Bank of Maharashtra: The Swadeshi Bank That Survived It All

I. Introduction & Episode Roadmap

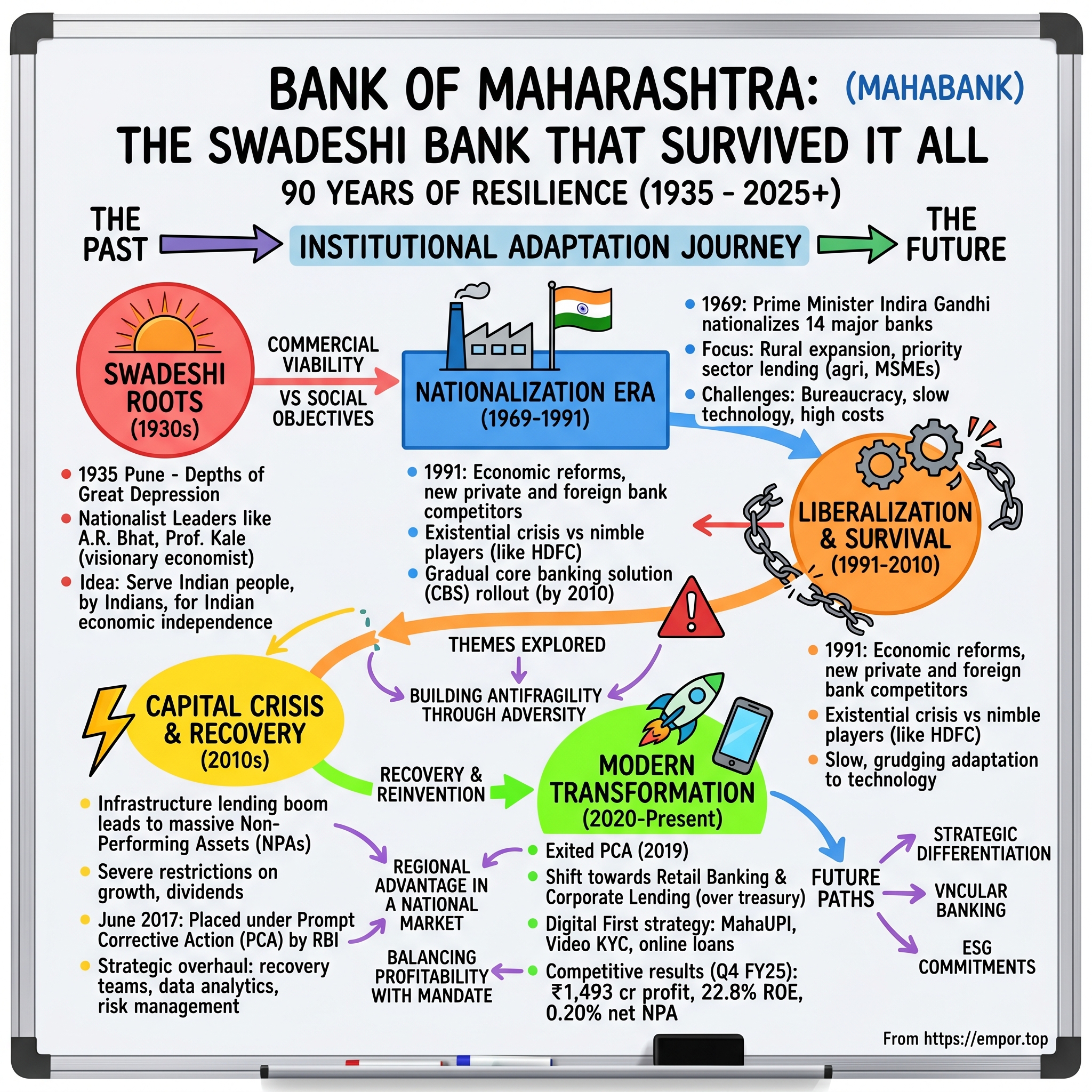

Picture this: It's 1935, the depths of the Great Depression. In the Bombay Presidency alone, 54 banks have collapsed in the past two decades. The streets of Pune are filled with merchants and traders who've lost their life savings, their businesses starved of credit. In a small conference room at the Kesari Mahratta office, a group of idealistic nationalists gather around a wooden table, dreaming of something audacious—a bank that would serve Indians, by Indians, for the economic independence of Indians.

Fast forward to 2025: That same institution, Bank of Maharashtra, commands a market capitalization of ₹42,673 crore, serves 35 million customers through 2,641 branches, and just posted a 22.61% jump in quarterly profits. It survived the Great Depression, thrived through Independence, endured nationalization, weathered liberalization, and is now navigating digital disruption. How did a regional Swadeshi movement bank become one of India's most resilient public sector banks?

This is a story of institutional survival that spans nine decades—from colonial India to Digital India. It's about how a bank born from nationalism adapted to socialism, then to capitalism, and now to algorithmic banking. It's about maintaining regional identity while scaling nationally, about being government-owned yet market-competitive, about preserving legacy while embracing transformation.

The themes we'll explore cut to the heart of Indian economic history: the role of public sector banking in nation-building, the tension between social objectives and commercial viability, the challenge of competing with nimble private players while carrying the weight of government ownership, and ultimately, what it means to be a "people's bank" in the age of neo-banks and UPI.

We'll trace this journey through distinct eras—each presenting existential challenges that would have killed lesser institutions. From the Swadeshi origins and the visionary leadership of the Mahratta Chamber of Commerce, through the seismic shift of nationalization in 1969, the shock therapy of 1991's liberalization, the capital crisis of the 2010s, to today's digital battlefield where traditional banks face off against fintechs with billion-dollar valuations but no physical branches.

What emerges is not just a corporate history, but a masterclass in institutional adaptation—how an organization can maintain its core purpose while completely reinventing its methods, multiple times over. It's about reading the political economy correctly at each inflection point and making the hard choices that ensure survival without losing soul.

II. The Great Depression & The Birth of a Vision (1914–1935)

The conference room at the Kesari Mahratta office hummed with tension on May 19, 1935. Outside, the streets of Pune bore witness to an economic catastrophe of staggering proportions. Between 1914 and 1935, India had watched 380 banks fail—54 in the Bombay Presidency alone. Each collapse wasn't just a business failure; it was thousands of depositors losing life savings, small traders denied credit, farmers unable to finance the next harvest. The human wreckage of financial instability littered every major city and town.

A.R. Bhat, the founder secretary of the newly established Mahratta Chamber of Commerce, looked around the table at the assembled group. These weren't bankers—they were educators, economists, freedom fighters. Professor V.G. Kale, the former member of the Indian Tariff Board and renowned economist, carried the intellectual weight of understanding what economic self-sufficiency meant. D.K. Sathe brought the merchant community's perspective. Each face reflected the same realization: political freedom without economic freedom was meaningless.

The Swadeshi movement of the early 1900s had planted the seed. Indians had boycotted British goods, spun khadi, built indigenous industries. But credit—the lifeblood of commerce—remained largely in foreign or traditional moneylender hands. The few Indian banks that emerged during the Swadeshi wave couldn't survive the post-World War I economic turbulence. The survivors were mostly exchange banks focused on foreign trade, or presidency banks that served British commercial interests.

Bhat was no ordinary visionary. Having witnessed the systematic exclusion of Indian businesses from formal credit markets, he understood that a bank wasn't just a financial institution—it was an instrument of economic liberation. His proposal was radical yet practical: create a bank that would specifically serve the small and medium enterprises of Maharashtra, provide credit to those ignored by established banks, and build an institution robust enough to survive economic cycles.

The founding committee's discussions revealed sophisticated understanding of banking economics. They debated optimal capital structure—how much initial capital would inspire confidence without being unrealistic to raise? They argued about board composition—should it be purely businessmen, or include professionals and academics? The geographic focus sparked the most heated debates: should they remain hyper-local to Pune, cover all of Maharashtra, or think nationally from day one?

Professor Kale's economic training proved invaluable. He had studied the failures of the 380 collapsed banks and identified common patterns: undercapitalization, concentrated loan books, poor governance, and crucially, the lack of connection to their communities. His prescription was clear—build conservatively, diversify from the start, maintain strong governance, but most importantly, embed the bank in the social and economic fabric of Maharashtra.

The context made their ambition even more audacious. The Great Depression had decimated agricultural prices—cotton, the backbone of Maharashtra's economy, had crashed. The traditional banking system had completely frozen lending to Indians. The colonial government's monetary policy prioritized currency stability over economic growth. Into this environment of extreme risk aversion, these men were proposing to launch a new bank.

What distinguished this effort from previous failed attempts was the institutional backing of the Mahratta Chamber of Commerce. The MCC wasn't just another trade body—it represented a coalition of Maharashtrian business interests that had coalesced around economic nationalism. This provided not just initial capital commitments but a ready customer base and, crucially, a distribution network through merchant associations.

The committee's decision-making process reflected remarkable strategic clarity. The initial authorized capital was set at US$1 million (approximately ₹13 lakh then)—substantial enough to inspire confidence but achievable through the Maharashtrian business community. The shareholding would be broad-based to prevent concentration of control. The board would blend business acumen with professional expertise. The bank would start in Pune but with explicit plans for expansion across Maharashtra.

By the end of that May meeting, the blueprint was clear. This wouldn't be just another bank—it would be Maharashtra's bank, a financial institution that would channel the savings of Maharashtrians into credit for Maharashtrian enterprises. It would be conservative in risk-taking but progressive in customer acquisition. It would compete with established players not through size but through superior understanding of local needs.

The timing seemed impossible—launching a bank during the Great Depression, in a colonized country, in a region still reeling from bank failures. But perhaps that was precisely why it could work. When everyone else was retreating, when credit had dried up, when businesses were desperate for a lifeline—that's when a new institution focused on serving the underserved could find its market. The foundation was being laid not just for a bank, but for an institution that would outlive empires, economic systems, and technological revolutions.

III. Foundation & Early Operations (1935–1944)

September 16, 1935—the day of Ganesh Chaturthi, when Maharashtra celebrates the remover of obstacles. The symbolism wasn't lost on anyone as the Bank of Maharashtra was formally registered under the Indian Companies Act. The auspicious timing was deliberate; this was as much a cultural statement as a business launch. When the bank opened its doors for operations on February 8, 1936, at 287 Bhawani Peth in Pune, it wasn't just offering banking services—it was offering hope.

The first board of directors read like a who's who of Pune's progressive elite. The chairman, B.G. Gokhale, brought credibility from his legal practice and social reform work. The managing director, K.V. Hardikar, had cut his teeth in cooperative banking and understood grassroots finance. The board included educators, industrialists, and professionals—a deliberate mix that signaled this bank would be different. These weren't career bankers; they were nation-builders who happened to be running a bank.

The early operational model was revolutionary for its time. While established banks focused on trade finance and large businesses, Bank of Maharashtra deliberately targeted what we'd now call the "missing middle"—small traders, artisans, professionals, and emerging entrepreneurs. The first loan ledgers, preserved in the bank's archives, tell remarkable stories: ₹500 to a textile trader to purchase inventory, ₹300 to a goldsmith to expand his workshop, ₹1,000 to a group of farmers to buy a irrigation pump collectively.

Building trust in a post-depression era required extraordinary measures. The bank's officers didn't wait for customers to come to them—they went to the markets, the mandis, the industrial areas. They held financial literacy sessions in Marathi, explaining how banking worked, why keeping money in a bank was safer than under the mattress, how credit could expand businesses. This grassroots engagement was unheard of in formal banking then.

The numbers from the first year revealed both struggle and promise. Total deposits by end of 1936: ₹7.2 lakhs. Total advances: ₹4.8 lakhs. Net profit: ₹8,000. Modest by any measure, but the trajectory was clear. By 1939, deposits had grown to ₹42 lakhs, and the bank had opened three more branches across Maharashtra. The conservative lending approach—no single exposure exceeding 10% of capital, mandatory collateral, regular monitoring—meant virtually no bad loans in the early years.

Then came World War II, transforming everything. Suddenly, the colonial government needed to finance the war effort, creating massive demand for banking services. Supply chains were disrupted, creating opportunities for local businesses to fill gaps. Inflation surged, driving savers to banks. Bank of Maharashtra was perfectly positioned—it had the local network, the trust of small businesses, and crucially, the operational discipline to scale safely.

The war years saw explosive growth. The bank pioneered what would later be called "supply chain financing"—providing credit to small manufacturers supplying to larger war contractors, using the contracts as collateral. It created special products for retailers dealing with rationed goods. Most innovatively, it developed a system for transferring money for families whose members had joined the armed forces—a precursor to modern remittance services.

The transformation culminated in 1944 when Bank of Maharashtra achieved scheduled bank status from the Reserve Bank of India. This wasn't just a regulatory milestone—it was validation that a Swadeshi institution could meet the highest banking standards. Scheduled status meant access to RBI refinancing, ability to hold government deposits, and most importantly, a stamp of credibility that attracted larger depositors and borrowers.

The internal culture developing during these years would define the bank for decades. Every morning began with a prayer for ethical conduct. Employees were encouraged to learn about their customers' businesses, not just their financials. The bank sponsored Marathi literary events, supported local schools, and its officers often served as informal business advisors to their clients. This wasn't corporate social responsibility—CSR didn't exist as a concept then—it was simply how the founders believed a bank should operate.

The operational innovations were remarkable for their prescience. The bank created what it called "survey committees"—groups that would study emerging sectors and recommend lending strategies. One 1943 report on "Post-War Industrial Opportunities for Maharashtra" accurately predicted the rise of automotive components, pharmaceuticals, and processed foods as key sectors. The bank began building relationships in these areas years before they boomed.

Risk management, learned from studying the failures of the 1920s, was embedded in the bank's DNA. Every loan above ₹1,000 required two independent assessments. Concentration limits were strictly enforced—no more than 20% exposure to any single sector. Regular audits were conducted by external chartered accountants, unusual for that era. The bank maintained higher cash reserves than legally required, understanding that liquidity was survival.

By 1944, Bank of Maharashtra had eight branches, ₹2.8 crore in deposits, and had financed everything from textile mills to grain merchants to cinema halls. But more than the numbers, it had built something intangible—an institutional reputation for being the bank that understood Maharashtra, that spoke the language of its entrepreneurs, that took measured risks on dreams.

The foundation was now solid. What started in a small office in Bhawani Peth had become a legitimate financial institution. The question was no longer whether the bank would survive, but how far it could grow. Little did anyone know that the biggest transformation—political independence followed by nationalization—would soon test everything they had built. The Swadeshi bank was about to become a socialist one, whether it wanted to or not.

IV. The Nationalization Era (1969–1991)

July 19, 1969, 8 PM—All India Radio crackled to life with an announcement that would reshape Indian banking forever. Prime Minister Indira Gandhi's voice, steady and resolute, declared the nationalization of 14 major commercial banks, including Bank of Maharashtra. In boardrooms across Pune and Mumbai, directors who had spent decades building the bank sat in stunned silence. The institution born from Swadeshi idealism was now property of the Indian state.

The bank's chairman at the time, M.L. Apte, later recalled the cognitive dissonance of that moment. Here was a bank founded on economic nationalism being nationalized by a government pursuing socialist policies. The irony was sharp—the Swadeshi dream of Indian ownership was fulfilled, but not in the way the founders had imagined. Private Indian ownership had become public Indian ownership overnight.

The immediate transformation was jarring. Government nominees replaced independent directors. Lending priorities shifted from commercial viability to social objectives. The mandate expanded from serving Maharashtra's entrepreneurs to fulfilling national development goals. Branch expansion targets arrived from Delhi, not Pune. The autonomous bank had become an instrument of state policy.

But the story of Bank of Maharashtra during nationalization wasn't one of simple subordination—it was adaptation and subtle resistance. The bank's middle management, mostly Maharashtrians who had risen through the ranks, became masters at translating Delhi's directives into locally workable solutions. When the government mandated rural expansion, they didn't just open branches—they identified rural areas with genuine economic potential. When priority sector lending targets came, they found ways to make agricultural loans commercially viable.

The numbers tell a story of explosive, sometimes reckless, growth. From 97 branches in 1969, the network expanded to 987 by 1985. Deposits grew from ₹38 crores to ₹1,847 crores. The employee count ballooned from 2,800 to 28,000. But buried in these headlines were profound operational challenges. Many rural branches operated at losses. Priority sector loans often turned into NPAs. The bureaucratization slowed decision-making to a crawl.

The rural expansion deserves special attention because it reveals both the nobility and naivety of socialist banking. Bank officers, many urban-educated and Marathi-speaking, were posted to remote villages in Bihar, Rajasthan, and Karnataka. The cultural displacement was severe. One retired manager recalled reaching his branch in rural Rajasthan only to find it was 15 kilometers from the nearest paved road. Yet these same officers often became local legends, providing the first formal credit many villagers had ever accessed, breaking the stranglehold of moneylenders charging 120% annual interest.

The License Raj years created peculiar opportunities. Every business needed government permits, and government-owned banks became unofficial facilitators. Bank of Maharashtra developed expertise in what could charitably be called "regulatory navigation"—helping businesses understand which forms to file, which offices to approach, which timelines to expect. This wasn't written in any manual, but loan officers knew that their borrowers' success depended as much on managing bureaucracy as managing businesses.

The bank's relationship with the state government of Maharashtra became particularly complex. As a nationalized bank, it was supposed to serve national interests uniformly. But its historical roots and concentrated branch network in Maharashtra meant it remained the de facto banker to the state government and its enterprises. This created a delicate balance—serving Delhi's mandates while maintaining Pune's relationships.

Technology adoption during this period was painfully slow, constrained by government procurement processes and union resistance. While private banks in developed countries were computerizing, Bank of Maharashtra was still maintaining handwritten ledgers in most branches well into the 1980s. A single inter-branch transaction could take weeks. Customer service became synonymous with long queues and longer lunch breaks.

Yet within these constraints, pockets of excellence emerged. The bank's treasury operations, staffed by sharp minds who couldn't find opportunities elsewhere due to license raj limitations, became surprisingly sophisticated. They pioneered structured products for public sector enterprises, developed early forex hedging mechanisms for exporters, and built one of the better government securities trading desks among PSU banks.

The human dimension of nationalization was perhaps most poignant. The old guard, who had joined when it was a private bank with a mission, watched their institution transform into something unrecognizable. Some adapted, some resisted, many simply endured. The new recruits, joining through nationwide competitive exams, brought different skills but often lacked connection to the bank's heritage. The culture became bifurcated—Maharashtrian old-timers and pan-Indian newcomers, coexisting uneasily.

Union power reached its zenith during this period. The Bank of Maharashtra Employees Union became a force unto itself, capable of shutting down operations statewide. Wage negotiations were theatrical affairs, with dramatic walkouts and last-minute compromises. Productivity metrics were resisted as "anti-worker." The joke in banking circles was that it was easier to close a branch than to fire an employee.

By 1991, Bank of Maharashtra was unrecognizable from its 1969 avatar. It had become a pan-Indian institution with over 1,400 branches, but had lost much of its entrepreneurial DNA. It was fulfilling its social mandate with priority sector lending reaching 42% of advances, but commercial viability was increasingly strained. It had achieved the scale the founders could never have imagined, but at the cost of agility they had valued.

The nationalization era was ending, though nobody knew it yet. The bank had survived its transformation from private to public, from regional to national, from commercial to social. But the biggest test was about to come. Economic liberalization would force this slow-moving giant to compete with nimble private players in a game where the rules were about to change completely. The question wasn't whether Bank of Maharashtra could compete—it was whether it could remember how to.

V. Liberalization & The Survival Game (1991–2010)

The first HDFC Bank branch opened in Mumbai in 1995, just a few blocks from Bank of Maharashtra's regional office. Inside HDFC, customers found air-conditioning, computer terminals, and service with a smile. Transactions that took days at public sector banks happened in hours. The message was clear: Indian banking would never be the same. For Bank of Maharashtra, comfortable in its government-backed stability, this was the beginning of an existential crisis that would last two decades.

The 1991 reforms had unleashed forces that PSU banks were spectacularly unprepared for. New private banks like ICICI and HDFC weren't just competing—they were redefining what banking meant. Foreign banks like Citibank and Standard Chartered, previously restricted, were now expanding aggressively. These players brought technology, service standards, and salary packages that made PSU banks look prehistoric.

Bank of Maharashtra's initial response was denial, then panic, then grudging adaptation. The denial phase was almost comical in retrospect. Senior management insisted that government backing and branch network would always trump service quality. "Let them serve the rich," one executive committee meeting noted, "we serve the masses." But the masses, it turned out, also preferred not waiting three hours to deposit a cheque.

The technology gap was staggering. While HDFC was offering phone banking, Bank of Maharashtra was still figuring out how to network its branches. The computerization process, started half-heartedly in the late 1990s, became a saga of vendor disputes, union resistance, and incompatible systems. Different branches used different software. Data couldn't be consolidated. A customer couldn't access their account from another branch of the same bank.

But necessity bred innovation, albeit slowly. The bank's younger officers, frustrated by the archaic systems, began pushing for change. A group of tech-savvy managers in the Pune head office created what they called the "parallel project"—unofficially testing modern banking software while officially following procurement procedures. This skunkworks operation eventually became the blueprint for the bank's core banking solution.

The transformation accelerated dramatically in the mid-2000s. By 2010, Bank of Maharashtra had achieved something remarkable—complete core banking implementation across all 1,453 branches. Every account was now accessible from any branch. Internet banking, mobile banking, and ATM networks were fully operational. The achievement was even more impressive considering the complexity—migrating millions of accounts from paper to digital while keeping the bank running.

The mobile banking launch in 2008 deserves special mention. While private banks targeted smartphones (still rare in India), Bank of Maharashtra built a system that worked on basic Nokia phones through SMS. It wasn't sexy, but it was practical. Rural customers who would never own an iPhone could still check balances and transfer money. This pragmatic approach to technology—high-tech backbone, low-tech interface—became the bank's digital strategy. The culmination of this digital journey came in 2010 with a symbolic milestone—Bank of Maharashtra crossed the business level of Rs 1,00,000 crore. This wasn't just a number; it represented successful navigation through two decades of existential challenges. The bank had proven it could adapt, albeit slowly and painfully, to a world it wasn't designed for.

The competitive dynamics revealed uncomfortable truths about public sector banking. Private banks cherry-picked profitable customers and products, leaving PSU banks with the expensive mandate of financial inclusion. Foreign banks dominated corporate banking and treasury. Fintechs were beginning to unbundle banking services. Bank of Maharashtra found itself in the uncomfortable middle—too big to be nimble, too small to dominate, too public to be purely commercial.

Yet survival bred innovation in unexpected ways. The bank developed deep expertise in government business—managing treasury operations for state governments, distributing welfare payments, collecting taxes. This wasn't glamorous, but it provided stable fee income and sticky relationships. The bank became indispensable to the administrative machinery of Maharashtra and other states.

The human capital transformation was perhaps most dramatic. The old guard, who joined expecting lifetime employment and predictable promotions, suddenly faced performance reviews and sales targets. Young MBAs, attracted by signing bonuses, arrived with different expectations and left quickly for better opportunities. The culture became schizophrenic—part sarkari, part corporate, fully neither.

One particularly telling initiative was the "Project Navodaya" launched in 2008—an attempt to identify and fast-track high performers. The project revealed the depth of talent hidden in the organization, constrained by seniority-based promotions. Young officers who had innovative ideas but no voice suddenly found platforms. Some rose rapidly, others left for private banks, but the message was clear—meritocracy was possible, even in a PSU.

The cost structure remained the bank's Achilles heel. With over 1,400 branches and 30,000 employees by 2010, the cost-to-income ratio was stubbornly high. Private banks operated with a fraction of the branches and employees but generated similar revenues. The math was brutal—Bank of Maharashtra needed three employees to generate what HDFC generated with one.

But the branch network, costly as it was, also proved to be an unexpected moat. As India's economy boomed in the 2000s, financial inclusion became a government priority. Bank of Maharashtra's extensive rural network, built during the nationalization era, suddenly became valuable again. The same branches that were considered deadweight became channels for government schemes, microfinance, and agricultural credit.

The treasury operations during this period deserve special mention. As interest rates became more volatile and forex markets deepened, the bank's treasury transformed from a sleepy government securities desk to a sophisticated trading operation. Young dealers, trained in Mumbai's dealing rooms, brought modern risk management techniques. The treasury began contributing significantly to profits, sometimes covering for the losses in retail banking.

Customer service improvements, while slow, were real. ATM networks expanded from 12 machines in 2000 to over 800 by 2010. Phone banking, initially resisted by unions as job-threatening, became standard. Internet banking, after multiple false starts, finally worked reliably. The bank even experimented with Sunday banking in select branches, heresy for a PSU but necessary to compete.

The relationship with regulators evolved significantly. The Reserve Bank of India, pushing banking reforms, became both taskmaster and guide. RBI's guidelines on risk management, corporate governance, and technology adoption forced changes that internal inertia would have prevented. The bank learned to navigate this regulatory push—complying with the letter while sometimes missing the spirit.

By 2010, Bank of Maharashtra had survived liberalization, but survival isn't thriving. It had adapted to competition but hadn't learned to win. It had adopted technology but hadn't transformed digitally. It had improved service but hadn't delighted customers. The next decade would determine whether survival was enough, or whether the weight of accumulated problems—rising NPAs, costly operations, government interference—would finally prove too much. The real test wasn't liberalization; it was what came after.

VI. The Capital Crisis & Recovery (2010–2020)

The conference room at the Reserve Bank of India headquarters in Mumbai was silent except for the shuffling of papers. June 2017. The Bank of Maharashtra delegation sat across from RBI officials, knowing what was coming but hoping against hope. When the words were finally spoken—"Bank of Maharashtra is being placed under Prompt Corrective Action"—they landed like a death sentence. For a bank that had survived the Great Depression, nationalization, and liberalization, being put under PCA was the ultimate humiliation. The journey to PCA had begun years earlier with the infrastructure boom of the mid-2000s. Bank of Maharashtra, like all PSU banks, had enthusiastically funded power projects, steel plants, textile mills, and real estate developments. The lending officers, under pressure to meet targets, had overlooked red flags. The credit appraisal processes, designed for an earlier era, couldn't properly assess complex project finance risks. When the economy slowed after 2011, these loans turned toxic with frightening speed.

Bank of Maharashtra was placed under Prompt Corrective Action (PCA) by RBI in June 2017, in view of its high net NPA. The restrictions were severe—no branch expansion, no dividend payments, lending restrictions, and enhanced monitoring. For a bank that had operated freely for 82 years, it was like being put in regulatory prison.

The numbers tell the story of distress. Net NPAs had breached 6%, well above the RBI's tolerance threshold. Return on assets had turned negative. The capital adequacy ratio was dangerously close to regulatory minimums. But behind these numbers were thousands of human stories—branch managers who had sanctioned loans under political pressure, recovery officers trying to salvage value from defunct projects, and employees watching their institution's reputation crumble.

The government's response was capital infusion, but it came with strings. During the year under review, Bank of Maharashtra issued 10,51,50,787 equity shares amounting to Rs 394 crore (including share premium) to Government of India (GoI) on preferential allotment basis. This wasn't just money—it was life support that diluted existing shareholders and increased government control to over 80%.

Management developed what they called the "Monitorable Action Plan"—a detailed roadmap for recovery. This wasn't corporate strategy; it was survival tactics. Every NPA above ₹10 lakhs was reviewed individually. Recovery teams were strengthened. One-time settlement schemes were launched. The bank introduced innovative recovery mechanisms like "Ghar Ghar Dastak Yojana" for small NPAs and "MahaMukti" schemes for larger exposures.

The cultural impact of PCA was devastating. Employees who had joined a respected institution now worked for a "weak bank." Customers questioned the safety of their deposits. Competitors poached relationship managers and key accounts. The Pune headquarters, once bustling with activity, became subdued. Board meetings transformed from strategy sessions to damage control exercises.

Yet within this crisis, transformation accelerated. The bank's technology infrastructure, neglected during the boom years, received urgent attention. Risk management systems were overhauled. Credit appraisal processes were completely redesigned. The bank began using data analytics to identify early warning signals. What PCA forced was what complacency had prevented—genuine operational reform.

The recovery came faster than expected. By January 2019, just 18 months after being placed under PCA, Bank of Maharashtra was released from restrictions. Bank of Maharashtra's NPA was 5.91% by the third quarter of FY2019, below the 6% threshold. Bank of Maharashtra which meet the regulatory norms including Capital Conservation Buffer (CCB) and have Net NPAs of less than 6% as per third quarter results, are taken out of the PCA framework subject to certain conditions and continuous monitoring.

The exit from PCA wasn't just regulatory relief—it was institutional redemption. The bank had proven it could reform under pressure, clean up its balance sheet, and return to profitability. The employees who had endured the humiliation of PCA now wore their survival as a badge of honor. The bank had been to the brink and back.

The decade also saw significant strategic initiatives despite the crisis. The bank formed The Maharashtra Executor & Trustee Company as a wholly-owned subsidiary, diversifying revenue streams. Digital initiatives continued with the launch of MahaUPI in 2016, positioning the bank for the digital payments revolution. The branch network was rationalized—unprofitable branches closed, new ones opened in strategic locations.

The leadership during this period deserves special mention. A.S. Rajeev, who took charge as MD & CEO in December 2018, brought a combination of technical expertise and emotional intelligence crucial for navigating the post-PCA recovery. His approach—acknowledging past mistakes while building future capabilities—helped restore both internal morale and external credibility.

By 2020, Bank of Maharashtra had emerged fundamentally different from what entered the decade. It was leaner, more technologically advanced, and critically, more risk-aware. The infrastructure lending excesses had been purged. The credit culture had been reformed. The operational processes had been digitized. It wasn't the same bank that had crossed ₹1 lakh crore in business in 2010—it was arguably better, forged in the crucible of crisis.

The lessons were expensive but valuable. Political interference in lending decisions had nearly destroyed the bank. Rapid growth without adequate risk management was suicidal. Technology wasn't optional but essential. Most importantly, institutional resilience wasn't about avoiding crises but surviving them. Bank of Maharashtra had proven, once again, that it was a survivor. The question now was whether it could become a winner.

VII. Modern Transformation & Current Position (2020–Present)

The earnings call in Q4 FY2025 was electric. CEO Nidhu Saxena's voice carried a confidence that hadn't been heard from Bank of Maharashtra's leadership in years: The bank reported a standalone net profit of Rs 1,493.08 crore in Q4 FY25, registering a growth of 22.61%. The bank had earned a net profit of Rs 4,055 crore in the previous fiscal. For an institution that was in regulatory intensive care just five years ago, these weren't just numbers—they were a declaration of arrival.

The transformation began with a fundamental reimagining of the revenue model. Revenue Breakup Retail Banking: ~39% in FY24 vs ~35% in FY22 Corporate/ Wholesale Banking: ~36% in FY24 vs ~30% in FY22 Treasury: 21% in FY24 vs 32% in FY22. This shift wasn't accidental—it was strategic. The bank deliberately reduced its dependence on volatile treasury income, building instead a more stable base of retail and corporate lending revenues.

The digital transformation story is particularly compelling. What started as regulatory compliance during PCA became competitive advantage. The bank's digital lending platform now processes personal loans in minutes, not days. Video KYC enabled 13,000 account openings in FY24 without customers visiting branches. The MahaUPI app competes credibly with fintech offerings. This isn't your grandfather's PSU bank—it's a digital-first institution that happens to have 2,641 physical branches.

The numbers tell a story of operational excellence finally achieved. Current Price ₹ 55.4, Stock P/E 7.44, Book Value ₹ 37.3, Dividend Yield 2.70 %, ROE 22.8 %. That ROE of 22.8% is remarkable—it's not just profitable, it's generating returns that would make private banks envious. Yet the market values it at just 7.44 times earnings, a fraction of private bank valuations. This disconnect between performance and perception is the modern Bank of Maharashtra paradox. The recent Q2 2024 results paint a picture of sustained excellence. State-owned Bank of Maharashtra (BoM) on Tuesday posted a 44 per cent jump in its profit at Rs 1,327 crore in the second quarter ended September 2024 on account of improvement in interest income. With regard to asset quality, the bank has demonstrated improvement with gross Non-Performing Assets (NPAs) moderating to 1.84 per cent of the gross loans by the end of September 2024 from 2.19 per cent a year ago. Similarly, net NPAs or bad loans came down to 0.20 per cent from 0.23 per cent at the end of the second quarter of the previous fiscal.

The government ownership dynamics have evolved significantly. During the quarter, BoM raised Rs 3,500 crore from Qualified Institutional Placement while Rs 1,000 crore from Tier II bonds. Following QIP, the government stake in the bank came down 79.60 per cent compared to 86.46 per cent in the previous quarter. This reduction in government stake, while still maintaining control, signals confidence in market-based capital raising.

The operational metrics reveal a bank firing on all cylinders. The credit-deposit ratio of 78.72% shows efficient deployment of resources. The cost-to-income ratio at 38.81% demonstrates operational efficiency rarely seen in PSU banks. The provision coverage ratio of 98.31% suggests conservative risk management. These aren't the metrics of a struggling PSU bank—they're the numbers of a well-run financial institution.

The regional dominance story remains compelling. It has the largest network of branches of any public sector bank in the state of Maharashtra. This isn't just geographic presence—it's deep market penetration. In Maharashtra's tier-2 and tier-3 cities, Bank of Maharashtra isn't just a bank; it's THE bank. This local monopoly in many markets provides pricing power and customer stickiness that new-age banks can't replicate.

The digital initiatives have moved beyond catch-up to innovation. The bank's collaboration with fintech companies has yielded products that compete directly with digital-first players. The "Maha Krishi Samruddhi Scheme" for agro and food processing industries shows sector-specific innovation. The video KYC platform, online loan processing, and API banking services demonstrate that this isn't your father's PSU bank anymore.

The human capital transformation is perhaps most remarkable. The old guard of lifetime employees has given way to a more dynamic workforce. Performance-linked incentives, previously anathema in PSU culture, are now standard. The bank actively recruits from IIMs and IITs, competing for talent with private banks. Training programs focus on digital skills and customer service, not just regulatory compliance.

The subsidiary strategy adds another dimension. The Bank's segments include Treasury, Corporate/Wholesale Banking, Retail Banking and Other banking operations. The Maharashtra Executor & Trustee Company provides fee income diversification. These aren't just regulatory requirements but strategic revenue streams that reduce dependence on traditional banking income.

Risk management has evolved from compliance to competitive advantage. The bank's early warning systems now use artificial intelligence to flag potential NPAs. Credit underwriting combines traditional relationship banking with algorithmic scoring. The treasury operations use sophisticated hedging strategies. This isn't the risk management that failed during the infrastructure boom—it's modern, data-driven, and proactive.

The ESG (Environmental, Social, Governance) initiatives position the bank for future relevance. Green financing products, financial inclusion programs, and governance improvements aren't just compliance—they're strategic differentiators. The bank's role in distributing government welfare schemes provides both social impact and fee income.

Looking at the current position, Bank of Maharashtra has achieved something remarkable—it has become both commercially successful and socially relevant. The 22.8% ROE proves it can generate returns. The 2,641 branches prove it can serve the masses. The digital platforms prove it can compete with fintechs. The recovering brand proves it can overcome reputational damage.

Yet challenges remain stark. The valuation discount to private banks persists despite superior performance. Government ownership, while providing stability, limits strategic flexibility. The branch-heavy model, while providing reach, pressures costs. Competition from both ends—premium private banks and no-frills payment banks—squeezes margins.

The transformation from 2020 to present isn't just recovery—it's reinvention. Bank of Maharashtra has proven that a PSU bank can be profitable, efficient, and innovative while maintaining its social mandate. It has shown that government ownership doesn't necessarily mean operational mediocrity. Most importantly, it has demonstrated that institutional resilience—the ability to adapt, survive, and thrive—might be the most valuable asset of all.

VIII. Business Model & Competitive Position

Walk into any Bank of Maharashtra branch in Pune, Mumbai, or Nashik, and you'll see something unique in Indian banking—three distinct customer segments under one roof. In one corner, a farmer discusses a Kisan Credit Card with a rural banking officer who speaks fluent Marathi. At the premium banking desk, a tech entrepreneur negotiates terms for working capital finance. Near the entrance, a college student opens her first savings account through a tab-wielding assistant. This isn't market segmentation theory—it's the lived reality of a business model that serves everyone from daily wage earners to large corporates.

The segment performance tells the strategic story. The Bank's segments include Treasury, Corporate/Wholesale Banking, Retail Banking, and Other Banking Operations. The evolution of the revenue mix is particularly revealing: Retail Banking grew from ~35% in FY22 to ~39% in FY24, Corporate/Wholesale Banking expanded from ~30% to ~36%, while Treasury contracted from 32% to 21%. This isn't random drift—it's deliberate rebalancing toward more stable, relationship-based income streams.

The retail banking transformation deserves deeper examination. Five years ago, retail was the neglected stepchild, contributing barely 30% of revenues. Today, with 35 million customers and growing, it's the growth engine. The bank didn't achieve this through aggressive pricing—it can't compete with HDFC on rates. Instead, it leveraged what private banks lack: trust in smaller markets, vernacular capability, and patience with smaller ticket sizes.

Corporate banking presents a different dynamic. Bank of Maharashtra can't win the Reliance or Tata accounts—those go to SBI or foreign banks. But in the ₹50-500 crore revenue segment—successful Maharashtrian SMEs growing into mid-corporates—the bank dominates. These aren't price-sensitive commodity relationships but deeply embedded partnerships where the bank has financed growth from startup to scale.

The CASA ratio tells a story of competitive disadvantage turned into strength. At 49.29%, it's lower than private banks achieving 55-60%. But the composition is different—these aren't urban salary accounts that switch banks for better apps. These are rural savings accounts, small business operating accounts, trust accounts from institutions that value stability over convenience. The stickiness is remarkable—customer attrition rates are among the lowest in Indian banking.

Technology infrastructure has evolved from weakness to adequacy, though not yet advantage. The core banking system, fully implemented across all branches, provides the backbone. The mobile app, while not as slick as Kotak's, works reliably on basic smartphones. The internet banking platform handles 80% of corporate transactions. It's pragmatic technology—built for reliability over elegance, accessibility over innovation.

The branch network strategy reveals sophisticated thinking. While private banks close branches and fintechs mock physical presence, Bank of Maharashtra sees branches differently. In urban areas, they're transaction centers being converted to sales and service points. In semi-urban markets, they're community centers providing financial education alongside banking. In rural areas, they're often the only formal financial institution for miles.

The cost structure remains the elephant in the room. With over 30,000 employees and 2,641 branches, the cost-to-income ratio of 38.81% is actually impressive—but achieved through wage suppression rather than productivity gains. The average employee cost is a fraction of private banks, but so is productivity. The bank generates roughly ₹1.5 crore of business per employee compared to ₹3-4 crore at efficient private banks.

Government business provides a unique competitive moat. As a PSU bank, Bank of Maharashtra is the default choice for government departments, public sector enterprises, and government schemes. This isn't just about deposits—it's about fee income from distributing subsidies, managing government payments, and providing cash management services. When the Maharashtra government pays salaries or pensions, it flows through Bank of Maharashtra's systems.

The subsidiary strategy adds specialized capabilities. The Maharashtra Executor & Trustee Company Pvt Ltd isn't just a regulatory requirement—it's a fee income generator providing estate planning and trustee services. These high-margin, low-risk services leverage the bank's trust advantage and provide cross-selling opportunities to high-net-worth customers.

Competition analysis reveals a nuanced position. Against SBI and other large PSU banks, Bank of Maharashtra competes on local knowledge and agility. Against private banks, it leverages trust and reach. Against small finance banks and payment banks, it offers full-service banking. Against fintechs, it provides physical presence and regulatory safety. It's not winning every battle, but it's not losing the war either.

The pricing power varies dramatically by segment and geography. In rural Maharashtra, the bank often faces no competition and can price accordingly. In urban corporate banking, it's a price taker. In retail lending, it sits in the middle—not the cheapest but not premium either. This geographic and segment diversity provides resilience—weakness in one area offset by strength in another.

Digital capabilities have evolved from non-existent to competitive. The bank processes over 100,000 digital transactions daily. The API banking platform serves 50+ corporate clients. The WhatsApp banking service handles basic queries. It's not cutting-edge—no blockchain experiments or AI chatbots—but it's functional and improving. The digital strategy is pragmatic: fast-follow rather than first-mover.

Risk management has become a competitive differentiator. The bank's provision coverage ratio of 98.31% is among the highest in Indian banking. The underwriting standards, tightened post-PCA, are conservative but not restrictive. The early warning systems flag stress before it becomes distress. This isn't the aggressive lending culture that created the NPA crisis—it's sustainable, profitable growth.

Partnership strategies multiply capabilities without multiplying costs. Tie-ups with insurance companies provide fee income. Fintech collaborations bring digital capabilities. Government partnerships ensure steady business flow. Corporate tie-ups provide salary accounts. These aren't transformative individually, but collectively they create an ecosystem that's hard to replicate.

The innovation pipeline, while not Silicon Valley-esque, shows promise. The bank is piloting voice-based banking for illiterate customers. It's experimenting with satellite branches—tech-enabled kiosks in remote areas. It's developing supply chain financing products for agricultural value chains. These aren't headline-grabbing innovations, but they solve real problems for real customers.

Looking at the business model holistically, Bank of Maharashtra has achieved something rare—a sustainable competitive position despite obvious disadvantages. It can't match private banks on service or technology. It can't match SBI on scale. It can't match fintechs on innovation. But it doesn't need to. It has found a profitable niche serving customers others ignore, in markets others avoid, with products others don't offer.

The competitive position is best described as "embedded resilience." The bank is so deeply woven into Maharashtra's economic fabric that dislodging it would be enormously difficult. Every small business that got its first loan here, every farmer who receives MSP payments through the bank, every government employee whose salary account sits here—they create a network effect that technology alone can't break.

IX. Playbook: Lessons from a Survivor

The boardroom at Lokmangal, Bank of Maharashtra's headquarters, has witnessed every crisis Indian banking could throw at an institution. The walls, if they could speak, would tell stories of survival that read like a masterclass in institutional resilience. From those stories emerge patterns—not lucky breaks or government bailouts, but deliberate strategies that enabled a regional bank to survive existential threats that killed many peers.

Lesson 1: Building Through Adversity Creates Antifragility

The Great Depression didn't break Bank of Maharashtra; it created it. Born when 54 banks had failed in Bombay Presidency alone, the institution developed DNA that assumed crisis as normal. This shaped everything—conservative underwriting when times were good, capital buffers above regulatory requirements, diversification as religion not option. While peers leveraged up during booms, Bank of Maharashtra remembered busts. This institutional memory, encoded in culture and process, proved invaluable when 2008, 2013, and 2017 crises hit.

The pattern repeated through nationalization and liberalization. Each disruption forced adaptation that made the bank stronger. Nationalization killed entrepreneurial spirit but taught scale and process. Liberalization destroyed competitive advantage but forced customer focus. PCA was humiliating but catalyzed operational transformation. The bank didn't just survive these shocks—it metabolized them into capabilities.

Lesson 2: Regional Advantage in a National Market

Bank of Maharashtra discovered something counterintuitive—in banking, being deeply local can be more valuable than being broadly national. While peers chased pan-India presence, diluting focus and increasing complexity, Bank of Maharashtra doubled down on Maharashtra and contiguous markets. This concentration created information advantages (knowing every major business in Pune), relationship advantages (three-generation banking families), and operational advantages (Marathi-speaking staff serving Marathi-speaking customers).

The regional strategy extended beyond geography to psychography. The bank understood the Maharashtrian entrepreneurial mindset—conservative but ambitious, relationship-oriented but performance-focused, traditional but adaptive. Products were designed for this specific culture. The home loan product assumes joint families. The business loan product accommodates seasonal cash flows. The savings products align with local festival cycles.

Lesson 3: Government Ownership as Shield and Sword

Conventional wisdom says government ownership is purely negative—bureaucracy, interference, inefficiency. Bank of Maharashtra's experience suggests a more nuanced reality. Government ownership provided patient capital during crises when private shareholders would have fled. It guaranteed survival when pure market dynamics would have forced closure. It provided automatic trust in markets where private banks faced skepticism.

But the bank also learned to minimize ownership disadvantages. It created informal "air gaps" between operations and political interference. It used regulatory requirements as shields against unreasonable demands. It built professional management layers that absorbed political pressure while protecting operational integrity. The key was accepting government ownership as reality while preventing it from becoming destiny.

Lesson 4: Technology Transformation for Legacy Institutions

The digital transformation playbook for a 90-year-old PSU bank differs radically from a startup's approach. Bank of Maharashtra couldn't abandon legacy systems—millions of accounts depended on them. It couldn't move fast and break things—regulatory compliance demanded stability. It couldn't hire hundreds of engineers—government pay scales prevented it.

Instead, the bank developed a "parallel track" approach. New digital services ran alongside legacy systems, gradually migrating functionality. Partnerships provided capabilities that couldn't be built internally. The focus was on customer-facing digitization first, back-office later. Mobile banking targeted feature phones, not smartphones. The transformation took a decade, but it worked—today the bank is digitally competitive without having abandoned a single customer.

Lesson 5: Cost Management in a High-Fixed-Cost Model

With 30,000+ employees and 2,600+ branches, Bank of Maharashtra faced a cost structure problem that seemed unsolvable. Mass layoffs were impossible (unions), branch closures were politically sensitive, and salary increases were government-mandated. Traditional cost-cutting was off the table.

The solution was creative cost management. Branches were converted from cost centers to profit centers through aggressive cross-selling. Technology eliminated routine work, allowing staff redeployment to revenue-generating activities. Voluntary retirement schemes, carefully designed, reduced headcount without confrontation. Real estate assets were monetized through sale-and-leaseback arrangements. The cost-to-income ratio improved not through denominator reduction but numerator expansion.

Lesson 6: Capital Allocation Under Regulatory Constraints

PSU banks face unique capital allocation challenges—priority sector lending mandates, government scheme participation requirements, social banking obligations. Bank of Maharashtra turned these constraints into strategy. Priority sector lending focused on profitable agricultural value chains. Government schemes provided fee income alongside social impact. Financial inclusion initiatives built tomorrow's customers while serving today's mandate.

The key insight was that regulatory requirements weren't uniformly unprofitable—they were mispriced opportunities. While private banks avoided priority sectors, Bank of Maharashtra developed expertise that made these segments profitable. Agricultural lending, considered high-risk, became stable through deep local knowledge. MSME lending, seen as operational-intensive, generated strong returns through relationship banking.

Lesson 7: Building Culture in a Public Sector Enterprise

Cultural transformation in a PSU faces unique obstacles—job security reduces performance pressure, government ownership limits incentive flexibility, union power constrains management authority. Bank of Maharashtra's approach was evolutionary, not revolutionary.

Performance culture was built through recognition, not just compensation. High performers were celebrated publicly, given choice postings, and fast-tracked for promotions. Training programs shifted from compliance focus to skill development. Young talent was given real responsibility early. Retirement celebrations honored service while signaling change. The culture shifted gradually—from entitlement to engagement, from process to performance, from survival to success.

Lesson 8: Managing Stakeholder Complexity

Bank of Maharashtra navigates a stakeholder maze that would paralyze most organizations—government owner, regulatory supervisor, union representatives, depositor interests, shareholder expectations, social obligations. The conventional approach would be sequential satisfaction. Bank of Maharashtra developed simultaneous optimization.

Each major decision was framed through multiple lenses. Branch closure saved costs (shareholder lens) but was repositioned as service improvement through digital channels (customer lens) and staff redeployment to growth areas (union lens). Priority sector lending met regulatory requirements while building tomorrow's corporate clients. CSR initiatives generated goodwill that translated into business.

Lesson 9: Strategic Patience in a Quarterly World

While private banks optimize for quarterly earnings and fintechs chase monthly metrics, Bank of Maharashtra operates on geological time. Relationships are measured in generations. Strategies unfold over decades. Investments are evaluated on lifecycle returns. This temporal arbitrage—being long-term in a short-term world—creates unique advantages.

The bank holds loans through cycles rather than selling at distress. It maintains branches in locations that won't be profitable for years. It invests in training knowing employees might leave. This patience isn't passive—it's strategic. In banking, survival is victory, and Bank of Maharashtra has survived longer than most.

Lesson 10: The Power of Institutional Memory

Every crisis teaches lessons, but most organizations forget them within a generation. Bank of Maharashtra built institutional memory into structure and process. Credit committees include members who remember previous cycles. Risk frameworks encode lessons from past failures. Training programs teach history alongside technique.

This memory prevents repeated mistakes. When infrastructure lending boomed in the 2000s, old-timers remembered the textile bust of the 1980s. When fintechs promised revolution, veterans recalled the dotcom bubble. When private banks агgressively grabbed market share, historians noted who survived previous wars. Memory didn't prevent participation but enforced moderation.

The Meta-Lesson: Resilience as Strategy

The overarching lesson from Bank of Maharashtra's journey is that resilience itself can be strategy. While competitors optimized for growth, efficiency, or innovation, Bank of Maharashtra optimized for survival. This wasn't defensive but adaptive—building capabilities that ensured existence while enabling evolution.

Resilience meant maintaining capital buffers when others leveraged up. It meant diversification when others specialized. It meant serving unprofitable customers who became profitable over time. It meant accepting lower returns in good times to avoid destruction in bad times. It meant being the cockroach, not the unicorn—less glamorous but more likely to survive the asteroid.

X. Bear vs. Bull Case Analysis

The investment committee meeting at a major Mumbai mutual fund is heated. The analyst presenting Bank of Maharashtra is facing sharp questions. "Why should we own a PSU bank trading at 7x earnings when HDFC Bank trades at 18x?" The analyst's response will determine whether the fund takes a position. This scene plays out across dozens of institutions, and their collective decision shapes the stock's destiny. Let's examine both sides of this debate.

The Bear Case: Why Skeptics See Structural Challenges

Valuation Discount Persistence

The most glaring bear argument starts with valuation. Bank of Maharashtra trades at a P/E of 7.44 versus 15-20x for leading private banks. This isn't a temporary dislocation—it's a persistent discount that has lasted years despite improving fundamentals. Bears argue this reflects structural issues that won't disappear: government ownership preventing true independence, limited pricing power in competitive markets, and chronic underinvestment in technology and talent.

The market is essentially saying: "We don't believe the current ROE of 22.8% is sustainable." History supports this skepticism. PSU banks have repeatedly shown strong performance only to stumble on asset quality issues, political interference, or competitive displacement. The market has been burned before and demands a margin of safety.

Government Ownership Constraints

At 79.6% government ownership, Bank of Maharashtra remains fundamentally a state enterprise. This brings inescapable limitations: CEO selection based on seniority rather than merit, board decisions influenced by political considerations, lending pressures during election cycles, and inability to make bold strategic moves like acquisitions or closures.

The government's priorities—financial inclusion, priority sector lending, scheme implementation—often conflict with commercial objectives. While the bank has learned to manage these tensions, they remain binding constraints. Every loan to an unviable PSU, every branch in an unprofitable location, every scheme participation with negligible fees—these are taxes on profitability that private competitors don't pay.

Competitive Disadvantage Intensifying

The competitive landscape is becoming more hostile, not less. Private banks are aggressively expanding into tier-2 and tier-3 markets, Bank of Maharashtra's stronghold. Fintechs are unbundling profitable products like payments and personal loans. Small finance banks are competing for the same priority sector borrowers but with better technology and service.

The technology gap, while narrowing, remains substantial. Bank of Maharashtra's technology budget is a fraction of HDFC Bank's. Its ability to attract tech talent is limited by government pay scales. While the bank has made impressive progress, it's running to stand still while competitors accelerate. In a business increasingly determined by technology, this gap might prove insurmountable.

Asset Quality Concerns

Bears point to history—every PSU bank boom has ended in an asset quality bust. While current NPAs are controlled at 1.84% gross and 0.20% net, skeptics see warning signs. Retail lending growth of 22% annually raises questions about underwriting standards. Corporate lending expansion coincides with an economic slowdown. Agricultural lending faces climate change risks.

The provision coverage ratio of 98.31% looks conservative, but it assumed normal economic conditions. A serious downturn, a real estate crash, or a corporate debt crisis could quickly erode this buffer. The bank's improved risk management is untested in a severe crisis. Bears remember that Bank of Maharashtra required PCA intervention just five years ago—can leopards really change their spots?

Limited Pricing Power

In urban markets, Bank of Maharashtra is a price taker competing against better brands. In rural markets where it has pricing power, yields are constrained by regulatory caps and political sensitivity. The sweet spot—profitable customers willing to pay premiums—increasingly goes to private banks with better service or fintechs with better convenience.

The CASA ratio at 49.29% and declining reflects this challenge. Customers maintain accounts for transaction convenience but invest surpluses elsewhere. The bank is becoming a utility—essential but commoditized. Utilities can be profitable, but they rarely command premium valuations.

Management Continuity Risks

PSU bank leadership is notoriously unstable. CEOs serve three-year terms, barely enough time to implement strategy. The current management has delivered impressive results, but what happens when they rotate out? Will the next leadership maintain momentum or revert to PSU mediocrity?

The talent pipeline is concerning. High performers leave for private sector opportunities. Government pay scales can't compete for specialized skills. Training investments often benefit competitors who poach trained staff. This human capital disadvantage compounds over time.

The Bull Case: Why Believers See Hidden Value

ROE Transformation Is Real and Sustainable

Bulls start with the numbers: ROE of 22.8% isn't a fluke but the result of systematic improvements. Asset quality has been cleaned up. Operational efficiency has improved. Digital adoption is reducing costs. These aren't temporary factors but structural improvements that should persist.

The ROE improvement trajectory—from negative during PCA to 22.8% now—suggests momentum, not mean reversion. Operating leverage remains substantial; as the bank grows, fixed costs spread over larger revenue base. Technology investments are beginning to pay off. The best is yet to come.

Valuation Discount Creates Asymmetric Opportunity

Trading at 1.48x book value versus 3-4x for private banks, the downside is limited while upside is substantial. Even reaching 10x P/E—still a discount to private banks—implies 35% upside. If the bank continues executing and the market recognizes improvement, rerating to 12-15x is possible, suggesting 60-100% returns.

The dividend yield of 2.70% provides income while waiting for rerating. Government ownership ensures no bankruptcy risk. This is a classic value investment—buying quality assets at distressed prices. The margin of safety is substantial.

Maharashtra Growth Story

Maharashtra contributes 14% of India's GDP and hosts the country's financial capital. As the state grows, Bank of Maharashtra benefits disproportionately given its dominant position. Infrastructure development, industrial growth, and urbanization all drive credit demand where the bank is strongest.

The bank's 2,641 branches in Maharashtra provide unmatched distribution. Relationships built over generations create switching costs. Local knowledge enables better underwriting. This isn't just market share—it's an embedded position that would take competitors decades to replicate.

Digital Transformation Gaining Momentum

Bulls see digital progress as underappreciated. The bank processed over ₹1 lakh crore digitally last quarter. Video KYC, API banking, and WhatsApp banking show innovation capability. The technology gap, while real, is narrowing faster than bears appreciate.

More importantly, the bank is leapfrogging legacy technology. While private banks struggle with 1990s core banking systems, Bank of Maharashtra's recent implementation is more modern. Cloud adoption, API architecture, and mobile-first design position the bank for future competition.

Government Backing Provides Stability

While bears see government ownership as purely negative, bulls see hidden positives. Implicit sovereign guarantee means no depositor losses. Priority sector lending requirements become advantages as financial inclusion expands addressable market. Government business provides steady fee income. Political connections facilitate corporate relationships.

In uncertain times, stability has value. Bank of Maharashtra survived demonetization, GST implementation, COVID-19, and multiple economic cycles. This resilience, backed by government support, is worth something—perhaps more than the market appreciates.

Under-Earning Asset with Upside

The bank is deliberately conservative, maintaining high provision coverage and strong capital buffers. This depresses current profitability but creates future upside. As confidence builds, provisions can normalize, releasing earnings. Capital optimization could boost ROE further.

The branch network, currently a cost burden, could become valuable as financial inclusion expands. Rural and semi-urban markets are under-penetrated. As incomes rise and financial awareness grows, these branches become profit centers. The investment has been made; returns are beginning.

Management Execution Validates Strategy

Current management has delivered on every promise—exiting PCA, improving asset quality, growing profitably, digital transformation. This execution track record suggests competence, not luck. The strategic vision—become Maharashtra's premier bank while maintaining national presence—is clear and achievable.

The culture change, while gradual, is real. Performance orientation, customer focus, and digital adoption are becoming embedded. This isn't just one management team but institutional transformation that should survive leadership changes.

The Synthesis: A Nuanced View

The truth lies between extremes. Bank of Maharashtra is neither the value trap bears describe nor the hidden gem bulls proclaim. It's a recovering institution with genuine improvement but persistent challenges. The investment case depends on time horizon, risk tolerance, and belief in India's financial inclusion story.

For traders seeking quick gains, better opportunities exist elsewhere. For investors willing to wait 3-5 years, the risk-reward is attractive. The bank won't become HDFC Bank, but it doesn't need to. Being a profitable, growing, dividend-paying bank in India's largest state economy is enough.

The key monitorable metrics are clear: ROE sustainability above 20%, asset quality through economic cycles, digital adoption versus customer attrition, and government stake reduction below 75%. If these trends continue, bulls win. If any reverse, bears are vindicated.

XI. Epilogue: The Future of Public Sector Banking

The year is 2030. The Reserve Bank of India Governor is addressing a gathering of global central bankers in Basel. On the presentation screen is an unlikely case study—Bank of Maharashtra, now cited as a model for public sector bank transformation in emerging markets. The audience, skeptical of state-owned banks after decades of failures worldwide, listens intently. How did an institution written off as a relic become relevant again?

This future isn't guaranteed, but it's possible. The paths from here to there reveal not just Bank of Maharashtra's trajectory but the evolution of public sector banking itself in an economy transforming at digital speed while carrying analog obligations.

The Privatization Debate: A False Binary

The drumbeat for PSU bank privatization has grown louder with each passing year. The narrative is seductive—private ownership brings efficiency, innovation, and profitability. The evidence from HDFC Bank, Kotak, and ICICI seems conclusive. Why maintain state-owned banks that chronically underperform?

But Bank of Maharashtra's journey suggests the debate misses nuance. The issue isn't ownership structure but operational freedom. A government-owned bank run professionally can outperform a private bank run poorly. The key variables are governance quality, management autonomy, and regulatory framework—not just capital structure.

More fundamentally, India needs different types of banks for different purposes. Private banks excel at serving profitable customers in profitable markets. But who serves the marginal farmer in Vidarbha? Who finances the first-generation entrepreneur in Solapur? Who maintains branches in locations that won't be profitable for decades? Market failure in financial services is real, and public sector banks are the correction mechanism.

The likely future isn't mass privatization but strategic differentiation. Some PSU banks will privatize, others will merge, and a few will remain public but transform. Bank of Maharashtra, with its regional strength and improving metrics, is positioned for the third path—remaining public but becoming profitable.

Financial Inclusion: The Unfinished Revolution

India has 400 million people who remain unbanked or underbanked. They transact in cash, borrow from moneylenders, and save in gold. Bringing them into the formal financial system isn't just social justice—it's economic opportunity. This is where Bank of Maharashtra's 2,641 branches become strategic assets, not legacy burdens.

The financial inclusion opportunity isn't about basic accounts—Jan Dhan Yojana solved that. It's about graduated services: micro-insurance for crop failure, micro-pensions for old age, micro-credit for enterprise. These products require trust, local presence, and patience for profitability—exactly what PSU banks provide.

Technology changes the inclusion equation. A branch with satellite connectivity and biometric authentication can serve villages miles away. A relationship manager with a tablet can onboard customers in their homes. A WhatsApp bot can answer queries in Marathi. Physical presence enhanced by digital capability is powerful combination.

By 2030, Bank of Maharashtra could serve 100 million customers—triple today's count. Most will be small-balance, low-transaction customers initially. But as India's per capita income doubles, these customers become profitable. The bank that serves them through the journey from poverty to prosperity captures generational loyalty.

Technology as Equalizer, Not Differentiator

The technology gap between PSU and private banks is narrowing because technology itself is democratizing. Cloud computing eliminates infrastructure advantages. Open banking APIs level the playing field. Fintech partnerships provide capabilities without capital investment. AI and machine learning are available as services, not proprietary advantages.

Bank of Maharashtra's technology strategy for 2030 isn't about competing with HDFC Bank on innovation but achieving parity on functionality. Customers should be able to do anything digitally they can do at a private bank. The differentiation comes from combining digital capability with physical presence, algorithmic efficiency with human judgment.

The real technology opportunity is in vernacular banking. While private banks optimize for English-speaking urban customers, Bank of Maharashtra can build Marathi-first, Hindi-second, English-third interfaces. Voice banking for illiterate customers. Video banking for complex products. Visual banking for young customers. Technology that serves India, not just Indianapolis.

ESG: From Compliance to Competitive Advantage

Environmental, Social, and Governance considerations are transforming from reporting requirements to business imperatives. Climate change threatens agricultural lending. Social inequality constrains market growth. Governance failures destroy franchises overnight. ESG isn't Corporate Social Responsibility 2.0—it's risk management and opportunity capture.

Bank of Maharashtra's ESG positioning could become a unique advantage. Financing renewable energy projects in Maharashtra. Supporting sustainable agriculture practices. Enabling women entrepreneurship. These aren't charity but investments in future markets. The bank that helps Maharashtra transition to sustainable growth captures value from that transition.

Governance improvements matter most. Independent directors with real power. Risk committees with teeth. Audit functions with autonomy. Transparent reporting beyond regulatory requirements. The market values governance quality increasingly, and PSU banks that demonstrate genuine improvement will see valuation re-rating.

Success Metrics for 2030

What would success look like for Bank of Maharashtra in 2030? Not becoming India's largest bank—that's unrealistic. Not achieving the highest ROE—that's unsustainable. Success would be:

- Financial Performance: ROE consistently above 18%, ROA above 1.5%, Cost-to-income below 35%

- Market Position: Among top 3 banks in Maharashtra, Top 10 nationally by profitability

- Digital Adoption: 80% transactions digital, 90% accounts digitally active

- Financial Inclusion: 100 million customers served, 50% from rural/semi-urban markets

- Asset Quality: Gross NPA below 2%, Credit costs below 50 basis points

- Valuation: P/E ratio above 12x, P/B ratio above 2x

- Sustainability: Carbon neutral operations, 20% loan book in sustainable finance

These aren't stretch targets but achievable goals given current trajectory. They represent a bank that has successfully navigated the transition from survival to success, from public sector laggard to responsible banking leader.

The Broader Implications

Bank of Maharashtra's transformation carries lessons beyond banking. It shows that institutional renewal is possible even after near-death experiences. That government ownership doesn't doom organizations to mediocrity. That serving social purposes and generating profits aren't mutually exclusive. That regional focus can triumph over national ambition.

For investors, it demonstrates that value exists in unlikely places. For policymakers, it proves that PSU reform is possible without privatization. For competitors, it warns that written-off players can return stronger. For employees, it shows that culture can change even in government organizations.

Most importantly, for the millions of Indians still struggling to access formal finance, Bank of Maharashtra's journey offers hope. If a bank born in colonial India, nationalized in socialist India, and nearly broken in liberalized India can transform itself for digital India, then perhaps financial inclusion isn't just rhetoric but achievable reality.

The Last Word

Standing in that Basel conference room in 2030, the RBI Governor concludes the presentation with a simple observation: "Bank of Maharashtra survived everything the 20th century threw at it and is thriving in the 21st. It's not the biggest, fastest, or most innovative bank in India. But it might be the most resilient. In a world of black swans and grey rhinos, resilience is the ultimate competitive advantage."

The audience applauds politely, still skeptical but intrigued. Another presenter takes the stage to discuss neo-banks and embedded finance. But a few audience members linger on the Bank of Maharashtra case, wondering if they've been too quick to dismiss public sector banking. Perhaps there's wisdom in institutions that measure success in decades, not quarters. Perhaps survival itself is a form of innovation.

Bank of Maharashtra's story isn't finished. At 90 years old, it might just be getting started. The Swadeshi bank that survived it all might have one more transformation left—from survivor to winner. Time, that most patient of judges, will tell.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube