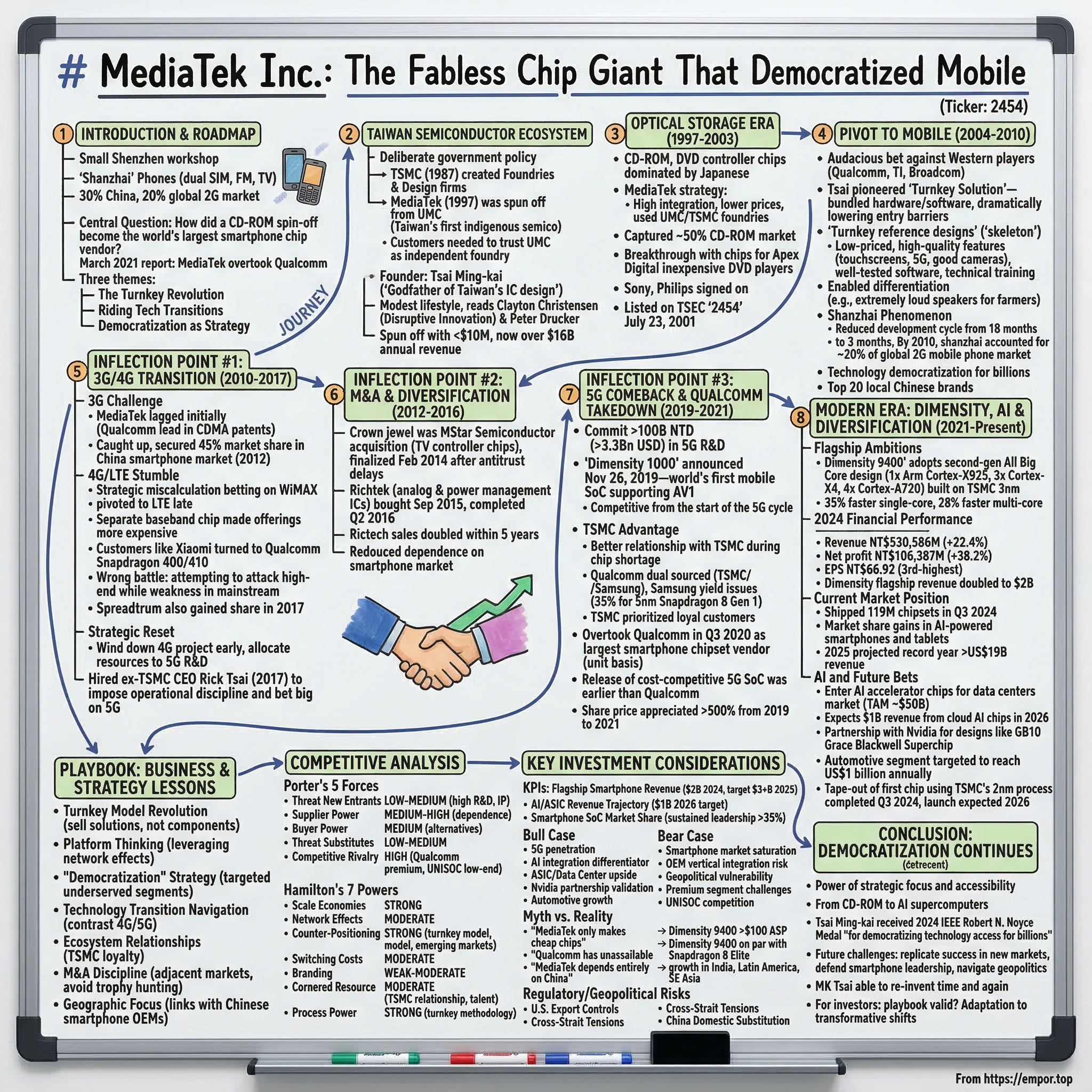

MediaTek Inc.: The Fabless Chip Giant That Democratized Mobile

I. Introduction & Episode Roadmap

Picture a cramped workshop in Shenzhen circa 2008—a handful of entrepreneurs crowded around worktables, assembling mobile phones for mere dollars. Not knockoffs of Nokia or Samsung, but original creations: handsets with dual SIM cards, FM radio, TV tuners, and even cigarette-pack designs. These were the "shanzhai" phones—the bandit handsets that captured 30% of China's domestic market and 20% of global 2G sales. The brains behind every one of them? MediaTek chipsets, powering the democratization of mobile technology from Hsinchu, Taiwan to the remotest villages of Africa and Latin America.

Today, MediaTek stands as the world's fifth-largest global fabless semiconductor company, powering more than 2 billion connected devices a year. The journey from CD-ROM controller chips to the silicon inside your smartphone is one of the great underdog stories in tech—a tale of brilliant strategic pivots, near-fatal missteps, and a relentless focus on removing friction for customers.

The central question we'll explore: How did a CD-ROM chipset spinoff from Taiwan become the world's largest smartphone chip vendor, beating Qualcomm—the company that invented CDMA and dominated mobile silicon for decades?

A March 2021 report revealed that MediaTek had overtaken Qualcomm for the first time as the world's biggest smartphone chipset vendor in 2020, with 351.8 million chipsets shipped that year. The report attributed MediaTek's performance to its focus on less expensive smartphones. But this wasn't just about being cheap. MediaTek's story illuminates three transformative themes in modern technology:

The Turnkey Revolution: MediaTek didn't just sell chips—it sold complete solutions. Tsai Ming-kai pioneered a turnkey solution that bundled hardware and software for feature phone chipsets, which dramatically lowered entry barriers for handset manufacturing. His strategic insight was to remove friction for system makers and own the ecosystem.

Riding Technology Transitions: MediaTek's history is a masterclass in navigating generational shifts—sometimes brilliantly, sometimes disastrously. The company's near-death experience during the 4G transition and triumphant 5G comeback offers crucial lessons for any technology investor.

Democratization as Strategy: As the Founder and Executive Chairman of MediaTek Incorporated, Tsai Ming-kai helped develop the mobile phone SOC market and created a new business model called "Turnkey Solutions," which made mobile communication technologies affordable to nearly everyone. Tsai is the 2024 recipient of the IEEE Robert N. Noyce Medal for "vision and leadership in the global semiconductor industry, democratizing technology access for billions of people."

What follows is a deep examination of how MediaTek emerged from Taiwan's semiconductor ecosystem, survived multiple technology transitions, and positioned itself at the center of the AI and 5G revolution. Understanding MediaTek's playbook reveals fundamental truths about platform economics, emerging market dynamics, and the art of competing against entrenched incumbents.

II. Taiwan's Semiconductor Ecosystem & Founding Context

To understand MediaTek, you must first understand the peculiar genius of Taiwan's semiconductor industry—a deliberate creation of government policy, brilliant engineering, and strategic positioning that transformed a small island into the world's most critical chokepoint for advanced technology.

TSMC's founding in 1987 would launch two new types of semiconductor firms: Foundries and design firms. This was a radical innovation. Before Morris Chang established TSMC, semiconductor companies were integrated—they designed chips and fabricated them in their own factories. TSMC pioneered the "pure-play foundry" model: we'll build your chips, but we won't design our own. This unlocked an entirely new species of company.

MediaTek began in 1997 as a spinoff startup. It had been a part of United Microelectronics Corporation or UMC. UMC was Taiwan's first indigenous semiconductor company and had been operating as an integrated device manufacturer—it designed, fabbed, and sold its own chips.

The spin-off wasn't arbitrary. Customers could not accept UMC as an independent foundry unless they knew that UMC would not compete with them. So to gain customer trust, they decided to spin off their semiconductor design operations as multiple companies. Thus was founded MediaTek, which had once been UMC's R&D department for multimedia devices.

This origin matters because it positioned MediaTek at the intersection of Taiwan's unique advantages: deep engineering talent cultivated at research institutes like ITRI, close relationships with foundries like TSMC and UMC, and an industrial culture oriented toward customer service and rapid iteration rather than prestige product development.

The man who would guide MediaTek through its first quarter-century of existence was Tsai Ming-kai (born April 6, 1950), a Taiwanese billionaire entrepreneur and electrical engineer best known as the founder and executive chairman of MediaTek Inc., a global leader in fabless semiconductor design specializing in system-on-chip solutions for mobile devices, wireless communications, and multimedia applications.

Tsai's background was quintessentially Taiwanese tech establishment. He earned a bachelor's degree in electrical engineering from National Taiwan University and a master's degree from the University of Cincinnati. His early career included roles at the Industrial Technology Research Institute (ITRI) and, in the 1980s, integrated circuit design at United Microelectronics Corporation (UMC), where he rose to become president of the products business unit and pioneered advancements in CPUs, mass storage, communications, and multimedia chips.

Within Taiwan's technology community, Tsai earned a singular nickname: "Godfather of Taiwan's IC design industry." This wasn't mere flattery. Over the years, Tsai has mentored dozens of design engineers who went on to become key leaders in today's chip design industry. UMC spun off its products division to form several independent fabless design companies, including MediaTek, NovaTek, and Faraday. These spinoffs, together with numerous rising fabless design startup companies, were chaired or directed by Tsai and many of these businesses later developed into major IC design companies.

Understanding Tsai's personality helps explain MediaTek's culture. He avoids most media interactions, with his first face-to-face press interview in three years occurring in 2010, highlighting his preference for privacy. Despite his status as a billionaire, Tsai leads a modest lifestyle, often seen queuing for meals in the company canteen alongside employees. Among his personal interests, Tsai enjoys reading history books and studying management theories, drawing inspiration from authors such as Clayton Christensen and Peter Drucker.

The Clayton Christensen reference is particularly telling. MediaTek's entire strategy would embody Christensen's theory of disruptive innovation—entering markets at the low end where incumbents had little incentive to compete, then gradually moving upmarket as capabilities improved.

MediaTek was established on May 28, 1997, as a fabless integrated circuit (IC) design house spun off from the design arm of United Microelectronics Corporation (UMC), Taiwan's pioneering semiconductor foundry. MediaTek's paid-in capital at incorporation totaled NT$200 million (approximately US$7.4 million at the time), with an additional NT$30 million valued from transferred technology and patents, enabling the startup to establish operations.

This modest beginning—less than $10 million in capital—would grow into a company that today generates over $16 billion in annual revenue. But first, MediaTek needed to find its footing, and it would do so in an unglamorous but lucrative corner of consumer electronics: optical storage.

III. Optical Storage Era: CD-ROM to DVD Dominance (1997-2003)

The late 1990s saw an explosion in consumer demand for CD-ROM drives. Every personal computer needed one. Every DVD player needed controller chips. The market was dominated by established Japanese semiconductor firms who commanded premium prices and maintained comfortable margins. Into this market stepped MediaTek with a characteristically disruptive approach.

True to its multimedia device roots, MediaTek began with the opportunity afforded by the growing CD-ROM, DVD, and Blu-Ray market. Those devices needed controller chips to work. That chip market was currently dominated by Japanese suppliers.

MediaTek's strategy against these incumbents established a template it would employ repeatedly over the following decades. Rather than competing on performance at the high end, MediaTek offered highly integrated solutions at substantially lower prices. The company contracted with independent foundries like UMC and TSMC to build chips, eliminating the massive capital expenditures required for manufacturing. This allowed MediaTek to focus purely on design and customer relationships.

The results came quickly. Taiwan-based CD-ROM manufacturers like BTC and Lite-On adopted MediaTek's solution first, attracted by the combination of adequate performance and significant cost savings. Soon thereafter, major global brands including Hitachi, Sony, and LG followed. MediaTek would capture approximately 50% of the CD-ROM controller market.

The DVD segment proved even more lucrative. MediaTek's big breakout hit came through supplying chips to Apex Digital, which manufactured an inexpensive DVD player that became a sensation in America. When Sony and Philips signed on for their own DVD players, MediaTek's trajectory was set. Just four years after the spin-off, the company was generating approximately $200 million in annual revenue.

MediaTek Inc. was listed on the Taiwan Stock Exchange (TSEC) under the "2454" code on July 23, 2001. The IPO provided capital to fuel further expansion and validated Tsai Ming-kai's vision for a fabless semiconductor champion focused on integration and affordability rather than bleeding-edge performance.

But even as MediaTek celebrated its optical storage success, Tsai was already looking toward the next great technology transition. The mobile phone market was exploding, particularly in emerging markets. The question was whether MediaTek's playbook—high integration, low cost, turnkey solutions—could translate from CD-ROM drives to cellular handsets.

The answer would transform not just MediaTek, but the entire global mobile ecosystem.

IV. The Pivot to Mobile: The Turnkey Revolution (2004-2010)

The Strategic Bet

In 2000, MediaTek evaluated the mobile phone chip industry and felt it would be a critical growth area for the company. A major investment was made and MediaTek started to produce chipsets for 2G feature phones in 2004.

This was an audacious bet. The mobile chip market was dominated by established Western players like Qualcomm, Texas Instruments, and Broadcom. These companies had decades of wireless expertise, extensive patent portfolios, and deep relationships with major handset manufacturers. MediaTek had none of these advantages.

What MediaTek did have was an insight that would prove revolutionary. Tsai pioneered a turnkey solution that bundled hardware and software for feature phone chipsets, which dramatically lowered entry barriers for handset manufacturing. His strategic insight was to remove friction for system makers and own the ecosystem.

To appreciate the magnitude of this innovation, consider what it took to build a mobile phone before MediaTek's turnkey solution. A manufacturer needed to source a baseband processor from one vendor, integrate it with an applications processor from another, license operating system software, develop custom drivers, test wireless compliance, and navigate complex intellectual property arrangements. The process took 18 months or more and required substantial engineering resources.

MediaTek's turnkey solution changed everything. MediaTek's style of business is to attack entrenched players in markets after they mature. Their go-to-market strategy for doing so is to offer a "turnkey" solution to their customers. That means MediaTek offers for a particular device category a "skeleton," called a reference design. These MTK turnkey reference designs might be low-priced, but boast high quality features like touchscreens, 5G connectivity and good cameras. They also come with well-tested software. To help their customers best modify the reference design, MediaTek also offers a development SDK as well as technical training.

Customers buy these designs and modify them to best suit their business strategy. How so? It depends on the customer. One smartphone maker specialized in phones for farmers. They modified their phones to have extremely loud speakers so that the farmers can hear them ring while in the fields.

This example perfectly captures MediaTek's philosophy: enable customers to differentiate on features that matter to their specific markets, while handling the complex underlying technology.

The Shanzhai Phenomenon

Known in China as "shanzhai ji," or bandit phones, China's gray market handset industry was virtually non-existent just a few years ago. While a handful of illegal companies produced black market mobiles, they often were of poor quality mainly because the technology needed to make them was hard to come by and even harder to master. This all changed in 2005 when Mediatek, a microchip design company from Taiwan, developed what experts call a turnkey solution—a platform that integrated many complex mobile phone software systems onto a single chip. This made it much easier and cheaper to build handsets and churn out new models at astounding speeds. "[Mediatek] basically commoditized the entire market," said Jonathan Li, founder of Shanghai-based technology design studio Asentio Design. "They made it really simple and really cheap to make your own phone."

The implications were staggering. MediaTek's turnkey solution reduced the development cycle from 18 months to just 3 months. Suddenly, small workshops with minimal engineering expertise could produce functional mobile phones. This wasn't about counterfeiting—many shanzhai manufacturers created original designs that reflected local preferences better than products from Nokia or Motorola.

By the end of 2006, it is estimated that shanzhai mobile phone manufacturers accounted for around 30 percent of the domestic phone market in China. In 2010, the Financial Times estimated that shanzhai phones accounted for about 20 percent of the global 2G mobile phone market. Demand for these 2G-era shanzhai mobile phones was not only in China, but particularly in developing countries in Asia, Africa, and Latin America as well.

Global Expansion

The shanzhai business got another boost a couple of years later when the Chinese government relaxed regulations limiting the number of companies that could manufacture handsets, lowering the entry barrier for hundreds of entrepreneurs eager to have a piece of the world's biggest mobile phone market.

By 2008, an estimated 3,000 to 4,000 shanzhai businesses had emerged, many with fewer than a dozen employees operating in offices sometimes comprised only of a back bedroom in a small apartment or basement of a private home.

The explosion of shanzhai manufacturers created a virtuous cycle for MediaTek. More manufacturers meant more chip volume, which meant lower per-unit costs, which meant more manufacturers could afford to enter the market. MediaTek became the platform upon which an entire industry ecosystem developed.

Critics—particularly established handset makers—viewed shanzhai phones as knockoffs that damaged brand equity and evaded safety regulations. But from a different perspective, shanzhai represented exactly what Tsai Ming-kai had envisioned: technology democratization. Hundreds of millions of people who could never afford a Nokia or Motorola phone gained access to mobile communications through shanzhai handsets powered by MediaTek silicon.

"The local Chinese phone-makers made huge losses in 2005-06 due to the rise of shanzhai ji," said Knock of JPMorgan, to the extent that the top 20 local Chinese brands have used MediaTek chips for their phones.

The scale of MediaTek's success in this era is hard to overstate. The company went from being a niche optical storage chipmaker to the dominant supplier of feature phone SoCs, powering billions of devices worldwide. MediaTek's business model of selling reference designs for others to modify and resell is pretty unique. It was classic disruptive innovation: enter at the low end where incumbents had little incentive to compete, then build capabilities and relationships that would enable expansion into higher-margin segments.

But the mobile industry was about to undergo its most significant transformation since the invention of the cellular phone. The smartphone era was dawning, and MediaTek's dominance in feature phones would not guarantee success in the new world of 3G and 4G devices.

V. Inflection Point #1: The Painful 3G/4G Transition (2010-2017)

The 3G Challenge

The next evolution came when the mobile market shifted from 2G feature phones to 3G smartphones. This period was challenging as Qualcomm's lead in 3G (as the inventor of CDMA technology) meant MediaTek lagged initially.

This was more than just a product gap—it was a structural disadvantage. Qualcomm had invented CDMA technology and held the fundamental patents that underpinned 3G networks. Every 3G chipmaker had to license from Qualcomm. While MediaTek could design competitive 2G chips using well-understood GSM technology, 3G required navigating Qualcomm's patent thicket and mastering significantly more complex radio engineering.

MediaTek spent a few years catching up before securing 45% market share (+29% YoY) in China smartphone market in 2012. This recovery demonstrated MediaTek's resilience and the strength of its customer relationships. Chinese OEMs preferred working with MediaTek's engineering-focused culture over Qualcomm's more rigid, take-it-or-leave-it approach.

The 4G/LTE Stumble

If the 3G transition was challenging, the 4G transition nearly proved fatal. MediaTek made a strategic miscalculation that would cost the company billions in lost revenue and years of market share erosion.

MediaTek, initially aligned with WiMAX, found itself two to three years behind when it pivoted to LTE, delaying its chip rollout and leading to more than 20% market share loss between 2015 and 2017.

The backstory involves Taiwan's government betting on the wrong standard. Around 2009, Taiwan's telecommunications authorities were promoting WiMAX as the preferred 4G technology. MediaTek, influenced by domestic policy considerations, invested in WiMAX development. But the global market coalesced around LTE, leaving MediaTek with technology nobody wanted.

MediaTek started shipping chips with integrated 4G LTE baseband in volume in the second half of 2014, later than its largest competitor Qualcomm. The additional cost of the separate baseband chip required in every 4G handset made MediaTek's offerings more expensive and prompted some of its larger customers, like Alcatel One Touch and ZTE, to choose competing SoCs like the Qualcomm Snapdragon 400 and 410 platforms, negatively affecting MediaTek's revenue stream.

The timing could not have been worse. China's major carriers were aggressively rolling out 4G networks, and consumers wanted 4G phones. MediaTek couldn't deliver competitive solutions, so customers like Xiaomi—which had helped make MediaTek a smartphone power—increasingly turned to Qualcomm.

MediaTek and Spreadtrum lost market share in 2017 because they could not accelerate their LTE product roadmaps through innovation. A sharp decline in 3G baseband chips added problems to MediaTek and Spreadtrum.

Another strategic error compounded the problem. Rather than focusing on regaining competitiveness in the mid-range where MediaTek had natural advantages, the company attempted to attack the high-end segment. This was the wrong battle at the wrong time—stretching resources while competitors exploited MediaTek's weakness in mainstream 4G.

Strategic Reset

Tsai Ming-Kai later acknowledged the strategic misstep and made the decisive call to wind down the 4G project ahead of schedule, swiftly reallocating resources toward 5G R&D. Determined to avoid falling behind again, MediaTek set its sights on becoming a technological and commercial leader in the next generation of wireless.

This decision required extraordinary humility. Tsai Ming-kai had to admit—to himself, his board, and his employees—that MediaTek had failed to anticipate the market correctly. Rather than throwing good money after bad trying to catch up in 4G, he bet the company's future on being ready for 5G from day one.

At the same time, Tsai Ming-Kai hired ex-TSMC CEO Rick Tsai to become the new CEO of MediaTek. Tsai Ming-Kai acknowledged that MediaTek has grown too big and enlisted Rick Tsai in 2017 to impose operational discipline on the company.

Rick Tsai brought credibility and operational rigor that MediaTek desperately needed. Having led TSMC—the world's most important semiconductor manufacturer—he understood both cutting-edge technology and manufacturing realities.

Rick Tsai also recognized the need to bet big on 5G early so that it does not lose out to Qualcomm early in the cycle transition.

The 4G debacle taught MediaTek a painful but invaluable lesson: in the semiconductor industry, being late to a technology transition can erase years of carefully accumulated market position. The company would not make the same mistake with 5G.

VI. Inflection Point #2: The MStar Acquisition & Diversification (2012-2016)

The MStar Mega-Deal

Even as MediaTek navigated the turbulent 3G/4G transition, Tsai Ming-kai was executing a different strategy: using M&A to build moats in adjacent markets. The crown jewel of this effort was the acquisition of MStar Semiconductor.

MediaTek announced the deal in June 2012, saying it planned first to buy 48 per cent of MStar, followed by a full takeover. The rationale was clear: MStar was the dominant supplier of LCD TV controller chips, commanding approximately 65% of the Chinese market. MediaTek and MStar will together have a market share as high as 61% in the global market and 80% in the China market.

But the path to completion proved torturous. MediaTek acquired a 48 percent stake in MStar in August 2012 but since then has been battling to gain approval from authorities in Taiwan, South Korea, and China for a total merger and has postponed the closing deadline for the deal multiple times.

The entire review process of the concentration lasted for more than a year. The filing was first submitted to MOFCOM on July 6, 2012, and was officially accepted by MOFCOM on September 4, 2012.

China's antitrust regulators were particularly concerned about the combined entity's dominance in TV controller chips. MStar must keep its liquid-crystal display television chip businesses as a separate entity for at least the next three years in order to ensure fair competition in the market, according to a statement posted on Mofcom's website.

The following merger between MediaTek and MStar was delayed by antitrust concerns in China and South Korea and finalized on February 1, 2014.

The MStar deal illustrated both MediaTek's strategic vision and the challenges of executing transformative M&A in markets with significant regulatory oversight. MediaTek is the world's leading supplier of chips for smart TVs, digital TVs, and set-top boxes. The MStar merger in 2012 made MediaTek dominant in this segment.

The Richtek Acquisition

MediaTek followed the MStar playbook with a second major acquisition. On September 7, 2015, MediaTek announced to buy Richtek Technology Corp., a fabless vendor of analog ICs and power management ICs based in Hsinchu, Taiwan. Richtek became a wholly subsidiary of MediaTek after the completion of the acquisition in the second quarter of 2016.

Upon completion of the tender offer, MediaTek plans to further acquire 100% of Richtek's outstanding shares and it is now expected to be completed at the second quarter of 2016, subject to relevant regulatory approvals. "As a global leader with significant presence in smartphones, tablets, and the digital home, MediaTek offers tremendous growth opportunities for power management related products through the cross-platform advantage," said Mr. Ming-Kai Tsai, MediaTek Chairman & CEO. "Richtek is a leader in analog ICs and provides comprehensive power management solutions to satisfy various customer demand, backed by an experienced management and R&D team."

Power management might seem unglamorous compared to smartphone processors, but it's essential to MediaTek's system-level value proposition. Every mobile device needs sophisticated power management to balance performance and battery life. By acquiring Richtek, MediaTek could offer customers more complete solutions while capturing additional value per device.

MediaTek has built a strong track record of generating attractive returns on its M&A investments. Both MStar Semiconductor and Richtek Technology have become integral parts of MediaTek's core business. Notably, MediaTek successfully doubled Richtek's sales within five years of completing its acquisition.

The diversification strategy served multiple purposes. It reduced MediaTek's dependence on the volatile smartphone market. It built positions in markets where MediaTek could leverage its existing customer relationships and engineering culture. And it created optionality for future growth as smart home, IoT, and other connected device categories expanded.

VII. Inflection Point #3: The 5G Comeback & Qualcomm Takedown (2019-2021)

The 5G Bet

For the merchant silicon market, it is largely dominated by Qualcomm, MediaTek and UNISOC from China. The turning point for MediaTek was in 2020 when 5G first took off in volume. MediaTek was early to invest in 5G technology and its 5G chipset was no longer inferior to Qualcomm.

This wasn't luck—it was the result of deliberate strategic choices made years earlier, when MediaTek was still bleeding market share from its 4G stumble.

MediaTek has committed over 100 billion NTD (>3.3Bn USD) in 5G R&D to date and has a long track record of R&D achievements, 3GPP involvement (5G/cellular standards consortium), and a growing, broad 5G-enabled product range that has established an ecosystem of 100+ global 5G operators, industry partners and global brands. Below is our timeline of 5G IP and product development, collaborations including 25+ 5G technology 'firsts' with global operators.

On November 26, 2019, MediaTek announced their 5G SoC Dimensity 1000, the world's first mobile SoC supporting AV1. Dimensity 1000 is MediaTek's first 5G mobile SoC in its 5G family of chipsets. The single 5G chip solution, with its integrated 5G modem, is a brilliant combination of advanced technologies packed into a 7nm chip and tuned for 5G performance. "Our Dimensity series is a culmination of MediaTek's investment in 5G and positions us as a leader driving 5G development and innovation."

The Dimensity 1000 represented a turning point. Unlike MediaTek's late entry into 4G, the company was now competitive from the start of the 5G cycle. "Our Dimensity series is a culmination of MediaTek's investment in 5G and positions us as a leader driving 5G development and innovation. Our 5G technology goes head-to-head with anyone in the industry," said MediaTek President Joe Chen.

The TSMC Advantage

MediaTek was in a better position during the period of chip shortage in 2021 due to a better relationship with TSMC. Back then, Qualcomm was trying to dual source between TSMC and Samsung which did not end up well for Qualcomm.

This is a crucial point that deserves elaboration. Qualcomm had been splitting its foundry business between TSMC and Samsung to maintain bargaining leverage and supply security. But Samsung's yields on advanced nodes lagged TSMC's, leading to performance and power consumption issues in Qualcomm's chips.

Qualcomm used Samsung to produce the 5nm Snapdragon 8 Gen 1 application processor (AP) which was introduced in December 2021. But a yield rate as low as 35% forced Qualcomm to leave Samsung and the chip designer switched to TSMC to produce the Snapdragon 8+ Gen 1.

Meanwhile, MediaTek had maintained a consistent, loyal relationship with TSMC. When chip shortages struck during the pandemic, TSMC prioritized its best customers—and MediaTek was among them. Wilson said Taiwan-based MediaTek does not expect the chipset shortage to affect shipments of its own products to smartphone vendors like Xiaomi and Samsung, nor does it expect the situation to affect the overall sale of smartphones.

Market Leadership

MediaTek overtook Qualcomm as the largest vendor of smartphone chipsets in the world in the third quarter of 2020, mainly due to significant growth in the Indian and Latin American markets.

When 5G adoption came in 2020, MediaTek was able to release the Dimensity series, a cost-competitive 5G SoC, that was earlier than Qualcomm. This is the 1st time since the botched 3G and 4G transition that MediaTek is neck-to-neck in competition with Qualcomm. The success of the 5G transition can be seen from MediaTek's share price which appreciated more than 500% from 2019 to 2021.

This was a vindication of everything Tsai Ming-kai had bet on: early 5G investment, operational discipline under Rick Tsai's leadership, strong TSMC relationships, and focus on emerging markets where MediaTek's cost-effectiveness resonated.

MediaTek's expansion over Snapdragon in the 5G smartphone market is largely attributed to the increasing availability of phones priced under $250 equipped with 5G chipsets—a segment dominated by MediaTek. This has particularly favored MediaTek, as it is the preferred choice in this price range for 5G phones, while Snapdragon leads in mid-range 5G phones and Apple dominates the premium segment.

VIII. The Modern Era: Dimensity, AI & Diversification (2021-Present)

Flagship Ambitions

Post the 5G cycle, MediaTek's volume share is relatively stable and it started to target the premium market with Dimensity 9000 series. It is not easy to target the premium market in China as consumers often have the impression that Snapdragon-powered phone is better than MediaTek's.

MediaTek's flagship push represents its most ambitious attempt yet to break out of its "value player" positioning. The Dimensity 9400, the fourth and latest in MediaTek's flagship mobile SoC lineup, offers a massive boost in performance with its second-generation All Big Core design built on Arm's v9.2 CPU architecture, combined with the most advanced GPU and NPU for extreme performance in a super power-efficient design. The Dimensity 9400 adopts MediaTek's second-gen All Big Core design, integrating one Arm Cortex-X925 core operating over 3.62GHz, combined with 3x Cortex-X4 and 4x Cortex-A720 cores. This design offers 35% faster single-core performance and 28% faster multi-core performance compared to MediaTek's previous generation flagship chipset, the Dimensity 9300.

Powered by TSMC's 3nm technology and Arm V9 architecture, MediaTek's Dimensity 9400 is almost on par in performance with Qualcomm's Snapdragon 8 Elite. The ASP of Dimensity 9400 is more than $100, which is several times more than the average 5G chipset.

2024 Financial Performance

The Taiwan-based technology company reported a 22.4 percent increase in its 2024 revenue, reaching NT$530,586 million. Mobile phone customers accounted for 59 percent, Smart Edge Platforms 35 percent, and Power IC 6 percent of total revenue.

For the full year of 2024, MediaTek's consolidated revenue reached NT$530.586 billion, a 22.4% increase from the previous year. Net profit attributable to the parent company was NT$106.387 billion, a 38.2% year-over-year growth. Earnings per share were NT$66.92, the third-highest in the company's history.

On February 7, 2025, MediaTek held its Q4 2024 and full-year earnings conference, reporting better-than-expected results driven by strong Dimensity flagship chip sales and growing AI-driven ASIC demand. The company's 2024 Dimensity flagship chip revenue doubled to $2 billion.

Current Market Position

Despite the Dimensity 9400 launching in the fourth quarter this year, MediaTek enjoyed massive success during Q3 2024, when it was estimated to have shipped 119 million chipsets.

MediaTek reported revenue of NT$142.1 billion (US$4.64 billion)—down 5.5 percent quarter-over-quarter but up 7.8 percent year-over-year for the third quarter ended September 30, 2025. The company said the year-over-year growth was driven by market share gains in AI-powered flagship smartphones and AI-enabled tablets. MediaTek's Mobile Phones business contributed 53 percent of total revenue, rising 4 percent from the previous year but declining 4 percent sequentially. In US dollar terms, this segment grew 13 percent year-over-year.

MediaTek said demand for its Dimensity 9500 chipset exceeded expectations, powering devices such as the vivo X300 and OPPO X9 series in China, with expansion planned into India, Southeast Asia, and Europe by year-end. MediaTek, which competes with US-based Qualcomm, expects mobile revenue to grow strongly in the fourth quarter of 2025, targeting more than US$3 billion in flagship smartphone revenue for 2025—representing over 40 percent annual growth.

With this outlook, 2025 is projected to be a record year with over US$19 billion in total revenue. Looking ahead, CEO Rick Tsai said MediaTek sees major opportunities in AI data center chips.

AI and Future Bets

MediaTek's most dramatic expansion is into AI accelerator chips for data centers—a market dominated by Nvidia. Taiwan's top chip design company, MediaTek, expects to earn revenue of billions of dollars from its AI accelerator ASIC chips by 2027, as the company pushes further into the data centre business. Chief Executive Rick Tsai told a quarterly earnings conference call that MediaTek was on track to generate $1 billion in revenue from its cloud AI chips in 2026 after its first AI accelerator ASIC project was well executed. "The first project we generate multiple billions in 2027," Tsai said. "And another project we'll start delivering revenue starting 2028 and beyond." The total addressable market (TAM) for data center ASIC chip is now estimated at $50 billion and MediaTek is striving to gain market share of at least 10 to 15 percent in the next two years.

The company's most visible AI partnership is with Nvidia. MediaTek today announced it has collaborated with NVIDIA on the design of the NVIDIA GB10 Grace Blackwell Superchip for NVIDIA Project DIGITS, a personal AI supercomputer. MediaTek, a market leader in Arm-based SoC designs, collaborated on the design of GB10, contributing to its best-in-class power efficiency, performance and connectivity.

"The age of AI is here. The combination of MediaTek's industry-leading CPU performance and power efficiency with NVIDIA's accelerated computing technologies will drive the next wave of innovation," said Jensen Huang, founder and CEO of NVIDIA. "Project DIGITS, with the new GB10 Superchip designed with MediaTek, makes our most powerful Grace Blackwell platform more accessible—placing it in the hands of developers, researchers and students to solve the most pressing issues of our time."

MediaTek's Smart Edge Platforms accounted for 42 percent of quarterly revenue, up 14 percent year-over-year and down 6 percent quarter-over-quarter. The diversification into automotive is also accelerating. MediaTek's automotive segment is targeted to reach US$1 billion annually.

MediaTek completed the tape-out of its first chip using TSMC's 2nm process in the third quarter of this year, and the product is expected to be launched in 2026.

IX. Playbook: Business & Strategy Lessons

MediaTek's three-decade journey offers several enduring lessons for technology investors and business strategists:

The Turnkey Model Revolution

MediaTek's most transformative insight was understanding that customers often don't want components—they want solutions. The turnkey approach shifts the value proposition from "here's a chip, good luck integrating it" to "here's a complete reference design you can customize and ship." This reduces customer risk, accelerates time-to-market, and creates stickier relationships than pure component sales.

Platform Thinking

MediaTek's business model of selling reference designs for others to modify and resell is pretty unique. This platform approach enabled MediaTek to leverage network effects: more customers using MediaTek platforms meant more software optimization, more reference designs, and more ecosystem knowledge—making the platform more valuable for the next customer.

The "Democratization" Strategy

MediaTek consistently targeted underserved segments where incumbents had little incentive to compete. Feature phones in emerging markets, then budget 5G smartphones, then mid-range devices. Each time, MediaTek established dominance at the entry level before moving upmarket as capabilities improved.

Technology Transition Navigation

The contrast between MediaTek's 4G failure and 5G success is instructive. With 4G, MediaTek followed government policy (WiMAX) rather than market signals (LTE) and invested too late. With 5G, MediaTek invested early ($3.3 billion in R&D), participated actively in standards development, and was ready to ship competitive chips when the market emerged.

Ecosystem Relationships

MediaTek's close relationship with TSMC proved crucial during the chip shortage. In a capacity-constrained environment, TSMC prioritized its most loyal, long-term customers. MediaTek's exclusive commitment to TSMC—unlike Qualcomm's dual-sourcing with Samsung—meant it secured adequate supply when competitors couldn't.

M&A Discipline

MediaTek's acquisitions of MStar, Richtek, and Ralink share common characteristics: they expanded capabilities in adjacent markets where MediaTek could add value through existing customer relationships and engineering culture. The company avoided the trophy hunting that has destroyed value in so many tech M&A deals.

Geographic Focus

MediaTek's focus on the mid to low-end price tier "comes from their portfolio of chipsets but also through their longstanding ties and links with Chinese smartphone OEMs such as Transsion and Xiaomi, which also specialize in that price tier." MediaTek built deep relationships with the OEMs that dominate high-volume segments, particularly in China and India.

X. Competitive Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's 5 Forces Analysis

| Force | Analysis |

|---|---|

| Threat of New Entrants | LOW-MEDIUM: Extremely high R&D costs (>25% of revenue), years of IP development required, complex foundry relationships essential. However, Chinese competitors like UNISOC are emerging with government support. |

| Supplier Power | MEDIUM-HIGH: Deep dependence on TSMC for advanced nodes (3nm, 2nm); ARM for architecture licensing. Any TSMC disruption represents existential risk. TSMC is the world's most important contract chip foundry in the world as it builds chips for some of the most influential fabless chip designers in the world. TSMC has no trouble getting orders. |

| Buyer Power | MEDIUM: Major OEMs (Xiaomi, OPPO, Vivo, Samsung) have alternatives (Qualcomm), but MediaTek's cost advantage and turnkey approach create switching costs. Long-term customer relationships mitigate negotiating pressure. |

| Threat of Substitutes | LOW-MEDIUM: Apple's vertical integration model represents the ultimate substitute—OEMs designing their own chips. Xiaomi has signaled intentions to internalize key components like smartphone SoC. This is likely to have a bigger impact on Qualcomm. |

| Competitive Rivalry | HIGH: Qualcomm remains fierce competitor in premium; UNISOC in low-end. "While MediaTek is the biggest industry rival to Qualcomm, I don't think they necessarily challenge one another hugely," said West, noting they focus on different price tiers. |

Hamilton's 7 Powers Analysis

| Power | MediaTek Application |

|---|---|

| Scale Economies | STRONG: R&D costs spread across massive volumes. MediaTek ships 2+ billion devices annually, creating substantial per-unit R&D cost advantages over smaller competitors. |

| Network Effects | MODERATE: More devices using MediaTek platforms means more software optimization, driver development, and ecosystem knowledge. Reference designs become more valuable with broader adoption. |

| Counter-Positioning | STRONG: MediaTek's turnkey model and emerging market focus initially positioned it where Qualcomm had little incentive to compete. Moving downmarket would have cannibalized Qualcomm's margins. |

| Switching Costs | MODERATE: OEMs build software stacks, driver expertise, and testing infrastructure around specific chipset families. Switching requires significant engineering investment. |

| Branding | WEAK-MODERATE: Consumer brand recognition growing but still trails Qualcomm Snapdragon. It is not easy to target the premium market in China as consumers often have the impression that Snapdragon-powered phone is better than MediaTek's. |

| Cornered Resource | MODERATE: TSMC relationship and Taiwan engineering talent pool represent partially defensible resources. "MK is a key figure in the establishment of Taiwan's IC design industry, leading MediaTek to become a significant company in the global semiconductor industry," remarked Dr. Morris Chang, Founder of TSMC. |

| Process Power | STRONG: MediaTek's turnkey development methodology and customer support infrastructure are difficult to replicate. Years of accumulated reference designs represent embedded organizational capabilities. |

XI. Key Investment Considerations

Key Performance Indicators to Monitor

For investors tracking MediaTek's ongoing performance, three metrics deserve particular attention:

1. Flagship Smartphone Revenue ($B): MediaTek's ability to grow in the premium segment represents its path to margin expansion. The company reported $2 billion in Dimensity flagship chip revenue in 2024, targeting $3+ billion in 2025. Success here validates the technological competitiveness of MediaTek's highest-margin products against Qualcomm's Snapdragon 8 series.

2. AI/ASIC Revenue Trajectory: CEO Rick Tsai stated MediaTek was on track to generate $1 billion in revenue from its cloud AI chips in 2026. This new business line represents MediaTek's most significant TAM expansion opportunity and its entry into the booming AI infrastructure market.

3. Smartphone SoC Market Share (Unit Basis): MediaTek has maintained smartphone SoC leadership for 15+ consecutive quarters. Sustained market share above 35% indicates the durability of MediaTek's cost leadership and customer relationships.

Bull Case

- 5G Transition Tailwind Continues: 5G penetration in emerging markets still has substantial runway, particularly in price-sensitive segments where MediaTek dominates

- AI Integration Differentiator: MediaTek's NPU capabilities enable on-device AI features that increasingly influence smartphone purchase decisions

- ASIC/Data Center Upside: The $50 billion data center ASIC TAM offers meaningful diversification beyond smartphones

- Nvidia Partnership Validation: Although speculation around a hypothetical $73 billion buyout has been gaining steam recently, the engineering behind GB10 shows how much NVIDIA is leaning on MediaTek's strengths, making this partnership significant beyond just the hardware itself.

- Automotive Growth: Connected car infotainment and ADAS represent expanding TAM with higher margins than smartphones

Bear Case

- Smartphone Market Saturation: Global smartphone shipments have been essentially flat for several years; MediaTek's largest market lacks growth catalyst

- OEM Vertical Integration Risk: If major OEMs like Xiaomi successfully develop in-house chips, MediaTek loses its largest customers

- Geopolitical Vulnerability: As a Taiwanese company dependent on TSMC and selling heavily into China, MediaTek sits at the intersection of U.S.-China technology conflict

- Premium Segment Challenges: "Qualcomm has arguably done a better job in being cutting-edge and building a reputation with both vendors and consumers for producing the best chipsets." Breaking Snapdragon's premium brand moat requires sustained investment

- UNISOC Competition: Chinese government-backed UNISOC is gaining share in low-end segments where MediaTek built its foundation

Myth vs. Reality

| Common Narrative | Reality Check |

|---|---|

| "MediaTek only makes cheap chips" | The Dimensity 9400 competes with Qualcomm's flagship at >$100 ASP. MediaTek's 2024 flagship revenue doubled to $2B. |

| "Qualcomm has unassailable technology lead" | MediaTek's Dimensity 9400 is almost on par in performance with Qualcomm's Snapdragon 8 Elite. The gap has narrowed significantly. |

| "MediaTek depends entirely on China" | While China remains crucial, MediaTek's growth in India, Latin America, and Southeast Asia provides geographic diversification. |

Regulatory and Geopolitical Considerations

MediaTek faces meaningful geopolitical risks as a Taiwanese company with significant China exposure:

- U.S. Export Controls: Tightening restrictions on semiconductor technology exports to China could constrain MediaTek's access to key customers or manufacturing capabilities

- Cross-Strait Tensions: Any disruption to Taiwan would devastate MediaTek's operations and TSMC's manufacturing

- China Domestic Substitution: Chinese government policies promoting domestic semiconductor champions could eventually threaten MediaTek's position with Chinese OEMs

CEO Tsai noted that MediaTek's direct exposure to the U.S. accounts for about 10% of its total revenue, and therefore, the potential impact is "limited." However, secondary effects through customer dynamics and supply chain disruption represent harder-to-quantify risks.

XII. Conclusion: The Democratization Continues

MediaTek's story is ultimately about the power of strategic focus and the value of making technology accessible. From CD-ROM controllers to AI supercomputers, the company has consistently identified opportunities where integration, cost-effectiveness, and customer service could overcome incumbent advantages.

Tsai Ming-kai received the 2024 IEEE Robert N. Noyce Medal "for vision and leadership in the global semiconductor industry, democratizing technology access for billions of people."

This recognition captures something essential about MediaTek's impact. The company didn't just compete in existing markets—it created new ones by making technology affordable for customers and consumers who were previously priced out.

Looking ahead, MediaTek faces familiar challenges in unfamiliar markets. Can it replicate its mobile success in automotive, AI infrastructure, and edge computing? Can it defend its smartphone leadership against both premium competitors like Qualcomm and low-end challengers like UNISOC? Can it navigate geopolitical crosscurrents that threaten its supply chain and customer relationships?

"M.K. Tsai, the founder of MediaTek, has been able to re-invent MediaTek time and again with new business models to turn challenges into opportunities in the unpredictable and fast-moving technology industry," said Mark Liu, Chairman of TSMC.

If history is any guide, MediaTek will approach these challenges the same way it always has: by finding the segments where customers need solutions rather than components, by investing early in emerging technologies, and by executing with the disciplined intensity that has made Taiwan's semiconductor ecosystem the world's most critical technology infrastructure.

For investors, the key question is whether MediaTek's playbook remains valid in a world of AI-driven computing, geopolitical fragmentation, and potential OEM vertical integration. The company's 5G comeback demonstrated it could learn from past mistakes. The coming years will reveal whether that adaptability extends to even more transformative market shifts.

This analysis is for informational purposes only and should not be construed as investment advice. Semiconductor markets are subject to rapid technological change, geopolitical risks, and cyclical demand fluctuations that can materially impact company performance.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube