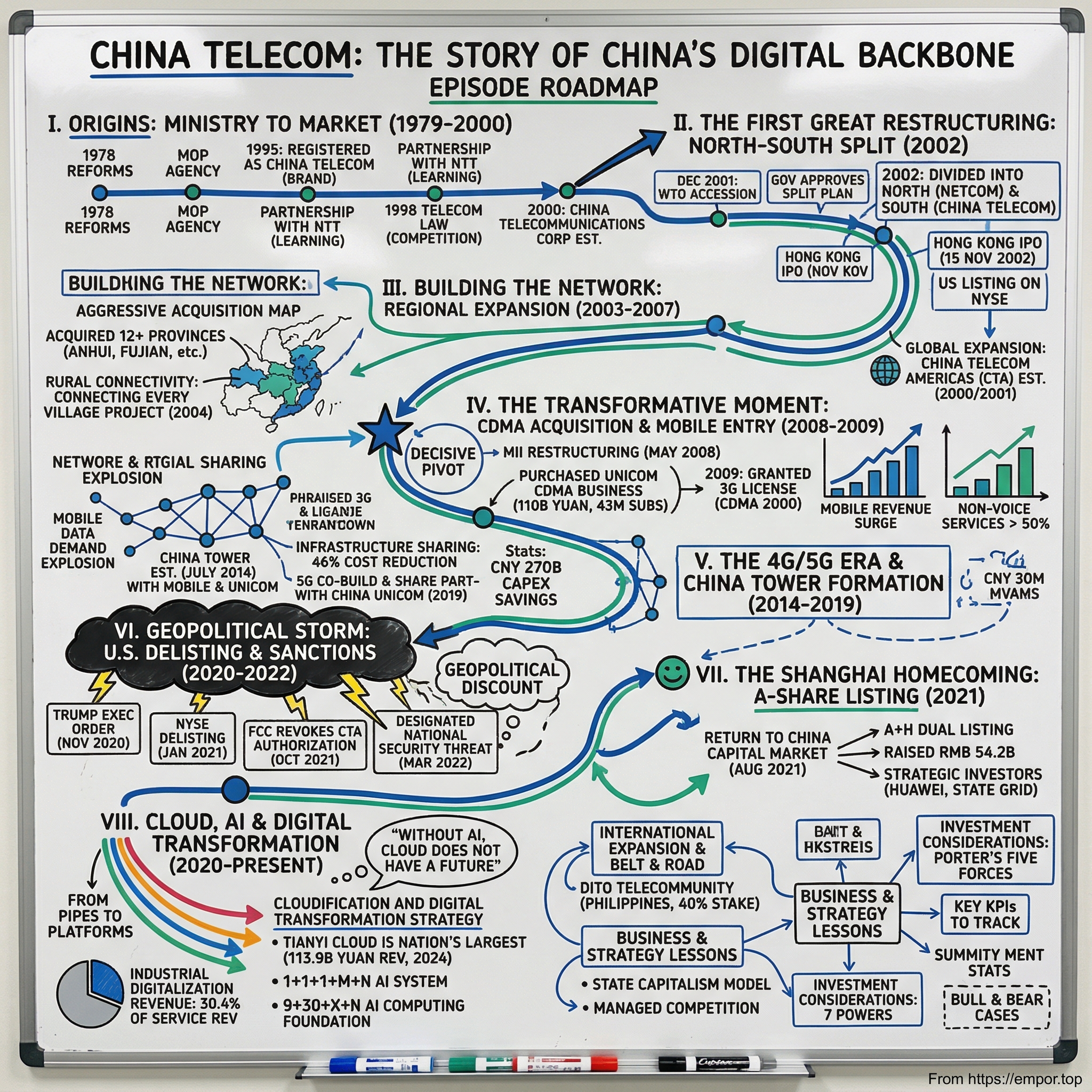

China Telecom: The Story of China's Digital Backbone

I. Introduction & Episode Roadmap

In the annals of global telecommunications, few transformations rival the sheer scale and complexity of China's journey from a centrally planned economy with barely one telephone per hundred citizens to an interconnected superpower boasting over four million 5G base stations and more than a billion mobile connections. At the heart of this metamorphosis stands China Telecom Corporation Limited—a company that embodies both the promise and paradox of state capitalism in the twenty-first century.

China Telecom is the second-largest wireless carrier in China, with 362.49 million subscribers as of June 2021. By the close of 2024, the company serves a mobile user base of 425 million. In 2024, China Telecom Corporation's revenue was 529.42 billion yuan, an increase of 3.09% compared to the previous year's 513.55 billion. Earnings were 33.01 billion, an increase of 8.43%. The company has 277,674 total employees—a workforce larger than many mid-sized cities.

The central question driving this exploration: How did a government ministry, operating telephone exchanges in a developing economy, metamorphose into a telecommunications giant navigating the world's most complex regulatory and geopolitical landscape?

China Telecom Corporation Limited provides mobile communications, wireline and satellite communications, internet access, cloud computing and computing power, AI, big data, quantum, ICT integration in the People's Republic of China. It offers mobile communications; wireline and smart family; industrial digitalisation; and other services.

The narrative that unfolds is not merely a corporate biography but a window into understanding state capitalism, forced breakups and restructurings, geopolitical flashpoints that rattled global markets, and a digital transformation that positions this telecom operator at the vanguard of China's AI ambitions. This is the story of China Telecom.

II. Origins: From Ministry to Market (1979–2000)

Picture Beijing in the late 1970s: rotary dial telephones remain scarce luxuries, long-distance calls require operator assistance and hours of patience, and the very concept of mobile communications exists only in science fiction. Prior to the economic reforms initiated in 1978, China's telecommunications sector operated under a centrally planned system characterized by limited infrastructure and low penetration rates, with services primarily managed by provincial post and telecommunications administrations subordinate to the central government. The sector's development lagged behind broader economic liberalization, maintaining a monopoly structure that prioritized state control over market dynamics, resulting in teledensity below 1 telephone line per 100 people as late as the early 1990s.

In 1979, a seismic shift began. The Chinese government looked to open areas of the Chinese economy to foreign investment and competition through a series of market-oriented legislative and legal changes. Yet the telecommunications sector remained stubbornly entrenched under the old system.

The company originated as a government agency of the Ministry of Posts and Telecommunications. On 27 April 1995, it was registered as a separate legal entity as Directorate General of Telecommunications, P&T, China, using "China Telecom" as brand name.

This formal registration marked the first step in a long march toward corporatization. But creating a legal entity was merely paperwork; the harder work lay in building actual infrastructure. Company director Ni Yifeng had plans to increase the number of telephone exchanges by 20 million lines each year. Part of the company's goal was to enhance the nationwide transmission network as well, as the actual number of telephone users for the year 2000 turned out to be more than twice the projected number. This exponential growth caught even the planners by surprise—a harbinger of the explosive demand that would characterize China's telecom market.

The ambitions extended beyond basic telephony. The company also wanted to develop products for VPNs (virtual private networks), frame relays, Internet, and ISDN lines. To get help with these plans China Telecom called on an old ally, Nippon Telegraph and Telephone Corporation (NTT) for help, requesting management lessons as well as technical assistance. The relationship between NTT and the Chinese government dated back to 1980.

This NTT partnership reveals a crucial element often overlooked in discussions of Chinese state enterprises: their willingness to learn from foreign expertise. Japan's telecom giant served as a template—demonstrating how a former monopoly could modernize while maintaining technical excellence.

In March 1998, the government had passed a telecommunications law that changed the regulatory structure and allowed more competition in the industry. This legislative milestone coincided with China's ambitious goal to join the World Trade Organization. However, WTO membership required proof of a competitive atmosphere and a demonstrated customer-centered market environment—difficult to demonstrate when a single state entity controlled virtually all telecommunications infrastructure.

On 17 May 2000 it was registered as China Telecommunications Corporation. China Telecommunications Corporation was established on May 17, 2000, through reforms in China's telecommunications sector that separated government regulatory functions from state-owned enterprise operations and divided postal and telecommunications services. This creation stemmed from the restructuring of the former Ministry of Posts and Telecommunications, aiming to enhance operational efficiency and market competitiveness in basic telecommunications services.

The newly constituted China Telecommunications Corporation inherited a vast empire of copper wires, switching stations, and—critically—the relationships with provincial governments that determined where infrastructure would be built. Yet this empire was about to be carved up.

III. The First Great Restructuring: North-South Split (2002)

In the summer of 2001, whispers began circulating through Beijing's corridors of power about another breakup of China Telecom. The logic was straightforward yet revolutionary: how could China demonstrate competitive telecommunications markets to skeptical WTO negotiators when one company controlled the entire fixed-line infrastructure? The answer came in December when the government approved a plan that would literally divide the nation.

This separation addressed the monopoly dominance of fixed-line infrastructure while aligning with World Trade Organization accession requirements for market liberalization. On May 16, 2002, the fixed-line China Telecom underwent further geographic division by the State Council, splitting assets into northern operations and southern operations to curb regional monopolies and stimulate local access competition.

The geographic logic was elegant in its simplicity: In accordance with the State Council's comprehensive restructuring plan relating to wireline telecommunication sector in 2001, the telecommunications business of China Telecom was divided geographically into two businesses. Telecommunications business in northern ten provinces, autonomous region and centrally administered municipalities in China (namely Beijing, Liaoning, Tianjin, Hebei, Shandong, Henan, Heilongjiang, Jilin, Neimenggu and Shanxi) was merged with those of China Netcom Corporation and Jitong Communications Co., Ltd. to form China Netcom.

The southern half—comprising 21 provinces and representing the more economically dynamic regions of coastal China—remained China Telecom. This geographic division was not random; it reflected underlying economic realities. The southern provinces included Guangdong, Shanghai, Jiangsu, and Zhejiang—the engines of China's export-driven growth miracle. The company that retained these territories inherited the customers with the deepest pockets and the greatest appetite for telecommunications services.

The IPO that followed represented China Telecom's formal debut on the global capital markets. China Telecom Corp., Ltd. was incorporated on 10 September 2002 as a limited company in order to float some of the assets of the group on the stock exchange. The company's H shares have been traded on the Stock Exchange of Hong Kong since 15 November 2002.

But this successful listing obscured a more tortured history. In December 2000, China Telecom had begun to prepare for an initial public offering to raise US$10 to US$15 billion on the New York and Hong Kong stock exchanges. Scheduled for July 2001, it was to be one of Asia's biggest IPOs. Merrill Lynch and Morgan Stanley were hired to underwrite the IPO. However, in May of that year, the company placed all its plans on hold indefinitely. The investment climate was bad, and global interest in telecom stocks was down. Industry analysts also blamed China Telecom's reform process.

The timing was catastrophic. The dot-com bubble had burst, Enron's collapse was destroying confidence in corporate governance, and global investors had soured on telecommunications after the spectacular implosion of WorldCom. China Telecom had to wait—and when it finally listed in late 2002, the offering was significantly smaller than originally envisioned.

On December 11, 2001, when China joined the World Trade Organization, it promised, as a condition of membership, to allow foreigners to own up to 50 percent of telecoms ventures in China after two years, and 49 percent of mobile-phone companies after five years. These promises would prove more aspirational than actual, but they signaled China's intent to participate in global telecommunications markets—even as the state maintained ultimate control.

For investors, the North-South split established a template that would recur throughout China Telecom's history: the government's willingness to restructure state-owned enterprises for strategic purposes, regardless of market preferences. This willingness to impose top-down reorganization represents both a risk and an opportunity. The risk lies in unpredictability; the opportunity lies in the state's demonstrated commitment to creating competitive dynamics, even if artificially engineered.

IV. Building the Network: Regional Expansion (2003–2007)

With the dust of the North-South split settling, China Telecom's new management faced an immediate challenge: consolidate the inherited southern territories while expanding into new markets. The company embarked on an aggressive acquisition strategy that would quadruple its provincial footprint within two years.

China Telecom Corp., Ltd. was incorporated on 10 September 2002 as a limited company in order to float some of the assets of the group on the stock exchange, specifically the wireline telecommunications businesses in Shanghai, Guangdong, Jiangsu, and Zhejiang, as well as other assets from the parent company.

This represented merely the initial core—the economic crown jewels. But China Telecom had larger ambitions. By 2003 and 2004, the company had acquired businesses across a dozen additional provinces, paying billions of yuan to bring Anhui, Fujian, Jiangxi, Guangxi, Chongqing, Sichuan, Hubei, Hunan, Hainan, Guizhou, Yunnan, Shaanxi, Gansu, Qinghai, Ningxia, and Xinjiang into its network.

Since 2004, when China Telecom made the strategic decision for transformation from a traditional basic telecom operator to an integrated information services provider, the company began developing in a steadier and more sustainable manner. This strategic pivot recognized that voice telephony—once the golden goose—faced structural decline as mobile phones proliferated and internet-based communications emerged.

China Telecom was among six state-owned companies that built the communications infrastructure and assisted in financing the Ministry of Industry and Information Technology's Connecting Every Village Project, which began in 2004. The project aimed to promote universal telecommunications and internet access in rural China. The program successfully extended internet infrastructure throughout rural China.

This rural connectivity initiative exemplified the dual nature of Chinese state-owned enterprises: commercial entities expected to generate returns while simultaneously serving as instruments of national development policy. The Connecting Every Village Project required significant capital expenditure in areas that would never generate market-rate returns—yet it cemented China Telecom's position as an indispensable partner to the central government.

Meanwhile, the company was planting flags abroad. China Telecom Americas (CTA) began in San Jose, California in 2000 before moving its headquarters to Herndon, VA in 2001. CTA was the first overseas representative office of China Telecommunications Corporation.

China Telecommunications Corporation opens a North American representative office in San Jose, California with the blessing of the US government, making China Telecom one of the first Chinese Fortune 500 companies to go global. China Telecom Americas establishes business partnerships with U.S. and European carriers and gives American companies the ability to buy Chinese telecom services in the USA, under US laws and contracts, rather than procuring directly in China. This helps American and foreign companies with operations in China efficiently procure telecom services.

This global expansion, approved by U.S. regulators in a less fraught era of U.S.-China relations, would later prove a liability when geopolitical tensions escalated. But in the early 2000s, it represented a natural extension of China's "going out" strategy—encouraging state-owned champions to establish international presence.

V. The Transformative Moment: CDMA Acquisition & Mobile Entry (2008–2009)

The Decisive Pivot

For all its scale and ambition, China Telecom faced a fundamental weakness throughout the early 2000s: it remained primarily a fixed-line operator in an increasingly mobile world. Mobile subscribers were migrating to China Mobile and China Unicom in droves, taking their voice minutes—and their data revenues—with them. The company's revenues suffered as fixed-to-mobile substitution accelerated.

Then came 2008—a year of Olympic glory and seismic industry restructuring.

The telecommunications industry in China is dominated by three state-run businesses: China Telecom, China Unicom and China Mobile. The three companies were formed by restructuring launched in May 2008, directed by the Ministry of Information Industry (MII), National Development and Reform Commission (NDRC) and the Minister of Finance. Since then, all three companies gained nationwide fixed-line and cellular mobile telecom licenses in China.

This restructuring represented the most significant reshaping of China's telecommunications landscape since the North-South split. On 24 May 2008, the Ministry of Industry and Information, the National Development and Reform Commission and the Ministry of Finance issued the Announcement on Deepening the Reform of the Structure of the Telecommunications Sector.

On 2 June 2008, China Telecommunications Corporation announced that it would purchase China Unicom's nationwide CDMA business and assets for CN¥110 billion, giving it 43 million mobile subscribers. According to the company, the listed portion of China Telecom Group (China Telecom Corp., Ltd.) paid CN¥43.8 billion, the unlisted portion of China Telecom Group (China Telecommunications Corporation) paid CN¥66.2 billion.

The math was staggering: 110 billion yuan—roughly $16 billion at the time—for a network and 43 million subscribers. This acquisition transformed China Telecom from a fixed-line operator watching the mobile revolution from the sidelines into a genuine full-service competitor.

The main aim of the restructuring is to stimulate competition and enhance the overall competitiveness of the country's telecoms industry. Most significantly, the industry reshuffle will create a more level playing field among all telecoms operators, helping Telecom and the merged entity of Netcom and Unicom to compete more effectively with China Mobile, which dominates 70% of the country's mobile subscribers.

The government's strategic intent was transparent: China Mobile had grown too dominant, controlling seven of every ten mobile connections. This dominance threatened both competitive dynamics and the government's ability to play operators against each other. By giving China Telecom mobile capabilities and strengthening China Unicom through merger with China Netcom, Beijing created a more balanced oligopoly.

On 7 January 2009, China Telecommunications Corporation was awarded CDMA 2000 license to expand its business to 3G telecommunication. In 2019, all three telecoms were issued 5G national licenses.

The 3G license was the crucial complement to the network acquisition. Without a license, China Telecom would have been stuck operating an obsolete 2G network; with it, the company could leap directly into third-generation services, competing on more equal footing with rivals.

The results validated the strategy. Especially after the telecom system restructure in 2008, and obtaining the mobile business license and 3G service license in 2009, China Telecom realized a strong beginning of development. By the end of 2009, total revenue reached 242.896 billion yuan—a 9.77% increase over the previous year—and non-voice services climbed to 52.8% of the mix, signaling successful diversification beyond traditional telephony.

For investors, this episode demonstrated a critical characteristic of Chinese telecom: the government's role as market architect. The CDMA acquisition was not a voluntary market transaction but a state-directed restructuring. The price was negotiated under government oversight, and the licenses were allocated according to policy priorities rather than auction dynamics. This means valuation models must incorporate political economy considerations that would be irrelevant in more market-driven telecommunications sectors.

VI. The 4G/5G Era & China Tower Formation (2014–2019)

Scaling the Network Mountain

In the mobile communications sector, China experienced a remarkable ascent from 1G to 5G over four decades. In 2014, a milestone arrived: the number of mobile internet users surpassed traditional PC internet users for the first time, thanks to the evolution of mobile networks driven by telecom service providers like China Telecom.

This mobile-first shift fundamentally altered China Telecom's strategic calculus. The company that had struggled to escape its fixed-line heritage found itself riding an unprecedented wave of mobile data demand. Smartphones proliferated, video streaming exploded, and mobile payment became the default transaction method for hundreds of millions of Chinese consumers.

Yet building the infrastructure to serve this demand required massive capital expenditure—expenditure that seemed wasteful when duplicated across three competing operators. The solution came in a novel form of "co-opetition."

China Tower was established in July 2014 by merging the telecom tower businesses among China's three telecom giants – China Mobile, China Unicom and China Telecom, which are customers and shareholders of China Tower. It was listed on Hong Kong Stock Exchange on 8 August 2018 at a price of HK$1.26 per share which raised US$6.9 billion.

China Tower Corporation Limited was established by China Mobile Communication Company Limited, China United Network Communications Corporation Limited and China Telecom Corporation Limited on 15 July 2014 as a limited liability company in the People's Republic of China, with a total registered capital of RMB10,000 million. Upon its establishment, China Mobile Company, China Unicom Corporation and China Telecom subscribed for 4,000 million shares, 3,010 million shares and 2,990 million shares of the Company respectively, accounting for 40.0%, 30.1% and 29.9% of equity interests in the Company respectively.

The establishment of the new firm will allow the three carriers to rent services from the new firm instead of building towers themselves. Such a move could reduce redundant construction of telecom infrastructure, optimize investment efficiency and further promote resources-sharing of telecom infrastructure. Building three separate towers will cost the three carriers a total investment of 531,000 yuan, but the cost will be reduced to 284,000 yuan if they share one tower.

This 46% cost reduction through shared infrastructure represented an elegant solution to a classic coordination problem. Each operator individually had incentive to build towers for competitive positioning, yet collectively this produced socially wasteful duplication. China Tower internalized this externality, creating a quasi-monopoly tower company whose customers were also its shareholders.

As of 2022, China Tower Corporation is the largest telecommunications tower operator in the world, owning over 1.9 million towers across mainland China. The company has become essential in supporting the rapid expansion of mobile telecommunications and the rollout of 5G networks.

China Telecom, the smallest of the three carriers, will benefit most from the establishment of the tower venture, as it has the least number of existing towers, the company's chairman Wang Xiaochu told a shareholders' meeting on May 29. China Mobile currently owns more towers than its two smaller counterparts, but it will gradually lose the advantage after the new firm starts operation.

This observation proved prescient. The tower-sharing arrangement effectively democratized infrastructure access, reducing China Mobile's first-mover advantage in network coverage. For China Telecom, which lagged in tower deployment, this leveled a playing field that had previously tilted sharply toward its larger rival.

The 5G era accelerated this cooperative dynamic. China Unicom and China Telecom will co-build and -share 5G network access nationwide to save costs and improve efficiency. With a permit to operate 5G digital cellular mobile service, China Telecom entered into a 5G network co-building and -sharing framework cooperation agreement with China United Network Communications Corporation Limited of China Unicom.

Since their partnership began in 2019, China Telecom and China Unicom have overcome numerous challenges, from bandwidth constraints to multi-frequency coexistence, to build the world's first and largest 5G standalone shared network.

Through 4G-5G network co-construction and sharing, they have saved more than CNY270 billion of CAPEX, in addition to CNY30 billion of OPEX annually, while cutting carbon emissions by over 10 million tons per year.

These numbers bear emphasizing: 270 billion yuan in capital expenditure savings, plus 30 billion yuan annually in operating expenses. This co-build arrangement represents one of the largest infrastructure-sharing agreements in telecommunications history. Cooperation with China United Network Communications continues to deepen with a total of 1.375 million 5G mid-high frequency base stations.

VII. Geopolitical Storm: U.S. Delisting & Sanctions (2020–2022)

When Politics Trumped Capital Markets

The year 2020 brought a pandemic that accelerated digital transformation globally—and geopolitical tensions that would sever China Telecom's hard-won access to American capital markets. What began as trade disputes escalated into a wholesale decoupling, with telecommunications companies caught in the crossfire.

The NYSE announced on Thursday it will remove U.S.-traded shares of China Telecom, China Mobile and China Unicom from the Big Board to comply with an executive order signed by President Donald Trump.

The path to delisting followed a tortuous route. In November 2020, U.S. President Donald Trump issued an executive order prohibiting U.S. companies and individuals from owning shares in companies that the United States Department of Defense has listed as having links to the People's Liberation Army, which included China Telecom. In consequence of the executive order, the New York Stock Exchange delisted China Telecom in January 2021.

On January 6, 2021, the NYSE announced the NYSE Regulation's decision to delist CUHK along with China Telecom Corporation Limited, and China Mobile Limited, effective January 11, 2021.

The delisting process itself became a drama of reversals. The New York Stock Exchange said it no longer plans to delist three Chinese telecommunications giants, reversing a decision announced four days earlier. The NYSE said late Monday it dropped the plans after "further consultation with relevant regulatory authorities in connection with Office of Foreign Assets Control."

But this reprieve proved temporary. The final reversal came quickly, demonstrating the regulatory whiplash that characterized this period.

The FCC delivered an even more devastating blow. On October 26, 2021, the Federal Communications Commission (FCC) unanimously adopted an order revoking and terminating its authorizations for China Telecom (Americas) Corporation to provide telecommunications services within the United States. The order cites the Chinese government's control over China Telecom; evolving U.S. national security concerns with respect to China; and China Telecom's lack of candor, trustworthiness, and reliability in its interactions with the FCC and other federal agencies as reasons for the revocation. The order directs China Telecom to discontinue service in the U.S. within 60 days following the release of the order.

The Federal Communications Commission (FCC) ordered China Telecom Americas to discontinue its services within 60 days, ending a nearly 20-year operation in the United States. The firm's "ownership and control by the Chinese government raise significant national security and law enforcement risks," the FCC said in a statement.

The regulatory actions intensified over subsequent years. In March 2022, the FCC designated China Telecom (Americas) Corp a national security threat. In April 2024, the FCC ordered U.S. units of China Telecom to discontinue operations in the country. In December 2024, the United States Department of Commerce moved to crack down on China Telecom's cloud and internet routing business in the U.S.

The accusations centered on specific technical concerns. The FCC previously found that China Telecom used Border Gateway Protocol vulnerabilities to misroute U.S. internet traffic on at least six occasions.

For investors, these developments crystallized a crucial risk: Chinese state-owned enterprises operating in sensitive sectors face fundamental constraints in Western markets, regardless of their commercial merits. The two decades of China Telecom Americas' U.S. operations—built with regulatory approval and serving legitimate business needs—evaporated as geopolitical considerations overwhelmed commercial logic.

The broader implications extend beyond China Telecom. Any valuation of Chinese technology and telecommunications companies must now incorporate a "geopolitical discount" reflecting the risk of sanctions, delistings, and operational restrictions in Western markets. This discount varies by company and sector but represents a structural feature of investing in Chinese state-owned enterprises.

VIII. The Shanghai Homecoming: A-Share Listing (2021)

Finding Capital in Home Waters

With American doors slamming shut, China Telecom turned homeward—and found a warmer welcome than many expected.

The company was debuted on the MB of Shanghai Stock Exchange on 20 August 2021. In its A-share offering, China Telecom offered 10.4 billion shares raising about RMB47.1 billion. Assuming the full exercise of its over-allotment option, the IPO could offer as many as 12 billion shares and raise up to RMB54.2 billion.

China Telecom Corp., the country's second largest mobile operator, surged 35% over its offer price of 4.53 yuan in its market debut in Shanghai, cementing its status as the world's biggest listing so far in 2021.

The rise cemented its status as the world's biggest listing so far in 2021, exceeding the $6.3 billion initial public offering by TikTok-rival Kuaishou Technology in Hong Kong in February. The surge indicates enthusiasm in the markets for China's push to build the world's largest 5G networks—and monetize the high-speed technology behind them.

On August 20, 2021, China Telecom (stock code: 601728) was officially listed on the main board of the Shanghai Stock Exchange until the close, the stock price is 6.11 yuan per share, an increase of 34.88%, and the market value is 558.017 billion yuan. Since then, China Telecom has officially realized the full layout of "A+H" domestic and overseas capital markets.

The timing was laden with symbolism. The New York Stock Exchange initiated the delisting of the American Depository Receipts of three Chinese telecommunications operators in January 2021. In March 2021, China Telecom announced its return to China's capital market. China Telecom's return listing is a clear demonstration of the success of reform of the A-share capital market and the attractiveness of its abundant liquidity.

The strategic investor roster told its own story. Among the 20 strategic investors, there are large central enterprises such as State Grid, State Energy, SDIC, FAW Group, China Electronics, and China Power Technology. Industrial funds such as China Chengtong, China Guoxin, China-Africa Fund, and Integrated Circuit Fund, as well as local industrial funds in Beijing, Shanghai, Suzhou, Shenzhen, Chengdu and other places, as well as Oriental Pearl, Huawei, Anheng Information, Sangfor, and Bilibili—well-known Internet and private enterprises.

Huawei's participation as a strategic investor deserves particular attention. The telecommunications equipment giant—itself a target of U.S. sanctions—was placing a bet on China's domestic telecom operator. This cross-investment cemented the domestic supply chain relationships that would prove essential as U.S. technology restrictions tightened.

The Shanghai listing also demonstrated the depth of mainland Chinese capital markets. A decade earlier, an IPO of this magnitude would have strained domestic market capacity; by 2021, the A-share market absorbed it without difficulty. The company raised 54.2 billion yuan ($8.36 billion) on the first day of its listing on the Shanghai Stock Exchange, exceeding expectations by around 12%. The stock was trading 16.34% higher at 5.27 yuan per share.

For China Telecom, the A-share listing represented more than a capital markets pivot—it was a strategic repositioning. The company's shareholder base shifted from global institutional investors to Chinese state-affiliated entities and domestic retail investors. This reduces pressure for short-term earnings optimization while increasing alignment with national policy objectives.

IX. Cloud, AI & Digital Transformation (2020–Present)

From Pipes to Platforms

The telecommunications industry faces an existential question: as voice revenue collapses and data becomes a commodity, what justifies premium valuations? China Telecom's answer lies in a strategic pivot that is reshaping the company's identity.

In March 2024, China Telecom's Chairman Ke Ruiwen said at the company's 2023 Annual Results Announcement, "Without AI, cloud does not have a future." This pithy observation encapsulates the company's strategic direction.

China Telecom is deeply invested in innovation and technology to fuel its growth, primarily through a 'Cloudification and Digital Transformation' strategy. This approach emphasizes a strong network foundation, a cloud-centric core, and a significant focus on artificial intelligence to shape its future prospects.

China Telecom continues to implement its "Cloudification and Digital Transformation" strategy, leveraging its cloud-network integration advantages to drive intelligent development. China Telecom has actively strategized in the field of AI, and established the "1+1+1+M+N" artificial intelligence system, which includes: 1 AI Computing Cloud Foundation, 1 General AI Model Foundation, 1 Data Foundation, M Internal AI Models, N Large Industrial Models. This framework empowers cloud, network, and AI capabilities to enable intelligent upgrades and promote high-quality digital transformation across industries.

China Telecom has also built a robust AI computing infrastructure with its eSurfing Cloud, which is the largest telecom cloud globally. The company has adopted a "9+30+X+N" resource distribution strategy for AI computing, ensuring broad availability and scalability.

The financial results validate this strategic shift. With its Tianyi Cloud, or China Telecom Cloud, now ranking as the nation's largest cloud service provider by revenue — 113.9 billion yuan in 2024, surpassing Alibaba Cloud — the company is positioning itself as the "National Cloud" to spearhead China's transition from digitization to intelligent transformation.

Tianyi Cloud revenue reached 113.9 billion yuan. Additionally, revenue from artificial intelligence (AI) and intelligent computing services surged by 195.7 percent year-on-year. Most strikingly, quantum business revenue increased by 238.7 percent year-on-year, and satellite communication revenue grew by 71.2 percent, with direct-to-cell satellite users surpassing 2.4 million.

The capital allocation tells the story of transformation. China Telecom announced on Tuesday that its CAPEX for 2024 came to 93.51 billion yuan ($12.9 billion), 5% lower than the previous year. The forecast for this year is even lower, at 83.6 billion yuan, down 11%. However, with soaring demand for AI computing, it plans a further hike in digital infrastructure spending. It will boost investment in cloud computing and data centers by 22% to RMB45.5 billion ($6.3 billion), making it the biggest single capex item, accounting for 38% of the total.

A pivotal strategic evolution occurred in 2025, upgrading the company's core strategy from "Cloudification and Digital Transformation" to "Cloudification, Digital Transformation, and AI for Good," integrating artificial intelligence across operations to drive intelligent services.

The 2024 financial results demonstrate the success of this pivot. In 2024, the company's operating income was RMB 529.4 billion, a year-on-year increase of 3.1%, with service revenue at RMB 482 billion, up 3.7% year-on-year. EBITDA was RMB 140.8 billion, an increase of 2.9% compared to the previous year. Net income reached RMB 33 billion, a rise of 8.4%, with basic net income per share at RMB 0.36. Capital expenditure was RMB 93.5 billion, a decrease of 5.4% year-on-year. Free cash flow was RMB 22.2 billion, a 7% increase year-on-year.

Industry digitization revenue reached 146.6 billion yuan, a year-on-year increase of 5.5%, accounting for 30.4% of service revenue. This represents a remarkable transformation: nearly one-third of China Telecom's service revenue now comes from industrial digitalization rather than traditional telecommunications services.

As of the end of last year, free cash flow reached 22.2 billion yuan, a year-on-year increase of 70.7%. This dramatic improvement in cash generation reflects both operating leverage and disciplined capital allocation—a combination that should enable sustained dividend growth.

The total amount of dividends distributed for the year increased by 11.4% year-on-year. There is a commitment to gradually increase the cash dividend ratio to over 75% within three years.

X. International Expansion & Belt & Road

Despite the setbacks in the United States, China Telecom continues to build its global footprint, particularly in markets aligned with China's Belt and Road Initiative.

China Telecom Global Limited, established in 2012 and headquartered in Hong Kong, serves as the primary international arm of China Telecommunications Corporation, offering integrated telecommunications solutions including internet access, data centers, cloud computing, and ICT services. As a wholly-owned subsidiary, it operates across 53 countries and markets, supported by 251 overseas points-of-presence, 162 terabits of international bandwidth capacity, connections to 53 submarine cables, and 15 proprietary data centers.

The Philippines expansion represents China Telecom's most ambitious international venture. Dito Telecommunity Corporation, formerly known as Mindanao Islamic Telephone Company, Inc. or Mislatel, is a telecommunications company in the Philippines. It is a consortium of DITO CME Holdings Corporation, a subsidiary of the Udenna Corporation, and China Telecommunications Corporation, a state-owned enterprise of the government of mainland China. The consortium is known as the sole winner of the government-sanctioned bidding that would allow the consortium to become the third major telecommunications provider in the Philippines challenging the duopoly of PLDT and Globe Telecom. DITO Telecommunity began its commercial operations on March 8, 2021.

Dito, which began operations in March 2021 with China Telecom as a 40% shareholder, faces its final national audit in July.

The Philippines venture has achieved notable success despite challenges. On February 27, 2024, DITO obtained the Rated #1 Mobile Network place in the Philippines at the Ookla Speedtest Awards 2023. In Opensignal's April report, on internet speed contest, DITO outplaced Smart Communications and Globe Telecom in the first quarter, with a download speed of 32 Mbps. It is also now the fastest operator for 5G, averaging 302.9 Mbit/s as against Smart's 143.3 Mbit/s.

Internationally, China Telecom is strategically expanding its presence in key overseas markets, with Southeast Asia, the Middle East, and Africa identified as significant growth areas. Its international business revenue reached 16.9 billion yuan in 2024, a 15.4% year-on-year increase.

The company expanded its global network capabilities, launching new international gateways in Kunming and Haikou and establishing key transit routes along the Belt and Road Initiative.

XI. Playbook: Business & Strategy Lessons

The State Capitalism Model

China Telecom's structure embodies a distinctive hybrid: state ownership with market-listed subsidiaries. Formed through the 2000 restructuring of the former China Telecommunications Corporation under the State-owned Assets Supervision and Administration Commission, it maintains majority control by the Chinese central government, enabling tight integration with national infrastructure priorities including 5G deployment and digital economy initiatives.

As a central state-owned enterprise (SOE), China Telecommunications Corporation is wholly owned and supervised by the State-owned Assets Supervision and Administration Commission (SASAC). This dual structure enables the corporation to balance commercial objectives with national priorities—though the balance tilts decisively toward national priorities when conflicts arise.

Managed Competition

The Chinese government engineers competition among SOEs rather than relying on market forces. The 2008 restructuring that gave China Telecom mobile capabilities, the formation of China Tower in 2014, and the mandated 5G co-build partnership with China Unicom all demonstrate deliberate orchestration of competitive dynamics.

This approach yields efficiency gains from competition while maintaining state control over strategic outcomes. For investors, it means that competitive positioning can shift rapidly based on policy decisions rather than market dynamics.

Capital Allocation Under Constraints

The company is focused on enhancing shareholder value through increased cash profit distribution, aiming for over 75% of profit attributable to equity holders within three years from 2024.

This commitment to dividend growth reflects a maturing business generating substantial free cash flow. China Telecom Corp. Ltd. Class A dividend yield was 3.61% in 2024, and payout ratio reached 72.32%.

Co-opetition with Rivals

Since 2019, China Telecom and China Unicom have deeply cultivated a new track for 5G co-construction, becoming the industry's first pairs to jointly build and share mobile networks. They have now engineered the world's largest, fastest shared 5G standalone (SA) network.

This partnership model reduces capital intensity while enabling competitive service offerings. The companies maintain independent brands and customer relationships while sharing infrastructure costs—a model increasingly relevant as 6G development costs loom.

XII. Investment Considerations: Porter's Five Forces and Competitive Dynamics

Threat of New Entrants: Very Low

The telecommunications sector in China operates under strict licensing regimes. New entrants require government approval, spectrum allocation, and massive capital investment. China Broadnet (中国广电), a fourth telecom player, does exist but operates on a much smaller scale than the three incumbents. China Broadnet was founded in 2014 as China Broadcasting Network Corporation. Even this modest new entrant required state sponsorship and took nearly a decade to achieve limited commercial operations.

Supplier Power: Moderate

China's telecommunications equipment supply chain includes Huawei, ZTE, and increasingly domestic chip manufacturers—many of which are themselves subject to U.S. sanctions. This creates mutual dependency: suppliers need the operators' volume while operators need domestic suppliers amid technology decoupling.

Buyer Power: Low to Moderate

Individual consumers have limited bargaining power, though price competition among the three operators constrains pricing. Enterprise customers hold more leverage, particularly for cloud and digitalization services where alternatives exist.

Threat of Substitutes: Evolving

Over-the-top (OTT) applications like WeChat have cannibalized voice revenue, but operators have successfully pivoted toward data-centric business models. Cloud and AI services face competition from internet giants like Alibaba and Tencent, though China Telecom's "National Cloud" positioning provides differentiation for government and SOE customers.

Competitive Rivalry: Moderate

The three-operator structure creates genuine competition within policy guardrails. Market share shifts gradually, and price wars are discouraged through regulatory supervision.

Hamilton Helmer's 7 Powers Analysis

- Scale Economies: China Telecom benefits from massive scale in network operations, though this advantage is partially neutralized by infrastructure sharing arrangements.

- Network Effects: Limited in traditional telecom, but emerging in cloud platforms where ecosystem effects can create switching costs.

- Counter-Positioning: The "National Cloud" strategy counter-positions against private cloud providers by emphasizing security, data sovereignty, and government alignment—benefits that private companies cannot credibly claim.

- Switching Costs: Moderate for consumers (phone number portability reduces lock-in), higher for enterprise cloud customers with significant migration costs.

- Branding: Limited differentiation among the three operators for consumer services; stronger for enterprise digital transformation services.

- Cornered Resource: Spectrum licenses represent a cornered resource, though government-allocated rather than competitively acquired.

- Process Power: Emerging in AI and cloud services where China Telecom's integration of telecommunications infrastructure with computing capabilities creates unique service delivery advantages.

Key KPIs to Track

For investors monitoring China Telecom's ongoing performance, three metrics stand out as most indicative:

-

Industrial Digitalization Revenue as % of Total Service Revenue: Currently at 30.4%, this metric captures the success of China Telecom's transformation from pipes to platforms. A rising percentage indicates successful execution of the cloud/AI pivot; stagnation would suggest commoditization of core telecom services without offsetting growth.

-

5G Mobile ARPU (Average Revenue Per User): This captures the company's ability to monetize 5G investments through premium pricing. The company now serves a mobile user base of 425 million, with an average revenue per user (ARPU) of 45.6 yuan. ARPU stability or growth signals successful service differentiation; declining ARPU indicates commoditization pressure.

-

Free Cash Flow Generation: Free cash flow reached 22.2 billion yuan, a year-on-year increase of 70.7%. This dramatic improvement reflects the transition from capital-intensive 5G buildout to harvest mode. Sustained strong free cash flow enables dividend growth and strategic investments without dilution.

XIII. Bull and Bear Cases

The Bull Case

China Telecom operates at the intersection of several structural growth themes: China's digital transformation, AI infrastructure buildout, and "National Cloud" positioning that provides preferential access to government and SOE customers representing a significant share of Chinese IT spending.

"Cloud is the cornerstone of AI development," said Ke Ruiwen, chairman of China Telecom, during his keynote speech. "The company is committed to building Tianyi Cloud into a world-class intelligent cloud platform that integrates computing power, data, models and applications."

The pivot from telecommunications to technology is gaining traction. Cloud revenue growing at 17% annually, AI services revenue nearly tripling year-over-year, and expanding industrial digitalization represent genuine business transformation rather than financial engineering.

Capital allocation is improving. Capex is declining as 5G buildout matures, while free cash flow surges. The commitment to 75%+ dividend payout ratios provides income certainty for patient investors. At current valuations—trading at roughly 10-13x earnings—the stock appears to price in limited growth despite structural tailwinds.

The co-build partnership with China Unicom creates sustainable cost advantages that should persist through the 6G transition. International expansion in Southeast Asia, Middle East, and Africa provides diversification away from the saturating domestic market.

The Bear Case

State ownership creates agency problems that transcend normal corporate governance concerns. When national priorities conflict with shareholder interests—as in the U.S. delisting episode—shareholder interests are subordinate. The same regulatory apparatus that enables market position can redirect corporate resources toward non-commercial objectives.

Geopolitical risk extends beyond the U.S. market. France Castro says that action by the US regulator, the Federal Communications Commission (FCC), against China Telecom may affect its international partners and customers. Castro explained that the termination of China Telecom's operations in the US may prevent Dito from interconnecting to the US. Secondary sanctions risk could constrain international expansion.

The telecommunications industry faces structural headwinds globally. Voice revenue is declining irreversibly, and data pricing faces continuous pressure. Cloud and AI growth, while impressive in percentage terms, start from smaller bases and face competition from established technology giants.

Valuation multiples for Chinese state-owned enterprises have been compressed by investor concerns about governance, geopolitics, and capital allocation. There's limited evidence this discount will narrow, and it could widen further amid escalating U.S.-China tensions.

XIV. Conclusion: The Infrastructure of Transformation

The story of China Telecom is ultimately a story about infrastructure—not just the physical infrastructure of cables, towers, and data centers, but the institutional infrastructure of Chinese state capitalism.

AI is a direction even more; it is a reality. China Telecom will fully embrace AI. We will firmly affirm our direction, grab opportunities, and promote deeply the AI plus action to foster AI applications to empower economic and social development and expedite the building of a world-class enterprise.

From a government ministry operating telephone exchanges in a developing economy to a technology conglomerate positioning itself at the vanguard of AI infrastructure, China Telecom has navigated restructurings, delisting, sanctions, and strategic pivots. The company that emerged from the Ministry of Posts and Telecommunications now generates over 520 billion yuan in annual revenue, employs nearly 280,000 people, and operates what it claims is the world's largest telecommunications cloud.

The central question—how a government ministry became a telecom giant navigating the world's most complex regulatory and geopolitical landscape—has a multifaceted answer. State sponsorship provided the foundation: spectrum allocation, market protection, and restructuring that created competitive balance. Global capital markets, before geopolitical tensions foreclosed them, provided the financing discipline and valuation benchmarks that encouraged efficiency. And increasingly, domestic capital markets provide both the funding and the strategic investor base aligned with national objectives.

For investors considering China Telecom, the key insight is that this is not merely a telecommunications company to be valued on subscriber metrics and ARPU trends. It is an infrastructure platform for China's digital transformation, a policy instrument for strategic objectives, and a bellwether for the evolving relationship between Chinese state-owned enterprises and global capital markets.

The transformation from pipes to platforms continues. The shift from "Cloudification and Digital Transformation" to "Cloudification, Digital Transformation, and AI for Good" signals the next phase of evolution. Whether this transformation generates adequate returns for shareholders—or primarily serves national strategic objectives—remains the central uncertainty for investors in China's digital backbone.

Myth vs. Reality

| Myth | Reality |

|---|---|

| China Telecom is just a telecom utility | Industrial digitalization now comprises 30.4% of service revenue; Tianyi Cloud surpassed Alibaba Cloud in revenue |

| U.S. delisting devastated the company | Shanghai A-share listing raised $8+ billion and achieved 35% first-day pop; A+H structure maintained capital access |

| State ownership means inefficient operations | Free cash flow grew 70.7% in 2024; operating expenses grew slower than revenue; R&D increased 11% |

| The 5G buildout requires perpetual capital destruction | CAPEX declining 11% in 2025; co-build partnership saved CNY270 billion; dividend payout rising to 75%+ |

| Chinese telecoms are interchangeable | China Telecom's "National Cloud" positioning, quantum security capabilities, and southern regional strength create differentiation |

This analysis reflects publicly available information as of November 2025. Investors should conduct their own due diligence and consider geopolitical, regulatory, and market risks specific to Chinese state-owned enterprises. The regulatory and sanctions environment continues to evolve.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube