Baidu, Inc.: China's AI Giant and the Search for Tomorrow

I. Introduction & Episode Roadmap

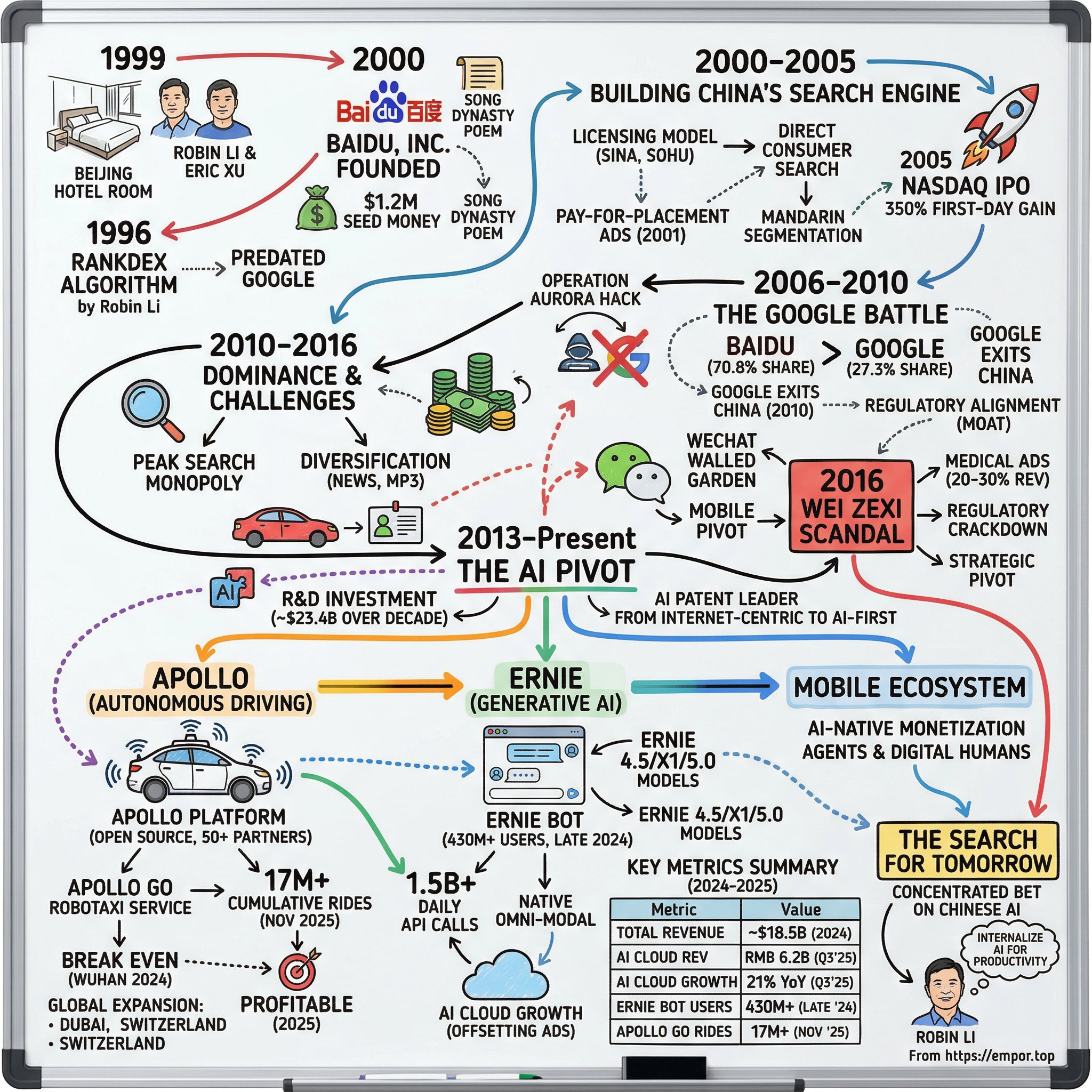

In the smoky haze of a Beijing hotel room in late 1999, two men hunched over laptops, armed with $1.2 million from Silicon Valley investors and a conviction that would reshape China's digital landscape. One of them, Robin Li, had spent years in America perfecting algorithms that could make sense of the internet's chaos. Now he and his partner Eric Xu were betting everything on a simple idea: that China needed its own search engine, built by Chinese engineers who understood the language, culture, and aspirations of a billion people.

Twenty-five years later, that hotel-room startup has become something far more ambitious than anyone could have imagined. Baidu, Inc. announced its unaudited financial results for fiscal year 2024, marking what CEO Robin Li called "a pivotal year in our ongoing transformation from an internet-centric to an AI-first business." The company that once dominated search—China's answer to Google—now operates fully driverless robotaxis on the streets of Wuhan, powers generative AI applications for 430 million users, and runs a cloud platform handling 1.5 billion API calls per day.

Baidu is the largest internet search engine in China with over 50% share of the search engine market in 2024. The firm generated 70% of core revenue from online marketing services from its search engine in 2024. But those figures only tell part of the story. The central question that animates Baidu's current chapter is this: Can a company that built its empire on search advertising reinvent itself as an AI infrastructure provider before its core business erodes?

The numbers frame the challenge starkly. According to Baidu's latest financial reports, the company's current revenue (TTM) is $18.49 billion USD. In 2024, the company made a revenue of $18.49 billion USD, a decrease over the revenue in the year 2023 that was $18.99 billion USD. Revenue is declining even as AI investments accelerate. Revenue from Baidu Core was RMB27.7 billion ($3.80 billion) in Q4 2024, increasing 1% year over year; online marketing revenue was RMB17.9 billion ($2.46 billion), decreasing 7% year over year, and non-online marketing revenue was RMB9.8 billion ($1.34 billion), up 18% year over year, mainly driven by AI Cloud business.

Baidu used to be part of the BAT group—the three biggest companies in China, along with Alibaba and Tencent. But while Alibaba conquered e-commerce and Tencent built a social media empire through WeChat, Baidu's trajectory has been more volatile, more contested, and ultimately more interesting as an investment case study. The company has made four pivotal bets: surviving Google's challenge, pivoting to AI before it was fashionable, building an autonomous driving platform, and launching China's most prominent generative AI chatbot. Understanding how those bets are paying off—or not—is essential for any investor trying to evaluate China's tech landscape.

This deep dive will trace Baidu's arc from hyperlink algorithms to robotaxis, examining the strategic decisions that defined each era and the competitive dynamics that continue to shape its future.

II. Founding Context & Robin Li's Origin Story

The Algorithm That Predated Google

Before there was PageRank, there was RankDex. In 1994, Robin Li joined IDD Information Services, a New Jersey division of Dow Jones and Company, where he helped develop a software program for the online edition of The Wall Street Journal. He also worked on improving algorithms for search engines. He remained at IDD Information Services from May 1994 to June 1997. In 1996, while at IDD, Li created the Rankdex site-scoring algorithm for search engine page ranking.

This is one of the most remarkable and least-discussed facts in internet history. Google cofounder Larry Page filed a patent for the PageRank search algorithm two years later in 1998, which references Li's work on RankDex. Li later used his Rankdex technology for the Baidu search engine. Robin Li didn't merely imitate Google—he had been working on similar concepts before Larry Page and Sergey Brin formalized their approach at Stanford.

Robin Li, born Li Yanhong on November 17, 1968, in Yangquan, Shanxi Province, is a prominent Chinese internet entrepreneur. His development of the RankDex algorithm for ranking search engine pages significantly contributed to Baidu's rise and made him a multibillionaire, positioning him among the wealthiest individuals in China.

Li's path to that hotel room in Beijing was shaped by a combination of technical brilliance and fortunate timing. Li studied information management at Peking University and computer science at the University at Buffalo. In 1996, he created RankDex. His academic training bridged two worlds: the theoretical foundations of information retrieval from China's most prestigious university and the practical computer science skills from an American institution during the internet's formative years.

Li worked as a staff engineer for Infoseek, a pioneer internet search engine company, from July 1997 to December 1999. An achievement of his was the picture search function used by Go.com. Since founding Baidu in January 2000, Li has turned the company into the largest Chinese search engine, with over 80% market share by search query, and the second largest independent search engine in the world.

The Return to China

The decision to leave Silicon Valley wasn't made in isolation. In 1999, the Chinese communist government, aware of Li's computer science expertise, invited Li to return to China for the regime's fiftieth anniversary celebrations. Dedicated to their vision of building a major media company and inspired by Jerry Yang, Li and Xu started Baidu in a hotel room in Beijing that year.

Through a friend, Eric Xu, Li and his wife, Melissa Ma, were introduced to Yahoo co-founder and billionaire Jerry Yang in Silicon Valley. Li and Xu were inspired by Yang's success, and decided to build a Chinese search engine. They presented their business plan throughout the Bay Area, and received $1.2 million in seed money from venture capitalists Bob King, Greg Penner, Scott Walcheck and Hugo Shong.

The early days were marked by the kind of scrappy determination that characterizes legendary startup stories. They left their wives in the United States and worked tirelessly, armed with $1.2 million from U.S. venture firms Integrity Partners and Peninsula Capital. Working from that Beijing hotel overlooking Peking University, Li and Xu built the foundation of what would become China's most important internet company.

In 2000, Draper Fisher Jurvetson and IDG Technology Ventures invested another $10 million. Baidu, Inc.'s search engine was launched on October 11, 1999. The name Baidu came from an eight-hundred-year-old Song Dynasty poem. Its literal translation means "hundreds of times" and stands for finding retreating beauty in chaos or searching for an ideal.

The name itself carries cultural weight that Western observers often miss. In a country where literary references carry deep meaning, choosing a name from a Song Dynasty poem signaled Baidu's identity as a distinctly Chinese enterprise—not a clone of American technology, but something rooted in Chinese tradition and purpose.

Li comes from very humble beginnings. Born in 1968, Li was the 4th of 5 children born to factory workers in Yangquan. This background—a factory worker's son who became a billionaire through technological innovation—resonated with China's emerging entrepreneurial class and the government's narrative of national rejuvenation through technology.

III. Building China's Search Engine (2000-2005)

Early Technical Foundation

Baidu's initial approach was not to compete directly with users but to power other companies' search capabilities. Li and Xu developed a search indexing software and licensed it to Chinese Web giants Sina and Sohu.com, generating revenue each time a user ran a query. A dispute with Sina over licensing payments led to Baidu developing its own search site in the early 2000s.

This pivot from B2B licensing to direct consumer search would prove transformative. The technical challenges were formidable and uniquely Chinese. Unlike English, Mandarin Chinese doesn't use spaces between words, making word segmentation—determining where one word ends and another begins—a fundamental algorithmic challenge. A query like "北京大学" could be interpreted as "Peking University" or "north capital big learn" depending on how the algorithm segments the characters.

Baidu's engineers developed proprietary solutions for these problems, giving them advantages that foreign competitors struggled to replicate. By 2002, the company had indexed over 100 million pages, and its relevance algorithms were specifically tuned for Chinese language patterns, including handling polysemous terms common in Mandarin.

Business Model Innovation

Baidu charged advertisers to appear at the top of search results, and became profitable in 2004. This pay-for-placement model, which Baidu implemented in 2001, actually predated Google's AdWords system. The approach was controversial from the start—and would eventually lead to the company's most damaging scandal—but it generated the cash flow that funded Baidu's expansion.

By 2003, Baidu had launched a news search engine and picture search engine, diversifying beyond basic web search. These moves demonstrated Li's understanding that search was not a single product but an ecosystem of services built around user intent.

The IPO Moment

The IPO on August 5, 2005, became one of the most dramatic debut performances in NASDAQ history. Baidu received takeover offers from Yahoo, Microsoft and Google in 2005—all for more than $1 billion—after the company became the largest Internet search site in China. To prevent Li from leaving, Baidu board members voted to sell shares. The company had an initial public offering on Aug. 5, 2005; the shares leapt from $27 to $122 each in their first day of trading on the Nasdaq—briefly valuing the company at more than $4 billion, and catapulting Li to billionaire status for the first time.

The 350% first-day gain represented the largest opening on the NASDAQ since the dot-com bubble burst—a stunning validation of investor appetite for China's internet potential. In December 2007, Baidu became the first Chinese company to be included in the NASDAQ-100 index.

What distinguished Baidu's IPO from other Chinese internet listings was the clarity of its competitive position. Unlike e-commerce or social media companies that faced fragmented markets, Baidu had already established search dominance. The company controlled over 60% of China's search market, with a technical and linguistic moat that foreign competitors would find difficult to breach.

For investors, the IPO validated a thesis that remains relevant today: the Chinese internet market was large enough to support indigenous champions, and those champions would benefit from both regulatory protection and cultural advantages that foreign competitors couldn't easily overcome.

IV. The Google Battle & Regulatory Dynamics (2006-2010)

The Competitive Landscape

The period from 2006 to 2010 represented Baidu's most consequential competitive battle—and its outcome would shape the company's trajectory for the next fifteen years.

In the last quarter of 2009, Google's market share in China was 35.6%, compared to Baidu's 58.4%. Google had been steadily building its presence, and the competition was real. Google had the world's best engineers, vast financial resources, and the most sophisticated search technology on the planet. Yet Baidu would not only survive but emerge stronger.

In the end, though, it wasn't censorship or competition that drove Google out of China. It was a far-reaching hacking attack known as Operation Aurora that targeted everything from Google's intellectual property to the Gmail accounts of Chinese human rights activists. The attack, which Google said came from within China, pushed company leadership over the edge. On January 12, 2010, Google announced, "We have decided we are no longer willing to continue censoring our results on Google.cn."

Why Baidu Won (Beyond Regulation)

The simplistic narrative is that Baidu won because Google was forced out by the Chinese government. The reality is more nuanced and more instructive for investors trying to understand competitive dynamics in emerging markets.

Long before $99 Xiaomi smartphones became ubiquitous nationwide, China's internet industry heavily relied upon internet cafés, where many Chinese consumers from lower-tier cities first accessed the internet. The company paid internet café franchises to switch the default homepage of their browsers to Baidu, whereby increasing its visibilities and successfully reached China's new internet users.

This distribution strategy was something Google, with its "don't be evil" mantra, was unwilling or unable to replicate. At the time when Baidu had built a sizable sales team of four thousand marketers, Google's China branch had only a few hundred employees, primarily operated through third-party partnerships, and did not even build its own marketing team.

Baidu also took advantage of China's less stringent intellectual property environment. For a time, Baidu operated something resembling Napster, offering easy access to unlicensed MP3 files through its mp3.baidu.com service. While controversial, this drove massive user traffic.

Google's share of the search engine market in China fell in the second quarter after its January 2010 announcement. Google had a 27.3 percent market share in the second quarter, down from the 29.5 percent in the previous quarter. Baidu's share rose to 70.8 percent from 67.8 percent in the first quarter, the first time it has exceeded 70 percent.

Regulatory Alignment as Strategy

Baidu's approach to Chinese regulation stands in stark contrast to Google's principled resistance. Under Robin Li's leadership, Baidu implemented content filtering and compliance mechanisms as core operational capabilities rather than reluctant concessions.

This strategic alignment created what some analysts call a "regulatory moat"—protection from foreign competition that doesn't depend on tariffs or explicit barriers but on the fundamental incompatibility between Western companies' values and China's internet governance model.

Noticeably, Baidu's market share grew rapidly to 80% after Google announced its withdrawal from mainland China. The departure of its most capable competitor handed Baidu near-monopoly status in China's search advertising market.

For investors, the Google episode illustrates a fundamental reality of Chinese tech investing: companies that align with government priorities gain sustainable competitive advantages, while those that resist face existential risks. Baidu chose alignment, and that choice—whatever its ethical implications—proved commercially decisive.

V. The Dominance Era & Challenges (2010-2016)

Peak Market Position

The years following Google's exit represented Baidu's greatest period of dominance—and the emergence of challenges that would eventually force its transformation.

In 2000, Robin (Yanhong) Li founded Baidu and turned the company into the largest Chinese search engine (with over 80% market share by search query) and the world's second largest search engine. This position made Baidu the default gateway to China's internet for hundreds of millions of users.

The company diversified beyond core search. In 2007, Baidu became the first Chinese search engine to receive a license allowing it to operate as a full-fledged news website, capable of providing original reports rather than just aggregating search results. This regulatory approval deepened Baidu's integration into China's information ecosystem.

Emerging Competition

By 2014, cracks in Baidu's dominance began appearing. Qihoo 360, originally an antivirus company, launched an aggressive search challenge. Mobile internet growth shifted user behavior away from desktop search, where Baidu was strongest, toward apps and platforms where its advantages were less pronounced.

More fundamentally, the rise of WeChat created a parallel internet ecosystem largely invisible to Baidu's crawlers. Content published within WeChat's walled garden couldn't be indexed by Baidu, meaning a growing share of China's most valuable content was beyond the company's reach.

The 2016 Medical Advertising Scandal

Then came the scandal that would force Baidu into a genuine reckoning with its business model.

Wei Zexi was a 21-year old Chinese college student from Shaanxi who died after receiving DC-CIK, an experimental treatment for synovial sarcoma at the Second Hospital of the Beijing Armed Police Corps; he had learned of it from a promoted result on the Chinese search engine Baidu. Wei's death led to an investigation by the Cyberspace Administration of China, prompting Chinese regulators to impose new restrictions on Baidu advertisements. State media outlets broadly condemned the role of the hospital and Baidu in his death, while users online additionally denounced Baidu's advertising practices. Baidu shares fell almost 14 percent in the days following reports of Wei's death.

Wei went through four treatments at the hospital, spending upwards of 200,000 yuan ($31,008 USD) with his family, but the treatments proved unsuccessful, causing Wei to die on April 12, 2016. Before his death, Wei accused Baidu of promoting false medical information; he also denounced the hospital for claiming high success rates for the treatment. Following Wei's death, several Internet users expressed disdain for Baidu's advertising practices.

The Wei Zexi incident exposed fundamental problems with Baidu's pay-for-placement model. Unlike other search engines such as Google and Yahoo!, promoted search results on Baidu are not clearly distinguished from other content. The investigation concluded that Baidu's pay-for-placement results influenced the fairness and objectivity of search results and therefore influenced Wei's medical choices. Regulators ordered Baidu to attach "eye-catching markers" and disclaimers to advertisements, reduce the amount of promoted results to 30% of the page, and establish better channels for users to complain about their services.

In a letter to employees, Baidu chief executive Robin Li wrote: "If we lose the support of users, we lose hold of our values, and Baidu will truly go bankrupt in just 30 days!" Li's letter said employees were making compromises for the sake of commercial interests and placing earnings growth above user experience.

The scandal accelerated Baidu's strategic pivot. Medical advertising had contributed 20-30% of search revenues. The regulatory crackdown and reputational damage made clear that Baidu needed new growth engines—not just for expansion, but for survival.

VI. The AI Pivot: From Search to Intelligence (2013-2019)

Strategic Reorientation

The AI pivot that would define Baidu's modern identity began earlier than most observers recognize—and with a level of investment commitment that distinguishes Baidu from its Chinese tech peers.

Since 2013, Baidu has significantly increased its R&D investment in AI, totaling nearly RMB 170 billion (~USD 23.4 billion) over the past decade. As of the end of 2023, Baidu led China in AI patent filings, with over 19,000 applications and over 9,200 patents granted, maintaining its leading position for six consecutive years.

In 2013, Baidu opened an AI research lab in Silicon Valley, developing technologies like visual perception, speech recognition, and human-machine interaction. This was no incremental R&D effort—it was a fundamental strategic reorientation that bet the company's future on AI before AI became fashionable.

In 2013, Baidu commenced development of autonomous driverless vehicles, through the Baidu research institute. This project gradually expanded to including 10,000 developers working on an open platform, and more than 50 partners across the world.

Robin Li's conviction about AI's importance predated the current generative AI boom by nearly a decade. The near-simultaneous launches of ChatGPT and Baidu's Ernie Bot highlighted how Baidu's sustained investment—over 20% of its budget directed to R&D during the mobile internet boom—secured its competitive edge.

Deep Learning and Early ERNIE Development

The ERNIE (Enhanced Representation through Knowledge Integration) series began in 2019, years before ChatGPT would make large language models a household topic. Ernie Bot is built on the company's ERNIE series of large language models, which have been in development since 2019. The service was first launched for invited testing on March 16, 2023, and was released to the general public on August 31, 2023, after receiving approval from Chinese regulators.

Baidu's early AI investments also extended into practical applications. The DuerOS voice assistant platform, smart speakers, and cloud AI services all emerged from this period of heavy R&D spending. Baidu's active AI venture made it the largest owner of machine learning and AI patents in 2022.

The strategic logic was clear: as search advertising matured and faced disruption from mobile apps and social media, AI capabilities could both defend existing businesses and create new revenue streams. Voice search would extend Baidu's relevance; AI cloud services would monetize its infrastructure investments; and autonomous driving would eventually create an entirely new transportation platform.

What distinguished Baidu's AI bet from similar pivots by other tech companies was its comprehensiveness. Rather than pursuing AI as an add-on capability, Baidu reorganized itself around AI as a core competency—a bet that is still playing out today.

VII. Apollo & The Autonomous Driving Bet (2017-Present)

Building the Platform

In April 2017, Baidu announced a project that would become the centerpiece of its AI transformation: Apollo.

Baidu announced a new project named "Apollo" which will provide an open, complete and reliable software platform for its partners in the automotive and autonomous driving industry to develop their own autonomous driving systems with reference vehicles and hardware platform. By opening up its robust, mature, and secure autonomous driving technology to the industry, Baidu aims to build a collaborative ecosystem.

Baidu now claims one of the largest partner ecosystems for an autonomous driving platform in the world: Its Apollo autonomous driving program now counts over 50 partners, including FAW Group, one of the major Chinese carmakers. Other partners include Chinese auto companies Chery, Changan and Great Wall Motors, as well as Bosch, Continental, Nvidia, Microsoft Cloud, Velodyne, TomTom, UCAR and Grab Taxi. The Apollo program also includes five of China's top universities. Baidu's COO Qi Lu called the platform the "Android of the autonomous driving industry, but more open and powerful."

The Android analogy was deliberate and strategically significant. Just as Google's Android created an ecosystem that generated returns through services rather than hardware, Baidu designed Apollo as an open platform that would position the company at the center of China's autonomous driving industry—regardless of which automakers ultimately succeeded.

Apollo is an open platform that provides a comprehensive, secure and reliable solution that supports all major features and functions of an autonomous vehicle. Since its launch in July 2017, Apollo has brought together 118 global partners across both automotive and technology industries.

Apollo Go Robotaxi Service

The platform strategy evolved into something more ambitious: operating the robotaxis directly. Apollo Go launched as Baidu's autonomous ride-hailing service, and its growth metrics have become increasingly impressive.

The autonomous vehicle service has transitioned to fully driverless operations across China in February 2025, removing safety drivers from its vehicles. Baidu's programme's fleet has covered 130 million autonomous kilometres.

Baidu's Apollo Go robotaxi unit said fully driverless weekly rides as of Oct. 31 have now surpassed 250,000 orders. Alphabet's Waymo reported the same number of paid weekly robotaxi rides in the U.S. back in April. Apollo Go also said that so far its robotaxis have not been involved in a major accident involving human injury or death.

The comparison with Waymo is instructive. Both companies have now achieved comparable weekly ride volumes, but Baidu has done so in a more challenging regulatory and infrastructure environment—and with dramatically lower vehicle costs.

Baidu may have an advantage in vehicle costs. Its sixth-generation model costs less than 30,000 USD, and the seventh generation is reportedly expected to cost under 20,000 USD.

Path to Profitability

The economics of robotaxi operations have been the critical question for investors. Chen Zhuo, general manager of Baidu's autonomous driving business unit, stated: "Our goal is that Apollo Go will break even in Wuhan by the end of 2024 and be profitable overall by 2025." Apollo Go will be the world's first commercially profitable self-driving mobility service platform, he added.

A spokesperson from Baidu's autonomous driving business unit previously indicated that Apollo Go's operations in Wuhan are nearing the break-even point, thanks to continuous expansion of operational scope and efficiency improvements. Based on current trends, Apollo Go is projected to achieve profitability by 2025.

Apollo's growth accelerated significantly, delivering over 3 million fully driverless operational rides in Q3 2025, representing a 212% year-over-year growth. AI cloud business continues to scale with healthy momentum, with subscription-based revenue from AI accelerator infrastructure surging 128% year over year.

Global Expansion

Baidu also received permits to test autonomous vehicles in Hong Kong in November 2024, marking its first entry into a right-hand drive market, demonstrating the adaptability of its autonomous driving technology to different traffic systems.

Baidu's Apollo Go primarily operates robotaxis in Wuhan and parts of Beijing, Shanghai and Shenzhen in mainland China. The company is also expanding to Hong Kong, Dubai, Abu Dhabi and, most recently, Switzerland.

Baidu plans to implement an asset-light strategy for its global expansion. "We have identified a variety of potential partners, including mobility service providers, local taxi companies, third-party fleet operators, and other potential partners. This asset-light approach will allow us to scale up efficiently while maintaining flexibility," Robin says.

For investors, Apollo Go represents both Baidu's most ambitious bet and its most uncertain one. Success would create an entirely new business line with recurring revenue and network effects; failure would mean a decade of heavy investment with limited returns. The path to profitability announced for 2025 will be a crucial proof point.

VIII. ERNIE & The Generative AI Race (2023-Present)

Launch and Development

When OpenAI released ChatGPT in late 2022, it ignited a global race that Baidu was uniquely positioned to join—thanks to years of prior investment in large language models.

Ernie Bot, full name Enhanced Representation through Knowledge Integration, is an artificial intelligence chatbot developed by the Chinese technology company Baidu. Ernie Bot rivals GPT models in Chinese NLP tasks. It is built on the company's ERNIE series of large language models, which have been in development since 2019. The service was first launched for invited testing on March 16, 2023, and was released to the general public on August 31, 2023, after receiving approval from Chinese regulators. Since its public launch, Ernie Bot has undergone several updates, with newer versions like ERNIE 4.0 and 4.5 released to improve its capabilities. The service has seen rapid user adoption, reportedly reaching over 200 million users by April 2024.

Rapid User Adoption

The growth trajectory has been remarkable. As of June 2024, Ernie Bot, the Chinese counterpart to OpenAI's ChatGPT, has attracted more than 300 million users and also supports 14.65 million developers.

The user base reportedly grew to 200 million by April 2024 and 300 million by June 2024. In September 2024, Baidu changed the chatbot's Chinese name from "Wenxin Yiyan" (文心一言) to "Wenxiaoyan" (文小言) to position it as a search assistant.

The API usage metrics are equally impressive. ERNIE handled approximately 1.65 billion API calls daily in December 2024, with external API calls increasing by 178% quarter over quarter, highlighting particularly strong momentum.

Technical Capabilities and Competitive Positioning

Baidu launched its latest foundation models, including native multimodal foundation model ERNIE 4.5 and deep-thinking reasoning model ERNIE X1. Both models are now freely accessible to individual users through ERNIE Bot's official website.

With the launch of ERNIE 4.5 and ERNIE X1, ERNIE Bot is made free to the public ahead of schedule. As a deep-thinking reasoning model with multimodal capabilities, ERNIE X1 delivers performance on par with DeepSeek R1 at only half the price.

The decision to make ERNIE Bot free was strategic—responding to the emergence of DeepSeek as a formidable Chinese AI competitor. Some pundits speculate that Baidu's founder and CEO Robin Li Yanhong's absence at the meeting between Chinese officials, including President Xi Jinping and private sector business leaders like Jack Ma, was the reason for a stock drop on Monday. Others point to Baidu's recent announcement of making ERNIE Bot, its AI model, free from April 1.

Most recently, ERNIE 5.0 is the latest foundation model of the company. As a natively omni-modal model, ERNIE 5.0 jointly models text, images, audio, and videos. Baidu unveiled the natively omni-modal foundation model, ERNIE 5.0, at its annual flagship event, Baidu World 2025. ERNIE 5.0 jointly models text, images, audio, and videos for comprehensive multimodal understanding and generation.

For investors, the generative AI race presents both opportunity and risk. Baidu has first-mover advantage in China and deep technical capabilities, but the competitive landscape is intensifying rapidly. DeepSeek's emergence demonstrates that new entrants can challenge established players, and the economics of generative AI—with high infrastructure costs and uncertain monetization paths—remain challenging.

IX. Current Business & Financial Overview (2024-2025)

Revenue and Business Mix

Baidu's recent financial performance reflects the tension between a declining legacy business and growing AI initiatives.

Baidu announced its unaudited financial results for the third quarter ended September 30, 2025. "In the third quarter, we demonstrated AI's transformative value across our portfolio. AI Cloud maintained solid growth momentum, driven by broadening enterprise adoption of our AI products and solutions. Apollo Go significantly accelerated the scaling of its fully driverless operations and kept advancing global expansion, including entry into Switzerland, all while maintaining industry-leading safety standards. In our Mobile Ecosystem, AI-native monetization products such as agents and digital humans delivered rapid revenue growth, showing strong long-term potential," said Robin Li.

Baidu Inc. reported its third-quarter 2025 financial results, highlighting a mixed performance with a decline in overall revenue but significant growth in its AI Cloud segment. The company posted total revenues of RMB 31.2 billion, a 7% decrease year-over-year. Despite the revenue decline, Baidu's AI Cloud revenue surged by 21%, reaching RMB 6.2 billion.

The revenue mix shift is accelerating. In the third quarter of 2025, AI Cloud Infra generated RMB 4.2 billion, up 33% year over year. AI Applications, including products such as Baidu Wenku, Baidu Drive and Digital Employee, produced RMB 2.6 billion. Meanwhile, AI-native Marketing Services surged to RMB 2.8 billion, up 262%, as customers increasingly adopted AI-driven agents and digital humans to boost productivity and marketing performance.

AI Cloud Growth

The AI Cloud segment has become Baidu's primary growth engine. "Our AI Cloud business demonstrated robust momentum with fourth-quarter revenue growth accelerating to 26% year over year, offsetting the softness in online marketing business," said Junjie He, Interim CFO of Baidu.

AI Cloud: Revenue reached RMB 6.5 billion in Q2 2025, up 27% year-over-year, with non-GAAP operating profit achieving year-over-year growth. Intelligent Driving: Apollo Go provided over 2.2 million fully driverless rides to the public in Q2, up 148% year-over-year.

Balance Sheet and Capital Returns

Baidu returned US$356 million to shareholders since Q4 2024, bringing the cumulative repurchase to over US$1 billion since 2024 and to US$1.7 billion under the 2023 share repurchase program.

After this one-time impairment, our asset base and portfolio profile is in a much healthier position and better aligned with advanced AI computing demands. On capital expenditures, we are maintaining a high level of investment. Since Baidu launched ERNIE in March of 2023, we have invested well above CNY 100 billion in AI investment.

For long-term investors, the key question is whether AI Cloud and Apollo Go growth can offset the structural decline in search advertising before Baidu's balance sheet is depleted. The company has substantial cash reserves and continues generating positive operating cash flow, but the timeline for AI profitability remains uncertain.

X. Competitive Analysis & Investment Considerations

The Bull Case

Baidu's bull case rests on several mutually reinforcing advantages:

First-Mover Advantage in Chinese AI: Since 2013, Baidu has significantly increased its R&D investment in AI, totaling nearly RMB 170 billion (~USD 23.4 billion) over the past decade. As of the end of 2023, Baidu led China in AI patent filings, with over 19,000 applications and over 9,200 patents granted, maintaining its leading position for six consecutive years. This decade of investment has created technical capabilities and talent pools that newer entrants cannot easily replicate.

Apollo Go's Path to Profitability: If Apollo Go achieves profitable operations in 2025 as projected, it would validate years of autonomous driving investment and create a new recurring revenue stream with potential for global expansion. The asset-light international strategy could enable rapid scaling without proportional capital requirements.

ERNIE Ecosystem Effects: With 430+ million users and 1.5 billion daily API calls, ERNIE is building network effects that could strengthen Baidu's position in enterprise AI services. The integration across Baidu's product ecosystem—search, cloud, maps, productivity tools—creates cross-selling opportunities.

Regulatory Moat: Baidu's alignment with Chinese government priorities provides protection from foreign competition and potential preferential treatment in areas like autonomous driving permits and AI infrastructure contracts.

The Bear Case

Significant risks temper the bull thesis:

Structural Decline in Core Business: Online marketing revenue continues falling—down 15% year-over-year in Q2 2025. This core business generated 70% of revenue historically, and its erosion pressures overall profitability while AI businesses mature.

DeepSeek and Competition: The emergence of DeepSeek demonstrates that new entrants can match Baidu's AI capabilities at lower costs. The decision to make ERNIE Bot free suggests competitive pressure is intensifying. Unlike search, where Baidu had sustainable advantages, the generative AI landscape remains highly contested.

Regulatory and Geopolitical Risks: Baidu faces regulatory oversight on multiple fronts—content compliance, AI safety, autonomous vehicle operations—any of which could constrain operations. Additionally, U.S.-China technology tensions create risks for international expansion and semiconductor access.

Execution Risk: Baidu is attempting multiple simultaneous transformations: AI Cloud growth, autonomous driving scale-up, generative AI monetization, and core business stabilization. The complexity of executing all of these while managing declining advertising revenue creates operational challenges.

Porter's Five Forces Analysis

Threat of New Entrants (Moderate): While building a search engine or AI platform requires substantial capital, companies like DeepSeek have demonstrated that new entrants can compete effectively in AI. Baidu's regulatory relationships and distribution advantages provide some barriers, but technological disruption remains possible.

Bargaining Power of Suppliers (Moderate-High): Semiconductor constraints, particularly access to advanced chips following U.S. export controls, give suppliers significant leverage. Baidu has developed domestic chip partnerships but remains dependent on imported technology for some applications.

Bargaining Power of Buyers (High): Advertisers have alternatives including WeChat advertising, Alibaba's ecosystem, and ByteDance's platforms. Enterprise AI customers can choose from multiple providers. This buyer power constrains pricing.

Threat of Substitutes (High): Mobile apps, social media platforms, and specialized AI tools all substitute for traditional search. WeChat's ecosystem, in particular, captures user attention that previously flowed through Baidu.

Competitive Rivalry (High): Competition is intense across all segments. In search, Sogou and others compete for market share. In AI Cloud, Alibaba and Huawei are formidable rivals. In autonomous driving, Pony.ai, WeRide, and automakers' in-house efforts create pressure.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Baidu benefits from scale in AI infrastructure—the more users on ERNIE, the more data for improvement; the more Apollo Go miles driven, the better the autonomous driving models become. However, these scale advantages are contestable.

Network Effects: ERNIE's developer ecosystem (14.65 million developers) creates network effects where more developers attract more users, which attracts more developers. Apollo's partner ecosystem in autonomous driving functions similarly.

Switching Costs: Enterprise customers integrating Baidu's AI APIs face switching costs in terms of retraining and integration. However, the industry's move toward standardized interfaces may reduce these costs over time.

Counter-Positioning: Baidu's positioning as China's AI champion creates advantages that foreign competitors cannot easily replicate. However, domestic competitors can adopt similar positioning.

Cornered Resource: Baidu's regulatory relationships and licenses for autonomous driving operations in Chinese cities represent cornered resources. Its decade of AI patents also creates defensible intellectual property.

Process Power: Baidu has developed operational expertise in running robotaxi services at scale—from vehicle maintenance to regulatory compliance to customer service—that would take competitors years to replicate.

Branding: The Baidu brand remains strong in China, though the Wei Zexi scandal and competition from newer platforms have eroded its position among younger users.

Key KPIs to Track

For investors monitoring Baidu's ongoing performance, three metrics deserve particular attention:

-

AI Cloud Revenue Growth Rate: This is the clearest indicator of whether Baidu's AI transformation is generating commercial traction. The 21-27% year-over-year growth in recent quarters suggests momentum, but sustaining this rate while improving margins is essential.

-

Apollo Go Unit Economics: The path to profitability hinges on cost per ride, rides per vehicle per day, and revenue per ride. Management's guidance about breaking even in Wuhan by end of 2024 and overall profitability by 2025 provides specific targets against which to measure progress.

-

ERNIE API Call Volume and Monetization: Daily API calls (currently ~1.5 billion) indicate platform adoption. More importantly, the revenue generated per API call—and the trend toward paid enterprise usage—will determine whether ERNIE becomes a significant profit contributor.

Material Legal/Regulatory Overhangs

Investors should be aware of several ongoing regulatory considerations:

-

Content Compliance: Baidu operates under China's internet content regulations, which require ongoing investment in moderation and filtering. Regulatory enforcement actions could impact operations.

-

AI Safety Regulations: China is developing AI-specific regulations that could affect how ERNIE and other AI products are deployed and monetized.

-

Autonomous Driving Permits: Apollo Go's expansion depends on regulatory approvals in each new city and country. Delays or restrictions could slow growth.

-

VIE Structure: Like other Chinese companies listed in the U.S., Baidu uses a Variable Interest Entity structure that creates legal complexity and regulatory risk.

XI. Conclusion: The Search for Tomorrow

Twenty-five years after Robin Li and Eric Xu launched Baidu from a Beijing hotel room, the company finds itself at another inflection point—perhaps its most consequential since the Google battle of 2010.

The core search business that built Baidu's fortune is in structural decline, squeezed by mobile apps, social media platforms, and shifting user behavior. "2024 marked a pivotal year in our ongoing transformation from an internet-centric to an AI-first business," Robin Li declared. But transformation is not yet accomplished—it is underway, with the outcome still uncertain.

The assets Baidu brings to this transformation are substantial. Apollo Go, the company's autonomous ride-hailing service, has completed over 17 million cumulative rides, the world's largest. ERNIE has attracted 430+ million users. AI Cloud is growing at 20%+ annually. The patent portfolio, the engineering talent, and the regulatory relationships all provide foundation for continued innovation.

Yet the challenges are equally formidable. DeepSeek's emergence demonstrates that AI leadership is not guaranteed by historical investment. The advertising business decline is accelerating. Competition in every segment—cloud, autonomous driving, generative AI—is intensifying.

Robin Li highlighted the importance of internalizing AI capabilities: "When you internalize AI, it becomes a native capability and transforms intelligence from a cost into a source of productivity. We should focus on integrating AI with every task we do to make it a native driving force for corporate and personal growth."

For investors, Baidu represents a concentrated bet on Chinese AI development. Success would mean capturing significant value from one of the world's largest technology markets. Failure would mean watching a once-dominant company diminish as competitors claim the future it helped pioneer.

The search for tomorrow continues—now in robotaxis navigating Wuhan's streets, in AI models processing billions of daily queries, and in the ambitious vision of a company that has reinvented itself before and is determined to do so again.

Key Metrics Summary

| Metric | Value | Period |

|---|---|---|

| Total Revenue | ~$18.5 billion | 2024 |

| AI Cloud Revenue | RMB 6.2 billion | Q3 2025 |

| AI Cloud Growth | 21% YoY | Q3 2025 |

| ERNIE Bot Users | 430+ million | Late 2024 |

| Daily API Calls | 1.5+ billion | December 2024 |

| Apollo Go Weekly Rides | 250,000+ | October 2025 |

| Apollo Go Total Rides | 17+ million | November 2025 |

| R&D Investment (10-year) | ~$23.4 billion | 2013-2023 |

| Search Market Share | ~50% | 2024 |

This analysis is intended for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence and consider their individual circumstances before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube