UTI Asset Management Company: India's Mutual Fund Pioneer

I. Introduction & Episode Setup

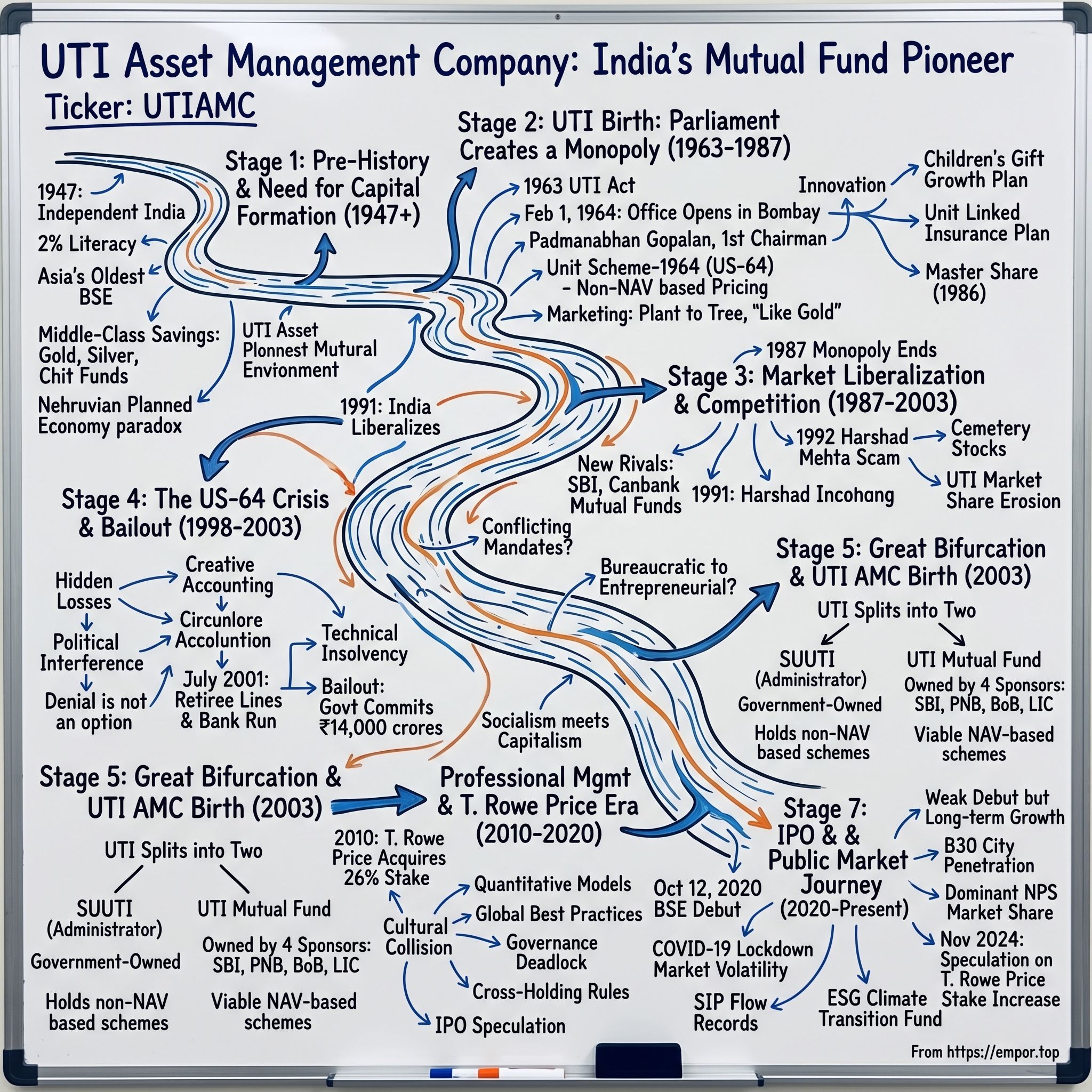

Picture this: It's 1963 in New Delhi, and inside the hallowed halls of Parliament, legislators are debating something unprecedented—should the government create a financial institution to help ordinary Indians invest in the stock market? The very idea seems paradoxical in Nehru's socialist India, where private capital markets are viewed with suspicion and the commanding heights of the economy are firmly in state hands. Yet here they are, crafting legislation to birth what would become India's first mutual fund.

Fast forward six decades. That government experiment—the Unit Trust of India—has morphed into UTI Asset Management Company, a publicly-traded powerhouse managing over ₹17 trillion in assets. Walk into any small town in India today, from the dusty lanes of Rajasthan to the humid villages of Kerala, and you'll find UTI's distinctive logo adorning modest offices where millions of Indians entrust their savings. This is the story of how a socialist-era monopoly transformed into a modern financial services giant, survived near-death experiences, and emerged as a testament to India's economic evolution. Today, UTI AMC manages assets of over ₹15.56 lakh crores (₹19.36 trillion including all businesses as of June 2024), making it one of India's asset management behemoths. In the mutual fund industry, it commands a market share of 5.04% on a quarterly average AUM basis, while dominating the National Pension System with a 27.4% market share. The company's shares trade at a market capitalization of ₹16,996 crores, testament to its evolution from state-owned entity to market-driven enterprise.

But here's what makes this story truly remarkable: UTI isn't just a business transformation tale. It's a mirror reflecting India's entire economic journey—from socialist planning to market capitalism, from financial repression to liberalization, from government paternalism to retail empowerment. Every pivot in UTI's history coincides with a watershed moment in India's development. Every crisis it faced revealed fundamental tensions in how a democracy balances market forces with social objectives.

As we embark on this deep dive, we'll uncover how a simple idea—helping ordinary Indians invest their savings—became entangled with politics, survived existential crises, and ultimately emerged as a case study in institutional resilience. We'll explore how UTI built trust in a country where financial literacy was minimal, how it navigated the treacherous transition from monopoly to competition, and how it reinvented itself after a bailout that shook the nation's faith in financial institutions.

The questions we'll answer go beyond UTI itself: What happens when a government creates a financial institution with conflicting mandates? How does an organization transform its DNA from bureaucratic to entrepreneurial? Can a company with political baggage compete against nimble private players? And perhaps most intriguingly—in an era of fintech disruption and passive investing, what's the playbook for a 60-year-old institution to remain relevant?

Welcome to one of Indian finance's most epic sagas—where socialism meets capitalism, where trust battles technology, and where the past constantly collides with the future.

II. Pre-History: India's Financial Markets & The Need for Capital Formation

The year is 1947. As the last British ships sail away from Bombay's harbor, independent India awakens to a harsh reality. The crown jewel of the British Empire has been left with less than 2% literacy rate, a life expectancy of 32 years, and an economy that produces just 3% of global output despite housing 15% of humanity. The Bombay Stock Exchange exists—it's actually Asia's oldest, established in 1875—but it might as well be on Mars for the average Indian, who earns less than ₹250 per year.

Jawaharlal Nehru, India's first Prime Minister, faces an impossible equation. The country needs massive capital formation to build steel plants, dams, and factories—the "temples of modern India" as he romantically calls them. But where will this capital come from? Foreign investors are wary of a newly independent nation with socialist leanings. The wealthy Indian merchants and industrialists who do exist are concentrated in a few families—the Tatas, Birlas, and Dalmias—and they're already fully deployed. The vast majority of Indians are subsistence farmers with no surplus to invest.

Into this vacuum steps an unlikely protagonist: the household savings of middle-class Indians. Even in poverty, Indians save. It's cultural, almost pathological—a response to centuries of uncertainty. They save in gold hidden under mattresses, in silver vessels passed through generations, in informal chit funds run by neighbors. The Reserve Bank of India estimates that household savings, though individually tiny, collectively represent nearly 8% of national income by the late 1950s. But this money sits idle, stuffed in steel almirahs or buried in backyards, contributing nothing to productive investment.

The intellectual architects of India's planned economy—P.C. Mahalanobis, V.K.R.V. Rao, and others huddled in the Planning Commission—recognize this paradox. They need these savings to flow into productive assets, but how do you convince a population that has seen banks fail during the Depression, that witnessed the chaos of Partition, to trust financial institutions with their life savings?

The global context provides both inspiration and warning. In America, mutual funds have existed since the 1920s, with Massachusetts Investors Trust pioneering the model. Britain has its unit trusts. But these evolved organically in mature capitalist economies with established property rights and regulatory frameworks. India is attempting something audacious: creating a mass investment vehicle in a poor, largely illiterate country with weak institutions and deep skepticism of financial markets.

By 1960, the limitations of relying solely on government resources and foreign aid become apparent. The Second Five-Year Plan (1956-61) faces a severe foreign exchange crisis. Industrial production is growing, but not fast enough. The stock market exists but remains the playground of a few thousand speculators in Bombay and Calcutta. Of the 1,203 companies listed on Indian stock exchanges, most are closely held by promoter families. Free float is minimal, manipulation is rampant, and retail participation is virtually non-existent.

The government's solution is characteristically Indian—a fusion of socialist planning with market mechanisms. The Unit Trust of India would be designed to encourage saving by providing various classes of investors the facility of investing their money in units of the Trust. Unlike Western mutual funds that emerged from private initiative, this would be a state-created entity with an explicit developmental mandate.

Finance Minister Morarji Desai, a austere Gandhian who neither drinks nor smokes and famously advocates urine therapy, becomes an unlikely champion of capital markets. In parliamentary debates of 1962-63, he argues that small savers need a vehicle that offers "the advantages of reasonable return, liquidity and capital appreciation" while being backed by government credibility. The opposition raises prescient concerns: Won't political interference corrupt investment decisions? How can the same government that distrusts private capital manage public money in private markets?

These questions would haunt UTI for decades. But in 1963, optimism prevails. India is young, confident, and ready to experiment. The Unit Trust of India Act is drafted with ambitious objectives: mobilize savings, provide returns to small investors, and channel funds into productive investments that align with national priorities. It's social engineering through financial engineering—a uniquely Indian approach to capital formation.

As parliamentarians debate the bill, nobody imagines that this institution will one day manage trillions of rupees, survive multiple crises, and outlast the very economic system that created it. They're simply trying to solve an immediate problem: how to fund India's industrialization using the small savings of its people. In doing so, they're about to create India's first mass market financial product and forever change how Indians think about investing.

III. The Birth of UTI: Parliament Creates a Monopoly (1963-1987)

On February 1, 1964, a small office opens on the second floor of Bombay's Reserve Bank building. The brass nameplate reads "Unit Trust of India," but the handful of employees inside joke that it should say "Uncharted Territory of India." They have no computers, no precedents, and no real idea if anyone will actually buy what they're selling. The chairman, Padmanabhan Gopalan, a career RBI bureaucrat, sits at a wooden desk calculating by hand what the initial units should be priced at. After much deliberation, he settles on ₹10 per unit—affordable enough for a schoolteacher, yet substantial enough to feel like real investing.

The Unit Trust of India was established by an Act of Parliament in 1963, initially functioning under the regulatory and administrative control of the Reserve Bank of India. In 1964, UTI launched its first investment scheme Unit Scheme-1964, a product that would become both UTI's greatest success and eventual near-undoing. The scheme's structure was revolutionary for its time yet contained fatal flaws that wouldn't manifest for decades. Units could be purchased and redeemed at prices fixed by UTI itself, not based on net asset value—a deviation from global mutual fund practices that reflected both paternalistic protection of investors and dangerous opacity.

The early marketing campaigns reveal the challenge of selling an abstract financial product to a tangible-asset-obsessed population. UTI's first advertisements, appearing in vernacular newspapers, don't mention returns or portfolios. Instead, they show illustrations of a small plant growing into a mighty tree, with the tagline "Your small savings, the nation's big progress." Branch managers are instructed to explain units as "like gold, but productive"—an analogy that resonates in a culture where gold is the ultimate store of value.

Building distribution in pre-liberalization India requires ingenuity. UTI can't simply hire agents (private agency is suspect) or rely on banks (they barely exist outside cities). Instead, it pioneers a uniquely Indian model: leveraging the postal system. By 1970, you can buy UTI units at 8,000 post offices across India. The postmaster in a small Tamil Nadu village, who also sells stamps and delivers telegrams, now moonlights as a mutual fund distributor. It's financial inclusion decades before the term exists.

The investment philosophy during these monopoly years reflects the era's commanding heights economy. UTI's portfolio reads like a roster of Nehruvian industrialization: Steel Authority of India, Bharat Heavy Electricals, Hindustan Machine Tools. These aren't necessarily the best investments—many are chronically loss-making—but they align with national priorities. Fund managers, mostly deputees from RBI and state banks, see themselves as nation-builders, not alpha-generators.

In 1978, UTI was de-linked from the RBI and the Industrial Development Bank of India (IDBI) took over the regulatory and administrative control. This shift from central bank to development bank oversight signals a subtle but important change—UTI is now expected to more directly support industrial development, adding another layer to its already complex mandate.

The numbers tell a story of steady, almost inevitable growth. From ₹5 crores in 1964, assets under management grow to ₹100 crores by 1970, ₹500 crores by 1975, and ₹2,000 crores by 1985. By the end of 1988, UTI had Rs. 6,700 crores of assets under management. These aren't spectacular returns—often barely beating fixed deposits—but that's not the point. UTI is creating equity culture in a country where "playing the share market" is considered barely more respectable than gambling.

The product innovations during this period seem quaint today but were revolutionary then. The UTI Children's Gift Growth Plan (1970) lets parents invest for their children's education—the first goal-based investment product in India. The Unit Linked Insurance Plan (1971) combines investment with insurance, predating the ULIP boom by three decades. The Reinvestment Plan (1976) automatically reinvests dividends, introducing Indians to the power of compounding.

But the most audacious move comes in 1986 with the launch of Master Share—India's first IPO-focused scheme. In a masterstroke of financial innovation, UTI essentially becomes the retail gateway to primary markets. When companies go public, UTI subscribes on behalf of millions of small investors who would otherwise never access these offerings. It's democratization of capitalism, socialist-style.

The relationship between UTI and the government during these years is complex, often contradictory. On paper, UTI is autonomous. In practice, it's an extension of state policy. When the government needs to shore up a failing public sector company, UTI mysteriously increases its investment. When industrial houses close to the ruling party need capital, UTI's funds flow their way. These decisions are never explicitly directed—that would be too crude. Instead, they happen through "informal suggestions" and "aligned thinking."

The employees who lived through these years describe a unique culture—part bank, part government office, part startup. The head office in Bombay develops its own rituals: the 4 PM tea where investment decisions are debated, the Saturday morning sessions where branch managers call in their weekly collection numbers, the annual conference where the Chairman reads out a speech that's equal parts financial report and nation-building manifesto.

By 1987, UTI has achieved something remarkable: it has 4.5 million investors, more than the entire population of New Zealand. In small towns across India, "UTI agent" becomes a respectable profession. Families frame their Unit Certificates next to pictures of gods. The orange and blue UTI logo becomes as recognizable as national symbols.

Yet beneath this success, structural problems fester. The fixed-price mechanism of US-64 means UTI is essentially running a Ponzi scheme, using new investments to pay old redemptions. The portfolio is laden with sick public sector units that will never recover. Political interference in investment decisions has created massive concentration risks. Most dangerously, investors have been told their money is as safe as government deposits—a promise that will soon be tested.

As 1987 draws to a close, UTI stands at an inflection point. The monopoly that began in 1963 is about to end, with the Government of India permitting public sector banks and financial institutions to sponsor mutual funds. For 24 years, UTI has had the Indian mutual fund market to itself. Now, competition is coming. The question isn't whether UTI can compete—it's whether an institution designed for a controlled economy can survive in a market economy.

IV. Market Liberalization & Competition Arrives (1987-2003)

In July 1991, as India pledges its gold reserves to avoid sovereign default, finance minister Manmohan Singh stands before Parliament to deliver a budget speech that will reshape the nation. He quotes Victor Hugo: "No power on earth can stop an idea whose time has come." That idea is liberalization, and for UTI—comfortable in its monopolistic cocoon—it's about to become an existential challenge.

But the winds of change had started blowing four years earlier. UTI's monopoly of the mutual fund industry ended in 1987 when the Government of India permitted public sector banks and financial institutions to sponsor mutual funds. The first competitor arrives in November 1987: SBI Mutual Fund, backed by the country's largest bank. By 1993, six public sector banks have launched mutual funds. They're followed by insurance companies, and then, in a move that truly signals the new era, private sector funds enter in 1993.

The competitive landscape that emerges is fascinatingly complex. Public sector funds like SBI and Canbank Mutual Fund have vast branch networks but carry the same bureaucratic DNA as UTI. The private players—Kothari Pioneer (a joint venture with Pioneer of the US), Morgan Stanley, Jardine Fleming—bring sophisticated investment processes but lack distribution reach. UTI watches from its perch, initially dismissive. "Let them come," says one senior executive in a 1992 interview. "We have 30 years of trust. That can't be replicated overnight."

This confidence isn't entirely misplaced. While competitors struggle to gather assets, UTI continues its innovation streak. The Master Gain scheme of 1992 becomes India's first growth-oriented mutual fund, moving away from the dividend-obsession of Indian investors. The India Fund, launched in 1986 but gaining traction now, becomes the vehicle for foreign investors to access Indian markets before full liberalization. It's listed on the New York Stock Exchange, making UTI arguably India's first global financial institution.

Yet the same liberalization that creates opportunities also exposes weaknesses. As the Bombay Stock Exchange Sensex rockets from 1,000 in 1990 to 4,500 by 1992 during the Harshad Mehta-fueled bull run, UTI faces an impossible situation. Its flagship US-64 scheme, still selling at artificial prices, sees massive inflows from investors expecting equity-like returns. But the scheme's portfolio, heavy with government securities and public sector stocks, can't deliver such returns without taking enormous risks.

The pressure manifests in increasingly questionable decisions. UTI begins investing in dubious companies, often at the behest of well-connected promoters. A former fund manager, speaking anonymously, recalls: "We would get calls from Delhi saying 'look favorably' at certain stocks. Nobody ordered us directly—that would leave a paper trail. But the message was clear." The portfolio starts accumulating what traders colorfully call "cemetery stocks"—shares of companies that are essentially dead but haven't been buried yet.

The 1992 securities scam provides the first major shock. While UTI isn't directly implicated, the revelation that banks and financial institutions have been manipulating government securities markets sends tremors through the mutual fund industry. Investors, for the first time, question whether their money is truly safe. UTI responds by launching India's first gilt fund, focusing solely on government securities—an ironic move given that these very securities were at the heart of the scam.

Competition intensifies through the 1990s. Private funds introduce concepts alien to Indian investors: sectoral funds, index funds, systematic investment plans. Kothari Pioneer launches India's first open-ended diversified equity fund. Morgan Stanley brings quantitative models. Templeton introduces global investing. UTI, constrained by its legacy structure and political oversight, struggles to respond with similar agility.

The numbers tell a story of gradual erosion. UTI's market share, 100% in 1987, falls to 80% by 1995, then 64% by 2000. More worryingly, it's losing the narrative war. Young professionals in Bangalore's emerging IT sector prefer private funds with their sleek marketing and promises of market-beating returns. The old slogan of "steady returns with safety" sounds increasingly antiquated in an India intoxicated with liberalization's possibilities.

Under Unit Scheme-1964, UTI had sold and repurchased units at prices fixed arbitrarily by its management rather than on the basis of actual value of underlying assets. Investment decisions based on political compulsions taken by those in key positions, exacerbated by political instability in the 1990s and the consequent market rout, took a toll on the Unit Scheme-1964.

By 1998, the situation becomes critical. The Asian Financial Crisis has crashed Indian markets. The nuclear tests at Pokhran have triggered international sanctions. Foreign investors are fleeing. The Sensex falls from 4,500 to 2,900. UTI's equity portfolio, built during the bull years, is underwater. More dangerously, US-64's declared NAV of ₹13.50 per unit masks an actual value closer to ₹8. The fund is technically insolvent, but nobody wants to acknowledge it.

The political economy of this period adds layers of complexity. Coalition governments, changing every few years, each bring their own priorities. Industrial houses curry favor by subscribing to UTI schemes, expecting quid pro quo investments in their companies. State governments pressure UTI to invest in their infrastructure projects. The institution designed to mobilize savings for national development has become a vehicle for crony capitalism.

Yet even as storm clouds gather, UTI maintains its innovation momentum. It launches India's first index fund in 1999, tracking the Sensex. The Monthly Income Plan introduces regular income generation for retirees. The Venture Capital Fund supports the nascent IT industry. These products show that buried within the bureaucratic behemoth are fund managers who understand where markets are heading.

The irony is palpable. At the very moment UTI faces existential crisis, India's mutual fund industry is exploding. Assets under management across the industry grow from ₹47,000 crores in 1993 to ₹1,00,000 crores by 2000. Retail participation is increasing. Financial literacy is improving. The market UTI created is thriving—but UTI itself is dying.

As the millennium approaches, denial gives way to reality. In closed-door meetings, RBI officials acknowledge that US-64 needs urgent restructuring. The finance ministry recognizes that a UTI collapse could trigger systemic crisis—there are now 20 million investors whose life savings are at stake. The question isn't whether to intervene, but how to do so without destroying public faith in financial markets.

The stage is set for one of Indian finance's most dramatic episodes: a crisis that will test whether an institution too big to fail can be saved without moral hazard, whether public trust once broken can be rebuilt, and whether a government-created entity can truly transform into a market-driven enterprise.

V. The US-64 Crisis & Government Bailout (1998-2003)

On a humid Mumbai morning in July 2001, thousands of retirees queue outside UTI offices across the country, clutching their Unit Scheme-64 certificates like lifelines. Many have been standing since 4 AM. Some faint in the heat. Police battalions are deployed to control crowds. The scene resembles a bank run from the Great Depression, except this is happening in 21st century India, in an economy supposedly modernizing at breakneck speed.

The crisis that culminates in these desperate scenes has been building for years, hidden behind creative accounting and political denial. By 2001, US-64's actual NAV has plummeted to ₹6.30 per unit while UTI continues declaring it at ₹14.25. The gap—nearly ₹8 per unit across 600 crore units—represents a hole of ₹48,000 crores, roughly 2% of India's GDP. To put this in perspective, it's as if America's largest money market fund suddenly announced it had lost $400 billion but hadn't told anyone.

The anatomy of this disaster reads like a textbook on how not to run a financial institution. Through the 1990s, US-64 had morphed from a balanced fund into a speculative vehicle, making increasingly desperate bets to maintain its dividend payouts. A forensic audit later reveals holdings in 400 companies, many of them small, illiquid stocks with no business being in a scheme meant for conservative investors. There are investments in companies that exist only on paper, in projects that will never be completed, in promoters who have already fled the country.

Former UTI chairman P.S. Subramanyam, brought in to clean up the mess, later describes finding investment files that read like fiction: "Companies with three employees valued at hundreds of crores. Real estate deals where the land didn't exist. Loans to entities that were just post office boxes." The political interference hasn't just been subtle anymore—by the late 1990s, it has become brazen. Ministers call directly demanding investments in their constituency projects. Chief ministers threaten to ban UTI operations unless their favored companies receive funding.

The government's initial response exemplifies the paralysis that often grips Indian policymaking during crises. In 1998, when the problems first become undeniable, Finance Minister Yashwant Sinha announces a dividend cut for US-64—the first in its history. The market reaction is swift and brutal. Redemptions accelerate. UTI is forced to sell its good assets to meet withdrawals, further deteriorating the portfolio quality. It's a death spiral in slow motion.

By 2001, denial is no longer an option. The new Finance Minister, Jaswant Singh, faces a stark choice: let UTI collapse and risk systemic contagion, or engineer a bailout that will cost taxpayers dearly. The debates in North Block are fierce. Reform-minded economists argue for allowing market discipline. Politicians worry about 20 million angry voters. The RBI warns of broader financial instability.

The bailout package announced in 2002 is staggering in its complexity and scale. The government commits ₹14,000 crores immediately, with potential exposure of up to ₹30,000 crores. US-64 is frozen—no new subscriptions, phased redemptions over time. Other schemes are segregated into NAV-based funds that will continue. Most dramatically, UTI itself will be split into two entities: the old, sick portfolio under government administration, and a new UTI to be run on commercial principles.

The human cost is devastating. In Surat, a diamond merchant who invested his entire retirement corpus of ₹50 lakhs commits suicide. In Chennai, a widow discovers her husband's secret US-64 investments, now worth a fraction of what he paid. Across India, middle-class families realize their parents' savings, accumulated over decades of frugal living, have evaporated. The Reserve Bank Governor later admits: "We failed in our basic duty—protecting ordinary savers from systemic malpractice."

The political theater surrounding the crisis is equally dramatic. Parliamentary sessions turn into shouting matches. The opposition demands criminal prosecution of UTI officials and their political masters. Investigative journalists uncover trails leading to the highest offices. The Central Bureau of Investigation raids UTI offices, seizing documents that reveal the depth of rot. Several senior executives are arrested, though most cases eventually collapse due to lack of evidence or political intervention.

Yet amidst this chaos, something remarkable happens. The government's bailout, despite its cost, is structured to minimize moral hazard. Investors in US-64 don't receive full redemption immediately—they must wait, accepting lower returns. The message is clear: government backing doesn't mean zero risk. Other UTI schemes, those operating on NAV basis, are protected but must prove their viability. It's a delicate balance between preventing panic and ensuring accountability.

The restructuring process itself becomes a case study in institutional transformation under pressure. McKinsey consultants fly in from New York, working alongside Indian Administrative Service officers who've never heard of modern portfolio theory. Software systems are upgraded overnight—literally, in some cases, with engineers working through weekends to shift from paper ledgers to computerized records. New risk management frameworks are implemented, with daily VAR calculations replacing the old system of "gut feel" investing.

International observers watch with fascination and horror. The Economist calls it "India's Enron moment." The Financial Times warns of broader emerging market contagion. Yet foreign investors, paradoxically, see opportunity. If India can manage a crisis of this magnitude without systemic collapse, perhaps its financial system is more resilient than believed. Foreign institutional investor flows, after an initial dip, actually increase in 2002-03.

The role of the media during this period deserves special mention. Financial journalists, many covering their first major crisis, struggle to explain complex financial products to readers who barely understand basic investing. Television channels, still nascent in their business coverage, resort to sensationalism. "YOUR MONEY IS GONE" screams one headline, causing panic redemptions even in healthy schemes. UTI takes to publishing daily advertisements with actual portfolio holdings, trying to counter rumors with transparency.

The legal aftermath drags on for years. Public interest litigations challenge the bailout's constitutionality. Investors file class-action suits demanding full compensation. Criminal cases against UTI officials wind through courts, most ending in acquittals due to the difficulty of proving intentional fraud versus incompetence. The Serious Fraud Investigation Office's report, when finally released, runs to 10,000 pages but leads to few convictions.

By 2003, the immediate crisis has passed, but its scars remain. The erstwhile Unit Trust of India was bifurcated with the non-NAV based schemes brought under government purview and other under SEBI. The former came under SUUTI (Administrator of the Specified Undertaking of The Unit Trust of India) and the latter became UTI Mutual Fund. Public trust in mutual funds has plummeted—industry assets actually decline in 2002-03, the first such instance. UTI's reputation, built over four decades, lies in tatters.

Yet from this nadir emerges an unexpected opportunity. The crisis forces reforms that modernization advocates had sought for years. SEBI tightens mutual fund regulations. NAV-based pricing becomes mandatory. Independent trustees gain real power. Risk management evolves from afterthought to obsession. The Indian mutual fund industry, purged of its worst practices, prepares for its next phase of growth.

The US-64 crisis represents more than financial failure—it's a watershed in India's economic evolution. It demonstrates that even in a democracy with powerful vested interests, market discipline can prevail. It shows that institutions can be reformed under pressure. Most importantly, it proves that Indian investors, despite suffering losses, won't abandon financial markets if treated with transparency and respect. The crisis that nearly destroyed UTI ultimately catalyzes its transformation into a modern asset management company.

VI. The Great Bifurcation & Birth of UTI AMC (2003)

February 1, 2003, marks a second independence day for UTI—exactly 39 years after its first office opened, the institution is reborn as two separate entities. The symbolism isn't lost on employees gathered at the Mumbai headquarters. Some wear black badges in protest, viewing the bifurcation as dismemberment of a national institution. Others distribute sweets, celebrating escape from political interference. The schizophrenia captures perfectly the contradictions UTI has embodied since inception.

The mechanics of the split are staggeringly complex. Imagine dividing a conjoined twin where the organs are not just shared but impossibly intertwined. Restructuring of Unit Scheme-1964 brought the large equity holdings along with other assets including real estate and 25 assured-return schemes to the Specified Undertaking of The Unit Trust of India (SUTTI). This entity, fully government-owned, inherits the toxic legacy: US-64's obligations, assured return schemes that promise returns mathematics can't deliver, and real estate investments ranging from prime Mumbai properties to vacant land in districts nobody can locate on a map.

The new UTI Mutual Fund, meanwhile, gets the viable NAV-based schemes and, crucially, the right to use the UTI brand. But it faces an unusual ownership structure: State Bank of India, Punjab National Bank, Bank of Baroda, and Life Insurance Corporation of India each hold 18.24% stakes. Four powerful institutions with often conflicting interests must now collectively steer a ship that nearly sank. It's corporate governance by committee—a structure that management textbooks would call unworkable.

The first CEO of the restructured entity, U.K. Sinha (later SEBI chairman), faces challenges that would break most executives. The technology infrastructure is archaic—some branches still use paper ledgers. The employee base of 8,000 includes many who joined expecting government job security, not private sector accountability. The distribution network, while extensive, operates on relationships and trust built during monopoly years, not competitive service. Most critically, the brand is toxic—"UTI" has become synonymous with betrayal in middle-class vocabulary.

Yet Sinha and his team accomplish something remarkable: they make boring beautiful. Instead of chasing hot products or promising spectacular returns, they focus on operational basics. Branches are modernized—computers replace ledgers, air conditioning replaces ceiling fans. Customer service, previously an oxymoron, becomes an obsession. Employees undergo training that seems radical for its simplicity: answer phones within three rings, respond to complaints within 48 hours, smile when greeting customers.

The investment philosophy undergoes similar back-to-basics reform. The cowboys who made speculative bets are replaced with process-driven professionals. Risk management, previously non-existent, becomes embedded in every decision. A new investment committee structure ensures no single person can override collective judgment. The portfolio is cleaned up ruthlessly—dubious holdings are sold regardless of losses, concentration limits are enforced, and quality becomes the watchword.

The numbers during this transition period tell a story of gradual stabilization. Assets under management, which had peaked at ₹64,000 crores in 2001, fall to ₹38,000 crores by 2003 as investors flee. But the bleeding slowly stops. By 2004, AUM stabilizes. By 2005, growth returns. The equity market boom of 2003-2007 helps, but UTI's recovery isn't just market beta—its market share, which had fallen to 35%, stabilizes around 25%.

The relationship with the four sponsors evolves in unexpected ways. Rather than micromanaging, they provide strategic cover. When private competitors poach talent with astronomical salaries, the sponsors approve retention bonuses. When technology upgrades require massive capital expenditure, they provide backing. Most importantly, they resist political pressure for directed investments. The very fact that there are four sponsors, no single one dominant, creates a balance that prevents capture.

Meanwhile, SUUTI—the "bad bank" holding toxic assets—begins its own unexpected journey. As of 2016, SUUTI had stakes in 43 listed and 8 unlisted companies valued at more than Rs. 60,000 Crores. These holdings, accumulated through decades of directed investments, include substantial stakes in blue-chip companies like Axis Bank, ITC, and Larsen & Toubro. What was considered toxic in 2003 becomes valuable as India's economy booms. The government, through patient holding, eventually recovers far more than the bailout cost.

The cultural transformation within UTI AMC during these years is profound. The old headquarters, with its babu culture of long lunches and longer tea breaks, transforms into something resembling a modern financial institution. Young MBAs join, bringing energy and ambition. Performance-linked bonuses replace automatic annual increments. The average age drops from 48 to 38 within five years.

Distribution strategy evolves from dependence to diversification. While maintaining relationships with traditional distributors, UTI begins building direct channels. Online platforms are launched—primitive by today's standards but revolutionary for an institution where forms were previously only available in physical branches. Independent financial advisors, previously ignored for being too small, are courted aggressively. The message is clear: UTI needs distributors more than they need UTI.

Product innovation, frozen during the crisis years, resumes with vengeance. But instead of copying competitors, UTI leverages its unique strengths. The UTI Retirement Benefit Pension Fund targets the massive government employee market that private players can't access. The Children's Career Plan resurrects the goal-based investing philosophy from the 1970s but with modern portfolio construction. The Banking & Financial Services Fund capitalizes on UTI's deep understanding of the sector through its sponsor relationships.

The regulatory environment also evolves favorably. SEBI, under new leadership, implements reforms that level the playing field. Entry loads are banned, forcing AMCs to compete on performance rather than distributor commissions. Expense ratios are capped, preventing excessive fee extraction. Disclosure norms are tightened, making it harder to hide poor performance. These reforms hurt all players initially but ultimately benefit those, like UTI, focused on long-term wealth creation rather than asset gathering.

By 2007, four years after bifurcation, UTI AMC has achieved something remarkable: it's profitable, growing, and relevant. The company that many wrote off as a relic has demonstrated resilience that surprises skeptics. International investors take notice. In 2008, T. Rowe Price, the Baltimore-based global asset manager, begins discussions about acquiring a strategic stake. It's validation that UTI has transformed from political tool to professional enterprise.

The employees who lived through this period describe it with mixture of trauma and pride. "We went from being untouchables to being respected again," says a senior fund manager. "Every day, we had to prove we weren't the old UTI. Every investment decision, every customer interaction, every basis point of return—everything was scrutinized. It was exhausting but also liberating."

Yet challenges remain enormous. Private sector competitors like HDFC and ICICI Prudential are growing faster. Foreign players like Franklin Templeton and Fidelity have superior investment processes. The distribution landscape is shifting toward banks and online platforms where UTI has limited presence. Most fundamentally, the question remains whether an institution with government DNA can truly compete in a capitalist marketplace.

The answer would come through an unlikely partnership with one of America's most respected investment houses—a collaboration that would bring global expertise to an Indian institution while preserving its local character. The next phase of UTI's evolution was about to begin.

VII. Professional Management & The T. Rowe Price Era (2010-2020)

The January 2010 boardroom at UTI's Mumbai headquarters buzzes with an energy unseen in years. Executives from Baltimore-based T. Rowe Price, impeccably dressed and jet-lagged, sit across from representatives of India's four state-owned sponsors. The deal on the table seems straightforward: T. Rowe Price will acquire a 26% stake in UTI Asset Management Company Limited and UTI Trustee Company for INR 6.5 billion (US $142.4 million). But what unfolds over the next decade will be anything but simple—a case study in cultural collision, bureaucratic inertia, and the perils of public-private partnership.

T. Rowe Price acquired a 6.5% stake from each of the original four stockholders—State Bank of India, Punjab National Bank, Bank of Baroda, and Life Insurance Corporation of India—who would each retain an 18.5% stake. The structure made T. Rowe Price International the single largest shareholder, theoretically giving it significant influence. James A.C. Kennedy, T. Rowe's CEO, speaks optimistically about "forming a cooperative relationship with UTI" and notes "their general investment approach and client-focused model lends itself to a solid cultural fit" while looking forward to "a mutually beneficial relationship to share expertise".

The rationale seems compelling. India was one of the fastest-growing countries by GDP in the world, and millions of people were moving up to join the middle class, poised to allocate more of their savings to mutual funds, away from bank deposits and gold. Ed Bernard, T. Rowe's vice chairman, captures the zeitgeist: "If I look out the next ten to 15 years, the Indian fund industry will have a higher growth rate than the U.S. fund industry".

What T. Rowe Price brings to the table is substantial: sophisticated risk management systems, quantitative research capabilities, global investment expertise, and a reputation for long-term thinking dating back to 1937. Their investment philosophy—focusing on fundamental research and consistent style—aligns perfectly with what UTI needs to compete against nimble private players. The Americans envision transferring best practices, upgrading technology, and professionalizing operations.

The initial honeymoon period sees genuine progress. T. Rowe Price executives embed themselves in Mumbai, working alongside UTI teams. New research processes are implemented—sector specialists are hired, company visit protocols are established, and investment committee structures are strengthened. The equity research team, previously ad-hoc, is organized into systematic coverage universes. Fixed income, traditionally managed by relationship rather than analytics, gets quantitative models.

Product development accelerates with T. Rowe's input. UTI launches international funds giving Indian investors access to global markets, leveraging T. Rowe's expertise in managing cross-border portfolios. Systematic investment plans are redesigned with behavioral finance insights from Baltimore. The technology infrastructure, creaking under legacy systems, receives much-needed investment—portfolio management systems are upgraded, risk analytics are implemented, and straight-through processing is introduced.

Yet beneath this operational progress, fundamental tensions simmer. T. Rowe spent the next ten years butting heads with the co-owners of the Indian business, including taking them to court because they couldn't agree on who would manage the business. The upshot: UTI was left without a CEO for four of those ten years, and its market share nearly halved.

The governance structure proves to be the Achilles heel. Each sponsor—SBI, PNB, BoB, and LIC—has its own agenda. SBI wants UTI to complement its banking operations. LIC sees potential synergies with insurance. The banks view it as a fee-generating opportunity. Meanwhile, T. Rowe Price wants professional management focused solely on investment excellence. When CEO positions become vacant, the sponsors cannot agree on successors. Board meetings devolve into stalemates. Strategic decisions requiring unanimous consent languish for months.

Two of the Indian shareholders, along with T. Rowe Price, pushed for an IPO, but Life Insurance Corp. of India was dallying with the idea of absorbing UTI into its eponymous fund company, which would have effectively squeezed out T. Rowe. As all shareholders failed to agree to the listing, the matter went to the Ministry of Finance for a "no objection certificate." It never came.

The cultural divide extends beyond boardroom politics. T. Rowe's American executives, accustomed to data-driven decision-making and quarterly performance reviews, encounter an organization where relationships matter more than metrics. A senior UTI manager, speaking off-record, describes the friction: "They would send 100-page presentations for every decision. We would make the same decision over tea in five minutes based on 30 years of market experience. Neither approach was wrong, but they couldn't coexist."

The regulatory environment adds another layer of complexity. In 2018, a new securities rule required that the Indian owners of UTI, all of whom were also running their own asset management companies, cut their UTI stakes to less than 10 percent. This cross-holding regulation, designed to prevent conflicts of interest, suddenly makes the sponsor structure untenable. Each sponsor must choose: divest UTI or shut down their own asset management arms. The deadline creates urgency but also paralysis—nobody wants to sell at a discount. Despite the governance deadlock, operational progress continues. UTI AMC emphasizes digital transformation, enhancing its online platforms to provide seamless access to investment services. The company reports a significant increase in digital transactions, with a year-on-year growth of 32.4% in online mutual fund transactions for FY 2023. The partnership with global technology providers transforms backend operations—business-critical, customer-facing applications are hosted on AWS, with managed cloud environment driving enhanced productivity, while VMware-based public cloud platform reduces the cost and complexities of conventional DR practices.

The distribution strategy undergoes radical transformation. Recognizing that bank-led distribution favors competitors with banking parentage, UTI pivots toward independent financial advisors and digital channels. Nearly 48% of equity/hybrid gross sales were mobilized through digital platforms in Q4FY25, reflecting successful digital integration and marketing automation. The company builds proprietary platforms—'UTI Buddy' for distributors and 'UTI HART' for analytics—that level the playing field against better-funded competitors.

Geographic expansion becomes a strategic differentiator. While competitors chase wealthy metros, UTI leverages its historical presence in smaller cities. UTI AMC continues to deepen its presence in B30 (beyond top 30) cities, with 22% of monthly average AUM in March 2025 originating from these regions—well above the industry average of 18%. The addition of 68 branches in Tier-2 and Tier-3 locations during FY25 has driven net folio additions of 0.9 million.

The retirement solutions business emerges as an unexpected bright spot. UTI's legacy relationships with government entities translate into mandates for managing Employee Provident Fund Organization (EPFO) corpus and Postal Life Insurance funds. The National Pension System, where UTI maintains dominant market share, becomes a growth engine as pension awareness increases. These institutional mandates provide stable fee income insulated from retail market volatility.

Yet the fundamental governance issues remain unresolved. The Officers' Association challenges the T. Rowe Price stake sale in court, arguing that foreign investors cannot hold stakes in trustee companies under the UTI Repeal Act. Legal battles drag through the Bombay High Court and Supreme Court, creating regulatory overhang. Meanwhile, SEBI fines the sponsor banks for not reducing their cross-holdings as required, adding another layer of complexity.

The impact on business performance is undeniable. Market share in mutual funds continues sliding—from over 10% when T. Rowe entered to around 5% by 2020. Talented fund managers leave for competitors offering clearer career paths. Product launches are delayed awaiting board approvals that never come. The company that pioneered mutual funds in India increasingly looks like a relic, unable to capitalize on the industry's explosive growth.

By 2019, resolution becomes imperative. The sponsor banks face regulatory deadlines to reduce stakes. T. Rowe Price, frustrated after a decade of deadlock, pushes for an IPO as the only viable exit. The government, recognizing that continued paralysis helps nobody, finally provides the long-awaited no-objection certificate. The stage is set for UTI's next transformation—from quasi-government entity to public company.

The T. Rowe Price era, despite its frustrations, leaves important legacies. Investment processes are institutionalized. Risk management becomes embedded in culture. Digital capabilities, though late, position UTI for the future. Most importantly, the partnership proves that even with the best intentions and complementary strengths, cross-border financial services partnerships require more than operational synergies—they need aligned governance, compatible cultures, and patient capital willing to navigate regulatory mazes.

As 2020 approaches, UTI stands at another crossroads. The IPO promises to resolve ownership deadlock, bring market discipline, and provide growth capital. But questions remain: Can a company with such complex history attract public investors? Will market forces finally unleash UTI's potential? Or will the weight of legacy continue dragging down an institution that should be leading India's savings revolution?

VIII. IPO & Public Market Journey (2020-Present)

On October 12, 2020, UTI Asset Management Company made its public market debut at the Bombay Stock Exchange. As the opening bell rang at 9:15 AM, UTI shares opened at ₹490, an 11.5% discount to the IPO price of ₹554, before falling to ₹470. For the institution that introduced mutual funds to India 57 years ago and once monopolized the industry, it was a disappointing public market validation.

The IPO journey had begun months earlier in a vastly different world. When UTI filed its draft papers in December 2019, COVID-19 was an unknown term, markets were buoyant, and the asset management industry was riding high on financialization of savings. By the time the IPO opened on September 29, 2020, India was emerging from one of the world's strictest lockdowns, markets had witnessed unprecedented volatility, and investor sentiment had turned cautious.

The offer structure itself tells a story of transformation. This isn't a fresh issue raising growth capital—it's entirely an offer for sale of 38,987,081 shares by existing shareholders. State Bank of India, Life Insurance Corporation, and Bank of Baroda each sell 10,459,949 shares, while Punjab National Bank and T. Rowe Price each offload 3,803,617 shares. The sponsors are finally exiting, forced by regulatory requirements but also recognizing that continued government ownership constrains UTI's potential.

The subscription numbers reveal lukewarm interest: overall subscription of just 2.31 times, with QIBs at 3.34x, HNIs at a concerning 0.93x, and retail at 2.32x. For context, quality IPOs in India routinely see subscriptions exceeding 50 times. The grey market premium, which had started at ₹50-60, evaporates as listing approaches. Institutional investors, burned by governance issues and declining market share, remain skeptical.

Yet the weak debut masks underlying strengths that would emerge over time. The company is debt-free, generates consistent cash flows, and trades at a P/E of 17.37 based on annualized latest earnings—significantly cheaper than peers HDFC AMC (35.19x) and Nippon Life AMC (35.08x). The valuation discount reflects skepticism about government-linked entities, concerns about market share erosion, and questions about growth potential.

CEO Imtaiyazur Rahman, who took charge in 2019 after yet another leadership vacuum, faces the challenge of convincing public market investors that UTI can compete effectively. His strategy focuses on three pillars: leveraging UTI's unmatched distribution in smaller cities, dominating the pension and retirement solutions space, and digital transformation to acquire younger investors. "We're not trying to out-HDFC HDFC," he says in a post-listing analyst call. "We're building on strengths others can't replicate. "The post-IPO journey proves more eventful than the lukewarm debut suggested. After touching a low of ₹470 in October 2020, UTI shares embark on a remarkable recovery. By August 2021, they hit an all-time high of ₹1,216.55, driven by the broader financialization theme playing out in Indian markets. The pandemic, paradoxically, accelerates mutual fund adoption as retail investors, stuck at home with surplus savings and easy digital access, discover equity investing.

The stock was trading at its highest level since November 2021. The stock had hit a record high of Rs 1,216.55 on August 31, 2021. This peak coincides with peak optimism about India's asset management industry. SIP (Systematic Investment Plan) flows are hitting records monthly. The narrative is compelling: India's mutual fund penetration at 15% of GDP compares to 100%+ in developed markets, suggesting massive growth potential.

But 2022 brings reality checks. Global interest rates rise, foreign investors flee emerging markets, and Indian equities correct sharply. UTI's stock falls to ₹896 by June 2022, giving back most of its gains. The company's fundamental challenges resurface—market share continues eroding, expense ratios remain elevated compared to private peers, and fund performance remains mediocre in key categories.

The management responds with strategic initiatives that gradually gain traction. Digital transformation accelerates—nearly 48% of equity/hybrid gross sales were mobilized through digital platforms in Q4FY25, reflecting successful digital integration and marketing automation. The company launches 'UTI Buddy' and 'UTI HART' platforms, enabling effective cross-selling and upselling.

Geographic expansion into smaller cities becomes a differentiator. UTI AMC continues to deepen its presence in B30 (beyond top 30) cities, with 22% of monthly average AUM in March 2025 originating from these regions—well above the industry average of 18%. The addition of 68 branches in Tier-2 and Tier-3 locations during FY25 has driven net folio additions of 0.9 million.

The retirement solutions business emerges as a crown jewel. UTI's dominance in the National Pension System, with 27.4% market share, provides stable, long-term assets. The company manages mandates for EPFO (Employees' Provident Fund Organisation), Postal Life Insurance, and other government retirement schemes—relationships that private competitors cannot easily replicate.

By 2024, financial performance improves markedly. In the April to June 2024 quarter (Q1FY25), UTI AMC reported a nine per cent growth in profit after tax (PAT) to Rs 254 crore, as against Rs 234 crore in the same quarter a year ago. The company's total revenue from operations rose 13 per cent to Rs 529 crore during the quarter under review, as compared to Rs 468 crore in the April-June quarter of the preceding financial year (2023-24).

The stock market responds positively. UTI Asset Management Company (AMC) share price hit an over two-year high of Rs 1,119 on the BSE on Tuesday, August 20, 2024. This comes after UTI AMC share rallied 6 per cent in the intraday trade today on earnings improvement. The stock surpassed its previous high of Rs 1,113.80 touched on July 16.

Analyst sentiment turns constructive. Analysts at InCred Equities said they like UTI AMC considering the improving performance of its schemes leading to steady inflow and healthy AUM, rationalisation of operating expenses to strengthen operating performance and a favourable risk-reward ratio. "We retain ADD rating on the stock with a higher target price of Rs 1,200 (Rs 1,100 earlier), corresponding to ~13.8x FY26F EPS".

The ownership structure post-IPO reveals interesting dynamics. While technically promoter-less, the four sponsors still hold significant stakes through various entities. T. Rowe Price remains invested, suggesting confidence in long-term prospects despite governance frustrations. Institutional ownership increases steadily, with domestic mutual funds and insurance companies recognizing value in UTI's transformation story.

Corporate governance improves materially as a listed entity. Independent directors gain real influence. Quarterly earnings calls bring transparency previously absent. Related-party transactions face scrutiny. Executive compensation aligns with performance. The market discipline that reformers promised during the 2003 restructuring finally materializes.

Product innovation accelerates without bureaucratic constraints. UTI launches thematic funds targeting emerging sectors—technology, healthcare, infrastructure. Passive products, previously ignored, gain focus as index funds and ETFs grow popular. The international fund offerings expand, giving Indian investors global diversification. ESG funds are introduced, targeting socially conscious millennials.

The distribution strategy evolves dramatically. Direct plans, sold without distributor commissions, gain traction through digital channels. Robo-advisory services target young investors. WhatsApp and social media become transaction channels. The company that once relied on post offices now processes majority of transactions digitally.

Yet challenges persist. Market share in equity funds—the highest-margin products—remains under pressure from aggressive private players. Expense ratios, while declining, remain above industry leaders. Fund performance, while improving, lacks consistency across categories. The brand, despite rehabilitation, still carries baggage among sophisticated investors.

The broader industry context provides both tailwinds and headwinds. In the long term, i.e., between fiscal 2024 and fiscal 2029, the overall industry's AUM is projected to sustain a high growth trajectory of 17-18 per cent CAGR, reaching approximately Rs 120 trillion. This growth benefits all players, but market share shifts toward digital-first, low-cost providers pose structural challenges for traditional players like UTI.

As we write in 2024, UTI trades around ₹1,300, up nearly 135% from its IPO price. The market capitalization of ₹16,996 crores makes it India's third-largest listed AMC after HDFC and Nippon Life. The company consistently pays dividends, with special dividends supplementing regular payouts—a sign of cash generation and capital discipline.

The investment case remains nuanced. Bulls point to cheap valuation (trading at discount to peers), improving operational metrics, dominance in retirement solutions, and potential for market share gains in underserved segments. Bears worry about continued share loss in retail equity, structural cost disadvantages, and technological disruption from fintech players.

Perhaps most intriguingly, speculation persists about T. Rowe Price increasing its stake or other strategic investors entering. Considering the improving efficiency of UTI AMC, T Rowe Price (already being an investment manager) can opt to buy majority stake from public sector banks (the easiest route) and can become the promoter. Such a move could unlock value by bringing professional management and removing the overhang of government influence.

The public market journey, still early, validates both optimists and skeptics. UTI has proven it can operate as a commercial entity, generate profits, and reward shareholders. But whether it can reclaim its position as India's premier asset manager—or must content itself as a profitable niche player—remains an open question.

IX. Business Model Deep Dive

Understanding UTI AMC's business model requires peeling back layers of complexity accumulated over six decades. Unlike typical asset managers who focus on a core competency, UTI operates across virtually every segment of India's investment management landscape—from tiny SIP investments of ₹500 monthly to managing trillion-rupee government pension funds.

The revenue architecture rests on four pillars, each with distinct economics. Domestic mutual funds generate approximately 73% of revenues through management fees ranging from 0.05% for liquid funds to 2.5% for equity funds. The blended yield of roughly 34 basis points seems thin, but applied to ₹3.5 trillion in AUM, it generates substantial income. The beauty of this model lies in its operating leverage—managing ₹100 crores costs almost the same as managing ₹1,000 crores.

The second pillar, institutional mandates, contributes 15% of revenues but punches above its weight in profitability. Managing EPFO's corpus or Postal Life Insurance funds involves lower fees—often below 10 basis points—but requires minimal distribution costs and marketing expenses. These mandates are won through competitive bidding where UTI's government parentage and six-decade track record provide decisive advantages.

Portfolio Management Services (PMS) for high-net-worth individuals represents the third pillar, contributing 8% of revenues but growing rapidly. With minimum tickets of ₹50 lakhs, PMS clients demand customized portfolios and personal attention. UTI charges 1-2.5% management fees plus performance fees of 10-20% above hurdle rates. The economics are attractive—higher fees, stickier assets, limited regulatory restrictions—but competition from boutique PMS providers and private banks is fierce.

The fourth pillar encompasses alternative investments, international business, and advisory services. Though contributing just 4% of revenues currently, these businesses represent optionality. The alternative investment funds target sophisticated investors seeking private equity or structured credit exposure. International business leverages India's demographic dividend, managing money for NRIs and foreign institutions seeking India exposure.

The cost structure reveals both legacy burdens and modernization efforts. Employee costs consume 35% of revenues—higher than nimble competitors but lower than during government ownership. UTI employs 2,500 people, many inherited from the pre-2003 era when lifetime employment was assured. The average employee cost of ₹15 lakhs annually is reasonable by industry standards, but productivity varies widely between old-timers and new recruits.

Distribution expenses, at 40% of revenues, represent the largest cost category. This includes commissions to 51,000 independent financial advisors, fees to banking partners, and digital platform charges. The distribution economics are brutal—upfront commissions can reach 1% of investments, trail commissions continue indefinitely, and competition for quality distributors intensifies annually. UTI's strategy of maintaining physical presence in smaller cities adds to costs but provides differentiation. Technology infrastructure, once a liability, becomes mission-critical. Cloud migration, API-based architecture, and data analytics platforms require continuous investment. Cybersecurity alone costs ₹20 crores annually—a line item that didn't exist during monopoly days. Yet these investments are non-negotiable; digital natives like Zerodha and Groww have reset customer expectations.

Administrative expenses consume 15% of revenues, including rent for 163 branches, regulatory compliance costs, and corporate overhead. The Mumbai headquarters alone costs ₹15 crores annually in rent—a legacy of signing long-term leases during boom times. Branch rationalization is politically sensitive; closing a loss-making branch in a small town invites media criticism about abandoning financial inclusion.

Marketing expenses, surprisingly modest at 10% of revenues, reflect UTI's strategy of leveraging brand heritage rather than aggressive advertising. While HDFC AMC sponsors cricket tournaments and ICICI Prudential blankets television with celebrity endorsements, UTI focuses on investor education programs and digital content marketing. The approach is cost-effective but limits brand visibility among younger investors.

The profitability metrics tell a story of gradual improvement with persistent challenges. Net profit margin hovers around 44.4%—healthy in absolute terms but lagging peers who achieve 50%+. Return on equity at 10.5% trails the industry average, reflecting the capital-heavy balance sheet inherited from the restructuring. The company's profitability score of 66/100 suggests room for improvement.

The cash generation capability remains robust. Operating cash flow of ₹325 crores provides ample resources for dividends and growth investments. The company maintains zero debt—a conservative approach that limits financial leverage but provides stability. With ₹2,000 crores in investments and cash, UTI has firepower for acquisitions or aggressive expansion if opportunities arise.

The competitive dynamics of different businesses vary dramatically. In retail equity funds, UTI faces intense competition from HDFC, ICICI, and SBI mutual funds who leverage banking relationships. The battleground is performance—even 50 basis points of underperformance triggers redemptions. UTI's equity funds have improved but lack the consistency of category leaders.

In debt funds, the game is different. Scale matters more than performance; larger funds achieve better negotiation power and lower transaction costs. UTI's ₹1.5 trillion debt AUM provides competitive advantage, but regulatory changes like credit risk norms and duration limits constantly alter the landscape. The Franklin Templeton credit crisis of 2020 reminded everyone that debt funds aren't risk-free.

The passive business—index funds and ETFs—represents both threat and opportunity. UTI was late to recognize the shift but now aggressively builds capabilities. The economics are brutal—fees of 5-10 basis points leave minimal margins—but the sticky assets and minimal operational complexity are attractive. UTI's government relationships help win mandates for EPFO investments in ETFs, providing scale that private players struggle to match.

International business remains subscale but strategic. Managing money for NRIs through offshore funds generates premium fees and foreign currency revenues. The partnership with T. Rowe Price should theoretically provide global distribution, but regulatory restrictions and operational complexities limit growth. The opportunity is massive—Indians abroad hold $500 billion in financial assets—but execution remains challenging.

The technology platform undergoes continuous evolution. The core portfolio management system, upgraded in 2018, handles complex calculations across multiple asset classes and regulatory regimes. The customer-facing applications—mobile apps, WhatsApp banking, robo-advisory—require constant updates to match fintech competitors. The challenge isn't just building technology but changing organizational culture to embrace digital-first thinking.

Risk management, once an afterthought, now consumes significant resources. Credit risk teams analyze thousands of bonds, equity risk systems monitor portfolio concentrations, operational risk frameworks track process failures. The 2020 pandemic tested these systems—markets crashed 40%, redemptions spiked, employees worked remotely—yet UTI navigated without major incidents, validating investments in risk infrastructure.

The regulatory framework continues evolving, creating both challenges and opportunities. SEBI's rationalization of expense ratios squeezes margins but levels the playing field. Direct plan regulations reduce distribution dependence. Categorization norms limit product proliferation but improve investor understanding. UTI's compliance-first approach, while costly, avoids regulatory penalties that plague aggressive competitors.

The human capital strategy balances legacy obligations with future needs. The average employee age has declined from 48 to 38, but pockets of resistance remain. Fund managers recruited from IIMs coexist with clerks hired in the 1980s. Performance-based compensation, revolutionary when introduced, now needs updating to match private sector standards. The challenge is transforming culture without destroying institutional knowledge.

Looking ahead, the business model faces structural questions. Can a traditional asset manager survive when Vanguard-style passive funds and Robinhood-style trading apps reshape investing globally? Should UTI double down on its strengths—retirement, B30 cities, government relationships—or attempt to compete directly in urban retail? How does it balance the conflicting demands of growth, profitability, and social responsibility?

The answers aren't obvious, but UTI's journey provides clues. The company that survived monopoly, competition, crisis, and transformation has demonstrated remarkable adaptability. The business model, while complex and sometimes inefficient, generates consistent cash flows and serves millions of Indians. Whether that's enough in an industry facing disruption remains the billion-rupee question.

X. Competitive Landscape & Market Dynamics

The Indian asset management industry in 2024 resembles a gladiatorial arena where 44 fund houses battle for a pie that's simultaneously growing rapidly and becoming increasingly competitive. Total industry AUM has exploded to ₹66 trillion, yet the spoils are unevenly distributed—the top five players control 55% of assets, while the bottom twenty scramble for less than 10%.

HDFC Asset Management stands as the undisputed emperor, with ₹7.5 trillion in AUM and a market share that seems unassailable. Born from India's largest housing finance company, HDFC AMC leverages unmatched distribution through parent banking channels, consistent fund performance, and a brand that resonates from metros to mohallas. Their systematic investment plan (SIP) book of ₹25,000 crores monthly is larger than most competitors' total AUM.

ICICI Prudential AMC, the second giant, brings technological sophistication and aggressive marketing to the battle. Their digital-first approach attracts young investors, while the ICICI Bank relationship provides captive distribution. With ₹6.8 trillion in AUM, they've mastered the art of product innovation—launching thematic funds that capture investor imagination, from technology to ESG to multi-asset allocation.

SBI Mutual Fund, backed by India's largest bank, operates like a steady supertanker. With 30,000 bank branches as distribution points and natural access to rural India, SBI commands ₹9.2 trillion in AUM. Their strategy is volume over margin—accepting lower fees to maximize assets, betting that scale economics will eventually prevail.

In the mutual fund industry, UTI commands a market share of 5.04% on a QAAUM basis (FY25), it also has an overall Market Share of 27.4% in the National Pension System. This split personality—declining in retail, dominant in retirement—defines UTI's competitive position.

The foreign players bring global sophistication but struggle with local execution. Franklin Templeton's 2020 credit fund crisis, where six schemes were wound up, shattered investor confidence and demonstrated the perils of transplanting Western strategies to Indian markets. Invesco, Mirae, and Motilal Oswal focus on niche strategies, content with profitable corners rather than market dominance.

The new-age disruptors represent the most fascinating dynamic. Zerodha's Coin platform offers direct mutual funds with zero commissions, appealing to cost-conscious millennials. Groww, Paytm Money, and ETMoney have turned mutual fund investing into a social media-friendly experience—gamification, influencer marketing, and one-click investing. These platforms don't manufacture funds but control distribution, potentially kingmaking or breaking traditional AMCs.

The distribution battlefield reveals why UTI struggles despite its heritage. Banks control 35% of mutual fund distribution, and UTI lacks a banking parent. Independent financial advisors (IFAs) contribute 40%, but they're increasingly courted by competitors offering higher commissions and foreign junkets. Digital platforms, growing at 50% annually, favor funds with strong performance and simple narratives—neither UTI's strength. The industry numbers paint a picture of explosive growth masking intense competition. Indian mutual fund industry achieved new heights in 2024 as it surpassed Rs 68 lakh crore in assets under Management (AUM). Yet this growth is concentrated—the top 3 AMCs – SBI Funds Management, ICICI Prudential AMC, and HDFC AMC – control a significant portion of the market, with a combined market share of over 41%. SBI Funds Management is the clear leader, with a market share of 17.6%.

The product battleground has shifted dramatically. Equity funds now dominate, with equity mutual fund AUM stood at Rs 30.5 lakh crore - 45% of the total AUM. The rise of systematic investment plans fundamentally alters industry dynamics—Monthly SIP inflows witnessed an impressive 48% growth year-over-year, surging from Rs 17,073 crore in November 2023 to Rs 25,320 crore in November 2024. Over the past 12 months, cumulative SIP inflows reached an unprecedented Rs 2.59 lakh crore.

Passive investing emerges as the great disruptor. Index funds and exchange-traded funds (ETFs) experienced excellent growth, driven by increasing retail adoption and a surge in thematic and sectoral investing. Investment accounts (folios) in index funds will double this year, while folios in ETFs have already risen by 37%. The AUM in the passive investment segment grew by 23%, reaching approximately Rs 11 lakh crore during the first 11 months of the year. The growth was driven by rising awareness of passive investing and an unprecedented 116 passive fund launches by November.

UTI's response to this competitive landscape reveals both adaptation and constraint. In equity funds, where competition is fiercest, UTI struggles to differentiate. Its large-cap funds underperform benchmarks, mid-cap offerings lack the excitement of category leaders, and sectoral funds arrive late to themes. The company's strength in debt and liquid funds—built on decades of institutional relationships—provides stable revenues but limited growth.

The retirement solutions space offers UTI rare competitive advantage. The company's 27.4% market share in the National Pension System isn't just about numbers—it represents deep expertise in managing long-term, regulated money that competitors struggle to replicate. Government employees trust UTI with their retirement savings because of heritage, not just performance. This trust translates into sticky assets that compound over decades.

Digital disruption accelerates competitive pressures. Digital-first distributors are winning the bulk of new accounts thanks to gamified mobile journeys, vernacular investor-education content, and low-value micro-SIPs that start at INR 100. UPI integration now permits same-day liquid-fund redemptions, effectively positioning select fintech apps as high-yield payments wallets that rival conventional savings accounts.

The distribution dynamics reveal why market share battles are so fierce. online trading platforms secured a 33.16% share of the India mutual fund market in 2024 and are anticipated to lead growth at 9.15% CAGR. Traditional distributors, who once controlled the game, now compete with robo-advisors, influencer recommendations, and algorithm-driven portfolio suggestions.

International competition adds another layer. Global giants like BlackRock and Vanguard eye India's growth but struggle with regulatory restrictions on foreign ownership. Their strategy involves partnerships and technology transfer rather than direct entry. UTI's relationship with T. Rowe Price provides some protection, but the threat of a major global player acquiring a domestic AMC looms constantly.

The fee compression battle intensifies annually. SEBI's expense ratio caps force AMCs to compete on scale rather than pricing power. Direct plans, which eliminate distributor commissions, grow rapidly among sophisticated investors. The race to zero fees, pioneered by Vanguard globally, hasn't fully arrived in India but casts a long shadow. UTI's relatively high cost structure makes this trend particularly threatening.

Regional dynamics add complexity. In metros, UTI is an also-ran, competing against slicker brands with better digital interfaces. In Tier-2 and Tier-3 cities, its physical presence and government associations provide advantages. But even here, digital platforms rapidly erode traditional moats. A young professional in Lucknow is as likely to invest through Groww as through the local UTI branch.

The thematic fund explosion reveals changing investor preferences. Sectoral and Thematic Funds gained immense popularity, with their AUM rising by 79% to Rs. 4.61 lakh cr., up from Rs. 2.58 lakh cr. in December 2023. UTI, traditionally conservative in product launches, struggles to capture this trend. While competitors launch ESG funds, technology funds, and global opportunity funds, UTI's product pipeline remains conventional.

Consolidation pressures build across the industry. There are just 45 fund houses or asset management companies (AMCs). Of these, only 14 fund houses boast an AUM in excess of Rs 1 lakh crore each. Smaller players struggle for viability, creating acquisition opportunities. UTI, with its strong balance sheet, could be consolidator or consolidated—the strategic direction remains unclear.

The competitive dynamics ultimately reflect a fundamental tension: commoditization versus differentiation. In a world where every AMC offers similar products through similar channels at similar prices, what distinguishes one from another? For UTI, the answer lies in leveraging unique strengths—government relationships, retirement expertise, small-city presence—rather than competing head-to-head in commoditized segments.

Looking ahead, the competitive landscape will likely polarize further. A handful of giants will dominate retail equity, passive players will capture flow through low costs, and specialists will thrive in niches. UTI's challenge is determining which game to play—and whether its historical advantages translate into future competitiveness in an industry where past performance increasingly doesn't guarantee future results.

XI. Power & Politics: The Unique Governance Structure

The boardroom at UTI AMC resembles a delicate diplomatic summit more than a typical corporate gathering. Four state-owned giants—each holding equal 18.24% stakes through the 2003 restructuring—must somehow align their often-conflicting agendas. T. Rowe Price, the lone foreign voice with 23% ownership since 2010, advocates for professional management while navigating the labyrinth of Indian public sector politics. This structure, unique among global asset managers, creates a governance puzzle that would challenge even Machiavelli.

State Bank of India, the largest sponsor, views UTI through the lens of India's biggest bank. With 30,000 branches and deep rural penetration, SBI sees natural synergies in distribution. Yet SBI also runs its own mutual fund, creating an inherent conflict—should it prioritize selling UTI products or its own? The answer varies with political winds and individual branch manager incentives.