Embassy Developments: The Phoenix of Indian Real Estate

I. Introduction & Cold Open

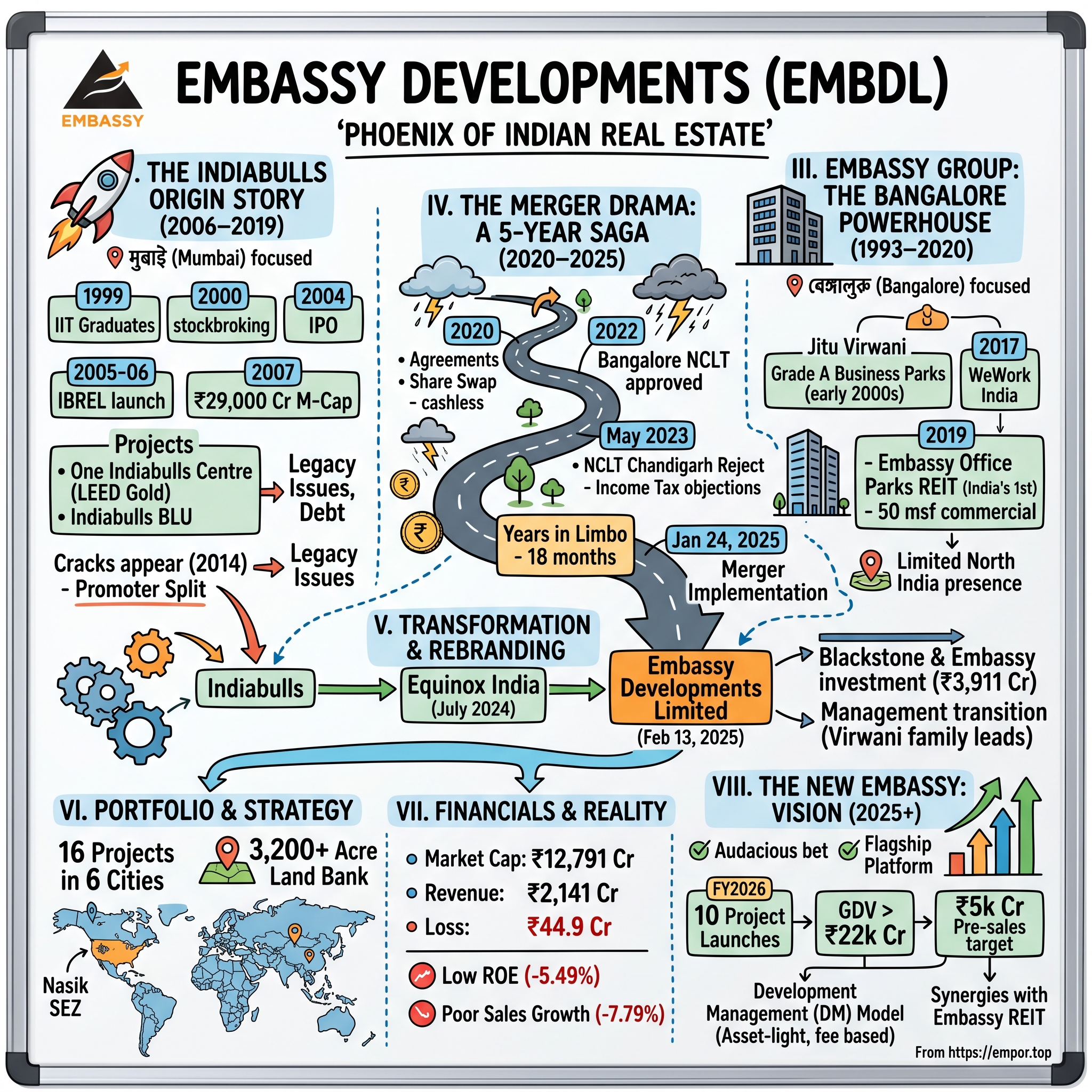

Picture this: January 24, 2025. The trading screens at the National Stock Exchange light up with a flurry of activity. EMBDL shares hit the 20% upper circuit, locking in buyers as a five-year corporate saga finally reaches its climax. After years of regulatory battles, court appeals, and strategic maneuvering, the company once known as Indiabulls Real Estate has completed its transformation into Embassy Developments—creating one of India's most intriguing real estate stories.

This isn't just another corporate merger. It's the tale of how a Mumbai-centric developer bleeding cash joined forces with Bangalore's commercial real estate titan to forge a pan-India powerhouse. It's about survival, reinvention, and the audacious bet that Indian real estate's next chapter will be written by those who can operate at national scale. Today, Embassy Developments stands at a fascinating crossroads. With a market cap of ₹12,757 crore, the company controls one of India's largest land banks—3,200+ acres near major metros—yet has struggled to convert this vast potential into profits. The company has delivered a poor sales growth of -7.79% over past five years and has a low return on equity of -5.49% over last 3 years.

But here's where it gets interesting: Following the NCLAT approval on January 7, 2025, Embassy Group (Mr Jitendra Virwani, Mr Aditya Virwani with certain group entities) has become the new promoter with a 42.96% controlling stake. The merger was successfully implemented with effect from January 24, 2025, and the Company has been renamed as Embassy Developments Limited effective February 13, 2025.

The transformation isn't just cosmetic. The company targets 10 project launches in FY2026 with GDV in excess of ~Rs. 22k Cr with a pre-sales target of ~Rs. 5k Cr, a 150% jump over FY2025; estimated collections of ~Rs. 2.2k Cr. This aggressive expansion represents a bet that Embassy's commercial real estate DNA can revolutionize a residential portfolio that has long underperformed.

As we unpack this story, we'll explore how a company bleeding cash for years convinced one of India's most successful real estate families to stake their reputation on its revival. We'll examine the five-year regulatory battle that nearly derailed everything. And we'll ask the question every investor needs answered: Can the Embassy magic that built Asia's largest office REIT transform a struggling residential developer into a national champion?

The answer lies in understanding two very different real estate journeys that have now converged into one.

II. The Indiabulls Origin Story (2006–2019)

The year was 1999. In a cramped Delhi office, three IIT graduates—Sameer Gehlaut, Rajiv Rattan, and Saurabh Mittal—were about to disrupt India's financial services landscape. Indiabulls was started in 2000 with the establishment of Indiabulls Financial Services, a stockbroking firm co-founded by three IIT Delhi graduates–Sameer Gehlaut, Rajiv Rattan and Saurabh Mittal. What began as an online stock brokerage would, within six years, morph into one of India's most aggressive real estate players.

The timing couldn't have been more fortuitous. India's economy was opening up, foreign capital was flowing in, and a new generation of entrepreneurs was ready to capitalize on the boom. In 1999, just a few years after graduating, Gehlaut co-founded Indiabulls as an online stock brokerage, starting operations from a small office in Delhi with two college friends from IIT. The young Indiabulls team managed to attract prominent investors – for example, industrialist Lakshmi N. Mittal and US-based Farallon Capital invested in the company in its early years.

By 2004, the transformation was already underway. Gehlaut took Indiabulls to the public markets in September 2004, when Indiabulls Financial Services had a successful IPO at ₹19 per share. But the real pivot came in 2005-2006. Indiabulls Real Estate Ltd (IBREL) – The realty arm launched in 2005 after Indiabulls acquired prime land in Mumbai. The company was officially demerged in 2006, creating a standalone real estate entity that would soon become synonymous with Mumbai's skyline. The real estate transformation was audacious in scale. Within a few years, IBREL grew into one of India's significant realty developers – it was noted as one of the country's largest real estate companies by assets, with high-profile commercial and residential projects in cities like Mumbai and Delhi (and even an expansion to London). The company focused on premium developments, creating iconic structures that would reshape Mumbai's skyline.

One Indiabulls Centre became the crown jewel—a dramatic complex in Mumbai's emerging Central Business District of Lower Parel, strategically located between Nariman Point and Bandra-Kurla Complex. It is a LEED "Gold" Certified Building, located strategically in Central Mumbai's emerging Central Business District of Lower Parel. It is one of the first projects to be built on the Mill lands of Mumbai. The project is a commercial development and with its dynamic form and architecture integrates function and design to create a landmark amidst a fast developing Business District.

The pre-2008 boom years were intoxicating. In a matter of just two years, the group's market cap had grown from ₹3,000 crores to a whooping ₹29,000 crores in 2007, lifting them up amongst the top 20 business conglomerates in India, by market value. Sameer Gehlaut, the driving force behind this expansion, was riding high—Forbes would later describe him as "India's youngest self-made billionaire."

But the 2008 financial crisis hit like a sledgehammer. Global capital dried up, real estate prices crashed, and overleveraged developers went under. Indiabulls Real Estate survived, but the scars ran deep. The company had to pivot from aggressive expansion to survival mode, focusing on completing existing projects rather than acquiring new land. The post-crisis years saw a strategic shift toward completion rather than expansion. The company delivered flagship projects that would define its legacy: Welcome to Indiabulls BLU Estate & Club, the most exclusive residential development in Worli, Mumbai. This unique development is in a vibrant location of Worli, with spectacular views of the Arabian Sea. It is set in 10 acres and is the last time a real estate development of this size will be created in South Mumbai that will provide this type of luxury flats in South Mumbai. BLU Estate & Club boasts of fully grown gardens complete with gigantic sculptures from international artists, generous entertainment decks and spacious pools. With a football pitch, a walking trail, ultra-modern gym, spa and every kind of indoor & outdoor sports, the club surpasses any members club in Mumbai making it one of the best properties in South Mumbai to invest in!

The project represented everything Indiabulls Real Estate had aspired to be—ultra-luxury, world-class amenities, and a premium South Mumbai address. But delivering such ambitious projects came at a cost. The company's balance sheet was stretched, debt was piling up, and the market had fundamentally changed post-2008.

By 2014, cracks were showing in the Indiabulls edifice. Last year, in 2014, what came as a shock to many was that, the promoters of the Indiabulls Group would be parting ways harmoniously. Going by the words of the management – they are doing so, to maintain their focus on the companies they have been handling of Indiabulls Group. This news was followed by an elaborate restructuring of the shareholding and management control of its various businesses. Adding on – Sameer would be acquiring back maximum shareholding from Rajiv and Saurabh in the housing finance and real estate businesses, and would also be selling his ownership in the power business. The management and control of housing finance, real estate, securities, and wholesale trading businesses would remain under Sameer, while, Rattan and Saurabh have already resigned as directors of Indiabulls Housing Finance and Indiabulls Real Estate.

The company needed a lifeline. It needed a partner with deep pockets, execution expertise, and most importantly, a reputation that could restore market confidence. The search for this strategic partner would lead them to Bangalore, to a man who had built his empire on a very different philosophy than the high-leverage, rapid-expansion model that had defined Indiabulls Real Estate.

As 2019 drew to a close, Indiabulls Real Estate had become a company at crossroads—valuable assets weighed down by legacy issues, strong brand recognition offset by financial stress, and a portfolio that promised much but delivered inconsistently. The stage was set for one of Indian real estate's most dramatic transformations.

III. Embassy Group: The Bangalore Powerhouse (1993–2020)

While Indiabulls was riding the waves of India's real estate boom from Mumbai, a very different story was unfolding 1,000 kilometers south in Bangalore. In 1993, when India's economy was just beginning to liberalize, Jitendra Virwani took control of a small family business and began building what would become Embassy Group.

Embassy Group or Embassy Property Developments Pvt. Ltd is an Indian real estate developer based in Bengaluru, established in 1993. Embassy Group is headed by Jitu Virwani, Chairman & Managing Director of the group. But unlike the high-leverage, rapid-expansion strategy that characterized many real estate players of that era, Virwani took a fundamentally different approach.

The early 2000s proved to be Embassy's defining moment. In early 2000s, a large number of companies started expanding their operations, which led to the creation of a huge volume of new jobs. Embassy witnessed a steep growth in demand for office spaces, especially from global companies in India. Jitu seized this great opportunity and took an important decision to capitalize on it.

Mr. Virwani introduced the concept of Grade A integrated business parks in early 2000, being one of the first to act on the potential of office and business parks in Bengaluru. This wasn't just about building office space—it was about creating ecosystems. Embassy's business parks included everything from cafeterias to childcare centers, from gymnasiums to shuttle services. They weren't selling square feet; they were selling a lifestyle to India's emerging IT workforce. The real masterstroke came in 2019. Embassy Office Parks REIT came out with an Initial Public Offering (IPO) of 158,333,200 Equity Shares for cash at a price of Rs 300 per unit by raising capital through equity aggregating up to Rs 4,750 Crores. When listed, it became India's first REIT IPO. The Units of the Trust were listed on the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE) on April 1, 2019.

This wasn't just a financial achievement—it was a philosophical statement. While other developers were struggling with debt and unsold inventory, Embassy had created a vehicle that provided stable, predictable returns from income-producing commercial assets. Embassy Office Parks REIT is now India's first and Asia Pacific's largest REIT, comprising around 50 million square feet of completed and operational commercial properties.

The success of the REIT transformed Embassy from a regional player into a national force. Under his leadership, Embassy has grown to 85 msf across commercial, residential, hospitality, services, retail, and education sectors, with a presence in key Indian and international markets including Bengaluru, Mumbai, Pune, NCR, and Serbia.

But there was something missing from Embassy's portfolio. While they dominated commercial real estate in South India, their residential presence was limited. And they had virtually no footprint in North India, particularly in the lucrative Mumbai and NCR markets. The company has developed projects in Indian cities such as Bengaluru, Chennai, Hyderabad, Pune, Coimbatore, Trivandrum, and two countries overseas (Serbia and Malaysia). But Mumbai—India's financial capital and its most expensive real estate market—remained elusive.

In 2017, he introduced WeWork to India, which now has over 100,000 desks across 60+ locations in eight cities. In 2024, he was appointed WeWork India's Non-Executive Chairman. This demonstrated Embassy's ability to partner with global brands and adapt international concepts to Indian markets.

By 2019, Jitendra Virwani had built something remarkable: a real estate company that generated consistent cash flows, had minimal debt, enjoyed institutional credibility through its REIT, and had deep relationships with global corporations. But he knew that to truly dominate Indian real estate, Embassy needed scale beyond South India. They needed a platform that could take their execution capabilities national.

The opportunity would come from an unexpected source—a struggling Mumbai developer bleeding cash but sitting on prime land assets across North India. The stage was set for one of Indian real estate's most ambitious mergers.

IV. The Merger Drama: A 5-Year Saga (2020–2025)

August 18, 2020. The announcement sent shockwaves through India's real estate industry. IBREL and Embassy Group executed definitive agreements in August 2020 confirming their participation in a merger and their respective boards had approved and announced corresponding share swap ratio. Under the terms of the agreement, which has been unanimously approved by both boards of directors from Indiabulls Real Estate (IBREL) and Embassy Group, IBREL's shares are being valued at Rs 92.50 per share, a 25.76% premium from Tuesday's closing price.

The structure was elegant: a cashless scheme of amalgamation. NAM shareholders will get 6.619 shares of IBREL for every 10 shares of NAM whilst NAM Opco shareholders will get 5.406 shares of IBREL for every 10 shares in NAM Opco. Following the merger being effected, the resultant listed entity shall be owned 44.9% by Embassy Group, 26.2% by the existing public & institutional shareholders, 9.8% by existing IBREL Promoter Group and 19.1% by BREP & other Embassy institutional investors.

The strategic logic was compelling. The proposed merger will create one of India's leading listed real estate development platforms with launched/planned area totaling to 80.8 mn sq. ft, having 53% commercial and 47% residential assets, and 30 projects with key geographical focus in Mumbai (MMR), NCR, and Bengaluru. The amalgamated company will have a strong market leadership potential, post amalgamation, with net surplus from residential projects (including launched and planned projects) of Rs 18,592 crore; potential annual rent on completion of planned commercial projects of Rs 4,241 crore; land bank (with future development potential) of 3,353 acres.

For Embassy, it was about gaining access to North India. For Indiabulls, it was about survival and credibility. For Sameer Gehlaut, it was an exit from real estate—he would become a passive shareholder while Jitendra Virwani would take control of the combined entity.

Initial regulatory approvals came quickly. The Competition Commission of India, SEBI, and the stock exchanges all signed off. By early 2022, even the Bangalore bench of the National Company Law Tribunal (NCLT) had sanctioned the merger. Everything seemed on track for completion by the second quarter of FY2022.Then, in May 2023, disaster struck. The NCLT, Chandigarh Bench, which has jurisdiction over IBREL, had earlier raised certain concerns based on the objections cited by the Income Tax department to the merger. The Chandigarh bench of NCLT rejected it and withheld permission on May 9, 2023, over the objections filed by the Income Tax Department regarding valuation and swap ratio.

The market's reaction was brutal. Following the development, shares of Indiabulls Real Estate fell 18.88 per cent to hit a low of Rs 56.10 on BSE. Years of planning, negotiations, and strategic positioning seemed to evaporate in a single judicial order.

The Income Tax department's objections centered on technical issues—valuation methodologies, swap ratios, and concerns about past tax liabilities. Embassy Group Chairman Jitu Virwani said they have addressed all details and clarifications sought by NCLT regarding the assets. An undertaking had also been given that any past tax issues will be borne by Embassy Group, not IBREL shareholders.

But the damage went beyond stock prices. The prolonged delay in completing the proposed merger is seen to be hampering decision making and impacting Embassy Group's growth plans. Projects worth ₹11,000 crore were put on hold. Management bandwidth was consumed by legal battles rather than business development. The merged entity aimed to unlock development potential worth Rs. 11,000 crore but remains on hold pending resolution of legal issues.

For 18 months, the companies were stuck in limbo. IBREL strongly believes that these objections and concerns were unfounded, unjustified and do not impact the merger in a significant manner and had accordingly addressed the same before the NCLT. They filed appeals with the National Company Law Appellate Tribunal (NCLAT), but the process dragged on.

The irony was stark: The merger has already received overwhelming support from 99.9987 per cent of its shareholders who voted on the same and has also received approval from other regulators. The Scheme has been approved by an overwhelming majority of nearly 100 per cent shareholders and 100 per cent of the creditors, and has already been approved by NCLT Bengaluru with reference to the transferor companies. Yet one tribunal's objections had brought everything to a standstill.

Finally, on January 7, 2025, relief arrived. NCLAT, in a 46-page-long order, set aside the NCLT order observing that the valuation of shares and determination of Fair Equity Share Exchange Ratio has been done by experts, and the method of valuation used, namely, Discounted Cash Flow Method is universally accepted as a valid recognised method for valuation of shares.

"After going through the facts and circumstances and the relevant judicial precedences, we hold that NCLT, Chandigarh has erred in interfering in the Scheme ignoring the commercial wisdom of shareholders, creditors and Board of Directors of the appellant companies," said NCLAT.

The five-year saga had finally ended. But the delay had cost more than just time—it had tested relationships, strained balance sheets, and forced both companies to operate in a state of perpetual uncertainty. As the merger was finally implemented on January 24, 2025, the question remained: Could the combined entity make up for lost time?

V. The Transformation & Rebranding Journey

The identity crisis began even before the merger was complete. In July 2024, six months before the NCLAT approval, Indiabulls Real Estate was renamed as Equinox India Developments. The timing was peculiar—changing names while still fighting for merger approval sent mixed signals to the market.

The rebranding reflected a deeper truth: Indiabulls as a brand had become toxic in real estate circles. The name carried baggage—memories of overleveraged deals, stalled projects, and the group's broader struggles in financial services. Equinox represented a fresh start, a neutral identity that could bridge the gap until Embassy's brand equity could be fully leveraged. The capital injection in April 2024 provided crucial breathing room. The board has approved raising Rs 3,911 crore through the issuance of shares and warrants to investors, including the Blackstone Group and Embassy Group. Global investment firm Blackstone will invest Rs 1,235 crore, while the Bengaluru-based Embassy Group will infuse Rs 1,160 crore. This wasn't just about money—it was a vote of confidence from two of the world's most sophisticated real estate investors.

Post investments, Embassy Group will hold 18.7% and Blackstone 12.4% stake in IBREL. The funds were earmarked for specific purposes: capital expenditure for the completion of existing projects and new launches as well as proposed acquisitions, other working capital requirements and general corporate purposes.

The cultural integration presented its own challenges. Embassy's culture—conservative, relationship-driven, focused on long-term value creation—clashed with the remnants of Indiabulls' more aggressive, deal-focused approach. Jitendra Virwani and Embassy promoters now leading the merged entity had to navigate these differences carefully.

The physical integration was equally complex. The merged entity would be co-headquartered in Mumbai & Bengaluru, reflecting the dual nature of the combined operations. But maintaining two headquarters created its own inefficiencies and communication challenges.

By February 2025, the transformation was nearly complete. The Company has been renamed as Embassy Developments Limited effective February 13, 2025, finally aligning the corporate identity with the new reality. The Board of Directors at its meeting on February 25, 2025, approved the appointment of Jitendra Virwani as Chairman of the Board, and Aditya Virwani as Managing Director of the Company.

The leadership transition was carefully orchestrated. Sachin Shah, who continues as Chief Executive Officer and Executive Director, alongside Rajesh Kaimal appointed as Chief Financial Officer and Executive Director. This blend of Embassy's vision with professional management expertise was designed to bridge the old and new cultures.

The integration efforts began immediately following its completion. This includes combining processes, policies, IT applications, and preparing merged opening financials. The merged entity will operate under a unified corporate brand—Embassy—with plans for eventual relocation of its registered office to Bengaluru while maintaining co-headquarters in Mumbai.

But the market remained skeptical. Despite the successful merger and capital infusion, the stock price continued to languish. The transformation from Indiabulls to Equinox to Embassy was more than a rebranding—it was an attempt to shed the past and embrace a new future. Whether the market would buy into this transformation remained to be seen.

VI. Portfolio & Strategic Assets

The combined entity's portfolio reads like a geography lesson of urban India. Total 16 projects in 6 cities with 12.3 million sq ft built-up area—the numbers alone tell only part of the story. What matters more is the strategic positioning of these assets.

The crown jewel remains the land bank: 3,200+ acres near major metros. In Indian real estate, where land acquisition can make or break a developer, this represents generational wealth. The company controls 2,588 acres of SEZ land in Nasik alone, with a Gross Development Value of ₹32,189 crore. This isn't just land—it's optionality, the ability to pivot between residential, commercial, and industrial development as market dynamics shift.

The residential portfolio spans the entire spectrum from affordable to uber-luxury. In Mumbai, the Blu Estate in Worli represents the apex of luxury living, while projects in the Mumbai Metropolitan Region cater to the burgeoning middle class. The dichotomy is intentional—luxury projects generate margins, affordable housing generates volume.

The geographic focus is laser-sharp: MMR (Mumbai Metropolitan Region) and NCR (National Capital Region) dominate the portfolio. These two regions account for nearly 60% of India's real estate consumption by value. It's a bet on India's economic geography—that Mumbai will remain the financial capital and Delhi-NCR the political and commercial hub.

But there are gaps. The Chennai presence is minimal. Hyderabad, India's new IT capital, is absent entirely. The portfolio reflects Embassy's South Indian roots merged with Indiabulls' North Indian focus, but hasn't yet evolved into a truly pan-Indian footprint.

The commercial portfolio, inherited largely from Embassy, includes some of India's most prestigious business addresses. But unlike the REIT assets, these are development properties—they need capital, time, and execution to generate returns. With 1.8 million sq ft of commercial space under development, the company is betting on India's continued economic growth and the return of office demand post-pandemic.

The SEZ lands present both opportunity and challenge. Special Economic Zones were India's attempt to create export-focused manufacturing hubs, but policy changes and global trade dynamics have dimmed their attractiveness. The company's 2,588 acres in Nasik need reimagining—perhaps as logistics hubs, data centers, or mixed-use developments.

The development management model, increasingly adopted by the company, represents a strategic pivot. Q1 FY26: Signed DM deals worth ₹5,600 crore, earning ₹560 crore fees. This asset-light approach allows Embassy Developments to leverage its brand and execution capabilities without tying up capital. It's a page from the playbook of companies like Godrej Properties—generate returns through intellectual property rather than financial capital.

VII. Financial Performance & Market Reality

The numbers tell a sobering story. Market cap: ₹12,791 crore (down 27.9% in 1 year). Revenue: ₹2,141 crore, Loss: ₹44.9 crore. For a company with such vast assets and ambitious plans, the financial performance remains stubbornly disappointing.

The structural issues run deep. Poor 5-year sales growth of -7.79% reflects not just market conditions but execution challenges. The company struggled through the real estate downturn of 2016-2019, the pandemic of 2020-2021, and the merger uncertainty of 2021-2024. Each crisis compounded the previous one's damage.

The low ROE of -5.49% over 3 years is particularly concerning for long-term investors. Real estate is a capital-intensive business where returns on equity determine competitive advantage. Negative returns mean the company is destroying shareholder value, not creating it.

Debt remains a concern, though improving. The company has low interest coverage ratio, indicating that even reduced debt levels strain operational cash flows. More worryingly, Promoters pledged 33.9% of holdings, suggesting financial stress at the holding company level.

But there are green shoots. Q1 FY26: Signed DM deals worth INR 3,060 Cr and 2,540 Cr, earning ~INR 560 Cr fees. The development management business requires minimal capital and generates high-margin fees. If scaled successfully, it could transform the company's return profile.

FY2025 showed tentative signs of recovery. FY2025 PAT of ~Rs. 203 Cr; Revenue, Pre-sales, Collections more than ~Rs. 2k Cr each. The return to profitability, even if modest, marks an important psychological milestone.

The ₹22,000 crore new launch pipeline announced for FY2026 represents both opportunity and risk. Targets 10 project launches in FY2026 with GDV in excess of ~Rs. 22k Cr. Pre-sales target of ~Rs. 5k Cr, a 150% jump over FY2025; estimated collections of ~Rs. 2.2k Cr. These are ambitious targets that assume strong market conditions and flawless execution.

The proposed acquisition opportunity to Embassy REIT for ~3.3 msf commercial development in Whitefield, Bengaluru with expected GDV of Rs. 3,200 Cr – 3,700 Cr on completion demonstrates the synergies with the Embassy ecosystem. Selling completed assets to the REIT provides capital recycling opportunities.

The investment community remains divided. Bulls point to the Embassy brand, massive land bank, and turnaround potential. Bears focus on historical losses, execution risks, and competitive pressures. The stock trades at a significant discount to book value, suggesting the market doesn't believe the stated asset values are realizable.

VIII. The New Embassy: Vision & Strategy (2025–Forward)

The vision is audacious: creating a flagship platform for residential, office, and future asset classes that dominates Indian real estate. But vision without execution is hallucination, and Embassy Developments faces formidable challenges in realizing its ambitions.

The ₹22,000 crore new launch pipeline isn't just about scale—it's about proving the merger's thesis. Each successful launch validates the combination of Embassy's execution capabilities with Indiabulls' land bank. Each failure reinforces market skepticism.

The asset-light development management model represents a fundamental strategic shift. Instead of being a capital-intensive developer, Embassy Developments aims to become a brand licensor and project manager. It's a model perfected by hotel chains—own the brand and operations, let others own the real estate.

But this model requires something Embassy Developments is still building: unquestionable brand power. While Embassy commands respect in commercial real estate, its residential brand remains nascent. The Indiabulls legacy, despite the rebranding, continues to cast shadows.

The competitive landscape has evolved dramatically. DLF has roared back to life, with its stock price near all-time highs. Godrej Properties has perfected the development management model Embassy Developments is trying to adopt. New-age developers like Prestige Estates and Brigade Group are expanding aggressively.

International expansion possibilities remain distant dreams. While Embassy Group has projects in Serbia and Malaysia, Embassy Developments needs to fix its India business before looking abroad. The domestic opportunity—a $200 billion annual market growing at 10%+ annually—provides sufficient runway for decades.

The synergies with Embassy Office Parks REIT could prove decisive. The ability to develop commercial assets and sell them to the REIT provides a natural exit strategy and capital recycling mechanism. It's a virtuous circle—if executed well.

Technology adoption will be crucial. The real estate industry is being disrupted by proptech—from virtual reality tours to blockchain-based property transactions. Embassy Developments' ability to embrace these changes while maintaining its relationship-driven culture will determine its relevance.

The focus on sustainability and ESG (Environmental, Social, Governance) factors isn't just about compliance—it's about accessing global capital. International funds increasingly mandate ESG compliance, and Embassy's track record here provides competitive advantage.

IX. Playbook: Lessons from the Trenches

The Embassy Developments story offers hard-won lessons for investors, entrepreneurs, and industry observers. These aren't theoretical insights but practical wisdom earned through crisis and transformation.

Surviving real estate cycles requires patient capital and diversification. The companies that survived 2008, 2016, and 2020 had either deep-pocketed sponsors or diversified revenue streams. Pure-play residential developers with high leverage invariably failed. Embassy's commercial focus and Indiabulls' geographic diversification, when combined, create resilience.

Strategic partnerships in capital-intensive businesses are marriages, not dates. The five-year merger saga demonstrates that partner selection, alignment, and integration matter more than deal terms. Embassy and Indiabulls spent five years in regulatory purgatory because they didn't anticipate bureaucratic resistance. Due diligence must extend beyond finances to regulatory, cultural, and operational compatibility.

Regulatory navigation can make or break deals. The Income Tax department's objections nearly derailed a merger approved by 99.99% of shareholders. In India, regulatory risk isn't a footnote—it's often the main text. Companies must invest in regulatory relationships and expertise as much as in operations.

Brand value in real estate compounds over decades. Embassy's 30-year reputation commands premium pricing and attracts institutional capital. Indiabulls' tainted brand, despite strong assets, trades at a discount. In real estate, trust is the ultimate currency, and trust takes generations to build but moments to destroy.

The REIT innovation changes everything. Embassy's creation of India's first REIT transformed it from a developer to an asset manager. This shift from development profits to fee income provides stability and scalability. The future belongs to developers who can create institutional-quality assets and monetize them through REITs.

Managing stakeholder expectations during prolonged mergers requires overcommunication. The five-year merger process tested every stakeholder's patience. Employees faced uncertainty, investors saw volatility, and customers hesitated to commit. Regular, transparent communication—even when there's no news—maintains stakeholder confidence.

Timing matters more than strategy in cyclical businesses. Indiabulls expanded aggressively pre-2008, suffered post-crisis, and couldn't recover during the 2016-2019 downturn. Embassy, conversely, focused on commercial real estate when IT/ITES demand exploded. In real estate, when you do something matters more than what you do.

X. Analysis & Investment Case

The investment case for Embassy Developments polarizes opinion. It's simultaneously a value trap and a turnaround story, a distressed asset and a growth platform.

The Bull Case rests on five pillars:

The Embassy brand brings institutional credibility that Indiabulls never achieved. This translates to lower capital costs, better partner access, and premium pricing power.

The massive land bank—3,200+ acres—provides optionality worth multiples of the current market cap. Land in Mumbai and Bangalore appreciates at 12-15% annually. Even modest development generates substantial value.

Pan-India presence post-merger creates economies of scale in procurement, financing, and branding. National developers command valuation premiums over regional players.

Turnaround potential under Embassy management is significant. The same assets that generated losses under Indiabulls could generate profits under Embassy's execution model.

India's real estate market, growing at $20 billion annually, provides tailwind for decades. Housing demand from urbanization, nuclearization, and aspiration remains robust.

The Bear Case is equally compelling:

Historical losses demonstrate execution inability. Five consecutive years of negative returns suggest structural, not cyclical, problems.

Debt concerns persist despite reduction. Interest coverage remains weak, and promoter pledging suggests holding-company stress.

Execution risks in launching ₹22,000 crore of projects are enormous. Each delay or failure damages credibility and consumes capital.

Market competition has intensified. DLF, Godrej Properties, and Prestige Estates have stronger brands, better execution, and cleaner balance sheets.

The merger integration remains incomplete. Cultural differences, system integration, and organizational alignment typically take 3-5 years post-merger.

Comparison with peers is unflattering:

DLF trades at 2.5x book value; Embassy Developments at 0.8x. DLF's ROE exceeds 15%; Embassy Developments' is negative.

Godrej Properties' development management model generates 20%+ ROE with minimal capital. Embassy Developments is still building this capability.

Prestige Estates' Bangalore dominance overlaps with Embassy's stronghold, creating direct competition for land, customers, and talent.

The role of real estate in India's growth story cannot be ignored. Real estate contributes 7% of GDP and employs 50 million people. As India urbanizes—adding 300 million urban residents by 2050—real estate demand will explode. The question isn't whether the opportunity exists, but whether Embassy Developments can capture it.

Why timing matters: Real estate moves in 7-10 year cycles. We're potentially at the beginning of a new upcycle, driven by economic growth, infrastructure investment, and pent-up demand. Companies that survive the downturn often thrive in the upturn. Embassy Developments, having survived its near-death experience, might be positioned for recovery.

XI. Epilogue & Looking Forward

What does success look like for Embassy Developments in five years? The optimistic scenario sees a company generating ₹10,000 crore in annual revenues, ₹1,500 crore in profits, and trading at ₹250 per share. The pessimistic scenario involves continued losses, asset sales, and potential restructuring.

Key milestones to watch:

FY2026 launch execution: Achieving the ₹22,000 crore launch target validates the merger thesis. Missing it badly undermines credibility.

Development management scale: Reaching ₹1,000 crore in annual DM fees transforms the business model from capital-intensive to capital-light.

Debt reduction to below ₹500 crore provides financial flexibility for growth investments.

Commercial asset sales to Embassy REIT exceeding ₹5,000 crore demonstrate the synergy value.

Brand perception shift from Indiabulls legacy to Embassy future, measured through pricing power and customer preference.

The broader implications for Indian real estate consolidation are profound. If Embassy Developments succeeds, it proves that distressed assets can be transformed through strategic combinations. This could trigger a wave of consolidation, with strong developers acquiring weak ones' land banks.

The story isn't just about real estate—it's about transformation, resilience, and the possibility of redemption. Indiabulls Real Estate was a cautionary tale of leverage and hubris. Embassy Developments might become an inspiration for turnaround and strategic transformation.

As we watch this story unfold, we're witnessing more than a corporate merger. We're seeing whether Indian real estate can evolve from a fragmented, family-driven industry to an institutional, professionally-managed sector. Embassy Developments, with all its flaws and potential, embodies this transition.

The phoenix metaphor is overused in business, but here it fits. From the ashes of Indiabulls Real Estate, something new is emerging. Whether it soars or crashes remains to be seen. But for investors, industry observers, and anyone interested in Indian business, Embassy Developments provides a masterclass in corporate transformation—messy, uncertain, but ultimately human in its ambition to build something lasting from the ruins of the past.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube