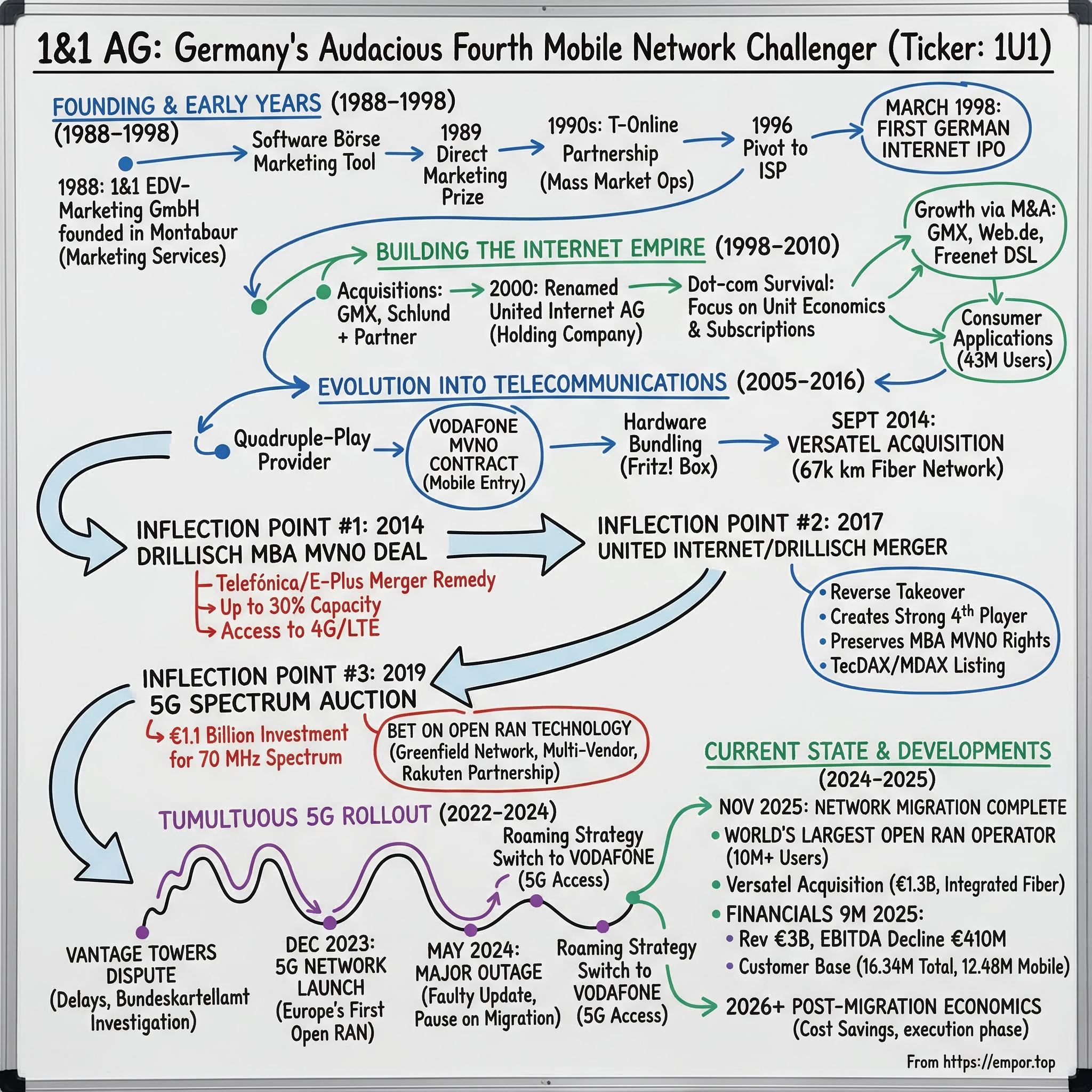

1&1 AG: Germany's Audacious Fourth Mobile Network Challenger

I. Introduction & Episode Roadmap

In the quiet, rolling hills of the Westerwald—a rural region so far removed from Germany's financial and tech centers that few would ever expect it to birth a telecommunications giant—sits the small town of Montabaur. Population roughly 13,000. Medieval architecture. Winding streets. Not exactly the image that comes to mind when you think "European telecom disruptor."

Yet it was here, in a modest office just a short walk from a 12th-century castle, that Ralph Dommermuth built what has become one of the most audacious corporate stories in German business history. 1&1 AG is a network-independent telecommunications provider in Germany. The company has two business segments which include Access and 1&1 Mobile Network. The Access segment offers internet access products based on landline and mobile networks.

Today, 1&1's current market cap is $3.8B with 176M shares. As of 30-Jun-2025, 1&1 has a trailing 12-month revenue of $4.4B.

But these numbers, impressive as they are, barely hint at the magnitude of the transformation underway. In November 2025, the German mobile operator made an announcement alongside the presentation of its third quarter results. While the numbers themselves are far from stellar, the network migration is an important milestone for 1&1, which has faced more hurdles than it expected in its Open RAN rollout.

Here's the central question this story explores: How did a marketing company from a sleepy German town become Europe's first fully-virtualized Open RAN mobile network operator?

The answer involves regulatory arbitrage at its finest, a merger that reversed corporate ownership conventions, a €1.1 billion bet on unproven technology, and the kind of founder-led persistence that separates lasting enterprises from flash-in-the-pan ventures.

A pioneer in digital infrastructure, the company operates Europe's first mobile network based on innovative Open RAN technology, underscoring its commitment to shaping Germany's digital development for over 30 years.

The story of 1&1 AG is, at its core, a story about what happens when an entrepreneur who started selling marketing services for software companies in 1988 decides—three decades later—that he wants to take on Deutsche Telekom, Vodafone, and Telefónica in their own backyard. And not just compete with them, but fundamentally reimagine how a mobile network should be built.

What follows is a journey through five distinct inflection points—moments when 1&1's trajectory shifted fundamentally—and the strategic chess moves that transformed a scrappy marketing firm into Germany's fourth mobile network operator.

II. Founding & Early Years: From Marketing Agency to Internet Pioneer (1988-1998)

Picture Germany in 1983. The Berlin Wall still stands. Personal computers are exotic creatures found mostly in university labs and forward-thinking corporations. The internet, as a commercial concept, doesn't exist. And a 20-year-old from Montabaur named Ralph Dommermuth, having just completed his banking apprenticeship at Deutsche Bank, takes an unlikely career turn.

Ralph Dommermuth started his career as a sales freelancer for a local PC dealer in 1983. This wasn't the glamorous path to riches. He was selling hardware in a small German town, far from the corporate corridors where careers were made.

But something happened in that PC shop that would shape everything that followed. Dommermuth began his career with an apprenticeship at Deutsche Bank, after which he worked for a PC retailer in his hometown of Montabaur. There he met Wendelin Abresch and together they founded 1&1 EDV Marketing GmbH.

The history of the Group goes back to 1&1 EDV-Marketing GmbH, which was founded in 1988 by Ralph Dommermuth and Wendelin Abresch as a service provider for marketing and advertising.

The founding vision was deceptively simple. In 1988, Dommermuth founded the 1&1 EDV Marketing GmbH together with a business partner. The first business idea was called "Software Börse", a marketing tool for software companies. For this product the company won the German direct marketing prize in 1989.

Think about what Dommermuth was doing: he wasn't building technology—he was building the connective tissue between technology companies and their customers. In 1988, Ralph Dommermuth, born in 1963, founded 1&1 EDV Marketing GmbH, the company that was to grow into what is today United Internet AG. His initial business was the provision of systematised marketing services to small software providers. He later developed additional marketing services for large customers such as IBM, Compaq and Deutsche Telekom.

The winning of that direct marketing prize in 1989—just one year after founding—signaled something important. Dommermuth had an instinct for distribution, for reaching customers at scale, that would prove invaluable in the decades to come.

The early 1990s brought transformative partnerships. In cooperation with the Federal Ministry of Posts and Telecommunications, 1&1 positions T-Online (then still BTX) as a universal and modern online service. Millions of PC users have their first online experience with 1&1 and T-Online becomes the largest online service in Europe.

This relationship with Deutsche Telekom deserves special attention. By helping position T-Online—what would become Europe's largest online service—1&1 wasn't just building a client relationship. It was learning, from the inside, how mass-market telecommunications worked. How millions of customers could be acquired and retained. How infrastructure scaled. This operational education would prove crucial when Dommermuth later decided to compete against his former client.

After the initial success as a marketing service provider Dommermuth converted 1&1 into an internet service provider, beginning in 1996. In March 1998, the company had its IPO as the first German Internet company. Due to the capital increase carried out in this context, 1&1 had opportunity to participate in other IT companies such as GMX and Schlund + Partner AG.

The pivot from marketing agency to internet service provider wasn't just a business decision—it was a bet on the future. While most German businesses in the mid-1990s viewed the internet as a curiosity, Dommermuth saw it as the next great platform for reaching consumers directly.

What's remarkable about this period is Dommermuth's willingness to cannibalize his own business. He had built a successful marketing services operation serving major corporations. Walking away from that to build something entirely new—an ISP competing directly with his largest client—required either extraordinary vision or extraordinary confidence. Perhaps both.

For investors trying to understand what makes 1&1 different, this origin story matters. The company was never primarily about technology. It was about distribution, about reaching customers efficiently, about building systems that could scale. These capabilities—developed over years of marketing services work—would become the foundation for everything that followed.

III. The IPO and Building the Internet Empire (1998-2010)

March 1998. The dot-com boom is gaining momentum. Amazon has been public for less than a year. Google won't be founded for another six months. And in Frankfurt, something unprecedented is about to happen.

A pivotal moment in the 1&1 history occurred in March 1998 with its Initial Public Offering (IPO) on the Frankfurt Stock Exchange. This made 1&1 the first internet company to be publicly listed, a move that facilitated capital infusion for further expansion. The funds raised were instrumental in acquiring stakes in other IT companies, including GMX and Schlund + Partner AG.

By 1998, United Internet AG went public and the proceeds of the company's Initial Public Offering, worth $60 million, were used to expand 1&1 Internet into a group of Internet companies by bringing in Schlund + Partner.

Being first matters in business narratives. But being first also meant taking risk when the path wasn't clear. The Frankfurt Stock Exchange had no playbook for internet companies. Investors had no comparable German peers to evaluate. Dommermuth was asking the market to bet on a vision of the internet's future that most couldn't fully articulate.

The market response was enthusiastic, perhaps irrationally so given what would follow two years later. But for 1&1, the timing proved fortuitous. The IPO capital enabled a series of acquisitions that would transform the company from a single-brand operation into a diversified internet conglomerate.

By the year 2000, Ralph Dommermuth orchestrated a significant restructuring, transforming 1&1 into United Internet AG, solidifying its position as a leading European internet specialist.

In March 1998, 1&1 becomes the first Internet company to be listed on the Frankfurt Stock Exchange. The listed company 1&1 AG & CO. KGaA is renamed United Internet AG in 2000 and, as a holding company, forms the umbrella for 17 independent affiliated companies. Internet connections continue to be provided via the already established 1&1 brand.

At the height of the internet boom in the early 2000s, 1&1 Holding held shares in 17 internet companies and Dommermuth renamed the company to United Internet.

The restructuring into United Internet AG wasn't just corporate housekeeping. It reflected Dommermuth's understanding that the internet industry would consolidate around companies with multiple capabilities—email, hosting, access, advertising—rather than point solutions. By 2000, he had assembled the pieces to compete across multiple verticals.

Then came the dot-com crash. The Neuer Markt—Germany's equivalent of NASDAQ—collapsed spectacularly. Companies that had IPO'd alongside 1&1 went bankrupt. Stock prices fell 90% or more. It was a massacre that killed most of European internet ambition for half a decade.

But 1&1 survived. More than survived—it emerged stronger. Why?

The answer lies in Dommermuth's obsession with unit economics. Even during the boom, 1&1 had focused on profitable customer acquisition, on subscription models that generated recurring revenue, on marketing efficiency that produced positive returns. When advertising budgets evaporated and venture capital dried up, 1&1 had a sustainable business model to fall back on.

The post-crash period saw accelerated consolidation. Between 2000 and 2003, the subsidiary 1&1 entered various foreign markets, including the UK, France and the USA. In May 2005, United Internet acquired the portal and e-mail business of Web.de, which was merged with its in-house offering GMX to form 1&1 Mail & Media GmbH.

In 2003, 1&1 Internet opened its business in the United States and offered its services free of charge for three years to US customers to explore the company's potential. By 2004, 1&1 Internet launched its complete service offerings.

The US market entry strategy was characteristically aggressive. Offering free services for three years to establish the brand—absorbing those customer acquisition costs in exchange for market position—demonstrated the long-term thinking that differentiated 1&1 from more financially constrained competitors.

GMX is a web portal that became popular in Germany at the end of the 1990s thanks to its e-mail service. Shortly after its launch in 1997, 1&1 Beteiligungen GmbH & Co. KG, which later became United Internet AG, acquired 50% of GMX. From 2001, editorial content appeared on the portal and at the end of the year United Internet took over the company completely.

The acquisition of GMX and Web.de gave United Internet something invaluable: massive reach. Within the Group, GMX (alongside Web.de and Mail.com) is bundled under the "Consumer Applications" segment. Together, the three services have almost 43 million users (2023), around 40 million of whom use the free email service.

In May 2009, United Internet announced the acquisition of the DSL business of Freenet AG. As a result, the company's DSL customers – most recently around 700,000 – were transferred to United Internet for a total of 123 million euros. As a result of the takeover, the connections of former Freenet customers temporarily failed to work, while former Tiscali customers had their connections switched off in this context.

The Freenet DSL acquisition wasn't just about adding subscribers. It signaled United Internet's evolution from pure-play internet services into telecommunications proper. DSL customers required network infrastructure, customer service operations, and regulatory expertise that the company hadn't needed before. This acquisition was practice for much bigger plays to come.

For investors, this period established a pattern that persists today: 1&1 grows through a combination of organic customer acquisition and opportunistic M&A. The company has repeatedly demonstrated willingness to pay up for strategic assets when they become available, then integrate them efficiently into its operations.

IV. The Evolution into Telecommunications: DSL, Mobile, and Versatel (2005-2016)

The mid-2000s marked 1&1's transition from internet company to full telecommunications provider. But the path wasn't obvious, and the strategy evolved through experimentation.

With the integration of VOIP (2004), Video-on-Demand (1&1 in cooperation with Maxdome), and the 1&1 mobile-services tariff (2007) in the DSL-based bundled offer, 1&1 became a Quadruple-Play provider.

The term "Quadruple-Play"—voice, video, internet, and mobile—sounds like marketing jargon. But it represented a genuine strategic insight. Customers who bought multiple services from the same provider exhibited dramatically lower churn. Bundling created switching costs that protected the customer base. And the economics of serving an existing customer were far superior to acquiring new ones.

1&1 and Vodafone sign Germany's first MVNO (Mobile Virtual Network Operator) contract.

This Vodafone MVNO deal was foundational. An MVNO—Mobile Virtual Network Operator—uses another company's physical network infrastructure to offer mobile services under its own brand. It's telecommunications arbitrage: buying wholesale network access and selling retail mobile plans.

The MVNO model had obvious limitations. Margins were thin because you paid whatever the network operator charged. You couldn't differentiate on network quality. And if the relationship soured, you had no alternative.

But for 1&1, the MVNO model was never the destination—it was a stepping stone. By operating as an MVNO, the company learned the mobile business: customer acquisition, churn management, network planning, regulatory compliance. This operational knowledge would prove essential when 1&1 decided to build its own network.

The hardware bundling strategy deserves mention because it exemplifies 1&1's approach to market entry. Rather than compete purely on price—a race to the bottom—1&1 differentiated through hardware-software integration. In partnership with AVM, the German maker of the Fritz! Box router, 1&1 offered customers premium hardware bundled with their connectivity packages. The Fritz! Box became iconic in German households, and 1&1's relationship with AVM created a distribution advantage that competitors struggled to replicate.

Then came the move that would transform United Internet's telecommunications position entirely.

On 3 September 2014 United Internet announced that the remaining 74.9% of shares in the fixed-line and fiber-optic network operator Versatel GmbH, or its parent company, would be taken over economically retroactively as of 1 July 2014 by the previous main shareholder, the private equity company KKR. Shortly afterwards, the company was renamed 1&1 Versatel.

Today, 1&1 Versatel has its own fiber optic network with a total length of over 67,000 kilometers in Germany. The telecommunications provider specializes in corporate customers and is represented in over 350 cities with its own network infrastructure.

The Versatel acquisition changed everything. United Internet went from being dependent on Deutsche Telekom's infrastructure to owning its own fiber backbone. It has significantly increased the reach of its fibre infrastructure in the intervening 11 years. Its network now covers 67,000 km in 350 cities, up from 37,000 km across 226 cities.

For €586 million paid to KKR for the 74.9% stake, United Internet acquired independence. The fiber network would serve as backhaul for the eventual mobile network, connect data centers across Germany, and support the B2B business that Versatel brought with it.

In 2016, 1&1 Internet SE also split into two business divisions: 1&1 Telecommunications SE, which continues to operate the Consumer Access business, and the internationally active Business Applications division with the current IONOS brand for hosting and cloud service.

The corporate restructuring into separate telecommunications and applications businesses reflected their fundamentally different characteristics. Applications (hosting, cloud, email) was global, scalable, and capital-light. Telecommunications was local, infrastructure-intensive, and regulated. Running them in the same organizational structure created confusion about capital allocation and strategic priorities.

For investors, this period established 1&1's willingness to make large, transformative acquisitions when infrastructure assets become available at attractive prices. The Versatel deal—buying fiber assets from a private equity firm looking to exit—exemplified opportunistic capital deployment that would become a recurring theme.

V. INFLECTION POINT #1: The Drillisch MBA MVNO Deal (2014)

This is where the story gets interesting. And complicated. And perhaps a little bit diabolical in its strategic elegance.

In 2014, something happened in German telecommunications that would reshape the industry for a decade: Telefónica Deutschland announced plans to acquire E-Plus from KPN for €8.6 billion. The deal would consolidate Germany from four mobile network operators to three.

European competition authorities don't like three-player markets. They worry about tacit collusion, reduced price competition, and consumer harm. When mergers reduce competition, regulators typically demand "remedies"—concessions that partially offset the competitive harm.

Telefónica Deutschland said it has agreed to provide network capacity to German mobile virtual network operator (MVNO) Drillisch to help smooth the regulatory path of Telefónica's proposed €8.6 billion ($11.7 billion) merger with KPN-owned E-Plus.

In 2014, when the merger between Telefónica and E-Plus was approved by the EU, albeit under certain conditions, Drillisch received the opportunity to lease 20% of Telefónica's mobile-network capacity. Drillisch's corporate subsidiary, MS Mobile Services GmbH (MS Mobile) entered into the contract in 2015 for a starting period of five years with the potential for extension up to 15 years total. This capacity was made available as Mobile Bitstream Access (MBA) in the form of data transfer and data volume. Until 2020, the used proportion of the total network capacity may be increased to 30%. This contract has made Drillisch the only MBA MVNO on the German mobile-services market.

Let's unpack why this mattered so much.

An MBA MVNO agreement is fundamentally different from a traditional MVNO deal. In a standard MVNO arrangement, the virtual operator pays per-customer or per-minute rates, with pricing set by the network owner. The network owner retains all the leverage.

Mobile Bitstream Access flips that dynamic. Drillisch didn't buy services—it bought capacity. A guaranteed percentage of Telefónica's network, at regulated rates, for up to fifteen years. This was wholesale access with teeth.

Such mergers have often resulted in competition regulation, and in the German market it resulted in an imposition of up to 30% of the then newly joint network capacities to be accessible to MVNOs. Drillisch was a clear winner in these regulator-imposed remedies and has the right to use 20% of O2 capacity.

Think about what happened here. The EU required Telefónica to give away a substantial chunk of its network capacity as the price of merger approval. Drillisch—a relatively small MVNO at the time—positioned itself as the remedy recipient. The European Commission essentially gave Drillisch a competitive weapon that money couldn't buy.

Drilisch is a so-called mobile virtual network operator and does not have a mobile telecommunications network of its own. However, in the context of the Telefónica/E-Plus merger, Telefónica gave an undertaking to the European Commission to grant Drillisch access to up to 30 per cent of the capacities used in the merged Telefónica/E-Plus mobile telecommunications networks. In this context, Drillisch was granted access to 4G (LTE) and other new technologies.

Access to 4G (LTE) was crucial. Previous MVNO deals often limited virtual operators to older network technologies, making them uncompetitive for smartphone users who demanded fast data. The MBA MVNO deal gave Drillisch access to cutting-edge network capabilities at regulated prices.

Why did Drillisch, rather than a larger player, end up with this deal? Partly because larger players didn't want it—the economics of being a quasi-fourth-operator without owning infrastructure seemed unattractive. Partly because Drillisch's management recognized the strategic value that others missed. And partly because being small and entrepreneurial let them move faster than bureaucratic competitors.

Sources told Reuters that Telefónica is not talking to others after the Drillisch deal and that approval of the E-Plus acquisition should now not be a problem. Under the agreement, Drillisch is to acquire 20 per cent of the capacity of all mobile networks that will be under the control of Telefónica Deutschland following the completion of the proposed acquisition of E-Plus.

The deal closed, Telefónica got its merger, and Drillisch suddenly held the keys to becoming a major force in German mobile. All they needed was capital and distribution capability to exploit the opportunity.

Which is where United Internet enters the picture.

For investors, the Drillisch MBA MVNO deal represents perhaps the most consequential regulatory arbitrage moment in German telecom history. Drillisch recognized that merger remedies, properly structured, could create competitive advantages that no amount of capital investment could replicate. This deal would become the foundation for everything that followed.

VI. INFLECTION POINT #2: The United Internet/Drillisch Merger (2017)

The MBA MVNO deal gave Drillisch an asset—network access rights—but limited capability to exploit it fully. Drillisch was a discount mobile brand operator. It had customers, but not the scale, the distribution, or the fixed-line capabilities to maximize the value of its Telefónica deal.

United Internet, meanwhile, had all those things. Millions of email users at GMX and Web.de. A growing DSL customer base. The Versatel fiber network. Marketing expertise honed over decades. What it lacked was competitive mobile network access.

The strategic logic was obvious. The execution was anything but.

On May 12, 2017, the Management Boards of United Internet AG and Drillisch AG entered into a Business Combination Agreement governing the step-by-step acquisition of 1&1 Telecommunication SE by Drillisch under the umbrella of United Internet. The agreement has the approval of both companies' Supervisory Boards. With the conclusion of the agreement, the companies aim to merge United Internet's mobile and fixed-network business, which is bundled in 1&1 Telecommunication SE, with Drillisch's mobile communications business. This will create a strong fourth player in the German telecommunications market alongside the three major full-service providers (Deutsche Telekom, Vodafone and Telefónica).

As both companies announced on 12 May 2017, the majority of Drillisch shares would be acquired by United Internet by December 2017 as part of a reverse takeover. It was furthermore planned for United Internet to provide Drillisch AG with its own mobile-network and DSL divisions, namely 1&1 Telecommunication SE, by way of two real capital increases. As the former company boasted a much higher shareholder value, the transaction yielded majority shares of Drillisch for United Internet AG (at least 73.7%).

The reverse takeover structure was clever. Rather than United Internet acquiring Drillisch—which would have been the natural direction given relative sizes—Drillisch technically acquired 1&1 Telecommunication SE. Why? Because this structure preserved Drillisch's stock listing, its existing shareholder base, and—crucially—its MBA MVNO contract with Telefónica.

As part of the step-by-step acquisition of 1&1 Telecommunication SE by Drillisch AG under the umbrella of United Internet AG, 97.85 percent of the represented share capital at today's extraordinary General Meeting of Drillisch voted in favor of the proposed capital increase by way of a contribution-in-kind. The majority of 75 percent required for approval was therefore achieved. Ralph Dommermuth, Chairman of the Management Board of United Internet, states: "We're delighted of the clear approval which the Drillisch shareholders have given to the capital increase. It allows us to create a strong fourth player in the German telecommunications market."

Together, we can offer our customers the complete range of products with full access to the network technologies of today and tomorrow from a single source: high-speed DSL, mobile internet and the associated services. The shareholders of United Internet and Drillisch will benefit from the significant growth potential and synergies offered by the merger in the form of value increases and dividends.

The Bundeskartellamt has cleared the takeover of the mobile telecommunications provider Drillisch AG by United Internet AG. Andreas Mundt, President of the Bundeskartellamt: "There are three major network operators on the mobile telecommunications market: Telekom, Vodafone and Telefónica. If Drillisch joins forces with United Internet, this may have a stimulating effect on the market. The merger therefore does not raise any competition concerns."

The Bundeskartellamt's reasoning is worth noting. Rather than viewing this as concerning concentration, the German competition authority saw the merger as pro-competitive—creating a stronger challenger to the three established network operators.

In 2017, 1&1 Telecommunication SE and the then Drillisch AG merged to form a fourth force in the German telecommunications market – today's 1&1 AG. In addition to 1&1, the brands of 1&1 AG also include the brands of Drillisch Online GmbH (including yourfone, smartmobil.de WinSIM).

In January 2018, the company changed its name from Drillisch Aktiengesellschaft to 1&1 Drillisch Aktiengesellschaft. On 24 September 2018, 1&1 Drillisch was additionally adopted into the TecDAX listing of MDAX.

The combined entity had everything needed to compete at scale: the 1&1 premium brand, Drillisch's discount brands (yourfone, smartmobil.de, WinSIM), the MBA MVNO network access, Versatel's fiber infrastructure, and United Internet's massive customer reach through GMX and Web.de.

1&1's mobile subscriber base is the second largest MVNO subscriber share in Germany, competing neck and neck with Freenet. Their combined subscriber reach as well as network capacity gets the duo closer to an MNO eye level.

But the merger also set the stage for something even more ambitious. With the MBA MVNO deal providing breathing room and the combined entity generating substantial cash flow, the question became: why stop at being Germany's best MVNO? Why not become a full network operator?

For investors, the 2017 merger created the entity that exists today. The reverse takeover structure, the preservation of the MBA MVNO rights, and the combination of complementary assets demonstrate strategic sophistication that distinguishes 1&1 from pure financial acquisitors. This wasn't about rolling up subscriptions—it was about building something structurally different.

VII. INFLECTION POINT #3: The 5G Spectrum Auction (2019)

What happened in June 2019 changed everything. Again.

Germany's Bundesnetzagentur—the federal network agency—conducted an auction for 5G spectrum. The stakes couldn't have been higher. 5G wasn't just faster 4G; it promised to enable entirely new applications: autonomous vehicles, industrial IoT, augmented reality. The companies that won spectrum would shape German telecommunications for a generation.

The auction for 2 GHz and 3.6 GHz mobile spectrum has come to an end in Mainz after 52 days and 497 rounds of bidding. "The end of the auction fires the starting gun for 5G in Germany. I'm pleased that four companies have acquired spectrum and will compete to expand the network for 5G. The spectrum is to be used not just for the new mobile communication standard, 5G, but also to improve mobile coverage in Germany. It is now up to the companies to put the spectrum to use quickly and to fulfil their coverage obligations," said Jochen Homann, Bundesnetzagentur President.

The Award of spectrum in the 2 GHz and 3.6 GHz bands (5G bands) ended on June 12, 2019 after 497 auction rounds with a total revenue of 6.55 billion Euro.

52 days. 497 rounds. €6.55 billion total. This was an auction battle that tested the financial resolve of every participant.

Germany's Federal Network Agency Bundesnetzagentur announced that the auction for 2 GHz and 3.6 GHz mobile spectrum has come to an end after 52 days and 497 rounds of bidding. The government confirmed it will raise a total of EUR 6.5 billion ($7.31 billion) for 420 megahertz of 5G spectrum. The process will pave the way for the entrance of a fourth operator, 1&1 Drillisch, which spent a total of EUR 1.1 billion for 70 megahertz of 5G spectrum. Deutsche Telekom committed to pay EUR 2.2 billion for 130 megahertz of spectrum in both 5G bands, while Vodafone will spend a total of EUR 1.9 billion to acquire 130 megahertz of 5G spectrum. Meanwhile, Telefonica Deutschland committed to pay EUR 1.4 billion for a total of 90 megahertz of spectrum.

Let's put those numbers in context. 1&1 Drillisch—a company that had never operated a mobile network—spent €1.1 billion on spectrum. That's not a rounding error; it's an existential bet.

The auction ended after 497 rounds on the 12th of June 2019. 1und1 Drillisch secured 50 MHz TDD spectrum in the 3.6 GHz band. 1und1 Drillisch also secured 2x10 MHz FDD spectrum in the 2.1 GHz FDD band, which will be critical to roll out a nationwide network with reliable indoor coverage and support of legacy non-5G terminals.

The spectrum mix matters for network planning. The 3.6 GHz spectrum provides capacity—lots of bandwidth for fast data speeds—but limited coverage. Radio waves at higher frequencies don't travel as far or penetrate buildings as well. The 2.1 GHz spectrum provides better coverage but less capacity. A real network needs both.

In 2019, 1&1 AG successfully participated in the 5G frequency auction of the German Federal Network Agency and is now in the construction phase of the first fully virtualized mobile network in Europe based on the new OpenRAN technology.

The established operators were not pleased. Deutsche Telekom's board member Dirk Wossner said: "The network rollout in Germany has suffered a significant setback. The price could have been much lower. Once again, the spectrum in Germany is much more expensive than in other countries. Network operators now lack the money to expand their networks." Markus Haas, CEO of Telefonica Deutschland, told reporters that part of the money used to bid in the auction could have been used for network deployments. "We must learn from our mistakes, and from other top 5G nations that are a good nose-length ahead of us," he told reporters.

"With the auction proceeds one could have built approximately 50,000 new mobile sites and closed many white spots," Deutsche Telekom noted, referring to areas with inadequate coverage. Vodafone's head of German operations, Hannes Ametsreiter, described the auction as a "disaster for Germany."

The incumbents' complaints were predictable—they had to spend more than expected because a new entrant was bidding aggressively. But their logic was questionable. Yes, spectrum is expensive in Germany. But that expense creates barriers to entry that protect incumbents' market positions. The incumbents were essentially complaining that they had to compete.

With spectrum in hand, 1&1 faced a fundamental choice: what technology to use for the network build? The conventional answer—buy integrated systems from Ericsson, Nokia, or Huawei—would have been the safe choice. Proven technology. Established support. Predictable execution.

1&1 chose differently.

German mobile service provider 1&1 Drillisch, which acquired 5G spectrum in 2019, is to build a greenfield Open RAN network with help from Japan's Rakuten Mobile, the two companies announced today. By doing so, 1&1 will become the first European operator to commit to building a complete Open RAN-based network and add fuel to the growing fire raging under the Open RAN sector. The German operator, part of the United Internet AG empire and which currently provides mobile services to more than 10 million customers on an MVNO basis, had stated previously that it planned to go down the Open RAN route.

CEO Ralph Dommermuth stated: "We have been closely following the development of the new Open RAN technology from the very beginning. So when Rakuten launched the first fully virtualized mobile network in Tokyo, Nagoya and Osaka, we knew for sure: This is the future!"

In an announcement to the Frankfurt stock exchange, 1&1's CEO Ralph Dommermuth stated: "With Rakuten we have the world's only Open RAN expert at our side who really has extensive practical experience with this new technology. Rakuten optimally complements our know-how in telecommunications networks, data centres and cloud applications. Together we will build a high-performance mobile network that has extensive automation and agility to fully exploit the potential of 5G. Thanks to complete virtualization and the use of standard hardware, we can flexibly combine the best products. This is how we become a manufacturer-independent innovation driver in the German and European mobile communications market."

The Rakuten partnership represented another €1+ billion commitment. When you add spectrum costs to network construction, 1&1 was betting €2-3 billion on becoming Germany's fourth network operator.

For investors, the 2019 spectrum auction was the point of no return. 1&1 transformed from a company that could theoretically build a network to one that had committed to doing so. The combination of spectrum investment, Rakuten partnership, and Open RAN technology choice created a differentiated strategy—but also introduced execution risk that would manifest in the years ahead.

VIII. The Tumultuous 5G Rollout (2022-2024)

Building a mobile network from scratch is hard. Building one based on unproven Open RAN technology is harder. Building it while dependent on a towers company owned by your competitor is nearly impossible.

That's the situation 1&1 found itself in starting 2022, and the years that followed would test every assumption underlying the company's strategy.

Under the terms of its mobile license, 1&1 was supposed to have installed at least 1,000 5G antenna sites by Silvester, as the Germans call New Year's Eve. Blaming its main antenna site partner for delays, it will miss the regulatory target and does not expect to have those sites up and running until summer 2023.

The Düsseldorf-based company Vantage Towers has a central role in the dispute. Vantage builds radio towers that are used by various network operators. Vantage received the order from 1&1 at the end of 2021 for a large part of the sites that the newcomer from Montabaur needs for its network. The major contract for the joint use of 3,800 rooftop and mast sites until the end of 2025 and the option to expand by 5,000 extra sites caused some frowning in the telecommunications industry at the time. After all, Vantage is a subsidiary of Vodafone, i.e., a competitor of 1&1. Doesn't Vantage's contract help a newcomer get on its feet, which could make life difficult for the parent company Vodafone in the future? As of today, it doesn't look like it. Rather the opposite is the case, because Vantage built far fewer masts for 1&1 last year than contractually agreed. A government expansion obligation stipulated that 1&1 must operate at least 1,000 5G sites by the end of 2022. Vantage was supposed to handle two-thirds of that.

The situation was delicious in its irony. 1&1 had contracted Vantage Towers—a Vodafone subsidiary—to build out the physical infrastructure for a network that would compete directly with Vodafone. Everyone involved knew the conflict of interest existed. But 1&1 needed Vantage's existing tower assets; building from scratch would take too long and cost too much.

1&1's original goal was to have 1,000 sites activated by the end of 2022. Just 20 were operational by May 2023, according to an interview Dommermuth gave that month with Germany's Handelsblatt newspaper. In June 2023, Bundeskartellamt said it was investigating whether or not Vantage or Vodafone had violated German and European competition law "by impeding 1&1's options for co-using radio masts." The findings thus far appear pretty damning for the tower provider and its key shareholder. Indeed, it notes that since 2021, when Vantage Towers concluded an agreement with 1&1 "on the co-use of a number of antenna sites in the four-digit range," there have been "massive delays" in providing the agreed sites to 1&1. Bundeskartellamt wryly added that while 1&1 is still not able to use more than a "small fraction" of the contractually agreed sites, Vodafone Germany "has significantly expanded its own network in the years following the agreement.

United Internet-owned 1&1 must be feeling somewhat vindicated following a report from Germany's Federal Cartel Office (Bundeskartellamt) that suggests the market's fourth mobile operator had good reason to blame Vantage Towers and Vodafone for its slow 5G rollout progress over the past few years. Andreas Mundt, president of Bundeskartellamt, said preliminary findings from an investigation into the matter indicate that the delay in the contractually agreed provision of sites "is to be considered an anti-competitive impediment to 1&1's market entry as a fourth network operator."

The Cartel Office's preliminary findings were remarkable. They essentially accused Vodafone and Vantage of deliberately sabotaging a competitor's network rollout—a serious allegation that could result in significant penalties and mandatory site delivery.

The regulator says it "provisionally classifies the conduct of Vodafone and Vantage Towers as abusive obstruction." It adds that, based on current knowledge, the companies would have had numerous options to respond to any difficulties in fulfilling the contract without causing such massive delays. The regulator also noted that the fulfilment of the contract would not have hindered Vodafone's own network expansion goals. "The Federal Cartel Office is provisionally considering, in addition to establishing the antitrust violations, ordering the provision of the remaining sites within three years and accompanying this order with further measures," added the regulator.

Despite the tower delays, 1&1 eventually launched its network. 1&1 eventually launched its 5G mobile network in December 2023.

1&1 is now officially the fourth mobile network operator in Germany, having finally launched its own, albeit fairly limited scale, 5G network. And more than that, it is also able to lay claim to being the operator of Europe's first Open RAN network. We have been talking about 1&1 as Germany's fourth MNO for some time now. Then an MVNO, it won 5G spectrum as long ago as 2019, but its full market entry has been beset by delays. The rollout of a greenfield Open RAN network was never going to be a quick endeavour, and difficulties with both roaming deals and towers access added to the challenge. 1&1 declared its Open RAN network, well, open, at the start of this year, but presumably it wasn't fully open; the company was talking about having three active sites at the time. It hasn't commented on the number of sites in this latest launch announcement, but it's safe to presume that it now has more than that, although probably not scores more.

Then came May 2024, and disaster struck.

The outage, which was attributed to a faulty software update, affected around 500,000 customers, German newspaper der Spiegel reported at the time. While the initial problem had reportedly been dealt with on the same day it occurred, some customers also faced network problems in the following days.

In the report accompanying its H1 2024 results, its parent company, United Internet, said the fault clearance process revealed that "central components were not sufficiently dimensioned for further network growth." While 1&1 added that this situation had since been rectified, it has delayed a planned capacity extension. Only "a small number" of customers have been migrated to 1&1's own mobile network since the May outage, which the operator said will delay savings in the purchase of wholesale services. In its Q1 update issued in May, it said around 700,000 customers had been migrated to its own network as of March.

1&1 is carrying out more robust testing before two planned data centers are brought online and has paused migration of existing customers, which would be taking place at a pace of 50,000 a day, to avoid running out of capacity in case further problems arise. United Internet acknowledged that the issue prompted a wave of customer terminations in addition to the slowdown in customer migration, but it did not provide firm numbers.

The outage exposed a brutal reality of Open RAN: the technology was newer, less tested, and more prone to integration issues than traditional systems. When something went wrong, diagnosing and fixing it was harder. The legal experts are still dealing with the consequences, as 1&1 is arguing with the responsible general contractor in court about possible compensation.

Amid the tower delays and technical problems, 1&1 also pivoted its roaming strategy. 1&1 signed a national roaming agreement with Vodafone in 2023, replacing Telefónica. The agreement with Vodafone, which could last up to 18 years, officially kicks off on Thursday.

There's irony here too: the same Vodafone whose tower subsidiary was allegedly sabotaging 1&1's network build became its roaming partner. Business relationships in telecom are complicated.

1&1 has not divulged all the reasons behind its switch to Vodafone, no doubt owing to confidential aspects of the agreement. The operator said the two operators "have a history of collaboration," having previously worked together under an MVNO agreement, although the same is true of Telefónica. Notably, the Vodafone roaming agreement provides 1&1 with access to 5G, which was not the case initially with Telefónica.

For investors, the 2022-2024 period demonstrated both the risks and the resilience of 1&1's strategy. The company faced operational challenges that would have destroyed a less determined organization. Tower delays, software outages, regulatory uncertainty—any one of these could have been fatal. That 1&1 navigated through suggests organizational capability that doesn't show up in financial statements.

IX. Current State & Recent Developments (2024-2025)

The 2024 financial year was, by management's own admission, challenging. But as autumn 2025 arrives, the picture has clarified substantially.

1&1 completed the migration at the beginning of November, it said, fulfilling a major requirement of its 5G licence. It picked up 5G frequencies in Germany's 2019 auction that came with a requirement to achieve competitive independence as the country's fourth mobile network operator by the end of this year. With all of its customers on its network it has now ticked that particular box.

"Unlike traditional mobile networks, where closed systems create dependencies on individual equipment suppliers, like Huawei, we cooperate with around 100 powerful and trustworthy partners," 1&1's management board, headed by CEO Ralph Dommermuth, wrote in a message to shareholders alongside the Q3 numbers. "50 percent of these companies come from Germany, a further 40 percent from Europe. As the world's largest Open-RAN operator in terms of users, we are contributing to a more independent European telecommunications market."

That claim—"world's largest Open RAN operator in terms of users"—is significant. That number means that 1&1 now has the largest number of customers amongst the small number of operators globally that run solely on Open RAN networks. Rakuten Mobile, which launched in 2020 and which owns 1&1's prime integrator and supplier Rakuten Symphony, had just over 9 million customers at the end of July 2025.

In June 2025, 1&1 reached 10 million users on its new Open RAN 5G network just 18 months after initial launch. German fourth mobile operator 1&1 has surpassed 10 million users on its 5G network powered by Open RAN (O-RAN) technology just 18 months after launching its mobile services. In a release, the German telco noted that this milestone marks one of the fastest mobile network expansions in Europe. "Hardly any other mobile network has grown faster than the 1&1 O-RAN," said Michael Martin, chief executive officer of 1&1 Mobilfunk.

The network infrastructure continues to scale. The Montabaur-based company explained at MWC 2025 in Barcelona that the new Open RAN network now comprises 1,000 active antenna sites. "1&1 has made great progress in selecting and securing antenna sites in recent months," said Michael Martin, CEO of 1&1 Mobilfunk GmbH in Barcelona. "As of March 2025, there are 1000 sites and a further 5000 are being developed." For the far-edge data centers, 241 of the planned 500 sites have so far been completed and are connected to the network.

The financials tell a nuanced story. In the first nine months of 2025, the company achieved revenue of 3,016.26 million EUR, compared with 3,017.24 million EUR in the prior-year period. Net profit totaled 110.71 million EUR, down from 196.33 million EUR in the previous year.

As of the end of September 2025, 1&1 had a total of 16.34 million contracts in its base, 12.48 million mobile internet contracts, and 3.86 million broadband contracts. This represents a decrease of 50,000 contracts in the first nine months of 2025.

Revenues for the period were flat at a shade over €3 billion, but EBITDA fell by 11.5% on-year to €409.8 million, hurt by higher start-up costs for the 1&1 mobile network, although the company notes that that was expected. Customer numbers are heading in the right direction, in mobile at least, with 40,000 additions taking the company's base to 12.48 million, but overall its customer contracts are down slightly, hit by fixed broadband losses.

The customer dynamics reveal an important transition. Mobile is growing; broadband is declining. This reflects broader market trends—more customers consuming connectivity through mobile—and 1&1's strategic focus on the mobile network where it now has infrastructure advantages.

For the financial year 2025, the company confirms its forecast updated in June 2025 and expects for the 2025 a stable contract base and service revenue at the previous year's level (2024: €3,303.1 million). EBITDA is expected to decline by approx. 7.8 percent to approx. €545 million (2024: €590.8 million). This decline is due to a lower EBITDA in the Access segment, which is expected to reach approx. €810 million (2024: €856.1 million). The reasons for the decline in EBITDA are higher advance payment costs for national roaming due to a lower than expected network growth at Vodafone and the expiry of the national roaming agreement with Telefónica. This agreement provided for one-time payments every five years, which were capitalized and amortized as planned, whereas the new national roaming agreement with Vodafone does not provide for such one-time payments.

EBITDA loss in the 1&1 mobile network segment will also remain roughly unchanged in 2025, at around -EUR265 million (2024: -EUR 265.3 million). However, the company said this includes approximately EUR100 million in expenses for those customer migration and network services, which will now cease with the completion of that migration.

That €100 million in migration costs that will cease after 2025 represents a significant inflection point. The heavy lifting of building the network and migrating customers is largely complete. From 2026 onward, the economics should improve substantially.

Just this week, another major development: 1&1 has agreed to buy sister company Versatel for €1.3 billion in an intra-group acquisition that shows how the German fibre firm's value has risen over the past decade. The deal means 1&1 is essentially bringing its fixed-line capabilities under closer control. Versatel already provides the network for 1&1's fixed broadband customers and its mobile backhaul. By bringing the whole lot in house, 1&1 will have more flexibility going forward.

Versatel is also doing significant upfront work to roll out 1&1's network. Versatel provides fiber optic connectivity for its base stations, four core data centers, 24 edge data centers, and currently approximately 300 Far Edge data centers. With this acquisition, 1&1 will have all the infrastructure needed for both fixed-line and mobile communications, as well as business customer solutions.

This acquisition consolidates the infrastructure stack within 1&1, reducing dependency on the parent company and creating a more integrated telecommunications platform.

For investors evaluating 1&1 today, the operational complexity is largely behind the company. Network migration is complete. The Versatel acquisition brings fixed-line infrastructure in-house. The regulatory overhang from the Vantage dispute should resolve. What remains is executing on the customer growth strategy while harvesting the efficiency benefits of operating on owned infrastructure.

X. Playbook: Business & Investing Lessons

Myth vs. Reality: What the Market Gets Wrong About 1&1

Myth #1: 1&1 is just another discount telecom brand competing on price.

Reality: 1&1 operates a multi-brand strategy spanning premium (1&1) and discount (yourfone, smartmobil.de, WinSIM) segments. More importantly, it now owns Germany's only independent Open RAN infrastructure, giving it cost advantages and vendor flexibility that pure-play MVNOs or resellers will never achieve. The discount brands are distribution channels, not the core strategy.

Myth #2: The Open RAN bet was reckless.

Reality: Open RAN created execution risk—as the 2024 outage demonstrated—but it also created strategic differentiation. Traditional networks lock operators into single-vendor relationships (typically Ericsson, Nokia, or Huawei). 1&1's multi-vendor approach provides negotiating leverage, technology flexibility, and—increasingly important—freedom from Chinese suppliers that face regulatory scrutiny across Europe.

Myth #3: Being the fourth network operator in a mature market is structurally disadvantaged.

Reality: Germany's mobile market had consolidated to three operators after the 2014 Telefónica/E-Plus merger, creating pricing power for incumbents that came at consumers' expense. Regulatory authorities explicitly supported 1&1's entry as a competitive remedy. The regulatory tailwind—from spectrum allocation to the Cartel Office investigation of Vantage—suggests authorities want 1&1 to succeed.

Porter's Five Forces Analysis

Threat of New Entrants: LOW The €1.1 billion spectrum investment, €1+ billion network build, and decade of regulatory navigation create formidable barriers. No new greenfield entrant is likely to replicate this path.

Bargaining Power of Suppliers: MODERATE and IMPROVING Open RAN architecture explicitly reduces supplier power by enabling multi-vendor procurement. The 100+ partner ecosystem 1&1 cites represents deliberate fragmentation of supplier leverage.

Bargaining Power of Customers: HIGH German consumers remain price-sensitive and willing to switch. However, 1&1's multi-brand strategy allows it to capture customers across price points without cannibalizing premium pricing.

Threat of Substitutes: MODERATE Fixed-line internet could substitute for mobile data in some use cases. OTT services (WhatsApp, Zoom) substitute for traditional voice and messaging. However, mobile connectivity remains essential for smartphones—the primary computing device for most consumers.

Competitive Rivalry: HIGH but DIFFERENTIATED Three well-capitalized incumbents compete intensely. However, 1&1's cost structure—Open RAN efficiency, owned fiber backhaul, no legacy network depreciation—may allow profitability at price points where competitors struggle.

Hamilton Helmer's 7 Powers Framework

Scale Economies: BUILDING 1&1 is still scaling its network, so scale economies are nascent. However, each additional customer adds incremental revenue while fixed network costs remain stable. The company is approaching the scale inflection where unit economics improve dramatically.

Network Effects: WEAK Telecommunications doesn't exhibit strong network effects. One customer's experience doesn't improve when another customer joins.

Counter-Positioning: STRONG This is 1&1's most powerful strategic position. Open RAN represents counter-positioning against incumbents who have billions invested in traditional vendor relationships. Deutsche Telekom, Vodafone, and Telefónica cannot easily adopt Open RAN without stranding existing capital investments and disrupting supplier relationships. 1&1's greenfield approach—no legacy infrastructure to protect—allowed a technology choice incumbents can't easily replicate.

Switching Costs: MODERATE Number portability reduces switching costs for consumers. However, bundling (mobile + broadband + hardware) creates friction. Contract terms provide some retention.

Branding: MODERATE 1&1 has meaningful brand recognition in Germany through decades of marketing and the GMX/Web.de email platforms that reach 43 million users. However, brand doesn't command the premium pricing power it might in other industries.

Cornered Resource: MODERATE The MBA MVNO contract from the 2014 merger remedies was a cornered resource that no competitor could access. The 5G spectrum acquired in 2019 provides exclusive rights. The Versatel fiber network creates backhaul capabilities competitors must rent.

Process Power: EMERGING 1&1's multi-decade experience in customer acquisition—from marketing services to ISP to MVNO to MNO—represents accumulated process knowledge. The Open RAN deployment, despite setbacks, is building organizational capabilities in next-generation network operations.

Key KPIs to Track

1. Mobile Net Adds (Quarterly) The single most important metric for 1&1's trajectory. The company needs to grow its mobile customer base to leverage its fixed-cost network infrastructure. Each net add represents incremental high-margin revenue. Watch for acceleration as network quality improves and roaming costs decline.

Target: Positive quarterly net adds accelerating from current ~40,000/quarter toward 100,000+ as network coverage expands.

2. Mobile Network Segment EBITDA Loss Currently around -€265 million annually. The path to profitability depends on migrating roaming traffic to owned infrastructure (eliminating wholesale payments) while growing the customer base. Management guidance suggests €100 million of current costs will disappear after 2025 migration completion.

Target: EBITDA loss narrowing toward breakeven by 2027-2028, then turning profitable.

3. Service Revenue Per Customer This metric captures both pricing power and product mix. As 1&1 migrates customers to its own network and potentially offers differentiated services (lower latency, better speeds), watch whether service revenue per customer increases.

Target: Stable to increasing as network quality enables value-added services.

Regulatory and Legal Overhangs

The Bundeskartellamt investigation into Vantage Towers/Vodafone conduct remains unresolved. The Federal Cartel Office said it would provide a final decision on the allegation around the middle of this calendar year. A ruling in 1&1's favor could include mandatory site delivery orders and potentially damages, representing upside not reflected in current valuations.

The pending 2025 spectrum decisions for 800 MHz, 1800 MHz, and 2600 MHz bands could affect 1&1's competitive position. These lower-frequency bands are crucial for rural coverage; 1&1 currently lacks them.

Investment Considerations

Bull Case: - Network migration complete; €100M+ annual cost savings begin 2026 - Counter-positioning via Open RAN creates durable cost advantages - Regulatory support for fourth operator suggests favorable spectrum treatment - Versatel acquisition creates integrated infrastructure platform - Parent company United Internet (50%+ owned by Dommermuth) provides strategic patience

Bear Case: - German telecom market remains intensely competitive with pricing pressure - Open RAN technology still maturing; further outages possible - Fixed broadband losses offsetting mobile gains - €265M annual mobile segment losses burden consolidated results - Incumbent response could intensify (aggressive pricing, accelerated 5G deployment)

Final Thoughts

Ralph Dommermuth started selling marketing services for software companies in a small German town in 1988. Thirty-seven years later, he runs Europe's first fully virtualized Open RAN mobile network operator.

The path involved regulatory arbitrage (the MBA MVNO deal), corporate restructuring creativity (the reverse takeover), technology bets (Open RAN and Rakuten), and the kind of founder-led persistence that doesn't appear in strategic frameworks but explains more about business success than any analytical model.

1&1 is not yet a proven investment success. The mobile network segment loses hundreds of millions annually. Customer growth is positive but modest. The competitive environment remains brutal.

But the structural position is compelling. 1&1 owns infrastructure that enables economics competitors can't match. It operates technology that provides flexibility traditional operators surrendered long ago. And it's led by a founder with a 37-year track record of building through cycles rather than optimizing for quarterly results.

The coming years will reveal whether the audacious bet to become Germany's fourth network operator pays off. The infrastructure is built. The customers are migrating. What happens next depends on execution—and on whether European telecommunications has room for a genuine challenger.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube