Woodward Inc.: The 155-Year-Old Energy Control Pioneer

I. Introduction: A Hidden Champion in Plain Sight

Picture every commercial aircraft you've ever flown on. Somewhere inside those engines—feeding fuel, regulating combustion, actuating flight controls—sits precision-engineered hardware from a company most passengers have never heard of. Woodward, Inc., a global leader in energy control solutions for aerospace and industrial markets, was named one of America's Best Midsize Companies by TIME and Statista. Yet despite operating for over 150 years, this Fort Collins, Colorado-based manufacturer remains largely invisible to the public consciousness.

Woodward reported record financial results for fiscal year 2024, with total sales reaching $3.3 billion, up 14% year-over-year. "We delivered record sales in fiscal 2024 with Woodward revenue exceeding $3 billion for the first time." The company achieved this milestone while simultaneously posting significant earnings growth with full-year EPS of $6.01, up 59%.

The central question animating this analysis: How does a company founded in 1870 to build waterwheel governors become essential to virtually every aircraft engine in the sky—and what does that journey reveal about building enduring competitive advantage in mission-critical industrial markets?

The themes that emerge from Woodward's 155-year history are instructive for any investor seeking to understand durable business models: the compounding power of multi-generational engineering excellence, the strategic patience required to ride secular technology shifts, and the art of becoming indispensable to customers who cannot afford failure.

Woodward was named one of Forbes America's Best Companies for 2026 on November 19, 2025, joining the top 300 U.S. public companies chosen from over 2,000 entrants. Forbes assessed 11 categories across 60+ metrics including public trust, employee satisfaction, customer sentiment, workforce stability, financial strength and cybersecurity.

This is a company that has navigated the transition from waterwheels to turbine engines, from mechanical governors to digital controls, from industrial power to aerospace dominance—all while maintaining its core identity as the entity that ensures machines run precisely when they must. And now, as the aviation industry enters its next transformation and the maritime sector confronts decarbonization, Woodward finds itself once again positioned at the critical junction of established technology and emerging opportunity.

II. The Founding Era: Waterwheels and the Governor (1870–1900)

The Amos Woodward Story

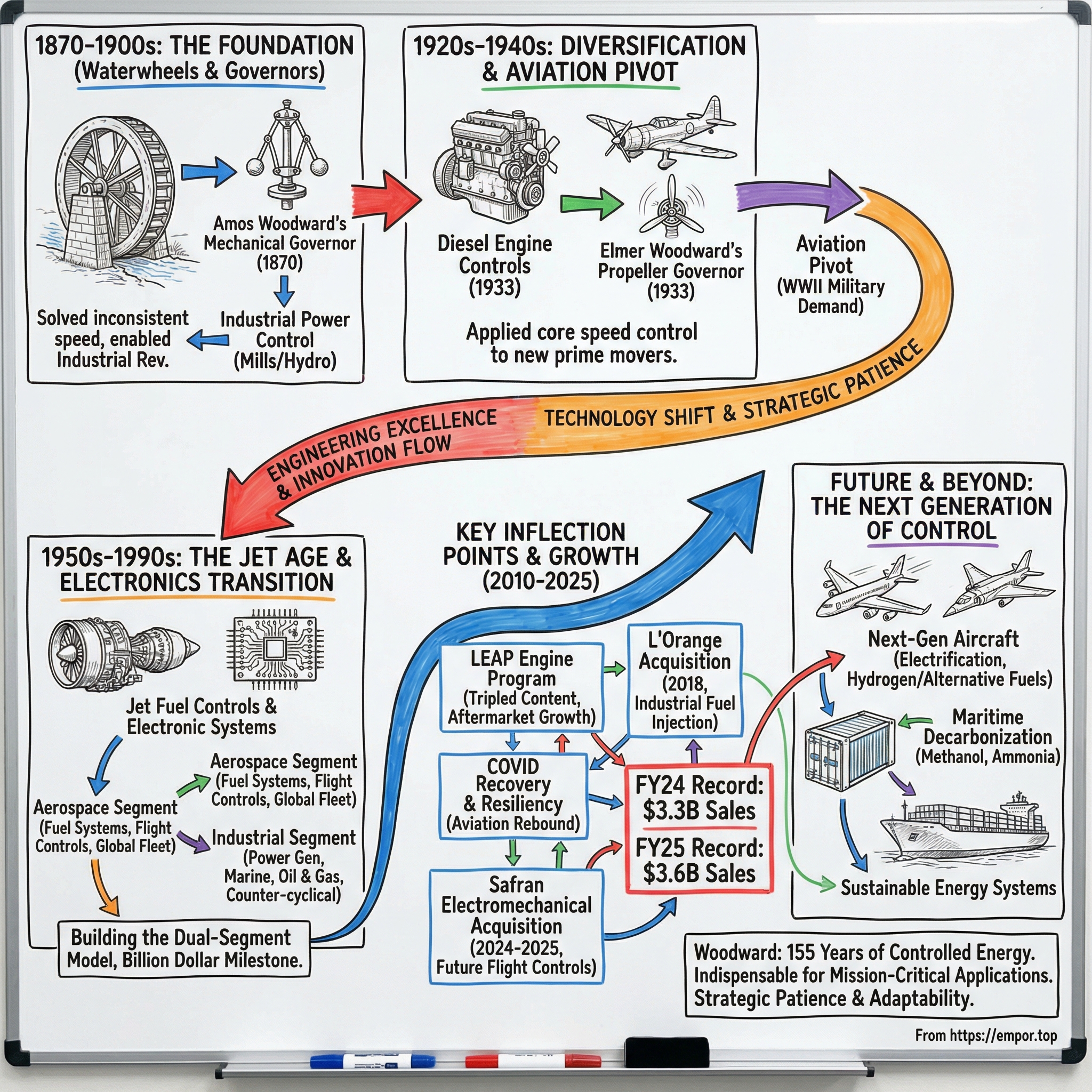

In the decades following the Civil War, America's industrial transformation ran on water. Mills dotted riverbanks across the nation, their waterwheels turning raw power into productive capacity. But a critical problem plagued these early power systems: inconsistent speed. When water flow varied, wheels would accelerate or decelerate unpredictably, damaging equipment and disrupting operations.

The company was founded in Rockford, Illinois, in 1870 with Amos W. Woodward's invention of a non compensating mechanical waterwheel governor (U.S. patent No. 103,813). This device—essentially a feedback mechanism that automatically adjusted water flow to maintain constant wheel speed—solved a fundamental challenge of the nascent hydroelectric age.

This device, patented under U.S. Patent No. 103,813, provided responsive speed regulation for waterwheels without the oscillations common in prior compensating designs, enabling more stable power output for mills and early hydroelectric applications.

What made Amos Woodward's innovation significant wasn't complexity—it was reliability. The innovation addressed a critical need in water-powered machinery, where inconsistent speeds could damage equipment or disrupt operations, and Woodward quickly began commercial production and sales of these governors.

What Is a Governor? Why Does It Matter?

The concept of a "governor"—from the Latin gubernare, to steer or control—represents one of the foundational principles of control systems engineering. James Watt's centrifugal governor for steam engines, developed in the late 18th century, established the paradigm: a mechanical device that senses operating conditions and automatically adjusts inputs to maintain desired outputs.

Woodward's waterwheel governor applied this principle to hydropower. As water flow increased, the wheel would begin to speed up; the governor would sense this acceleration and partially close the water gate, reducing flow. When flow decreased, the governor would open the gate wider. The result: stable speed regardless of variable water conditions.

This may sound trivial from a 21st-century perspective, where digital feedback loops govern everything from smartphone battery management to autonomous vehicles. But in 1870, automatic control was revolutionary. It meant factories could operate without constant human monitoring. It meant hydroelectric generators could produce consistent voltage. It meant the Industrial Revolution could scale.

In 1891, the business had three employees and was selling about $8,000 worth of governors annually. During the 1890s, though, the company grew and even expanded into a larger manufacturing facility.

The Second Generation: Elmer Woodward's Breakthrough

The transition from founder to next generation is where most family businesses falter. Amos Woodward navigated this transition by bringing his son Elmer into the business and encouraging his engineering development.

At the same time that he was helping to run the business, Elmer Woodward, like his father, continued to invent. Importantly, in 1898, when he was 36 years old, Elmer received a patent for a governor that was an improvement over the one his father had designed.

Thirty years later, his son Elmer patented the first successful mechanical compensating governor for hydraulic turbines (U.S. patent No. 583,527).

The breakthrough device gave the company an important advantage in the burgeoning market for governors needed to control new hydroelectric generators. This timing proved fortuitous: the late 1890s saw massive investment in hydroelectric infrastructure, from Niagara Falls to countless smaller installations across North America.

In 1902 Amos and Elmer Woodward incorporated as Woodward Governor Company. In 1910, the company relocated to a five-story manufacturing plant in Rockford to accommodate increased production, reflecting the surge in hydroelectric installations during the early 20th century.

Amos Woodward died in 1919, a few years short of his 90th birthday, and his son continued to lead Woodward throughout the 1920s. Early in 1929, when he was 67 years old, Elmer Woodward hired son-in-law Irl Martin to take over day-to-day operations, while he continued to design new products and make pivotal contributions to the company well into his 70s. By 1929, Woodward Governor was employing 50 workers and had established itself as a leader in the design and manufacture of prime mover controls; that year, the firm posted net income of $65,000 on sales of $318,000.

The father-son innovation model established a template that would define Woodward for generations: technical excellence passed down through deliberate mentorship, combined with continuous improvement on core products rather than reckless diversification.

III. Diversification and The Aviation Pivot (1920s–1940s)

The Diesel Revolution

In the 1920s and 1930s, Woodward began designing controls for diesel and other reciprocating engines and for industrial turbines.

This diversification wasn't random. It represented a strategic recognition that the core competency—precision speed control—was transferable across prime mover technologies. In 1933, the company expanded its product line to include diesel engine controls (U.S. patent No. 2,039,507) and aircraft propeller governors (British patent No. 470,284). Woodward governors followed the rapid advancement of diesel engine applications for railroads, maritime and electrical generation in many fields.

The diesel market presented different technical challenges than hydropower but rewarded the same underlying expertise: understanding rotating machinery, designing reliable mechanical feedback systems, and manufacturing to tight tolerances. Woodward's governors enabled diesel engines to maintain constant speed regardless of load variations—critical for power generation, marine propulsion, and railroad applications.

The Pivotal Aircraft Propeller Governor

The most consequential pivot in Woodward's history came not from diesels but from aviation. Elmer E. Woodward conceived, designed, and developed the first successful propeller control in 1933.

Early aircraft used fixed-pitch propellers—the angle of the blades relative to the direction of travel was constant. This created fundamental performance tradeoffs: a pitch optimized for takeoff produced poor cruise efficiency, while cruise-optimized pitch made takeoff sluggish. Variable-pitch propellers, which could adjust blade angle in flight, promised to solve this problem.

But variable-pitch propellers introduced a new control challenge: how to automatically adjust pitch to maintain optimal engine speed across varying flight conditions. Enter Elmer Woodward.

By 1934, the company entered the aviation sector with a governor for controlling variable-pitch aircraft propellers, invented by Elmer Woodward, which adjusted blade angles to optimize thrust and efficiency during flight. This innovation addressed vibration and performance issues in early aircraft engines, positioning Woodward as a supplier to aviation firms and marking its diversification into aerospace engine controls.

The Model PW-34 propeller governor represented the application of six decades of governor expertise to an entirely new domain. Rather than adjusting water gates or fuel racks, it adjusted propeller blade pitch to maintain desired engine RPM.

On December 31, 1940, 78-year-old Elmer Woodward, or "Pops" as he had come to be called, worked a full day, returned home, and then died of a heart attack. He lived to see his propeller governor become standard equipment on modern aircraft—and to position the company for the transformative military buildup that World War II would bring.

World War II: The Company Goes to War

World War II accelerated growth, with surging orders for propeller governors in military aircraft and ships to minimize vibrations and ensure operational stability.

The war economy did for Woodward what it did for many precision manufacturers: it transformed a successful small company into an essential defense contractor. Military aircraft demanded extreme reliability—governors that worked perfectly under combat conditions, at altitude, in temperature extremes.

In 1943, Woodward introduced its first aircraft turbine control, supporting gas turbine engines amid wartime production.

This transition to turbine controls marked a crucial evolution. Jet engines were entering service in the final years of World War II, and their control requirements differed fundamentally from piston engines. Fuel flow, rather than propeller pitch, became the primary control variable. Woodward's engineers tackled this new challenge, establishing relationships with engine manufacturers that would define the company's next seven decades.

The advent of gas turbine engines for aircraft and industrial uses offered still more opportunities for Woodward designed fuel controls.

The company emerged from World War II with three critical assets: manufacturing expertise in precision controls, deep relationships with aerospace OEMs, and a reputation for reliability in mission-critical applications. These assets would prove more valuable than anyone could have imagined as commercial aviation exploded in the postwar decades.

IV. The Jet Age and Electronics Transition (1950s–1990s)

From Mechanical to Electronic Controls

And, of course, the science of electronics has added impetus to this industry.

The transition from mechanical to electronic controls represents perhaps the most significant technological shift in Woodward's history. Mechanical governors relied on springs, weights, and hydraulic actuators—components that had physical limits in response speed and control precision. Electronic controls, by contrast, could process sensor inputs almost instantaneously and modulate fuel flow with far greater accuracy.

The company navigated this transition through patient investment rather than revolutionary disruption. Early electronic governors supplemented rather than replaced mechanical systems—adding digital supervisory control while retaining mechanical backup modes. This gradualism suited aerospace customers who valued proven reliability over cutting-edge innovation.

Building the Dual-Segment Business Model

Through the post-war decades, Woodward solidified a business structure that persists today: two complementary segments serving distinct but related markets.

The Aerospace segment expanded from propeller governors to comprehensive fuel control systems for turbine engines. Each new commercial aircraft program—the Boeing 707, 727, 737, DC-9, and their successors—represented an opportunity for Woodward to win design-in contracts that would generate revenue for decades through original equipment sales and aftermarket support.

The Industrial segment leveraged the same core competencies—precision fuel controls, engine governors, combustion management—for applications in power generation, marine propulsion, and eventually oil and gas production. This diversification provided counter-cyclical balance: when commercial aviation softened, industrial applications often remained strong.

The Billion Dollar Milestone

By the early 2000s, the cumulative effect of decades of compound growth became apparent. The company had evolved from a three-person operation selling $8,000 in governors annually to a global enterprise with facilities across multiple continents.

The milestone reflected not just revenue growth but expanding content per application. Rather than selling simple governors, Woodward increasingly provided integrated systems—fuel metering units combined with actuators, combustion controls, and electronic management systems. Higher content per engine translated to higher revenue per aircraft.

The company's geographic expansion—Amos Woodward led until his death in 1919, after which the company continued emphasizing mechanical controls vital to the era's energy infrastructure—had evolved into global manufacturing and service operations serving customers worldwide.

V. Key Inflection Points: The Last Two Decades (2010–2024)

Inflection #1: The LEAP Engine Program

The most significant aerospace development of the 2010s for Woodward was securing content on the CFM International LEAP engine family. The CFM International LEAP ("Leading Edge Aviation Propulsion") is a high-bypass turbofan engine produced by CFM International, a 50–50 joint venture between the American GE Aerospace and the French Safran Aircraft Engines. It competes with the Pratt & Whitney PW1000G for narrow-body aircraft. The LEAP uses 15% less fuel and produces 15% less CO₂ compared to the CFM56.

The LEAP powers the three most important narrow-body aircraft programs in commercial aviation: the Airbus A320neo, the Boeing 737 MAX, and the COMAC C919. Securing content on this engine platform represented a generational opportunity.

By July 2018, the LEAP had an eight-year backlog with 16,300 sales. At that time, more LEAPs were produced in the five years it was on sale than CFM56s in 25 years. It is the second-most ordered jet engine behind the 44-year-old CFM56, which achieved 35,500 orders.

The magnitude of Woodward's content gains on the LEAP is striking. We have just about tripled the shipset content on both 737 MAX, A320 versus their predecessors. For the 737 MAX, that equates to around $350,000 of shipset content, 12 components on the LEAP engine versus one small component on the CFM56-7, so big change there.

This high level of content on the MAX and NEO drives Woodward OE and aftermarket sales growth long term. Having significant content on all the engine choices results in a forecast of about 5x the service content of the legacy narrow-body fleet for Woodward, which is a big gain that should bode well for us into the next decade.

This content expansion transforms Woodward's long-term aftermarket opportunity. As LEAP engines enter their maintenance cycles, the company anticipates revenue growth from shop visits that far exceeds what legacy CFM56 content provided.

Inflection #2: The L'Orange Acquisition (2018)

Rolls-Royce and Woodward, Inc. jointly announced today that they have signed an agreement for Woodward to acquire L'Orange GmbH and its related operations located in Germany, the United States and China ("L'Orange"), for an enterprise value of €700 million (US$859 million).

L'Orange supplies fuel injection technology for engines that power a wide range of industrial applications including marine power and propulsion systems, special-application vehicles, oil and gas processing, and power generation. L'Orange serves some of the world's best known specialist diesel engine manufacturers, including Rolls-Royce Power Systems' leading subsidiaries, MTU Friedrichshafen and Bergen Engines, and other low to high speed engine builders.

L'Orange, which will be renamed Woodward L'Orange, will be integrated into Woodward's Industrial segment. The acquisition establishes Woodward as a premier technology and system provider of engine control systems to the industrial engine market.

L'Orange has a significant intellectual property portfolio including over 55 active patents, with 75 patents pending. The acquisition brought not just revenue but technological capability in high-pressure fuel injection for large diesel engines—technology that would prove essential as maritime and industrial customers explored alternative fuels.

L'Orange will remain an important partner and supplier for Rolls-Royce Power Systems in the future through a long-term supply agreement, with an initial term of 15 years. L'Orange is based in Stuttgart, Germany and has approximately 1,000 employees based mostly in Germany, but also in the US and China.

Inflection #3: The Failed Hexcel Merger (2020)

In January 2020, Woodward announced what would have been its most transformative transaction ever: a merger of equals with Hexcel Corporation. Hexcel Corporation and Woodward Inc, which makes components for the aerospace and industrial markets, have mutually agreed to terminate their merger agreement, previously announced in January 2020.

The strategic rationale centered on creating a larger, more diversified aerospace supplier combining Woodward's engine and flight controls with Hexcel's advanced composite materials. The stock-swap deal, announced Jan. 12, was supposed to create a horizontally powerful entity—not vertically integrated—that could especially capitalize on lightweighting and other sustainability technologies increasingly demanded as commercial aviation battles a bad climate-change image.

Key aerospace and defense suppliers Woodward and Hexcel have called off their planned merger due to the novel coronavirus outbreak, ending a three-month saga that always baffled many industry insiders and has since been overtaken by survival necessities. But financial analysts and aerospace advisers never bought the pitch and openly questioned the combination of such different companies—Hexcel is a leading provider of composites to A&D while Woodward excels in aircraft parts and fluid- and motion-control systems. At industry conferences in February and March, many commenters would tell audiences they did not understand the reasons. Also, their stock prices have both dropped around 57% since the merger announcement.

Neither company will pay a breakup fee to the other.

In retrospect, the merger cancellation may have been fortuitous. Both companies faced significant COVID-related headwinds that would have complicated integration. Woodward retained strategic flexibility and a clean balance sheet, positioning it to navigate the pandemic downturn and emerge stronger.

Inflection #4: COVID-19 Impact and Recovery (2020–2023)

The pandemic devastated commercial aviation demand, and Woodward's aerospace business suffered accordingly. The recovery that followed, however, demonstrated the durability of Woodward's customer relationships and the embedded nature of its content.

As airlines resumed operations and aircraft utilization climbed, Woodward's aftermarket business recovered rapidly. Legacy aircraft flew longer than anticipated, generating shop visits that exceeded pre-pandemic forecasts. Meanwhile, the Boeing 737 MAX returned to service and narrow-body production rates gradually rebuilt.

Inflection #5: Safran Electromechanical Acquisition (2024–2025)

Woodward (NASDAQ: WWD), a global leader in aerospace and industrial energy control solutions, announced today that it has signed a definitive agreement to acquire the Safran Electronics & Defense electromechanical actuation business based in the United States, Mexico and Canada.

The acquisition, first announced in December 2024, includes intellectual property, operations assets, talent, and long-term customer agreements, including those for Horizontal Stabilizer Trim Actuation (HSTA) systems for aircraft stabilization to support safe and efficient flight, notably used for the Airbus A350. The A350 HSTA, a key product within the acquired portfolio, represents one of the most advanced electromechanical control technologies in large commercial aviation.

"The acquisition of Safran's electromechanical actuation business aligns perfectly to Woodward's growth and innovation value drivers," said Chip Blankenship, Chairman and CEO of Woodward. "It increases our shipset content for current widebody programs and expands our industry-proven technology platform for Next Generation Single Aisle aircraft."

Woodward announced today it has completed its acquisition of Safran's Electronics & Defense electromechanical actuation business based in the United States, Mexico, and Canada in July 2025.

This acquisition positions Woodward for the next wave of aircraft development. As aircraft systems increasingly transition from hydraulic to electromechanical actuation, the company gains proven technology and customer relationships that extend its reach into primary flight control systems.

VI. Business Model Deep Dive

The Two-Segment Structure

Woodward, Inc. designs, manufactures, and services control solutions for the aerospace and industrial markets worldwide. The company operates through two segments, Aerospace and Industrial. The Aerospace segment provides fuel pumps, metering units, actuators, air valves, specialty valves, fuel nozzles, and thrust reverser actuation systems for turbine engines and nacelles, and flight deck controls, actuators, servocontrols, motors, and sensors for aircraft. These products are used on commercial and private aircraft and rotorcraft, as well as on military fixed-wing aircraft and rotorcraft, guided weapons, and other defense systems. It also provides aftermarket maintenance, repair and overhaul, and other services to commercial airlines, repair facilities, military depots, third party repair shops, and other end users.

The Aerospace segment generated approximately 64% of total revenues in recent quarters, with the Industrial segment contributing the balance. This mix has shifted toward aerospace as aviation recovered from pandemic lows and LEAP engine content ramps.

The Defense Business

Woodward's defense exposure provides diversification from commercial aviation cycles. Products serve platforms across the U.S. military services, with content on aircraft including the V-22 Osprey tiltrotor and the F/A-18 fighter.

The defense business operates on long-term program cycles that provide revenue visibility but require patient investment during development phases. Margins tend to be lower than commercial aftermarket but more stable across economic cycles.

The Industrial Segment and Energy Transition

The Industrial segment guidance includes broad-based market strength in power generation and marine transportation, offset by a significant decline in sales related to China on-highway natural gas trucks. Our fiscal year 2025 guidance includes $40 million in sales related to China on-highway natural gas trucks, which would be a year-over-year decline of approximately $175 million.

The China natural gas truck headwind illustrates both the volatility risk in industrial markets and the specificity of certain revenue streams. This business, which had grown rapidly as China promoted LNG-fueled trucking, contracted sharply as Chinese domestic manufacturers gained capability.

More strategically significant is Woodward's positioning for maritime decarbonization. For applications that require the highest levels of power density and efficiency, Woodward is developing a High-Pressure Dual-Fuel (HPDF) platform for methanol and ammonia injection with full diesel backup capability. "The combustion engine industry is accelerating its efforts to decarbonize and switch from fossil fuels to alternative fuels produced from renewable sources (P2X) such as hydrogen, methanol and ammonia, and as a leading global injector manufacturer we need to ensure we have tailor made solutions for this transition."

Woodward, a leading global manufacturer of fuel injection systems, is proud to showcase its comprehensive range of injection systems for P2X fuels, including methanol and ammonia.

The Aftermarket Razor/Blade Model

The economics of Woodward's aerospace business increasingly resemble a classic razor-and-blade model. Original equipment sales provide modest margins but establish installed base; aftermarket spares, repairs, and overhauls generate higher margins over the multi-decade life of aircraft programs.

On the Leap engine that powers the Boeing 737 MAX and Airbus A320neo, and the Pratt & Whitney geared turbofan (GTF) that also powers the A320neo as well as the A220, Woodward has three times the shipset content it had on the predecessor 737NG and A320ceo programs. "Given Boeing's and Airbus' delivery delays, the commercial aftermarket will be stronger for longer, and Woodward will see outsized earnings per share and free cash flow growth as Leap and GTF shop visits ramp throughout this decade."

Management identified the ramp in LEAP and GTF aftermarket repair activity and stated LEAP/GTF repair revenue will surpass legacy engines in late 2026 or early 2027.

This transition represents a generational shift in Woodward's revenue composition. The tripled shipset content on current-generation narrow-body aircraft, combined with their extended operational lives as production delays persist, creates a multi-year tailwind for aftermarket revenue and margins.

VII. Financial Performance and Metrics

Record-Breaking FY2024

"We delivered record sales in fiscal 2024 with Woodward revenue exceeding $3 billion for the first time. Robust end market demand along with contributions from operational excellence fueled significant sales growth and earnings expansion," said Chip Blankenship, Chairman and Chief Executive Officer.

In 2024, Woodward's revenue was $3.32 billion, an increase of 14.06% compared to the previous year's $2.91 billion. Earnings were $372.97 million, an increase of 60.51%.

Profitability and Margin Expansion

The outperformance of earnings relative to revenue reflects meaningful operating leverage. As production volumes increased to meet customer demand, fixed costs spread across more units, and pricing actions absorbed cost inflation.

Woodward exceeded earnings expectations, with FY24 sales at $3.3 billion and a 46% growth in free cash flow, driving a stock price surge.

Capital Allocation: Aggressive Buybacks Signal Confidence

Woodward's Board of Directors has approved a new $1.8 billion, three-year share repurchase authorization, marking a decisive and strategic use of its strong balance sheet to drive shareholder value. Woodward completed its prior $600 million authorization in November 2025, more than a year ahead of plan, reflecting the Company's ongoing commitment to purposeful and disciplined capital deployment.

"This new authorization reflects the Board's confidence in Woodward's long-term growth trajectory, robust cash generation, and our commitment to delivering compelling shareholder returns," said Chip Blankenship. "We continue to see substantial growth opportunities across our end markets, driven by strong demand, technology leadership, and our disciplined execution."

Valuation Context

The firm has a market capitalization of $15.66 billion, a PE ratio of 41.33, a P/E/G ratio of 2.61 and a beta of 1.26. Woodward has a fifty-two week low of $146.82 and a fifty-two week high of $274.50.

The latest closing stock price for Woodward as of November 18, 2025 is 257.64. The all-time high Woodward stock closing price was 274.03 on November 12, 2025.

According to our calculations, a $1000 investment made in May 2015 would be worth $4,141.95, or a 314.20% gain, as of May 19, 2025. Investors should keep in mind that this return excludes dividends but includes price appreciation. In comparison, the S&P 500 gained 180.69% and the price of gold went up 153.90% over the same time frame.

VIII. Leadership: The Chip Blankenship Era

Mr. Blankenship's prior leadership roles before joining Woodward include the CEO of Arconic, an aerospace advanced alloys and components company, a 24-year career at GE where he held significant leadership roles in Aviation, Energy, and Appliances, including the CEO of Appliances, Vice President and General Manager Commercial Aircraft Engines, and General Manager Aero Energy (aero-derivative industrial turbines). Most recently, Mr. Blankenship served as the Montgomery Distinguished Professor of Practice at The University of Virginia's School of Engineering and Applied Sciences. Mr. Blankenship holds a PhD in Material Science and Engineering from The University of Virginia and a bachelor's degree from Virginia Polytechnic Institute and State University.

Charles "Chip" P. Blankenship, Jr: Chairman of the Board, Chief Executive Officer and President since May 9, 2022. Prior to joining Woodward, Mr. Blankenship served as the Montgomery Distinguished Professor of Practice at the University of Virginia's School of Engineering and Applied Sciences from August 2019 through January 2022. Mr. Blankenship served as Chief Executive Officer of Arconic from January 2018 through February 2019.

Blankenship's background—deep GE Aviation experience combined with CEO tenure at an aerospace materials company—equipped him with customer relationships and industry understanding relevant to Woodward's strategic positioning. His materials science PhD provides technical credibility with engineering-driven customers.

Tom Gendron has been Chairman of the Board of Woodward, Inc. since January 2008, and has been President and Chief Executive Officer since July 2005. The transition from Gendron's 31-year tenure represented a significant generational shift, bringing external perspective while maintaining operational continuity.

IX. Competitive Landscape and Strategic Position

The Competitive Set

Parker Hannifin is a top competitor of Woodward. Parker Hannifin was founded in 1917, and is headquartered in Cleveland, Ohio. Like Woodward, Parker Hannifin also competes in the Aerospace & Defense field. Parker Hannifin generates $16.4B more revenue vs. Woodward.

Woodward is a top competitor of Moog. Woodward was founded in 1870, and is headquartered in Fort Collins, Colorado. Like Moog, Woodward also competes in the Aerospace field. Woodward generates $307.5M less revenue vs. Moog.

In its 2024 annual report, Parker lists key rivals across its segments: in aerospace markets Crane Co., Eaton, Honeywell, Moog, RTX, Safran, Senior, Triumph and Woodward.

The competitive landscape reveals Woodward's positioning as a focused specialist competing against much larger diversified industrials. While Parker Hannifin generates nearly six times Woodward's revenue, much of that scale comes from non-aerospace markets where Woodward doesn't compete.

Porter's Five Forces Analysis

Threat of New Entrants: LOW

Aerospace certification requirements create nearly insurmountable barriers. Qualifying a new fuel system or flight control component for commercial aviation requires years of testing, millions in investment, and existing customer relationships to sponsor development programs. The 155 years of accumulated engineering expertise and institutional knowledge cannot be replicated quickly.

Supplier Power: MODERATE

Woodward relies on specialized raw materials and precision components. Long-term supply agreements and the L'Orange acquisition (which brought vertical integration in injection systems) provide some protection. However, supply chain disruptions during the pandemic revealed vulnerabilities.

Buyer Power: MODERATE-HIGH

Customer concentration presents real risk. Boeing, Airbus, GE, and Safran represent significant revenue percentages, and these customers possess sophisticated procurement organizations capable of extracting pricing concessions. However, the cost of switching suppliers mid-program is extremely high, and Woodward's content on multi-decade production programs provides embedded positioning.

Threat of Substitutes: LOW

There are no viable substitutes for precision aircraft engine controls. Electrification creates opportunity rather than threat—the Safran acquisition positions Woodward for electromechanical actuation as aircraft systems evolve. Regulatory requirements mandate specific control architectures.

Competitive Rivalry: MODERATE

While Woodward faces capable competitors, specialized niches reduce direct overlap. Moog's Aircraft Controls and Defense Controls segments directly compete with Parker's aerospace hydraulics and electronic controls. In FY2023, Moog grew sales 9% to a record $3.32B, benefiting from civilian jet demand and defense programs.

Long product cycles (20-30 years for aircraft programs) mean competition occurs primarily at program inception. Once designed into a platform, suppliers rarely get displaced. Most competitive intensity focuses on winning positions on new programs rather than unseating incumbents.

Hamilton's 7 Powers Framework

Scale Economies: MODERATE

Manufacturing scale provides cost advantages, and the MRO network creates service scale benefits. However, highly engineered products limit mass production advantages—this is precision manufacturing, not commodity production.

Network Effects: LIMITED

Woodward's business doesn't exhibit traditional network effects. There are some ecosystem benefits from integration across customer platforms, but nothing comparable to platform businesses.

Counter-Positioning: STRONG

Woodward's focus on turbine and engine control systems differentiates from larger competitors. The company has maintained strategic discipline, avoiding the temptation to diversify into adjacent aerospace segments where it lacks competitive advantage.

Switching Costs: VERY HIGH

This represents Woodward's strongest strategic power. Once content is designed into an aircraft or engine program, switching suppliers requires re-certification, re-qualification, and customer re-acceptance—a process so expensive and time-consuming that it rarely occurs during a program's production life.

Cornered Resource: MODERATE

155 years of accumulated engineering expertise in control systems represents institutional knowledge that competitors cannot easily replicate. The company's patent portfolio and trade secrets in precision manufacturing constitute meaningful barriers.

Process Power: STRONG

Woodward's ability to consistently deliver precision components that meet aerospace certification requirements reflects process capabilities embedded in organizational culture. The workforce's manufacturing expertise develops over years; it cannot be quickly hired or acquired.

Branding: LIMITED

In B2B aerospace, Woodward's brand represents reliability and technical capability rather than consumer preference. It matters—OEMs specify Woodward by name—but works differently than consumer brand power.

X. Investment Considerations: Key Metrics to Monitor

For investors evaluating Woodward, two metrics deserve primary attention:

1. Aerospace Aftermarket Revenue Growth

This metric captures the core thesis: that tripled shipset content on current-generation narrow-body aircraft will drive aftermarket revenue well above historical levels as LEAP and GTF engines enter maintenance cycles. Management identified the ramp in LEAP and GTF aftermarket repair activity and stated LEAP/GTF repair revenue will surpass legacy engines in late 2026 or early 2027.

Quarterly aftermarket disclosures reveal whether this inflection is proceeding as anticipated. Strong growth validates the investment thesis; deceleration would raise questions about competitive positioning or pricing power.

2. Operating Margin Trajectory

Woodward has demonstrated meaningful margin expansion alongside revenue growth. Continued expansion would indicate operating leverage and pricing power; margin compression would suggest competitive pressure or cost challenges.

Woodward had a net margin of 11.32% and a return on equity of 16.57%. Woodward has set its FY 2026 guidance at 7.500-8.000 EPS.

Bull Case

The bull case rests on secular aerospace tailwinds and Woodward's enhanced positioning to capture them:

- Commercial aviation remains structurally undersupplied, with production rates below demand and aging fleets requiring replacement

- LEAP and GTF content provides 3x legacy shipset value, driving both OEM and aftermarket growth

- Electromechanical acquisition positions for next-generation aircraft architecture

- Maritime energy transition creates industrial segment opportunity

- Strong free cash flow enables both growth investment and shareholder returns

Bear Case

Risks include:

- Customer Concentration: Dependence on Boeing, Airbus, and major engine OEMs creates vulnerability to their production and financial challenges

- China Industrial Weakness: The Industrial segment guidance includes broad-based market strength in power generation and marine transportation, offset by a significant decline in sales related to China on-highway natural gas trucks

- Valuation: The firm has a PE ratio of 41.33—premium multiples assume flawless execution on growth initiatives

- Commercial Aviation Cyclicality: Despite current undersupply, aerospace remains cyclical; recession would pressure production rates

- Defense Budget Uncertainty: Political shifts could affect military program funding

XI. Conclusion: The Power of Strategic Patience

Woodward's 155-year journey from waterwheel governors to aircraft engine controls illustrates a distinctive approach to corporate longevity: patient expertise development combined with opportunistic pivots when technology transitions create new possibilities.

The company didn't predict in 1870 that aircraft would dominate its future revenue. It didn't know in 1933 that jet engines would replace propellers as the primary application for its control expertise. It couldn't foresee in 2018 that an acquisition of German fuel injection technology would position it for maritime decarbonization.

What Woodward did know—and has demonstrated across 155 years—is that precision control of energy conversion represents enduring value. Waterwheels give way to turbines; turbines evolve from steam to gas to jet propulsion; fuels transition from coal to diesel to kerosene to perhaps hydrogen and ammonia. Through each transition, the fundamental challenge persists: controlling the rate at which energy converts to useful work.

Woodward reported fiscal 2024 revenue above $3 billion and employs more than 10,000 globally.

The coming decade will test whether Woodward's positioning for the LEAP aftermarket cycle and electromechanical aircraft evolution justifies current valuations. For investors, the question is whether 155 years of demonstrated adaptability provides sufficient confidence in the company's ability to navigate whatever transformations aviation and industrial energy systems encounter next.

What seems clear is that Woodward occupies a strategic position—mission-critical components with extreme switching costs in markets that reward reliability above all else—that few competitors can replicate. Whether that position translates to shareholder returns depends on execution, capital allocation, and the endurance of secular growth in global aviation and energy systems.

As Amos Woodward understood in 1870, controlling energy conversion matters. His descendants—corporate rather than biological—continue proving him right.

XII. The Cultural Foundation: Engineering Excellence as Institutional Identity

The Rockford-to-Fort Collins Journey

Woodward's geographic evolution reflects broader shifts in American manufacturing and aerospace industry clusters. The company maintained its Rockford, Illinois headquarters for over a century before establishing its current home in Fort Collins, Colorado. After 137 years in Rockford, Woodward Governor Co. moved its corporate headquarters to Fort Collins, Colorado. The move was largely symbolic, involving only about a half-dozen staffers. The company moved its headquarters to Fort Collins from Rockford, Illinois, in 2007, and had maintained a presence in Northern Colorado for the past 60 years.

In 2016, Woodward completed the new $225 million Lincoln campus on a 700-acre site in downtown Fort Collins to house the new industrial turbomachinery systems building as well as the new headquarters building. As Tom Gendron explained, "We wanted to locate in a competitive community with a skilled workforce, good infrastructure and great quality of life. We examined all our options and landed in Northern Colorado for all of these reasons."

Yet Woodward maintained its Rock Cut campus in Rockford, Illinois, which was featured in Manufacturing Today highlighting the company's "rich history and diverse capabilities across the aerospace business segment."

Manufacturing Footprint ExpansionIn September 2025, Woodward announced it selected Spartanburg County to establish a new manufacturing operation in South Carolina. The nearly $200 million investment will create approximately 275 new jobs.

The 300,000-square-foot facility will focus on production of servo-hydraulic actuation systems, which are critical components used in aircraft flight control. Initially, most of the factory's capacity will be dedicated to producing spoiler actuation for the Airbus A350.

CEO Chip Blankenship framed the significance: "It will be a showcase manufacturing site, much like our Rock Cut campus, vertically integrated, highly automated, and built on the capabilities and methodologies in operational excellence we've developed through our LEAP and GTF aircraft engine programs." "Beyond supporting the Airbus A350, this facility positions us to extend our hydraulic flight control design and industrialization expertise to additional applications as well as other commercial aircraft manufacturers."

The site is expected to become operational in 2027 and will progressively scale production and hiring in subsequent years to meet market demand.

Employee Culture and DevelopmentThe company's culture reflects its engineering heritage. Woodward is committed to creating a great workplace for all team members. The company and its members are committed to acting with integrity, being respectful and accountable to one another, and staying humble and driven, while maintaining the highest professional and ethical standards.

In September 2025, Woodward announced that the company has been named one of the World's Best Companies by TIME and Statista. The Employee Satisfaction component was based on survey data from approximately 200,000 employees in over 50 countries, encompassing direct and indirect recommendations of companies as well as evaluations of employers across the dimensions of image, atmosphere, working conditions, salary, workplace, and equality by verified employees.

The staff at Woodward come from unusually diverse demographic backgrounds, with the company being 40.8% female and 33.1% ethnic minorities. The company has great employee retention with staff members usually staying for 5.2 years.

XIII. ESG and Sustainability Positioning

The Energy Transition OpportunityWoodward's approach to sustainability centers on its core business purpose: energy control solutions that enhance system performance, increase fuel efficiency, and reduce carbon emissions. Together with its customers, the company is enabling the path to a cleaner, decarbonized world.

CEO Chip Blankenship has stated that "Sustainability is not just a buzzword, but a fundamental aspect of doing business in today's interconnected world." The company takes pride in its focus on energy control solutions that enhance system performance, increase fuel efficiency, and reduce carbon emissions, exemplifying its dedication to creating a cleaner, better future.

With 33 locations in 14 countries around the world, Woodward continues on its journey to continuously improve its sustainable outcomes, including tracking and improving global environmental impact, creating value for members and communities, and comprehensive governance around sustainability programs.

The company's products inherently support efficiency and emissions reduction—fuel systems that optimize combustion reduce both fuel consumption and emissions. Aircraft equipped with Woodward controls operate more efficiently; industrial turbines with Woodward combustion systems achieve lower emissions profiles.

Hydrogen and Alternative FuelsThe aviation industry's evolution toward alternative fuels presents both opportunity and complexity for Woodward. After investing in research into both hydrogen combustion and hydrogen fuel cell technology, Airbus determined in 2025 that fuel cells are the most promising option for a future hydrogen-powered aircraft. Airbus committed to taking on this challenge in 2020 when it launched the ZEROe project, which aims to bring a hydrogen-powered aircraft to the skies, and after investing in research into both hydrogen combustion and hydrogen fuel cell technology, determined in 2025 that fuel cells are the most promising option.

For Woodward, the transition to hydrogen or electric propulsion could reshape the competitive landscape in ways that remain uncertain. Fuel systems for hydrogen combustion would require different engineering than kerosene-based systems, while fuel cell propulsion might reduce demand for some traditional Woodward products while creating opportunities in electromechanical actuation and power electronics.

The company's 2024 Safran electromechanical acquisition and continued investment in actuation systems position it for scenarios where aircraft systems become increasingly electrified. Whether hydrogen gains traction or conventional jet fuel remains dominant for large commercial aircraft, Woodward's core competency—precision control of energy systems—remains relevant.

XIV. Risk Factors and Challenges

Customer Concentration

Woodward's dependence on a concentrated customer base represents inherent risk. Boeing, Airbus, GE, Safran, and the major defense contractors collectively represent substantial revenue percentages. Any production disruption, financial difficulty, or strategic shift by these customers would have direct consequences for Woodward's financial performance.

The Boeing 737 MAX grounding in 2019-2020 illustrated this vulnerability, though Woodward's diversified OEM relationships provided some buffer. The company's multi-decade program relationships create lock-in that protects against displacement but also creates exposure when specific platforms face challenges.

China Industrial ExposureThe China on-highway natural gas truck market has proven particularly volatile for Woodward's Industrial segment. Sales for on-highway natural gas trucks in China totaled $21 million in the last reported quarter. Management earlier announced that it expects full-year revenues from China on-highway natural-gas trucks to reach only $40 million, indicating a significant decline of $175 million from fiscal 2024.

The Industrial segment has faced a more turbulent environment. A 5% revenue decline in Q2, driven by an 18% drop in China on-highway natural gas truck sales, has raised concerns about geographic and market concentration. However, this weakness is not a reflection of operational failure but rather a consequence of external factors, including China's economic slowdown and regulatory shifts in its transportation sector.

When asked about the volatility in the China on-highway natural gas truck market, management indicated that they continuously evaluate their portfolio for strategic alignment, and are currently focused on serving their customers with the best technology and managing through the downturn efficiently.

Supply Chain Vulnerabilities

The global supply chain disruptions that emerged during the pandemic exposed vulnerabilities in precision manufacturing. Aerospace components require specialized materials and sub-components from multiple suppliers, and disruptions anywhere in the chain can cascade through production schedules.

Woodward has invested in supply chain resilience through vertical integration (such as the L'Orange acquisition) and supplier relationship management. However, the company remains dependent on global supply chains for critical materials and components.

Tariff and Trade Risks

Woodward's management stated: "Based on what we know today, we are confident in Woodward's ability to manage the announced tariff levels and current operating environment in the second half of the fiscal year. We are raising the low end of our sales and earnings guidance and reaffirming the other elements of our full-year outlook. Our long-term value proposition remains intact, and we are committed to achieving sustainable growth and enhancing shareholder value."

However, the company's revised guidance did not incorporate potential effects from further escalation of announced tariff levels, significant changes in customer demand, or recession globally—representing downside scenarios that remain possible.

XV. Recent Developments: Fiscal Year 2025Just yesterday, on November 24, 2025, Woodward reported financial results for its fiscal year 2025 and fourth quarter ending September 30, 2025.

"Woodward delivered another year of record sales in fiscal 2025, driven by strong demand and disciplined execution that expanded earnings and strengthened our foundation for growth," said Chip Blankenship, Chairman and Chief Executive Officer. "Aerospace delivered substantial sales and margin expansion supported by high aircraft utilization and robust defense activity, while Industrial achieved double-digit growth across power generation and oil & gas markets.

For the full fiscal year 2025, Woodward achieved record sales of $3.6 billion, a 7% increase from $3.3 billion in FY24. Adjusted net earnings rose 12% to $424 million, with adjusted EPS growing 13% to $6.89.

Woodward reported record fiscal 2025 results with $3.6B sales (+7% YoY), $442M net earnings (+19%) and $7.19 EPS (+20%). Fourth-quarter sales were $995M (+16%) with net earnings of $138M (+66%).

The results beat Wall Street expectations. The average estimate of four analysts surveyed by Zacks Investment Research was for earnings of $1.83 per share.

The aerospace segment was the primary growth driver for Woodward in FY25, with sales increasing 14% to $2.3 billion and segment earnings rising 32% to $507 million.

Fiscal 2026 Guidance

Fiscal 2026 guidance calls for sales growth 7%–12%, EPS of $7.50–$8.00, free cash flow of $300–$350M, and capex ~$290M.

At the consolidated level, Woodward net sales growth is expected to be between 7-12%. Aerospace sales growth is expected to be between 9-15% and industrial sales are expected to grow 5% to 9%. In aerospace, the company expects sales growth across the segment weighted towards OEM driven by a return to growth in commercial OEM and continued strength in defense OEM.

Key Fiscal 2025 Achievements

The company announced several major accomplishments during fiscal 2025:

Completed strategic acquisition of Safran's North American Electromechanical Actuation business, enhancing existing portfolio with industry-leading Horizontal Stabilizer Trim Actuation technology and other complementary products. The board authorized new three-year $1.8 billion share repurchase program. The company was selected by Airbus to supply 12 of the 14 spoiler actuation systems for the A350, its first primary flight control system on a commercial aircraft. It also broke ground on a cutting-edge facility in Spartanburg County, South Carolina.

During fiscal 2025, as anticipated, the company returned over $238 million to stockholders, including $173 million in share repurchases and $65 million in dividends. In November 2025, it successfully completed its previous three-year $600 million share repurchase authorization, more than one year ahead of schedule, reflecting ongoing commitment to return cash to shareholders.

"Fiscal 2025 was a pivotal year for Woodward. With enhanced capabilities and deep customer partnerships, we are well positioned to capture opportunities from the next generation of aircraft and energy systems. We remain focused on growth, operational excellence, and innovation to drive sustained performance and long-term shareholder value."

XVI. Conclusion: 155 Years of Controlled Energy

The story of Woodward, Inc. offers a compelling case study in industrial longevity. From Amos Woodward's waterwheel governor patented in 1870 to the precision fuel systems and electromechanical actuators powering today's most advanced aircraft, the company has demonstrated remarkable adaptability while maintaining focus on a singular mission: controlling energy conversion for machines that cannot afford to fail.

The Compounding Value of Engineering Excellence

Woodward's competitive advantages derive from capabilities that accumulate over decades rather than years. The institutional knowledge embedded in its engineering workforce—the tacit understanding of how fuel systems behave under extreme conditions, how actuators respond to varying loads, how electronic controls integrate with mechanical systems—represents intellectual capital that competitors cannot quickly replicate.

The company's 155-year track record provides credibility with customers who stake their own reputations on component reliability. When Boeing, Airbus, GE, or Safran selects a supplier for a new aircraft program, the decision carries twenty-year consequences. Woodward's demonstrated ability to deliver across multiple technology generations—from mechanical governors to digital controls, from propeller pitch to jet engine fuel management—provides confidence that it will navigate whatever transitions the future brings.

The Aerospace Aftermarket Thesis

For investors, the central thesis currently centers on the LEAP and GTF engine aftermarket cycle. Management has stated that LEAP/GTF repair revenue will surpass legacy engines in late 2026 or early 2027. With tripled shipset content compared to predecessor programs, this transition represents a step-change in aftermarket revenue potential.

The fiscal 2025 results validate this trajectory. Aerospace segment earnings reached $507 million, representing 21.9% of segment net sales—a meaningful margin expansion that reflects both pricing power and operating leverage as content ramps on high-value programs.

The Industrial Diversification Reality

The Industrial segment tells a more complex story. Strength in power generation and marine transportation has been offset by significant weakness in China on-highway natural gas trucks. The company's positioning for maritime decarbonization through its L'Orange capabilities offers long-term potential, but near-term results remain volatile.

This segment diversification provides ballast when aerospace cycles inevitably turn negative, but at the cost of exposure to industrial market dynamics that management cannot fully control. The fiscal 2026 guidance for 5-9% Industrial sales growth suggests management expects stabilization, though China-related risks persist.

Strategic Positioning for the Next Decade

The recent acquisitions and investments position Woodward for several potential future scenarios:

-

The Safran electromechanical acquisition positions for increased aircraft electrification regardless of whether propulsion systems shift to hydrogen or remain kerosene-based

-

The Airbus A350 spoiler actuation win and South Carolina facility expand flight control content beyond engine systems to primary airframe actuation

-

The L'Orange portfolio enables participation in maritime energy transition as shipping decarbonizes through methanol, ammonia, and other alternative fuels

-

The Rock Cut and MRO investments prepare for the aftermarket surge as LEAP and GTF engines mature

The Price of Quality

Woodward's current valuation—trading near all-time highs with an elevated price-to-earnings ratio—reflects market confidence in the aerospace aftermarket thesis and the company's execution track record. The premium valuation leaves limited room for disappointment; any stumble in program execution, customer production rates, or aftermarket timing would likely produce meaningful share price volatility.

For long-term investors, the question is whether Woodward's competitive positioning—extreme switching costs, multi-decade program relationships, accumulated engineering expertise—justifies premium valuation despite the inevitable cyclicality of aerospace markets.

The Final Assessment

What makes Woodward remarkable is not any single innovation but rather the consistent application of engineering excellence across technology transitions spanning more than a century and a half. Amos Woodward's waterwheel governor addressed the same fundamental challenge that Woodward's digital fuel controls address today: ensuring that energy conversion happens precisely when and how operators require.

In a business world obsessed with disruption and rapid change, Woodward offers a different model: patient expertise development, strategic customer alignment, and unwavering focus on mission-critical reliability. The company has navigated the death of waterwheel power, the transition from propellers to jets, and the shift from mechanical to digital controls—all while maintaining its core identity.

Whether Woodward will navigate the next great transitions—aircraft electrification, alternative aviation fuels, autonomous flight systems—with similar success remains to be seen. What the historical record suggests is that a company with 155 years of demonstrated adaptability, locked-in customer relationships, and accumulated engineering excellence deserves the benefit of the doubt.

As CEO Chip Blankenship noted, "With enhanced capabilities and deep customer partnerships, we are well positioned to capture opportunities from the next generation of aircraft and energy systems."

For those who believe global aviation will continue growing, that aircraft reliability will remain paramount, and that precision energy control will retain its value regardless of fuel source—Woodward represents a company that has proven, across a century and a half, that it knows how to remain indispensable to customers who cannot afford failure.

That is a record worth understanding, even for those who never fly knowing that Woodward hardware ensures their safe arrival.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube