Performance Food Group: From Richmond Peddler to Foodservice Giant

I. Introduction & Episode Hook

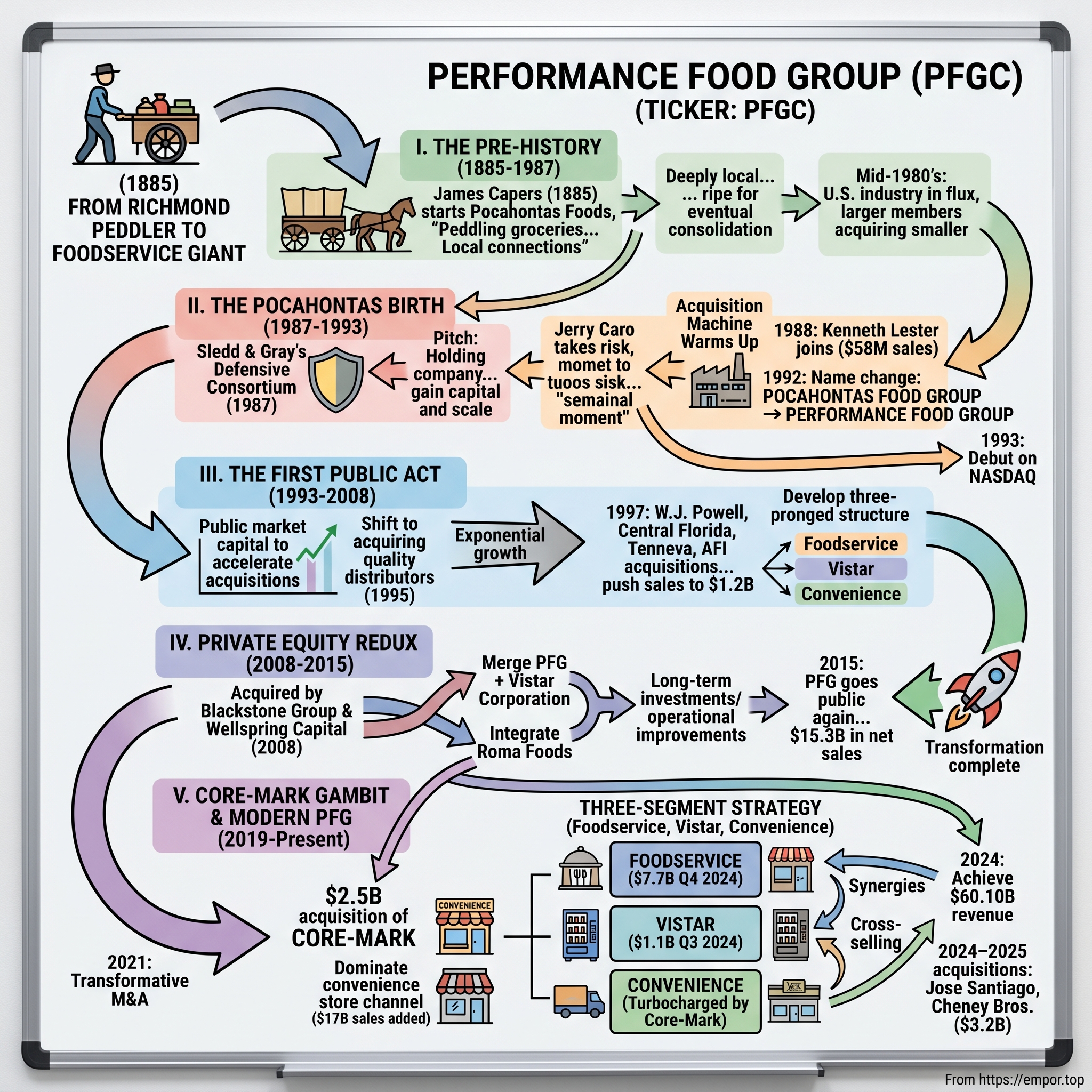

Picture this: A food peddler named James Capers pushes his cart through the dusty streets of Richmond, Virginia in 1885. The Civil War ended just twenty years ago. The South is rebuilding. Capers sees opportunity in the basic human need—feeding people. He starts what would become one of Richmond's foundational food distribution businesses. Fast forward 139 years, and the company bearing the Performance Food Group name commands $58.3 billion in annual sales, serving over 300,000 locations across North America. Yet here's the fascinating paradox: while the roots trace to 1885, Performance Food Group as we know it was actually born in 1987.This is the story of how a holding company strategy—roll up fragmented regional distributors, consolidate operations, leverage scale—built one of America's largest food distribution powerhouses. The company is now "one of the largest food and foodservice distribution companies in North America with more than 150 locations" and markets and delivers products to "300,000+ locations". In 2024, the company achieved revenue of $60.10 billion, up from $57.87 billion in 2023.

The story contains multitudes: private equity buyouts, public offerings, massive acquisitions, segment diversification. Today, if Performance Food Group merged with US Foods—as was proposed in 2024—the combined entity would command 18% of the $371 billion U.S. foodservice distribution market, creating America's largest foodservice distributor. Yet even at its current scale, PFG remains the scrappy independent operator's champion, with 46% of sales coming from independent restaurants compared to just one-third for US Foods.

What makes this story remarkable isn't just the scale achieved, but the strategic evolution from turnaround specialist to disciplined acquirer, from single-segment operator to three-pronged distribution powerhouse. This is the Acquired-style deep dive into how Richmond's food peddling legacy transformed into a modern distribution colossus.

II. The Pre-History: Richmond's Food Distribution Legacy (1885-1987)

The year is 1885. Richmond, Virginia carries the scars and opportunities of post-Civil War reconstruction. James Capers begins peddling groceries for a wholesaler in Richmond, with his business eventually growing into Pocahontas Foods, which would distribute branded products to restaurants and foodservice outlets across the United States.

Think about the America Capers inhabited. No interstate highway system. No refrigerated trucks. No supply chain management software. Distribution meant horse-drawn wagons, local relationships, and intimate knowledge of every restaurant, hotel, and institution in your territory. The business was intensely local, deeply fragmented, and ripe for eventual consolidation—though that consolidation would take another century to materialize. The fragmentation that Capers' business operated within persisted for a century. By the mid-1980s, the U.S. food distribution industry served hundreds of thousands of restaurants, hotels, schools, and institutions through thousands of local and regional distributors. During the mid-1980s, the U.S. food distribution industry was in flux. With increasing frequency, the larger members of the industry were acquiring smaller distributors, hoping to take advantage of a highly fragmented industry by swallowing up as many companies as feasible and secure a greater share of the market.

The catalyst for change came from an unlikely source: fear. Two industry participants who were watching the consolidation surrounding them--and growing increasingly anxious--were Robert Sledd and Michael Gray. Sledd was president of Taylor & Sledd, a family food marketing company that owned a distributor buying group named Pocahontas Foods USA. Gray served as president of Pocahontas Foods USA. As the two executives surveyed the developments affecting their industry, noting that in one energetic fit Kraft Foodservice had acquired eight of the 50 largest distributors in the country in 1986 alone, they grew alarmed.

Think about that moment: Kraft Foodservice acquiring eight of the top 50 distributors in a single year. The consolidation wave wasn't coming—it had arrived with hurricane force. Small and mid-sized distributors faced a stark choice: sell to a giant and lose autonomy, or band together and create their own destiny.

James Capers' business grew into Pocahontas Foods, which distributed branded products to restaurants and foodservice outlets across the United States. The company continued to grow and evolve through the mid-1980's when leaders had a vision for a new company that would bring together a network of distributors with the corporate support to become an industry giant.

This sets the stage for one of the most audacious holding company plays in food distribution history—the birth of Performance Food Group in 1987.

III. The Pocahontas Food Group Birth: Private Equity's First Bite (1987-1993)

The conference room tension was palpable in early 1987. Robert Sledd and Michael Gray sat across from three skeptical distributor owners, each fielding competing offers from larger players. Their pitch was simple yet revolutionary: form a holding company that preserves local management autonomy while gaining the capital and scale advantages of consolidation. To turn Pocahontas Food Group into a reality, Sledd and Gray approached three Pocahontas Foods USA members in 1987. As they discovered, their fears of potentially losing a portion of their distributor base were not unfounded. Caro Produce and Institutional Foods, a family-run distribution company based in Houma, Louisiana, had an offer from a suitor. I. Feldman Co., based in Washington, D.C., had been approached as well. Lebanon, Tennessee-based K.O. Lester Co. was entertaining a bid from a larger concern. Sledd and Gray asked each distributor to ally itself with the newly formed Pocahontas Food Group, promising that each would be allowed to retain its management. The two executives also argued that, as part of a greater whole, each distributor would benefit from the advantages of a larger capital base.

The first domino to fall was Jerry Caro of Caro Produce. Kenneth O. Lester, head of the eponymic distributor, balked at Sledd and Gray's proposal, while he weighed the merits of an offer by Kraft Foodservice. The fledgling consortium appeared destined for failure, but Jerry Caro, head of Caro Produce, decided to take the risk and ally his company with Pocahontas Food Group. Caro's decision represented a seminal moment in Pocahontas Food Group's history, its importance not lost on Sledd. "If Jerry hadn't taken that step," Sledd remarked to ID in September 1998, "there would be no PFG (Performance Food Group) today."

Although Pocahontas Food Group did not get off to a roaring start, the company did have a founding distributor company, the $67-million-in-sales Caro Produce, and a founding chairman, Jerry Caro. The holding company's constituency would soon increase, however. The acquisition machine was warming up.

Before the end of 1987, the company completed its first acquisition, purchasing a distributor based in Gainesville, Florida named Hi Neighbor Wholesale. The acquisition was subsequently renamed Pocahontas Foodservice. Notice the pattern already emerging: acquire, rebrand under the Pocahontas umbrella, maintain local operations.

The real coup came in July 1988. Kenneth O. Lester, meanwhile, was still considering Kraft Foodservice's offer, but by July 1988 he had decided to bring his $58-million-in-sales company into the Pocahontas Food Group fold. After the acquisition of his company, Lester took over as chairman of Pocahontas Food Group and Caro took on the title of vice-chairman, concurrent with the relocation of corporate headquarters from Richmond, Virginia to Nashville, Tennessee.

Consider the strategic brilliance here: Lester, who initially resisted the consortium, not only joined but became chairman. His $58 million in sales combined with Caro's $67 million created instant scale—$125 million in combined revenue from just two companies. The headquarters move to Nashville signaled a break from the Richmond past while positioning the company in a more central location for national expansion.

The early acquisition playbook focused on distressed assets. These weren't glamour purchases—they were turnaround opportunities where Pocahontas could apply operational improvements, leverage combined purchasing power, and restore profitability. The strategy was pure arbitrage: buy broken distributors cheap, fix operations, benefit from scale economies.

But the real transformation came in 1992. The company shed its historical name—Pocahontas Food Group—and emerged as Performance Food Group. The name change wasn't cosmetic; it signaled a shift from regional heritage to national ambition. "Performance" implied excellence, efficiency, results. This was no longer your grandfather's food distributor.

Performance Food Group debuts on the NASDAQ Exchange in 1993, marking the end of the startup phase. The IPO provided crucial growth capital and public market credibility. For Sledd, Gray, Lester, and Caro, it validated their contrarian bet: that independent distributors could band together and compete with the giants while maintaining entrepreneurial spirit.

The numbers tell the story of breakneck growth. By 1993, what started as a defensive consortium had become an offensive weapon, ready to roll up the fragmented foodservice distribution landscape. The foundation was set for the next phase: using public market capital to accelerate acquisitions and build true national scale.

IV. The First Public Act: Building Scale Through M&A (1993-2008)

The post-IPO Performance Food Group faced a strategic inflection point. With public capital in hand and a proven consolidation playbook, management made a crucial decision: shift from buying distressed assets to acquiring quality distributors. As one executive noted at the time, "We don't have time to do turnarounds now." The emphasis moved from rehabilitation to acceleration. The 1995 acquisitions perfectly exemplified this new approach. In 1995, when headquarters were relocated back to Richmond, the company acquired Milton's Foodservice, based outside of Atlanta, and Cannon Foodservice, a distributor based in Asheville, North Carolina. Milton's wasn't just any distributor—it traced its history back to 1961 when it began as the Blue Ribbon Packing Company before becoming Milton's Institutional Foods. By the time PFG acquired it in 1995, Milton's had built a strong presence serving restaurants, country clubs, hospitals, schools, and nursing homes primarily in Georgia, Alabama, North Carolina, and South Carolina.

The headquarters relocation back to Richmond in 1995 carried symbolic weight. Nashville had served its purpose during the Lester era, but returning to Richmond reconnected PFG with its historical roots while positioning the company closer to East Coast markets. It signaled confidence—PFG was no longer running from its past but embracing it.

The late 1990s witnessed exponential growth through strategic acquisitions. A second offering of stock was completed in March 1996 to fuel the company's acquisition campaign during the late 1990s, a buying binge that began in late 1996 when PFG acquired McLane Foodservice, a distributor to fast food chains, such as Kentucky Fried Chicken, Dairy Queen, and Dunkin' Donuts, and to vending customers. The acquisition of McLane increased PFG's annual sales by more than 20 percent, marking PFG's entry into chain restaurant distribution—a higher-volume, lower-margin business that provided scale advantages.

In 1997 the company completed acquisitions that pushed sales toward Sledd's projected total, purchasing W.J. Powell Company, Central Florida Finer Foods, Inc., Tenneva Foodservice, Inc., and AFI Food Service Distributors. By the end of 1997, sales towered at $1.2 billion, nearly doubling in two years' time.

The numbers tell a remarkable story: Acquisitions and internal growth lift sales to $1.6 billion, a more than threefold increase in three years by 1998. This wasn't just growth—it was hypergrowth achieved through disciplined execution of a proven playbook. According to 1997 figures, 55 percent of the industry's $141 billion in annual sales was controlled by distributors one-tenth PFG's size, presenting the company with numerous opportunities to secure greater market share. The fragmentation that enabled PFG's creation still provided ample consolidation runway.

The three-segment model foundation was taking shape during this period. Rather than being a single-focused broadline distributor, PFG developed specialized capabilities across different customer segments—independent restaurants, chains, institutions, and eventually vending and convenience. This diversification would prove crucial during economic downturns when different segments performed differently.

By 2008, PFG had grown into a formidable player, but the financial crisis changed everything. The credit markets froze. Public market valuations cratered. For PFG, it created an unexpected opportunity to go private again—this time with heavyweight private equity backing.

V. The Private Equity Redux: Blackstone & Wellspring Era (2008-2015)

The boardroom at Performance Food Group must have felt the weight of history in early 2008. Twenty-one years after the original defensive consortium formed to avoid being swallowed by giants, PFG was now choosing to be acquired. But this wasn't capitulation—it was strategic opportunism.

On January 18, 2008, Performance Food Group announced it has signed a definitive merger agreement to be acquired by an affiliate of The Blackstone Group (NYSE: BX) and Wellspring Capital Management in a transaction valued at approximately $1.3 billion. The actual closing value reached $1.4 billion. Under the terms of the merger agreement, Performance Food Group shareholders will receive $34.50 in cash for each outstanding share of Company common stock, representing a premium of 33.4% over the average closing share price for the 30 trading days and 42.6% over the closing share price of $24.19.

The timing seems counterintuitive—going private just as the financial crisis was unfolding. Other notable investments that Blackstone completed in 2008 and 2009 included AlliedBarton, Performance Food Group, Apria Healthcare, and CMS Computers. During the 2008 financial crisis, Blackstone closed only a few transactions, making PFG one of the select deals that cleared their investment committee during this tumultuous period.

But here's where it gets strategically brilliant: The transaction will be structured as a combination of Performance Food Group and Vistar Corporation, a foodservice distributor controlled by affiliates of Blackstone and Wellspring. Performance Food Group is being merged with a wholly owned subsidiary of VISTAR Corporation, a leading specialty foodservice distributor. The newly combined company, known as Performance Food Group, is expected to have revenues approaching $10 billion and more than 10,000 associates.

George Holm, president and chief executive officer of VISTAR, becomes chief executive officer for the combined PFG. This wasn't just a financial engineering play—it was a transformative merger that added an entirely new distribution vertical. Vistar brought expertise in vending, office coffee service, and theater concessions—high-margin, specialized distribution channels that complemented PFG's restaurant and institutional focus.

Two other foodservice companies owned by the private equity firms, snack food distributor Vistar and Italian foodservice company Roma Foods, were then merged into PFG. Roma Foods added ethnic food expertise and additional scale in Italian cuisine products, a growing segment in American dining.

Consider what Blackstone and Wellspring accomplished: They took PFG private at depressed valuations during the financial crisis, immediately bolted on two complementary businesses (Vistar and Roma), created a more diversified platform, and positioned the company for the recovery. Blackstone senior managing director Prakash Melwani noted: "We are very pleased to be able to combine two leading companies in the foodservice distribution industry. The companies are highly complementary in terms of distribution networks, customer focus and product offerings."

Wellspring partner William F. Dawson Jr. added perspective on the strategic logic: "The combined company represents a dynamic, growing foodservice platform with substantial breadth and diversity across a broad range of customers, products and channels."

The private equity playbook during this era focused on operational improvements, technology investments, and continued strategic acquisitions. Being private allowed management to make long-term investments without quarterly earnings pressure—crucial during the slow recovery from the financial crisis. The company could optimize routes, consolidate facilities, upgrade systems, and integrate the Vistar and Roma acquisitions without public market scrutiny. By 2015, the transformation was complete. PFG went public on October 2, 2015, at NYSE with issuing 14.5 million shares at $19 per share. The Company issued and sold 12,777,325 shares in the offering and certain selling stockholders offered and sold 3,897,675 shares. The financial sponsor of the PFG IPO was The Blackstone Group, which would continue to own a majority of the shares following the offering.

The IPO priced at $19, below the expected range of $22 to $25 per share—a somewhat disappointing debut that Fortune described as an "underwhelming IPO in October 2015." But the metrics told a different story: In the fiscal year ended June 27, 2015, PFGC generated $15.3 billion in net sales and $328.6 million in adjusted EBITDA, representing compound annual growth rates of 9% and 11%, respectively, since fiscal 2010.

The private equity era had delivered spectacular results. The company entered private ownership in 2008 with roughly $10 billion in revenue post-merger; it emerged in 2015 with $15.3 billion. More importantly, it now operated three distinct segments—Performance Foodservice, Vistar, and PFG Customized—each targeting different customer channels with specialized capabilities.

The stage was set for the next chapter: leveraging this diversified platform to make the company's most transformative acquisition yet.

VI. The Core-Mark Gambit: Convenience Store Domination (2019-2021)

The morning of May 18, 2021, marked a watershed moment in Performance Food Group's history as CEO George Holm announced their most transformative acquisition: the $2.5 billion purchase of Core-Mark Holding Company. The transaction included Core-Mark's net debt, with CORE shareholders receiving $23.875 in cash and 0.44 PFG shares for every CORE share.

The strategic logic was compelling. Adding convenience store distribution in 2019 built up the core strength of our organization, providing another avenue for growth, Patrick Hagerty, CEO of Vistar, said in a statement. That 2019 foundation came through PFG's acquisition of Eby-Brown, which first broke the company into the convenience store business. Now, with Core-Mark, PFG wasn't just entering the space—it was dominating it.

The addition of Core-Mark brings one of the largest wholesale distributors to the convenience retail industry in North America into PFG's family of companies, with approximately $17 billion in net sales. The company has approximately 8,000 employees and operates 32 distribution centers across the United States and Canada. Core-Mark services approximately 41,000 customer locations in all 50 U.S. states and five Canadian provinces.

The numbers were staggering: Acquisition expands PFG's geographic reach and market diversification into the growing convenience store channel, adding approximately $17 billion to net sales, resulting in total PFG pro-forma LTM net sales of approximately $44 billion. In a single transaction, PFG was adding nearly 40% to its revenue base.

But this wasn't just about scale. The transaction creates a best-in-class convenience business within PFG's Vistar segment that includes the Core-Mark and Eby-Brown businesses. The expanded convenience business will continue to operate under Core-Mark and will be headquartered in Westlake, Texas with Eby maintaining ongoing operations in Naperville, Illinois.

The timing reflected both strategic foresight and pandemic-driven urgency. Distributors had been looking at diversifying their business lines for some time, but that intensified a year ago when many of them lost a lot of business as restaurants were forced to close dining rooms to prevent the spread of COVID-19. Many companies started eyeing retailers, including grocers and convenience stores, to hedge their bets. Others started delivering pantry supplies to consumers' homes.

While competitors scrambled to adapt during COVID-19, PFG had already laid the groundwork with Eby-Brown. The Core-Mark acquisition wasn't reactive—it was the culmination of a multi-year strategy to diversify beyond restaurant distribution. For a company like PFG, which is competing with two larger rivals in Sysco and US Foods, the c-store business provides another growth opportunity.

Leadership continuity was crucial to the integration strategy. Scott McPherson will continue in his role as President and Chief Executive Officer of Core-Mark, and Tom Wake will continue as President and Chief Executive Officer of Eby-Brown, reporting to Mr. McPherson. This wasn't a typical "acquire and gut" approach—PFG recognized the value in Core-Mark's operational expertise and customer relationships.

The synergy potential was significant but achievable: PFG expects to achieve annual run-rate net cost synergies of approximately $40 million by the third full year after closing. These weren't pie-in-the-sky projections but conservative estimates based on procurement leverage, route optimization, and back-office consolidation.

Scott McPherson, Core-Mark President and Chief Executive Officer noted: "This transaction brings together two companies known for their customer-focused approach and dedication to their employees... our Board evaluated the transaction and determined this combination provides our investors immediate value and the opportunity to participate in the upside potential of being part of a larger, diversified and customer-centric supplier in the foodservice and convenience retail industry".

The transaction closed on September 1, 2021, creating a convenience distribution powerhouse. The transaction, completed in September, builds upon PFG's current foodservice focus within the convenience channel, adding additional customers and product offerings, particularly in the fresh-food space. The fresh food emphasis was critical—convenience stores were evolving from cigarettes and candy to fresh sandwiches and salads, aligning perfectly with PFG's foodservice expertise. The impact was immediate and substantial. Post-acquisition, Fourth-quarter fiscal 2024 net sales for Convenience decreased 0.5% to $6.3 billion compared to the prior year period, but this represented massive scale from the base. To put this in perspective, the Convenience segment now generates over $25 billion annually—nearly half of PFG's total revenue. The segment faced headwinds from declining cigarette sales but offset these with growth in fresh food and foodservice offerings.

The integration proved the strategic thesis correct. The Vistar segment's net sales grew by 7.4% to $1.2 billion, and the Convenience segment's net sales increased by 1.3% to $5.9 billion in Q2. Adjusted EBITDA for these segments also showed positive trends, with Convenience notably increasing by 20.5% to $83.5 million in Q2. The synergies weren't just cost-driven—they came from cross-selling foodservice products into convenience stores and leveraging PFG's procurement scale.

Three years post-acquisition, the Core-Mark gambit has proven transformative, creating a third pillar of growth alongside traditional foodservice and vending distribution. The convenience channel provides counter-cyclical benefits—when restaurants struggle, convenience stores often thrive as consumers trade down. This diversification would prove crucial as PFG navigated post-pandemic market dynamics.

VII. Three-Segment Strategy: Foodservice, Vistar, and Convenience

The modern Performance Food Group operates as a three-headed hydra, each segment targeting distinct customer channels with specialized capabilities. Today we have three segments—Foodservice, Vistar and Convenience—each of which focuses on delivering delicious food and excelling at customer service. This isn't just organizational structure—it's strategic architecture designed for resilience and growth.

The Foodservice segment remains the heritage heart of PFG, serving independent restaurants, regional chains, and healthcare facilities. Fourth-quarter fiscal 2024 net sales for Foodservice increased 4.6% to $7.7 billion compared to the prior year period. This increase in net sales was driven by case volume growth in our independent and Chain business. Securing new and expanding business with independent customers resulted in organic independent case growth of 3.7% for the fourth quarter of fiscal 2024 compared to the prior year period. For the fourth quarter of fiscal 2024, independent sales as a percentage of total segment sales were 40.6%.

The independent restaurant focus is no accident. While Sysco and US Foods chase large chain accounts with razor-thin margins, PFG has positioned itself as the champion of independent operators. These customers value service, flexibility, and local market knowledge—areas where PFG's decentralized operating model excels. Independent restaurants also generate higher margins and demonstrate greater loyalty than chain accounts.

Vistar, the second segment, operates in what outsiders might consider unglamorous channels: vending machines, office coffee service, theaters, and concessions. But these channels offer attractive economics. Vending operators need reliable, frequent deliveries of small quantities. Theaters require specialized packaging and portion control. Office coffee service demands consistent quality and timely replenishment. For the third quarter of fiscal 2024, net sales for Vistar increased 1.7% to $1.1 billion compared to the prior year period. This increase was driven primarily by a recent acquisition.

The Convenience segment, turbocharged by Core-Mark, now represents the growth engine. Vistar sales were $1.2 billion, down by 1.8%. Convenience sales were $6.3 billion, down by 0.5% in the fourth quarter of 2024. While these numbers show slight declines, they mask the strategic transformation underway. Convenience stores are evolving from cigarette and candy outlets to fresh food destinations. PFG's foodservice expertise positions it perfectly to capture this transition.

Consider the customer economics across segments. A single convenience store might generate $500,000 in annual purchases, visited multiple times weekly. An independent restaurant could represent $250,000 annually with daily deliveries. A vending location might only generate $50,000 but requires minimal sales effort and offers predictable volumes. This diversification creates multiple growth vectors and natural hedges.

The operational synergies between segments create competitive advantages. A PFG truck delivering to a convenience store can also service nearby restaurants. Procurement teams can leverage volume across all three segments for better pricing. Technology investments in routing software or inventory management benefit all channels. The corporate shared services model spreads costs across a larger revenue base.

Product overlap drives cross-segment opportunities. The same beverages sold in restaurants flow through vending machines and convenience stores. Fresh sandwiches developed for convenience stores can be offered to workplace cafeterias. Snacks procured for theaters can be distributed through vending channels. This isn't three separate businesses—it's an integrated distribution platform.

The segment strategy also provides resilience during economic cycles. During recessions, consumers trade down from restaurants to convenience stores. When the economy booms, office coffee and vending volumes surge. Theater attendance correlates with blockbuster releases, not GDP growth. This diversification smooths earnings volatility and provides multiple levers for growth.

Looking at segment profitability, each contributes differently to the bottom line. Fourth-quarter fiscal 2024 Adjusted EBITDA for Foodservice increased 14.1% to $311.8 million compared to the prior year period, demonstrating the segment's margin expansion potential. The Convenience segment generated strong cash flow despite top-line pressure from declining cigarette sales. Vistar maintains steady margins through specialized service offerings.

The three-segment model positions PFG uniquely among major distributors. Sysco remains primarily focused on foodservice. US Foods has limited convenience exposure. Regional players lack the scale to compete across all three channels. PFG's diversified platform creates competitive moats that are difficult to replicate.

VIII. Competition & Market Dynamics: David vs. Two Goliaths

The foodservice distribution battlefield resembles a three-way chess match played across a $371 billion board. Such a combination would create the largest U.S. foodservice distributor, with 18% of the market, surpassing Sysco Corp.'s 17%. Since 2015, Sysco's share has increased to 17%, PFG doubled to 8%, and US Foods grew to 10%. The three now control about 35% of the market, up from 28% less than a decade ago.

Performance Food Group occupies a unique strategic position in this competitive dynamic. While Sysco commands the largest share at 17% and US Foods holds 10%, PFG's 8% market share understates its competitive positioning. The company has doubled its market share since 2015—the fastest growth rate among the big three. More importantly, PFG's diversified business model creates competitive advantages that pure market share metrics don't capture.

The independent restaurant battlefield reveals PFG's strategic differentiation. Independent business as "the calling card" - 46% of PFG's sales vs. one-third for US Foods demonstrates PFG's dominance in this attractive segment. Independent restaurants value local relationships, flexibility, and personalized service—areas where PFG's decentralized operating model excels compared to Sysco's more centralized approach.

Sysco remains the 800-pound gorilla, with advantages in scale, purchasing power, and national account relationships. Houston, Texas, U.S.A.-based foodservice giant Sysco also reported an increase in sales and profits in its fiscal third quarter of 2024. Its sales increased 2.7 percent year over year to USD 19.4 billion. But size brings challenges. Sysco's massive scale makes nimble market response difficult. The company posted a 2 percent decline in U.S. case volume for its fiscal third quarter, suggesting market share losses to more agile competitors.

US Foods represents the most direct competitive threat to PFG. Rosemont, IL-based U.S. Foods supplies restaurants, hospitals, schools and hotels, and generated $37.9 billion in revenue last year. Our differentiated model and strong value proposition are resonating with our customers which has helped propel us to grow share with independent restaurants for twelve consecutive quarters, US Foods CEO Dave Fittman noted. The company's focus on independent restaurants directly competes with PFG's core strength.

The competitive dynamics shifted dramatically in 2015 when regulatory intervention blocked consolidation among the giants. In 2015, Sysco Corp.'s planned $3.5 billion acquisition of U.S. Foods was blocked by a federal judge who said the deal would likely reduce competition. US Foods went public the following year under its current name. This regulatory precedent created an implicit ceiling on further consolidation among the top three players.

Yet beneath the big three, fragmentation remains extreme. Foodservice distribution is highly fragmented, with Sysco holding just 17% share as the leader of the roughly $370 billion US market. This means 65% of the market remains controlled by regional and local distributors—providing ample consolidation opportunities for all three majors. PFG itself will add almost a point of the market via the $2.1 billion acquisition of privately held Cheney Bros., a deal announced alongside fiscal fourth quarter numbers.

The acquisition strategies differ markedly. PFG bought Cheney Brothers and Jose Santiago last year. Sysco acquired Jacmar last year and Edward Don and BIX Produce in 2023. US Foods bought IWC Foodservice in 2024 and Renzi Foodservice and Saladino's Foodservice in 2023. PFG focuses on transformative acquisitions that add new capabilities or segments. Sysco pursues geographic fill-ins and specialty distributors. US Foods targets regional players with strong independent restaurant relationships.

Technology increasingly differentiates competitors. Digital ordering platforms, inventory management systems, and routing optimization create competitive advantages. Smaller distributors struggle to match the technology investments of the big three, accelerating market share shifts. PFG's three-segment structure allows it to leverage technology investments across multiple channels, improving returns on IT spending.

The margin dynamics reveal competitive positioning. The company is not only the biggest in the space but by some measures the best: as Sysco itself notes, its profit margins are still better than those of US Foods and PFG. However, PFG's margin expansion trajectory suggests operational improvements are closing this gap. The convenience and vending segments provide higher margins than traditional foodservice, giving PFG mix advantages.

Looking ahead, the competitive landscape favors continued consolidation. All three companies claimed to take market share in the quarter, which offset some pockets of weakness in demand. Increased share allowed all three companies to grow U.S. revenue and, importantly, case volume despite weak restaurant traffic in the quarter. The big three continue taking share from smaller players, but competition among themselves intensifies. PFG's diversified model positions it uniquely to compete across multiple fronts while maintaining focus on its independent restaurant stronghold.

IX. The US Foods Pursuit & Future Consolidation

The phone call came in July 2024, shaking the foodservice distribution world. US Foods is reportedly in talks to buy Performance Food Group Co., according to Bloomberg. Performance Food Group has attracted takeover interest from US Foods, a potential deal that would create a food distribution company with combined sales of roughly $100 billion. If the rumored merger, reported by Bloomberg on 11 July, were to go through, it would create the largest broadline distributor in the U.S.

The strategic logic was compelling yet complex. The combined company would become the No. 1 U.S. food service distributor, with 18% of the $371 billion market, according to Bloomberg Intelligence. That would surpass current market leader Sysco Corp., which has a 17% share. For US Foods, acquiring PFG would provide instant scale advantages and diversification into convenience and vending channels where it had minimal presence.

The complementary nature of the businesses created obvious synergies. Performance Food does well with independent pizzerias, convenience stores, and candy and snacks, all areas of weakness for US Foods, according to Transport Topics, which viewed a note from senior analyst Michael Halen. He added that a merger would create scale and synergies, but hurt US Foods' EBITDA margins. The margin dilution reflected PFG's lower margins—2.58% EBITDA margins versus US Foods' 4.6%—but the scale benefits could offset this over time.

Market reaction was swift and telling. Shares of Performance Food rose as much as 6.2% on Friday, the biggest intraday gain in three months, to hit an all-time high. They closed up 4.8% in New York, giving the company a market capitalization of about $14.8 billion. US Foods shares closed broadly flat for a market value of $18.6 billion. The divergent stock movements suggested investors saw PFG as the acquisition target, not the acquirer.

But regulatory ghosts haunted the proposal. In 2015, Sysco Corp.'s planned $3.5 billion takeover of US Foods Inc. was blocked by a federal judge who said a merger of the food distribution giants would probably have reduced competition. US Foods went public the following year under its current name. The FTC's successful challenge established precedent that would scrutinize any combination among the top three players.

The antitrust concerns were substantial. Together, PFG and US Foods would control 18% of the market versus Sysco's 17%, but in specific regions and customer segments, the combined entity would dominate. Independent restaurants, where both companies were strong, could face reduced competition for their business. Convenience store distribution, where PFG's Core-Mark held significant share, might see pricing pressure.

Yet the fragmented nature of the market provided counterarguments. Even with the merger, 65% of the foodservice distribution market would remain unconsolidated. Regional players like Gordon Food Service, Ben E. Keith, and Shamrock Foods could expand to fill competitive gaps. New entrants using technology platforms could disrupt traditional distribution models.

The financial engineering presented challenges. US Foods could structure a deal to minimize pressure on debt ratios by using more equity to complete an acquisition, and any increase in leverage would be temporary, Bloomberg Intelligence senior credit analyst Julie Hung wrote. Given that US Foods has the higher market value: Its market capitalization is $18.6 billion, while PFG's is $14.9 billion, an all-stock deal would significantly dilute US Foods shareholders.

Strategic alternatives existed beyond a full merger. The companies could pursue joint ventures in specific segments, combine procurement operations while maintaining separate sales organizations, or focus on acquiring smaller regional players to grow independently. Each path offered growth potential without regulatory risk.

The market dynamics evolve rapidly. By late 2024, PFG announced another transformative move, this time targeting the Southeast. Performance Food Group completed the acquisition of Cheney Bros., Inc., a leading independent broadline foodservice distributor based in Riviera Beach, Florida, which generates approximately $3.2 billion in annual revenue and has approximately 3,600 employees operating five distribution centers in Florida and North Carolina. PFG agreed to acquire Cheney Brothers for $2.1 billion in cash, with the purchase amount reflecting a multiple of 13.0x to Cheney Brothers' unaudited 12-month Adjusted EBITDA.

The technology disruption question looms large. While Amazon Business and other digital players nibble at the edges, the complexity of foodservice distribution—temperature control, specialized handling, regulatory compliance, local relationships—creates barriers to entry. Yet PFG cannot ignore the digital transformation imperative. Technology investments in routing software, inventory management, and customer ordering platforms become table stakes for competing effectively.

X. Financial Performance & Operating Model

The financial architecture of Performance Food Group reveals both the power and challenges of distribution economics. For Q4 2024, net sales increased 2.2% to $15.2 billion, gross profit improved 4.7% to $1.7 billion, net income increased 10.9% to $166.5 million, and Adjusted EBITDA increased 18.4% to $456.2 million. These numbers demonstrate operational leverage—EBITDA growing faster than sales suggests improving efficiency and scale benefits.

For the first quarter of fiscal 2025, net sales increased 3.2% to $15.4 billion, gross profit improved 6.1% to $1.8 billion, though net income decreased 10.5% to $108.0 million while Adjusted EBITDA increased 7.3% to $411.9 million. The divergence between net income and EBITDA reflects acquisition-related costs and integration expenses—the price of growth through M&A.

The capital allocation philosophy balances growth investments with shareholder returns. The company prioritizes acquisitions that add strategic capabilities or geographic density, as demonstrated by the Cheney Brothers deal. PFG expects to generate approximately $50 million of annual run-rate cost synergies in the third full fiscal year following the closing of the Cheney Brothers transaction. These synergy targets appear conservative given the scale of the combination, suggesting potential upside.

Technology investments increasingly drive competitive differentiation. Digital ordering platforms reduce order processing costs while improving accuracy. Route optimization software cuts delivery expenses and improves customer service. Warehouse automation reduces labor dependency in tight employment markets. These investments carry high upfront costs but generate sustainable operating leverage.

The working capital dynamics of distribution create both opportunities and challenges. Inventory turns must balance availability with carrying costs. Receivables management requires disciplined credit policies while maintaining customer relationships. Payables optimization leverages scale for extended payment terms without straining supplier relationships. Even small improvements in working capital efficiency release significant cash for growth investments.

Supply chain innovation represents the next frontier. Predictive analytics improve demand forecasting, reducing waste and stockouts. IoT sensors monitor temperature throughout the cold chain, ensuring food safety and quality. Blockchain technology could eventually provide transparency from farm to table. These innovations require substantial investment but create competitive moats difficult for smaller players to replicate.

The operating model balances centralization with local autonomy. Corporate functions like procurement, technology, and finance achieve scale advantages through centralization. Local operations maintain the customer relationships and market knowledge critical in foodservice. This hybrid approach allows PFG to compete with both national giants and regional specialists.

Looking at the broader financial trajectory, PFG has transformed from a $1.3 billion company at its 2008 privatization to a $60+ billion enterprise today. This 46-fold increase in just 16 years represents one of the most successful growth stories in distribution. The combination of organic growth, strategic acquisitions, and operational improvements created extraordinary value.

XI. Playbook: Lessons in Distribution Consolidation

The Performance Food Group story offers a masterclass in distribution consolidation strategy. The playbook begins with timing—knowing when to buy distressed assets versus quality operators. During the early years, PFG focused on turnarounds, acquiring struggling distributors at attractive valuations and applying operational improvements. As the company scaled, the strategy shifted to acquiring well-run businesses that could immediately contribute to earnings.

Segment diversification emerged as a critical competitive advantage. Rather than competing head-to-head with Sysco and US Foods in traditional foodservice, PFG built positions in vending, convenience, and specialized channels. This diversification provides counter-cyclical benefits—when restaurants struggle, convenience stores often thrive. The three-segment model creates multiple growth vectors and natural hedges against economic volatility.

Managing through private equity ownership cycles requires strategic flexibility. The 2008 Blackstone/Wellspring buyout allowed PFG to make long-term investments without quarterly earnings pressure. The company could integrate major acquisitions, upgrade technology, and optimize operations away from public market scrutiny. The 2015 return to public markets came with a stronger, more diversified platform ready for the next growth phase.

Building scale while maintaining local relationships represents the central tension in distribution. PFG's solution involves preserving local management and brand identities while leveraging corporate resources for procurement, technology, and back-office functions. This approach maintains the entrepreneurial spirit and customer intimacy that independent restaurants value while achieving scale economies in purchasing and operations.

The importance of timing in transformative M&A cannot be overstated. The Core-Mark acquisition in 2021 capitalized on pandemic-driven changes in consumer behavior, positioning PFG in the growing convenience channel just as eating habits shifted. The Cheney Brothers deal in 2024 expanded Southeast presence when that region's population and economic growth accelerated. Strategic patience combined with decisive action when opportunities arise defines the PFG acquisition approach.

Cultural integration often determines acquisition success or failure. PFG's approach emphasizes welcoming acquired companies into the "family" while respecting their heritage and operational expertise. Leadership continuity, as seen with Core-Mark and Cheney Brothers executives remaining in key roles, ensures knowledge transfer and relationship preservation. This cultural sensitivity distinguishes PFG from competitors who impose standardized operating models.

The technology adoption curve in distribution favors fast followers over pioneers. Rather than betting on unproven technologies, PFG implements solutions already validated in other industries or by competitors. This approach reduces implementation risk while capturing most of the efficiency benefits. The company's scale allows it to negotiate favorable terms with technology vendors and spread implementation costs across a larger base.

Financial discipline underlies the entire playbook. Conservative synergy projections ensure acquisitions deliver promised returns. Balanced capital structures maintain financial flexibility for opportunistic deals. Working capital optimization funds growth without external financing. This financial rigor creates credibility with investors and lenders, ensuring access to capital when strategic opportunities emerge.

XII. Bear vs. Bull Case

Bull Case:

The path to continued consolidation appears clear and compelling. With the big three controlling only 35% of the $371 billion foodservice distribution market, massive fragmentation remains. PFG's proven ability to acquire and integrate distributors positions it perfectly to capture additional share. Each acquisition brings scale benefits in procurement, technology leverage, and route density that smaller competitors cannot match.

The independent restaurant channel represents PFG's fortress. With 46% of sales from independents versus one-third for US Foods, PFG dominates the most attractive customer segment. Independent restaurants value service, flexibility, and local relationships—areas where PFG's operating model excels. As consumers increasingly seek unique dining experiences over chains, this positioning becomes even more valuable.

Diversification across three segments—Foodservice, Vistar, and Convenience—creates resilience unmatched by pure-play competitors. Economic cycles affect each segment differently, smoothing earnings volatility. Cross-selling opportunities abound as convenience stores expand foodservice offerings and offices upgrade dining options. This platform approach creates competitive moats difficult to replicate.

Scale advantages in procurement and logistics compound with each acquisition. Larger purchasing volumes drive better supplier terms. Route density improves delivery economics. Technology investments spread across a bigger base. These scale benefits create a virtuous cycle where size begets efficiency, funding further growth.

Bear Case:

Margin pressure from competitive dynamics threatens profitability. With EBITDA margins of 2.58% versus US Foods' 4.6%, PFG operates with less cushion for error. Intense competition for independent restaurants could force pricing concessions. Labor shortages and wage inflation particularly impact distribution operations. Even small margin compression significantly impacts earnings given the low absolute margin levels.

Regulatory scrutiny on further consolidation could limit growth options. The FTC's successful challenge of the Sysco-US Foods merger established precedent for blocking large combinations. While PFG remains smaller than both competitors, continued acquisitions could trigger antitrust concerns, particularly in specific geographic markets or customer segments. The regulatory overhang might prevent the transformative deals needed for step-function growth.

Technology disruption from new entrants poses an existential threat. Amazon Business continues expanding into B2B distribution. Restaurant supply marketplaces connect suppliers directly with operators. Ghost kitchens and meal kit services bypass traditional distribution entirely. While barriers exist in foodservice, technology companies excel at identifying and exploiting inefficiencies in traditional industries.

Customer concentration in certain segments creates vulnerability. Large convenience chains wield significant negotiating power. The loss of a major customer could materially impact results. As customers consolidate, their bargaining power increases, potentially pressuring margins. The company's growth through acquisition also brings integration risk if cultural clashes or operational disruptions damage customer relationships.

XIII. Final Analysis & What's Next

The inevitability of further foodservice consolidation seems assured. Market forces—technology requirements, customer demands for efficiency, supplier consolidation—all push toward fewer, larger distributors. The question isn't whether consolidation continues but who captures the value. PFG's diversified platform and proven execution capabilities position it as a likely winner, though the path won't be linear.

Technology's role in distribution evolution accelerates. Digital ordering, now table stakes, evolves toward predictive analytics and automated replenishment. Warehouse automation addresses labor challenges while improving accuracy. Last-mile delivery innovations could reshape customer expectations. PFG must balance technology investment with its relationship-driven culture, using technology to enhance rather than replace human connections.

ESG and sustainability emerge as competitive differentiators. Customers increasingly demand transparency in sourcing, packaging reduction, and carbon footprint management. Food waste reduction through better forecasting and inventory management addresses both environmental and economic imperatives. PFG's scale enables investments in electric delivery vehicles, renewable energy, and sustainable packaging that smaller competitors cannot afford.

The ultimate question remains: who wins the distribution wars? The answer likely isn't a single victor but a stable oligopoly with 3-5 major players controlling 60-70% market share, similar to other mature distribution industries. PFG's diversified model positions it among the winners, though the company must execute on integration, technology, and operational excellence to realize this potential.

Looking forward, several catalysts could reshape PFG's trajectory. A successful integration of Cheney Brothers that exceeds synergy targets would validate the acquisition strategy. Renewed US Foods merger discussions could create transformational value or regulatory clarity. Economic recession might accelerate consolidation as smaller distributors struggle. Breakthrough technology applications could create competitive advantages or disruption threats.

The Richmond peddler's legacy lives on, transformed beyond James Capers' imagination. From horse-drawn wagons to algorithmic routing, from local suppliers to global sourcing, from family businesses to public corporations—the evolution continues. Performance Food Group stands at an inflection point where scale, technology, and execution capability converge. The next chapter promises to be as dramatic as the previous 139 years, with PFG positioned to write much of that story.

XIV. Recent News

In October 2024, Performance Food Group completed the acquisition of Cheney Bros., Inc., a leading independent broadline foodservice distributor based in Riviera Beach, Florida, creating a stronger presence in the Southeast region and providing additional distribution capacity, with Cheney Brothers generating approximately $3.2 billion in annual revenue and having approximately 3,600 employees operating five distribution centers in Florida and North Carolina.

The company's 2025 outlook includes expected results for José Santiago—a Puerto Rican foodservice distributor acquired in July 2024. This acquisition expanded PFG's presence in the Caribbean market, adding another geographic growth platform.

PFG raised its 2025 outlook to $62.5-63.5 billion in sales and $1.7-1.8 billion in EBITDA. These projections reflect confidence in the underlying business momentum and successful integration of recent acquisitions.

The competitive landscape continues evolving with all three major players pursuing acquisitions. Sysco acquired Jacmar and Edward Don, while US Foods bought IWC Foodservice, intensifying the battle for market share among the industry giants.

XV. Links & References

Company Resources: - Performance Food Group Investor Relations: investors.pfgc.com - Annual Reports and SEC Filings: SEC EDGAR Database - Quarterly Earnings Presentations: PFG Investor Events

Industry Analysis: - Technomic Foodservice Distribution Reports - Bloomberg Intelligence Food Distribution Analysis - FTI Consulting Foodservice Industry Studies

Historical References: - "The Performance Food Group Story" - Company Archives - Richmond Times-Dispatch Historical Archives - ID: The Information Source for Managers & DSRs Historical Articles

Books and Publications: - "The Box: How the Shipping Container Made the World Smaller" - Marc Levinson (distribution innovation context) - "Private Equity at Work" - Eileen Appelbaum and Rosemary Batt (PE ownership cycles) - "The Everything Store" - Brad Stone (Amazon's distribution ambitions)

Regulatory Documents: - FTC vs. Sysco/US Foods merger challenge documents (2015) - Hart-Scott-Rodino filing notifications - State regulatory approval documents for major acquisitions

Trade Publications: - Food Business News - Foodservice Equipment & Supplies Magazine - Progressive Grocer - Convenience Store News

Financial Analysis: - J.P. Morgan Equity Research Reports - Morgan Stanley Distribution Sector Analysis - Stephens Inc. Foodservice Coverage - Baird Equity Research Reports

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube