People's Insurance Company of China: The Original Dragon of Chinese Insurance

I. Introduction: The 75-Year Survivor

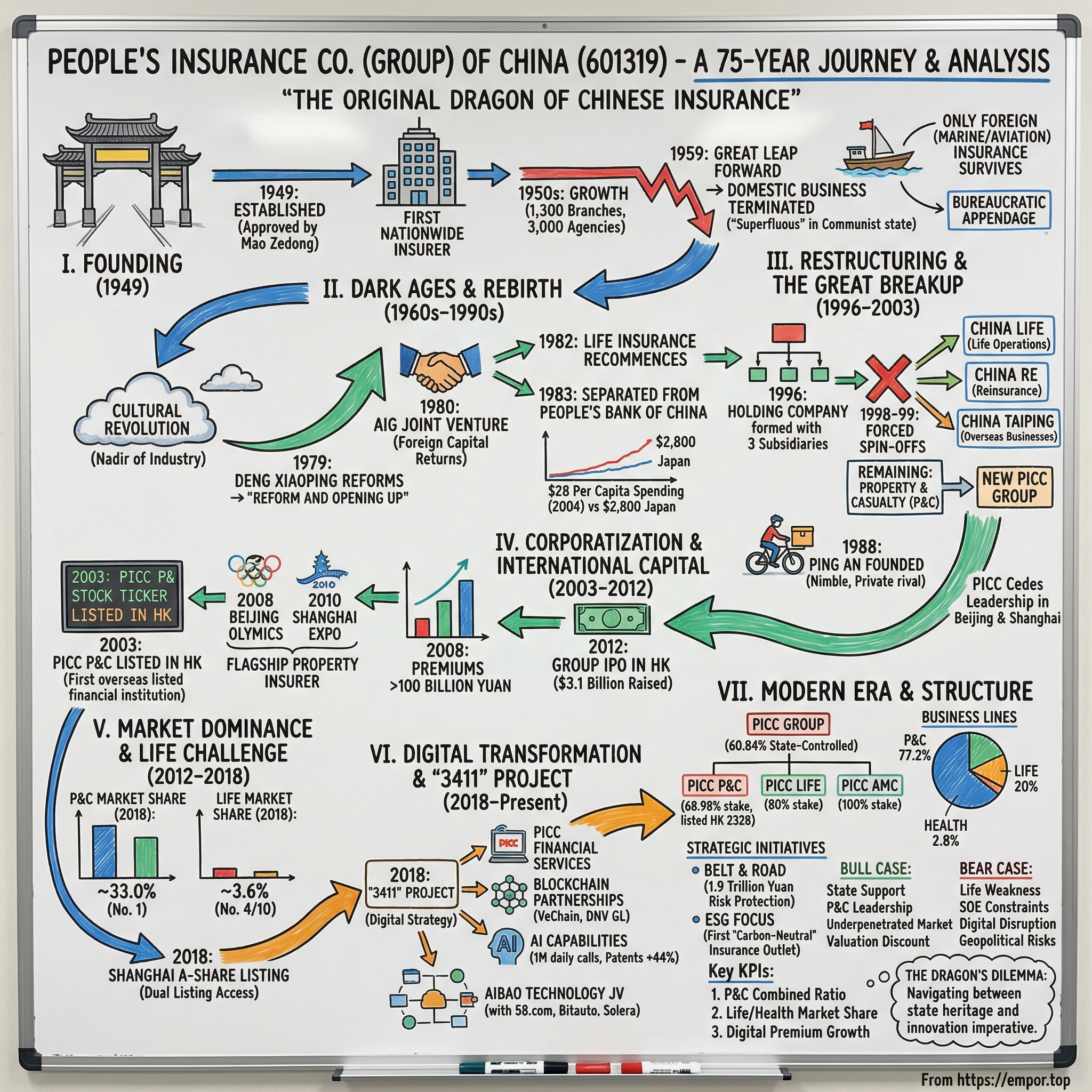

Picture this: October 1949. The People's Liberation Army has just finished securing the mainland after years of civil war. Chairman Mao Zedong stands at Tiananmen Gate, proclaiming the birth of the People's Republic of China. In those same days, amid the chaos of nation-building, a handful of bureaucrats gathered in Beijing to create something that would outlast revolutions, political purges, and market disruptions—China's first insurance company.

"Approved by MAO Zedong and other central leaders, the People's Insurance Company of China was founded on October 1, 1949. It is renowned as 'the eldest son of the insurance industry of new China,' as the pioneer and founder of insurance undertaking nationwide."

Today, PICC stands as one of the most remarkable corporate survivors in modern Chinese history. The Company ranked 158th in the Fortune Global 500 (2024), a position it has maintained for fifteen consecutive years. But this ranking barely scratches the surface of what makes PICC worthy of deep examination.

Founded in 1949, PICC is China's first nationwide insurer and has 2.42 million institutional insurance clients and about 130 million individual insurance customers—more than the entire population of Japan. The People's Insurance Company (Group) of China Limited (PICC Group) is controlled by the central government through the Ministry of Finance of the People's Republic of China, which holds a 60.84% stake, ensuring dominant influence over strategic decisions.

The central question of this analysis: How did the first insurance company founded alongside the People's Republic survive the Cultural Revolution, government breakups, and digital disruption to remain a market leader 75 years later?

The answer lies at the intersection of state capitalism, market liberalization, regulatory navigation, and the ongoing battle between legacy incumbents and digital-native disruptors. PICC's story is not merely corporate history—it is a window into how China's economic transformation actually works at the enterprise level.

II. Founding Era: Birth of a Nation, Birth of an Industry (1949–1959)

To understand PICC's founding, one must first understand what it replaced. By then, China boasted more than 240 insurance companies—some 180 of which were Chinese owned. Following the revolution, the Mao government set up the People's Insurance Company of China (PICC), which took over all insurance interests on the mainland.

The consolidation was total and swift. PICC was founded in 1949 as The People's Insurance Company of China, as a subsidiary of the People's Bank of China. This was not a market-driven merger—it was revolutionary nationalization, absorbing the assets of pre-1949 insurers into a single state-controlled entity.

The early growth was remarkable for a nascent communist state. By 1952, PICC had built a national network of 1,300 branches and 3,000 agency outlets—an astonishing feat of institution-building in a country still recovering from war and facing international isolation. The company represented Mao's vision of insurance as a state function, not a capitalist enterprise.

But ideology would soon trump practicality. "During the three decades from 1949 to 1979, there was not sufficient recognition of the role of the insurance industry in China, and the insurance industry grinded to a halt."

The turning point came during the Great Leap Forward. In 1959, the Chinese government, in its fervent effort to transform the nation into a communist utopia, determined that insurance was superfluous in a state where the government was meant to provide all social welfare for its citizens. All domestic insurance business was terminated.

"Insurance operations are abolished, except for foreign (marine and aviation) insurance needs, and PICC becomes a department of the central bank."

PICC's role was reduced to providing coverage for the country's foreign policy needs—marine cargo for exports, aviation for international flights, essentially the insurance equivalent of diplomatic passports. The company became a bureaucratic appendage, surviving only because China needed some interface with international commerce.

For investors today, this period illustrates a fundamental truth about PICC that persists: the company exists at the pleasure of the state. Its survival through the 1950s came not from commercial viability but from geopolitical necessity. This DNA has never been fully altered.

III. The Dark Ages & Rebirth (1959–1990s)

The Cultural Revolution (1966-1976) represented the nadir of China's experiment with radical communism—and the near-death experience for insurance as an industry. "The last foreign insurance company was closed in 1953 as the government first imposed substantial deposit requirements on insurance companies, and then imposed heavy taxation. In 1953, the private Chinese insurance companies were consolidated into Taiping Insurance Co., which was effectively an arm of PICC."

For nearly two decades, domestic insurance essentially did not exist in China. The concept itself was ideologically suspect—why would socialist citizens need protection from risk when the state provided everything?

The resurrection came from an unlikely source: Deng Xiaoping's economic reforms. "In 1965, PICC was re-established." But this was merely institutional survival. The true rebirth began in 1979, when Deng launched his "Reform and Opening Up" policy.

"China's insurance industry was revived following the country's economic opening up in the late 1970s. In 1979, PICC was reinstated."

The separation from the central bank formalized PICC's commercial character. "In 1983, it was separated from the People's Bank of China as a separate entity that under the supervision of the State Council of the People's Republic of China."

"In 1980, as the first initiatives to bring foreign investment capital in the country emerged, PICC formed a joint venture with American Insurance Group—allowing the American company to test the waters before making a broader return to the mainland insurance market in the 1990s."

This AIG partnership is historically significant. It marked the first time a foreign insurer had any formal presence in mainland China since the revolution. AIG would become a recurring character in PICC's story—sometimes partner, sometimes competitor, eventually cornerstone investor.

"PICC began offering life insurance policies again in 1982, targeting the small but growing numbers of middle-class and wealthy Chinese, as well as government officials. Nonetheless, the Chinese life insurance market remained tiny—as late as 2004, per capita spending on life insurance amounted to the equivalent of just $28, compared with average per capita spending of as much $2,800 or more in Japan, offering tantalizing prospects for future growth."

This gap—$28 versus $2,800—encapsulates both the challenge and the opportunity that would define PICC's next four decades. China was spectacularly underinsured, and whoever could tap that market would access one of the largest pools of unmet demand in financial services history.

IV. Restructuring & The Great Breakup (1996–2003)

The mid-1990s brought a regulatory revolution that would fundamentally reshape PICC—and not entirely to its benefit. The government decided that China's insurance industry needed modernization, specialization, and eventually, competition.

"In 1996, it became a holding company, as People's Insurance Company (Group) of China. Three subsidiaries were formed, as property insurer, life insurer and reinsurer respectively."

This restructuring seemed rational from a regulatory perspective—separating life and non-life insurance into distinct entities followed international best practices. But what came next was genuinely seismic.

"However, in 1998–99, China Life and China Re were spin-off from the group, while the overseas businesses, belongs to yet another former subsidiary, now known as China Taiping Insurance Group Limited. After the split, The property insurer of the group assumed as the new holding company of PICC group, and named The People's Insurance Company of China again. The regulator of the company, China Insurance Regulatory Commission, also established in 1998."

This was not merely a corporate reorganization—it was a forced dismemberment. PICC lost its life insurance operations to what became China Life Insurance Company, which would grow into one of the world's largest life insurers by market capitalization. It lost its reinsurance arm to China Re. It lost its overseas operations to what became China Taiping.

What remained was the property and casualty operation—significant, but no longer the integrated insurance powerhouse it had been.

The regulatory rationale was clear: under new rules, insurance companies were prohibited from operating in both the non-life and life insurance markets. But the practical effect was to create new competitors from PICC's own flesh.

The competitive disadvantage went deeper. "At the time of the sharp economic turnaround in the late 1970s, the state-owned People's Insurance Company of China (PICC), which had a market monopoly in China, had a limited range of products that stopped short of meeting the new needs of both Chinese and foreign companies... To meet this pressing need for coverage, Peter Ma, founder and Chairman of Ping An, seized the opportunity to create a private insurance company."

Ping An Insurance, founded in 1988 by Peter Ma in Shenzhen, represented a new model—nimble, technology-focused, and unencumbered by state-owned enterprise bureaucracy. "Ping An staff had to cycle around town and knock on the doors of every potential client to pitch business, aiming to achieve the goal of RMB5 million in insurance premiums a year, merely one-thousandth of the premiums earned by PICC at the time."

But that hungry startup mentality translated into market gains. "It has already surpassed PICC as the number one life insurer in Beijing and Shenzhen. In addition to overtaking China Pacific Insurance Company as the number two insurer in China, Ping An possesses the unusual ability to deal in other financial services."

The arrival of AIG had introduced a new tied-agency system into the Chinese market, encouraging the development of branch networks. Yet PICC, as a state-owned enterprise, was initially constrained in developing its own network of branch offices and tied agents. As a result, the company ceded the leadership spot in two of the country's most important markets—Beijing to Ping An, and Shanghai to China Pacific.

For investors, the 1996-2003 period established a pattern that continues today: PICC dominates property and casualty insurance but struggles in life insurance, the higher-margin, faster-growing segment that competitors have captured.

V. Corporatization & International Capital (2003–2012)

The early 2000s marked PICC's transformation from state bureaucracy to publicly traded corporation—though the state never loosened its grip on the steering wheel.

"A new subsidiary PICC Property and Casualty (PICC P&C) was established in July 2003 (effective date backdated to September 2002) from the former property and casualty insurance division of the PICC Group. In July 2003, the People's Insurance Group founded the People's Property & Casualty Insurance Company of China (PICC P&C), with a registered capital of 12.25598 billion yuan."

"In 2003, PICC Property and Casualty Company Limited (stock code 02328) was successfully listed in Hong Kong Stock Exchange, becoming the first domestic financial institution listed overseas."

This IPO was a landmark moment—not just for PICC, but for China's financial sector. It demonstrated that state-owned financial enterprises could access international capital markets while remaining under government control.

"US-based multinational insurer American International Group (AIG) was the cornerstone investor in the 2012 IPO, as well as in 2003 for the IPO of the subsidiary PICC P&C." AIG's dual role—investing in both the 2003 subsidiary IPO and the later group IPO—reflected both strategic positioning and a bet on China's insurance growth story.

The years between the two IPOs saw PICC establish itself as a national institution. PICC P&C became the insurance partner for the 2008 Beijing Olympics and the 2010 Shanghai Expo—prestige assignments that cemented its brand as China's flagship property insurer. In 2008, its premium income exceeded 100 billion yuan, making it the first property insurance company in mainland China to achieve this milestone and entering the top 10 global property insurance companies by business volume.

"PICC Holding reverted to the name People's Insurance Company Group of China in 2007. The company also re-incorporated as a joint stock company with limited liabilities in 2009."

The group IPO finally came in December 2012. "State-owned insurer PICC started meeting institutional investors in Hong Kong on Thursday to gauge demand for the IPO, braving a slump this year in equity deals."

The timing was challenging. "People's Insurance Company (Group) of China (PICC), one of China's largest insurers, is tapping the Hong Kong equity market at a time when IPO volumes in the financial center have tumbled more than 80 percent. PICC will be the biggest Hong Kong IPO since another insurer, AIA Group Ltd, raised $20.5 billion in 2010."

"PICC secured commitments from cornerstone investors for about $1.8 billion worth of stock offered in the IPO, easing concerns it may not find enough demand for the deal. Major investors included U.S. insurer American International Group (AIG), China utility State Grid Corp, the country's leading gold miner Zijin Mining Group and China Life Insurance."

"U.S. insurer AIG was added to the list of cornerstone investors who initially signed up, pledging $500 million to the IPO."

The deal ultimately priced near the bottom of its range, raising $3.1 billion. "Chinese state-owned insurer PICC Group raised $3.1 billion in Hong Kong's biggest initial public offering in two years after pricing the deal near the bottom of an indicative range, the latest sign of a tepid appetite for new listings in much of Asia."

For long-term investors, the 2003-2012 period established PICC's capital market access while highlighting a persistent challenge: international investors remained somewhat skeptical of Chinese state-owned insurers, demanding discounts to comparable valuations in other markets.

VI. Market Dominance & The Life Insurance Challenge (2012–2018)

The years following the Hong Kong listing revealed both PICC's enduring strengths and stubborn weaknesses. The company dominated property and casualty insurance—"As of 2018, the market share of PICC P&C in its sector is 33.0%."

"According to S&P Global Ratings citing China Insurance Regulatory Commission, PICC P&C's market share (by direct premium) in property and casualty insurance in the first half of year 2017 was 34.0% and ranked the first. The second was Pingan Insurance (19.6%)."

One-third market share in the world's largest P&C market is an extraordinary position. But the story in life insurance told a different tale.

"As of 2018, the market share of PICC Life in its life insurance sector is 3.6%. While according to S&P Global Ratings, PICC Life's market share (by policy written) in life insurance market in the first half of year 2017 was 4.3% and ranked 4th (10th in 2016)."

The disparity is striking: 34% in P&C, less than 4% in life. This imbalance meant PICC was dominant in the slower-growing, lower-margin business while competitors captured the higher-growth life and health segments.

The Shanghai A-share listing, long planned, finally materialized in 2018. "The People's Insurance Company (Group) of China (PICC), China's oldest insurance company, gained final approval on Tuesday for a Chinese mainland listing after years of applications, in a deal valued at about $2.4 billion. The country's top non-life insurer will issue up to 4.6 billion shares in its Shanghai listing, representing about 9.78% of its total."

"PICC will be joining four other major insurers, including Ping An Insurance and China Life Insurance, to be listed in both Hong Kong and the domestic A-share market. It will be the first insurance IPO on the A-share market since 2011."

The dual listing gave PICC access to both international and domestic capital markets—important for a company whose growth requires continuous capital infusion to meet regulatory solvency requirements.

But the life insurance challenge remained unresolved. PICC Life Insurance struggled to undergo transformation to pursue new business value growth, caught between the need for scale and the competitive pressure from nimbler rivals.

VII. Digital Transformation & The "3411" Project (2018–Present)

The late 2010s brought an existential question to PICC's doorstep: How does a 70-year-old state-owned enterprise compete against technology giants?

"In 2018, PICC Group released the '3411' project, implemented the innovation driven development and digital strategy, strengthened the innovation guidance, and promoted the quality transformation and development of the industry."

"As a part of the strategic disposition of PICC Group in the field of Fintech, PICC Financial Services actively explores the path of insurtech innovation. This time, in response to the requirements of the national financial supply side structural reform and in-depth promotion of the transformation of innovation driven development strategy to productivity, PICC Financial Services cooperates with Plug and Play China to build the 'Insurance and Innovation Space' to become the first insurtech accelerator in China."

The blockchain partnership announced in September 2018 illustrated PICC's approach to technology: partner with specialists rather than build internally. "People's Insurance Company of China (PICC) enters into a partnership relationship with DNV GL and VeChain to bring digital transformation to the insurance industry."

"PICC believes that blockchain technology can bring digital transformation, resulting in reduced turnaround time, premiums, prevent fraud and improve KYC compliance and claim experience."

"PICC said the partnership will enable it to provide robust assured solutions that protect user data, distribute ownership and enhance existing artificial intelligence (AI). PICC is one of the largest P&C insurers globally with $126bn total assets."

The Aibao Technology joint venture, established in 2017, represented a different approach. "Aibao Technology was established in 2017 as a joint venture of the People's Insurance Company of China (PICC), domestic privately owned technology companies 58.com and bitauto.com, and a US-based software company Solera."

"Aibao focuses primarily on developing technological solutions for PICC and China's leading insurance companies. PICC takes one third of the insurance market of the country so at a strategic level, the Aibao company is putting an emphasis on cooperation with PICC … the top ten insurance companies have taken about 70% of the whole insurance market."

"Aibao Insurance Technology's startup team underwent a year of incubation and received investments totaling RMB 200 million from PICC Financial Services, Bitauto, 58 Group, and Solera Holdings (United States)."

More recently, "PICC Property & Casualty Co has inked a deal with Aibao Technology to enhance its customer services, focusing on motor vehicle insurance and online activities. This agreement, effective from January 2025, aims to provide value-added services and online advertising, with an estimated annual service fee cap of RMB800 million."

The Group has continued building AI capabilities. In the first half of 2024, the daily average calls of the intelligent technology service platform exceeded 1.00 million. The Group reorganized its science and technology innovation laboratory, and in the first half of 2024, the number of patent applications within the Group increased by 44% year-on-year. The Group has vigorously promoted the construction of a large model ecosystem, completing the pilot launch of products such as "PICC Zhiyou" and "PICC Zhiwen."

For investors, PICC's digital transformation strategy raises the classic incumbent dilemma: Can a large, bureaucratic, state-owned enterprise genuinely innovate, or is it destined to be a fast follower at best? The evidence suggests PICC is taking the threat seriously but remains behind pure digital players in execution speed.

VIII. Modern Era: Strategic Initiatives & ESG Focus (2020–2025)

The Belt and Road Initiative has become central to PICC's strategic positioning. "In recent years, PICC HK has proactively provided its service under the 'Belt and Road Initiative', and has successively participated in landmark projects including Hong Kong-Zhuhai-Macao Bridge, Nam Ou River Hydropower Plants in Laos, Kamchay Hydropower Plants in Cambodia."

"We also played a pivotal role in supporting the Belt and Road Initiative, providing 1.9 trillion yuan in risk protection for overseas investments and infrastructure projects, expanding our international business footprint to over 140 countries and regions."

"Starr Insurance Companies today announced a cooperation with PICC Health Insurance Company Limited (PICC Health) to provide industry-leading, innovative insurance for Chinese company employees working overseas in Belt & Road Initiative (BRI) countries."

"Chubb Limited today announced that it has entered into a strategic cooperation agreement with PICC Property & Casualty Company of China that will leverage Chubb's global capabilities in support of PICC's customers and other Chinese-affiliated companies around the world in line with the Chinese government's drive to promote the country's 'Going Out' and 'One Belt One Road' initiatives."

ESG leadership has become another strategic pillar. "PICC is committed to harmonious coexistence with nature, actively driving green finance and insurance to foster a sustainable future. As a pioneer in green finance standards, we drove the China Belt and Road Reinsurance Pool in releasing the Green Investment Principles for the Belt and Road, setting industry benchmarks."

PICC innovated green insurance products, launching China's first Photovoltaic Power Sales Credit Compensation Insurance and Energy Storage System Long-Term Quality and Performance insurance. The company has established a unified green insurance statistical system and an ESG risk assessment system for insurance clients—firsts for the industry.

"It was the first 'carbon-neutral' insurance outlet of PICC and in China."

The recent partnership activity has continued: "December 2024: Zhibao Technology partnered with PICC and Munich Re to launch AI-based medical products tailored to middle-class needs, combining local data with global reinsurance capacity."

IX. Current Business Performance & Structure

"The company reported original premiums income of CNY693,015 million for the fiscal year ended December 2024 (FY2024), an increase of 6.7% over that in FY2023."

"The People's Insurance Company (Group) of China Limited is an insurance group organised around 3 business lines: - non-life insurance (77.2% of gross written premiums); - life insurance (20%); - health insurance (2.8%)."

"The Company operates its property and casualty ('P&C') insurance business in the PRC through PICC P&C (listed on the Hong Kong Stock Exchange, stock code: 2328, in which the Company holds approximately 68.98% equity interests) and operates P&C insurance business in Hong Kong and Macau of China through PICC Hong Kong (in which the Company holds approximately 89.36% equity interests). The Company operates its life and health insurance businesses through PICC Life and PICC Health, in which the Company, directly and indirectly, holds 80.00% and approximately 95.45% equity interests, respectively. The Company centrally and professionally utilises and manages most of its insurance assets through PICC AMC, in which the Company holds 100% equity interest."

"The Group's business development continued to improve. In the first half of 2024, the insurance revenue recorded RMB261,629 million, representing a year-on-year increase of 6.0%, and the original premiums income recorded RMB427,285 million, representing a year-on-year increase of 3.3%. In terms of the P&C insurance business, the business scale of PICC P&C grew steadily."

"The assets under management for the second-pillar annuity exceeded RMB600.0 billion, representing an increase of 4.9% compared to the beginning of 2024."

PICC AMC, the asset management subsidiary, employs a range of financial instruments to optimize returns on insurance funds. As of the end of 2023, PICC AMC oversaw assets under management totaling approximately 2.5 trillion yuan.

"The interim dividend of RMB 0.12 per share for H1 2024 and a 45% year-on-year rise in Q1 2025 EPS (RMB 0.29) further validate its ability to generate consistent cash flows. This stability contrasts with peers in the insurance sector, many of which face pressure from low interest rates and regulatory uncertainties."

X. Competitive Landscape Analysis

The Chinese insurance market structure presents a concentrated but contested landscape. "Despite the opening of the market to foreign insurers, the Chinese insurance landscape remains strongly dominated by four national giants: Ping An, China Life, PICC, China Pacific Insurance. In 2021, they accounted for 53.5% of the local market."

"The market shows moderate concentration. PICC P&C, Ping An, and China Pacific lead volumes, but the combined share of the top five carriers is more than half of the premium share, confirming space for agile challengers."

The Ping An Challenge

"Two of the Chinese insurance companies, Ping An Insurance and China Life Insurance, are among the top five largest insurance companies in the world according to market capitalization."

"Ping An Insurance Group started off in 1988 as a property and casualty insurance company, later diversifying into insurance, banking, asset management, financial services and healthcare services. Ping An has licenses to offer financial services, including insurance, banking, trusts, securities, futures and financial leasing. Ping An has also adopted an integrated financial model on a mix of business lines, including life insurance, P&C insurance, banking and securities."

"China Life Insurance (brand value up 5% to USD18.3 billion), ranked 4th, and PICC (brand value up 13% to USD15 billion), ranked 8th, also secured places in the top 10 most valuable insurance brands globally."

The Digital-Native Threat

"Digital-native ZhongAn lifted premium 24.7% in 2024 by white-labelling its policy-admin stack to incumbents, exemplifying competition on technology rather than balance-sheet heft."

"Ping An, harnessing its universal-banking ecosystem, adeptly cross-sells policies spanning wealth management, loans, and healthcare services. ZhongAn, a frontrunner in pure online distribution, swiftly rolls out micro-duration covers in mere days, due to its cloud-native architecture. Ant Insurance Services, capitalizing on Alipay's vast user base of 1 billion, drives the Chinese online insurance market towards a focus on contextual, event-based products. Meanwhile, traditional powerhouses like PICC and China Pacific, in a bid to safeguard their market share, are modernizing their legacy systems in collaboration with AI partners."

"ZhongAn Online P&C Insurance Co. Ltd. is a Chinese online-only insurance company. Founded in 2013, the company's headquarters are based in Shanghai, China... The company's CEO is Jin 'Jeffrey' Chen but was initially co-founded by China's most notable business magnates- the chairmen of Chinese multinational conglomerates. This includes Alibaba's Jack Ma, Tencent's Pony Ma and Ping An Insurance's Mingzhe Ma."

"ZhongAn was able to scale up quickly by embedding itself in the ecosystems of its founding investors Alibaba (e-commerce), Ping An (insurance) and Tencent (social platforms including WeChat). There is a similarity between ZhongAn's business model and Google's original web search and transaction model."

Market Dynamics

"The China insurance market size was valued at USD 731.04 billion in 2024. The market is projected to grow from USD 779.22 billion in 2025 to USD 1,409.62 billion by 2032, exhibiting a CAGR of 8.8% during the forecast period."

"The China Property And Casualty Insurance Market is expected to reach USD 302.71 billion in 2025 and grow at a CAGR of 10.54% to reach USD 499.61 billion by 2030."

XI. Porter's Five Forces & Hamilton's Seven Powers Analysis

Porter's Five Forces

1. Threat of New Entrants: MODERATE-LOW

"C-ROSS II capital rules pressure sub-scale players, raising merger chatter and potential inorganic expansion for market leaders."

"The 2025 NFRA framework grants streamlined digital-only charters, lowering capital hurdles and enabling technology-native firms to enter the China online insurance market quickly."

The regulatory framework creates barriers through capital requirements under C-ROSS II (China Risk Oriented Solvency System), but digital-only licenses offer lower-cost entry for technology-native firms. The net effect is moderate barriers for traditional insurers but lower barriers for specialized digital players.

2. Bargaining Power of Suppliers: LOW

Reinsurance capacity remains available from global players including Munich Re and Swiss Re. PICC's scale gives it substantial leverage in reinsurance negotiations. Capital markets access through dual Hong Kong and Shanghai listings provides financing flexibility. Technology partnerships with multiple vendors (VeChain, Aibao, Plug and Play) prevent lock-in.

3. Bargaining Power of Buyers: MODERATE-HIGH

"By customer type, government and state-owned enterprises supplied 33.2% of the premium in 2024; small and medium enterprises recorded the fastest gain at 6.52% CAGR to 2030."

Framework tenders for government and SOE contracts typically bundle property, liability, and business-interruption clauses, with competitive bidding that compresses margins. Large corporate clients wield significant negotiating leverage. Individual consumers have become increasingly price-sensitive with the proliferation of digital comparison tools and embedded insurance offers.

4. Threat of Substitutes: MODERATE (Rising)

"WeChat and Alipay embed micro-insurance offers within daily payments, pushing the China online insurance market toward friction-free purchase journeys."

The mutual aid phenomenon—particularly Ant Group's Xiang Hu Bao, which at its peak amassed over 100 million participants—demonstrated that Chinese consumers would adopt insurance substitutes. Although regulators shut down many mutual aid schemes, the underlying demand for alternative risk-sharing persists.

Government social safety nets continue expanding, potentially reducing demand for basic protection products. However, health and pension insurance demand driven by aging demographics may offset this.

5. Competitive Rivalry: HIGH

"However, insurers are facing challenges in terms of competition, regulatory complexity, and the impact of calamity events. While the industry offers considerable growth potential, it also has challenges, such as competitive pressure and exposure to disaster risks."

Motor insurance, which accounts for approximately 55% of P&C insurance revenue, faces intense price competition following regulatory reforms. Technology investment has become an arms race among major insurers.

Hamilton's Seven Powers Analysis

1. Scale Economies: STRONG

"PICC uses a nationwide branch grid and close government ties to secure infrastructure contracts."

With 33%+ market share in P&C insurance, PICC enjoys significant underwriting data advantages and distribution network economies. The company's position as the default insurer for major state infrastructure projects creates scale advantages that smaller competitors cannot replicate.

2. Network Effects: MODERATE

Traditional insurance has limited direct network effects, but PICC's ecosystem partnerships—particularly through Aibao Technology's integration with 58.com and Bitauto's platforms—create indirect network effects in automotive insurance. The 130 million+ individual customers generate data network effects that improve underwriting accuracy over time.

3. Counter-Positioning: WEAK

PICC cannot credibly counter-position against digital disruptors because its state-owned nature prevents the kind of radical business model innovation that would cannibalize existing channels. Competitors like ZhongAn can build entirely digital operations without legacy branch infrastructure constraints.

4. Switching Costs: LOW-MODERATE

Insurance products are generally commoditized, particularly in motor and property lines where PICC dominates. Corporate accounts have moderate switching costs due to relationship depth and bundled services. Individual policies have minimal switching costs.

5. Branding: STRONG

As China's oldest insurer with "People's" in its name, PICC carries significant brand equity in state-related business. The Olympic and World Expo partnerships reinforced brand prestige. However, brand strength varies by segment—stronger in commercial lines, weaker in consumer-facing digital channels where newer brands may have more appeal to younger customers.

6. Cornered Resource: MODERATE

PICC's state-ownership creates privileged access to government contracts and Belt and Road projects, but this is a two-edged sword that also constrains strategic flexibility. "Additional control mechanisms include the embedding of Communist Party of China (CPC) committees within PICC Group's governance framework, which enforce ideological alignment and vet key appointments, such as executives and board members, to prioritize national objectives over purely commercial ones."

7. Process Power: MODERATE

Claims processing and underwriting capabilities have improved through technology investments, but PICC lags pure digital players. "Ping An and ZhongAn deploy machine-learning engines that underwrite 90% of standard proposals in under 30 minutes and settle most motor claims within 3 hours." PICC is working to match these capabilities but has not yet achieved comparable process advantages.

XII. Bull Case & Bear Case

Bull Case

State Support as Competitive Moat: PICC's position as a central government-controlled entity provides implicit support and preferential access to major infrastructure and SOE contracts. As Belt and Road projects expand and domestic infrastructure investment continues, PICC remains the default insurer for state-affiliated risk.

Market Leadership in P&C: With 33%+ market share in China's P&C market, PICC benefits from underwriting data advantages, distribution scale, and brand recognition that would take decades for competitors to replicate.

Underpenetrated Market: "China's personal insurance market is expected to grow in the range of 5% to 10% by 2035... Given the country's aging population, its heightened interest in health and wellness in the wake of the COVID-19 pandemic, and a prevailing low interest rate environment, China's personal insurance sector is poised for a growth spurt."

Valuation Discount: "PICC's current dividend yield of 4.28% exceeds the sector average of 3.6%, offering income-oriented investors an attractive entry point. Its price-to-book (P/B) ratio of 0.82—a 12% discount to its five-year average—suggests undervaluation relative to historical norms and regional peers."

Digital Transformation Progress: The "3411" project, Aibao partnership, and blockchain initiatives demonstrate management's recognition of technology imperatives. Patent applications increased 44% year-on-year in H1 2024.

Bear Case

Life Insurance Weakness: With less than 4% market share in life insurance versus 34% in P&C, PICC remains overexposed to the slower-growing, lower-margin segment. Life and health insurance offer higher margins and faster growth, but PICC has been unable to break through competitive barriers.

State-Owned Enterprise Constraints: "Communist Party of China (CPC) committees within PICC Group's governance framework... prioritize national objectives over purely commercial ones." This political overlay limits strategic flexibility and may compromise shareholder value in favor of policy objectives.

Digital Disruption Risk: "ZhongAn, a frontrunner in pure online distribution, swiftly rolls out micro-duration covers in mere days, due to its cloud-native architecture." Legacy insurers like PICC may struggle to match the speed and cost structure of digital-native competitors.

Concentration Risk: Motor insurance dominance (approximately 55% of revenue) creates exposure to regulatory reform in auto insurance pricing and new energy vehicle adoption patterns.

Geopolitical Overhang: "PICC's exposure to geopolitical risks, including Sino-U.S. trade tensions and domestic regulatory shifts, poses tail risks."

XIII. Key Performance Indicators for Ongoing Monitoring

For investors tracking PICC's ongoing performance, three KPIs deserve particular attention:

1. P&C Combined Ratio The combined ratio (claims plus expenses divided by premiums) is the fundamental measure of underwriting profitability. PICC's P&C business is the core earnings driver, and the combined ratio reveals whether scale advantages translate into superior underwriting performance. A combined ratio below 100% indicates underwriting profit; the trend matters more than the absolute level.

2. Market Share in Life and Health Insurance PICC's strategic challenge is the imbalance between P&C dominance and life insurance weakness. Progress in life and health market share would signal successful diversification into higher-margin segments. Current market share hovers around 3.6-4.3%; meaningful improvement would require breaking 5% and trending toward 10%.

3. Digital Channel Premium Growth Rate The competitive threat from ZhongAn, Ant Insurance, and Tencent's WeSure is real. Tracking what percentage of PICC's premium comes from digital channels—and the growth rate of that share—reveals whether the company is successfully defending against digital disruption or ceding ground to technology-native competitors.

XIV. Risk Factors and Regulatory Considerations

Regulatory Environment: The National Financial Regulatory Administration (NFRA), established in 2023, has consolidated supervision previously split across multiple agencies. New regulations on sales practices (effective March 2024), data security (December 2024), and capital adequacy under C-ROSS II create compliance burdens but may also benefit large, well-capitalized incumbents like PICC over smaller players.

Interest Rate Sensitivity: "Interest rate fluctuations could also compress margins, as insurers rely on long-term investments to fund liabilities." PICC's investment portfolio—approximately 2.5 trillion yuan under management—generates returns that depend significantly on the interest rate environment.

Natural Catastrophe Exposure: "The increasing frequency of extreme weather events in China could test the profitability and risk-selection processes of major property and casualty insurers." Climate change increases catastrophe exposure for property insurers, potentially driving reinsurance costs higher.

Related Party Transactions: The partnership with Aibao Technology, in which PICC is an investor, creates potential conflicts of interest. The 2025 agreement caps annual service fees at RMB 800 million, a material sum requiring investor scrutiny.

XV. Conclusion: The Dragon's Dilemma

PICC's 75-year journey from revolutionary nationalization to Fortune Global 500 company encapsulates the contradictions of Chinese state capitalism. The company survived the Cultural Revolution, navigated forced breakups, accessed international capital markets, and remains China's dominant property and casualty insurer.

Yet PICC faces the classic incumbent's dilemma: its historical strengths—state backing, nationwide distribution, brand heritage—may not translate into advantages against digital-native competitors building insurance businesses without branches, without legacy systems, without party committees overseeing strategic decisions.

The company's future likely depends on whether it can successfully navigate between its state-owned heritage and the innovation imperative. The "3411" project, Aibao partnership, and blockchain initiatives suggest management understands the challenge. Whether execution can match aspiration remains to be seen.

For investors, PICC offers exposure to China's vast underinsured population through a company trading at a discount to book value with above-market dividend yields. The bull case centers on market position, state support, and market growth. The bear case points to life insurance weakness, SOE constraints, and digital disruption risk.

As with many Chinese state-owned enterprises, the investment case ultimately depends on one's view of the sustainability of state capitalism and whether government backing represents a feature or a bug in an era of rapid technological change.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube