TE Connectivity: The Hidden Giant Behind Every Connection

I. Introduction & Episode Roadmap

The control room of a modern electric vehicle doesn't look much like a traditional car dashboard. Banks of screens, dozens of sensors, kilometers of wiring—all orchestrated by thousands of tiny connectors that most people will never see. When a Tesla Model S accelerates silently from a stoplight, or when a Boeing 787 Dreamliner banks gracefully over the Pacific, or when a surgeon guides a robotic arm through a millimeter-precise incision, the same invisible architecture is at work: connectivity infrastructure that routes power, data, and signals through the nervous system of modern technology.

What if there were a company that supplied the critical connectors for virtually all of these applications—a $66 billion enterprise whose products touch nearly every car, airplane, smartphone, and data center on Earth—yet whose name barely registers outside of engineering circles?

That company is TE Connectivity, a $17 billion global industrial technology leader in connectivity and sensor solutions that enable a safer, sustainable, productive, and connected future. With more than 85,000 employees, including 8,000 engineers, working alongside customers in approximately 130 countries, TE ensures that "EVERY CONNECTION COUNTS."

Consider the scale: TE Connectivity employs approximately 87,000 people worldwide and maintains a market capitalization of $66.544 billion. The company's sales to the automotive market alone accounted for approximately 60% of its total sales during fiscal year 2024, positioning it as one of the most important but least understood suppliers in the global automotive supply chain.

The central question driving this analysis: How did a company making "invisible" connector components become one of the most essential businesses in the modern economy? The answer takes us through eight decades of transformation—from wartime innovation above a New Jersey restaurant, through one of the most spectacular corporate scandals in American history, to emergence as the dominant force in electric vehicle connectivity and AI-driven data center infrastructure.

This is not merely a story about connectors. It's a case study in corporate reinvention, strategic focus, and the compounding value of engineering excellence in unsexy but essential technologies. When Warren Buffett speaks of "moats," he often points to brand recognition or network effects. TE Connectivity represents a different kind of moat: the irreplaceable middleware of modern industrial civilization.

II. The Origin Story: AMP's Founding & WWII Innovation (1941-1945)

The Founder's Insight

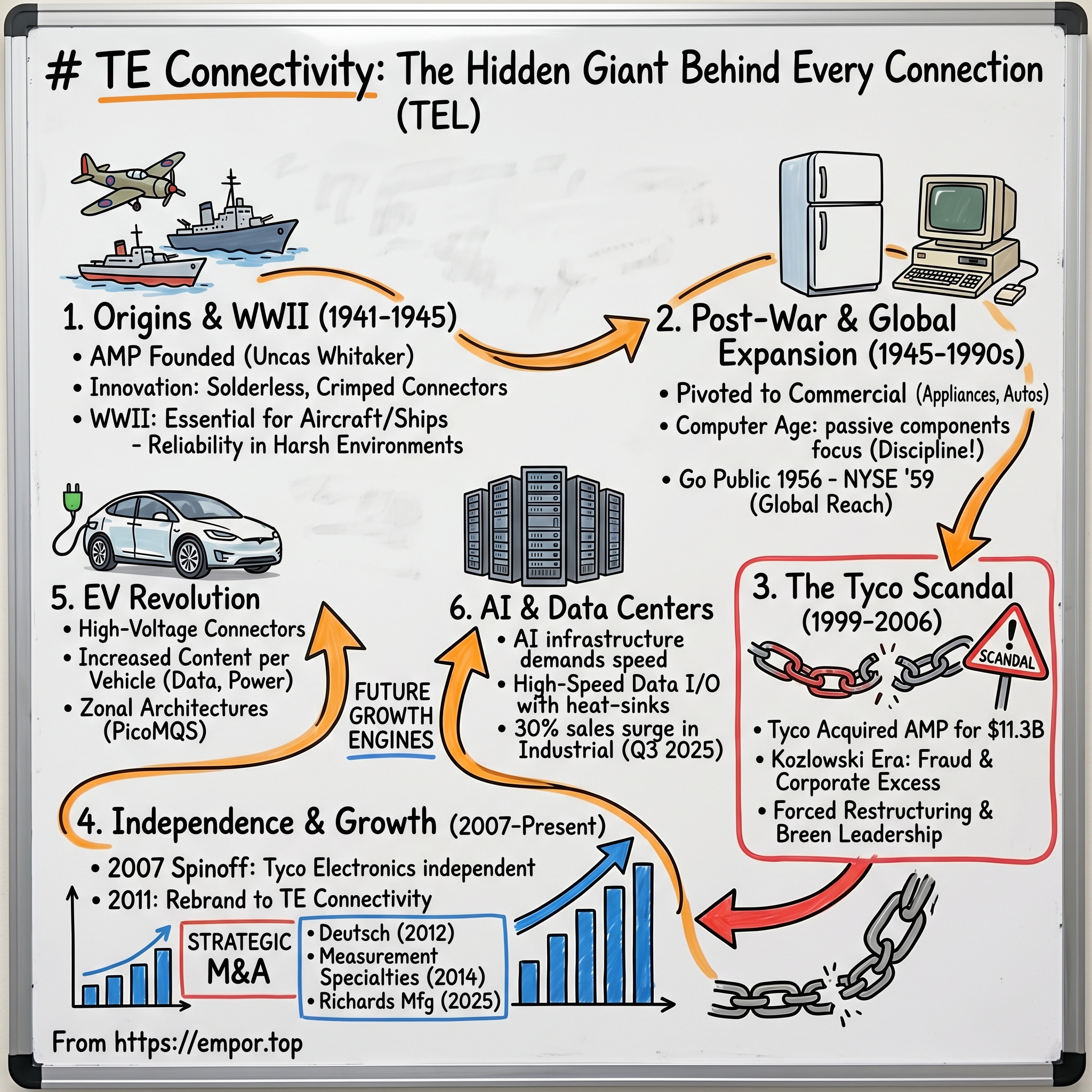

On a late afternoon in September 1941, in a cramped office above a Greek restaurant in Elizabeth, New Jersey, an engineer named Uncas Aeneas Whitaker was wrestling with a problem that would change the course of industrial history.

Uncas Aeneas Whitaker was born March 22nd, 1900, and is known for founding Aircraft-Marine Products, AMP Inc., and his philanthropic work sharing his fortune. He received a degree in mechanical engineering from MIT, and electrical engineering degree from Carnegie Institute of Technology, and a law degree from the Cleveland Law School.

This unusual combination of technical and legal training would prove invaluable. The founder of AMP was Uncas A. Whitaker, a former employee of Westinghouse Electric and the Hoover Company. In 1941, after two years as a senior engineer for American Machine & Foundry in New York, Whitaker decided to start his own company.

Whitaker's insight was deceptively simple but profoundly important. At the time, electrical connections were almost universally made through soldering—heating metal and flux to create permanent bonds between wires and terminals. This worked adequately for stationary applications, but was problematic in environments with vibration, temperature extremes, and space constraints. Aircraft, ships, and vehicles of the early 1940s were becoming increasingly complex electrical systems, and soldered connections were proving unreliable.

The Revolutionary Product

Aircraft Marine Products, as the company was called, specialized in solderless, uninsulated electrical connections for aircraft and boat manufacturers: a short metal tube with a ring on the end and a crimping tool. The device allowed electricians to make quick, removable wire connections without a heating element or flux. It was simple, unique, and very popular.

The crimped termination—where a specialized tool mechanically compresses a metal terminal onto a wire—offered several advantages over soldering: faster installation, more reliable performance in vibration-prone environments, easier maintenance, and critically, connections that could be made in cramped spaces where heating elements were impractical or dangerous.

At the age of 41, he founded Aircraft Marine Products (AMP), in Harrisburg, Pennsylvania, which would become the world's largest manufacturer of electrical devices and connectors. His company was instrumental in the development of miniature components and advanced computer technologies which have been incorporated into thousands of business operations and commercial products.

Perfect Timing: World War II

The timing could not have been more providential. From a small office in New Jersey, Aircraft Marine established supply contracts with some of the largest industrial manufacturers in the world. Less than three months after the company was created, the United States entered World War II.

The war transformed AMP from a promising startup into an essential defense contractor. Wartime production of battleships and aircraft led to great success for the company. The higher-performance aircraft being developed operated at higher altitudes and experienced dramatically higher shock and vibration conditions than their predecessors. AMP's crimped connectors maintained electrical connections in these demanding and harsh environmental conditions—exactly the problem Whitaker had set out to solve.

Boeing, Electric Boat (the submarine manufacturer), and Ford Motor Company all became early customers. Every B-17 Flying Fortress, every submarine slipping beneath the Pacific, every jeep rolling off Ford's assembly lines carried AMP connectors. By war's end, the company had proven that its technology was not a niche curiosity but a fundamental improvement in electrical engineering.

For investors studying TE today, this origin story establishes a pattern that persists eighty years later: TE's competitive advantage derives from solving demanding engineering problems in harsh environments. The company did not invent electrical connectors—it invented better electrical connectors for the most demanding applications.

III. Post-War Transformation & Growth (1945-1990s)

Pivoting from Military to Commercial

The end of World War II brought an existential crisis that many defense contractors failed to survive. Still, the transition was stressful for Aircraft Marine. It was able to survive the sudden drop in orders through drastic austerity measures and additional underwriting from Midland Investment Company, its primary benefactor.

Many of Aircraft Marine's customers went bankrupt, were acquired, or were forced into mergers; in general they were compelled to reduce the scale of their operations drastically. Aircraft Marine, however, needed little product conversion in order to adapt to the postwar economy, because its connections were versatile components rather than more specialized finished products.

This versatility proved crucial. The same technology that maintained electrical integrity in a dive bomber at 20,000 feet could maintain connections in an automobile, a refrigerator, or an early computer. The company pivoted aggressively toward commercial applications.

Aircraft Marine re-entered the commercial market with another new product, the strip-formed terminal. During 1952, the company created a marketing unit called AMP Special Industries, and established sales of existing products and the introduction of connectors for pin and sockets, coaxial cables, and printed circuits resulted in unprecedented growth.

The strip-formed terminal represented a manufacturing innovation as important as the original crimped connection. Combined with AMP's automated lead terminating machines, manufacturers could produce thousands of quality-inspected wire terminations per hour—essential for meeting the growing demand for post-war consumer electronics and appliances.

The Computer Age Expansion

In the 1950s, as the computer industry emerged, AMP positioned itself as an essential supplier. The ENIAC, UNIVAC, and their successors required thousands of reliable connections, and AMP's products were ideal for these applications. Whitaker built the world's largest manufacturer of electrical devices and connectors. His company was instrumental in the development of miniature components and advanced computer technologies which have been incorporated into literally thousands of business operations and commercial products.

The strategic decision to focus on connectors rather than diversify into active electronic components proved prescient. AMP made a conscious decision during the 1960s against diversification into a wider range of products. Instead, management elected to concentrate on the "passive components" market it had come to dominate. AMP had experienced 15% annual growth in the ten years since the mid-1950s and anticipated an increasingly difficult "active component" market in the ensuing decades.

This discipline paid enormous dividends. Indeed, though Japanese electronics manufacturers were developing new capabilities in active components—particularly transistors—they neglected to take advantage of trade regulations that would have allowed them to establish an enduring position in passive components. As a result, AMP became the largest passive component manufacturer in Japan.

Going Public & Global Expansion

Expanding through sales-led growth rather than by acquisition, in the 1950s Aircraft Marine added subsidiaries in Australia, Britain, the Netherlands, Italy, Japan, Mexico, and West Germany.

Aircraft Marine changed its name to AMP Incorporated upon incorporation as a public company in 1956. The company thereafter raised additional capital through share offerings. AMP improved and expanded its plant space and began a more ambitious research and development effort. Having demonstrated brisk and stable growth, AMP was listed on the New York Stock Exchange in October 1959.

By the 1990s, boasting more than 100,000 types and sizes of products in its line and a reputation for dependable customer service and high quality, AMP has long enjoyed steady growth through heavy research and development spending and aggressive global expansion.

Whitaker relinquished the company presidency to George A. Ingalls in 1961. Although he remained chairman, Whitaker wished to emphasize a more democratic form of leadership. He assigned many of his own managerial responsibilities to other managers and slowly removed himself from the company's daily operations.

Whitaker, however, served as chairman until his death in 1975. His death neither interrupted the company's business nor caused a management battle for power.

By the late 1990s, AMP Incorporated had become the world leader in electrical and electronic connection devices, claiming 19 percent of the $19 billion worldwide interconnections market. The company Whitaker founded above a Greek restaurant had become one of the most successful industrial enterprises in American history.

For investors, the 35-year arc from 1956 to 1991 demonstrates the power of focused excellence. AMP resisted the conglomerate temptation that destroyed many postwar industrial companies, instead pursuing what would now be called "sticking to the knitting." This discipline built a dominant market position that proved tremendously valuable—which brings us to the next, more turbulent chapter.

IV. The Tyco Acquisition & Conglomerate Era (1999-2006)

The $11.3 Billion Acquisition

In 1999, AMP Incorporated—the proud, disciplined connector company that Whitaker had built—was swallowed by one of the most aggressive conglomerates of the era. In 1999, Tyco acquired two S&P 500 companies in a buyout. They acquired the electronics connector manufacturer AMP Inc., for $12.22 billion and a materials science company, Raychem Corp., for $1.4 billion.

The acquisition integrated AMP into Tyco International, transforming it into Tyco Electronics—a division of a sprawling conglomerate that would soon become synonymous with corporate excess and fraud.

The Kozlowski Era & Tyco Scandal

To understand TE Connectivity today, one must understand the scandal that forced its creation as an independent company. The Tyco story is one of the most spectacular corporate frauds in American history—mentioned in the same breath as Enron and WorldCom.

Leo Dennis Kozlowski (born November 16, 1946) is a former CEO of Tyco International, convicted in 2005 of crimes related to his receipt of $81 million in unauthorized bonuses, the purchase of art for $14.725 million and the payment by Tyco of a $20 million investment banking fee to Frank Walsh, a former Tyco director. He served more than six and a half years in New York state prisons, and was released in 2014.

The company consistently beat Wall Street's expectations and through a series of strategic mergers and acquisitions, ushered in a new era of mega-conglomerates. Kozlowski left Tyco in 2002, amid a controversy in regard to his compensation package. Kozlowski was tried twice.

The stolen funds financed one of the most outlandishly extravagant executive lifestyles in corporate history. Dennis Kozlowski wasn't just a CEO—he was a man who lived life king-sized, with Tyco's funds footing the bill. His excesses became the stuff of legend: A $6,000 gold-threaded shower curtain for his Manhattan apartment. A $2 million Sardinian birthday party for his wife, complete with ice sculptures and celebrity performances.

From 1997 to 2002, Kozlowski took an aggregate of approximately $270 million dollars from Tyco's Key Employee Corporate Loan Program. He used the remaining $242 million of supposed KELP loans for personal expenses, including yachts, fine art, estate jewelry, luxury apartments and vacation estates, personal business ventures and investments, all unrelated to Tyco.

The pleas came hours after Manhattan District Attorney Robert Morgenthau announced the indictments, charging Kozlowski and Swartz with stealing $170 million in company loans and other funds, as well as obtaining more than $430 million through fraudulent sales of securities.

Both were convicted on 22 counts of grand larceny, falsifying business records, securities fraud and conspiracy. His aggregate minimum sentence was set at 8 years and 4 months, and his aggregate maximum sentence was 25 years.

A class action lawsuit followed the Tyco International scandal criminal trial with a verdict handed down by Federal District Court Judge Paul Barbadoro in May of 2007. Tyco consented to pay out $2.92 billion to a class of the cheated shareholders. Their corporate auditors Pricewaterhouse Coopers also agreed to pay $225 million in damages to the injured investors.

Why This Matters for TE's Story

The Tyco scandal created the conditions for TE Connectivity's emergence as an independent company. With Kozlowski gone and billions in settlements to pay, Tyco was forced to restructure fundamentally.

As a precautionary act, however, Edward Breen, who replaced Kozlowski, removed nine members of Tyco's original board. In July 2002, Edward D. Breen was appointed president, CEO, and chairman of Tyco for an initial three-year term. Breen had previously been president and COO of Motorola, and brought a reputation for operational discipline that Tyco desperately needed.

Between 2002 and 2006, Tyco had to take numerous writeoffs in value of acquired businesses that had been improperly valued on the balance sheet. In 2004, it started a review of what its core businesses should be, leading to the 2007 spinoffs.

The Tyco scandal thus represents the dark prelude to TE's independence. Without Kozlowski's fraud, AMP might have remained buried within a conglomerate indefinitely. Instead, the scandal forced a reckoning that ultimately liberated what would become one of the most successful industrial spinoffs in history.

V. The 2007 Spinoff: Independence Day

The Three-Way Split

The Board of Directors of Tyco International Ltd. formally approved the spin-offs of its healthcare and electronics businesses through a tax-free dividend distribution to Tyco International shareholders. The distributions were made on June 29, 2007 to shareholders of record on June 18, 2007. "We are very pleased to reach this important milestone in the separation of Tyco International into three independent, publicly traded companies," said Tyco Chairman and Chief Executive Officer Edward Breen. "We are now in the final stages of completing this complex transaction which will provide these businesses with the focus and flexibility to achieve their long-term growth potential."

The separation was completed in July 2007, when Tyco separated into three publicly independent companies: Covidien Ltd. (formerly Tyco Healthcare), Tyco Electronics Ltd. (now TE Connectivity), and Tyco International Ltd.

On June 29, 2007, Tyco split into three publicly held companies—Covidien (formerly Tyco Healthcare Group), Tyco Electronics, and the new Tyco International (formerly Tyco Fire & Security and Tyco Engineered Products & Services). And now, Covidien and Tyco Electronics are classified as discontinued operations. Tyco International, the last company standing, had a continuing revenue base of about $19 billion in 2007. Its 2006 revenue base was $41 billion, so the breakup cut the company in half.

At the time of spinoff, Tyco Electronics declared: "We look forward to operating as an independent company—serving our customers and growing our business in ways that make the most sense for Tyco Electronics and its shareholders. We are a $12.8 billion global provider of electronic components, network solutions and wireless systems, backed by more than 60 years of innovation, excellence and experience."

The Liberation Premium

The thesis behind the spinoff—that focused companies outperform conglomerates—proved dramatically correct. Freed from the Tyco umbrella and the ongoing scandal baggage, Tyco Electronics (later TE Connectivity) was able to focus entirely on connectivity and sensors.

The performance differential has been striking. While the original Tyco remnant and Covidien followed different paths (Covidien was ultimately acquired by Medtronic in 2015), TE Connectivity has compounded shareholder value at rates far exceeding the broader market. Since the 2009 market lows, TE has outperformed substantially—vindication for the strategic logic of focus.

On June 29, 2007, Tyco International Ltd. entered into a Separation and Distribution Agreement with Covidien Ltd. and Tyco Electronics Ltd. to effect the spin-offs of Covidien and Tyco Electronics and provide a framework for Tyco's relationship with those companies after the spin-offs. These agreements govern the relationships among Covidien, Tyco Electronics and Tyco subsequent to the completion of the spin-offs and provide for the allocation among Covidien, Tyco Electronics and Tyco of Tyco's assets, liabilities and obligations attributable to periods prior to the spin-offs.

The spinoff structure allocated legacy liabilities proportionally among the three companies—Tyco assumed 27%, Covidien assumed 42% and Tyco Electronics assumed 31% of certain of Historical Tyco's contingent and other corporate liabilities, which include securities litigation, certain legacy tax contingencies and any actions with respect to the spin-offs or the distributions made or brought by any third party.

For investors, the 2007 spinoff illustrates a recurring theme in corporate history: conglomerate discount versus focus premium. AMP's integration into Tyco had obscured its value within a scandal-plagued holding company. Independence allowed the market to value the business on its own merits, and the subsequent share price appreciation reflected both improved operational performance and rerating.

VI. The Rebrand & Strategic Transformation (2011-2015)

Becoming TE Connectivity

On March 10, 2011, Tyco Electronics Ltd. officially rebranded as TE Connectivity, reflecting its identity as a connectivity and sensor component manufacturer. The name change was more than cosmetic—it represented a deliberate break with the Tyco legacy and a statement about strategic direction.

The company ultimately ended up dropping Tyco from its name in 2011 to better represent its market position. "TE Connectivity" captured what the company actually did—enable connections—while shedding the association with corporate scandal.

This period also saw the emergence of leadership that would shape the company's current trajectory. A 14-year veteran of the company, Terrence Curtin was most recently President of the company's Industrial Solutions segment which includes TE's Aerospace, Defense, Oil and Gas business; Energy business; and Industrial and Medical businesses. In fiscal year 2014, the Industrial Solutions segment reported sales of $3.3 billion, grew operating income 12 percent and made strategic acquisitions that increased the company's leadership in harsh environment applications.

Mr. Terrence R. Curtin was Chief Executive Officer and Director of TE Connectivity Ltd. since March 8, 2017. Prior to assuming the role of Chief Executive Officer of the Company in March 2017, Mr. Curtin served as TE's President, where he was responsible for all of the company's connectivity and sensor businesses, as well as mergers acquisition activities.

Strategic Acquisitions

Following independence and rebranding, TE Connectivity pursued strategic growth through targeted acquisitions—a marked contrast to the conglomerate-era approach of acquiring anything available.

In April 2012, TE purchased Deutsch Group SAS for 1.55 billion euros (approximately $2.06 billion), strengthening its offerings in high-performance connectors for aerospace and harsh-environment applications. This acquisition deepened TE's position in exactly the kind of demanding applications where its technology excels.

In 2014, it acquired Measurement Specialties, Inc. for about $1.7 billion, significantly expanding its sensor portfolio and positioning it as a leader in high-growth sensor technologies for industrial and medical uses. The sensor acquisition reflected strategic recognition that connectors and sensors increasingly work together in modern systems.

ERNI Group AG (Acquired by TE Connectivity, 2021): Ranked 46th in 2020 with sales of $175 million, ERNI's acquisition expanded TE's reach in industrial applications.

Portfolio Optimization: The CommScope Sale

The transformation also involved strategic divestitures. On August 28, 2015, TE Connectivity completed the sale of its broadband-networks business to CommScope Holding Co. for about $3 billion. This was TE's largest disclosed sale, removing a non-core business and sharpening focus on transportation and industrial connectivity.

The pattern of acquisitions and divestitures reveals a disciplined approach: strengthen positions in harsh-environment connectivity and sensors; exit businesses that don't fit the core value proposition. This stands in stark contrast to the conglomerate era's "buy everything" mentality.

For investors evaluating TE today, the 2011-2015 transformation period established the strategic template that continues to guide capital allocation. Management has demonstrated willingness to both acquire at scale (Deutsch, Measurement Specialties) and divest significant businesses (broadband networks) in service of strategic coherence.

VII. The EV Revolution: TE's Next Act (2015-Present)

Positioning for Electrification

The electrification of transportation represents the most significant structural shift in TE Connectivity's core automotive market since the company's founding. Traditional internal combustion vehicles typically require a certain level of electrical content—connectors for engine management, lighting, infotainment. Electric vehicles require dramatically more.

TE Connectivity leads with high-voltage connectors and SDV platform solutions, supported by acquisitions, R&D investments, localization efforts, and recyclable material use.

TE Connectivity has been leading the electrification charge since the beginning. The company works with virtually every automotive OEM and tier-one supplier around the world to build high-voltage connectivity solutions that serve as the electrical foundation for safe and reliable zero-emission vehicles.

The EV Content Advantage

The content-per-vehicle opportunity in EVs versus traditional vehicles is substantial. Where a conventional car might have a few hundred dollars of electrical content, an electric vehicle can have multiples of that figure—high-voltage battery connections, charging infrastructure interfaces, power distribution for electric motors, and the extensive sensor arrays needed for driver assistance and autonomous features.

To meet increasing demands for compact packaging and reduced vehicle weight, TE introduced the PicoMQS connector system, designed with a 1.27 mm pin pitch, supporting up to 4 A at 80°C, and qualified for automotive vibration standards. In 2024, the company extended the PicoMQS portfolio with additional variants such as receptacles and headers, targeting applications in zonal architectures and compact electronic modules.

In March 2024, TE Connectivity launched AMP+ high-voltage connectors for compact BMS setups in cylindrical and prismatic cells, offering enhanced creepage, clearance, and EMI shielding. These connectors featured improved creepage and clearance characteristics along with integrated shielding to minimize EMI, ensuring robust signal and power transmission in high-vibration environments.

Product Innovation

TE showcased products including AMP+ ACI 800 adaptive charging inlets. The company now offers a plug-in-ready, safe and reliable family of charging inlets that transfers up to 1,000 amperes at 1,000 volts DC, achieving ultra-high-power "Boost" charging speeds. These newest inlets are fully serviceable, easy to install, and offer modular, connectorized AC and DC flexibility.

With the ACI 800 Adaptive Charging Inlet, EV drivers benefit from faster charging times, enhanced convenience, improved efficiency, and support for larger battery packs that deliver greater range.

Market Position in EV Connectors

The EV connector market is projected to reach USD 8.80 billion by 2032, from USD 2.73 billion in 2025, with a CAGR of 18.2%.

The leading players in the EV connector market are TE Connectivity (Ireland), Aptiv (Ireland), Yazaki Corporation (Japan), Molex (US), and Hirose Electric Co., Ltd. (Japan), among others, who are shifting toward miniaturization and advancements in EMI shielding connectors.

TE Connectivity Ltd., Tesla, and Aptiv PLC held a significant market share of over 21% in 2023. TE Connectivity leads in developing high-performance connectors with advanced safety features for electric vehicles.

For investors, the EV transition represents both opportunity and risk. The opportunity: dramatically higher content per vehicle as fleets electrify. The risk: any slowdown in EV adoption directly impacts a business now substantially exposed to this secular trend. TE's diversification across automotive, industrial, and communications provides some buffer, but the automotive exposure—approximately 60% of revenue—makes EV penetration rates a critical variable for the company's growth trajectory.

VIII. Recent Strategic Moves (2024-2025)

The Ireland Redomiciliation

On September 30, 2024, TE Connectivity plc (NYSE: TEL) completed the change in the place of incorporation of the publicly traded parent company of TE Connectivity from Switzerland to Ireland.

TE Connectivity has changed its place of incorporation from Switzerland to Ireland, effective September 30, 2024. TE Connectivity's stock (TEL) continues to trade on the New York Stock Exchange (NYSE) without any changes to the ticker symbol.

If approved, TE expected to implement the change in 2024. TE Connectivity does not anticipate any material change in its operations or financial results as a result of the change of domicile. The company will continue to be registered with the U.S. Securities and Exchange Commission (SEC) and will be subject to the same SEC reporting requirements.

Ireland has tax advantages for technology companies and hosts Apple and Intel. "After careful consideration, our board of directors has determined that this change is in the best long-term interest of the company and our shareholders and will help position TE for continued success," said Chief Executive Officer Terrence Curtin.

The Richards Manufacturing Acquisition

On February 12, 2025, TE Connectivity plc (NYSE: TEL), a world leader in connectors and sensors, entered into a definitive agreement to acquire Richards Manufacturing Co. from funds managed by Oaktree Capital Management, L.P. and members of the Bier family, long-standing owners and leaders of the business.

TE Connectivity acquired Richards Manufacturing on February 12, 2025 for $2.3 billion.

The transaction will strengthen TE's position in serving electrical utilities in North America by combining complementary product portfolios and adding the expertise of the Richards team, enabling TE to benefit from strong growth trends in underground electrical networks. Richards is widely recognized as a best-in-class provider of utility grid products and, over the last several years, has experienced double-digit revenue growth. The company, headquartered in Irvington, N.J., is a leader in underground distribution equipment, with differentiated positions in both medium voltage cold-shrink cable accessories and network protector products.

On April 1, 2025, TE Connectivity plc completed the previously announced acquisition of Richards Manufacturing Co. Richards is a North American leader in utility grid products, including underground distribution equipment. The acquisition will enable TE to capitalize on the region's grid replacement and upgrade cycle, strengthening its leadership in serving utilities and other energy customers around the world.

"One of the key pillars of our strategy is investing in long-term secular growth trends that further our commitments to being a trusted partner to customers around the world and creating value for our owners," said TE Connectivity CEO Terrence Curtin. "We have been strategically investing in our Energy business over the past several years to be a growth driver for TE. We've benefited from our focus on utility scale renewables and grid reliability by providing our customers with innovative products required for the ongoing evolution of the energy grid. The acquisition of Richards Manufacturing aligns with our strategy and positions us to further capitalize on an accelerating grid replacement and upgrade cycle in North America, driven by aging infrastructure, the increased hardening of the network and the upgrades that are required to support the increase in energy demand.

Overall M&A Track Record

TE Connectivity has made a total of 27 acquisitions spanning 8 countries, including 18 in the United States, 3 in Germany, and others in the United Kingdom and elsewhere. These acquisitions span 9 sectors, including Sensors (7), Cardiac and Vascular Disorders (3), and Micro Electro Mechanical Systems (2). The years 2021, 2019 and 2014 saw the most acquisitions, with 4 each.

The Richards acquisition represents TE's largest to date, signaling strategic intent to expand into the energy infrastructure market at a moment when grid modernization and renewable energy integration are creating substantial demand for specialized connectivity products.

IX. Current Business Model & Financials

Business Segments

The Company's businesses in the former Communications Solutions segment have been moved into the Industrial Solutions segment. Also, the appliances and industrial equipment businesses have been combined to form the automation and connected living business. In addition, the Company realigned certain product lines and businesses from the Industrial Solutions and former Communications Solutions segments to the Transportation segment.

Beginning in fiscal 2025, the company will have two reportable segments – Transportation Solutions and Industrial Solutions – resulting from a reorganization announced in the fourth quarter of fiscal 2024.

Transportation Solutions represents the company's largest segment, generating approximately $8.2 billion in FY2024 with 2% year-over-year growth. This segment includes automotive connectors, sensors, and electronic components for electric vehicles, traditional automotive applications, and commercial transportation.

Industrial Solutions encompasses energy, aerospace, defense, marine, medical, and factory automation applications. Industrial segment sales increased 24% during the year, driven by innovations that serve AI and energy customers as demand continues to accelerate.

Recent Financial Performance

Fourth Quarter FY2024 Highlights: Net sales were above guidance at $4.1 billion, up 1% on a reported basis year over year and 2% organically. GAAP diluted earnings per share (EPS) from continuing operations were $0.90, down 49% year over year, including a one-time tax-related impact of $0.78. Adjusted EPS exceeded guidance at an all-time record $1.95, up 10% year over year. Operating margins were 16.0% and adjusted operating margins were a fourth quarter record at 18.6%, driven by strong operational performance.

Cash flow from operating activities was approximately $1 billion and free cash flow was $833 million, with $952 million returned to shareholders, continuing the company's strong cash generation and disciplined deployment model.

"Our team finished the fiscal year strong, delivering quarterly sales that were above guidance and a record $1.95 adjusted EPS," said TE Connectivity CEO Terrence Curtin. "For the full year, we set records in key areas including EPS, cash generation and operating margins, delivering on our commitment to expand margins in a dynamic market environment."

For fiscal 2025, the momentum continued. Fourth Quarter FY2025: Net sales were a record $4.75 billion, an increase of 17% on a reported basis year over year and 11% organically, driven by growth in both the Industrial and Transportation segments.

GAAP diluted earnings per share (EPS) from continuing operations was $2.23, up 148% year over year. Adjusted EPS was a record $2.44, an increase of 25% year over year. Orders increased in both Segments to $4.7 billion, up 22% year over year and 5% sequentially. GAAP Operating margin was 19% and adjusted operating margin was 20%, driven by strong operational performance across both segments. Cash flow from operating activities was $1.4 billion and free cash flow was a record at $1.2 billion, with nearly $650 million returned to shareholders.

"Our teams executed at a high level against our business model to deliver strong results for the fourth quarter as well as the full year," said CEO Terrence Curtin. "Our performance resulted in records on the top line, earnings and cash flow in 2025 and sets TE up well going into our new fiscal year. These results against an uneven macro environment demonstrate the strategic positioning of our portfolio and the investments we've made to broaden the business to benefit from long-term growth trends."

Product Portfolio

The company's products include automotive connectors, industrial sensors, fiber optic solutions, circuit protection devices, and aerospace interconnect systems. Notable products include the AMPSEAL automotive connector series, industrial pressure and temperature sensors, and fiber optic connectivity solutions.

TE Connectivity's product portfolio is focused on connectors and sensors made to withstand harsh environments—extreme temperatures, vibration, moisture, and electromagnetic interference. This focus on demanding applications creates both technical barriers to entry and pricing power.

Capital Allocation

"We will continue to capitalize on our operational strengths and innovations in long-term growth trends such as electrification and data connectivity in transportation, renewable energy and AI. In a reinforcement of our long-term value creation model, I'm pleased that our board authorized a $2.5 billion increase in our share repurchase program that will continue to benefit our owners."

The company's capital allocation priorities are clear: invest in organic growth through R&D and capacity, pursue strategic acquisitions that deepen competitive position in attractive markets, return excess capital to shareholders through dividends and buybacks.

X. Competitive Landscape & Strategic Analysis

Direct Competition

TE Connectivity's top 14 competitors are Yazaki, Aptiv, Sumitomo, Sensata, Honeywell, Molex, Amphenol, Hubbell, Belden, 3M, Esterline, Phoenix Contact, Leviton and Tyco. TE Connectivity's top 3 competitors are Yazaki, Aptiv, Sumitomo.

TE Connectivity operates in highly competitive markets with both large multinational corporations and specialized niche players. In the automotive connectivity segment, primary competitors include Aptiv (APTV), Molex (owned by Koch Industries), and Yazaki Corporation. The company competes on product innovation, manufacturing scale, and global reach, with particular strength in harsh environment applications and electric vehicle components. In industrial markets, TE Connectivity faces competition from Amphenol Corporation (APH), Phoenix Contact, and Weidmüller. The company differentiates through its broad sensor portfolio and integrated connectivity solutions for industrial automation applications. In communications infrastructure, competitors include CommScope (COMM), Corning (GLW), and Huber+Suhner, with TE Connectivity maintaining strong positions in data center connectivity and fiber optic solutions.

The top four connector manufacturers are all US-based companies: TE Connectivity (1), Amphenol (2), Molex (3), and Aptiv (4). TE Connectivity has remained the largest connector company since 1980. The name changed from AMP to Tyco International to Tyco Electronics and to its current name, TE Connectivity. Molex and Amphenol have remained in the top 10 throughout the 38-year time frame.

TE Connectivity has grown its market share from 13.2% in 2000 to 14.8% in 2024. Amphenol Corporation's aggressive acquisition strategy propelled it from 6th place in 2000 to 2nd in 2024, with projections suggesting it may become the leading connector company by 2025.

Porter's Five Forces Analysis

Threat of New Entrants: LOW The connector and sensor industry presents significant barriers to entry. Product qualification cycles in automotive and aerospace can take years. Customers require proven reliability records across millions of connection cycles. The capital investment for precision manufacturing at scale is substantial. And the installed base of engineering relationships and technical specifications creates switching costs that protect incumbents.

Supplier Power: MODERATE TE uses commodity metals (copper, gold for plating, specialty alloys) and engineered plastics. These materials are generally available from multiple sources, limiting supplier leverage. However, during supply chain disruptions (as seen in 2020-2022), materials constraints can impact production.

Buyer Power: MODERATE TO HIGH TE's largest customers—major automotive OEMs like Toyota, Volkswagen, GM, and Ford—are sophisticated negotiators who can pressure suppliers on pricing. However, the switching costs from designed-in components and the risk of reliability problems from changing suppliers provide some countervailing power. The fragmented nature of the customer base (no customer likely exceeds 10% of revenue) also limits buyer concentration effects.

Threat of Substitutes: LOW Electrical connections are fundamental to electronic systems. While connection technologies evolve (from soldered to crimped to surface-mount), the basic function—reliable transmission of power, data, and signals—has no substitute. Integration of connectors into more complex subassemblies could shift value capture, but TE has moved into integrated solutions to capture this value.

Competitive Rivalry: HIGH The connector industry features several capable global competitors. Price competition is intense in commodity segments. However, TE's focus on harsh-environment applications—where reliability is paramount and failure costs are high—positions it in segments where price is less determinative than performance.

Hamilton Helmer's 7 Powers Framework

Scale Economies: TE benefits from substantial scale advantages in manufacturing. Precision connector production involves significant fixed costs for tooling, quality systems, and process engineering. Higher volumes spread these costs, enabling competitive pricing while maintaining margins.

Network Effects: Limited direct network effects, though TE's position as a standards-setting industry leader creates indirect benefits. When TE develops a connector standard that becomes widely adopted (like AMPSEAL in automotive), the installed base creates switching costs for the industry.

Counter-Positioning: TE's commitment to focus and operational excellence represents a form of counter-positioning versus conglomerates. Competitors who might attempt to replicate TE's strategy would face the challenge of maintaining focus versus the temptation to diversify—exactly the trap that damaged AMP under Tyco ownership.

Switching Costs: Once a connector is designed into a vehicle or industrial system, changing suppliers requires requalification—a process that can take 12-24 months and involves substantial engineering expense and risk. For long-cycle products like aircraft (25-year programs), the initial design win creates decades of recurring revenue.

Branding: TE has invested in the "EVERY CONNECTION COUNTS" positioning, but connector branding is ultimately less about consumer perception than engineering reputation. OEMs specify connectors based on technical performance, reliability data, and relationship trust—a form of industrial "branding" that TE has cultivated over decades.

Cornered Resource: TE's 8,000+ engineers represent a significant human capital moat. Deep expertise in connector physics, materials science, and application engineering is difficult to replicate quickly.

Process Power: TE's continuous improvement in manufacturing—achieving record operating margins even in challenging macro environments—demonstrates process power. The ability to produce precision components at high volumes with consistent quality represents institutional knowledge that competitors cannot easily copy.

Key Performance Indicators for Investors

For tracking TE Connectivity's ongoing performance, three metrics deserve particular attention:

1. Automotive Content per Vehicle Growth Rate The most important secular driver for TE's largest business segment is the expansion of electrical content as vehicles electrify and add autonomous features. Monitoring TE's content growth versus vehicle production growth reveals whether the company is capturing the EV transition opportunity. A widening gap between TE automotive revenue growth and global vehicle production growth indicates successful content expansion.

2. Adjusted Operating Margin by Segment TE has demonstrated consistent margin expansion—achieving record adjusted operating margins of 20% in FY2025. Continued margin expansion validates the operational model and pricing power. Margin compression could signal competitive pressure or mix shift toward lower-value products.

3. Orders Growth versus Revenue Growth The relationship between orders and revenue provides insight into near-term trajectory. Orders growing faster than revenue (book-to-bill above 1.0) suggests acceleration; orders lagging revenue suggests potential deceleration. Orders increased in both Segments to $4.7 billion, up 22% year over year and 5% sequentially—a positive signal for near-term momentum.

XI. Bull Case & Bear Case

The Bull Case

AI-Driven Data Center Demand Creates a Second Growth Engine

In August 2025, TE Connectivity reported third-quarter adjusted earnings of US$2.27 per share and revenue of US$4.5 billion, both beating estimates, and projected continued sales and earnings growth, especially in its Industrial Solutions segment. The company's results highlighted the significant impact of strong demand for AI-driven data center connectivity and modern infrastructure, positioning it to benefit from ongoing secular trends in digitalization and electrification.

The most relevant recent announcement is TE Connectivity's Q3 2025 earnings, where management underscored robust revenue growth, particularly a 30% year-over-year sales surge in Industrial Solutions driven by AI and data center demand.

The AI thesis for TE is straightforward: AI training and inference require massive computing infrastructure, and that infrastructure requires connectors—high-speed data connections between GPUs, power delivery to increasingly energy-hungry processors, and cooling system interfaces.

TE's I/O products have built-in heat-sink capability to transfer thermal energy away from these modules and keep things operating cooler, improving the system's overall efficiency and reliability. The demand for more speed and bandwidth to support increasingly sophisticated AI applications at the data center level is essentially insatiable.

Electric Vehicle Transition Provides Multi-Decade Growth Runway

The EV transition remains in early innings globally. As EV penetration grows from approximately 15% of global new vehicle sales toward eventual dominance, TE's content-per-vehicle advantage compounds. Each percentage point of EV penetration growth increases TE's addressable market.

Portfolio Optionality and Management Excellence

CEO Terrence Curtin has demonstrated disciplined capital allocation—acquiring strategically (Richards Manufacturing for energy infrastructure), divesting non-core businesses, and returning capital to shareholders. The consistent margin expansion and record financial performance validate the operational model.

Strong Competitive Position with High Switching Costs

TE's position as the largest global connector company, combined with the switching costs inherent in designed-in components, creates a defensive moat that supports sustained profitability.

The Bear Case

Automotive Concentration Risk

With approximately 60% of revenue from automotive markets, TE is heavily exposed to vehicle production cycles. Any significant slowdown in global vehicle production—whether from recession, trade wars, or unexpected shifts in EV adoption—would disproportionately impact TE.

EV Transition Timing Uncertainty

While the long-term EV transition seems inevitable, the timing and pace remain uncertain. Slower-than-expected EV adoption, infrastructure challenges, or policy reversals could delay TE's content growth opportunity. The company's investments in EV-specific capacity and capabilities carry execution risk if the transition stalls.

Competitive Pressure from Amphenol

Amphenol Corporation's aggressive acquisition strategy propelled it from 6th place in 2000 to 2nd in 2024, with projections suggesting it may become the leading connector company by 2025.

Amphenol has closed the gap with TE through aggressive M&A and may overtake TE as the industry leader. Increased competition could pressure margins and market share.

AI Demand Sustainability

The current surge in AI infrastructure spending reflects aggressive investment by hyperscale cloud providers and enterprises. If AI returns disappoint or investment cycles normalize, the high growth rates in TE's Industrial segment could moderate significantly.

Geopolitical and Supply Chain Risks

TE operates in approximately 130 countries with complex supply chains. Trade tensions, particularly between the US and China, create risks for a company with substantial Asian manufacturing and customer exposure.

Myth versus Reality

MYTH: TE is a boring, slow-growth industrial company. REALITY: TE has delivered 17% sales growth and record earnings by positioning for secular trends in electrification and AI. The "boring" label obscures a business model capturing structural growth in multiple end markets.

MYTH: Connectors are commodities with limited differentiation. REALITY: In harsh-environment applications—automotive, aerospace, industrial automation—connectors must meet demanding specifications for temperature, vibration, moisture, and electromagnetic interference. TE's engineering expertise and reliability track record create meaningful differentiation.

MYTH: The Tyco legacy creates ongoing risk. REALITY: TE has thoroughly separated from the Tyco scandal through rebranding, redomiciliation, and nearly two decades of independent operation under different leadership. The Tyco connection is historical rather than operational.

XII. Conclusion: Every Connection Counts

The story of TE Connectivity spans the arc of modern industrial history—from a cramped office above a New Jersey restaurant in 1941 to a $66 billion global technology leader today. Along the way, the company has survived world war, navigated corporate scandal, emerged triumphant from a conglomerate breakup, and positioned itself at the center of the two most important technology transitions of our era: vehicle electrification and artificial intelligence.

The company Uncas Whitaker founded to make better electrical connections for aircraft has evolved into something far larger, yet remains fundamentally focused on the same core proposition: reliable connectivity in demanding environments.

For investors, TE Connectivity presents a case study in how "invisible infrastructure" businesses can compound value over long periods. The connectors in your car, the sensors in your phone, the data connections in the servers powering AI—none of these attract consumer attention or generate headlines, yet they represent essential components that create substantial economic value.

The risks are real: automotive concentration, EV transition timing, competitive pressure from Amphenol, and cyclical exposure to industrial production. But the opportunity is equally substantial: structural growth from electrification, AI infrastructure buildout, grid modernization, and the general increase in electronic content across virtually every category of equipment.

"Our Transportation segment performed well in a challenging end market, delivering content growth from increased data connectivity and growth of the electrified power train. We are well positioned to keep capitalizing on these and other key long-term growth trends."

Every connection counts. After eighty years, that simple proposition—making connections that work, even in the most demanding circumstances—has built one of the world's most essential industrial technology companies. The next eighty years will determine whether TE Connectivity can maintain its position as the hidden giant connecting our increasingly electronic world.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube