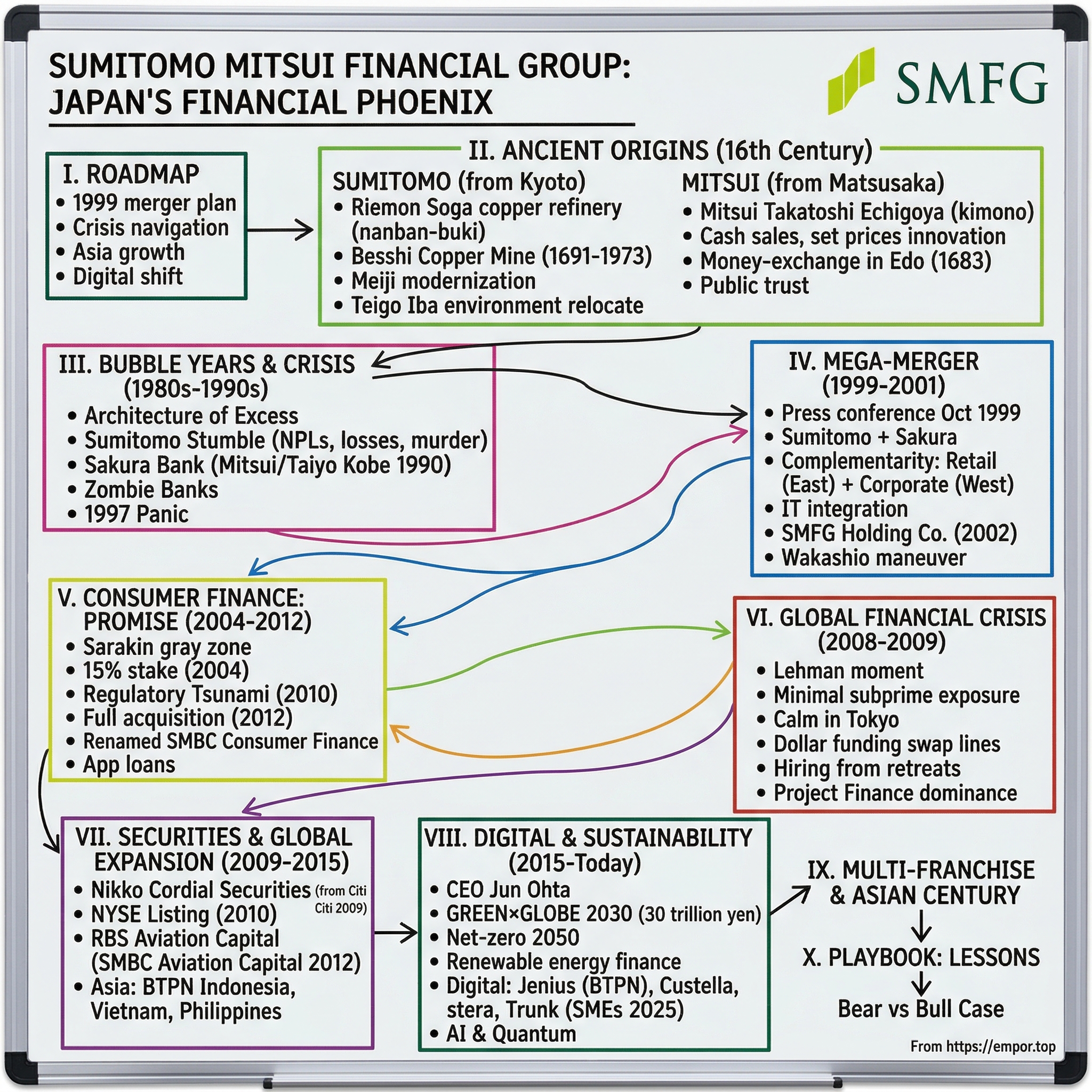

Sumitomo Mitsui Financial Group: Japan's Financial Phoenix

I. Introduction & Episode Roadmap

Picture this: It's October 1999, and two of Japan's most storied financial institutions—bitter rivals for over 400 years—are sitting across a negotiating table in Tokyo. Outside, Japan's economy is drowning in bad loans, the aftermath of the greatest asset bubble in modern history. Inside, executives from Sumitomo Bank and Sakura Bank (itself the product of an earlier merger with Mitsui Bank) are crafting what would become one of the most audacious financial mergers in history. The stakes? Nothing less than survival in a banking landscape littered with corporate casualties.

This is the story of Sumitomo Mitsui Financial Group—a $2 trillion colossus that emerged from the ashes of Japan's lost decade to become the world's 12th largest bank by assets. But SMFG isn't just another mega-bank formed through crisis-driven consolidation. It's a living embodiment of Japanese capitalism's evolution: from ancient copper mines and kimono shops to aircraft leasing and digital payments, from insular zaibatsu to global systematically important bank.

The question that drives our narrative isn't simply how two 400-year-old rivals merged to create a banking powerhouse. It's deeper: How does an institution built on centuries of tradition reinvent itself for the digital age? How does a bank that once served samurai merchants position itself for the Asian century? And perhaps most intriguingly—in an era when Western banks dominate financial headlines, why should global investors care about a Japanese bank?

Over the next several hours, we'll journey from 16th-century Kyoto copper refineries to 21st-century sustainable finance initiatives. We'll explore how SMFG navigated Japan's bubble economy collapse, survived the global financial crisis with minimal damage while Western peers imploded, and strategically acquired its way into consumer finance, securities, and emerging Asian markets. We'll examine the cultural alchemy required to merge ancient rivals, the strategic chess moves that built "second and third SMBCs" across Asia, and the digital transformation that's reshaping this centuries-old institution.

This isn't just a story about banking—it's about resilience, transformation, and the peculiarly Japanese art of turning crisis into opportunity. It's about understanding how patient capital, consensus-building, and long-term thinking can create value in ways that quarterly capitalism often misses. And for investors, it's about recognizing patterns: how financial institutions survive existential threats, how they expand internationally from domestic bases, and how they balance tradition with innovation.

The narrative arc ahead spans four distinct eras: the ancient origins that established DNA still visible today; the bubble years that nearly destroyed Japanese banking; the mega-merger era that created modern SMFG; and the current transformation into a pan-Asian financial services platform. Each phase reveals strategic lessons about crisis management, capital allocation, and competitive positioning that transcend geography and industry.

What makes SMFG particularly fascinating for students of business history is its embodiment of contradictions. It's simultaneously ancient and modern, domestic and global, traditional and innovative. It's a bank that counts samurai-era merchant houses as ancestors yet runs one of Asia's most sophisticated digital banking platforms. It's an institution that survived by merging with its greatest rival, then thrived by acquiring everything from consumer lenders to aircraft lessors.

As we dive into this epic tale, keep three questions in mind: First, what enabled SMFG to survive crises that destroyed peers? Second, how does its distinctly Japanese approach to banking create competitive advantages—or disadvantages—in global markets? And third, as Asian economies eclipse Western growth rates, is SMFG positioned to become the financial bridge between East and West?

The answers lie in understanding not just what SMFG is today, but how 400 years of history, culture, and strategic evolution created an institution unlike any other in global finance. Let's begin where all great stories do—at the very beginning, in the ancient merchant houses of Kyoto where copper refiners and kimono dealers planted seeds that would grow into one of the world's largest financial empires.

The Ancient Origins: Sumitomo & Mitsui's Legacy in 16th Century Japan

In the mist-shrouded mountains of 16th-century Kyoto, a young man of just nineteen years held a piece of copper ore up to the light, watching silver glint within its depths—silver that Japanese refiners had been sending overseas for centuries, unknowingly enriching foreign merchants. Riemon Soga had learned from Europeans how to separate silver from copper using lead, a revolutionary technique called "nanban-buki" (literally "Southern barbarian blowing") that would transform not just his fortune, but the destiny of an entire nation. In 1590, at the age of 19, he opened a copper refinery and workshop in Gojo, Teramachi, Kyoto, under the name of Izumiya—the "Fountainhead Shop," its logo the ancient igeta symbol of a well frame, suggesting endless depths of wealth yet to be discovered.

Meanwhile, across the same ancient capital fifty years later, another ambitious young man was plotting his own revolution. Mitsui Takatoshi, the fourth son of a shopkeeper in Matsusaka, waited 24 years until his older brother died before he could take over the family shop, Echigoya, then opened a new branch in 1673—a large gofukuya (kimono shop) in Nihonbashi, the bustling heart of Edo. But Takatoshi wasn't content to follow tradition. Where other kimono merchants visited wealthy customers' homes with samples, taking orders for custom garments, he introduced the sales at labeled prices concept to merchandising and sold fabric at whatever lengths his buyers desired—revolutionary ideas that seem mundane today but were scandalous in 1673.

These two origin stories—separated by decades but united by ambition—would eventually converge four centuries later in one of the most consequential mergers in banking history. But first, they would build parallel empires that would define Japanese commerce for generations.

The Copper Dynasty: From Refinement to Empire

The Sumitomo Group traces its roots to a bookshop in Kyoto founded circa 1615 by Masatomo Sumitomo, a former Buddhist monk whose "Founder's Precepts" still guide the company today. But it was his brother-in-law Riemon's copper breakthrough that transformed spiritual wisdom into commercial empire. After long striving he managed to complete his copper refining technique, reportedly during the Keicho era (1596-1615), which helped Izumiya prosper and enhanced its position in the copper industry.

The genius of Riemon's nanban-buki technique cannot be overstated. Previously, precious metals were sold to foreign traders as copper and were later extracted overseas at a great profit. Riemon's method involved adding lead to molten copper and smelting with charcoal to remove silver from copper, and later lead from silver. In an era when technical knowledge was jealously guarded, Riemon unselfishly instructed his competitors in the nanban-buki method—a move that seems counterintuitive but established Sumitomo as the acknowledged master of copper refining in Japan.

The business passed through family lines with dynastic precision. Riemon's first son, Tomomochi, married Masatomo's daughter and was adopted by the Sumitomo family. He established a separate copper refinery and crafting shop also named Izumiya, and at age 16 moved his business from Kyoto to Osaka. This wasn't just geographic expansion—it was strategic positioning. Osaka became Japan's copper refining center, with Sumitomo at its heart.

But the true transformation came in 1691, a date that would echo through centuries. Izumiya obtained permission from the Tokugawa Shogunate to open the Besshi Copper Mine in what is now Ehime Prefecture. This wasn't just another mine—it would become Sumitomo's beating heart for nearly three centuries. With accumulated copper production of 650,000 tons during the entire period of operation from 1691 to 1973, the Besshi Copper Mines were the second biggest source of copper in Japan.

The early years at Besshi read like an industrial fairy tale. The Besshi Copper Mines, whose annual output had reached 1,521 tons of copper by 1698, was one of the world's foremost sources of copper. Annual copper production had reached 1,500 tons within seven years from the opening, accounting for a quarter of Japan's copper production. This wasn't just mining—it was nation-building. During the Edo Period, Japan was one of the world's leading copper producing countries.

The Meiji Restoration of 1868 could have destroyed Sumitomo—many traditional businesses didn't survive the transition from feudal to modern Japan. But here emerged one of those pivotal figures that change corporate destiny: Saihei Hirose, the mine's general manager. Sumitomo overcame the crisis due largely to the unceasing efforts of Saihei Hirose. Hirose fought to stop factions within the Sumitomo family from selling the Besshi mine. The various measures he took laid the foundations for the mine's ultimate revival.

Hirose's modernization campaign was breathtaking in scope. In 1874, Hirose hired the French mining engineer Larroque to advise on the introduction of Western technology. Larroque wrote a detailed report on how to reform methods at Besshi. By 1897, annual copper output had grown to 3,500t, some six times the production figure thirty years earlier.

But prosperity brought problems that would presage modern corporate social responsibility debates. The rapid modernization of the copper mine led to deforestation of the surrounding mountains, and sulfur dioxide gas discharged from the smelting plant caused trees to die off and damaged crops. The response, led by Teigo Iba, Sumitomo's second Director General, was extraordinary: he decided to embark on a huge project to relocate the smelting plant to an uninhibited island located 20 km off the coast. The total actual construction costs was around 1.7 million yen, equivalent to 2 years net earnings of the Besshi Copper Mine at that time—a massive gamble on environmental responsibility when such concepts barely existed.

The Merchant House: From Kimonos to Modern Banking

While Sumitomo built its empire on copper and industrial might, the Mitsui story unfolded through commerce and finance. Originally a samurai family, Governor of Echigo Province Mitsui Takayasu was exiled to Matsusaka after being defeated by Oda Nobunaga, and his son Takatoshi renounced his status as a samurai and established himself as a sake and miso merchant and a pawnbroker. The business was named "Lord Echigo's Sake" to commemorate Takayasu's office.

The transformation from samurai to merchant—a dramatic fall in social status in feudal Japan—proved to be the family's making. Takatoshi's wife Shuhō was a skilled merchant and practically in charge of the business. She grew the business by introducing many business methods that were ground-breaking at the time, such as forfeited pawn and low-margin high-turnover. Her son Takatoshi is said to have inherited his business skills mostly from his mother.

When Takatoshi finally took control of Echigoya in 1673, he unleashed a retail revolution. Traditionally, gofukuyas had made clothing to order; a salesperson visited the customer at his home, showed samples of cloth, took an order, and was paid when the finished product was delivered. Mitsui Takatoshi implemented a new system, manufacturing ready-made items which could be purchased directly at his shop for cash. This wasn't just process improvement—it was democratization of commerce, making quality goods accessible beyond the aristocratic elite.

But Takatoshi's true genius lay in recognizing that moving goods meant moving money. As the business of Echigo-ya was growing, related money-exchange transactions increased, which encouraged Takatoshi Mitsui to launch a money-exchange business in Edo in 1683. The timing was perfect. Regional feudal governments had begun to pay taxes to the central Edo government in cash, but thieves and bandits made the transportation of cash dangerous. In 1683, the shogunate granted permission for money exchanges to be established in Edo. The Mitsui "exchange shops" facilitated transfers by accepting goods and cash at regional centers in exchange for notes that could then be redeemed for cash in Edo.

This was revolutionary financial engineering—creating what we'd now call a payments network that reduced risk while generating fees. Mitsui's customers included the central government, which asked the company to handle public money, thus developing its businesses, and building a public reputation.

The Banking Evolution: From Money Exchange to Modern Finance

The parallel evolution of these two houses into modern banks reveals much about Japanese capitalism's unique character. The Sumitomo family established Sumitomo Bank in November 1895, transforming centuries of copper wealth into financial capital. While expanding the copper mine development business centering on the Besshi Copper Mine, the family engaged in a money-exchange service during the 1660s—meaning banking was always part of Sumitomo's DNA, funded by industrial profits.

Mitsui's path was even more direct. In July 1876, based on its solid businesses and the reputation it had built, Mitsui family established Mitsui Bank, Japan's first private bank. This wasn't just first-mover advantage—it was centuries of accumulated trust crystallized into modern institutional form.

Both banks rode Japan's industrialization wave brilliantly. Driven by the buoyant economic recovery after World War I, Sumitomo Bank expanded operations rapidly while increasing branches in Japan. But they also exemplified the zaibatsu model—vast conglomerates where banking, industry, and commerce reinforced each other in ways that would be illegal in most Western economies today.

The post-WWII occupation brought forced dissolution of the zaibatsu, but like phoenixes, both banking groups reconstituted themselves. Sumitomo Bank emerged stronger, often earning top position among city banks in revenue. But it had a critical weakness: The bank was inferior to other top ranked city banks in terms of branch network in the Tokyo metropolitan area. To address this concern, the bank merged with Heiwa Sogo Bank in October 1986.

Mitsui Bank took a different path, merging with Taiyo Kobe Bank in 1990 to form Sakura Bank—itself a response to competitive pressures and the need for scale. These mergers were preludes to the ultimate convergence, setting the stage for a union that would have seemed impossible to the feuding merchant houses of centuries past.

Cultural DNA: The Philosophies That Endure

What's remarkable about both Sumitomo and Mitsui is how their founding philosophies—established in an era of samurai and shoguns—remain relevant in the age of algorithms and derivatives. Management of the group is guided by Masatomo Sumitomo's "Founder's Precepts", written in the 17th century. These aren't corporate platitudes but living documents that have guided decisions through centuries of change.

For Sumitomo, the environmental crisis at Besshi became a defining moment that crystallized these values. The restored lush mountains surrounding the Besshi Copper Mines remind us of one of the credos of Sumitomo's Business Philosophy: "Benefit for self and others, private and public". This wasn't greenwashing—it was investing two years of profits to relocate a smelter when no law required it.

Mitsui's philosophy emphasized innovation and human development. Takatoshi proactively implemented human resource development measures targeting young people, thereby further expanding his business and fostering innovation beyond the scope of the kimono textile industry. This focus on talent development would become a hallmark of Japanese management philosophy.

Both houses also shared a peculiarly Japanese approach to competition and cooperation. Riemon Soga sharing his copper refining secrets with competitors seems irrational by Western standards, but it established Sumitomo as the acknowledged leader while growing the entire industry. Similarly, Mitsui's innovations in retail and finance often became industry standards, benefiting competitors but cementing Mitsui's position as innovator.

These weren't just businesses—they were institutions that saw themselves as part of Japan's social fabric. "The operation of copper mines is a task of national importance, transcending the interests of a commercial enterprise"—this conception shaped Sumitomo's actions from the Edo period onward. It's a philosophy that would prove crucial when, centuries later, two ancient rivals would need to merge not just for profit, but for survival.

The stage was now set for these parallel histories to converge. Two houses that had built Japan's modern economy, survived wars and occupations, and adapted from feudalism to capitalism, would soon face their greatest challenge: Japan's bubble economy and its catastrophic collapse. The DNA they'd developed over centuries—patience, adaptation, social responsibility—would be tested as never before. And from that test would emerge something neither Riemon Soga nor Mitsui Takatoshi could have imagined: a unified banking giant built on four centuries of rivalry, ready to face the digital future while honoring its analog past.

III. The Bubble Years & Banking Crisis (1980s–1990s)

The morning of December 29, 1989, should have been euphoric at the Tokyo Stock Exchange. The Nikkei 225 index kissed an all-time high of 38,957.44—a number that would haunt Japanese finance for the next three decades. Champagne corks popped in trading rooms across Marunouchi. At Sumitomo Bank's headquarters in Osaka, executives celebrated what seemed like vindication of Japan's economic model. From 1985 to 1989, Japan's Nikkei stock index tripled to 39,000 and accounted for more than one third of the world's stock market capitalization. In 1989, of the world's top 50 companies by market capitalization, 32 were Japanese.

But three days later, as 1990 dawned, the party ended with shocking suddenness. The Nikkei began a descent that would eventually erase 80% of its value. Land prices, which had reached levels where the 1.15 square kilometer Tokyo Imperial Palace grounds were estimated to be worth more than the entire real estate value of California, began their own sickening plunge. Japan's bubble economy—'bubble economy' was an economic bubble in Japan from 1986 to 1991 in which real estate and stock market prices were greatly inflated—was bursting, and with it, the dreams of an entire generation of bankers, including those at Sumitomo and the newly formed Sakura Bank.

The Architecture of Excess

To understand how Japan's most conservative banks became casualties of history's most spectacular asset bubble, we must first grasp the unique confluence of forces that created it. By the late 1980s, the Japanese economy experienced an asset price bubble caused by loan growth quotas dictated upon the banks by Japan's central bank, the Bank of Japan, through a policy mechanism known as the "window guidance". This wasn't just monetary policy—it was industrial policy masquerading as banking regulation.

The roots trace back to the 1985 Plaza Accord, that fateful agreement where major economies conspired to weaken the dollar. The 1985 Plaza Accord, an agreement among major economies to depreciate the US dollar, led to a rapid appreciation of the yen. An expensive yen made Japanese exports less competitive, putting pressure on the country's export-driven economy. The Bank of Japan responded by slashing interest rates, spurring the domestic lending and borrowing that inflated the bubble.

To prevent the yen from appreciating further, monetary policymakers pursued aggressive monetary easing and slashed the official discount rate to as low as 2.5% by February 1987. This was monetary morphine for an economy already high on its own success.

However, the trend seemed to reverse by the late 1980s as more Japanese opted to shift funding from banks to the capital market – leaving banks in a tight squeeze as lending costs grew with the shrinking customer base. In fact, bank behaviour has gradually become aggressive since 1983 (even before the monetary easing policy in Japan) after the ban on fund-raising in the securities market was lifted around 1980. However, major firms were not keen to use the bank as the source of funding. For this reason, banks were forced to aggressively promote loans to smaller firms backed by properties. Soon, especially around 1987–1988, banks were even more apt to lend to individuals backed by properties. Evidently, even an ordinary salaryman could easily borrow up to 100 million yen for any purpose, provided his house was used as collateral.

Sumitomo's Swagger and Stumble

For Sumitomo Bank, the bubble years represented both triumph and tragedy. The bank that had survived centuries, weathered wars, and financed Japan's industrialization suddenly found itself playing a different game—one where prudence was punished and recklessness rewarded. The conservative DNA that Riemon Soga had encoded into the institution's culture was overwhelmed by the intoxicating fumes of easy money.

The numbers tell a story of progressive intoxication. By 1991, commercial land prices rose 302.9% compared to 1985, while residential land and industrial land price jumped 180.5% and 162.0%, respectively, compared to 1985. Nationwide, statistics showed that commercial land, residential land, and industrial land prices were up by 80.9%, 51.1%, and 51.7%, respectively. Sumitomo, like all Japanese banks, lent against these inflated values with abandon. The collateral seemed bulletproof—after all, Japanese land prices had never fallen significantly in the postwar era.

But beneath the surface, rot was spreading. The cozy relationship of corporations to banks and the implicit guarantee of a taxpayer bailout of bank deposits created a significant moral hazard problem, leading to an atmosphere of crony capitalism and reduced lending standards. Sumitomo's loan officers, once known for their meticulous credit analysis, became order-takers in a system where saying "no" to a loan request was career suicide.

The bank's international adventures during this period read like a cautionary tale of hubris. Sumitomo poured money into overseas real estate, leveraged buyouts, and exotic financial instruments it barely understood. Banks started to take increasingly excessive risks that were partly funded by 186 trillion worth of Yen borrowed from various capital markets. Nearly $40 billion was invested in risky leveraged buyouts in the USA, including 40% of the amount used in the buyout of RJR Nabisco.

When the music stopped, Sumitomo found itself holding catastrophic losses. In the face of financial difficulties that resulted from the collapse of the bubble economy, Sumitomo Bank posted a loss in the fiscal year 1994, becoming the first city bank to do so, and wrote off non-performing loans. This wasn't just a financial loss—it was a psychological earthquake. In 1995, it posted the first net loss of a major Japanese bank in the postwar era. The bank that had epitomized Japanese financial strength was bleeding red ink.

The human cost was even more tragic. In 1993, it wrote off 100 billion yen in bad loans, and in 1994 its Nagoya branch manager was murdered in possible connection with a bad debt collection. The murder sent shockwaves through Japan's banking community—a violent reminder that beneath the spreadsheets and board meetings, real lives and dangerous money were at stake.

The Birth of Sakura: A Merger Born of Weakness

While Sumitomo struggled with its demons, another mega-merger was reshaping Japan's banking landscape. It was formed in April 1990 as the Mitsui Taiyo Kobe Bank (MTKB) by the merger of Mitsui Bank (founded 1876) and Taiyo Kobe Bank (founded 1973). The Sakura Bank name was adopted in April 1992.

The timing could not have been worse. Mitsui Bank agreed to merge with Taiyo Kobe Bank in 1989. At the time (in the midst of the Japanese asset price bubble), the merger was to create the second largest bank in the world behind Dai-Ichi Kangyo Bank. What seemed like a marriage of strength at the bubble's peak became a union of weakness as asset prices collapsed.

The bank was looking to increase its earning capacity. Unfortunately, however, the bubble economy collapsed at almost the same time as when the integration was completed. As a result, the bank faced the severe challenge of non-performing loans before leveraging the effects of the integration, which led Sakura Bank to the decision to merge with Sumitomo Bank.

The newly christened Sakura Bank inherited the worst of both parents' portfolios. Mitsui's exposure to large corporate borrowers and Taiyo Kobe's aggressive retail lending had both turned toxic. However, Sakura incurred massive bad loan write-offs in 1998 and approached one of its major corporate customers, Toyota, for financial support, which was rejected. The rejection by Toyota—a company that owed its postwar resurrection partly to Mitsui financing—symbolized how far the mighty had fallen.

The Lost Decade Begins

As the 1990s progressed, what initially seemed like a sharp correction morphed into something far more sinister: a balance sheet recession that would define a generation. Economist Richard Koo wrote that Japan's "Great Recession" that began in 1990 was a "balance sheet recession". It was triggered by a collapse in land and stock prices, which caused Japanese firms to become insolvent.

The mechanism Koo identified was insidious. Despite zero interest rates and expansion of the money supply to encourage borrowing, Japanese corporations in aggregate opted to pay down their debts from their own business earnings rather than borrow to invest as firms typically do. Corporate investment, a key demand component of GDP, fell enormously (22% of GDP) between 1990 and its peak decline in 2003. Japanese firms overall became net savers after 1998, as opposed to borrowers.

This wasn't just economic theory—it was corporate Japan's collective trauma response. Companies that had borrowed aggressively during the bubble now focused obsessively on debt reduction, creating a deflationary spiral that the Bank of Japan seemed powerless to stop.

The Zombie Bank Phenomenon

Perhaps no term better captures the horror of Japan's banking crisis than "zombie banks"—institutions that were technically alive but economically dead, kept breathing only by regulatory forbearance and accounting tricks. Yalman Onaran of Bloomberg News writing in Salon stated that the zombie banks were one of the reasons for the following long stagnation. Additionally, Michael Schuman of Time magazine wrote that these banks kept injecting new funds into unprofitable "zombie firms" to keep them afloat, arguing that they were too big to fail. However, most of these companies were too debt-ridden to do much more than survive on bail-out funds.

Both Sumitomo and Sakura found themselves in this netherworld. The easily obtainable credit that helped create and engorge the real estate bubble continued to be a problem for several years, and as late as 1997, banks were still making loans that had a low probability of being repaid. Loan officers and investment staff had a hard time finding anything to invest in that had the prospect of returning a profit. They would sometimes resort to depositing their block of investment cash, as ordinary deposits, in a competing bank.

The government's response oscillated between denial and panic. It is generally acknowledged that the Bank of Japan (BoJ), Japan's central bank, made several mistakes that may have added to and prolonged the negative effects of the bursting of the equity and real estate bubbles. For example, monetary policy was stop-and-go; concerned about rising prices called inflation and soaring asset prices. The Bank of Japan put the brakes on the money supply in the late 1980s, which may have contributed to the bursting of the equity bubble. As equity values fell, the BoJ continued to raise interest rates because it remained concerned with still-appreciating real estate values. Higher interest rates contributed to the end of rising land prices, but they also pushed the overall economy into a downward spiral. In 1991, as equity and land prices fell, the Bank of Japan dramatically reversed course and cut interest rates. But it was too late, a liquidity trap had already been set, and a credit crunch was setting in.

The 1997 Crisis: The System Nearly Breaks

If the early 1990s were about denial, 1997 was about panic. In 1997, a leading securities firm went under, creating instability in the financial market and prompting many financial institutions to pursue partnerships and mergers. The failure of Yamaichi Securities, one of Japan's Big Four brokerages, sent shockwaves through the system. Suddenly, institutions that had seemed too big to fail were failing.

For Sumitomo and Sakura, 1997 marked a turning point. The fiction that they could muddle through was shattered. Bad loans weren't just a temporary problem to be managed—they were an existential threat. The two banks, ancient rivals whose predecessors had competed for four centuries, began to realize that their survival might depend on the unthinkable: joining forces.

Corporate Culture in Crisis

The human dimension of the crisis often gets lost in the statistics, but it was perhaps the most profound change. Japan's lifetime employment system, the bedrock of corporate culture, crumbled. During the 1970s and 1980s, life-time employment schemes were widespread, but in a response to the recession that followed the bursting of the bubble, Japanese companies restructured their businesses, which included downsizing and outsourcing. Life-time employment schemes were modified and uncommon, and new college graduates failed to find stable jobs, resorting to unstable and poorly paid jobs.

At both Sumitomo and Sakura, the cultural transformation was wrenching. Bankers who had joined expecting lifetime employment and steady promotion found themselves expendable. The social contract that had defined Japanese capitalism—the implicit bargain where loyalty was exchanged for security—was torn up. Young employees watched senior colleagues, men who had devoted their lives to the bank, being pushed into early retirement or transferred to dead-end subsidiaries.

Corruption and Consequences

As the crisis deepened, darker truths emerged. At the end of the bubble, it was revealed that corruption, which included bribery, insider trading, stock manipulation schemes and fraud, was pervasive in every aspect of Japanese society, from government officials to ordinary people, during the economic bubble. The Recruit scandal of 1988, whereby shares in a human resources firm were offered to politicians in return for favors, implicated the entire cabinet and revealed the close relationship between the government and the private sector. Nui Onoue, a former restaurant owner in Osaka, was convicted of fraud, and was responsible for the collapse of The Industrial Bank of Japan and Tōyō Shinyo Kinko Bank.

The scandals revealed that Japan's economic miracle had been partly built on a foundation of collusion and corruption. The same informal networks and relationship-based lending that had facilitated rapid growth had also enabled massive fraud and misallocation of capital.

Setting the Stage for Transformation

By the late 1990s, both Sumitomo and Sakura had exhausted their options for independent survival. The mathematics were brutal: non-performing loans that dwarfed their capital, share prices that had collapsed, and a business model that no longer worked in a deflationary economy. From 1991 to 2003, the Japanese economy, as measured by GDP, grew only 1.14% annually, while the average real growth rate between 2000 and 2010 was about 1%, both well below other industrialized nations.

The stage was set for a merger that would have seemed impossible just a decade earlier. Two of Japan's most storied financial institutions, inheritors of 400-year-old merchant traditions, would need to combine just to survive. The bubble economy hadn't just destroyed balance sheets—it had shattered the assumptions that had governed Japanese banking for centuries. From this wreckage would emerge something new: a banking giant built not on the certainties of the past but on the hard lessons of the crisis. The merger talks that began in 1999 weren't just about creating a bigger bank—they were about creating a different kind of bank, one that could navigate a world where Japanese exceptionalism had given way to global competition and where tradition alone was no longer enough to ensure survival.

IV. The Mega-Merger: Creating SMBC (1999-2001)

The press conference on October 14, 1999, was staged with military precision. Sumitomo Bank and Sakura Bank signed a basic agreement on a full partnership and integration plan, making public their intent to execute the merger by April 2002. In the wood-paneled conference room at Tokyo's Palace Hotel, executives from both banks sat side by side—an image unthinkable even five years earlier. The body language spoke volumes: stiff postures, forced smiles, centuries of rivalry barely concealed beneath corporate courtesy.

Akishige Okada, Chairman of Sakura Bank, and Yoshifumi Nishikawa, President of Sumitomo Bank, took turns at the podium, their words carefully choreographed to project unity while preserving face. Even more than the earlier announced deal, analysts said, the planned merger of Sumitomo and Sakura is deeply significant because it represents an almost unprecedented mixed marriage of companies from competing business groups that would never have wanted to team up in the past.

The numbers they presented were staggering. The combined entity would have assets exceeding 100 trillion yen, making it the world's second-largest bank by assets. The banks said they have 30,000 employees altogether. They plan to cut 9,300 jobs by March 2004. They also plan to close 151 of their 800 domestic branches, 32 of 45 foreign branches and save a significant amount of money on investments in information technology. These weren't just statistics—they represented thousands of careers ending, branches that had served communities for generations shuttering, a fundamental reshaping of Japanese banking.

The Logic of Desperation

Behind the choreographed optimism lay a brutal reality: neither bank could survive alone. The bank was looking to increase its earning capacity. Unfortunately, however, the bubble economy collapsed at almost the same time as when the integration was completed. This wasn't Sakura's first failed merger—the Mitsui-Taiyo Kobe combination had never truly gelled before asset prices collapsed, leaving the merged entity weaker than the sum of its parts.

For Sumitomo, the mathematics were equally grim. Despite its proud history and industrial connections, Sumitomo Bank posted a loss in the fiscal year 1994, becoming the first city bank to do so, and wrote off non-performing loans. In 1997, a leading securities firm went under, creating instability in the financial market and prompting many financial institutions to pursue partnerships and mergers.

The strategic rationale went beyond mere survival. Sakura, based in Tokyo, is strong in retail banking, while Sumitomo, based in Osaka, is ahead in corporate and investment banking. This geographic and business complementarity looked elegant on paper—Sakura's eastern Japan retail network combined with Sumitomo's western Japan corporate strength, creating a truly national champion.

But everyone knew the real driver was the Tokyo Big Bang—Japan's attempt to transform its financial markets to compete with New York and London. The Tokyo Big Bang was the name given to Japanese-style financial system reforms introduced by the Ryutaro Hashimoto administration in November 1996. It aimed for upgrading Japan's financial market functions so that Tokyo could more effectively compete with New York and London as an international financial center by 2001. In preparation for this grand initiative, the Financial Systems Reform Act was enacted in June 1998, launching a range of deregulation measures, including the full liberalization of brokerage commissions and a mutual participation framework between banking, securities and insurance businesses.

Cultural Alchemy: Merging the Unmergeable

The cultural challenges were immense. The two companies are affiliated with different business groups, or keiretsu, that have interests in many of Japan's main industries. The keiretsu traditionally worked very closely with other members of their own group–including owning shares in each other and buying each other's products–but avoided dealings with the others. But this deal, expected to be completed in 2002, brings together Sumitomo Bank, a mainstay of the Sumitomo keiretsu, and Sakura bank, which is part of the Mitsui keiretsu and was the result of the 1990 merger of Mitsui Bank and Taiyo Kobe Bank.

These weren't just corporate cultures—they were civilizational identities. Sumitomo bankers, shaped by centuries of Osaka merchant pragmatism and industrial financing, viewed their Mitsui counterparts as effete Tokyo bureaucrats more concerned with government connections than credit analysis. Mitsui bankers saw Sumitomo as provincial roughnecks who'd gotten lucky with copper money but lacked sophistication in modern finance.

The integration planning revealed these fault lines immediately. Teams from both banks were paired to design the new organization, but meetings often devolved into polite warfare. Systems integration alone was a nightmare—Sumitomo's technology platform, built for corporate banking, was fundamentally incompatible with Sakura's retail-focused infrastructure. The decision to maintain dual headquarters—one in Tokyo (former Mitsui territory) and one in Osaka (Sumitomo's base)—was a diplomatic necessity that would create operational headaches for years.

The Acceleration: From 2002 to 2001

Events soon overtook the leisurely three-year integration timeline. As 2000 progressed, Japan's banking crisis deepened. Downward spirals of land and stock prices delivered a heavy blow to quite a few companies that had borrowed heavily to invest in real estate and stocks, throwing them into financial turmoil. This resulted in non-performing loans, particularly those related to real estate, piling up and being written off by lending institutions. Among those, a number of remarkably large financial institutions went bankrupt in and after 1997, which created financial instability.

The decision to accelerate the merger from 2002 to April 2001 was driven by survival instinct. Waiting meant more quarters of losses, more erosion of capital, more risk that one or both banks might not make it to the altar. Speed became essential, even if it meant compressing years of planning into months.

April 1, 2001: Birth in Crisis

Sumitomo Mitsui Banking Corporation (SMBC) was formed in 2001 through the merger of Sakura Bank and Sumitomo Bank. The new bank was launched in an environment of unprecedented financial turmoil. It was under such a backdrop that we embarked on our journey to make SMBC the most trusted brand in banking and become a true global player.

The opening ceremony at the newly designated Tokyo headquarters was a study in contrasts. Traditional Shinto priests blessed the merger while investment bankers ran probability models on loan defaults. Akishige Okada assumed the chairmanship while Yoshifumi Nishikawa became president—a careful balance between the two legacy institutions that fooled no one about the underlying tensions.

The challenges facing the newborn SMBC were staggering. Non-performing loans exceeded 8 trillion yen. The bank's capital adequacy ratio hovered dangerously close to regulatory minimums. International rating agencies maintained negative watches. Most ominously, the integration of 30,000 employees from rival traditions had barely begun.

The Holding Company Revolution

The creation of SMBC was just the first act. In December 2002, Sumitomo Mitsui Banking Corporation (SMBC) formed Sumitomo Mitsui Financial Group, Inc. (SMFG), a holding company, through an equity transfer, and became a wholly owned subsidiary of the new company. This wasn't merely corporate restructuring—it was institutional revolution.

The holding company structure, modeled on American financial conglomerates but adapted for Japanese sensibilities, offered several advantages. It allowed for cleaner separation between banking and other financial services, facilitating expansion into securities, insurance, and consumer finance. It provided a mechanism for raising capital at the holding company level without diluting the bank's operations. Most importantly, it created a governance structure that could transcend the Sumitomo-Mitsui rivalry by establishing a neutral corporate parent.

SMBC announced on July 30, 2002 that it would establish a holding company by December and reorganize three related companies, its subsidiary Sumitomo Mitsui Card Company, Sumitomo Mitsui Bank Leasing, and The Japan Research Institute, a sister think tank, as subsidiaries of the holding company. The holding company had a capital of 1 trillion yen, and SMBC CEO Takashi Nishikawa and Chairman Akira Okada each served as president and chairman of the holding company.

The Public Funds Dilemma

Perhaps no issue better illustrated the delicate balance between pride and pragmatism than public funds. Japanese banks had accepted massive government capital injections during the crisis—a necessary evil that came with stigma and government oversight. In July 2002, SMBC announced that it would repay 2,000 billion yen of public funds, which had been accepted in the form of perpetual subordinated bonds. The funds were part of a total of 1.5 trillion yen that had been injected into the Japanese banking system following the financial crisis of the late 1990s.

The push to repay these funds wasn't just about financial flexibility—it was about honor. Being beholden to government money meant being seen as weak, as needing protection. For institutions with 400-year histories, this was intolerable. The race to repay public funds became a proxy for institutional virility, with SMFG, Mitsubishi UFJ, and Mizuho competing to see who could achieve independence first.

Integration Reality: The First Years

Behind the public displays of unity, integration proceeded in fits and starts. The IT systems merger, originally planned for 2002, was delayed repeatedly as incompatibilities proved more severe than anticipated. Since the merger of Sakura Bank and Sumitomo Bank in April 2001, headquarters operations have been divided into two locations, at Hibiya and Otemachi in Tokyo. The relocation will enable us to centralize dispersed headquarters operations and seek further efficiency.

Cultural integration proved even more challenging. Former Sumitomo employees dominated corporate banking while ex-Sakura staff controlled retail operations, creating parallel organizations within the same bank. Promotion decisions became political minefields, with careful attention paid to maintaining balance between the legacy institutions. Customers noticed the dysfunction—corporate clients found themselves dealing with multiple relationship managers, while retail customers encountered different policies at branches depending on their legacy affiliation.

The Wakashio Maneuver

One of the most creative—and controversial—moves in the early integration was the reverse merger with Wakashio Bank. In March 2003, SMBC initiated a reverse merger with its subsidiary, Wakashio Bank (est. June 1996), to secure financial resources to cover large deferred losses from its equity holdings. Although SMBC was technically dissolved and Wakashio Bank became a company that survived, under the Japanese Commercial Code, the surviving entity took the name Sumitomo Mitsui Banking Corp., just like the disbanded bank name. The purpose of the merger was to generate about 2 trillion yen in book profits (merger surplus) by making the Wakashio Bank the surviving company, and to eliminate the hidden losses of SMBC, such as those on stocks.

This accounting alchemy—legal under Japanese rules but raising eyebrows internationally—demonstrated both the creativity and desperation of SMBC's management. By technically dissolving the original SMBC and having a small subsidiary absorb it, they could realize massive paper gains that cleaned up the balance sheet. It was financial engineering at its most aggressive, a far cry from the conservative banking traditions of both Sumitomo and Mitsui.

Early Victories and Ongoing Challenges

Despite the chaos, some early wins emerged. The combined entity's scale allowed for more aggressive workout of bad loans. International operations, where legacy rivalries mattered less, integrated more smoothly. The corporate and investment banking division, leveraging relationships from both parents, won mandate after mandate from Japanese corporations expanding abroad.

But fundamental challenges remained. The Japanese economy continued to stagnate, making loan growth nearly impossible. Competition from megabanks Mitsubishi UFJ and Mizuho intensified. Foreign banks, sensing opportunity in chaos, picked off top talent and blue-chip clients. Most troublingly, the non-performing loan problem, while improving, remained massive.

Looking Forward: A New Identity

By 2004, three years after the merger, SMBC was beginning to forge a new identity—neither Sumitomo nor Mitsui, but something different. Younger employees, hired after the merger, had no allegiance to legacy institutions. New business lines, particularly in consumer finance and investment banking, created power centers independent of traditional commercial banking.

The merger that had seemed impossible in 1999 had happened, but transformation would take much longer. Creating SMBC was relatively simple—forms filed, signs changed, systems (eventually) integrated. Creating a unified culture, a coherent strategy, and a sustainable business model would require not just merging two banks but reimagining what a Japanese bank could be in the 21st century.

The path ahead would require more than integration—it would demand innovation. The next phase of SMFG's evolution would see bold moves into consumer finance through the Promise acquisition, expansion across Asia, and eventually a transformation into something neither Riemon Soga nor Mitsui Takatoshi could have imagined: a global financial services platform built on Japanese foundations but competing worldwide. The merger was complete, but the real work of building a modern financial institution had just begun.

V. The Consumer Finance Play: Promise Acquisition (2004-2012)

The boardroom at Promise Co.'s headquarters in Tokyo's Minato district had seen better days. It was June 21, 2004, and executives from Japan's second-largest consumer finance company were about to sign away their independence. Across the table sat representatives from Sumitomo Mitsui Banking Corporation, ready to acquire a 15 percent equity stake in Promise Co. by July 13 and eventually boost it to 20 percent. The capital tieup to make SMBC the biggest shareholder in Promise is part of a business collaboration agreement between SMFG and the consumer finance firm.

This wasn't a hostile takeover—it was a lifeline disguised as a strategic alliance. Promise, founded in 1962 as Kansai Financial Corporation, had built an empire on small, unsecured loans to millions of Japanese consumers. But storm clouds were gathering over Japan's consumer finance industry, and Promise's executives knew they needed a powerful partner to survive what was coming.

The Sarakin Paradox

To understand why SMBC would venture into consumer finance—a business that traditional Japanese banks had long viewed with disdain—requires understanding Japan's peculiar credit market dynamics. Consumer finance companies, derisively called "sarakin" (salary loan) lenders, occupied a gray zone in Japanese finance. They served millions of customers that banks wouldn't touch: young salarymen needing bridge loans until payday, small business owners requiring quick capital, housewives managing household cash flow gaps.

Promise and its competitors—Acom, Aiful, Takefuji—had built multi-billion dollar businesses charging interest rates up to 29.2% annually, the legal maximum under Japan's Interest Rate Restriction Act. While banks lent at 2-3%, consumer finance companies justified their rates through convenience (loans approved in 30 minutes), accessibility (branches in train stations and shopping districts), and willingness to lend without collateral or guarantors.

But this business model contained seeds of its own destruction. The high rates created a vicious cycle—borrowers who couldn't repay took new loans from other lenders, eventually drowning in debt. By 2004, an estimated 2.3 million Japanese were caught in this "multiple debtor" problem, owing money to five or more lenders.

SMBC's Strategic Gambit

For SMFG leadership, the Promise investment represented more than opportunistic expansion—it was recognition that Japanese banking needed to fundamentally reimagine its relationship with individual consumers. SMFG is the second of Japan's four major banking groups to conclude a capital tieup with a consumer loan company after Mitsubishi Tokyo Financial Group Inc., which announced a deal in March to buy a stake of more than 15 percent in Acom Co.

The strategic logic was compelling. Promise brought 2.3 million active customers, sophisticated risk management systems for unsecured lending, and a nationwide network of automated loan machines. In addition to the capital tieup, the business collaboration accord calls for SMBC and Promise to expand their consumer finance business by marketing loan products with annual interest rates of 8 percent to 12 percent through SMBC.

This wasn't just about cross-selling—it was about learning. SMBC's traditional approach to retail lending—requiring extensive documentation, multiple branch visits, and weeks of processing—was hopelessly outdated in an era of instant gratification. Promise's ability to assess credit risk in minutes, not weeks, represented capabilities SMBC desperately needed.

The Regulatory Tsunami

Even as SMBC was cementing its Promise alliance, Japan's political establishment was turning against consumer finance. Media exposés of borrower suicides, aggressive collection practices, and the multiple debtor crisis had created a public relations disaster. Politicians across the spectrum called for reform, setting the stage for regulatory changes that would devastate the industry.

The first blow came in 2006 when the Supreme Court ruled that interest charged above 20% was legally unenforceable, even though the Interest Rate Restriction Act technically allowed rates up to 29.2%. This "gray zone" interest suddenly became returnable to borrowers, triggering an avalanche of refund claims that would eventually total trillions of yen.

But the death blow came with the 2010 Money Lending Business Act revisions. The new regulations capped interest rates at 20% and introduced the "total volume control" rule: In June 2010, total loan volume control was introduced for the purpose of prohibiting lenders from offering new loans to borrowers with a total loan balance exceeding one-third of the annual income of the borrower. Owing to these stricter regulations, consumer finance companies faced a significant decline in outstanding borrowings, which led to restructuring of the industry, resulting in oligopolization.

Promise Under Pressure

The regulatory tsunami devastated Promise's business model. Revenues plummeted as interest rates were forcibly reduced. The total volume control rule disqualified millions of existing customers from new loans. Most painfully, the company faced massive liabilities from gray-zone interest refunds—money that had already been booked as profit now had to be returned.

The revised Money Lending Business Act had a huge impact on Promise, an equity-method affiliate of SMFG at that time. In a prompt response to the business environment, Promise implemented business restructuring plans in January 2010 in order to survive in a shrinking market. Branch networks were slashed, thousands of employees laid off, and the aggressive marketing that had built the Promise brand disappeared.

Industry consolidation was swift and brutal. Takefuji, once Japan's largest consumer lender, filed for bankruptcy in 2010 with liabilities exceeding 433 billion yen. Aiful narrowly avoided collapse through debt restructuring. The consumer finance industry that had once boasted over 10,000 companies shrank to fewer than 2,000.

The Full Acquisition Decision

By 2011, SMFG faced a decision: abandon the consumer finance experiment or double down. The Promise investment, which had seemed strategic in 2004, now looked like a liability. The company was bleeding money from refund claims, its loan book was shrinking, and its brand was toxic.

But SMFG's leadership saw opportunity where others saw disaster. The regulatory changes, while painful, had cleaned up the industry's worst practices. Surviving players would operate in a more regulated but also more legitimate market. Most importantly, the capabilities Promise had developed—instant credit decisioning, automated lending, behavioral scoring models—were exactly what SMBC needed to compete in digital banking.

On September 30, 2011, SMBC's board made the decisive move: a tender offer for all remaining Promise shares. The lender currently owns a 22 percent stake in Promise. In a consolidation move, SMBC will pay nearly $1.30 million for the acquisition of the stake that it does not already hold. This wasn't just increasing an investment—it was a full embrace of consumer finance as core to SMFG's future.

The Transformation: From Promise to SMBC Consumer Finance

SMFG made Promise a wholly owned subsidiary in April 2012, and it was renamed SMBC Consumer Finance Co., Ltd., in July 2012. The rebranding was more than cosmetic—it represented full integration into the SMFG family and a deliberate distancing from the controversial sarakin past.

Under SMFG ownership, SMBC Consumer Finance underwent radical transformation. The cowboy culture of aggressive lending gave way to SMBC's more conservative risk management. Interest rates were voluntarily reduced below the 20% cap. Collection practices were reformed to eliminate the harassment that had given the industry its unsavory reputation.

But SMFG was careful not to destroy what made Promise valuable. The company retained its speed advantage—loans could still be approved in under an hour. The automated lending machines, rebranded with SMBC colors, remained in convenient locations. Most importantly, the credit scoring algorithms and risk management systems that had been refined over decades continued to operate.

Building the New Business Model

The post-acquisition strategy focused on three pillars: legitimacy, integration, and innovation. Legitimacy meant operating to bank standards while maintaining consumer finance efficiency. Integration meant connecting Promise's capabilities with SMBC's broader product suite. Innovation meant using Promise as a laboratory for digital banking experiments.

Promise is one of our financing business arms. Its main offering is Free Cashing (revolving loans), which meets the various borrowing needs of individual customers. Other offerings include Card Loans for the Self-employed, which meet the funding needs of self-employed individuals, and Consolidation Loans, which aim to ease the burden on those who are repaying multiple loans.

The integration with SMBC created new possibilities. Promise customers could be offered SMBC bank accounts, credit cards, and eventually mortgages as they built credit history. SMBC customers could access quick loans through Promise's infrastructure without visiting a branch. The V Point system, a shared point reward service for the SMBC Group, created incentives for customers to use multiple products.

International Expansion: Exporting the Model

While rebuilding domestically, SMBC Consumer Finance also looked abroad. Based on our track record at PROMISE (HONG KONG), we established PROMISE(THAILAND) in 2004. PROMISE (THAILAND) operates 90 service points throughout Thailand and strives to enhance sales promotions through TV commercials and Internet advertising, aiming to become an accessible personal loan company.

The international expansion wasn't just about growth—it was about proving the model worked beyond Japan's unique context. In markets like Thailand, China, and Indonesia, millions of consumers were entering the middle class but lacked access to formal credit. SMBC Consumer Finance's ability to serve these customers profitably while maintaining acceptable risk levels validated the acquisition thesis.

Digital Transformation and Innovation

By 2015, SMBC Consumer Finance had become SMFG's digital innovation lab. The company pioneered app-based lending in Japan, allowing customers to apply, get approved, and receive funds entirely through their smartphones. In recent years, we have introduced various new services, including App Loans using our official app Promise as a platform.

The company also led SMFG's experiments with alternative data for credit scoring. Starting in January 2024, in order to respond to customers' financial needs more quickly and enhance convenience, we have introduced a service that allows customers to submit their income information via Seven Bank ATMs using their My Number Card and a "digital screening" service that completely digitizes the process from application to borrowing.

These innovations had implications far beyond consumer finance. The technologies and processes developed at SMBC Consumer Finance were gradually adopted across SMFG, accelerating digital transformation of the entire group.

Lessons Learned: The Value of Patience

The Promise acquisition story offers several crucial lessons about strategic M&A in financial services. First, timing matters less than commitment—SMFG stuck with Promise through the worst crisis in consumer finance history and emerged stronger. Second, cultural integration requires deliberate preservation of what makes acquired companies valuable—SMFG reformed Promise's excesses while maintaining its innovative DNA. Third, regulatory change creates opportunity for those with patience and capital to weather the storm.

Most importantly, the Promise acquisition demonstrated that traditional banks could successfully expand into adjacent financial services if they were willing to learn and adapt. The capabilities SMFG gained—digital lending, automated credit decisions, behavioral analytics—proved invaluable as banking itself became increasingly digital.

By 2020, SMBC Consumer Finance had evolved from controversial acquisition to core strategic asset. With over 2.5 million active customers, profitable operations across Asia, and technology leadership within SMFG, the company validated the vision that led to that first investment in 2004. The consumer finance play that had seemed risky, even reckless, had become essential to SMFG's retail banking strategy.

The transformation from Promise to SMBC Consumer Finance represents more than successful post-merger integration—it demonstrates how established financial institutions can reinvent themselves through strategic acquisitions, even in the most challenging circumstances. As SMFG looked toward the next phase of growth, the lessons learned from consumer finance would prove invaluable in navigating an increasingly digital, increasingly competitive global banking landscape.

VI. Surviving the Global Financial Crisis (2008–2009)

The emergency board meeting at SMFG headquarters on September 15, 2008, had been called for 6 AM Tokyo time—an ungodly hour that signaled the gravity of the situation. On screens around the room, Bloomberg terminals flashed red as news broke that Lehman Brothers, America's fourth-largest investment bank, had filed for bankruptcy. CEO Teisuke Kitayama and his leadership team watched in real-time as a financial tsunami that started in Manhattan began racing across the Pacific toward Tokyo.

But unlike their Western counterparts, who were discovering massive exposures to toxic subprime securities, SMFG's executives experienced an unusual emotion for bank leaders during a global crisis: relief. A quick portfolio review confirmed what they already knew—SMFG's direct exposure to U.S. subprime mortgages was minimal, less than 100 billion yen across the entire group. The conservatism that had made Japanese banks seem boring during the go-go years of 2003-2007 suddenly looked like genius.

In Japan, the business climate in general, and especially for the financial sector, became challenging starting around 1990 due to a series of unfavorable events. The stock market crash began in January 1990, followed by the collapse of the bubble economy. The total volume control for real estate loans was introduced in April of the same year. Eventually, the business cycle peaked in February 1991. Downward spirals of land and stock prices delivered a heavy blow to quite a few companies that had borrowed heavily to invest in real estate and stocks, throwing them into financial turmoil. This resulted in non-performing loans, particularly those related to real estate, piling up and being written off by lending institutions. Among those, a number of remarkably large financial institutions went bankrupt in and after 1997, which created financial instability.

Having survived their own banking crisis a decade earlier, Japanese banks had learned painful lessons about leverage, real estate exposure, and complex securities. While Citigroup, UBS, and Merrill Lynch were writing down tens of billions in subprime losses, SMFG was wondering if this crisis might actually present opportunity.

The Lehman Moment

September 2008: Lehman Brothers bankruptcy accelerates global financial crisis—this clinical description barely captures the panic that gripped global markets. In New York and London, century-old financial institutions collapsed or required government bailouts within days. Credit markets froze completely. Nobody would lend to anybody, at any price.

For SMFG, the immediate concern was operational. The bank had approximately $2 billion in exposure to Lehman through various trading relationships and derivatives contracts—manageable, but requiring careful unwinding. More concerning was the broader freeze in dollar funding markets. Japanese banks, including SMFG, relied on wholesale dollar funding for their international operations and suddenly found that market effectively closed.

But Kitayama and his team had advantages their Western peers lacked. First, SMFG's balance sheet was relatively clean—the hard work of resolving bad loans from Japan's bubble era was largely complete. Second, the bank had strong retail deposit funding in Japan, providing stable liquidity even as wholesale markets seized. Third, and most importantly, Japanese regulators and the Bank of Japan moved quickly to provide dollar liquidity through swap lines with the Federal Reserve.

The View from Tokyo

The contrast between Tokyo and New York in autumn 2008 was stark. While Wall Street firms were collapsing or merging in shotgun weddings, Japanese banks were relatively calm. The Nikkei fell sharply—from over 13,000 in September to under 7,000 by March 2009—but this felt manageable compared to the existential crisis of the 1990s.

SMFG's third-quarter 2008 earnings call was revealing. While Western bank CEOs were explaining massive writedowns and government bailouts, Kitayama could report that SMFG's subprime-related losses were just 48 billion yen, barely a rounding error on the bank's 100 trillion yen balance sheet. The bigger concern was the indirect impact: Japanese corporations were suffering as global demand collapsed, potentially creating a new wave of problem loans.

The numbers tell the story of divergent fates. While Citigroup lost $27.7 billion in 2008 and Bank of America lost $4 billion, SMFG's losses were primarily due to increased provisioning for future loan losses and mark-to-market losses on equity holdings. SMFG posts consolidated net loss of 373.5 billion yen for fiscal 2008—substantial, but manageable given the bank's capital position.

Strategic Positioning During Chaos

As Western banks retreated to their home markets, SMFG sensed opportunity. Corporate clients globally were desperate for credit as their traditional banks pulled back. Asian companies, in particular, found their European and American banking relationships suddenly unavailable. SMFG, with its strong capital position and Asian presence, could fill the void.

The bank's wholesale banking division went on the offensive. Teams were deployed across Asia to pick up relationships abandoned by retreating Western banks. In Singapore, Hong Kong, and Shanghai, SMFG hired talented bankers laid off by collapsing or retrenching competitors. The message to clients was simple: while others retreat, we're here to stay.

One symbolic victory came in project finance. As Western banks pulled back from infrastructure lending, SMFG stepped in. The bank would later win "Global Bank of the Year" six times since 2008 from Project Finance International magazine—recognition that would have been unthinkable before the crisis created opportunity.

The Domestic Challenge

While SMFG navigated the global crisis relatively well, the domestic impact was severe. Impact on Japanese economy: stock market crash and increased credit costs. Japanese exporters, the backbone of the economy, saw demand evaporate as Western consumers stopped buying. Toyota, Sony, and Panasonic all reported massive losses. The strong yen, rising as investors fled to safety, made Japanese exports even less competitive.

For SMFG, this meant a surge in credit costs as corporate borrowers struggled. The bank's consolidated credit costs rose to 935 billion yen in fiscal 2008, more than double the previous year. Unlike the bubble-era bad loans, which were concentrated in real estate, these problem loans were scattered across manufacturing, retail, and service sectors.

The consumer finance subsidiary, Promise (not yet fully owned), faced its own crisis. Already struggling with regulatory changes, the company now dealt with rising defaults as unemployment increased and overtime pay—crucial for many borrowers—disappeared. The integration challenges SMFG had anticipated became more complex in crisis conditions.

Government Response and Public Funds

The Japanese government's response to the global financial crisis was shaped by its 1990s experience. Rather than wait for problems to metastasize, authorities acted quickly. The Bank of Japan cut rates (already near zero) and expanded quantitative easing. The Financial Services Agency relaxed some accounting rules to prevent forced selling of depreciated securities.

Crucially, the government made capital injections available to banks—but with a critical difference from the 1990s. SMFG announced on October 17, 2006, that it had repaid all of its public funds. MUFG repaid the funds it had inherited from its predecessor, UFJ Bank, in June. MHFG repaid its public funds in July, which had once approached 3 trillion yen. SMFG had initially targeted repaying its public funds by the end of the fiscal year, but it moved up the repayment schedule out of concern that it would be "half a lap behind" the other megabanks.

Having repaid public funds in 2006—ahead of schedule and ahead of competitors—SMFG had the credibility to resist pressure for new government capital. This was more than pride; accepting public funds again would signal weakness and potentially limit strategic flexibility. The bank chose instead to raise capital privately, including a controversial $1.8 billion preferred share issue to the government of Singapore in February 2009.

Learning from Lehman

The Lehman bankruptcy offered SMFG valuable lessons about interconnected global finance. The bank's relatively small direct exposure masked larger indirect risks through counterparty relationships, trade finance, and currency swaps. The crisis revealed how quickly liquidity could evaporate and how correlation increased during stress—all assets except government bonds and gold fell together.

SMFG's risk management evolved significantly post-crisis. Stress testing became more severe and more frequent. Liquidity buffers were increased. Most importantly, the bank developed better early warning systems for identifying bubbles and excessive risk-taking, whether in Japanese real estate or American subprime mortgages.

The crisis also validated SMFG's universal banking model. While pure investment banks like Lehman collapsed and pure commercial banks struggled with trading losses, diversified institutions weathered the storm better. SMFG's mix of commercial banking, consumer finance, leasing, and securities provided multiple revenue streams and natural hedges.

Competitive Dynamics Shift

The global financial crisis fundamentally altered competitive dynamics in international banking. Before 2008, Japanese banks were often viewed as second-tier players globally—solid but unexciting, conservative to a fault. After 2008, that conservatism became a valuable brand attribute.

European banks, devastated by the crisis and subsequent Eurozone problems, retreated from Asia. American banks, facing new regulations and political pressure, focused on domestic markets. Chinese banks, while growing rapidly, lacked international experience and faced trust issues. This created space for Japanese banks to expand internationally, particularly in Asia.

SMFG's strategic response was measured but ambitious. Rather than dramatic acquisitions of distressed competitors—a strategy that rarely works in banking—the bank focused on organic growth and small, strategic purchases. Hiring teams from retreating competitors. Building out product capabilities in areas like cash management and trade finance. Gradually expanding the geographic footprint.

The Securities Opportunity

One unexpected benefit of the crisis was the opportunity it created in securities and investment banking. The collapse or forced merger of major Wall Street firms—Lehman, Bear Stearns, Merrill Lynch—created opportunity for survivors. In Japan, foreign securities firms that had dominated certain markets suddenly retreated or disappeared.

This set the stage for what would become one of SMFG's most important strategic moves: the acquisition of Nikko Cordial Securities. In October 2009, in the depths of the crisis, SMFG acquired Nikko from Citigroup, which desperately needed capital. The price—approximately 545 billion yen—seemed expensive during a crisis, but would prove a bargain as markets recovered.

Recovery and Lessons

By mid-2009, the acute phase of the crisis had passed. Markets began recovering, credit spreads narrowed, and something approaching normal banking resumed. For SMFG, the crisis had been painful—the 373.5 billion yen loss in fiscal 2008 was the worst since the merger—but not existential.

More importantly, the bank emerged from the crisis stronger competitively. While Western banks spent the next decade dealing with regulatory sanctions, litigation, and restructuring, SMFG could focus on growth. The bank's reputation for stability attracted new clients. Its strong capital position allowed opportunistic investments. Its Asian franchise, already strong, became a key differentiator.

The global financial crisis also validated a crucial strategic insight: in banking, surviving crises matters more than maximizing returns during booms. SMFG's conservative culture, often criticized during the boom years for missing opportunities, had proven its value when markets turned. The bank that seemed boring in 2007 looked brilliant by 2009.

Setting the Stage for Expansion

As 2009 drew to a close, SMFG's leadership began planning for the post-crisis world. The competitive landscape had been fundamentally altered. Regulatory changes would create new compliance costs but also barriers to entry. Technology was becoming increasingly important as customers demanded digital services. Asia's growth trajectory, temporarily interrupted by the crisis, would resume and likely accelerate.

The strategic priorities that emerged from this planning would drive SMFG's next decade: build out securities and investment banking capabilities through Nikko Cordial; expand in high-growth Asian markets; invest in technology and digital transformation; maintain conservative risk management while seeking profitable growth; use the strong balance sheet for strategic acquisitions.

The global financial crisis had been a near-death experience for global banking but merely a stress test for SMFG. Having passed that test, the bank was ready to move from defense to offense. The next phase would see aggressive expansion into securities, strategic acquisitions across Asia, and eventually, transformation into something its founders could never have imagined: a digital-first, Asia-focused, globally significant financial services platform. The crisis that had destroyed so many competitors had become SMFG's opportunity to leap forward.

VII. The Securities & Global Expansion Era (2009–2015)

The morning of May 1, 2009, represented a watershed moment in Japanese securities history. In a conference room high above Tokyo's financial district, executives from Sumitomo Mitsui Financial Group and Citigroup signed documents that would fundamentally reshape Japan's capital markets landscape. SMBC would acquire Nikko Cordial Securities and other businesses from Citigroup for 545 billion yen—a price that seemed steep in the depths of the global financial crisis but would prove prescient as markets recovered.

The acquisition wasn't just about buying a securities firm—it was about transformation. Citigroup, subject to a bailout with injection of public funds related to the financial crisis, announced large-scale business restructuring plans that included the sell-off of retail securities and asset management businesses. For SMFG, this represented the opportunity they'd been waiting for: a chance to build a full-service investment banking capability that could compete with global giants.

The Nikko Cordial Prize

In October 2009, Nikko Cordial Securities became a wholly owned subsidiary of SMBC, and in April 2011, changed its name to SMBC Nikko Securities Inc. The strategic logic was compelling. By adding New Nikko Securities based on Nikko Cordial as a new group partner, SMFG would gain access not only to Nikko Cordial's ¥24 trillion in financial assets under account, but also approximately 3,000 high-quality sales personnel who served as the foundation for its advanced consulting services, a branch office network with 109 locations nationwide, and a reputable online trading channel.

This wasn't SMFG's first attempt at securities expansion. SMFG and Daiwa Securities Group announced in September 2009 the agreement on the dissolution of their joint venture as of December 31, 2009, which was an outcome of failed efforts to reconcile differences in basic concepts concerning the management policies of the venture. The failure of the Daiwa Securities SMBC joint venture made the Nikko acquisition even more critical—it was SMFG's chance to control its securities destiny rather than rely on partnerships.

The integration challenges were immense. Nikko Cordial Securities had developed its business mostly on domestic retail services, with overseas operations at almost zero, before it became a wholly owned subsidiary of SMBC in October 2009. SMFG needed to build international capabilities from scratch while preserving the domestic franchise that made Nikko valuable.

The NYSE Listing: Coming of Age

Eleven months after completing the Nikko acquisition, SMFG achieved another milestone that would have seemed impossible during the dark days of Japan's banking crisis. SMFG was listed on the New York Stock Exchange (NYSE) on November 1, 2010. This was a long-term goal accomplished after years of preparations which started when SMFG completed the repayment of public funds injections in October 2006.

The NYSE listing represented more than access to capital—it was a declaration of global ambition. SMFG acknowledged benefits of listing on the NYSE, such as that the company gained excellent credentials for the transparency and soundness of management by passing the stringent listing eligibility criteria applied by the U.S. Securities and Exchange Commission (SEC). For a Japanese bank that had survived its own crisis and the global financial meltdown, meeting SEC standards validated its recovery.

At the reception held in New York City to celebrate the company's listing on the NYSE in its tenth year since the merger, President Kitayama described the significance of the event as a "cornerstone for our endeavor to become a globally competitive financial services group". The timing was symbolic—exactly a decade after the emergency merger that created SMBC, the institution was ready to compete on the global stage.

The Aviation Gambit

While securities represented SMFG's push into capital markets, the 2012 acquisition of RBS Aviation Capital demonstrated ambition in specialized finance. In 2012, the company was acquired by the Japanese consortium for $7.3 billion, which was the largest ever global sale of an aircraft leasing business. The sale completed on 1 June 2012 and the business was renamed SMBC Aviation Capital.