Nebius Group: From Russia's Google to the New AI Infrastructure Giant

Introduction: A Phoenix From Geopolitical Flames

In the summer of 2024, a remarkable scene unfolded in Amsterdam's financial district. Arkady Volozh, the Kazakhstan-born founder who had spent 25 years building Russia's most valuable technology company, sat in an office that bore no trace of his past. Gone were the Yandex logos, the Cyrillic scripts, the connections to Moscow. In their place stood something entirely new: Nebius Group, a company betting everything on the insatiable global appetite for artificial intelligence infrastructure.

The central question is extraordinary: How did the founders of Russia's greatest tech company, forced to give up that business and start again almost from scratch, come to announce a $20 billion deal with Microsoft just over 12 months later—one that has seen the company surge past Yandex in terms of overall value?

Shares of artificial intelligence infrastructure firm Nebius Group soared nearly 50% after the company disclosed a multi-billion-dollar deal with Microsoft. The Amsterdam-based firm announced it had struck a multi-year deal with Microsoft worth up to $19.4 billion to provide cloud computing power for AI workloads.

The numbers tell a staggering resurrection story. Nebius Group N.V. has emerged as a standout AI/cloud hyperscaler, surging 211% year-to-date, making it one of the best-performing technology stocks of 2025. As of late November 2025, the company commands a market cap of approximately $22 billion—a valuation built in barely eighteen months from the ashes of a company that lost 80% of its value overnight when Russia invaded Ukraine.

This is not merely a corporate turnaround story. It's a tale of reinvention at the intersection of geopolitics, the AI infrastructure gold rush, and founder perseverance. And it begins, as so many great technology stories do, with two childhood friends and an improbable dream.

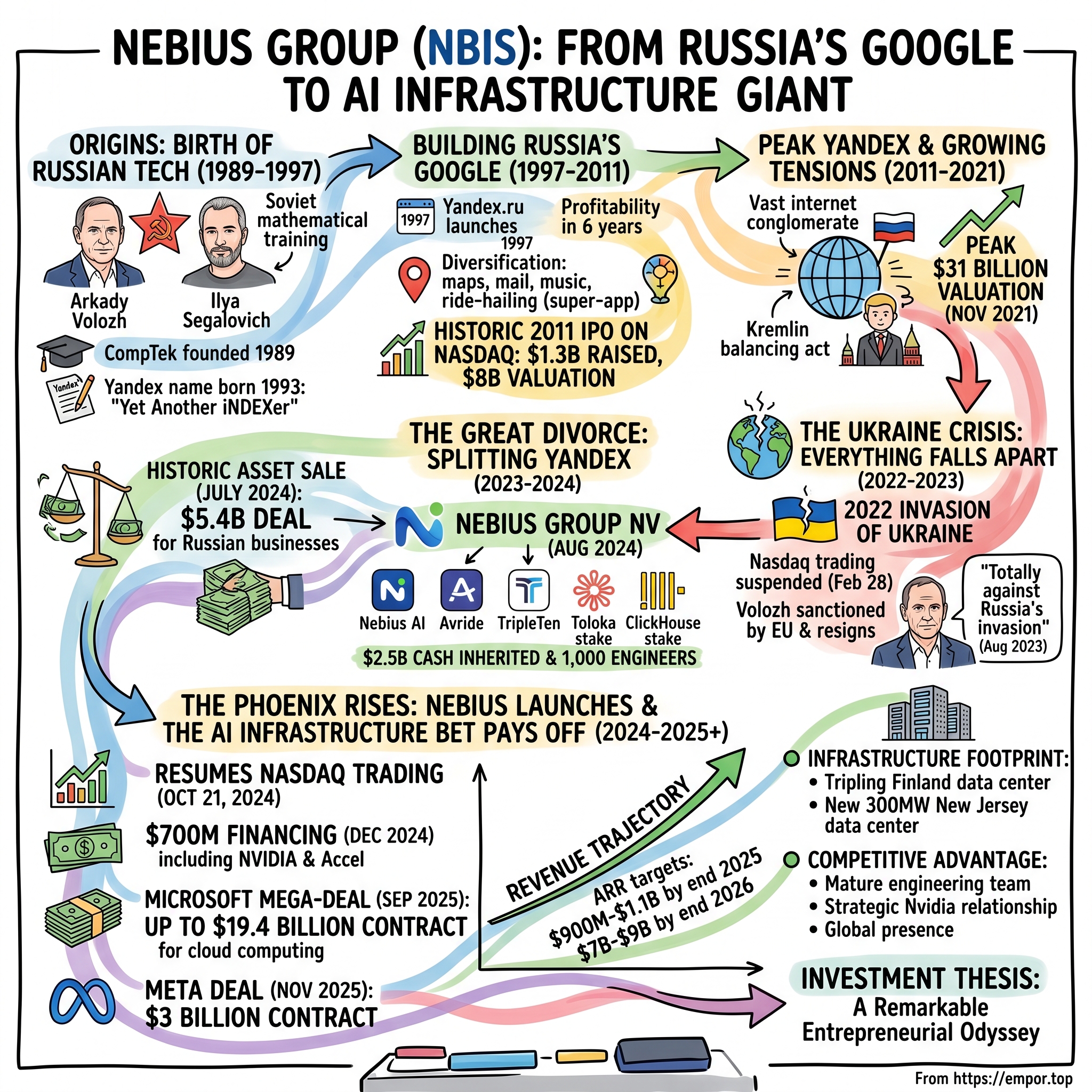

Origins: The Birth of Russian Tech (1989–1997)

The Founder's Journey: From Soviet Kazakhstan to Moscow's Tech Scene

In a sprawling oil town on the western edge of Soviet Kazakhstan, a child who would one day become one of Russia's most consequential technology entrepreneurs was absorbing two very different worlds. Arkady Yuryevich Volozh was born in 1964 in Guryev (now Atyrau, Kazakhstan) into a Russian-Jewish family. His father was a petroleum geologist, his mother a music teacher. He attended the Republican School of Physics and Mathematics in Almaty, Kazakhstan, and then studied applied mathematics at Gubkin Russian State University of Oil and Gas in Moscow, graduating in 1986.

The intersection of rigorous mathematical training and an oil-industry background would prove prophetic. Volozh learned to think about complex systems—how to extract value from vast quantities of unstructured data, whether geological formations or digital information. But what truly shaped his future was a friendship forged in the mathematics classrooms of Almaty.

Ilya Segalovich, born in 1964 in Gorky (now Nizhny Novgorod) into a Russian-Jewish family, graduated from the same Republican School of Physics and Mathematics in Almaty, Kazakhstan. The two boys—"equally precocious youngsters," as contemporaries described them—formed a bond that would survive the collapse of the Soviet Union and fuel one of the greatest entrepreneurial partnerships in Russian history.

Early Entrepreneurship in Post-Soviet Russia

The late 1980s were a time of unprecedented chaos and opportunity in the Soviet Union. Mikhail Gorbachev's reforms had opened the door to private enterprise, and young technologists saw possibilities that had been unimaginable to their parents. After working at a state pipeline research institute, Volozh started a small business importing personal computers from Austria. He went on to co-found several IT enterprises, including a Russian provider of wireless networking technology InfiNet Wireless and CompTek International, one of the largest distributors of network and telecommunications equipment in Russia. Volozh co-founded CompTek in 1989.

But Volozh was not content merely selling hardware. He also started working on search in 1989, which led to him establishing Arkadia Company in 1990. The company was developing search software. In 1993, Arkady Volozh and Ilya Segalovich developed a search engine for "non-structured information with Russian morphology."

This was not a trivial technical challenge. The Russian language, with its complex inflections and morphological variations, presented problems that Western search engines simply could not solve. One thing computer scientists noted was that Yandex at least matched Google and perhaps was far ahead of Google in terms of using machine learning to understand conjugation, tenses, and cases—things that have a major impact on the meaning of words in Russian text.

The Yandex Name is Born

In 1990, Arkady Volozh contacted Ilya Segalovich, a friend of his from high school, to join his venture developing algorithms to search Russian texts. They developed search software together under the company name Arcadia. In 1993, they invented the name "Yandex" as an easy way to remember "Yet Another iNDEXer." This is also a bilingual pun on "index" since "Я" ("ya") means "I" in Russian.

Segalovich and Volozh started Yandex more than 20 years ago, first as a search engine that indexed the Bible and rapidly ramping it up to cover other searching. The linguistic sophistication that set Yandex apart from its competitors was not a marketing gimmick—it was fundamental to making search work in a language that defeated Western algorithms.

The pair headed to Moscow for college and after graduation started a series of small IT companies in the 1990s, "tinkering" with "the possible but unproven commercial potential of the internet." Volozh likes to boast that their first search engine went live in September 1997, almost a year before Google.

This timing would prove crucial. While the world celebrated Google's emergence in 1998, Russia already had a homegrown search champion—one that understood its language, its users, and its market in ways that no American competitor could match.

Building Russia's Google (1997–2011)

The Launch of Yandex.ru

Yandex was founded by Arkady Volozh and launched its first product, a search engine, in 1997. In the frenetic atmosphere of the late-1990s dot-com boom, two Russian mathematicians bet their careers on the idea that search could be a business. When they launched Yandex.ru in September 1997, the company had revenue of under $100,000 and a handful of employees.

The timing was fortuitous. Russia's economy was still reeling from the Soviet collapse, but a new generation of urban Russians was discovering the internet. They needed a search engine that understood their language—and Yandex delivered.

Scaling the Business

The company's early growth required capital, and in 2000, Volozh made a decision that would shape Yandex's future. In 2000, Baring Vostok Capital Partners acquired 35.72% of the company for $5.28 million. This investment, from one of Russia's most respected private equity firms, provided both capital and credibility.

In 2001, Yandex launched the Yandex. Direct online advertising network. The company became profitable in 2003. This was a remarkable achievement—profitability in just six years, well ahead of many Western internet companies that burned through billions before turning a profit.

What made Yandex special was its refusal to remain merely a search engine. Lately Volozh had begun "tiptoeing westward" in a bid to make the firm less reliant on its Russian business—and on the whims of Vladimir Putin. Yandex formed a joint venture with Uber and launched delivery services in London and Paris. But its most showy project was a Michigan-based self-driving car trial launched in partnership with Grubhub.

The company expanded into maps, mail, music streaming, ride-hailing, food delivery, and e-commerce—becoming, in effect, Russia's answer to Google, Uber, Spotify, and Amazon combined. Starting as a search engine—more widely used in Russia than Google—it added e-commerce, ride-hailing, music streaming and much more. When Vladimir Putin visited Yandex's Moscow office for its 20th anniversary, in 2017, Volozh showed off the company's self-driving car.

The Historic IPO

On May 24, 2011, the holding company that owned Yandex, Yandex N.V. (now called Nebius Group), raised $1.3 billion in an initial public offering on NASDAQ, the biggest initial public offering for a dot-com company since Google's offering in 2004. At that time, Baring Vostok Capital Partners owned a 35% stake in the company and Tiger Technologies owned a 15% stake.

Yandex NV, owner of Russia's most popular Internet search engine, jumped 55 percent in Nasdaq trading after raising $1.3 billion in an initial public offering that sold above the proposed price range. The shares rose $13.84 to $38.84. The Moscow company sold 52.2 million shares, or a 16.2 percent stake, at $25 each, valuing the company at about $8 billion. Tuesday's premiere for Yandex, which has almost triple Google's market share in Russia, is the biggest technology IPO worldwide in 2011.

After pricing its IPO at $25 per share, the Russian search giant's share price jumped close to 40% immediately after its flotation. The price per share opened at $35, giving Yandex a market cap of roughly $11.2 billion at its debut. That means its value far surpassed that of LinkedIn, which went public that week. An IPO at $25 per share would have already valued Yandex at more than 500 times its worth when investors bought into the company back in 2000.

For investors who had backed Baring Vostok's $5.28 million bet in 2000, the returns were staggering. For Volozh and Segalovich, it represented vindication of their two-decade bet on Russian technology. And for Russia, it demonstrated that the country could produce global technology champions.

Peak Yandex & Growing Tensions (2011–2021)

Expansion and Diversification

The years following the IPO were a period of extraordinary expansion. Volozh co-founded Yandex—initially Russia's answer to Google, but what became a sprawling internet conglomerate covering taxis, e-commerce and payments—back in the 1990s. He led the company through massive growth and expansion, before stepping back from operational management in 2014.

The company built what technology journalists came to call a "super-app"—a single ecosystem that Russians used for everything from hailing rides to ordering food to streaming music. By the early 2020s, Yandex had become indispensable to Russian daily life.

But the company's success came with complications. Due to its significant media activities in Russia, the company has long faced pressure for control by the government of Russia. Operating an independent media and technology business in Putin's Russia required a delicate balancing act.

The Kremlin Balancing Act

Volozh clearly has skills in diplomacy—mastering the "high-wire act" of running an independent business while remaining on the right side of the Kremlin.

This was not merely diplomatic politeness. Yandex controlled the news that Russians saw, the rides they took, the deliveries they received. In a country where information was power, a company with Yandex's reach was inherently political.

Around 2019, Volozh pretty much stopped visiting Russia, but remained on the Yandex payroll both through his shares and as CEO. Within three months of Russia's invasion of Ukraine, he was sanctioned by the EU and quit. The invasion and sanctions effectively killed Volozh's long-term dream of using Yandex to build a major international tech business.

Over the period from 2000 to 2014, Volozh served as CEO of Yandex. Later, he stepped down as CEO and became the head of the Yandex Group with a seat on the company board. This transition was telling—Volozh was already positioning himself at arm's length from day-to-day operations in Russia.

The $30 Billion Peak

Yandex's core market was very much its domestic Russia plus a handful of neighboring countries, however its parent was a Dutch holding organization called Yandex N.V. which went public on the Nasdaq in 2011, followed by a secondary listing three years later on the Moscow Exchange. Yandex N.V. was doing well as a public company, reaching a valuation of $31 billion at the end of 2021 before the Russia-Ukraine conflict kickstarted a series of global sanctions.

Yandex had been performing well as a public company, hitting a peak market cap of $31 billion in November 2021.

At that moment, Arkady Volozh was one of Russia's richest men, with a net worth measured in billions. His company employed tens of thousands of people. His search engine was used by more than 60% of Russian internet users. And everything was about to collapse.

The Ukraine Crisis: Everything Falls Apart (2022–2023)

Invasion and Immediate Fallout

On February 24, 2022, Russian forces crossed the border into Ukraine. Within days, the world that Arkady Volozh had spent 25 years building began to disintegrate.

The Nasdaq Stock Market announced that trading would resume in Nebius Group N.V. (formerly Yandex) at 9:00 a.m. Eastern Time on October 21, 2024. Trading in the company's stock was halted on February 28, 2022 at 6:38 a.m. Eastern Time under its former name and symbol, Yandex N.V.

It took Arkady Volozh 20 years to build Yandex into Russia's Google, Uber, Spotify and Amazon combined—and just 20 days for "everything to crumble." The invasion saw Yandex's stock plunge by 80%, and the NASDAQ suspended its stock trading in March 2022.

For shareholders, the halt was devastating. For Volozh personally, it was catastrophic. His net worth, which was based mainly on the value of his stake in Yandex, plummeted from a high of $2.6 billion to $580 million, according to Forbes.

Sanctions and Resignation

Yandex co-founder and CEO Arkady Volozh was forced to resign after the European Union placed him on a sanctions list, although he was removed from the list in March 2024, which paved the way for his return as CEO of the next version of Yandex N.V.

The EU's stated reasons were that Volozh was a "leading businessperson involved in economic sectors providing a substantial source of revenue to the Government of the Russian Federation." The reasons cited by the EU for sanctioning Volozh included that Russian State-owned banks such as Sberbank and VTB were shareholders and investors in Yandex. These reasons were called "poor and dubious" by Anders Åslund, and Gerhard Mangott commented that "It is hard to understand what Volozh is being accused of."

In contrast to the EU, the US and the UK never sanctioned Volozh. This asymmetry would later prove crucial to his ability to rebuild.

The Controversial Condemnation

For eighteen agonizing months, Volozh remained silent about the war. Then, in August 2023, he broke his silence.

In August 2023, Volozh announced that he was "totally against Russia's barbaric invasion of Ukraine, where I, like many, have friends and relatives. I am horrified by the fact that every day bombs fly into the homes of Ukrainians." He also stated that although he moved to Israel in 2014, he has to take his share of responsibility for Russia's actions. By the time of his announcement, Volozh was only the second sanctioned Russian businessman to take a stance against the invasion.

Why had it taken so long? In January 2025, Volozh said that it took 18 months to issue a statement on the war because he first needed to relocate 1,000 Yandex employees who wanted to leave Russia.

This detail reveals both Volozh's sense of responsibility to his people and the impossible position he faced. Speaking out earlier might have trapped employees in Russia, unable to escape. Waiting allowed hundreds of engineers and their families to reach safety—but at enormous personal and reputational cost.

Fighting Delisting

While the Nasdaq had said in 2022 that it would delist Yandex and several other Russian-affiliated companies, Yandex successfully appealed the ruling. The company fought to maintain its listing—a crucial strategic decision that would later enable Nebius to return to public markets without the complications of a new IPO.

Yandex had already been divesting some of its properties, including selling its news service to a rival with close ties to the Russian State. The company announced plans for a corporate restructuring to further distance itself from its Russian roots. Yandex had also said previously that it would re-brand its Dutch holding company.

The path forward was clear: to survive, Yandex N.V. would have to become something else entirely.

The Great Divorce: Splitting Yandex (2023–2024)

The Historic Asset Sale

Dividing a $30 billion technology conglomerate across geopolitical fault lines while satisfying the demands of the Kremlin, Western sanctions authorities, and thousands of minority shareholders was an exercise in corporate complexity that few companies have ever attempted.

Yandex and the Kremlin had been engaged in negotiations for around 18 months to try and spin off Yandex's Russian businesses from its Dutch parent company, Yandex NV.

A deal to split the assets of Russian technology company Yandex was finalized on July 15, with a Russian consortium of investors buying the bulk of Yandex's businesses in a cash and shares deal worth around $5.4 billion. The split marks the end of foreign ownership in Yandex, often dubbed "Russia's Google," while potentially tightening the Kremlin's control of the Internet space in Russia. The move is the largest corporate exit from Russia since Moscow invaded Ukraine over two years ago.

The deal, encompassing the divestiture of all Yandex N.V.'s ventures in Russia and several adjacent markets, was pegged at approximately 475 billion rubles ($5.2 billion), which was about half the Netherlands-based firm's market value. This considerable discount stems from a Russian regulatory mandate requiring sales of Russian assets by entities based in nations labeled as "unfriendly" by Moscow to be conducted at a minimum discount of 50 percent.

The publicly identified investor group includes Alexander Chachava (25%), Pavel Prass (15%), Lukoil (15%), Alexander Ryazanov (10%), and senior management (35%). However, it is speculated that the publicly identified owners are intermediaries for others.

Birth of Nebius

The company was formerly known as Yandex N.V. and changed its name to Nebius Group N.V. in August 2024. Nebius Group N.V. was founded in 1989 and is headquartered in Amsterdam, the Netherlands.

Four AI-focused businesses in cloud, data labeling, self-driving cars and education technology are being retained by YNV and will be developed under the Nebius Group name.

A two-year saga of how to divide up Yandex's assets and extricate Volozh from the Russian business wrapped up with him becoming CEO of Nebius Group, technically the rump holding company that previously owned Yandex. It retained the Netherlands-based headquarters and the rights to develop four Yandex business lines internationally. The biggest of those became Nebius AI, based on Yandex's cloud technology.

What Nebius Kept

In essence, it started by selling AI developers access to computing power from Yandex's former data center in Finland, which Volozh inherited. It gave the firm a nice starting point, but to become a base for specialized services, the center had to be both greatly expanded and almost entirely reequipped.

Nebius Group N.V., headquartered in Amsterdam, is a technology company that provides artificial intelligence infrastructure. The company also owns Avride and TripleTen, as well as stakes in Toloka and ClickHouse. It is headquartered in Amsterdam with offices in Israel and the United States.

After the sale, Yandex NV would be left with its international businesses—employing 1,300 people—including self-driving technology and generative artificial intelligence as well as a data center in Finland.

The rump company inherited approximately $2.5 billion in cash from the sale, a Finnish data center, a handful of promising AI-adjacent businesses, and—perhaps most importantly—a team of approximately 1,000 engineers who had chosen to leave Russia and build something new.

The Phoenix Rises: Nebius Launches (July–October 2024)

The "Startup with $2.5 Billion"

When Arkady Volozh describes Nebius, he uses language that would seem paradoxical for a publicly traded company. Nebius, the European AI infrastructure company formerly known as Yandex, has raised $700 million in financing to power its U.S. expansion. The financing came from "dozens of very well-known investors," Nebius CEO Arkady Volozh told TechCrunch during a press briefing.

"It's like a startup because we are 'starting up,' but it's an unusually big one," Volozh explained. What made Nebius unique was the combination of startup agility with public-company resources. Of the company's 1,300 employees, around 1,000 of them were engineers, mostly transitioning from the old Yandex business. "Technologically, this is what this whole team has been doing for the past 15 to 20 years," Volozh noted. "They have built pretty large infrastructure globally, with hundreds of megawatts of data centers."

When this story began, the infrastructure market for AI was only just forming. Volozh was smart, because he could feel where it was moving ahead of time: he could see that there would be huge demand for computing power, and that it would keep growing.

Return to Nasdaq

Nebius Group N.V. announced that it had been informed by The Nasdaq Stock Market LLC that trading in the Company's Class A ordinary shares was scheduled to resume on Monday October 21, 2024.

Nebius, the company formerly known as Yandex that's now focused on cloud infrastructure for AI uses, began trading on the public markets once again—more than two years after the Nasdaq halted trading due to economic sanctions. The Netherlands-based company is vying to become one of Europe's leading players in the burgeoning "GPU-as-a-service" space, and sits in a somewhat unique position—it is a startup in many ways as it's starting out afresh as a new business, but being a public company means that anyone can invest in it.

After some early turbulence, the company's shares bounced back, closing 5.6% higher on Monday, marking its first trading day since February 2022. Despite a rocky start where shares dropped 26% in pre-market trading, they ended the day with a solid gain, closing at $20 per share—above their pre-suspension price of $18.94.

The company had annualized run-rate revenue of $120 million as of September 30, 2024, and expected to be on track for $170 million to $190 million in annualized run-rate revenue by year end 2024.

The AI Infrastructure Bet Pays Off (2024–2025)

Nvidia Investment and Strategic Positioning

The private placement saw Nebius issue 33.3 million Class A shares at $21, implying a 3% premium on the stock's average price since trading resumed in October. The fundraise came some six weeks after Nebius resumed trading on the Nasdaq.

Nebius Group N.V., a leading AI infrastructure company, announced that it had entered into definitive agreements for a USD 700 million private placement financing from a select group of institutional and accredited investors, including participation from Accel, NVIDIA, and certain accounts managed by Orbis Investments.

The next best performer in Nvidia's holdings is AI cloud computing company Nebius. Since the end of Q1, the value of Nvidia's Nebius holdings has risen about 140%. While the $60 million stake is much smaller than Nvidia's stake in CoreWeave, Nebius is not like other startups.

In October 2024, Nebius became a preferred cloud service provider in the NVIDIA Partner Network, gaining access to advanced GPU technology, including the latest H100 and H200 Tensor Core GPUs.

The Microsoft Mega-Deal

On September 8, 2025, Nebius announced the deal that transformed its trajectory.

The deal will be worth $17.4 billion through 2031 to Nebius, which counts the likes of Nvidia and Accel as investors. Microsoft may also acquire additional computing capacity under the arrangement, boosting overall contract value to $19.4 billion.

Under this multi-year agreement, Nebius will deliver dedicated capacity to Microsoft from its new data center in Vineland, New Jersey starting later this year.

Microsoft's deal with neocloud company Nebius Group NV will provide computing power to internal teams creating large language models and a consumer AI assistant. The arrangement, which is worth as much as $19.4 billion, sparked a rally in Nebius shares. As part of the deal, Microsoft will get access to more than 100,000 of Nvidia Corp.'s latest GB300 chips.

Nebius shares climbed 60% Monday in extended trading and continued to surge Tuesday amid investor excitement over the deal.

Nebius Group plans to raise $3 billion in convertible notes and equity to help it expand in the wake of a major deal to provide artificial intelligence infrastructure to Microsoft. The new financing includes $2 billion in convertible notes as well as $1 billion in new shares, the Amsterdam-based company said. The funds will be used to buy land and computing power.

The Meta Deal

The company announced a new deal to provide $3 billion worth of AI infrastructure over five years to Meta Platforms, which has been investing heavily to ramp up its own AI infrastructure, including its Llama large language model, AI-based advertising products, and customer-facing AI features such as Meta AI.

The Meta agreement represents the second major hyperscaler contract for Nebius following its $17.4 billion deal with Microsoft announced in September. These partnerships underscore how even technology giants struggle to secure sufficient computing capacity to meet their AI ambitions. Nebius indicated it would deploy the necessary capacity for the Meta contract within the next three months. Company officials noted that demand proved so intense that they had to limit the contract size to match available capacity.

Revenue Trajectory

Nebius reported revenues of $146.1 million for the third quarter, up 355% from a year ago. In the first nine months of the year, Nebius's revenue is up 437%, from $56.3 million in 2024 to $302 million in the first three quarters of 2025.

Nebius believes it will have between $7 billion and $9 billion in annualized run rate revenue by the end of 2026, which would be a massive jump.

The company's guidance represents a stunning projection: from roughly $500 million in annualized revenue at the end of 2025 to potentially $9 billion by the end of 2026—an 18x increase in a single year if management hits the top end of its range.

The Nebius Business Model Deep Dive

Core AI Infrastructure Business

Nebius' core business is an AI-centric cloud platform built for intensive AI/ML workloads. With proprietary cloud software architecture and hardware designed in-house (including servers, racks and data center design), Nebius provides AI and ML practitioners the compute, storage, managed services and tools they need to build, tune and run their models.

Nebius and CoreWeave might seem similar, but their business models are different. Nebius is a "full stack" AI infrastructure company that plugs its cloud-based GPUs into managed services like Kubernetes and PostgreSQL. CoreWeave mainly processes GPU-intensive workloads instead of handling smaller managed services.

Nebius offers two core services: Nebius AI Cloud and Nebius AI Studio. The flagship product, Nebius AI Cloud, is a full-stack platform purpose-built for AI training, inference, and data-heavy processing. It competes directly with Lambda, CoreWeave, Paperspace, Vultr, TogetherAI, DeepInfra, and hyperscalers like AWS, GCP, Azure, and Oracle. Mistral, JetBrains, Brave, Behavox, Converge, and others already rely on Nebius to power their AI infrastructure.

The Portfolio of Businesses

As well as its core AI infrastructure business, Nebius Group includes other companies growing under distinctive individual brands. Avride develops autonomous cars and delivery robots for sectors such as ride-hailing, logistics, e-commerce, and food and grocery delivery. Avride's highly experienced team has deployed and operated its autonomous driving solutions in many different contexts. TripleTen is a leading edtech platform, specializing in reskilling and upskilling individuals for successful careers in tech.

Nebius announced a strategic investment in Toloka, its AI data solutions business, led by Bezos Expeditions (the investment arm of Jeff Bezos) with participation from Mikhail Parakhin, CTO of Shopify. The investment marks a pivotal step in Toloka's evolution, and will enable the company to scale rapidly amid accelerating global demand for reliable, high-quality AI data solutions.

Both Toloka and Avride could eventually follow a similar path to that of ClickHouse, creators of the eponymous open source database management system that spun out of Yandex in 2021. While the commercial ClickHouse entity secured big-name backers such as Index Ventures, Benchmark Capital, and Coatue, Nebius has retained a minority stake. "ClickHouse became very popular, and we were approached by investment funds to create a business around the open source project. Now they have revenues, and they're growing," Volozh said.

Infrastructure Footprint

Nebius only owns a single data center in Finland, but it leases additional data centers through colocation deals in Missouri, France, and Iceland. It's building its second first-party data center in New Jersey, and it recently signed another colocation deal in the United Kingdom. CoreWeave operates 33 first-party data centers across the U.S. and Europe.

Nebius announced that it will triple the capacity of its data center in Mäntsälä, Finland. The current expansion phase will enable Nebius to place up to 60,000 GPUs at the Mäntsälä location alone, with annual revenue potential of over USD 1 billion at full capacity utilization. The expansion of the Finnish data center is part of Nebius's program to invest more than USD 1 billion in AI infrastructure in Europe by mid-2025.

The data center that Nebius has commissioned in New Jersey will be built to Nebius's own design, enabling the company to achieve maximum efficiency and offer superlative performance to customers. The facility is a phased development expandable up to a total capacity of 300 MW, with the first capacity expected to be completed as early as summer 2025. This delivers on the company's previous guidance for 100 MW of installed capacity by the end of 2025.

Competitive Landscape: The Neocloud Wars

The Emerging Neocloud Category

The term "neocloud" has emerged to describe a new category of cloud infrastructure providers that specialize in GPU-focused services for AI workloads. CoreWeave, Inc. and Nebius Group N.V. are emerging AI-focused cloud infrastructure providers positioning themselves as agile alternatives to traditional hyperscalers like Amazon Web Services and Azure, aiming to capitalize on the growing demand for AI cloud solutions. The rapid proliferation of AI is transforming the entire tech scene, and AI infrastructure has become a high-stakes battleground for tech companies. Per an IDC report, spending on AI infrastructure is expected to top $200 billion by 2028.

As AI computing demands continue to rise, companies and cloud providers often turn to GPU rentals when their own resources fall short. "AI Neocloud" emerged in response to this trend. This new cloud service provider specializes in AI-focused solutions, prioritizing GPU-centric data centers. According to Grand View Research, the GPU-as-a-Service market is projected to grow at a compound annual rate of 22.9% over the next five years. The leading Neocloud providers currently include CoreWeave, Crusoe, Nebius, Lambda Labs, and Applied Digital.

CoreWeave: The Primary Competitor

In terms of scale, CoreWeave significantly outpaces Nebius, with approximately 10 times more GPUs. CoreWeave has contracted 1.6GW of power, about four times its current operational capacity. However, Nebius is also expanding rapidly. Their 2025 target is 35,000-60,000 GPUs, with a mid-term goal of 240,000 GPUs, requiring 240MW of power.

CoreWeave's 77% of total revenues in 2024 came from the top two customers. This intense customer concentration is a major risk, especially if the client migrates—the revenue impact could be material.

CoreWeave and Nebius are two key players in the emerging GPU cloud industry. While CRWV has significant earnings headwinds and offers a more 'bare metal' approach, NBIS's clean balance sheet, solid outlook, and vertical product stack should produce outperformance.

Differentiation Strategy

Nebius is focusing on building a global footprint, with capacity in the United States, Europe, and the Middle East. It added three new regions, including a strategic data center in Israel. Like CoreWeave, NBIS' partnership with NVDA (also an investor in the company) is another plus. Nebius will be one of the first AI cloud infrastructure platforms to offer the NVIDIA Blackwell Ultra AI Factory Platform.

Nebius, a cloud computing company with roots in Europe, is also targeting the growing demand for AI infrastructure. Its strategy focuses on diversifying its customer base and maintaining a more balanced approach to financing. Nebius recently gained credibility with a 17.4 billion dollar agreement with Microsoft.

Investment Thesis: Bull and Bear Cases

The Bull Case

1. Proven Infrastructure Expertise The Nebius team built one of the world's largest technology companies over 25 years. Nebius is an international company headquartered in the Netherlands, with engineering hubs in Finland, Serbia and Israel. 500+ professionals: the mature team of engineers has a proven track record in developing sophisticated cloud and ML solutions and designing cutting-edge hardware.

2. Massive Contracted Revenue With the Microsoft deal worth up to $19.4 billion through 2031 and the Meta deal worth $3 billion over five years, Nebius has secured over $22 billion in contractual commitments from two of the world's largest technology companies—a remarkable achievement for a company that barely existed eighteen months ago.

3. Strategic Nvidia Relationship Nebius benefits from long-standing relationships in the industry, most notably with Nvidia. As one of Nvidia's largest European clients during the Yandex era, Nebius leveraged that partnership to deploy state-of-the-art GPU clusters. This relationship proved instrumental during Nebius's recent $700 million private placement, as Nvidia elected to directly invest in Nebius.

4. Explosive Growth Trajectory Nebius posted 385% year-over-year revenue growth in the first quarter of 2025, driven by accelerating demand for its AI infrastructure services.

The Bear Case

1. Profitability Remains Distant Despite its exceptional top-line growth, NBIS remains unprofitable, with management reaffirming that adjusted EBITDA will be negative for the full year 2025. Though it added that adjusted EBITDA will turn positive at "some point in the second half of 2025." Like CoreWeave, NBIS has also raised its 2025 capital expenditure forecast to approximately $2 billion from the previous estimate of $1.5 billion.

2. Execution Risk Valuation risk: even after the pullback, NBIS trades at premium multiples that leave little room for execution missteps, delays in GPU deliveries, or any renegotiation of its megadeals. Execution and concentration: Nebius is highly dependent on a handful of large contracts (Microsoft, Meta, and a small group of mega-customers). Any setback in one of these relationships could materially impact growth.

3. Capital Intensity Capital expenditures ballooned to $955.5 million in the September quarter from $172.1 million a year earlier as the company invests aggressively in securing graphics processing units, land and power infrastructure. Building AI infrastructure is extraordinarily capital-intensive, requiring continuous investment in expensive GPUs, real estate, and power infrastructure.

4. Competitive Pressure The intense competition from behemoths remains a concern. Nebius competes not only with other neoclouds like CoreWeave but also with hyperscalers like AWS, Azure, and Google Cloud—companies with vastly greater resources.

Porter's Five Forces Analysis

Threat of New Entrants: MODERATE High capital requirements and Nvidia relationships create barriers, but the market's attractiveness is drawing new competitors.

Bargaining Power of Suppliers: HIGH Nvidia dominates GPU supply, giving it tremendous leverage over all neocloud providers.

Bargaining Power of Buyers: MODERATE While large customers like Microsoft and Meta have significant negotiating power, the scarcity of AI infrastructure capacity limits their alternatives.

Threat of Substitutes: LOW to MODERATE Companies could build their own infrastructure, but the complexity and time required make outsourcing attractive for most.

Competitive Rivalry: HIGH and INCREASING The neocloud space is intensely competitive, with CoreWeave, Lambda, Crusoe, and others all vying for the same customers.

Hamilton Helmer's Seven Powers Framework

Scale Economies: Emerging as Nebius expands its infrastructure footprint. Network Effects: Limited in infrastructure businesses. Counter-Positioning: Nebius offers a "full-stack" approach versus competitors' more limited offerings. Switching Costs: Moderate—once AI workloads are configured on a platform, switching involves friction. Branding: Building through association with Microsoft, Meta, and Nvidia. Cornered Resource: Deep relationships with Nvidia and experienced engineering team from Yandex. Process Power: Proprietary data center design and AI-optimized infrastructure.

Key Metrics to Watch

For investors following Nebius, three metrics matter most:

1. Annual Run-Rate Revenue (ARR) Management targets $7-9 billion ARR by end of 2026. Nebius' annual run-rate (ARR) revenue continues to expand, underscoring the resilience and scalability of its business model. Nebius is on track to achieve its ARR guidance of $900 million to $1.1 billion by the end of 2025. This metric captures the true revenue velocity of the business and is the single most important indicator of whether Nebius is executing on its ambitious growth plans.

2. Contracted Power (GW) Last quarter, the company guided for 1GW of contracted power by the end of 2026. They are currently in the process of securing additional sites that would bring total contracted power to approximately 2.5GW by the end of 2026. Of this contracted amount, they expect to have 800MW to 1GW of connected power by the end of 2026. Power capacity determines the upper bound of revenue potential.

3. Customer Pipeline Nebius Group faces extreme demand overflow, with the Q3 pipeline soaring 70% QoQ to $4B, far exceeding current energizable capacity. Microsoft's $17–19.4B deal and Meta's $3B contract are capped by power limits, not customer appetite. The pipeline size indicates whether demand remains robust.

Conclusion: The Next Chapter

Arkady Volozh has spent thirty-five years building technology companies, first in the chaos of post-Soviet Russia, then in the global arena of Nasdaq-listed technology giants. He has survived the collapse of the Soviet Union, the rise and fall of the Russian internet, personal sanctions, and the destruction of a company worth $31 billion.

Now, at sixty years old, he is attempting something that few entrepreneurs ever achieve: building a second technology giant from the wreckage of the first.

CEO Arkady Volozh said in a letter to investors: "2025 has been a building year as we put in place the infrastructure and framework for future rapid growth. This year, we believe that we have successfully laid the foundations for an outstanding 2026—a year that should firmly position us among the top AI cloud businesses globally. And at the same time, 2026 is still just the beginning."

The story of Nebius is still being written. The company faces enormous execution challenges, intense competition, and the ever-present risk that the AI infrastructure boom could slow. But it also possesses assets that few competitors can match: a proven leadership team, deep technical expertise, strategic relationships with Nvidia and the hyperscalers, and—perhaps most importantly—the hunger that comes from having lost everything once before.

As of January 2025, Volozh has a net worth of $1.5 billion, according to Forbes. He has rebuilt much of what sanctions destroyed. Whether Nebius becomes one of the defining infrastructure companies of the AI era—or a cautionary tale about the risks of capital-intensive technology businesses—remains to be seen.

What is certain is that the journey from Guryev, Kazakhstan to the heights of Russian technology to exile and back to the pinnacle of AI infrastructure represents one of the most remarkable entrepreneurial odysseys of our time. The phoenix has risen. Now comes the harder part: proving that the rebirth was not merely survival, but the beginning of something even greater than what came before.

Key Dates and Timeline

| Date | Event |

|---|---|

| 1964 | Arkady Volozh born in Guryev, Kazakh SSR |

| 1989 | Volozh co-founds CompTek |

| 1990 | Arkadia Company founded; Ilya Segalovich joins |

| 1993 | "Yandex" name created |

| 1997 | Yandex.ru launches |

| 2000 | Baring Vostok invests $5.28 million |

| 2003 | Yandex becomes profitable |

| May 2011 | Yandex IPO raises $1.3 billion on Nasdaq |

| July 2013 | Ilya Segalovich dies at age 48 |

| 2014 | Volozh steps back from CEO role; moves to Israel |

| November 2021 | Yandex reaches $31 billion peak valuation |

| February 2022 | Russia invades Ukraine; Nasdaq suspends Yandex trading |

| June 2022 | EU sanctions Volozh; he resigns from Yandex |

| August 2023 | Volozh publicly condemns Russia's invasion |

| March 2024 | EU removes Volozh from sanctions list |

| July 2024 | Russian assets sold for $5.4 billion |

| August 2024 | Yandex N.V. renamed Nebius Group N.V. |

| October 2024 | Nebius resumes trading on Nasdaq |

| December 2024 | $700 million private placement from Nvidia, Accel |

| September 2025 | Microsoft deal announced ($17.4-$19.4 billion) |

| November 2025 | Meta deal announced ($3 billion) |

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube