Valmont Industries: The Hidden Giant That Revolutionized How the World Grows Food

I. Introduction: The $5,000 Bet That Reshaped the American Landscape

Somewhere above the Great Plains, if you look down from an airplane window at 30,000 feet, you'll notice something strange—enormous green circles, scattered like crop medallions across an otherwise tan landscape. These aren't mysterious phenomena or alien artwork. They're the visible signature of center pivot irrigation, a technology that Scientific American once called "perhaps the most significant mechanical innovation in agriculture since the replacement of draft animals by the tractor."

Frank Zybach's center pivot irrigation machine invention has revolutionized irrigated agriculture around the world. And behind that revolution stands a company that most Americans have never heard of, even as they drive past its utility poles every day, send text messages through towers it manufactures, and eat food grown under its irrigation systems.

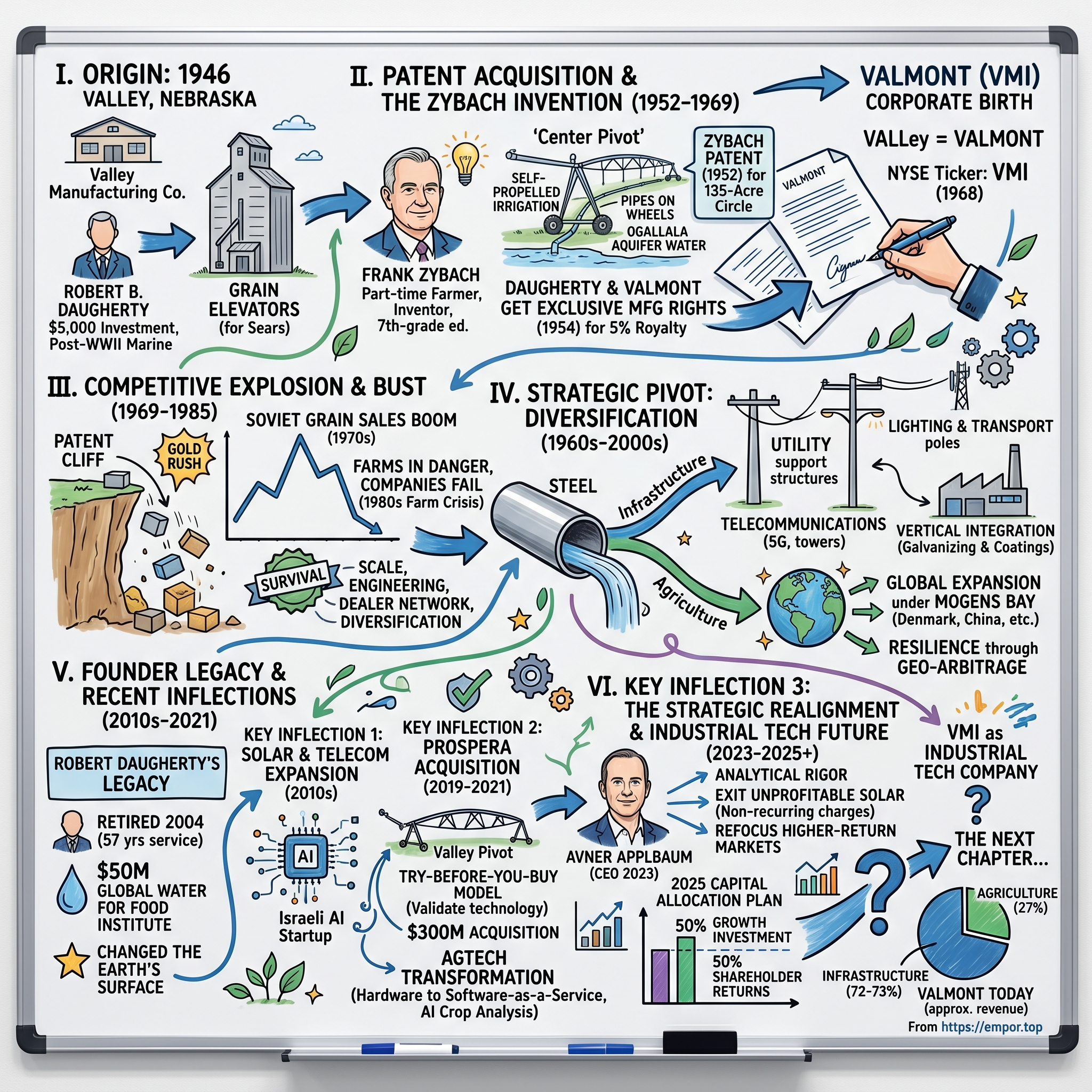

Valmont Industries, Inc. is an American multinational corporation specializing in the manufacture of engineered products and services for infrastructure and agriculture, founded in 1946 by Robert B. Daugherty in Valley, Nebraska, and headquartered in Omaha, Nebraska. The company operates through two primary business segments: Infrastructure, which includes utility support structures, lighting and transportation poles, telecommunications components, solar tracking systems, and protective coatings for metal products; and Agriculture, focused on mechanized irrigation systems such as center pivot and linear equipment for large-scale farming. Publicly traded on the New York Stock Exchange under the ticker symbol VMI since 1968, Valmont has grown into a global leader with operations in over 20 countries across North America, Europe, Asia, Latin America, and Australia, employing approximately 11,000 people worldwide as of 2024.

How did a returning World War II Marine's $5,000 investment—roughly $75,000 in today's dollars—turn into a company with a market cap as of November 2025 of approximately $8 billion? The answer lies in a remarkable combination of savvy patent acquisition, survival through devastating industry downturns, brilliant diversification, and—most recently—a digital transformation that's turning an old-economy manufacturer into what leadership calls an "Industrial Tech company."

This is the story of Valmont Industries—a "hidden gem," as current CEO Avner Applbaum puts it, that built critical infrastructure you likely interact with every day without ever knowing its name.

II. The Origin Story: A Marine's $5,000 Bet (1946-1953)

Picture Valley, Nebraska, in 1946. The war was over. Millions of young men were returning home, uncertain about their futures. Among them was Robert B. Daugherty, a 24-year-old Marine who had served in the Pacific Theatre and later in China. Born in 1922 in Omaha, Daugherty was a graduate of Central High School in Omaha and Carleton College in Northfield, Minnesota. He was commissioned a second lieutenant in the Marine Corps, first serving in the Pacific Theatre, and later in China.

Daugherty was considering a career in the Marines when destiny intervened. At the time, Daugherty was considering a career in the Marines until his uncle and mentor, Frank Daugherty, convinced him to consider post-war business options. Daugherty made a small investment to acquire a half interest in a Valley, Nebraska, farm machine shop that produced built-to-order grain elevators for area farmers.

In 1946, Robert Daugherty was a young Marine coming home after World War II. He was from Omaha and a self-described "city kid," but he knew something about agriculture. His father, Robert Daugherty Sr., owned one of the larger livestock commission firms at the Omaha Stock Yards. During the summers, young Robert worked in the stockyards, unloading cattle and other livestock that farmers were hiring his father to sell.

This wasn't just anyone stepping into agriculture. Daugherty understood the industry from the inside—the economics, the challenges, the customers. When he invested his $5,000 life savings in that modest Valley machine shop, he wasn't gambling blindly. He was betting on what he knew.

The small venture, Valley Manufacturing Company, initially focused on mundane but essential farm equipment. The partner's firm, Platte Valley Manufacturing Co., produced built-to-order grain elevators for area farmers. After being awarded an order for 1,000 elevators for Sears Roebuck, the small company began mass production and expansion.

By the early 1950s, however, the post-war agricultural boom was showing signs of strain. In 1952, Valley Manufacturing started looking for ways to diversify. Daugherty was searching for something that could transform his modest farm equipment business into something more. What he found would literally change the surface of the Earth.

III. The Zybach Patent: Acquiring a Revolution (1952-1969)

The Inventor: Frank Zybach

About 100 miles west of Valley, Nebraska, lived a man named Frank Zybach—a part-time farmer with a seventh-grade education and an extraordinary mechanical mind. Frank Zybach, son of Edward and Lena Liebengut Zybach, was born in Lafayette, Oregon on July 10, 1894 but was raised on a farm near Columbus, Nebraska to which his parents moved when he was a small boy. While his formal education was discontinued following the seventh grade, Frank Zybach was an astute observer and he spent many hours with his father who was a neighborhood blacksmith. He grew up with a keen interest in working with metals—an attraction that remained throughout the rest of his life.

Zybach's genius lay in his ability to observe problems and engineer solutions. Zybach began developing a self-propelled irrigation system after observing another farmer irrigate crops by using a tractor to systematically tow a long pipe, outfitted with sprinklers, across the field. By 1947, Zybach's system featured two sections of pipes on skids, suspended by cables from two towers. By 1949, the device included five towers with pipes running on wheels and could irrigate 40 acres. Zybach then added water valves for siphoning pressurized water from the main pipe to drive the wheels and maintain tower alignment.

In 1952, Zybach was granted a patent on a larger irrigation system with a 600-foot boom that could water a 135-acre circle (all but the corners of a standard 160-acre section of land).

Here was the critical insight: The Great Plains had vast underground water reserves (the Ogallala Aquifer) but limited rainfall. Traditional gravity-flow irrigation was labor-intensive and wasteful. Zybach's machine could cover most of a standard quarter-section of farmland while a single farmer watched from his truck, drinking coffee. It was elegant, efficient, and—for anyone with vision—revolutionary.

The Deal

After he received his patent in July 1952, Zybach contacted a Columbus automobile dealer and entrepreneur, Mr. A.E. Trowbridge. Trowbridge agreed to put up some capital to begin producing Zybach's center-pivot systems in a rented machine shop in Columbus. In return, Zybach sold him 49% interest in the patent rights. From the spring of 1953 to September 1954, 10 center-pivot systems were manufactured by the Zybach-Trowbridge partnership. During this time, Zybach redesigned the system so the main pipeline was suspended about 9 feet above the ground so it could be used to irrigate taller-growing crops.

Then came Robert Daugherty. During the summer of 1954, Zybach and Trowbridge decided to sell the manufacturing rights to the center-pivot system. Robert B. Daugherty, then President of Valley Manufacturing Company (now Valmont Industries, Inc.), negotiated arrangements in September 1954 for exclusive manufacturing rights to the center-pivot system in exchange for a 5% royalty on each system sold by Mr. Daugherty's firm until the patent expired in 1969.

This was one of the great patent acquisitions in American industrial history. Daugherty wasn't just buying a product—he was acquiring a monopoly on a technological revolution that would transform global agriculture. For a royalty payment that would cease in 15 years, he secured the exclusive right to manufacture and improve upon an invention that would make previously marginal land productive.

The Transformation

Daugherty's engineers spent the next decade refining Zybach's innovation, making it sturdier, taller, and more reliable, and converting it from a hydraulic power system to electric drive. Daugherty's company went on to grow into Valmont Industries, with Valley Irrigation being its subsidiary.

In 1954, Valley produced only five of the units. By 1960, the company produced 50 systems annually. The growth was slow but steady, and critically, Daugherty's team was continuously improving the technology.

Through much of the 1950s and 60s, Valley had the market for center pivot systems pretty much to itself. Their patent protected Valley until 1969.

The company underwent a corporate transformation to match its technological one. In 1966, the Valley Manufacturing Company became Valmont Industries, named after the two neighboring towns of Valley and Fremont. The company went public in 1968, listing on the New York Stock Exchange (NYSE) under the ticker symbol VMI.

By the time the Zybach patent expired in 1969, Valmont had achieved what might be called "pioneer's advantage"—a decade and a half head start in manufacturing expertise, engineering improvements, dealer relationships, and brand recognition. The question was whether they could maintain that advantage in open competition.

IV. The Patent Cliff & Competitive Explosion (1969-1985)

The expiration of Zybach's patent in 1969 triggered what can only be described as a gold rush. After 1969, other Nebraska manufacturers followed in Valmont's footsteps.

By the mid-1970s, interest in center-pivot irrigation had grown dramatically with nearly 30 firms involved at one time or another in the manufacture and sale of these systems. More than 80 individuals and companies tried to manufacture and sell center pivot systems through the boom years—a competitive explosion comparable to the dot-com bubble decades later.

The frenzy was fueled by extraordinary market conditions. In 1973, the Soviet Union began purchasing massive quantities of American grain, driving prices skyward and creating seemingly insatiable demand for increased agricultural production. In the 1970s, there were about 3,000 pivots in operation in Nebraska, while most irrigated acres were still gravity flow. Today, thanks to Zybach's innovation, there are well over 55,000 pivots in operation in Nebraska alone, covering the vast majority of the state's 8.6 million irrigated acres.

But the boom proved unsustainable. By 1980, the export market dried up. Agricultural credit dried up. Farmers were in danger of losing their farms. And almost all of the center pivot companies went out of business.

The post World War II years of agricultural boom slowly but steadily gave way to an economic downturn in farming, which had reached a new low by the 1980s. As irrigation equipment was closely tied to the highly volatile agricultural economy, the company was operating $1.9 million in the red by 1985. Adding to the domestic farm depression, orders from the oil-rich Near East dried up as that region became more agriculturally self-sufficient.

The 1980s farm crisis was existential—not just for Valmont, but for rural America. Farm bankruptcies soared. Agricultural banks failed. And irrigation equipment manufacturers, whose fortunes were tied directly to farmer purchasing power, faced annihilation.

Why Valmont Survived

Of the 80+ competitors that rushed into center pivot manufacturing after 1969, only a handful remain today. Today, Lindsay is the largest exporter of center pivot systems and pushing Valmont for overall market share. The survivors include Valmont Industries, Lindsay, Reinke Manufacturing Co, T-L Irrigation, Alkhorayef Group, Bauer GmbH, and Rainfine (Dalian).

What distinguished the survivors? Scale economics, engineering expertise, dealer networks, and—critically—diversification. Daugherty had seen the danger of single-product dependency and had begun plotting Valmont's escape from agriculture-only dependence years before the crisis hit.

V. The Diversification Pivot: Infrastructure & Beyond (1960s-2000s)

The Strategic Insight

Even as center pivot irrigation was driving Valmont's growth in the 1960s and 1970s, Robert Daugherty recognized a fundamental vulnerability: his company's fortunes were tied to a single, highly cyclical market. One bad farm season could devastate the business. He needed diversification—but not random diversification. He needed to leverage what Valmont did best.

Discussing his strategy for success in an article in Investment News & Views, Daugherty cautioned, "New business development will occur only in those areas where we can capitalize on our existing channels of distribution, market knowledge, and investments."

What Valmont did best was work with steel. Large quantities of pipe were needed to produce the center pivot so the Valmont team began manufacturing it on their own. An outpouring of new applications for their pipe products led to a prominence in two markets: food production and infrastructure development.

The insight was brilliant in its simplicity: The same steel fabrication skills that built irrigation booms could build utility poles. The same galvanizing processes that protected irrigation pipe from corrosion could protect transmission towers. The same dealer networks selling to rural customers could sell to municipalities and utilities.

Infrastructure Expansion

Beginning in the 1960s, Valmont started manufacturing tapered metal light poles, traffic signal supports, and eventually transmission structures. Throughout the 1970s and 1980s, Valmont expanded beyond agricultural irrigation into utility structures, lighting poles, and other infrastructure products, establishing itself as a diversified industrial manufacturer.

The company developed vertical integration in its coating services—galvanizing became a standalone business unit serving both internal needs and external customers. The company, renamed Valmont Industries in 1967, created a hot-dipped galvanizing process for its own irrigation pipe.

In 1987 the United States Federal Highway Bill began a five-year, $70 million expenditure program, boosting Valmont's position. Infrastructure spending became a counter-cyclical buffer against agricultural downturns.

Global Expansion Under Mogens Bay

The internationalization of Valmont accelerated dramatically under new leadership. In 1993 the company named Mogens C. Bay, a native of Denmark with impressive global operating experience, president and chief executive officer.

He moved to Madrid, Spain, in 1982 as vice president-sales and later vice president-marketing of Valmont International. In 1986, he was assigned to corporate headquarters as the president and general manager of Valmont International and, four years later, he was named president and general manager of Valmont Irrigation. He became president and CEO of Valmont Industries, Inc. in 1993. Mogens was named chairman and CEO in 1997. From 1974 to 1978, Mogens was the manager of the East Asiatic Company's office in Beijing, the People's Republic of China. The East Asiatic Company was the only western company permitted to operate an office in the People's Republic of China at that time.

Bay's international experience was transformative. Bay's international experience—he's a native of Denmark and spent his early career in Hong Kong and Beijing—spurred Valmont's expansion. Under his leadership, Valmont's sales grew from roughly $400 million to over $3 billion at peak.

At that time, sales had been flat for five years at around $400 million. Bay narrowed Valmont's focus, selling businesses including its investment in InaCom, a firm with roots in a Valmont arm that sold personal computers to farmers. He also broadened Valmont's international reach, looking to take advantage of growing markets and shield the company's exposure to a downturn in any one region's market.

The dual strategy—geographic diversification and product diversification—created resilience. When North American agriculture was weak, international sales and infrastructure could compensate. When infrastructure spending slowed, agricultural replacement demand could provide a floor.

VI. Leadership Transitions & The Founder's Legacy (2004-2010)

In 2004, Robert Daugherty retired from Valmont's Board of Directors after an extraordinary 57 years of service. Daugherty retired in 2004 from Valmont's board of directors after serving for 57 years. Mogens Bay was appointed Head Chairman and C.E.O. following the retirement of founder Robert B. Daugherty in 2004.

The transition from founder-led to professional management was complete, but Daugherty remained engaged with the causes closest to his heart. In April 2010, Daugherty committed $50 million to the University of Nebraska to found the Global Water for Food Institute, a multi-campus center for research, education and policy analysis relating to the use of water for agriculture. The institute will allow the university to develop solutions to the challenges of hunger, poverty, agricultural productivity and water management.

Daugherty summed it up by saying, "Improving agricultural productivity has been my life's work."

Seven months after making that commitment, Robert Daugherty passed away. Robert B. Daugherty, the man who pioneered center pivot irrigation and founded Valmont Industries in Omaha, Nebraska, passed away on November 24, after a short illness.

The tributes were extraordinary. "We've lost much more than our founder," said Valmont's Chairman and CEO Mogens C. Bay. "We've lost a great leader, mentor, innovator and friend. His vision laid the groundwork for a global industry. He literally changed the surface of the earth."

That last phrase wasn't hyperbole. Center pivot irrigation systems are visible from space—the green circles that transformed the semi-arid Great Plains into one of the world's most productive agricultural regions. Daugherty didn't invent the technology, but he recognized its potential, acquired the rights, improved it relentlessly, and built the company that brought it to scale.

Bay also is a trustee of Boys Town, vice president of the Henry Doorly Zoo & Aquarium's governing board and chairman of the board of the Robert B. Daugherty Foundation, which has assets of nearly $1 billion and provides grants to Nebraska nonprofits funded by the fortune of Valmont founder Daugherty.

The Daugherty Foundation continues his legacy of philanthropy, while Valmont continues his legacy of industrial innovation.

VII. Key Inflection Point #1: The Solar & Telecommunications Expansion (2010s)

The 2010s brought new growth vectors for Valmont's Infrastructure segment. Valmont's telecommunications infrastructure encompasses towers and monopoles optimized for 5G and wireless networks.

The wireless buildout created enormous demand for telecommunications structures. As 4G networks expanded and 5G began rolling out, carriers needed thousands of new towers, small cell structures, and concealment solutions. Valmont's steel fabrication expertise translated directly into this market.

Valmont serves two primary segments—agriculture and infrastructure—with seven markets we serve: Utility, Lighting and Transportation, Telecom, Solar, Coatings, Irrigation and Ag Tech. We manufacture products in 84 facilities spread across six continents, and we do business in 21 different countries.

The utility infrastructure market offered particularly strong secular tailwinds. Valmont is well-positioned to benefit from strong multi-year utility transmission and electrification investment trends. Grid modernization, renewable energy integration, and aging infrastructure replacement created sustained demand for Valmont's transmission poles and structures.

Valmont Industries operates through two primary reportable segments: Infrastructure and Agriculture, reflecting its focus on vital infrastructure solutions and agricultural productivity. The company maintains a portfolio of brands integrated across these segments to optimize supply chain efficiency and drive strategic growth in renewables and sustainability. The Infrastructure segment, which accounted for approximately $3.0 billion in net sales in fiscal 2024 or about 74% of total revenue, encompasses utility structures, lighting and transportation solutions, telecommunications, solar applications, and coatings services. This division plays a pivotal role in supporting global infrastructure needs, including energy transmission, urban development, and renewable energy projects, with an emphasis on engineered steel and concrete products protected by corrosion-resistant finishes.

Solar tracker systems represented another expansion avenue. Valmont developed single-axis solar trackers that follow the sun across the sky, optimizing energy capture from photovoltaic installations. This was a natural extension of the company's steel structure and motor expertise.

However, as we'll see, the solar business would prove challenging, eventually becoming one of the segments management chose to exit in 2024-2025.

VIII. Key Inflection Point #2: The Prospera Acquisition & AgTech Transformation (2019-2021)

The Partnership Model

In 2019, Valmont did something unusual: rather than rushing to acquire an Israeli AI startup, they entered a strategic partnership first. Since 2019, Valmont and Prospera have successfully integrated AI technologies with center pivot irrigation to develop real-time crop analysis and anomaly detection solutions, resulting in strong adoption and greater returns for the grower. Leveraging Prospera's unique technology, the partnership has expanded its intelligent solutions, monitoring five million acres in 2020 against an original estimate of one million, with twice as many growers using the service as compared to 2019.

The results exceeded all expectations. The original target was one million monitored acres by 2020. They achieved five million—a five-fold outperformance. Grower adoption doubled year-over-year.

The $300 Million Acquisition

On 5 May 2021, Valmont Industries, a US-based leader in the design and production of mechanised agricultural irrigation equipment, announced it had acquired Prospera, an Israeli crop analytics startup, for a headline price of $300 million. Founded in 2014 in Tel Aviv (Israel), 100 employee Prospera is a developer of machine vision technologies that continuously monitor and analyse plant development, health and stress. The company's platform captures multiple layers of climate and visual data from the crop field and provides actionable, easy-to-read insights to growers via mobile and web dashboards. As of 2020, Prospera claims to process 50 million data points daily, with 4,700 fields and $5 billion worth of produce monitored.

The merging of the firms will create the "largest global, vertically-integrated artificial intelligence (AI) company in agriculture," the companies said in a statement.

The strategic rationale was compelling. Unique, Disruptive and Differentiated Value Proposition: The transaction will create the largest global, vertically-integrated AI company in agriculture, immediately providing a highly differentiated in-season solution. Using the pivot as the digital data hub, this solution brings demonstrated, advanced agronomy and unprecedented visibility to the field, enabling the grower to take immediate action to remediate issues. Leveraging Prospera's technology and Valmont's global reach and omnipresence on the field, the combination will create the first commercially available subscription model of its kind, providing innovative and disruptive solutions to help growers lower costs, increase yields, use less land and save time.

The Try-Before-You-Buy Model

Valmont's techquisition of Prospera Technology is the result of a two-year journey that started with a strategic partnership to develop transformative AgTech solutions. In 2019, the two companies started working on a project to integrate AI technology with centre pivot irrigation, to develop real-time crop analysis and anomaly detection solutions. At the time, the goal was to have this new solution used on one million acres by the 2020 growing season. Prospera recently announced that this target was actually surpassed by 4x, with five million acres monitored in 2020—and twice as many growers using the service as compared to 2019.

This "try-before-you-buy" approach represents a model for how traditional industrial companies can navigate technology acquisitions. The two-year partnership allowed both sides to: - Validate the technology in real-world conditions - Build integration between hardware and software - Demonstrate market demand - Reduce acquisition risk

According to Daniel Koppel, Prospera's CEO, the company's major roadblock was its go-to-market strategy, as a result of the company's focus on product development and R&D to the detriment of a strong sales and marketing department ("we are 90 people and most of them are scientists"). As such, Koppel decided the transaction with Valmont was the best way to focus on the company's core competency—its technological expertise—and allow an established industry player such as Valmont define the commercialisation strategy, instead of having to develop a D2C model and pursue multiple partnerships.

The Prospera acquisition signaled Valmont's transformation from a pure-play hardware manufacturer to a company capable of offering software-as-a-service solutions integrated with its physical products.

IX. Key Inflection Point #3: The 2023-2025 Strategic Realignment

New CEO, New Direction

In July 2023, Valmont announced a leadership transition that would reshape the company's strategic direction. Valmont Industries, Inc. (NYSE: VMI), a global leader that provides vital infrastructure and advances agricultural productivity while driving innovation through technology, today announced that its Board of Directors has named Avner M. Applbaum, current Executive Vice President and Chief Financial Officer, as President and Chief Executive Officer, effective immediately. Mr. Applbaum succeeds Stephen G. Kaniewski, CEO since December 31, 2017, who is stepping down to pursue other opportunities.

Applbaum became President and CEO in 2023 after joining Valmont in 2020 as Executive Vice President and Chief Financial Officer. In that role, he shaped and executed the company's financial strategy while overseeing all financial operations, as well as information technology, cybersecurity, and technology innovation.

Avner M. Applbaum, age 53, has served as Chief Executive Officer of Valmont Industries since July 2023 and as a director since July 2023; he previously served as Executive Vice President and Chief Financial Officer from March 2020 to July 2023. He is a Certified Public Accountant (inactive) with 17 years of operational and financial roles at publicly traded manufacturing companies.

Applbaum brought analytical rigor and a transformation mindset. Mogens C. Bay, Chairman of the Board, commented, "We have much to look forward to with Avner as our next President and CEO. During his tenure, Avner has meaningfully elevated our finance organization, bringing analytical rigor and increased transparency to our stakeholders, and has been instrumental in executing our long-term growth strategy and driving efforts to digitize the way we do business as we continue to transform into an Industrial Tech company."

Portfolio Refinement

Applbaum moved quickly to reshape Valmont's portfolio. The company recorded approximately $138.3 million in non-recurring charges, primarily related to exiting the North American solar market and significantly downsizing solar operations in Brazil.

In Q2 2025, Valmont reported a GAAP loss of ($1.53) per share, driven by $112.1 million in one-time charges. These included $91.3 million in non-cash asset impairments (notably $71.1 million from the Solar and Access Systems businesses) and $9.8 million in severance and other costs. While the loss contrasts sharply with the prior year's $4.91 EPS, the company's adjusted EPS of $4.88 underscores the exclusion of these non-recurring items. This realignment, initiated under CEO Avner Applbaum in 2023, was not a reactive measure but a strategic overhaul. By exiting underperforming segments like Solar and Access Systems, Valmont is shedding low-margin activities to refocus on higher-return markets such as Utility infrastructure, Telecommunications, and International Agriculture.

The restructuring was painful but decisive. The company incurred approximately $138.3 million in non-recurring charges related to organizational realignment and portfolio refinements, with the majority ($105.5 million) associated with exiting the North American solar market and downsizing solar operations in Brazil. The company is exiting the North American solar market and downsizing solar operations in Brazil, while also assessing its APAC Access Systems business. These strategic moves resulted in substantial one-time charges but position the company for improved long-term profitability. The realignment includes headcount reductions in Solar and North American Agriculture, shifting resources to growth opportunities, reducing management layers, and integrating operations.

2025 Capital Allocation

The company's Board has approved a $700 million share repurchase authorization and a 13% increase in quarterly dividend to $0.68 per share ($2.72 annualized), payable April 15, 2025. The company plans to allocate approximately 50% of operating cash flow to high-return growth opportunities, including strategic capacity expansion in the Infrastructure segment and strategic acquisitions. The remaining 50% will be directed to shareholder returns through repurchases and dividends. Valmont intends to maintain its Investment Grade credit rating with a long-term target for net leverage of 2.5X or less.

When I joined the company around 2020 until today, we more than doubled our earnings per share. Our return on invested capital almost doubled to 16.4%.

The results have been notable. Under his leadership, Valmont delivered 2024 revenue of $4.075 billion, net earnings of $350.624 million, adjusted ROIC of 16.4%, and company TSR of 214.41 for 2024, with long-term incentives paying out at 200% of target on ROIC/OIG goals.

X. The Business Today: Segment Deep Dive

Infrastructure (72-73% of Revenue)

The Infrastructure segment (72.6% of net sales) saw sales decrease 2.4% to $706.2 million, with growth in Utility and Telecommunications offset by lower Solar sales. The Agriculture segment (27.4%) increased 3.3% to $267.3 million, driven by strong international performance, particularly in EMEA and Brazil, despite North American softness.

Within Infrastructure, subsegment performance varied dramatically: Telecommunications showed exceptional growth of 40.5%, while Utility sales increased by 5.4%. However, these gains were largely offset by declines in Lighting and Transportation (-6.9%) and Solar (-47.4%).

The Utility segment benefits from powerful secular tailwinds: grid modernization, renewable energy integration, and aging infrastructure replacement. Valmont Industries is set for strong revenue growth, driven by a robust U.S. utility investment cycle, 5G telecom demand, and international agriculture strength.

Under the "Valley Irrigation" brand, Valmont manufactures and distributes a wide range of advanced irrigation equipment. The company provides a wide range of irrigation solutions, such as drip, sprinkler, and variable rate irrigation technologies. With around 270 dealers in North America and another 270 across over 60 countries, Valmont Industries, Inc. has built a robust global distribution network for its precision irrigation products.

Agriculture (27% of Revenue)

The Agriculture segment demonstrated stronger overall performance with sales of $289.4 million, up 2.7% year-over-year. This growth was driven entirely by international markets, which saw sales increase by 22.0% to $146.9 million. North American agricultural sales declined by 11.7% to $142.5 million, reflecting challenging market conditions in the region.

The contrast is stark: international agriculture is growing at 22% while North American agriculture declines at nearly 12%. This geographic arbitrage—the ability to offset weakness in one region with strength in another—is precisely what Mogens Bay built the global footprint to achieve decades ago.

As the global leader in center pivot irrigation, our expertise with agricultural productivity and smart technology will help growers feed the world more efficiently.

Global Footprint

We manufacture products in 84 facilities spread across six continents, and we do business in 21 different countries.

This global manufacturing footprint creates procurement advantages, localized production efficiencies, and—critically—tariff mitigation capabilities. Notably, Valmont manufactures the majority of its U.S.-bound products across 24 domestic facilities.

XI. Playbook: Business & Investing Lessons

1. The Power of Patent Acquisition

Daugherty's acquisition of the Zybach patent for a 5% royalty (expiring in 1969) created a multi-billion dollar franchise. He didn't invent center pivot irrigation—he recognized its potential, secured the rights, and spent 15 years improving the technology while competitors were locked out. The lesson: Sometimes the best innovation strategy is buying the right to innovate on someone else's foundation.

2. Survive the Commodity Bust

More than 80 competitors entered the center pivot market after the patent expired. Almost all failed. Valmont survived through diversification, scale economics, and continuous engineering improvement. The lesson: Being first matters, but surviving industry shakeouts requires disciplined capital allocation and diversification.

3. Core Competency Transfer

Steel fabrication skills applied across agriculture → infrastructure → telecom → solar (and back out of solar when returns weren't adequate). The Daugherty principle—"New business development will occur only in those areas where we can capitalize on our existing channels of distribution, market knowledge, and investments"—proved remarkably durable.

4. Geographic Arbitrage in Agriculture

International markets currently offsetting North American cyclicality demonstrates the value of global footprint. When one region's farmers struggle, another region's farmers may be investing.

5. Hardware to Software Evolution

The Prospera acquisition demonstrates how industrial companies can evolve toward software-as-a-service models. The "try-before-you-buy" partnership model reduced risk while validating technology.

6. Capital Allocation Discipline

The 50/50 split between growth investment and shareholder returns, combined with the $700 million buyback authorization and consistent dividend increases, signals management confidence and capital discipline. Valmont maintained a balanced approach to capital allocation in Q2 2025, with approximately 50% directed toward growing the business and 50% returned to shareholders. The company invested $32 million in capital expenditures during the quarter while returning $13.6 million to shareholders through dividends. Share repurchases were particularly robust, with the company buying back $100 million of shares at an average price of $279.35 per share.

7. The "Boring" Business Advantage

Utility poles and irrigation equipment aren't exciting. They don't generate viral tweets or attract CNBC coverage. But they're essential—and essential businesses often compound quietly while flashier stories capture attention.

8. Founder Culture Persistence

Nearly 80 years after founding, Valmont remains headquartered in Omaha. The Daugherty Foundation carries forward the founder's philanthropic vision. Key executives reference the company's values and culture. Institutional memory and culture can be durable competitive advantages.

XII. Porter's 5 Forces Analysis

| Force | Assessment | Key Factors |

|---|---|---|

| Threat of New Entrants | LOW | Only a handful of center pivot companies remain after 80+ tried and failed. High capital requirements for manufacturing, established relationships with utilities, and decades of engineering expertise create significant barriers. |

| Supplier Bargaining Power | MODERATE | Steel is a commodity, but specialized galvanizing and coating capabilities reduce dependency. Vertical integration in coatings provides some insulation from supplier power. |

| Buyer Bargaining Power | MODERATE-HIGH | Large utility companies and agricultural cooperatives have negotiating leverage, but Valmont's global scale and service capabilities create switching costs. Long-term relationships matter. |

| Threat of Substitutes | LOW | It has been said the center pivot irrigation machine is "perhaps the most significant mechanical innovation in agriculture since the replacement of draft animals by the tractor." For infrastructure, utility poles and transmission structures have no practical substitutes. |

| Competitive Rivalry | MODERATE | In irrigation, a concentrated oligopoly of Nebraska-based manufacturers (Valmont, Lindsay, Reinke, T-L). In infrastructure, more fragmented but Valmont's scale provides advantages. Valmont Industries is a pioneer in the field of center pivot irrigation system. |

XIII. Hamilton's 7 Powers Analysis

| Power | Assessment | Evidence |

|---|---|---|

| Scale Economies | ✅ STRONG | We manufacture products in 84 facilities spread across six continents, and we do business in 21 different countries. This global manufacturing footprint creates procurement advantages and localized production efficiencies that smaller competitors cannot match. |

| Network Effects | 🔶 MODERATE | The dealer network (270 dealers in North America, 270 internationally) creates distribution advantages. AgTech platform adoption may eventually create data network effects. |

| Counter-Positioning | 🔶 MODERATE | Valmont's integrated hardware + software + service model (particularly with Prospera) creates a value proposition that pure hardware or pure software competitors struggle to replicate. |

| Switching Costs | ✅ STRONG | Installed base of irrigation equipment creates aftermarket parts and service revenue streams. Utility customers with long infrastructure lifecycles have high switching costs. |

| Brand | ✅ STRONG | Valley Irrigation is the oldest and most recognized brand in center pivot. Utilities have multi-decade relationships with Valmont's infrastructure products. |

| Cornered Resource | 🔶 MODERATE | Engineering expertise accumulated over 70+ years is difficult to replicate, but not truly "cornered." |

| Process Power | ✅ STRONG | Galvanizing processes, high-precision welding for steel transmission poles, and automated production lines represent accumulated manufacturing know-how. |

XIV. Bull Case vs. Bear Case

Bull Case:

- Infrastructure Super-Cycle: Grid modernization, electrification, renewable integration, and 5G deployment create sustained demand for Valmont's core products over the next decade+.

- Water Scarcity Tailwind: Climate change increases demand for efficient irrigation globally, driving adoption of center pivot systems in new markets.

- Restructuring Benefits: Exit from unprofitable solar business and organizational streamlining should improve margins and ROIC as charges normalize.

- AgTech Optionality: Prospera acquisition positions Valmont for hardware + software + service recurring revenue model.

- Capital Return: $700 million buyback at ~10% of market cap plus growing dividend signals management confidence.

- Valmont aims to increase sales by $500 million to $700 million and boost EPS by $7 to $12.

Bear Case:

- Steel Price Volatility: As a steel fabricator, Valmont is exposed to raw material price swings that can compress margins.

- Agricultural Cyclicality: Despite diversification, ~27% of revenue remains tied to highly cyclical agricultural equipment demand.

- Tariff Exposure: International manufacturing and steel sourcing create tariff uncertainty, though domestic manufacturing mitigates some risk.

- North American Agriculture Weakness: Continued softness in North American agricultural markets (down 11.7% in recent quarter) may persist.

- Technology Integration Risk: Successfully scaling AgTech/Prospera technology while maintaining hardware quality is not guaranteed.

XV. Key Performance Indicators for Investors

1. Utility Backlog and Order Trends The single most important leading indicator for Valmont's largest growth driver. Monitor utility backlog levels, order growth rates, and utility capital expenditure announcements. Strong backlog indicates future revenue visibility.

2. Operating Margin by Segment As Valmont exits low-margin businesses (solar) and focuses on higher-return markets, operating margin improvement should materialize. Watch for Infrastructure segment margins approaching management's long-term targets.

3. International Agriculture Growth Rate International agriculture sales growing at 22% vs. North American declines of 12% demonstrates geographic arbitrage working. Sustained international momentum offsets domestic cyclicality.

XVI. Conclusion: The Hidden Giant's Next Chapter

In 1946, Robert Daugherty invested $5,000 in a Nebraska machine shop. In 2025, Valmont Industries operates 84 manufacturing facilities across six continents, employs 11,000 people, generates over $4 billion in annual revenue, and commands a market capitalization exceeding $8 billion.

The company has survived agricultural booms and busts, outlasted 80+ competitors in the center pivot market, diversified from irrigation into infrastructure, expanded from Nebraska to the world, and now stands at the intersection of physical infrastructure and digital technology.

Why am I so confident about our future? Let me just share a little bit of the groundwork. Those were CEO Applbaum's words at a recent investor conference. The confidence stems from Valmont's positioning at the intersection of multiple secular trends: grid modernization, 5G deployment, electrification, water scarcity, and precision agriculture.

The company remains, as Applbaum puts it, "this hidden gem"—a critical infrastructure provider that most investors have never heard of, even as they encounter its products every day. The green circles visible from space? Valmont. The utility poles carrying power to your home? Often Valmont. The cell towers enabling your mobile connection? Frequently Valmont.

Frank Zybach invented center pivot irrigation with a seventh-grade education and a blacksmith's intuition. Robert Daugherty recognized its potential and built a company. Mogens Bay took it global. Avner Applbaum is now transforming it into an "Industrial Tech company" capable of delivering both hardware and software solutions.

Nearly 80 years after its founding, Valmont remains headquartered in Omaha, still rooted in its Midwestern values, still solving critical challenges in infrastructure and agriculture. The $5,000 bet has paid off spectacularly—and the next chapter is still being written.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube