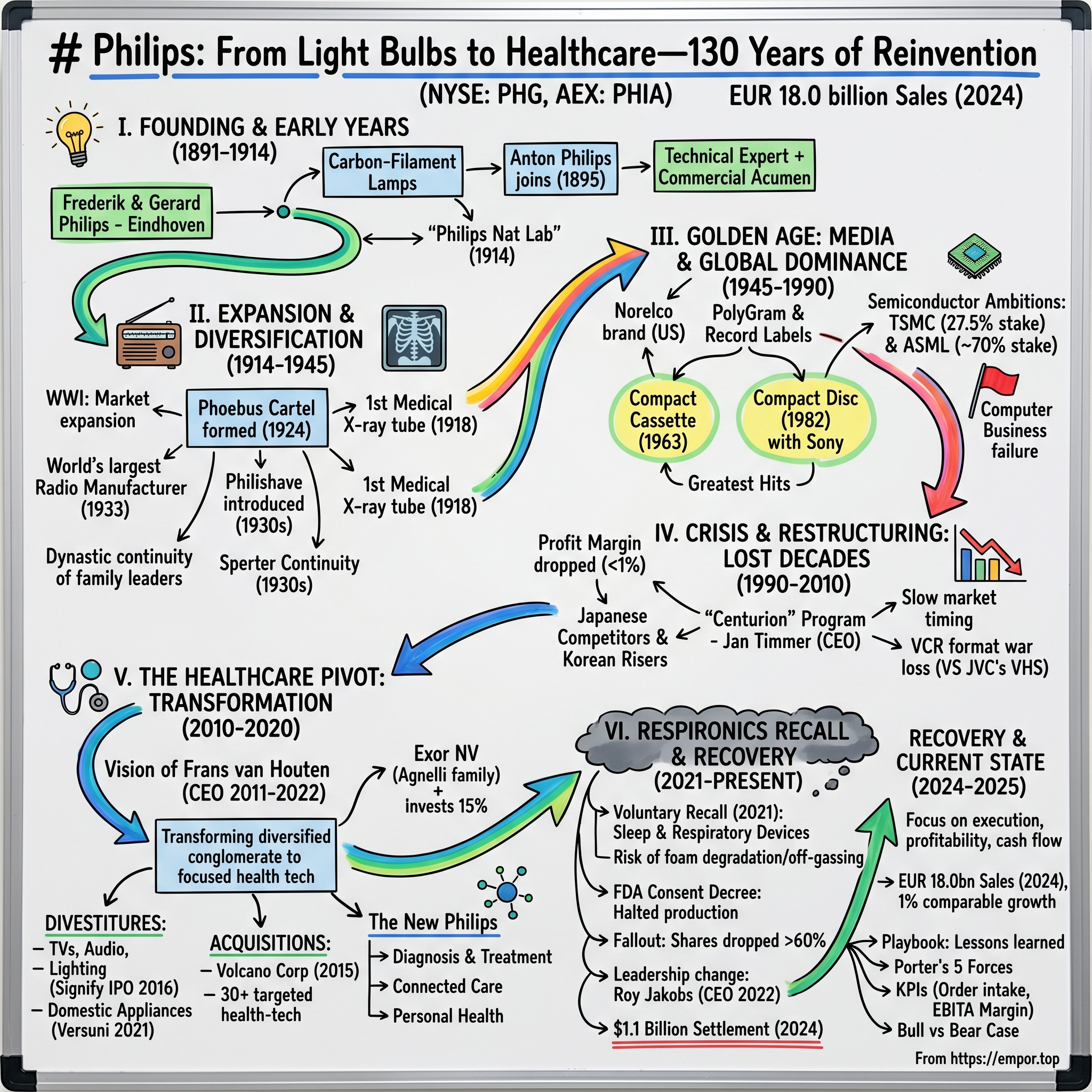

Philips: From Light Bulbs to Healthcare—130 Years of Reinvention

I. Introduction & Episode Roadmap

Picture Eindhoven in 1891—a modest industrial town in southern Netherlands, far from the commercial centers of Amsterdam or Rotterdam. In a small factory there, a father and son are placing an audacious bet on a new technology: the incandescent light bulb. Neither Frederik nor Gerard Philips could have imagined that their humble lamp company would one day become one of the world's largest electronics conglomerates, invent the compact cassette and co-invent the compact disc, help birth the semiconductor foundry industry, and ultimately transform into a focused healthcare technology giant.

Today, Royal Philips (NYSE: PHG, AEX: PHIA) is a leading health technology company, generating 2024 sales of EUR 18.0 billion and employing approximately 67,800 people with sales and services in more than 100 countries. The company's journey from light bulbs to MRI scanners spans three centuries and represents one of business history's most dramatic corporate metamorphoses.

The central question animating Philips' story is deceptively simple: How did a light bulb company become one of the world's largest healthcare technology firms—and what went catastrophically wrong along the way?

Through the 20th century, Philips grew into one of the world's largest electronics conglomerates, with global market dominance in products ranging from kitchen appliances and electric shavers to light bulbs, televisions, cassettes, and compact discs. At one point, it played a dominant role in the entertainment industry through PolyGram. However, in the 2010s, the company began downsizing, selling its TV manufacturing, lighting, and home appliance units, eventually becoming a healthcare-focused company.

But this transformation hasn't been smooth. Since the initial recall in June 2021, Philips' shares have plummeted more than 60%. A catastrophic product recall of sleep therapy devices has cost the company billions, forced out its long-tenured CEO, and raised fundamental questions about whether a company can successfully execute such a dramatic strategic pivot while maintaining the quality culture essential to healthcare.

This deep dive explores three major themes: Innovation vs. Execution—how a company can repeatedly invent breakthrough technologies yet fail to capture their full economic value; Conglomerate to Pure-Play Transformation—the 25-year journey from diversified electronics giant to focused healthcare company; and Crisis Management—what happens when quality systems fail in a healthcare company.

II. Founding & Early Years: The Light Bulb Empire (1891–1914)

The story begins with Frederik Philips, a prosperous merchant and banker from the southern Netherlands who saw opportunity in the nascent electrical lighting industry. In 1891, Frederik and his son Gerard founded Philips & Co in Eindhoven. Gerard Philips brought something crucial to the venture: technical expertise. He had worked as an engineer with the Anglo-American Brush Electric Light Corporation Ltd, gaining hands-on experience with the still-developing technology of incandescent lighting.

Gerard was a relentless experimenter. He continually refined light bulb designs, seeking to improve longevity while simultaneously optimizing production procedures. In the capital-intensive light bulb industry, manufacturing efficiency was as important as product quality—a lesson that would echo through the company's history.

A significant turning point occurred in 1895 when Gerard's younger brother, Anton Philips, joined the firm. Anton, despite his engineering degree, initially worked in sales but quickly demonstrated exceptional commercial acumen. Where Gerard was the inventor and optimizer, Anton was the expansionist and dealmaker. This complementary partnership was instrumental in the company's rapid expansion and international growth.

The Philips sons established what would become a defining characteristic of the company: an autocratic but paternalistic management style, with a tradition of taking care of their workers "from the cradle to the grave." Philips built housing, schools, and hospitals in Eindhoven, and from 1900 onward provided free medical aid to employees. This social contract created fierce employee loyalty and helped the company weather numerous storms over the following century.

Initially, the company concentrated on making carbon-filament lamps, and by the turn of the century it was one of the largest producers in Europe. The brothers had transformed a regional manufacturer into a continental powerhouse in less than a decade.

Recognizing the value of scientific research to product innovation, the first Philips research laboratory—known as 'Philips Nat Lab'—opened in 1914. This wasn't mere corporate research; it was fundamental physics and chemistry. The Nat Lab would become one of the world's most productive industrial research facilities, spawning technologies that would eventually reshape entire industries. The decision to invest heavily in basic research when the company was barely two decades old reflected a belief that would define Philips: sustainable competitive advantage comes from deep scientific understanding, not just incremental product improvement.

For investors, the early Philips story illustrates a recurring pattern: technical excellence combined with commercial acumen creates exponential growth, and investment in fundamental R&D, while expensive, can yield transformative returns over long time horizons.

III. Expansion & Diversification: From Radio to Shavers (1914–1945)

The outbreak of World War I in 1914 transformed Philips' strategic landscape. The Netherlands' neutrality proved a commercial blessing in disguise, allowing Philips to capture many new markets as competitors from combatant nations like Germany, France, and Britain faced disruption. While others fought, Philips built.

The Nat Lab's investments began paying dividends. In 1918, the company introduced a medical X-ray tube and began exporting it to the United States by 1926—the origin of Philips' healthcare involvement. This seemingly minor product line would eventually become the company's entire identity, though that transformation would take nearly a century.

In 1924, Philips made a controversial strategic move that would shape the global lighting industry for decades. Together with General Electric Company and Osram GmbH, Philips formed the Phoebus cartel to divide up the lightbulb market worldwide and to set the standard life of a lightbulb at 1,000 hours. Critics claimed that the cartel stifled innovation and competition in lighting for several decades, and it remains a case study in planned obsolescence. The cartel demonstrated Philips' market power but also its willingness to prioritize stable profits over disruptive innovation—a tension that would recur.

By 1919, Philips had expanded into the production of radio tubes, leveraging its expertise in vacuum tube manufacturing from the lighting business. In 1927, it introduced a simple affordable radio, and by 1933 it was the world's largest radio manufacturer. The pattern was classic Philips: scientific expertise from the Nat Lab, manufacturing excellence from the factory floor, and aggressive commercial expansion.

During the 1930s, Philips introduced its pioneering rotary electric razor, the Philishave. With its ergonomics and attractive appearance, the Philips Philishave heralded the age of mass-market consumerism. The product showed that Philips could translate technical innovation into consumer-friendly designs—and that it could successfully enter entirely new product categories.

The approach of World War II presented existential challenges. Just before the outbreak, Philips moved its headquarters to Curaçao in the Dutch Caribbean, keeping the company out of German control when the Netherlands fell in May 1940. Nevertheless, Philips's role in the war became the subject of some controversy, as factories in occupied Eindhoven continued production under German supervision while the company's management operated from overseas.

Members of the Philips family led the company until 1977 and maintained great influence into the 1980s. The succession ran from Gerard as CEO from 1891-1922, to Anton from 1922-39, Frans Otten from 1939-61, Frits Philips from 1961-71, and Henk van Riemsdijk from 1971-77. This dynastic continuity provided strategic consistency but eventually created challenges as the company faced increasingly dynamic markets requiring faster adaptation.

IV. The Golden Age: Media Innovations & Global Dominance (1945–1990)

After 1945, Philips emerged from the war with its management structure intact, its international distribution networks recovering, and its technical capabilities undiminished. The company expanded its product range aggressively, bringing its rotating blade electric razor to the United States in 1947 under the brand name Norelco—"Norelco" being "North American Philips Electrical Company." Over the next few decades, the company added several hair removal products, as well as electric toothbrushes and other oral care products.

In 1951, the company launched the Philips record label, acquired Mercury Records in 1960, and continued to invest in record labels such as Deutsche Grammophon, Decca, and Motown through its PolyGram subsidiary. This foray into entertainment content was driven by a strategic belief: controlling both hardware (turntables, cassette players) and software (recorded music) would create synergies. The theory was elegant; the execution proved messier.

The Compact Cassette & Compact Disc: Philips' Greatest Hits

The cassette tape, also called Compact Cassette, was invented by Lou Ottens and his team at the Dutch company Philips, and the Compact Cassette was introduced in August 1963. The format was revolutionary in its simplicity: a pocket-sized plastic shell containing magnetic tape that could record and play back audio.

Philips made a fateful decision regarding the Compact Cassette that would shape its approach to later innovations. Philips agreed to waive royalties but did not give Sony exclusive rights to the technology. In 1965, based on a patent that guaranteed compatibility, Philips made the technology available free of charge to manufacturers all over the world. The decision to license freely sacrificed short-term profits for market adoption, and it worked brilliantly. From 1983 to 1991, the cassette tape was the most popular audio format for new music sales in the United States.

The Compact Cassette proved that Philips had the ability to lay down a worldwide standard—a capability the company would leverage two decades later with an even more important innovation.

The success of the compact disc has been credited to the cooperation between Philips and Sony, which together agreed upon and developed compatible hardware. The unified design of the compact disc allowed consumers to purchase any disc or player from any company and allowed the CD to dominate the at-home music market unchallenged.

The year 1979 is one of the most important years in CD development history. World renowned Dutch electronics manufacturer Philips brought a prototype CD player to Japan to demonstrate it. The team from the Netherlands included Lou Ottens, technical director of the Philips Audio Industry Group, Joop Sinjou, also from the Audio Industry Group, and chief engineer Jacques Heemskerk. They visited each of the major manufacturers in turn.

The desire to achieve this aim also benefitted from hindsight, in that it was considered essential to avoid a repetition of the current situation in the video-recorder market—where no single system has yet emerged as the universal system of choice. With this objective in mind, negotiations started with another major audio company, the Sony Corporation, resulting in an agreement being reached in August 1979.

Philips coined the term compact disc in line with another audio product, the Compact Cassette, and contributed the general manufacturing process, based on video LaserDisc technology. Philips also contributed eight-to-fourteen modulation (EFM), while Sony contributed the error-correction method, CIRC.

The Compact Disc Digital Audio System was developed by the Dutch consumer electronics company PHILIPS Gloeilampen N.V. in cooperation with the Japanese consumer electronics company SONY Corp. and introduced to the market in Japan in 1982 and worldwide in 1983.

After their commercial release in 1982, compact discs and their players were extremely popular. Despite costing up to $1,000, over 400,000 CD players were sold in the United States between 1983 and 1984. By 1988, CD sales in the United States surpassed those of vinyl LPs, and, by 1992, CD sales surpassed those of prerecorded music-cassette tapes.

The CD represented Philips at its best: fundamental scientific innovation from the Nat Lab, strategic partnership to ensure industry adoption, and successful commercialization. The decision to collaborate with Sony rather than compete for a proprietary standard was masterful—learned from the VCR format war that Philips lost to JVC's VHS.

Semiconductor & Computing Ambitions

In 1985, Philips made an investment that would eventually prove more valuable than virtually anything else in its history—though the company would exit before capturing most of the value.

Texas Instruments and Intel turned down Morris Chang. Only Philips was willing to sign a joint venture contract with Taiwan to put up $58 million, transfer its production technology, and license intellectual property in exchange for a 27.5 percent stake in TSMC.

Although Philips initially held a 27.5% stake in TSMC, its influence extended beyond financial investment. In addition to capital, Philips played a crucial role by transferring semiconductor manufacturing technology, intellectual property, and patents to TSMC, enabling the company to scale more rapidly. Philips also provided TSMC's first CEO, James E. Dykes, who had previously worked at Philips North America.

The TSMC deal, which has become known in Taiwan's high-tech history as a miracle investment, earned Philips a return of 300 times its initial investment. Moreover, Philips was able to safely navigate the financial crises of the 1990s by raising money through the sale of its stake in TSMC.

This meant that by the mid 1990s, Philips owned 28% of TSMC at its 1994 IPO and closer to 70% of ASML at its 1995 IPO—arguably two of the most important companies in the world today. Philips gradually sold out of both companies, and had in 2007 fully exited both. Since then, TSMC and ASML have returned over 9,500% and 78,300% respectively, and both companies combined are worth roughly 56x times that of Philips itself as of this writing.

Philips was much less successful in entering the computer business. By the time the company released its P-1000 mainframe system in the mid-1960s, the IBM 360 was well established as the market standard. The failure illustrated a recurring Philips weakness: technical excellence without market timing is insufficient.

V. Crisis and Restructuring: The Lost Decades (1990–2010)

The Philips that entered the 1990s was a company that had invented the future multiple times—cassettes, CDs, early smartphones—yet increasingly struggled to profit from it. In the 1980s, Philips's profit margin dropped below 1 percent, and in 1990 the company lost more than US$2 billion, the biggest corporate loss in Dutch history.

The troubles continued into the 1990s as its status as a leading electronics company was swiftly lost. Japanese competitors, led by Sony, Matsushita, and Sharp, had overtaken Philips in consumer electronics. Korean companies like Samsung and LG were rising fast. Chinese manufacturers were emerging as low-cost producers.

In 1990, the newly appointed CEO, Jan Timmer, decided to sell off all businesses that dealt with computers, which meant the end of Philips Data Systems as well as other computer activities. In 1991, the businesses were acquired by Digital Equipment Corporation. Timmer's "Centurion" restructuring program cut costs brutally but couldn't address the fundamental problem: Philips was a technology company that struggled to commercialize its technologies.

The company remained driven by technology, however, often striving for high quality rather than low cost. In later years the company was often slow to bring its innovative technologies to market. The VCR format war loss—Philips backed Betamax-style technologies while the VHS standard won—became a cautionary tale. The CD-i interactive multimedia player, launched in 1991, was a commercial failure despite embodying technologies that would later become standard. The digital compact cassette (DCC), launched in 1992 to compete with Sony's MiniDisc, was discontinued by 1996.

Why couldn't Philips capitalize on its innovations? Several factors converged: The company's culture prioritized engineering excellence over speed-to-market. Its European cost base was higher than Asian competitors. Its conglomerate structure created bureaucracy and diffused management attention. And its brand, while respected, lacked the consumer cachet of Sony or the commercial relationships of GE.

After weeks of speculation, on May 22, 1998, Philips announced that they would sell PolyGram to Seagram for $10 billion. Some of the reasons cited for the deal were a lack of pop hits from the music side of the company, and an equal lack of box-office successes from the film side.

The board of the Dutch consumer electronics company Philips Electronics NV, which owned 75 percent of PolyGram, approved the sale of its stake yesterday. Philips decided to get out of the "content" side of the entertainment industry after failing to find much synergy with its hardware businesses.

Philips spun-off poorly performing units throughout the 2000s, including its semiconductor and television businesses, to counter sluggish growth. In December 2005, Philips announced its intention to divest Philips Semiconductors into an independent legal entity. In September 2006, Philips completed the sale of an 80.1% stake in Philips Semiconductors to a consortium of private equity investors consisting of KKR, Bain Capital, Silver Lake Partners, Apax Partners and AlpInvest Partners. The new company name NXP (from Next eXPerience) was announced on August 31, 2006.

The former semiconductor unit of Royal Philips Electronics, recently sold to a group of equity firms for 8.3 billion euros (about US $10.6 billion), was relaunched as a new company, NXP ("Next Experience"). The firm remained headquartered in Eindhoven, the Netherlands.

The lost decades taught a painful lesson: being an innovative conglomerate was no longer a sustainable business model. The future required focus.

VI. The Healthcare Pivot: Strategic Transformation (2010–2020)

Frans van Houten's Vision

François Adrianus "Frans" van Houten (born 26 April 1960) is a Dutch businessman. He was the CEO of Royal Philips Electronics from April 2011 to October 2022.

The son of a member of the board of directors of Philips, Frans van Houten studied Economics at Erasmus University Rotterdam, and started his career at Philips in 1986 in marketing and sales at Philips Data Systems. He held several positions in the company, becoming co-head of the consumer electronics division in 2002. In November 2004, he became CEO of Philips Semiconductors, where he led the spin-off of the division, resulting in the formation of NXP Semiconductors on 1 October 2006.

Van Houten's background was uniquely suited to the transformation ahead. He had led the NXP spinoff, proving he could execute a complex divestiture. On 8 July 2010, van Houten was nominated to succeed Gerard Kleisterlee as CEO of Philips in order to focus more on healthcare. Since then, he and his team drove the transformation and revitalization of the Philips portfolio to become a focused health technology company through targeted divestment, acquisition and organic business development.

In his role as CEO, he transformed the organisation from a diversified conglomerate into a focused health technology solutions company. This transformation doubled Philips' organic growth and profitability.

Led the transformation of Philips from a diversified conglomerate into a focused health technology solutions company, separating and divesting TV, Audio/Video, Lighting, Domestic Appliances and Lumileds. Highlights: Radically transformation of the portfolio: Divested ~€12B revenue to PE and through IPO, and used the proceeds for 30+ targeted Health-Tech acquisitions.

The strategic logic was clear: Philips sold its first light bulb a few years after it was founded in 1891, but for the past dozen years had increasingly shifted its focus on medical equipment, which now accounts for more than 40% of sales. Philips said it was making the move into medical technology where margins are strong and less vulnerable to competition from emerging markets.

Key Divestitures & Acquisitions

"Today's announcement is a historic one for Philips as we aim to separate our company into two market-leading companies focused on capturing opportunities in the health technology and connected LED lighting solutions markets respectively," Philips chief executive Frans van Houten said in the statement.

In February 2015, Philips acquired Volcano Corporation to strengthen its position in non-invasive surgery and imaging.

Signify N.V., formerly known as Philips Lighting N.V., is a Dutch multinational lighting corporation formed in 2016 as a result of the spin-off of the lighting division of Philips, by means of an IPO.

On May 27, 2016, Philips Lighting was listed and started trading on Euronext in Amsterdam under the ticker "LIGHT". On May 31, 2016, the closing and settlement of the offering and the start of unconditional trading were announced.

The lighting business was valued at $3.4 billion by the offer, and a 25 percent stake was put on the Euronext stock exchange. Shares were priced at €20, or a little over $22, ahead of the IPO.

In March 2018, Philips Lighting announced that the company would change its name to Signify, which became effective on 16 May 2018.

In 2021, Philips sold their Domestic Appliances business to Hillhouse Investment, a Chinese private-equity firm controlled by entrepreneur Zhang Lei, for €3.7 billion (US$4.37 billion). As part of the deal, the new company received the right to use the Philips brand name for consumer electronics for a period of 15 years following the deal, at an estimated cost of €700 million over that time period.

Philips received cash proceeds after tax and transaction-related costs of approximately EUR 3 billion. The transaction values Domestic Appliances, a global leader with EUR 2.2 billion sales in 2020 in kitchen, coffee, garment care and home care appliances, at an enterprise value of approximately EUR 3.7 billion. The total deal value amounts to approximately EUR 4.4 billion resulting from an additional 15-year brand license agreement with annual payments that represent an estimated net present value of approximately EUR 0.7 billion.

In 2023, the company was rebranded as Versuni.

The New Philips: Healthcare Technology

The transformation was comprehensive. As of 2024, Philips is organized into three main divisions: Diagnosis and Treatment (manufacturing healthcare products such as MRI, CT and ultrasound scanners), Connected Care (manufacturing patient monitors, as well as respiratory care products under the Respironics brand), and Personal Health (manufacturing electric shavers, Sonicare electric toothbrushes and Avent childcare products).

The Agnelli family's Exor NV bought a minority stake in Koninklijke Philips NV, a vote of confidence for the troubled Dutch medical company as it grapples with a costly product recall. Exor bought a 15% holding in Philips through on-market share purchases and an agreement with a major financial institution, according to a statement Monday. The deal is valued around €2.6 billion ($2.8 billion).

Exor amassed a 15% stake in Philips in 2023 as it began diversifying into healthcare, technology, financial services and luxury goods. The deal gave Exor the ability to increase its stake in the maker of ventilators and cardiographs to 20%.

The investment holding company Exor NV, controlled by the Agnelli family, has further increased its influence over Philips. According to a document submitted to the Securities and Exchange Commission (SEC) in the USA, Exor now holds 18.7% of the Dutch health technology giant's capital.

VII. The Respironics Recall: Catastrophe & Crisis (2021–Present)

The Recall

In June 2021, after discovering a potential health risk related to the foam in certain CPAP, BiPAP and Mechanical Ventilator devices, Philips Respironics issued a voluntary Field Safety Notice (outside U.S.) / voluntary recall notification (U.S. only).

The recalled devices were produced over the last decade. The goal was to "ensure patient safety" because of risk of exposure to particulates released from polyester-based polyurethane sound abatement foam and off-gassing of potentially toxic or carcinogenic concentrations of volatile organic compounds (VOCs).

The consent decree came after Philips recalled certain ventilators, CPAP machines, and BiPAP machines in June 2021 because of potential health risks—impacting 15 million devices worldwide.

In the years prior to 2021, complaints related to possible PE-PUR foam degradation were investigated, evaluated, and addressed by Philips Respironics primarily on a case-by-case basis. When Philips became aware of the issue and its potential significance in early 2021, Philips and Philips Respironics took actions that led to the voluntary recall.

The Fallout

Since April 2021, the FDA has received more than 116,000 MDRs [Medical Device Reports], including 561 reports of death that were either reported or suspected to be related to problems with insulating foam in the Philips devices, the FDA said earlier this year.

Philips did not admit liability, wrongdoing or fault in the settlement. Between 2010 and 2021, Philips withheld the vast majority of the warnings about black particles, dirt, dust and other contaminants in devices' airway chambers from the FDA even as the reports became more alarming each year, according to investigation.

Under the terms of this decree, Philips' Respironics must halt the production of most sleep and respiratory devices at three of its facilities located in Pennsylvania. This directive will remain in effect until Philips meets the specific requirements set out in the consent decree. So the company is prohibited from selling new CPAP, BiPAP, or other respiratory care devices within the U.S.

Leadership Change & Settlement

Roy Jakobs was appointed CEO of Philips in October 2022, taking the helm during a challenging period following a major product recall of its breathing machines, including hospital ventilators. "It had to be crystal clear from the moment I took charge that for me, safety was the number one priority," Jakobs told Fortune.

On 16 August 2022, Philips announced that they had parted ways with van Houten due to a mass product recall of Philips Respironics CPAP devices that halved the company's stocks and would further reduce it below the value it had prior to his appointment as CEO.

Current role: CEO Royal Philips. Since: 2022. Nationality: Dutch and German. His track record over the last 25 years reflects his passion to help address wider societal challenges. He has driven (digital) transformations in energy, scientific information publishing, and health technology in multinational companies.

Since joining Philips in 2010, other positions he has held include Business Leader of Domestic Appliances, based in Shanghai, Market Leader for Philips Middle East & Turkey and Chief Marketing Officer for Philips Lighting. Prior to his career at Philips, he held various management positions at Royal Dutch Shell in their retail businesses and at Reed Elsevier, where he transformed the business from print to digital as Managing Director.

Philips Respironics reached a $1.1 billion settlement over CPAP lawsuits on April 29, 2024. Of that, $1.075 billion would go toward personal injury claims that its devices caused serious complications or death.

Most of the related payments are expected in 2025 and to be funded from cash on hand. On December 5, 2024, the Court granted final approval of the medical monitoring class action settlement.

Globally, Philips has remediated 99% of actionable sleep therapy device registrations to date.

VIII. Recovery & Current State (2024–2025)

"We delivered better care for more people by enhancing execution and focusing on driving improvements in profitability and cash flow, as well as order and sales growth," stated CEO Roy Jakobs.

Sales of EUR 18.0 billion in 2024, comparable sales growth 1%; EUR 5.0 billion in Q4, comparable sales growth 1%, despite double-digit decline in China. Comparable order intake increased 1% in 2024; up 2% in Q4, despite double-digit decline in China. Income from operations was EUR 529 million in 2024; EUR 199 million in Q4. Adjusted EBITA margin increased 90 basis points to 11.5% of sales in 2024; up 60 basis points to 13.5% in Q4.

Net cash flow from operating activities was EUR 1,569 million in 2024; EUR 1,459 million in Q4. Free cash flow was EUR 906 million in 2024; EUR 1,285 million in Q4. Finalized Philips Respironics recall-related medical monitoring and personal injury settlements in US. Proposed dividend maintained at EUR 0.85 per share. Increased productivity savings target for 2023-2025 from EUR 2 billion to EUR 2.5 billion, EUR 800 million in 2025.

Since 2023, productivity initiatives have delivered savings of more than EUR 1.7 billion. Philips raised its productivity savings target for the 2023-2025 period from EUR 2 billion to EUR 2.5 billion, driven by cost efficiencies and further simplification of its operating model.

For 2025, Philips expects: 1%-3% comparable sales growth, including a mid- to high-single-digit decline in China. Adjusted EBITA margin increasing 30-80 bps to 11.8%-12.3%. Free cash flow before payment of the USD 1.1 billion cash-out relating to the US medical monitoring and personal injury settlements will be at the lower end of the range of EUR 1.4 billion to EUR 1.6 billion.

Before we conclude, I would like to share that we will host a Capital Markets Day next February. The event will mark the completion of the three-year plan I launched when I became CEO. It will provide an opportunity to reflect on the fundamental progress we have been delivering since.

The China challenge remains significant. The Amsterdam-based tech manufacturer has been blindsided by an anti-corruption campaign across China's healthcare sector after the Asian nation began to scrutinise local medical-technology procurement.

IX. Playbook: Business & Investing Lessons

Innovation vs. Commercialization

Philips invented or co-invented cassettes, CDs, VCRs, and more—yet often failed to capture full economic value. The cassette tape licensing decision prioritized market adoption over royalties, which made strategic sense. But the pattern repeated: breakthrough innovation followed by value capture by others.

The importance of standards partnerships cannot be overstated. The Sony collaboration on the CD was masterful—learned from the VCR format war. Two competitors agreed on a standard, divided the technology contributions, and jointly conquered the market. In an era of proprietary ecosystems, this cooperative approach seems almost quaint.

The Nat Lab's R&D culture prioritized quality over speed-to-market. This produced Nobel Prize-winning science but often left commercial opportunities for faster-moving competitors.

Conglomerate to Pure-Play Transformation

The 25-year journey from diversified electronics giant to focused healthcare company offers several lessons:

Strategic Divestitures: Philips divested lighting (Signify), TVs (TP Vision), appliances (Versuni), and semiconductors (NXP). Each transaction required careful execution to maximize value while managing brand licensing arrangements.

Capital Allocation Discipline: The proceeds from divestitures funded healthcare acquisitions. Van Houten's team made 30+ targeted health-tech acquisitions while divesting €12 billion in non-core revenue.

Shrinking to Grow: Sometimes the path to value creation runs through contraction. Philips became more valuable by becoming smaller and more focused.

Crisis Management & Quality Culture

The Respironics recall offers a case study in what happens when quality systems fail in a healthcare company:

- Complaints about foam degradation existed for years before the recall

- The company investigated on a "case-by-case basis" rather than recognizing a systemic issue

- When the recall came, it affected 15 million devices globally

- The FDA consent decree effectively shut down U.S. respiratory device production

The importance of MDR (Medical Device Report) monitoring and regulatory relationships cannot be understated. In healthcare, quality culture isn't a nice-to-have; it's existential.

Family Dynasty to Professional Management

Members of the Philips family led the company until 1977 and maintained great influence well into the 1980s. The transition from dynastic to professional management brought both opportunities and challenges.

The paternalistic culture—housing, schools, healthcare for workers—created loyalty but also complacency. Professional managers brought financial discipline but sometimes lacked the long-term perspective that family ownership provides.

X. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's 5 Forces Analysis

Threat of New Entrants: Low-Medium

Healthcare equipment requires massive capital investment, regulatory expertise, and clinical validation. FDA approval processes create years-long barriers for new entrants. However, Chinese competitors like Mindray and United Imaging are emerging with lower cost structures and government support.

Supplier Power: Medium

Philips depends on specialized components, including semiconductors where supply chain disruptions have been severe. The company partners with foundries like TSMC for production flexibility. The 2020-2023 chip shortage demonstrated supplier vulnerability.

Buyer Power: High

Hospital systems and Group Purchasing Organizations (GPOs) have significant bargaining power. Government healthcare budgets increasingly constrain spending. Single-payer systems in many countries negotiate aggressively on price.

Threat of Substitutes: Low-Medium

Imaging and monitoring are essential; there's no substitute for an MRI scan when needed. However, AI-enabled diagnostics could eventually reduce the need for some imaging procedures. Point-of-care devices could substitute for some hospital-based equipment.

Competitive Rivalry: High

Siemens Healthineers operates in a highly competitive landscape, with key players such as GE Healthcare, Philips Healthcare, and Canon Medical Systems leading the charge. These competitors showcase varying sizes, revenues, and strengths across medical imaging and health technologies.

Siemens Healthineers AG held the highest market share in Diagnostic Imaging (North America) in 2023 with a share of 43.09%.

Siemens Healthineers dominates with revenues exceeding $23.4 billion, largely attributed to its imaging and diagnostics segments. Philips Healthcare represents a significant portion of the market, with 42% of its revenue derived from healthcare services.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Moderate. Healthcare equipment manufacturing benefits from scale, but isn't as scale-dependent as semiconductors. Philips' ~EUR 18 billion revenue provides meaningful scale advantages in R&D amortization.

Network Effects: Limited. Unlike software platforms, medical equipment doesn't become more valuable as more hospitals use it. However, installed base matters for consumables and service contracts.

Counter-Positioning: Weak currently. Philips' healthcare-only positioning was distinctive in 2015; now all major competitors have similar focus. The company hasn't found a strategic position that incumbents can't or won't match.

Switching Costs: Moderate-High. Hospital systems invest heavily in training staff on specific equipment. IT integration with hospital systems creates stickiness. Long service contracts lock in relationships.

Branding: Strong in some segments. The Philips brand carries positive associations in personal health (Sonicare, Norelco). In professional healthcare, brand matters less than clinical outcomes and TCO.

Cornered Resource: Limited. Philips doesn't control a unique resource that competitors cannot access. Patents provide some protection, but the patent landscape in medical devices is complex.

Process Power: Under rebuilding. The Respironics recall suggests Philips' quality processes failed. Rebuilding process power—the ability to consistently manufacture safe, effective devices—is management's primary focus.

Competitive Positioning

Philips Healthcare offers a broad portfolio, including diagnostic imaging, image-guided therapy, and connected care solutions. This positions Philips as a strong competitor, especially in cardiology and patient monitoring. Philips' 2023 sales reached approximately EUR 18.5 billion, demonstrating its substantial footprint in the healthcare technology sector.

Philips is the smallest of the "Big Three" medical imaging companies (behind Siemens Healthineers and GE Healthcare). This creates both challenges (less scale) and opportunities (more focused).

XI. Key KPIs to Track

For fundamental investors, three metrics deserve close monitoring:

1. Comparable Order Intake Growth This leading indicator reveals demand trends before they appear in revenue. Comparable order intake increased 1% in 2024; up 2% in Q4, despite double-digit decline in China. Order intake is particularly important in a lumpy business where large hospital contracts can swing quarterly results.

2. Adjusted EBITA Margin Adjusted EBITA margin increased 90 basis points to 11.5% of sales in 2024. This margin remains below pre-recall levels and below competitors. The target of 11.8%-12.3% for 2025 still trails Siemens Healthineers' profitability. Margin expansion indicates whether the transformation is creating a more profitable business model.

3. China Revenue Trend China has swung from a growth driver to a drag on results. The anti-corruption campaign in healthcare and broader economic challenges have created "double-digit declines." China recovery—or further deterioration—will significantly impact overall results.

XII. Bull Case vs. Bear Case

Bull Case

Transformation Complete: Philips has shed its conglomerate past and is now a focused healthcare technology company. The EUR 1.1 billion Respironics settlement removes a major overhang. The Exor investment from the Agnelli family signals sophisticated investor confidence.

Valuation Gap: At current levels, Philips trades at a significant discount to Siemens Healthineers and GE Healthcare. If the company can approach competitor margins and rebuild its respiratory business, substantial revaluation is possible.

Healthcare Secular Tailwinds: Aging populations, rising chronic disease, and healthcare system capacity constraints create sustained demand for diagnostic imaging, patient monitoring, and connected care solutions. AI integration could enhance productivity and create new revenue streams.

Cost Actions Taking Hold: Productivity initiatives have delivered EUR 1.7 billion in savings since 2023, with EUR 800 million more targeted for 2025. Operating leverage should improve as sales recover.

Bear Case

Quality Concerns Linger: The Respironics recall exposed systemic quality failures. Rebuilding trust with regulators, clinicians, and patients takes years. A second quality issue could be catastrophic.

China Structural Challenge: The China market may not recover to previous growth rates. Government procurement practices, anti-corruption campaigns, and local competitor preferences could permanently impair the China business.

Competitive Position Weakening: Siemens Healthineers and GE Healthcare have greater scale, higher margins, and stronger market positions in key imaging segments. Philips may be caught in a middle position—too small to compete on scale, unable to differentiate sufficiently on innovation.

DOJ Investigation Ongoing: The Q3 and full-year 2025 outlook excludes potential wider economic impact and the ongoing Philips Respironics-related proceedings, including the investigation by the U.S. Department of Justice. The DOJ investigation remains unresolved and could result in additional financial penalties or operational restrictions.

XIII. Myth vs. Reality

| Myth | Reality |

|---|---|

| Philips invented the CD | Philips co-invented the CD with Sony. Philips coined the term compact disc and contributed the manufacturing process. Sony contributed error-correction technology. |

| Philips missed the semiconductor opportunity | Philips owned 28% of TSMC at its 1994 IPO and closer to 70% of ASML at its 1995 IPO. They captured early returns but exited before the exponential growth. |

| Healthcare is "new" for Philips | Philips introduced its first medical X-ray tube in 1918. Healthcare has been part of the portfolio for over a century. |

| The Respironics recall was a "surprise" | Complaints about foam degradation existed for years. The recall reflected failure to recognize systemic issues, not sudden discovery of a problem. |

| Philips is primarily a consumer company | 42% of Philips' revenue derives from healthcare services. Consumer products (Personal Health) are now a minority of the business. |

XIV. Conclusion: The Reinvention Continues

Royal Philips stands at another inflection point in its 130+ year history. The company has successfully completed the most dramatic corporate transformation in Dutch business history—from diversified electronics conglomerate to focused healthcare technology company. It has navigated a catastrophic product recall that might have sunk a less resilient organization. It has attracted sophisticated long-term investors in the Agnelli family. And it operates in a sector with strong secular tailwinds.

Yet challenges remain formidable. China weakness persists. Margins lag competitors. The DOJ investigation hangs unresolved. Rebuilding quality culture and regulatory trust takes years, not quarters.

The Philips story offers enduring lessons for business strategists and investors alike. Technical excellence without commercial execution creates ephemeral advantage. Conglomerate diversification no longer protects against disruption—focus does. Quality culture in healthcare isn't optional—it's existential. And corporate transformations, even successful ones, generate volatility that tests investor patience.

For those tracking Philips' ongoing recovery, order intake growth reveals demand trends before revenue; EBITA margin expansion demonstrates operating leverage; and China performance indicates whether the toughest market is stabilizing or deteriorating further.

The light bulb company that became a conglomerate that became a healthcare company continues reinventing itself. Whether this latest version creates lasting shareholder value remains the central question—and opportunity—for investors in the years ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube