Salesforce: From Upstart to Enterprise Software Empire

I. Introduction & Episode Roadmap

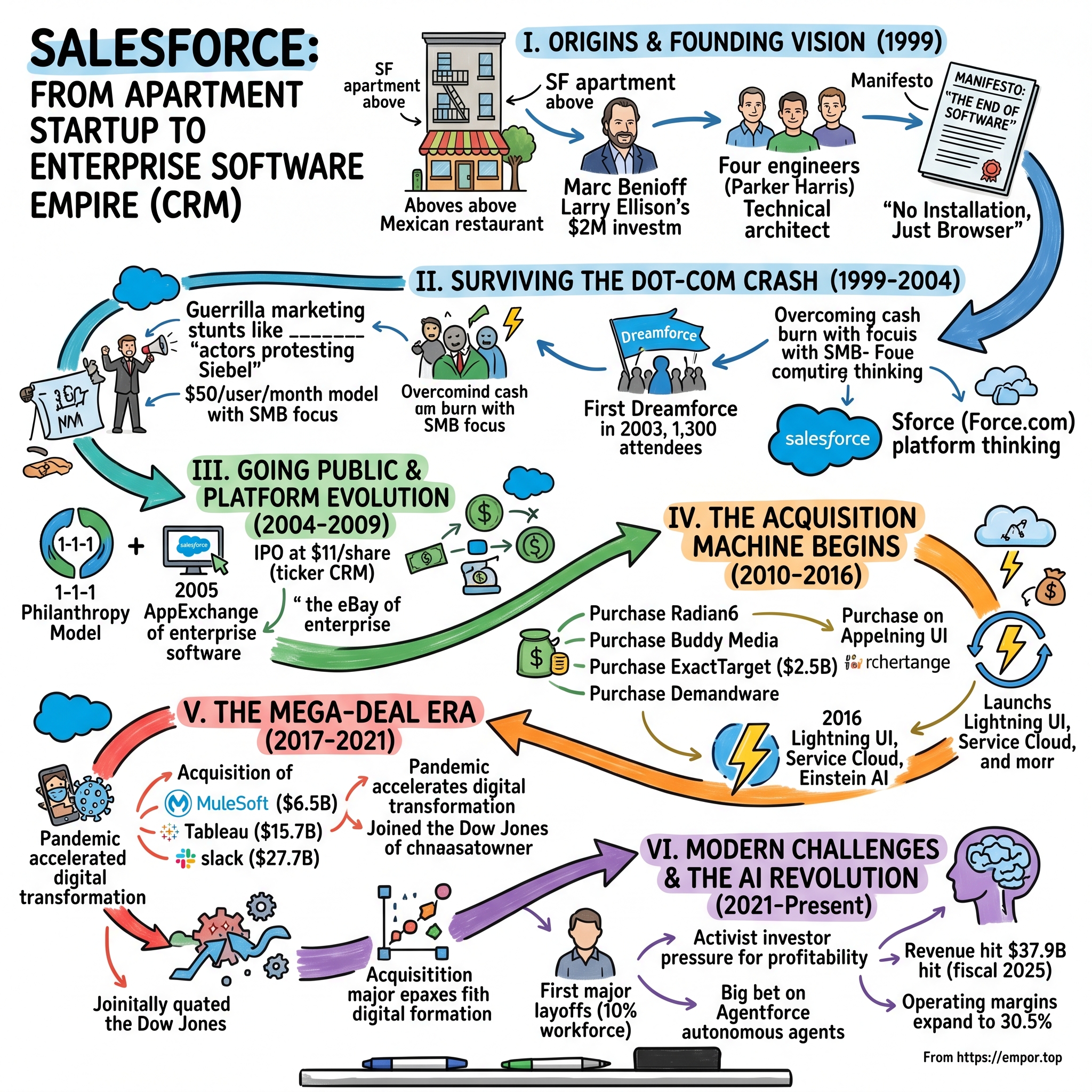

Picture this: March 1999, a cramped San Francisco apartment above a Mexican restaurant, four engineers huddled around borrowed computers, and a radical manifesto taped to the wall—"The End of Software." Marc Benioff, fresh off a spiritual sabbatical in Hawaii, is pitching his co-founders on an idea so audacious that even his mentor Larry Ellison thought he was crazy: What if enterprise software didn't require installation? What if it just... worked, right from your browser?

Twenty-five years later, that apartment startup has become Salesforce, a $300 billion colossus that fundamentally rewrote the rules of enterprise software. From its theatrical IPO in 2004—when the stock soared 55% on day one at $11 per share—to today's price hovering around $330, Salesforce hasn't just grown; it's consumed entire categories of business software, acquiring everything in its path like a benevolent Pac-Man with a social conscience. The CRM that ate enterprise software: How a San Francisco apartment startup became a $235 billion behemoth. Picture Marc Benioff pacing that cramped apartment in 1999, pitching his co-founders on what seemed like technical heresy—enterprise software that required no installation, no servers, no IT department headaches. Just open a browser and start selling.

From its theatrical IPO in 2004—when the stock soared at $11 per share—to today's price around $246, Salesforce hasn't just grown; it's consumed entire categories of business software. The company that started with four engineers has swelled to 76,450 employees, generating $37.9 billion in fiscal 2025 revenue—a testament to one of the most successful platform plays in technology history.

This is a story of three acts: First, the scrappy startup that survived the dot-com crash through sheer theatrical marketing genius and a radical business model. Second, the platform company that turned customers into developers and acquisitions into growth engines. And third, the enterprise colossus grappling with the laws of large numbers while betting its future on artificial intelligence agents that could fundamentally reshape how businesses operate.

What makes Salesforce particularly fascinating for students of business strategy is how it repeatedly reinvented itself without losing its core identity. The "No Software" rebels became the software establishment. The CRM specialists became a platform for everything. The growth-at-all-costs unicorn transformed into a profit-generating machine when activist investors came knocking. Each transformation required not just strategic vision but cultural revolution—and somehow, Benioff orchestrated them all while maintaining his image as both a spiritual guru and ruthless competitor.

II. Origins: The Oracle Years & The Founding Vision

The origin story begins not in Silicon Valley's garages but in the gleaming towers of Oracle, where a young Marc Benioff was making waves. At 23, he became Oracle's youngest vice president ever—a wunderkind who'd already displayed his entrepreneurial DNA by creating "How to Juggle" software at 14 (sold for $75 a pop) and founding Liberty Software at 15, building Atari games that generated $1,500 monthly royalties while he was still in high school.

But by 1996, after thirteen years at Oracle, Benioff was burning out. The relentless corporate grind had taken its toll. Larry Ellison, his mentor and Oracle's legendary CEO, suggested something unconventional: take a sabbatical. Go to Hawaii. Clear your head. What happened next would reshape enterprise software forever.

In Hawaii, Benioff didn't just relax on beaches—though there was plenty of that. He swam with dolphins, which he later described as a quasi-spiritual experience that helped him think differently about technology's role in the world. He met with Hindu gurus and meditation teachers who challenged him to think about business as a vehicle for social change, not just profit. The seeds of what would become Salesforce's famous 1-1-1 philanthropy model—dedicating 1% of equity, product, and employee time to charitable causes—were planted in those Hawaiian meditation sessions.

When Benioff returned to the mainland in 1998, he couldn't shake a persistent thought: Why was enterprise software so terrible? Why did companies need armies of consultants and IT specialists just to track customer relationships? The internet had already revolutionized consumer experiences—Amazon was selling books, eBay was hosting auctions. Why couldn't enterprise software be that simple?

The technical epiphany came while attending a conference where Oracle was demonstrating its latest CRM software. Installation alone took months. Customization required more months. Training? Even more months. The total cost could reach millions. Benioff thought: "This is insane. Why can't this just work like Amazon?"

In March 1999, Benioff recruited three engineers who shared his vision. Parker Harris, who'd worked with him at Left Coast Software, became the technical architect who could actually build this cloud-based dream. Dave Moellenhoff brought deep CRM expertise from his time at Clarify. Frank Dominguez rounded out the founding team with his systems architecture knowledge.

The four founders set up shop in a Telegraph Hill apartment, with Benioff famously writing "The End of Software" on the wall—a manifesto that would become their battle cry. But they needed capital. Here's where Benioff's Oracle connections paid off spectacularly: Larry Ellison himself invested $2 million, taking a 25% stake. The irony wasn't lost on anyone—Oracle's CEO funding a company whose mission was to destroy Oracle's business model.

Ellison's investment came with conditions. He insisted Benioff officially leave Oracle before launching Salesforce (Benioff had initially planned to moonlight). But Ellison also provided something invaluable: credibility. When the founder of enterprise software's biggest company backs your "end of software" startup, people pay attention.

The early product was deliberately simple—almost primitively so compared to existing CRM systems. No modules for manufacturing. No supply chain management. No complex financial forecasting. Just the basics: track leads, manage accounts, monitor opportunities. Harris coded the initial version in just a few months, building everything on commodity hardware and open-source databases. The simplicity was the point.

The business model was even more radical than the technology. Instead of charging hundreds of thousands upfront for licenses, Salesforce would charge $50 per user per month. No installation fees. No consultants. No hardware purchases. Just subscribe and start selling. Wall Street analysts called it "financial suicide"—how could you build a sustainable business on such tiny monthly payments?

The founding team had an answer: volume and virality. Make it so easy to try that sales teams would adopt it without IT approval. Make it so affordable that managers could expense it on credit cards. Make it so useful that once teams started using it, they'd never stop. The subscription model wasn't just about technology—it was about fundamentally changing software's power dynamics, shifting control from IT departments to end users.

By late 1999, they had a working prototype and a handful of beta customers. The apartment was getting crowded with new hires. Benioff was evangelizing at every conference, often wearing his signature "No Software" logo—a red circle with a line through the word "software," deliberately mimicking anti-establishment protest symbols. Oracle executives were not amused. Siebel Systems, then the CRM market leader, dismissed them as "not serious."

They were about to become very serious indeed. The dot-com boom was creating thousands of new companies that needed CRM but couldn't afford traditional solutions. Salesforce was perfectly positioned to capture this market—if they could survive what was about to come. The apartment startup was about to face its first existential crisis, and how they navigated it would determine whether "The End of Software" was prophetic or merely provocative.

III. The Early Years: Surviving the Dot-Com Crash (1999–2004)

February 2000: Siebel Systems was hosting its annual user conference at the Los Angeles Convention Center, a gathering of thousands of CRM professionals. Outside, something unprecedented was happening. Protesters carrying signs reading "The End of Software" and "No Software" were marching, chanting slogans against enterprise software complexity. TV crews showed up. Attendees stopped to watch. Security was called.

The "protesters"? Actors hired by Marc Benioff for $20 an hour.

This guerrilla marketing stunt—which Benioff called "tactical theater"—perfectly captured early Salesforce's David-versus-Goliath mentality. With minimal marketing budget, they generated massive attention by positioning themselves as revolutionaries against the enterprise software establishment. Siebel executives were furious. The press ate it up. Salesforce had announced itself to the world not through traditional channels but through calculated controversy.

The timing seemed perfect. The dot-com boom was creating a gold rush of startups, each needing CRM but lacking the resources for traditional solutions. By mid-2000, Salesforce had grown to 150 employees and was burning through cash to capture market share. Revenue was accelerating: from essentially zero in 1999 to $5.4 million in fiscal 2001.

Then the music stopped.

The dot-com crash of 2000-2001 wasn't just a market correction—it was an extinction event for technology companies. Salesforce's target market of venture-funded startups evaporated almost overnight. Customers disappeared. Those that survived stopped buying new software. The company that had positioned itself as the CRM for the new economy suddenly found itself selling into an economy that no longer existed.

By early 2001, Salesforce was hemorrhaging money. The board pressured Benioff to cut costs dramatically. In one of the most painful decisions of his career, he laid off 20% of the workforce—people he'd personally recruited with promises of changing the world. The remaining employees took pay cuts. Benioff himself went without salary for several months.

But the crisis forced innovation. If startups couldn't buy Salesforce, who could? The answer: small and medium businesses that still existed but had been ignored by enterprise software vendors. Salesforce pivoted its messaging from "CRM for the new economy" to "CRM for every economy." They introduced a free trial—revolutionary at the time—letting potential customers test the product without talking to a salesperson.

The numbers tell the survival story: revenue grew to $22.4 million in fiscal 2002, then $51 million in 2003. Not explosive growth, but steady progress through the darkest period in technology history. They achieved this by solving a problem the crash had actually exacerbated: companies needed to do more with less. Salesforce let them deploy CRM without capital expenditure, without IT staff, without the risk of a failed implementation.

The product evolved rapidly during this period. The original version was, frankly, simplistic—Harris later admitted it was "embarrassingly basic" compared to Siebel. But simplicity became a virtue when companies were firing IT staff. Each quarter, Salesforce pushed updates directly to all customers simultaneously—no installation required. This continuous delivery model, now standard in SaaS, was revolutionary in 2002.

Competition during this period was fierce but confused. Siebel tried to respond with "Siebel OnDemand," but it was essentially their traditional software hosted in Siebel's data center—lipstick on the legacy pig. Oracle launched various hosted offerings that never gained traction. Microsoft was still focused on desktop software. The incumbents couldn't pivot without cannibalizing their lucrative license revenue.

The real breakthrough came in 2003 with the first Dreamforce conference. Benioff, ever the showman, wanted to create "the Woodstock of cloud computing." The first event drew 1,300 attendees to San Francisco's Westin St. Francis hotel—tiny by today's standards but significant for a company most still considered a curiosity. The conference did more than showcase products; it created a community, a movement of businesses embracing the cloud before "cloud" was even the term.

Dreamforce also marked Salesforce's evolution from product to platform thinking. At the event, Benioff announced Sforce (later Force.com), allowing customers to customize Salesforce beyond recognition. This wasn't just configuration—it was a development platform. Customers could build entirely new applications on Salesforce's infrastructure. The CRM company was becoming something else entirely: a platform company.

By late 2003, the metrics were undeniable. Revenue hit $100 million run rate. The company had 8,000 customers and 200,000 subscribers. Customer satisfaction scores consistently exceeded 90%. The subscription model, once mocked, was proving its power: predictable revenue, high retention rates, and customers who became more valuable over time rather than less.

The sales organization Benioff built during this period became the template for all SaaS companies. Instead of enterprise sales reps making million-dollar deals, Salesforce employed inside sales teams making thousands of small deals monthly. They pioneered the "land and expand" strategy—start with a small team, prove value, then grow within the organization. Sales cycles shortened from 18 months to 18 days.

Marketing remained theatrical. The "No Software" logo appeared on everything from t-shirts to taxi tops. Benioff staged another protest at a Oracle conference. He sent Siebel executives copies of Sun Tzu's "The Art of War" with passages about disruption highlighted. Some called it juvenile; others recognized genius-level brand building on a shoestring budget.

The IPO roadshow began in early 2004. Investment bankers were initially skeptical—subscription revenue was still a foreign concept to Wall Street. But the numbers were compelling: growing at 60% annually, approaching profitability, with subscription renewal rates above 90%. The question wasn't whether Salesforce would go public, but whether the market was ready for a pure-play SaaS company.

IV. Going Public & Platform Evolution (2004–2009)

June 23, 2004: The New York Stock Exchange floor was buzzing with unusual energy. Marc Benioff, wearing his signature Hawaiian shirt under his suit jacket, rang the opening bell as Salesforce began trading under the ticker "CRM"—a audacious claim to the entire category. The IPO price of $11 per share valued the company at $1.1 billion. By day's end, the stock had soared 55% to $17.00. The subscription software model had been validated by the ultimate judge: public markets.

Fiscal 2005 revenue hit $176 million, and the company now employed 767 people. But Benioff wasn't celebrating. During the IPO roadshow, he'd heard the same question repeatedly: "What happens when Microsoft enters your market?" His answer was about to reshape Salesforce's entire strategy.

The platform pivot began almost immediately after going public. Benioff realized that competing solely as a CRM vendor meant eventual commoditization. But what if Salesforce wasn't just software you used, but infrastructure you built upon? What if every customer became a potential developer? This thinking led to one of enterprise software's most important innovations: the AppExchange.

Launched in 2005, AppExchange was positioned as "the eBay of enterprise software." Third-party developers could build applications on Salesforce's platform and sell them to Salesforce customers. The first apps were simple—industry-specific modifications, integration tools, reporting enhancements. But the implications were profound. Salesforce was no longer a product company; it was becoming an ecosystem.

The technical foundation for this platform play was Force.com, introduced gradually between 2004 and 2007. This wasn't merely opening up APIs—it was exposing Salesforce's entire development environment to external developers. Custom objects, workflow rules, approval processes, even Salesforce's proprietary Apex programming language. Customers could build applications that had nothing to do with CRM but ran on Salesforce's infrastructure.

The numbers validated the platform strategy. By 2006, over 300 applications were available on AppExchange. By 2008, that number exceeded 800. More importantly, customers using AppExchange applications had significantly higher retention rates—they weren't just using Salesforce, they were building their businesses on it. Switching costs increased exponentially when your custom applications, integrations, and workflows all depended on Salesforce's platform.

Competition intensified during this period, but in unexpected ways. Microsoft finally entered with Dynamics CRM in 2003, but it was primarily on-premise software trying to look cloudy. Oracle acquired Siebel for $5.85 billion in 2005—a defensive move that validated Salesforce's disruption. SAP remained focused on large enterprises. The real competition came from an unexpected source: Google.

Google launched Google Apps for Business in 2006, offering email, documents, and collaboration tools via browser. While not direct CRM competition, it validated and accelerated cloud adoption. Suddenly, running business applications in browsers wasn't radical—it was rational. Salesforce cleverly positioned itself as complementary to Google Apps, even building integrations, turning a potential threat into market validation.

The financial crisis of 2008-2009 should have devastated Salesforce. Enterprises were slashing IT budgets. Sales teams were being reduced. Credit was frozen. Yet Salesforce not only survived but thrived. Revenue crossed $1 billion in fiscal 2009, a symbolic milestone that placed them among enterprise software's elite.

Why did Salesforce thrive during the recession? The subscription model that once seemed risky now appeared prudent. CFOs loved predictable operating expenses versus volatile capital expenditures. The ability to scale up or down monthly—impossible with traditional software—became crucial as businesses navigated uncertainty. Salesforce had accidentally built the perfect recession-resistant business model.

The cultural foundation laid during this period proved equally important. The 1-1-1 model, established at founding, had evolved into a comprehensive corporate philanthropy program. By 2009, Salesforce had donated millions in grants, provided free software to 20,000 nonprofits, and employees had contributed 250,000 volunteer hours. This wasn't just corporate responsibility—it was recruitment and retention strategy. Top talent, especially younger workers, increasingly wanted meaning alongside compensation.

Dreamforce evolved from conference to phenomenon. The 2009 event drew 12,000 attendees, featured musical performances by Neil Young and Stevie Wonder, and generated headlines beyond the tech press. Benioff understood that enterprise software purchasing had become as much about emotion and community as features and pricing. Dreamforce created evangelical customers who didn't just use Salesforce—they believed in it.

Product development accelerated through this period. Service Cloud launched in 2008, extending beyond sales into customer service. Salesforce Content provided document management. Salesforce Mobile brought CRM to BlackBerries and early iPhones. Each addition made leaving Salesforce harder and staying more valuable.

The platform strategy's success created an interesting dynamic: Salesforce's biggest competitors were often its closest partners. Companies built million-dollar businesses on Force.com, then worried about Salesforce copying their features. Benioff navigated this carefully, acquiring some partners (like Kieden for quote-to-cash functionality) while maintaining arms-length relationships with others. The message was clear: build on our platform and you might get acquired, but cross us and we'll build it ourselves.

By the end of 2009, Salesforce had 82,400 customers and 2.3 million subscribers. The stock had recovered from its financial crisis lows to trade above $60. The scrappy startup had become the establishment, the revolutionary had become the platform. But the biggest transformation—from product company to acquisition machine—was just beginning. The next decade would see Salesforce spending tens of billions to buy its way into new markets, new capabilities, and ultimately, a new identity as the operating system for digital business.

V. The Acquisition Machine Begins (2010–2016)

The Radian6 acquisition in March 2011 for $326 million seemed unremarkable at the time—a social media monitoring tool that most analysts dismissed as overpriced. But it marked the beginning of Salesforce's transformation into enterprise software's most aggressive acquirer. Over the next five years, Benioff would spend over $10 billion on acquisitions, fundamentally reshaping not just Salesforce but the entire SaaS industry's approach to growth.

The strategy crystallized with two massive deals in 2012-2013. Buddy Media, acquired for $745 million in 2012, brought social media marketing capabilities. ExactTarget, purchased for $2.5 billion in 2013, added email marketing and digital advertising tools. Combined with Radian6, these formed the foundation of Marketing Cloud—Salesforce's first major expansion beyond CRM into an entirely new category.

The ExactTarget deal deserves special attention. At $2.5 billion, it was Salesforce's largest acquisition to date, roughly 10% of Salesforce's own market cap. Wall Street was skeptical—the price represented 7x revenue for a company growing at 30%. But Benioff saw something others missed: the convergence of sales and marketing technology. CMOs were becoming as important as CIOs in software purchasing decisions. Marketing budgets were shifting from agencies to technology. Salesforce needed to be there.

Integration became Salesforce's secret weapon. While Oracle and others struggled to integrate acquisitions—often running them as separate business units for years—Salesforce had a different playbook. Within 6-12 months, acquired products were rebuilt on Force.com, integrated into the core platform, and sold by Salesforce's massive sales organization. The acquired company's customers were migrated to Salesforce infrastructure, immediately improving margins and reliability.

The cultural integration was equally sophisticated. Salesforce would typically retain the acquired company's product leadership but replace sales and administrative functions. Key engineers received generous retention packages tied to integration milestones. The acquired company's brand might remain (like ExactTarget Marketing Cloud) but was always prefixed with "Salesforce." The message: you're joining a family, not being absorbed by a blob.

2016's acquisition of Demandware for $2.8 billion represented another category expansion—into e-commerce. This wasn't obvious territory for a CRM company, but Benioff's logic was compelling: modern commerce was about knowing your customer across every channel. Demandware, rebranded as Commerce Cloud, let retailers manage online stores while integrating with Salesforce's customer data. Suddenly, Salesforce could offer a complete digital transformation package: marketing, sales, service, and commerce.

The acquisition strategy wasn't without failures. Salesforce's $390 million purchase of Steelbrick in 2015 for CPQ (configure, price, quote) functionality struggled with integration. The $750 million acquisition of Krux, a data management platform, never achieved its promise. But the hits far outweighed the misses, and even failures taught valuable lessons about integration and market timing.

Competition during this period shifted from product features to ecosystem battles. Oracle responded with its own acquisition spree, buying dozens of cloud companies. Microsoft accelerated Dynamics investment. Adobe emerged as a surprising competitor in marketing technology. But Salesforce had advantages: a single platform architecture, a unified data model, and most importantly, customer trust that acquisitions would be integrated rather than abandoned.

The platform evolution continued alongside acquisitions. 2015 saw the launch of Lightning, a complete reimagining of Salesforce's user interface. This wasn't just cosmetic—it was architectural, enabling component-based development and responsive design. The App Cloud provided enterprise app development tools. IoT Cloud connected Salesforce to the emerging Internet of Things. Wave Analytics (later Einstein Analytics) brought business intelligence capabilities.

The Einstein announcement at Dreamforce 2016 marked Salesforce's entry into artificial intelligence. Unlike standalone AI products, Einstein was embedded across the platform—predictive lead scoring in Sales Cloud, automated case routing in Service Cloud, audience segmentation in Marketing Cloud. Salesforce acquired multiple AI companies to build Einstein, including MetaMind, PredictionIO, and RelateIQ, spending over $700 million. The message was clear: AI wasn't a product, it was a platform capability.

Dreamforce itself had become a universe unto itself. The 2016 event drew 171,000 registered attendees, taking over San Francisco for a week. U2 performed. CEOs gave keynotes. Customers treated it like a pilgrimage. The economic impact on San Francisco exceeded $200 million. Critics called it excessive; Benioff called it necessary community building at scale.

Financial performance during this period was remarkable. Revenue grew from $2.27 billion in fiscal 2012 to $8.39 billion in fiscal 2017. The stock price tripled. But growth came at a cost—operating margins remained stubbornly in the single digits as Salesforce prioritized expansion over profitability. The strategy was deliberate: dominate categories while competitors hesitated, worry about margins later.

The organizational structure evolved to manage this complexity. Salesforce created "Cloud CEOs" for each major product line, giving them P&L responsibility while maintaining platform coherence. The sales organization specialized into industry verticals and product specialists while maintaining the core "Customer 360" message—every product worked better together.

By the end of 2016, Salesforce had assembled an enterprise software portfolio that spanned the entire customer journey. The scrappy CRM startup had become a platform behemoth generating over $8 billion annually. But the biggest acquisitions—and the greatest challenges—lay ahead. The next phase would test whether Salesforce could maintain its growth trajectory while finally delivering the profitability Wall Street demanded.

VI. The Mega-Deal Era: MuleSoft, Tableau & Slack (2017–2021)

March 20, 2018: Wall Street was stunned. Salesforce announced the acquisition of MuleSoft for $6.5 billion—a 36% premium to its already elevated public market valuation. Analysts called it "desperate," "reckless," even "Benioff's folly." MuleSoft, an integration platform company, seemed tangentially related to CRM at best. Why would Salesforce pay such an astronomical sum for enterprise plumbing?

The answer revealed Benioff's evolved understanding of enterprise software. The problem wasn't selling software anymore—Salesforce had solved that. The problem was connecting software. The average enterprise used 1,000+ applications, each with its own data silo. MuleSoft's integration platform could connect them all, making Salesforce the nervous system of the digital enterprise. It wasn't a desperate move; it was a strategic masterpiece.

Integration had always been Salesforce's Achilles' heel. Customers loved the products but struggled connecting them to SAP, Oracle, or homegrown systems. Professional services firms made billions on Salesforce integrations. MuleSoft changed that dynamic overnight. Now Salesforce owned the pipes as well as the applications. The acquisition paid for itself through reduced customer churn and increased deal sizes within 24 months.

The Tableau acquisition in June 2019 dwarfed even MuleSoft. At $15.7 billion, it was the largest software acquisition ever at the time. Tableau, the leading analytics platform, seemed like an odd fit—it was primarily used by data analysts, not sales teams. Critics argued Salesforce was empire-building without strategy.

But Benioff saw convergence others missed. Every business process generated data. Every decision required analytics. By combining Salesforce's operational data with Tableau's visualization capabilities, customers could finally close the loop between insight and action. A sales manager could see pipeline trends in Tableau and immediately adjust territories in Sales Cloud. A service director could identify satisfaction patterns and instantly modify Service Cloud workflows.

The integration approach for these mega-deals differed from earlier acquisitions. Instead of immediately rebuilding on Force.com, Salesforce maintained the acquired platforms independently while building connection points. MuleSoft kept its own architecture. Tableau retained its desktop application. This "federated" approach acknowledged that forcing everything onto one platform would destroy value. The goal was interoperability, not uniformity.

Then came 2020, and everything changed.

The pandemic transformed digital transformation from buzzword to survival strategy. Companies that planned three-year cloud migrations executed them in three months. Remote work became mandatory. Digital engagement wasn't nice-to-have but necessary-for-existence. Salesforce's stock soared from $160 to $280 as investors recognized the permanent acceleration of enterprise cloud adoption.

In this context, the December 2020 announcement of Slack's acquisition for $27.7 billion seemed almost inevitable. Slack had emerged as the communication platform for remote work, growing from 10 million to 18 million daily active users during the pandemic. But Microsoft Teams was growing faster, bundled free with Office 365. Slack needed a larger partner to compete.

The strategic rationale was compelling. Salesforce called it building the "Digital HQ"—combining Salesforce's customer data with Slack's collaboration platform. Sales teams could collaborate on deals in Slack with real-time Salesforce data. Service agents could swarm on complex problems. Marketing teams could coordinate campaigns. It wasn't just about competing with Microsoft Teams; it was about reimagining how work happened in the digital age.

But the price tag caused revolt. Salesforce's market cap was around $250 billion—Slack represented over 10% of the company's value. The stock dropped 17% on announcement. Activist investors began circling. The narrative shifted from "Salesforce the disruptor" to "Salesforce the bloated." Had Benioff finally overpaid?

The integration challenge was immense. Unlike previous acquisitions where Salesforce was clearly the acquirer, Slack had its own strong culture and devoted user base. Stewart Butterfield, Slack's founder-CEO, joined Salesforce as CEO of Slack, maintaining quasi-independence. The companies had to merge while preserving what made each special—Salesforce's enterprise strength with Slack's consumer-grade user experience.

Cultural integration proved even trickier. Slack employees prided themselves on product craftsmanship and design aesthetics. Salesforce, despite improvements, was still known for complex, feature-heavy interfaces. Slack's San Francisco headquarters had meditation rooms and artisanal coffee; Salesforce's towers had sales floors and war rooms. The companies shared values around social responsibility but differed drastically in execution style.

Product integration proceeded carefully. Rather than forcing Slack into existing clouds, Salesforce created "Slack-first" experiences—new workflows that assumed Slack as the primary interface. Sales Cloud alerts appeared in Slack channels. Service Cloud cases could be discussed in threads. Marketing Cloud campaigns were coordinated through Slack workflows. The goal: make Slack the conversational interface for all Salesforce products.

The financial impact was immediate and mixed. Fiscal 2022 revenue hit $26.49 billion, up 25% year-over-year. But operating margins remained compressed as integration costs mounted. The stock languished, failing to exceed its 2021 highs despite revenue growth. Wall Street's patience was exhausting.

Meanwhile, Salesforce made smaller but strategic acquisitions. Vlocity for $1.33 billion brought industry-specific solutions. ClickSoftware added field service capabilities. Evergage provided real-time personalization. Each acquisition filled a gap, but the aggregate spending—over $50 billion since 2016—raised questions about organic innovation capabilities.

The pandemic boom also brought challenges. Salesforce hired aggressively, adding 30,000 employees in two years. Real estate expanded with new towers in Sydney, Dublin, and Chicago. The culture, already strained by remote work, struggled to absorb so many new people. The famous "Ohana" (Hawaiian for family) spirit felt diluted.

By late 2021, Salesforce had joined the Dow Jones Industrial Average, replacing ExxonMobil—a symbolic passing of the torch from industrial to digital economy. But storm clouds were gathering. Interest rates were rising. Tech valuations were compressing. Activist investors were sharpening their knives. The age of unlimited growth was ending, and Salesforce would need to prove it could generate profits, not just revenue. The reckoning was about to begin.

VII. Modern Challenges & The AI Revolution (2021–Present)

January 2023 started with a shock that nobody at Salesforce saw coming—not even Marc Benioff. The company that had never done significant layoffs, that prided itself on "Ohana" culture and taking care of its family, announced it was cutting 10% of its workforce. Approximately 7,000 employees received notice. The growth-at-all-costs era had officially ended.

The activist siege had been building for months. ValueAct, Starboard Value, Elliott Management, and Third Point had all taken positions, collectively controlling billions in Salesforce stock. Their message was unified: margins were unacceptably low, acquisition integration was failing, and management had lost focus. They pointed to Microsoft's 40% operating margins versus Salesforce's 20%. They questioned why Slack integration was taking so long. They demanded board seats, buybacks, and most of all, profitability.

Benioff's response was swift and unprecedented. Beyond the layoffs, Salesforce announced its first-ever share buyback program—$10 billion initially, later expanded. M&A activity ground to a halt; no significant acquisitions were announced in 2023. The company that had grown through buying was forced to grow through building. Every division faced margin improvement targets. The message from the tower was clear: prove you can be profitable or face elimination.

The transformation was remarkable. Operating margins expanded from 18.7% to 30.5% in fiscal 2024. Sales and marketing spend, traditionally 45% of revenue, dropped to 35%. Real estate footprint shrank as remote work policies liberalized. The company that had spent lavishly on Dreamforce concerts and employee perks suddenly discovered fiscal discipline.

But cost-cutting alone wouldn't satisfy growth investors. Salesforce needed a new narrative, and it found one in artificial intelligence—specifically, in the promise of autonomous agents that could handle customer interactions without human intervention. The AI revolution wasn't just another platform shift; it was existential. If Microsoft's partnership with OpenAI created superior AI capabilities, customers might abandon Salesforce entirely.

The Agentforce announcement at Dreamforce 2024 represented Salesforce's biggest bet since the original cloud transition. Unlike Einstein's predictive analytics, Agentforce promised autonomous action—AI agents that could resolve service cases, qualify leads, even negotiate deals. Early results were promising: Agentforce handled 380,000 conversations on Salesforce's own help site with an 84% resolution rate.

The technical architecture of Agentforce revealed lessons learned from previous platform transitions. Instead of building everything internally, Salesforce partnered with multiple AI providers while maintaining its own layer of business logic. The Data Cloud, assembled from acquisitions like Tableau and MuleSoft, became the foundation—AI was only as good as the data it could access. The platform approach that had served Salesforce for two decades evolved to accommodate the AI age.

Competition in AI was fierce but fragmented. Microsoft's Copilot integrated OpenAI throughout Office and Dynamics. Google pushed Vertex AI through its cloud platform. Amazon offered Bedrock for custom AI development. But Salesforce had an advantage: twenty-five years of customer data and business process expertise. While competitors offered general-purpose AI, Salesforce could deliver AI specifically trained on sales, service, and marketing workflows.

The financial results validated the strategy. Fiscal 2025 revenue reached $37.9 billion, up 9% year-over-year. More importantly, operating cash flow hit record levels, and the stock began recovering from its 2022 lows. The company that Wall Street had written off as a bloated has-been was engineering one of enterprise software's great comebacks.

But challenges remained formidable. Growth had slowed to high single digits—respectable for a company Salesforce's size but disappointing for a stock still priced for expansion. Nearly half of the Fortune 100 were AI and Data Cloud customers, but penetration in the mid-market remained limited. The Slack integration, three years post-acquisition, still felt incomplete.

The competitive landscape had also shifted dramatically. Microsoft, once dismissed as a legacy vendor, had emerged as Salesforce's most formidable rival. Teams had decimated Slack's growth trajectory. Dynamics, bundled with Office, won deals on price. The Copilot AI assistant threatened to make traditional CRM redundant. Benioff, who had spent decades fighting Oracle, now faced a different beast entirely.

Organizational challenges compounded external pressures. The layoffs had damaged morale, particularly among longtime employees who felt betrayed by the "Ohana" culture's abandonment. Remote work policies created have and have-not dynamics between workers who could work from anywhere and those required in offices. The acquisition pipeline that had brought fresh talent and ideas dried up.

The succession question loomed larger. Benioff, at 60, showed no signs of stepping down, but investors increasingly asked about life after Marc. Bret Taylor, once heir apparent, had left to start his own AI company. Amy Weaver, the CFO who'd orchestrated the margin expansion, announced her departure. The bench looked thin just when leadership stability mattered most.

Product development accelerated despite the challenges. The Einstein 1 Platform unified previously disparate clouds. Industry-specific solutions for healthcare, financial services, and retail gained traction. The Commerce Cloud, neglected during the Slack integration, received major updates. But innovation felt incremental rather than revolutionary—improving existing products rather than creating new categories.

Current remaining performance obligation stood at $30.2 billion, indicating solid future growth, but the composition worried analysts. Large enterprise deals dominated while small business growth stagnated. The company that had democratized CRM was increasingly dependent on Fortune 500 contracts. The platform that promised simplicity had become complex enough to require armies of consultants.

The AI revolution's ultimate impact remained uncertain. Would Agentforce deliver the autonomous enterprise Benioff promised, or would it join the graveyard of overhyped enterprise AI? Could Salesforce maintain its position as the system of record when every interaction might be mediated by AI? Would customers pay premium prices for specialized AI when general-purpose models improved daily?

As 2024 ended, Salesforce stood at an inflection point. The profitability transformation had succeeded—margins approached best-in-class levels. The AI platform showed promise. The competitive position, while challenged, remained strong. But the fundamental question persisted: Could a 25-year-old company reinvent itself once more, or had Salesforce reached the natural limits of enterprise software growth?

VIII. Playbook: Business & Investing Lessons

The Salesforce story offers a masterclass in building and scaling enterprise software, but the real lessons transcend industry boundaries. Understanding how Benioff transformed a four-person apartment startup into a $235 billion behemoth requires examining the strategic playbook that emerged—sometimes deliberately, often accidentally—over twenty-five years.

The SaaS Pioneer: Creating an Entirely New Business Model

Salesforce didn't invent software-as-a-service, but they perfected and popularized it. The genius wasn't technical—running software on servers wasn't revolutionary even in 1999. The genius was economic and psychological. By charging monthly subscriptions instead of upfront licenses, Salesforce aligned vendor and customer incentives. Traditional software companies made money on initial sales regardless of implementation success. Salesforce only made money if customers renewed—forcing obsessive focus on customer success.

The subscription model also democratized enterprise software. A five-person startup could use the same CRM as General Electric, paying $250 monthly instead of $250,000 upfront. This wasn't just market expansion; it was market creation. Millions of businesses that never considered CRM suddenly could afford it. The TAM (Total Addressable Market) expanded by orders of magnitude overnight.

The model's resilience appeared during economic downturns. While license revenues collapsed in recessions, subscription revenues merely slowed. Customers might reduce seats but rarely canceled entirely—the switching costs and operational disruption weren't worth the savings. This predictability allowed Salesforce to invest counter-cyclically, hiring when competitors fired, acquiring when others retreated.

Platform Economics: From Product to Ecosystem

The transition from product to platform remains Salesforce's most underappreciated innovation. Most enterprise software companies talked about platforms but built products with APIs. Salesforce built a true platform—infrastructure that others could build upon, not just integrate with.

The AppExchange created network effects in enterprise software. Every app made Salesforce more valuable. Every customer made building apps more attractive. Every developer made customers more likely to choose Salesforce. This virtuous cycle, common in consumer technology, was revolutionary in enterprise software where vendors traditionally hoarded all value.

Platform economics also changed competitive dynamics. Competing with Salesforce meant competing with thousands of developers and hundreds of solutions. Oracle might match Salesforce's CRM features, but could they match the ecosystem? Microsoft might bundle Dynamics free, but did they have industry-specific solutions for 50 industries? The platform moat proved wider than any product moat could be.

M&A Mastery: 65+ Acquisitions Without Losing Identity

Salesforce completed over 65 acquisitions totaling more than $70 billion—a remarkable feat of capital deployment. But the real achievement was integration. While Oracle and others struggled with "Frankenstein" architectures, Salesforce successfully absorbed acquisitions while maintaining platform coherence.

The integration playbook evolved through trial and error. Early acquisitions were completely rebuilt on Force.com—expensive but ensuring consistency. Later acquisitions like Tableau and MuleSoft maintained independence while building bridges. The key insight: preserve what made the acquisition valuable while eliminating redundancy. Keep the product visionaries, replace the back office. Maintain the brand equity, migrate the infrastructure.

Cultural integration mattered as much as technical integration. Salesforce developed sophisticated retention strategies—generous packages for key engineers, accelerated vesting for successful integration, roles for acquired executives. The "Trailblazer" community welcomed acquired company users. Dreamforce celebrated acquisitions as expansion, not conquest.

The "Trust" Mantra: Making Security and Reliability Core

From day one, Benioff understood that selling cloud software meant selling trust. Enterprises wouldn't put customer data in the cloud without absolute confidence in security and reliability. Salesforce made trust a core value, not a feature—building trust.salesforce.com to provide real-time transparency on system performance, creating rigorous security certifications, and establishing the industry's first Chief Trust Officer role.

This trust investment paid compound returns. When competitors faced outages or breaches, Salesforce's reliability became a differentiator. When regulations like GDPR emerged, Salesforce's privacy infrastructure was ready. When enterprises finally embraced the cloud, they chose the vendor they'd trusted longest. Trust became a moat that money couldn't buy—it had to be earned over decades.

Stakeholder Capitalism: The 1-1-1 Model

The 1-1-1 model—donating 1% of equity, product, and time—seemed like idealistic excess when Salesforce was burning cash. But it became a strategic advantage. Top talent, especially younger workers, increasingly chose employers based on values alignment. Salesforce's philanthropy became a recruiting superpower.

The model also created customer loyalty beyond reason. Nonprofits that received free Salesforce became evangelists. Employees who volunteered together bonded beyond work relationships. Communities that benefited from Salesforce grants welcomed Salesforce offices. The 1-1-1 model transformed stakeholder capitalism from buzzword to business strategy.

Timing Markets: Riding Three Waves

Salesforce's growth coincided with three technology waves: cloud computing (2000s), mobile (2010s), and AI (2020s). This wasn't luck—it was positioning. Benioff consistently invested ahead of the curve, accepting short-term losses for long-term positioning.

The cloud bet seemed premature in 1999 when browsers could barely handle complex applications. The mobile investments in 2008 preceded the iPhone's enterprise adoption. The AI acquisitions in 2016 came before transformer models made AI practical. Each time, Salesforce was early but not too early—positioned to ride the wave when it crested.

The Enterprise Sales Machine

Salesforce pioneered the SaaS go-to-market playbook that every B2B startup now follows. Inside sales teams nurturing leads through automated campaigns. "Land and expand" strategies starting with small deployments. Customer success managers ensuring renewal and growth. Sales development representatives qualifying leads before expensive account executives engaged.

This machine achieved remarkable efficiency. Customer acquisition costs (CAC) remained stable even as deal sizes grew. Sales cycles shortened even as products became more complex. Win rates improved even as competition intensified. The sales machine became as important as the product—many competitors had comparable technology but couldn't match Salesforce's distribution.

Managing Hypergrowth While Maintaining Culture

Growing from 4 to 76,000 employees while maintaining cultural coherence seems impossible, yet Salesforce largely succeeded until recent years. The "Ohana" culture, V2MOM (Vision, Values, Methods, Obstacles, Measures) planning process, and Dreamforce community created shared identity across geographies and functions.

But culture proved harder to maintain through acquisitions and remote work. The Slack integration showed the limits—two strong cultures struggling to merge. The pandemic-era hiring boom diluted cultural intensity. The 2023 layoffs shattered the "family" mythology. The lesson: culture scales through systems and symbols, but authenticity requires constant reinforcement from leadership.

These playbook elements weren't all planned. Many emerged from crisis responses or fortunate accidents. But together, they formed a replicable model for building enterprise software companies—a model that spawned hundreds of imitators and defined an entire industry's evolution. Whether Salesforce can execute this playbook in the AI age remains the billion-dollar question.

IX. Analysis & Bear vs. Bull Case

The investment case for Salesforce in 2024 presents a fascinating study in contrasts. Bulls see a reformed growth company finally delivering profitability while positioned perfectly for the AI revolution. Bears see a mature incumbent facing slowing growth, fierce competition, and integration challenges from poorly-timed acquisitions. Both perspectives have merit.

Bull Case: The Transformation Story

The bullish thesis starts with Salesforce's dominant market position. With 22% global market share in cloud-based CRM, Salesforce remains the undisputed category leader. This isn't just about size—it's about entrenchment. The average large enterprise has spent years customizing Salesforce, training users, and building workflows. Ripping out Salesforce would be like performing organ transplants—theoretically possible but practically dangerous.

The platform network effects keep strengthening. With thousands of apps on AppExchange and millions of developers certified on the platform, Salesforce has created an ecosystem that becomes more valuable with scale. Every new customer makes building for Salesforce more attractive. Every new app makes choosing Salesforce more compelling. These network effects create winner-take-all dynamics that should accelerate as the market matures.

The profitability transformation validates the bull case. Adjusted operating margins expanding from 18.7% to 30.5% proves Salesforce can generate cash when it stops acquiring. With the activist pressure subsiding and management focused on efficiency, margins could expand further toward Microsoft's 40% levels. Apply a 35% margin to $40+ billion in revenue, and you get $14+ billion in operating income—justifying a much higher valuation.

AI integration creates new moats rather than threats. While generalists like OpenAI excel at general intelligence, Salesforce's twenty-five years of customer data and business process expertise enable specialized AI that actually works in enterprise contexts. Agentforce's early success suggests customers will pay premiums for AI that understands their specific workflows rather than generic chatbots.

The improving fundamentals support further upside. Record cash flow generation enables both growth investment and capital returns. The $10+ billion buyback program reduces share count while signaling management confidence. The dividend initiation attracts value investors previously uninterested in growth stocks. These technical factors create natural buyers as the company transitions from growth to GARP (Growth at a Reasonable Price).

The massive TAM expansion opportunity remains untapped. Digital transformation, accelerated by COVID but far from complete, represents trillions in IT spending over the coming decade. Customer experience investments continue growing faster than GDP. The shift from on-premise to cloud still has years to run in conservative industries. Salesforce, as the trusted incumbent, should capture disproportionate share of this spending.

Bear Case: The Maturity Trap

The bearish perspective starts with undeniable deceleration. Revenue growth slowing to 8-9% in fiscal 2025 might seem respectable for a $40 billion company, but Salesforce trades at growth multiples. At 7x forward revenue, the valuation implies either acceleration or margin expansion to 40%+. Neither seems likely given competitive pressures and market maturation.

Microsoft poses an existential threat that bulls underestimate. Teams destroyed Slack's momentum despite Salesforce's backing. Dynamics, while smaller, wins on price when bundled with Office. Copilot's integration throughout Microsoft's suite could make standalone CRM obsolete—why switch applications when AI can handle customer interactions within Outlook? Microsoft's $3 trillion market cap provides unlimited resources for subsidizing competition.

The integration challenges from massive acquisitions remain unresolved. Three years post-acquisition, Slack still feels bolted-on rather than integrated. Tableau operates largely independently. MuleSoft maintains its own architecture. Customers complain about complexity and costs. The promise of unified customer experiences remains largely promise. Meanwhile, integration costs and complexity tax margins and innovation.

The expensive valuation assumes perfect execution. At 45x forward earnings, any disappointment triggers violent selloffs. The multiple expansion from 2020-2021 hasn't fully corrected despite rising rates. Value investors remain skeptical given limited capital returns history. Growth investors question whether high single-digit growth justifies premium multiples. The stock remains stuck between styles.

Dependence on large enterprise spending creates vulnerability. Fortune 500 companies drive the majority of Salesforce's revenue and all of its growth. These customers face their own pressures—recession fears, budget constraints, layoffs. IT spending, while resilient, isn't immune to economic cycles. A recession would hit Salesforce's core market directly, and the subscription model that provides stability also limits upside in recoveries.

The AI revolution might commoditize rather than differentiate CRM. If large language models can handle customer interactions directly, why需要 expensive CRM systems? If every employee becomes augmented by AI, do specialized sales and service applications matter? The bull case assumes AI enhances Salesforce's products, but disruption often comes from unexpected angles.

The Balanced View

Reality likely lies between extremes. Salesforce remains a high-quality company with real moats, but growth has permanently decelerated. The profitability transformation is genuine but probably complete—margins might reach 35% but not 40%. AI creates both opportunities and threats, likely benefiting incumbents like Salesforce but not exclusively.

The stock's performance will depend on multiple factors beyond fundamentals. Interest rates affect all growth stocks disproportionately. The broader cloud software sector's sentiment matters more than individual execution. Merger and acquisition activity could provide upside surprises or integration disappointments.

For long-term investors, the key question isn't whether Salesforce succeeds but whether success is properly priced. At current valuations, the market expects both continued growth and expanding margins. Delivering either would justify the stock price. Delivering both would drive substantial upside. Disappointing on both would trigger meaningful downside. The risk-reward seems balanced but uninspiring—appropriate for a company transitioning from growth story to value stock.

X. Power & What Makes Salesforce Special

Understanding Salesforce's enduring competitive advantages requires examining the company through Hamilton Helmer's 7 Powers framework—the strategic foundations that enable persistent differential returns. Salesforce exhibits multiple, reinforcing powers that explain both its historical success and future durability.

Network Effects: The AppExchange Ecosystem

The AppExchange represents Salesforce's strongest competitive moat. With over 4,000 applications and 9 million installs, it's created a two-sided network effect that strengthens with scale. Developers build for Salesforce because that's where the customers are. Customers choose Salesforce because that's where the applications are. This virtuous cycle took twenty years to build and would be nearly impossible to replicate.

But the network effects go deeper than just applications. The Trailblazer community—millions of administrators, developers, and users—creates knowledge network effects. Every blog post, forum answer, and certification makes Salesforce easier to adopt. Every trained professional makes hiring easier. Every success story makes buying less risky. These human networks prove more durable than technical ones.

The data network effects might be most powerful. As customers use Salesforce, they generate insights that improve the platform's AI capabilities. Einstein's predictions get better with more data. Industry solutions become more refined with more customers. Best practices emerge from aggregate usage patterns. Unlike consumer networks where users can switch instantly, this enterprise data gravity creates permanent adhesion.

Switching Costs: Deep Integration into Enterprise Workflows

The switching costs for leaving Salesforce border on prohibitive for established customers. It's not just the software—it's the customizations, integrations, workflows, and training. Large enterprises have spent millions and years configuring Salesforce precisely for their needs. Switching would mean rebuilding everything from scratch while maintaining business continuity.

The human capital switching costs matter equally. Companies have thousands of employees trained on Salesforce interfaces and processes. Sales methodologies are built around Salesforce's opportunity management. Service procedures assume Salesforce's case routing. Marketing campaigns depend on Salesforce's automation. Switching systems would require retraining entire organizations—a cost measured not just in money but in productivity losses and change management pain.

The ecosystem switching costs compound the lock-in. If you're using ten AppExchange applications, switching means finding alternatives for all of them. If you've built custom applications on Force.com, switching means rebuilding them entirely. If you've integrated with MuleSoft, switching means re-architecting your entire integration strategy. The totality of these switching costs creates customer captivity that competitors can't overcome with features or pricing alone.

Scale Economies: R&D and Sales Efficiency

Salesforce's scale enables R&D investments no competitor can match. Spending $5 billion annually on development across multiple clouds and platforms, Salesforce can pursue initiatives that would bankrupt smaller competitors. The Einstein AI platform required hundreds of millions in investment before generating revenue. The Lightning interface rebuild took three years. These moon shots are only possible at scale.

The sales and marketing efficiency improves with scale. Salesforce's brand recognition means lower customer acquisition costs. The massive sales force—over 30,000 people—can be deployed efficiently because overhead is spread across a huge base. The Dreamforce conference, costing tens of millions, becomes economical when marketing to millions of customers. These scale advantages create a "rich get richer" dynamic.

Infrastructure scale economies matter increasingly. Running data centers for millions of users means lower per-user costs. Negotiating with Amazon Web Services for petabytes of storage yields better pricing. Compliance certifications become cheaper per customer at scale. Security investments protect more users. These technical scale economies create cost advantages that translate directly to margins.

Brand: "No One Gets Fired for Buying Salesforce"

The Salesforce brand has achieved what IBM once had—default safety in enterprise purchasing decisions. CIOs know that choosing Salesforce might not be innovative, but it won't be career-ending. This brand power enables premium pricing and shorter sales cycles. Competitors must overcome not just feature comparisons but institutional risk aversion.

The brand extends beyond product to vision. Benioff's thought leadership on stakeholder capitalism, digital transformation, and social justice makes Salesforce more than a vendor—it's a movement. Customers aren't just buying software; they're joining a community with shared values. This emotional connection transcends rational purchasing decisions.

The employer brand creates talent advantages. Top engineers want Salesforce on their resumes. Universities teach Salesforce-specific courses. Professionals build careers around Salesforce expertise. This talent magnetism ensures Salesforce gets first pick of the best people, creating product advantages that reinforce brand advantages.

Counter-Positioning: Cloud-Native vs Legacy Architecture

Salesforce's pure-cloud architecture was initially a weakness—limited functionality, internet dependence, security concerns. But as technology evolved, it became an insurmountable advantage. Legacy vendors like Oracle and SAP couldn't match Salesforce's agility without abandoning their installed bases. Their attempts at cloud offerings were compromised by the need to support on-premise deployments.

The continuous deployment model exemplifies this counter-positioning. Salesforce pushes updates three times annually to all customers simultaneously. Legacy vendors, supporting hundreds of versions across thousands of installations, can't match this pace. By the time they've developed, tested, and deployed a feature, Salesforce has moved on to the next innovation.

The subscription model created business model counter-positioning. Traditional vendors couldn't adopt subscriptions without devastating their quarterly revenue. Their sales forces, compensated on large upfront deals, resisted the model. Their investors, expecting license revenue, punished attempts at transition. Salesforce's model, initially a constraint, became a competitive weapon.

The Benioff Factor: Visionary Leadership

While not technically a "power" in Helmer's framework, Benioff's leadership created advantages that transcend traditional strategy. His ability to see around corners—cloud, social, mobile, AI—consistently positioned Salesforce ahead of trends. His theatrical marketing generated attention that money couldn't buy. His stakeholder capitalism created loyalty that compensation couldn't match.

The cultural power Benioff created might be most important. The V2MOM planning process aligned thousands of employees. The Ohana culture created belonging that retained talent. The Dreamforce experience created customer evangelism. These cultural innovations, while intangible, created competitive advantages as real as any technology.

Reinforcing Loops

These powers don't operate independently—they reinforce each other. Network effects increase switching costs. Scale economies enable brand building. Counter-positioning protects network effects. The combination creates a competitive position that's nearly impossible to assault frontally. Competitors must find orthogonal attacks or wait for Salesforce to stumble.

The durability of these powers varies. Network effects and switching costs should strengthen over time. Scale economies face diminishing returns. Brand requires constant investment. Counter-positioning weakens as cloud becomes standard. Understanding this evolution helps predict where Salesforce is vulnerable and where it's invincible.

XI. Epilogue & Future Outlook

As Salesforce enters its twenty-sixth year, the company faces an identity crisis that mirrors the broader enterprise software industry's evolution. The scrappy revolutionary that promised "The End of Software" has become the establishment it once fought against. The question isn't whether Salesforce succeeded—by any measure, it has. The question is what comes next when you've already conquered the mountain you set out to climb.

The Transition from Growth to Value Stock

The mathematical reality is undeniable: Salesforce has entered the realm of large-cap value stocks whether it admits it or not. At nearly $40 billion in annual revenue, growing at high single digits, the days of 30% growth are permanently behind. The company that once commanded 10x revenue multiples now trades at 6-7x—still premium but approaching traditional software valuations.

This transition requires psychological adjustment from all stakeholders. Employees accustomed to generous equity compensation must accept that stock appreciation will be measured rather than meteoric. Investors who bought for growth must decide whether to stay for dividends and buybacks. Management must balance growth investments with capital returns. The company must learn to act its age while maintaining its innovative spirit.

Can Salesforce Win the AI War Against Microsoft?

The existential question facing Salesforce is whether specialized AI beats generalized AI in enterprise applications. Microsoft's partnership with OpenAI provides access to cutting-edge models that improve faster than any company can develop internally. But Salesforce's bet—that twenty-five years of customer data and business process knowledge matter more than raw AI capability—remains unproven.

Early indicators are mixed. Agentforce shows promise in narrow use cases where Salesforce's domain expertise shines. But Microsoft's Copilot demonstrates the power of AI integrated across an entire productivity suite. The battle might not be winner-take-all—enterprises might use Microsoft for general productivity and Salesforce for specialized customer interactions. But that scenario still represents share loss for Salesforce.

The key determinant might be data gravity. If customer data remains the critical asset, Salesforce's position as the system of record provides insurmountable advantage. But if AI can operate effectively across disparate data sources, that advantage evaporates. The next 24 months will likely determine whether Salesforce's AI strategy validates or evaporates.

The Next $100B in Revenue: Where Will It Come From?

Reaching $100 billion in annual revenue—Benioff's stated goal—requires finding $60+ billion in new revenue. That's almost two current Salesforces. Where does this growth originate?

International expansion offers the clearest path. Salesforce generates 70% of revenue from the Americas, suggesting massive opportunity in Europe and Asia. But international expansion requires localization, compliance, and cultural adaptation that Salesforce has historically struggled with. The company that perfected selling to American businesses must learn to sell to Japanese enterprises and European governments.

Industry verticalization presents another avenue. Generic CRM increasingly feels antiquated when competitors offer purpose-built solutions for healthcare, financial services, or retail. Salesforce's Industry Clouds, while promising, remain subscale. The challenge: building deep industry expertise while maintaining platform coherence.

The platform economy could accelerate if Salesforce truly enables customers to build their own applications. Imagine if every company became a software company on Salesforce's platform, paying for compute, storage, and services. This vision—Salesforce as the AWS of business applications—could generate tens of billions in revenue. But it requires technical capabilities and pricing models that don't yet exist.

Succession Planning: Life After Benioff?

Marc Benioff IS Salesforce in ways that few founders embody their companies. His vision, charisma, and relationships drove every major strategic decision. His departure, whenever it comes, will test whether Salesforce has institutional greatness or merely reflected individual brilliance.

The succession pipeline looks concerningly thin. Bret Taylor, the obvious successor, left for his own AI startup. Keith Block, the former co-CEO, departed after strategic disagreements. Amy Weaver, the CFO who engineered the profitability transformation, announced her resignation. The remaining executives are competent operators but lack Benioff's visionary qualities.

The board faces an impossible choice: promote internally and risk losing innovation, or hire externally and risk losing culture. The most likely scenario—Benioff remaining CEO while gradually ceding operational control—creates its own challenges. Founder-CEOs rarely transfer power gracefully, and the limbo period often paralyzes organizations.

The Ultimate Test: Building the Autonomous Enterprise

Salesforce's ultimate vision—the autonomous enterprise where AI agents handle most customer interactions—represents both opportunity and threat. If successful, it could drive another S-curve of growth as companies rebuild operations around AI. But it also could cannibalize existing revenue as AI reduces the need for human users.

The technical challenges are immense. Current AI lacks the judgment, creativity, and empathy that define excellent customer experiences. Customers might accept AI for simple transactions but demand humans for complex problems. Regulatory frameworks for AI decision-making remain undefined. The autonomous enterprise might be perpetually five years away.

The business model implications are equally complex. If AI agents don't require seats, how does Salesforce price them? If one agent can do the work of ten humans, does Salesforce capture that value or does it flow to customers? If every vendor offers AI agents, what differentiates Salesforce? These questions don't have obvious answers.

The Final Analysis

Salesforce stands at a crossroads that every successful technology company eventually faces. The innovations that drove growth have been absorbed by the market. The acquisitions that expanded capability have reached diminishing returns. The culture that enabled success has evolved beyond recognition. The founder who provided vision contemplates succession.

Yet Salesforce possesses attributes that suggest continued relevance. The customer relationships built over decades provide distribution advantages. The platform ecosystem creates innovation beyond what Salesforce could build alone. The brand commands respect even from critics. The financial resources enable bold bets on uncertain futures.

The next chapter of the Salesforce story won't be written by Marc Benioff alone—it will be written by millions of customers, developers, and employees who've made Salesforce central to their digital operations. Whether that chapter describes continued growth or gradual decline depends on decisions being made today in Salesforce Tower, in customer boardrooms, and in the AI laboratories that are reshaping enterprise software's future.

The one certainty: the company that promised "The End of Software" won't go quietly. Whether through innovation, acquisition, or transformation, Salesforce will fight to remain relevant. The playbook that built the company might not sustain it, but the ambition that drove its creation remains undiminished. In enterprise software, as in life, the only constant is change—and nobody has proven more adaptable to change than Salesforce.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube