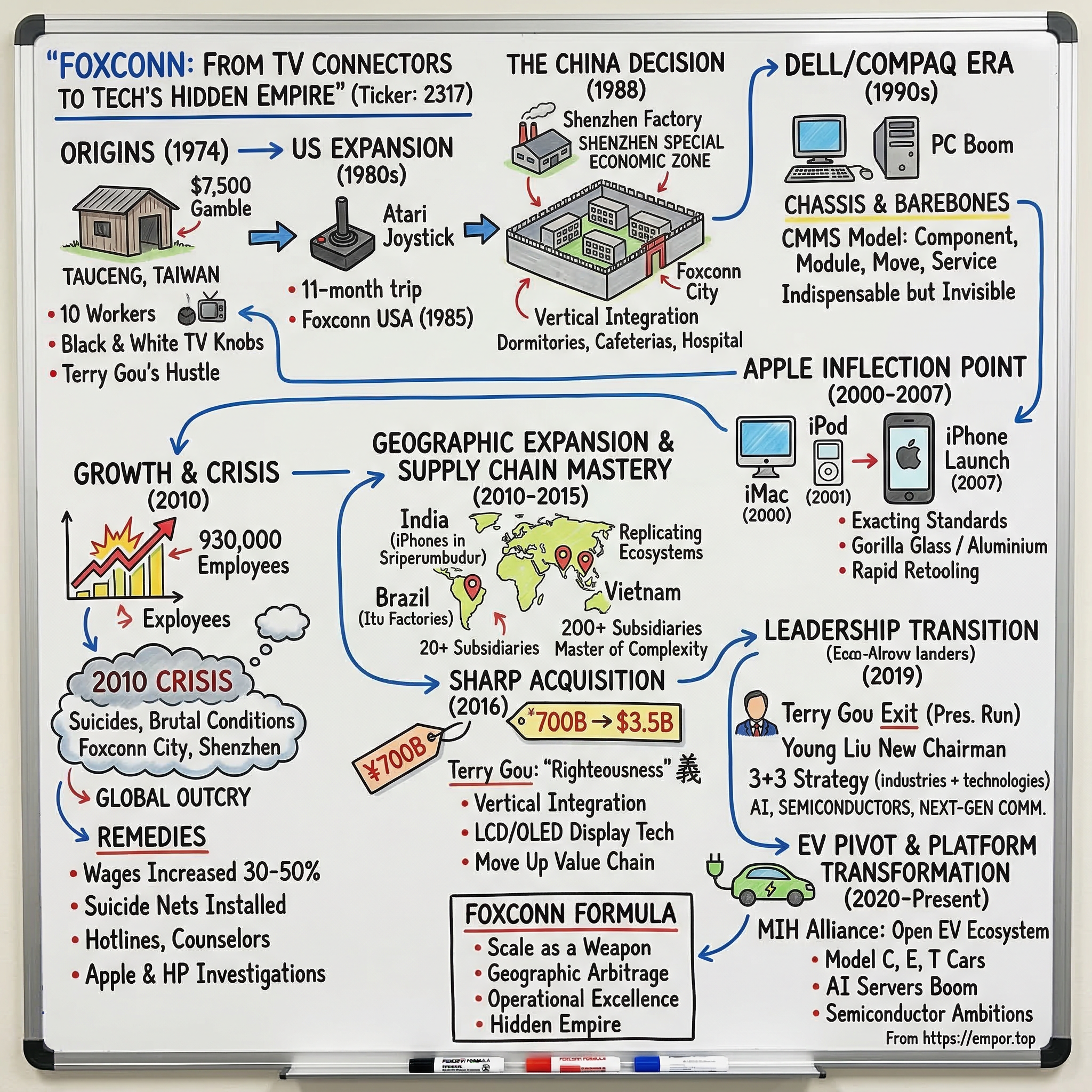

Hon Hai Precision Industry (Foxconn): From TV Connectors to Tech's Hidden Empire

I. Introduction & Episode Roadmap

Picture this: A company that generates more revenue than Nike, McDonald's, and Starbucks combined—yet most people couldn't tell you what they actually make. In 2024, Hon Hai Precision Industry, better known as Foxconn, reached NT$6.86 trillion in revenue (approximately USD$213 billion)—larger than the GDP of nations like Portugal or New Zealand. Walk into any Apple Store, pick up an iPhone, and you're holding a piece of Foxconn's invisible empire. But here's the kicker: despite assembling nearly half the world's consumer electronics, the average person has never heard their name.

The provocative question isn't just how a plastic TV parts maker became indispensable to Apple—it's how they became the world's largest contract manufacturer of electronics while remaining virtually invisible to consumers. At this time, Foxconn made up approximately 40% of worldwide consumer electronics production, yet their brand appears on nothing you own. They employ over a million people globally, operate facilities in 24 countries, and their decisions ripple through the entire tech ecosystem—from the chips in your car to the servers powering ChatGPT.

Today, we're pulling back the curtain on tech's most important company you've never thought about. We'll explore how Terry Gou turned $7,500 and a rented shed into a manufacturing colossus, why Steve Jobs bet Apple's future on a Taiwanese contract manufacturer, and how a wave of tragedies in 2010 nearly brought down the entire operation. This is the story of scaling manufacturing as an art form, the China paradox that made it all possible, and the power of being the invisible hand behind every screen you touch.

II. Origins: Terry Gou's $7,500 Gamble

Terry Gou founded Foxconn, established as Hon Hai Precision Industry in Taiwan in 1974 with $7,500 in startup money and a workforce of ten elderly employees, making plastic parts for television sets in a rented shed in Tucheng, a suburb of Taipei. The year was significant—Taiwan was transforming from an agricultural economy into an electronics manufacturing hub, riding the wave of Japanese companies outsourcing production. But Gou wasn't thinking about global supply chains yet. He was thinking about survival.

Imagine the scene: a cramped workshop in industrial Taipei, the acrid smell of molten plastic, ten workers—all older, experienced hands that younger companies wouldn't hire—manually pressing out TV channel selector knobs. The company manufactured a specific channel-changing knob for black and white television sets, the kind that made that satisfying "click" when you turned them. These weren't sexy products. They weren't innovative. But they were precise, they were reliable, and they were cheap. Gou's philosophy from day one: "Quality first, then speed, then price." In that order.

The Taiwan of 1974 offered unique advantages. The government was pumping money into electronics infrastructure, creating export processing zones with tax breaks. Labor was skilled but inexpensive. Most importantly, Taiwanese entrepreneurs had something mainland China wouldn't have for another decade: unfettered access to Western markets and technology. While Mao's Cultural Revolution raged across the strait, Gou was building relationships with Japanese TV manufacturers, learning their obsessive attention to detail, their manufacturing philosophy of kaizen—continuous improvement.

Then came the moment that changed everything. A turning point came in 1980 when he received an order from Atari to make the console joystick. This wasn't just another plastic part—this was Silicon Valley calling. The Atari 2600 was exploding in popularity, and they needed someone who could make joysticks at scale, with consistency, fast. Gou didn't just deliver; he over-delivered. He flew to California, studied Atari's operations, understood their supply chain needs better than they did themselves. Gou expanded his business in the 1980s by embarking on an 11-month trip across the US in search of customers. An aggressive salesman, Gou arrived uninvited at many companies' headquarters; often, he won orders despite security being called on him.

This 11-month American odyssey became legend within Foxconn. Gou would show up at company lobbies with product samples, no appointment, just pure hustle. Security would escort him out; he'd come back the next day. He slept in his rental car to save money, survived on convenience store food, and slowly, order by order, built a network of American clients who needed someone in Asia who understood both Eastern manufacturing efficiency and Western quality standards.

In 1985, Hon Hai established its U.S. subsidiary, named Foxconn, a strategic move influenced by rising labor costs in Taiwan. This expansion was crucial for securing contracts with major American companies. The name "Foxconn" itself was strategic—it sounded Western, technological, trustworthy. It was easier for American purchasing managers to sell internally than "Hon Hai Precision Industry."

By the mid-1980s, Gou had built something remarkable: a company that could pivot from making TV knobs to computer connectors to whatever the next wave of electronics required. When the company went public in 1991, its revenue was less than NT$10 billion. But Gou was just getting started. He had learned the American market, mastered Japanese quality standards, and built a Taiwanese operation that could compete globally. The foundation was set. Now he needed scale. And for that, he would need China.

III. The China Decision: Shenzhen 1988

In 1988, Gou opened his first factory in Shenzhen where his largest factory remains. To understand the audacity of this move, you need to understand the China of 1988. Tiananmen Square was one year away. Foreign investment was a trickle, not a flood. Shenzhen had only been designated a "Special Economic Zone" eight years earlier, and it was still more experiment than sure thing. Most Taiwanese businesses saw mainland China as too risky—politically unstable, infrastructurally underdeveloped, legally opaque.

But Gou saw what others didn't: unlimited labor, hungry workers, and a government desperate to industrialize. The Shenzhen factory started small—a few production lines, basic assembly work. But Gou wasn't just building a factory; he was building an ecosystem. Gou scaled up production by integrating vertically the assembly process and facilities for workers. The manufacturing site became a campus that included housing, dining, medical care and burial for the workers, and even chicken farming to supply the cafeteria.

This vertical integration of life itself was revolutionary and controversial. Workers didn't just clock in for shifts; they lived in Foxconn dormitories, ate in Foxconn cafeterias, were treated in Foxconn hospitals. It was paternalistic, totalizing, and incredibly efficient. A worker could go months without leaving the compound. Some called it a company town; critics would later call it something darker.

The economics were undeniable. This initial investment ultimately led the company to grow exponentially, and by 2005 about 90 percent of the company's net profits came from its operations in mainland China. Labor costs were a fraction of Taiwan's. The Chinese government offered land at below-market rates, tax holidays, and most importantly, flexibility on labor laws that would have been impossible in Taiwan or the West. Gou could scale up by thousands of workers for a major order, then scale down just as quickly.

But it wasn't just about cheap labor. Gou understood something fundamental: China wasn't just offering workers; it was offering an entire supply chain ecosystem. Need a specific type of screw? There's a factory two miles away. Need custom packaging? Three miles. Need to ramp up production by 100,000 units next week? The workers are ready. This clustering effect—what economists call agglomeration—meant that Foxconn could respond to customer demands with a speed and flexibility that was impossible anywhere else.

The Shenzhen factory grew from hundreds of workers to thousands, then tens of thousands. The largest Foxconn factory is located in Longhua Subdistrict, Shenzhen, where hundreds of thousands of workers are employed at the Longhua Science & Technology Park, a walled campus sometimes referred to as "Foxconn City". Covering about 3 km2 (1.2 sq mi), the park includes 15 factories, worker dormitories, four swimming pools, fire brigade, own television network (Foxconn TV), city centre with grocery store, bank, restaurants, book store, hospital.

By the mid-1990s, Foxconn had become the bridge between American design and Chinese manufacturing. But the company was still primarily making components—connectors, cables, the unsexy internals of electronics. The real transformation would come when Gou decided to move up the value chain, from making parts to assembling entire products. And that's when Michael Dell came calling.

IV. The Dell/Compaq Era: Learning to Scale (1990s)

The 1990s PC boom was Foxconn's university, and Dell was its most demanding professor. In 1996, Hon Hai started building chassis for Compaq desktops. This was a breakthrough moment that led to building the bare bones chassis for other high-profile customers, including HP, IBM, and Apple. But it wasn't just about landing big names—it was about learning how to think like them.

Dell's revolutionary model was built on just-in-time manufacturing and direct sales. They needed a partner who could deliver a customized computer within days of a customer clicking "buy." This meant Foxconn couldn't just be a manufacturer; they had to become an extension of Dell's entire operation. Gou pioneered what he called the "CMMS" model—Component, Module, Move, and Service. It sounds like corporate jargon, but it represented a fundamental shift: Foxconn would handle not just assembly, but component sourcing, modular design, logistics, and after-sales service.

The art of being indispensable but invisible was perfected during these years. When a Dell computer had problems, customers called Dell, not Foxconn. When Dell announced a new product line, the press praised Dell's innovation, not Foxconn's manufacturing prowess. This anonymity was by design. Gou understood that brands wanted to own the customer relationship entirely. Foxconn's value proposition was simple: "We'll make you look good, and we'll never take credit."

One of the important milestones for Foxconn occurred in 2001 when Intel selected Foxconn to manufacture its Intel-branded motherboards instead of Asus. This was huge. Intel, the most powerful company in tech hardware, was essentially saying Foxconn could be trusted with their brand, their quality standards, their reputation. It was validation that Foxconn had graduated from contract manufacturer to strategic partner.

The numbers tell the story of this period's explosive growth. When Hon Hai went public in 1991, revenue was less than NT$10 billion. By 2000, it had grown to NT$145 billion—a 14-fold increase in less than a decade. The company was adding factory space at a rate of one football field per day. They were hiring 1,000 workers per week during peak seasons. The scale was becoming incomprehensible.

But all of this was just preparation. The PC industry had taught Foxconn how to scale, how to manage complexity, how to deliver quality at quantity. They had built the infrastructure, the processes, the relationships. They were ready for something bigger. And in Cupertino, California, a recently returned CEO named Steve Jobs was about to bet his company's future on a colorful computer that looked like nothing the industry had ever seen.

V. The Apple Inflection Point: 2000-2007

More than just a subcontracted manufacturer, Foxconn originally landed an order to produce Apple's iMacs in 2000 which presented the opportunity to enhance its technological prowess. But to understand why this mattered, you need to understand where Apple was in 2000. They were bleeding money, their market share was in single digits, and Michael Dell had publicly suggested they should shut down and return money to shareholders. Steve Jobs, back for three years, was betting everything on design-forward products that would command premium prices. The candy-colored iMac G3 had proven the concept. Now he needed someone who could manufacture it at scale without compromising quality.

Jobs was notorious for his exacting standards. He would reject entire production runs because a screw was a millimeter off. He obsessed over the internal components that users would never see, demanding they be as beautiful as the exterior. Most manufacturers ran from this level of scrutiny. Gou ran toward it. He saw in Jobs not a difficult customer but a kindred spirit—someone who understood that the difference between good and great was in the details nobody else noticed.

The relationship started with the iMac but deepened with the iPod in 2001. The iPod required precision that pushed Foxconn's capabilities—the iconic scroll wheel, the mirror-finish back that showed every fingerprint (Jobs insisted on it anyway), the seamless integration of hardware and software. Foxconn didn't just manufacture the iPod; they helped engineer it. Their engineers would work side-by-side with Apple's, sometimes for 20-hour days, iterating on prototypes until Jobs was satisfied.

But the real test came with the iPhone. The launch of the era-defining first iPhone in 2007. Its subsequent manufacture seamlessly combined aluminium parts with frictional heat, using a pioneering technique known as anodisation. The iPhone wasn't just a phone—it was a computer, camera, iPod, and internet device in a package smaller than existing smartphones. The manufacturing challenges were unprecedented. Glass that wouldn't scratch (Gorilla Glass didn't exist yet; it was developed for the iPhone), aluminum that felt premium but wouldn't interfere with the antenna, tolerances measured in fractions of millimeters.

Six months before launch, Jobs decided he wanted a glass screen instead of plastic. Any other manufacturer would have said it was impossible. Gou mobilized thousands of workers, retooled entire production lines, and delivered. When Jobs wanted design changes weeks before launch, Foxconn engineers would work through the night implementing them. The Shenzhen factory would prototype during the day, fly the samples to Cupertino that evening, get Jobs' feedback, and implement changes before the next morning's production run.

By November 2007, Foxconn further expanded with an announced plan to build a new US$500 million plant in Huizhou, Southern China. This wasn't just expansion; it was preparation. Gou knew the iPhone would change everything. He could see the future—a world where everyone carried a supercomputer in their pocket, where devices would be refreshed annually, where hundred-million-unit production runs would become routine.

The Apple-Foxconn partnership redefined both companies. For Apple, it meant they could focus on design and software while trusting manufacturing to a partner who could match their perfectionism. For Foxconn, it meant steady, massive orders that justified enormous capital investments. By 2007, Apple products were generating an estimated 20% of Foxconn's revenue. Within five years, it would be over 40%. The partnership was so successful it became a dependency. And dependencies, as both companies would soon learn, have a way of becoming vulnerabilities.

VI. iPhone Manufacturing & The 2010 Crisis

The iPhone was supposed to be Foxconn's crowning achievement. By 2010, the Shenzhen factory was producing iPhones at a rate that seemed impossible—one every second, 24 hours a day, seven days a week. The iPad had just launched, adding another product to the mix. In 2010, the company's employee count was a reported 930,000 people, making Foxconn one of the world's largest private employers. But beneath this triumph, something was breaking.

The Foxconn suicides were a spate of suicides linked to low pay and brutal working conditions at the Foxconn City industrial park in Shenzhen, China, that occurred alongside several additional suicides at various other Foxconn-owned locations and facilities in mainland China. The numbers were stark and horrifying: In 2010 alone, 14 young workers had committed suicide by jumping to their deaths from Foxconn buildings. All of the workers were in their late teens or early twenties. Each had their own story, their own breaking point, but patterns emerged: extreme work hours, military-style discipline, isolation from family, and wages that, while better than rural farming, couldn't keep pace with rising costs or aspirations.

The first suicide in January 2010 barely made news. By May, when the ninth worker jumped, it had become a global crisis. The series of suicides drew media attention, and employment practices at Foxconn—one of the world's largest contract electronics manufacturers—were investigated by several of its customers, including Apple and Hewlett-Packard (HP). The world suddenly wanted to know: what was happening inside the factories that made their beloved gadgets?

The 2010 suicides prompted 20 Chinese universities to compile an 83-page report on Foxconn, which they described as a "labor camp". Interviews of 1,800 Foxconn workers at 12 factories found evidence of illegal overtime and failure to report accidents. The report also criticized Foxconn's management style, which it called inhumane and abusive. Additionally, long working hours, discrimination towards Mainland Chinese workers by their Taiwanese coworkers, and a lack of working relationships were all presented as potential problems.

The stories that emerged painted a picture of alienation on an industrial scale. Workers spoke of 12-hour shifts that stretched to 14 or 16 hours during product launches. They described standing for entire shifts, forbidden to sit even when production lines stopped. Some hadn't seen their families in years. The dormitories, meant to house workers efficiently, had become isolation chambers—eight to twelve people per room, often working different shifts, never forming connections.

Steve Jobs defended Apple's relationship with the company in June 2010, citing that its Chinese partner is "pretty nice" and is "not a sweatshop". Apple issued a public statement about the suicides, and company spokesperson Steven Dowling said "[Apple is] saddened and upset by the recent suicides at Foxconn. A team from Apple is independently evaluating the steps they are taking to address these tragic events, and we will continue our ongoing inspections of the facilities where our products are made".

Foxconn's initial response made things worse. In May 2010, the Foxconn human resources director attempted to make workers sign a no-suicide pledge containing a disclaimer clause: Should any injury or death arise for which Foxconn cannot be held accountable (including suicides and self-mutilation), I hereby agree to hand over the case to the company's legal and regulatory procedures. I myself and my family members will not seek extra compensation above that required by the law so that the company's reputation would not be ruined and its operation remains stable. The no-suicide 'consent letter' sought not only to limit Foxconn's liability but to ensure that the responsibility for future suicides was placed on the individual worker. Following intense criticism by workers and from wider society, Foxconn dropped this administrative requirement.

Then came the nets. In response to the suicides, Foxconn substantially increased wages for its Shenzhen factory workforce, installed suicide-prevention netting, brought in Buddhist monks to conduct prayer sessions and asked employees to sign no-suicide pledges. As an emergency measure, Foxconn placed safety nets around the roofs, on both sides of corridors, and all the windows were covered with wire and locked tight. The visual was dystopian—one of the world's most valuable companies literally catching falling workers in nets rather than addressing root causes.

But changes did come, gradually. Wages increased by 30%, then 50%. Working hours were capped (though often still exceeded). Foxconn hired counselors, set up hotlines, tried to create recreational facilities. Some changes were cosmetic, others substantial. The fundamental tension remained: how do you humanely manage a million workers producing devices that demand perfection, on deadlines that never slip, at prices that keep falling?

The Economist asserts that although the number of workplace suicides at Foxconn was large in absolute terms, number of people who died by suicide at Foxconn factories was lower than the overall suicide rate of China. Steve Jobs has asserted that it is lower than the rate of suicide for the US. This became Foxconn's defense—statistically, their workers were less likely to commit suicide than the general population. True perhaps, but it missed the point. These weren't statistics; they were young people who had come to the city with dreams and found themselves trapped in a machine that ground those dreams to dust.

The 2010 crisis fundamentally changed the Apple-Foxconn relationship. It was no longer invisible. Every iPhone launch would now carry the shadow of those suicides. Apple increased audits, published supplier responsibility reports, and pushed for improvements. Foxconn accelerated automation plans, partly to improve conditions, partly to reduce their reliance on human workers altogether. The crisis had passed, but its lessons lingered: the true cost of our devices isn't just paid at the checkout counter.

VII. Geographic Expansion & Supply Chain Mastery (2010-2015)

The 2010 crisis taught Foxconn a crucial lesson: concentration was vulnerability. Having so much production in China, especially in Shenzhen, created multiple risks—labor unrest, regulatory changes, rising costs, and increasingly, geopolitical tension. The solution was elegant in its simplicity: replicate the Foxconn model everywhere.

In 2015, Foxconn announced that it would be setting up twelve factories in India and would create around one million jobs, and in 2017, Foxconn started the production of iPhones in Sriperumbudur, near Chennai. India wasn't just another low-cost location; it was a strategic bet on the next China. A billion-person market, a young workforce, a government eager for manufacturing jobs, and crucially, a democracy that Western companies felt more comfortable with as US-China tensions rose.

In September 2012, Foxconn announced plans to invest US$494 million in the construction of five new factories in Itu, Brazil, creating 10,000 jobs. Brazil offered access to Latin American markets and local production that avoided import tariffs. Vietnam became another hub, with factories producing everything from smartphones to tablets, offering costs even lower than China and a government eager to follow China's manufacturing-led development model.

The geographic expansion revealed Foxconn's true genius: they weren't just replicating factories; they were replicating entire ecosystems. Each major facility came with dormitories, suppliers, logistics networks—a mini Foxconn City that could be dropped anywhere. They had turned their manufacturing model into a template, scalable and adaptable to local conditions while maintaining global standards.

Managing this complexity required innovation beyond manufacturing. Foxconn developed proprietary systems to coordinate production across continents. A component made in China could be seamlessly integrated with one from India, assembled in Vietnam, and shipped from Brazil. They built redundancy into every level—if one factory had problems, others could compensate within hours.

The supply chain web they wove was intricate beyond comprehension. Foxconn has more than 200 subsidiaries and branch offices across over 20 countries. A single iPhone might contain components from 43 countries, assembled in China, with final quality control in California. Foxconn managed this with military precision, tracking millions of components in real-time, coordinating shipments across oceans, ensuring that production never stopped.

By 2015, Foxconn had achieved something remarkable: they had become too big to fail, too integrated to replace. Apple might want to diversify suppliers, but who else could produce 200 million iPhones a year? Who else had the infrastructure, the expertise, the sheer scale? Other companies tried—Pegatron, Wistron—but they were essentially Foxconn's students, often run by former Foxconn executives, using Foxconn's playbook.

The million-employee milestone was both achievement and burden. In China alone, Foxconn employed more people than lived in San Francisco. Globally, their workforce exceeded the population of several European countries. Each employee was a potential point of failure, a potential scandal, a human being with needs and dreams that had to be balanced against production targets and profit margins. The human resources challenges alone were staggering—recruiting, training, housing, feeding, managing a constantly churning workforce where turnover could exceed 10% monthly.

Yet they managed it, day after day, year after year, iPhone after iPhone. The scale had become self-reinforcing. They were so big that suppliers came to them. So essential that governments bent regulations for them. So profitable that they could invest billions in automation and new technologies. But Terry Gou, now in his 60s, knew that maintaining this empire required more than operational excellence. It required strategic vision. And in 2016, he would make his biggest bet yet.

VIII. The Sharp Acquisition: Moving Up the Value Chain (2016)

On 25 February 2016, Sharp accepted a ¥700 billion (US$6.24 billion) takeover bid from Foxconn to acquire over 66 percent of Sharp's voting stock. The news sent shockwaves through both the tech and business worlds. This wasn't just another acquisition—it was the first foreign takeover of a major Japanese electronics manufacturer, a company that had been making electronics since 1912, when Taiwan was still a Japanese colony.

To understand the audacity of this move, you need to understand Sharp. This was the company that invented the mechanical pencil, created the first commercial LCD calculator, pioneered LCD television technology. In Japan's corporate hierarchy, Sharp was royalty—a century-old company with deep government connections and cutting-edge display technology. They were also bleeding money, losing market share to Korean competitors, and desperately in need of capital.

The negotiation was drama worthy of a business thriller. As Sharp had undisclosed liabilities which was later informed by Sharp's legal representative to Foxconn, the deal was halted by Foxconn's board of directors. Foxconn asked to call off the deal, but it was proceeded by the former Sharp president. Terry Gou, in the meeting, then wrote the word "義", which means "righteousness", on the whiteboard, saying that Foxconn should honor the deal.

This moment—Gou writing "righteousness" on a whiteboard—became legend within Foxconn. It was classic Gou: theatrical, principled, and strategically brilliant. He knew walking away would damage relationships not just with Sharp but with all of corporate Japan. He also knew that by honoring a deal despite new revelations, he was buying something more valuable than assets: reputation.

A month later, on 30 March 2016, the deal was announced as finalized in a joint press statement, but at a lower price. Foxconn, formally known as Hon Hai Precision Industry Co, will pay about $3.5 billion for a two-thirds stake. The price cut was significant—from $6.2 billion to $3.5 billion—but Gou had gotten what he wanted: Sharp's display technology, their patents, and most importantly, vertical integration.

Why did display technology matter so much? Screens were typically 20-30% of a smartphone's cost, one of the most expensive components. By owning Sharp, Foxconn could capture those margins. More strategically, they would no longer depend on competitors like Samsung and LG for displays—companies that also competed with Foxconn's biggest customer, Apple. The vertical integration meant Foxconn could offer Apple a more complete solution: design to display to assembly, all under one corporate umbrella.

On 28 April 2017, Sharp turned its first operating profit in three years, citing the restructuring efforts by Foxconn. Gou had done what Japanese management couldn't: cut costs ruthlessly, streamlined operations, and leveraged Foxconn's scale to reduce component costs. But he was careful to maintain Sharp's R&D capabilities, particularly in next-generation display technologies like OLED.

The Sharp acquisition was transformative in ways beyond the obvious. It gave Foxconn credibility as more than just an assembler—they were now a technology company that owned crucial intellectual property. It opened doors in Japan, a notoriously insular market. Most importantly, it signaled Gou's vision for Foxconn's future: moving from the middle of the value chain to owning key technologies at both ends.

Foxconn had agreed to invest in multiple areas of Sharp's business, including its OLED screen segment. Sharp said its plans to increase its production of OLED screens, which are increasingly replacing LEDs thanks to better performance, to 90 million 5.5-inch screens per year by 2019. That output volume is estimated to worth around 260 billion yen, or $2.3 billion. This wasn't just about current products—it was about positioning for the future when every surface would potentially become a screen.

The acquisition also revealed something else: at 66 years old, Terry Gou was thinking about legacy. He had built the world's largest electronics manufacturer, but what would happen when he was gone? The Sharp deal was partly about ensuring Foxconn's future relevance, giving it assets and capabilities that transcended any single leader or customer relationship. It was also, perhaps, about respect—proving that a Taiwanese company could successfully manage a Japanese icon, that the student had become the master.

IX. Leadership Transition & The Terry Gou Exit (2019)

Foxconn named Young Liu its new chairman after the retirement of founder Terry Gou, effective on 1 July 2019. Young Liu was the special assistant to former chairman Terry Gou and the head of business group S (semiconductor). The announcement, when it came, surprised no one and everyone simultaneously. Industry watchers had long speculated about succession, but Gou, even at 69, seemed immortal, irreplaceable—the kind of founder who would die at his desk.

But Gou had other plans. In 2019, Gou resigned from Foxconn and joined the Kuomintang (KMT) to run for president, declaring he was instructed by the sea goddess Mazu in a dream to contest the election. The sea goddess story was vintage Gou—mystical enough to resonate with traditional voters, memorable enough to dominate news cycles. Whether he truly believed Mazu had spoken to him or it was calculated political theater, only Gou knew. What was clear was that after 45 years, he was ready for a second act.

Young Liu represented a different kind of leadership for a different era. Young-way Liu was born in 1956. In 1978, he graduated from the National Chiao Tung University with a degree in electrophysics. He went on to complete a master's degree in computer engineering from the University of Southern California in 1986. He joined Foxconn in 2007. In 2019, he was appointed the Chief Executive Officer and Chairman. Where Gou was charismatic and impulsive, Liu was analytical and methodical. Where Gou built through sheer force of will, Liu built through systems and processes.

Mr. Liu, appointed to his current role in 2019, initiated the company's direction and strategies that are enabling it to chart its next phase of global growth. Known as the 3+3 strategy, Foxconn's primary growth drivers cover three major industries and three core technologies. The three industries were electric vehicles, digital health, and robotics. The three technologies were artificial intelligence, semiconductors, and next-generation communications. It was ambitious, almost hubristic—Foxconn trying to be not just a manufacturer but a technology innovator.

The transition revealed the challenge of replacing a founder-emperor. Gou had been Foxconn's face, its negotiator, its visionary. He had personal relationships with Steve Jobs, Michael Dell, the CEOs of every major tech company. He could make billion-dollar decisions over dinner, pivot entire strategies based on instinct. Liu had to lead differently—through committee, through consensus, through careful planning rather than bold gestures.

Since taking over as Foxconn chairman in 2019, Young Liu has steered the company through a series of global challenges, including the pandemic, supply chain disruptions, evolving US-China relations, and geopolitical shifts. As chairman, Liu has driven Foxconn's transformation into a benchmark for corporate governance. Initiatives such as the rotational CEO program, streamlined processes, and a focus on ESG have positioned the company as a leader in sustainability and progressive leadership within Taiwan's corporate ecosystem.

The rotational CEO program was particularly innovative—different executives would take turns leading operations, bringing fresh perspectives while Liu maintained strategic oversight. It was an acknowledgment that no single person could replace Gou, so they wouldn't try. Instead, they would distribute leadership, build institutional knowledge, create systems that transcended individuals.

Under Liu, Foxconn also became more transparent, more willing to engage with media and investors. Where Gou had cultivated mystery, Liu sought clarity. Earnings calls became more detailed. Strategy documents more explicit. The message was clear: Foxconn was evolving from a one-man empire to a modern corporation.

Gou ultimately lost the election, coming in second in the Kuomintang primary. He would try again in 2023, running as an independent before ultimately dropping out. But his political ambitions, successful or not, had achieved something important: they had forced Foxconn to prove it could survive without him. And under Young Liu's leadership, it was not just surviving but transforming, preparing for a world beyond smartphones, beyond Apple, beyond the business model that had made it great.

X. The EV Pivot & Platform Transformation (2020-Present)

The smartphone market was maturing. Growth was slowing. Everyone who could afford an iPhone had one, and upgrade cycles were lengthening. Young Liu knew Foxconn needed its next act, and he believed he'd found it in electric vehicles. In 2020, Foxconn initiated MIH Alliance to create an open EV ecosystem that promotes collaboration in the mobility industry, with more than 2,200 companies joining the open standard since its launch. The company announced plans to become more involved as a contract assembler of EVs. In HHTD21, Foxconn introduced for the first time three self-developed EV models: the Model C recreational vehicle, the Model E sedan, and the Model T electric bus.

The logic was seductive. Cars were becoming "iPhones on wheels"—packed with sensors, screens, semiconductors. If Foxconn could manufacture the world's most complex consumer electronics, why not cars? The MIH Alliance was their attempt to create an Android-like open platform for EVs, where Foxconn would provide the hardware platform and others could customize on top.

But cars weren't phones. The technical challenges were orders of magnitude greater—safety regulations, durability requirements, the sheer physics of moving two tons of metal at highway speeds. The supply chains were different, the customers different, the entire business model different. Where phone manufacturers refreshed models annually, car companies thought in terms of decade-long platforms.

Liu's strategy was clever: don't compete with Tesla or traditional automakers directly. Instead, become the Foxconn of EVs—the invisible manufacturer behind multiple brands. They partnered with Fisker, Stellantis, and others, offering to handle the complex, capital-intensive manufacturing while brands focused on design and marketing. Chairman Liu also shared news about the Group's cooperation with Mitsubishi Motors Corp. In the future, we expect to assist Mitsubishi in selling models we design and develop for Oceania, he said, adding that this hits one of our most important EV milestones: securing orders from traditional automakers.

The platform transformation went beyond EVs. Hon Hai Technology Group has actively invested in the three emerging industries of "electric vehicles, digital health, and robots" in recent years, as well as "artificial intelligence, semiconductor, and new generation communication technology". Combined with the Group's important long-term development strategy, it provides a complete solution for global benchmark customers, becoming a comprehensive smart life provider. This wasn't just diversification; it was recognition that the old model—being a contract manufacturer, even the world's best—had a ceiling.

The AI boom provided unexpected validation. Looking at the first quarter, Foxconn's AI server revenue is expected to grow more than 100% both quarter-on-quarter and year-to-year. As the GB200 enters mass production, we believe AI server revenue will improve quarter by quarter. Looking at the full year, AI server revenue will reach the trillion-dollar scale, in local currency terms, accounting for more than half of the Group's total server share. Suddenly, Foxconn's expertise in cooling, in power management, in handling complex assemblies at scale, was exactly what the AI industry needed.

The transformation revealed something profound about Foxconn's evolution. They were no longer just responding to customer needs; they were trying to anticipate and shape them. The MIH Alliance wasn't just about making EVs; it was about owning the standard, the platform, the ecosystem. They wanted to be not just the manufacturer but the enabler, the platform on which others built.

Yet challenges remained enormous. The EV market was brutal, littered with failed startups and struggling incumbents. The capital requirements dwarfed even Foxconn's resources. The technology was evolving so rapidly that billion-dollar investments could become obsolete overnight. And lurking behind everything was the question: could a company built on perfect execution learn to innovate?

Liu's answer was to hedge, to diversify, to build capabilities across multiple fronts. If EVs didn't work out, they'd have autonomous driving technology to license. If that failed, they'd have healthcare devices. The strategy was less focused than Gou's single-minded pursuit of manufacturing excellence, but perhaps more appropriate for an uncertain future. Foxconn was trying to transform from a company that made things to a company that made things possible.

XI. Playbook: The Foxconn Formula

Scale as a Weapon:

Foxconn's scale isn't just big—it's weaponized. When you're manufacturing 40% of the world's consumer electronics, you don't negotiate with suppliers; you dictate terms. Need a million screws by tomorrow? When Foxconn calls, entire factories pivot to serve them. This scale creates a gravitational pull that warps the entire industry around them. Smaller manufacturers can't match their component costs because Foxconn buys in quantities that trigger entirely different pricing tiers. It's not economies of scale; it's economies of dominance.

The mathematics of razor-thin margins at massive volume is counterintuitive but powerful. While competitors chase 15% margins on thousands of units, Foxconn accepts 3% margins on hundreds of millions. That 3% of a $200 billion revenue stream generates $6 billion in profit—more than most companies' entire revenue. The scale becomes self-reinforcing: the bigger you are, the lower your costs, the more orders you can win, the bigger you become.

The Invisible Giant Strategy:

Foxconn's invisibility is their greatest strategic asset. When an iPhone has problems, nobody blames Foxconn. When it succeeds, Apple gets the credit. This anonymity is worth billions. It means they can work with competing brands simultaneously—making iPhones and Samsung phones, PlayStation and Xbox. Their brand is their lack of brand.

Managing customer concentration risk when Apple represents 40-50% of revenue requires delicate balance. They're dependent enough that losing Apple would be catastrophic, but valuable enough that Apple can't easily replace them. It's mutually assured destruction as business strategy. Both companies are trapped in a profitable embrace, neither able to leave without massive pain.

The paradox of being essential but replaceable keeps everyone honest. Foxconn must constantly prove their value, can never rest on relationships, must always be cheaper, faster, better than alternatives. Apple must keep Foxconn profitable enough to invest in new capabilities but not so profitable they lose hunger. It's a tension that drives both companies forward.

Geographic Arbitrage Mastery:

Following labor costs globally seems simple—go where it's cheapest. But Foxconn understood it's not just about cost but about flexibility. China offers scale. India offers growth. Vietnam offers stability. Brazil offers market access. Each geography is a option in their portfolio, valuable not just for what it costs but for what it enables.

Building government relationships as a core competency sounds corrupt but isn't—it's about understanding that manufacturing at scale requires partnership with states. Foxconn doesn't just negotiate tax breaks; they offer governments employment, technology transfer, prestige. When Foxconn arrives, governors cut ribbons, presidents take credit. They're not just building factories; they're delivering political wins.

Creating industrial ecosystems, not just factories, is the masterpiece of their strategy. A Foxconn facility attracts suppliers, logistics companies, service providers. Within five years, a Foxconn factory becomes a Foxconn city, with its own economy, its own logic, its own gravitational pull. Competitors can build factories; only Foxconn builds ecosystems.

Vertical Integration vs. Flexibility:

The Sharp acquisition showed when to own the stack—when technology is crucial, differentiated, and expensive. Displays were all three. By owning Sharp, Foxconn captured margin, guaranteed supply, and gained technological capability that elevated their entire offering.

But they've also shown when to stay nimble. They don't make chips (yet), don't own logistics companies, don't backward integrate into raw materials. They understand that ownership brings rigidity. In fast-moving markets, the ability to switch suppliers, to pivot strategies, to abandon technologies is more valuable than integration.

The platform evolution—trying to become a solutions provider, not just a manufacturer—is the ultimate test of this balance. Can they maintain flexibility while building platforms? Can they be open while being integrated? Can they be both the platform and the player? The answer will determine whether Foxconn remains relevant for another generation or becomes another cautionary tale of a giant that couldn't adapt.

XII. Bear vs. Bull Analysis

Bear Case:

The Apple concentration risk isn't theoretical—it's existential. With Apple representing 40-50% of revenue, Foxconn is essentially a levered bet on one company's continued success. If Apple decides to diversify suppliers more aggressively, bring manufacturing in-house, or simply sees iPhone sales plateau, Foxconn's revenue could collapse overnight. Apple has already started diversifying to companies like Luxshare and Pegatron. Each percentage point of Apple business lost is hundreds of millions in revenue gone.

China dependency despite geographic expansion remains real. Yes, they have facilities in India, Vietnam, and elsewhere, but the heart of Foxconn—the engineering talent, the ecosystem, the institutional knowledge—remains in China. As US-China relations deteriorate, Foxconn finds itself caught between its biggest customer (American companies) and its biggest manufacturing base (China). They're trying to serve two masters who increasingly see each other as enemies.

Margin compression as electronics commoditize is relentless. Every year, the pressure grows to deliver more for less. Automation helps but requires massive capital investment. Moving to lower-cost countries helps but increases complexity. The fundamental problem remains: in commodity manufacturing, margins naturally trend toward zero.

EV transition uncertainty looms large. Cars aren't phones. The capital requirements are 10x higher. The development cycles are 5x longer. The regulatory complexity is 100x greater. And the competition includes century-old companies with deep expertise Foxconn lacks. Their EV strategy might be visionary or delusional—we won't know for years.

Labor and automation challenges create a no-win scenario. Human workers create PR nightmares and rising costs. Automation requires billions in investment and eliminates Foxconn's core advantage—managing human complexity at scale. They're caught between a past they're trying to escape and a future they might not be equipped for.

Bull Case:

Irreplaceable scale and expertise can't be replicated. Building another Foxconn would take decades and tens of billions of dollars. The institutional knowledge—how to ramp production from prototype to millions, how to manage supply chains across continents, how to deliver perfection at scale—is invaluable. Apple might want alternatives, but when they need 100 million iPhones for a launch, only Foxconn can deliver.

EV and new product categories represent massive TAM expansion. The global auto market is $2 trillion. If Foxconn captures even 5% of EV manufacturing, that's $100 billion in new revenue. Add in healthcare devices, robotics, smart city infrastructure—the addressable market is 10x their current position. They don't need to dominate; they just need to participate.

AI server boom beneficiary positioning is perfect. Foxconn, the world's largest electronics contract manufacturer, announced record-breaking revenue for 2024, reaching NT$6.86 trillion (US$216 billion). The AI infrastructure buildout requires exactly what Foxconn offers: complex assembly, thermal management, scale manufacturing. Every ChatGPT query, every AI image generated, runs on servers Foxconn likely assembled.

Geographic diversification finally happening reduces risk. India operations are scaling rapidly. Vietnam facilities are expanding. The concentration risk is real but diminishing. In five years, China might be less than 50% of production. That's still significant but not existential.

Platform transformation could unlock higher margins. If Foxconn succeeds in becoming a platform company—providing not just manufacturing but design, software, services—margins could double or triple. The MIH Alliance for EVs, if successful, could generate licensing revenue with software-like margins. They're trying to evolve from selling hours of labor to selling intellectual property.

XIII. The Future: What's Next for the Hidden Empire

The India opportunity isn't just big—it's transformative. Apple's push to manufacture in India isn't just about diversification; it's about accessing a billion-person market with local production. Apple supplier Foxconn is starting production of the iPhone 15 in India, the first time that a new iPhone has been made outside China prior to its announcement. The devices are to be manufactured at a Foxconn plant in Sriperumbudur, Tamil Nadu. This isn't just moving production; it's replicating the entire ecosystem that took 30 years to build in China, compressed into a decade.

In 2024, Hon Hai's annual revenue reached USD $213 billion, but the composition of that revenue is shifting dramatically. Servers for AI are growing at triple-digit rates. Traditional smartphone assembly is flat to declining. The company that built its fortune on consumer electronics is becoming an enterprise infrastructure giant, and the transition is happening faster than anyone expected.

Can EVs be the next iPhone moment? The jury's still out. The Model T electric bus is running in Taiwan. The partnerships with traditional automakers are promising. But the EV market is nothing like the smartphone market circa 2007—it's more competitive, more capital-intensive, more regulated. Foxconn might become the world's largest EV manufacturer, or they might lose billions chasing a dream. Most likely, something in between.

The semiconductor ambitions are serious but secondary. Foxconn is looking for a way out, and one of the key directions is to focus its strength on semiconductors. It has invested hundreds of millions of yuan in Zhuhai, Guangdong province and Jinan in Shandong province to build chip factories over the past year. They'll never compete with TSMC in cutting-edge chips, but they don't need to. Older-generation chips for cars, IoT devices, industrial applications—that's a growing market with better margins than assembly.

Will they ever become a consumer brand? Probably not, and that's fine. Foxconn's power comes from invisibility. The moment they compete with customers is the moment customers look for alternatives. They've learned from Samsung's model—being both supplier and competitor creates inevitable conflicts. Better to remain the arms dealer who sells to all sides.

The US-China tech war implications are enormous and unavoidable. Foxconn is caught in the middle—a Taiwanese company, manufacturing in China, serving American customers, navigating increasingly incompatible regulatory regimes. Every US sanction, every Chinese retaliation, every Taiwanese election creates new complexity. They're trying to be neutral in a world that increasingly demands you pick a side.

XIV. Epilogue: Lessons & Reflections

The power of being the "picks and shovels" in tech gold rushes is Foxconn's fundamental insight. During the California Gold Rush, the people who got rich weren't the miners but the ones selling them supplies. Foxconn sells the manufacturing capacity that every tech company needs but doesn't want to build. They profit from every trend—PCs, smartphones, tablets, wearables, EVs, AI—without betting on any single winner.

Why operational excellence beats innovation sometimes is heretical in Silicon Valley but obvious in Shenzhen. Foxconn has never invented a breakthrough product, but they've manufactured all of them. Innovation is risky, expensive, and often fails. Operational excellence is boring but profitable. In a world obsessed with disruption, Foxconn proves that perfect execution of established ideas can build an empire.

The Terry Gou legacy isn't just building a company but building an industry. Before Foxconn, electronics manufacturing was fragmented, inefficient, artisanal. Gou turned it into a science, scalable and reproducible. Every contract manufacturer now uses some version of Foxconn's playbook. He didn't just win the game; he changed the rules.

What Silicon Valley can learn from Taiwanese/Chinese manufacturing is humility. The Valley designs the future, but Asia builds it. The genius of the iPhone isn't just Jony Ive's design or Steve Jobs' vision—it's also Foxconn's ability to manufacture it at scale, with quality, on time. Innovation without execution is just an idea. Foxconn is where ideas become reality.

Final thought: In a world obsessed with software, Foxconn proves atoms still matter. Every app needs a device. Every cloud needs a server. Every Tesla needs a battery. The physical world hasn't been digitized away; it's been made more complex, more interconnected, more dependent on companies like Foxconn that can manage that complexity at scale. They remain invisible not because they're unimportant but because they're so fundamental we forget they exist—like the foundation of a building, unseen but holding everything up.

The next time you pick up your phone, remember: you're holding the product of a million-person orchestra, conducted from Taiwan, performed in China, composed in California. Foxconn is the stage, the instruments, and half the musicians. They are everywhere and nowhere, essential and invisible, the hidden empire that manufactures our modern world. And as long as we keep wanting better devices, faster servers, smarter cars, they'll keep building them—one component, one assembly line, one factory city at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube