Weyerhaeuser: America's Timber REIT Titan

I. Introduction & Episode Roadmap

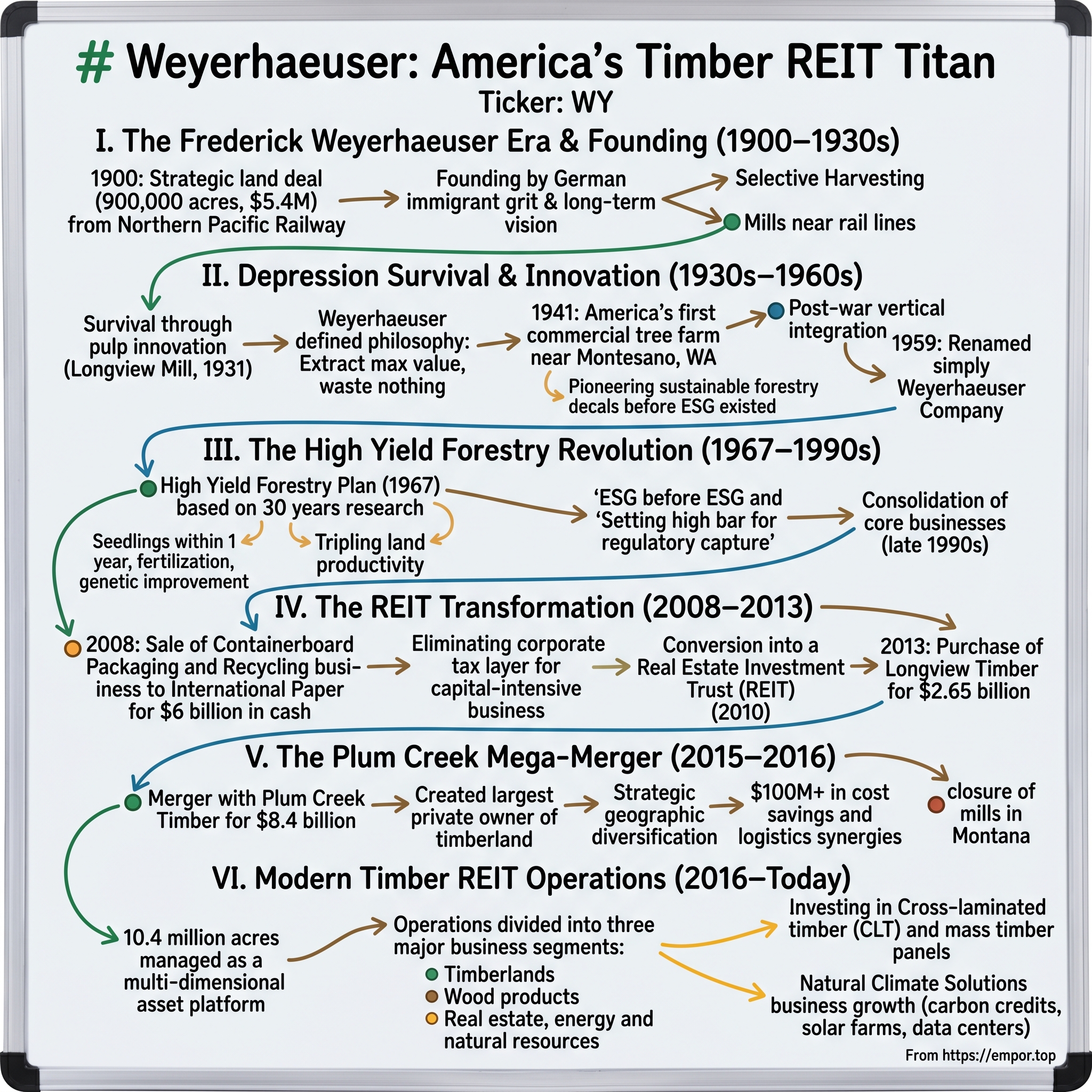

Picture this: A single land deal in 1900 that would reshape American capitalism for the next century. Frederick Weyerhaeuser, a German immigrant who started as a night watchman at a sawmill, stood before 900,000 acres of Washington wilderness—virgin Douglas fir forests stretching from Puget Sound to the Cascade Mountains. The price tag? $5.4 million from James J. Hill's Northern Pacific Railway, making it one of the largest private land transfers in American history. Today, that transaction's descendant company manages 10.4 million acres across America, generates $7.1 billion in annual revenue, and has transformed from a traditional timber baron into one of the nation's most sophisticated real estate investment trusts.

How exactly does a 125-year-old lumber company become Wall Street's darling timber REIT? The answer involves German immigrant grit, surviving the Great Depression through pulp innovation, pioneering sustainable forestry decades before ESG existed, and executing one of the most elegant financial engineering transformations of the 21st century. This is the story of Weyerhaeuser—a company that turned trees into a financial instrument, patience into profit, and land into the ultimate economic moat.

We're going to trace this journey from railroad-era timber barons through REIT transformation, examining how Weyerhaeuser navigated boom-bust lumber cycles, integrated vertically then stripped down to pure-play, and ultimately merged with rival Plum Creek to create America's timber colossus. Along the way, we'll uncover lessons about patient capital, the power of irreplaceable assets, and why in the age of software and semiconductors, owning dirt and trees might be the smartest play of all.

II. The Frederick Weyerhaeuser Era & Founding (1900–1930s)

The snow was still melting in the Cascade foothills when Frederick Weyerhaeuser stepped off the Northern Pacific train in Tacoma, Washington, in January 1900. At 65, most men would be thinking about retirement. But Weyerhaeuser, who'd built a Mississippi River lumber empire with his partner Frederick Denkmann, saw something others missed: the last great timber frontier in America. The forests of Michigan and Wisconsin were nearly exhausted. The pine stands of Minnesota were thinning. But here in the Pacific Northwest stood Douglas firs so massive that a single tree could frame an entire house.

The deal that brought him west was audacious even by Gilded Age standards. James J. Hill, the "Empire Builder" of railroad fame, needed cash to expand his rail network and held vast timber grants from the federal government—payment for building tracks across the wilderness. Weyerhaeuser offered $5.4 million for 900,000 acres, roughly $6 per acre. Hill's associates thought he was getting fleeced; one called it "selling gold for the price of lumber." But Weyerhaeuser saw what they didn't: these weren't just trees, they were a perpetual asset that, properly managed, could generate wealth for generations.

The founding philosophy he articulated to his 15 initial partners was prescient: "This is not for us, nor for our children, but for our grandchildren." Think about that mindset in 1900—an era of slash-and-burn logging, where timber companies would strip land bare and move on. Weyerhaeuser was already thinking in generational terms, envisioning replanting, sustained yield, and permanent ownership. This wasn't just progressive; it was revolutionary.

The Weyerhaeuser Timber Company incorporated on January 18, 1900, with Frederick as president and headquarters in Tacoma. The initial capitalization was $4 million, with Weyerhaeuser himself holding the largest stake. His partners included other Mississippi River lumber families—the Mussers, Denkmanns, and Moons—creating what historians would later call the "Weyerhaeuser Syndicate." They weren't just buying timberland; they were establishing a new model of resource capitalism.

Early operations focused on selective harvesting and establishing mills near rail lines. By 1902, they'd opened their first major sawmill in Everett, Washington, with a capacity of 300,000 board feet per day—massive for the era. The company pioneered the use of logging railroads, laying temporary tracks deep into forests to extract timber efficiently. A 1905 company report noted they were harvesting at a rate that would take 80 years to exhaust their holdings—already thinking in terms of rotation and regeneration rather than depletion.

Frederick's management style blended German precision with American entrepreneurialism. He insisted on detailed forest surveys, something most competitors considered unnecessary expense. Company foresters would map every section, noting species composition, age classes, and accessibility. This data-driven approach—radical for its time—would become Weyerhaeuser's hallmark. By 1910, they owned 2 million acres across Washington, Oregon, and Idaho, making them America's largest private landowner.

The founder's death in 1914 at age 79 could have fragmented the empire. Instead, his son John Philip Weyerhaeuser took the helm, maintaining the long-term vision while modernizing operations. The 1920s brought the first stirrings of what would become scientific forestry. Company foresters began experimenting with selective cutting patterns, leaving seed trees to naturally regenerate logged areas. They established the industry's first forestry research program in 1925, hiring university-trained foresters when most competitors still relied on rule-of-thumb methods. By 1929, as Wall Street soared to unsustainable heights, Weyerhaeuser made a contrarian bet that would define its next century. They broke ground on what was then the world's largest sawmill in Longview, Washington—a massive complex that could process more timber in a day than most mills handled in a week. The timing seemed catastrophic. Within months, the stock market crashed, lumber prices collapsed, and competitors shuttered operations across the Pacific Northwest. But Weyerhaeuser had an ace: diversification beyond just cutting boards.

III. Depression Survival & Innovation (1930s–1960s)

The rain hadn't stopped for three days when the first railcar of wood pulp rolled out of Longview in March 1931. America was sliding deeper into economic catastrophe—unemployment hit 16%, construction had virtually ceased, and lumber prices had fallen 70% from their 1929 peak. Competitors were liquidating timberlands for pennies on the dollar. Yet here was Weyerhaeuser, opening a revolutionary new facility that would transform wood waste into high-grade pulp for paper production.

Weyerhaeuser's pulp mill in Longview, which began production in 1931, sustained the company financially during the Great Depression. This wasn't just survival; it was strategic brilliance. While sawmills across the Northwest went dark, the Longview pulp operation ran three shifts, producing 250 tons of bleached sulphite pulp daily. The key insight: even in a depression, people still needed paper for newspapers, packaging, and government documents. By 1933, when lumber revenues had nearly disappeared, pulp sales kept the company solvent and its workforce employed.

The company's Depression-era innovation went beyond product diversification. In 1933, they developed Presto Logs—compressed sawdust formed into artificial fireplace logs—turning literal waste into a consumer product. This wasn't just clever recycling; it embodied a philosophy that would define Weyerhaeuser for decades: extract maximum value from every tree, waste nothing, think in cycles not transactions.

But the real revolution came in 1941 when Weyerhaeuser established America's first commercial tree farm near Montesano, Washington. The 120,000-acre Clemons Tree Farm represented a radical departure from the cut-and-run mentality that had devastated forests from Maine to Minnesota. Company foresters planted six million seedlings that first year, establishing regeneration cycles that would ensure perpetual harvest. The marketing was brilliant too—they opened the land to public recreation, hosted school tours, and positioned Weyerhaeuser as stewards rather than exploiters. By 1945, they were replanting more acres than they harvested, a ratio unheard of in the industry.

World War II transformed Weyerhaeuser from a regional timber company into a strategic national asset. The Longview pulp mill pivoted to producing thousands of tons of bleached sulfite pulp for the War Production Board to make smokeless gunpowder. Military contracts for lumber to build barracks, ships, and aircraft crates pushed revenues to record levels. By 1945, Weyerhaeuser employed over 15,000 workers and had become Longview's largest employer and one of the Pacific Northwest's economic anchors.

The post-war boom brought new challenges and opportunities. Housing construction exploded as returning GIs started families, driving lumber demand to unprecedented levels. Weyerhaeuser responded with vertical integration, adding plywood mills, particleboard plants, and eventually engineered wood products. The company also began its first serious international expansion. In 1965, Weyerhaeuser built its first bleached kraft pulp mill in Canada, marking the beginning of what would become a global footprint.

Perhaps most significantly, in 1959, the company eliminated the word "Timber" from its name, becoming simply Weyerhaeuser Company. This wasn't mere rebranding—it signaled a fundamental shift from seeing itself as a timber harvester to a diversified forest products enterprise. The company now operated everything from seedling nurseries to chemical plants producing chlorine for pulp bleaching. They'd even ventured into real estate development, creating planned communities on logged-over lands near growing cities.

By the mid-1960s, Weyerhaeuser had survived the Depression, thrived through war, and emerged as America's largest private landowner with over 3.6 million acres. But the real test was coming: could a company built on extracting natural resources adapt to an era of environmental consciousness? The answer would reshape not just Weyerhaeuser but the entire concept of industrial forestry.

IV. The High Yield Forestry Revolution (1967–1990s)

George Weyerhaeuser stood before a skeptical audience of Wall Street analysts in 1967, holding up two Douglas fir seedlings. One was scraggly, wild-grown. The other, genetically selected and scientifically cultivated, was twice its size despite being the same age. "Gentlemen," he said, "this is the future of forestry. We're not just growing trees anymore—we're manufacturing them."

Weyerhaeuser implemented its High Yield Forestry Plan in 1967 which drew upon 30 years of forestry research and field experience. It called for the planting of seedlings within one year of a harvest, soil fertilization, thinning, rehabilitation of brushlands, and, eventually, genetic improvement of trees. This wasn't incremental improvement—it was agricultural revolution applied to forestry. The company's research stations had been quietly developing "super trees" since the 1950s, selecting for straight grain, disease resistance, and rapid growth. By 1970, Weyerhaeuser seedlings grew 30% faster than wild trees. By 1980, some experimental plots showed 100% productivity gains.

The numbers were staggering. Traditional forestry might yield 50 cubic feet of wood per acre per year. High Yield Forestry pushed that to 150, even 200 cubic feet on prime sites. Weyerhaeuser was essentially tripling the productivity of its land without acquiring a single new acre. Wall Street loved it—here was a commodity business that had discovered how to manufacture its own competitive advantage.

But High Yield Forestry required massive upfront investment. The company spent $50 million annually (over $300 million in today's dollars) on forestry research throughout the 1970s. They built sophisticated nurseries that could produce 250 million seedlings per year. They pioneered aerial fertilization, dropping nitrogen pellets from helicopters across thousands of acres. They developed computerized growth models that could predict timber yields decades into the future.

The environmental movement of the 1970s could have been Weyerhaeuser's existential crisis. Instead, the company turned it into a marketing opportunity. They opened their tree farms to environmental groups, hosted Sierra Club hikes, and positioned industrial forestry as the sustainable alternative to deforestation. The message was clever: "We're not cutting forests, we're harvesting crops—crops that happen to be 80 feet tall."

In 1975 the company bought the 3,200 acres of land of the Northwest Landing and developed the town of DuPont, Washington using a New Urbanism model. This wasn't just real estate development—it was Weyerhaeuser demonstrating that logged lands could become thriving communities. DuPont, with its walkable neighborhoods and preserved green spaces, became a showcase for responsible land use. The company was learning that sometimes the highest value of timberland wasn't the timber at all.

The 1980s brought new challenges as foreign competition intensified and environmental regulations tightened. The spotted owl controversy erupted, threatening to lock up millions of acres of federal forests and by extension, increasing the value of private timberlands. Weyerhaeuser navigated carefully, supporting sustainable forestry regulations that it could meet while smaller competitors couldn't. It was regulatory capture through superior practice—set the bar high enough that you've already cleared it while others struggle.

By 1990, Weyerhaeuser's transformation was complete. The company that had started as a timber cutter now managed the world's most sophisticated forest products research program. They'd proven that industrial forestry could be sustainable, profitable, and even environmentally progressive. Their genetically improved trees were capturing more carbon, growing faster, and producing better wood than anything nature had evolved.

But success had made Weyerhaeuser complex—perhaps too complex. Weyerhaeuser consolidated its core businesses in the late 1990s and ended its services in mortgage banking, personal care products, financial services, and information systems consulting. The company had become a conglomerate, with operations ranging from disposable diapers to financial services. The next chapter would require painful choices about what Weyerhaeuser really was: a forest products company, a technology company, or something else entirely?

V. The REIT Transformation (2008–2013)

The phone call came at 2 AM Pacific time on September 15, 2008. Lehman Brothers had just collapsed. Steven Rogel, Weyerhaeuser's CEO, stared at the Bloomberg terminal in his home office as credit markets seized up in real-time. The company had $8 billion in debt, lumber prices were in freefall, and housing starts had plummeted 80% from their 2006 peak. Every forest products company in America was hemorrhaging cash. But Rogel saw something his board initially thought was insane: the perfect moment for radical transformation.

Six months earlier, in March 2008, Weyerhaeuser Company announced the sale of its Containerboard Packaging and Recycling business to International Paper for $6 billion in cash. The timing seemed prescient in retrospect—closing the deal just weeks before the financial system imploded. The transaction included nine containerboard mills, 72 packaging locations, 10 specialty-packaging plants, four kraft bag and sack locations and 19 recycling facilities, affecting approximately 14,300 employees. At $6 billion, it was one of the largest industrial asset sales of 2008, providing Weyerhaeuser with a massive war chest just as competitors were scrambling for liquidity.

But the containerboard sale was merely the opening move in a larger chess game. Rogel and his team had been studying real estate investment trusts (REITs) for years, watching how timber REITs like Plum Creek and Rayonier traded at significant premiums to traditional forest products companies. The math was compelling: REITs paid no corporate income tax if they distributed 90% of taxable income as dividends. For a capital-intensive, low-margin business like timber, eliminating the corporate tax layer could transform economics overnight.

The REIT conversion playbook was elegant but complex. First, Weyerhaeuser needed to separate its manufacturing operations from its timberland ownership—the IRS required REITs to derive at least 75% of gross income from real estate. The containerboard sale had started this process, but the company still operated dozens of lumber mills, plywood plants, and other manufacturing facilities that generated non-qualifying income. Throughout 2009, as the economy cratered, Weyerhaeuser methodically restructured, creating a taxable REIT subsidiary (TRS) to house manufacturing while moving timberlands into the REIT structure.

Weyerhaeuser converted into a REIT when it filed its 2010 tax return. The transformation was complete—125 years after its founding, America's oldest timber company had become its newest financial innovation. The market reaction was immediate: shares jumped 15% on the announcement as investors recognized the value unlock. The company could now return massive cash flows to shareholders while maintaining operational control of its timberlands.

The REIT structure forced discipline that ultimately strengthened the company. Required to pay out 90% of taxable income, Weyerhaeuser couldn't hoard cash for marginal acquisitions or empire building. Every investment had to clear a high hurdle rate. This constraint became a strength, forcing management to focus ruthlessly on the highest-return opportunities while returning billions to shareholders through dividends.

In 2013, Weyerhaeuser purchased Longview Timber for $2.65 billion including debt from Brookfield Asset Management. The acquisition added 645,000 acres of timberland to Weyerhaeuser's holdings in Oregon and Washington. This wasn't just a land grab—these were premium Douglas fir forests in the heart of the Pacific Northwest, exactly the kind of irreplaceable assets that justified REIT premiums. The Longview lands had been part of the original Weyerhaeuser empire before being spun off decades earlier; bringing them home completed a circle while demonstrating the REIT's acquisition capacity.

In 2014, Weyerhaeuser spun off its home building unit to TRI Pointe Homes in a $2.8 billion transaction. This was the final piece of the simplification strategy—exiting the volatile, capital-intensive homebuilding business to focus purely on timberland ownership and wood products manufacturing. The company that had once sprawled into diapers and financial services was now laser-focused on trees and lumber.

The REIT transformation wasn't just financial engineering—it fundamentally changed how investors valued timberland. Pre-REIT, Weyerhaeuser traded at maybe 1.2x book value of its land. Post-REIT, multiples expanded to 1.5x, even 2x book value as investors recognized these weren't just trees but perpetual cash-flow streams with inflation protection, carbon sequestration potential, and development optionality. The company had unlocked billions in shareholder value without cutting a single tree.

VI. The Plum Creek Mega-Merger (2015–2016)

The boardroom at Two Union Square in downtown Seattle was silent except for the hum of the air conditioning. Rick Holley, Plum Creek's CEO, stared across the mahogany table at Doyle Simons, his Weyerhaeuser counterpart. It was October 2015, and after months of secret negotiations, they were about to shake hands on the timber industry's deal of the century. "We're not just merging companies," Holley said. "We're creating the Amazon of timber—except we were here first."

On November 8, 2015, it was announced that Weyerhaeuser would buy Plum Creek Timber for $8.4 billion, forming the largest private owner of timberland in the United States. The announcement sent shockwaves through the industry. Here were two fierce competitors, each with over a century of history, combining to create a timber colossus with 13 million acres—roughly the size of West Virginia.

The strategic logic was impeccable. Plum Creek brought 6.2 million acres concentrated in the South and intermountain West, perfectly complementing Weyerhaeuser's Pacific Northwest and Southern holdings. That includes 7.3 million acres of Southern yellow pine forests in the Southern U.S., 3 million acres of Douglas fir forest in Oregon and Washington, and 2.6 million acres of mixed hardwoods in Michigan and the Northeast. Geographic diversification meant protection against regional weather events, pest outbreaks, or local market downturns.

But the deal structure was where the financial engineering got interesting. Under the terms of the agreement, which has been unanimously approved by the boards of directors of both companies, Plum Creek shareholders will receive 1.60 shares of Weyerhaeuser for each share of Plum Creek held. Each outstanding share of Plum Creek common stock immediately prior to the merger converted into the right to receive 1.60 common shares of Weyerhaeuser Company. In total, approximately 278.9 million common shares of Weyerhaeuser will be issued to Plum Creek stockholders, representing approximately 35 percent of the total shares outstanding.

The clever twist came next. Weyerhaeuser intends to execute a $2.5 billion share repurchase shortly after closing. The repurchase will result in a net financial impact on the company that is as if the deal were structured with approximately 70% stock and 30% cash. This wasn't just financial wizardry—it was tax-efficient structuring that satisfied both sets of shareholders while maintaining REIT compliance.

The synergies were real and immediate. CEOs for the two companies said they expected the merger to result in at least $100 million in cost savings. These weren't just paper savings from eliminating duplicate corporate functions. "You think about logistics and hauling costs, where we pass each other on the road right now, we're not going to have so many empty back-hauls," said Plum Creek CEO Rick Holley, in a conference call early Monday. When your product is logs and your transportation cost is often 30% of delivered price, eliminating empty truck miles translates directly to the bottom line.

The cultural integration proved more challenging than the financial engineering. Plum Creek had been the industry's bad boy—aggressive, entrepreneurial, with roots in railroad land grants and a reputation for clear-cutting that earned it the nickname "the Darth Vader of the state of Washington." Weyerhaeuser, by contrast, cultivated an image of responsible stewardship, sustainable forestry, and long-term thinking. Merging these cultures required delicate navigation.

Leadership structure reflected this balance. Weyerhaeuser also announced the members of the combined company's board of directors. As previously announced, the 13-person board includes eight directors from the pre-closing Weyerhaeuser board and five directors from the pre-closing Plum Creek board. The directors include: Rick R. Holley (non-executive chairman), David P. Bozeman, Mark A. Emmert, Sara Grootwassink Lewis, John I. Kieckhefer, John F. Morgan Sr., Nicole W. Piasecki, Marc F. Racicot, Lawrence A. Selzer, Doyle R. Simons, D. Michael Steuert, Kim Williams, and Charles R. Williamson.

Shareholders of both companies approved the transaction at separate special meetings of shareholders held on Feb. 12, 2016. The transaction closed on February 19, 2016. With that, 116 years of Weyerhaeuser history merged with Plum Creek's railroad baron heritage to create America's undisputed timber king.

But success brought scrutiny. Within months of closing, reality bit. As Montanans will recall, they purchased Plum Creek Timber Company in November 2015 for $8 billion, a move that surprised many people in Montana, including our entire Congressional delegation and the governor. By June 2016, Weyerhaeuser announced the closure of two mills in Montana that Plum Creek had operated, eliminating hundreds of jobs. Critics argued the company knew these closures were coming when they announced the merger—that "synergies" was just corporate-speak for job cuts.

The combined company also faced a strategic crossroads. Weyerhaeuser also plans to explore the possibility of selling or spinning off its cellulose-fibers business segment, which produced $1.9 billion in sales in 2014. A sale would mean Weyerhaeuser would no longer be one of the world's largest producers of absorbent fluff pulp, which is used in diapers. The segment includes a plant in Longview that makes packaging for liquids, like those used in juice boxes. The company was signaling its future: pure-play timberland REIT, not diversified manufacturer.

VII. Modern Timber REIT Operations (2016–Today)

Devin Stockfish stands in Weyerhaeuser's new Seattle headquarters at 200 Occidental Avenue, floor-to-ceiling windows framing Elliott Bay. It's 2024, and as CEO since 2019, he oversees an empire that would astonish Frederick Weyerhaeuser: 10.4 million acres of timberlands managed not just for timber but as a multi-dimensional asset platform generating value from carbon credits to solar farms to data centers. "We don't just grow trees anymore," Stockfish explains to analysts. "We optimize every molecule of value from every acre we own."

The modern Weyerhaeuser owns or controls approximately 10.4 million acres of timberlands in the U.S., and in 2024, the company generated $7.1 billion in net sales and employed approximately 9,400 people who serve customers worldwide. The company's operations are divided into three major business segments: Timberlands—growing and harvesting trees in renewable cycles; Wood products—manufacturing and distribution of building materials for homes and other structures; Real estate, energy and natural resources—all surface and subsurface resources in timberlands that are worth more than the timber itself.

The geographic footprint tells the story of strategic positioning. Weyerhaeuser's highest concentration of U.S. forestland today is in the South, where it owns approximately 7 million acres stretching from southeastern Oklahoma through the Carolinas and up to West Virginia. The Southern forests are the company's cash cow—fast-growing loblolly pine that reaches harvest age in 25 years versus 45 years for Douglas fir in the Pacific Northwest. It owns about 2.5 million acres in the Northwest, premium Douglas fir and hemlock forests that command top prices for structural lumber. And around 1 million acres in the Northeast, primarily in Maine, hardwood and softwood forests that diversify the portfolio.

The REIT structure has fundamentally changed how Weyerhaeuser operates. Required to distribute 90% of taxable income, the company has become a dividend machine. Weyerhaeuser returned $735 million to shareholders, including a $153 million share repurchase, and advanced its Natural Climate Solutions business significantly. This isn't just financial engineering—it's forcing operational excellence. Every dollar of capital expenditure must compete with simply returning cash to shareholders, creating relentless pressure for efficiency.

But the real revolution is happening beyond traditional timber. The engineered wood products division represents Weyerhaeuser's bet on construction innovation. Cross-laminated timber (CLT), mass timber panels, and other engineered products can replace steel and concrete in buildings up to 18 stories tall. The company announced plans to invest approximately $500 million in a new TimberStrand facility in Arkansas, expected to generate over $100 million of annual adjusted EBITDA. This isn't incremental improvement—it's positioning for a potential transformation of urban construction. The Natural Climate Solutions business represents perhaps the most radical transformation in Weyerhaeuser's 125-year history. The company saw a 79% increase in adjusted EBITDA from Natural Climate Solutions, driven by strong contributions from conservation, mitigation banking, and renewables. This isn't greenwashing—it's hard economics. Weyerhaeuser announced an agreement for the sale of nearly 32,000 forest carbon credits at $29 per credit. This agreement marks Weyerhaeuser's first transaction in the voluntary carbon market and represents the sale of all credits issued by ACR for the first year of the company's Kibby Skinner Improved Forest Management (IFM) Project in Maine. Weyerhaeuser will immediately retire these credits on behalf of the buyer.

The carbon strategy is sophisticated. Weyerhaeuser's carbon credits are generated only from changes made to remove and store additional carbon beyond normal, business-as-usual operations. Our carbon projects are designed to store carbon removed from the atmosphere through the length of the project commitment, and often well beyond. We also take measures to ensure that carbon emissions removed in one geography are not displaced to another geography. By delaying harvests on select acreage, extending rotation periods, or changing species mix, the company can generate verified carbon credits worth millions while still maintaining timber operations on the majority of its land.

But carbon is just one revenue stream. We grant easements on our land to reputable industry leaders who identify, evaluate, permit and build wind and solar projects. A single wind farm on a ridgeline can generate $10 million in annual lease payments while using less than 1% of the land area, allowing timber operations to continue below. Solar installations on cutover land provide income during the years before replanting. We evaluate the development of geologic carbon capture and sequestration (CCS) opportunities across our footprint through partnerships and lease agreements with qualified companies. The subsurface rights Weyerhaeuser owns could be worth billions as carbon capture technology scales.

The operational excellence story is equally compelling. Modern Weyerhaeuser mills are marvels of efficiency. We meet more than two-thirds of the energy needs in our manufacturing facilities by using renewable biomass—sawdust, bark, and manufacturing residuals that once were waste now power the entire operation. Computer-vision systems scan every log, optimizing cuts to extract maximum value. What can't become lumber becomes engineered wood; what can't become engineered wood becomes pulp; what can't become pulp becomes energy. Nothing is wasted.

Technology has transformed forest management too. Drones equipped with LiDAR map every acre, measuring tree height, density, and health. Satellite imagery tracks growth rates in real-time. AI models predict optimal harvest timing down to the individual stand. The company that once relied on foresters walking the woods with clipboards now runs one of North America's most sophisticated agricultural operations—except the crop cycle is 25 years, not 25 weeks.

VIII. Financial Performance & Market Dynamics

The numbers tell a story of resilience through cycles. The company reported its financial results for the fourth quarter and full year of 2024, highlighting net earnings of $396 million and net sales of $7.1 billion for the year. Weyerhaeuser returned $735 million to shareholders, including a $153 million share repurchase. These aren't tech company growth rates, but for a business tied to housing and construction, they represent remarkable stability.

The lumber market cycles that once threatened Weyerhaeuser's existence have become manageable volatility within a larger portfolio. When lumber prices spiked during COVID—reaching $1,700 per thousand board feet in May 2021, up from a historical average of $400—Weyerhaeuser's wood products division printed money. When prices crashed back to $350 by August 2021, the timberlands segment's steady performance and the REIT's dividend requirements cushioned the blow.

Housing dependency remains both Weyerhaeuser's greatest opportunity and largest risk. Every 100,000 increase in housing starts translates to roughly $50 million in additional EBITDA. With housing starts still 20% below historical averages due to elevated mortgage rates, there's significant pent-up demand. Millennials entering prime home-buying years, chronic underbuilding since 2008, and migration to the Sun Belt all favor Weyerhaeuser's geographic footprint.

Weyerhaeuser's strategic initiatives involved enhancing its timberlands portfolio with acquisitions in Alabama and planning a new engineered wood products facility in Arkansas. The Arkansas TimberStrand facility represents a $500 million bet on engineered wood's future, expected to generate over $100 million of annual adjusted EBITDA. This isn't just capacity expansion—it's positioning for a potential revolution in construction where engineered wood replaces steel and concrete in mid-rise buildings.

The REIT structure enforces capital discipline that's rare in commodity businesses. Unable to retain earnings for empire building, management must justify every dollar of capital expenditure against simply returning cash to shareholders. This has led to industry-leading returns on invested capital, typically 8-10% even through down cycles. The dividend yield of approximately 3% provides a floor for the stock, attracting income investors who might never consider a traditional materials company.

But the real financial story is optionality. At current valuations, the market prices Weyerhaeuser primarily as a timber and lumber company. The Natural Climate Solutions business, which could generate hundreds of millions in high-margin revenue, essentially comes for free. If carbon markets mature and prices rise from $29 to $100 per credit—not unrealistic given European prices—Weyerhaeuser could generate more profit from carbon than from cutting trees.

IX. Playbook: Business & Investing Lessons

The Power of Patient Capital in Natural Resources

Weyerhaeuser's story demonstrates that in natural resources, time horizon is everything. Frederick Weyerhaeuser's famous quote—"This is not for us, nor for our children, but for our grandchildren"—wasn't just philosophy; it was economic strategy. By thinking in decades rather than quarters, the company could make investments that seemed irrational short-term but created insurmountable competitive advantages long-term. The High Yield Forestry program of the 1960s took 30 years to show full results, but when it did, Weyerhaeuser had essentially tripled the productivity of its land without buying an acre.

REIT Conversion as Strategic Financial Engineering

The 2010 REIT conversion wasn't just tax optimization—it was brilliant capital structure design. By eliminating corporate taxes and forcing dividend distributions, Weyerhaeuser increased its cost of capital for marginal projects while decreasing it for high-return investments. This structural discipline prevented the value destruction that plagued integrated forest products companies for decades. The REIT structure also attracted a completely new investor base—income-focused funds that would never touch a volatile commodity business but love the steady dividends from timber harvests.

Vertical Integration vs. Focus: The Journey from Conglomerate to Pure-Play

Weyerhaeuser's evolution from a vertically integrated conglomerate (timber, lumber, paper, diapers, financial services) to a focused timber REIT with select manufacturing is a masterclass in strategic focus. Each divestiture—containerboard in 2008, homebuilding in 2014, potentially cellulose fibers next—increased value by removing complexity and allowing pure-play valuation. The lesson: in modern capital markets, clarity beats diversification. Investors can diversify themselves; they pay premiums for focused excellence.

Land as the Ultimate Moat

In an era obsessed with network effects and software moats, Weyerhaeuser reminds us that physical scarcity remains the ultimate competitive advantage. You can't download timberland. You can't disrupt Douglas fir with an app. The 10.4 million acres Weyerhaeuser owns would cost $30+ billion to replicate today—if you could even find that much contiguous, productive forestland for sale. This irreplaceability provides pricing power, operational flexibility, and optionality that no amount of innovation can erode.

ESG Before ESG: 100+ Years of Sustainable Forestry

Weyerhaeuser was practicing sustainable forestry when ESG was just random letters. The company's 1941 tree farm—America's first—predated the environmental movement by 30 years. This wasn't altruism; it was economics. By maintaining forest health, replanting immediately, and thinking in rotation cycles, Weyerhaeuser ensured perpetual cash flows. Today's ESG investors are just catching up to what Frederick Weyerhaeuser understood in 1900: sustainable resource management is simply good business.

M&A Excellence: The Plum Creek Integration Playbook

The Plum Creek merger demonstrated textbook M&A execution. Clear strategic rationale (geographic diversification, scale economies), clever deal structure (stock with buyback to simulate cash), rapid integration (achieved $100 million synergies within two years), and ruthless portfolio optimization (closed redundant mills immediately). Most importantly, Weyerhaeuser didn't try to preserve everything—they took the best assets and practices from both companies and eliminated the rest.

Capital Allocation Through Cycles

Weyerhaeuser's capital allocation through commodity cycles offers a masterclass in countercyclical thinking. Buying Longview Timber in 2013 when lumber markets were depressed. Selling containerboard in 2008 just before the financial crisis. Investing $500 million in engineered wood capacity when housing is weak but demographics are favorable. The pattern is clear: deploy capital when others are fearful, return capital when others are greedy, and always maintain balance sheet strength to survive the inevitable downturns.

X. Analysis & Bear vs. Bull Case

Bull Case: The Irreplaceable Asset Thesis

Start with the irreplaceable asset base: 10.4 million acres of productive timberland that would be impossible to assemble today. These aren't just trees; they're perpetual cash-flow machines with embedded inflation protection. As construction costs rise, so does the value of timber. As cities expand, the development value of strategically located parcels soars. As carbon markets mature, every acre becomes a potential carbon credit factory.

The housing recovery story remains compelling despite rate headwinds. America is short 3-5 million homes by most estimates. Millennials are entering prime homebuying years. The Sun Belt migration continues, driving construction in Weyerhaeuser's core Southern markets. Even modest recovery to historical housing starts would drive 20-30% EBITDA growth from current levels.

Climate solutions optionality could be transformative. At $100 per ton of CO2—the price needed to incentivize meaningful carbon reduction—Weyerhaeuser's forest carbon potential could generate $500+ million in annual EBITDA. Add renewable energy leases, carbon sequestration rights, and conservation credits, and the Natural Climate Solutions business could rival traditional timber in profitability.

The REIT structure enforces the discipline that commodity businesses usually lack. Unable to waste capital on low-return projects, management must focus on operational excellence and smart capital allocation. The dividend requirement attracts stable, long-term investors rather than momentum traders, reducing volatility.

Operational excellence provides margins of safety. As the lowest-cost producer in most markets, Weyerhaeuser can remain profitable when competitors lose money. The geographic diversity, species mix, and integrated manufacturing provide multiple levers to pull during downturns.

Bear Case: The Structural Headwinds Thesis

Housing market vulnerability looms large. With mortgage rates above 7%, housing affordability is at multi-decade lows. A recession would crush housing starts, sending lumber prices and Weyerhaeuser's earnings into freefall. The company's beta to housing is inescapable—when construction stops, no amount of operational excellence matters.

Commodity price exposure means Weyerhaeuser is ultimately a price taker. When lumber drops from $1,700 to $350—as it did in 2021—profits evaporate regardless of management skill. The company can't control Chinese demand, Canadian supply, or transportation bottlenecks that determine realized prices.

Climate change poses existential risks that are difficult to quantify. Increased wildfire frequency could destroy millions of acres of timber—Weyerhaeuser lost 50,000 acres in Oregon's 2020 fires alone. Pest outbreaks, amplified by warming temperatures, could devastate entire regions. Extreme weather events disrupt harvesting and transportation, adding cost and volatility.

Competition from engineered alternatives threatens long-term demand. Steel studs, concrete construction, and composite materials all compete with traditional lumber. If 3D-printed homes or modular construction gain traction, demand for dimensional lumber could structurally decline.

Interest rate sensitivity as a REIT creates vulnerability. Rising rates make Weyerhaeuser's dividend less attractive relative to bonds, pressuring the stock price. Higher rates also increase the cost of capital for expansion, limiting growth opportunities. The REIT structure that provides tax advantages also constrains financial flexibility during downturns.

The Verdict: Quality at the Right Price

Weyerhaeuser represents a rare combination: a commodity business with competitive advantages, a cyclical company with structural growth drivers, and a traditional industry with technology optionality. The bear case risks are real but manageable through cycles. The bull case offers multiple ways to win. At the right price—typically when housing pessimism peaks—Weyerhaeuser offers compelling risk-reward for patient investors who can think beyond the next quarter's lumber prices.

XI. Epilogue & "If We Were CEOs"

Standing in a Weyerhaeuser forest in western Washington, you're struck by the temporal paradox. These 80-year-old Douglas firs were planted when FDR was president. The seedlings going in the ground today won't be harvested until 2050. Yet the company must navigate quarterly earnings calls, daily lumber price volatility, and algorithm-driven trading. How do you manage for centuries while performing for quarters?

The future of timber in a carbon-conscious world is fascinating. As the built environment becomes humanity's largest carbon sink, wood—the only major building material that stores rather than emits carbon—could experience a demand renaissance. Mass timber construction, barely a rounding error today, could become a multi-billion market. Cities might become vertical forests, with wooden skyscrapers storing millions of tons of CO2.

Technology disruption cuts both ways. Yes, 3D printing and modular construction might reduce lumber demand. But biotechnology could create super-trees that grow twice as fast with disease resistance. AI-optimized forestry could double per-acre yields. Blockchain carbon credits could create liquid markets for forest sequestration. Weyerhaeuser's massive land base and data advantage position it to benefit from, rather than be disrupted by, technology.

Climate solutions monetization potential feels underappreciated by markets. Carbon credits at $29 are just the beginning. As corporations face mandatory net-zero requirements, high-quality, verified forest credits could trade at multiples of current prices. Weyerhaeuser's ability to generate credits at scale, with full chain of custody and verification, creates a moat in carbon markets as wide as in timber.

Geographic expansion opportunities remain. Climate change is pushing productive forest zones northward. Weyerhaeuser's Canadian licenses could become increasingly valuable. International expansion into sustainable forestry in developing markets could provide growth beyond North America. The expertise in managing forests for multiple values—timber, carbon, biodiversity—is exportable.

If we were CEOs, we'd triple down on climate solutions while maintaining timber excellence. Create a carbon credit "factory" that generates predictable, verified credits at scale. Partner with tech companies needing carbon offsets, offering multi-decade contracts that provide visibility. Invest aggressively in mass timber manufacturing to capture value as construction transforms. Use the REIT structure's forced dividends as a feature, not a bug—it prevents the empire building that destroyed value at integrated forest products companies.

Most importantly, we'd embrace the paradox. Manage for centuries while performing for quarters. Think like a farmer while acting like a trader. Be patient with trees, impatient with capital. Weyerhaeuser has survived 125 years by understanding that in the timber business, time isn't just money—it's everything. The company that started with Frederick Weyerhaeuser seeing value where others saw wilderness continues today, finding carbon credits where others see only trees, data centers where others see cutover land, and permanence where others see commodity volatility.

The next 125 years will look nothing like the last 125. But one thing remains certain: People will need shelter. Carbon will need sequestration. And Weyerhaeuser's 10.4 million acres will keep growing, 24 hours a day, 365 days a year, converting sunlight and CO2 into value. In a world of exponential change and digital disruption, sometimes the best investment is the one that grows at exactly the speed of nature—not faster, not slower, but persistently, inevitably, compound by compound, ring by ring, year after year.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube