Webster Financial: From Depression-Era Thrift to Northeast Banking Powerhouse

I. Introduction & Episode Roadmap

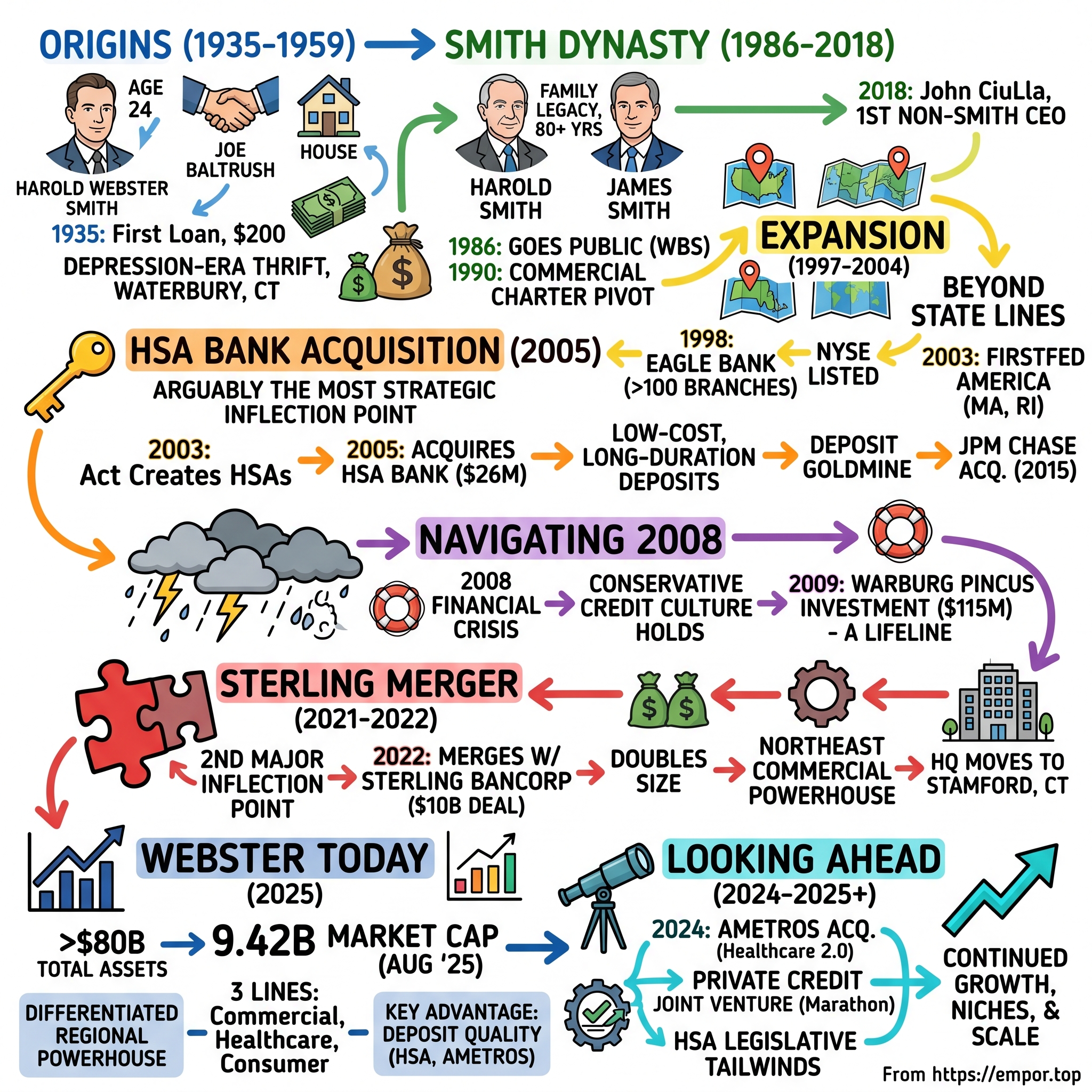

On a December morning in 1935, a young man stood on the steps of a modest home at 114 Chambers Street in Waterbury, Connecticut. Harold Webster Smith, just 24 years old, was about to deliver the first loan in the history of First Federal Savings and Loan Association of Waterbury—$200 to Joe Baltrush to help him build a home amid the wreckage of the Great Depression. The photograph of that handshake, preserved in Webster Bank's archives, captures something essential: a banker who believed that the path to prosperity runs through helping ordinary people achieve their financial goals.

Founded in 1935 and headquartered in Stamford, CT, Webster is a values-driven organization with more than $80 billion in total assets. Webster Bank is a commercial bank that provides a wide range of financial products and services to businesses, individuals, and families across three differentiated lines of business: Commercial Banking, Healthcare Financial Services, and Consumer Banking.

The central question of Webster's story is both simple and profound: How did a $25,000 savings and loan, started with borrowed money from friends and family, transform into one of the largest commercial banks in the Northeast, with a market capitalization approaching $10 billion?

The answer reveals a masterclass in patient capital, niche specialization, and transformational M&A—lessons that resonate far beyond banking. Webster Financial market cap as of August 2025 is $9.42B.

Several themes thread through Webster's nine-decade journey. First is the power of family legacy: the Smith dynasty—father Harold and son James—guided the bank for over 80 years combined, providing the kind of continuity that enabled long-term thinking over quarter-by-quarter management. Second is the genius of strategic pivots: Webster's 2005 acquisition of HSA Bank, a tiny Wisconsin health savings account custodian, would prove to be perhaps the most prescient acquisition in modern regional banking history, creating a deposit franchise that competitors still envy two decades later. Third is the importance of transformational M&A: the 2022 merger with Sterling Bancorp didn't just double Webster's size—it fundamentally repositioned the bank as a major Northeast commercial banking platform.

This story matters for anyone trying to understand regional banking consolidation in America. Webster isn't just a Connecticut bank that got bigger. It represents a different model—one built on specialized deposit verticals, conservative credit culture, and the patient accumulation of competitive advantages that compound over decades.

II. The Founding Story: Depression-Era Origins (1935–1959)

Harold Webster Smith's Vision

The late Harold W. Smith was just 24 years old when he took a chance at starting a bank in 1935, as the Great Depression was painfully afoot. The timing could not have been worse—or, as it turned out, more fortuitous. With unemployment still above 20% and trust in financial institutions at rock bottom following the wave of bank failures that had accompanied the crash, Smith saw something others missed: a vacuum that could be filled by a different kind of banking.

Mr. Smith founded First Federal Savings of Waterbury at age 24 in 1935 and was its sole employee for the bank's first year. He was the epitome of the conservative, hardworking, hometown banker whose handshake was as good as any contract.

The National Housing Act of 1934 had created the framework for a new breed of institution: federally chartered savings and loans designed to channel deposits into home mortgages. Smith, a Dartmouth graduate and former Navy man, recognized this as an opportunity to build something meaningful. Founder Harold Webster Smith opened First Federal Savings and Loan Association of Waterbury in Connecticut with $25,000 from friends and family to help people build and buy homes during the Great Depression.

Smith's background shaped his approach to banking. He graduated from Crosby High School, attended Deerfield Academy and was a cum laude graduate of Dartmouth College in 1933, where he was captain tennis team and a standout intercollegiate swimmer. He was both athlete and intellectual, competitive but disciplined—traits that would define First Federal's culture for decades.

First Federal was the first bank in Connecticut to issue GI loans and the first to make Federal Housing Administration (FHA) home improvement loans in the Waterbury area. This willingness to pioneer new products while maintaining conservative underwriting became a hallmark of the institution. Operations centered on attracting deposits through competitive savings rates and issuing home loans to working-class families, helping to rebuild trust in financial institutions. By 1938, the thrift had achieved a significant milestone, growing its assets to over $1 million.

The Slow-and-Steady Model

What's remarkable about First Federal's early history isn't its growth rate—it's the deliberate pace of that growth. The bank didn't open its first branch until 1959 when it had $50 million in assets. Its first branch outside of Waterbury opened in 1959 in Watertown and a second opened 10 years later.

This was not the expansion model of an institution in a hurry. Over 24 years, First Federal had grown from $25,000 to $50 million—a compound annual growth rate of roughly 30%—before opening a single branch. The focus was singular: serve Waterbury, build relationships, make good loans, gather deposits.

The thrift model that Smith practiced was patient capital in its purest form. Unlike commercial banks that relied on demand deposits and short-term lending, savings and loans gathered long-term savings deposits and matched them with long-term mortgages. The business model was simple: pay depositors a fair rate, charge borrowers a slightly higher rate, operate conservatively, and compound the difference over decades.

After Harold Smith died in 1997, the Webster banking family ran an advertisement asking what someone who started a bank during depression should be called. "Some people might say it's crazy to start a bank in a depression," the younger Smith said.

But crazy it was not. Harold Webster Smith understood something fundamental: financial crises create opportunities for those with courage, capital, and a long-term view. First Federal emerged from the Depression not just surviving but thriving, with a culture of conservatism that would serve it well through every subsequent crisis.

III. The Smith Dynasty: Father to Son Transition (1986–2018)

Going Public and Charter Conversion

By the mid-1980s, the banking landscape was changing rapidly. Deregulation was reshaping competitive dynamics, and Connecticut's banking industry was consolidating. In 1986, First Federal underwent a structural transformation by converting to stock ownership and establishing Webster Financial Corporation as its holding company, named after Smith's middle name to honor his foundational role. This shift positioned the institution for greater capital access and strategic flexibility amid evolving regulatory and competitive landscapes in the savings and loan industry.

In 1986, he and his father realized First Federal needed to place itself in an optimum capital position to take advantage of any expansion opportunities the state's rapidly changing banking landscape might yield in the future. Smith succeeded his father as CEO in 1986, a year after the bank went public.

The decision to go public was transformational. It gave First Federal access to public market capital for acquisitions, provided liquidity for the Smith family's ownership stake, and professionalized the institution's governance. The new holding company was named Webster Financial Corporation—using Harold's middle name—as a tribute to the founder who had built the institution from nothing.

A year later, in 1987, Harold Smith retired as CEO, after having managed the bank's day-to-day operations for 52 years. That tenure is almost incomprehensible by modern standards—52 years as chief executive of a single institution. "The average CEO these days lasts three years. It's phenomenal," one director noted.

Transformation to Commercial Bank

After having operated as a thrift for its first 55 years, First Federal converted its charter to that of a commercial bank in 1990. This was a crucial strategic pivot. The savings and loan crisis of the late 1980s had devastated the thrift industry; by converting to a commercial bank charter, Webster could offer a full suite of business banking services while maintaining its consumer mortgage franchise.

He served as CEO until 1987 and as chairman of the board until 1995 when First Federal was renamed Webster Bank in his honor. 1987: James C. Smith became the company's second chief executive officer, succeeding his father, Harold Webster Smith, who continued as chairman.

James C. Smith had spent four years at a brokerage firm before joining the family bank, bringing a broader perspective on financial services. Both father and son grew up in Waterbury and attended public schools there before heading to Deerfield Academy, a four-year, college preparatory school in Massachusetts and then on to Dartmouth College.

Under James Smith's leadership, Webster transformed from a single-state thrift to a regional commercial banking powerhouse. Webster grew to be the largest commercial bank headquartered in New England under James C. Smith's leadership through 15 strategic acquisitions of other banks and branches.

"Mission's evolve. Today, our mission is to help people achieve their financial goals," Smith said. "Instead of just trying to be the best bank in the neighborhood, you try to be the best bank in Southern New England."

The Third Leadership Generation

By 2018, after more than three decades of Smith family leadership under James, succession planning became paramount. Smith retired as Webster Bank's chief executive in 2018, part of a succession plan that installed John Ciulla as CEO. Ciulla also will now take on the duties of chairman.

John Ciulla represented the first non-Smith CEO in the bank's history—a significant moment for an institution so closely associated with its founding family. John joined Webster in 2004 as senior vice president for Middle Market Banking and has held several executive management positions with increasing responsibility, including Chief Credit Risk Officer from 2008 to 2010.

Prior to joining Webster, John was with The Bank of New York, having last served as managing director. He practiced law in New York as an associate with McDermott Will & Emery and Hughes Hubbard & Reed.

Ciulla's background—legal training, Bank of New York pedigree, experience navigating the 2008 crisis as Chief Credit Risk Officer—made him ideally suited to lead Webster through its next phase of growth. Webster Financial Corporation is led by John R. Ciulla as Chairman and Chief Executive Officer, a position he has held since 2018, with his role as Chairman commencing in February 2024. Ciulla also serves as President and CEO of Webster Bank, guiding the organization's strategic initiatives in commercial banking and community-focused services.

For investors, the Smith-to-Ciulla transition represented a classic case of successful family business succession: a founder who built the foundation, a son who professionalized and scaled the enterprise, and a hand-picked successor who could take it to the next level without losing the culture that made it special.

IV. The Expansion Era: Building Scale Through Acquisitions (1997–2004)

In-State Consolidation

The late 1990s marked a new chapter for Webster. Having converted to a commercial bank charter and established its holding company structure, the institution was ready to grow aggressively through acquisition.

1997: Webster Trust Company, N.A. and Investment Services were added to the bank's offerings. 1998: Webster acquired Eagle Bank of Bristol, pushing its statewide branch total over 100. 1998: Webster became the first bank in Connecticut to purchase an insurance agency (Damman Insurance).

These acquisitions reveal a deliberate strategy: build scale through in-state consolidation while diversifying revenue streams into adjacent businesses like insurance and wealth management. The Eagle Bank acquisition was particularly significant—pushing past 100 branches signaled that Webster had emerged as a true statewide competitor.

2002: Webster became listed on the New York Stock Exchange under the ticker symbol "WBS". Moving from NASDAQ to the NYSE was both symbolic and practical—it increased visibility with institutional investors and provided access to a broader investor base.

Breaking Beyond State Lines

2003: Webster announced a definitive agreement to acquire FIRSTFED AMERICA BANCORP, INC., the holding company for First Federal Savings Bank of America. The deal, which closed in May 2004, marked Webster's first retail expansion beyond Connecticut's borders and into the southeastern Massachusetts and Rhode Island markets.

Webster crossed state lines for the first time in late 2003 when it announced the $465 million acquisition of Swansea, Mass.-based First Federal Savings Bank of America, which had 19 branches in Massachusetts and seven in Rhode Island. A few months later, in May 2004, it opened a new branch in Scarsdale, N.Y., its first foray into neighboring Westchester County.

The FIRSTFED acquisition was strategically significant. By expanding into southeastern Massachusetts and Rhode Island, Webster was building a contiguous New England footprint while entering the economically affluent greater Boston market. The Westchester County expansion, meanwhile, positioned Webster in one of the wealthiest suburban markets in America—a beachhead for future New York expansion.

2004: Webster announced that the Office of the Comptroller of the Currency (OCC) had accepted the company's application to be a chartered commercial bank.

By 2004, Webster had transformed from a Connecticut thrift into a regional New England commercial bank with a foothold in the New York metropolitan area. The foundation was laid for what would prove to be the bank's most important strategic move: the acquisition of a tiny Wisconsin health savings account custodian that would fundamentally reshape Webster's competitive positioning.

V. The HSA Bank Acquisition: The Genius Move (2005)

This is arguably the most strategically significant inflection point in Webster's modern history

Background: The Birth of HSAs

To understand why the HSA Bank acquisition was so brilliant, you need to understand the regulatory landscape of early 2000s healthcare. The Medicare Prescription Drug, Improvement and Modernization Act of 2003 created a new tax-advantaged savings vehicle: Health Savings Accounts. Unlike their predecessor Medical Savings Accounts (MSAs), HSAs were available to a much broader population—anyone enrolled in a high-deductible health plan.

Health savings accounts were first marketed in 2004 and offer consumers a tax-advantaged way to pay and save for current and future medical expenses. Besides being pre-tax, contributions to an HSA are fully portable and can remain in the account and grow until withdrawn.

HSA Bank began as the State Bank of Howards Grove, which opened in January 1913 in northern Sheboygan County. This rural, community bank would become HSA Bank decades later. In 1997, State Bank of Howards Grove entered the consumer-driven healthcare market by providing MSAs.

In rural Wisconsin, a small community bank had been positioning itself for this moment. After the advent of health savings accounts in 2004, MSA Bank redirected its energy and resources on HSAs and changed its name to HSA Bank. In March 2005, HSA Bank officially became a division of Webster Bank, N.A., Member FDIC, a subsidiary of Webster Financial Corporation.

The Acquisition Story

Webster Financial Corporation, the holding company for Webster Bank, N.A., announced the completion of its acquisition of Eastern Wisconsin Bancshares, Inc., the holding company of State Bank of Howards Grove, which operates under the trade name HSA Bank. As previously announced, Webster will divest State Bank's retail branches and related loans and deposits to National Exchange Bank and Trust and will retain the bank's HSA operation and HSA deposits.

The purchase price is approximately $26 million in cash.

Twenty-six million dollars. For that modest sum, Webster acquired what would become one of the most valuable deposit franchises in American banking. The structure of the deal was clever: Webster kept the HSA business and sold the community banking branches, ensuring the acquisition was purely about the HSA platform.

Why This Was Brilliant

"The completion of our acquisition of HSA Bank represents a major deposit gathering opportunity, a key strategic objective. As the largest bank provider of health savings accounts in the country, HSA Bank has strong growth potential as employers increasingly turn to consumer-driven health plans to address the escalating problem of health care costs."

"Account volume doubled in 2004, and in January 2005 alone, more than 16,000 new accounts were opened. Since the announcement of our acquisition in September, deposits have increased 64% to more than $155.4 million."

The growth trajectory was remarkable. But what made HSA deposits truly special wasn't just their growth rate—it was their quality as a funding source.

The Deposit Goldmine

"They are the lowest-cost and least rate-sensitive and have the longest liability profile," says Massiani. In addition, as medical prices continue to rise year after year, the amount of money HSA savers want to put aside to protect themselves rises.

"They are the longest-duration deposits that we have in our book of business." By that, Massiani means decades. These accounts are the opposite of hot money.

Consider what this means from a bank's perspective. Traditional deposits—checking accounts, savings accounts, even CDs—are rate-sensitive and can flee to competitors offering higher rates. HSA deposits are fundamentally different: they're tied to long-term healthcare savings, grow automatically through payroll deduction, and stay with the account holder for decades.

"If you're somebody who is in good financial health and in good personal health, the best thing you can do is take advantage of these deposit products and the investment products we also provide," says Massiani.

Continued Dominance

Today Webster is the largest bank HSA administrator and depository, thanks both to growth and acquisitions, including the 2015 acquisition of the HSA business at JPMorgan Chase.

The deal will bring approximately 700,000 accounts, including an estimated $1.3 billion in deposits and $175 million in investments, from JPMorgan Chase to HSA Bank, a Wisconsin-based health savings account administrator that Webster acquired in 2005.

When JPMorgan Chase—the largest bank in America—decided to exit the HSA business, they chose Webster as the buyer. That speaks volumes about Webster's platform capabilities and market position.

This commitment to leadership has propelled us to become one of the nation's largest providers of Health Savings Accounts (HSAs) with $7 billion in assets under administration.

From $26 million to $7 billion in assets under administration. The HSA Bank acquisition stands as one of the most successful strategic moves in regional banking history—a case study in identifying an underserved market before anyone else recognized its potential.

VI. Navigating the 2008 Financial Crisis

The Storm Hits Regional Banks

The 2008 financial crisis, also known as the global financial crisis (GFC) or the Panic of 2008, was a major worldwide financial crisis centered in the United States. The causes included excessive speculation on property values by both homeowners and financial institutions, leading to the 2000s United States housing bubble.

The 2008 financial crisis led to many bank failures in the United States. The Federal Deposit Insurance Corporation (FDIC) closed 465 failed banks from 2008 to 2012. In contrast, in the five years prior to 2008, only 10 banks failed.

For a Connecticut-based bank with significant mortgage exposure, the crisis posed existential questions. Would Webster's conservative credit culture hold? Would the HSA deposit franchise prove as stable as anticipated?

Warburg Pincus Investment: The Lifeline

In 2009, Warburg Pincus invested in Webster. Warburg Pincus worked extensively with the management team to de-risk the bank's loan portfolio, stabilize the bank's funding, and retool and grow the retail banking and asset management divisions.

Webster Financial Corporation today announced that Warburg Pincus, the global private equity firm, has agreed to invest $115 million in Webster through a direct purchase of newly issued common stock at $10 per share, junior non-voting preferred stock, and warrants.

The Warburg Pincus investment was a vote of confidence from one of the world's most sophisticated private equity investors. In announcing the investment, Webster Chairman and Chief Executive Officer James C. Smith said, "Warburg Pincus investment further strengthens Webster's capital base which already significantly exceeded regulatory requirements for well-capitalized banks."

"The additional capital will enable us to capitalize on the extraordinary banking opportunities in the market as we pursue our vision to be New England's bank." "Webster's ability to attract a long-term value investor of Warburg Pincus caliber and experience in the banking sector underscores the inherent strength of our core business and long-term strategy."

Lessons from the Crisis

The 2008 crisis validated Webster's conservative culture in two crucial ways. First, the HSA deposit franchise proved remarkably stable—these were not "hot money" deposits that fled at the first sign of trouble. Second, the bank's Connecticut thrift origins had instilled a conservative credit culture that limited exposure to the toxic assets that destroyed so many competitors.

Warburg Pincus's due diligence process was rigorous. They reviewed dozens of bank recapitalization opportunities before selecting Webster as one of only three U.S. banks to receive their investment. The criteria: strong market share, manageable balance sheet risk, top-tier management, and attractive acquisition opportunities. Webster checked every box.

VII. The Post-Crisis Build: Strategic Positioning (2010–2020)

Citibank Branch Acquisition

2016: Webster acquired 17 Citibank branches in the Boston area and added additional ATMs to support the network.

When Citigroup decided to exit retail banking in certain markets, Webster pounced. The acquisition of 17 branches in the Boston area significantly expanded Webster's presence in the economically dynamic greater Boston market. This wasn't just about branch count—it was about customer relationships and deposits that would fund future loan growth.

HSA Bank Dominance

Through the post-crisis period, Webster continued to invest heavily in its healthcare financial services franchise. Today, HSA Bank is recognized as a pioneer in Consumer-Directed Health (CDH) accounts and an experienced administrator of many types of health accounts and more, including accounts such as Health Savings Accounts (HSAs), Health Reimbursement Arrangements (HRAs), Flexible Spending Accounts (FSAs), and Commuter Benefits.

The expansion from HSAs into adjacent products—FSAs, HRAs, commuter benefits—demonstrated Webster's ability to leverage its healthcare financial services platform across multiple product lines. Each new product added deposits and diversified revenue streams.

By the late 2010s, Webster had established itself as the clear leader in health account administration. But leadership understood that to compete in the increasingly consolidated Northeast banking market, the bank needed transformational scale. That opportunity would come in the form of Sterling Bancorp.

VIII. The Sterling Merger: Transformational M&A (2021–2022)

The second major inflection point of the modern era

The Deal

In April 2021, Webster Bank and Sterling Bancorp's Sterling National Bank agreed to an all stock merger in an all-stock deal worth about $10.3 billion. The merger was completed on February 1, 2022 and will keep the name Webster Bank.

Webster Financial Corporation and Sterling Bancorp jointly announced today the completion of their previously announced merger, creating one of the largest commercial banks in the Northeast.

But the biggest milestone in Webster Bank's long history came in 2022, when it acquired Sterling Bancorp for $10 billion. With the purchase of Sterling Bancorp, Webster virtually doubled in size, becoming one of the largest commercial banks.

What Sterling Brought

As CEO and President of the previous Sterling Bancorp, his vision of growing Sterling Bancorp into a regional bank by becoming a leader in delivering superior service to owner-led businesses and families has yielded strong operating results. The company has grown from $3.2 billion in assets in 2011 to $32 billion in assets in 2020.

Headquartered in Montebello, New York, Sterling Bancorp's shares were traded on the New York Stock Exchange. The bank was founded in 1888 under the name Provident Bank.

Sterling brought something Webster needed: deep commercial banking expertise in the New York metropolitan market. The deal creates one of the largest commercial banks in the Northeast and extends Webster Bank's presence in New York to include Long Island and the Hudson River Valley.

The Combined Entity

The merged institution now operates 202 financial centers and had $65 billion in assets, $44 billion in loans, and $53 billion in deposits based on balances as of December.

The combined company is a unique financial institution, with a differentiated funding base that includes HSA Bank, as well as consumer and commercial banking businesses. Webster has a broad range of regional and national asset generation capabilities, particularly through its growing commercial banking business with deep industry expertise and an expanded geographic footprint.

The Strategic Rationale

The merger created something genuinely differentiated in Northeast banking. Webster brought the HSA franchise—the lowest-cost, longest-duration deposits in the industry. Sterling brought commercial banking expertise and New York market presence. Together, they could fund commercial loans with stable healthcare deposits, generating spreads that traditional banks couldn't match.

"Today marks a transformative moment in Webster's history that will greatly benefit our colleagues, clients, communities and shareholders," said John Ciulla. "Our bank will have enhanced scale, significant loan growth potential, best-in-class deposit franchises and a longstanding commitment to community development and corporate citizenship."

Cultural Integration

Jack Kopnisky, who had been chief executive officer of Sterling Bancorp, is now the executive chairman of Webster Financial's board of directors.

But with the arrival of the merger, the bank headquarters has relocated from Waterbury to Stamford. Webster officials have said Waterbury will be part of what they call "a multi-campus presence" where some executives will still be based.

The move from Waterbury to Stamford was symbolically significant. Waterbury—Harold Webster Smith's hometown, where the bank had been headquartered for 87 years—gave way to Stamford, closer to New York City and the commercial banking opportunities the combined entity would pursue. It marked Webster's evolution from a Connecticut community bank to a major Northeast commercial banking platform.

IX. The Ametros Acquisition: Healthcare Financial Services 2.0 (2024)

Doubling Down on Healthcare

Webster Financial Corporation today announced that its principal bank subsidiary Webster Bank, N.A. has completed the acquisition of Ametros Financial Corp ("Ametros"). The business will continue to operate under the Ametros and CareGuard brands following the acquisition. Ametros, the nation's largest professional administrator of medical insurance claim settlements, helps individuals manage their ongoing medical care through their CareGuard service and proprietary technology platform.

Webster will acquire Ametros for $350 million in cash, subject to customary adjustments.

The Ametros acquisition was vintage Webster: identifying a specialized deposit vertical with favorable characteristics and acquiring the market leader. Just as HSA Bank dominated health savings accounts, Ametros dominated medical insurance claim settlement administration.

Strategic Fit

The acquisition of Ametros provides Webster a fast-growing source of low-cost and long-duration deposits, further diversifying Webster's deposits as well as noninterest income. Its operations will be fully integrated into Webster during the first quarter of 2024.

As of December 2023, Ametros has over 24,000 members and $804 million in deposits under custody, which will become deposits of Webster following the closing of the transaction; deposits under custody have more than doubled over the past three years and the average deposit balance per account was $33,000. Ametros' deposit characteristics provide a unique value to Webster: Average cost of less than 10 basis points with near-zero beta.

Deposits are projected to grow at a five-year CAGR of approximately 25%.

The deposit characteristics were remarkable: less than 10 basis points cost, near-zero beta (meaning the deposits are insensitive to interest rate changes), and projected 25% annual growth. This was essentially the HSA Bank playbook applied to a new vertical.

"This acquisition closely aligns with our strategic focus on building a diverse and unique funding base," said John Ciulla, President and Chief Executive Officer of Webster Financial Corporation. "Ametros' market position and value proposition for its clients and partners underpin a robust growth trajectory for this highly complementary business."

X. Webster Today: Current State of the Business (2025)

Financial Performance

Webster Financial Corporation reported strong Q2 2025 financial results with net income of $251.7 million, or $1.52 per diluted share, up from $175.5 million ($1.03/share) in Q2 2024. The bank achieved revenue of $715.8 million and maintained solid growth with loans reaching $53.7 billion (up 1.2% QoQ) and deposits of $66.3 billion (up 1.1% QoQ).

Our results were solid with a return on tangible common equity of 18%, ROAA of nearly 1.3% and growth in both loans and deposits of over 1% linked quarter. Overall, revenue grew 1.6% over the prior quarter.

Capital levels remained strong, with Common Equity Tier 1 (CET1) at 11.33% and tangible common equity at 7.46%. Tangible book value per share increased by 3.4% to $35.13 compared to the previous quarter and was up 14.0% year-over-year.

These metrics reveal a well-run regional bank: 18% return on tangible common equity places Webster among the best performers in its peer group; the 1.3% return on assets demonstrates efficient capital deployment; and the strong capital ratios provide buffer for economic uncertainty.

Business Lines

The company's differentiated lines of business include Commercial Banking, Healthcare Financial Services and Consumer Banking. Webster's Commercial Banking and Consumer Banking lines deliver solutions nationally and regionally to companies, investors, government entities, other public and private institutions as well as families, private clients and small business owners. Its Healthcare Financial Services business helps millions of clients nationwide manage complex healthcare financial needs.

The company's deposit profile spans multiple business lines, including Consumer Bank/brio direct (42% of total deposits), Commercial Bank (24%), HSA Bank (14%), interSYNC (13%), Corporate (5%), and Ametros (2%).

The deposit diversification is striking. Nearly 30% of deposits come from specialized verticals (HSA Bank, interSYNC, Ametros)—funding sources that competitors cannot easily replicate.

Footprint

Webster Bank is an American commercial bank based in Stamford, Connecticut. It has 177 branches and 316 ATMs located in Connecticut; Massachusetts; Rhode Island; New Jersey; Westchester, Orange, Ulster, and Rockland counties in New York as well as New York City.

With this diversified portfolio, we are a national financial services company with $83.2 billion in assets and one of the largest, publicly-traded commercial banks in the United States.

XI. Playbook: Business & Strategy Lessons

Key Takeaways for Entrepreneurs and Investors

1. Patient Capital Pays Off

Harold Webster Smith's 52-year tenure as CEO demonstrates the power of long-term thinking. In an era of short-term quarterly earnings pressure, Webster's multi-generational leadership enabled decisions that would take decades to compound—like the slow, deliberate build of deposit market share in Connecticut before any geographic expansion.

2. Niche Dominance Creates Moats

The HSA Bank acquisition exemplifies the power of finding an underserved market early. Webster didn't just enter the HSA market—it became the dominant player, creating switching costs and scale advantages that protect its position today. The same playbook drove the Ametros acquisition.

3. Deposit Quality Over Quantity

HSA deposits are "the opposite of hot money." For bank investors, deposit quality matters as much as quantity. A bank with $10 billion in rate-sensitive brokered CDs is fundamentally different from a bank with $10 billion in long-duration HSA deposits. Webster's differentiated funding base is its most important competitive advantage.

4. Transformational M&A Requires Vision

The Sterling merger wasn't just about size—it was about combining complementary capabilities. Webster's deposit franchise plus Sterling's commercial banking expertise created something neither could have built organically.

5. Family Business Succession Can Work

Webster successfully transitioned across three leadership generations: founder Harold Smith to son James Smith to hand-picked successor John Ciulla. Each leader built on their predecessor's foundation while adapting to changing market conditions.

6. Crisis Creates Opportunity

The Warburg Pincus investment during the 2008 crisis positioned Webster for future growth. Banks with strong capital positions can use downturns to acquire competitors, enter new markets, and build market share.

7. Regional Banking Evolution

Webster's journey from thrift to commercial bank to diversified financial services company illustrates how successful regional banks must continually evolve. Staying still means falling behind.

XII. Competitive Landscape & Investment Framework

Porter's Five Forces Analysis

Threat of New Entrants: Medium-High

Fintech disruptors like Chime and SoFi have lowered barriers in consumer banking. However, Webster's specialized businesses create natural moats. The HSA market has high switching costs—once an employer chooses an HSA administrator, changing is operationally complex. Commercial banking relationships are similarly sticky.

Bargaining Power of Suppliers: Low

Capital markets provide commoditized funding. Webster's differentiated deposit base reduces reliance on rate-sensitive wholesale funding, lowering supplier power relative to peers.

Bargaining Power of Buyers: Medium

Commercial clients have options among regional and national banks. However, Webster's specialized expertise in healthcare financial services and commercial lending verticals creates differentiation that reduces price sensitivity.

Threat of Substitutes: Medium-High

Non-bank financial services providers, fintech lenders, and private credit funds compete for commercial lending market share. However, Webster's deposit-funded balance sheet provides cost advantages over non-bank competitors that rely on more expensive funding.

Competitive Rivalry: High

M&T Bank's primary competitors in the regional banking space include a formidable group of institutions such as The PNC Financial Services Group, Truist Financial, Fifth Third Bancorp, First Citizens BancShares, Huntington Bancshares, Regions Financial, KeyCorp, East West Bancorp, First Horizon, and Webster Financial.

The Northeast regional banking market is intensely competitive. Webster competes with M&T Bank, Citizens Financial Group, KeyCorp, PNC Financial, and national banks with regional presence. Scale matters, which is why the Sterling merger was strategically important.

Hamilton's Seven Powers Analysis

Scale Economies: Moderate. Banking has scale advantages in technology, compliance, and branch operations. The Sterling merger improved Webster's position.

Network Effects: Limited in traditional banking. However, HSA Bank's employer relationships create some network dynamics—more employers on the platform attract more distribution partners.

Counter-Positioning: Strong. Webster's specialized deposit verticals (HSA, Ametros) represent a business model that larger banks cannot easily replicate without cannibalizing existing businesses.

Switching Costs: Strong in HSA and commercial banking. Changing HSA administrators is operationally complex for employers. Commercial banking relationships are similarly sticky.

Branding: Moderate. Webster has strong brand recognition in Connecticut but limited national brand awareness except in healthcare financial services.

Cornered Resource: The HSA Bank franchise represents a unique asset—the largest bank HSA administrator with decades of accumulated expertise and technology investment.

Process Power: Webster has developed operational capabilities in HSA administration that would take competitors years to replicate.

Key KPIs to Track

For investors monitoring Webster's ongoing performance, three metrics warrant particular attention:

-

Healthcare Financial Services Deposit Growth: The rate of deposit growth in HSA Bank and Ametros is the single most important leading indicator of Webster's competitive position. Target: mid-to-high single-digit annual growth.

-

Net Interest Margin (NIM): Webster's differentiated deposit base should support stable-to-improving NIMs even in changing rate environments. The bank's current NIM of approximately 3.44% compares favorably to regional peers.

-

Return on Tangible Common Equity (ROTCE): This metric captures profitability adjusted for intangible assets from acquisitions. Webster's current 18% ROTCE places it among the best regional bank performers.

Bull Case

Webster represents a differentiated regional bank with: - The lowest-cost, longest-duration deposit franchise in the industry through HSA Bank and Ametros - Significant commercial banking scale following the Sterling merger - Proven management with a track record of value-creating acquisitions - Favorable positioning for HSA market expansion as high-deductible health plans continue to grow

Bear Case

Risks include: - Commercial real estate concentration in the New York metropolitan market - Regulatory changes that could affect HSA tax advantages - Integration execution risk from recent acquisitions - Competition from fintech in consumer banking segments - Interest rate sensitivity if the Fed cuts rates significantly

Regulatory Considerations

As a bank approaching $100 billion in assets, Webster faces increasing regulatory scrutiny. Jason joined us as Chief Risk Officer this week as we had previously announced Dan Bley's intent to retire. Jason has 15 years of experience at a Category 4 bank, most recently as Chief Risk Officer, particularly valuable experience as we grow our bank toward $100 billion in assets.

The hiring of a Chief Risk Officer with Category 4 bank experience signals management's awareness that regulatory expectations will increase as the bank crosses size thresholds.

XIII. The Webster Story: 90 Years and Counting

"Acknowledging 90 years is much more than a recognition of our longevity. We are grateful for the generations of clients who have trusted us, the communities that embrace us and the colleagues who consistently go the extra mile," said John R. Ciulla, chairman and CEO of Webster Financial Corp.

Celebrating this milestone reinforces our focus on making progress with purpose in the years ahead. We continue to position ourselves to succeed in rapidly changing markets. With a disciplined approach to managing risk and a thoughtful strategy for growth, we are building for the long term, ensuring our company remains strong and reliable for generations to come.

Webster's 90-year journey from a $25,000 Depression-era savings and loan to an $80+ billion commercial banking powerhouse offers enduring lessons. Harold Webster Smith's founding vision—helping ordinary people achieve their financial goals—remains relevant. But the institution he built has evolved into something far more complex: a diversified financial services company with specialized deposit franchises that competitors cannot easily replicate.

The story isn't over. As Webster approaches $100 billion in assets, it will face new regulatory requirements, new competitive challenges, and new opportunities for growth. The HSA market continues to expand. The Ametros acquisition opens new healthcare financial services verticals. Commercial banking opportunities in the New York metropolitan market remain abundant.

What hasn't changed is the culture Harold Webster Smith instilled: conservative credit standards, patient capital, and a long-term view. These principles guided the bank through the Depression, through the S&L crisis, through 2008, and through every other challenge in between. They'll guide it through whatever comes next.

For investors, Webster offers something increasingly rare in American banking: a regional franchise with genuine competitive advantages, proven management, and a business model that rewards patience. In a world of quarterly earnings pressure and short-term thinking, Webster remains—90 years after Harold Webster Smith's first handshake on Chambers Street—a bank built for the long term.

Now I have sufficient information to continue the article. Let me continue from where the existing article left off.

XIV. Looking Ahead: Growth Catalysts and Strategic Initiatives

The Marathon Asset Management Joint Venture

Webster Financial Corporation and Marathon Asset Management, L.P., a leading global credit manager with $23 billion in assets under management, announced in 2024 that they were forming a private credit joint venture, which will deliver direct lending solutions to sponsor-backed middle market companies. The partnership combines each firm's credit expertise, private equity sponsor relationships and standing in the middle market with Webster Bank's full banking product suite that serves companies primarily in the middle market and Marathon's 26-plus years of experience in asset management.

This joint venture represents a strategic evolution in Webster's commercial banking capabilities. "This joint venture allows Webster to better serve and support our clientele, while at the same time diversifying our revenue and realizing a greater portion of our Sponsor franchise's capabilities," said John Ciulla, chairman and CEO of Webster Financial.

By the third quarter of 2025, the private credit joint venture with Marathon Asset Management became fully operational, with Webster working through a significant pipeline of potential lending opportunities. Early returns were positive, with good alignment between the two organizations on operations, risk appetite, and good referral activity on loan, deposit, and fee opportunities. The JV is working as intended and has expanded Webster's ability to offer more lending solutions to its existing sponsors' client base.

In the second quarter of 2025, $242 million of loans were moved to held-for-sale status for contribution to the joint venture with Marathon Asset Management. This enables Webster Financial to participate in larger, more complex sponsor-backed transactions, broadening access to fee-based income and enhancing its private credit platform without materially altering its on-balance-sheet credit profile.

The joint venture expected to launch in the third quarter, with fee income expected to meaningfully ramp in 2026 and beyond.

HSA Legislative Tailwinds

Perhaps the most significant growth catalyst for Webster in 2025 came from Washington. The enactment of the One Big Beautiful Bill Act in July 2025 broadened the accessibility of HSAs and could expand the number of participants by three to four million. Rising contribution limits are also strengthening the appeal of HSAs.

Webster Financial highlighted the realization of multiple strategic initiatives, notably the legislative expansion of its subsidiary, HSA Bank's addressable market. The reconciliation bill signed into law expands HSA eligibility, particularly for the approximately 7 million participants in "bronze" ACA health plans, creating significant incremental deposit growth potential for the HSA Bank segment. Management estimates the change could result in $1 billion to $2.5 billion of additional HSA deposits over the next five years, with further upside if additional pending legislation is enacted.

Webster management expressed further encouragement that for the first time eligibility for HSA accounts has been decoupled from high deductible health plans and that several provisions that were initially included but didn't make the final spending bill have strong support in both the House and Senate. Additional substantive legislation in 2025 is likely, including the possibility of another reconciliation bill. If all of the provisions that were in the original spending bill passed by the House were to become law, management believes this could double their range of opportunity for incremental deposits.

The broader HSA market continues its strong growth trajectory. By year-end 2024, HSA assets reached nearly $147 billion across over 39 million accounts, reflecting a year-over-year increase of 19% for assets and 5% for accounts. HSA investment assets maintained strong growth, supported, in part, by a growing recognition of HSAs' long-term benefits. During 2024, HSA investment assets increased by 38%, reaching $64 billion by year-end.

Devenir projects continued growth in the HSA market, forecasting over 45 million accounts and approximately $199 billion in total assets by the end of 2027.

For Webster, as the largest bank HSA administrator, these industry tailwinds translate directly into competitive advantage. The company's position at the top of the market, combined with favorable legislation, creates a multi-year deposit growth opportunity that few competitors can match.

XV. Recent Financial Performance: Q3 2025

Webster's third quarter 2025 results demonstrated the continued execution of its strategic vision. Webster Financial Corporation reported strong third-quarter 2025 results on October 17, with earnings per share of $1.54 exceeding analyst expectations of $1.52. The financial institution demonstrated solid growth across key metrics despite some margin pressure.

Results were strong, with a return on tangible common equity of 18%, ROA of nearly 1.3%, and growth in both loans and deposits of over 2% linked quarter. Overall revenue grew 2.3% over the prior quarter. In aggregate, Webster's results reflected how its strategic position fuels performance, including diverse balance sheet growth while maintaining substantial liquidity and conservative credit positioning.

The company's bottom line came in at $254.05 million, or $1.54 per share, compared with $186.80 million, or $1.10 per share, in the year-ago period.

Webster Financial reported total assets of $83.2 billion at quarter-end, representing an increase of $1.3 billion or 1.6% from the previous quarter. The company's balance sheet showed strength across multiple categories, with loan growth across all segments and continued deposit expansion. Loan growth was broad-based across all categories, with commercial loans increasing by $1.2 billion or 2.7% from the previous quarter.

As of September 30, 2025, total loans and leases increased 2.6% on a sequential basis to $55.1 billion. Further, total deposits increased 2.8% from the prior quarter to $68.2 billion.

"We're not looking to sell the bank. We're also pragmatic and good fiduciaries with our board," CEO John Ciulla stated during the earnings call. President and COO Luis Massiani highlighted growth opportunities, particularly in health savings accounts, noting, "We view that as being one of the big opportunities and untapped channels."

XVI. Industry Context: Regional Banking in 2025

Webster operates within a regional banking landscape that has experienced significant evolution in recent years. For 2025, U.S. bank net interest income is projected to increase 5.7% year on year, according to S&P Capital Global Market Intelligence, a step up from essentially no growth last year.

Optimism is rising among banking and capital markets executives. The combination of continued Federal Reserve rate cuts, a pro-growth agenda in Washington and expectations for streamlined regulations creates an environment primed for banks to go on offense. Expanding loan origination activity and pursuing capital markets underwriting appear to be attractive early 2025 growth drivers.

A re-steepening of the yield curve—a normal-for-longer environment—presents a more optimal environment for regional bank returns. These conditions are likely to support strong revenue and earnings growth in the years ahead.

Banks are optimistic about the second half of 2025 and beyond amid favorable economic, regulatory and technological developments.

However, the industry faces challenges as well. The U.S. banking industry, particularly its regional sector, is navigating a period of heightened uncertainty as growing concerns over bad loans, primarily in commercial real estate (CRE), threaten to destabilize balance sheets. As of October 2025, a confluence of factors, including elevated interest rates, declining property values, and isolated incidents of loan fraud, is placing significant pressure on banks.

In the short term, elevated credit losses are anticipated, driven primarily by continued distress in the CRE sector. The significant volume of commercial mortgages maturing in 2025, originated in a more favorable interest rate environment, makes refinancing difficult, potentially leading to a wave of defaults. Office loan delinquencies are already surging, and consumer loan delinquencies are expected to rise modestly.

Webster's differentiated funding base—particularly its HSA and Ametros deposits—provides a buffer against these industry headwinds. Webster's multiple low-cost deposit sources represent a significant competitive advantage in an environment where funding costs remain a key determinant of bank profitability. This advantage could become even more pronounced if market conditions lead to increased competition for deposits among financial institutions. The bank's strong deposit base provides stability and flexibility, allowing Webster to pursue lending opportunities without becoming overly dependent on wholesale funding.

XVII. Analyst Perspectives and Market Outlook

Wall Street analysts maintain a generally favorable view of Webster Financial. According to 14 analysts, the average rating for WBS stock is "Strong Buy." The 12-month stock price target is $71.0, which is an increase of 25.49% from recent prices.

Earnings projections for Webster remain strong, with analysts forecasting earnings per share (EPS) between $5.90 and $6.04 for the first fiscal year and between $6.54 and $6.94 for the second fiscal year. These projections reflect confidence in Webster's ability to execute its growth strategy and navigate potential market challenges.

Barclays raised its price target to $80 from $78 in November 2025, while Morgan Stanley raised its target to $77 from $64 in September 2025.

Webster's growth strategy centers around three primary initiatives that analysts believe will provide significant tailwinds. The expansion of Health Savings Accounts represents a major focus area, with recent improvements in HSA legislation creating new opportunities for the bank to grow this segment. HSAs provide a stable and growing deposit base while generating fee income, making them an attractive component of Webster's overall business model.

The combination of traditional banking services with specialized offerings creates a diversified business model that may provide more stability than banks relying primarily on conventional deposit and lending activities.

XVIII. Risks and Considerations

While Webster's strategic positioning is strong, investors should consider several risk factors.

Commercial Real Estate Exposure

Webster management acknowledged an increase in uncertainty compared to January 2025, as noted during the London America's Select conference in May. This rising uncertainty could potentially slow the anticipated loan growth that forms a key part of the bank's strategy.

Total non-performing assets were $545.3 million as of September 30, 2025, up 27.6% from the year-ago quarter. While this increase reflects broader industry trends in commercial real estate, it bears monitoring.

Interest Rate Sensitivity

Webster Financial's current interest rate positioning includes a hedge portfolio of $5.25 billion, which provides benefits to net interest income in a declining rate environment. This strategic positioning should help mitigate the impact of anticipated rate cuts in the coming quarters.

Regulatory Evolution

As Webster approaches $100 billion in assets, it faces heightened regulatory requirements. The company has proactively addressed this by strengthening its risk management infrastructure with experienced leadership from larger institutions.

Competitive Dynamics

As the gap between the largest banks and their smaller rivals widens, scale is emerging as the ultimate competitive advantage. Webster's position as a mid-sized regional bank requires continued execution on differentiation strategies to compete effectively with both larger national banks and smaller, nimbler community banks.

XIX. Conclusion: A Blueprint for Regional Banking Success

Webster Financial's 90-year journey from Harold Webster Smith's modest Waterbury office to a diversified financial services company with over $80 billion in assets offers a masterclass in sustainable business building.

The company's success rests on several interconnected pillars. First is the power of patient capital—the multi-generational leadership of the Smith family created an institutional culture that prioritized long-term value creation over short-term earnings optimization. Second is the genius of niche specialization—the 2005 acquisition of HSA Bank demonstrated that finding an underserved market early and dominating it creates competitive moats that compound over decades. Third is the importance of transformational M&A—the Sterling merger proved that well-conceived combinations can create value greater than the sum of parts.

Anticipated loan growth forms a key pillar of Webster's strategy. The bank's commercial clients remain optimistic despite increased uncertainty compared to earlier in the year, suggesting potential for continued expansion of the loan portfolio.

The legislative tailwinds for HSA Bank, combined with the Marathon joint venture's fee income potential and the Ametros deposit franchise, position Webster for continued growth in an industry facing significant headwinds. Provisions in recently passed legislation accelerate growth in HSA deposits, reinforcing Webster Financial's competitive advantage in health-focused banking and positioning HSA Bank as a significant contributor to long-term balance sheet growth.

For the regional banking industry, Webster represents a different model—one built not on being the biggest, but on being the best in carefully selected verticals. As Harold Webster Smith understood in 1935, the path to prosperity runs through helping people achieve their financial goals. Nine decades later, that philosophy continues to guide an institution that has grown from $25,000 to over $80 billion in assets while maintaining the values-driven culture its founder instilled.

The challenges ahead are real: commercial real estate pressures, competitive intensity, regulatory evolution, and macroeconomic uncertainty will test management's execution capabilities. But Webster enters this environment from a position of strength—differentiated funding, proven leadership, and strategic optionality that few regional banks can match.

In a world of increasingly commoditized financial services, Webster Financial has built something rare: a regional bank with genuine competitive advantages that compound over time. That, ultimately, is what Harold Webster Smith would have wanted when he made that first $200 loan to Joe Baltrush on Chambers Street in 1935—a bank built not just to survive, but to thrive for generations to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube