Tencent Holdings Limited: The Everything App Empire

I. Introduction & Episode Preview

Picture this: It's 1999 in Shenzhen, and five engineers are huddled in a cramped office, desperately trying to keep their servers running as millions of Chinese internet users flood their messaging platform. They have no revenue model, they're hemorrhaging cash, and they've just been sued by AOL for copying ICQ. Fast forward to today, and that same company controls the digital lives of over a billion people, generates more gaming revenue than Sony, Nintendo, and Activision Blizzard combined, and runs an app so essential to Chinese society that the government treats it as critical infrastructure.

How did an ICQ clone become one of the world's most valuable companies?

Tencent today stands as a colossus straddling multiple worlds. From its gleaming twin towers in Shenzhen's Nanshan district—designed to look like two massive server racks—the company orchestrates an empire that defies easy categorization. It's simultaneously the world's largest video game company by equity investments, China's dominant social media platform, a major fintech player processing trillions in transactions, and an AI powerhouse quietly building the infrastructure for China's digital future. With a market cap hovering around $450 billion despite regulatory headwinds, Tencent remains one of the most valuable technology companies globally. With a market cap of $697.48 billion as of September 2025, making it the world's 14th most valuable company, Tencent remains one of the most valuable technology companies globally.

But here's what makes the Tencent story particularly fascinating for investors: this is a company that has mastered the art of platform economics at a scale matched only by the American tech giants, yet operates in a fundamentally different ecosystem with its own rules, opportunities, and constraints. It's built a business model that Western companies have tried—and largely failed—to replicate, centered around the concept of the "super app" that seamlessly blends social networking, gaming, payments, e-commerce, and virtually every aspect of digital life.

The big question we'll wrestle with throughout this analysis: Can a Chinese tech giant's playbook work globally? And perhaps more intriguingly—why haven't Western tech giants been able to replicate Tencent's super-app model, despite numerous attempts?

As we trace Tencent's journey from a desperate startup copying Western software to a global technology powerhouse, we'll uncover the strategic decisions, cultural insights, and sheer adaptability that transformed five engineers' side project into an empire. From the early days of selling virtual clothes for QQ avatars to orchestrating multi-billion dollar gaming acquisitions, from surviving regulatory crackdowns to pioneering new frontiers in AI, this is the story of how Tencent built the everything app empire—and what it means for the future of technology and investing.

II. The Founding Story & Early Internet Gold Rush (1998-2003)

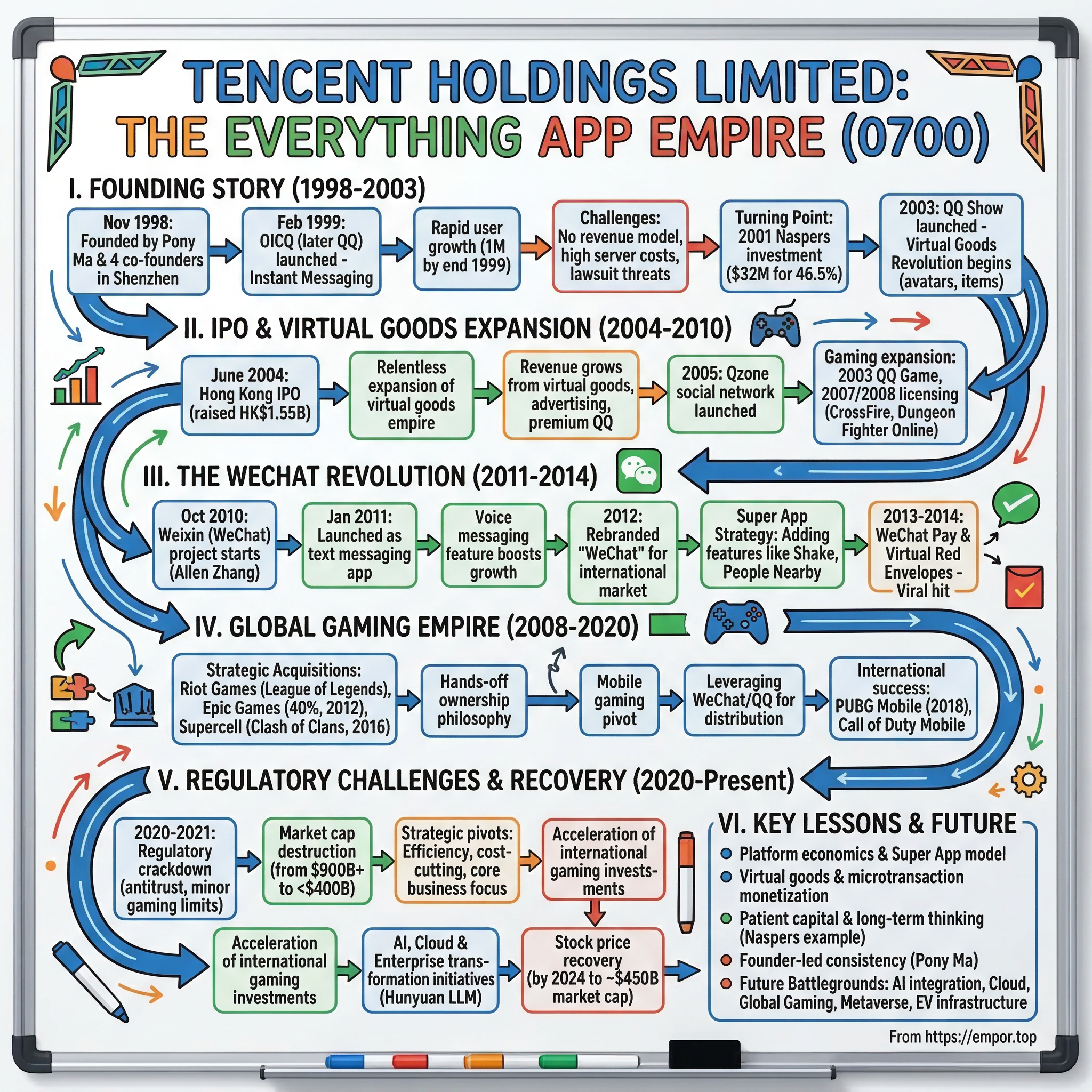

The fluorescent lights hummed in the borrowed office space as Ma Huateng—known to the English-speaking world as Pony Ma—stared at his computer screen. It was November 11, 1998, a date that would later become China's biggest shopping holiday, but on this particular day, Ma and his four co-founders were registering a company that would reshape not just Chinese technology, but global gaming and social media forever. Tencent was founded by Pony Ma, Zhang Zhidong, Xu Chenye, Charles Chen and Zeng Liqing in November 1998 as Tencent Inc, in the Cayman Islands. The computer science graduates from Shenzhen University had pooled their savings—about 500,000 yuan ($60,000 at the time)—betting everything on China's nascent internet boom. Ma Huateng, better known as Pony Ma (a play on his surname which means "horse" in Chinese), was just 27 years old, a shy programmer who had previously worked for China Motion Telecom. Zhang Zhidong, the technical genius of the group, would become the architect of Tencent's infrastructure. The other three—Xu Chenye, Charles Chen (Chen Yidan), and Zeng Liqing—brought expertise in operations, administration, and marketing respectively.

The name "Tencent" is based on its Chinese name Tengxun (Chinese: 腾讯), which incorporates part of Pony Ma's Chinese name (Ma Huateng; 马化「腾」) and literally means "galloping fast information". It was an ambitious name for a company with no clear business model, operating in a country where only 2.1 million people—less than 0.2% of the population—had internet access.

China in 1998 was a nation in technological adolescence. The reform and opening-up policies initiated by Deng Xiaoping twenty years earlier had created pockets of prosperity, particularly in coastal cities like Shenzhen, which sat just across the border from Hong Kong. The Asian Financial Crisis was still reverberating through the region, but China's partially closed capital account had insulated it from the worst effects. More importantly, the government was beginning to see the internet not as a threat but as a tool for economic modernization—though always under careful state supervision.

In February 1999, Tencent's messenger product OICQ was released. Shortly after, Tencent had the client's name changed to QQ; this was said to be due to a lawsuit threat from ICQ and its owner AOL. The product was essentially a Chinese-language clone of ICQ, the Israeli-developed instant messaging service that had taken the Western world by storm. But OICQ had localization advantages: it stored contact lists on servers rather than locally (crucial when most Chinese users accessed the internet from shared computers in internet cafés), it worked better on China's slower internet connections, and it featured cuter, more culturally resonant avatars. The growth was explosive. OICQ registered users reached 200,000 within two months of launch in February 1999. Later in November, the users broke 1 million. By the end of 1999, QQ achieved 1 million registered users in China. By 2000, the peak number of concurrent QQ users surpassed 100,000—an astonishing number for a company with no revenue model and servers held together by prayer and venture capital.

But success brought problems. The company remained unprofitable for the first three years. Server costs were astronomical—each new user meant more infrastructure expense with no corresponding revenue. Pony Ma later recalled nights spent in the server room, physically restarting machines that had crashed under the load. The founders considered selling the company multiple times. In one desperate moment, they tried to sell OICQ to search companies for just 3 million yuan (about $360,000 at the time), but found no buyers. The lack of interest proved to be one of the luckiest rejections in business history. The turning point came in 2001. In May 2001, Naspers purchased 46.5% of Tencent, with the South African media company paying $32 million for what would become one of the most successful venture capital deals of all time. Koos Bekker, then CEO of Naspers, had been burning money trying to enter the Chinese market with Western media models. But he saw something different in Tencent—a genuinely local innovation that understood Chinese users' unique needs. Against his legal counsel's advice, Bekker made the investment and, crucially, took a hands-off approach, letting the local entrepreneurs run the business.

The timing was fortuitous. Just as Tencent secured this lifeline, it discovered its business model. The breakthrough came not from advertising or subscription fees—the Western models everyone expected—but from something uniquely Asian: virtual goods. In 2003, Tencent launched QQ Show, a service that allowed users to have a virtual image and buy clothes, accessories and backgrounds to dress up their avatars—"quite like the meta-universe of today," as one observer put it. For a generation of Chinese internet users who were chatting without knowing what each other looked like, QQ Show provided a way to express identity and status in the virtual world. Users could spend small amounts—typically 0.5 to 2 yuan—to purchase virtual clothing, hairstyles, and accessories for their cartoon avatars. It seemed trivial, even absurd to Western observers, but QQ Show was a huge success as soon as it was launched, becoming Tencent's most profitable business.

The psychology was brilliant. In a collectivist society where standing out in real life carried social risks, virtual self-expression became a safe outlet for individuality. A teenager in Wuhan could transform into a punk rocker online; an office worker in Beijing could dress their avatar in designer clothes they couldn't afford in reality. By 2005, charging for QQ mobile, virtual goods sales, and even licensing the penguin mascot for merchandise had become significant income generators. By 2008, Tencent was seeing substantial profit growth from the sale of virtual goods.

The company remained unprofitable for the first three years. South African media company Naspers purchased a 46.5% share of Tencent in 2001. The company originally derived income solely from advertising and premium users of QQ, who pay monthly fees to receive extras. By 2005, charging for use of QQ mobile, its cellular value-added service, and licensing its penguin character, which could be found on snack food and clothing, had also become income generators. By 2008, Tencent was seeing profit growth from the sale of virtual goods.

The founder and chairman, Huateng "Pony" Ma, famously said, "[To] copy is not evil." A former CEO and president of SINA.com, Wang Zhidong, said, "Pony Ma is a notorious king of copying." Jack Ma of Alibaba Group stated, "The problem with Tencent is the lack of innovation; all of their products are copies." These criticisms would dog the company for years, but they missed something crucial: Tencent wasn't just copying—it was localizing, improving, and most importantly, finding business models that worked in the Chinese context.

As we approach 2004 and Tencent's public listing, the company had transformed from five engineers with a copycat messaging app into a profitable business with a revolutionary approach to monetization. The virtual goods model they pioneered would later be adopted by Facebook, Fortnite, and virtually every modern free-to-play game. But first, they needed to convince public market investors that selling digital clothing to Chinese teenagers was a real business.

III. IPO & The Virtual Goods Revolution (2004-2010)

The morning of June 16, 2004, broke humid and uncertain over Hong Kong's financial district. Inside the Stock Exchange building, Pony Ma rang the opening bell, marking Tencent's debut as a public company. The IPO raised HK$1.55 billion ($200 million), valuing the company at just under $1 billion—a respectable but not spectacular debut. Few watching that day could have imagined they were witnessing the birth of what would become one of the world's most valuable technology companies. The initial offer price for the initial public offering of Tencent's ordinary shares was fixed at HK$3.70 per share. At that offer price per share and assuming the over-allotment option is not exercised the net proceeds from the offering are estimated to be approximately HK$1437.8 million. The IPO was significantly underpriced—later analysis would suggest the shares were offered at a deep discount, perhaps five times below their intrinsic value.

But what made Tencent's post-IPO journey remarkable wasn't the stock price appreciation—it was the company's relentless expansion of its virtual goods empire and its transformation from a messaging platform into China's digital Switzerland, where every major internet activity would eventually flow through its servers.

The revenue evolution during this period tells the story of a company finding its rhythm. In 2004, revenue stood at RMB 1.14 billion ($138 million). By 2008, this had exploded to RMB 7.15 billion ($1.04 billion), a compound annual growth rate exceeding 50%. But more importantly, the revenue mix was shifting. While mobile value-added services and advertising remained important, virtual goods were becoming the profit engine. The QQ ecosystem expansion during this period was remarkable. In 2003, Tencent officially began to enter the game business, with QQ Game being released. In 2004, QQ Hall was released for public beta, and the highest number of simultaneous online users of QQ Games exceeded 1 million, making QQ Game the world's leading casual game portal. Tencent Games published its first game QQ Tang (QQ堂) in 2004, based on its social media platform QQ. In 2005, QQ Pet was launched and QQ Fantasy was released for public beta, with the highest number of simultaneous online users exceeding 660,000. Tencent's structure was adjusted, and the interactive entertainment business system was formally established for the online game business.

In 2005, Tencent launched Qzone, a social networking/blogging service integrated within QQ. Qzone would become one of the largest social networking services in China, with a user base of 645 million by 2014. This was Facebook before Facebook—at least in China. Users could create blogs, share photos, and most importantly, customize their spaces with virtual goods. The integration was seamless: your QQ identity carried over, your friends were already there, and the virtual currency worked across platforms.

By 2006, the highest number of simultaneous online users of QQ Games exceeded 2 million, and the maximum number of simultaneous online users of QQ Pet exceeded 1 million, making it the largest online virtual pet community in the world. Every product launch wasn't just a new feature—it was another tentacle of the octopus, another way to keep users within the Tencent ecosystem, another opportunity to sell virtual goods.

The gaming expansion accelerated dramatically between 2007 and 2008. While Tencent's services had included online gaming since 2004, around 2007/2008, it rapidly increased its offerings by licensing games. The company started by developi Cross Fire, QQ Free Fantasy, QQ Dazzling Dance, Cross Fire, Seeking Immortals, and Dungeon Fighter Online (DNF) were beta-tested in succession. While at least two, CrossFire and Dungeon Fighter Online, were originally produced by South Korean game developers, Tencent localized them perfectly for the Chinese market. The move that would define Tencent's gaming future came through strategic acquisitions. Tencent had already held 22.34% of the equity interest out of a previous investment in 2008 in Riot Games. On February 18, 2011, Tencent acquired a majority of equity interest (92.78%) in Riot Games, developer of League of Legends, for about US$230 million. On December 16, 2015, Riot Games sold its remaining equity to Tencent, giving the Chinese company full ownership.

This wasn't just an acquisition—it was a masterclass in strategic patience. Tencent signed a Chinese distribution deal for League of Legends in November 2008, before the game even launched, and made an initial investment in 2009. They saw the potential of the multiplayer online battle arena (MOBA) game from its inception, when most Western publishers were baffled by the game's lack of a single-player mode and free-to-play business model.

Building the social network fortress before Facebook's Asia push was crucial during this period. Facebook was banned in China in 2009, but even before that, Tencent had created an impenetrable moat. Qzone, launched in 2005, wasn't just a social network—it was a lifestyle platform where hundreds of millions of users spent hours customizing their spaces, playing games, and yes, buying virtual goods. By the time Western social networks started paying attention to Asia, Tencent had already locked in an entire generation of Chinese internet users.

The "copy to China" criticism reached its peak during this period. A former CEO and president of SINA.com, Wang Zhidong, said, "Pony Ma is a notorious king of copying." Jack Ma of Alibaba Group stated, "The problem with Tencent is the lack of innovation; all of their products are copies." The criticisms aimed at Tencent included that QQ farm was a direct copy of Happy Farm, QQ dance originated from Audition Online, and QQ speed featured gameplay highly similar to Crazyracing Kartrider.

But Ma Huateng had a different perspective. "[To] copy is not evil," he famously said. And in a sense, he was right. What Tencent did wasn't mere copying—it was localization at its finest. They took Western and Korean games and transformed them for Chinese tastes, adding social features tied to QQ, implementing virtual goods models that worked in the Chinese context, and most importantly, operating them at a scale that dwarfed the originals.

By 2010, Tencent had become the largest online gaming company in China, with millions of users of QQ Flying Car, QQ Dazzling Dance, DNF, and Cross Fire online simultaneously. The revenue mix had completely transformed. Gaming was no longer an experiment or a side business—it was the core profit engine, funding everything else the company would do.

As we transition into the next phase of Tencent's story, the company stood at a crossroads. They had conquered desktop gaming in China, built a social network fortress, and perfected the virtual goods business model. But a new challenge was emerging: the smartphone revolution was about to begin, and with it would come both the company's greatest triumph and its most existential threat.

IV. The WeChat Revolution (2011-2014)

Allen Zhang was not your typical Tencent executive. A chain-smoker who preferred working alone to managing teams, he had joined the company through acquisition when Tencent bought his email client Foxmail in 2005. By late 2010, he was running QQ Mail from Tencent's Guangzhou office, physically and culturally distant from the main operations in Shenzhen. But Zhang had been watching something interesting happening in the mobile messaging space, and he was about to convince Pony Ma to let him build what would become China's most essential app. WeChat began as a project at Tencent Guangzhou Research and Project center in October 2010. The original version of the app was created by Allen Zhang, named "Weixin" (微信) by Pony Ma, and launched on January 21, 2011. The project started with just ten engineers—a remarkably small team for what would become one of the world's most important applications.

The launch was underwhelming. WeChat 1.0 was largely a copy of Kik, with only text message functionality. Users in China's tech community wondered why they needed another messaging app when QQ already dominated. Growth was sluggish, and internal skepticism ran high. Pony Ma later admitted that even he had doubts about whether the app would succeed.

The TalkBox voice messaging inspiration changed everything. In early 2011, a Hong Kong startup called TalkBox had discovered a crucial insight: many older generations in China never learned to type using roman characters. The romanization of Chinese characters, called Pinyin, was only developed in the 1950s and wasn't adopted as an international standard until the 1980s. TalkBox launched as a walkie-talkie-like application that allowed users to send voice messages. By April 2011, TalkBox had over 1 million users and was the most popular social app in China and Southeast Asia.

According to TalkBox's co-founder, Pony Ma and Allen Zhang were active users of TalkBox, having downloaded the app in its first weeks of launch. Tencent even approached TalkBox about investment or acquisition, but the startup turned them down—a decision they would later regret. By May 2011, WeChat had added its own voice messaging feature. The impact was immediate and dramatic. After the release of the walkie-talkie-like voice messaging feature in May of that year, growth surged.

The voice messaging breakthrough was more than just a feature—it was a cultural unlock. In a society where typing Chinese characters on early smartphones was cumbersome, where many users were accessing the internet for the first time through mobile devices, voice messages provided an intuitive, human way to communicate. Users could hold down a button, speak their message, and send it instantly. It felt magical.

By 2012, when the number of users reached 100 million, Weixin was re-branded "WeChat" for the international market. The name change signaled ambition beyond China's borders, but more importantly, the product was finding its rhythm. WeChat wasn't trying to be QQ on mobile—it was something entirely new.

Building a super app required more than messaging. The transformation from messaging to lifestyle platform happened through a series of calculated additions. Each new feature wasn't just bolted on; it was carefully integrated into the existing user experience. The "Shake" feature, launched in 2011, allowed users to shake their phones and connect with other users doing the same at that moment. "People Nearby" let users discover and chat with strangers in their vicinity. These features, which might seem trivial or even problematic in Western contexts, were perfect for China's rapidly urbanizing population of young people moving to new cities for work. The 2013-2014 WeChat Pay launch and the virtual red envelope genius move transformed everything. WeChat Pay was officially launched in August 2013, but initial adoption was slow. Users already had Alipay for online payments and didn't see the need for another payment system. Then came Chinese New Year 2014, and with it, one of the most brilliant product launches in technology history.

On January 17, 2014, WeChat launched the red envelope application. The concept was based on the Chinese tradition of hongbao (red envelope), where money is given to family and friends as gifts during holidays. But WeChat turned it into something more—a viral, social, gamified experience. Users could send money to contacts and groups as gifts. When sent to groups, the money could be distributed equally or in random shares ("Lucky Money"), turning the simple act of giving money into an exciting game.

The feature was launched through a promotion during China Central Television's heavily watched New Year's Gala, where viewers were instructed to shake their phones during the broadcast for a chance to win sponsored cash prizes from red envelopes. According to the Wall Street Journal, 16 million red envelopes were sent in the first 24 hours. A month after its launch, WeChat Pay's user base expanded from 30 million to 100 million users, and 20 million red envelopes were distributed during the New Year holiday.

Alibaba founder Jack Ma called it a "Pearl Harbor moment" for his company. Alipay had practically owned payments and commerce in China, but WeChat had found a way to make payment social, fun, and irresistibly viral. The red envelope feature wasn't just about money—it was about social connection, cultural tradition, and the thrill of chance all rolled into one.

Growing to 889 million MAU by 2016 wasn't just about adding features—it was about becoming indispensable. By 2016, WeChat had over 889 million monthly active users. By 2012, when the number of users reached 100 million, Weixin was re-branded "WeChat" for the international market. The app had evolved far beyond messaging. It was where Chinese people chatted with friends, paid bills, ordered food, hailed taxis, made doctor appointments, and even got divorced (some Chinese cities allowed divorce proceedings to be initiated through WeChat).

The comparison with Western apps becomes almost absurd at this point. Imagine if WhatsApp, Venmo, Uber, Instagram, and your banking app were all the same application, and you begin to understand WeChat's position in Chinese society. But even that doesn't capture it fully—WeChat wasn't just combining existing services; it was creating entirely new user behaviors and social norms.

Why WeChat succeeded where others failed comes down to several factors. First, timing—it caught the mobile wave perfectly, launching just as smartphones were becoming affordable for middle-class Chinese consumers. Second, localization—every feature was designed with deep understanding of Chinese culture and behavior. Third, the ecosystem advantage—Tencent could leverage its existing QQ user base and gaming properties to drive adoption.

But perhaps most importantly, WeChat succeeded because it understood that in China, the super app model made sense. In a market where consumers were leapfrogging from limited internet access directly to mobile, where trust in institutions was low but trust in major platforms was high, where the government preferred a small number of controllable platforms to a fragmented ecosystem, the conditions were perfect for a single app to become everything.

As we move into the next phase of Tencent's story, the company had achieved something remarkable: it had built not one but two dominant platforms—QQ for desktop and WeChat for mobile. The next challenge would be leveraging these platforms to dominate the fastest-growing segment of entertainment: gaming. And this time, Tencent wouldn't just copy or license games—it would buy the entire industry.

V. The Gaming Empire & Global M&A Spree (2008-2020)

The conference room in Los Angeles was tense. It was February 2011, and Brandon Beck and Marc Merrill, the co-founders of Riot Games, were about to sign documents that would give a Chinese company they'd barely heard of three years ago control of their baby, League of Legends. The game was exploding in popularity, on its way to becoming the most-played PC game in the world. Why sell now? Beck would later explain: "We realized we needed a partner who understood games as a service, who had patient capital, and who would let us maintain our independence. Tencent was the only company that checked all three boxes."

The acquisition represented everything Tencent had learned about gaming investments. Unlike Western acquirers who often imposed their culture and processes on acquired studios, Tencent practiced what industry insiders called "hands-off ownership." Riot would continue operating independently from Los Angeles, maintaining its company culture and creative freedom. Tencent's role would be to provide capital, share operational expertise in games-as-a-service, and crucially, handle the complex Chinese market where League of Legends would eventually become a cultural phenomenon.

The 2012 Epic Games minority stake marked another strategic masterstroke. Tencent acquired a 40% stake in Epic Games for $330 million in June 2012, valuing the company at less than $1 billion. This investment triggered one of the most dramatic shifts in PC gaming of the last decade, ushering in a new era of games-as-a-service. The partnership led to significant changes in Epic's operations, including the adoption of a free version of the Unreal Engine and the success of Fortnite.

Tim Sweeney, Epic's CEO, would later defend the partnership when critics raised concerns about Chinese influence, emphasizing that Epic remained an American company with full operational independence. The investment gave Epic the capital to develop Fortnite, which would become one of the most lucrative games in history, while Tencent gained exposure to the Unreal Engine—the technology powering countless games across the industry.

But the crown jewel of Tencent's acquisition spree came in 2016. On June 21, 2016, Tencent announced a deal to acquire 84.3% of Supercell, developer of Clash of Clans, for $8.6 billion. This wasn't just the largest gaming acquisition at the time—it was a bet on mobile gaming's future that many thought insane. Supercell, a Finnish company with just 200 employees, was generating billions in revenue from games like Clash of Clans, Clash Royale, and Hay Day.

The deal structure was complex: In October 2013, GungHo Online Entertainment and its parent SoftBank had acquired 51% of Supercell for $1.51 billion. By June 2015, SoftBank had increased its stake to 73.2%, becoming the sole external shareholder. When Tencent made its move, it created Halti S.A., a Luxembourg-based consortium that was 50%-owned by Tencent. SoftBank valued Supercell at $10.2 billion at the time. In October 2019, Tencent increased its stake in the consortium to 51.2% by acquiring shares worth $40 million as part of a convertible bond.

The Supercell acquisition embodied Tencent's philosophy perfectly. The Finnish studio reportedly retained most of its independence and remained located in Finland, continuing to operate with its unique "cell" structure where small teams had autonomy to create and kill games rapidly. Ilkka Paananen, Supercell's CEO, remained in charge, and the company culture stayed intact. What Tencent brought was patient capital, expertise in live operations and monetization, and access to the Chinese market.

The mobile gaming pivot and leveraging WeChat/QQ distribution became Tencent's superpower during this period. While Western publishers were still focused on console and PC gaming, Tencent recognized that mobile would become the dominant platform, especially in emerging markets. They could leverage their massive WeChat and QQ user bases—over 1 billion users combined—as distribution channels for mobile games. This wasn't just about owning games; it was about controlling the entire ecosystem from creation to distribution to payment.

The international games success story that best exemplifies this strategy is PUBG Mobile. PUBG Mobile is a free-to-play battle royale game co-developed by LightSpeed & Quantum Studio and PUBG Studios, published by Tencent Games. It launched for Android and iOS on March 19, 2018, with development taking just 4 months to complete.

The game's financial performance has been staggering. Tencent's mobile revenue jumped to $4.44 billion in 2018, with PUBG Mobile generating $91.9 million in its first year, setting the foundation for its huge breakout ahead. By August 2019, PUBG Mobile revenue had grown from approximately $25 million in August 2018 to slightly more than $160 million—an increase of about 540%. Even excluding China, monthly revenue more than doubled year-over-year, reaching nearly $63 million.

PUBG Mobile reached $5.1 billion in lifetime revenue by 2021, having accumulated $2.7 billion in 2020 alone. The game averaged approximately $704 million in player spending per quarter between Q1 and Q3 2020, generating an average of $7.4 million per day. By December 2022, PUBG Mobile had accumulated around 1.3 billion downloads while grossing over $9 billion. The game grossed over $2.6 billion in 2020, making it the highest-grossing game of the year.

The China localization story adds another layer of complexity. PUBG Mobile had been awaiting government approval for release in China, where it could only be offered as a public test. However, Tencent's planned release was suspended due to the government approval freeze across most of 2018. By May 2019, Tencent announced it would re-release the game under the title Game for Peace, changing elements to meet China's content restrictions, such as eliminating blood and gore.

This pivot proved incredibly lucrative. PUBG Mobile generated about 66% of its all-time revenue from its Chinese version Game for Peace. The United States was the second most important market, contributing about 11% of revenue. In May 2019 alone, the two versions combined generated an estimated $146 million, about 126% more than PUBG Mobile alone had grossed in April. Game for Peace on iOS accounted for about 48% of this spending, or approximately $70 million.

Gaming as the cash cow funding the entire ecosystem cannot be overstated. By 2020, Tencent had become the world's largest gaming company by revenue, with its games division generating tens of billions annually. This wasn't just profitable on its own—it provided the capital for Tencent's expansion into cloud computing, AI, fintech, and other frontier technologies. Every virtual gun skin sold in PUBG Mobile, every gem purchased in Clash of Clans, every champion bought in League of Legends was funding Tencent's transformation into a global technology conglomerate.

The acquisition strategy expanded beyond the headline deals. By 2020, Tencent owned 80% of New Zealand's Grinding Gear Games ("Path of Exile"), 14.5% of Glu Mobile, 11.5% of Bluehole, and 5% stakes in Activision Blizzard, Ubisoft, and Paradox Interactive. The Wall Street Journal reported in 2018 that Tencent had bought stakes in 277 tech companies since 2013, with that number rising to 600 companies by 2019.

Each investment followed a similar playbook: identify talented studios with proven or promising IP, provide capital and operational support while maintaining creative independence, leverage Tencent's distribution and monetization expertise, and critically, bring the games to China through careful localization. It was a formula that turned Tencent from a Chinese internet company into a global gaming empire.

VI. The WeChat Ecosystem & Super App Strategy (2015-Present)

The conference room in Tencent's Shenzhen headquarters was packed with engineers, product managers, and executives. It was January 2017, and Allen Zhang was about to unveil something that would fundamentally change not just WeChat, but the entire concept of what a mobile app could be. "Mini Programs," he announced, "will make WeChat the operating system of mobile life in China." The room erupted in discussion—some saw the revolutionary potential, others worried about the technical challenges. Three years later, those Mini Programs would be processing over 2 trillion yuan in transactions quarterly.

WeChat as China's "app for everything" represents perhaps the most successful execution of the super-app concept in technology history. By 2015, WeChat had already evolved far beyond messaging, but what happened next transformed it into something unprecedented in Western technology: a single app that effectively replaced the need for hundreds of others.

The expansion accelerated in 2016 when Tencent made significant moves in adjacent industries, including acquiring a majority stake in China Music Corporation in July 2016, integrating music streaming directly into the WeChat ecosystem. Users could share songs, create playlists, and even purchase concert tickets without leaving the app.

The 2017 Mini Programs launch was the game changer for ecosystem lock-in. Mini Programs are essentially apps within WeChat—lightweight applications that don't require downloading or installation. Users can access everything from e-commerce stores to government services, from games to productivity tools, all within WeChat's interface. The brilliance was in the execution: Mini Programs load instantly, share WeChat's login credentials and payment system, and can be shared as easily as sending a message.

The initial skepticism from developers quickly turned to enthusiasm as the numbers became undeniable. By 2018, there were over 1 million Mini Programs on the platform. By 2020, that number had doubled. The ecosystem wasn't just growing—it was becoming essential infrastructure for Chinese business. Small retailers who couldn't afford to build their own apps could launch sophisticated e-commerce operations through Mini Programs. Restaurants could take orders and reservations. Government agencies could provide services. Even luxury brands like Burberry and Louis Vuitton launched Mini Program boutiques.

By Q3 2024, Mini Programs' gross merchandise value (GMV) exceeded RMB 2 trillion, a staggering figure that represents more transaction volume than many entire e-commerce platforms globally. This isn't just commerce—it's an entire parallel economy running inside a messaging app.

WeChat Pay versus Alipay became the defining financial technology battle in China. While Alibaba's Alipay had dominated online payments through its association with Taobao and Tmall, WeChat Pay attacked from a different angle: social payments. The red envelope feature had given WeChat Pay its initial boost, but the real victory came from ubiquity. Every Mini Program, every in-app purchase, every peer-to-peer transfer strengthened WeChat Pay's position.

By 2019, WeChat Pay had achieved near parity with Alipay in mobile payments, each controlling about 50% of China's multi-trillion dollar mobile payment market. But WeChat Pay's integration advantage was clear—while users had to open Alipay separately, WeChat Pay was always there, embedded in the app they already had open dozens of times per day. The payment wars forced both companies to innovate rapidly, driving down transaction costs and expanding into wealth management, insurance, and credit products.

Building the transaction layer from social to commerce required careful orchestration. WeChat introduced Official Accounts, allowing businesses, media companies, and individuals to broadcast content to followers. These weren't just marketing channels—they were fully functional business platforms where companies could sell products, provide customer service, and process transactions. A user could read an article about a product, click to purchase, pay with WeChat Pay, and share their purchase with friends, all without leaving a single conversation thread.

The Moments advertising platform, launched in 2015, provided the monetization engine. Unlike the aggressive advertising on other platforms, WeChat limited Moments ads to two per user per day initially, maintaining user experience while commanding premium prices from advertisers. The targeting capabilities were unprecedented—combining social graph data, payment history, location information, and behavioral patterns to deliver ads with surgical precision.

Video Accounts, launched in 2020, represented WeChat's answer to the short video revolution led by ByteDance's Douyin (TikTok in international markets). But rather than copying Douyin's addictive algorithm-driven feed, WeChat integrated short videos into its existing social framework. Videos from friends and followed accounts appeared in a separate tab, but could be shared into chats and Moments, maintaining WeChat's social-first approach. By 2024, Video Accounts had over 900 million users, with average viewing time exceeding 100 minutes per day for active users.

Channels, the live-streaming commerce feature, merged entertainment with e-commerce in ways that seemed foreign to Western observers but became central to Chinese digital commerce. Influencers could broadcast live, demonstrate products, and viewers could purchase items in real-time without leaving the stream. During major shopping festivals, top streamers could generate hundreds of millions in sales in a single session. The integration was seamless—products featured in streams could be saved to wishlists, shared with friends for opinions, and purchased with a few taps.

The data advantage and network effects moat that WeChat built became virtually insurmountable. Every interaction—every message sent, payment made, article read, video watched, product purchased—fed into Tencent's data ecosystem. This wasn't just big data; it was complete data, a comprehensive view of users' digital lives. The network effects were multi-dimensional: more users attracted more businesses, which created more Mini Programs, which provided more services, which attracted more users.

Privacy concerns that would have torpedoed such a system in the West were managed differently in China. Users accepted the trade-off: comprehensive data collection in exchange for unprecedented convenience. The Chinese government's support for domestic tech champions and different cultural attitudes toward privacy enabled WeChat to build features that would be legally or culturally impossible in Western markets.

The ecosystem's power became evident during the COVID-19 pandemic. Health codes—Mini Programs that tracked users' travel history and health status—became mandatory for entering buildings, using public transport, and traveling between cities. WeChat wasn't just convenient anymore; it was essential. Citizens without WeChat effectively couldn't participate in society during the pandemic. This level of integration between a private platform and public services would be unthinkable in most Western democracies.

The financial performance of the WeChat ecosystem is difficult to isolate from Tencent's broader business, but analysts estimate that WeChat-related revenues—including payments, advertising, and Mini Program transactions—exceed $50 billion annually. More importantly, WeChat acts as the glue binding Tencent's entire empire together. Games are promoted through WeChat, cloud services are sold to Mini Program developers, and AI capabilities are deployed to improve user experience across the platform.

The competitive moat WeChat has built extends beyond features or user numbers. It's embedded in the fabric of Chinese digital life to such an extent that switching costs aren't just high—they're almost insurmountable. Your entire social graph, payment history, business relationships, and daily service interactions exist within WeChat. Even if a competitor offered superior features, the coordination problem of moving an entire society to a new platform makes disruption nearly impossible.

International expansion attempts have revealed both the power and limitations of the WeChat model. While WeChat has found success among Chinese diaspora communities and businesses dealing with China, it has struggled to gain mainstream adoption in Western markets. The super-app model that works perfectly in China faces regulatory, cultural, and competitive challenges elsewhere. Users accustomed to specialized apps for different functions are skeptical of putting all their digital eggs in one basket.

Yet the influence of WeChat's model extends far beyond its direct user base. Every major tech company globally has studied WeChat's super-app playbook. Facebook's attempts to integrate payments and commerce into WhatsApp and Messenger, Google's expansion of Google Pay, and even Apple's gradual addition of features to iMessage all show WeChat's influence. The question isn't whether the super-app model will spread globally, but how it will be adapted for different markets and regulatory environments.

VII. Regulatory Challenges & The New Reality (2020-2024)

The emergency board meeting convened at 3 AM Beijing time on December 24, 2020. Pony Ma and his leadership team had just received word that regulators were opening an antitrust investigation into Alibaba, and Tencent knew they could be next. The era of unfettered growth for Chinese tech giants was ending, and what followed would be the most challenging period in Tencent's history—a regulatory storm that would wipe out over $500 billion from its market value before the company would engineer one of the most remarkable recoveries in corporate history.

The 2020-2021 regulatory crackdown began with what seemed like routine criticism of monopolistic practices but quickly escalated into a fundamental restructuring of China's technology sector. The government's concerns were multifaceted: the immense power concentrated in a few tech platforms, the social impact of gaming on youth, data security and privacy issues, and the broader goal of "common prosperity" that President Xi Jinping had articulated.

For Tencent, the gaming restrictions hit particularly hard. In August 2021, state media described online games as "spiritual opium," evoking memories of China's historical humiliation during the Opium Wars. New regulations limited minors to just three hours of online gaming per week—8 to 9 PM on Fridays, weekends, and holidays only. Tencent had to implement facial recognition technology to enforce these restrictions, checking users' identities against a national database.

The immediate impact was severe. Although minors represented less than 5% of Tencent's gaming revenue, the signaling effect was catastrophic. International investors, already nervous about Chinese regulatory risk, fled en masse. Tencent's stock price plummeted from a peak of HK$774 in February 2021 to HK$267 by October 2022—a destruction of over $500 billion in market capitalization.

But the regulatory pressure extended beyond gaming. In November 2021, authorities ordered Tencent to give up exclusive music licensing rights, ending its competitive advantage in digital music. The company was fined for past acquisitions that hadn't received proper antitrust approval. Payment processing fees were capped. Even WeChat's dominant position came under scrutiny, with regulators forcing Tencent to open WeChat Pay to competitors and allow users to share links from rival platforms.

The market cap destruction from $900B+ to under $400B represented one of the largest wealth destructions in corporate history. At its peak in early 2021, Tencent briefly touched a market capitalization of $950 billion, making it one of the world's ten most valuable companies. By late 2022, it had fallen below $400 billion. International investors who had poured money into Chinese tech stocks during the pandemic boom faced catastrophic losses. Naspers, which had held its Tencent stake for over two decades, saw the value of its position fall by hundreds of billions.

Yet beneath the headlines, Tencent was adapting its strategy with remarkable agility. The focus on efficiency and core business became a mantra. The company cut costs aggressively, laying off employees from non-core divisions—unusual for a Chinese tech giant. Marketing spending was slashed. Marginal business units were shut down or sold. The company that had been known for aggressive expansion and experimentation suddenly became disciplined and focused.

The strategic pivots during this period revealed Tencent's resilience. Unable to pursue major acquisitions in China due to antitrust concerns, Tencent accelerated international investments. The company increased its stakes in existing portfolio companies and made new investments in European and Japanese gaming studios. When domestic gaming approvals froze for months, Tencent doubled down on developing games for international markets.

The company also embraced the government's strategic priorities. When authorities emphasized "hard tech" over consumer internet, Tencent announced massive investments in cloud infrastructure, artificial intelligence, and enterprise software. The company positioned itself as a partner in China's technological self-sufficiency drive, developing domestic alternatives to foreign software and supporting small businesses' digital transformation.

International expansion challenges revealed the double-edged sword of being a Chinese tech giant. While Tencent's gaming investments generally avoided political scrutiny, other ventures faced headwinds. In India, PUBG Mobile was banned along with dozens of other Chinese apps amid border tensions. In the United States, the Committee on Foreign Investment (CFIUS) scrutinized Tencent's investments more carefully. The company had to navigate an increasingly complex geopolitical landscape where technology had become a battlefield for great power competition.

The Snap investment illustrated both opportunities and challenges. Tencent had quietly built a 12% stake in Snapchat's parent company, but as U.S.-China tensions escalated, such investments became politically sensitive. American lawmakers questioned whether Chinese companies should be allowed to own significant stakes in U.S. social media platforms. Tencent had to maintain a delicate balance—engaged enough to protect its investments but distant enough to avoid triggering regulatory intervention.

AI initiatives became a crucial part of Tencent's recovery strategy. The company unveiled its Hunyuan large language model in 2023, positioning it as a domestic alternative to GPT models. Unlike consumer-focused AI products, Tencent emphasized enterprise applications—using AI to improve gaming development, enhance advertising targeting, and automate cloud services. This aligned with government priorities while avoiding the social concerns associated with consumer AI products.

The resilience test proved Tencent's fundamental strength. Despite the regulatory storm, the company's core businesses remained robust. Gaming revenue continued growing internationally even as domestic growth slowed. WeChat's user base remained stable, and Mini Program transactions kept expanding. The company's diverse revenue streams—gaming, advertising, fintech, cloud—provided resilience that more focused competitors lacked.

By mid-2023, signs of recovery emerged. The government, recognizing the economic importance of the tech sector and facing its own economic challenges, began softening its stance. Gaming approvals resumed, though at a slower pace. Regulatory clarity improved, with authorities publishing clearer rules rather than ruling through unpredictable crackdowns. International investors, seeing the worst was over, began tentatively returning.

Tencent emerged stronger in several ways. The efficiency drive had improved margins significantly. The company had proven it could generate substantial cash flow even in the worst conditions. The forced focus on core businesses had eliminated distractions. Most importantly, Tencent had demonstrated that it could adapt to any regulatory environment—a crucial capability for long-term survival in China's state-guided capitalism.

The stock price recovery from the October 2022 lows has been remarkable, with shares more than doubling from the trough. By 2024, Tencent's market capitalization had recovered to around $450 billion—still below the peaks but representing a dramatic recovery from the depths of the regulatory crisis.

The new reality for Tencent is one of constrained but sustainable growth. The days of unchecked expansion and winner-take-all competition are over. The company must balance growth with social responsibility, profits with common prosperity, and innovation with stability. It's a more complex operating environment, but one that may ultimately produce a more sustainable business model.

VIII. Financial Performance & Business Model Analysis

The numbers tell a story of resilience that few corporations could match. In Q3 2024, Tencent reported revenue of RMB 167.2 billion ($23.2 billion), up 8% year-over-year, with net profit of RMB 53.2 billion ($7.4 billion), surging 47% from the previous year. These weren't just recovery metrics—they represented a business model that had been stress-tested through regulatory hell and emerged more profitable than ever.

The revenue breakdown reveals a carefully orchestrated diversification strategy. Gaming, still the crown jewel, generated RMB 51.8 billion (31% of total revenue), with international gaming revenue growing 11% year-over-year to RMB 14.5 billion. The shift toward international markets—now representing 28% of gaming revenue—demonstrates Tencent's successful geographic diversification. Titles like PUBG Mobile, Call of Duty Mobile, and League of Legends continue dominating global charts, proving that Tencent's gaming expertise transcends cultural boundaries.

Social networks revenue, primarily from WeChat and QQ, reached RMB 30.7 billion, growing 4% year-over-year. While growth has moderated from the explosive rates of the previous decade, the stability of this revenue stream provides ballast for the entire business. Video accounts monetization is still in early stages, with enormous potential as engagement metrics approach those of dedicated short-video platforms.

The real surprise has been advertising revenue, which reached RMB 25.7 billion, up 17% year-over-year—remarkable growth in a challenging economic environment. The recovery was driven by Video Accounts advertising, which grew over 60% year-over-year, and improved Mini Program advertising capabilities. Tencent's advertising revenue per user remains far below that of Western peers like Meta, suggesting significant room for growth without degrading user experience.

Fintech and business services, the segment including WeChat Pay and cloud services, generated RMB 53.1 billion, up 2% year-over-year. The modest growth masks a dramatic shift in composition. Payment revenue has been pressured by regulatory caps on transaction fees, but cloud services and enterprise software have grown rapidly, now representing over 40% of segment revenue. This shift from consumer to enterprise services aligns with government priorities and provides more stable, higher-margin revenue streams.

The virtuous cycle that Tencent has built—Social → Gaming → Payments → Everything—creates compounding advantages. A new user joining WeChat for messaging discovers Mini Programs for services, uses WeChat Pay for transactions, gets introduced to Tencent's games through social features, and eventually becomes embedded in an ecosystem that touches every aspect of digital life. Each additional service increases switching costs and customer lifetime value.

This ecosystem effect shows in user metrics. WeChat's 1.38 billion monthly active users spend an average of over 90 minutes daily on the platform. The average user opens WeChat 10+ times per day. Mini Program users exceed 1 billion, with average transactions per user growing 20% annually. These aren't just users—they're citizens of Tencent's digital nation, conducting their daily lives within its borders.

Margin expansion through operating leverage has been remarkable. Despite revenue growing at high single digits, operating profit has grown at double that rate. The key has been the inherent scalability of digital platforms. The marginal cost of serving an additional WeChat user or game player is essentially zero. Fixed costs for infrastructure and development are spread across an ever-larger base. Marketing efficiency has improved as the ecosystem markets itself—users bring their friends and family into WeChat and Tencent's games naturally.

The company's operating margin reached 35% in Q3 2024, up from 31% a year earlier. This expansion occurred despite continued investment in AI, cloud infrastructure, and international expansion. Management has guided toward continued margin improvement, targeting 40%+ operating margins in the medium term as the business mix shifts toward higher-margin services and operational efficiency improves further.

Capital allocation at Tencent reflects both confidence and pragmatism. The company has accelerated share buybacks, repurchasing over HK$100 billion worth of shares in 2024 alone. This represents a dramatic shift from the acquisition-heavy strategy of the previous decade. With domestic M&A effectively frozen by regulatory concerns and international acquisitions facing geopolitical headwinds, returning capital to shareholders has become the default option.

R&D investment continues at massive scale, exceeding RMB 60 billion annually (about 9% of revenue). This R&D intensity matches or exceeds most Western tech giants, funding everything from game development to AI research to quantum computing experiments. The company has over 20,000 engineers and technical staff, with major research centers in Shenzhen, Beijing, Shanghai, and Seattle.

The investment portfolio remains a hidden asset on Tencent's balance sheet. Stakes in companies like Epic Games, Snap, Sea Limited, and hundreds of smaller companies are carried at historical cost but worth far more at current valuations. Analysts estimate the portfolio's market value exceeds $150 billion, though Tencent has been selectively trimming positions both to generate cash for buybacks and to address regulatory concerns about monopolistic behavior.

Comparison with global tech peers reveals both Tencent's strengths and the "China discount." On fundamental metrics, Tencent compares favorably with any global tech giant. Its revenue growth matches Microsoft's, its margins approach those of Google, and its return on equity exceeds Apple's. Yet it trades at a significant discount—roughly 15x forward earnings compared to 25-30x for U.S. tech giants.

This valuation gap reflects real risks: regulatory uncertainty, geopolitical tensions, and currency controls that complicate capital returns. But it also reflects more nebulous concerns about Chinese corporate governance, data transparency, and the ultimate control of the Communist Party over private enterprises. For investors, the question becomes whether these risks justify a 40-50% discount to Western peers with similar financial characteristics.

The balance sheet strength provides a buffer against any storm. Tencent holds over RMB 250 billion in cash and equivalents, with minimal debt. Free cash flow generation exceeds RMB 150 billion annually. This fortress balance sheet allowed Tencent to weather the regulatory storm without financial distress and provides flexibility for future investments or increased shareholder returns.

The business model's evolution from virtual goods seller to platform orchestrator represents one of the most successful transformations in technology history. Tencent began by selling digital clothing for QQ avatars. Today, it operates platforms that process trillions in transactions, host billions of social interactions, and entertain hundreds of millions of gamers daily. The journey from product to platform to ecosystem created compounding competitive advantages that become stronger with scale.

Looking at unit economics reveals the model's elegance. Customer acquisition cost approaches zero for most services—users join WeChat because their friends are there, download games because of social recommendations, and use payment services because they're already embedded. Lifetime value is essentially infinite for core users who conduct their digital lives within Tencent's ecosystem. The ratio of LTV to CAC—the fundamental metric of digital business models—approaches theoretical maximums.

IX. AI, Cloud & The Future Battlegrounds (2023-Beyond)

Inside Tencent's AI lab in Shenzhen, engineers are training models not to write poetry or generate images, but to make video game characters feel alive, to predict payment fraud with microsecond precision, and to optimize cloud infrastructure in real-time. This pragmatic approach to artificial intelligence—focused on enhancing existing products rather than chasing AGI dreams—exemplifies Tencent's strategy for the next decade.

Tencent Hunyuan, the company's large language model debuted in 2023 for enterprise use, marking Tencent's entry into the LLM race. But unlike Western companies positioning AI as revolutionary consumer products, Tencent embedded Hunyuan across its existing ecosystem. Game developers use it to generate dialogue and design levels. Advertisers employ it for copywriting and targeting. Cloud customers access it for code generation and data analysis.

The infrastructure investments tell a story of massive ambition. Tencent has committed over $70 billion to technology infrastructure through 2028, building data centers across China and expanding internationally. The company operates over 1 million servers globally, with particular emphasis on GPU clusters for AI training. This isn't just supporting existing services—it's building the foundation for an AI-native future.

Yuanbao AI assistant, launched in 2024, represents Tencent's consumer-facing AI strategy. Integrated into WeChat and QQ, Yuanbao can answer questions, summarize articles, and assist with tasks—but always within Tencent's ecosystem walls. Rather than competing with ChatGPT directly, Yuanbao enhances the super-app experience, making WeChat even more indispensable. Early adoption has exceeded 50 million users, with daily queries surpassing 100 million.

The competitive positioning in AI reveals both advantages and challenges. Tencent has unmatched data from billions of social interactions, gaming sessions, and transactions. Its compute infrastructure rivals any tech giant's. The ecosystem provides perfect distribution and monetization channels. Yet the company faces constraints: regulatory oversight of AI development, restrictions on data usage, and the challenge of competing globally while operating primarily in Chinese.

Cloud services and enterprise transformation have become unexpected growth drivers. While Alibaba dominates China's public cloud market, Tencent has carved out niches in gaming infrastructure, video streaming, and enterprise collaboration. The acquisition of Sogou's enterprise products and aggressive pricing have helped Tencent Cloud grow to over 18% market share in China. International expansion, particularly serving Chinese companies going global and international companies entering China, provides a differentiated strategy.

The integration of AI across products is happening at breathtaking pace. In gaming, AI-powered NPCs (non-player characters) in Honor of Kings can now adapt to individual playing styles, making single-player modes feel multiplayer. In advertising, AI optimizes bidding and placement in real-time, improving ROI by 30-40%. In fintech, AI models detect fraud patterns that human analysts would never spot, saving billions in potential losses.

WeChat's AI transformation deserves special attention. The platform now uses AI for content recommendation in Moments and Video Accounts, competing directly with ByteDance's legendary algorithm. Machine translation enables cross-language communication, crucial for international business. Voice recognition and natural language processing power the growing trend of voice-based Mini Programs. The platform that started as simple messaging has become an AI-orchestrated digital experience.

International expansion remains the trillion-yuan question. Can WeChat work outside China? The attempts have been mixed. WeChat has over 100 million users outside China, primarily among Chinese diaspora and businesses dealing with China. But mainstream adoption in Western markets remains elusive. The super-app model faces regulatory resistance, user skepticism about putting everything in one app, and competition from entrenched players.

Yet Tencent's international strategy has evolved beyond WeChat export. The company now focuses on providing infrastructure and services that work behind the scenes. Tencent Cloud serves international gaming companies. Its AI models power applications users never know are Tencent-powered. The investment portfolio provides exposure to international markets without operational complexity. It's a humble approach that may prove more successful than aggressive expansion.

Competition with ByteDance represents the defining rivalry of Chinese tech's next decade. ByteDance's Douyin/TikTok has captured user attention globally with its addictive algorithm. Its Feishu/Lark enterprise products compete with Tencent in workplace collaboration. The companies battle for gaming talent and IP. Yet they also coexist—many users have both WeChat and Douyin on their phones, using them for different purposes.

The ByteDance threat is real but manageable. While Douyin dominates entertainment, WeChat owns utility. Users might spend hours on Douyin, but they live their lives on WeChat. The platforms serve different needs, and Tencent's ecosystem lock-in provides defensive moats. Video Accounts may never match Douyin's engagement, but it doesn't need to—it just needs to keep users within WeChat's walls.

Alibaba presents a different competitive dynamic. Once fierce rivals in payments and cloud, the companies have reached a détente partly enforced by regulators wary of winner-take-all dynamics. They've opened their platforms to each other's services and even collaborate on some initiatives. The competition continues but within boundaries that prevent mutual destruction.

New entrants pose limited threats to Tencent's core franchises but could nibble at the edges. Companies like Xiaohongshu (Little Red Book) have carved out niches in social commerce. Gaming studios like miHoYo (Genshin Impact) have proven that Tencent doesn't monopolize gaming innovation. Yet none threaten the core ecosystem that makes Tencent indispensable to Chinese digital life.

The next S-curves reveal where Tencent places its bets for the future. The metaverse, despite Meta's struggles, remains a long-term focus. Tencent's advantages—gaming expertise, social platforms, payment infrastructure—position it perfectly for virtual worlds. The company has been quietly building capabilities, from virtual concerts in games to digital collectibles on blockchain infrastructure.

Autonomous vehicles represent another frontier. While Tencent isn't building cars, it's providing the digital infrastructure for China's automotive transformation. WeChat integration in vehicles, cloud services for autonomous driving companies, and HD mapping services position Tencent as a crucial enabler of mobility transformation. The company has invested in several AV startups and partnered with traditional automakers on smart cabin technology.

Healthcare technology has emerged as a strategic priority aligned with government goals. WeChat already hosts thousands of hospital Mini Programs for appointment booking and result checking. Tencent's AI assists in medical imaging analysis. The company has invested in digital health platforms and telemedicine services. The aging population and healthcare system strain create enormous opportunities for digital transformation.

The international gaming push continues with massive investments. New studios in Los Angeles, Montreal, and Tokyo are developing AAA titles for global release. Partnerships with Hollywood studios bring IP for game adaptation. The success of games like PUBG Mobile and Call of Duty Mobile proves Tencent can compete globally. Gaming may be the vector through which Tencent truly becomes a global company.

Blockchain and Web3 present complex opportunities. While cryptocurrency remains banned in China, blockchain technology is government-endorsed for applications like supply chain tracking and digital identity. Tencent has patents for numerous blockchain innovations and operates consortium chains for various industries. International gaming provides a sandbox for NFT and token experiments outside China's borders.

The sustainability technology initiative reflects both regulatory pressure and genuine opportunity. Tencent has committed to carbon neutrality by 2030, investing in renewable energy for data centers and AI optimization for energy efficiency. The company's technology helps other businesses reduce emissions through cloud migration and process digitization. Green technology could become a significant business as China pursues its dual carbon goals.

X. Playbook: Lessons for Founders & Investors

The "fast follower" strategy that built Tencent offers profound lessons that challenge Silicon Valley orthodoxy. While Western culture celebrates first movers and original invention, Tencent proved that excellence in execution, localization, and monetization can be more valuable than being first. QQ copied ICQ, but made it work for Chinese internet cafés. WeChat followed WhatsApp and Kik, but created the super-app. The lesson isn't that copying is good, but that solving real user problems matters more than being original.

The key insight is that innovation comes in many forms. Product innovation—creating something entirely new—is just one path. Business model innovation, distribution innovation, and localization innovation can be equally powerful. Tencent's virtual goods model, pioneered with QQ Show, predated and influenced Western free-to-play gaming. The company didn't invent messaging or gaming, but it invented new ways to monetize and distribute them.

Building ecosystems versus standalone products represents perhaps Tencent's most important strategic insight. Every successful Tencent product becomes a platform for the next. QQ users became gamers. Gamers needed payment methods. Payment users discovered Mini Programs. Mini Program developers needed cloud services. Each layer reinforces the others, creating compounding competitive advantages that standalone products can never achieve.

The ecosystem approach requires patient capital and long-term thinking. Many Tencent services ran at losses for years while building user bases. WeChat didn't generate significant revenue for its first three years. Cloud services required massive upfront investment. This patience is only possible with either founder control or extremely aligned investors—Tencent had both with Pony Ma's leadership and Naspers' hands-off approach.

The power of patient capital cannot be overstated. Naspers' 2001 investment of $32 million for 46.5% of Tencent has grown to be worth over $100 billion—one of the greatest venture investments in history. But this return required holding through SARS, the global financial crisis, multiple regulatory crackdowns, and 80% drawdowns. Most investors would have sold during any of these crises. Naspers' patience wasn't passive—they provided expertise and connections—but they resisted the temptation to over-manage or exit prematurely.

Virtual goods and microtransaction psychology revealed a fundamental truth about human behavior: people value digital status and self-expression enough to pay for it. Tencent discovered this with QQ Show avatars and perfected it across gaming. The key insights: make base products free to maximize reach, offer paid customization for self-expression, create social dynamics where purchases are visible, and keep individual transaction sizes small to reduce friction.

The psychology goes deeper than simple vanity. Virtual goods satisfy fundamental human needs: belonging (team uniforms in games), achievement (rare items showing skill), creativity (customization options), and social connection (gifts to friends). Tencent understood these motivations intuitively and designed monetization systems that felt like features, not taxes.

Platform thinking—treating every product as a distribution channel—multiplied Tencent's effectiveness. When Tencent launched a new game, it had immediate distribution through QQ and WeChat. When it needed payment processing adoption, it could mandate integration across all services. When cloud services launched, thousands of Mini Program developers were natural customers. This platform leverage means Tencent's customer acquisition costs approach zero for new services.

The platform advantage extends beyond distribution to data and insights. Every user interaction across any Tencent service informs product development, advertising targeting, and risk management across all services. This data network effect creates an intelligence advantage that grows with scale. A standalone company could never match Tencent's understanding of user behavior derived from billions of daily interactions across dozens of touchpoints.

Managing regulatory risk in emerging markets requires a delicate dance that Western companies often fumble. Tencent mastered the art of being successful enough to matter but not so dominant as to threaten. The company maintained close government relationships, aligned with policy priorities, and accepted regulatory constraints as the cost of doing business. When regulations changed, Tencent adapted quickly rather than fighting.

The regulatory playbook includes several key principles: maintain multiple revenue streams to survive hits to any one business, keep significant operations and employment in the home country, invest in government priorities like AI and semiconductors, accept that some profits must be shared through taxes and social programs, and never challenge political authority directly or indirectly.

The importance of founder-led long-term thinking shows in every major Tencent decision. Pony Ma, still CEO after 26 years, provides consistency rare in tech companies. He's technical enough to understand products, strategic enough to see long-term trends, and humble enough to admit mistakes and change course. His low profile—rarely giving interviews or public speeches—contrasts with celebrity tech CEOs but fits Chinese cultural preferences.

Founder leadership enabled bold bets that professional managers might avoid. Investing billions in gaming when it was considered frivolous. Building WeChat when QQ was still growing. Accepting lower margins to build ecosystems. These decisions require someone with skin in the game, thinking in decades not quarters. The contrast with professionally managed competitors who optimize for short-term metrics is stark.

The acquisition integration philosophy—buying companies but preserving cultures—differed from typical M&A approaches. Riot Games kept its Los Angeles headquarters and creative independence. Supercell maintained its cell structure and Helsinki base. Epic Games continued operating independently despite Tencent's 40% stake. This hands-off approach preserved the magic that made these companies valuable while providing resources and market access they couldn't achieve alone.

The integration philosophy extends to operational support. Tencent provides acquired companies with user acquisition expertise, monetization best practices, and live operations capabilities developed over decades. But it doesn't impose standardized processes or cultural uniformity. Each studio maintains its identity while benefiting from Tencent's scale. It's federation, not empire.

The importance of timing can't be ignored. Tencent rode multiple waves perfectly: China's internet adoption, the mobile transition, the gaming boom, and the super-app era. But this wasn't luck—it was preparation meeting opportunity. The company maintained capabilities across multiple fronts, allowing it to capitalize when conditions aligned. Many competitors focused too narrowly and missed transitions.

XI. Bear vs Bull Case & Valuation

The bull case for Tencent starts with ecosystem lock-in so profound that it's essentially infrastructure. WeChat isn't just an app in China—it's the digital nervous system of the world's second-largest economy. With 1.38 billion users spending 90+ minutes daily, generating trillions in transaction value, the platform has achieved a position that would take decades and hundreds of billions of dollars to replicate—if it's even possible given regulatory and network effect barriers.

Gaming dominance provides the second pillar of the bull case. Tencent owns or has significant stakes in many of the world's most valuable gaming franchises: League of Legends, Fortnite (40% via Epic), PUBG Mobile, Honor of Kings, Clash of Clans (84% via Supercell), and Call of Duty Mobile. Gaming is growing faster than any other form of entertainment, and Tencent controls more premium gaming IP than any other company. The shift to games-as-a-service models means these aren't just games but annuity streams generating predictable, high-margin revenue for decades.

The AI upside remains largely unmonetized. Tencent has the data, compute infrastructure, and distribution channels to be an AI winner, but hasn't yet pulled the monetization lever hard. AI-enhanced advertising could double revenue per user. AI-powered enterprise services could transform the cloud business. AI agents in games could revolutionize engagement and monetization. The company investing RMB 60+ billion annually in R&D will eventually see returns that could transform the business.

The valuation discount to global peers is perhaps the most compelling bull argument. At 15x forward earnings, Tencent trades at a 40-50% discount to comparable U.S. tech giants. Even adjusting for country risk, this gap seems excessive for a company with similar growth rates, higher margins than many peers, and comparable competitive positions. If the discount narrows even partially—say to 20x earnings—the stock would appreciate 33%.

The hidden asset value in the investment portfolio provides additional upside. Stakes in Epic, Snap, Sea Limited, and hundreds of other companies are worth an estimated $150+ billion but largely unmarked on the balance sheet. Tencent has been selectively monetizing these investments, generating cash for buybacks while maintaining strategic positions. This portfolio could be worth $50+ per share alone.

International expansion potential remains enormous. While WeChat may not conquer Western markets, Tencent's gaming properties are truly global. International gaming revenue is growing double-digits and could eventually exceed domestic gaming. Cloud services for gaming companies, AI models for enterprise use, and fintech infrastructure for emerging markets all represent massive opportunities barely scratched.

The bear case begins with regulatory overhang that may never fully lift. The 2021 crackdown showed that the Chinese government can destroy hundreds of billions in value overnight with regulatory changes. While the worst appears over, the threat remains. Future regulations on AI, data usage, gaming, or payments could materially impact Tencent's business. The uncertainty itself demands a valuation discount.

Growth slowdown concerns are real and structural. China's economy is maturing, with GDP growth slowing from double digits to mid-single digits. The internet penetration story is complete—everyone who will use WeChat already does. Gaming faces both demographic headwinds (aging population) and regulatory constraints (limits on new game approvals and minor usage). The hyper-growth days are definitively over.

Geopolitical risk has evolved from tail risk to central concern. U.S.-China tensions could impact Tencent in multiple ways: forced divestiture of U.S. assets, restrictions on technology transfer, loss of access to advanced semiconductors, or even delisting from U.S. exchanges (though Tencent primarily lists in Hong Kong). The possibility of Taiwan conflict, while hopefully remote, would be catastrophic for Chinese asset prices.

Competition from ByteDance and others is intensifying. ByteDance has proven that Tencent's moats aren't impenetrable, building a global empire with TikTok/Douyin. In gaming, companies like miHoYo have shown that hit games can come from anywhere. In enterprise services, Alibaba and Huawei have stronger positions. Tencent must defend on multiple fronts while facing constraints on acquisition-driven growth.

The China discount may be permanent, reflecting real differences in corporate governance, rule of law, and capital controls. VIE structures that allow foreign ownership remain legally uncertain. The ultimate control of the Communist Party over private enterprises is a risk without parallel in Western markets. Currency controls complicate returning capital to international shareholders. These aren't risks that will disappear with time—they're structural features of investing in China.