Jabil: The Manufacturing Giant Behind Your Technology

I. Introduction & Episode Roadmap

Picture this: You wake up, check your iPhone, drive your Tesla to work, use medical devices at your doctor's appointment, and come home to game on your PlayStation. What you don't realize is that a single company likely had its hands in manufacturing critical components for every single one of those products. That company is Jabil—a $28.9 billion revenue giant that's somehow remained invisible to most consumers despite being absolutely everywhere.

The paradox is striking. Jabil touches nearly every aspect of modern technology—from the circuit boards in your smartphone to the sophisticated electronics in your car's ADAS system, from medical devices that save lives to the servers powering AI datacenters. Yet walk down any street and ask people about Jabil, and you'll get blank stares. This anonymity isn't a bug; it's a feature of their business model.

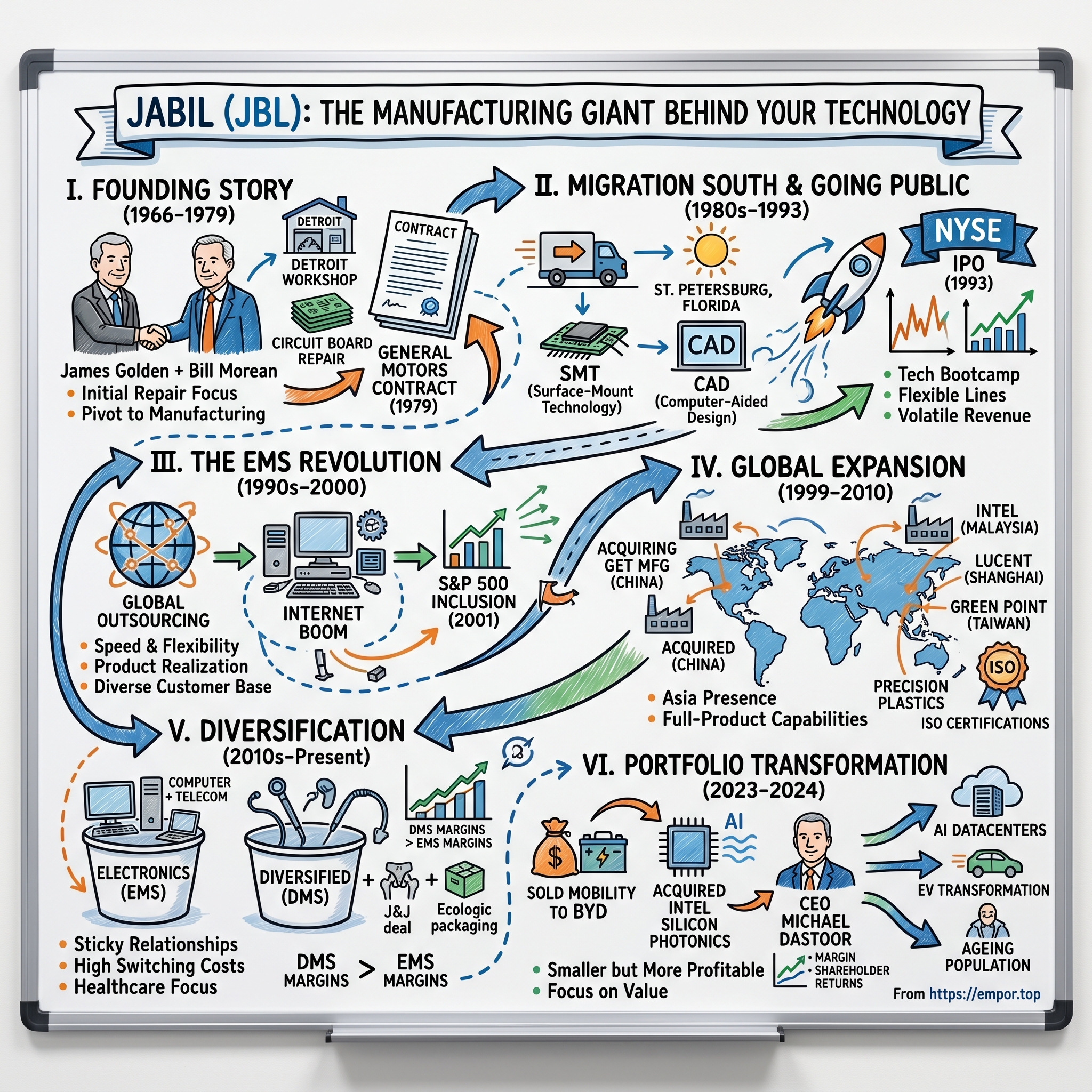

Founded in 1966 in a modest Detroit workshop, Jabil began as exactly what its name suggests: a portmanteau of its founders' first names—James Golden and Bill Morean. What started as a small circuit board repair shop servicing Control Data Systems has evolved into one of the world's three largest electronics manufacturing services (EMS) providers, with 138,000 employees across 100 locations in 30 countries.

The central question that drives this story isn't just how a repair shop became a manufacturing colossus—it's how Jabil built a business model so essential yet so invisible, so massive yet so nimble, so dependent on others' innovations yet so innovative itself. This is the story of American manufacturing that actually survived and thrived through globalization, a tale of strategic pivots that would make any MBA professor weep with joy, and ultimately, a masterclass in building indispensable infrastructure for the modern economy.

What makes Jabil particularly fascinating for investors is its recent transformation. After decades of riding the electronics outsourcing wave, the company is actively reshaping its portfolio—divesting legacy businesses like mobility manufacturing to BYD, acquiring strategic assets like Intel's silicon photonics operations, and positioning itself at the intersection of the economy's most powerful secular trends: AI infrastructure, electric vehicles, and healthcare technology.

II. The Founding Story: JAmes + BILL = Jabil (1966-1979)

The year was 1966. The Vietnam War dominated headlines, the Beatles had just released "Revolver," and in Detroit—still the undisputed capital of American manufacturing—two men pooled together $5,000 to start something that seemed almost quaint: an electronics repair shop. James Golden and William "Bill" E. Morean weren't trying to revolutionize manufacturing. They just wanted to fix circuit boards.

Their timing, whether by luck or intuition, was impeccable. The automotive industry, Detroit's lifeblood, was beginning its first tentative experiments with electronics. While cars were still fundamentally mechanical beasts, the seeds of electronic control systems were being planted. Jabil's first customers weren't Silicon Valley startups (Silicon Valley barely existed as we know it)—they were automotive OEMs, the giants of Detroit who needed someone to repair and maintain the primitive electronic components creeping into their supply chains.

The partnership between Golden and Morean was complementary but ultimately unsustainable. Golden was the technical mind, understanding circuits and components with an engineer's precision. Morean brought business acumen and an entrepreneur's hunger for growth. For over a decade, they built a steady, profitable business fixing what others had built. But by the late 1970s, tensions emerged about the company's direction. Golden was content with the repair business—stable, predictable, profitable. Morean saw bigger opportunities.

The resolution came through a buyout that would prove pivotal. Golden exited the business, taking his share of a company that was generating steady but unspectacular returns. Bill Morean, now sole owner, immediately brought in fresh blood—his son, William D. Morean (known as "Bill Jr." though he'd later drop the suffix). The younger Morean didn't just join the family business; he transformed it.

Where others saw Jabil as a repair shop, Bill Jr. saw a manufacturing platform waiting to be built. He began pursuing new contracts, not for repair work but for actual production. His philosophy was simple but radical for the time: why just fix other people's boards when you could build them better in the first place?

The inflection point came in 1979 with a contract that would define Jabil's trajectory for decades. General Motors, the undisputed king of American manufacturing, needed a partner for high-volume circuit board production. This wasn't repair work—this was real manufacturing, automated assembly lines, quality control at scale. The GM contract forced Jabil to evolve from craftsmen to industrialists.

The transformation was brutal. Jabil had to invest in automated equipment, develop quality systems that could meet GM's exacting standards, and scale from dozens of employees to hundreds. The younger Morean mortgaged everything, convinced that this was the future. He was betting that electronics would eat the world, starting with cars, and that companies would increasingly outsource non-core manufacturing.

By the end of 1979, Jabil had crossed a critical threshold. Revenue had jumped from low millions to approaching $10 million annually. More importantly, they'd proven they could handle high-volume, high-quality manufacturing for the world's most demanding customers. The repair shop was dead; a manufacturing services company was born.

What the Moreans understood—and what would drive Jabil's strategy for the next four decades—was that successful manufacturing wasn't about the lowest cost or the fanciest technology. It was about trust. When GM handed over circuit board production to Jabil, they weren't just outsourcing a commodity; they were entrusting a critical component of their vehicles to an outside partner. That trust, once earned, created switching costs that went far beyond price.

As the 1970s ended, Jabil stood at a crossroads. They could remain a regional player serving Detroit's automotive industry, or they could think bigger. The younger Morean, now firmly in control, chose bigger. But first, they'd need to leave Detroit behind.

III. The Migration South & Going Public (1980s-1993)

In 1982, Bill Morean made a decision that seemed almost treasonous to Detroit's manufacturing establishment: he packed up Jabil's headquarters and moved to St. Petersburg, Florida. While executives tried to spin it as a strategic move for lower costs and better weather, employees knew the truth—Morean had fallen in love with Florida's Gulf Coast during a vacation and decided that's where he wanted to build his empire.

The move was more transformative than anyone anticipated. In Detroit, Jabil was just another supplier in an ecosystem dominated by automotive giants. In St. Petersburg, they were pioneers, bringing high-tech manufacturing to a region better known for beaches and retirees. The psychological shift was profound—freed from Detroit's hierarchies and traditions, Jabil could reinvent itself.

The early 1980s became Jabil's technology bootcamp. In 1981, they launched independent test engineering services, essentially offering to be the quality control department for companies that didn't want to build their own. A year later, they began volume production with surface-mount technology (SMT)—a revolution in circuit board assembly that allowed components to be mounted directly onto boards rather than through holes. While competitors debated whether SMT was a fad, Jabil went all-in.

By 1984, Jabil had implemented computer-aided design services, allowing customers to send designs electronically rather than through physical blueprints. This seems quaint now, but it was revolutionary then—Jabil could iterate on designs in days rather than weeks, collapsing development cycles. The next year, they achieved highly automated volume production using SMT processes, with machines placing components at speeds human hands could never match.

The late 1980s brought a lesson in the volatility that would forever mark the EMS industry. Fiscal 1988 was a banner year—$96 million in sales, $3.8 million in profit, margins that made other manufacturers envious. Management celebrated, expanded capacity, hired aggressively. Then 1989 hit like a sledgehammer: sales jumped to $135 million, but profits cratered to just $694,000. The culprit? Price wars as competitors flooded into electronics manufacturing, combined with customers demanding ever-lower prices.

The rollercoaster continued into the 1990s. Revenue in 1990 actually declined to $124 million—imagine explaining that to investors today—while profits limped along at $1 million. Jabil was learning a harsh truth about contract manufacturing: you lived and died by your customers' fortunes, and when they struggled, you bled.

But 1991 brought redemption and revealed Jabil's resilience. Revenue exploded to $233 million with profits of $10.3 million. What changed? The Gulf War had created massive demand for military electronics, and Jabil's reputation for quality made them a trusted supplier for defense contractors. When national security was on the line, nobody wanted the cheapest manufacturer—they wanted the best.

The whiplash continued in 1992 as military spending cooled and revenue fell to $173 million. But something had fundamentally changed in how Morean and his team thought about the business. They stopped trying to smooth out the cycles and instead built a company that could thrive on volatility. Flexible manufacturing lines that could switch between products, a diverse customer base across industries, and a balance sheet strong enough to survive the lean years while competitors failed.

This philosophy would be tested as Jabil prepared for its most ambitious move yet. In April 1993, they filed to go public on the New York Stock Exchange. The IPO roadshow was a masterclass in managing expectations. When investors asked about the revenue volatility, Morean didn't hide it—he embraced it. "We're building the manufacturing platform for the electronics age," he told skeptics. "It's going to be bumpy, but the secular trend is unstoppable."

The market agreed. Jabil went public at $11 per share, raising capital that would fuel its next phase of growth. But more importantly, going public forced disciplines that would serve them well: quarterly reporting that demanded operational excellence, investor scrutiny that prevented complacency, and access to capital markets that would enable the acquisition spree to come. As the 1990s began, Jabil was a public company with ambitions that far exceeded its Florida headquarters. The world was about to enter the great outsourcing revolution, and Jabil had positioned itself perfectly to ride the wave. They just needed to figure out how to serve customers who weren't in Detroit or even America—customers whose names they couldn't yet pronounce but whose business would transform them from a regional player into a global giant.

IV. The EMS Revolution: Riding the Outsourcing Wave (1990s-2000)

The Berlin Wall had fallen, China was opening up, and corporate America was having an epiphany: why own factories when you could rent someone else's expertise? This wasn't just about cost-cutting—though that mattered. It was about speed, flexibility, and focus. OEMs realized they could accelerate time-to-market, access cutting-edge manufacturing tech without capital investment, leverage someone else's purchasing power, and most importantly, focus on what actually differentiated them: design and marketing.

For Jabil, this shift was like watching the entire ocean suddenly flow in their direction. By the mid-1990s, the company had evolved far beyond simple board assembly. They offered complete product realization—from prototype to production, from single boards to complete systems. When a Silicon Valley startup needed to go from napkin sketch to shipping product in six months, Jabil could make it happen.

The Internet boom turbocharged everything. Jabil's IPO on April 29, 1993 now looked prescient. By 1995, tech companies were growing so fast they couldn't possibly build manufacturing capacity quickly enough. Jabil's customer mix tells the story: by the late 1990s, some 20% of revenues came from Internet equipment suppliers like Chipcom and Compression Labs, up from just 8% in 1995.

Think about what this meant operationally. Jabil was simultaneously managing production for mature automotive customers with 18-month product cycles and Internet startups whose entire business model might pivot quarterly. They had to be both tortoise and hare, maintaining automotive-grade quality while moving at Internet speed.

The company's response was to build redundancy and flexibility into everything. In 1997, they completed a new 120,000-square-foot facility in St. Petersburg—not to replace existing capacity but to complement it. The philosophy was simple: every customer should have a backup facility, every product line should have alternate sources, every process should have a Plan B.

This paranoid redundancy proved brilliant when the Internet bubble began showing cracks in 2000. While pure-play Internet manufacturers collapsed as their customers evaporated, Jabil's diverse base—automotive, medical, industrial—kept the lights on. Revenue actually grew through the dot-com crash, a feat that seemed impossible for a company with such Internet exposure.

The ultimate validation came in 2001 when Jabil was added to the S&P 500 Index. This wasn't just a symbolic achievement. S&P inclusion meant index funds had to buy the stock, analyst coverage expanded, and Jabil joined the ranks of American corporate blue chips. For a company that started as a repair shop, it was the equivalent of getting inducted into the Hall of Fame.

But even as Wall Street celebrated, Jabil's management knew the easy growth was ending. The Internet boom had pulled forward years of demand. Competitors were flooding into EMS, commoditizing basic assembly. Labor costs in America were becoming untenable for high-volume production. If Jabil wanted to maintain its growth trajectory, it needed to go where the customers were going: Asia.

V. Strategic Acquisitions & Global Expansion (1999-2010)

In 1999, while Americans worried about Y2K and tech stocks hit stratospheric valuations, Jabil made a move that would define its next decade: acquiring GET Manufacturing in China. This wasn't just opening an office or building a factory—it was buying an established operation with relationships, permits, and most crucially, understanding of how business actually worked in China.

The timing was perfect and terrible simultaneously. Perfect because every Western company was racing to establish Chinese manufacturing. Terrible because Jabil was walking into a market where labor costs were 1/20th of Florida's, where intellectual property was treated as a suggestion, and where government relationships mattered more than quarterly earnings.

But Jabil had an insight that many competitors missed: China wasn't just about cheap labor. It was about being where the entire supply chain was migrating. When your resistor supplier, your plastic molder, and your cable assembler are all within a 50-mile radius, magic happens. Lead times collapse, iterations accelerate, costs plummet not just from labor but from logistics.

The acquisition engine kicked into overdrive. In 2001, Jabil bought Intel's Malaysian manufacturing facility—Intel, the company that practically invented modern semiconductors, was admitting that manufacturing wasn't their core competency. A year later, Jabil acquired a Lucent Technologies factory in Shanghai and Philips' contract manufacturing services. Each acquisition wasn't just about capacity; it was about customer relationships, technical capabilities, and geographic footprint.

The 2005 acquisition of Varian's electronics manufacturing business for $195 million showcased Jabil's evolution. Varian made sophisticated medical and scientific equipment—products where a manufacturing defect could literally kill someone. By acquiring and successfully integrating Varian's operations, Jabil signaled they could handle the most demanding, regulated manufacturing challenges.

The crown jewel came in 2006: Green Point, acquired for $881 million through Jabil's Taiwanese subsidiary. Green Point wasn't just another Asian manufacturer—they were the kings of precision plastic and metal work, making the gorgeous enclosures for products like Apple's iPod. This acquisition gave Jabil capabilities far beyond electronics; they could now manufacture the entire product, from the circuit board to the sleek exterior that consumers actually touched.

By 2002, Jabil had crossed $3.5 billion in revenue. By 2010, that number had nearly quadrupled to $13.4 billion. But the real achievement wasn't growth—it was quality. Jabil achieved Global ISO 9001 and ISO 14001 certification, essentially proving they could maintain consistent quality whether manufacturing in Malaysia, Mexico, or Michigan.

The financial crisis of 2008-2009 tested everything. Customers canceled orders, credit markets froze, and several competitors went bankrupt. Jabil not only survived but used the crisis to consolidate. They acquired distressed assets at fire-sale prices, hired talent from failing competitors, and emerged from the recession with greater market share than they entered with.

By 2010, Jabil had transformed from an American company with international operations to a truly global platform. They could tell a customer: "We can build your product in China for Asia, Mexico for the Americas, and Eastern Europe for EMEA. We can shift production between facilities based on tariffs, currency, or customer preference. We're not just your manufacturer; we're your supply chain strategy."

VI. Diversification Beyond Electronics (2010s-Present)

The smartphone wars of the early 2010s taught Jabil a painful lesson. They'd become incredibly successful at manufacturing mobile devices, but success in consumer electronics was a double-edged sword. Product lifecycles were measured in months, margins were razor-thin, and customer concentration was dangerous—lose one major phone manufacturer and billions in revenue evaporated overnight.

The strategic response was bold: if electronic manufacturing was becoming commoditized, Jabil would become something more. They would apply their manufacturing expertise to industries where switching costs were higher, margins were better, and relationships were stickier.

Healthcare became the spearhead of this transformation. In 2018, Jabil made a move that raised eyebrows across the industry: acquiring Johnson & Johnson's medical device manufacturing business. This wasn't just buying factories—it was acquiring FDA-certified facilities, quality systems that had been refined over decades, and expertise in manufacturing products where failure meant lawsuits, not just returns.

The J&J deal included 14 manufacturing sites globally, covering everything from endoscopy equipment to surgical instruments, spinal implants to trauma devices. Overnight, Jabil became one of the largest medical device manufacturers nobody had heard of. They were now making products that surgeons used to save lives, a far cry from assembling circuit boards for routers.

The transformation accelerated in 2015 with two acquisitions that seemed to come from left field. First, Shemer Group, an Israeli metal fabrication company specializing in high-tech capital equipment. Then Plasticos Castella, a Spanish packaging manufacturer. What did metal fabrication and food packaging have to do with electronics? Everything, if you understood Jabil's strategy: they were building manufacturing capabilities that transcended any single industry.

The 2021 acquisition of Ecologic Brands pushed even further into sustainability and packaging. Ecologic made eco-friendly packaging from recycled materials—about as far from circuit boards as you could get. But the underlying competency was the same: precision manufacturing at scale, supply chain management, quality control.

By the early 2020s, Jabil had reorganized into two distinct segments that reflected this evolution. The Electronics Manufacturing Services (EMS) segment remained focused on traditional strengths—computer components, telecom equipment, consumer electronics. But the Diversified Manufacturing Services (DMS) segment was the growth story, encompassing healthcare, packaging, automotive, and industrial products.

The numbers validated the strategy. DMS margins consistently exceeded EMS margins, sometimes by 200 basis points or more. Customer relationships in DMS were measured in decades, not quarters. And perhaps most importantly, DMS gave Jabil resilience—when semiconductor shortages crushed electronics manufacturing in 2021, healthcare and packaging picked up the slack.

VII. The Portfolio Transformation & Leadership Change (2023-2024)

August 2023 marked a watershed moment in Jabil's history. The company announced it was selling its mobility business in China to BYD, the electric vehicle giant that had quietly become one of the world's largest manufacturers. The sale price wasn't the headline—though the pre-tax gain of $942 million was substantial. The real story was what it represented: Jabil walking away from billions in revenue to focus on higher-margin, more strategic businesses.

The mobility business had been Jabil's gateway into consumer electronics, manufacturing components for virtually every major smartphone brand. But it had become an albatross—massive revenue, minimal margins, and concentration risk that kept executives awake at night. Selling to BYD wasn't surrender; it was strategic pruning.

Then came April 2024, bringing corporate drama worthy of a Netflix series. CEO Kenny Wilson, who had led the company since 2013, was suddenly placed on paid leave pending an investigation. The carefully worded press release stressed this wasn't about financial statements or accounting—coded language that usually means personal conduct. The board moved swiftly, appointing CFO Michael Dastoor as interim CEO.

The investigation's details never became public, but the resolution was decisive. Wilson resigned, and Dastoor was named permanent CEO. For a company that prided itself on operational excellence and staying out of headlines, it was a jarring moment. Yet the transition proved remarkably smooth—evidence of Jabil's institutional strength beyond any single leader.

Dastoor wasted no time establishing his vision. Where Wilson had been willing to chase revenue at almost any margin, Dastoor was ruthlessly focused on profitability. His first earnings call as permanent CEO was a masterclass in expectation setting: Jabil would be smaller but more profitable, less diverse but more focused, less exciting but more predictable.

The November 2023 acquisition of Intel's Silicon Photonics business exemplified the new strategy. Silicon photonics—using light instead of electrons to transmit data—was exactly the kind of high-tech, high-margin manufacturing Dastoor wanted. As AI datacenters demanded ever-faster interconnects, silicon photonics was moving from science experiment to commercial necessity.

Under Dastoor's leadership, Jabil's capital allocation became increasingly shareholder-friendly. The company returned $2.5 billion to shareholders via buybacks in FY24 and announced another $1 billion authorization. The message was clear: Jabil would only invest in businesses that met strict return thresholds. Everything else would go back to shareholders.

VIII. Business Model & Manufacturing Excellence

Step inside a Jabil facility and you enter a world that seems almost contradictory. Half the floor might be producing medical devices in clean rooms where workers wear bunny suits and a single particle of dust could ruin a batch. The other half might be churning out automotive components on lines that run 24/7, where speed and cost are everything. This isn't schizophrenia—it's the parallel production strategy that makes Jabil unique.

The parallel global production model is elegant in its complexity. Jabil can manufacture the same product in multiple facilities across different continents simultaneously. This isn't just redundancy—it's optionality. When Trump imposed tariffs on Chinese goods, Jabil shifted production to Mexico and Vietnam almost seamlessly. When COVID shut down Malaysian facilities, capacity in Eastern Europe ramped up. Customers barely noticed the disruption.

This flexibility comes from standardization that borders on obsession. Every Jabil facility uses the same equipment, same processes, same quality systems. An engineer in Shanghai can video-call a colleague in Guadalajara and they're literally looking at identical production lines. This standardization enables Jabil's secret weapon: they can quote a new project and be in production faster than competitors because they're not reinventing the wheel—they're just deploying a proven template.

The business model is deceptively simple: Jabil maintains long-term relationships with leading companies that benefit from highly automated, continuous flow manufacturing. But the execution is anything but simple. With operations in over 100 locations across 30 countries and approximately 138,000 employees, Jabil manages complexity that would break most organizations.

Customer concentration remains both Jabil's strength and achilles heel. Their top customers—names they rarely disclose but which industry insiders know include Apple, HP, and Johnson & Johnson—represent massive portions of revenue. Losing any one of them would be catastrophic. But this concentration also creates deep integration. Jabil engineers sit in customer facilities, participate in product design, and essentially become an extension of the customer's organization.

The manufacturing-as-a-service model has evolved far beyond simple assembly. Jabil now offers concurrent engineering, where they help design products for manufacturability. They manage entire supply chains, leveraging purchasing power that individual customers could never achieve. They handle aftermarket service, managing warranty repairs and upgrades. For many customers, Jabil isn't just a supplier—they're the entire operations department.

IX. Financials & Performance Analysis

The numbers tell a story of transformation, not just growth. FY24's net revenue of $28.9 billion was actually down from previous years—and management celebrated. Why? Because core margins hit 5.5% and core diluted EPS reached $8.49, levels that would have seemed impossible during the mobility-dominated era.

The margin expansion story is particularly compelling. In the early 2010s, when mobility revenue was peaking, Jabil's operating margins often struggled to exceed 3%. Today, even after divesting billions in revenue, margins are approaching 6%. This isn't financial engineering—it's portfolio transformation. Every percentage point of margin on a $27+ billion revenue base represents $270 million in operating income.

Cash generation has become a hallmark of the Dastoor era. FY24 generated more than $1 billion in adjusted free cash flow, remarkable for a capital-intensive manufacturing business. This cash generation enables the aggressive shareholder returns that have made Jabil a favorite among value investors. The $2.5 billion returned to shareholders in FY24 wasn't a one-time windfall from the mobility sale—it reflected sustainable cash generation.

Looking to FY25, management forecasts $27.0 billion in net revenue, a core operating margin of 5.4%, and core diluted EPS of $8.65. The stability of these projections—revenue roughly flat, margins stable, EPS growing modestly—might seem boring. But for a company that historically rode violent cycles, boring is beautiful.

The competitive positioning data point is telling: Jabil has grown into the world's third-largest EMS by revenue. Only Foxconn and Flex are larger, and both are more concentrated in consumer electronics. Jabil's diversification into healthcare, automotive, and industrial gives it a resilience its larger peers lack.

Capital allocation under Dastoor has become increasingly disciplined. The new $1 billion share repurchase authorization signals confidence, but more importantly, it reflects a framework: if Jabil can't find acquisitions that meet return hurdles, they'll return capital to shareholders rather than empire-build.

X. Future Growth Vectors & Strategic Positioning

The AI datacenter boom isn't just another tech cycle for Jabil—it's a generational opportunity that plays to every strength they've built over six decades. The company's Intelligent Infrastructure segment, led by Matt Crowley, has been architected specifically for this moment. From cloud to datacenter to the networking gear that connects them, Jabil touches every layer of AI infrastructure.

Consider what building an AI datacenter actually requires: sophisticated cooling systems to manage heat from thousands of GPUs, power management systems that can handle megawatts of electricity, optical interconnects that move data at light speed, and the physical infrastructure to house it all. Jabil manufactures components for every single one of these systems. When Nvidia needs someone to manufacture cooling systems for their DGX servers, they call Jabil. When hyperscalers need custom power distribution units, they call Jabil.

The automotive transformation presents another multi-decade growth vector. Every year, Jabil adds new automotive OEM customers, building a portfolio that now spans traditional manufacturers pivoting to EVs and new entrants trying to disrupt transportation. The content per vehicle opportunity is staggering—a modern EV contains 10x the electronic content of a traditional car, from battery management systems to ADAS sensors to infotainment systems.

The geographic diversification strategy has proven prescient given geopolitical tensions. While Jabil benefits from 44 million square feet of facility space in China, they're far from dependent on it. Manufacturing presence in 29 countries means Jabil can play geopolitical arbitrage—when US-China tensions rise, they shift production to Vietnam or Mexico. When Brexit complicates UK manufacturing, Eastern European facilities pick up slack.

The healthcare secular trend might be the most underappreciated growth driver. As populations age globally, demand for medical devices explodes. As procedures move from hospitals to outpatient settings, devices need to become more sophisticated yet more portable. As precision medicine advances, manufacturing requirements become more complex. Jabil is positioned at the intersection of all these trends.

The warehouse automation opportunity emerged from the e-commerce boom but has legs far beyond it. As labor shortages persist and same-day delivery becomes table stakes, warehouses are transforming from storage facilities to high-tech production environments. Jabil manufactures the robots, conveyor systems, and control systems that power this transformation.

XI. Playbook: Key Lessons & Analysis

The power of being industry-agnostic while maintaining deep expertise is Jabil's core paradox and greatest strength. They can manufacture pacemakers and printer cartridges, satellite components and soda packaging. This isn't jack-of-all-trades dilettantism—it's recognizing that manufacturing excellence transcends industries. The same disciplines that ensure a medical device is defect-free can make automotive components more reliable.

Building trust as a manufacturing partner versus potential competitor requires walking a careful line. Jabil has access to their customers' most sensitive information—product designs, cost structures, supplier relationships. They could theoretically forward-integrate and compete with customers. But they never do. This discipline, maintained over decades, creates trust that becomes its own moat.

Customer concentration risk management is an ongoing challenge. Jabil's solution isn't to avoid concentration but to make it mutual. They embed themselves so deeply in customers' operations that switching costs become prohibitive. When you've co-designed products, shared IT systems, and integrated supply chains, changing manufacturers isn't just expensive—it's existential.

The acquisition integration playbook has been refined through dozens of deals. Jabil doesn't just buy factories; they buy capabilities and customer relationships. Integration focuses on three things: standardizing processes to Jabil's systems, retaining key technical talent, and maintaining customer relationships through the transition. Financial synergies come last—operational excellence comes first.

Managing complexity at scale requires systems thinking that few companies master. Jabil runs 100+ facilities producing thousands of products for hundreds of customers. The only way this works is through radical standardization of processes combined with local flexibility in execution. It's McDonald's meets Boeing—consistent quality with aerospace complexity.

Why haven't most people heard of a $29 billion company? Because invisibility is strategic. Consumer brands need recognition; Jabil needs trust from a small number of sophisticated buyers. Every dollar spent on Super Bowl ads would be wasted. Their customers know them intimately—that's all that matters.

XII. Bear vs. Bull Case

The Bull Case:

The secular tailwinds are undeniable. AI infrastructure spending is in the first innings of a nine-inning game. Electric vehicle penetration globally sits below 20%, suggesting years of growth ahead. Healthcare spending grows regardless of economic cycles. These aren't hopes—they're demographic and technological certainties.

Cash generation remains robust and shareholder returns are programmatic. This isn't a company promising returns someday—they're delivering them now, with billion-dollar buyback authorizations backed by actual cash generation, not financial engineering.

The diversified end-market exposure provides resilience most manufacturers lack. When automotive slumps, healthcare compensates. When consumer electronics crater, infrastructure spending continues. This isn't perfect hedging, but it's portfolio theory applied to manufacturing.

Deep customer relationships create switching costs that approach infinity for complex products. When you've spent three years co-developing a medical device that required FDA approval, you don't switch manufacturers to save 2% on unit costs.

The Bear Case:

Customer concentration risk remains existential. Lose Apple or J&J, and billions in revenue evaporate overnight. This isn't theoretical—Jabil has lost major customers before and suffered accordingly.

Margin pressure in the competitive EMS industry is structural, not cyclical. As manufacturing becomes more automated, differentiation erodes. Chinese competitors with state support can underprice Western manufacturers indefinitely.

Cyclical exposure to tech spending means Jabil can't escape the boom-bust cycles that have plagued them historically. AI spending will eventually slow, automotive will hit saturation, healthcare will face pricing pressure.

Execution risk in portfolio transformation is real. Divesting businesses, acquiring new capabilities, and managing leadership transitions simultaneously creates complexity that could overwhelm even excellent operators.

The geopolitical risks are escalating, not moderating. US-China tensions, reshoring pressures, and supply chain nationalism all threaten the global manufacturing model Jabil has perfected.

XIII. Closing Thoughts

Jabil's story is ultimately about evolution—from repair shop to manufacturer, from regional to global, from electronics specialist to diversified industrial. But it's also about persistence, about building excellence in an unglamorous industry, about creating value through operational excellence rather than financial engineering.

For investors, Jabil represents a fascinating study in transformation. This is a company actively shrinking revenue to grow margins, divesting legacy businesses to invest in the future, returning capital while simultaneously investing for growth. These apparent contradictions make sense only when you understand the strategic framework: Jabil will only do what they can do excellently, and they'll return everything else to shareholders.

The next decade will test whether Jabil's transformation is complete or just beginning. Can they maintain margins as competition intensifies? Can they capture enough of the AI infrastructure boom to offset declining legacy businesses? Can they navigate geopolitical tensions while maintaining global operations?

What's certain is that Jabil will remain essential yet invisible, critical yet unrecognized, massive yet unknown. In a world obsessed with consumer brands and software unicorns, there's something refreshing about a company that just makes things—brilliantly, consistently, profitably. That's the Jabil story: the manufacturing giant behind your technology that you've never heard of, and probably never will.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube