WillScot Holdings: The Modular Empire Nobody Talks About

I. Introduction & Episode Roadmap

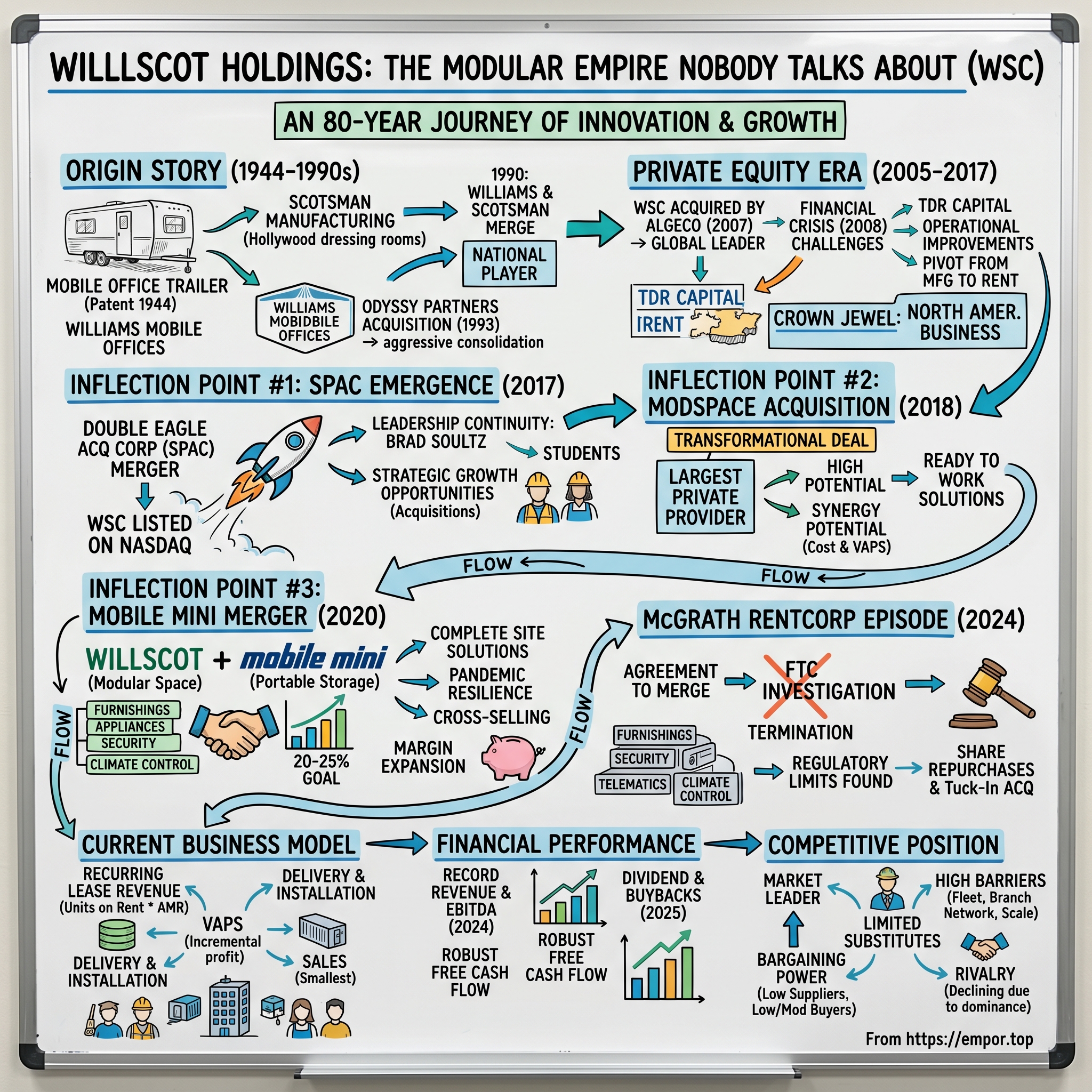

Picture this: It's 1944, and somewhere in Baltimore, a company called Williams Mobile Offices files a patent for something seemingly mundane—the mobile office. A trailer on wheels, designed to follow construction crews from site to site. Nobody could have predicted that eight decades later, that humble innovation would spawn a $6 billion enterprise that has quietly become the dominant force in North America's flexible space market.

What if I told you there's a company that invented the mobile office in 1944, survived multiple private equity owners, emerged through a SPAC in 2017 before SPACs became a Silicon Valley obsession, and has since grown its enterprise value roughly fivefold—all while remaining virtually unknown to the average investor? That company is WillScot Holdings Corporation, and its story reveals more about the mechanics of value creation in "boring" industries than a hundred high-flying tech IPOs ever could.

"From 1944, when our predecessor company Williams Mobile Offices created and patented the first mobile office, to the more than 135 million square feet of turnkey space solutions we offer today, we have continuously innovated," CEO Brad Soultz declared during the company's 2024 rebranding announcement. That statement encapsulates something remarkable: an 80-year journey from construction trailers to a sophisticated business services platform.

Today, WillScot combines all of its constituent brands under a unified WillScot brand, leaning into both its 80-year legacy as the pioneer of modular and mobile space solutions and its modern-day industry leadership.

The business model is deceptively simple. WillScot's comprehensive range of products includes modular office complexes, mobile offices, classrooms, temporary restrooms, portable storage containers, protective buildings and climate-controlled units, and clearspan structures, as well as a curated selection of furnishings, appliances, and other supplementary services, ensuring turnkey solutions for its customers. Headquartered in Phoenix, Arizona, and operating from a network of approximately 260 branch locations and additional drop lots across the United States, Canada, and Mexico, WillScot's business services are essential for diverse customer segments spanning all sectors of the economy.

This article will trace WillScot's improbable journey: from its Baltimore origins and the Odyssey Partners acquisition that turbocharged national expansion, through the private equity wilderness under European ownership, to the SPAC emergence that freed North American operations, the transformational ModSpace and Mobile Mini mergers, the heartbreaking McGrath RentCorp deal that regulators killed, and finally to the VAPS revolution that has turned a capital-intensive rental business into a margin expansion machine.

Understanding WillScot matters because it represents a masterclass in consolidation strategy, pricing discipline, and the art of extracting more revenue from existing assets. This is not a growth-at-all-costs story. It's a story about operational excellence in a fragmented industry—and the compounding power of doing simple things extraordinarily well.

II. The Origin Story: Inventing an Industry (1944–1990s)

The modular space industry didn't emerge from a moment of entrepreneurial brilliance in a garage. It grew organically from a simple observation: construction projects need office space, but that space doesn't need to be permanent. Williams Mobile Offices, founded in 1944, originally sold construction trailers small enough to be towed by a car.

These weren't architectural marvels—they were functional boxes designed to survive being dragged across muddy job sites. But they solved a real problem. Before mobile offices, project managers worked out of makeshift shelters or drove off-site to handle paperwork. The mobile office brought administration to the construction zone.

Later, the company began to sell and lease mobile double-wide office structures. During the 1960s, the company expanded outside the Baltimore area for the first time with branch locations in Atlanta and Chicago. Leasing its signature, two-tone green mobile structures, Williams developed business operations along the East Coast and into the Midwest.

Meanwhile, on the West Coast, a parallel evolution was taking place. Scotsman Manufacturing, founded in 1945, manufactured recreational vehicles for rental companies. The company began to lease mobile office structures in 1965, as manufacturers started offering larger structures with amenities, such as toilets and showers. Scotsman leased these structures to movie studios for dressing rooms.

This Hollywood connection is fascinating. The entertainment industry's need for on-location facilities created demand for increasingly sophisticated temporary structures. What worked for movie sets could work for construction sites, schools during renovations, healthcare facilities expanding capacity, and corporate offices needing flexibility.

At the time of the merger between Williams and Scotsman Manufacturing, Williams was the second largest supplier of mobile offices in the United States, with 15,000 rental units leased through 17 offices in 13 Eastern states. Scotsman operated 11 offices in four Western states with a fleet of 7,500 rental units. The merger was recorded as an acquisition of Williams Mobile Offices from the Williams Family Trust by the Trijka Family Trust, which owned Scotsman Manufacturing.

Williams Scotsman formed in 1990, through the merger of Williams Mobile Offices/Modular Structures and Scotsman Manufacturing Co. From Baltimore, Maryland, and Gardena, California, respectively, the two companies combined their geographically disparate operations for the purpose of developing a national company.

The combined entity represented something new: a truly national player in a historically local business. Mobile offices had always been a regional affair—the cost of transporting heavy units meant you needed to be close to your customers. By combining East Coast and West Coast operations, Williams Scotsman suddenly had the beginnings of coast-to-coast coverage.

Odyssey Partners, a private investment group, acquired Williams Scotsman for $234 million in 1993. The new owners, having the financial capability to develop Williams Scotsman rapidly on a national level, acquired 19 mobile office leasing companies between 1994 and 1997, adding 23,000 units to the fleet.

This is where the consolidation playbook first emerged. Odyssey Partners recognized that scale mattered enormously in this business. A larger fleet meant better utilization. More branch locations meant faster delivery. National coverage meant the ability to serve multi-location customers. And purchasing power meant better economics on everything from steel to financing.

In 1996 Williams Scotsman entered the market for storage products for onsite use, including vans, trailers, and ground level containers. Some customers used the containers for temporary storage during a building or renovation project; Wal-Mart and Kmart used the storage units to hold extra merchandise inventory during the Christmas season.

This diversification into storage containers foreshadowed the Mobile Mini merger that would come decades later. The logic was straightforward: if you're already delivering a mobile office to a construction site, why not deliver a storage container too? The customer relationship, the delivery infrastructure, and the local branch network could serve both products.

By the end of 1997 Williams Scotsman generated $235 million in revenues through 73 branch offices in 38 states, leasing a fleet of 48,000 mobile offices; the company served more than 12,500 customers in 450 different industries.

Becoming a publicly traded company in 1997 provided access to the capital needed for strategic acquisitions and market expansion. The IPO wasn't just about liquidity for existing shareholders—it was about ammunition for the acquisition engine that would define the next two decades.

For investors today, the origin story reveals something crucial about WillScot's DNA: this has always been a rollup story. From the 1990 merger through the Odyssey era's aggressive acquisitions, the company's leaders understood that consolidation in a fragmented local industry creates value. That insight would be tested, refined, and ultimately vindicated through the tumultuous years ahead.

III. The Private Equity & Global Conglomerate Era (2005–2017)

The years between 2005 and 2017 represent WillScot's wilderness period—a decade when the company was subsumed into a global conglomerate, lost its independence, and yet somehow emerged stronger for the experience. It's a story that illuminates both the promise and the peril of private equity ownership.

Williams Scotsman was founded in 1955 and went public in 2005, then was acquired by Paris-based Algeco two years later.

The Algeco acquisition was transformational. Williams Scotsman agreed to be acquired by the parent company of Algeco, the European space rental company, in an all-cash transaction for $2.2 billion, which includes the refinancing of outstanding debt. Under the terms of the transaction, Williams Scotsman shareholders received $28.25 per share in cash, which represents a premium of approximately 21% to Williams Scotsman's closing price.

London-based TDR Capital acquired Algeco from TUI AG in September 2004. TDR, a London-based private equity firm with deep experience in business services, saw an opportunity to create a global modular space champion.

The transaction established the combined company as the leading global provider of modular space solutions and a top-five global player in the rental services market through the combination of Williams Scotsman's North American modular solutions business and Algeco's space rental businesses in Europe. Upon completion of the acquisition, the combined company operated in 16 countries, and employed over 4,600 employees.

Williams Scotsman combined with Algeco, creating Algeco Scotsman and operating globally in 25 countries.

On paper, this looked like empire-building. Algeco Scotsman became one of the largest modular space companies on the planet. Algeco Scotsman is the leading global business services provider focused on modular space, secure portable storage solutions, and remote workforce accommodation management. Headquartered in Baltimore, Algeco Scotsman has operations in 24 countries with a modular fleet of approximately 201,000 units and 11,400 remote accommodations rooms.

But there was a problem. The European business, with its fragmented markets, diverse regulations, and different customer dynamics, operated very differently from the North American franchise. The synergies that looked compelling in PowerPoint presentations proved elusive in practice.

More critically, the combined company carried significant debt from the acquisition, and the 2008 financial crisis hit commercial construction hard. Non-residential construction starts—the lifeblood of the modular space business—collapsed along with the broader economy.

TDR Capital deserves credit for navigating these challenges. Rather than strip-mining the company for short-term returns, they invested in operational improvements and positioned the business for long-term value creation. Manjit Dale, Founding Partner of TDR Capital, commented, "We are delighted to be partnering with DEAC on this important transaction for Williams Scotsman. This transaction highlights TDR's continued strong commitment to Williams Scotsman and we look forward to embarking on this new phase of growth for the business alongside a new set of public shareholders."

The strategic pivot during this era cannot be overstated. The company shifted from manufacturing modular buildings to renting them—a fundamental transformation in the business model. Manufacturing is capital-intensive with lumpy revenues tied to construction cycles. Renting generates recurring revenue with long asset lives and predictable cash flows.

By 2017, it became clear that the North American business was the crown jewel. The U.S. market was larger, more consolidated, and offered better unit economics than the fragmented European operations. Separating the two would allow focused management and dedicated capital allocation for each region.

The Williams Scotsman division had proven remarkably resilient. Even as the parent company navigated complex global operations and significant leverage, the North American team continued to execute—improving utilization, expanding value-added services, and preparing for what would become a transformational decade.

IV. Inflection Point #1: The SPAC Emergence (2017)

The year 2017 marked a turning point—not just for WillScot, but for the SPAC market itself. Before SPACs became synonymous with speculative excess and celebrity-backed ventures, they served a legitimate purpose: providing private companies with an efficient path to public markets. WillScot's transaction with Double Eagle Acquisition Corp. stands as one of the SPAC era's genuine successes.

Double Eagle, now WillScot, was created by entertainment veterans Jeff Sagansky and Harry Sloan. Sagansky is a former president of CBS Entertainment and Sloan is a former CEO of MGM.

The pairing seemed unlikely. What would Hollywood executives know about mobile offices? But Sagansky and Sloan weren't looking for media deals exclusively—they were looking for good businesses at reasonable valuations that could benefit from public market access. Double Eagle Acquisition went public in September 2015 and acquired WillScot Corp. in November 2017, with shares gaining 296% from the $10 offer price.

Veteran Hollywood executives Jeff Sagansky and Harry Sloan launched Double Eagle Acquisition Corp. with a $500 million initial public offering. It was the third such acquisition vehicle that the duo had developed since 2011, following Global Eagle Acquisition and Silver Eagle Acquisition.

Double Eagle was created by Jeff Sagansky and Harry Sloan, who raised $500 million in an initial public offering for the company to acquire another company. Last October, it was in talks to acquire Playboy Enterprises, according to The Hollywood Reporter, but that deal apparently fell through.

The Playboy deal collapse proved fortuitous. Instead of acquiring a struggling consumer brand, Double Eagle found Williams Scotsman—a market-leading business services company with recurring revenues, high customer retention, and clear consolidation opportunities.

Williams Scotsman, a specialty rental services company providing modular space and portable storage solutions across North America, returned to the public markets with a well-capitalized balance sheet and enhanced financial flexibility to consolidate its market-leading position and support its future growth strategy. Double Eagle Acquisition Corp. acquired Williams Scotsman from Algeco Scotsman for a total pre-money enterprise value of US$1.1 billion, implying an acquisition multiple of 7.9x its projected 2018 adjusted EBITDA before transaction expenses.

Williams Scotsman International Inc. and Double Eagle Acquisition Corp., a NASDAQ-listed special purpose acquisition company, announced that they completed the previously announced stock purchase agreement. Under the agreement, Double Eagle Acquisition Corp. changed its name to WillScot Corporation and purchased all of the outstanding shares of WSII for an aggregate purchase price of $1.1 billion. Beginning November 30, 2017, the Class A common stock and public warrants of WillScot Corporation traded on the NASDAQ stock exchange under the ticker symbols "WSC" and "WSCWW," respectively.

The deal structure reflected the complexity of unwinding Williams Scotsman from its European parent. Under the deal, Double Eagle paid Algeco $1.02 billion, to be used largely to pay down debt, and gave a 30 percent equity stake in Williams Scotsman valued at $79 million to TDR Capital LLP, a London-based private equity firm that was Algeco's controlling shareholder.

Williams Scotsman essentially became publicly traded again through Double Eagle's stock. Brad Soultz, Williams Scotsman's president and CEO, continued to lead the company, which remained in Baltimore, and former CEO Gerry Holthaus returned as chairman.

Leadership continuity mattered enormously. Brad Soultz serves as CEO of WillScot and was the President and CEO of WillScot before the merger with Mobile Mini. Prior to becoming WillScot's President and CEO in November of 2017, he served as President and CEO of Williams Scotsman International Inc. beginning in January 2014, where he was responsible for the strategic and operational aspects of the North American business and played a key role in preparing the company for its reemergence as a public company. Before joining WSII, Mr. Soultz served as the Chief Commercial and Strategy Officer of Novelis Inc. and held various leadership roles at both Novelis and Cummins Inc.

Soultz's background in industrial companies—not financial engineering—signaled that this would be an operationally focused story. His experience at Cummins, a paragon of operational excellence in manufacturing, and Novelis, a global aluminum rolling company, prepared him for the asset-intensive nature of the modular space business.

Brad Soultz commented, "We are very excited for the return of Williams Scotsman to the public markets. Our capital structure provides us ample flexibility to continue to fund and drive forward our business objectives. As a public company, Williams Scotsman is well positioned to capitalize on additional strategic growth opportunities and will be better positioned to serve our customers and stakeholders."

The phrase "strategic growth opportunities" was code for acquisitions—and the company wasted no time proving it meant business. Williams Scotsman announced it would acquire Acton Mobile from Prophet Equity for a cash purchase price of $235 million just weeks after the SPAC transaction closed.

The message was clear: WillScot intended to be a consolidator, and the SPAC transaction was merely the first step in a much larger plan.

V. Inflection Point #2: The ModSpace Acquisition (2018)

If the SPAC transaction was WillScot's declaration of independence, the ModSpace acquisition was its coming-out party as a consolidator. Less than a year after going public, the company announced the largest deal in the modular space industry's history.

WillScot Corporation announced that it entered into a definitive agreement to acquire Modular Space Holdings, Inc., the parent holding company of Modular Space Corporation (d/b/a "ModSpace"), for an enterprise value of approximately $1.1 billion. Total enterprise value represented 6.6x ModSpace's Adjusted EBITDA for the twelve month period ended March 31, 2018, inclusive of forecast cost synergies and the expected value of acquired tax attributes.

Williams Scotsman acquired MS Holdings for a purchase price comprising $1,063,750,000 of cash consideration, 6,458,500 shares of WSC Class A common stock and warrants to purchase 10,000,000 shares of WSC Class A common stock at an exercise price of $15.50 per share, subject to customary adjustments.

ModSpace was no small player. ModSpace, based in Berwyn, Pa., was the largest privately held provider of office trailers, portable storage units and modular buildings for temporary or permanent space needs in North America. ModSpace reported $453 million of total revenue, $18 million of net income, and $106 million of adjusted EBITDA for the 12 months ended March 31.

With the addition of ModSpace, Williams Scotsman now manages over 160,000 modular space and portable storage units serving an even broader customer base from over 120 locations across the United States, Canada and Mexico. The acquisition also expands the breadth and depth of its Ready to Work solutions to existing and incremental customers and markets.

"ModSpace is highly complementary to our business which, when combined with Williams Scotsman, provides our shareholders with a transformational value creation opportunity," Brad Soultz declared.

The synergy thesis was compelling. Williams Scotsman expected to capture $60 million in annual cost synergies after integration, with approximately 80% of the forecast synergies expected to be realized on a full run-rate basis by the end of 2019. Williams Scotsman also expected to benefit from the net operating tax loss carryforwards to be acquired in the transaction, and for the transaction to be accretive to earnings in 2019.

At its core, ModSpace was an outstanding business perfectly complementary to Williams Scotsman in almost every respect. The companies share common passion for customers. They have the same compelling unit economics and recurring revenue characterized by long lease durations coupled with long asset lives. They also share a common geographic footprint with significant branch overlap.

The overlap was the key. When two rental companies have branches in the same markets, consolidation creates powerful economics. You can close redundant locations, combine delivery fleets, centralize back-office functions, and leverage purchasing power—all while retaining customers who now have access to a larger, more capable provider.

Williams Scotsman had driven sustained growth of VAPS over the last five years with cumulative average annual growth rates of 23% on its modular space units. The ModSpace Acquisition provided the opportunity to expand the recurring revenue from value-added products on new contracts relative to the averages across the acquired portfolio. ModSpace's modular space units had average monthly VAPS rates of approximately $86 as of March 31, 2018. This compared to average monthly VAPS rates on delivered units in Williams Scotsman's Modular US segment over the twelve months ended March 31, 2018 of $226 per modular space unit.

This disparity—$86 versus $226 in VAPS per unit—represented a massive revenue opportunity. If WillScot could bring ModSpace's customer base up to its own VAPS penetration levels, the revenue uplift would be substantial. And crucially, this revenue came with minimal incremental capital requirements—the units were already on rent, after all.

WillScot completed its acquisition of Modular Space Holdings, Inc. for a total purchase price of approximately $1.2 billion. The deal closed in August 2018, just nine months after WillScot emerged from the Double Eagle transaction.

Brad Soultz commented, "We are pleased to confirm the completion of this transformational acquisition and would like to thank our collective customers, employees, and stakeholders for their support." Soultz continued, "We are excited to welcome the talented and experienced ModSpace employees to our fast growing company. Together we become an even stronger company and partner for our customers. In sum, we believe the value created through the inherent synergies, coupled with the multi-year revenue opportunity associated with the expansion of our Ready to Work solutions, will benefit our shareholders for years to come."

The ModSpace acquisition established the integration playbook that would guide future M&A. The company demonstrated it could identify targets, finance transactions, execute integrations, and deliver synergies on schedule. This track record would prove invaluable when an even larger opportunity emerged.

VI. Inflection Point #3: The Mobile Mini Merger (2020)

If ModSpace was transformational, the Mobile Mini merger was industry-defining. The combination created an entity so dominant that, years later, regulators would block WillScot's attempt to acquire its next-largest competitor.

Mobile Mini (originally Mobile Mini Storage Systems) was founded in 1983 by Richard Bunger and was started by selling storage containers to construction companies and manufacturers. By 1986, the company expanded into markets outside Phoenix, Arizona but in the Southwest region.

Richard Bunger's origin story is quintessentially American. The man behind the creation of Mobile Mini was Richard E. Bunger, who started out as a designer for dairy and rodeo feed lot units. Because his initial endeavor was uncertain from year to year, he became involved in the mini-storage business. However, he soon discovered problems with this new industry as well. As he explained in a 1999 interview, "The problem with mini-storage is, as soon as you build on a prime location, pretty soon three competitors move in and dilute your business." In 1982, Bunger conceived of a way to offset this limitation: instead of having the customer come to him for storage, he would take a transportable storage solution to the customer.

He refined this concept after learning from friends involved in the seagoing shipping industry that they had an abundance of old shipping containers and no particular use for them. Bunger launched Mobile Mini Storage Systems in Phoenix in 1983 and began buying up excess shipping containers and modifying them.

Mobile Mini grew into a formidable business. Mobile Mini, Inc. is an American portable storage company founded in 1983 and based in Phoenix, Arizona. The company manufactures, leases, sells, and transports welded steel mobile storage containers, converted into storage units, guard shacks, and offices. The lengths of the units are 5 to 45 feet long and can be customized with up to 100 different configuration options. Mobile Mini's lease fleet totals approximately 235,000 portable storage and office units. The company has 177 locations throughout the United States of America, Canada, and the United Kingdom.

The strategic logic of combining WillScot and Mobile Mini was elegant. WillScot dominated modular space—mobile offices, classrooms, modular complexes. Mobile Mini dominated portable storage—steel containers for job sites, retail inventory, and commercial storage. Together, they could offer complete site solutions: offices, storage, and everything in between.

Mobile Mini stockholders received 2.4050 shares of WillScot common stock for each share of Mobile Mini common stock held in an all-stock merger of equals transaction. Based on the closing price of WillScot's Class A common stock on February 28, 2020, the consideration implied a premium of 8% to the closing price of Mobile Mini common stock on the same day.

The implied total enterprise value of the combined company was approximately $6.6 billion. Upon completion, current WillScot stockholders owned 54% and Mobile Mini stockholders owned 46% of the combined company.

The timing seemed terrible. The merger was announced in March 2020, just as COVID-19 was beginning its march across America. Construction sites shut down. Commercial activity ground to a halt. Investors fled to safety.

But the deal closed anyway. WillScot Corporation and Mobile Mini, Inc. announced the successful completion of the previously announced merger pursuant to which WillScot, a leading specialty rental services provider of innovative modular space and portable storage solutions across North America, combined with Mobile Mini, a leading provider of portable storage solutions serving customers in the U.S., U.K., and Canada. The combined company is named WillScot Mobile Mini Holdings Corp. and its common stock traded, beginning July 2, 2020, on Nasdaq under the ticker symbol "WSC."

WillScot Mobile Mini Holdings is a North American leader in modular space and portable storage solutions. It was formed in 2020 upon the merger of leaders in the modular space and portable storage markets. Together the WillScot and Mobile Mini brands operate approximately 375 locations across the United States, Canada, Mexico, and the United Kingdom with a combined fleet of over 350,000 portable offices and storage containers.

"The fact that we consummated this transaction and have continued to deliver outstanding operating results, while prioritizing the welfare of our employees and customers during an unprecedented pandemic, is truly a testament to the grit of our organizations and the resilience of our combined businesses. We are entering the next chapter of our transformation with a stronger team, more diversified assets and end markets, a solid and rapidly de-leveraging balance sheet, robust free cash flow, and multiple compelling revenue and earnings growth levers that are within our control."

The pandemic, paradoxically, highlighted the strength of WillScot's business model. When companies needed to add space quickly—for testing sites, vaccination centers, emergency facilities—modular solutions offered the fastest path. When supply chains required additional storage, portable containers appeared on loading docks across America.

The cross-selling opportunity proved real. A customer renting a mobile office for a construction project might also need storage containers. A retailer using Mobile Mini containers for seasonal inventory might need temporary office space during store renovations. The combined company could serve both needs from a single relationship.

VII. The VAPS Revolution: From Asset Rental to Solutions Provider

If WillScot's acquisition strategy created scale, its VAPS strategy transformed the economics. VAPS—Value-Added Products and Services—represents one of the most elegant business model evolutions in recent industrial history.

The concept is simple: when you rent a customer a mobile office, you can also rent them furniture, appliances, HVAC systems, security systems, telematics, and climate controls. Each additional item generates incremental revenue with minimal incremental capital—the office is already being delivered, after all.

The VAPS portfolio continued to play an increasingly critical role, representing over 17% of revenue in Q1 FY2025. Value-added offerings include furnishings, appliances, security solutions, telematics, and climate controls.

WillScot's long-term growth trajectory is supported by its VAPS strategy, which has delivered a 26% CAGR from 2012-2024 and is projected to continue growing at a 10-20% CAGR from 2024-2029.

The company is targeting VAPS to comprise 20-25% of total revenue in the next 3-5 years.

Value-Added Products and Services (VAPS) represented over 17% of revenue in the quarter, with accounts receivable reduction of $30 million in the quarter. Value-added products and services represented over 17% of revenue in the quarter, moving towards a long-term goal of 20% to 25% of total revenue.

The genius lies in the margin profile. While renting a mobile office requires significant capital investment—the unit itself, delivery equipment, maintenance facilities—renting furniture or appliances requires far less. The assets are smaller, lighter, and less expensive. The incremental logistics cost is negligible when you're already delivering the office. Yet customers willingly pay meaningful monthly fees for the convenience.

Consider the math: If a customer rents a mobile office for $500/month, and you can add $100/month in VAPS (furniture, HVAC, security), you've increased revenue per unit by 20% without meaningful incremental capital. That additional $100/month flows largely to profit.

The company's unit economics remain compelling, with portable storage containers generating IRRs of over 30% over their 30-year useful lives, and modular space units delivering approximately 25% IRR over 20+ years. WillScot's lease duration strategy helps mitigate revenue volatility through economic cycles. The company's average lease duration of approximately 3 years, combined with end-market diversification, has enabled lease revenue to outpace both GDP and non-residential construction starts.

The VAPS evolution hasn't been accidental. It reflects sustained investment in product development, sales training, and customer insight. Brad Soultz noted, "Our evolution accelerated when our Company re-entered the public markets in 2017. Since then, we embarked on a series of technology transformations, successfully consolidating our ERP system in 2021, harmonizing our CRM system in 2023, and implementing field optimization tools in 2024."

For investors, the VAPS trajectory offers a powerful lever for margin expansion even in periods when unit growth is challenged. The company has demonstrated that pricing plus VAPS can offset volume headwinds—exactly what occurred throughout 2024 and into 2025, when construction markets softened but revenue per unit continued climbing.

VIII. Technology Transformation & Operational Excellence

Behind WillScot's financial performance lies a less visible but equally important story: the systematic professionalization of a traditionally fragmented industry. Mobile offices and storage containers may seem low-tech, but managing hundreds of thousands of units across hundreds of locations requires sophisticated systems.

"From 1944, when our predecessor company Williams Mobile Offices created and patented the first mobile office, to the more than 135 million square feet of turnkey space solutions we offer today, we have continuously innovated and invested to improve customer experiences and generate value for our stakeholders. Our evolution accelerated when our Company re-entered the public markets in 2017. Since then, we embarked on a series of technology transformations, successfully consolidating our ERP system in 2021, harmonizing our CRM system in 2023, and implementing field optimization tools in 2024. Most recently, we aligned our branch network with a unified go-to-market strategy."

The technology investments served multiple purposes. A unified ERP system enables real-time visibility into fleet utilization, maintenance requirements, and financial performance across the entire organization. A harmonized CRM system allows cross-selling between legacy WillScot and Mobile Mini customers and ensures consistent customer experiences regardless of location.

WillScot announced it is combining all of its constituent brands – including Mobile Mini – under a unified WillScot brand. In conjunction with the rebranding announcement, the WillScot parent company also changed its name from "WillScot Mobile Mini Holdings, Corp." to "WillScot Holdings Corporation."

The company was formerly known as WillScot Mobile Mini Holdings Corp. and changed its name to WillScot Holdings Corporation in July 2024.

The brand consolidation was more than cosmetic. Operating under a single brand simplifies marketing, reduces confusion among customers, and enables a unified go-to-market strategy. It also signals that the Mobile Mini integration is complete—the combined company is now simply WillScot.

The logistics advantage deserves attention. Unlike many rental businesses that outsource delivery, WillScot operates its own fleet. This provides several benefits: faster response times, better quality control, and the ability to optimize routes across the entire branch network.

WillScot's comprehensive range of products includes modular office complexes, mobile offices, classrooms, temporary restrooms, portable storage containers, protective buildings and climate-controlled units, and clearspan structures, as well as a curated selection of furnishings, appliances, and other supplementary services, ensuring turnkey solutions for its customers. Headquartered in Phoenix, Arizona, and operating from a network of approximately 260 branch locations and additional drop lots across North America, WillScot's business services are essential for diverse customer segments spanning all sectors of the economy.

The phrase "turnkey solutions" captures the company's strategic direction. Rather than simply renting boxes, WillScot aims to provide complete workspace solutions—delivered, installed, furnished, and supported. This shift from asset rental to solutions provision justifies higher prices and deepens customer relationships.

IX. The McGrath RentCorp Episode: Ambition Meets Regulation (2024)

Every successful acquisition strategy eventually encounters regulatory limits. For WillScot, that limit arrived in the form of the Federal Trade Commission's investigation of the proposed McGrath RentCorp merger.

WillScot announced that it entered into an agreement with McGrath RentCorp to terminate the companies' previously announced merger, pursuant to the terms of the January 28, 2024 merger agreement, under which WillScot would have acquired McGrath for a mix of cash and stock consideration.

The deal would have been significant. McGrath RentCorp, a Livermore, California-based company with substantial modular and portable storage operations, represented the next logical consolidation target.

On February 22, 2024, McGrath announced that both it and WillScot had received second requests for additional information from the FTC in connection with the agency's review of the proposed acquisition.

A "second request" is FTC parlance for a deep dive—the agency believed the transaction warranted extended scrutiny. For WillScot, this meant months of document production, depositions, and economic analysis.

Although both companies continue to believe in the merits and procompetitive benefits of the combination, WillScot and McGrath mutually agreed to terminate the transaction based on a joint determination that there was no commercially reasonable path to clear the necessary regulatory requirements for the transaction. Despite extensive and exhaustive engagement with the U.S. Federal Trade Commission over several months, in recent weeks, it became evident that the path to regulatory clearance would be excessively onerous.

"Strong competition in the markets for modular and portable storage solutions is essential to ensuring low prices and high levels of product quality and customer service for businesses and school districts nationwide. The FTC is pleased that WillScot has announced that it is terminating its proposed deal to acquire McGrath RentCorp in the face of a potential Commission challenge. FTC staff worked tirelessly to investigate the potential impacts of the proposed acquisition."

The FTC's statement reveals how regulators view WillScot's market position. The agency was concerned about competition "for businesses and school districts nationwide"—suggesting that in certain markets or customer segments, the combined company would have had excessive pricing power.

"With the obvious overhang on our valuation related to the McGrath transaction, our Board of Directors increased our share repurchase authorization to $1 billion. We will deploy the repurchase authorization thoughtfully, as we have in the past, while funding organic investments in our business and pursuing smart tuck-in acquisitions," said Tim Boswell, President and Chief Financial Officer. "At current valuation levels, we will prioritize investing in our own stock given the embedded growth in our earnings."

"While we are disappointed with this process, we are confident in our strategy and there are numerous opportunities to continue reinvesting in our business to deliver sustainable growth and returns over time," said Brad Soultz. "WillScot's position as the leading provider of temporary space solutions has never been stronger."

The McGrath episode carries important implications for investors. On one hand, it demonstrates that WillScot's consolidation runway may be shorter than bulls hoped—regulators are clearly watching. On the other hand, the company's pivot to share repurchases suggests management believes the stock is undervalued, and the focus on "tuck-in acquisitions" indicates smaller deals remain viable.

Perhaps most importantly, the FTC's objection validates WillScot's market position. Regulators don't typically block mergers involving undifferentiated commodity providers. The very fact that the FTC intervened suggests WillScot has achieved a level of dominance worth protecting through competition policy.

X. Current Business Model Deep Dive

Understanding WillScot's economics requires examining how money flows through the business. The company operates what appears to be a simple rental model but has evolved into something considerably more sophisticated.

"We achieved record revenues of $2,396 million and Adjusted EBITDA of $1,063 million in 2024."

The revenue mix tells the story. WillScot generated revenue of $603 million in Q4 2024, with gross profit margin percentage of 55.8%, income from continuing operations of $89 million and diluted earnings per share of $0.48. Increased average monthly rates, inclusive of Value-Added Products ("VAPS"), offset much of the year-over-year impact from decreased units on rent. Delivered Adjusted EBITDA of $285 million, with Adjusted EBITDA Margin expanding sequentially to 47.3% and up 30 basis points year-over-year.

Leasing and services—the recurring revenue streams—dominate. Delivery and installation, while necessary, contribute less margin and depend on activity levels. Sales represent the smallest component and are inherently episodic.

Portable storage containers generate IRRs of over 30% over their 30-year useful lives, and modular space units deliver approximately 25% IRR over 20+ years. The company's average lease duration of approximately 3 years, combined with end-market diversification, has enabled lease revenue to outpace both GDP and non-residential construction starts.

These unit economics deserve attention. A 30% IRR over 30 years on storage containers means the company can earn back its initial investment multiple times over the asset's life. The long useful lives create an embedded value that doesn't appear on GAAP balance sheets at full market value—units are depreciated over time even as they continue generating revenue.

The customer base is deliberately diversified. The company highlighted that no single customer represents more than 2% of revenue, providing significant diversification. This reduces concentration risk and ensures that no single contract loss can materially impact results.

End markets span construction, education, healthcare, retail, government, energy, and commercial sectors. This diversification means WillScot isn't wholly dependent on construction cycles—when one sector weakens, others may strengthen. Education, for instance, tends to follow different patterns than commercial construction.

XI. Financial Performance & Capital Allocation

WillScot's financial performance since the 2017 SPAC transaction demonstrates the power of disciplined execution in a consolidating industry.

"We achieved record revenues of $2,396 million and Adjusted EBITDA of $1,063 million in 2024."

Adjusted EBITDA Margin expanded sequentially to 47.3% and up 30 basis points year-over-year.

The company's free cash flow generation remained strong, with Adjusted Free Cash Flow Margin at 22% in Q3 and 23% over the last twelve months. This cash flow strength supports WillScot's capital allocation strategy, including investments in the business and shareholder returns.

"At current valuation levels, we will prioritize investing in our own stock given the embedded growth in our earnings. As we progress into 2025, we will continue to execute the disciplined approach to capital allocation that we initiated in 2021, which has resulted in the return of over $2 billion of capital to our shareholders and nearly a 25% reduction in our economic share count."

On February 18, 2025, the Company broadened its capital allocation framework with the Board of Directors initiating a quarterly cash dividend program of $0.07 per share. The Board will regularly assess the cash dividend program with a long-term focus on increasing the dividend payment over time.

The dividend initiation marks a maturation point. Companies typically initiate dividends when management believes cash generation exceeds investment opportunities—or when they want to signal confidence in sustainable cash flows. For WillScot, the dividend complements rather than replaces buybacks and acquisitions.

WillScot's long-term growth algorithm targets 5-10% organic lease revenue growth, combining modest volume increases (0-2%) with more substantial rate and VAPS contributions (5-10%). The company's ambitious three-to-five-year targets include reaching $3 billion in revenue, $1.5 billion in adjusted EBITDA, and $700-900 million in adjusted free cash flow.

The company is aiming for $3 billion in revenue, $1.5 billion in Adjusted EBITDA, and $700 million in Adjusted Free Cash Flow in the next 3-5 years. The company's Return on Invested Capital (ROIC) stood at 15.4% for the twelve months ended Q3 2025, within its target range of 15-20%.

Returned $270 million to shareholders by repurchasing 7.1 million shares of Common Stock, reducing outstanding share count by 3.4% over the twelve months ended December 31, 2024. FY 2025 Revenue and Adjusted EBITDA ranges of $2,275 million to $2,475 million and $1,000 million to $1,090 million, respectively, excluding the incremental contribution from any acquisitions.

The share count reduction warrants emphasis. A 25% reduction in economic share count since 2021 means existing shareholders own proportionally more of the business. Combined with EBITDA growth, this creates powerful per-share value accretion.

XII. Porter's Five Forces & Competitive Analysis

Understanding WillScot's competitive position requires systematic analysis of industry dynamics. The company operates in what might be called a "boring but beautiful" industry—one that generates exceptional returns precisely because it attracts little competition.

Threat of New Entrants: LOW

Building a fleet comparable to WillScot's 400,000+ units would require billions in capital. WillScot continues to maintain its position as the market leader in the approximately $20 billion North American flexible space solutions market.

The branch network presents perhaps the greater barrier. Operating from 260 locations nationwide took decades to build. Each branch requires real estate, equipment, personnel, and customer relationships. A new entrant starting from scratch would face years of losses before achieving meaningful scale.

Local delivery economics favor incumbents. Mobile offices are heavy and expensive to transport long distances. A company with branches every 35 miles can serve customers faster and more economically than one shipping from distant locations.

Bargaining Power of Suppliers: LOW TO MODERATE

WillScot sources modular buildings from manufacturers and acquires used shipping containers from leasing companies and shipping lines. Multiple suppliers exist for each category, preventing any single supplier from exercising pricing power.

The company's in-house refurbishment capabilities further reduce supplier dependence. Rather than purchasing new units, WillScot can acquire used containers and modular buildings, then recondition them to rental quality.

Bargaining Power of Buyers: LOW TO MODERATE

WillScot's customer base is fragmented across industries and geographies. No single customer represents more than 2% of revenue. This fragmentation prevents any single buyer from negotiating exceptional terms.

More importantly, customers often prioritize reliability over price. Construction projects operate on tight schedules—a delayed mobile office can cost far more in project delays than any rental savings. WillScot's national coverage and track record justify premium pricing.

Threat of Substitutes: LOW

The alternatives to modular space and portable storage are limited. Permanent construction is expensive and time-consuming—precisely the opposite of what customers need. Buying rather than renting ties up capital and creates disposal challenges when needs change.

Modular solutions are increasingly preferred for speed and flexibility. School districts expanding temporarily during renovations, healthcare systems adding capacity during emergencies, and construction companies needing job-site offices all face the same calculus: renting modular space is faster, cheaper, and more flexible than alternatives.

Industry Rivalry: MODERATE (Declining)

The McGrath RentCorp episode demonstrates that WillScot has achieved a level of dominance that limits further consolidation. The FTC's intervention suggests the company cannot acquire its nearest remaining competitors without regulatory challenge.

However, this same dynamic reduces competitive pressure. The remaining independent operators are too small to challenge WillScot on price or service quality across national markets. Regional players may compete in specific markets but cannot match WillScot's scale economics.

Hamilton Helmer's 7 Powers Analysis

WillScot exhibits several durable competitive advantages under Helmer's framework:

Scale Economies: The company's fleet and branch network create unit cost advantages that smaller competitors cannot match. Fixed costs—headquarters staff, technology systems, brand marketing—spread across a larger revenue base.

Network Effects: Limited but present. National customers value working with a single provider across multiple markets. A construction company operating in ten states prefers one relationship to ten.

Switching Costs: Moderate. While individual rentals can end, long-term customer relationships are sticky. Changing providers means learning new processes, establishing new contacts, and accepting delivery uncertainty.

Process Power: WillScot's integration playbook, VAPS penetration capabilities, and operational systems represent accumulated know-how that competitors cannot easily replicate.

XIII. Bull and Bear Case Assessment

The Bull Case

Continued VAPS Expansion: VAPS represents 17% of revenue today with a target of 20-25% over three to five years. If management executes, this drives meaningful margin expansion without proportional capital investment. The VAPS compounding story has years to run.

Pricing Power Persistence: The company has demonstrated the ability to raise prices through economic cycles. Average monthly rates continue climbing even as unit volumes fluctuate. This pricing power reflects market position and customer value perception.

Tuck-In Acquisition Runway: While large deals face regulatory scrutiny, smaller acquisitions remain viable. The company has announced tuck-in acquisitions in climate-controlled storage and other adjacencies, suggesting organic consolidation continues.

Share Repurchase Accretion: A 25% reduction in share count since 2021 demonstrates commitment to per-share value creation. If the company continues buying back shares at current valuations while EBITDA grows, per-share metrics compound attractively.

Defensive Characteristics: The business has demonstrated resilience through COVID-19 and construction cycle downturns. Long lease durations, diversified customers, and sticky relationships provide stability that many industrial businesses lack.

The Bear Case

Construction Cycle Exposure: Despite diversification, construction remains a significant end market. Extended weakness in non-residential construction starts would pressure volume growth and utilization rates.

Regulatory Constraints on M&A: The McGrath episode demonstrates that large acquisitions face regulatory headwinds. If the company cannot consolidate further, growth becomes dependent on organic initiatives that may prove slower than historical M&A-driven expansion.

Interest Rate Sensitivity: As a capital-intensive business with significant debt, WillScot's interest expense matters. Higher-for-longer interest rates reduce free cash flow available for buybacks and dividends.

Leverage Concerns: Net debt to EBITDA around 3.5x provides limited cushion for a cyclical business. A severe construction downturn could stress the balance sheet and constrain capital allocation flexibility.

Volume Headwinds Persist: WillScot reported total revenues of $567 million for Q3 2025, a 6% decrease year-over-year, while Adjusted EBITDA fell 9% to $243 million. Volume challenges have proven more persistent than management initially expected, and the path to unit growth remains uncertain.

XIV. Key Performance Indicators to Track

For investors monitoring WillScot, three KPIs warrant particular attention:

1. VAPS as Percentage of Total Revenue

This metric captures the transition from asset rental to solutions provision. Currently at 17%, management targets 20-25% over three to five years. Progress toward this target indicates successful execution of the higher-margin strategy. If VAPS stalls or declines, the margin expansion story weakens.

2. Average Monthly Rate (AMR) Growth (Inclusive of VAPS)

AMR measures revenue per unit and incorporates both base rental rates and VAPS contribution. Consistent mid-single-digit AMR growth demonstrates pricing power and VAPS penetration. This metric matters more than unit volume in the current environment—the company can grow revenue per unit even if total units on rent decline.

3. Adjusted Free Cash Flow Margin

This metric captures the business's cash generation efficiency—how much of each revenue dollar converts to discretionary cash flow after all necessary investments. Current margins around 22-23% support dividends, buybacks, and acquisitions. Sustained decline would signal deteriorating economics or increased capital requirements.

XV. Conclusion: The Compounding Machine Hidden in Plain Sight

WillScot Holdings represents something increasingly rare in public markets: a dominant market position in a stable, cash-generative industry with multiple levers for value creation. The company has transformed from a Baltimore-based mobile office pioneer into North America's leading flexible space solutions provider through disciplined execution of a consolidation playbook refined over decades.

The story isn't complicated. WillScot rents mobile offices and storage containers to customers who need temporary space. It has assembled the largest fleet, the broadest branch network, and the most comprehensive service offering in the industry. These advantages compound over time—each acquisition strengthens the network, each VAPS innovation enhances revenue per unit, each technology investment improves operational efficiency.

The McGrath episode revealed both the company's strength and its limitation. Regulators blocked the deal because WillScot has become too dominant to acquire major competitors—a backhanded compliment to the consolidation strategy's success. The company must now grow through organic initiatives and smaller acquisitions, a slower but potentially more sustainable path.

For long-term investors, WillScot offers exposure to a business model that has proven remarkably durable across economic cycles. The combination of recurring lease revenue, long asset lives, customer diversification, and pricing power creates a cash flow profile that can support dividends, buybacks, and reinvestment regardless of short-term construction market volatility.

The company nobody talks about has quietly become one of the most successful SPAC stories of its era—not through hype and speculation, but through the unglamorous work of consolidating a fragmented industry and extracting more value from existing assets. In a market obsessed with disruption, WillScot demonstrates that execution in "boring" industries can compound wealth just as effectively as the next revolutionary technology.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube