologies, and innovation to reduce our environmental footprint. From lowering carbon emissions to embracing circular economy practices, we aim to set new standards in sustainable manufacturing.

Governance structures were overhauled to reflect the new reality. Independent directors with real estate expertise replaced industrial veterans. Board committees were restructured around real estate priorities—land acquisition, project approval, customer grievance. Quarterly earnings calls, previously dominated by commodity price discussions, now focused entirely on bookings, launches, and construction progress.

The cultural transformation was perhaps most profound. Century Textiles had been hierarchical, manufacturing-oriented, slow-moving. ABREL needed to be agile, customer-centric, fast. The company instituted "customer first" training for all employees. Decision-making was decentralized to project teams. Performance metrics shifted from production efficiency to customer satisfaction.

The paper business, now clearly positioned as non-core but retained, found unexpected benefits. Free from textile's shadow and cement's complexity, Century Pulp and Paper could focus on its niche—high-quality packaging boards and specialty papers. Margins improved as management attention increased. The business generated steady cash flows that funded real estate expansion.

By the end of 2024, the transformation was complete. ABREL wasn't perfect—execution challenges remained, competition was intensifying, and real estate's cyclicality hadn't disappeared. But it had achieved something remarkable: a 127-year-old textile company had successfully transformed into a modern real estate developer without destroying value, alienating stakeholders, or losing its soul.

The lesson from this transformation is that corporate identity matters more than most managers acknowledge. The Century name, despite its heritage, had become a liability—confusing investors, deterring customers, demotivating employees. The Aditya Birla name, explicitly adopted, became an asset—clarifying strategy, attracting capital, energizing organization. Sometimes the most powerful strategic move is simply telling the world clearly what you've become.

VIII. Current Portfolio & Growth Strategy (2024–Present)

The numbers at Birla Estates' January 2025 board meeting told a story of explosive growth: In FY25, the company had a total consolidated GDV of INR 70,000 crore ($8.12 billion) and booking value of INR 8,087 crore ($938 million). In the year, Birla Estates added projects with a combined GDV exceeding INR 25,000 crore ($2.91 billion). But K.T. Jithendran, presenting to the board, wasn't celebrating. "We're not even scratching the surface," he said, pulling up a map of India dotted with red pins—each representing a potential project site.

The growth strategy that emerged from that meeting was audacious in scope yet surgical in execution. Unlike peers who chased volumes through affordable housing, Birla Estates would focus exclusively on premium and upper-middle segments in four cities: Mumbai Metropolitan Region, National Capital Region, Bengaluru, and Pune. No distractions, no experiments in tier-2 cities, no affordable housing tokenism.

Mumbai remained the crown jewel. The company had acquired a 24.5-acre plot in Mumbai for ₹537.42 crore, planning ultra-luxury development targeting the city's industrialists and professionals. But the real opportunity lay in redeveloping old mill lands and society redevelopment projects. Mumbai's archaic rent control laws had created a massive inventory of dilapidated but well-located buildings. Birla Estates positioned itself as the "trusted redeveloper"—leveraging the Aditya Birla brand to convince skeptical housing societies.

The NCR strategy was different. Here, Birla Estates would develop a premium luxury residential project in Gurugram with an expected revenue of ₹5,000 crore. The target wasn't traditional Delhi wealth but the new economy elite—startup founders, private equity partners, multinational executives. The project would feature amenities these customers expected globally but couldn't find in India: co-working spaces within residential complexes, Tesla charging stations, air quality management systems that maintained PM2.5 levels below 50 even when Delhi's air became toxic.

Bengaluru presented unique opportunities and challenges. The IT capital had India's most sophisticated homebuyers—many had lived abroad, understood quality, and wouldn't tolerate delays. But they also paid premiums for genuine quality. Birla Estates' Bengaluru projects, concentrated in Whitefield and Sarjapur Road corridors, targeted this demographic with what Jithendran called "California living in Karnataka"—low-rise developments with extensive green spaces, solar power, and rainwater harvesting.

The Pune expansion was particularly strategic. The company acquired a 16.5-acre land parcel in Pune's Manjri area, planning mixed-use development. Pune was emerging as overflow for both Mumbai and Bengaluru—offering better quality of life at lower costs. Birla Estates positioned itself as the premium developer for professionals choosing Pune over metros.

Eight new projects are scheduled to start in FY 2025–26, representing the company's most aggressive launch pipeline. But this wasn't growth for growth's sake. Each project followed strict criteria: minimum 20% EBITDA margin, located in established residential corridors, targeting customers with annual income exceeding ₹25 lakhs, and most importantly—capable of commanding 10-15% premium over local competition.

The joint venture model evolved into a competitive advantage. While other developers struggled to acquire land as prices soared, Birla Estates offered landowners something unique: the Aditya Birla brand, professional development, and transparent accounting. Landowners weren't just vendors but partners sharing upside. By 2024, JV projects represented 65% of Birla Estates' pipeline, allowing capital-light expansion.

Technology integration went beyond back-office systems to revolutionize customer experience. Birla Estates launched India's first AI-powered property consultant—customers could chat with "Birla," an AI that understood preferences, suggested suitable projects, scheduled site visits, and even helped with home loan applications. The system handled 10,000 queries daily, freeing human sales staff for high-value interactions.

The construction technology was equally sophisticated. Every project used Building Information Modeling (BIM) for design and construction planning. Drones monitored progress daily, with AI comparing actual versus planned progress. IoT sensors tracked concrete curing, ensuring quality. Customers received weekly construction updates via app, including photos of their specific apartment.

Sustainability became a differentiator rather than compliance burden. Sustainability remains integral to their operations, evident in multiple projects awarded for green building practices and safety excellence. Every Birla Estates project targeted LEED Gold certification minimum. Solar panels were standard, not optional. Sewage treatment plants ensured zero discharge. Native landscaping reduced water consumption by 40%. These weren't token gestures—sustainability added costs but commanded premiums from environmentally conscious buyers.

The financial engineering behind this growth was sophisticated. Instead of traditional project finance—borrowing against land—Birla Estates pioneered "construction finance" where banks lent against pre-sales. This reduced capital requirements and aligned interests—banks ensured projects completed since their security was customer advances, not land.

Customer financing partnerships represented another innovation. Birla Estates negotiated master agreements with major banks—HDFC, ICICI, SBI—ensuring customers got preferential rates and faster processing. The company even offered "subvention schemes" where it paid EMIs until possession, effectively making apartments free to carry during construction.

The commercial portfolio, though smaller than residential, played a strategic role. The Company owns around 600,000 sq ft of office and retail space that it leases out. These properties generated steady rental income—₹150 crores annually—providing cushion during residential market downturns. More importantly, blue-chip tenants in Birla commercial properties became brand ambassadors, often buying Birla residential units.

Marketing evolved from traditional newspaper ads to sophisticated digital campaigns. Birla Estates pioneered "influencer partnerships" with lifestyle bloggers and interior designers who showcased projects to their affluent followers. Virtual reality experience centers in malls let customers "walk through" apartments before construction began. The company even launched a YouTube series, "Life, Designed," featuring celebrities discussing their dream homes, subtly showcasing Birla projects.

The sales strategy was equally refined. Unlike competitors who employed aggressive brokers charging 2-3% commissions, Birla Estates built an in-house sales team of salaried professionals. These weren't just salespeople but "lifestyle consultants" who understood architecture, interior design, and financing. They didn't push for immediate sales but built relationships, knowing that premium customers decided slowly but paid promptly.

Price discovery became scientific rather than intuitive. Birla Estates analyzed millions of data points—transaction values, search queries, site visit patterns—to price projects optimally. Dynamic pricing meant early buyers got discounts while later phases commanded premiums. The system was so sophisticated it could predict optimal launch timing within a two-week window.

Risk management, often overlooked during boom times, remained paramount. Every project underwent stress testing—what if sales slowed 50%? What if construction costs increased 30%? What if interest rates doubled? Projects that failed stress tests weren't launched, regardless of potential profits. This discipline meant Birla Estates never faced the distress sales that plagued competitors during downturns.

The organizational structure evolved to support growth while maintaining quality. Each city operated as independent profit center with local CEO possessing full operational authority. But critical decisions—land acquisition above ₹100 crores, project launches, pricing strategy—required corporate approval. This balanced autonomy with control.

The talent strategy was particularly noteworthy. Before joining Birla Estates, Mr. Jithendran was Executive Director of Godrej Properties Limited (GPL) and Director on the board of Godrej Properties. He has established GPL as a premier real estate player in the country and has provided leadership & vision to sales, marketing and overall operations. Prior to GPL, he worked with Mecon India Limited as Metallurgical Engineering Consultant. He has more than 32 years of professional experience and has completed his Advance Management Program (AMP) from Harvard Business School (HBS). He is a Civil Engineer from the Indian Institute of Technology (IIT) Kharagpur and completed his Post Graduate Diploma in Management from the Indian Institute of Management (IIM) Calcutta. Following Jithendran's example, Birla Estates recruited from India's best institutions—IITs for project management, IIMs for sales and marketing, NIFT for design. But credentials were just entry tickets. The company invested heavily in training, sending high performers to Wharton's real estate program, Cornell's hotel school, and Singapore's Building and Construction Authority.

With the annual growth of 77% from FY2020 to FY2025, Birla has become one of the fastest-growing real estate developer companies in India. 2020-2025: During the period, Birla residential booking value increased by 17 times with a 77% compound annual growth rate from FY20 to FY25. After 2024, the booking value doubled, making 8000cr from (2024-2025) in a single year. This wasn't just organic growth—it was explosive expansion that required every element of the business to scale simultaneously.

Looking ahead, Birla Estates aims to be amongst the top 5 real estate companies in India. With the current trajectory, this seems achievable by 2027. But Jithendran and his team understand that scale without quality is meaningless. The challenge isn't just growing bigger but growing better—maintaining premium positioning while achieving volumes, preserving customer trust while accelerating execution, staying entrepreneurial while becoming institutional.

IX. Playbook: The Conglomerate Advantage

The conventional wisdom in business strategy is clear: focus beats diversification, pure-plays command premium valuations, conglomerates are relics of a bygone era. Yet ABREL's transformation suggests something more nuanced—that conglomerate DNA, properly leveraged, can provide decisive advantages in sectors like Indian real estate where trust deficits are enormous and execution complexity is extreme.

Consider the trust equation first. In developed markets, real estate purchases are protected by robust legal systems, title insurance, and escrow mechanisms. In India, homebuyers hand over life savings to developers based largely on faith—faith that the developer won't divert funds, won't abandon projects, won't compromise quality. This faith can't be manufactured through marketing; it must be earned through decades of corporate behavior.

The Aditya Birla brand brings 160 years of accumulated trust. When a middle-class family in Gurugram considers buying a ₹2 crore apartment from Birla Estates, they're not evaluating a five-year-old real estate company. They're drawing on experiences with Birla Cement that built their parents' home, Idea cellular that connected them to loved ones, Pantaloons where they shop for clothes. Every positive interaction with any Aditya Birla company becomes a trust deposit that Birla Estates can draw upon.

This trust premium is quantifiable. Birla Estates consistently achieves price realizations 10-15% above local competition. More importantly, it achieves faster sales velocity—projects sell 60-70% during launch phase versus industry average of 30-40%. In an industry where construction finance depends on pre-sales, this velocity advantage translates directly to lower capital costs and higher returns.

The capital access advantage is equally powerful. Stand-alone real estate developers in India face perpetual skepticism from institutional capital. Banks remember the 2008-2013 period when real estate NPAs soared. Private equity demands excessive returns reflecting perceived risks. Public markets apply discounts reflecting governance concerns.

But ABREL isn't just another real estate developer seeking capital. It's an Aditya Birla Group company with combined revenues exceeding $60 billion, relationships with every major financial institution globally, and access to patient capital from group companies. When IFC invested $50 million in ABREL, it wasn't taking a punt on Indian real estate—it was deepening a decades-old relationship with one of Asia's most respected conglomerates.

This capital advantage manifests in multiple ways. ABREL can undertake larger projects that stand-alone developers can't finance. It can hold land through down cycles without distress sales. It can invest in technology and sustainability that may not pay back immediately. Most crucially, it can survive market downturns that kill leveraged competitors.

The operational synergies, though less visible, are equally valuable. Century's paper business taught environmental compliance—crucial for real estate approvals. The cement experience provided understanding of construction materials and logistics. Textile operations developed expertise in managing large workforces and complex supply chains. Even the painful process of closing textile mills taught valuable lessons about stakeholder management during transformations.

Cross-business learning flows in unexpected ways. The paper mill's farm forestry program, which works with 50,000 farmers, provides a template for aggregating fragmented land parcels. The cement business's dealer network offers insights into tier-2 city distribution. The textile business's experience with fashion cycles helps understand real estate's style evolution.

The talent advantage is often underestimated. The Aditya Birla Management Corporation, the group's leadership development arm, has created a bench of professional managers comfortable with complexity, experienced in stakeholder management, and aligned with long-term value creation. When Birla Estates needs a CFO, it doesn't just search the real estate industry—it can tap financial leaders from across the group's 40+ companies.

This talent mobility works both ways. High performers at Birla Estates aren't stuck in real estate careers—they could potentially move to Ultratech, Grasim, or Aditya Birla Capital. This career optionality attracts talent that wouldn't join stand-alone developers. It also creates knowledge spillovers as managers bring best practices from other industries.

The governance advantage deserves special mention. Indian real estate has historically been plagued by weak governance—related party transactions, fund diversion, aggressive accounting. The Aditya Birla Group's governance standards, developed over decades as a public conglomerate, automatically apply to Birla Estates. Independent directors, audit committees, compliance frameworks—these aren't innovations but inheritance.

This governance premium is particularly valuable when dealing with international investors and customers. Non-resident Indians, who represent 20% of premium housing demand, are particularly sensitive to governance issues. The Aditya Birla name provides comfort that their investment is protected by institutional frameworks, not just personal relationships.

The patient capital philosophy, deeply embedded in conglomerate DNA, suits real estate's long cycles perfectly. While listed pure-play developers face quarterly earnings pressure, ABREL can take multi-year views. Land can be held for optimal development timing. Projects can be designed for long-term value rather than quick sales. Customer relationships can be nurtured beyond transaction completion.

This patience extends to market cycles. Real estate is inherently cyclical—boom periods of excessive optimism followed by busts of desperate pessimism. Stand-alone developers often can't survive the busts, forcing distress sales that destroy value. ABREL, backed by diversified cash flows and patient shareholders, can counter-cyclically invest during downturns, acquiring assets at attractive prices.

The portfolio approach to risk management, natural for conglomerates, provides resilience. While Birla Estates focuses on residential development, ABREL also owns commercial properties generating steady rentals and operates the profitable paper business. This diversification within focus—different revenue streams within real estate, plus non-real estate cash flows—provides stability without losing strategic clarity.

The institutional memory accumulated over 127 years provides perspective that new-age developers lack. ABREL has survived world wars, independence, socialist planning, liberalization, global financial crisis, demonetization, GST implementation, and COVID-19. This experience breeds confidence that current challenges, however daunting, can be overcome with patience and prudence.

The ecosystem advantages multiply over time. Aditya Birla Group employees become natural customers for Birla Estates. Corporate relationships open doors—a bank CEO who knows Kumar Mangalam Birla personally is more likely to approve project finance. Government relationships, built over decades, smooth regulatory approvals. Media relationships ensure favorable coverage.

But perhaps the greatest conglomerate advantage is cultural: the ability to think in decades, not quarters. When Birla Estates launches a project, it's not maximizing IRR for a private equity fund with a five-year horizon. It's building assets that could remain in the portfolio for generations. This long-term orientation shows in design quality, construction standards, and customer service—investments that may not pay back immediately but compound over time.

The playbook lesson is counterintuitive: in industries with trust deficits and execution complexity, conglomerate heritage can be a competitive advantage rather than burden. The key is selectively leveraging conglomerate strengths—brand, capital, governance, patience—while maintaining entrepreneurial agility and market focus. ABREL isn't succeeding despite being part of a conglomerate; it's succeeding because of it.

X. Bear vs. Bull Case Analysis

The investment case for ABREL presents a fascinating study in contrasts—transformational growth story meets concerning operational metrics, prestigious brand meets execution challenges, massive opportunity meets intense competition. The bear and bull cases are both compelling, making ABREL either a generational buying opportunity or a value trap depending on your perspective.

The Bear Case: Red Flags in the Financials

The bears start with a sobering fact: The company has delivered a poor sales growth of -18.7% over past five years. This isn't just disappointing—it's alarming for a company supposedly riding India's real estate boom. While management explains this as portfolio transition from textiles to real estate, skeptics see a company that destroyed revenue without yet proving it can rebuild.

More concerning is profitability, or lack thereof. Company has a low return on equity of 1.22% over last 3 years. For context, simply parking money in government bonds would have yielded 7%. The company is essentially destroying shareholder value even as management celebrates transformation success.

The balance sheet raises additional red flags. Company has low interest coverage ratio, meaning earnings barely cover interest payments. This is particularly worrying for a real estate company entering an interest rate upcycle. If rates rise further or sales slow, ABREL could face financial distress despite the Aditya Birla backing.

The recent financial performance contradicts the growth narrative. Profit: -202 Cr—the company is actually losing money despite claiming to be in hypergrowth mode. How can a company with ₹8,000 crore in bookings lose money? Either the bookings aren't converting to revenue, margins are negative, or accounting is aggressive.

The valuation appears stretched. Stock is trading at 5.39 times its book value, expensive for a company with negative profits and low returns. The market is pricing in perfect execution of the transformation—any disappointment could trigger significant correction.

Real estate sector risks loom large. Indian real estate is notoriously cyclical, with boom-bust cycles that destroy developers regularly. The current boom, driven by post-COVID demand and low interest rates, may be ending. Rising rates, inflation, and global uncertainty could trigger a downturn just as ABREL is scaling aggressively.

Competition is intensifying from every direction. Established players like DLF and Oberoi have deeper experience and better land banks. New-age developers like Prestige and Brigade are more agile. International players like Brookfield are entering with deeper pockets. ABREL is a subscale player in a consolidating industry—it could become prey rather than predator.

The execution track record is unproven at scale. While Birla Estates has launched successful projects, it hasn't demonstrated ability to execute multiple large projects simultaneously. Real estate development is operationally complex—land acquisition, approvals, construction, sales, customer service. One major project failure could destroy the carefully built brand.

Geographic concentration is risky. Focusing on just four cities—Mumbai, NCR, Bengaluru, Pune—provides clarity but increases vulnerability. A downturn in any of these markets would disproportionately impact ABREL. Diversified developers can offset regional weakness; ABREL can't.

The asset-light JV model, while capital efficient, has hidden risks. Joint ventures with landowners mean sharing economics and control. Disputes with JV partners are common in Indian real estate. One high-profile dispute could damage Birla Estates' reputation and freeze multiple projects.

Management transition risks exist. Mr. Jithendran has more than 32 years of professional experience and has completed his Advance Management Program (AMP) from Harvard Business School (HBS). He is a Civil Engineer from the Indian Institute of Technology (IIT) Kharagpur and completed his Post Graduate Diploma in Management from the Indian Institute of Management (IIM) Calcutta. While impressive, he's essentially running a one-man show. If Jithendran leaves, Birla Estates could struggle to maintain momentum.

Regulatory risks are ever-present in Indian real estate. RERA has improved transparency but also increased compliance costs. Environmental regulations are tightening. Land acquisition laws remain complex. Any regulatory change could impact profitability significantly.

The paper business, while profitable, is a distraction. Management attention spent on paper is attention not given to real estate. The ₹1,000 crore locked in paper assets could fund real estate growth. The market applies a conglomerate discount precisely because of this lack of focus.

Customer concentration in premium segments is risky. Economic downturns hit luxury spending first. If India's economic growth slows or wealth creation stalls, premium housing demand could evaporate. ABREL has no exposure to affordable housing, which enjoys government support and structural demand.

The Bull Case: Transformation Momentum

The bulls see the negative backward-looking metrics as precisely the opportunity. The -18.7% revenue decline reflects deliberate exit from low-return businesses. The low ROE reflects transition costs. The losses reflect investment in future growth. This is a transformation story—judging it on historical metrics misses the point.

The growth trajectory validates the strategy. With the annual growth of 77% from FY2020 to FY2025, Birla has become one of the fastest-growing real estate developer companies in India. This isn't incremental improvement—it's explosive expansion that demonstrates model validity.

The forward pipeline is even more impressive. Large Project Pipeline: Upcoming developments have a gross development value (GDV) of over ₹60,000 crore. At 20% EBITDA margins (conservative for premium real estate), this translates to ₹12,000 crore of potential profits—more than half current market capitalization.

The booking momentum continues accelerating. In FY 2024–25, Birla Estates achieved bookings worth ₹8,000 crore. This is actual customer commitment, not just pipeline. At typical construction cycles, these bookings convert to revenue over 3-4 years, providing visibility rare in cyclical industries. The market opportunity is massive and structural. Real estate sector in India is expected to reach US$ 1 trillion in market size by 2030, up from US$ 200 billion in 2021 and contribute 13% to the country's GDP by 2025. This isn't cyclical recovery but secular transformation driven by urbanization, formalization, and financialization.

The premium segment opportunity is particularly attractive. The demand for luxury homes in India, particularly those priced at Rs. 4 crore (US$ 0.5 million) and above, saw a remarkable surge in 2024, with sales rising by 53% across seven major cities. According to data from real estate consultancy firm CBRE, the total number of luxury housing units sold last year stood at 19,700. A notable shift in homebuyer preferences toward high-end properties was evident in the sales distribution by price segment. Residential units priced above INR 10 million (USD 118,399) accounted for 46% of total sales, recording a 29% year-on-year increase and emerging as the primary driver of overall market growth in the second half of 2024. This is exactly where Birla Estates is positioned.

The brand advantage is becoming more valuable as the sector consolidates. Trust matters more as ticket sizes increase and customers become sophisticated. The Aditya Birla name commands premiums that pure-play developers can't achieve. This isn't speculation—it's demonstrated in pricing power and sales velocity.

The Aditya Birla Group backing provides strategic advantages beyond brand. Access to patient capital means ABREL can hold land through cycles. Corporate relationships open doors for land acquisition and approvals. The group's ESG commitments attract institutional capital that avoids traditional developers.

The asset-light JV model is proving scalable. By partnering with landowners rather than buying outright, Birla Estates can expand rapidly without straining the balance sheet. The model also aligns interests—landowners become partners in success rather than mere sellers.

Management quality is exceptional. Jithendran brings proven track record from Godrej Properties and deep industry relationships. The ability to attract talent from hospitality and technology sectors demonstrates cultural magnetism. The governance standards inherited from Aditya Birla Group provide institutional stability.

The digital and sustainability initiatives position ABREL for the future. Younger, affluent buyers increasingly demand tech-enabled, environmentally conscious homes. ABREL's investments here aren't costs but moats that will compound over time.

Valuation, while optically expensive, may be reasonable for the growth profile. If ABREL achieves even 50% of its ₹60,000 crore GDV target at 15% margins, the implied valuation is attractive. The market is pricing the transformation risk, not the execution upside.

The portfolio approach provides downside protection. Commercial properties generate steady rentals. The paper business produces cash flow. Multiple revenue streams reduce dependence on residential cycles. This isn't a pure-play bet but a diversified exposure to Indian real estate.

The Verdict: Transformation in Progress

The bear and bull cases for ABREL aren't mutually exclusive—they're both right, just on different timeframes. The bears correctly identify current operational challenges, execution risks, and valuation concerns. The bulls accurately see transformational opportunity, structural advantages, and long-term potential.

The investment decision ultimately depends on time horizon and risk tolerance. For traders and momentum investors, ABREL's volatility and operational uncertainty make it unattractive. For long-term investors who believe in India's real estate transformation and Aditya Birla Group's execution capability, current prices may represent a generational opportunity.

The key insight is that ABREL isn't really a real estate company yet—it's a transformation story. The company is essentially rebuilding itself while flying, dismantling a century-old industrial conglomerate to create a modern real estate developer. Such transformations are messy, non-linear, and risky. But when successful, they create enormous value.