UMC: Taiwan's First Semiconductor Company and the Art of Strategic Retreat

Introduction: The Overlooked Pioneer

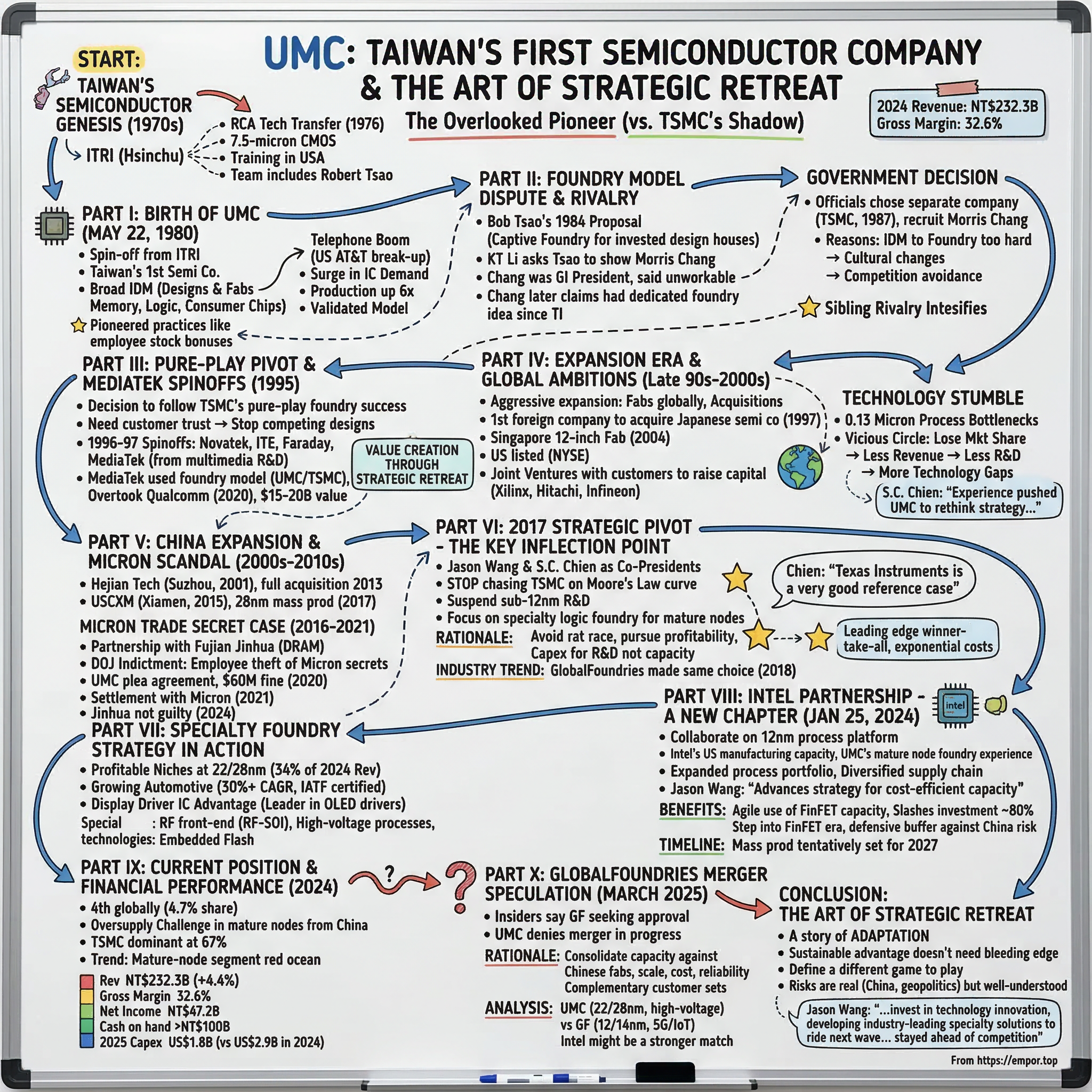

In the shadow of Taiwan Semiconductor Manufacturing Company's $500 billion-plus market capitalization and its status as the world's most valuable semiconductor company sits its older sibling—United Microelectronics Corporation. UMC was there first. It was Taiwan's first semiconductor company, the first to go public on the Taiwan Stock Exchange, and arguably the original innovator of the foundry concept that TSMC would later perfect and dominate.

UMC, founded in 1980 as a spin-off from the government-sponsored Industrial Technology Research Institute (ITRI), was Taiwan's first semiconductor company. Today, in 2024, UMC's consolidated revenue totaled NT$232.3 billion with a gross margin of 32.6% and an operating margin of 22.2%, resulting in earnings per share of NT$3.80.

In Q4 2024, UMC ranked fourth globally in foundry revenue, holding a 4.7% market share. This is the story of a company that could have been TSMC—that perhaps should have been TSMC—but instead charted a different course, one that offers profound lessons about the economics of Moore's Law, the wisdom of knowing when to retreat, and the strategic value of finding your niche in an industry dominated by giants.

The central question for investors studying UMC isn't whether it can catch TSMC—that ship sailed decades ago. The more interesting question is this: How did Taiwan's first semiconductor company transform from a would-be technology leader into a profitable specialty foundry, and what does its 2024 partnership with Intel signal about the future of the mature-node market?

Part I: Taiwan's Semiconductor Genesis and the Birth of UMC

The RCA Technology Transfer: Seeds of an Industry

To understand UMC, one must first understand Taiwan's deliberate national strategy for semiconductor industry development in the 1970s. The island faced an existential economic challenge: TSMC was founded in 1987 by Morris Chang in cooperation with the government-funded Industrial Technology Research Institute (ITRI) based in Hsinchu. However, the history of semiconductor production in Taiwan stretches back to the early 1970s.

Taiwan's economy in the 1970s relied heavily on textiles and basic electronics—industries with limited long-term growth potential in the face of rising competition from lower-cost producers. The island's leadership, guided by economic architects like Dr. K.T. Li (李國鼎), recognized that semiconductor manufacturing represented a strategic opportunity to leapfrog into higher-value industries.

After the government gave the green light, a team of engineers was sent to various fabs in the U.S., particularly an RCA fab in Ohio, where the engineers learned the fundamentals of chip production. Meanwhile, in Taiwan, ITRI was busy building the foundations of the country's first fab in Hsinchu.

The RCA technology transfer agreement, signed in 1976, gave Taiwan access to 7.5-micron CMOS technology—considered mature even then but sufficient to bootstrap an indigenous capability. The engineers who traveled to America for training would become the founding generation of Taiwan's semiconductor industry. Among them was a young engineer named Robert Tsao (曹興誠).

Robert Tsao was born in China in 1947, but his parents moved to Taiwan in 1948 and he grew up and built his career there. Mr. Tsao earned a Bachelor's degree in Electrical Engineering from National Taiwan University and a Master's degree in Management Science from National Chiao Tung University in 1972. He was recruited to be the Vice Chairman of Electronics Research & Service Organization (ERSO) where he played a very key role from 1979 to 1981. He was instrumental in organizing ITRI where he oversaw the development of Taiwan's first integrated circuit manufacturing line which became the basis for UMC.

May 22, 1980: Taiwan's First Semiconductor Company

UMC was founded as Taiwan's first semiconductor company in 1980 as a spin-off of the government-sponsored Industrial Technology Research Institute (ITRI). Being spun off from ITRI in 1980 wasn't just a founding event; it was transformative. It marked Taiwan's deliberate entry into semiconductor manufacturing, setting the stage for the island's dominance.

Tsao founded UMC as a spin-off from the government research establishment ITRI in 1980 and set it up as a broad-based IDM designing and fabbing memory, standard logic, microprocessors including x86 clones, telecoms chips, custom ICs and consumer devices including watch chips.

The early years were not easy. At the close of 1982, UMC generated less than $5 million USD in revenue and turned a net loss. But the next year, things turned around.

The Telephone Boom: UMC's First Big Break

Over in the United States, the AT&T Bell System monopoly was breaking up. This necessitated a large surge in ICs for new telephones, and the Japanese could not meet the sudden, massive demand. UMC answered the call at the right time, and production surged 6 times over from 4 million pieces to 24 million pieces—turning a substantial profit. But this rapid export surge was only temporary.

This early success did more than validate UMC's business model—it gave the Taiwanese government confidence to continue investing in the semiconductor industry. UMC, spun off from ITRI's Electronics Research and Service Organization in 1980, turned a profit in its very first year by riding the wave of the electronic watch boom. That early success gave the government the confidence to back a second, more ambitious semiconductor initiative—the VLSI Project—which directly led to the founding of TSMC.

For almost a decade, UMC was "the only player in town." The company pioneered practices that would become standard in Taiwan's tech sector, including employee stock bonus plans that helped attract top engineering talent—a practice common in Silicon Valley but rare in Taiwan at the time.

For investors, UMC's early history illustrates a crucial point: being first matters less than being right about the business model. UMC proved the concept that Taiwan could manufacture semiconductors competitively. But what UMC could not predict was that a new business model—the pure-play foundry—would emerge to reshape the entire industry.

Part II: The Foundry Model Dispute and the Birth of a Rivalry

The 1984 Proposal: Who Really Invented the Foundry?

The relationship between UMC and TSMC is one of the semiconductor industry's most fascinating sibling rivalries—tinged with bitterness, accusations, and the fog of competing historical narratives.

TSMC and UMC have long been rivals. This dates back to Tsao's "accusation" that Morris Chang stole the independent foundry idea, and then prevented UMC from adopting the model until after TSMC was founded.

According to Robert Tsao's account, in 1984, after the telephone boom ended and UMC needed to find new business, he submitted an expansion plan to Taiwan's Ministry of Economic Affairs. His proposal recognized that the semiconductor industry was fragmenting—that integrated device manufacturers were finding it increasingly difficult to master every step of the value chain. He proposed an "OEM foundry" model where UMC would focus exclusively on manufacturing while investing in Taiwanese design houses that would bring their designs to UMC for fabrication.

This idea sounds similar to though not quite entirely like the independent foundry idea that Morris Chang and TSMC pioneered. The main difference was that Tsao's proposal would only serve design houses that UMC invested in—mostly favoring those in Taiwan. Chang's dedicated foundry would take on all comers.

The distinction is crucial. Tsao's vision was essentially a captive foundry model tied to a portfolio of affiliated design companies. Morris Chang's vision—the one that would ultimately revolutionize the semiconductor industry—was a fully independent foundry that would manufacture chips for any customer, including competitors. This "take all comers" approach eliminated channel conflict and created a trusted neutral platform that even the most secretive chip designers could use.

According to Tsao, he showed the proposal to the Ministry of Economic Affairs. Dr. KT Li—who had previously served as the Minister of Finance and is known as the father of Taiwan's modern economy—asked Tsao to bring the proposal to Morris Chang. At this time, Dr. Chang had just become President of General Instrument—a semiconductor manufacturer in New York. Dr. Chang had already then gained widespread respect in the Chinese community for rising to the Number 3 spot in Texas Instruments. Tsao sent the proposal to Chang and had dinner with him but nothing came out of it.

Shortly thereafter, the Ministry of Economic Affairs dropped UMC's expansion proposal. Tsao later claims that this was because Dr. Chang sent a letter to KT Li, saying that the proposal was unworkable.

Morris Chang for his part says that he has had his dedicated foundry idea since his days at Texas Instruments. He had proposed it to both Texas Instruments and Intel, who turned it down.

The Government's Decision: A New Company, A Sweeter Deal

Behind the scenes, the government strongly considered UMC's proposal but opted to create a separate company, TSMC. Ultimately, officials had two major concerns. First, they felt that it would be easier to set up a dedicated manufacturer from scratch than it would be to convert an IDM into one. Their thinking on this turned out to be correct. UMC later discovered that becoming a foundry not only meant big cultural changes but also working with their former competitors.

Then in 1987, Morris Chang was recruited from a government research position to found TSMC as an entirely private enterprise.

Regardless of how it happened, you can only imagine Tsao's frustration when TSMC opened its doors in 1987. To add to the insult of losing the first mover's advantage, UMC felt that the Taiwanese government gave its second child a sweeter deal during the transfer and founding. This includes larger amount of subsidies and a better process node. The sibling rivalry between the two companies bubbled up and intensified as the Taiwan semiconductor industry took off in the late 1980s and 1990s.

At the start, TSMC took orders from everyone except UMC. The reasoning apparently being that TSMC felt that doing wafer manufacturing for UMC would allow the latter to triple their capacity and take more share.

The rivalry extended to the boardroom. Early on, Morris Chang served as chairman of both UMC and TSMC. Then in 1991, Bob Tsao and the other directors of the UMC board asked Chang to resign in the name of "competition avoidance."

For investors, this historical dispute contains an important lesson: in technology industries, subtle differences in business model design can compound into enormous outcome differences over decades. Tsao's captive foundry model and Chang's open foundry model might have seemed similar in 1984. But the open model's ability to attract customers who feared competing with their own manufacturer created a self-reinforcing cycle of trust, volume, and learning that would ultimately make TSMC the world's most valuable semiconductor company.

Part III: The Pure-Play Pivot and the MediaTek Spinoffs

1995: The Decision That Created Billions

By 1995, it had become clear that TSMC's pure-play foundry model was winning. Customers preferred dealing with a manufacturer that didn't compete with them, and TSMC was accumulating manufacturing expertise at an accelerating pace. UMC faced a choice: continue operating as an integrated device manufacturer with its own products, or pivot to match TSMC's model.

The decision to transform from an IDM to a pure-play foundry was one of the most consequential strategic choices in UMC's history. But there was a catch: UMC decided that in order to keep up, it needed to pivot and also adopt the independent foundry business model. But customers could not accept UMC as an independent foundry unless they knew that UMC would not compete with it. So to gain customer trust, they decided to spin off their semiconductor design operations as multiple companies.

In 1995, following on the runaway success of TSMC, UMC decided to drop proprietary products and become a foundry.

The Spinoff Factory: Creating Taiwan's Fabless Ecosystem

In 1996 and 1997, UMC spun off its IC design units into multiple independent companies. A decision was made by UMC to transform into a pure-play foundry in 1995, which led to the spin-off of multiple design subsidiaries such as Novatek, AMIC, ITE Tech, Davidcom, Faraday and MediaTek.

MediaTek began in 1997 as a spinoff startup. It had been a part of United Microelectronics Corporation or UMC. UMC was Taiwan's first indigenous semiconductor company and had been operating as an integrated device manufacturer. Thus was founded MediaTek, which had once been UMC's R&D department for multimedia devices.

The MediaTek spinoff story deserves particular attention because it illustrates how UMC's strategic retreat created enormous value—just not for UMC shareholders directly.

On May 28, 1997, the unit was spun off and incorporated. MediaTek Inc. was listed on the Taiwan Stock Exchange under the "2454" code on July 23, 2001. The company started out designing chipsets for optical drives and subsequently expanded into chips for DVD players, digital TVs, mobile devices.

MediaTek defeated those incumbents by offering a cheaper, highly integrated system on a chip. They contracted with independent foundries like UMC and TSMC to build this chip. Since the foundries took care of the manufacturing, it allowed MediaTek to focus on the design and selling. This is the crux of the fabless semiconductor model. It is also, as it turns out, very profitable.

The results were spectacular. Within just four years of its spinoff, MediaTek achieved an annual revenue of around $200 million, making it the second-largest fabless semiconductor firm in Taiwan.

MediaTek overtook Qualcomm as the largest vendor of smartphone chipsets in the world in the third quarter of 2020, mainly due to significant growth in the Indian and Latin American markets.

Today, MediaTek is worth approximately $15-20 billion and is one of the world's largest fabless semiconductor companies. Novatek became the global leader in driver ICs. Both MediaTek and Novatek are among the world's top 10 biggest fabless companies.

For investors, this raises a fascinating counterfactual: what would UMC be worth today if it had retained these design businesses? The answer is probably "much less," because the companies' success depended on the credibility that came from independence—independence from any manufacturing bias. UMC's willingness to let go of these businesses was not a failure of corporate strategy; it was an essential ingredient in their success.

Part IV: The Expansion Era and Global Ambitions

Building a Global Footprint

Through the late 1990s and 2000s, UMC pursued an aggressive expansion strategy, building fabs and making acquisitions around the world. UMC was also the first foreign company to acquire a Japanese semiconductor company in 1997.

UMC listed on the New York Stock Exchange as Taiwan's second semiconductor company to do so, following TSMC. The company invested heavily in capacity expansion and technology development, including early adoption of copper interconnect technology and 0.13 micron process technology.

In 2004, UMC's 12-inch wafer fab in Singapore entered mass production, giving the company manufacturing presence outside Taiwan years before TSMC would establish similar international operations.

In 2019, United Microelectronics Corporation (UMC) acquired Mie Fujitsu Semiconductor, a Japanese semiconductor foundry. The acquisition allowed UMC to expand its manufacturing capabilities and gain access to new markets and customers.

The company pursued customer partnerships aggressively. Lacking the large, rich customers that TSMC cultivated, UMC resorted to joint ventures with customers to raise capital for fab construction—partnerships with companies like Xilinx, Hitachi, and Infineon.

This expansion-through-partnership model reflected a fundamental difference in competitive position. TSMC's customers were willing to fund capacity expansion through long-term agreements because they trusted TSMC's technology roadmap. UMC, already falling behind technologically, had to offer equity stakes to secure commitments.

The Technology Stumble: 0.13 Micron and Beyond

The seeds of UMC's eventual retreat from leading-edge technology were planted in the early 2000s. Co-President Chien explained: "UMC encountered some bottlenecks in the 0.13-micron process race. It was a vicious circle in which we lost market share in the advanced node market segment and saw impacts on our revenues, coupled with a decline in our available R&D capital. Such experience pushed UMC to rethink its strategy to avoid being trapped again in a rat race."

This "vicious circle" is one of the most important dynamics in semiconductor manufacturing economics. Advanced process development requires enormous R&D investment. That investment is justified by winning high-volume customers who need leading-edge processes. Those customers choose manufacturers based on yield, reliability, and technology roadmap credibility. A single stumble—a yield problem, a delay, a technical setback—can cause customers to shift to competitors. Lost customers mean lost revenue to fund the next generation of R&D, which means more technology gaps, which means more lost customers.

TSMC, with its larger customer base, greater accumulated learning, and stronger relationship with Apple and other premium customers, could survive technical hiccups. UMC, operating on thinner margins with less customer loyalty, found that each stumble compounded into lasting competitive disadvantage.

Part V: The China Expansion and the Micron Scandal

Entering the Chinese Market

In 2001, UMC moved into China by setting up Hejian Technology (Suzhou) Co. in Jiangsu. This led to Tsao being charged in 2005 with violating Taiwan's Business Entity Accounting Act. He was found not guilty in 2010 by the Taiwan High Court.

In 2013, UMC fully acquired Hejian Technology Wafer Fab in Suzhou. In 2015, the company established USCXM, a 12-inch wafer fab in Xiamen, Fujian Province. By 2017, 28nm mass production began at the Xiamen facility.

The Micron Trade Secret Case: A Cautionary Tale

The most damaging episode in UMC's recent history began in 2016 when the company signed an agreement with Fujian Jinhua, a Chinese state-owned enterprise, to jointly develop DRAM process technology. The partnership would lead to criminal charges, a U.S. Department of Justice indictment, and a plea agreement that cost UMC $60 million and years of legal uncertainty.

The Department of Justice announced that United Microelectronics Corporation, Inc., a Taiwan semiconductor foundry, pleaded guilty to criminal trade secret theft and was sentenced to pay a $60 million fine, in exchange for its agreement to cooperate with the government in the investigation and prosecution of its co-defendant, a Chinese state-owned-enterprise. A federal grand jury had indicted UMC in September 2018, along with Fujian Jinhua, for conspiracy to steal trade secrets from Micron Technology.

The mechanics of the alleged theft involved former Micron employees who joined UMC. According to the facts admitted in connection with the guilty plea, UMC hired three individual defendants from Micron's Taiwan subsidiary. UMC made Chen a senior vice president and assigned him to lead negotiation of an agreement with Fujian Jinhua to develop DRAM technology. As a foundry company, UMC previously made logic chips designed by other companies but did not make DRAM memory chips. Chen hired Ho and Wang to join the DRAM development team, and Ho and Wang brought Micron's confidential information to UMC from Micron's Taiwan subsidiary.

As part of the Plea Agreement, DOJ agreed to dismiss the original indictment against UMC, including allegations of conspiracy to commit economic espionage and conspiracy to steal multiple trade secrets from Micron Technology.

The actions by employees were both unauthorized and contrary to UMC policies. UMC top management was not aware at the time of the above actions. Upon learning about the conduct referenced above, UMC undertook significant efforts to remove any unauthorized information from the process technology.

In November 2021, UMC and Micron agreed to withdraw complaints against each other globally following a years-long legal dispute. UMC made an undisclosed one-time payment to Micron Technology. Both parties also announced their intention to seek mutual business cooperation opportunities in the future.

In February 2024, US District Judge Maxine M. Chesney ruled that US prosecutors failed to prove that Chinese firm Fujian Jinhua had misappropriated trade secrets from Micron. Therefore, the Court found Jinhua not guilty.

For investors, the Micron case illustrates the risks that come with China partnerships in the semiconductor industry. The U.S.-China technology conflict has made such collaborations increasingly fraught with regulatory and reputational risk. UMC's experience—even though the company maintained that its top management was unaware of the misconduct—demonstrates how quickly a business partnership can become a legal and geopolitical liability.

Part VI: The 2017 Strategic Pivot—The Key Inflection Point

The Most Important Decision in Modern UMC History

In 2017, when Jason Wang and S.C. Chien took over as co-presidents, UMC announced it would no longer invest in nodes more advanced than 12nm, citing limited customer demand.

This decision—to stop chasing TSMC down the Moore's Law curve and instead focus on profitable leadership in mature process nodes—is arguably the defining strategic choice of UMC's modern era. At the time, it looked like surrender. With the benefit of hindsight, it looks like wisdom.

In 2017, UMC recognized its role could make a difference. Rather than fighting to be a technology leader in the advanced-node process segment, UMC can be more capable of being a leader in the more mature process segments. Besides, in the 14nm and older process segment, there's still room for growth.

UMC disclosed previously plans to enhance its 14nm and 12nm process offerings but to suspend sub-12nm process R&D. UMC has shifted its focus away from keeping up in the process-technology race and re-positioned itself to a specialty logic foundry.

The co-presidents explained the rationale in detail:

There were a number of factors we had considered behind the decision we made in 2017. As UMC steps into the FinFET segment, we intend to put our capex focus on technology R&D rather than manufacturing capacity. In fact, UMC's investment in 28nm manufacturing capacity has still been a burden for the company. As we enter the era of FinFET, we want to slow down the pace of expansion and pursue our growth in mature and specialty market segments for profitability.

The Texas Instruments Inspiration

When asked about reference cases for this transformation, Co-President Chien revealed: "Texas Instruments is a very good reference case for us."

Texas Instruments had made a similar strategic decision years earlier, exiting commodity digital chips to focus on analog and embedded processing—lower-margin businesses that had proven to be highly durable and profitable over time. TI's success demonstrated that you didn't need to be on the bleeding edge of Moore's Law to build a great semiconductor company.

GlobalFoundries Made the Same Choice

UMC wasn't alone in recognizing the unsustainability of the leading-edge race. In 2018, GlobalFoundries announced its decision to halt the development of sub-7nm nodes and refocus on specialized processes.

GlobalFoundries was on track to tape out its clients' first chips made using its 7nm process technology, but "a few weeks ago" the company decided to take a drastic, strategic turn. The CTO stressed that the decision was made not based on technical issues, but on a careful consideration of business opportunities.

"The vast majority of today's fabless customers are looking to get more value out of each technology generation to leverage the substantial investments required to design into each technology node," explained GlobalFoundries CEO Tom Caulfield. "Essentially, these nodes are transitioning to design platforms serving multiple waves of applications, giving each node greater longevity. This industry dynamic has resulted in fewer fabless clients designing into the outer limits of Moore's Law."

The economics were simple but brutal. Development of leading-edge process technologies is extremely expensive. Every new node requires billions of dollars in investments. Those costs are eventually amortized over each chip the company makes, so to keep increasing R&D costs from driving up chip prices, foundries need to produce more chips.

The Fundamental Economics: Why Leading Edge Became Winner-Take-All

The semiconductor industry's evolution toward winner-take-all dynamics at leading-edge nodes reflects a fundamental economic reality. Each new process node requires exponentially more capital investment—not just in equipment, but in the armies of engineers needed to develop and debug the process. A cutting-edge fab now costs $20 billion or more to build. The equipment required—particularly extreme ultraviolet (EUV) lithography machines from ASML—costs hundreds of millions per unit and has multi-year lead times.

To earn an acceptable return on these investments, a foundry needs massive volumes. And to get massive volumes, it needs to win the highest-volume customers—Apple, Nvidia, AMD, Qualcomm. These customers choose foundries based on technology leadership, yield rates, and roadmap credibility. A foundry that falls behind on one generation will lose these customers to competitors, reducing the revenue available to fund the next generation. The result is a reinforcing cycle where the leader gets stronger and the followers fall further behind.

TSMC's dominant position—Taiwan dominates the global semiconductor foundry market, with TSMC alone commanding a staggering 62% share of total foundry revenue—reflects decades of accumulated advantage from this dynamic.

For UMC and GlobalFoundries, the choice was clear: either accept billions in annual losses chasing an ever-receding leader, or find a different game to play.

Part VII: The Specialty Foundry Strategy in Action

Finding Profitable Niches at 22/28nm

Since 2017, UMC has executed on its specialty foundry strategy with increasing discipline. UMC's 22/28nm portfolio remained the largest contributor, with revenue increasing 15% in 2024. Notably, customers are showing strong interest in migrating to 22nm specialty platforms for next-generation networking and display driver applications, which offer significant power savings and performance advantages over 28nm solutions.

Revenue contribution from 22/28-nanometer technology was 34% of total revenue for 2024.

The company has developed deep expertise in specialty processes that serve specific applications:

UMC, an industry leader in RF front-end module IC solutions, has announced the industry's first 3DIC solution for RFSOI technology. Available on UMC's 55nm RFSOI platform, the stacked silicon technology reduces die size by more than 45% without any degradation of radio frequency performance, enabling customers to efficiently integrate more RF components to address the greater bandwidth requirements of 5G applications.

Automotive: A Growing Strategic Priority

UMC is a significant supplier to the automotive industry. The company's automotive electronics business has grown by more than 30% a year in recent years, and all 12 of UMC's fabs in production are certified with IATF 16949 automotive quality standard.

The automotive semiconductor market represents exactly the kind of opportunity UMC's strategy was designed to capture. The global automotive semiconductor market size was valued at USD 50.43 billion in 2024 and is expected to grow to reach USD 86.81 billion by 2033, growing at a CAGR of 6.22%.

Automotive chips don't need leading-edge processes—in fact, automotive customers often prefer older, more proven nodes because of their reliability and long qualification cycles. Mature geometries at 28nm and above retained healthy utilization thanks to power-management ICs, microcontrollers, and RF front-ends whose specifications rely more on analog performance, radio characteristics, or embedded Flash, not transistor density.

The Display Driver IC Advantage

UMC's strategy was to avoid direct competition with TSMC by pulling resources out of advanced nodes and instead focusing on "making an impact in mature processes." For example, UMC became a dominant force in OLED display driver ICs thanks to its early lead in developing 28nm high-voltage processes.

Display driver ICs represent a sweet spot for UMC—high enough volume to generate meaningful revenue, technically demanding enough to create barriers to entry, but not requiring bleeding-edge process technology. The company's investment in specialty high-voltage processes for these applications has created durable competitive advantages.

Part VIII: The Intel Partnership—A New Chapter

January 25, 2024: An Unlikely Alliance

On January 25, 2024, Intel Corp. and United Microelectronics Corporation announced that they will collaborate on the development of a 12-nanometer semiconductor process platform to address high-growth markets such as mobile, communication infrastructure and networking.

The long-term agreement brings together Intel's at-scale U.S. manufacturing capacity and UMC's extensive foundry experience on mature nodes to enable an expanded process portfolio. It also offers global customers greater choice in their sourcing decisions with access to a more geographically diversified and resilient supply chain.

Jason Wang, UMC co-president, said, "Our collaboration with Intel on a U.S.-manufactured 12nm process with FinFET capabilities is a step forward in advancing our strategy of pursuing cost-efficient capacity expansion and technology node advancement in continuing our commitment to customers."

The Strategic Logic: Complementary Capabilities

TrendForce believes that this partnership, which leverages UMC's diversified technological services and Intel's existing factory facilities for joint operation, not only aids Intel in transitioning from an IDM to a foundry business model, it also allows UMC to agilely leverage FinFET capacity without the pressure of heavy capital investments. TrendForce forecasts that this collaboration slashes average investment by a staggering 80%, compared to the cost of new equipment.

The new process node will be developed and manufactured in Fabs 12, 22 and 32 at Intel's Ocotillo Technology Fabrication site in Arizona.

UMC, focused on 28nm and 22nm processes and known for its High Voltage technology, found itself at a crossroads due to the rapid development of mature processes in its China facilities. This partnership is UMC's bold response to the challenge, allowing it to step into the FinFET era without the burden of excessive investment costs.

Advancing Beyond 14nm Without the Capital Burden

For UMC, partnering with Intel enables it to mass-produce chips that are more advanced than its mainstream 22nm to 28nm products.

In 2017, when Jason Wang and S.C. Chien took over as co-presidents, UMC announced it would no longer invest in nodes more advanced than 12nm. Since then, its process roadmap has largely plateaued at 28nm.

This strategic pivot forms the foundation of UMC's re-entry into the performance process game. And it marks a sharp departure from the company's 2017 stance, when it exited advanced node development beyond 12nm. Now, in 2025, UMC is doubling down on this node, channeling most of its critical R&D into the Arizona-based project with Intel.

The production is expected to commence in 2027.

The Geopolitical Dimension

However, the U.S.-China tech war has dramatically upended UMC's game plan. As China prepares to flood the market with mature-node capacity, the once-safe 28nm-and-below segment is turning into a red ocean. In January 2024, UMC announced a surprise partnership with Intel to develop and manufacture a 12nm process platform—an area where Chinese foundries have struggled to gain traction.

The node falls under U.S. export controls, making it significantly harder for Chinese foundries like SMIC to obtain the necessary equipment and EDA tools. This allows 12nm to act as a defensive buffer as China scales its mature-node output.

Part IX: Current Financial Performance and Market Position

2024 Results: Steady Performance in a Challenging Market

For the full year of 2024, UMC achieved NT$232.3 billion in revenue, a 4.39% increase from the previous year, marking the second-highest annual revenue in company history.

Annual revenue growth was 4.4% year-over-year to NT$232.3 billion for 2024. Annual gross margin was 32.6% for 2024. Operating expenses were 10.9% of revenue. Annual net income was NT$47.2 billion. Cash on hand exceeded NT$100 billion at the end of 2024.

Taiwan's UMC, the world's fourth largest foundry vendor, reported mixed results in the fourth quarter of 2024. Fourth quarter consolidated revenue was US$1.84 billion, down 0.2% from the previous quarter but up 9.9% from the like period a year ago.

The company expects its 2025 capital spending budget to be US$1.8 billion. That compares to US$2.9 billion in 2024.

Market Position: Solid Fourth Place

According to TrendForce, TSMC held a dominant 67% market share in Q4 2024, maintaining its lead in the foundry market. UMC and GlobalFoundries ranked 4th and 5th, with 4.7% and 4.6% shares respectively, trailing behind Samsung (8.1%) and China's SMIC (5.5%).

The Oversupply Challenge

UMC is experiencing an oversupply situation in the foundry industry, which may affect pricing and market dynamics moving forward.

For some time, there has been oversupply, lackluster demand and price pressure in the mature-node foundry business. China's foundry vendors, which compete in this segment, have simply built up too much capacity in the market. This in turn has put price pressure on GF, Tower, TSMC and other multinational foundry vendors in the market.

Part X: GlobalFoundries Merger Speculation

March 2025: Rumors of Consolidation

While TSMC makes strides in cutting-edge nodes and aims for 2nm mass production by year-end, its Taiwanese foundry counterpart, UMC, is rumored to be exploring a potential merger with U.S.-based GlobalFoundries. However, the speculation has been denied by UMC, as it states that there is currently no merger in progress.

UMC had stated that there is currently no merger in progress, but according to Economic Daily News, insiders say GlobalFoundries has already sought approval from Taiwan's Ministry of Economic Affairs, hoping to get the green light.

There is a rationale for GlobalFoundries to buy its rival and for UMC to become a part of GF. The mature-node segment is increasingly threatened by low-cost Chinese fabs, and a combined GF-UMC entity could consolidate global capacity and better compete on cost, scale, and reliability. Also, UMC and GF have different but complementary customer sets, so a merger could enable cross-selling, better utilization of fabs, and more diversified revenue streams.

According to Commercial Times, UMC and GlobalFoundries bring unique strengths to the table, with little overlap in their product portfolio and customer bases. Notably, UMC focuses on 22/28nm, and it has been pushed toward more specialized, high-voltage CMOS processes. Meanwhile, GlobalFoundries centers on 12/14nm, catering to 5G and IoT markets with major U.S. clients like Qualcomm, Broadcom, and AMD.

If UMC were to merge, Intel would be a stronger match. As Intel brings deep technical expertise, UMC has practical foundry experience, making for a more competitive combination.

Part XI: Investment Framework—Bull Case, Bear Case, and Key Metrics

The Bull Case

1. Structural Demand for Mature Nodes The AI boom has captured investor attention with its insatiable demand for leading-edge chips. But every AI server also needs power management ICs, networking chips, and peripheral semiconductors manufactured on mature nodes. Electric vehicles require hundreds of chips per car—mostly on mature processes. IoT devices, industrial automation, and 5G infrastructure all create demand for the processes where UMC excels.

2. The China Hedge The 12nm node falls under U.S. export controls, making it significantly harder for Chinese foundries like SMIC to obtain the necessary equipment and EDA tools. As customers seek supply chain resilience away from China risk, UMC's global footprint—Taiwan, Japan, Singapore, and soon Arizona through the Intel partnership—provides geographic diversification that Chinese competitors cannot match.

3. Intel Partnership Upside The Intel collaboration represents optionality with limited downside. If successful, UMC gains access to advanced FinFET technology and U.S. manufacturing capacity without massive capital investment. TrendForce forecasts that this collaboration slashes average investment by 80%, compared to the cost of new equipment.

4. Shareholder Returns With a strong balance sheet (cash on hand exceeding NT$100 billion), reduced capital expenditure requirements (2025 capex budget of US$1.8 billion, down from US$2.9 billion in 2024), and steady cash generation, UMC has significant capacity for dividends and buybacks. UMC aims to maintain a better-than-average dividend yield and ensure stable and consistent cash dividends.

The Bear Case

1. Chinese Competition Intensifying China's foundry vendors have built up too much capacity in the mature-node market, putting price pressure on UMC and other multinational foundry vendors. State-subsidized Chinese fabs can operate at lower margins or even losses indefinitely, potentially commoditizing the mature-node market.

2. Technology Stagnation Risk By definition, a specialty foundry strategy means not developing leading-edge processes. If the boundary between "mature" and "advanced" shifts—if applications that currently use 28nm migrate to more advanced nodes—UMC could lose significant business.

3. Intel Partnership Execution Risk UMC's 14nm process, in development since 2017, is yet to hit mass production, and its 12nm process is still in the R&D phase, with mass production eyed for late 2026. This collaboration's mass production timeline is tentatively set for 2027, with the FinFET architecture's stability under careful watch.

4. Geopolitical Risk UMC operates fabs in Taiwan, China, Japan, and Singapore, with the Intel partnership adding U.S. exposure. Cross-strait tensions could disrupt Taiwan operations. U.S.-China tensions could complicate China operations. The company faces geopolitical risk from multiple directions.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Limited advantage. UMC lacks the scale to match TSMC's cost position at any given node.

Network Effects: Not applicable in manufacturing.

Counter-Positioning: Potentially relevant. UMC's specialty focus may be difficult for TSMC to match while pursuing leading-edge customers.

Switching Costs: Moderate. Customers face significant switching costs once a chip is qualified on a particular process, but these apply equally to all foundries.

Branding: Minimal in B2B semiconductor manufacturing.

Cornered Resource: UMC has accumulated deep expertise in specific specialty processes (RF-SOI, high-voltage CMOS, driver ICs) that represents a form of cornered resource.

Process Power: UMC's 40+ years of foundry experience represents embedded knowledge that is difficult to replicate quickly.

Porter's Five Forces

Threat of New Entrants: Low at leading edge (prohibitive capital requirements), but rising in mature nodes as Chinese players expand.

Bargaining Power of Suppliers: Moderate. Equipment suppliers like ASML have significant power, but UMC uses older tools with multiple sources.

Bargaining Power of Buyers: Moderate to high. Large customers can negotiate pricing, but qualification costs create switching friction.

Threat of Substitutes: Low in the near term. Advanced packaging and chiplets could reduce demand for leading-edge nodes but not for mature nodes.

Competitive Rivalry: Intense. TSMC, Samsung, GlobalFoundries, SMIC, and numerous Chinese players compete for mature-node business.

Key Metrics to Watch

1. 22/28nm Revenue Contribution and Utilization Currently 34% of revenue, this is UMC's core franchise. Declining contribution would signal erosion of competitive position; increasing contribution validates the specialty strategy.

2. Gross Margin Trend At 32.6% for 2024, gross margin reflects UMC's pricing power and cost efficiency. Sustained margin compression would indicate Chinese competition is commoditizing the market; margin stability or expansion would validate the specialty premium positioning.

3. Intel Partnership Milestones Watch for tape-out announcements, customer design wins, and production timeline updates. Slippage from the 2027 target date would be concerning; on-time execution would validate the partnership model.

Conclusion: The Art of Strategic Retreat

UMC's story is not a story of failure. It's a story of adaptation—of recognizing when the rules of competition have changed and having the courage to define a different game to play.

Taiwan's first semiconductor company lost the technology race to its younger sibling. That much is undeniable. But in losing that race, UMC learned something that may prove equally valuable: that sustainable competitive advantage in semiconductors doesn't require being on the bleeding edge. It requires finding a profitable position you can defend.

In 2017, UMC recognized its role could make a difference. Rather than fighting to be a technology leader in the advanced-node process segment, UMC can be more capable of being a leader in the more mature process segments.

Today, UMC faces a new challenge—the rise of Chinese foundries flooding the mature-node market with subsidized capacity. The Intel partnership represents one response: a way to advance technologically while sharing capital burden, while also gaining a U.S. manufacturing footprint that Chinese competitors cannot match.

For long-term fundamental investors, UMC represents an interesting proposition: a company with a clear strategic identity, modest valuation, strong cash generation, and optionality from both the Intel partnership and potential industry consolidation. The risks—Chinese competition, geopolitical uncertainty, execution challenges—are real but well-understood.

The semiconductor industry's history teaches that the winners are often those who correctly identify which game they're playing. TSMC won by playing the leading-edge foundry game better than anyone. UMC, after trying and failing to match TSMC's strategy, has found a different game to play. The next decade will reveal whether that game is one worth winning.

Co-president Wang commented, "Looking into 2025, the semiconductor market is poised for another year of growth, driven by strong demand for AI servers as well as increasing semiconductor content in smartphones, PCs, and other electronic devices. To capture opportunities in this fast-moving market, UMC continues to invest in technology innovation, developing industry-leading specialty solutions to ride the next wave of system upgrades and stay ahead of the competition."

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube