Ageas: From the Ashes of Fortis — A Phoenix Story of European Insurance

I. Introduction & Episode Roadmap

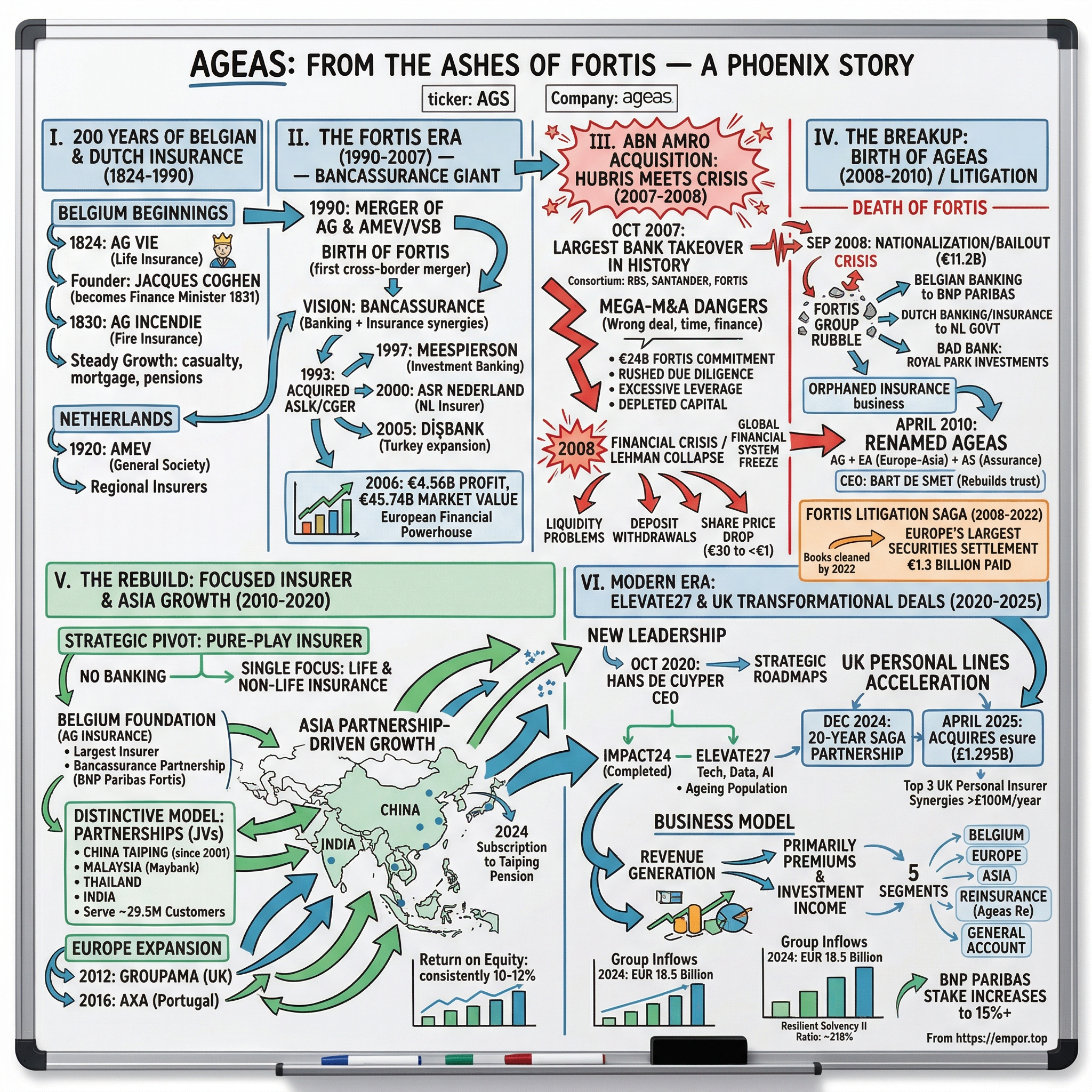

The smoke hadn't yet cleared from the wreckage of one of Europe's most spectacular corporate collapses when a small band of insurance executives began rebuilding something from the rubble. In the autumn of 2008, as governments scrambled to prevent financial Armageddon, the once-mighty Fortis Group—a €45 billion Benelux banking and insurance colossus—had been torn apart in a matter of weeks. Its banking operations were nationalized, sold off, or absorbed by larger players. What remained was an orphaned insurance business, burdened with toxic assets, haunted by litigation, and stripped of its very name.

Fast forward to November 2025: Ageas is a Belgian multinational insurance company co-headquartered in Brussels, and Belgium's largest insurer, operating in 13 countries worldwide. The company has a trailing twelve-month revenue of $9.2 billion and a market capitalization of approximately $13 billion. This is no longer the wounded survivor of a banking crisis—this is a focused, disciplined insurance pure-play that has reinvented itself through a partnership-driven growth model that many analysts consider best-in-class.

The central question that defines this story: How did the surviving insurance arm of one of Europe's most spectacular corporate collapses rebuild itself into a thriving international insurer?

The company was renamed from Fortis Holding in April 2010 and consists of those insurance activities remaining after the breakup and sale of the financial services group Fortis during the 2008 financial crisis. But this isn't merely a story of survival—it's a masterclass in corporate reinvention. The themes that run through Ageas's transformation offer powerful lessons for investors and business strategists alike: the dangers of mega-M&A, the phoenix strategy of rebuilding after catastrophic failure, the superiority of partnership-based growth models, and the strategic value of geographic diversification when executed with discipline.

The company that emerged from the Fortis wreckage has generated returns on equity consistently between 10-12% over the past decade, outperforming many European insurance peers. It has settled Europe's largest securities class action, expanded aggressively into Asia through joint ventures, and—most recently—has been making bold moves to consolidate its position in the UK personal lines market. This is the story of how a corporate phoenix rose from the ashes.

II. Origins: 200 Years of Belgian & Dutch Insurance

In the summer of 1824, as Belgium still lay unified with the Netherlands under King William I, two members of the Brussels Chamber of Commerce—vice-chairman François Rittweger and banker Jacques Coghen—became captivated by an idea that had been spreading through the financial centers of Europe: life insurance. In September 1823, King Willem I had authorized the creation of a Dutch life insurance company in Amsterdam. The idea of creating a life insurance company seduced these Brussels businessmen. The project received royal assent on 12 June 1824 with the company adopting the name of Compagnie d'Assurances Générales sur la Vie, les Fonds Dotaux et les Survivances (AG Vie).

Coghen himself took charge as "General Agent." The capital was set at 600,000 florins divided into 300 shares. At the end of February 1825, the company AG Vie opened its office, after its five employees had sworn loyalty in front of the members of the board of directors. This small Belgian enterprise would ultimately become the foundation stone for what is today Ageas—Belgium's largest insurer.

The young company's trajectory was transformed by Belgian independence in 1830. In April 1830 AG Vie's directors decided to create a fire insurance company, the Compagnie d'Assurances Générales contre les Risques d'Incendie (AG Incendie). In September 1830, following Belgium's declaration of independence, general agent Jacques Coghen was appointed Financial Administrator-General of the provisional government. In July 1831, Leopold I entrusted him with the Finance portfolio in his first government. When your company's founder becomes your nation's first finance minister, it suggests you're building something significant.

The company grew steadily through the late 19th and early 20th centuries. With the extension of the company's activities to related branches like casualty insurance and mortgage operations, AG Vie's premium income rose from 2.4 million Belgian francs at the end in 1889 to 20 million in 1912, and the number of employees from 12 in 1890 to 140 in 1924. In 1909, AG Vie's shares were listed on the Stock exchange. From 1919 onwards, collective pension insurance, a new branch of insurance primarily for company employees, contributed largely to the increase in premium income.

Meanwhile, across the border in the Netherlands, another insurance company was taking shape. AMEV had originally been founded in Utrecht in 1920 as Algemeene Maatschappij tot Exploitatie van Verzekeringsmaatschappijen (English: General Society for Operation of Insurance).

The name origins of today's Ageas tell the story of its ambitions and heritage. The first two letters "AG" were derived from AG Leven, the life insurance company formed in Belgium in 1824. The "e" and "a" in the new name stand for Europe and Asia—the focus of Ageas's growth strategy. The "a" plays another role when combined with "s", standing simply for assurance. The insurer also noted that Ageas derives from the Latin word "agere," which means action, drive, and a conviction to forge ahead.

By the late 20th century, both the Belgian AG Group and the Dutch AMEV had grown into substantial regional players. But the deregulatory wave sweeping through European financial services would soon create opportunities—and temptations—for something far more ambitious.

III. The Fortis Era: Building a European Banking & Insurance Giant (1990–2007)

The 1990 merger that created Fortis was revolutionary for its time. In 1990 AG took over the Netherlands-based firm AMEV/VSB to form Fortis. AMEV/VSB had itself been formed earlier that year by the combination of a savings bank, VSB (Verenigde Spaarbank), and an insurer, AMEV, which followed the end of legislation preventing mergers between banks and insurers. This was the first European cross-border financial merger—a precedent-setting transaction that combined Belgian insurance prowess with Dutch banking capabilities.

Fortis N.V./S.A. was a Benelux-centered global financial services group active in insurance, banking and investment management, initially formed in 1990 by a three-way Belgian-Dutch merger and headquartered in Brussels. It grew rapidly through multiple acquisitions, and in 2007 was the 20th largest financial services business in the world by revenue.

The man who orchestrated this creation was Maurice Lippens, who had joined the AG Group in 1981, became managing director in 1983, and then Chairman/Managing Director in 1988. He has been the Chairman of Fortis since 1990, participating in the creation of the group. In 2000, he became chairman of the executive committee of Fortis. Count Maurice Lippens was co-founder of Fortis, created in 1990, as the first European cross-border banking and insurance group.

The bancassurance model—the combination of banking and insurance under one roof—was the strategic vision that animated Fortis. The logic was seductive: bank customers are natural prospects for insurance products, and the distribution synergies between the two businesses could create powerful competitive advantages. Banks could cross-sell insurance, insurers could leverage banking relationships, and the combined entity could offer integrated financial solutions that neither could provide alone.

Throughout the 1990s and early 2000s, Fortis executed a relentless acquisition strategy to build out this vision. In 1993, Fortis acquired a majority stake in ASLK/CGER, a major Belgian bank, and took full ownership in 1999. In March 1997, Fortis acquired MeesPierson from ABN AMRO, establishing its presence in investment banking. In 2000, Fortis acquired Dutch insurer ASR Nederland, which made it the second-largest insurer in the Netherlands and the largest overall in the Benelux. In April 2005, Fortis started expanding farther abroad by acquiring the Turkish bank Dışbank from Doğan Holding.

By 2006, the company had become a genuine European financial powerhouse. As of that year, the company's profits were €4.56 billion, with a market value of €45.74 billion according to Forbes magazine. The transformation from a modest Belgian insurer founded in 1824 into one of the world's largest financial conglomerates had taken less than two decades.

Jean-Paul Votron, who became CEO in 2004, commented: "I see it as a great honour and challenge to take over from Anton van Rossum and build further on Fortis's success story by developing, with the members of the Executive Committee, the great potential of the people and the businesses of Fortis. Fortis is a respected and leading financial institution. It is still the first successful cross-border company in the industry."

Votron had started his career in 1975 at Unilever, where he had management responsibilities in international sales, marketing and general management. Between 1991 and 1997 he served in different positions with Citibank in Europe and the US, including President of Citibank Belgium, Director of Marketing and technology U.S. and Europe Consumer Bank, and Chairman and CEO of Citibank FSB. He brought the aggressive, growth-oriented mindset of a global banking veteran to Fortis.

But success bred ambition, and ambition bred hubris. The very strategies that had built Fortis into a continental champion would soon be taken to a dangerous extreme. The stage was being set for one of the most catastrophic corporate decisions in European business history.

IV. The ABN AMRO Acquisition: Hubris Meets the Financial Crisis (2007–2008)

KEY INFLECTION POINT #1

Picture a conference room in Edinburgh on August 10, 2007. Maurice Lippens, Executive Chairman of Fortis, Jean-Paul Votron, CEO of Fortis, Fred Goodwin, CEO of Royal Bank of Scotland, and Emilio Botin, Chairman of Spanish banking group Santander Central Hispano, posed during a photocall following an extraordinary general meeting of RBS. These four men had just achieved something unprecedented: shareholder approval for the largest bank takeover in history.

Fortis was part of the consortium with Royal Bank of Scotland Group (RBS) and Banco Santander, that announced on October 8, 2007, that an offer for 86% of outstanding ABN AMRO stock had been accepted, making way for the largest ever bank takeover in history.

The widely publicized banking takeover battle sustained by the British Barclays and a consortium led by the Royal Bank of Scotland that included the Dutch Fortis and the Spanish Santander, for the Dutch ABN AMRO, took place during six months, from March through October of 2007. The myriad legal and economic complexities involved and the mammoth size of the transaction (more than $100 billion) made it the largest banking industry M&A ever.

RFS formally acquired ABN AMRO on 17 October 2007. Fortis would receive ABN AMRO's Dutch and Belgian operations, Banco Santander would get Banco Real in Brazil and Banca Antonveneta in Italy, and RBS would get ABN AMRO's wholesale division and all other operations, including those in Asia.

Fortis would commit €24 billion of the total €72 billion bid, which offered better conditions than the rival Barclays bid. At a general assembly, on 6th August 2007, the acquisition plan was overwhelmingly supported, winning approximately 95% of the votes in Brussels and in Utrecht. Only one shareholder questioned the recklessness of this ambitious strategy.

That lone dissenting voice deserves recognition. Amid the triumphalism and the champagne, one shareholder saw what others refused to acknowledge: this was madness. Fortis announced excellent half-year results, with a statement that the sub-prime crisis would have limited impact. However, gradually, the market conditions changed with the first problems in the sub-prime market appearing in America during August 2007. In order to finance the deal, Fortis had to increase its capital substantially. The share issue on 21st September 2007 was a success thanks to the huge discount premium.

The takeover was badly timed and overly ambitious, and to fund it Fortis started selling noncore divisions while writing down collateralized debt. As Fortis' capital began to decline, the company initiated a rights issue, and the long-held promised dividend was suspended. As Fortis' share price began to decline and financial market conditions continued to worsen, with a series of leadership changes, customers began to withdraw deposits.

The foundation later filed suit seeking declaratory judgment against Fortis for defrauding investors through a 2007 rights issue to acquire ABN AMRO—the offering raised more than €13 billion, most of which was wiped out during the financial crisis.

Fortis had no realistic path to fixing its liquidity issues once short-term markets froze during the 2008 financial crisis. Its capital was depleted by the acquisition of ABN Amro deal, a €70 billion deal completed just before the crisis broke out. Fortis had financed much of that acquisition with short-term debt and disposal of assets, making it vulnerable to liquidity stress.

Both RBS and Fortis were increasingly visibly overextended following the ABN AMRO acquisition. On 22 April 2008, RBS announced the largest rights issue in British corporate history, which aimed to raise £12 billion in new capital to offset a writedown of £5.9 billion resulting from bad investments and to shore up its reserves following the purchase of ABN AMRO. On 11 July 2008, Fortis CEO Jean Votron stepped down after the ABN AMRO deal had depleted Fortis's capital.

On July 11, 2008, the CEO of Fortis Jean Votron stepped down. The total value of Fortis, as reflected by share value, was at that time a third of what it had been before the acquisition, and just under the value it had paid for ABN Amro's Benelux activities alone. Share price continued to waver below €10. Votron was succeeded as CEO by Herman Verwilst, who after a few weeks held a press conference to introduce himself and to reassure the shareholders that Fortis was solid. He succeeded in making a good impression for a short while and share price firmed up. This was helped by the announcement that Maurice Lippens, from the supervisory board, had personally bought a large number of shares (at just below €9 per share).

Then came September 2008, and the collapse of Lehman Brothers. The global financial system froze. Banks stopped lending to each other. Customers who had deposited money at Fortis began withdrawing it. Fortis was the largest Belgian bank in early 2008, positioned mainly in the Benelux. From mid-2008 onwards, the bank began facing severe liquidity problems and its stock value began rapidly declining. The problem was exacerbated by the earlier acquisition of the Dutch bank ABN Amro, which had depleted Fortis' capital. Since the beginning of 2008, about 3% of the deposits stalled at the bank were withdrawn. Belgian and Dutch ministers and financial regulators met each other on 27 September to tackle the crisis. The following day, Fortis was partially nationalised on 28 September 2008, with Belgium, the Netherlands and Luxembourg investing a total of €11.2 billion in the bank.

The speed of the collapse was breathtaking. In the 18 months between April 2007 and October 2008, the Fortis share price dropped from €30 to under €1.

On July 13, 2018, the Amsterdam Court of Appeals finally approved the €1.3 billion ($1.5 billion) settlement of a series of shareholder claims against Fortis in the wake of the global financial crisis. On October 4, 2008, the Dutch government took over the company's operations for 16.8 billion Euros ($23 billion).

Over a 12-month period from 2007-08, shareholder equity at Fortis fell from €33 billion to €6.8 billion. After the acquisition failed, Fortis encountered financial difficulties and broke up in the fall of 2008. Its investors lost as much as 90% of the value of their investments.

The ABN AMRO acquisition stands as perhaps the definitive case study in the dangers of mega-M&A: the wrong deal, at the wrong time, with the wrong financing structure. Every element was misjudged. The due diligence was rushed. The timing was catastrophic. The leverage was excessive. And the management team, intoxicated by years of successful acquisitions, had lost the capacity to recognize when a deal was simply too big and too risky.

V. The Breakup: Death of Fortis, Birth of Ageas (2008–2010)

KEY INFLECTION POINT #2

The rescue of Fortis in late September 2008 was only the beginning of its dissolution. What followed was a complex legal and political drama that would take years to fully resolve.

On December 12, 2008, a court decision made the sales of October 3, 5, and 6 contingent on shareholder approval (at the latest on February 12, 2009). Until that time, the Dutch government held the parts it bought, Fortis Bank was the property of the Belgium government, while Fortis Insurance Belgium remained with Fortis Group (together with Fortis Insurance International). On February 11, 2009, the shareholders declined to approve the sales, making the sales illegitimate; actual ownership of the various parts became a matter of further negotiations and/or litigation. A re-negotiation led to new deal, subject to shareholder approval (meetings on April 8–9, 2009).

Considered "too big to fail", Fortis received an €11.2 billion bailout from the Benelux governments and saw its retail banking operations in Belgium sold to BNP Paribas, and its insurance and banking subsidiaries in the Netherlands nationalised. The remaining assets of the company, consisting principally of insurance operations but also including some distressed assets, were rebranded Fortis Holding. In April 2010 its shareholders agreed a formal change of name to Ageas SA/NV, with ownership of the Fortis brand passing to BNP Paribas.

Fortis Bank Nederland was nationalised by the Dutch government and merged in July 2010 with ABN AMRO's former Dutch operations, which had not yet been integrated with Fortis following the 2007 takeover, to form a new group also called ABN AMRO; the other banking operations were acquired in 2008 by BNP Paribas and became part, respectively, of BNP Paribas Fortis in Belgium, BGL BNP Paribas in Luxembourg, BNP Paribas Bank Polska in Poland, and Türk Ekonomi Bankası in Turkey; Fortis's Dutch insurance operations were reorganized as ASR Nederland; the remaining insurance operations, still the largest in Belgium, were rebranded to Ageas in April 2010.

Toxic assets were placed in a bad bank called Royal Park Investments. Thanks in part to good management and multi-billion euro guarantees by the government the holding performed better than expected.

The man who would lead the resurrection was Bart De Smet. Bart De Smet joined the company in 1998 as a member of the management committee of Fortis AG (now AG Insurance) with responsibility for Fortis Employee Benefits. In 2005, he took charge of the Non-Life business and Broker Channel at Fortis Insurance Belgium, assuming the position of CEO of Fortis Insurance Belgium in 2007. In June 2009 he became CEO of Fortis, which was renamed Ageas in 2010. Under his leadership, the legacies from the financial crisis were resolved and Ageas transformed into a strong and independent international insurance Group.

Divested of banking operations that brought it to the verge of insolvency, the company that would become Ageas re-emerged with a single-minded focus on life and general insurance. The strategic logic was clear: the bancassurance model had been the source of Fortis's strength, but also the source of its downfall. The new company would be different—a pure-play insurer with a focused geographic strategy and a disciplined approach to partnerships.

The renaming to Ageas in April 2010 symbolized a complete break with the past. The Fortis brand—once synonymous with European financial ambition—now belonged to BNP Paribas. What remained was something smaller, more focused, and determined to prove that the insurance expertise at the heart of Fortis had value independent of the banking debacle.

VI. The Fortis Litigation Saga: Europe's Largest Securities Settlement (2008–2022)

KEY INFLECTION POINT #3

Even as Ageas was rebuilding its insurance operations, a legal storm was gathering. Shareholders who had lost fortunes in the Fortis collapse were not going quietly.

On October 22, 2008, Fortis shareholders filed a securities class action lawsuit against Fortis, certain of its directors and officers, and its offering underwriters in the Southern District of New York, seeking damages based on alleged violations of the U.S. securities laws. In their amended complaint, the plaintiffs alleged that the defendants misrepresented the value of its collateralized debt obligations; the extent to which its assets were held as subprime-related mortgage backed securities; and the extent to which its ill-fated decision to acquire ABN-AMRO had compromised the company's solvency.

On January 10, 2011, two U.S. securities law firms announced that they had filed an action in Utrecht Civil Court on behalf of a specially formed foundation, Stichting Investor Claims Against Fortis. The lawsuit action was filed against Ageas NV/BV, as Fortis is now known, certain of its directors and officers, and its offering underwriters. A separate Dutch shareholder foundation, Stichting FortisEffect also was organized on behalf of Fortis shareholders. In addition, the Dutch shareholder group VEB also organized an effort in the Netherlands on behalf of Fortis shareholders. Shareholder rights group Deminor separately filed an action against Fortis and its directors and officers in the Commercial Court in Belgium.

The litigation dragged on for years. The Amsterdam Court of Appeal approved a €1.3 billion collective settlement of claims asserted on behalf of shareholders of the former Fortis (now Ageas). The July 13, 2018 decision again shows that the Dutch Act on Collective Settlement of Mass Claims (the "WCAM") can be used to resolve transnational disputes regardless of whether those claims could be litigated adversarially on a classwide basis in the Netherlands or elsewhere.

The €1.3 billion settlement resolves all shareholder claims that relate to the 2007-2008 acquisition of ABN Amro and is the largest shareholder recovery in Europe to date. The settlement was the result of extensive multiparty negotiations between Ageas, SICAF, and three other groups of investors who actively pursued claims in either the Netherlands or Belgium. The settlement was declared binding and enforceable by the court under the WCAM, a provision of Dutch law that allows for the settlement of mass claims on a global basis.

Ageas increased the settlement amount by €100 million (from €1.204 billion to €1.3 billion), and the parties agreed to give Active and Non-Active Claimants the same base amounts of compensation, with Active Claimants being entitled to additional compensation of 25% to cover their costs.

A Dutch appeals court officially approved the largest securities settlement ever reached in Europe, clearing the way for international insurance company Ageas N.V./S.A. to begin payment of $1.5 billion (€1.3 billion) to multiple groups of institutional and individual investors from Europe and the United States. The ruling was issued by the Amsterdam Court of Appeals, following seven years of litigation in the Dutch courts. The approved settlement resolves four separate cases brought against Ageas (formerly known as Fortis) by various investor claimant groups. The lawsuit of one of the claimant groups, the foundation Stichting Investor Claims Against Fortis (SICAF), had over 180 participating institutional investors holding more than 80 million shares.

Fortis supremos Maurice Lippens and Jean-Paul Votron will now not have to face a trial. Prosecutors say that proving fraud would be too difficult. After the collapse of Fortis Brussels prosecutors opened an investigation into possible attempts to mislead investors. Five years later it decided to prosecute seven leading Fortis figures including former chairman Lippens and former CEO Votron, his successor Herman Verwilst, former financial director Gilbert Mittler as well as Filip Dierckx, Reginald De Gols and Lars Machenil. Charges included misleading investors during the 2007 capital enhancement because a gloss was allegedly put on the bank's performance. It was argued investors were told too late in the day of the exposure to the sub-prime market of US junk mortgages that triggered the global crisis. Suspects were charged with fraud, misleading investors and failing to provide investors with sufficient information. Belgian prosecutors have decided to drop charges against seven former executives at Fortis.

The net impact of the proposed settlements on the Group net IFRS result amounted to €889 million. Ageas announced that the claims administrator paid the final instalments to claimants in 2022, closing the Fortis settlement for almost all claimants—nearly fifteen years after the crisis began.

For investors considering Ageas today, the settlement represents both a legacy burden that has been resolved and a cautionary reminder. The company paid dearly for the sins of its predecessor. But by 2022, the books were finally clean. The phoenix could fly unencumbered.

VII. The Rebuild: Focused Insurance Pure-Play Strategy (2010–2020)

The strategic pivot that defined the new Ageas was both simple and radical: become a focused insurance pure-play. No more banking adventures. No more conglomerate ambitions. Instead, the company would concentrate on what it knew best—insurance—and grow through a distinctive partnership model that contrasted sharply with the empire-building that had destroyed Fortis.

In 2010, Ageas reported a net profit of €400 million and total revenues reached €8.6 billion, reflecting a solid footing in the industry post-restructuring. This was a company starting over, but starting with genuine assets: a 200-year heritage in Belgian insurance, strong market positions, and a team that understood the industry deeply.

The company is the largest provider of insurance in Belgium, owning 75% of AG Insurance (the remainder is held by Fortis Bank N.V./S.A., which was sold to BNP Paribas in 2009). Products are sold through independent agents, brokers and financial planners, and through branches of BNP Paribas Fortis and its subsidiary Banque de La Poste/Bank van De Post.

In 2024 AG celebrated its 200-year anniversary, marked by a special visit from King Philippe of Belgium. Back in 1824 nobody could have predicted that 200 years on, one in two Belgian families would be insured by AG; that over 4,400 employees and close to 5,000 distribution partners would work every day to support 3 million customers; and that AG is Belgium's largest institutional investor with close to EUR 70 billion in assets under management.

The approach contrasted with the conglomerate overreach that contributed to the Fortis collapse, emphasizing partnerships with local banks for distribution leverage and bolt-on deals to capture market share without excessive leverage.

In September 2012, Ageas acquired Groupama's UK insurance operations, boosting its presence in the automobile and home sectors. The deal saw Ageas add another million policyholders in the UK. Dutch-Belgian insurance group Ageas confirmed that it had signed an agreement, through its UK subsidiary, to acquire Groupama Insurance Company Limited (GICL), the UK subsidiary of France's Groupama, for a total consideration of £116 million (€145 million). Ageas said the acquisition would see it become the "fifth largest UK Non-Life insurer (with a 5.2 percent market share); fourth largest Private Motor insurer (with a 11.7 percent market share); and fourth largest Personal lines insurer (with a 7.1 percent market share)."

In 2016, Ageas acquired AXA insurance operations in Portugal, becoming the second largest insurer by premiums, the third Non-Life insurer (with a 14% market share) and the third largest Life insurer (with a 19% market share). This transaction would strengthen Ageas's position in Portugal—one of Ageas's core markets—especially in Non-Life and complements Ageas's activities by broadening distribution reach beyond the current focus on bancassurance. CEO Bart De Smet said: "After acquiring full control of our Non-Life activities in Portugal in 2014, we would be further strengthening our position in one of our core markets."

By 2015, insurance net profit reached €755 million, driven by strong performances in Asia and Belgium's non-life segments. Return on equity averaged approximately 10-12% from 2010 to 2020, outperforming many European insurance peers, whose ROE normalized at 8-10%.

The disciplined approach paid dividends—both literally and figuratively. Ageas rebuilt shareholder trust through consistent dividend payments and steady profit growth. It avoided the temptation to make transformative acquisitions that might recreate the risks that had destroyed Fortis. Instead, it focused on operational excellence, geographic diversification through partnerships, and gradual expansion into adjacent markets.

VIII. The Asia Expansion: Partnership-Driven Growth

KEY INFLECTION POINT #4

If the Fortis collapse taught Ageas anything, it was the danger of controlling everything. The company that emerged from the crisis developed a distinctive alternative: the partnership model. Nowhere was this approach more evident—or more successful—than in Asia.

Ageas operates in 9 countries in Asia including China, Malaysia, Thailand, India, the Philippines and Vietnam, through well-established joint venture partnerships with highly respected local partners and financial institutions. Many of these partnerships date back more than a decade, providing important access to customers and knowledge of the local market. Together Ageas and its partners serve around 29.5 million customers across the region, supported by a regional office in Hong Kong.

Ageas has been active in China since 2001 when it entered into a joint venture with China Taiping Group. Ageas holds 24.9% in the capital of the joint venture.

In 2001 Ageas took the decision to take a minority stake in Taiping Life Insurance with a view to building a leading nationwide life insurance company in China. This partnership fully leveraged the unique position of CTIH and its experience in the Chinese market. In what has been a long journey of cooperation between the two companies, Ageas has further broadened its interest in the Chinese market, and the successful partnership with CTIH through equity investments in Taiping Asset Management Company Limited, Taiping Financial Services Company Limited, and most recently in Taiping Reinsurance Company Limited.

Ageas announced that it has concluded an agreement with China Taiping Insurance Holdings (CTIH) to subscribe to a capital increase of its wholly controlled subsidiary Taiping Reinsurance Co. Ltd. (TPRe) for a total consideration of HKD 3,100 million (around EUR 340 million). With this transaction, Ageas reinforces its strong long-term strategic partnership with China Taiping. The participation in TPRe, one of the top Asian reinsurance companies with a strong track record and promising growth potential, allows Ageas to expand in the fast-growing Asian reinsurance market from leading positions in Hong Kong and China. Moreover, the subscription to the capital increase, which is a further step in a long history of cooperation between Ageas and CTIH, will increase the share of Non-Life activities in the Group's business portfolio. Since 2013, TPRe's gross written premiums have grown annually on average by 27% resulting in EUR 1.7 billion in 2019.

Ageas announced in 2024 that following confirmation of its participation in the capital increase tender in November 2023, an agreement was concluded with China Taiping Insurance Holdings (CTIH) to subscribe to the capital increase of its wholly controlled subsidiary Taiping Pension Co., Ltd ("TPP") for a total consideration of RMB 1,075 million (around EUR 137 million). After closing of the transaction Ageas will hold 10% of the enlarged share capital of TPP. The investment in TPP will allow Ageas to tap into the significant growth potential of the Chinese pension market, capitalising on the increasing demand for personal pension products in China. It also helps Ageas to strengthen its presence in the largest growth market in Asia, diversify its business offerings, and consolidate its long-standing strategic partnership with China Taiping.

Recognising the distinct regional differences, Ageas chose to restructure its Asian leadership team in 2024 by appointing three Regional Executive Directors, for China, South-East Asia and India, ensuring the right organisation and know-how is in place to best support its JV partners on the ground. These JVs are longstanding in nature, with Thailand this year joining China and Malaysia in a 20+ year club of which we are immensely proud.

The partnership approach offers several strategic advantages. First, it provides access to local distribution networks that would take decades to build organically. Second, it limits capital at risk while still participating in high-growth markets. Third, it allows Ageas to learn from local partners while sharing its own insurance expertise.

2024 was a year in which Asia, especially China, felt the full impact of macroeconomic and geopolitical developments that challenged the region. With interest rates in China at historic lows, the region came under scrutiny with investors. Against this backdrop however the underlying insurance needs of consumers remain high, even after more than 20 years of significant growth. Despite macroeconomic challenges, the region, especially China, saw strong commercial performance over the past year, with premium inflows reaching a record high. This demonstrates the resilience of the insurance sector amid the broader economic slowdown. Far from being one homogenous economic entity, Asia comprises a mix of emerging and more mature markets; each one at distinct stages of maturity and socio-economic development. Low insurance penetration rates are still a common characteristic of all markets, however, which also points to new opportunities in the future.

Having successfully experimented with digital platforms in India, Ageas concluded in 2024 eight new partnerships delivering 10% of new business inflows in India. This digital-first approach in emerging markets positions Ageas to capture growth without the capital intensity of traditional distribution.

IX. Modern Era: Elevate27 and UK Expansion (2020–2025)

KEY INFLECTION POINT #5

The leadership transition that occurred in October 2020 marked a new chapter for Ageas. Ageas announced that, subject to the necessary approvals, Hans De Cuyper would succeed Bart De Smet as CEO of Ageas with effect from 22 October 2020. At the same time, Bart De Smet became the Chairman of the Group replacing Jozef De Mey who recently announced his decision to step down. With Hans De Cuyper, the current CEO of Ageas's Belgian subsidiary AG Insurance, Ageas appointed an experienced leader and people manager with extensive knowledge of the Group and the insurance sector. Through various senior management positions held in both Asia and Belgium Hans is extremely well equipped to bring the best of both cultures together and to successfully lead Ageas in the next phase of its development.

Hans De Cuyper holds a Master Degree in Actuarial Sciences from the University of Leuven (1993) and an Executive MBA in Financial Services from the Vlerick Leuven Gent Management School (2004). Hans joined Ageas group in 2004 as Director Insurance Management Asia in Hong Kong. In 2007, he moved to Malaysia as Chief Financial Officer in Etiqa Insurance & Takaful, the joint venture between Maybank and Ageas. From 2011 until 2013, he was member of the Executive Committee of Maybank, the leading Malaysian bank, and Chief Executive Officer for Etiqa. From September 2013 until September 2015, Hans held the position of Chief Financial Officer of AG Insurance, Ageas's Belgian subsidiary. In October 2015, Hans became Chief Executive Officer of AG Insurance and five years later he was appointed CEO of Ageas and non-independent executive member of the Board of Directors.

Under De Cuyper's leadership, Ageas launched its strategic roadmaps to drive growth. In 2022, Ageas launched its Impact24 strategic cycle, aimed at implementing a long-term growth strategy. A new chapter in Ageas's journey, Elevate27 is a plan for sustained profitable growth and accelerated progress in key areas of strength, that respond to the needs of the ageing population and SMEs, with the ambition to extend the Group's leadership in technical insurance and operational excellence while future-proofing distribution capabilities and enriching the customer experience. Over the past three years, we have successfully executed our Impact24 growth strategy, delivering on most targets we have set. This was achieved through strong commercial progress and robust operational performance, enabling us to meet our commitments to investors regarding earnings per share and dividend growth, while meeting Net Operating Result guidance.

Elevate27 is our Group's three-year strategy for the period 2025-2027. As the name suggests, it is about taking Ageas's strong performance to the next level, building on our unique growth profile and strong long-term track record, and the experience we have garnered over the years. Central to this strategy will be an increased emphasis on our People and on Tech, Data & AI capabilities, which will enable us to deliver on our ambitions. Our actions are still guided and influenced by a commitment to sustainability, our long-term perspective, and by our partnership DNA.

A major development came in the shareholder structure. In April 2024, it was revealed that BNP Paribas had acquired Fosun International's entire 9% stake in Ageas, worth €730 million. In accordance with the rules on financial transparency, BNP Paribas notified Ageas on 13 February 2025 that, on 10 February 2025, its interest had exceeded the legal threshold of 15% of the shares issued by Ageas. Its current shareholding stands at 15.07%.

The stake increase explains why shares have been rising over the past month, ING analyst Jason Kalamboussis said in a research note to clients. "This is an unexpected move that is likely to fuel speculation of a BNP Paribas eventual takeover approach," he wrote.

In the UK, Ageas pursued an aggressive expansion strategy. Personal lines insurer Ageas confirmed in December 2024 that its 20-year proposed partnership with specialist insurer Saga—including the acquisition of underwriting business Acromas Insurance Company (AICL)—had been formally agreed by both parties.

Ageas entered into exclusive negotiations with Saga plc, the UK specialist provider of products and services to people aged over 50, to establish a 20-year partnership with Saga Services Limited (SSL) for the distribution of personal lines Motor and Home insurance products to Saga's customers. Alongside this, Ageas would also acquire Saga's Insurance Underwriting business, AICL (Acromas Insurance Company Limited), which together form the Proposed Transaction. The Proposed Transaction aligns perfectly with Ageas's recently unveiled Elevate27 strategy, to capitalise on its robust Non-Life presence across Europe, while accelerating solutions targeted at an ageing population, a rapidly expanding customer segment where the Group and Ageas UK already has real strength and expertise. Furthermore, it presents Ageas with the opportunity to enhance its position as a leading personal lines insurer in the UK, adding scale to a core European market of the Group.

Then came the transformative deal. Ageas announced in April 2025 that it reached an agreement with Bain Capital to acquire esure, a leading digital personal lines insurer with strong positioning on price comparison websites (PCW) in the UK. The proposed transaction is fully aligned with Ageas's strategic priorities for M&A in Europe under Elevate27. It increases Ageas's European markets presence through the acquisition of a controlled entity, reinforces its positioning in the UK, generates shareholder value from the realisation of synergies and enhances the cash generation of the Group. The combination of Ageas UK and esure will create the third largest UK personal lines platform with a balanced and diversified distribution spanning Direct, PCW, brokers and partnerships. The acquisition of esure will enable Ageas UK to accelerate the diversification of its distribution strategy into the important PCW channel in the UK market.

Under the terms of the transaction, Ageas will pay Bain Capital a cash consideration of GBP 1.295 billion (EUR 1.510 billion) for esure. The integration of Ageas UK and esure is anticipated to be completed, in all material respects, during the Elevate27 strategic cycle. Entering the next strategic period, we project that the transaction will generate a full cost saving potential in excess of GBP 100 million (c. EUR 115 million) per annum, before tax. On a run-rate basis, this transaction is expected to generate an unlevered return on investment of over 12% for Ageas and an uplift in the Return on Equity of more than 1pp. It will become Holding Free Cash Flow accretive per share of c. 10% as from 2028. The completion of the transaction is expected to occur in 2H 2025 and remains subject to regulatory approvals.

International insurance group Ageas completed its acquisition of esure from Bain Capital for a total consideration of £1.295 billion. Initially announced in April 2025, Ageas confirmed that all necessary regulatory approvals have now been obtained and the transaction has been completed. The acquisition marks a major milestone for the Group, positioning Ageas among the top three personal lines insurers in the UK. It also creates a balanced and diversified distribution network across Direct, the prominent PCW channel, brokers, and partnerships, while broadening the range of customer demographics served. In addition, the deal adds scale, unlocks shareholder value by realising synergies, increases technology and data competencies, and enhances the Group's cash generation capabilities. The integration of Ageas UK and esure is expected to be completed during the Elevate27 strategic cycle, with holding free cash flow per share projected to be around 10% accretive after 2027.

The completion of the acquisition of esure represents a major milestone for the Group, establishing Ageas as one of the top three personal lines insurers in the UK. Today, Ageas ranks among the market leaders in the countries in which it operates (Belgium, the UK, Portugal, Türkiye, China, Malaysia, India, Thailand, Vietnam, Laos, Cambodia, Singapore, and the Philippines). It represents a staff force of about 50,000 people and reported annual inflows of EUR 18.5 billion in 2024.

X. Business Model & How Ageas Makes Money

Understanding how Ageas generates revenue and profit requires examining its multi-segment structure and the distinctive characteristics of insurance economics.

The company operates through five segments: Belgium, Europe, Asia, Reinsurance, and General Account. It provides property, casualty, and life insurance products, as well as pension products and reinsurance products.

The fundamental insurance business model is straightforward: the customer pays single or regular premiums to cover risks related to Life, Home, Car, Travel, and more specific types of risks which Ageas insures. Ageas in turn pays out claims in case of an adverse event. Fee income may also come from other sources in services beyond insurance.

Since starting out in 2023, Ageas Re has firmly established itself as a key engine for future growth within the Ageas Group and this very much continues within the context of the Group's new strategic plan Elevate27. 2024 was a year of robust growth and a year marked by further diversification of the portfolio. Established initially as a standalone segment alongside Europe, Asia, and Belgium, reinsurance was identified as one of the Group's key growth drivers within Impact24. The appointment of Emmanuel van Grimbergen as MD Reinsurance and Investments in the Executive Committee in early 2024, further confirmed the significance and long-term potential of this activity for the Group as a whole. Today Ageas Re is recognised as a fully-fledged insurance operation writing third party premiums in more than 50 countries around the world, while supporting the reinsurance needs of Ageas's Joint Venture partners. While initially the focus of Ageas Re's third party business was on Property, 2024 saw the business fulfil its ambition to further diversify its portfolio, successfully balancing its Property and Casualty portfolios. That success translated to a significant growth in business, with GWP rising to EUR 140 million in 2024, representing an increase of 250% year on year.

The investment of premiums into revenue-generating assets, such as government or corporate bonds, loans, equities, or real estate, generates additional financial returns. Through its subsidiary AG Real Estate, the group manages a diversified portfolio of real estate assets valued at around EUR 6.5 billion, making it the largest private real estate group in Belgium.

The financial results demonstrate the effectiveness of this model. Ageas delivered an excellent commercial performance in 2024 and successfully closed the Impact24 strategic plan. In 2024, Group inflows were up more than 10% at constant exchange rate and constant scope (excluding France) compared to the previous year, amounting to EUR 18.5 billion. In Life, Portugal posted a strong growth with several campaigns launched. Thanks to these campaigns, inflows in Portugal increased 45%. In Belgium Life, inflows returned to growth driven by Group Life & Invest, while the strong growth in Malaysia, India and China drove the 7% inflow increase in Asia. Non-Life inflows were up 14% primarily driven by the consolidated entities. Strong growth in the UK (21%) was driven by customer and premium growth alongside excellent underwriting profitability. Inflows in Portugal were up 11% with growth in all business lines supported by repricing actions in Health Care and Motor.

We grew inflows considerably, increased the profitability of our business and secured a Net Operating Result of 1.24 billion euro at the upper half of our guidance, while maintaining a strong cash and solvency position. This strong performance enables us to announce a total gross cash dividend of 3.50 euro for 2024, consistent with our Impact24 commitment. I am also proud that we successfully completed our Impact24 strategic cycle, achieving sustainable growth, strengthening profitability, and diversifying cash flows, while meeting all financial targets and most non-financial ones. While we have made significant progress in various aspects of our business, I am especially pleased that our ESG efforts have been recognised by rating agencies, which has led to the inclusion of the Ageas share in the BEL®ESG index.

In a volatile market environment, Ageas's Solvency II Pillar 2 ratio remained resilient increasing by 1 percentage point over 2024 to reach a high 218%, largely above the Group's neutral level of 175%. The insurance operations contributed 25 percentage points, more than covering the dividend. The solvency of the non-Solvency II scope companies stood at 296% up by 14 percentage points over 2024. The increase was mainly thanks to increased solvency in China supported by amongst other the decreasing interest rate. Operational Capital Generation over the period was up 23% in 2024, for the first time exceeding the EUR 2 billion mark. This included a significant amount of EUR 1.1 billion generated by the Solvency II scope companies driven by a high contribution from Belgium, Europe and Reinsurance. The non-Solvency II scope entities generated EUR 1.3 billion, while the General Account consumed EUR 164 million. This illustrates the strong operating performance across the Group. Operational Free Capital Generation, including both the Solvency II and the non-Solvency II scope, amounted to an exceptionally high EUR 1.5 billion in 2024.

Overall, Ageas's business model is grounded in a combination of insurance premiums, investment income, operational efficiency, and strategic expansions, which collectively drive its profitability and market resilience.

XI. Playbook: Business & Investing Lessons

The Ageas story offers several powerful lessons for investors and business strategists:

The Dangers of Mega-M&A

The ABN AMRO acquisition serves as perhaps the definitive cautionary tale about timing, leverage, and overconfidence in large-scale M&A. Due diligence around the deal at the time was accelerated and incomplete in comparison to normal conditions—Fortis' exposure to US subprime related assets was a concern and could have catalyzed further issues for the bank as the crisis worsened. In addition, Fortis still had unsettled liabilities from the ABN Amro acquisition that needed to be resolved.

Several specific failures compounded: The deal was financed predominantly with short-term debt during a period when credit markets were beginning to seize. The timing—completing a massive acquisition just as the subprime crisis was accelerating—was catastrophic. The integration complexity of absorbing ABN AMRO's Benelux operations was vastly underestimated. And perhaps most importantly, the deal was approved with 95% shareholder support despite only one dissenting voice questioning its recklessness.

The Phoenix Strategy: Rebuilding After Catastrophe

Ageas demonstrates how a company can rebuild corporate reputation and shareholder trust after catastrophic failure. The key elements of this phoenix strategy included:

Complete strategic pivot: Divesting all banking operations and becoming a pure-play insurer eliminated the source of risk that destroyed Fortis.

Leadership continuity with change: Bart De Smet, who had been running insurance operations during the crisis, provided continuity while representing a clean break from the decisions that led to collapse.

Patience with litigation: Rather than fighting the shareholder lawsuits indefinitely, Ageas ultimately settled for €1.3 billion, allowing it to close that chapter and move forward.

Consistent shareholder returns: By maintaining dividend commitments and steady profit growth, Ageas rebuilt trust with investors who had been burned.

Partnership Model Superiority

Ageas's partnership-based growth model in Asia offers an alternative to the empire-building approach that destroyed Fortis. The partnership model provides:

- Access to local distribution networks and market knowledge

- Lower capital intensity and risk exposure

- Learning opportunities from local partners

- Flexibility to enter and exit markets without massive sunk costs

The 20+ year partnerships with China Taiping, Malaysian banks, and Thai partners demonstrate that these arrangements can be stable and mutually beneficial over extended periods.

Framework Analysis

From a Porter's Five Forces perspective, Ageas operates in an industry with moderate competitive intensity. The Belgian market is consolidated with Ageas as the clear leader. The UK market is more competitive but Ageas has built scale through acquisitions. Asian markets are growing rapidly but remain fragmented.

Supplier power (primarily reinsurance) is moderate. Buyer power varies by segment—individual consumers have limited power, but large corporate clients and distribution partners have more leverage. Threat of new entrants is limited by regulatory barriers and capital requirements, though insurtechs pose some disruption risk. Threat of substitutes (self-insurance, government programs) is relatively low for most product lines.

From Hamilton Helmer's 7 Powers framework, Ageas demonstrates several competitive advantages:

Economies of Scale: The esure acquisition explicitly targets scale economies in UK personal lines.

Network Effects: The bancassurance distribution model creates network effects through bank partner relationships.

Switching Costs: Insurance policies create natural switching costs through renewal cycles and policy terms.

Process Power: Ageas's actuarial and underwriting expertise, developed over 200 years, constitutes genuine process power.

Key Performance Indicators to Watch

For investors tracking Ageas, two KPIs stand out as most important:

-

Combined Ratio (Non-Life): This measures underwriting profitability by comparing claims and expenses to premiums. A combined ratio below 100% indicates profitable underwriting. Ageas has consistently achieved strong combined ratios, and maintaining this discipline—especially as it integrates esure and scales UK operations—will be critical.

-

Solvency II Ratio: This regulatory capital metric indicates financial strength and the ability to absorb losses while still meeting policyholder obligations. Including the full impact of the esure and Saga acquisitions, the Group's pro forma Solvency II ratio would stand at a resilient 205%. Maintaining this ratio well above the 175% target level provides buffer for growth investments and dividend payments.

Material Risks and Overhangs

Investors should monitor several key risks:

Interest rate sensitivity: Life insurance profitability is sensitive to interest rate movements, particularly in low-rate environments like China.

Geographic concentration: Belgium remains the dominant profit contributor, creating concentration risk despite diversification efforts.

BNP Paribas relationship: The French bank's stake increase to 15% raises questions about future intentions. Is this a long-term strategic investment, a precursor to a takeover approach, or simply a financial investment? The answer could significantly impact Ageas's future.

Integration risk: The esure acquisition requires successful integration to realize the projected synergies.

The Ageas story is ultimately about the power of focus and discipline in the aftermath of disaster. From the ashes of Fortis—a company that reached for the stars and crashed to earth—emerged something smaller but stronger. A company that learned the hard lessons of excessive ambition and rebuilt itself on the foundation of what it knew best.

As Bart De Smet reflected: "As I look back on my tenure as CEO I do so with much pride. I had an incredible team of people behind me, and together we delivered on our promises. In accepting the role of Chairman of the Board of Ageas Group, I am pleased that I will continue to be a part of the Ageas growth story and to witness even more success in the coming years. I congratulate my successor and wish him well for the future. These are exciting times in our industry, and also challenging times for society, but I feel confident that under Hans's leadership we will continue to deliver what our stakeholders expect from us."

Two centuries after Jacques Coghen opened a small life insurance office in Brussels with five employees, the company he founded insures one in two Belgian families and operates across thirteen countries. The journey from 1824 to 2025 included periods of steady growth, ambitious expansion, catastrophic failure, and remarkable rebirth. For investors willing to look beyond the wreckage of 2008, Ageas offers a case study in how corporate phoenixes can rise from the ashes—patient, disciplined, and focused on what they do best.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube