Seagate Technology: From Disk Drive Pioneer to Data Infrastructure Giant

I. Introduction & Episode Roadmap

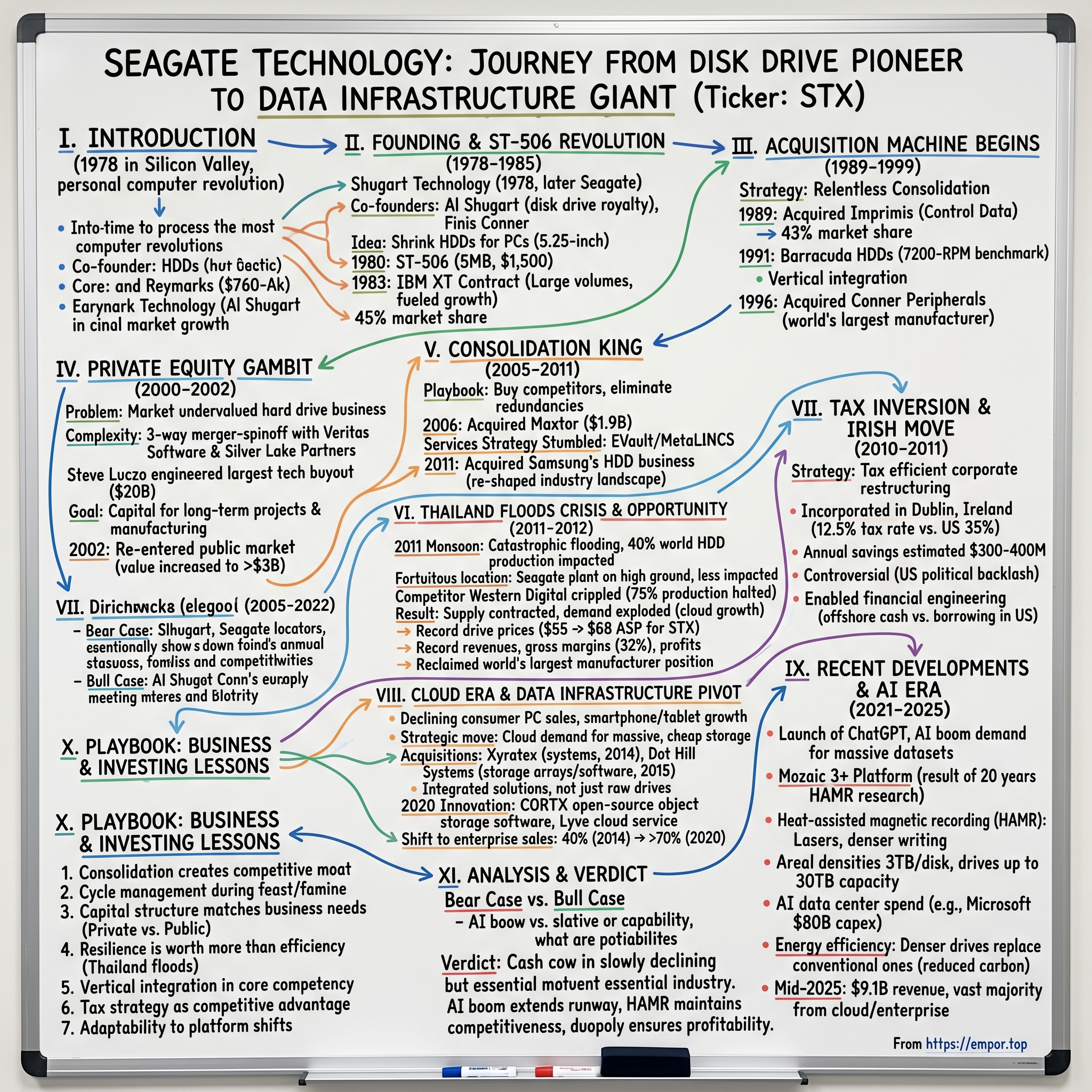

Picture this: It's 1978 in Silicon Valley, and the personal computer revolution is just beginning to stir. In a nondescript office in Scotts Valley, California, five engineers are about to launch a company that would outlive 216 of its 218 competitors in the hard drive industry. Today, Seagate, along with its competitor Western Digital, dominates the HDD market, controlling a duopoly that stores the vast majority of humanity's digital existence.

But here's the remarkable part—while tech giants like IBM, Hewlett-Packard, and Quantum have long abandoned the hard drive business, Seagate not only survived but thrived through every platform shift from mainframes to PCs to cloud to AI. How did a company selling mechanical spinning disks—essentially 1950s technology with incremental improvements—become indispensable to the AI revolution of 2025?

The answer lies in a playbook of relentless consolidation, strategic financial engineering, and a willingness to make contrarian bets when others retreated. This is the story of how Seagate Technology transformed from a scrappy startup making 5-megabyte drives into a $9 billion revenue giant shipping over one million Mozaic hard drives powered by heat-assisted magnetic recording to the world's hyperscalers.

Three themes will guide our journey through Seagate's 46-year saga: First, how aggressive M&A can create a competitive moat in a commoditized industry. Second, why going private at the right moment can unlock trapped value. And third, how surviving industry catastrophes—from natural disasters to technology disruptions—can actually strengthen market position.

Seagate Technology Holdings plc is an American data storage company. It was incorporated in 1978 as Shugart Technology and commenced business in 1979.Since 2010, the company has been incorporated in Dublin, Ireland, with operational headquarters in Fremont, California, United States.

II. Founding Story & The ST-506 Revolution (1978–1985)

The rain had just stopped in Los Gatos when Finis Conner knocked on Al Shugart's door in 1978. Shugart, who had been unceremoniously fired from his own company (Shugart Associates) after Xerox acquired it, was consulting and perhaps contemplating retirement. But Conner had other plans. He carried with him a vision that seemed almost laughable at the time: What if they could shrink hard drives down to fit inside personal computers?

Seagate Technology (then called Shugart Technology) was incorporated on November 1, 1978, and commenced operations with co-founders Al Shugart, Tom Mitchell, Doug Mahon, Finis Conner, and Syed Iftikar in October 1979. The company came into being when Conner approached Shugart with the idea of starting a new company to develop 5.25-inch HDDs which Conner predicted would be a coming economic boom in the disk drive market.

Al Shugart wasn't just any engineer—he was disk drive royalty. He began his career in 1951 as a field engineer at IBM. In 1955, he transferred to the IBM San Jose laboratory where he worked on the IBM 305 RAMAC. After 18 years at IBM, he'd moved to Memorex, then founded Shugart Associates, pioneering the floppy disk drive that became standard on personal computers. Now, at 48, he was about to start his most important venture.

The name was changed to Seagate Technology to avoid a lawsuit from Xerox's subsidiary Shugart Associates (also founded by Shugart). The irony wasn't lost on anyone—Shugart couldn't even use his own name for his new company.

The team worked furiously through 1979, and by 1980, they had done it. The company's first product, the ST-506, with a storage capacity of 5 megabytes (MB), was released in 1980. It was the first hard disk to fit the 5.25-inch form factor of the Shugart mini-floppy drive. To understand the audacity of this achievement, consider that existing hard drives were the size of washing machines and cost tens of thousands of dollars. The ST-506 was priced at $1,500—still expensive, but suddenly accessible.

The real breakthrough came in 1983. IBM was developing its new personal computer, the XT, and needed a hard drive supplier. They were a major supplier in the microcomputer market during the 1980s, especially after the introduction of the IBM XT in 1983. With this, Seagate secured a contract as a major OEM supplier for the IBM XT, IBM's first personal computer to contain a hard disk. The large volumes of units sold to IBM fueled Seagate's early growth.

The numbers tell the story of explosive growth: In their first year, Seagate shipped $10 million worth of units to consumers. By 1983, the company shipped over 200,000 units for revenues of $110 million. By this point, the company had a 45% market share of the single-user hard drive market, with IBM purchasing 60% of the total business Seagate was doing at the time.

But success brought its own challenges. In 1983, Al Shugart was replaced as president by then chief operating officer, Tom Mitchell, in order to move forward with corporate restructuring in the face of a changing market. The founder was being pushed aside, a pattern that would repeat throughout Seagate's history—bringing in operational expertise when growth demanded it, then returning to visionaries when innovation was needed.

By 1984 sales had shot up to $344 million as Seagate became the world's largest producer of 5.25-inch disk drives, with three-fourths of the company's shipments going to IBM. The ST-506 interface had become the de facto standard, cementing Seagate's position as the architectural leader of the PC storage industry. They had cracked the code: make drives smaller, cheaper, and in massive volumes.

III. The Acquisition Machine Begins (1989–1999)

The late 1980s brought Seagate to a crossroads. The company had conquered the PC hard drive market, but Tom Mitchell saw storm clouds gathering. Asian manufacturers were entering the market with lower costs, and the industry was fragmenting into dozens of competitors. Mitchell's solution was audacious: if you can't beat them on cost, buy them entirely.

In 1989, Seagate acquired Control Data Corporation's Imprimis division, the makers of CDC's HDD products, resulting in a combined market share of 43%. Seagate benefited from Imprimis' head technology and reputation while Imprimis gained access to Seagate's lower component and manufacturing costs. This wasn't just an acquisition—it was a blueprint for the next decade.

The Imprimis deal taught Seagate a crucial lesson: in a scale business, consolidation creates exponential advantages. Every competitor absorbed meant better supplier terms, eliminated price competition, and acquired new technologies. It was financial engineering meets industrial logic.

But the real masterstroke came with the return of Al Shugart. In September 1991, Tom Mitchell resigned as president under pressure from the board of directors, with Al Shugart reassuming presidency of the company. The founder was back, and he had learned from his first stint. Shugart refocused the company on its more lucrative markets, and on mainframe drives instead of external drives. He also pulled away from outsourcing component production overseas. This allowed Seagate to better keep up with demand for PCs, which increased extremely rapidly in 1993 across the market.

Shugart also launched one of Seagate's most successful product lines ever: the Barracuda hard drive, introduced in 1991. With a 7200-RPM spindle speed, it was the fastest hard drive ever made. The Barracuda would become to hard drives what the Porsche 911 was to sports cars—the performance benchmark everyone else chased.

In 1994, Seagate Technology Inc moved from the Nasdaq stock exchange to the New York Stock Exchange, trading under the ticker symbol SEG. The symbolism was clear: Seagate had graduated from startup to establishment.

The crescendo of this acquisition symphony came in 1996. In 1996, Luczo led the Seagate acquisition of Conner Peripherals, creating the world's largest disk drive manufacturer and completing the company's strategy of vertical integration and ownership of key disk drive components. After ten years as an independent company, Conner Peripherals was acquired by Seagate in a 1996 merger. The irony was delicious—Finis Conner, who had co-founded Seagate only to leave and start a rival, was now being bought back into the fold.

Innovation continued alongside consolidation. In 1996, Seagate introduced the industry's first hard disk with a 10,000 RPM spindle speed, the Cheetah 4LP. By 2000, they had pushed this to 15,000 RPM—drives spinning so fast they required special mounting to prevent vibration from affecting nearby components.

The decade closed with a leadership transition that would prove pivotal. In 1997, Seagate experienced a downturn, along with the rest of the industry. In July 1998, Shugart resigned his positions with the company. Stephen J. "Steve" Luczo became the new chief executive officer, also joining the board of directors.

Steve Luczo wasn't your typical tech CEO. Luczo joined Seagate Technology in October 1993 as Senior Vice President of Corporate Development. In March 1995, he was appointed Executive Vice President of Corporate Development and chief operating officer of Seagate Software Holdings. He thought like an investment banker (which he had been at Morgan Stanley) trapped in the body of an operations executive. And he was about to engineer one of the most complex financial transactions in tech history.

IV. The Private Equity Gambit (2000–2002)

By late 1999, Steve Luczo faced an infuriating paradox. Seagate sold its Network & Storage Management Group (NSMG) to Veritas Software in return for 155 million shares of Veritas' stock. With this deal, Seagate became the largest shareholder in Veritas, with an ownership stake of more than 40%. As the dot-com bubble inflated, Veritas stock soared 200% while Seagate's rose just 25%. The goal of the deal was to unlock the value of the 33% ownership stake Seagate had in Veritas, which had put the value of Seagate's stock at around $33 billion even though its market cap was only $15 billion.

The market was essentially saying that Seagate's actual hard drive business had negative value. Wall Street was so obsessed with software that it couldn't see the value in the company that stored all that software's data.

Luczo led a management buyout of Seagate, believing that Seagate needed to make significant capital investments to achieve its goals. He decided to turn the company private, since disk drive producers had a hard time obtaining capital for long-term projects. But this wouldn't be a simple buyout—it would be a three-dimensional chess move involving private equity, tax optimization, and corporate restructuring.

In early November 1999, Morgan Stanley arranged a meeting between Seagate executives and representatives of Silver Lake Partners to discuss a major restructuring of Seagate. Silver Lake wasn't just any PE firm—they were the pioneers of large-scale tech buyouts, and they saw what Luczo saw: a fundamentally sound business trapped in a bad capital structure.

On November 22, 2000, Seagate management, Veritas Software, and an investor group led by Silver Lake closed a complex deal that privatized Seagate. At the time, this was the largest buyout ever of a technology company. The total deal, worth about $20 billion, included the sale of its disk-drive operations for $2 billion to an investor group led by Silver Lake Partners.

The mechanics were breathtaking in their complexity. In 2000, the company was taken private by an investment group composed of Seagate management, Silver Lake Partners, Texas Pacific Group, and others in a three-way merger-spinoff with Veritas Software; Veritas merged with Seagate, which was bought by the investment group. Veritas was then immediately spun off to shareholders, gaining rights to Seagate Software Network and Storage Management Group (with products such as Backup Exec), as well as Seagate's shares in SanDisk and Dragon Systems.

The benefits of going private were immediate. Free from quarterly earnings pressure, Seagate could make long-term investments in manufacturing and R&D. They could restructure operations without activist investors second-guessing every decision. Both the Stanford Graduate School of Business and the Harvard Business School have written multiple case studies on the Seagate buyout and turnaround. In addition, several leading management books cite the Seagate turnaround.

Just two years later, the transformation was complete. In December 2002, Seagate re-entered the public market on the Nasdaq as STX. The company that went private at a $2 billion valuation came public again at over $3 billion. Silver Lake and the management team had nearly doubled their money in 24 months, while completely restructuring the business.

But the real winner was Luczo, who had engineered the entire transaction. Luczo became the chairman of the board of directors of Seagate Technology on June 19, 2002. He had taken the company private, fixed its problems, brought it public again, and emerged as both CEO and chairman. It was a masterclass in financial engineering that would become required reading at business schools.

V. Consolidation King: The Maxtor & Samsung Acquisitions (2005–2011)

Fresh from its successful return to public markets, Seagate under Luczo embarked on an acquisition spree that would reshape the entire hard drive industry. The playbook was simple but brutal: buy competitors, integrate their technology, eliminate redundancies, and dominate pricing.

The crown jewel came in 2006. In 2006, Seagate acquired Maxtor in an all-stock deal worth $1.9 billion and continued to market the separate Maxtor brand. Maxtor wasn't just another competitor—they were the number three player in the industry, with strong retail presence and a loyal customer base. Overnight, Seagate had eliminated a major price competitor and gained significant manufacturing capacity.

But Luczo had bigger ambitions than just hard drives. He envisioned Seagate as a complete data management company. The following year, Seagate acquired EVault and MetaLINCS, later rebranded as i365. EVault was particularly interesting—a cloud backup service before "cloud" was even a buzzword. Seagate paid $185 million for EVault, betting that online backup would become essential for businesses.

The bet didn't pay off as expected. Years later, Seagate would sell EVault to Carbonite for just $14 million—a $171 million loss that showed the dangers of straying too far from core competencies. Hardware companies trying to become software companies rarely succeeded, a lesson Seagate learned expensively.

But while the services strategy stumbled, the consolidation strategy soared. The masterstroke came in December 2011. Seagate acquired Samsung's HDD business in 2011, reshaping the entire industry landscape. After this deal, only three major hard drive manufacturers remained: Seagate, Western Digital, and Toshiba.

The Samsung acquisition was particularly elegant. Rather than paying cash, Seagate essentially traded market share for technology and capacity. Samsung got out of a business with declining margins, while Seagate gained Samsung's advanced technology and the right to use the Samsung brand on HDDs for five years.

The timing proved perfect. Just months before the acquisition closed, Thailand—where much of the world's hard drive manufacturing occurred—experienced catastrophic flooding. While competitors struggled, Seagate's expanded capacity from the Samsung deal helped it meet surging demand. By June 2012, Seagate had achieved record revenues, record gross margins, and record profits, reclaiming its position as the world's largest disk drive manufacturer.

The lesson was clear: in a commodity business, scale is everything. Every acquisition didn't just add revenue—it eliminated a competitor, improved supplier leverage, and created pricing power. Luczo had transformed Seagate from a manufacturer into a consolidator, from a competitor into a category king.

VI. The Thailand Floods Crisis & Opportunity (2011–2012)

October 15, 2011. Tawan Suppapunt, managing director at Western Digital's Bang Pa-In factory, watches helplessly as brown water rises past the sandbag barriers his workers had desperately stacked. The line marks the high-water point—1.8 meters from the ground—of the October 2011 flood that devastated this part of southern Thailand. Within hours, billions of dollars of precision manufacturing equipment would be submerged in muddy water.

Severe flooding occurred during the 2011 monsoon season in Thailand. The flooding began at the end of July triggered by the landfall of Tropical Storm Nock-ten. These floods soon spread through the provinces of northern, northeastern, and central Thailand along the Mekong and Chao Phraya river basins. In October floodwaters reached the mouth of the Chao Phraya and inundated parts of the capital city of Bangkok.

For the global technology industry, this wasn't just a natural disaster—it was a supply chain catastrophe. Thailand assembles about 40 percent of the world's hard drives, and if you account for drive component manufacturing, it's the global leader, according to Fang Zhang, a storage analyst at market research firm IHS iSuppli. Thailand is the world's second-largest producer of hard disk drives, supplying approximately 25 percent of the world's production. Many of the factories that made hard disk drives were flooded, including Western Digital's, leading some industry analysts to predict future worldwide shortages of hard disk drives.

But here's where geography became destiny. Seagate owes its return to market leadership to a fortuitous accident in geography: Its HDD manufacturing plant in Thailand is located on high ground. As a result, the company was less impacted by the October floods—the most destructive in the last 50 years for the Southeast Asian country. While Western Digital's facilities sat in the flood plain, Seagate's main facility was literally built on higher ground.

Unlike Western Digital, which according to estimates saw about 75% of its production temporarily shut down, Seagate suffered relatively minimally. Western Digital's manufacturing facility was severely damaged and 75% of its production capacity was halted, further crippled by flooded roads and infrastructure, while Seagate kept running.

The market impact was immediate and dramatic. In the last quarter of 2011, all five major HDD manufacturers shipped significantly fewer HDDs, down 30% from the previous quarter—123.3 million units in the fourth quarter compared with 175.2 million units in the third quarter. Supply contracted just as demand was exploding from cloud computing growth.

This created an extraordinary pricing environment. Seagate's average drive selling price surged from $55 in the third quarter to $68 in the fourth quarter of 2011, a strong 24% increase. Western Digital's average drive sales price shot up to $69, up from $46, during the same period. For context, in the hard drive industry, a 5% price increase in a quarter was considered exceptional. This was unprecedented.

The market share shift was even more dramatic. Seagate passed former market leader Western Digital Corp., which suffered heavy losses in the devastating Thailand floods last year. Seagate claimed 38% of HDD market share, compared with Western Digital's 23%. In the fourth quarter of 2011, Seagate shipped 46.9 million HDD units worldwide, compared to 28.5 million for archrival Western Digital.

Both Seagate and Western Digital saw their gross margins rise to record highs in the fourth quarter, due to across-the-board drive price increases in the wake of the flood-related shortages. Seagate's gross margins hit 32%—for a company that typically operated at 22-26% margins, this was extraordinary.

The ethical questions were unavoidable. Should Seagate have moderated price increases to help customers? Should they have shared capacity with competitors? Luczo's answer was brutally capitalistic: Seagate had invested in geographic diversification, maintained higher inventory levels, and built facilities on higher ground. These weren't lucky accidents—they were strategic choices that cost money. The windfall profits were the return on those investments.

By mid-2012, Western Digital had recovered and rebuilt, but the damage was done. By the second quarter of 2012, Western Digital held 45% HDD market share, Seagate 42%, and Toshiba 13%. While WD reclaimed the top spot, the industry had fundamentally changed. The flood had accelerated consolidation, eliminated marginal players, and proven that in the hard drive industry, manufacturing resilience was as important as technological innovation.

The Thailand floods revealed a truth about modern technology: for all our talk of cloud computing and virtual everything, the physical world still matters. Data lives on spinning disks in factories that can flood, supply chains that can break, and geography that can determine corporate destinies. Seagate had won not through innovation but through elevation—sometimes the oldest strategies are the best.

VII. The Tax Inversion & Irish Move (2010–2011)

While Seagate was navigating floods in Thailand, it was engineering an entirely different kind of maneuver in the corporate boardroom—a tax strategy that would save hundreds of millions of dollars and spark international controversy.

In 2000, Seagate incorporated in the Cayman Islands in order to reduce income taxes. This was already aggressive, but by 2010, even the Cayman Islands wasn't tax-efficient enough. The solution? Ireland—the emerald isle that had become the tax haven of choice for American technology companies.

Since 2010, the company has been incorporated in Dublin, Ireland, with operational headquarters in Fremont, California, United States. The mechanics were elegant: Seagate would maintain all its actual operations in the United States and Asia, but legally exist in Ireland where the corporate tax rate was 12.5% versus America's 35%.

The numbers made the controversy worthwhile. By incorporating in Ireland, Seagate could save an estimated $300-400 million annually in taxes—money that could be reinvested in R&D, returned to shareholders, or used for acquisitions. For a company operating on single-digit net margins, this was transformative.

The strategy was particularly powerful when combined with Seagate's global manufacturing footprint. Products made in Thailand, sold to customers in China, and invoiced through Ireland might never touch American soil—or American taxes. It was globalization weaponized for tax efficiency.

But the political backlash was swift. Senator Carl Levin called out Seagate specifically in Congressional hearings on tax inversions, arguing that companies shouldn't be able to enjoy the benefits of American infrastructure, education, and legal systems while avoiding American taxes. The Obama administration proposed regulations to stop inversions, though by then Seagate had already moved.

Western Digital, Seagate's main rival, remained a U.S. corporation throughout this period. This created an interesting competitive dynamic: Seagate had lower taxes but faced political and reputational risks, while Western Digital paid higher taxes but maintained government relationships that proved valuable for contracts and regulatory approvals.

The Irish incorporation also enabled another financial engineering trick: Seagate could borrow money in the U.S. at low rates (where interest was tax-deductible) while keeping profits offshore. This created a bizarre situation where Seagate had billions in offshore cash but would borrow money for U.S. operations and dividends.

By 2017, the U.S. tax reform partially neutralized Seagate's advantage by lowering the U.S. corporate rate to 21%. But by then, Seagate had saved over $2 billion in taxes—money that funded the company's transformation from disk drive manufacturer to data infrastructure provider. The lesson was clear: in commodity businesses with thin margins, tax strategy could be as important as technology strategy.

VIII. Cloud Era & Data Infrastructure Pivot (2014–2020)

By 2014, Steve Luczo could see the writing on the wall. Consumer PC sales were declining, tablets and smartphones used flash storage, and everyone was talking about the death of the hard drive. But Luczo saw something others missed: the cloud was about to create unprecedented demand for massive, cheap storage.

The strategy shift began with a series of acquisitions that puzzled analysts at the time. In 2014, Seagate acquired Xyratex, a storage systems company, for approximately $375 million. Xyratex didn't make drives—they made the systems that housed drives in data centers. The same year, it acquired LSI's flash enterprise PCIe flash and SSD controller products, and its engineering capabilities, from Avago for $450 million.

These weren't random purchases. Seagate was moving up the stack, from components to systems, from hardware to solutions. The message to hyperscalers was clear: Seagate wasn't just a drive vendor anymore—they were a data infrastructure partner.

The transformation accelerated with the 2015 acquisition of Dot Hill Systems for $696 million. Dot Hill made storage arrays and software—the kinds of systems that Facebook, Google, and Amazon needed to manage exabytes of data. Seagate was betting that as data exploded, customers would want integrated solutions, not just raw drives.

But the real innovation came in 2020, just as the pandemic drove digital transformation into overdrive. Seagate did something unprecedented for a hardware company: it went open source. The company announced CORTX, an open-source object storage software designed for massive scale. This was Seagate saying: we're not just selling you drives, we're giving you the software to manage them, for free.

Alongside CORTX came Lyve—Seagate's own cloud storage service. Launched in 2021, Lyve was positioned not as a competitor to AWS or Azure, but as a complement—a specialized service for customers who needed to move massive datasets between clouds or maintain them at the edge. It was Switzerland in the cloud wars, neutral territory where data could live without lock-in.

The gaming partnerships revealed another dimension of the strategy. Seagate partnered with both PlayStation and Xbox, but the Xbox relationship was special. When Microsoft designed the Xbox Series X/S, they worked with Seagate to create a proprietary expansion card—a high-margin product that only Seagate could manufacture. It was the razor-and-blades model applied to gaming storage.

By 2020, the strategy was working. While consumer drive sales declined, data center sales soared. Cloud service providers were buying drives not by the dozen but by the thousands, filling football-field-sized data centers with Seagate drives. Analyst firm IDC has estimated that 89% of data stored by leading cloud service providers is stored on hard drives.

The numbers told the story: in 2014, enterprise sales were 40% of Seagate's revenue. By 2020, they were over 70%. The company that had built its fortune on 5-megabyte desktop drives was now shipping 20-terabyte monsters to hyperscalers. The pivot was complete—Seagate had transformed from a PC component supplier to critical cloud infrastructure.

IX. Recent Developments & AI Era (2021–2025)

If 2020 was about surviving the pandemic, 2024 was about surfing the AI tsunami. The launch of ChatGPT in late 2022 had changed everything, and by 2024, every tech company was scrambling to build AI infrastructure. For Seagate, this was the opportunity they had been preparing for.

The breakthrough came from twenty years of research finally bearing fruit. Harnessing the potential of heat-assisted magnetic recording (HAMR) for substantial areal density gains, we dedicated two decades to perfecting the process, culminating in the groundbreaking Mozaic 3+ platform. Mozaic 3+ is the realization of Seagate's two decades of pioneering research and development in HAMR technology.

HAMR sounds like science fiction: using lasers to heat microscopic spots on a disk to 400 degrees Celsius for nanoseconds, allowing data to be written more densely than ever before. Seagate's implementation of HAMR technology drives areal densities of 3TB/disk and beyond. The first Mozaic drives shipped in early 2024 with 30TB capacity—double what conventional technology could achieve.

Seagate Technology Holdings plc (NASDAQ: STX), a global leader in mass-capacity data storage, announced the global channel availability of up to 30TB Exos® M and IronWolf® Pro hard drives. Built on Seagate's Mozaic 3+™ platform and powered by heat-assisted magnetic recording (HAMR) technology, these drives are engineered to meet increasing demand for scalable, high-performance storage driven by the rise of AI deployments that are supplementing traditional enterprise infrastructure development.

The AI boom created demand unlike anything the industry had seen. Data storage firm Seagate said it was working to develop a 100-terabyte hard drive by 2030, touting blistering demand from data centers for the 70-year-old technology in the artificial intelligence boom. BS Teh, Seagate's chief commercial officer, told CNBC that the company was aiming to launch such a drive—which would have about three times the capacity of the firm's top-of-the-line hard drives—by 2030.

The economics were staggering. At the start of the year, Microsoft said it expects to spend a whopping $80 billion on data centers in its fiscal year ending June 2025. Every large language model needed massive training datasets, and those datasets lived on hard drives. Sixty-one percent of respondents expect their organization's cloud-based storage – underpinned by hard drives – will increase by more than 100% by 2028 according to a recent survey commissioned by Seagate.

But the energy challenge loomed large. Goldman Sachs Research forecasts global power demand from data centers will increase by as much as 165% by 2030, compared with 2023. Seagate's new report reveals that energy usage is now a top concern for 53.5% of business leaders. A recent IEA report highlights that AI is set to double data centre electricity demand by 2030, pushing consumption to approximately 945 terawatt hours (TWH) – more than Japan's entire current electricity use. By then, data centres could account for as much as 8% of global carbon emissions.

Seagate's answer was efficiency through density. Seagate's HAMR-based Mozaic 3+ platform, then in volume production, enabled up to 3 times more capacity in the same footprint, reduced embodied carbon by over 70% per terabyte, and lowered cost per terabyte by 25%. A single 30TB Mozaic drive could replace two 16TB conventional drives, cutting power consumption per terabyte by 40%.

By mid-2025, the momentum was undeniable. Seagate was ramping Exos M to volume shipments on capacity points up to 32TB with a leading cloud service provider. The company had extended the platform to 36TB drives, with Dell among the early adopters. Seagate continued to lead in areal density, sampling drives on the Exos M platform of up to 36TB. The company was executing on its innovation roadmap, having successfully demonstrated capacities of over 6TB per disk within its test lab environments.

The gaming partnerships expanded too, with Seagate becoming the exclusive provider of expansion storage for Xbox Series X/S—a high-margin business that leveraged consumer relationships while the enterprise business boomed.

Looking at the numbers, the transformation was complete. As of mid-2025, the trailing twelve month revenue for Seagate Technology was $9.1B, with the vast majority coming from cloud and enterprise customers. The company that started by putting 5 megabytes in a PC was now putting 30 terabytes in AI data centers, with 100TB drives on the horizon.

The lesson? Sometimes the oldest technologies find new life in unexpected places. While everyone obsessed over AI chips and models, someone still had to store all that data. And increasingly, that someone was Seagate.

X. Playbook: Business & Investing Lessons

After 46 years of survival, transformation, and occasional triumph, what can we learn from Seagate's journey? The playbook reads like a masterclass in navigating a commoditized, cyclical industry.

Lesson 1: Consolidation as Competitive Advantage In commodity businesses, being the consolidator beats being consolidated. Seagate's systematic acquisition of Imprimis, Conner, Maxtor, and Samsung's HDD business wasn't just about growth—it was about eliminating price competition. Every deal made the industry more rational, margins more sustainable. In industries with high fixed costs and economies of scale, three players can be profitable while ten players guarantee mutually assured destruction.

Lesson 2: The Cyclical Nature of Hardware Businesses Hardware is feast or famine, and the famines are predictable. PC refresh cycles, data center buildouts, console launches—they all follow patterns. Seagate learned to hoard cash during booms to fund operations and acquisitions during busts. The Thailand floods taught an even more valuable lesson: in cyclical industries, the companies that survive the down cycles often emerge with pricing power that lasts for years.

Lesson 3: When to Go Private vs. Public The 2000 take-private transaction was a masterpiece of timing. Public markets hated hardware during the dot-com bubble, making Seagate's stock cheap. Private ownership allowed multi-year restructuring without quarterly earnings pressure. Going public again in 2002 after fixing the business captured the value creation. The lesson: capital structure should match business needs, not banker preferences.

Lesson 4: Managing Through Natural Disasters and Supply Chain Crises The Thailand floods revealed that in global manufacturing, resilience is worth more than efficiency. Seagate's higher-ground facilities and geographic diversification looked expensive until they became priceless. Modern supply chains are optimized for efficiency but fragile to disruption. Companies that invest in redundancy look stupid until they look genius.

Lesson 5: Vertical Integration vs. Horizontal Expansion Seagate tried both—integrating into heads and media while also expanding into software and services. The vertical integration worked (better component costs, quality control). The horizontal expansion into software mostly failed (EVault debacle). The lesson: integrate vertically in your core competency, partner horizontally for everything else.

Lesson 6: Tax Strategy as Competitive Moat The Ireland incorporation saved Seagate billions over a decade—money that funded R&D and acquisitions while competitors paid full freight. In low-margin businesses, tax efficiency can be the difference between reinvestment and retrenchment. Yes, it's controversial. Yes, it works.

Lesson 7: Adapting to Platform Shifts From mainframes to PCs to cloud to AI, Seagate survived four platform transitions. The key wasn't predicting the future but maintaining flexibility to pivot. When PCs declined, they shifted to enterprise. When enterprise moved to cloud, they became cloud suppliers. When AI exploded, they had the technology ready. Survival is about adaptation, not prediction.

The meta-lesson? In technology, the boring businesses that everyone thinks will die—disk drives, semiconductors, networking equipment—often generate better returns than the sexy startups. They have moats (scale, customer relationships, switching costs), generate cash, and benefit from the same trends that power their flashier customers. Seagate stored the PC revolution, the internet boom, the mobile explosion, and now the AI transformation. Not bad for spinning rust.

XI. Analysis & Bear vs. Bull Case

Bull Case: The AI Storage Supercycle

The optimists see Seagate at the beginning of a massive growth cycle. Start with the demand picture: IDC estimates that 291ZB of data will be generated in 2027. AI isn't just using existing data—it's creating new data at unprecedented rates. Every inference generates logs, every training run creates checkpoints, every model needs versioning.

The duopoly with Western Digital creates an almost OPEC-like pricing environment. With Toshiba a distant third and no new entrants possible (who's going to spend $10 billion to enter a "dying" industry?), Seagate and WD can maintain rational pricing. The Thailand floods proved this—when supply tightens, prices spike and stay elevated for years.

The technology moat is real and growing. Seagate expects the Mozaic platform to lead to 5TB/platter as early as 2028. Twenty years and billions invested in HAMR gives Seagate a 3-5 year lead that competitors can't quickly close. Western Digital is pursuing a different technology (microwave-assisted recording), creating differentiation rather than direct competition.

The unit economics are improving dramatically. The company is even quantifying that - the Exos X16's average power consumption of 9.44W translates to 0.59W / TB. The new Exos 30TB's equivalent number is a bit higher at 10.5W, but that translates to a 40% power savings on a per-TB basis at 0.35W / TB. As drives get denser, the cost per terabyte drops while prices remain stable—expanding margins.

Cloud concentration is a feature, not a bug. Yes, Seagate depends on a handful of hyperscalers, but these customers have massive budgets, multi-year planning cycles, and no alternative to HDDs for bulk storage. Nearly 90% of data in cloud data centers resides on hard drives. SSDs are 5-10x more expensive per terabyte and that gap isn't closing.

Bear Case: The Slow-Motion Disruption

The pessimists see a melting ice cube, profitable today but doomed tomorrow. SSDs keep getting cheaper, and at some point, the lines cross. Samsung is producing 256TB SSDs—yes, they cost $50,000 today, but what about in five years? Every iPhone that replaces a laptop, every photo that stays in cloud instead of local storage, chips away at HDD demand.

The cyclicality is brutal and unpredictable. Seagate's revenue swung from $11 billion to $8 billion and back based on factors entirely outside their control. When cloud capex slows, Seagate's revenue craters. When Thailand floods or pandemics hit, supply chains break. This isn't a business—it's a casino where the house only sometimes wins.

Geographic concentration remains terrifying. Most production is still in Thailand and China. Another flood, an earthquake, a geopolitical crisis—any could cripple production. The Thailand floods generated windfall profits, but next time Seagate might be the one underwater.

Customer concentration is extreme. The top five cloud providers probably account for 50%+ of revenue. If Amazon decides to design its own drives (like it did with chips), if Google shifts spending to AI training instead of storage, if Microsoft standardizes on Western Digital—any of these could crater Seagate's business overnight.

The innovator's dilemma looms. Seagate makes money from HDDs, so they'll never fully embrace SSDs or next-generation storage. Some startup working on DNA storage or quantum storage or something we haven't imagined will eventually make magnetic storage obsolete. Kodak dominated film until digital killed them—Seagate could be next.

The Verdict

The truth, as always, lies somewhere in between. Seagate isn't going to zero, but it's also not going to the moon. It's a cash cow in a slowly declining but still essential industry. The AI boom extends the runway by 5-10 years, HAMR technology maintains competitiveness, and the duopoly structure ensures profitability.

For investors, Seagate is a classic value play: single-digit P/E ratio, decent dividend yield, and exposure to AI infrastructure without AI valuation. It won't be the next Nvidia, but it also won't be the next Kodak. In a world of infinite data, someone has to store it. For now, that someone is still Seagate.

XII. Epilogue & "If We Were CEOs"

Standing in Seagate's Fremont headquarters, looking at a display case containing the original ST-506 drive next to a modern 30TB Mozaic monster, the evolution is staggering. Six million times more capacity in roughly the same physical space. If cars had improved at the same rate, a Toyota Camry would go 180 million miles per hour.

But what's next? If we were running Seagate, three moves seem obvious:

First, embrace the end game. Hard drives will eventually be replaced—maybe in 10 years, maybe in 30, but eventually. Instead of fighting it, plan for it. Use the cash flows from the HDD business to buy the companies building what's next. Seagate should be acquiring DNA storage startups, glass storage research, anything that could store exabytes in a shoebox.

Second, vertically integrate into recycling. Every hard drive manufactured eventually becomes e-waste. Seagate should own the recycling infrastructure, recovering rare earth materials from old drives to build new ones. It's environmentally responsible, creates a circular economy, and captures value currently left on the table.

Third, become the storage Switzerland. As data becomes geopolitical (data sovereignty, national security, privacy laws), Seagate should offer regionalized manufacturing and data residence guarantees. Build factories in every major market, offer drives that never leave national borders. In a deglobalizing world, local production becomes a premium feature.

The broader lesson transcends storage. In technology, the companies that survive longest aren't always the most innovative—they're the most adaptable. Seagate survived the transition from mainframes to PCs not by predicting it but by adapting to it. They're surviving the transition to cloud the same way.

The future of storage might be quantum, might be biological, might be something we can't imagine. But the need for storage is eternal. As long as humans create information, something needs to store it. For 46 years, that something has been Seagate. For the next 46? The only certainty is change, and Seagate's only strategy is to keep adapting.

In the end, Seagate's story isn't about technology—it's about survival. In an industry where 216 out of 218 companies died, Seagate lived. They weren't always the best, rarely the first, never the cheapest. But they endured. In business, as in evolution, survival is the ultimate victory.

XIII. Recent News & Links

The Seagate story continues to evolve daily. As of late 2024, the company has successfully ramped Mozaic 3+ production with over one million drives shipped. Major cloud providers are qualifying 36TB drives for 2025 deployment. The AI boom shows no signs of slowing, with data center investment at record levels.

For those wanting to go deeper, the Stanford Business School case study on the 2000 buyout remains definitive. The IEEE papers on HAMR technology explain the physics. The quarterly earnings calls, especially Luczo's commentary from 2000-2015, are masterclasses in strategic thinking.

The next chapter remains unwritten. Will HAMR extend HDD viability another decade? Will AI demand overwhelm even expanded capacity? Will some new technology render magnetic storage obsolete? The only certainty is that data will keep growing, and someone will need to store it. For now, that someone remains Seagate, still spinning after all these years.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube