Hewlett Packard Enterprise: The Edge-to-Cloud Transformation Story

I. Introduction & Episode Roadmap

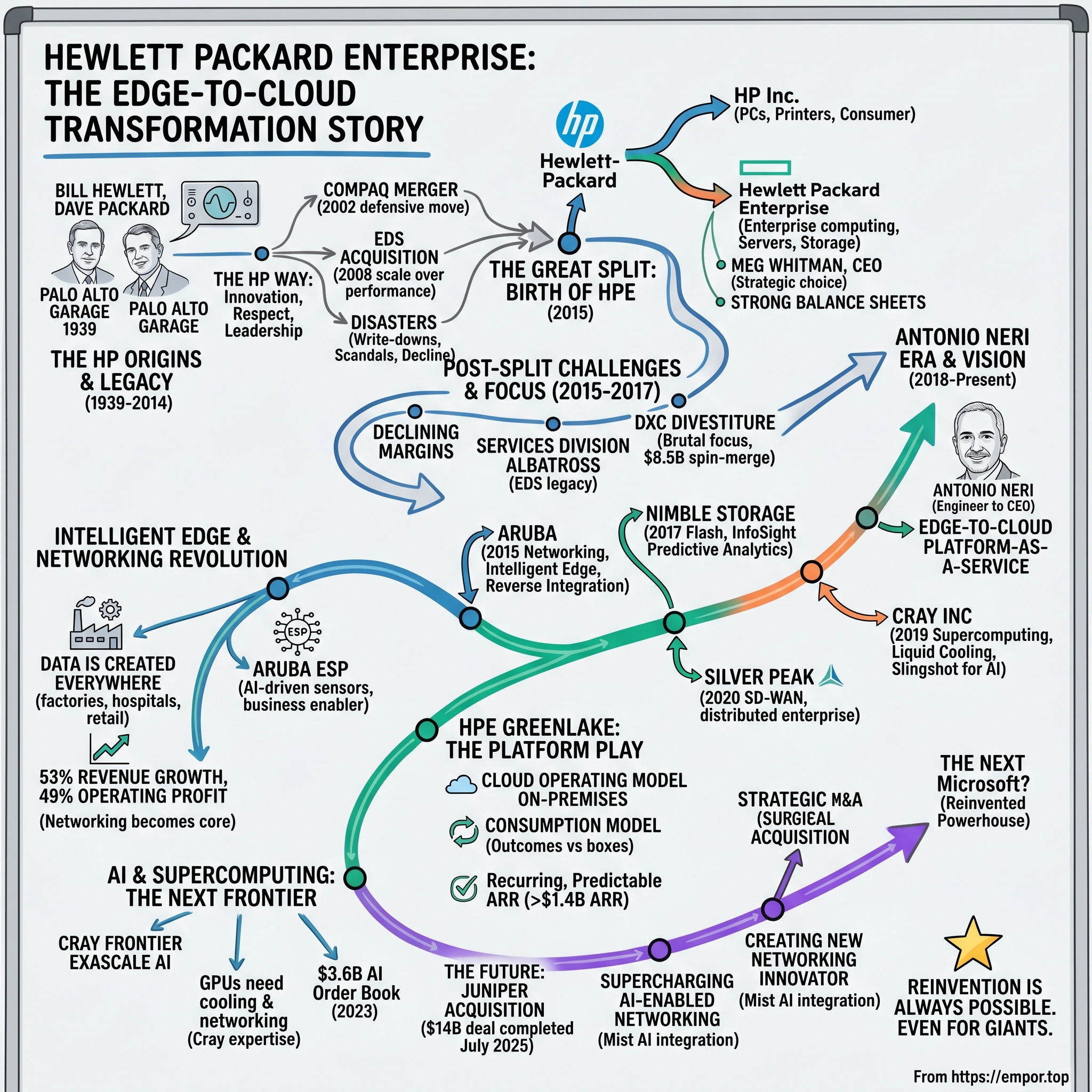

Picture this: November 1, 2015, Palo Alto, California. The very ground where Bill Hewlett and Dave Packard once tinkered in a garage—birthing Silicon Valley itself—witnesses another seismic moment. Hewlett-Packard, the original tech titan, splits in two. Not from weakness, but from strategic calculation. One half keeps the printers and PCs as HP Inc. The other emerges as Hewlett Packard Enterprise, carrying the weight of enterprise computing into an uncertain future.

The central question isn't whether this was necessary—it was. The real question is far more intriguing: How does a traditional enterprise hardware company, born from mainframes and servers, reinvent itself for the cloud era when Amazon Web Services already owns the sky?

This is a story of transformation under fire. Of a company that shed 100,000 employees in a single divestiture, watched its stock languish, then engineered one of the most dramatic pivots in enterprise technology. From selling boxes to selling outcomes. From fighting Dell in the data center to challenging Amazon at the edge.

We'll explore how HPE went from post-split chaos to commanding nearly half of its operating profit from networking—a business it didn't even own until 2015. How a consumptioN model called GreenLake grew from experiment to $1.4 billion in annual recurring revenue. And why Antonio Neri, an engineer who started as a customer support call center employee, might be the most underestimated CEO in tech.

This isn't just corporate history—it's a masterclass in portfolio management, strategic patience, and the art of transformation when everyone's already written your obituary.

II. The HP Origins & Legacy Context

The garage at 367 Addison Avenue tells you everything about Silicon Valley's creation myth. In 1939, two Stanford electrical engineering graduates, William Hewlett and David Packard, started with $538 in capital and a rented garage. Their first product? An audio oscillator that Disney bought eight units of for "Fantasia." The invoice read HP-200A—they wanted competitors to think they had a product line.

But here's what the plaques don't tell you: HP wasn't just first in Silicon Valley geography. They invented Silicon Valley culture. The "HP Way"—radical for its time—treated engineers like artists, profits like a scorecard for doing things right, and management as servants to innovation. Open floor plans before they were trendy. Profit-sharing when unions were the norm. Friday beer bashes that became the template for every startup thereafter. The HP Way was revolutionary: establishing the importance of respect for the individual, the value of leadership, the importance of integrity, the power of teamwork, and the need for adaptability, driving HP to leadership in many of the markets it chose to compete in. Management by objective referred to a system in which overall objectives are clearly stated and agreed upon, and which gives people the flexibility to work toward those goals in ways they determine best for their own areas of responsibility.

This wasn't corporate fluff. During the 1970 recession, rather than layoffs, HP shortened everyone's schedule and pay by ten percent such that the usual ten days of work during a two-week period was shortened to nine days, described as the "nine-day fortnight". Executives, managers and workers all joined in this reduction for six months until orders rose again in 1971. Using this solution, the company saved ten percent on labor across the board rather than laying off ten percent of the workforce.

Fast forward through decades of growth. HP became everything—printers, PCs, servers, services. The 1999 spin-off of test equipment into Agilent signaled something profound: HP was abandoning its founding business. The 2002 Compaq merger for $25 billion? A defensive move that made HP bigger but not better. By 2008, after acquiring EDS for $13.9 billion, HP earned combined revenues of $118.4 billion that year and a Fortune 500 ranking of 9 in 2009.

Then came the disasters. Mark Hurd's expense account scandal. Léo Apotheker's eleven-month tenure. The Autonomy acquisition for $11 billion that became an $8.8 billion write-down. By 2014, the company that invented Silicon Valley was dying from a thousand cuts.

III. The Great Split: Birth of HPE (2014–2015)

Meg Whitman walked into HP in September 2011 with the company in freefall. Stock down 40% in months. Three CEOs in two years. Board dysfunction so severe it made headlines. The former eBay chief had one overwhelming insight: HP wasn't one company anymore. It was two companies trapped in one body, each making the other weaker. She articulated it perfectly in October 2014: "We had to gather ourselves as one HP, but now we're in the position to take advantage of what's going on in the marketplace and position these two companies for growth." "They go after quite different market segments, and we now have the opportunity to align rewards and results, to respond to customer needs faster with these two big companies."

The strategic rationale was compelling. The PC and printer business—still profitable but declining—required consumer marketing, rapid product cycles, and cost discipline. The enterprise business needed long sales cycles, deep customer relationships, and massive R&D investments. Running them together was like having a marathon runner and a sprinter share the same training regimen.

But here's what made Whitman's approach masterful: timing. Three years earlier, in 2011, her predecessor Léo Apotheker had tried something similar and nearly destroyed the company. The difference? As Whitman explained during a Monday morning conference call with financial analysts: "Today was made possible by our turnaround. The work we have done in terms of fixing our balance sheet, improving our go-to-market sales, remaking our leadership, and igniting our innovation portfolios across both businesses has made this possible." She reminded analysts that HP was a mess three years ago and needed to rebuild "as one HP." The company is now "in a position of strength," she said, and by splitting into two Fortune-50 companies, each with approximately $57 billion in revenue, both companies could become "a lot more nimble, a lot more focused."

The mechanics of the split were elegant. HP Inc. would keep the $29 billion PC business and the $22 billion printing empire. Hewlett Packard Enterprise would take servers, storage, networking, software, and services—about $55 billion in revenue. Both would be Fortune 50 companies. Both would start debt-free with strong balance sheets.

Wall Street loved it. The stock jumped 5% on announcement. But employees? Different story. After 55,000 layoffs during Whitman's tenure, morale was fragile. The split meant more uncertainty, more reorganization, more cultural upheaval. The HP Way felt like ancient history.

Yet Whitman had one more surprise. Rather than stay with the safer, more predictable HP Inc., she chose to lead HPE—the enterprise business facing existential threats from cloud computing. It was the harder job, the riskier bet. Classic Silicon Valley move: go where the fear is greatest.

IV. The Post-Split Challenges & DXC Divestiture (2015–2017)

November 2, 2015. Day one of independence. HPE employees walked into offices worldwide wondering: what exactly are we now? The answer wasn't encouraging. A company with $53 billion in revenue but declining margins. A portfolio spanning everything from servers to software to services with no clear unifying vision. And most painfully, an enterprise services division hemorrhaging money.

The services business was HPE's albatross—100,000 employees, mostly from the 2008 EDS acquisition, running data centers and IT operations for Fortune 500 companies. Low margins, high complexity, massive contracts requiring armies of people. In the age of AWS, it looked like a relic. In May 2016, the company announced it would sell its enterprise services division to one of its competitors, Computer Sciences Corporation in a deal valued at US$8.5 billion. The spin-merge of the ES business unlocks a stronger, more focused HPE, well positioned to compete and win in today's rapidly changing market. The merger of HPE Enterprise Services with CSC, to form a new company DXC Technology, was completed on March 31, 2017.

The math was brilliant if brutal. The total value of the equity for HPE stockholders is valued at approximately $9.5 billion. In addition, as a result of the transaction, HPE received a $3 billion special cash payment, with $1.5 billion earmarked for the retirement of existing debt. Approximately 100,000 current HPE employees were affected—transferred to the new entity that would struggle from day one.

PC World wrote that "HPE, and before it, Hewlett-Packard, failed to develop middleware tools to really make a dent in the software market, where other companies like IBM, SAP, and Oracle are excelling." The criticism stung because it was true. HPE had tried repeatedly to build a software business—the Autonomy disaster being the most spectacular failure—and never succeeded.

To provide the expertise and financial services support customers need, HPE will retain and continue to invest in Pointnext, its technology services organization that draws on the expertise of more than 25,000 specialists in 80 countries to support customers across Advisory and Transformation Services, Professional Services and Operational Services. These teams collaborate with businesses worldwide to speed their adoption of emerging technologies, including cloud computing and hybrid IT, big data and analytics, the Intelligent Edge and Internet of Things (IoT).

But here's what outsiders missed: Whitman wasn't retreating. She was focusing. By divesting services, she freed HPE from its lowest-margin, most capital-intensive business. The $3 billion cash infusion strengthened the balance sheet. And most importantly, it cleared the deck for what came next.

In November 2017, Meg Whitman announced that she would be stepping down as CEO, after six years at the helm of HP and HPE, stating that, on February 1, 2018, Antonio Neri would officially become HPE's president and chief executive officer. The announcement shocked nobody inside HPE. Neri had been groomed for years, rising from customer support to running the entire enterprise group. But Wall Street was skeptical. Could an insider, an engineer no less, transform a company that had resisted transformation for so long?

V. The Antonio Neri Era & Edge-to-Cloud Vision (2018–Present)

Antonio Neri's story reads like Silicon Valley fan fiction. Started at HP in 1995 as a customer support engineer in the call center. No MBA. No pedigree. Just an electrical engineering degree and an obsession with solving customer problems. Twenty-three years later, he's running a $29 billion company.

His first all-hands as CEO set the tone: "We're not going to be the company that sells you a box and walks away. We're going to be the company that delivers outcomes." Simple words that signaled a revolution. Born in Argentina, he studied engineering at National Technological University and started working for Hewlett-Packard in 1995. Neri began military education and training at the age of 15, becoming an engineering apprentice for the Argentine Navy and working to repair ships' radar and sonar systems. Antonio's inspirational journey with the company started more than 25 years ago with a role as a customer service engineer in a European call center. He and his wife met at an HP call center and were married in the late 1990s.

The edge-to-cloud vision wasn't marketing fluff—it was a fundamental rethinking of enterprise computing. The premise: data isn't created in data centers anymore. It's created at the edge—in factories, hospitals, retail stores, vehicles. By 2025, 75% of enterprise data would be created outside traditional data centers. HPE would be the company that managed, analyzed, and secured that data wherever it lived.

In June 2018, Hewlett Packard Enterprise launched a hybrid cloud service called GreenLake Hybrid Cloud, built on top of HPE's OneSphere cloud management SaaS console, offered under its brand HPE GreenLake. GreenLake is designed to provide cloud management, cost control, and compliance control capabilities, and will run on AWS and Microsoft Azure. GreenLake includes cloud data services for containers, machine learning, storage, compute, data protection and networking through a management portal called GreenLake Central.

Neri's "Next Initiative" has been described as a "massive reimagining" of the company; the strategy has reduced HPE's number of stock keeping units by 75 percent, as well as the number of management levels, and works to increase innovation. By the end of 2020, HPE would consolidate from 11 ERP systems to one, from 23 master data systems to one. Complexity killed margins; simplicity restored them.

The cultural transformation was equally radical. "When I took over as CEO, I placed an emphasis on culture with a focus on rebuilding the company's confidence and swagger," he said. "I was struck and motivated by the incredibly passionate and talented team members we have around the world. And to this day, I still find myself inspired by how vibrant, genuine, and unconditionally committed to our purpose of advancing the way people live and work they are – just like my colleagues in the Amsterdam call centre back in 1995."

VI. Strategic M&A: Building the Portfolio (2015–2023)

While competitors pursued mega-mergers, HPE played a different game: surgical strikes. Each acquisition targeted a specific gap in the edge-to-cloud strategy. No transformational bets, no bet-the-company moves. Just methodical portfolio construction.HPE purchased Aruba in 2015 for around $3 billion USD (around $24.67 a share). The deal looked expensive then—Aruba had only $729 million in sales. But Neri, who helped drive the acquisition, saw something others missed: the explosion of mobile devices in enterprises wasn't a PC replacement story; it was an edge computing story. Every WiFi access point was becoming a mini data center.

The integration became a masterclass in acquisition management. Rather than absorb Aruba, HPE practiced what co-founder Keerti Melkote called "reverse integration"—letting Aruba's culture and go-to-market model influence HPE's broader networking strategy. "We've added a billion dollars of revenue in the last four years, so financially [the acquisition] has been a big success and it's growing really well. We wouldn't have achieved this without being able to integrate the cultures of both organisations in a productive way," Melkote stated. In April 2017, Hewlett Packard Enterprise completed its acquisition of hybrid flash and all flash manufacturer, Nimble Storage Inc, for US$1.2 billion or US$12.50 per share. The acquisition was expected to be accretive to HPE earnings in the first full fiscal year following the close. What mattered wasn't just the flash arrays—it was InfoSight, Nimble's predictive analytics platform. InfoSight is Nimble Storage's storage management and predictive analytics portal. It is designed to help with storage resource management as well as customer support. The InfoSight Engine, is a sophisticated data collection and analysis engine, equipped with data analytics, system modeling capabilities, and predictive algorithms. In September 2020, Hewlett Packard Enterprises (HPE) completed its acquisition of Silver Peak systems for $925 million. This is an insane acquisition price given that the overall market, according to HPE's own press release, is currently only worth $2.3 billion. The acquisition will strengthen Aruba ESP (Edge Services Platform), helping to advance enterprise cloud transformation with a comprehensive edge-to-cloud networking solution covering all aspects of wired, wireless local area networking (LAN) and wide area networking (WAN).

The timing was prescient. COVID-19 had just transformed every enterprise into a distributed enterprise. SD-WAN went from nice-to-have to mission-critical overnight. According to recent research by Futuriom, the SD-WAN tools and software market will accelerate to a growth rate of 34% CAGR to reach $2 billion this year. In May 2019, Hewlett Packard Enterprise announced plans to acquire Cray Inc for US$35 per share. The announcement came soon after Cray had landed a US$600 million US Department of Energy contract to supply the Frontier supercomputer to Oak Ridge National Laboratory in 2021. HPE paid $35.00 per share, in a transaction valued at approximately $1.4 billion, net of cash.

This wasn't about competing with Dell in the enterprise—it was about owning the future of AI infrastructure. Cray brought three game-changing assets: expertise in liquid cooling (critical for AI workloads), the Slingshot interconnect technology, and relationships with every major government lab. In 2024, HPE Cray supercomputer systems held the top three spots in the TOP500, which ranks the most powerful supercomputers in the world.

The portfolio construction strategy worked. Rather than one transformational deal that could have destroyed the company (remember Autonomy?), HPE built capabilities methodically. Each acquisition strengthened a specific edge-to-cloud pillar. Total spent: roughly $6 billion. Value created: multiples of that.

VII. The Intelligent Edge & Networking Revolution

Walk into any Fortune 500 campus today and you'll likely find Aruba gear. Not because it's cheapest—it isn't. Not because it has the most features—debatable. But because HPE understood something Cisco missed: the network isn't infrastructure anymore. It's the nervous system of digital business.

HPE's performance in the Intelligent Edge segment was particularly noteworthy in the quarter. Revenue increased 53% year-over-year and contributed 20% of our total company revenue. Operating profit more than doubled in another exceptional quarter for this business; it is now the largest source of HPE's operating profit, at 49% of our total segment operating profit.

Think about that transformation. A business that didn't exist at HPE before 2015 now generates nearly half the company's operating profit. How? By recognizing that "edge" isn't a place—it's everywhere data gets created, processed, or consumed outside traditional data centers.

The campus networking market underwent a generational shift starting in 2019. WiFi 6 wasn't just faster WiFi—it was deterministic, reliable enough for mission-critical applications. Aruba's timing was perfect. While Cisco focused on protecting its installed base, Aruba evangelized the new standard aggressively. Market share gains followed.

But the real innovation wasn't in speeds and feeds. It was in turning networking from a cost center into a business enabler. Aruba's AI-powered insights could tell retailers which store displays attracted attention, help hospitals track equipment, enable manufacturers to predict equipment failures. The network became a sensor platform, not just a pipe.

The SD-WAN integration via Silver Peak completed the picture. Now HPE could manage enterprise connectivity from headquarters to branch to cloud to individual devices. One platform, one set of policies, one throat to choke. For IT departments drowning in complexity, it was salvation.

Competition remains fierce. Cisco still dominates with 45% market share. But HPE's share has grown from essentially zero to over 15% in less than a decade. More importantly, they're winning the architectural battles—cloud-native, AI-driven, as-a-service—that will define the next decade.

VIII. HPE GreenLake: The Platform Play

Here's the $1 trillion question facing every enterprise IT vendor: How do you compete with public cloud? Dell's answer: you don't, you partner. IBM's answer: hybrid cloud consulting. HPE's answer: bring the cloud operating model on-premises. GreenLake started as a financing play—basically a lease with a fancy name. But Neri saw what others missed: customers didn't want to own infrastructure anymore, but they couldn't move everything to public cloud. Regulatory requirements, data sovereignty, latency, cost—all real constraints. HPE GreenLake supports multi-cloud experiences everywhere – including clouds that live on-premises, at the edge, in a colocation facility, and in a public cloud – and continues to drive strong demand worldwide. ARR grew 48% year-over-year to $1.9 billion, nearly doubling since Q1 2023 primarily driven by HPE GreenLake.

The transformation required rebuilding HPE from the ground up. New billing systems, new sales compensation models, new support structures. Selling outcomes instead of boxes requires a fundamentally different mindset. Channel partners rebelled initially—their business models depended on hardware margins. HPE had to essentially fund the channel's transformation alongside its own.

But here's the genius: GreenLake isn't competing with AWS on price or scale. It's solving a different problem. AWS gives you infinite capacity in their data centers. GreenLake gives you cloud-like consumption in your data center. For regulated industries, sovereign nations, and latency-sensitive applications, that's not a nice-to-have—it's the only option.

The economics work because HPE controls the full stack. They manufacture the hardware, write the software, provide the services. Every layer adds margin. And unlike traditional hardware sales, the revenue is recurring, predictable, and grows over time as usage expands.

IX. AI & Supercomputing: The Next Frontier

Walk into any AI conference today and you'll hear the same complaint: we can't get enough GPUs. NVIDIA has the entire industry by the throat. But here's what most miss: GPUs are useless without the infrastructure to support them—cooling, networking, storage, orchestration. That's HPE's wedge.

The Cray acquisition looks prescient now. Liquid cooling? Essential for AI workloads that generate 10x the heat of traditional computing. Slingshot interconnect? Purpose-built for the massive data flows AI training requires. Exascale expertise? Every AI model is pushing toward exascale compute requirements.

Demand in our AI solutions is exploding. We saw a significant uptick in customer demand in recent quarters for accelerated computing infrastructure and services. Our HPC & AI segment revenue grew 25% year-over-year in fiscal 2023. We ended this fiscal year with the largest HPC & AI order book on record, driven by $3.6 billion in accelerated processing unit (APU) orders.

Frontier at Oak Ridge National Laboratory tells the story. Built by HPE Cray, it became the world's first exascale computer and immediately got repurposed for AI research. The infrastructure built for climate modeling turned out to be perfect for training large language models. HPE didn't plan this convergence—nobody did—but they're positioned perfectly for it.

The competitive dynamics are fascinating. Dell partners with NVIDIA but lacks the cooling and interconnect expertise. IBM has the expertise but limited scale. Cloud providers have everything but can't serve regulated industries or sovereign nations. HPE sits in the sweet spot: proven technology, global scale, on-premises capability.

X. Playbook: Business & Strategic Lessons

The HPE transformation offers a masterclass in corporate reinvention. Not the flashy, bet-the-company kind that makes headlines, but the grinding, methodical kind that actually works.

Lesson 1: Portfolio surgery requires precision. HPE didn't just randomly divest businesses. Each move followed a clear logic: keep what differentiates, shed what commoditizes, acquire what accelerates. The ES divestiture removed a boat anchor. The Aruba acquisition provided a growth engine. The pattern is consistent.

Lesson 2: Business model transformation is harder than technology transformation. Moving from selling products to selling outcomes required rewiring everything—sales compensation, channel relationships, customer contracts, support models. The technology was the easy part.

Lesson 3: Timing matters more than vision. HPE tried the as-a-service model in 2008 and failed. The market wasn't ready. By 2018, cloud had educated customers on consumption models. Same strategy, different decade, different outcome.

Lesson 4: The innovator's dilemma is real but solvable. HPE's hardware business funded its transformation to services. The key was managing the transition gradually—GreenLake started small, grew organically, then accelerated as traditional revenues declined. No big bang, no burning platforms, just steady evolution.

Lesson 5: Culture eats strategy, but strategy shapes culture. Neri didn't try to preserve the old HP Way. He created a new culture—more aggressive, more focused, more accountable. The strategy drove the cultural change, not vice versa.

Lesson 6: Capital allocation is destiny. HPE returned cash to shareholders while investing in growth. Share count declined 20% since 2018. Dividend maintained throughout transformation. M&A disciplined and strategic. This balance kept investors patient during the transition.

XI. Analysis & Investment Case

Our steady execution has resulted in our third straight year of revenue growth, our highest gross margins, and our highest non-GAAP operating profit since I became CEO, and record-breaking results in non-GAAP diluted net earnings per share and free cash flow. Total revenue for the full year increased 5.5% year-over-year in constant currency to $29.1 billion.

The bull case is compelling. Edge computing is exploding—IDC projects $250 billion by 2024. Hybrid cloud is the end state for most enterprises—Gartner says 75% will deploy hybrid by 2025. AI infrastructure demands are insatiable and growing exponentially. HPE has leading positions in all three markets.

The Intelligent Edge business is approaching $5 billion in revenue with operating margins above 20%. GreenLake ARR of $1.9 billion growing 48% annually with 70% gross margins. AI systems revenue of $1.5 billion growing triple digits. These aren't mature businesses being milked—they're growth engines just hitting stride.

The bear case centers on execution risk. Can HPE integrate Juniper successfully? Can GreenLake scale to $10 billion ARR without margin compression? Can they compete with hyperscalers in AI? All valid concerns.

Competition remains intense. Dell's infrastructure business is 2x HPE's size. Cisco dominates networking with 45% share. AWS/Azure/Google own public cloud. NVIDIA controls AI compute. HPE must execute flawlessly to gain share.

Valuation tells an interesting story. At 10x forward earnings, HPE trades at half the multiple of peers. The market still sees it as a declining hardware vendor, not a growing edge-to-cloud platform. This disconnect creates opportunity if the transformation succeeds.

XII. Looking Forward: The Juniper Deal & Beyond

As we look ahead to the future of this market, we are excited about our pending Juniper Networks acquisition. Combining our complementary portfolios will supercharge HPE's edge-to-cloud strategy, accelerating our entire portfolio with AI-enabled innovation. When our proposed acquisition closes, we will create a new networking innovator with a comprehensive portfolio for customers and partners.

The $14 billion Juniper acquisition, completed in July 2025, represents HPE's boldest move yet. Under the terms of the agreement, which has been unanimously approved by the Boards of Directors of HPE and Juniper, Juniper shareholders will receive $40.00 per share in cash upon the completion of the transaction. The purchase price represents a premium of approximately 32% to the unaffected closing price of Juniper's common stock on January 8, 2024.

The strategic logic is compelling. Juniper brings enterprise routing, service provider relationships, and Mist AI—arguably the best AI-driven network management platform. Combined with Aruba's campus and edge leadership, HPE now offers a full networking stack from edge to core to cloud. Only Cisco can match this breadth.

Integration will be the test. HPE must preserve Juniper's innovation culture while achieving $450 million in synergies. Early signs are positive—keeping separate brands, maintaining R&D investment, retaining key talent including former Juniper CEO Rami Rahim to lead the combined networking unit.

The future battleground is clear: AI infrastructure. Every enterprise will need AI capabilities. Most can't use public cloud for regulatory, sovereignty, or latency reasons. HPE's edge-to-cloud platform, enhanced by Juniper, positions them perfectly. Liquid-cooled servers from Cray, high-speed networking from Juniper/Aruba, consumption models from GreenLake—it's a compelling package.

XIII. Recent News

The momentum continues. Q4 2024 results exceeded expectations with record quarterly revenue of $8.5 billion, up 15% year-over-year. AI systems revenue hit $1.5 billion. GreenLake ARR approached $2 billion. The transformation from hardware vendor to platform provider is accelerating.

The regulatory approval for Juniper, despite DOJ challenges, validates the strategic rationale. The combined networking business will contribute more than 50% of total company operating income—remarkable for a business that didn't exist at HPE a decade ago.

Looking ahead, HPE faces both opportunity and challenge. The AI gold rush creates insatiable demand for infrastructure. The edge computing explosion plays to HPE's strengths. But competition intensifies daily. Execution must be flawless.

Conclusion

The HPE story defies Silicon Valley convention. No moonshots. No pivots to crypto or metaverse. Just methodical transformation of a 85-year-old company for the next computing era. From selling boxes to selling outcomes. From fighting yesterday's wars to defining tomorrow's battlefields.

Antonio Neri's vision—edge-to-cloud platform-as-a-service—sounded like buzzword bingo in 2018. Today it looks prescient. The company that invented Silicon Valley is reinventing itself once again. Not through revolution but evolution. Not through disruption but transformation.

The next decade will test whether this transformation succeeds. Can GreenLake scale to rival public cloud? Can HPE integrate Juniper successfully? Can they capture meaningful share of the AI infrastructure boom? The answers will determine whether HPE becomes the next IBM—a faded giant living on legacy—or the next Microsoft—a reinvented powerhouse driving the future.

The smart money should watch the fundamentals: ARR growth, operating margins, market share gains. But also watch the intangibles: talent retention, innovation velocity, customer satisfaction. HPE has done the hard work of transformation. Now comes the harder work of execution.

For investors, HPE represents a rare opportunity: a transformation story with the hard part behind it. The portfolio is rebuilt. The business model is transformed. The growth engines are firing. At current valuations, the market hasn't recognized this yet. That disconnect won't last forever.

The company that began in a Palo Alto garage, that created Silicon Valley's culture, that defined enterprise computing for generations, is writing its next chapter. It's not the sexiest story in tech. But it might be the most important. Because if a company this old, this large, this traditional can transform for the AI era, it proves something profound: reinvention is always possible. Even for giants.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube