Walmart: The Empire of Everyday Low Prices

I. Cold Open & Episode Roadmap

Picture this: Every single second, Walmart rings up roughly $19,000 in sales. Every hour, 37 million people walk through its doors somewhere on Earth. Its parking lots alone cover an area larger than Tampa, Florida. With 2.1 million employees worldwide, if Walmart were a country, it would have the third-largest standing army on the planet—behind only China and India. Its annual revenue of $648 billion exceeds the GDP of Poland, Belgium, or Argentina.

Yet this behemoth started with a single five-and-dime store in Newport, Arkansas, run by a folksy Eagle Scout who drove a pickup truck until the day he died—despite being worth billions. The central question that drives our story today: How did Sam Walton, a small-town merchant from the Ozarks, build a retail empire that not only survived the rise of Amazon but learned to fight back?

This is a story of relentless operational excellence, of turning America's disdain for "big box" retail into grudging admiration for "everyday low prices." It's about how a company culturally engineered for rural Arkansas learned to operate in Shanghai, Mexico City, and Mumbai. Most surprisingly, it's about how a 62-year-old retailer became one of the most sophisticated technology companies in America, running the country's third-largest online marketplace behind only Amazon and eBay.

We'll trace Walmart's journey from Sam Walton's $5,000 investment in 1945 to today's retail colossus. We'll explore the operational innovations that allowed it to undercut every competitor, the international expansion that saw spectacular failures and surprising triumphs, and the digital transformation that has it growing faster than Amazon in North American e-commerce. Along the way, we'll unpack the key strategic decisions, the family dynamics that still shape the company, and what Walmart's evolution tells us about the future of retail itself.

The themes that emerge are unmistakable: the compounding power of scale economics, the delicate balance between standardization and localization, how operational excellence can become a sustainable moat, and why culture—not strategy—might be the ultimate differentiator in business. This is the Walmart story, from five-and-dime to Fortune One.

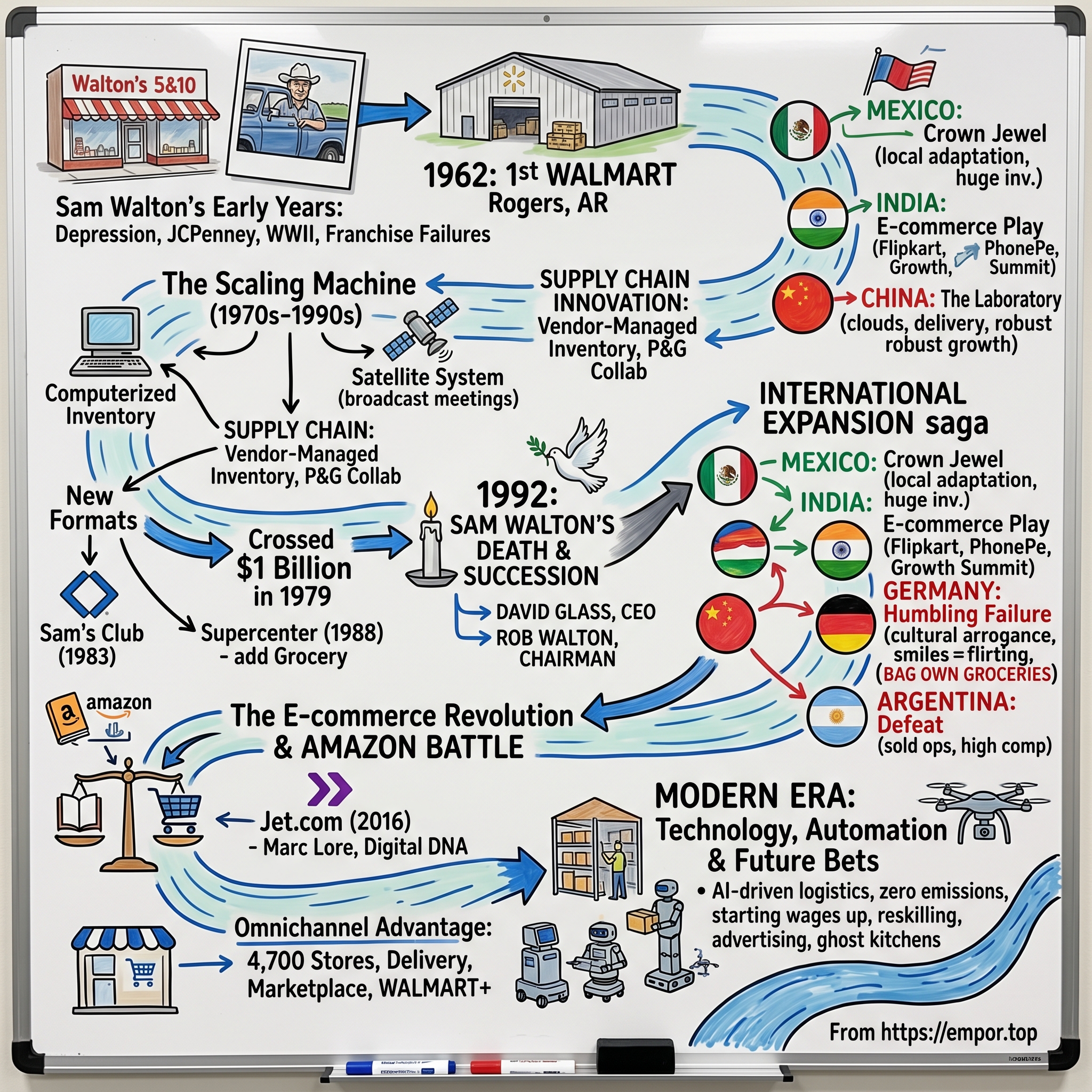

II. Sam Walton's Origin Story & Early Years

The Great Depression was grinding through its eighth year when Sam Walton graduated from David H. Hickman High School in Columbia, Missouri, in 1936. Born March 29, 1918, in Kingfisher, Oklahoma, young Sam had already shown the hustle that would define his life—milking cows, delivering newspapers, selling magazine subscriptions door-to-door. But it was his achievement in eighth grade that perhaps best foreshadowed his future: becoming the youngest Eagle Scout in Missouri's history, a feat requiring the kind of systematic goal-setting and execution that would later revolutionize retail.

At the University of Missouri, Walton waited tables in exchange for meals, continuing his relentless work ethic while studying economics. Upon graduation in 1940, he had two job offers: $75 per month at JCPenney or $85 at Sears. He chose Penney's—not for the money, but because he admired founder James Cash Penney's philosophy of treating associates as partners. His eighteen months as a management trainee in Des Moines would prove formative. Penney himself would occasionally visit, and Walton absorbed every lesson about customer service, merchandise presentation, and the critical importance of controlling expenses.

World War II interrupted his retail education. Walton joined the Army Intelligence Corps in 1942, serving as a communications officer supervising security at aircraft plants and prisoner-of-war camps. But even war couldn't slow his personal momentum—on Valentine's Day 1943, he married Helen Robson, daughter of a prosperous banker and rancher from Claremore, Oklahoma. Helen wasn't just bringing a dowry; she brought business acumen that would prove invaluable. "She's the one who had the confidence in me," Sam would later say. "She always told me I could do anything."

The war's end in 1945 found Captain Walton at a crossroads. His father-in-law, L.S. Robson, wanted him to join the family's banking and ranching businesses. But Sam had caught the retail bug. With $5,000 he'd saved from his Army pay and a $20,000 loan from his father-in-law (roughly $350,000 in today's dollars), he purchased a Ben Franklin variety store franchise in Newport, Arkansas—population 5,000. On September 1, 1945, at age 27, Sam Walton became a merchant.

The Newport store was a disaster waiting to be cleaned up. The previous owner had let it deteriorate; sales were just $72,000 annually. But Walton attacked the challenge with characteristic intensity. He'd drive to Memphis—two hours each way—to buy ladies' panties and children's clothes directly from manufacturers, cutting out the middleman. He'd study competitors obsessively, measuring their shelf heights, counting their checkout lanes, timing their service. Within a year, sales jumped 45%. By year three, his store led all Ben Franklin franchises in Arkansas in sales and profits.

Then came the gut punch that would redirect history. In 1950, Walton's landlord refused to renew his lease—he wanted the thriving store for his son. Walton had failed to secure a lease renewal option, a mistake he'd never repeat. Forced to sell, he loaded his family—now with four children—into the car and drove through the Ozarks looking for a new opportunity. They settled on Bentonville, Arkansas, population 3,000, where he opened Walton's 5&10 on the town square.

Here's where the Walton magic truly began to crystallize. While other variety store owners were content with the standard 25% markup, Walton experimented with something radical: lower margins, higher volumes. "If I could buy an item for 80 cents and sell it for $1, but I found I could sell three times as many if I priced it at 90 cents, the total profit was much better," he explained. This wasn't just arithmetic—it was philosophy.

By 1960, Walton owned fifteen Ben Franklin stores across Arkansas, Missouri, and Kansas, the largest independent variety store operation in the nation. Combined sales hit $1.4 million. He was successful by any measure—except his own. On a trip to Minnesota, he visited one of the new "discount stores" that were beginning to emerge. These weren't variety stores with their limited selection and small footprints. These were massive, 30,000-square-foot warehouses selling everything from clothing to sporting goods at prices 20% below department stores.

The numbers staggered him. A single discount store could generate $2 million in annual sales—more than his entire fifteen-store chain combined. Standing in that Minnesota store, watching customers load their carts with merchandise at prices he couldn't match with his current model, Sam Walton saw both extinction and opportunity. The variety store era was ending. But for someone willing to completely reimagine retail—starting with locations everyone else ignored—the discount store revolution was just beginning.

III. The Birth of Walmart: Small-Town Disruption (1962–1970)

On July 2, 1962, at age 44, Sam Walton stood in front of a 16,000-square-foot building on the outskirts of Rogers, Arkansas, watching customers stream through the doors of his new experiment: Wal-Mart Discount City. The hand-painted sign outside promised "We Sell for Less"—a boast that would have seemed laughable to his big-city competitors. That same year, mighty S.S. Kresge launched Kmart with a $80 million war chest, while Woolworth's unveiled Woolco backed by decades of retail dominance. Next to these giants, Walton's operation looked like a lemonade stand challenging Coca-Cola.

But Walton had spotted something his competitors missed—or dismissed. The retail establishment's dogma held that discount stores needed a population of at least 100,000 to succeed. Below that threshold, the economics supposedly didn't work: not enough traffic, not enough volume, not enough profit. Walton believed this "ironclad" rule was actually an opportunity in disguise. "Our strategy was to put good-sized discount stores into little one-horse towns that everyone else was ignoring," he later explained. In towns of 5,000 to 25,000 people, a Walmart wasn't competing against Kmart—it was competing against Main Street's tired variety stores and overpriced local merchants.

The first Walmart was deliberately primitive. Walton had cobbled together fixtures from wherever he could find them cheap—including old fixtures from his variety stores. The floor was concrete, the lights were bare fluorescent tubes, and merchandise was stacked on tables made from plywood and sawhorses. David Glass, who would later succeed Walton as CEO, remembered his first visit: "It was the worst retail store I had ever seen. Sam had brought a couple of trucks of watermelons and stacked them on the sidewalk. He also had donkey rides out in the parking lot. It was 115 degrees, and the watermelons began to pop. It was a mess."

Yet customers didn't care about aesthetics—they cared about prices. And Walton's prices were revolutionary for rural America. A shirt that cost $5 at the local department store sold for $3 at Walmart. The savings were even more dramatic on big-ticket items: bicycles, televisions, washing machines—goods that rural families often had to drive hours to city stores to purchase. Now they could buy them in their backyard at city prices or better.

The real innovation wasn't just low prices—it was the supply chain architecture that made those prices sustainable. While Kmart and other discounters built stores wherever opportunities arose, creating a scattered footprint, Walton expanded in concentric circles from Bentonville. He called it his "saturation strategy"—blanket a region with stores, build a distribution center in the middle, then move to the next region. No Walmart was more than a day's drive from a distribution center, dramatically reducing transportation costs and inventory requirements.

This hub-and-spoke model had another advantage: control. Walton could visit every store himself, often piloting his own plane from location to location. He'd walk the aisles, chat with associates, study the competition, then fly back to Bentonville to adjust strategy. While Kmart executives sat in Detroit boardrooms studying reports, Walton was on the ground, iterating in real-time.

By 1967, Walmart had expanded to 24 stores with $12.6 million in sales. But growth required capital, and Walton was stretched thin. Banks were skeptical—retail was considered high-risk, and Walmart's rural strategy seemed especially dubious. One banker told him bluntly: "You're overextended, Sam. You're going to go broke." The solution came from his brother Bud, who had joined the business: go public.

On October 1, 1970, Walmart offered 300,000 shares at $16.50 each, raising about $5 million. The timing was terrible—the market was in a slump, and retail stocks were particularly unloved. The IPO barely got done, with the underwriters having to buy unsold shares themselves. Fortune magazine wouldn't even mention Walmart for another three years. Wall Street's indifference would prove to be one of the great investing oversights in history.

The cash infusion transformed Walmart from a regional curiosity into a scaling machine. Walton immediately deployed the capital into new stores, new distribution centers, and something revolutionary for a discount retailer: technology. In 1969, he had already begun computerizing inventory management, years ahead of competitors. Now he could afford to accelerate, installing systems that tracked what was selling, what wasn't, and what needed reordering—in an era when most retailers still used paper and pencil.

As the 1960s ended, Kmart had 250 stores and seemed unstoppable. Gibson's Discount Centers had 200 stores. Woolco had dozens more. Next to them, Walmart's 32 stores looked almost quaint. But Walton understood something fundamental: in retail, the race doesn't always go to the swift or the strong. Sometimes it goes to the one who picks the right race to run. While his competitors fought bloody battles in big cities, Walton was building an empire in places they'd never bother to defend—because they'd never bothered to attack.

IV. The Scaling Machine: Building America's Retailer (1970s–1990)

The decade began with a milestone that even Sam Walton found hard to believe. In 1979, Walmart crossed $1 billion in annual sales—faster than any company in American history had reached that mark. The boy from Oklahoma had built something unprecedented: 276 stores, 21,000 associates, and a retail network stretching across the South and Midwest. Yet Walton, now 61, was just getting started. "Most people think we're at the end of our expansion," he told Forbes. "I think we're just beginning."

The 1980s would prove him spectacularly right. Walmart was opening stores at a velocity that stunned the retail industry—100 new locations per year, sometimes more. But this wasn't growth for growth's sake. Each store opening followed a methodical process that Walton had refined to near-perfection. Scout the location personally (often from his plane), negotiate the real estate deal himself, ensure the distribution center could service it efficiently, hire locals who understood the community, and then—critically—get out of the way and let them run it.

The technological edge that Walton had begun building now became a crushing advantage. In 1983, Walmart invested $24 million—a staggering sum for a retailer—in a satellite communications system. This wasn't just for data; Walton used it to broadcast his famous Saturday morning meetings from Bentonville to every store and distribution center. Managers would gather at 7 a.m. to hear Sam himself share sales figures, celebrate victories, and yes, lead them in the Walmart cheer. "Give me a W! Give me an A!" It was corny, it was cult-like, and it was devastatingly effective at maintaining culture across thousands of locations.

But the real revolution was happening in the back office. While competitors were still calling in orders to distributors, Walmart's computers were talking directly to Procter & Gamble's computers, automatically reordering Tide when supplies ran low. This "vendor-managed inventory" system was revolutionary—P&G could see Walmart's sales data in real-time and ship products before Walmart even asked. By cutting out layers of middlemen and buffer stock, both companies saved millions. Soon, other suppliers came knocking, wanting the same arrangement.

The numbers told the story: Walmart's cost of goods sold was running 2-3 percentage points lower than Kmart's, despite selling identical products. In retail, where net margins hover around 3%, this was like bringing a gun to a knife fight. Walmart could undercut everyone and still make money.

Then came the format innovations that would reshape American retail. In 1983, Walton opened the first Sam's Club in Midwest City, Oklahoma—a direct assault on Sol Price's Price Club warehouse concept. The idea was simple: charge customers a membership fee to shop in a no-frills warehouse where products were sold in bulk at near-wholesale prices. Small business owners loved it. So did large families. Within five years, Sam's Club had 100 locations and $6 billion in sales.

The Supercenter concept, launched in 1988 in Washington, Missouri, was even more audacious. Take a regular Walmart, add a full grocery store, a pharmacy, a photo center, an optical shop, a tire center—create a one-stop shop for literally everything a family needed. The first Supercenter was 185,000 square feet, larger than three football fields. Customers could drop off their film, get their eyes examined, buy a week's groceries, pick up a prescription, and grab new tires—all while their kids played in the McDonald's Walton had convinced to open inside the store.

Traditional supermarkets were terrified, and for good reason. Walmart didn't need to make money on groceries—it could use them as a loss leader to drive traffic for higher-margin general merchandise. Within a decade, Walmart would become America's largest grocer, a title it still holds today.

The cultural innovations were equally important. Walton's profit-sharing plan, started in 1971, had made thousands of hourly workers wealthy. Truck drivers who'd joined in the 1970s were retiring as millionaires. The company's stock had split nine times; that initial $16.50 IPO share was now worth $512 after adjusting for splits. Forbes crowned Sam Walton America's richest man in 1985, with a net worth of $2.8 billion. True to form, he still drove his red Ford pickup and flew economy class when he wasn't in his Cessna.

By 1987, a stunning reversal had occurred: Walmart surpassed Kmart in total revenue. The discounter that nobody took seriously was now America's third-largest retailer, trailing only Sears and Kmart. A year later, it became the most profitable. The combination of superior logistics, lower costs, better technology, and fanatical execution had created an unstoppable force.

The masterstroke of this era was how Walton handled succession. In February 1988, recognizing that the company needed professional management to reach the next level, he stepped down as CEO, naming David Glass as his successor while remaining chairman. Glass had been with Walmart since 1976, rising from executive vice president to president. He understood both Walton's vision and the operational excellence required to execute it at massive scale.

But even as he handed over daily operations, Walton couldn't stop innovating. He was fascinated by hypermarkets in Europe, studied warehouse clubs obsessively, and pushed for ever-lower prices. In 1990, he launched a new initiative: "Buy American." Walmart would actively seek out U.S. manufacturers, even paying slightly more to support domestic production. Critics called it a publicity stunt. Walton called it good business—keeping Americans employed meant keeping Walmart's customers employed.

By 1990, Walmart operated 1,573 stores with sales of $32.6 billion. It employed 328,000 people—more than General Motors, America's largest manufacturer. The transformation was complete: the five-and-dime operator from Arkansas had become the unstoppable force of American retail. And Sam Walton, now 72 and battling cancer, could see his life's work achieving something even he hadn't imagined: Walmart was about to become not just America's retailer, but America's largest company.

V. Sam Walton's Death & Leadership Transition

The diagnosis came in 1990: multiple myeloma, a cancer of the plasma cells with no cure. Sam Walton, the seemingly indefatigable merchant who still bounced into stores at dawn to check displays, was dying. Yet even facing mortality, he couldn't stop working. From his hospital bed at MD Anderson Cancer Center in Houston, he'd call store managers to quiz them about sales figures. Nurses found him sneaking out to visit a nearby Target, IV pole in tow, to check their prices.

"I want you to promise me something," he told his executives during one of his final Saturday morning meetings, his voice weakened but his eyes still fierce. "Promise me that you won't let this company lose its soul. We've built something special here—not because we're the biggest, but because we've never forgotten that this is about serving folks who don't have much money."

President George H.W. Bush flew to Bentonville in March 1992 to present Walton with the Presidential Medal of Freedom, America's highest civilian honor. Walton, confined to a wheelchair and down to 120 pounds, managed to stand when the President entered. "Mr. Sam," Bush said, "you embody the entrepreneurial spirit and epitomize the American dream." Walton's response was characteristic: "I'm just a merchant who got lucky."

On April 5, 1992—Easter Sunday—Sam Walton died at the University of Arkansas Medical Sciences Hospital in Little Rock. He was 74. That morning, Walmart operated 1,735 Walmart stores, 212 Sam's Clubs, and 13 Supercenters across 45 states. Annual sales had reached nearly $50 billion. The company employed 400,000 people—each one of whom Walton insisted on calling an "associate," never an employee.

The succession plan Walton had crafted was already in motion. David Glass, who'd been CEO since 1988, continued in that role. But the chairmanship—and with it, family control—passed to Sam's eldest son, S. Robson "Rob" Walton, on April 7, 1992, just two days after his father's death. Rob, a Columbia Law School graduate who'd served as Walmart's senior vice president and general counsel, understood his role perfectly: be the steward of his father's vision while letting professional management run the operations.

The family dynamics were fascinating and would shape Walmart for decades to come. Sam had been deliberate about involving his children without forcing them into the business. Rob, the lawyer, handled governance. John, the most entrepreneurial, had started his own investment firm but remained on the board. Jim, the youngest son, focused on the family bank, Arvest. Alice, the only daughter, pursued her passion for art, eventually founding the Crystal Bridges Museum of American Art in Bentonville.

Yet all four children understood their collective responsibility. Together with Sam's widow Helen, they controlled over 50% of Walmart's stock through their holding company, Walton Enterprises. This wasn't just wealth—with Walmart shares trading at $12 (adjusted for subsequent splits), the family's stake was worth over $25 billion, making them America's richest family. But it was also burden. Sam had structured things so that the family could never easily sell their control. This was their legacy to protect.

David Glass, now fully in charge, faced immediate challenges. The retail landscape was shifting. Category killers like Home Depot and Best Buy were using Walmart's own playbook against it in specialized retail. Target was moving upmarket, offering "cheap chic" that appealed to suburban customers who found Walmart too downscale. And there were rumblings about something called "online shopping," though few took it seriously.

But Glass had absorbed Sam's most important lesson: the moment you think you've got it figured out is the moment you start to fail. He pushed international expansion, opening Walmart's first foreign stores in Mexico through a joint venture with Cifra. He accelerated the Supercenter rollout, adding groceries to dozens of stores each year. Most importantly, he maintained the cost discipline that was Walmart's oxygen. Every penny saved was a penny that could be passed to customers or invested in growth.

The Saturday morning meeting continued, now led by Glass but still starting at 7 a.m. sharp. The Walmart cheer persisted, though some younger executives found it increasingly anachronistic. The fundamental philosophy—"servant leadership," as Sam had called it—remained intact. Store managers were still the heroes of the organization. The home office existed to serve the stores, not the other way around.

"Mr. Sam believed in leadership through service," Glass told associates at a memorial service. "He showed us that a leader's job is to remove obstacles for the people doing the real work—the folks in the stores serving customers. That principle, more than low prices or efficient distribution, is what made Walmart great."

In his autobiography, completed just before his death, Sam Walton had written his own epitaph: "I had to pick myself up and get on with it, do it all over again, only even better this time." His death marked not an ending but a transformation. The scrappy upstart was about to become a global colossus. The question was whether it could maintain its soul while conquering the world.

VI. The International Expansion Saga

The year before Sam Walton's death, he had sketched out a vision on a yellow legal pad that would have seemed insane to most retailers: Walmart stores in Mexico City, São Paulo, Beijing, Tokyo. "We're going to be a global company," he told the board in 1991, his voice already weakened by cancer. "The principles that work in Bentonville will work anywhere—people are people." This confidence would prove both prophetic and naive. The international expansion of Walmart would become a saga of spectacular successes, humbling failures, and lessons that would fundamentally reshape the company.

Mexico: The Crown Jewel

The conquest of Mexico began in 1991 through a joint venture with Cifra, Mexico's largest retailer. The partnership was brilliant in its simplicity—Cifra knew the market, Walmart knew systems and scale. The first Sam's Club opened in Mexico City in 1991, followed by a Walmart Supercenter in 1993. But this wasn't just exporting the Arkansas model wholesale. Walmart learned to adapt: smaller pack sizes for families without cars, credit programs for the unbanked, and acceptance that Mexican customers preferred to buy fresh produce from street vendors, not supercenters.

The 1994 peso crisis should have killed Walmart's Mexican adventure. The currency collapsed 50% overnight. Middle-class Mexicans saw their purchasing power evaporate. Cifra's stock price cratered. Most foreign retailers would have retreated. Instead, Walmart doubled down, buying out Cifra completely in 1997 to create Walmart de México. It was a massive bet on a broken economy—and it paid off spectacularly.

Today, Walmart de México y Centroamérica is the crown jewel of Walmart's international operations. In 2024 alone, the company invested $1.8 billion in Mexico—a 19% jump over the previous year—for store remodeling, new construction, and supply chain enhancement. The company opened 134 new stores last year, bringing its total to more than 2,500 locations. With 231,000 associates, Walmart is Mexico's largest private employer. The Bodega Aurrerá discount format, tailored specifically for lower-income Mexicans, generates margins that would make U.S. operations envious. The Mexican success story rests on three pillars. First, localization: Walmart de México reported an 8.3% increase in consolidated revenue for Q4 2024, with same-store sales growth of 4.3% in Mexico. Second, massive scale: the company reported consolidated revenue growth of 8.1% in 2024, with sales of more than 958 billion pesos, operated by more than 241,000 associates across more than 4,000 stores and clubs. Third, continued investment: Walmart announced a $6 billion investment in March 2025 to open additional stores across the country, equating to more than 125 billion pesos.

China: The Laboratory

If Mexico proved Walmart could succeed internationally, China became its laboratory for reinvention. The company entered in 1996, opening a hypermarket and Sam's Club in Shenzhen just as China was transforming from communist backwater to capitalist powerhouse. But this wasn't Arkansas or even Mexico—this was a market where customers expected to haggle, where "fresh" meant still swimming, and where the concept of returning merchandise was virtually unknown. The China story transformed dramatically during the pandemic. The China market performed strongly, with Walmart's net sales in Q2 fiscal year reaching US$4.6 billion, a year-on-year increase of 17.7%. Sam's Club store traffic has been growing positively and has become the engine of Walmart's performance growth.

The secret weapon has been Sam's Club, which operates 48 locations in China versus Costco's 7. But the real innovation is what Walmart calls "clouds"—micro fulfillment centers attached to each Sam's Club that enable one-hour delivery. Since 2018, Sam's Club has been building out its cloud warehouse network to support rapid delivery services. This hybrid model has enabled the retailer to achieve near-complete coverage in key cities. While its physical stores offer around 4,000 SKUs, the cloud warehouses feature a more curated selection of approximately 1,000 high-repeat-purchase items, tailored for quick commerce

Each store functions as a mini-distribution hub serving hundreds of neighborhoods through online orders.

In 2024, Walmart hosted the first India Growth Summit towards its goal to triple exports of Made-in-India goods to $10 billion annually by 2027.

India: The E-commerce Play

India represented Walmart's most strategic pivot—from physical retail to digital dominance. After years of regulatory battles trying to open stores, Walmart made its boldest international move: acquiring a 77% majority stake in the Indian e-commerce company Flipkart for $16 billion in 2018.

The Flipkart Group includes companies Flipkart, Myntra, Flipkart Wholesale, Flipkart Health+, Cleartrip, Ekart, Jeeves and Super. Money. Since 2007, Flipkart has enabled millions of consumers, sellers, merchants and small businesses to be part of India's eCommerce revolution. It has a registered user base of over 500 million and offers upwards of 150 million products across more than 80 categories.

The real jewel might be PhonePe, the digital payments platform that came with the Flipkart acquisition. The company has scaled rapidly to become India's leading consumer payments app with over 520 million registered users and a digital payments acceptance network of 38 million merchants. PhonePe processes over 230 million transactions every day, with an annualized Total Payment Value (TPV) of USD 1.5+ trillion.

In the U.S., Walmart is dabbling with a financial tech business, but nothing compared to the scale of mobile payments giant PhonePe in India. Walmart owns a majority stake in PhonePe, which was part of its $16 billion acquisition of Flipkart. Flipkart has since spun off the fintech operation, and in 2023, Walmart invested another $200 million in PhonePe.

The India strategy reflects a sophisticated understanding of market dynamics. Rather than fight regulations limiting foreign ownership in retail, Walmart leveraged e-commerce and fintech—sectors with fewer restrictions. PhonePe launched Indus Appstore in February 2024, an Android app store in challenge to Google's monopoly in its largest market by users. To fight Google Play Store, PhonePe has armed Indus Appstore with a range of unique and personalized features and developer-friendly terms. Indus Appstore supports 12 regional languages (including English) and around-the-clock support service.

Walmart executives cited both Flipkart and PhonePe as playing key roles in Walmart's goal of doubling its overseas gross merchandise volume to $200 billion in five years. "It is not crazy to think that both those businesses could be $100 billion businesses in the future," Walmart Chief Financial Officer John David Rainey said at an investors conference.

Failed Markets & Lessons

Not every international adventure ended in triumph. Germany became Walmart's most public and expensive failure—a cautionary tale of cultural arrogance meeting market reality.

Walmart's initial entry into German market was through the acquisitions of renowned 21 store Wertkauf chain for an estimated $1.04 billion in December 1997. It was followed one year later by the acquisition of Interspar's 74 hypermarkets from Spar Handels AG, the German unit of the French Intermarche Group, for €560 million.

The problems were immediate and fundamental. Walmart's cultural insensitivity led to its failure in Germany. Most of the Global mergers and acquisitions failed to produce any benefit for the shareholders or reduced value, which was mainly due to the lack of intercultural competence. Lack of sensitivity and understanding of language barriers, local traditions, consumer behavior, merchandising, and employment practices irreversibly damaged Walmart's image in Germany. One of the main reasons that failed Walmart in Germany is when it attempted to transport the company's unique culture and retailing concept to the new country.

The specifics ranged from comical to catastrophic. A regular day at a Walmart outlet in Germany started with light exercise and an almost cultish type of chant. Yes, the employees were made to chant "Walmart! Walmart! Walmart!" while doing light jumping and calisthenics. Maybe the reason behind this was to get them all excited about their shift and make them feel like a part of the Walmart family. However, the employees likely found this to be somewhat embarrassing. Also, the employees were not allowed to date or be romantically involved with each other.

Germans are known to have a quick and non-interactive shopping experience. Walmart smiling greeters and active floor helpers made customers feel uncomfortable. In addition, smiling female customer service appeared to males as if they were flirting. German's were used to bagging their own groceries as it was not sanitary or normal for others to touch their items. Customers were not used to and did not like that Walmart employees would bag their groceries for them.

Perhaps most critically, Walmart failed on its core promise. The German market at this point was an oligopoly with high competition among companies which used a similar low price strategy as Walmart. As a result, Walmart's low price strategy yielded no competitive advantage. Established discounters like Aldi and Lidl had already perfected the low-price model with German efficiency.

On July 2006, Walmart announced its official defeat in Germany and would sell its 85 German stores to the rival supermarket chain Metro and would book a pre-tax loss of about $1 billion (£536 million) on the failed venture.

Argentina told a similar story of misreading market dynamics. Walmart Argentina was founded in 1995 and operates stores under the banners Walmart Supercenter, Changomas, Mi Changomas, and Punto Mayorista. On November 6, 2020, it was announced that Walmart has sold its Argentine operations to Grupo de Narváez. The company faced supplier boycotts, couldn't execute its low-price strategy against entrenched local competitors, and never captured more than 2% market share.

Walmart's investments outside the U.S. have seen mixed results. Its operations and subsidiaries in Canada, the United Kingdom (ASDA), Central America, Chile (Líder), and China are successful; however, its ventures failed in Germany, Japan, South Korea, Brazil and Argentina.

The lesson was clear: operational excellence alone doesn't guarantee success. Understanding local culture, adapting business models, and respecting existing market dynamics matter as much as supply chain efficiency. As one CFRA analyst noted, divesting unprofitable international businesses was the most important step to improve Walmart's profit trajectory. These failures, painful as they were, taught Walmart to be a more sophisticated global operator—lessons that would prove invaluable in the coming battle with Amazon.

VII. The E-commerce Revolution & Amazon Battle

The Awakening

The year was 1995. Jeff Bezos was shipping books from his garage while Sam Walton's heirs were counting their billions. Nobody at Walmart's Bentonville headquarters was losing sleep over an online bookstore. That complacency would cost them dearly.

Walmart launched its first website in 1996, the same year as Amazon's IPO. But while Bezos was building for the future, Walmart treated online retail like a science experiment—interesting but not essential. By 2000, Walmart.com was generating just $100 million in sales. Amazon was doing $2.8 billion. The gap would only widen.

The wake-up call came gradually, then suddenly. By 2010, Amazon had surpassed Walmart in market capitalization despite having one-tenth the revenue. Wall Street was betting on the future, and that future didn't include driving to big-box stores. Walmart executives finally understood: this wasn't about competing with another retailer. This was about preventing their own Blockbuster moment.

The Acquisitions & Digital Transformation

Doug McMillon, who became CEO in 2014, recognized that Walmart couldn't out-Amazon Amazon by building from scratch. The company needed to buy its way into the digital future. The shopping spree began with Jet.com in 2016—$3.3 billion for a money-losing startup that had been in business for just one year. Wall Street was incredulous. Walmart was desperate.

But Marc Lore, Jet's founder who came with the deal, brought something Walmart desperately needed: digital DNA. Under his leadership, Walmart acquired a portfolio of digital-native brands: Hayneedle.com for furniture, Shoes.com for footwear, Moosejaw for outdoor gear, Modcloth for vintage-inspired fashion, and Bonobos for men's clothing. Each acquisition wasn't just about the brand—it was about acquiring talent, technology, and most importantly, knowledge of how to sell online to millennials who wouldn't be caught dead in a Walmart store.

The Jet.com acquisition alone increased Walmart's online sales by 63% and expanded its online inventory from 10 million to 67 million items. More importantly, it brought dynamic pricing algorithms and a marketplace model that could compete with Amazon's third-party seller platform.

The Competitive Response

By 2019, something remarkable was happening. Walmart's e-commerce sales were growing at 40% annually while Amazon's core North American retail growth had slowed to the mid-teens. Walmart International's revenue reached $114.6 billion last year, which represented 18% of Walmart's consolidated sales in fiscal 2024. The business sector holds tremendous growth potential in some of the world's most populated and fastest-growing countries.

The secret weapon was something Amazon couldn't replicate: 4,700 stores within 10 miles of 90% of Americans. Walmart transformed these stores into fulfillment centers. Online grocery pickup exploded from 40 locations in 2016 to over 3,100 by 2019. Customers could order groceries on their phone during lunch and pick them up on the way home without leaving their car. Amazon's Whole Foods, with just 500 stores, couldn't match that convenience.

The marketplace strategy showed even more promise. While Amazon had over one million active sellers, Walmart had been selective, focusing on quality over quantity with roughly 100,000 vetted sellers. The marketplace saw more than 30% sales growth in each of the past four quarters, and Walmart's growth rate was consistently outpacing Amazon's core online business in North America.

Then came the masterstroke: Walmart+ launched in September 2020, right in the middle of the pandemic. For $98 a year (deliberately undercutting Amazon Prime's $119), members got free shipping, fuel discounts at 14,000 stations, scan-and-go checkout, and free grocery delivery. Within two years, the program had an estimated 32 million members. Not Prime's 200 million, but enough to matter.

Omnichannel Advantage

What Walmart understood—finally—was that the future wasn't online or offline. It was both, seamlessly integrated. A customer might research a TV online, buy it through the app, pick it up at the store, and grab groceries while there. Or order groceries for delivery, add a prescription for store pickup, and throw in a bicycle that ships from a third-party seller.

In 2019, the Walmart app became the number one shopping app in the U.S. on Black Friday, toppling Amazon for the first time. It wasn't just symbolic—it showed that Walmart had finally figured out how to leverage its physical footprint in the digital age.

The pandemic accelerated everything. E-commerce sales jumped 79% in 2020, then another 11% in 2021 even as stores reopened. Walmart had built the infrastructure just in time. Stores became fulfillment centers, parking lots became pickup points, and employees became personal shoppers. The company that Sam Walton built for a physical world had successfully transformed for a digital one.

Today, Walmart's global e-commerce sales exceed $100 billion annually. The U.S. e-commerce segment consistently delivers double-digit growth. The company operates the third-largest online marketplace in the U.S., behind only Amazon and eBay. Most remarkably, Walmart's online grocery business is now larger than Amazon's—proof that in retail, the race doesn't always go to the first mover, but sometimes to the one with the deepest roots.

The battle with Amazon is far from over. But Walmart has proven it won't be the next Sears—killed by a digital upstart it dismissed until too late. Instead, it has become something Sam Walton might not recognize but would surely admire: a technology company that happens to run stores, competing with a store operator that happens to be a technology company. In this new retail reality, the spoils go not to the pure plays but to the platforms—and Walmart, against all odds, has become one.

VIII. Modern Era: Technology, Automation & Future Bets

Store & Supply Chain Innovation

Inside Walmart's Pedricktown, New Jersey distribution center, a ballet of robots unfolds 24 hours a day. Automated guided vehicles glide silently down aisles, retrieving products with millimeter precision. Robotic arms sort packages at superhuman speed. AI algorithms orchestrate the entire symphony, predicting what will be needed where, when, and in what quantity. This isn't science fiction—it's Walmart in 2024, and it's happening in dozens of distribution centers across America.

The transformation is staggering in scope. As of October 31, 2022, Walmart's international operations comprised 5,266 stores and 800,000 workers in 23 countries outside the United States. With 2.2 million employees worldwide, the company is the largest private employer in the U.S. and Mexico, and one of the largest in Canada. Each of these locations is becoming smarter, more automated, more connected.

The automation push isn't just about cost-cutting—though labor expenses have been trimmed by billions. It's about speed and accuracy. Automated fulfillment centers can process online orders in under an hour. Inventory accuracy has improved from 85% to over 95%. Store associates, freed from mundane tasks like inventory counting (now done by shelf-scanning robots), can focus on customer service and complex problem-solving.

But the real innovation is happening at the intersection of physical and digital. Walmart's stores now feature "market fulfillment centers"—automated storage systems built into the back of supercenters that can fulfill thousands of online orders daily. Customers might not see them, but these mini-warehouses are why Walmart can offer same-day delivery on 160,000 items in many markets.

The supply chain itself has become predictive rather than reactive. Machine learning models analyze weather patterns, social media trends, local events, and historical data to predict demand spikes before they happen. When a hurricane threatens Florida, Walmart's systems automatically route extra water, batteries, and Pop-Tarts (surprisingly, one of the most purchased pre-hurricane items) to stores in the storm's path.

Financial Performance

The numbers tell a story of transformation. Walmart's total revenue for fiscal 2024 reached $648 billion, making it the world's largest company by revenue for the 11th consecutive year. But revenue alone doesn't capture the dramatic shift in profitability and efficiency.

E-commerce, once a drag on margins, is approaching profitability in many markets. The company's gross margin rate has expanded for eight consecutive quarters, reaching levels not seen since the early 2000s. Operating cash flow exceeded $36 billion, funding massive investments in technology while still returning $16 billion to shareholders through dividends and buybacks.

International operations, after years of restructuring, are finally delivering. Walmart's international net sales jumped more than 5.7% to $34.3 billion in Q4 2024 from $32.4 billion in the year-ago period. The PhonePe business hit $1.7 trillion TPV (total payments volume) by the end of January 31 and they have something like 310 million transactions daily.

The Walton family's continued ownership—still controlling over 50% of shares—provides patient capital for long-term investments. While other retailers scramble quarter-to-quarter, Walmart can take five-year bets on autonomous vehicles, drone delivery, and virtual reality shopping.

The Cultural Evolution

Perhaps the most remarkable transformation has been cultural. The company that once symbolized everything wrong with American capitalism—low wages, destroyed Main Streets, cheaply made foreign goods—has quietly repositioned itself as a force for good.

Walmart became the largest corporate purchaser of renewable energy in the U.S. It committed to zero emissions by 2040. It raised starting wages to $14-19 per hour, well above federal minimum wage. It launched Live Better U, offering free college tuition to all associates. During COVID-19, it administered millions of vaccines, becoming America's largest civilian vaccination site.

The "Buy American" initiative Sam Walton started has been revived with $350 billion committed to U.S.-made products over 10 years. A 2005 economic study found that "Walmart's discounting on food alone boosts welfare of American shoppers by at least $50 billion per year." The company that once epitomized globalization is now betting on reshoring and local sourcing.

The workforce itself is evolving. Walmart's data scientists and engineers now number in the thousands. The company's tech campus in Austin rivals those of Silicon Valley giants. Walmart Labs in Silicon Valley focuses on next-generation retail technology. The company that started with a five-and-dime store now holds thousands of patents in artificial intelligence, robotics, and augmented reality.

Store associates are being reskilled rather than replaced. Through Walmart Academies, over one million associates have received training in everything from robotics maintenance to data analysis. The average store manager, who once focused on scheduling and shrinkage, now manages a complex omnichannel operation generating $100 million in annual revenue.

Even the stores themselves are evolving. Walmart is testing stores with no checkout lanes—just scan-and-go technology. Health clinics operated by major hospital systems. Financial service centers offering everything from check cashing to small business loans. Some locations feature ghost kitchens preparing meals for multiple delivery-only restaurant brands.

The company is also betting heavily on advertising, transforming its massive customer data into a $3 billion high-margin business. Walmart Connect allows brands to target ads based on actual purchase behavior—something even Amazon struggles to match. When Procter & Gamble wants to reach people who buy competitor products, Walmart knows exactly who they are.

This modern era represents Walmart's third act. The first was Sam Walton's discount revolution. The second was the scaling years under David Glass and Lee Scott. This third act—call it the Doug McMillon era—is about transformation. From retailer to technology platform. From employer of last resort to career launcher. From environmental villain to sustainability leader.

The challenges remain immense. Amazon continues to grow. Younger consumers prefer Target's style or Costco's treasure hunt experience. Labor activists still protest wages and working conditions. Small towns still mourn lost local businesses.

But Walmart in 2024 is unrecognizable from even a decade ago. It's a company that uses AI to predict what you'll want before you know you want it. That can deliver groceries by drone in 30 minutes. That operates one of America's largest healthcare businesses. That processes over $100 billion in e-commerce sales while still running 4,700 physical stores profitably.

Sam Walton built a retail empire on one insight: give ordinary folks the lowest prices possible. His successors are building something else—a platform that touches every aspect of American life, from how we shop to how we work to how we receive healthcare. Whether that's progress or peril depends on your perspective. What's undeniable is that Walmart, once again, is transforming retail. And everyone else is scrambling to keep up.

IX. Playbook: Business & Investing Lessons

Scale Economics & Operational Excellence

The Walmart playbook begins with a deceptively simple formula that Sam Walton scribbled on countless yellow legal pads: lower prices lead to more customers, which creates higher volumes, which generates better supplier terms, which enables lower prices. This virtuous cycle, what economists call "scale economies," isn't unique to Walmart. What's unique is the religious devotion to making it work.

Consider the numbers: Walmart purchases roughly $400 billion in goods annually. When you're buying that much toilet paper, every penny matters. A one-cent reduction in the cost of a roll, multiplied across billions of units, saves hundreds of millions. Those savings don't go to shareholders—they go to lower shelf prices, which drives more traffic, which increases volume, which improves negotiating power. The wheel keeps spinning.

But scale without operational excellence is just bureaucracy. Walmart's true genius lies in execution. Cross-docking—where products move directly from inbound to outbound trucks without entering storage—was perfected at Walmart. The company's distribution centers achieve 99.5% accuracy rates. Trucks depart on schedule 95% of the time. These aren't sexy metrics, but they're the difference between profit and loss in a business with 2% net margins.

Sam Walton famously told FedEx founder Fred Smith that he was "a pretty good retailer but a better logistician." This wasn't false modesty. Walmart spends less than 3% of sales on logistics while competitors average 5%. That 2% difference, on $600 billion in revenue, is $12 billion—roughly Walmart's entire annual profit.

The company's early investment in technology—computerized inventory in the 1970s, satellite communications in the 1980s, RFID in the 2000s—always aimed at one goal: perfect information about what's selling where. Today's AI systems are just the latest evolution. When every dollar of inventory turns 12 times per year instead of 8, that's billions in freed-up capital.

Cultural Adaptation vs. Standardization

The international expansion saga teaches a masterclass in humility. Walmart's failures—Germany, South Korea, Argentina—shared a common thread: applying the Arkansas playbook without adaptation. The successes—Mexico, China, India—required fundamental reimagination.

In Mexico, Walmart learned to operate everything from tiny Bodega Aurrerá discount stores to massive Supercenters, adapting format to neighborhood. Payment plans for the unbanked. Smaller pack sizes for daily shoppers. Integration with local suppliers who could deliver fresh tortillas twice daily. The BAIT Experience Centers allow Walmex to include mobile and home internet. BAIT has grown to 13 million active customers, and the service is 17% cheaper than the nearest competitor. In Mexico, Walmart has 1,500 pharmacy centers and 500 medical clinics that provide customers with physical and virtual visits for $2 a month.

China required even deeper transformation. Sam's Club succeeded not by replicating the American warehouse model but by becoming a premium destination for China's emerging middle class. The innovation of "clouds"—micro-fulfillment centers enabling one-hour delivery—couldn't have been conceived in Bentonville. It required Chinese management solving Chinese problems.

India represented the ultimate adaptation: abandoning physical retail entirely for e-commerce and fintech. Parent Walmart's CFO said that Flipkart's "improving" losses are giving the retail major a "lot of confidence" in what the ecommerce giant's financial profile would look in a few years. "They're (Flipkart and PhonePe) all on their path to profitability. We're seeing those ecommerce losses improve year after year after year, which gives us a lot of confidence in what the overall financial profile of this business looks like a few years from now."

The lesson for investors: beware companies that confuse their business model with universal truth. What works in Bentonville might fail in Berlin. The companies that endure are those that maintain core principles while adapting tactics. Walmart kept "everyday low prices" but learned that implementation varies by culture.

Technology as Competitive Moat

Walmart's technology investments reveal a crucial insight: in retail, technology isn't an add-on—it's the business. The company that Sam Walton started with a pencil and paper now employs thousands of data scientists and holds patents in artificial intelligence, autonomous vehicles, and blockchain.

But technology at Walmart serves operational excellence, not technology for its own sake. Blockchain tracks food supply chains not because blockchain is trendy but because it can identify contamination sources in seconds instead of days. Robots sort packages not to impress investors but because they're 3x faster than humans with 99.9% accuracy.

The real moat isn't any single technology but the integration of all of them. When online orders flow seamlessly to store fulfillment, when inventory systems talk directly to supplier factories, when pricing algorithms adjust in real-time based on competition—that system complexity becomes impossible to replicate. Amazon might have better AI, Target might have nicer apps, but nobody matches Walmart's end-to-end integration.

The Power of Patient Capital

The Walton family's continued control—maintaining over 50% ownership through all market cycles—provides a strategic advantage that public market investors often miss. Patient capital enables long-term thinking.

Consider Walmart's e-commerce journey. The company lost billions online for over a decade. Wall Street hammered the stock. Activists demanded digital divestiture. But the Waltons held firm, understanding that e-commerce capability wasn't optional but existential. Today's $100 billion online business vindicated that patience.

The same pattern repeats: international expansion (20 years to profitability), grocery (15 years of losses before dominance), healthcare (still investing after a decade). Public companies rarely have this luxury. Quarterly earnings calls force short-term optimization. Walmart can play the long game because the Waltons think in generations, not quarters.

For investors, this suggests a framework: look for companies with aligned, patient capital that can withstand short-term pain for long-term gain. The best investments often look terrible for years before looking brilliant. But you need the capital structure to survive the terrible years.

The Platform Evolution

Perhaps the most underappreciated aspect of modern Walmart is its evolution from retailer to platform. Like Amazon, but following a different path, Walmart is becoming infrastructure that others build upon.

The marketplace hosts 100,000 third-party sellers. Walmart Fulfillment Services handles their logistics. Walmart Connect sells their advertising. Walmart Data Ventures monetizes insights. Walmart GoLocal delivers for other retailers. Walmart Health partners with health systems. Each service leverages existing infrastructure while creating new revenue streams with minimal capital investment.

This platform strategy explains why Walmart's valuation multiple has expanded despite modest revenue growth. Platforms are worth more than retailers because they're capital-light, scalable, and create network effects. Every seller on Walmart's marketplace makes the platform more valuable to shoppers, which attracts more sellers. The cycle compounds.

The lesson extends beyond retail: in every industry, the winners are increasingly those who transform from operators to platforms. John Deere isn't just selling tractors but agricultural data platforms. Nike isn't just selling shoes but fitness ecosystems. The companies that recognize this shift early capture outsized returns.

X. Bear vs. Bull Case Analysis

Bull Case: The Unstoppable Force

The bullish thesis on Walmart rests on five pillars, each reinforcing the others in a virtuous cycle that competitors cannot break.

First, the sheer scale remains unmatched. With 4,700 U.S. stores within 10 miles of 90% of Americans, Walmart possesses a physical footprint that would cost hundreds of billions to replicate. These aren't just stores—they're fulfillment centers, healthcare clinics, financial service hubs, and community anchors. Amazon, despite its ambitions, operates just 500 Whole Foods locations. Target has 1,900 stores. Nobody comes close to Walmart's coverage.

Second, the omnichannel execution has reached an inflection point. Walmart's e-commerce growth consistently outpaces Amazon's North American retail business—a stunning reversal from five years ago. The company's unique ability to blend digital and physical—buy online, pick up in store; order groceries for delivery; ship from store—creates convenience that pure-play e-commerce cannot match. Walmart+ membership, while smaller than Prime, is growing 30% annually and deepening customer loyalty.

Third, international operations are finally delivering after decades of investment. Executives cited both Flipkart and PhonePe as playing key roles in Walmart's goal of doubling its overseas gross merchandise volume to $200 billion in five years. "It is not crazy to think that both those businesses could be $100 billion businesses in the future," Walmart CFO John David Rainey said. Mexico remains a cash cow, China is innovating rapidly, and India offers massive upside through Flipkart and PhonePe.

Fourth, new revenue streams are approaching materiality. Walmart Connect's advertising business generates $3 billion in nearly pure-margin revenue. Healthcare could become a $50 billion business. Financial services, logistics-as-a-service, data monetization—each represents billions in potential high-margin revenue that doesn't require new stores or inventory investment.

Fifth, the competitive moat keeps widening. Walmart's cost structure—2-3% lower than competitors—becomes more valuable as consumers feel economic pressure. The company's AI and automation investments, backed by $36 billion in annual cash flow, create capabilities that subscale competitors cannot match. The Walton family's patient capital enables long-term bets that public competitors cannot afford.

The bull case sees Walmart reaching $1 trillion in revenue by 2030, with expanding margins from digital advertising, marketplace fees, and service businesses. The stock could double as the market recognizes Walmart's transformation from low-margin retailer to high-margin platform.

Bear Case: The Disruption Ahead

The bearish perspective acknowledges Walmart's strengths but sees fundamental challenges that financial engineering cannot solve.

Start with demographic destiny. Walmart's core customer skews older, rural, and lower-income—demographics in relative decline. Millennials and Gen Z prefer Target's style, Costco's treasure hunt, or Amazon's convenience. Despite efforts to premiumize, Walmart cannot shake its discount DNA. The company that serves America's working class faces headwinds as that class shrinks and ages.

Labor presents an existential challenge. With 2.1 million employees, Walmart remains vulnerable to wage inflation and unionization pressure. The company's improved wages—now $14-19 per hour—still lag inflation in many markets. Healthcare benefits, while improved, remain controversial. A successful unionization campaign could add billions in costs overnight. Automation can only go so far in a business that requires human interaction.

E-commerce economics remain challenging. While growing rapidly, online sales generate lower margins than stores due to delivery costs and competitive pricing pressure. Walmart's massive e-commerce investments have yet to generate returns that justify the capital deployed. The company is essentially subsidizing online growth with store profits—a strategy that becomes harder as the online mix increases.

Amazon's competitive response is accelerating. With 200 million Prime members and growing physical presence through Whole Foods, Amazon Go, and newly announced department stores, Bezos' empire is attacking Walmart's stronghold. Amazon's cloud profits—$25 billion annually—provide war chest funding that Walmart cannot match. In technology, logistics, and customer data, Amazon maintains structural advantages.

Disruption lurks from unexpected corners. Autonomous delivery could eliminate Walmart's last-mile advantage. Social commerce platforms like TikTok Shop bypass traditional retail entirely. Subscription services for everything from groceries (HelloFresh) to clothing (Stitch Fix) reduce shopping trips. Generation Alpha might not shop at all, preferring virtual goods in digital worlds.

The bear case sees Walmart's revenue growth slowing to GDP levels while margins compress from competition and labor costs. The stock could stagnate for years as the market recognizes that even successful transformation cannot overcome structural retail decline.

The Balanced View

Reality likely lies between these extremes. Walmart has proven remarkably adaptable—transforming from rural discounter to omnichannel platform while maintaining industry-leading profitability. The company's scale, operational excellence, and financial resources create a resilience that bears underestimate.

Yet the challenges are real. Retail remains brutally competitive with thin margins and constant disruption. Walmart must simultaneously defend against Amazon, compete with specialized retailers, invest in technology, and maintain stores—all while keeping prices low. Success requires near-perfect execution in an imperfect world.

The investment case ultimately depends on time horizon and risk tolerance. Short-term traders might avoid Walmart's volatility as it navigates transformation. Long-term investors might embrace it, betting that a company that survived the transition from Main Street to strip malls to e-commerce can navigate whatever comes next.

What's certain is that Walmart's next decade will look nothing like its last. The company Sam Walton built for twentieth-century America must reinvent itself for a twenty-first-century world. Whether that reinvention succeeds will determine not just Walmart's fate but the future of retail itself.

XI. Epilogue: What Would Sam Think?

Sam Walton died on April 5, 1992, when Walmart's annual revenue was approaching $50 billion. Today, that same company generates $50 billion every month. The five-and-dime merchant from Oklahoma built something that outlived him, outgrew him, and ultimately transcended anything he could have imagined. The question that haunts Bentonville's headquarters: would Sam recognize—or even approve of—what Walmart has become?

In some ways, the answer is obviously yes. The fundamental mission remains unchanged: "Save people money so they can live better." Every decision, from automation investments to international expansion, theoretically serves this purpose. The everyday low prices that Sam evangelized still drive the company. A gallon of milk costs less at Walmart than anywhere else, just as Sam intended.

The operational excellence would delight him. Sam spent countless hours studying competitors, measuring shelf heights, timing checkout speeds. Today's data scientists and robotics engineers are his spiritual descendants, just with better tools. The logistics network that delivers products with 99.5% accuracy would seem like magic to a man who started by driving his own truck between stores.

But other aspects might trouble him. Sam Walton was a merchant, not a technologist. He understood people, not algorithms. The Walmart that employs thousands of engineers, that runs massive data centers, that develops artificial intelligence—this might seem alien to a man who preferred yellow legal pads to computers. "High tech stuff is Kmart's thing," he once said dismissively. Today, Walmart is as much a technology company as a retailer.

The sheer scale might disturb him too. Sam built his empire by thinking small—focusing on underserved rural communities that big retailers ignored. Today's Walmart is the ultimate big retailer, the very thing he positioned against. The company that championed small-town values now operates in Shanghai, São Paulo, and Mumbai. The insurgent became the incumbent.

The tension between scale and soul pervades modern Walmart. Associates still gather for the Walmart cheer that Sam invented, but it feels different when performed in a 200,000-square-foot Supercenter rather than a 16,000-square-foot discount store. The profit-sharing plan he created has made many employees wealthy, but 2.1 million associates can't all feel like partners in the way his original 20 employees did.

International expansion embodies this complexity. Sam was intensely American, building a company that reflected and served American values. Yet Walmart's future growth depends on markets where those values don't translate. The company succeeds abroad precisely when it stops being the Walmart that Sam built—adapting to local cultures, abandoning standardization, becoming something unrecognizable from Arkansas.

The evolution from discount retailer to technology platform would perhaps puzzle him most. Sam understood retail as relationship—knowing your customers, serving their needs, earning their loyalty through service. Today's Walmart knows customers through data, serves needs through algorithms, earns loyalty through Prime-like subscriptions. It works, but it's not what Sam did.

Yet perhaps Sam would surprise us with his pragmatism. He was, above all, a competitor who adapted to win. When discount stores threatened variety stores, he built discount stores. When computers offered advantage, he bought computers. When Kmart seemed unstoppable, he found ways to stop them. The man who flew his own plane to scout locations might have embraced drones delivering packages.

"Most everything I've done, I've copied from someone else," Sam once admitted with characteristic humility. Today's Walmart continues that tradition—copying Amazon's marketplace, Costco's membership model, CVS's health clinics. Sam might not understand the technology, but he'd understand the strategy: find what works and do it better.

The financial success would vindicate him. Walmart's market capitalization exceeds $500 billion. The Walton family's wealth approaches $300 billion. The company he started with $5,000 has become Earth's largest corporation. By the brutal metrics of capitalism, Sam Walton won bigger than any merchant in history.

But Sam measured success differently. In his autobiography, he wrote: "If we work together, we'll lower the cost of living for everyone...we'll give the world an opportunity to see what it's like to save and have a better life." By this standard, the record is mixed. Walmart has indeed lowered costs—economists estimate its price pressure saves consumers $300 billion annually. But whether this creates "a better life" remains fiercely debated.

The enduring power of everyday low prices—the strategy Sam identified in 1962—still drives everything. Whether expressed through Supercenters or same-day delivery, Mexican bodegas or Indian e-commerce, the core promise remains: give ordinary people access to goods they couldn't otherwise afford. That promise, more than any technology or strategy, is Sam Walton's true legacy.

Standing in a modern Walmart—with its self-checkout kiosks, pickup towers, and scan-and-go apps—you can barely glimpse the five-and-dime store Sam opened in 1945. The path from there to here wasn't straight or inevitable. It required countless decisions, many failures, constant adaptation. But the destination was always the same: serve the customer, control costs, and never be satisfied.

"There is only one boss—the customer," Sam liked to say. "And he can fire everybody in the company from the chairman on down, simply by spending his money somewhere else." This remains true whether the customer shops in stores or online, pays with cash or cryptocurrency, lives in Bentonville or Bangalore.

What would Sam think of modern Walmart? He'd probably grab a yellow legal pad, hop in his pickup truck, and drive to the nearest store. He'd talk to associates, observe customers, check prices. He'd measure what matters: are we serving people who need it most? Are we operating efficiently? Are we winning?

Then he'd head back to Bentonville with a list of improvements. Because for Sam Walton, and for the company that bears his name, the job is never finished. There's always someone to serve better, something to improve, some new way to deliver on that founding promise: save people money so they can live better.

The empire of everyday low prices endures, even as everything else changes.

XII. Recent News

The most significant recent development is Walmart's massive expansion commitment to Mexico. In March 2025, the company announced a $6 billion investment to open additional stores across Mexico, equivalent to more than 125 billion pesos. This follows 2024's $1.8 billion investment that saw 134 new store openings, bringing the total to more than 2,500 locations. The Mexican operation reported an 8.3% revenue increase in Q4 2024, with consolidated revenue exceeding 958 billion pesos for the full year.

In India, strategic discussions about monetization are accelerating. Walmart aims to maintain liquidity options in India and has begun talks to list Flipkart and PhonePe. However, challenges remain due to market conditions, fierce competition in fintech and e-commerce, and the companies' readiness for listing. The retail giant sees PhonePe's IPO as a more viable option and wants to list the company by the end of FY26 at the latest. PhonePe is expected to file its draft prospectus by June and Walmart's aspiration is to see the fintech list at a $15 billion valuation.

The India Growth Summit in 2024 marked another milestone, with Walmart committing to triple exports of Made-in-India goods to $10 billion annually by 2027. This builds on the existing ecosystem where Flipkart serves over 500 million registered users and PhonePe processes $1.5 trillion in annual payment volume.

China continues to show robust growth, with Q2 fiscal year net sales reaching $4.6 billion, a 17.7% year-over-year increase. Sam's Club China has emerged as a particular bright spot with 48 locations compared to Costco's 7, leveraging innovative "cloud" micro-fulfillment centers for one-hour delivery.

Technology initiatives continue to accelerate, with major advancements in warehouse robotics for picking, packing, and sorting. The company's focus on automation and AI investments positions it to better compete with Amazon while maintaining its cost leadership position.

Financially, the company remains on solid footing despite facing some pressure on net income and operating margins in fiscal 2023. The focus on key international markets—China, India, and Mexico—continues to drive growth, while the company maintains its position as the world's largest retailer with 10,750 stores and clubs across 19 countries.

XIII. Links & Resources

Essential Reading: - "Made in America" by Sam Walton with John Huey - The founder's autobiography remains the definitive account of Walmart's early years - "The Wal-Mart Effect" by Charles Fishman - Critical examination of Walmart's economic impact - "In Sam We Trust" by Bob Ortega - The unauthorized story of Walmart's rise

SEC Filings & Investor Resources: - Walmart Investor Relations (stock.walmart.com) - Latest quarterly earnings, annual reports, and presentations - SEC EDGAR Database - Complete filing history including 10-Ks, 10-Qs, and proxy statements - Walmart Corporate Website (corporate.walmart.com) - Company news, sustainability reports, and governance documents

Academic Studies: - "The Economic Impact of Wal-Mart" - Multiple studies from MIT, Harvard Business School, and Wharton - "Wal-Mart and the Architecture of Control" - Duke University analysis of supply chain innovation - "The Diffusion of Wal-Mart and Economies of Density" - University of Minnesota economic study

Competitor Analysis: - Amazon Investor Relations - Understanding the primary competitive threat - Target Corporation Reports - Analyzing the upmarket competitor - Costco Wholesale Investor Center - Warehouse club competition - Kroger and Albertsons - Traditional grocery competitors

Supply Chain & Logistics: - "The Machine That Changed the World" - MIT study on lean production applicable to Walmart - Council of Supply Chain Management Professionals - Industry best practices - "Clockspeed" by Charles Fine - Supply chain strategy evolution

International Retail Markets: - Euromonitor International - Retail market data across all Walmart countries - China Chain Store Association - Chinese retail market analysis - India Brand Equity Foundation - Indian retail and e-commerce reports - Asociación Nacional de Tiendas de Autoservicio (ANTAD) - Mexican retail data

Technology & Automation: - Walmart Labs Blog - Direct insights into technological innovation - MIT Center for Transportation & Logistics - Academic research on retail logistics - "The Everything Store" by Brad Stone - Amazon's parallel technology journey

Historical & Cultural Context: - Walmart Museum in Bentonville - Virtual exhibits and historical archives - "Nickel and Dimed" by Barbara Ehrenreich - Critical perspective on Walmart labor practices - "The Retail Revolution" by Nelson Lichtenstein - Academic history of Walmart's impact

Podcasts & Documentaries: - "The High Cost of Low Price" (2005) - Critical documentary on Walmart's practices - "Walmart: The High Cost of Low Price" - Frontline PBS investigation - Acquired.fm episodes on Amazon and Costco - Comparative analysis of retail strategies - Masters of Scale episode on Walmart - Reid Hoffman interviews Doug McMillon

Industry Reports: - National Retail Federation - Annual retail industry forecasts - McKinsey Global Institute - Future of retail studies - Deloitte Retail Volatility Index - Tracking retail disruption - PwC Global Consumer Insights Survey - Consumer behavior trends

Books on Retail Strategy: - "Good to Great" by Jim Collins - Features Walmart as a case study - "The Innovator's Dilemma" by Clayton Christensen - Disruption theory applicable to retail - "Competition Demystified" by Bruce Greenwald - Strategic analysis framework - "Pour Your Heart Into It" by Howard Schultz - Contrast with Starbucks' premium strategy

These resources provide a comprehensive foundation for understanding Walmart's history, current operations, competitive position, and future trajectory. For serious students of retail and business strategy, Walmart remains perhaps the most important case study of the past half-century—a testament to operational excellence, strategic adaptation, and the enduring power of serving customers with everyday low prices.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube