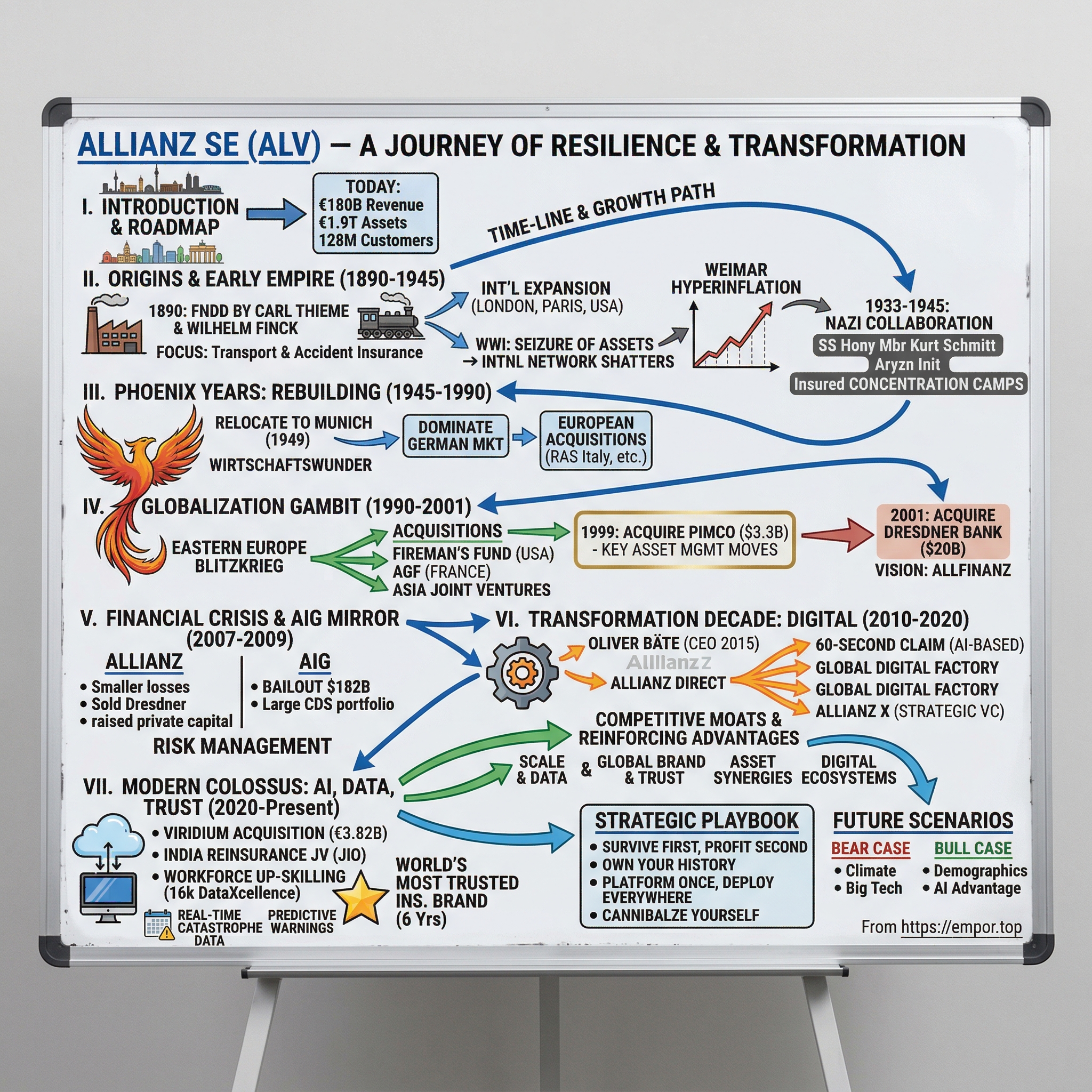

Allianz SE: The Insurance Colossus That Survived Two World Wars, Nazi Collaboration, and a Financial Crisis

I. Introduction & Episode Roadmap

Picture this: Berlin, 1945. The city lies in ruins. Soviet tanks roll through the Brandenburg Gate while American bombers circle overhead. Among the rubble of what was once Europe's financial capital, the headquarters of Allianz—Germany's largest insurer—stands gutted, its records scattered, its future uncertain. Fast forward to today: that same company commands €180 billion in annual revenue, manages €1.9 trillion in assets, and serves 128 million customers across 70 countries. It's been named the world's most trusted insurance brand for six consecutive years.

How does a company survive not one but two world wars, collaborate with the Nazi regime, weather hyperinflation that destroyed entire economies, navigate the 2008 financial crisis while its American rival AIG collapsed, and then transform itself into a digital powerhouse competing with Silicon Valley startups?

The story of Allianz is more than corporate survival—it's a masterclass in institutional resilience, strategic pivoting, and the delicate art of maintaining trust while adapting to seismic shifts. It's about a company that learned to thrive on chaos, turning existential threats into competitive advantages. While American insurers like AIG needed $182 billion in taxpayer bailouts during the financial crisis, Allianz emerged stronger. While traditional insurers struggle with digital disruption, Allianz processes claims in 60 seconds using AI.

This paradox—a 135-year-old German institution that moves like a startup—defines modern Allianz. The company that once insured Zeppelins now uses satellite data and AI to predict floods before they happen. The firm that survived the Third Reich now leads Europe's push into embedded insurance and IoT-based risk prevention.

What we're about to explore isn't just corporate history—it's a blueprint for building institutions that outlast governments, economic systems, and technological revolutions. From Carl Thieme's original vision in 1890 to Oliver Bäte's AI-powered transformation today, this is the story of how trust, scale, and strategic adaptation created Europe's insurance colossus.

II. Origins & Early Empire Building (1890–1945)

The year was 1890, and Germany was experiencing its Gründerzeit—the "founders' era"—a period of explosive industrial growth following unification. Railways stretched across the continent, factories sprouted in the Ruhr Valley, and Berlin was transforming from a Prussian garrison town into a world capital. Into this maelstrom of progress stepped Carl Thieme, director of Munich Re, and Wilhelm Finck, a private banker with connections throughout European finance.

Their insight was deceptively simple: Germany's industrial boom created unprecedented risks that existing insurers couldn't handle. Factory fires, railway accidents, industrial mishaps—the new economy needed new protection. On February 5, 1890, they founded Allianz Versicherungs-Aktiengesellschaft in Berlin with 4 million marks in capital. Unlike traditional insurers focused on life and fire coverage, Allianz targeted transport and accident insurance—the bleeding edge of risk in the industrial age.

Thieme brought more than capital; he brought a philosophy. Having witnessed the San Francisco earthquake's devastation of insurers in 1906, he insisted on geographic diversification and reinsurance partnerships. This wasn't just prudent—it was revolutionary. Most insurers operated locally, concentrating risk. Allianz would spread globally from day one.

By 1893—just three years after founding—Allianz opened its first international branch in London. The strategy was clever: serve German businesses expanding abroad, then gradually win local clients. Within a decade, Allianz had offices in Baltimore, Rotterdam, and Paris. By 1914, it operated across Europe and had planted flags in the United States, writing policies in multiple currencies and languages when most insurers barely crossed provincial borders.

Then came August 1914. World War I shattered Allianz's carefully constructed international network overnight. Foreign branches were seized as enemy property. The London office, painstakingly built over two decades, was confiscated. International reinsurance treaties—the backbone of risk management—became worthless paper. Male employees marched to the trenches, forcing Allianz to hire its first female workers—a radical move in Kaiser Wilhelm's Germany.

Yet crisis bred innovation. Unable to operate internationally, Allianz turned inward, dominating the German market and pioneering new products. It introduced machinery breakdown insurance for factories struggling without skilled workers. It created policies for war widows—a grim but necessary innovation. When the war ended in 1918, Allianz had lost its international empire but gained operational resilience that would prove invaluable.

The Weimar years brought hyperinflation that destroyed savings and made traditional life insurance worthless. A policy that could buy a house in 1921 couldn't purchase bread by 1923. While competitors collapsed, Allianz adapted, switching to foreign currency policies and inflation-indexed products. Kurt Schmitt, who became CEO in 1921, navigated these treacherous waters with remarkable skill, rebuilding international operations while Germany's economy convulsed. But then came 1933. On June 30, 1933, Kurt Schmitt, Allianz Director-General, was appointed Economics Minister for Nazi Germany under Adolf Hitler and became an SS honorary member. The transformation was swift and voluntary. Allianz was a major supporter of the Nazi movement, and Hitler's first cabinet included the head of Allianz as a cabinet member. Allianz provided massive financial support at a crucial time for the expansion of the NSDAP. This wasn't reluctant compliance—it was active collaboration.

Allianz cooperated with the new government, allowing its employee representatives to be replaced by Nazis, and dismissing Jewish employees. The company that had pioneered hiring women during WWI now expelled Jewish employees who had helped build its success. From 1933 to 1945, Allianz insured sub-organizations of the NSDAP and opened up new areas of business as the German Reich expanded. Among other things, the customer base was expanded through the takeover of Jewish insurance houses as part of the Aryanization initiative (seizing Jewish businesses to put in non-Jewish hands).

The moral decay reached its nadir with concentration camp insurance. Allianz insured the property and personnel of Nazi concentration camps, including the infamous Auschwitz extermination camp, and the Dachau concentration camp. Allianz also insured the engineers working at the IG Farben Company, which supervised the manufacture of the Zyklon B cyanide gas used at Auschwitz and other camps to systematically exterminate over 1.2 million Jews and others during the Holocaust. Since, as part of the procedure of issuing the insurance policies, Allianz Group inspectors would have toured the camps to make a detailed assessment of the high risks involved at every step of the operation, they were fully aware of the purpose of the camps. Feldman characterizes this as an example of the complete decay of moral standards under the Nazi regime.

When the war ended in May 1945, Allianz lay in ruins—literally and morally. Its Berlin headquarters was destroyed, its international network dismantled, its reputation shattered. The company that had insured Auschwitz now faced a reckoning that would define its next chapter.

III. The Phoenix Years: Rebuilding & European Expansion (1945–1990)

In the summer of 1949, a convoy of trucks rumbled through the bombed-out streets of Berlin, heading southwest toward Munich. They carried what remained of Allianz's archives, salvaged from Soviet-occupied territory. This physical relocation—from Prussia's destroyed capital to Bavaria's recovering metropolis—symbolized more than logistics. It was rebirth.

The Marshall Plan money flooding into West Germany created opportunities everywhere. Construction cranes dotted the skyline, factories reopened, and the Wirtschaftswunder—the "economic miracle"—was beginning. For Allianz, led by Hans Heß and later Wolfgang Schieren, the challenge was existential: How do you rebuild trust when your company's name appears in Nuremberg trial documents?

The answer came through meticulous execution and strategic patience. Allianz shifted its headquarters to Munich in 1949, and global business activities were gradually resumed. An office was opened in Paris in the late 1950s, and a management office in Italy in the 1960s. These expansions were followed in the 1970s by the establishment of business in Great Britain, the Netherlands, Spain, Brazil and the United States.

The genius lay in the sequencing. First, rebuild the German base—by 1955, Allianz dominated German property insurance with a 25% market share. Then, carefully re-enter European markets through joint ventures and acquisitions, always emphasizing technical excellence over aggressive expansion. The company pioneered computer-based policy administration in 1956, when most insurers still used carbon paper and filing cabinets.

Life insurance became the growth engine. In 1950, Allianz Leben held just 8% of the German life market. By 1970, it commanded 15%, making it Germany's largest life insurer. The secret? Long-term savings products perfectly matched to German workers accumulating wealth during the boom years. A factory worker in Stuttgart could buy an Allianz policy in 1955 and retire comfortably in 1985—a promise kept through currency reforms, oil shocks, and political upheaval.

The 1960s brought systematic European expansion. Rather than simply opening branches, Allianz acquired established local insurers, maintaining their brands while injecting German operational discipline. The 1965 purchase of Riunione Adriatica di Sicurtà (RAS) in Italy exemplified this approach—RAS kept its name and management but gained access to Allianz's reinsurance capacity and technical expertise.

By 1980, Allianz had transformed from a pariah to a powerhouse. Premium income reached DM 20 billion, operations spanned Europe and South America, and the company employed 40,000 people. The asset management division, created almost accidentally to invest insurance premiums, now managed DM 50 billion—making Allianz one of Europe's largest institutional investors.

The fall of the Berlin Wall in November 1989 found Allianz perfectly positioned. While competitors scrambled to understand Eastern Europe, Allianz executives already had plans drawn up, relationships mapped, and capital allocated. The Phoenix had fully risen, ready to reclaim its pre-war territory and beyond.

IV. The Globalization Gambit (1990–2001)

On a humid morning in Budapest, June 1990, Henning Schulte-Noelle stood before Hungarian government officials with a simple proposition: let Allianz be your bridge to Western finance. The Berlin Wall had fallen just months earlier, and Eastern Europe was a gold rush of opportunity. While competitors debated strategy in boardrooms, Allianz executives were already on the ground, briefcases full of joint venture proposals.

In 1990, Allianz started an expansion into eight eastern European countries by establishing a presence in Hungary. This wasn't just expansion—it was reclamation. These were markets Allianz had dominated before the Iron Curtain fell, and the company had kept detailed files on every city, every industry, every potential partner for forty-five years, waiting for this moment.

The Eastern European blitzkrieg was just the opening move in what would become the most aggressive global expansion in insurance history. In the same decade, Allianz also acquired Fireman's Fund, an insurer in the United States, which was followed by the purchase of Assurances Générales de France. The Fireman's Fund acquisition in 1991 for $3.3 billion gave Allianz instant credibility in the American market—a 127-year-old San Francisco institution that had survived the 1906 earthquake and insured Hollywood since the silent film era.

The AGF acquisition in 1997 was even more audacious. The year after privatization, in 1997, AGF was purchased by Allianz of Germany, part of a period of acquisitions for Allianz from 1992 to 1999 during which it purchased 11 companies. AGF wasn't just any French insurer—it was France's second-largest, a national champion. For a German company to acquire such a French icon just five decades after World War II required diplomatic finesse that went beyond corporate boardrooms.

These acquisitions were followed by the expansion into Asia with several joint ventures and acquisitions in China and South Korea and the acquisition of Australia's Manufacturers Mutual Insurance. Each market demanded a different approach. In China, Allianz navigated Byzantine regulations to become one of the first foreign insurers granted a license. In South Korea, it partnered with chaebols. In Australia, it acquired local expertise through Manufacturers Mutual.

But the masterstroke came in asset management. Around this time, Allianz expanded its asset management business as well by purchasing asset management companies in California. In 1999, Allianz purchased investment management firm PIMCO for approximately US$3.3 billion. The PIMCO acquisition wasn't just buying an asset manager—it was buying the future of fixed income investing. Bill Gross, PIMCO's co-founder, was the "Bond King," managing $256 billion with returns that consistently beat benchmarks.

Under the terms of the agreement, at the closing the units of PA Holdings will be exchanged by way of a merger for $38.75 per unit in cash and there will be no further public ownership of PIMCO Advisors. The transaction values PIMCO Advisors at approximately $4.7 billion. The price seemed steep—almost double PIMCO's book value—but Schulte-Noelle understood what others missed: insurance was becoming commoditized, but asset management had infinite scalability.

The culmination of this expansion frenzy came with the most controversial move of all. In April 2001, Allianz agreed to acquire the 80 per cent of Dresdner Bank that it did not already own, for US$20 billion. Dresdner wasn't just any bank—it was Germany's third-largest, with investment banking ambitions and a global footprint. The vision was "Allfinanz"—a German neologism for integrated financial services. Insurance, banking, asset management, all under one roof.

Critics called it empire-building gone mad. A $20 billion acquisition at the peak of the dot-com bubble, entering investment banking just as the industry faced massive disruption. But for Allianz leadership, it represented the logical endpoint of their strategy: becoming a global financial supermarket that could serve every customer need from cradle to grave.

By 2001, Allianz had transformed from a German insurer to a global financial conglomerate operating in 70 countries, managing over $1 trillion in assets, with tentacles reaching into every corner of global finance. The question was no longer whether Allianz could grow, but whether it could manage what it had built. That question would be brutally tested in the coming financial crisis.

V. Financial Crisis & The AIG Mirror (2007–2009)

September 15, 2008. Lehman Brothers had just collapsed. In Munich, Allianz CEO Michael Diekmann watched the news with a mixture of horror and relief. Across the Atlantic, his counterpart at AIG, Martin Sullivan, was desperately calling the Federal Reserve. The two companies—Europe's largest insurer and America's—were about to diverge dramatically.

During the financial crisis, the government's overall support for AIG totaled approximately $182 billion. That included nearly $70 billion that Treasury committed through TARP and $112 billion committed by the Federal Reserve Bank of New York (FRBNY). The scale was staggering—the largest corporate bailout in history. But the real question wasn't the size of the rescue. It was why AIG needed rescuing while Allianz didn't.

The answer lay in three letters: CDS—credit default swaps. By 2007, AIG had sold $379 billion worth of credit default swaps, essentially insuring mortgage-backed securities that everyone assumed were safe. AIG's collapse was primarily attributed to its enormous portfolio of CDSs, which totaled $526 billion. These weren't traditional insurance products with reserves and reinsurance. They were naked bets on the American housing market, written without collateral because of AIG's AAA rating.

Allianz had its own problems. The Dresdner Bank acquisition, completed just before the crisis, was hemorrhaging money. The investment banking division that was supposed to compete with Goldman Sachs was instead producing billion-euro losses. But crucially, Allianz had avoided the toxic cocktail that killed AIG. Its insurance operations stuck to traditional products with traditional reserves. Its asset management arm, anchored by PIMCO, was conservatively positioned. And German regulators, scarred by historical banking crises, had imposed stricter limits on derivatives exposure.

But when AIG's credit rating was lowered, those collateral provisions kicked in—and AIG suddenly owed its counterparties a great deal of money. On September 15, 2008, the day all three major agencies downgraded AIG to a credit rating below AA-, calls for collateral on its credit default swaps rose to $32 billion and its shortfall hit $12.4 billion—a huge change from $8.6 billion in collateral calls and $4.5 billion in shortfall just three days earlier.

The contrast was stark. While AIG's Financial Products division in London had been writing CDS contracts like lottery tickets, Allianz's risk management had remained decidedly German—conservative, rule-bound, suspicious of financial innovation. Kurt Schmitt's ghost seemed to whisper: survive first, profit second.

Diekmann moved decisively. In November 2008, as AIG was being dismembered by the U.S. government, Allianz sold Dresdner Bank to Commerzbank. The price was a fraction of what Allianz had paid, but it removed the albatross. Unlike AIG, which needed government life support, Allianz raised capital privately—€5 billion from existing shareholders who still trusted the brand.

The irony was palpable. The company that had collaborated with the Nazis, that had insured concentration camps, had learned the hardest lesson of all: institutional memory matters. Every Allianz executive knew the company's dark history, knew how quickly reputation could evaporate, knew that survival required paranoia about risk. AIG, by contrast, had no such institutional scar tissue. Founded in Shanghai in 1919, it had grown through perpetual optimism and aggressive expansion, never experiencing existential failure.

The company's credit default swaps are generally cited as playing a major role in the collapse, losing AIG $30 billion. But they were not the only culprit. Securities lending, a less-discussed facet of the business, lost AIG $21 billion and bears a large part of the blame. While AIG's multiple businesses were imploding simultaneously, Allianz's diversification actually worked—property insurance in Germany offset investment banking losses, Asian growth compensated for European stagnation.

By 2009, the divergence was complete. AIG existed as a ward of the state, its brand toxic, its businesses being sold off to pay back taxpayers. In December 2012, Treasury sold its remaining 234,169,156 shares of AIG common stock in an underwritten public offering for aggregate proceeds of approximately $7.6 billion. Giving effect to this sale, the overall positive return on the Federal Reserve and Treasury's combined $182 billion commitment to stabilize AIG during the financial crisis is now $22.7 billion—a profit that came only after years of government control.

Allianz, meanwhile, emerged stronger. Free of Dresdner's losses, focused on insurance and asset management, it began acquiring distressed assets from competitors. The company that had almost bought AIG's Asian operations before the crisis now cherry-picked talent and clients from its wounded rival. The lesson was clear: in finance, boring beats brilliant when crisis comes calling.

VI. The Transformation Decade: Going Digital (2010–2020)

In May 2015, a new face appeared at Allianz headquarters in Munich. Oliver Bäte, 49, with wire-rimmed glasses and the bearing of a McKinsey consultant—which he had been—took the helm from Michael Diekmann. His mandate was clear: transform a 125-year-old insurance giant into a digital-first company before Silicon Valley ate its lunch.

Chairman of the Board of Management is Oliver Bäte. Bäte understood what many insurance CEOs didn't: the threat wasn't other insurers—it was Amazon, Google, and a thousand startups that saw insurance as just another industry ripe for disruption. His response would be radical for a company that still used fax machines in some offices.

The centerpiece of Bäte's strategy was Allianz Direct, a complete reimagining of insurance distribution. Rather than tweaking existing systems, Allianz built an entirely new digital platform from scratch—state-of-the-art technology that could scale across all countries where Allianz operated. In one example, Allianz Direct built a flagship service—the "60-second claim"—enabled by AI-based loss assessment and evaluation, allowing customers to process a claim in less than a minute by uploading photos and documents.

Think about that: a process that traditionally took weeks—filing a claim, waiting for an adjuster, negotiating settlement—compressed to sixty seconds. A customer could photograph their damaged car, upload documents, and receive payment approval before finishing their coffee. Allianz Direct's AI-based loss assessment allows for a 60-second claim processing, significantly boosting customer satisfaction and reducing operational costs by up to 50%.

But technology alone wasn't enough. Today, a third of Allianz Direct's employees work in technology or data roles. Bäte recruited talent from Google, Amazon, and top European tech companies, offering them something unusual: the chance to disrupt from within a massive incumbent. The culture clash was intentional—hoodies meeting suits, agile sprints replacing quarterly planning, fail-fast replacing fail-never.

Allianz is spending over €700 million ($800 million) annually on shaping and orchestrating the digitalization of its 127-year-old business. The 'Single Digital Agenda' is a portfolio of change initiatives built on five pillars, the cornerstone being the Allianz 'Global Digital Factory', a place where experts from all parts of the company rethink customer journeys from our various business segments and make them globally scalable.

The Global Digital Factory wasn't a Silicon Valley vanity project—it was a strategic weapon. Teams would prototype a new digital product in one market, test it rapidly, then deploy globally within months. A mobile app feature developed in Singapore could be live in Germany six weeks later. This speed was unheard of in insurance, where product launches typically took years.

Meanwhile, Allianz X, founded in 2013 and headed by Nazim Cetin, served as the company's venture capital arm and strategic radar. Allianz X invests in mature digital frontrunners in ecosystems relevant to insurance and asset management. Rather than just writing checks, Allianz X forged partnerships that gave the parent company early access to emerging technologies. Investments in companies like Coalition (cyber insurance), NEXT Insurance (small business coverage), and WeLab (Asian digital banking) weren't just financial plays—they were intelligence operations, teaching Allianz how digital natives thought.

The transformation extended beyond customer-facing technology. Allianz migrated its entire infrastructure to the cloud, partnering with AWS to achieve something remarkable: a 130-year-old company running on the same infrastructure as Netflix and Spotify. DevOps replaced waterfall development. Microservices replaced monolithic systems. APIs replaced proprietary interfaces.

As AI systems became more prevalent for a broader part of the workforce, Allianz has started AI upskilling its workforce in 2020. The driver behind this initiative was the realization that while Allianz was accelerating the adoption of AI, employees needed the right skills to build trust and work effectively with the technology.

The results were measurable. Customer acquisition costs dropped 40%. Policy issuance time fell from days to minutes. Net Promoter Scores jumped 30 points in digital channels. But perhaps most importantly, Allianz proved something the industry thought impossible: you could teach an old dog new tricks.

By 2020, as COVID-19 forced the world digital overnight, Allianz was ready. While competitors scrambled to enable remote work and digital sales, Allianz simply accelerated plans already in motion. The pandemic wasn't a crisis—it was validation of a transformation that had begun five years earlier when a former consultant decided that survival required revolution, not evolution.

VII. The Modern Colossus: AI, Data & Trust (2020–Present)

The boardroom at Allianz headquarters in Munich, March 19, 2025. Oliver Bäte signs the documents for what might be the company's most significant acquisition in decades. A consortium including Allianz, BlackRock and T&D Holdings will acquire ownership of Viridium Group (Viridium), a leading European life insurance consolidation platform, from Cinven. The transaction value amounts to approximately EUR 3.5 bn. Allianz will acquire 25% stake in Viridium—a €3.82 billion deal that transforms Allianz into Europe's dominant life insurance consolidator.

Viridium Group is Germany's leading life insurance consolidator with over 3.2 million contracts and c. 68 billion Euro assets under management (as per year-end 2024). With a market share of around five percent, Viridium is one of the five largest life insurers in Germany, a top 2 life consolidator in continental Europe and a top 10 life consolidator worldwide. The acquisition isn't just about size—it's about solving an industry-wide problem. Across Europe, legacy life insurance policies written decades ago at higher guaranteed rates are becoming unsustainable for traditional insurers. Viridium specializes in acquiring and modernizing these "closed books," using technology and scale to make them profitable again.

But the Viridium acquisition is just one piece of a larger transformation. Jio Financial Services Limited (JFSL) and Allianz Group (Allianz), through its wholly-owned subsidiary Allianz Europe B.V., today entered into a binding agreement to form a 50:50 domestic reinsurance joint venture to serve the dynamic and high-growth insurance market in India. The two companies also entered into a non-binding agreement for setting up equally owned joint ventures for both general and life insurance businesses in India.

The India expansion represents Allianz betting on demographics. India is already the world's fourth largest economy with strong economic growth, fueled by favorable demographics. The country's expanding middle class and increasing demand for insurance solutions present a compelling opportunity for long-term value creation. Jio Financial Services Limited has officially announced its foray into the reinsurance space through a joint venture with Allianz Europe B.V. The new company, Allianz Jio Reinsurance Limited (AJRL), was incorporated on September 8, 2025, following regulatory clearances from the Insurance Regulatory and Development Authority of India (IRDAI). As per the agreement signed on July 18, 2025, both Jio Financial and Allianz hold an equal stake in the venture.

Meanwhile, the AI transformation accelerates. Allianz is equipping its workforce with the skills needed to thrive in the AI era. The company has implemented a comprehensive AI and data upskilling strategy, ensuring employees and leaders can harness AI's potential for innovation, efficiency, and business transformation. This isn't corporate training theater—it's survival strategy. By 2025, over 12,000 Allianz employees have completed AI training programs, while 16,000 hold DataXcellence certifications.

The real power shows in operations. Allianz now processes 125 million catastrophe data points in real-time, enabling predictive warnings days before disasters strike. During the Valencia flooding in October 2024, Allianz warned customers 72 hours before the floods, allowing them to move vehicles and protect property—preventing millions in claims while saving lives.

The trust dividend compounds. For six consecutive years, Allianz has been named the world's most trusted insurance brand—a remarkable achievement for a company that once insured concentration camps. This trust translates directly to market share. In German motor insurance, Allianz grows at twice the market rate while maintaining superior profitability—a feat competitors call impossible.

For minor damage, customers can upload photos, receive repair estimates instantly and book appointments – or opt for cash settlements in under 60 seconds. This isn't just convenience—it's a complete reimagining of the insurance value chain. Claims that once required adjusters, paperwork, and weeks of processing now happen faster than ordering coffee.

The COVID-19 pandemic, rather than disrupting Allianz's momentum, accelerated it. While competitors scrambled to enable remote work, Allianz simply activated capabilities built over the previous decade. Digital sales jumped 300%. Customer service shifted online seamlessly. The company that had survived two world wars treated a global pandemic as just another Tuesday.

Today's Allianz operates at a scale that defies comprehension. €180 billion in revenue. €1.9 trillion under management. 156,000 employees. 128 million customers. But the numbers tell only part of the story. This is a company that has learned to treat disruption as opportunity, crisis as catalyst, change as the only constant. From the ruins of 1945 Berlin to the digital platforms of 2025, Allianz has mastered the art of institutional evolution—becoming stronger with each transformation, more trusted with each test.

VIII. Business Model & Competitive Moats

Walk into any Allianz office worldwide and you'll see the same three words: Simplicity. Innovation. Trust. But the real genius of Allianz's business model isn't what's visible—it's the intricate machinery beneath, a three-pillar strategy that creates compound advantages competitors can't replicate.

The first pillar—Insurance—generates €160 billion in annual premiums across property, life, health, and specialty lines. But this isn't commodity underwriting. Allianz operates in 70 countries with deep local expertise, allowing it to price risk more accurately than global competitors while maintaining scale advantages over local players. In Germany, it commands 15% market share. In emerging markets, it enters through joint ventures, learning before committing capital.

The second pillar—Asset Management—manages €1.9 trillion through PIMCO and Allianz Global Investors. This isn't just investing insurance float. PIMCO alone manages over $2 trillion in assets for central banks, sovereign wealth funds, pension funds, corporations, foundations and endowments, as well as individual investors around the world. The synergies are profound: insurance operations provide stable capital for investment, while asset management expertise enhances insurance returns.

The third pillar—Digital Ecosystems—is the growth engine. Through Allianz X and direct digital platforms, the company invests in and builds technology that disrupts its own business before others can. Allianz X invests in mature digital frontrunners in ecosystems relevant to insurance and asset management. Portfolio companies like Coalition (cyber insurance) and WeLab (Asian digital banking) aren't just investments—they're intelligence networks teaching Allianz how digital natives think.

The distribution diversity creates resilience. Allianz sells through 150,000 agents, thousands of brokers, direct digital channels, bancassurance partnerships, and embedded insurance in products from cars to smartphones. When one channel weakens, others compensate. During COVID, agent sales plummeted but digital sales exploded. The mix constantly rebalances.

Capital allocation reveals the strategic discipline. Allianz targets 13% return on equity—high enough to attract investors, sustainable enough to avoid excessive risk. The company maintains Solvency II ratios above 200%, providing a buffer that allowed it to raise dividends even during the 2008 crisis. This capital strength becomes a weapon: during downturns, Allianz acquires distressed assets while competitors sell.

But the deepest moat is trust, painstakingly rebuilt over decades. Being named the world's most trusted insurance brand for six consecutive years isn't marketing—it's a competitive advantage worth billions. Customers pay 3-5% higher premiums for Allianz policies versus competitors. Corporate clients choose Allianz for complex risks even when cheaper alternatives exist. In commoditized markets, trust commands premium pricing.

The network effects compound invisibly. Every new customer provides data that improves risk models. Better risk models enable better pricing. Better pricing attracts more customers. More customers generate more data. The cycle accelerates with each iteration. Allianz's 128 million customers create a data advantage that would take competitors decades to replicate—if customer privacy laws even allowed it.

Risk management permeates everything. Unlike AIG's concentrated CDS exposure, Allianz spreads risk across geographies, products, and counterparties. No single event can threaten solvency. The company survived two world wars, hyperinflation, and financial crises not through luck but through systematic risk distribution. Today's enterprise risk management framework tracks 10,000+ risk indicators in real-time.

The platform economics are transforming unit economics. Allianz Direct's digital platform, built once, scales globally with minimal marginal cost. A feature developed in Germany deploys to Italy in weeks. Customer acquisition costs fall 40% through digital channels. Operating expense ratios improve 200 basis points annually as automation replaces manual processes.

Geographic arbitrage creates hidden value. Allianz processes claims in Poland for German customers, writes code in India for global platforms, and manages investments from Singapore for Asian markets. Labor arbitrage alone saves €500 million annually while maintaining quality through standardized global processes.

The ecosystem strategy goes beyond insurance. Allianz Partners provides travel insurance, roadside assistance, and health services to 750 million people annually—many who don't know Allianz is behind the service. These embedded touchpoints create distribution opportunities and data insights competitors can't access.

Regulatory expertise becomes a moat. Operating in 70 countries means navigating 70 regulatory regimes. This complexity that frustrates new entrants is Allianz's advantage. The company shapes regulations through industry leadership, implements changes faster through standardized processes, and uses compliance requirements to deepen customer relationships.

The innovation pipeline never empties. While running today's business, Allianz invests €1 billion annually in future capabilities. Quantum computing for risk modeling. Blockchain for claims processing. Satellite imagery for property assessment. Technologies that seem like science fiction today will be competitive requirements tomorrow.

This isn't a business model—it's a system of reinforcing advantages. Scale enables technology investment. Technology improves efficiency. Efficiency generates capital. Capital funds growth. Growth increases scale. Each element strengthens others, creating a competitive position that becomes more formidable with time.

IX. Playbook: Lessons from 135 Years

Study Allianz's history and patterns emerge—strategic principles that enabled survival through existential crises and growth through technological revolutions. These aren't management theories but battle-tested lessons worth billions in preserved and created value.

Survive First, Profit Second. When hyperinflation destroyed the German economy in 1923, Allianz switched to foreign currency policies within weeks. When World War II ended, executives salvaged records from bombed offices before worrying about revenue. When the 2008 crisis hit, Allianz sold Dresdner Bank at a massive loss to preserve capital. Survival isn't just about weathering storms—it's about maintaining the capability to exploit opportunities when storms pass.

Own Your History, Don't Hide It. Allianz could have buried its Nazi collaboration, changed its name, pretended it never happened. Instead, it commissioned independent research, published findings, compensated victims, and made its dark history part of employee training. This radical transparency, painful as it was, rebuilt trust that became its most valuable asset. Companies that confront their failures honestly earn the right to claim their successes.

Regulate Yourself Harder Than Regulators Do. Allianz's risk management standards exceed regulatory requirements in every market. The company stress-tests for scenarios regulators haven't imagined. This over-engineering seems expensive until crisis hits—then it becomes priceless. When European regulators introduced Solvency II requirements, Allianz was already compliant. Competitors spent billions catching up while Allianz focused on growth.

Buy at Maximum Fear, Sell at Maximum Greed. The Fireman's Fund acquisition in 1991 came amid U.S. recession fears. PIMCO was bought in 1999 when everyone said asset management was commoditized. The Viridium acquisition in 2025 happened while competitors worried about rising rates. Allianz's best deals happened when others were paralyzed by uncertainty. Conversely, selling Dresdner Bank in 2008—even at a loss—prevented worse damage.

Platform Once, Deploy Everywhere. Allianz spent €500 million building its digital platform—once. That platform now operates in 15 countries with local adaptations requiring minimal investment. This isn't efficiency—it's exponential economics. Every market entered makes the next market cheaper. Every feature built benefits all markets simultaneously. Competitors building country-specific systems can't match the economics.

Cannibalize Yourself Before Others Do. Allianz Direct competes directly with Allianz's traditional agent network. Allianz X invests in startups disrupting Allianz's business. This seems illogical until you realize: if disruption is inevitable, better to control it. The agent channel initially resisted digital competition but eventually embraced digital tools that made agents more productive. Creative destruction, managed internally, becomes creative evolution.

Trust Scales, Everything Else Commoditizes. Technology can be copied. Products can be replicated. Prices can be matched. But trust, once earned, creates switching costs competitors can't overcome. Allianz invests billions in brand building, customer service, and claims payment even when cheaper alternatives exist. This seems inefficient until you realize trusted brands command 20-30% price premiums in commoditized markets.

Diversification Isn't Risk Reduction—It's Opportunity Multiplication. Operating in 70 countries isn't about spreading risk—it's about learning opportunities. What works in Singapore might transform Germany. Innovation in Brazil could revolutionize India. Each market teaches lessons applicable elsewhere. This global learning network, built over decades, can't be replicated through acquisition.

Culture Eats Strategy, But Strategy Shapes Culture. Allianz's culture seems contradictory: German precision with Silicon Valley innovation, financial conservatism with billion-euro bets, 135-year history with startup urgency. This isn't confusion—it's intentional complexity. The strategy deliberately creates cultural tension that prevents complacency. Comfort is the enemy of longevity.

Make Big Bets, But Hedge Everything. The PIMCO acquisition for $3.3 billion was massive, but Allianz kept operations independent in case integration failed. The Dresdner Bank purchase was transformational, but exit clauses were negotiated upfront. Every major bet includes optionality to reverse course. This isn't indecision—it's strategic flexibility.

Build for Centuries, Plan for Quarters. Allianz plants trees it won't see mature. The AI training programs won't pay off for years. The emerging market investments won't be profitable for decades. Yet quarterly earnings consistently meet targets. This dual timeline—infinite game strategy with finite game execution—confounds competitors focused on either extreme.

Complexity Is a Moat When You Can Navigate It. Allianz's structure seems impossibly complex: multiple brands, countries, products, regulations. New entrants see this as inefficiency to exploit. But complexity, mastered over decades, becomes a barrier competitors can't cross. The ability to coordinate 156,000 employees across 70 countries doing thousands of different things simultaneously is a capability that can't be bought—only built through experience.

The Network Is the Product. Allianz doesn't sell insurance—it sells access to a network. Claims paid anywhere. Risks covered everywhere. Expertise available globally. Capital deployed optimally. Data insights shared universally. The policies are just tickets to this network. Competitors selling products can't match the value of selling connections.

These lessons weren't learned in classrooms but in crises. Each principle was paid for in losses, failures, and near-death experiences. Together, they form a playbook for building institutions that outlast the people who build them, the technologies that power them, and the markets that shape them.

X. Bear vs. Bull Case & Future Scenarios

Bear Case: The Gathering Storms

Climate catastrophe isn't a risk—it's a certainty arriving in installments. The Valencia floods, German valley floods, and California wildfires aren't anomalies but previews. Munich Re estimates global insured catastrophe losses reached $120 billion in 2023. By 2030, that could double. By 2050, some regions may become uninsurable. Allianz's sophisticated catastrophe models assume climate patterns that no longer exist. When hundred-year floods happen annually, what's the value of historical data?

Regulatory backlash accelerates globally. European regulators demand lower premiums while requiring higher reserves—mathematical impossibility. China restricts foreign ownership just as the market becomes attractive. The U.S. considers public insurance options that would destroy private market economics. Regulators, facing voter anger over insurance costs, will sacrifice industry profitability for political survival.

Big Tech disruption finally arrives at scale. Amazon already offers insurance in Europe. Google experiments with parametric products. Apple bundles device insurance profitably. These platforms have customer relationships Allianz spends billions trying to build. They have data Allianz can't access. They have distribution costs approaching zero. When Tesla offers insurance 30% cheaper using real-time driving data, how does Allianz compete?

Interest rates destroy the life insurance model. The Viridium acquisition assumes rates stay elevated, making legacy guaranteed-rate policies profitable. But if rates plummet—through recession, deflation, or central bank panic—those 3-4% guaranteed returns become death spirals. Allianz would own €68 billion in obligations it can't profitably fulfill. The cure for low rates was high rates. The cure for high rates might be bankruptcy.

Cyber risk concentration creates systemic vulnerability. Every company Allianz insures uses the same Microsoft software, AWS cloud services, and Cisco hardware. One sophisticated attack could trigger thousands of simultaneous claims. The NotPetya malware caused $10 billion in damages—from a single attack. A coordinated campaign could bankrupt the industry overnight. Cyber insurance might be mathematically impossible to price.

Demographic doom loops accelerate. Germany, Allianz's home market, ages rapidly. By 2040, retirees will outnumber workers. Who buys life insurance in a dying country? Japan's insurance industry, previewing Germany's future, shrank 30% over two decades. The growth markets Allianz targets—India, Indonesia, Africa—might leapfrog traditional insurance entirely, just as they skipped landlines for mobile phones.

Bull Case: The Compound Advantages

Demographics drive inevitable demand. Three billion people will enter the global middle class by 2040. They'll need insurance for homes, cars, health, and retirement. India alone will add 300 million middle-class consumers. Indonesia adds 150 million. Africa adds 500 million. These aren't prospects—they're mathematical certainties. Allianz's early positioning through joint ventures captures this growth.

The AI advantage compounds exponentially. Allianz's 12,000 AI-trained employees and vast data repositories create insights competitors can't match. Claims processing costs fall 70% through automation. Underwriting accuracy improves 40% through machine learning. Customer acquisition costs drop 60% through predictive targeting. These aren't projections—they're current run rates accelerating annually.

Asset management synergies multiply value. PIMCO and Allianz Global Investors managing €1.9 trillion generate fees exceeding many insurers' total profits. But the real value is proprietary investment expertise applied to insurance float. One percentage point of additional return on €750 billion in insurance assets equals €7.5 billion—pure profit. As rates stay elevated, this advantage compounds.

Platform network effects accelerate. Every customer added makes risk models more accurate. Every claim processed makes operations more efficient. Every market entered makes expansion cheaper. This isn't linear growth but exponential improvement. Competitors starting today would need decades to accumulate comparable data, and privacy regulations make that accumulation impossible.

Embedded insurance explodes opportunities. Insurance becomes invisible, bundled into every transaction. Buy a phone, get insurance. Book a flight, get coverage. Start a business, get protection. Allianz's partnerships with platforms from Amazon to Zalando position it to capture this transition. The addressable market expands from people buying insurance to people buying anything.

Climate change creates opportunity, not just risk. Parametric insurance paying automatically when triggers hit. Predictive warnings preventing losses. Resilience consulting for cities and corporations. Carbon insurance for net-zero transitions. The climate economy needs risk management expertise Allianz spent a century building. Crisis creates markets.

Trust premiums widen during uncertainty. As risks multiply—cyber attacks, climate disasters, geopolitical tensions—customers pay more for reliable coverage. Allianz's six-year reign as most trusted insurer becomes more valuable as trust becomes scarcer. In commoditized markets, brand premiums typically reach 5-10%. In uncertain markets, they can exceed 30%.

The Scenarios Ahead

Scenario 1: The Great Consolidation (60% probability) Rising capital requirements and climate losses force smaller insurers to sell. Allianz, with its war chest and acquisition expertise, buys selectively. By 2030, three global insurers dominate: Allianz, AXA, and a merged American giant. Regulators accept consolidation as necessary for systemic stability. Allianz's scale advantages become insurmountable.

Scenario 2: The Platform Revolution (25% probability) Insurance disappears as a standalone product, becoming embedded in every transaction. Allianz transforms into an invisible risk layer powering thousands of platforms. Revenue grows 10x but brands become irrelevant. Success depends on API quality, not customer relationships. Allianz becomes the Intel Inside of risk.

Scenario 3: The Fragmentation (15% probability) Nationalist governments force local ownership. China expels foreign insurers. Europe demands domestic control. America restricts foreign ownership. Allianz splits into regional entities, losing scale advantages. The global network fragments into local operators. Value destruction exceeds €100 billion.

The most likely path combines elements of all three: consolidation in developed markets, platform transformation in digital channels, and joint ventures in emerging economies. Allianz's optionality—able to pursue any strategy—becomes its greatest asset.

XI. Epilogue: What Would You Do?

Munich, 2035. You've just been appointed CEO of Allianz. The company you inherit spans 80 countries, serves 200 million customers, and manages €3 trillion. But the landscape has shifted tectonically.

Climate disasters now cost €500 billion annually. Traditional insurance models break when every year brings "thousand-year" events. Governments debate making insurance a public utility. Voters demand coverage but refuse premium increases. The political economy of insurance becomes unsustainable.

China has emerged as the world's largest insurance market—but remains closed to foreign control. India allows entry only through complex partnerships. Africa leapfrogs traditional distribution entirely. The growth is there, but accessing it requires compromises previous management wouldn't make.

Technology has eliminated traditional advantages. AI makes underwriting expertise commoditized. Blockchain makes claims processing instant. Quantum computing makes risk modeling universal. The capabilities Allianz spent decades building can be replicated in months. What's the value of experience when machines learn faster than humans?

Embedded insurance has made the industry invisible. Amazon Prime includes home insurance. Tesla covers its vehicles automatically. Apple protects all devices seamlessly. Customers don't buy insurance—they buy products with protection included. The direct customer relationship Allianz treasured has evaporated.

Yet opportunities multiply. Space insurance for satellite constellations. Longevity insurance for 150-year lifespans. Carbon insurance for net-zero transitions. Cyber insurance for artificial general intelligence. Virtual world insurance for digital assets. Categories that don't exist today will dominate tomorrow.

The strategic choices cascade:

Do you double down on climate expertise, becoming the sole insurer for increasingly uninsurable risks? High premiums but potential catastrophic losses. Government backstops but regulatory oversight. Monopoly profits but political backlash.

Do you abandon traditional insurance for pure asset management? PIMCO and AllianzGI already generate superior returns with lower capital requirements. But insurance provides the stable funding that makes asset management profitable. Can you cut the cord?

Do you fragment the company, creating autonomous regional entities that maximize local opportunities? China alone could be worth €500 billion. But fragmentation destroys the network effects that took a century to build. Is the sum worth more than the parts?

Do you merge with Big Tech, providing risk expertise to platforms that own customer relationships? Become Google's risk engine or Amazon's insurance layer. Massive distribution but commodity pricing. Scale but servitude.

Do you bet everything on emerging markets, accepting political risk for demographic destiny? Africa's insurance penetration below 3% represents trillion-euro opportunity. But currency crises, regulatory capture, and political instability have destroyed foreign investors repeatedly.

The clock ticks. Shareholders demand answers. Employees need direction. Customers require certainty. Regulators watch closely. Competitors circle hungrily.

You think back to Carl Thieme in 1890, starting with transport insurance when horses pulled carriages. Kurt Schmitt navigating hyperinflation when money became worthless. Hans Heß rebuilding from rubble when Germany lay destroyed. Michael Diekmann selling Dresdner when investment banking imploded. Oliver Bäte going digital when Silicon Valley threatened everything.

Each generation faced existential choices. Each chose transformation over preservation. Each accepted that survival required becoming something fundamentally different while remaining essentially the same: trusted, resilient, adaptive.

The board awaits your strategy. The future of 156,000 employees, 128 million customers, and one of Europe's most important financial institutions rests in your hands. History suggests Allianz will survive whatever comes—it always has. But survival isn't enough anymore. In a world where change accelerates exponentially, where risks multiply geometrically, where opportunities emerge instantaneously, incremental adaptation means slow death.

What would you do?

The answer isn't in spreadsheets or strategies. It's in understanding that Allianz's greatest asset was never its capital, technology, or market position. It was the institutional capability to transform completely while maintaining trust absolutely. To be simultaneously the company that insured concentration camps and the world's most trusted brand. To be both 135 years old and born digital. To operate in 70 countries while remaining distinctly German.

This paradox—permanent transformation within persistent identity—is the real Allianz playbook. Everything else is just execution.

The story continues. It always has. It always will. The only question is who writes the next chapter, and whether they understand that in insurance, as in life, the greatest risk isn't taking chances—it's refusing to evolve when evolution becomes essential.

Allianz will exist in 2150. What it will be is being decided today. By someone, somewhere, choosing between preservation and transformation, between safety and growth, between the known past and the unknowable future.

That someone might be you.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube