Schaeffler India: The Precision Engineering Powerhouse

I. Introduction & Episode Roadmap

Picture this: A massive automotive assembly line in Chennai, 2024. Hundreds of robots dance in synchronized precision, welding and assembling the latest electric SUV for one of India's leading manufacturers. Hidden within the powertrain, transmission, and wheel assemblies are dozens of components that most will never see—precision bearings, clutch systems, and now, sophisticated e-axle modules. The supplier? Schaeffler India, a company that has quietly become the circulatory system of India's automotive industry.

With a market capitalization of ₹63,906 crores, Schaeffler India stands as one of the most profitable engineering companies on the Indian exchanges. Yet mention the name at a dinner party, and you'll likely get blank stares. This is the paradox of being a tier-one automotive supplier—critical to everything that moves, invisible to everyone who drives.

The question that frames our exploration today: How did a German bearing manufacturer, born from the rubble of post-war Europe, become India's indispensable automotive supplier? It's a story that spans from 1962—when India was still finding its industrial feet—to today's electric vehicle revolution where Schaeffler's e-mobility components are defining the future of transportation. Our journey through Schaeffler India reveals several interconnected themes: the power of German Mittelstand philosophy transplanted to emerging markets, the critical importance of being embedded deep in supply chains, and the evolution from component supplier to systems integrator. Most importantly, it's a story about timing—arriving early enough to build capabilities but patient enough to wait for markets to mature.

This exploration unfolds across distinct eras. We begin in post-war Germany where two brothers transform agricultural equipment repair into industrial innovation. We then travel to 1962 India, where a young nation's industrial ambitions meet German engineering precision. Through liberalization, globalization, and now electrification, we'll trace how Schaeffler India navigated each transition.

The narrative structure follows chronological progression but with thematic depth at each stage. Early sections focus on building—technology, relationships, manufacturing capacity. Middle sections examine consolidation and market leadership. Recent chapters dive into the transformation challenge: How does a mechanical components company reinvent itself for the software-defined, electric future?

For investors, this isn't just another MNC subsidiary story. Schaeffler India's Q3 2024 revenue of Rs. 20,728 million represents 12.1% growth, with net profit margin of 11.9%—numbers that reflect both operational excellence and strategic positioning. The question isn't whether Schaeffler makes money—it clearly does. The question is whether its transformation into an e-mobility leader will sustain these returns through the next technological revolution.

As we embark on this journey from bearings to batteries, from mechanical to mechatronic, keep in mind the fundamental paradox: The more invisible the component, often the more critical it becomes. Schaeffler India has mastered this invisibility while becoming indispensable. Let's understand how.

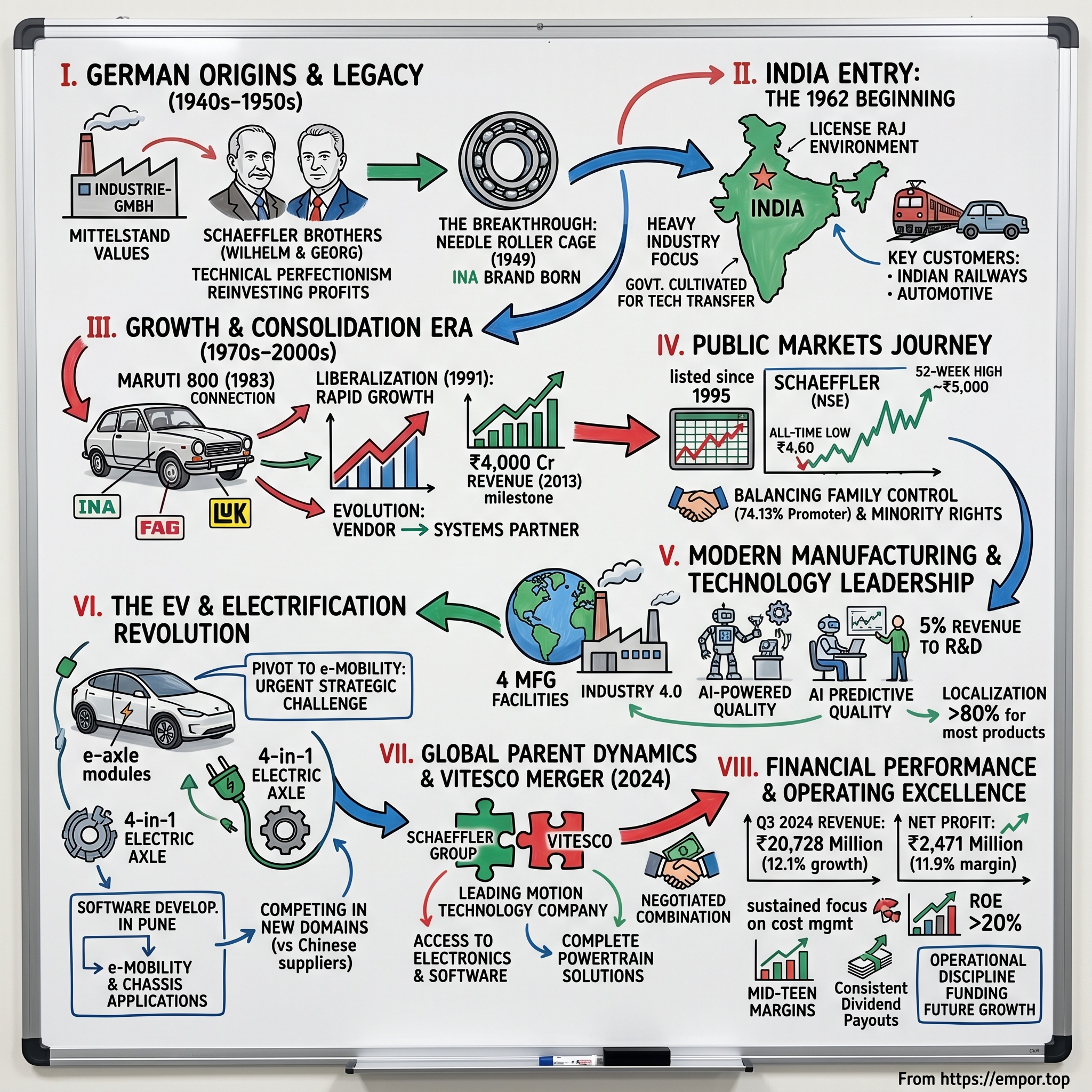

II. The Schaeffler Family Legacy & German Origins

The year is 1946. Herzogenaurach, a small Bavarian town, lies amid the rubble of defeated Germany. While most Germans scramble for food and shelter, two brothers—Wilhelm and Georg Schaeffler—see opportunity in devastation. Together with two partners, they establish Industrie-GmbH, initially focused on repairing agricultural equipment for American occupation forces and local farmers desperate to restart food production.

This wasn't their first venture. Before the war, the brothers had already shown entrepreneurial spirit. But like many German industrialists of that era, their wartime activities remain a complex chapter—one the company has openly addressed through historical commissions and reparations. What matters for our story is what came next: the transformation from repair shop to precision engineering powerhouse.

The breakthrough came in 1949. Georg Schaeffler, the engineering mind of the duo, developed something revolutionary yet elegantly simple: the needle roller cage. Until then, needle roller bearings were unreliable, prone to skewing and jamming. Georg's cage design held the needles in perfect parallel alignment, transforming them into dependable industrial components. This innovation would propel INA (Industrie Nadellager) from obscurity to industrial prominence.

What made the Schaeffler approach different? While American companies pursued scale and standardization, and Japanese firms would later perfect lean manufacturing, the Schaefflers embodied classic German Mittelstand values: technical perfectionism, long-term thinking, and stubborn independence. They refused outside capital, reinvested profits obsessively, and treated customers as partners in engineering challenges.

By the 1960s, INA had become synonymous with precision bearings in Germany. The company's philosophy was simple but demanding: solve the customer's problem, even if it means developing entirely new products. When Volkswagen needed lighter valve train components for the Beetle, INA developed new cam followers. When industrial machinery required higher speeds, INA engineered ceramic hybrid bearings. Each solution opened new markets, creating a virtuous cycle of innovation and growth.

The family structure evolved but remained tight. Wilhelm focused on finance and administration while Georg drove technical innovation. After Wilhelm's death in 1981, his widow Maria-Elisabeth Schaeffler took control of the business side, forming a powerful partnership with Georg that would last until Georg's death in 1996. Maria-Elisabeth, often underestimated as merely a widow inheriting wealth, proved to be a formidable businesswoman, orchestrating international expansion while maintaining family control. As of 2021, the firm was majority owned by Maria-Elisabeth Schaeffler-Thumann and her son Georg F. W. Schaeffler, continuing the lifelong work of her husband Dr. Ing. h.c. Georg Schaeffler, who died in 1996. The ownership structure reflects classic German Mittelstand principles: Georg F. W. Schaeffler owns 80% of the holding company INA Holding Schaeffler GmbH & Co. KG, while his mother Maria-Elisabeth owns the other 20%.

This family control isn't merely financial—it's philosophical. The Schaefflers view their company through a generational lens, making decisions that might seem irrational to quarterly-focused public markets but prove prescient over decades. When competitors outsourced production to Asia, Schaeffler maintained German manufacturing for critical components. When others diversified into unrelated businesses, Schaeffler stayed focused on motion technology.

The company's three-brand strategy emerged organically through history. INA represented the original needle bearing innovation. FAG (Fischer Aktien-Gesellschaft), acquired in 2001, brought ball bearing excellence and a century of heritage. LuK, fully acquired in 1999, added clutch and transmission expertise. Rather than consolidate these brands, Schaeffler maintained their distinct identities—each representing different engineering traditions and customer relationships.

By the early 2000s, Schaeffler had become a sprawling industrial empire: 30,000 employees, dozens of plants worldwide, and revenues exceeding €6 billion. Yet it remained stubbornly private, resistant to capital markets' short-term pressures. This independence would prove both a strength and, during the 2008 financial crisis following the Continental acquisition attempt, nearly its undoing.

The German engineering culture permeated everything. Engineers weren't just employees; they were craftsmen continuing centuries-old traditions. The apprenticeship system, where teenagers learned precision manufacturing alongside university-trained engineers, created a unique knowledge transfer mechanism. A Schaeffler bearing wasn't just a product—it was a promise of German reliability.

This cultural foundation would prove crucial as Schaeffler expanded globally. The question wasn't whether German engineering could succeed abroad, but whether German values could transplant to radically different environments. India, with its unique challenges and opportunities, would become one of the most important testing grounds for this thesis.

III. India Entry: The 1962 Beginning

The Ambassador car assembly line at Hindustan Motors' Uttarpara plant, 1962. Workers manually fit components, tighten bolts, adjust mechanisms. Everything moves slowly, deliberately. Quality control means a supervisor's experienced eye, not computerized sensors. Into this world of industrial infancy arrives a small team from Herzogenaurach, carrying blueprints for precision bearing manufacturing—technology that seems almost alien in Nehru's India.

Schaeffler's entry into India in 1962 wasn't driven by today's familiar narratives of emerging market growth or labor arbitrage. This was License Raj India—a economy where producing a simple ball bearing required multiple government permits, importing machinery meant navigating byzantine regulations, and foreign ownership faced severe restrictions. Why would a German family company venture into this bureaucratic labyrinth?

The answer lay in India's industrial ambitions. The Second Five-Year Plan (1956-61) had prioritized heavy industry, and the Third Plan continued this emphasis. India needed bearings—for railways, for steel plants, for the nascent automotive sector. Importing them drained precious foreign exchange. The government actively courted foreign technical collaboration, offering protected markets in exchange for technology transfer.

For Schaeffler, India represented a different calculus than other international markets. In Europe or America, they competed with established players. In India, they could shape an industry from scratch. The Indian Railways alone—with its thousands of locomotives and lakhs of wagons—represented massive bearing demand. State-owned enterprises in steel, power, and heavy machinery needed reliable suppliers. And somewhere in the future lay the promise of automotive growth.

The initial operations were modest—a small facility manufacturing standard ball bearings under technical collaboration. But even this simple beginning required enormous adaptation. German specifications assumed consistent steel quality, precise temperature control, skilled operators. India offered enthusiastic workers but inconsistent materials, erratic power supply, and extreme weather conditions that German engineers had never contemplated.

Consider the mundane challenge of maintaining clean room conditions for precision manufacturing. In Germany, this meant sealed environments and filtered air. In India's dust and monsoon humidity, it required complete reimagination. Schaeffler's engineers developed new protocols: multiple air-lock entries, localized cooling systems, innovative sealing techniques. Each solution became intellectual property, knowledge that would later prove valuable in other emerging markets.

The human dimension proved equally complex. Schaeffler's German training methods—rigorous, hierarchical, focused on individual perfectionism—met India's collaborative, jugaad-oriented work culture. Rather than impose German methods wholesale, smart managers created hybrid approaches. Indian workers brought innovative problem-solving to equipment maintenance; German systems provided quality frameworks. The synthesis produced something unique: German precision with Indian adaptability.

Early customers reflected India's industrial priorities. Indian Railways became a cornerstone account, requiring bearings that could withstand India's diverse geography—from Rajasthan's sand to Cherrapunji's moisture. Each failure became a learning experience, each success a foundation for expansion. The Integral Coach Factory in Chennai, established in 1955, needed specialized bearings for new passenger coaches. Heavy engineering companies like BHEL and L&T required industrial bearings for their expanding operations.

By the late 1960s, Schaeffler India had moved beyond simple import substitution. They began localizing production, finding Indian suppliers for steel and components. This wasn't easy—Indian steel quality varied wildly, heat treatment facilities were primitive, and precision measurement tools were scarce. Schaeffler responded by backward integration, establishing quality control at supplier facilities and sometimes helping suppliers upgrade capabilities.

The relationship with government proved delicate. License Raj meant navigating multiple ministries, managing production quotas, and accepting price controls. Yet Schaeffler's German reputation for quality provided leverage. When critical projects needed reliable bearings—whether for defense, railways, or power generation—bureaucrats often preferred Schaeffler despite higher costs. Quality became the company's license to operate.

Through the 1970s, despite the challenging business environment, Schaeffler quietly expanded. They established a second plant, diversified into automotive bearings as Maruti prepared to launch, and began exploring export opportunities to other developing countries. The foundation was being laid for something larger—though few could have predicted how liberalization would transform these patient investments into market leadership.

IV. Growth & Consolidation Era (1970s-2000s)

The Maruti 800 rolls off the production line in Gurgaon, December 1983. India's first truly affordable car needs hundreds of components, many imported at great expense. Among the critical suppliers already established and ready: Schaeffler India, whose bearings and clutch systems would become integral to every vehicle Maruti produced. This moment—when Indian automotive ambitions met established component expertise—would define Schaeffler's trajectory for the next three decades.

Through the 1970s and early 1980s, Schaeffler India had steadily built capabilities despite License Raj constraints. The company operated like a technical university, training not just its own workers but often helping customers understand bearing applications. When Tata Motors needed specialized bearings for commercial vehicles, Schaeffler engineers spent months at Tata facilities, understanding requirements and developing custom solutions. This consultative approach—unusual in vendor relationships—created deep customer loyalty.

The 1991 liberalization changed everything. Suddenly, Schaeffler could import advanced machinery, expand production without government approval, and price products based on market dynamics rather than bureaucratic formulas. More importantly, global automotive companies began entering India, and they brought international quality expectations. Schaeffler's two-decade preparation paid off spectacularly. The transformation accelerated dramatically in 2006, when Schaeffler AG acquired the Indian operations from the previous joint venture partner, enhancing its control over production and market strategy. This wasn't just a change in ownership—it marked a strategic inflection point. With full control, Schaeffler could implement global best practices without compromise, invest without seeking partner approval, and align Indian operations with worldwide strategy.

The three-brand architecture now fully deployed in India—INA, FAG, and LuK—each served distinct market segments. INA dominated needle bearings and linear guidance systems. FAG, with its century-old heritage, commanded premium positioning in ball bearings. LuK brought clutch and transmission expertise critical for India's growing automotive sector. Rather than confuse customers with brand consolidation, Schaeffler maintained these identities, allowing each to leverage its specific strengths.

The numbers tell the story of explosive growth. By 2013, Schaeffler India achieved a significant milestone in market presence, reporting a revenue of approximately ₹4,000 crores. This marked a compounded annual growth rate (CAGR) of around 18% over five years. But raw growth metrics don't capture the strategic positioning achieved during this period.

Consider the automotive transformation. In the 1990s, Schaeffler supplied perhaps 5-10 components per vehicle. By 2010, a typical passenger car contained 30-50 Schaeffler parts—bearings in the engine, transmission, wheels, and steering, plus increasingly sophisticated mechatronic components. The company had evolved from vendor to partner, involved in vehicle development from concept stage.

The shift wasn't just quantitative but qualitative. When Hyundai established its Chennai plant, Schaeffler didn't just supply bearings—they embedded engineers at Hyundai facilities, co-developing solutions for India-specific requirements. Indian roads demanded different durability standards than Korean or European markets. Schaeffler's ability to adapt global technology to local needs while maintaining quality standards became a competitive moat.

Technology transfer accelerated through the 2000s. The Pune facility evolved into a center of excellence for certain product lines, supplying not just India but global markets. This reversed the traditional narrative—instead of India always receiving technology, it began exporting innovation. When Schaeffler needed to develop cost-effective bearing solutions for emerging markets, the frugal engineering expertise came from India.

The talent development story paralleled technological advancement. Schaeffler India became a training ground for engineers who would later lead operations in other emerging markets. The company's apprenticeship program, modeled on German vocational training but adapted for Indian conditions, produced technicians whose skills rivaled global standards. Many Indian engineers moved to Germany for advanced training, returning with expertise that elevated local capabilities.

By 2013, Schaeffler India had transcended its original role as a local manufacturing outpost. It had become integral to global supply chains, a source of innovation, and a profit center contributing significantly to group earnings. The patient investment through difficult decades—maintaining quality when competitors cut corners, investing in training when others relied on job-hopping, building capabilities when markets didn't yet demand them—had created a formidable competitive position.

The stage was set for the next phase: public markets. After five decades of private operation, Schaeffler India would open itself to external shareholders, bringing both opportunities and challenges that would test whether German family values could coexist with Indian capital market expectations.

V. The IPO & Public Markets Journey

The boardroom at Schaeffler India's Mumbai office, 2000. The discussion is heated—should the company tap Indian capital markets? Global parent Schaeffler AG needs capital for expansions, Indian operations require investment for growth, but the family's ironclad principle of maintaining control seems incompatible with public listing requirements. This tension would simmer for years before resolution.

Unlike typical IPO stories driven by venture capital exits or founder liquidity needs, Schaeffler India's path to public markets was shaped by regulatory compulsion and strategic calculation. As the Indian subsidiary grew more profitable and strategic, questions arose about minority shareholder rights and governance standards. The solution was elegant: list the Indian entity while maintaining German family control through careful structuring. The company had been listed since January 17, 1995, but this was initially as FAG Bearings India Limited with limited float and modest trading volumes. The real transformation came post-2006 acquisition when Schaeffler AG consolidated control. Listing date: 17 Jan, 1995 marked the beginning of a three-decade journey in Indian capital markets.

What makes Schaeffler India's public market structure unique is the balance achieved between family control and minority rights. The company's shareholding pattern indicated a promoter stake of 74.13%, just below the 75% threshold that would trigger mandatory delisting requirements. This wasn't accidental—it represented careful calibration to maintain control while respecting regulatory boundaries.

The minority shareholder base evolved into an interesting mix. The foreign institutional investor stake in the company was 4.81%. Domestic mutual funds and other domestic institutional investors held a stake of 15.04%. Quality institutions dominated—funds like Kotak Emerging Equity, Axis Midcap, and UTI Flexi Cap held substantial positions, validating the company's governance and growth prospects.

Stock performance tells a story of steady wealth creation punctuated by dramatic moves. The Schaeffler India's 52-week high share price is Rs 4,950.00 and 52-week low share price is Rs 2,836.55. The journey from the all-time low of ₹4.60 in August 1998 to nearly ₹5,000 represents a 1,000-fold increase—extraordinary returns for patient shareholders who understood the underlying business quality.

But these returns didn't come smoothly. The stock experienced multiple 30-40% drawdowns during global automotive downturns, testing investor conviction. During the 2008 financial crisis, when parent Schaeffler's aggressive Continental acquisition nearly bankrupted the group, Indian minority shareholders faced existential uncertainty. Would the parent strip cash from the profitable Indian subsidiary to service German debt?

The answer revealed Schaeffler's governance philosophy. Despite desperate need for capital in Germany, the Indian subsidiary maintained its dividend policy, continued investments, and respected minority rights. This restraint during crisis—when many MNC parents would have extracted maximum value—built enormous trust with Indian institutional investors.

Dividend policy became another differentiator. Unlike many growth companies that retained all earnings, Schaeffler India balanced growth investment with shareholder returns. The company maintained consistent payouts, typically distributing 30-40% of profits while retaining sufficient capital for expansion. This attracted a different investor class—those seeking quality growth with income, not just capital appreciation.

The MNC premium—or sometimes discount—played out interestingly. In bullish markets, investors paid premium valuations for Schaeffler's technology access and German parentage. During pessimistic phases, the same parentage triggered concerns about profit repatriation and limited float. This valuation volatility created opportunities for astute investors who understood the underlying business stability.

Capital allocation under public scrutiny forced interesting decisions. Should the company maximize short-term profits by importing components, or invest in local manufacturing for long-term competitiveness? Should they pursue aggressive market share at lower margins, or maintain pricing discipline? The public market's quarterly focus sometimes conflicted with German long-term thinking, creating tension that management had to carefully navigate.

By 2020, Schaeffler India had evolved into something unique in Indian capital markets: a highly profitable MNC subsidiary with genuine local manufacturing, consistent governance, and strategic importance to its parent. The stock commanded premium valuations—often trading at 40-50x earnings compared to 20-25x for local competitors—reflecting both quality and scarcity value.

The public listing also facilitated talent retention and acquisition. Stock options, though limited given promoter control, provided additional compensation tools. More importantly, being a listed entity enhanced corporate prestige, making it easier to attract top engineering and management talent who might otherwise prefer purely Indian companies or global MNCs.

As we transition to examining modern manufacturing capabilities, remember that public market scrutiny forced operational excellence. Every capacity expansion, technology investment, and margin movement faced investor questioning. This accountability, initially seen as burden, ultimately strengthened decision-making and execution—preparing Schaeffler India for the technological disruptions ahead.

VI. Modern Manufacturing & Technology Leadership

Dawn breaks over Schaeffler's new Hosur facility, 2024. Inside, collaborative robots work alongside skilled technicians, laser-guided vehicles transport components autonomously, and AI-powered quality systems detect microscopic defects invisible to human inspection. This isn't just manufacturing—it's a glimpse into Industry 4.0's promise realized. Yet twenty meters away, master craftsmen still hand-finish specialized bearings for aerospace applications, their skills irreplaceable by any algorithm.

Schaeffler India currently operates four manufacturing facilities in Pune, Savli, Maneja, and Hosur, along with three research and development centers. But these aren't just production sites—each represents a distinct capability center serving specific market needs and technology domains.

The Pune facility, the oldest and most integrated, spans multiple product lines from automotive bearings to industrial solutions. Walking through its shopfloor reveals manufacturing evolution in microcosm: 1980s-era grinding machines operate beside latest-generation CNC centers, each optimized for specific products. This isn't inefficiency—it's pragmatic capital allocation, upgrading where precision demands while sweating older assets where adequate.

Savli in Gujarat emerged as the automotive hub, strategically located near OEM clusters. Here, just-in-time delivery isn't aspiration but necessity—components reach assembly lines within hours of production. The facility pioneered "milk run" logistics in India, with trucks following fixed routes collecting components from multiple suppliers, reducing transportation costs while ensuring reliability.

Q2 FY25: Revenue ₹2,282 Cr (+10%), EBITDA ₹449 Cr (19.7%), new plant inaugurated, e-axle production started. This new facility represents Schaeffler's bet on electrification—purpose-built for e-mobility components rather than retrofitted from conventional production. The economics are compelling: electric vehicles require different bearings (higher speeds, different loads) and entirely new components like e-axles that integrate motor, transmission, and power electronics.

The technology story extends beyond hardware. Schaeffler India has quietly built sophisticated software capabilities, essential for modern automotive systems. When a modern car's stability control activates, it relies on wheel speed sensors and algorithms—increasingly developed in Indian R&D centers. This software expertise, initially supporting hardware, has become a product category itself.

Consider the company's approach to quality—not as inspection but as process design. Every bearing produced undergoes multiple automated checks: dimensional accuracy via laser measurement, surface finish through optical scanning, material integrity using ultrasonic testing. But the real innovation lies in predictive quality—AI systems that identify process deviations before they produce defects. A slight temperature variation in heat treatment, an unusual vibration in grinding—the system flags these anomalies for investigation.

The numbers validate this operational excellence. The PBT margin stood at 16.1%, compared to 17.1% in Q3 2023—maintaining mid-teen margins in a capital-intensive manufacturing business requires exceptional efficiency. How does Schaeffler achieve this while competing against low-cost local players and Chinese imports?

The answer lies in value engineering—designing products for Indian conditions while maintaining global quality. A bearing for European highways experiences different stresses than one navigating Mumbai's monsoon potholes. Schaeffler India doesn't just tropicalize global designs; it fundamentally reengineers products for local requirements. This expertise now serves other emerging markets—bearings designed in India ship to Southeast Asia, Africa, and Latin America.

Employee productivity tells another story. The company employs over 3,700 people in India, generating over ₹8,000 crores in revenue—roughly ₹2.2 crores per employee, exceptional for Indian manufacturing. This isn't achieved through automation alone but through skilled workforce development. The company's apprenticeship program, modeled on German vocational training, produces technicians who understand both traditional machining and modern automation.

The localization journey deserves special attention. In the 1990s, Schaeffler India imported 60-70% of raw materials and components. Today, local sourcing exceeds 80% for most products. This wasn't easy—Indian steel initially couldn't meet specifications, heat treatment facilities lacked precision, and suppliers needed extensive development. Schaeffler invested in supplier capability, sometimes providing equipment and training, creating an ecosystem that benefits the entire industry.

R&D investment reveals strategic priorities. The company also emphasizes research and development, investing approximately 5% of its revenue into R&D activities annually. This exceeds most Indian manufacturers but remains below global automotive suppliers who typically invest 6-8%. The focus is pragmatic: less basic research, more application engineering and production optimization.

Digital transformation permeates operations but without Silicon Valley hype. Predictive maintenance systems monitor equipment health, preventing breakdowns that could halt just-in-time deliveries. Digital twins—virtual replicas of production lines—allow engineers to optimize processes through simulation before physical implementation. Yet the company avoids technology for its own sake, implementing only solutions with clear ROI.

The competitive moat isn't any single factor but the integration of multiple capabilities. A Chinese competitor might offer lower prices but can't match application engineering support. A local player might provide flexibility but lacks global technology access. European competitors have technology but can't match Indian cost structures. Schaeffler India sits at the sweet spot—global technology at Indian costs with local responsiveness.

As we examine the electric vehicle transformation next, remember that manufacturing excellence provides the foundation. The ability to produce millions of precision components with consistent quality, the infrastructure to support customers from prototype to production, the expertise to solve complex engineering challenges—these capabilities, built over decades, enable the rapid pivot to e-mobility that might otherwise seem impossible.

VII. The EV & Electrification Revolution

The Schaeffler India engineering center in Pune, late 2023. A cross-functional team huddles around a disassembled electric axle—motor, power electronics, and transmission integrated into a single unit. The discussion is heated: How to achieve the power density required by an Indian OEM while meeting cost targets 40% below global benchmarks? This scene, repeated daily, represents Schaeffler's transformation from mechanical component supplier to e-mobility solution provider.

The electric vehicle revolution poses an existential question for traditional automotive suppliers: What happens when vehicles no longer need engine bearings, transmission clutches, or many mechanical components that generated profits for decades? For Schaeffler India, this isn't theoretical—it's an urgent strategic challenge requiring fundamental business model transformation. The strategic response crystallized in 2022 with a bold move: the company inaugurated a new center of competence in software development in Pune, India. Electronics and software for the company's automotive components and systems especially for e-mobility and chassis applications will be developed here in the future as a strategically important part of a powerful international R&D network. Schaeffler will be investing 10 million euros in its new location. The newly formed entity Schaeffler Technology Solutions India Private Limited is a wholly owned subsidiary of the Schaeffler Group and will be employing 200 engineers in India—a clear signal that India isn't just a manufacturing base but a critical innovation hub for global e-mobility strategy.

The transformation goes deeper than adding software capabilities. Electric vehicles fundamentally alter component requirements. Traditional engines have hundreds of moving parts requiring multiple bearings; electric motors have essentially one moving part. Transmissions simplify from complex multi-gear systems to single or dual-speed units. The value shifts from mechanical complexity to electronic sophistication and system integration.

Schaeffler's response: don't just supply components, provide integrated systems. The company develops everything from individual electromobility components to highly complex systems such as its 4in1 electric axle that integrates electric motor, power electronics, transmission, and thermal management into one comprehensive system. This system-level approach transforms Schaeffler from commodity supplier to technology partner, capturing more value per vehicle even as component count decreases.

The Indian market presents unique e-mobility challenges that become global opportunities. Cost pressures are extreme—Indian OEMs demand 40-50% lower prices than developed markets. Range anxiety is acute given inadequate charging infrastructure. Durability requirements are severe given road conditions and climate extremes. Solving these challenges creates products applicable across emerging markets.

Consider thermal management, critical for battery life and performance. European solutions assume moderate temperatures and good roads. Indian conditions—50°C summers, monsoon humidity, pothole impacts—require fundamental redesign. Schaeffler India's engineers developed innovative cooling strategies using locally available materials and manufacturing processes, achieving similar performance at fraction of the cost.

Software capabilities prove surprisingly synergistic with traditional mechanical expertise. Modern vehicle stability systems require precise wheel speed sensing—Schaeffler's bearing expertise provides the hardware, while new software capabilities enable advanced algorithms. The convergence of mechanical and digital creates competitive advantages neither pure software nor traditional suppliers can match.

The order book validates the strategy. During the first nine months in 2022, the e-mobility business at Schaeffler totaled an order intake of 4.7 billion euros relating to the E-Mobility business division. While this is global data, Indian operations increasingly contribute through both local contracts and global supply agreements.

The talent transformation proves as important as technology. Recruiting software engineers in Pune means competing with IT giants offering higher salaries and stock options. Schaeffler's proposition differs: work on tangible products that move millions of people, combine software with hardware, see innovations reach production within years not decades. This appeals to engineers seeking impact beyond pure digital products.

Training existing mechanical engineers in software creates hybrid expertise valuable for system integration. A bearing designer who understands control algorithms can optimize hardware-software interaction. A software developer who grasps mechanical constraints writes more robust code. This cross-pollination, happening organically in Indian R&D centers, creates capabilities difficult to replicate.

The localization strategy extends to e-mobility. Rather than importing complete systems, Schaeffler develops local supply chains for electronic components, partners with Indian software firms for non-core modules, and collaborates with academic institutions on battery chemistry and power electronics. This ecosystem approach reduces costs while building strategic flexibility.

Competition intensifies from unexpected directions. Chinese suppliers, dominant in battery cells and power electronics, aggressively enter Indian markets with integrated solutions. Traditional tier-one suppliers like Bosch and Continental expand e-mobility offerings. New entrants from consumer electronics bring different capabilities and cost structures. Schaeffler must simultaneously defend traditional business while competing in new domains.

The investment thesis for e-mobility remains unproven. Will integrated systems command premium pricing, or will commoditization erode margins? Can Schaeffler maintain technology leadership against well-funded competitors? Will Indian OEMs value engineering support, or simply seek lowest-cost suppliers? These questions will determine whether the e-mobility transformation enhances or destroys shareholder value.

As we examine the global parent dynamics next, remember that India's e-mobility journey differs from developed markets. Without legacy automotive infrastructure to protect, India might leapfrog to electric mobility faster than expected. Schaeffler India's ability to serve this transition—providing both advanced technology and frugal innovation—positions it uniquely for whatever future emerges.

VIII. Global Parent Dynamics & The Vitesco Merger

The Schaeffler AG headquarters in Herzogenaurach, October 2024. After years of preparation, legal documentation, and regulatory approvals, a transformative moment arrives: The Schaeffler Group and Vitesco have completed their merger on 1st of October 2024 to become a Leading Motion Technology company. For Schaeffler India, 5,000 miles away, this isn't just corporate maneuvering—it's a fundamental reshaping of strategic possibilities and competitive positioning.

To understand the Vitesco merger's significance, we must first revisit Schaeffler's most audacious and nearly fatal move: the Continental acquisition attempt. In August 2008, the Schaeffler family agreed to a staggered €12 billion acquisition of larger rival Continental AG Germany—a company three times Schaeffler's size. The timing couldn't have been worse. Lehman Brothers collapsed weeks later, credit markets froze, and Schaeffler found itself drowning in debt just as automotive production plummeted globally.

The near-death experience taught valuable lessons. Schaeffler survived through desperate measures: asset sales, emergency refinancing, and Maria-Elisabeth Schaeffler personally guaranteeing loans with family assets. But they also learned strategic patience—rather than immediately flip Continental for cash, they held the stake, influenced strategy, and waited for value creation. By 2020, the Continental stake had appreciated significantly, validating the long-term thesis despite short-term pain.

The Vitesco merger represents evolution from that Continental experience. Rather than hostile acquisition of a larger entity, this was negotiated combination with a complementary business. Vitesco, spun off from Continental in 2021, brought exactly what Schaeffler needed: electronic control units, sensors, and actuators for electrified drivetrains. The combined entity would offer complete powertrain solutions from mechanical components to software—critical for competing in the integrated systems market.

For Schaeffler India, the merger implications cascade across multiple dimensions. First, technology access expands dramatically. Vitesco's electronic expertise combines with Schaeffler's mechanical prowess, enabling truly integrated solutions. An Indian OEM developing an electric vehicle can now source complete e-axle systems including motor, power electronics, transmission, and control software from a single supplier.

Second, customer relationships deepen. Vitesco's contracts with global OEMs complement Schaeffler's existing relationships. When Volkswagen or Stellantis expands Indian operations, the combined entity can offer comprehensive solutions rather than competing for component-level contracts. This systems-level engagement increases switching costs and strategic importance.

Third, scale economics improve. The combined entity's purchasing power reduces raw material costs. Shared R&D investments amortize across larger volumes. Manufacturing footprints optimize—perhaps Vitesco's electronics facility in Pune co-locates with Schaeffler's mechanical operations, reducing logistics costs and enabling tighter integration.

But mergers also create challenges, particularly for distant subsidiaries. Integration complexity multiplies across geographies. Corporate attention focuses on headquarters integration, potentially neglecting regional operations. Cultural differences—Vitesco's electronics DNA versus Schaeffler's mechanical heritage—must reconcile within Indian operations already managing their own integration challenges.

The talent dimension proves particularly complex. Vitesco India engineers, accustomed to Continental's corporate culture and processes, must adapt to Schaeffler's family-owned philosophy. Compensation structures, career paths, and decision-making processes all require harmonization. The risk: talent attrition during integration uncertainty, precisely when combined capabilities are most needed.

Governance structures evolve post-merger. Schaeffler India's reporting lines potentially change as global divisions reorganize. Investment approvals might require additional stakeholders. Transfer pricing between Indian operations and global entities could shift, affecting local profitability. These administrative complexities, while mundane, significantly impact operational efficiency.

The financial implications are substantial. The combined entity's revenue scale and profitability profile change investor perceptions. Schaeffler India might benefit from parent company's enhanced credit rating and capital access. Technology transfer agreements could provide access to Vitesco innovations at favorable terms. Yet integration costs, restructuring charges, and one-time expenses could pressure short-term margins.

Market positioning strengthens but also complicates. The combined entity competes more effectively against mega-suppliers like Bosch and Continental. But it also becomes a larger target for customer pricing pressure and competitive responses. Indian OEMs might worry about over-dependence on a single supplier for critical systems, potentially diversifying sourcing despite integration benefits.

The strategic rationale extends beyond products to capabilities. Vitesco brings software development methodologies, agile processes, and digital-first thinking. Schaeffler contributes deep manufacturing expertise, quality systems, and customer intimacy. The synthesis—if successfully achieved—creates unique competitive advantages in the mechatronic systems that define modern vehicles.

Looking ahead, the merger's success depends on execution across multiple fronts. Product roadmaps must integrate without disrupting ongoing programs. Sales teams need training on expanded portfolios. Manufacturing operations require optimization without compromising quality or delivery. IT systems must merge while maintaining business continuity. Each challenge multiplies across geographies, with India's distance from headquarters adding complexity.

For investors, the merger represents both opportunity and risk. The opportunity: Schaeffler India gains access to technologies and capabilities that would take decades to develop organically. The risk: integration complexity distracts from market opportunities while competitors capitalize on disruption. Historical precedent suggests successful integration takes 3-5 years—a lifetime in rapidly evolving automotive markets.

As we analyze financial performance next, remember that merger synergies materialize slowly while integration costs hit immediately. The patient investor might see transformational value creation. The impatient might see only short-term margin pressure and execution risk. Understanding this temporal mismatch between costs and benefits proves crucial for evaluating Schaeffler India's investment merit through the integration period.

IX. Financial Analysis & Operating Excellence

The CFO's office at Schaeffler India, quarterly earnings day. Analysts dial in from Mumbai, Singapore, London—all seeking to understand how a bearing manufacturer maintains 16% pre-tax margins in an industry where 8-10% is considered healthy. The answer isn't found in any single line item but in the cumulative effect of thousands of operational decisions executed with German precision and Indian frugality.

Revenue for Q3 2024 was Rs. 20,728 million, a 12.1% increase from Q3 2023. Net profit for the quarter was Rs. 2,471 million with an 11.9% margin. These headline numbers tell a story of consistent execution, but the real insights emerge from dissecting the components of profitability.

Start with gross margins, consistently hovering around 35-40%. In a manufacturing business dealing with steel and precision machining, these margins seem almost impossible. The secret: value-based pricing combined with cost engineering. Schaeffler doesn't sell bearings; it sells reliability, engineering support, and total cost of ownership. When a bearing failure can halt an entire production line, customers pay premiums for assured quality.

The sustained quality of earnings reflects our constant focus on cost management and realization of financial and operating margins. This isn't corporate speak—it's operational philosophy embedded across the organization. Every manufacturing cell tracks productivity metrics. Energy consumption per unit produced is monitored real-time. Scrap rates below 0.5% reflect world-class quality systems. These micro-optimizations compound into macro-advantages.

Working capital management deserves special attention. In an industry plagued by extended payment terms and inventory buildup, Schaeffler maintains negative working capital cycles with key customers. How? Strategic importance commands better terms. When you're the sole supplier for critical components, customers prioritize your payments to ensure supply continuity. Inventory turns exceed 12x annually for fast-moving products, though specialized industrial bearings might turn only 2-3x—a deliberate choice balancing service levels with capital efficiency.

The capital allocation framework reflects German conservatism tempered with emerging market pragmatism. Annual capex typically runs 5-7% of sales—enough to maintain competitiveness without over-investing ahead of demand. Growth investments focus on capabilities rather than pure capacity: precision grinding machines that enable tighter tolerances, heat treatment furnaces that improve metallurgy, software systems that enhance design capabilities.

R&D spending patterns reveal strategic priorities. While the global parent invests 6-8% of sales in R&D, Indian operations spend closer to 5%—but the nature differs. Less basic research, more application engineering. Less breakthrough innovation, more incremental improvement. This pragmatic approach suits Indian market needs while leveraging global technology investments.

The tax strategy optimizes legitimate incentives without aggressive planning. Manufacturing operations in SEZs (Special Economic Zones) benefit from tax holidays. R&D spending qualifies for weighted deductions. Export revenues enjoy favorable treatment. The effective tax rate around 25% reflects these benefits while maintaining conservative compliance—critical for a listed subsidiary of a German parent where reputation matters more than marginal tax savings.

Profitability analysis by segment reveals portfolio strength. Automotive OEM business generates 12-15% EBITDA margins through volume leverage and engineering value-add. Industrial bearings command 18-20% margins via specialization and customer stickiness. Aftermarket operations deliver 25%+ margins through brand premium and distribution control. This portfolio balance—growth from automotive, stability from industrial, profitability from aftermarket—creates resilience across cycles.

Cash generation remains robust despite growth investments. Operating cash flow consistently exceeds net income, reflecting low maintenance capex needs and efficient working capital. Free cash flow conversion above 70% funds both dividends and growth without external capital. The balance sheet remains debt-free—not from lack of investment opportunities but from operational excellence generating sufficient internal resources.

Peer comparison illuminates competitive positioning. SKF India, the Swedish competitor, generates similar margins but with higher capital intensity. Timken India offers lower margins despite comparable product quality, suggesting pricing discipline differences. Local competitors like NRB Bearings operate at 8-10% margins, validating Schaeffler's premium positioning. The persistent margin gap reflects genuine competitive advantages, not temporary market distortions.

The return metrics validate capital efficiency. Return on equity consistently exceeds 20%, remarkable for a manufacturing business. Return on capital employed above 25% suggests effective asset utilization. These returns, sustained over market cycles, justify premium valuations despite majority promoter holding and limited float.

Quarterly volatility requires careful interpretation. Automotive OEM revenues fluctuate with production schedules. Industrial sales follow capital expenditure cycles. Export orders bunch around shipping schedules. Smart investors look through this noise to underlying trends: market share gains, mix improvement toward higher-margin products, and operational leverage from scale economies.

The financial resilience was tested during COVID-19 and semiconductor shortages. While revenues declined, margins compressed less than feared. Variable cost structures, flexible manufacturing, and customer support investments paid off. The ability to maintain profitability during disruption validates the business model's robustness.

Looking forward, financial dynamics evolve with market transitions. Electric vehicle components carry different margin profiles than traditional products—initially lower as volumes build, potentially higher as technology content increases. Software and electronics capabilities require different investment patterns than mechanical manufacturing. The financial model must adapt while maintaining return expectations.

The investment paradox emerges clearly: Schaeffler India generates returns that should attract capital, yet the promoter holding limits institutional investment. The stock trades at premium valuations reflecting quality, yet the limited float creates volatility. These contradictions—quality business with structural constraints—define the investment challenge.

As we develop the investment playbook next, remember that financial excellence enables strategic flexibility. The ability to fund growth internally, maintain margins through cycles, and generate cash consistently provides options: aggressive expansion when opportunities emerge, defensive positioning during downturns, or strategic pivots as markets evolve. This financial strength, built over decades of operational discipline, becomes the foundation for future value creation.

X. Playbook: Business & Investing Lessons

Standing in Schaeffler India's Pune facility, watching a bearing take shape from raw steel to finished product, one observes more than manufacturing—it's a masterclass in how German Mittelstand philosophy transplants to emerging markets. The lessons extend beyond industrial companies to any business navigating the intersection of global technology and local markets.

Lesson 1: The Power of Patient Capital in Impatient Markets

Schaeffler's six-decade presence in India reflects a temporal arbitrage. While competitors entered and exited based on quarterly results, Schaeffler invested through License Raj, survived liberalization disruption, and emerged stronger from each crisis. The payoff: customer relationships spanning generations, engineering knowledge accumulated over decades, and manufacturing capabilities that competitors can't quickly replicate.

For investors, this suggests screening for companies with patient capital structures—family ownership, foundation control, or dual-class shares that enable long-term thinking. The market often discounts these structures as "poor governance," but they can enable strategic advantages in industries where time horizons matter more than quarterly earnings.

Lesson 2: Technology Leadership as a Sustainable Moat

Schaeffler doesn't compete on price—Chinese bearings cost 50% less. Instead, they compete on total system performance, engineering support, and failure prevention. A bearing failure might cost 100x the bearing price in downtime. This value proposition—preventing catastrophic failure rather than minimizing component cost—creates pricing power even in commoditized markets.

The broader principle: identify companies whose products represent small costs but prevent large losses. Software security, industrial safety equipment, critical components—these businesses often enjoy pricing power disproportionate to their perceived importance. The key is finding products where switching costs aren't just financial but existential.

Lesson 3: The Mittelstand Model in Emerging Markets

German Mittelstand companies—focused, specialized, often family-owned—dominate global niches through engineering excellence rather than scale or financial engineering. Schaeffler India demonstrates this model's power in emerging markets: combine German precision with local cost structures, maintain quality while adapting to local needs, and build slowly but steadily.

For investors, seek companies exhibiting Mittelstand characteristics: narrow focus but deep expertise, engineering-driven rather than marketing-driven, and organic growth over acquisitive expansion. These businesses often trade at discounts to conglomerates but generate superior returns through cycles.

Lesson 4: Managing Cyclicality Through Portfolio Construction

Schaeffler's three-pillar strategy—automotive OEM for growth, industrial for stability, aftermarket for margins—creates resilience. When automotive production slumps, industrial maintenance continues. When capital expenditure freezes, aftermarket replacement accelerates. This natural hedging reduces earnings volatility without complex financial derivatives.

The investment implication: evaluate companies not just by aggregate metrics but by segment dynamics. A seemingly cyclical business might contain counter-cyclical segments. Understanding these internal hedges helps identify companies with more stable earnings than headlines suggest.

Lesson 5: The Value of Being a Critical Supplier

Schaeffler's products often represent <1% of customer product cost but enable 100% of functionality. This criticality-to-cost ratio creates powerful dynamics: customers can't risk supplier failure, switching costs exceed potential savings, and technical support becomes embedded in customer operations. Once established, these positions become nearly unassailable.

Screen for companies with similar characteristics: small revenue per customer but mission-critical functionality, technical support creating switching costs, and reliability mattering more than price. These businesses often hide in industrial supply chains but generate exceptional returns for patient investors.

Lesson 6: Local Manufacturing as Strategic Asset, Not Just Cost Arbitrage

Schaeffler could import bearings from Germany or China, capturing margins without capital investment. Instead, they built local manufacturing, developed supplier ecosystems, and trained thousands of workers. This wasn't just about cost—it was about responsiveness, customization, and customer intimacy that distant suppliers can't match.

The broader lesson: distinguish between companies using emerging markets for labor arbitrage versus those building genuine local capabilities. The former face constant margin pressure as wages rise; the latter create sustainable competitive advantages that strengthen over time.

Lesson 7: R&D Investment in Emerging Markets

Conventional wisdom suggests R&D belongs in developed markets while emerging markets handle production. Schaeffler India invests 5% of revenue in R&D—not copying global products but solving local problems that become global solutions. Frugal engineering innovations developed for Indian conditions now serve other emerging markets.

For investors, identify companies conducting meaningful R&D in emerging markets, not just localizing global products. These companies often develop innovations that reverse-flow to developed markets, creating unexpected competitive advantages.

Lesson 8: The MNC Subsidiary Paradox

Schaeffler India trades at premium valuations despite majority promoter holding limiting float. This paradox—quality business with structural constraints—creates opportunity for patient investors who can tolerate illiquidity. The premium reflects scarcity value: few MNC subsidiaries combine genuine local manufacturing, consistent governance, and strategic importance to parents.

The investment strategy: build positions slowly during market distress when liquidity providers exit, hold through cycles rather than trade volatility, and focus on business quality over market dynamics. These investments require patience but can generate exceptional returns for those who understand the structural dynamics.

Lesson 9: Capital Allocation in Family-Controlled Public Companies

Schaeffler India balances competing demands: growth investment for market opportunity, dividends for minority shareholders, and support for parent strategy. The resolution—consistent dividend policy, measured growth investment, and transparent communication—builds trust despite structural conflicts.

When evaluating family-controlled companies, assess capital allocation history: consistency matters more than generosity, transparency builds trust over time, and alignment with minority interests indicates governance quality. Companies managing these tensions successfully often provide superior long-term returns despite governance concerns.

Lesson 10: Navigating Technological Disruption as an Incumbent

The shift to electric vehicles threatens Schaeffler's traditional business, yet they're investing aggressively in e-mobility. This isn't denial but pragmatic transformation: leverage existing customer relationships, redeploy manufacturing capabilities, and acquire new competencies while maintaining profitability. The transition will be messy, but the alternative—protecting legacy business while new entrants capture future markets—ensures obsolescence.

For investors, distinguish between companies denying disruption and those navigating it. Look for incumbents investing in new technologies while maintaining current profitability, hiring different talent while retaining core expertise, and cannibalizing existing products before competitors do. These companies face execution risk but offer optionality on successful transformation.

The meta-lesson from Schaeffler India's journey: sustainable competitive advantages emerge from accumulation of small edges rather than single breakthrough innovations. Patient capital, technical excellence, customer intimacy, operational discipline—individually insufficient but collectively formidable. For investors seeking quality companies in emerging markets, these lessons provide a framework for identifying enduring value creators hiding in plain sight among industrial supply chains.

XI. Bear vs. Bull Case & Future Outlook

The investment committee room at a Mumbai mutual fund, 2024. The debate is heated: Is Schaeffler India a secular growth story riding India's manufacturing renaissance, or an expensive cyclical at peak margins facing technological disruption? Both arguments have merit, and the resolution isn't obvious.

The Bull Case: Positioned for India's Manufacturing Ascent

Bulls begin with the structural story. The Indian automotive industry is projected to grow at a CAGR of approximately 10-12% from 2022 to 2027—and Schaeffler captures value across this growth. Every new vehicle production line, every capacity expansion, every model launch requires Schaeffler's components. The company isn't betting on specific OEMs or vehicle types but on mobility itself.

The technology transition accelerates the opportunity. While bears see EV disruption, bulls see transformation potential. Schaeffler's e-axle production, software capabilities, and mechatronic expertise position them for higher value capture per vehicle even as component counts decline. The Shoolagiri facility expansion reflects the company's strategy to meet growing demand in India's automotive sector, particularly as the industry transitions toward electrification and hybrid technologies—infrastructure investments that competitors can't easily replicate.

Global parent support provides unmatched advantages. Technology transfer accelerates Indian product development. Global customer relationships facilitate local contract wins. The Vitesco merger expands addressable markets from mechanical components to complete electronic systems. Few Indian suppliers can match this combination of local manufacturing and global technology access.

The financial profile supports premium valuations. Debt-free balance sheet provides flexibility for growth investment or acquisitions. ROE exceeding 20% demonstrates efficient capital deployment. Consistent dividend payments validate governance despite promoter control. These aren't temporary achievements but structural advantages built over decades.

Market share gains continue despite competition. Chinese suppliers offer lower prices but can't match engineering support. Local competitors lack technology depth. Global peers have technology but higher cost structures. Schaeffler sits at the sweet spot—global quality at local costs with customer relationships spanning decades.

The industrial and aftermarket segments provide ballast. Even if automotive faces headwinds, industrial modernization continues. India's infrastructure buildout—railways, power, steel—requires sophisticated bearings. The aftermarket grows with vehicle parc expansion. These segments generate higher margins and more stable revenues than automotive OEM.

ESG considerations increasingly favor established players. Customers demand supply chain transparency, environmental compliance, and social responsibility—areas where Schaeffler's German heritage and established processes provide advantages over emerging competitors. The company's 2030 carbon neutrality commitment resonates with global customers mandating sustainable suppliers.

Valuation remains reasonable relative to quality. While absolute P/E seems high, adjusting for capital efficiency, growth prospects, and business quality suggests fair value. Premium MNC subsidiaries in India consistently trade at elevated multiples—reflecting scarcity value and governance premium in markets where both remain rare.

The Bear Case: Peak Margins Facing Structural Headwinds

Bears counter with sobering realities. Current margins are unsustainably high—16% pre-tax in a manufacturing business facing increasing competition. Chinese suppliers improve quality while maintaining cost advantages. Local competitors develop capabilities through partnerships and acquisitions. Margin compression seems inevitable as competition intensifies.

The EV transition threatens more than acknowledged. Electric vehicles require 90% fewer moving parts than internal combustion engines. Many traditional components become obsolete. While Schaeffler invests in e-mobility, success isn't guaranteed. Pure-play EV component suppliers might capture this market, leaving traditional suppliers with stranded assets.

Automotive cyclicality looms large. Indian passenger vehicle sales remain below 2018 peaks despite population growth. Commercial vehicle cycles prove even more volatile. High inventory levels suggest production cuts ahead. Schaeffler's operating leverage—a strength during growth—becomes liability during downturns.

Technology disruption extends beyond electrification. Autonomous vehicles might reduce private ownership. Shared mobility could decrease vehicle production. Software-defined vehicles shift value from hardware to code. Schaeffler's mechanical heritage becomes disadvantage in digitized future.

Competition from unexpected directions intensifies. Consumer electronics companies enter automotive with different capabilities and cost structures. Battery manufacturers integrate forward into complete systems. Software companies partner directly with OEMs, bypassing traditional suppliers. The competitive landscape shifts faster than established players can adapt.

Promoter control limits upside. With 74.13% holding, minority shareholders have limited influence on capital allocation. The parent might prioritize global strategy over local optimization. Transfer pricing could shift profits to other geographies. These structural issues cap valuation regardless of operational performance.

Limited float creates liquidity risks. Daily trading volumes often represent <0.1% of market cap. Institutional investors struggle to build meaningful positions. Market dislocations could trigger severe price volatility. The stock might trade well below intrinsic value during risk-off periods when liquidity evaporates.

China risks multiply across dimensions. Chinese competitors improve capabilities through state support and scale advantages. Global supply chains shift away from China, potentially disrupting Schaeffler's sourcing. Geopolitical tensions could affect technology transfer and market access. These risks are difficult to quantify but potentially severe.

Customer concentration creates vulnerability. Top 10 customers likely represent >50% of revenues. Loss of single major account would significantly impact profitability. OEMs increasingly demand price reductions, longer payment terms, and development cost sharing. Supplier power diminishes as customers consolidate.

Execution risks around transformation remain substantial. Software development requires different capabilities than mechanical engineering. Attracting technology talent proves challenging given competition from IT services. Integration complexity from Vitesco merger could distract from market opportunities. Transformation success is aspiration, not achievement.

Future Outlook: Navigating Complexity

The reality likely lies between extremes. Schaeffler India will probably maintain above-average margins through differentiation while facing gradual compression from competition. The EV transition will destroy some value while creating new opportunities. Market share might remain stable in traditional products while growing in new categories.

Key monitorables for investors include: margin trajectory as competition intensifies, success in winning e-mobility contracts, industrial segment growth offsetting automotive volatility, and capital allocation balancing growth with shareholder returns.

The investment decision ultimately depends on time horizon and risk tolerance. Short-term investors face cyclical headwinds and valuation risks. Long-term investors might benefit from structural growth and transformation optionality. The business quality is undeniable; the price paid for that quality determines returns.

For fundamental investors seeking quality companies with sustainable competitive advantages, Schaeffler India merits consideration despite challenges. For value investors requiring margin of safety, current valuations might prove prohibitive. For growth investors betting on India's manufacturing story, Schaeffler provides leveraged exposure with proven execution.

The meta-question transcends Schaeffler: Can established industrial companies successfully navigate technological disruption while maintaining profitability? History suggests few succeed, but those that do generate exceptional returns. Schaeffler India's transformation journey—from bearings to batteries, mechanical to mechatronic—becomes a case study in industrial evolution. Whether it becomes a cautionary tale or success story remains to be written.

XII. Epilogue & Reflections

The story of Schaeffler India is, at its core, a meditation on value creation through patience, precision, and adaptation. From post-war German workshops to Indian factory floors, from mechanical bearings to intelligent e-mobility systems, the journey spans technological revolutions and economic transformations while maintaining a consistent thread: the pursuit of engineering excellence.

What makes Schaeffler India particularly instructive for students of business is how it challenges conventional narratives. This isn't a story of disruption but of evolution. Not of venture-backed hypergrowth but of patient capital compound returns. Not of winner-take-all dynamics but of specialized excellence in industrial niches. In an era obsessed with software eating the world, Schaeffler reminds us that physical products—the bearings that enable motion, the components that transfer power—remain indispensable.

The company embodies the paradox of being both invisible and essential. Consumers never see Schaeffler's products, yet they depend on them every time they drive, board a train, or use electricity. This invisibility is both weakness—limiting brand value and pricing power—and strength—creating switching costs and customer dependency that pure brands can't match.

The transformation from component supplier to systems integrator represents more than product evolution—it's a fundamental shift in value creation. When Schaeffler provides not just bearings but complete e-axle systems with embedded software, they capture more value while becoming harder to replace. This progression—from products to solutions to outcomes—defines successful industrial companies navigating technological change.

For India, Schaeffler represents both achievement and aspiration. Achievement in building world-class manufacturing capabilities, developing engineering talent, and competing globally from an emerging market base. Aspiration in the continued journey toward innovation leadership, technology development, and value chain progression. The company's evolution mirrors India's own manufacturing ambitions.

The governance structure—German family control with Indian minority shareholders—creates unique dynamics. It enables long-term thinking while demanding short-term performance. It provides technology access while requiring local value creation. It offers stability while limiting influence. These tensions, managed successfully over decades, demonstrate that governance perfection matters less than consistent execution.

The electric vehicle transition becomes a litmus test for industrial transformation. Can companies with century-old mechanical heritage develop software capabilities? Will customer relationships built on engine components transfer to battery systems? Does manufacturing excellence translate to electronic assembly? Schaeffler's answers to these questions will influence not just their future but provide lessons for entire industries facing similar disruptions.

The investment implications extend beyond Schaeffler to broader themes. Quality manufacturing companies in emerging markets often trade at discounts despite superior growth and returns. Patient capital structured appropriately can generate exceptional returns despite liquidity constraints. Technology transitions create opportunities for prepared incumbents, not just disruptive entrants.

Looking forward, Schaeffler India's trajectory depends on multiple variables: India's manufacturing competitiveness, global supply chain evolution, technology transition pace, and competitive dynamics. But the company's history suggests adaptive capacity—the ability to navigate License Raj and liberalization, financial crisis and recovery, technological disruption and transformation.

The human dimension deserves final reflection. Behind every precision bearing lies an apprentice learning to read micrometers, an engineer solving thermal expansion problems, a supervisor ensuring quality standards. Schaeffler India employs thousands who've built careers turning steel into components that move nations. Their accumulated expertise—tacit knowledge that can't be digitized or outsourced—remains the company's true competitive advantage.

Software might eat the world, but the world still runs on bearings. Electric vehicles need them. Wind turbines depend on them. Robots require them. As long as physical objects move, companies like Schaeffler will engineer that motion. The components might evolve from mechanical to mechatronic, from hardware to software-defined, but the fundamental value proposition—enabling reliable, efficient motion—endures.

For investors, Schaeffler India offers a case study in finding quality businesses in unexpected places. Not in glamorous technology companies or consumer brands, but in industrial supply chains where engineering excellence, customer relationships, and operational discipline create sustainable competitive advantages. These businesses might not capture headlines, but they capture value—steadily, consistently, compoundingly.

The Schaeffler story continues to unfold. New chapters on sustainability, digitalization, and emerging mobility models await. Whether the company maintains its trajectory through these transitions remains uncertain. But the principles underlying their success—patient capital, technical excellence, customer focus, operational discipline—provide guideposts for navigating uncertainty.

In conclusion, Schaeffler India represents more than an investment opportunity—it's a template for industrial value creation in emerging markets. The company's journey from post-war reconstruction to e-mobility transformation, from German workshops to Indian factories, from family enterprise to public company, illuminates pathways for businesses navigating technological disruption while maintaining profitability.

The ultimate lesson might be this: In a world accelerating toward digital abstraction, physical engineering still matters. In markets obsessed with disruption, evolution often wins. In industries facing transformation, prepared incumbents can successfully adapt. Schaeffler India embodies these principles, creating value for stakeholders while enabling the motion that moves modern society.

The bearings keep turning. The engineering continues. The transformation proceeds. And for those paying attention, the lessons accumulate—small, precise, and ultimately powerful, much like the products Schaeffler has manufactured for over seven decades.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube