Carborundum Universal: India's Century-Old Materials Science Pioneer

Introduction & Episode Setup

The grinding wheel spins at 12,000 RPM in a semiconductor fabrication plant in Taiwan, shaving nanometers off a silicon wafer that will eventually power an AI chip. Half a world away, in a Chennai boardroom overlooking the Bay of Bengal, executives at Carborundum Universal Limited are discussing their next acquisition target in Germany. These two scenes—one of cutting-edge technology, the other of old-world business strategy—are more connected than they appear.

Welcome to the unlikely story of how a 120-year-old South Indian conglomerate built a global materials science empire that touches everything from the smartphone in your pocket to the electric vehicle in your garage. Carborundum Universal Limited, or CUMI as insiders call it, represents one of India's most fascinating yet underappreciated industrial stories—a company that makes the tools that make the world. With a market capitalization hovering around ₹16,000-19,000 crore, CUMI operates from 25 locations across India, Russia, South Africa, Australia, China, Thailand and Canada, producing over 20,000 varieties of products that reach 43 countries. Yet for all its global reach, this remains a story deeply rooted in South Indian business culture, shaped by the unique ethos of the Murugappa Group and the patient, relationship-driven approach of Tamil Nadu's merchant families.

Why does a company making grinding wheels matter in 2024? Because every semiconductor chip requires precision grinding. Every electric vehicle battery needs specialized ceramics. Every wind turbine blade demands advanced composite materials. And behind all of these sits CUMI—the picks-and-shovels provider to the modern industrial economy.

This is the story of how a regional money-lending operation transformed into a global materials science powerhouse. It's about technology transfer during the License Raj, surviving liberalization, and then thriving through strategic acquisitions. It's about building trust across generations and geographies. And ultimately, it's about recognizing that in the race toward AI and electrification, someone still needs to make the tools that shape the future.

The Murugappa Legacy & Pre-Independence Origins

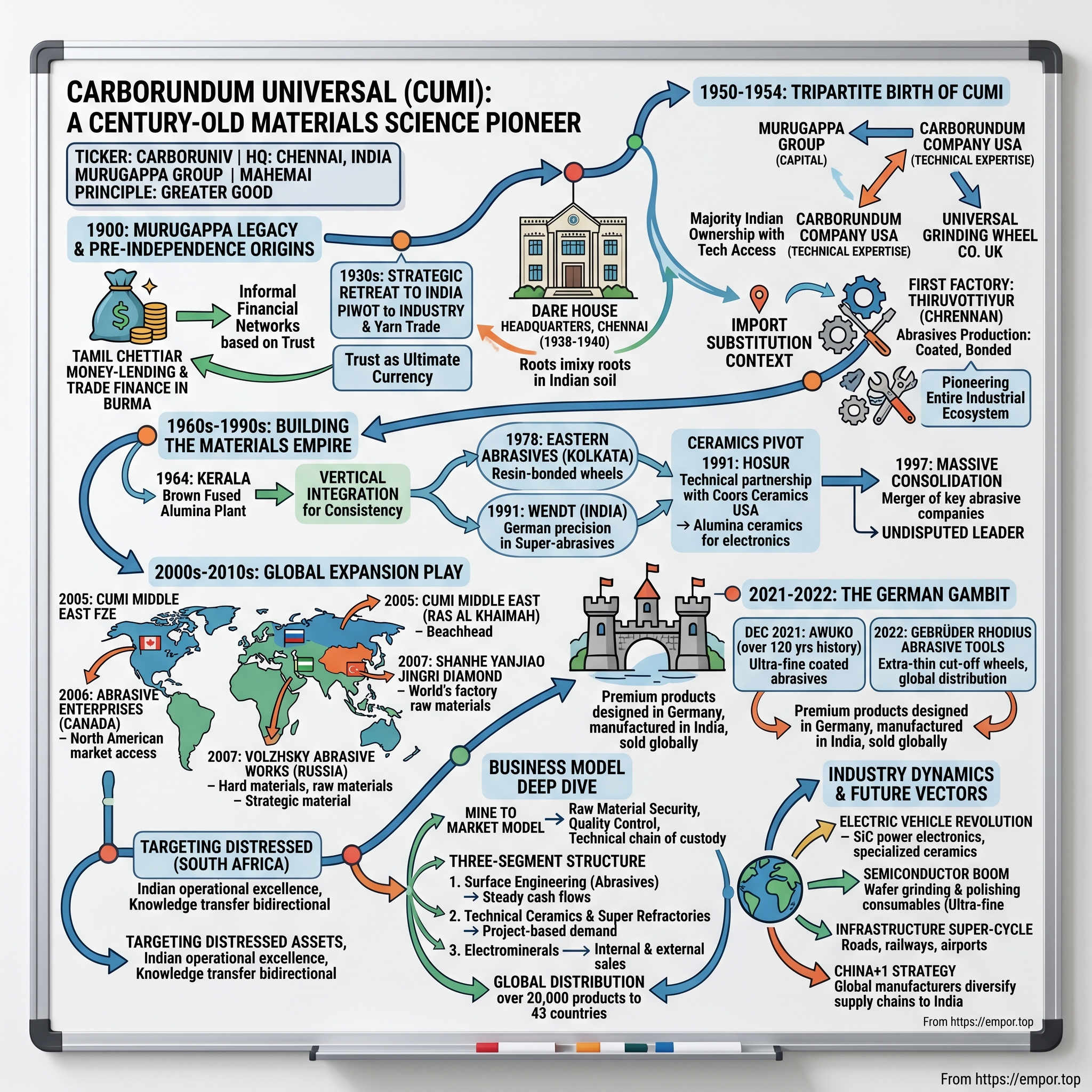

The year is 1900. In the bustling port city of Moulmein, Burma—now Myanmar—a young Tamil Chettiar named A.M. Murugappa is counting coins in his small office. The British Empire is at its zenith, and Southeast Asia is experiencing an unprecedented trade boom. Rice from Burma flows to India, textiles move the opposite direction, and financing it all are the Chettiars—Tamil Nadu's indigenous banking community who would become the venture capitalists of colonial Asia.

Dewan Bahadur A.M. Murugappa Chettiar didn't set out to build an industrial empire. He started with what his community knew best: money-lending and trade finance. But unlike many of his contemporaries who remained content with financial intermediation, Murugappa possessed an unusual vision—he saw that real wealth creation lay not in moving money, but in making things.

The Chettiar banking networks were remarkable for their time. Operating without formal banks, they created an informal financial system that stretched from Madras to Saigon, financing everything from small traders to large plantations. The business first established in Moulmein spread to British Malaya, Ceylon, Dutch East Indies and French Indo-China. They were essentially running a distributed ledger system a century before blockchain, built entirely on trust and community reputation. But the 1930s brought dramatic change. The business was moved back to India in the 1930s, a prescient decision that would prove crucial. The Japanese invasion of Burma during World War II would have wiped out the family's assets had they not executed this strategic retreat. The firm's diversification and entry into entirely new lines of business in Burma was markedly different from the others, facilitated partly because of the general standing and reputation of the firm and partly on account of the useful contacts the family had developed over time in the business and political circles of Burma.

The move to India wasn't just geographical—it represented a fundamental pivot in business philosophy. Around this time, in the 1930s, the AMM firm chose to move into the lucrative yarn trade in Coimbatore, with a clear and discernible shift from the traditional banking business to the more modern form of business, best reflected in their increasing use of the joint stock route of investment.

By the late 1930s, the group was constructing Dare House in Chennai—an art deco masterpiece that still serves as headquarters today, constructed between 1938 and 1940. This wasn't just a building; it was a statement of permanence, of roots being planted deep in Indian soil.

What set the Murugappa Group apart was their approach to business relationships. Before "ESG" became a boardroom buzzword, before "stakeholder capitalism" entered the lexicon, the Murugappas were practicing what they called "Mahemai"—a Tamil concept roughly translating to "the greater good." Every business decision was evaluated not just on profit potential but on its impact on employees, communities, and society at large.

In 2024, their net worth was estimated as ₹85,000 Crore (9.8 Billion USD), but the foundation for this wealth was laid not through financial engineering but through a simple principle: trust is the ultimate currency in business. The Chettiars understood that reputation, once lost, could never be fully recovered—a lesson that would guide every acquisition, every partnership, and every strategic decision for the next century.

The group's early industrial ventures were modest—emery paper here, steel furniture there. But each represented a crucial learning experience, building the operational DNA that would later enable them to manage complex manufacturing operations across continents. They were learning how to make things, not just finance them—a distinction that would prove critical when opportunity knocked in 1950.

The Tripartite Birth of CUMI (1950–1954)

Picture this scene: It's 1950, and in a wood-paneled conference room in Madras, three unlikely partners are hammering out the details of what would become one of India's most enduring industrial ventures. On one side sits the Murugappa Group, flush with capital but hungry for technical expertise. Across the table: representatives from Carborundum Company USA, the world's leading abrasives manufacturer, and Universal Grinding Wheel Company from the UK. The stakes? Nothing less than India's industrial future.

The timing was exquisite. Jawaharlal Nehru's government had just launched its ambitious industrialization program. The slogan "temples of modern India" referred to steel plants and dams, but someone needed to make the tools that would build these temples. Enter abrasives—the unsexy but utterly essential materials that grind, polish, and shape everything from turbine blades to surgical instruments.

Carborundum Universal Ltd, a part of the Chennai-based Murugappa group, is engaged in the manufacturing of abrasives, ceramics, refractories, and electro-minerals. But in 1950, this was just a dream sketched on paper. The technology transfer negotiations were Byzantine—the Americans wanted control, the British wanted influence, and the Indians wanted independence. The Murugappas, drawing on their decades of relationship-building, found the sweet spot: majority Indian ownership with guaranteed technology access.

The company was initially registered as Carborundum Universal of Madras, later renamed and incorporated in 1954 as Carborundum Universal Ltd (CUMI). The name itself was a compromise—"Carborundum" for the American technology, "Universal" for the British partner, and the Indian registration making clear where ultimate control lay.

The early manufacturing challenges were immense. Abrasives require precise chemistry—silicon carbide crystals must be grown at temperatures exceeding 2000°C, aluminum oxide grains need exact sizing, and bonding agents must withstand enormous mechanical stress. The first factory in Thiruvottiyur, Chennai, was essentially a laboratory at scale, with Indian engineers working alongside American and British technicians to adapt Western processes to Indian conditions.

They are known for pioneering coated and bonded abrasives in India and producing super refractories, electro minerals, industrial ceramics, and ceramic fibers. But "pioneering" understates the achievement. They were creating an entire industrial ecosystem from scratch—training workers who had never seen a grinding wheel, sourcing raw materials in a country with limited mining infrastructure, and selling to industries that were themselves just being born.

The import substitution context is crucial here. India in the 1950s was hemorrhaging foreign exchange, importing everything from steel to soap. Every grinding wheel made in Thiruvottiyur meant dollars saved. The government's support wasn't just political—it was existential. CUMI received preferential access to scarce raw materials, protection from imports, and most importantly, guaranteed orders from public sector enterprises.

But protection breeds complacency, and here the Murugappa DNA made the difference. While other import substitution beneficiaries grew fat and lazy behind tariff walls, CUMI obsessed over quality. They knew protection was temporary, that eventually they'd have to compete globally. Every defective grinding wheel was dissected, every customer complaint investigated. The Americans and British, initially skeptical of their Indian partners' capabilities, were soon sending their own people to Chennai to learn about low-cost manufacturing.

The strategic importance of abrasives cannot be overstated. You cannot have a manufacturing economy without them. Every automobile engine, every piece of precision machinery, every semiconductor requires grinding and polishing. By controlling abrasives, CUMI was positioning itself at a critical node in India's industrial value chain. They weren't just making products; they were enabling an entire economy.

Building the Materials Empire: Integration & Expansion (1960s–1990s)

The scorching heat of Kerala in 1964 made the furnaces at Kalamassery seem almost redundant. But for the engineers commissioning CUMI's Brown Fused Alumina plant, this was the beginning of something transformative. In 1964, CUMI Minerals commissioning its Brown Fused Alumina Plant at Kalamassery, Cochin marked the company's first major step toward vertical integration—a strategy that would define its next three decades.

Vertical integration in the abrasives industry isn't just about cost control; it's about consistency. A grinding wheel is only as good as its worst grain. By bringing electro-mineral production in-house, CUMI could control every variable from bauxite quality to fusion temperature. This obsessive attention to the entire value chain would become the company's signature move, repeated across geographies and product lines.

The 1970s brought political turbulence—the Emergency, nationalization threats, and socialist rhetoric that sent shivers through private enterprise. Yet CUMI thrived, partly through political astuteness (the Murugappas maintained cordial relations across the political spectrum) but mainly through operational excellence. When competitors struggled with power cuts, CUMI had backup generation. When raw material supplies dried up, CUMI had stockpiles.

CUMI stepped up its investment in abrasive industries by acquiring the Eastern Abrasives Ltd., Kolkata in 1978. This wasn't just buying capacity; it was acquiring market access in Eastern India, relationships with local industries, and most importantly, a trained workforce familiar with different manufacturing techniques. The Kolkata operation specialized in resin-bonded wheels, complementing Chennai's vitrified products.

The 1980s saw CUMI's product portfolio explode. They moved beyond traditional abrasives into super-refractories for steel plants, industrial ceramics for chemical processing, and specialized materials for emerging industries. Each product line required different expertise, different capital equipment, different customer relationships. Managing this complexity would have broken most companies, but CUMI had spent 30 years building systems and processes that could scale.

The real coup came in 1991. Wendt (India) Ltd, a joint ventured company of Wendt GmbH, Germany and The House of Khataus, was merged with the CUMI. Wendt brought German precision engineering in super-abrasives—diamond and CBN wheels used in aerospace and automotive applications. This wasn't incremental improvement; it was a quantum leap in technology.

The ceramics pivot deserves special attention. CUMI's first industrial ceramics division was established in Hosur, Tamil Nadu as a technical partnership with Coors Ceramics, USA in 1991. Why ceramics? Because CUMI's leadership saw what others missed: the convergence of materials science. The furnaces that made alumina for abrasives could, with modifications, make alumina ceramics for electronics. The quality systems for grinding wheels could ensure consistency in ceramic substrates. The customer selling abrasives to auto companies could also sell them ceramic components.

Throughout this period, CUMI was also building something intangible but invaluable: technical expertise. They weren't just licensing technology; they were absorbing it, improving it, and eventually innovating beyond it. Indian engineers who started by copying American designs were, by the 1990s, filing their own patents. The student was becoming the master.

The integration story culminated in 1997 when Cutfast Abrasive Tools Ltd., Eastern Abrasives Ltd., Cutfast Polymers Ltd. and Carborundum Universal Investment merged with Carborundum Universal Ltd. This massive consolidation created India's undisputed abrasives leader, with market shares exceeding 30% in most categories. But more than scale, it created operational synergies—shared R&D, combined purchasing power, and unified market presence.

The Global Expansion Play (2000s–2010s)

The liberalization of 1991 was supposed to destroy companies like CUMI. The narrative was simple: remove protection, and inefficient Indian manufacturers would be crushed by global competition. Instead, CUMI did something unexpected—it went shopping abroad.

The 2000s marked a fundamental shift in ambition. No longer content with being India's abrasives leader, CUMI wanted to be a global player. But how does a Chennai-based company compete with multinationals? The answer lay in careful targeting—acquiring distressed assets in developed markets and turning them around with Indian cost management and operational excellence.

In 2005 the company started CUMI Middle East FZE in Ras Al Khaimah, establishing a beachhead in the Gulf markets. The Middle East was experiencing a construction boom, and every building project needed abrasives. But CUMI wasn't just setting up a sales office; they were creating a distribution hub that could serve Africa and Central Asia.

The North American entry was surgical. CUMI bought Abrasive Enterprises Inc., Canada, for $2.24 Million by 2006. This wasn't about size—it was about market access. Canadian environmental and safety standards were among the world's strictest. Products certified there could be sold anywhere. Moreover, Abrasive Enterprises had relationships with North American industrial distributors that would have taken CUMI decades to build organically.

But the real transformation came in 2007. The company took over the Chinese firm, Sanhe Yanjiao Jingri Diamond Industrial Company Ltd., and the Russian Volzhsky Abrasive Works. These weren't random acquisitions—they were strategic chess moves. China was becoming the world's factory, and having local production gave CUMI access to the world's fastest-growing industrial market. Russia brought something different: Soviet-era technical expertise in super-hard materials and access to vast raw material reserves.

The Volzhsky acquisition in particular deserves examination. This was a 70-year-old plant that had supplied abrasives to the Soviet military-industrial complex. The technology was dated, the equipment needed upgrading, but the metallurgical knowledge was world-class. CUMI invested heavily in modernization while preserving the technical core. Within three years, Volzhsky was profitable and exporting to Western Europe.

In 2008, Foskor Zirconia Ltd., South Africa became a subsidiary of CUMI. Zirconia is a strategic material used in everything from fuel cells to dental implants. South Africa had the ore; CUMI had the processing expertise. The combination created one of the world's few integrated zirconia producers outside China.

Managing these acquisitions required a delicate balance. Push too hard on cost-cutting, and you lose technical talent. Move too slowly on integration, and you miss synergies. CUMI's approach was culturally sensitive but operationally firm. Local management was retained where possible, but Indian financial controllers and quality managers were embedded in every operation. Knowledge transfer was bidirectional—Russians taught Indians about cold-weather operations, Indians taught Russians about lean manufacturing.

The global distribution network that emerged was formidable. CUMI exports its products to 43 countries spread across the globe, but this understates the sophistication. They weren't just shipping products; they were providing technical support, customization, and just-in-time delivery to global customers. A German auto plant could order specialized grinding wheels from CUMI's German subsidiary, manufactured in Russia with Indian raw materials, and receive them within 48 hours.

The German Gambit: RHODIUS & AWUKO Acquisitions (2021–2022)

December 2021, midst of a global pandemic, and CUMI is finalizing its most audacious acquisition yet. AWUKO, with its over 120 years of history, was acquired by CUMI already in December 2021. This wasn't just buying a company; it was acquiring a piece of German industrial heritage. AWUKO had been making coated abrasives since 1899—before cars, before airplanes, before virtually every modern industry.

The AWUKO acquisition was strategic brilliance disguised as opportunity. European companies, battered by COVID and energy costs, were available at reasonable valuations. But CUMI wasn't bottom-fishing; they were seeking specific capabilities. AWUKO's expertise in ultra-fine coated abrasives—products used in aerospace and medical device manufacturing—was exactly what CUMI needed to move up the value chain.

Then came RHODIUS. The Burgbrohl-based family business Gebrüder RHODIUS GmbH & Co. KG has sold its abrasive tools division with more than 300 employees in Germany and abroad and annual sales of over EUR 60 million to CUMI. RHODIUS wasn't just another abrasives company; RHODIUS exports its grinding tools to more than 100 countries and sets industry standards as the manufacturer of extra-thin cut-off wheels.

Extra-thin cut-off wheels might sound mundane, but they represent the pinnacle of abrasives technology. Making a wheel thin enough to minimize material waste, strong enough to withstand rotational forces, and sharp enough to cut hardened steel requires metallurgy, chemistry, and physics expertise that few companies possess. RHODIUS had spent decades perfecting this.

The integration numbers tell the story: The segment's revenue increased by 63% from FY22 to FY24, fueled by high demand and the integration of newly acquired subsidiaries in Germany "RHODIUS Abrasive GmbH and CUMI AWUKO Abrasives GmbH" and India "PLUSS Advanced Technologies". This wasn't just adding revenues; it was creating a European platform for CUMI's global ambitions.

The cultural integration challenge was immense. German workers, proud of their engineering heritage, were now reporting to Indian management. CUMI's approach was masterful—they positioned themselves not as conquerors but as custodians of German engineering excellence. Investment in R&D increased, not decreased. The German brands were retained and strengthened. Local management was empowered, not replaced.

But beneath this cultural sensitivity was hard-nosed business logic. German manufacturing, with its high labor costs and strict regulations, couldn't compete on price. But combined with Indian low-cost manufacturing and Russian raw materials, it could compete on value. Premium products designed in Germany, manufactured in India, sold globally—this was the new CUMI playbook.

The technology acquisition aspect was crucial. Both AWUKO and RHODIUS brought proprietary manufacturing techniques—specific resin formulations, backing materials, grain orientation methods—that would have taken CUMI decades to develop independently. These weren't just trade secrets; they were accumulated knowledge encoded in everything from machine settings to worker training programs.

Business Model Deep Dive

Strip away the complexity, and CUMI's business model is elegantly simple: control the entire value chain from mines to end-user, and capture value at every step. But executing this model across three distinct segments requires operational sophistication that few companies possess.

The three-segment structure deserves examination. Surface Engineering (primarily abrasives) generates steady cash flows from industrial customers who need consumables. Technical Ceramics and Super Refractory Solutions serve project-based demand from infrastructure and heavy industry. Electrominerals feeds both internal consumption and external sales. This portfolio balance—recurring revenue, project revenue, and commodity exposure—provides resilience across economic cycles.

It is one of the largest producers of abrasives in the domestic market with over 30% market share. But market share in abrasives understates CUMI's position. In specialized segments like super-abrasives for semiconductor manufacturing or ceramic grains for medical devices, their share often exceeds 50%. This dominance in niches provides pricing power that commodity producers can only dream of.

The "mines to market" model isn't just vertical integration; it's about technical control. When you mine your own bauxite, you know its exact alumina content. When you fuse your own aluminum oxide, you control grain morphology. When you manufacture your own grinding wheels, you can guarantee performance. This technical chain of custody is CUMI's real moat.

The Company makes over 20,000 varieties of products manufactured at 25 locations across India, Russia, South Africa, Australia, China, Thailand and Canada. Managing this complexity requires sophisticated systems. CUMI's ERP implementation, completed over a decade, connects every plant, every warehouse, every sales office. A customer in Detroit can order a specialized product manufactured in Chennai, with Russian raw materials, and track it real-time.

R&D investment, at roughly 1.5% of revenues, might seem modest compared to pharmaceutical or technology companies. But in materials science, innovation is incremental and cumulative. CUMI's 200+ researchers aren't seeking blockbuster discoveries; they're making thousand small improvements—a better bonding agent here, a more efficient fusion process there. These compound over time into insurmountable competitive advantages.

Customer concentration is surprisingly low. No single customer exceeds 5% of revenues. This isn't accidental—CUMI deliberately diversifies across industries, geographies, and applications. When automotive slumps, construction might boom. When India slows, exports accelerate. This diversification provides stability but requires managing complexity that would overwhelm most companies.

The capital allocation philosophy reflects Murugappa conservatism. Growth capex is funded from internal accruals. Acquisitions are paid in cash, not stock. Dividends are steady but not excessive. Debt is minimal. This might seem overly cautious in an era of cheap money, but it provides flexibility during downturns—when competitors are deleveraging, CUMI can invest.

Competitive Moats & Market Position

Warren Buffett talks about moats, but CUMI has something more fundamental: accumulated technical knowledge that compounds over time. Seventy years of making abrasives creates expertise that money can't buy. Every failed experiment, every customer complaint, every process improvement adds to an institutional knowledge base that competitors can't replicate.

The raw material security through backward integration isn't just about cost; it's about quality consistency. When you're selling grinding wheels for jet engine manufacture, variations in grain quality aren't acceptable. CUMI's integrated model ensures that every batch meets specifications—a reliability that customers pay premiums for.

The Company makes over 20,000 varieties of products manufactured at 25 locations across India, Russia, South Africa, Australia, China, Thailand and Canada. This geographic spread isn't just market access; it's risk mitigation. Natural disasters, political upheaval, or pandemic lockdowns in one location don't cripple the company. Moreover, each location brings unique advantages—low-cost Indian manufacturing, Russian raw materials, German technology, Chinese market access.

Brand strength in industrial products seems oxymoronic, but it's real. A maintenance manager specifying abrasives for a critical application won't experiment with unknown suppliers. CUMI's brands—built over decades, proven in millions of applications—provide comfort that new entrants can't match. The cost of failure (production downtime, worker injury, product defects) far exceeds any savings from cheaper alternatives.

Switching costs are subtle but significant. It's not just about product compatibility; it's about technical support, training, supply chain integration. CUMI's field engineers don't just sell products; they solve problems. They optimize grinding parameters, recommend process improvements, train operators. Replacing CUMI means replacing this entire support ecosystem.

The company's position in specialized applications creates mini-monopolies. In certain ceramic formulations for electronics, CUMI is one of perhaps three global suppliers. In specific super-abrasive specifications, they might be the only qualified source. These niches, individually small but collectively significant, provide pricing power and customer stickiness.

Financial Analysis & Performance

The numbers tell a story of steady compounding rather than explosive growth. In 2023, Carborundum Universal's revenue was 47.02 billion, an increase of 1.03% compared to the previous year's 46.54 billion. Earnings were 4.61 billion, an increase of 11.42%. This isn't tech-style hypergrowth, but in materials science, consistency matters more than velocity.

Company is almost debt free. Company has been maintaining a healthy dividend payout of 19.5%. The debt-free status isn't just conservative finance; it's strategic flexibility. In commoditized industries, downturns are brutal. Companies with leverage face existential threats. CUMI can use downturns to acquire distressed assets, hire talent from struggling competitors, and gain market share.

Company has a low return on equity of 13.8% over last 3 years. This ROE might disappoint growth investors, but it reflects capital intensity inherent in materials manufacturing. Furnaces, fusion plants, and ceramic kilns require massive upfront investment. The returns are steady but not spectacular—the tortoise, not the hare.

Margin evolution reveals operational excellence. Despite raw material inflation and energy cost spikes, CUMI has maintained EBITDA margins in the mid-teens. This stability comes from operational leverage (fixed costs spread over growing volumes), mix improvement (shift toward higher-margin technical products), and cost discipline (continuous process optimization).

Working capital management in abrasives is challenging. Raw materials must be stockpiled (supply chain disruptions are catastrophic), finished goods inventory is necessary (customers expect immediate availability), and receivables cycles reflect industrial payment terms. CUMI's working capital turns have improved steadily, reflecting better inventory management and collection efficiency.

Capital efficiency metrics require context. Asset turns in materials manufacturing will never match asset-light businesses. But within the peer group, CUMI's capital efficiency is superior, reflecting better capacity utilization, modern equipment, and optimized plant layouts. Every percentage point improvement in asset turns, compounded over decades, creates enormous value.

Industry Dynamics & Future Vectors

The electric vehicle revolution isn't just changing automobiles; it's transforming the entire materials value chain. EVs require different abrasives—silicon carbide for power electronics, specialized ceramics for battery components, ultra-precise grinding for motor magnets. CUMI, with its broad materials portfolio, is positioned to benefit regardless of which EV technology wins. The semiconductor and electronics manufacturing boom in India represents perhaps CUMI's greatest opportunity. India's semiconductor market is expected to grow from $52 billion (Rs 4.5 trillion) in 2024 to $103.4 billion (Rs 9 trillion) by 2030, and every semiconductor fab requires specialized abrasives for wafer grinding and polishing. CUMI's ultra-fine alumina and silicon carbide powders are essential consumables in chip manufacturing.

The infrastructure super-cycle—roads, railways, metros, airports—drives demand for construction materials where CUMI's refractories and abrasives play crucial roles. Every kilometer of highway requires grinding wheels for concrete finishing. Every steel beam needs surface preparation. The multiplier effects are enormous.

The China+1 strategy adopted by global manufacturers benefits CUMI directly. As companies diversify supply chains away from China, India emerges as the logical alternative for abrasives and technical ceramics. CUMI, with its established infrastructure and technical capabilities, captures this shift without additional investment.

Sustainability concerns are reshaping materials science. CUMI's investment in recycling technologies—recovering abrasive grains from used wheels, reprocessing ceramic waste—positions them for a circular economy. Environmental regulations that burden competitors become competitive advantages for prepared players.

Competition from Chinese manufacturers remains the primary threat. Chinese abrasives, often 30-40% cheaper, pressure margins in commodity segments. CUMI's response—moving upmarket into technical products where quality matters more than price—is necessary but challenging.

Bear vs. Bull Case

The Bull Case:

CUMI sits at the intersection of multiple secular growth trends. The India manufacturing renaissance, driven by PLI schemes and infrastructure spending, directly benefits industrial consumables. Every new factory needs abrasives. Every infrastructure project requires refractories. This isn't speculative growth; it's mathematical certainty.

The European technology acquisitions provide competitive differentiation that Chinese competitors can't easily replicate. German engineering combined with Indian cost structures creates a unique value proposition. Customers get developed-market quality at emerging-market prices—an unbeatable combination.

The debt-free balance sheet provides strategic flexibility that leveraged competitors lack. When the next downturn arrives—and it will—CUMI can acquire distressed assets at attractive valuations. They've done it before in 2008-2009; they'll do it again. Each crisis strengthens their competitive position.

As a critical supplier to multiple growth industries—semiconductors, EVs, renewable energy—CUMI benefits regardless of which technologies win. They're selling picks and shovels to every prospector, a position that historically generates steady returns with lower risk than betting on specific outcomes.

The Bear Case:

Cyclical exposure to industrial capex creates earnings volatility that markets punish. When manufacturing slows—as it inevitably does—abrasives demand collapses. Fixed costs in capital-intensive manufacturing mean that revenue declines translate directly to margin compression.

Commodity input cost pressures—bauxite, energy, petroleum-based resins—squeeze margins unpredictably. CUMI can't easily pass through cost increases to industrial customers facing their own margin pressures. The lag between input cost inflation and price realization destroys value.

Integration risks from rapid acquisitions shouldn't be underestimated. Cultural clashes, system incompatibilities, and management attention dilution can destroy value even in strategically sound deals. CUMI's track record is good but not perfect; one bad acquisition could undo years of patient building.

ROE concerns persist. A return on equity of 13.8% over the last 3 years in a growing economy suggests either capital allocation inefficiency or structural industry challenges. Investors can find better returns elsewhere without the complexity and cyclicality.

Playbook: Key Lessons

The CUMI story offers timeless lessons for building enduring industrial enterprises. First and foremost: patient capital beats smart money. The Murugappa Group's multi-generational thinking—investing in capabilities that take decades to mature—created competitive advantages that quarterly-focused competitors can't replicate.

The power of technical partnerships deserves emphasis. CUMI didn't try to reinvent abrasives technology; they licensed it, learned it, and eventually improved it. Pride kills more companies than competition. Recognizing what you don't know and finding partners who do is wisdom, not weakness.

Managing conglomerate complexity while maintaining focus seems paradoxical but isn't. CUMI's three-segment structure provides diversification within a coherent theme—materials that shape other materials. This isn't random diversification; it's systematic expansion along technical and customer adjacencies.

Timing market cycles in commoditized industries requires discipline that most management teams lack. The temptation to expand capacity at cycle peaks, when profits are high and capital is available, destroys value. CUMI's counter-cyclical investments—buying when others are selling—created lasting advantages.

Building trust as a competitive advantage sounds soft but is anything but. In industrial markets, where switching costs are high and failure consequences severe, reputation matters more than price. CUMI's 70-year track record of reliability—never missing a delivery, never compromising quality—is a moat that money can't buy.

The technology absorption model—moving from licensing to learning to innovation—provides a roadmap for emerging market companies. You don't need to be first; you need to be better. CUMI's journey from importing technology to exporting it shows that capability building, not first-mover advantage, determines long-term success.

Recent News

The recent financial performance tells a nuanced story. Carborundum Universal Ltd (CUMI) reported a 68.8% year-on-year decline in net profit, posting ₹34.7 crore for the third quarter ended December 31, 2024, though revenue from operations grew 9% YoY to ₹1,255.5 crore. This profit compression reflects the challenges of integrating acquisitions while managing input cost inflation.

The company incurred capital expenditure of Rs 202 crore at a consolidated level during the first nine months of the current financial year, and the Board of Directors declared an interim dividend of Rs 1.50 per share (150 per cent on face value of Re 1). This demonstrates management's confidence in long-term prospects despite near-term headwinds.A strategic highlight was the acquisition completed in October 2024: CUMI entered into a binding Share Purchase Agreement to acquire a 100% stake from existing equity shareholders of Silicon Carbide Products, Inc. USA (SCP) at an Enterprise Value of USD 6.66 million (Rs 56 crore indicative). SCP, located in Horseheads, NY, USA, specializes in producing high-quality Nitride Bonded Silicon Carbide (NBSiC) products. NBSiC ceramics have superior wear and thermal shock resistance.

The managing director's comments reveal the strategic thinking: Sridharan Rangarajan stated, "The acquisition of SCP aligns with CUMI's strategic expansion plans. SCP concluded 2023 with sales of USD 4.2 million with a healthy profit and return profile". This acquisition strengthens CUMI's position in critical thermal applications for power, steel, and mining sectors while providing access to the Americas market.

Looking ahead, the company expects full year consolidated sales growth of 9% to 11% on a stable currency basis, with consolidated sales projected to be INR 51,000 million to INR 52,000 million. This guidance reflects management's confidence despite near-term margin pressures from integration costs and input inflation.

Links & Resources

Primary Sources: - CUMI Investor Relations: www.cumi-murugappa.com - Murugappa Group Corporate: www.murugappa.com - NSE/BSE Filings and Announcements

Industry Research: - India Semiconductor Mission Reports - IESA (India Electronics and Semiconductor Association) Publications - Abrasives Industry Global Market Reports

Historical Context: - "The House of Murugappa" - Corporate history publication - "Fortune Seekers: A Business History of Nattukottai Chettiars" by Raman Mahadevan - Indian industrial policy documents (1950s-1990s)

Technical Resources: - Materials Science journals on abrasives technology - Semiconductor manufacturing process documentation - Industrial ceramics technical specifications

Financial Analysis: - Annual Reports (FY2019-2024) - Quarterly earnings call transcripts - Broker research reports (accessible through financial terminals)

The Carborundum Universal story is ultimately about transformation—from money-lenders to manufacturers, from local to global, from imitators to innovators. It's a testament to the power of patient capital, technical excellence, and strategic thinking. In an era of quick flips and financial engineering, CUMI represents something increasingly rare: a company that makes real things that matter, built over generations, designed to last for generations more.

For investors, CUMI offers exposure to the physical infrastructure of the digital age. Every AI chip needs grinding, every EV battery requires ceramics, every wind turbine demands specialized materials. These aren't sexy businesses, but they're essential ones. And in the long arc of industrial history, essential usually wins.

The journey from a small office in colonial Burma to a global materials science leader spanning continents is remarkable. But perhaps more remarkable is what hasn't changed: the Murugappa values of trust, quality, and long-term thinking. In a world of quarterly capitalism, that might be the most valuable asset of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube