Western Alliance Bancorporation: The Phoenix That Rose Twice

I. Introduction: A Regional Bank's Near-Death Experience

On a Friday afternoon in March 2023, Ken Vecchione was driving to an emergency root canal when his phone rang. An investment banker was on the line with alarming news: Silicon Valley Bank had just announced a catastrophic $1.8 billion after-tax loss from selling long-term securities. The news jolted bankers across the country, with particular reverberations for firms like Western Alliance with technology industry-based depositors.

Vecchione never forgot that moment. When he arrived at the dentist's office, still processing the implications, the oral surgeon prepared his anesthetic. "He says, 'Ken, I gotta shoot you up with novocaine,'" Vecchione later recalled. "I said, 'No need, doc. I'm going to be numb for a couple of days.' And I was."

The numbness would give way to terror within seventy-two hours. Roughly $8 billion in deposits flowed out of Western Alliance on the Monday after SVB's Friday night failure, and another $1.5 billion left the bank that Tuesday. The bank's stock opened Monday down 74% from its Friday close. In three trading sessions, this Phoenix-based regional bank had lost nearly two-thirds of its market value. For a moment, it appeared Western Alliance might join Silicon Valley Bank, Signature Bank, and First Republic on the growing list of 2023's failed banks.

It didn't.

Western Alliance Bancorporation has emerged as a notable player in the regional banking sector, demonstrating resilience and strategic growth despite industry-wide challenges. The West-based bank has maintained strong financial performance through a diversified business model that spans multiple high-growth niches, positioning it favorably among its mid-cap banking peers.

Today, Western Alliance manages approximately $91 billion in assets, is on the list of largest banks in the United States and is ranked 97th on the Forbes list of America's Best Banks. Its market capitalization stood at approximately $8.69 billion as of October 2025—a remarkable recovery from the depths of March 2023 when its stock briefly touched $7 per share.

This is the story of a bank that has survived two existential crises—the 2008 financial crisis that decimated Arizona and Nevada real estate, and the 2023 banking panic that claimed three major regional banks. How did a small Las Vegas community bank founded in 1994 become one of America's best-performing banks—and survive when others didn't? The answer reveals lessons about specialization, crisis management, and the enduring importance of sound banking principles in an age of social media-accelerated bank runs.

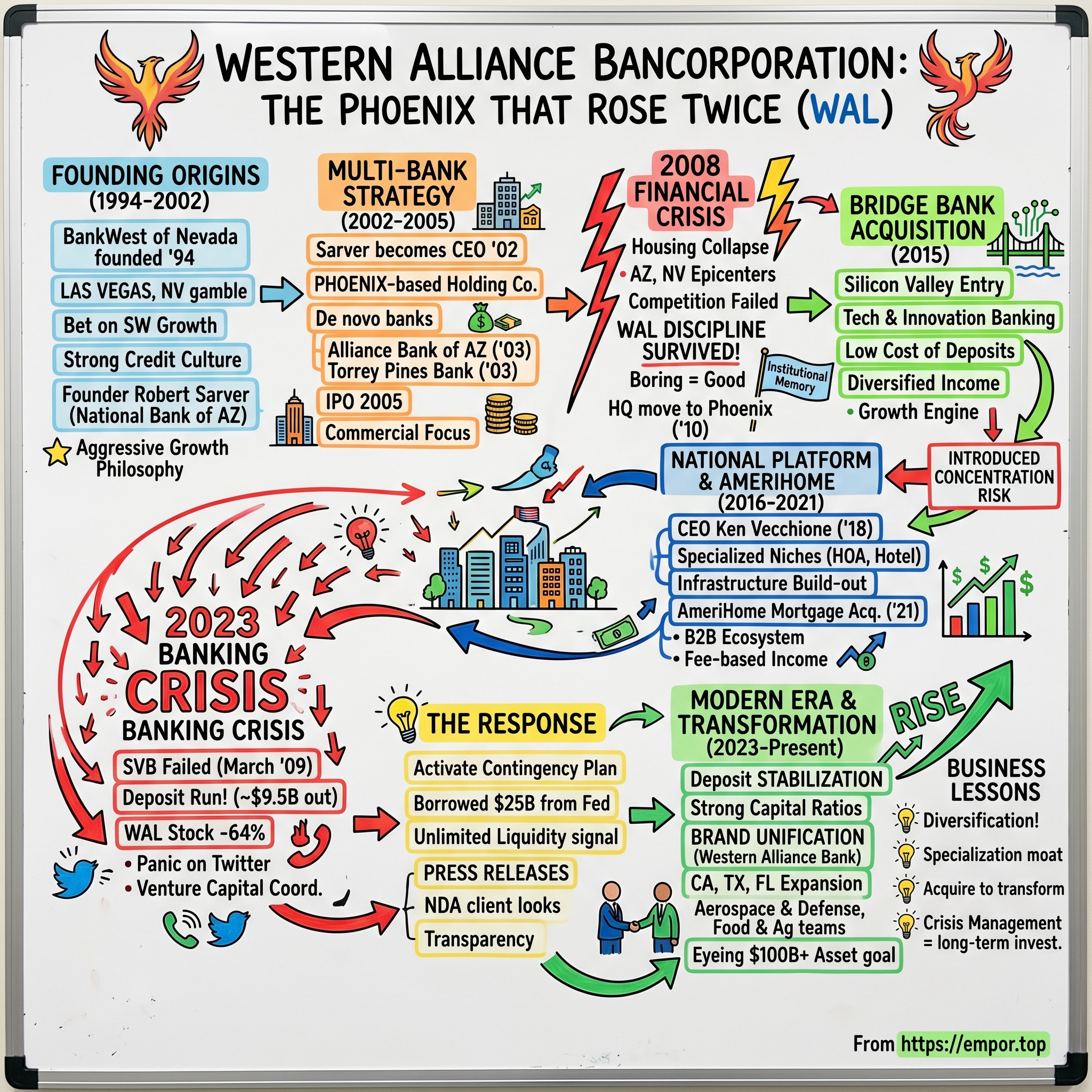

II. Founding Origins: The Las Vegas Gamble (1994-2002)

The origins of Western Alliance trace back to a city built on calculated risks. BankWest of Nevada was founded in 1994 by a group of individuals with extensive community banking experience in the Las Vegas market. The founding team included Robert Sarver, Donald D. Snyder, and James L. Gibson—names that would become synonymous with the bank's aggressive growth philosophy.

But it was Sarver who would prove to be the driving force. In 1984, at the age of 23, Robert Sarver founded the National Bank of Tucson, the youngest individual to charter a new bank in the United States at that time. He served as its president amid the era's banking deregulation under the Depository Institutions Deregulation and Monetary Control Act of 1980 and subsequent economic recessions.

Banking ran in Sarver's blood. Robert Sarver didn't cut his teeth on bank accounting ledgers, but he did start working as a part-time mortgage loan agent and internal auditor at his father's thrift, American Savings and Loan in Tucson, at age 16. His father, Jack Sarver, was a prominent Tucson businessman who died of a heart attack in 1979, leaving a legacy that Robert would eventually honor by funding the Sarver Heart Center at the University of Arizona.

Under Sarver's leadership, the institution expanded operations and rebranded as National Bank of Arizona, achieving status as the state's largest independent bank by assets and deposits before its acquisition by Zions Bancorporation in 1994. Following the sale, Sarver acquired Grossmont Bank in San Diego in 1995.

After selling National Bank of Arizona to Zions, Sarver spent the late 1990s as an executive at Zions Bancorporation, serving as Chairman and CEO of California Bank and Trust and as an Executive Vice President from June 1998 to March 2001. He also led Zions' acquisition of Sumitomo Bank of California in 1998. But Sarver was an entrepreneur at heart, not a corporate executive, and by 2002 he was ready to build something new.

The Las Vegas thesis was simple but powerful: bet on the explosive growth of the desert Southwest. Nevada was experiencing one of the fastest population growth rates in the country, fueled by California refugees seeking lower taxes and affordable housing, retirement migration, and the expansion of gaming and hospitality beyond the Strip. Since 1994, the bank's philosophy has been focused on understanding and serving the needs of local clients and pursuing growth markets and opportunities while emphasizing a strong credit culture.

This "strong credit culture" would prove prescient. While competitors would rush into subprime mortgages and condominium conversion loans during the mid-2000s housing boom, Western Alliance maintained discipline—a decision that would save the bank when the desert Southwest became ground zero for America's housing collapse.

III. The Multi-Bank Holding Company Strategy (2002-2005)

In 2002, he joined the board of directors at Western Alliance Bancorporation, a Phoenix-based holding company, and assumed the role of CEO. This wasn't just a job change—it was the beginning of an aggressive expansion strategy that would transform a single Las Vegas community bank into a multi-state powerhouse.

Sarver brought an audacious vision: replicate the BankWest success formula across the booming Southwest. In 2003, with the support of local banking veterans, we opened Alliance Bank of Arizona in Phoenix, Arizona and Torrey Pines Bank in San Diego, California. The approach was simultaneously local and scalable—each new bank would have its own identity, management team, and community relationships, while leveraging the holding company's capital, compliance infrastructure, and specialized lending platforms.

The de novo bank strategy produced remarkable early performance. Of the 230 banks founded in the United States since January 1, 2003, Alliance Bank of Arizona and Torrey Pines Bank both rank among the top ten in terms of total assets, loans and deposits as of December 31, 2004. This wasn't just good—it was best-in-class among hundreds of new bank charters nationwide.

The growth trajectory was explosive. On a consolidated basis, as of March 31, 2005, we had approximately $2.3 billion in assets, $1.3 billion in total loans, $2.0 billion in deposits and $137.1 million in stockholders' equity. The company had grown from $443.7 million in total assets and $410.2 million in total deposits as of December 31, 2000, to three chartered banks with $2.3 billion in total assets and $2.0 billion in total deposits by early 2005—a quintupling in less than five years.

The 2005 IPO marked Western Alliance's debut on the public markets. The prospectus filed with the SEC that June presented a company with a clear identity: a bank holding company headquartered in Las Vegas focused on commercial lending to small and mid-sized businesses across Nevada, Arizona, and California. The bank focused lending activities primarily on commercial loans, which comprised 88.0% of the total loan portfolio at March 31, 2005.

The Sarver era established patterns that would define Western Alliance for the next two decades: aggressive but disciplined growth, a focus on commercial relationships over consumer banking, the preservation of local brands and management teams after acquisitions, and an entrepreneurial culture willing to enter new markets when the opportunity presented itself.

IV. Surviving the First Fire: The 2008 Financial Crisis

Arizona and Nevada weren't just affected by the housing collapse—they were among the epicenters of the disaster. Phoenix and Las Vegas had experienced some of the most extreme home price appreciation during the boom years, and when the bubble burst, prices fell 50% or more in many neighborhoods. Unemployment soared. Construction companies that had been clients of every local bank went bankrupt. The "Arizona and Nevada thesis" that had seemed so brilliant in 2003 looked like a catastrophic miscalculation by 2009.

At Western Alliance, "we weren't a subprime mortgage lender. We didn't do leveraged buyout lending. We weren't financing condominium conversions of apartments. We weren't doing high-rise condominiums. We prepared for a real estate downturn, whereas a number of our competitors just thought this market was going to boom forever and ever."

This discipline—boring, perhaps, but essential—allowed Western Alliance to survive when competitors failed or were forced into distressed sales. The bank emerged from the crisis bloodied but alive, and began building for the next growth phase almost immediately.

The bank was founded in 1994 in Las Vegas, Nevada. In 2010, it moved its headquarters to Phoenix, Arizona. The relocation signaled more than a change of address—it marked a shift in identity from a Nevada community bank to a regional holding company with ambitions beyond any single market.

The crisis provided lessons that would pay dividends fifteen years later. "We were very fortunate that when this event took place, we had experienced people who had been through the 2007-2008 crisis," said Chairman Bruce Beach. The institutional memory of near-death, the muscle memory of crisis management, would prove invaluable when the next existential threat emerged.

During the recovery, Western Alliance continued acquiring and consolidating. In early 2006, Western Alliance announced two separate mergers: it would acquire Intermountain First Bancorp, the holding company for Nevada First Bank, for $108 million, as well as Bank of Nevada for $74 million. After the 2008 crisis, the company acquired Western Liberty Bancorp in 2012 for $55 million, continuing to build density in its core Nevada market.

V. Inflection Point #1: The Bridge Bank Acquisition (2015)

The 2015 acquisition of Bridge Capital Holdings marked a strategic inflection point that would reshape Western Alliance's identity—and, ironically, nearly destroy it eight years later.

Western Alliance Bancorp in Phoenix agreed to buy Bridge Capital Holdings in San Jose, Calif. The $10.6 billion-asset Western Alliance paid $425 million in cash and stock for the $1.8 billion-asset Bridge.

Why enter Silicon Valley's competitive banking market? The answer lay in Bridge Bank's unique positioning. Bridge Bank was founded in 2001 in Silicon Valley to offer a better way to bank for small-market and middle-market businesses across many industries, as well as emerging technology companies and the private equity community.

Robert Sarver articulated the strategic rationale with characteristic directness: "Bridge is a fast growing, well-managed organization that substantially strengthens our northern California presence, while providing new avenues for growth in technology and international services. Bridge Bank's exceptional funding profile and low cost of deposits provide the rare opportunity to improve our liquidity and margins simultaneously."

The acquisition transformed Western Alliance from a Southwest regional bank into a participant in the innovation economy. In 2015, Western Alliance acquired Bridge Bank as a key division of the top-performing national bank, focused on commercial, tech and innovation banking. In late 2025, Bridge Bank unified under the Western Alliance Bank brand.

Post-acquisition performance validated the thesis. Net income at the $14 billion-asset company grew 44.5% to $59.1 million, or 58 cents per share, from the same period last year. Net interest income rose 40.1%, to $137.4 million. Loans increased 35.7%, to $10.8 billion.

"A fundamental reason for our acquisition of Bridge Bank was the strength of its brand in the technology sector," said Robert Sarver. "During the past year, the strong performance of Bridge's technology and innovation banking division and expansion of its offerings has validated our decision."

But the Bridge acquisition also introduced concentration risk that would emerge dramatically during the 2023 crisis. Technology sector deposits were more volatile than traditional commercial deposits—they could grow explosively during boom times and evaporate rapidly during downturns. This was a feature, not a bug, during the long tech bull market from 2015 to 2021. It became an existential threat when the tech sector retreated and panic spread through regional bank stocks.

VI. The National Platform Build-Out (2016-2020)

Between 2016 and 2020, Western Alliance evolved from a regional bank with a tech division into a national platform with multiple specialized business lines. The company developed segments across Homeowners Association (HOA) Services, Hotel Franchise Finance, Public & Nonprofit Finance, Technology and Innovation, and other national business lines.

This specialization strategy reflected a deliberate competitive positioning. Rather than competing head-to-head with money center banks across all products and markets, Western Alliance built deep expertise in niches where relationship banking and specialized knowledge created defensible advantages.

The bank's philosophy became: "We have the capital, the product array, the sophistication of a larger bank but yet deliver those products and services on a personal basis like a smaller bank."

The Sarver era reached its formal conclusion in 2018. From 2002 to 2018 Sarver was the CEO of WAB. During his tenure, "Western Alliance would not be in the position it is today without the contributions of Robert Sarver. Robert's leadership and relationship with customers, colleagues, regulators and shareholders has driven our success and the growth of our service to communities and clients across the country."

Kenneth A. Vecchione was re-designated as Chief Executive Officer, Director of the Company effective April 1, 2018. Vecchione's background prepared him uniquely for the role. Credit card marketing giant MBNA Corp. promptly hired Vecchione in its finance department. Between 1998 and 2006, he rose to vice chairman and CFO at MBNA, staying through Bank of America's purchase of the firm for $35 billion.

Vecchione's next gig was CFO at private equity firm Apollo Global Management, and in 2006 Western Alliance asked him to join its board for his expertise in credit cards and payments. His experience at Apollo would prove particularly relevant—it was Apollo that would later sell AmeriHome to Western Alliance.

Business strategy is second nature to Vecchione. Growing up in Queens, New York, in the 1950s, his father was a truck driver-turned-entrepreneur who bought and sold retail operations, including dry cleaners, a liquor store, a car rental outlet and a messenger service. His mother paved the way for other women working at a local office-furniture store by first asking to work flexible hours, then negotiating to receive equal pay when she became the top salesperson at the store.

Under Vecchione, the bank began preparing infrastructure for the next phase of growth. The bank's leadership went through the strategic planning process and assessed its growth ambitions. At around $36 billion in assets, management decided they needed to start building the infrastructure needed for a $100 billion bank. This forward-looking investment in systems, compliance, and risk management would prove critical during the 2023 crisis.

VII. Inflection Point #2: The AmeriHome Mortgage Acquisition (2021)

In April 2021, Western Alliance completed its largest acquisition: the purchase of AmeriHome Mortgage for approximately $1.22 billion. Western Alliance announced it completed the acquisition of Aris Mortgage Holding Company, LLC, the parent company of AmeriHome Mortgage Company, LLC. Based on AmeriHome's closing balance sheet and a $275 million premium, total consideration is approximately $1.22 billion.

The deal represented a bold strategic pivot. AmeriHome brings a B2B approach to the mortgage ecosystem through its relationships with over 700 independent correspondent mortgage originator clients, including independent mortgage bankers, community and regional banks, and credit unions of all sizes. Based in Thousand Oaks, CA, AmeriHome is the nation's third largest correspondent mortgage acquirer, purchasing approximately $65 billion in conventional conforming and government insured originations during 2020.

The strategic logic was compelling. The transaction markedly increases the contribution from non-interest income sources. For a bank that had historically relied primarily on net interest income, diversifying into fee-based mortgage servicing provided counter-cyclical revenue streams—mortgage volumes tend to increase when interest rates fall, precisely when net interest margins compress.

When it acquired the company, Western Alliance said it expected the addition to be 30% accretive to its earnings by 2022, meaning its earnings with AmeriHome will be 30% larger than they would have been on a stand-alone basis. The bank also said AmeriHome should grow the bank's return on average tangible common equity by 5%.

The acquisition wasn't just about diversification—it was about deploying excess capital. Western Alliance's management team said the $1 billion to $1.5 billion of new loan growth per quarter is actually not dependent on AmeriHome—the bank was expecting to do that anyway. But AmeriHome provided a channel to purchase non-qualified and jumbo mortgages that the bank would retain on its balance sheet, boosting loan-to-deposit ratios back toward historical levels.

VIII. The 2023 Banking Crisis: Seventy-Two Hours That Almost Ended Everything

The Trigger

At 3 p.m. on Thursday, March 9, 2023, driving to a late-afternoon dental appointment, Western Alliance Bank CEO Ken Vecchione received a phone call from an investment banker alerting him to the news that SVB had just taken a $1.8 billion after-tax loss from selling mostly long-term investments including Treasury and mortgage bonds, without issuing any equity to cover the loss. The news jolted bankers across the country, with particular reverberations for firms like Western Alliance with technology industry-based depositors.

At 6 p.m., Vecchione, Western Alliance Chief Financial Officer Dale Gibbons and other top managers began an around-the-clock exchange of phone calls and texts tracking SVB's developments and weighing the Arizona bank's next moves. After a nearly sleepless night, Western Alliance executives learned SVB had failed to raise equity funds critically needed to offset the previous day's losses.

The Contagion

Western Alliance executives worried about market contagion and that their institution may also be hurt by investors and depositors, given its own exposure to the technology sector. About 13% of Western Alliance's deposits are tied to tech firms, through its Bay Area-based Bridge Bank brand.

While the failure of Silicon Valley Bank did create a contagion effect throughout other large regional banks—in the form of declining stock values and, in some cases, increased deposit outflows—research identifies only six banks acutely impacted by the crisis: SVB, Signature, First Republic, Pacific West Bank, Western Alliance Bank and Silvergate Bank.

The question confronting Vecchione and his team was stark: would Western Alliance's 13% tech exposure doom the bank, or was the company's broader diversification sufficient to weather the storm?

According to year-end financial disclosures from 2022, SVB and First Republic were the only banks in that cohort with unrealized losses and uninsured deposits meaningfully above industry averages. Western Alliance was slightly above the industry in both categories while the others only exceeded one of the two.

The Run

By Monday morning, the deluge had begun. Roughly $8 billion in deposits flowed out of Western Alliance on the Monday after SVB's Friday night failure, and another $1.5 billion left the bank that Tuesday. The bank's stock was in free fall. In three trading sessions, Western Alliance had lost nearly two-thirds of its market value.

The speed was unprecedented. Social media and mobile banking had compressed what might have taken weeks in prior bank runs into hours. Venture capital investors were coordinating on Twitter, urging portfolio companies to move funds. The panic was feeding on itself.

The Response

Western Alliance's crisis response unfolded with military precision—the product of years of preparation. Vecchione and Gibbons activated the bank's long-established contingency funding plan, moving significant collateral to the Federal Reserve Bank in order to receive an influx of emergency funding as a proactive measure. Western Alliance requested $25 billion in funds to arrive first thing Monday morning, more than double what bank leaders estimated they would need.

The bank borrowed $25 billion from the Federal Reserve Board after SVB and Signature failed, and although it had to weather an almost $7 billion loss of deposits, its deposit base stabilized at $46.7 billion by March 20.

For starters, leadership decided early on that any depositor who wanted to withdraw their money from Western Alliance would get it right away. The bank might try to persuade them to stay, Vecchione said, but he also understood this was a time when people were going to "shoot first and ask questions later" and that he couldn't necessarily reason with panicked depositors.

This was counterintuitive but strategically sound. By signaling unlimited liquidity, Western Alliance removed the primary motivation for a rational depositor to flee: the fear that waiting too long would mean not getting their money back.

Around noon on Monday, Western Alliance issued a press release with updated financial figures, and bank managers hit the phones. In the course of the day, Western Alliance contacted hundreds of corporate customers with at least $20 million in deposits, reassuring them of the bank's strong capital position.

At 2 p.m., Western Alliance issued a quickly produced 8-K detailing its expanded capital and liquidity status. Bank executives immediately sensed a positive shift in bank customers' moods. The firm's stock, which had bottomed out at about $7 a share earlier that day, rose to about $26 a share by day's end.

Finally, the bank approached its largest clients and offered them a look behind the scenes if they would sign non-disclosure agreements. "The mere fact that we went out and said, 'We'll tell you everything you want to know,' it made all the difference in the world," Vecchione said.

The Stabilization

By Friday, the worst was over. The Phoenix-based lender said in a filing that its net outflows have fallen sharply and returned to normalized levels by March 17. Deposit balances grew about $900 million to quarter end since March 30.

But rumors continued. On Wednesday, rumors began to circulate that Western Alliance was in trouble and seeking a buyer. At 7:30 a.m. Thursday, the Financial Times reported that Western Alliance was for sale. At 11 a.m., Western Alliance issued a statement denying the Financial Times story, calling it "categorically false," swiftly ending the rumors.

Why Western Alliance Survived When Others Didn't

The difference between Western Alliance and the banks that failed came down to several factors. First, diversification. Western Alliance has a more diverse deposit base and a broader range of commercial banking customers compared to Silicon Valley Bank, which relied heavily on early-stage tech and biotech depositors.

Second, unrealized losses were manageable relative to capital. While Western Alliance had paper losses on its securities portfolio—as did nearly every bank in the rising rate environment—these losses didn't threaten solvency.

Third, institutional memory and preparation. "Those folks that grew out of the great financial crisis or any other crisis, their bank had helped inform their decision-making," Vecchione noted. "That was very important, making sure we had people that could see the whole picture, understand strategically where we needed to go, and how tactically we needed to get there."

"The second rule was, any deals that were going to close that week, we closed them. We always thought we were going to be in business," Vecchione said. "Never once did I ever think that we were going to fail."

This confidence wasn't bravado—it was the product of years of preparation. What followed became a case study in how a bank's board and management team could work together through a fast-unfolding crisis and come out stronger on the other side. Western Alliance set the foundation for its crisis response about five years before the actual crisis happened.

IX. The Modern Era: Post-Crisis Transformation (2023-Present)

Western Alliance emerged from the 2023 crisis not just surviving but positioned for renewed growth. The experience validated both the bank's diversification strategy and its risk management infrastructure—and highlighted areas for improvement.

Financial Performance

Western Alliance reported earnings per share of $2.07 for Q2 2025, with net income reaching $237.8 million, a substantial 22.8% increase year-over-year. Net revenue totaled $845.9 million, while pre-provision net revenue grew 16.2% year-over-year to $331.2 million.

Loans held for investment increased by $1.2 billion to $55.9 billion, representing 6.7% year-over-year growth. Total deposits grew by $1.8 billion to $71.1 billion. The bank maintained strong capital ratios, with Common Equity Tier 1 at 11.2% and Tangible Common Equity at 7.2%. Tangible book value per share increased to $55.87, up 14.5% year-over-year, reflecting a 17.6% compound annual growth rate since year-end 2014.

Most recently, net interest income totaled $750.4 million in the third quarter 2025, an increase of $52.8 million, or 7.6%, from $697.6 million in the second quarter 2025. Net revenue totaled $938.2 million for the third quarter 2025, an increase of $92.3 million, or 10.9%, compared to $845.9 million for the second quarter 2025.

On November 24, 2025, Western Alliance Bank issued $400 million in 6.537% Fixed Rate Reset Subordinated Notes due in 2035. The proceeds from this issuance will be used for general corporate purposes, including growth support and securities management.

Brand Unification

A major post-crisis initiative has been the consolidation of the company's fragmented brand architecture. Western Alliance Bank today unveiled plans to unite all of the Bank's divisions under the Western Alliance Bank brand. By year-end, six division bank brands – Alliance Association Bank, Alliance Bank of Arizona, Bank of Nevada, Bridge Bank, First Independent Bank and Torrey Pines Bank – will take on the Western Alliance Bank name.

Originally focused on Western regional markets, the Bank has grown to include 17 national business lines today, with 57 offices and over 3500 employees located throughout the United States.

Bringing each brand under the Western Alliance name is an important milestone toward brand unity, said CEO Ken Vecchione. "By year-end, the markets we serve and the clients who are so important to us will know us as one strong bank, offering unmatched industry expertise and unparalleled, best-in-class service." In a separate statement, Vecchione said the bank has its sights set on becoming the next leading $100-billion-plus asset commercial bank in the U.S.

The company completed its brand unity initiative, consolidating its legacy division bank brands under a single unified name, Western Alliance Bank, as of October 4, 2025.

Geographic and Sector Expansion

Phoenix, Arizona-based Western Alliance is doubling down on middle-market companies in niches that have a heavy presence in California. Since Julian Parra, the lender's national head of commercial and industrial banking, joined the bank about a year ago, Western Alliance has added an aerospace and defense banker team, and a food and agriculture banker team, both based in California.

Western Alliance is also eyeing commercial expansion into other states through those industries. Parra flagged Texas and Florida as possibilities to scale in the food and agriculture sector; the Washington, D.C., area in aerospace and defense; and the southeastern U.S. for entertainment.

The lender has hired 12 new bankers in California since Parra joined last year, with the bulk of those hires focused on aerospace and defense or food and agriculture. "We could easily hire a similar number of bankers every year going forward for the next several years."

X. Playbook: Business & Investing Lessons

The Multi-Brand Regional Bank Model

Western Alliance's approach of operating full-service divisions with local identities while leveraging shared infrastructure represents a distinctive competitive strategy. For over a decade, the banking divisions operated under the same charter, providing commercial banking solutions while fostering strong relationships through personalized service.

Middle-market companies "get lost" at larger banks, while smaller lenders may not have the capabilities to stand out when it comes to people and service. Western Alliance, he argued, has the financial strength and capabilities of a large bank while remaining "small and nimble, in terms of the service that we can provide."

The bank's client "sweet spot" is companies generating between $20 million and $250 million in revenue, seeking traditional cash management products and loans, as well as foreign exchange, trade finance, and interest rate hedging capabilities.

Specialization as Competitive Advantage

Rather than competing across all segments, Western Alliance developed targeted national business lines. Western Alliance operates as a regional bank with a strategic focus on diversification across high-growth market segments. This approach has allowed the bank to develop multiple revenue streams that complement each other during varying market conditions.

The Innovation Banking Group, HOA Services, Hotel Franchise Finance, Public & Nonprofit Finance, Aerospace & Defense, and Juris Banking Group represent deep vertical expertise that creates switching costs and competitive moats.

Acquisition as Growth Engine

Western Alliance has executed four significant acquisitions with an average deal size around $415 million. The integration philosophy has consistently been to preserve brands and local relationships while leveraging shared services. This approach minimizes customer disruption while extracting cost synergies from back-office consolidation.

The Bridge Bank acquisition brought technology expertise; AmeriHome added mortgage servicing capabilities and fee income diversification. Each acquisition has been transformative rather than merely additive.

Crisis Management Excellence

Western Alliance set the foundation for its crisis response about five years before the actual crisis happened. That's when the bank's leadership went through the strategic planning process and assessed its growth ambitions. At around $36 billion in assets, management decided they needed to start building the infrastructure needed for a $100 billion bank.

The lessons for other financial institutions are clear: crisis management capability cannot be built during a crisis. It must be developed years in advance through scenario planning, infrastructure investment, and talent development.

"The Silicon Valley Bank crisis was rough, but the 2008 economic downturn was far worse, and you learn strategies to survive," Vecchione said. "What we learned in March 2023 was how to do it all faster."

XI. Porter's Five Forces Analysis

1. Competitive Rivalry: HIGH

In the massive California market, Western Alliance faces no shortage of competitors also targeting commercial lending, from banks based in the state such as Banc of California and Five Star Bank, to bigger names such as JPMorgan Chase and U.S. Bank, which have expanded their presence in California through acquisitions, and even regionals such as Citizens that have made recent hires to chase middle-market business in the state.

The regional banking sector features intense competition across multiple dimensions: deposit pricing, loan terms, product breadth, and relationship quality. Western Alliance's response has been to compete on specialization and service rather than price, targeting niches where deep expertise creates sustainable advantage.

2. Threat of New Entrants: MODERATE

New bank charters face significant regulatory barriers including capital requirements, charter approval processes, and extensive compliance costs. The 2023 crisis further tightened regulatory scrutiny on regional banks, raising the bar for new entrants.

However, fintech companies represent a genuine competitive threat in specific segments—particularly payments, small business lending, and consumer deposits. Western Alliance has responded by developing its own digital capabilities while maintaining relationship-driven commercial banking as its core.

3. Bargaining Power of Suppliers (Depositors): MODERATE-HIGH

The 2023 crisis demonstrated starkly how quickly deposits can flee. In a rising rate environment, competition for deposits intensifies as customers seek higher yields on their cash balances. Western Alliance's ECR-related deposit costs have been a notable expense line as the bank pays to retain commercial deposits.

The bank's deposit mix remains a critical strategic priority. As of early May 2023, more than 74% of total deposits were insured—up significantly from pre-crisis levels as the bank worked to reduce its exposure to uninsured deposit flight risk.

4. Bargaining Power of Customers (Borrowers): MODERATE

Commercial borrowers have multiple financing options but value relationship continuity, industry expertise, and execution speed. Western Alliance's specialization strategy creates switching costs—a hotel franchise finance client benefits from the bank's accumulated expertise in that sector and may be reluctant to educate a new lender.

5. Threat of Substitutes: MODERATE

Private credit, direct lending funds, and non-bank lenders represent genuine substitutes for commercial loans. The growth of private credit markets has created new competition for the middle-market loans that represent Western Alliance's core business.

XII. Hamilton Helmer's 7 Powers Framework

Scale Economies

Western Alliance benefits from moderate scale economies in its shared services infrastructure—compliance, technology, and risk management capabilities that serve all business lines. The brand unification initiative further enhances these economies by reducing complexity and enabling more efficient operations.

Network Effects

Limited direct network effects characterize traditional commercial banking. However, the bank's specialized business lines benefit from reputation effects and relationship networks within their target industries.

Counter-Positioning

Western Alliance's counter-positioning against money center banks centers on the proposition that middle-market companies receive inferior service from megabanks. As Parra articulated, these companies "get lost" at larger institutions. Western Alliance offers comparable capabilities with personalized attention.

Switching Costs

Commercial banking relationships feature meaningful switching costs. Treasury management integration, lending facilities, and relationship knowledge create friction that protects existing customer relationships. The bank's industry specialization amplifies these switching costs by adding domain expertise to the relationship.

Branding

The brand unification initiative represents a significant investment in building a coherent national brand. While regional brands like Torrey Pines and Bridge Bank carried local equity, the fragmented brand architecture limited national marketing efficiency and cross-selling opportunities.

Cornered Resource

The bank's specialized banking teams—particularly in areas like HOA services, hotel franchise finance, and legal industry services—represent accumulated expertise that competitors cannot easily replicate. The talent assembled over decades constitutes a valuable and difficult-to-reproduce resource.

Process Power

Crisis management capability represents genuine process power. Western Alliance's ability to execute a coordinated response during March 2023—borrowing $25 billion from the Fed, communicating with hundreds of major depositors, issuing regulatory filings within hours—reflected organizational capabilities developed over years. This process power is difficult to replicate through hiring or imitation.

XIII. Key Performance Indicators for Ongoing Monitoring

For investors tracking Western Alliance's ongoing performance, three metrics deserve particular attention:

1. Deposit Growth and Composition

Total deposits and the mix between insured and uninsured deposits remain the single most important indicators of franchise stability. The 2023 crisis demonstrated that deposit stability is foundational—without it, nothing else matters. Investors should monitor: - Quarter-over-quarter deposit growth - Percentage of deposits that are FDIC-insured - Cost of deposits (ECR and interest expense) - Deposit concentration by customer segment

2. Net Interest Margin

As a commercial lender, Western Alliance's profitability depends heavily on the spread between asset yields and liability costs. Net interest margin captures this spread. The bank's NIM has remained around 3.53% in recent quarters. Investors should watch for: - Trends in loan yields versus funding costs - Asset-liability duration matching - Sensitivity to interest rate changes

3. Tangible Book Value Per Share Growth

Tangible book value per share increased to $55.87, up 14.5% year-over-year, reflecting a 17.6% compound annual growth rate since year-end 2014. This metric captures the bank's compounding of economic value per share over time—the true measure of long-term shareholder value creation in banking.

XIV. Regulatory and Risk Considerations

Large Financial Institution Threshold

The bank reported significant year-over-year growth in key metrics while continuing to build momentum toward crossing the $100 billion Large Financial Institution threshold. The bank continues to prepare for crossing the Large Financial Institution threshold, which will bring additional regulatory requirements but also new opportunities for growth and market expansion.

Crossing the $100 billion threshold triggers enhanced prudential standards including stress testing requirements, liquidity requirements, and heightened supervisory expectations. Management has indicated they are investing proactively in infrastructure to meet these requirements.

Credit Quality

The Company recorded a provision for credit losses of $80.0 million in the third quarter 2025, an increase of $40.1 million from $39.9 million in the second quarter 2025, and an increase of $46.4 million from $33.6 million in the third quarter 2024.

Higher provisions reflect both loan growth and a potentially more cautious outlook on credit quality. Investors should monitor net charge-offs and non-performing loan trends closely, particularly in commercial real estate exposures.

Commercial Real Estate Exposure

Regional banks with CRE concentrations face heightened scrutiny from regulators and investors alike, given concerns about office property valuations and refinancing challenges in a higher interest rate environment. Western Alliance's CRE book requires ongoing monitoring.

XV. Conclusion: The Phoenix Rises Again

Western Alliance Bancorporation has survived two existential crises—the 2008 financial collapse that devastated its Southwest markets and the 2023 banking panic that claimed three major regional banks. Both times, the company emerged stronger than before.

The secret to Western Alliance's resilience isn't complicated: conservative credit culture, diversified revenue streams, deep liquidity planning, and institutional memory of past crises. These aren't glamorous competitive advantages. They don't generate viral tweets or conference presentations. But they keep a bank alive when panic sweeps through the financial system.

Looking forward, Western Alliance faces both opportunities and challenges. The $100 billion threshold brings enhanced regulation but also market perception as a more substantial institution. The brand unification creates marketing efficiencies but may dilute local brand equity. The California expansion deepens the bank's presence in a major market but introduces new competitive dynamics.

With more than $90 billion in assets, Western Alliance Bancorporation is one of the country's top-performing banking companies. Through its primary subsidiary, Western Alliance Bank, Member FDIC, clients benefit from a full spectrum of tailored commercial banking solutions and consumer products.

For Ken Vecchione and his team, the lessons of March 2023 remain fresh. The dentist's chair where he sat, numb from news rather than novocaine, reminds him that banking crises can emerge with terrifying speed. But the bank's survival—its stock recovering from $7 to the $80s—also demonstrates that preparation, transparency, and decisive action can overcome even the most severe market panic.

The phoenix, after all, doesn't just survive the fire. It emerges more powerful than before.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube