First Horizon: 160 Years of Southern Banking — From Civil War Memphis to Regional Powerhouse

Introduction: A Bank Forged in Crisis

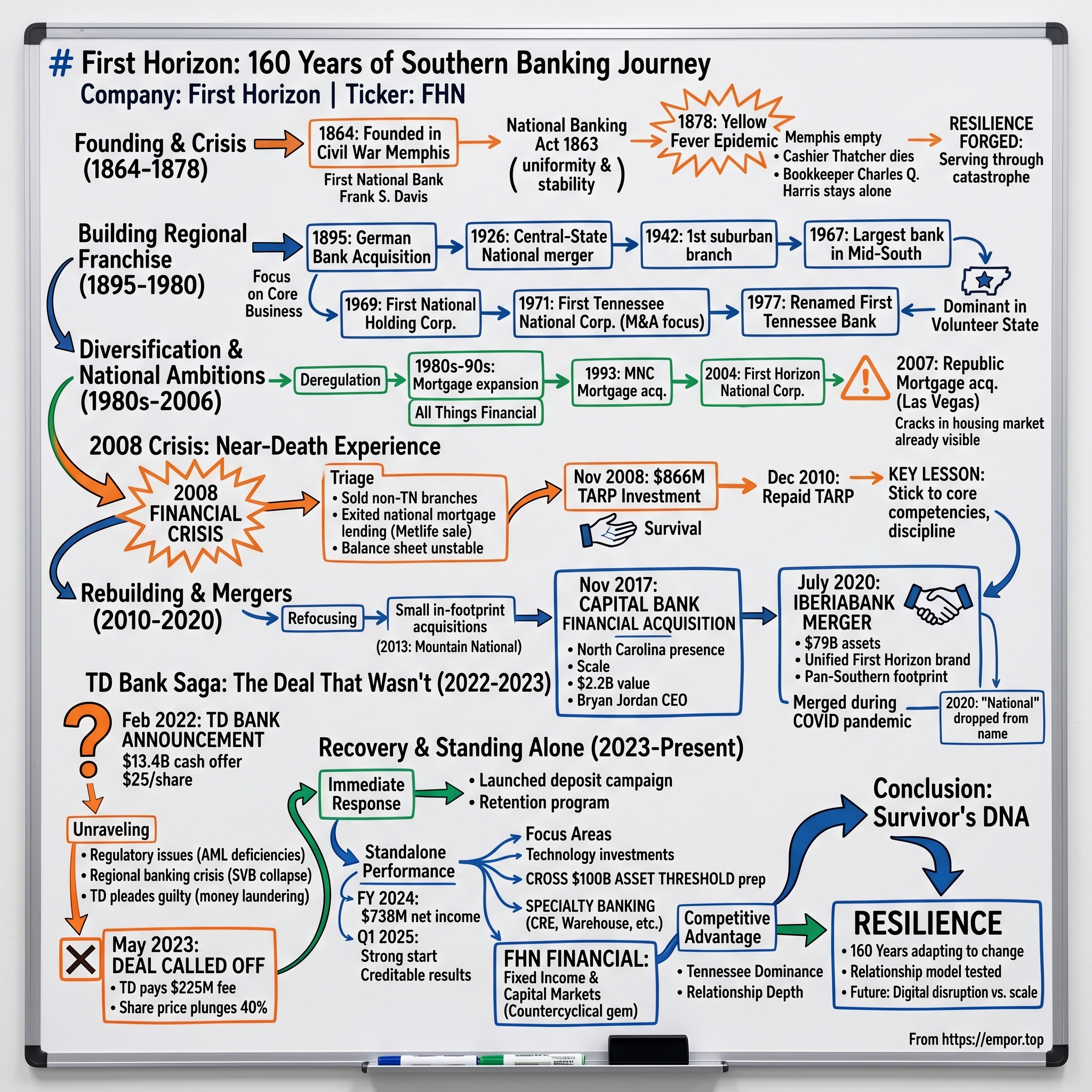

The Mississippi River cuts through Memphis like a slow, brown artery—as it has for millennia—indifferent to the wars, epidemics, and financial panics that have ravaged the city on its banks. In the spring of 1864, with Confederate forces still lurking in the Tennessee countryside and Union soldiers patrolling the streets under martial law, an Ohio businessman named Frank S. Davis did something that would have seemed absurd to most: he opened a bank.

Our story began in 1864, when Ohio businessman Frank S. Davis arrived in Memphis to open the city's first national bank. Davis saw a genuine need for banking and credit to finance rebuilding and new commercial growth.

Today, the institution Davis founded operates as First Horizon Corporation, with $82.2 billion in assets as of December 31, 2024 and 416 banking centers operating across 12 states primarily in the southeastern United States. The company employs more than 7,200 associates and stands as the fourth largest regional bank in the Southeast.

But the question that animates this deep dive is the improbable one: How did a bank founded during the Civil War in occupied Memphis survive yellow fever epidemics, the Great Depression, a near-catastrophic mortgage crisis, and a failed $13.4 billion acquisition—and still end up as one of the most respected regional banks in America?

First Horizon has served clients through civil war, two world wars, yellow fever epidemics, financial panics, the Great Depression and the Great Recession. Our clients and our companies have endured adversity, seized opportunity and embraced change.

The answer lies in a corporate culture that was forged in literal plague, tested during the 2008 financial crisis, and refined through one of the most dramatic M&A collapses in recent banking history. What emerges is not just a story about a regional bank, but a case study in institutional resilience—and the question of whether relationship-based banking can survive in an age of digital disruption and mega-bank dominance.

Founding Story: A Bank Born in Occupied Territory (1864-1878)

The Audacity of Starting a Bank During Civil War

Picture Memphis in early 1864. The city had fallen to Union forces on June 6, 1862, following a brief but decisive naval battle on the Mississippi. Once a bustling center of commerce, Memphis first suffered the destructive effects of war when in 1862 Union troops gained control of the city and placed it under military rule. The cotton trade—the economic engine of the antebellum South—had collapsed. Confederate sympathizers faced confiscation of property. The streets were patrolled by blue-uniformed soldiers with bayonets.

Into this chaos stepped Frank S. Davis.

Davis was convinced that Memphis would need additional banking and credit facilities, once a national system of banks regulated by the federal government emerged, a prospect ensured by the passage of the National Banking Act of 1863. To that end, he organized a meeting to be convened on March 10, 1864 to discuss the possibilities of organizing a nationally chartered bank. That day, Davis and several other Memphis residents drafted the articles of association for such an enterprise and filed an application for a national charter.

The National Banking Act of 1863 was one of the most consequential pieces of financial legislation in American history. Passed by Lincoln's administration to help finance the war effort, the federal acts were passed in part to create uniformity in a banking system in which banks had previously been chartered solely by the states. One goal of the new system was to ensure some regularity and consistency in banknote issue. Another goal was to help finance the war effort: national banks were to back their notes with U.S. bonds, which remained on deposit with the U.S. Comptroller of the Currency.

Davis understood that whoever secured these new national bank charters first would have a tremendous advantage in the post-war economy. Frank S. Davis founded First National Bank, the first nationally chartered bank in Memphis, after passage of the National Banking Act of 1863. Though the city was under martial law after being captured by Union forces in the Civil War, First National Bank of Memphis was officially chartered on March 25, 1864.

The bank grew rapidly, moving to its own two-story building within two months of opening. Davis had bet correctly: Memphis would rebuild, the cotton trade would resume, and the merchants and planters who survived the war would need credit.

The Yellow Fever Test: The Last Man Standing

Davis's bank weathered the immediate post-war chaos, but the true test of First National Bank's character came fourteen years later, in a calamity so devastating it nearly erased Memphis from the map.

In 1878, Memphis, Tennessee, faced one of its worst public health disasters: a massive Yellow Fever epidemic. This wasn't the first time Yellow Fever hit Memphis. The city had seen outbreaks before in 1828, 1855, and 1867, usually brought by steamboats from New Orleans.

But the epidemic of 1878 was different. On August 13, 1878, Kate Bionda, a restaurant owner, dies of yellow fever in Memphis, Tennessee, after a man who had escaped a quarantined steamboat visited her restaurant. The disease spread rapidly and the resulting epidemic emptied the city.

Twenty-five thousand people picked up and left within a week. For the most part, it was the African American residents who remained in town, although they died at a much lower rate than the white residents who contracted the disease. An average of 200 people died every day through September.

The commercial life of Memphis ground to a halt. The daily newspaper, which somehow managed to keep operating during the epidemic, warned visitors to stay away: "We know that our businessmen are impatient to get home and renew business. We say to them there is no business being transacted here. ... Memphis is dealing in death."

Most bank officials fled with everyone else who had the means to escape. But not everyone at First National Bank left.

Most bank officials left the city, along with other business leaders. Two First National employees stayed behind, however: cashier W.W. Thatcher and bookkeeper Charles Q. Harris. The bank stayed open only a few hours each day, mainly so it could handle cash donations sent to Memphis from relief organizations in other cities.

Thatcher quickly succumbed to the fever, but Harris stayed at his post.

Here was a young bookkeeper, watching colleagues die around him, knowing that each day he reported to the bank could be his last. A lone figure, Charles Q. Harris, remained to operate the new bank, serving customers by himself for three hours each day and distributing relief funds sent from across the country.

No one dreamed that the disease was carried by an insect; all anyone knew—based on past, less deadly epidemics—was that it inexplicably faded away as soon as the scorching summer weather came to an end. So eventually a cold spell did come in mid-October of that year, killing off the mosquitoes, and ending the epidemic.

The epidemic ended with the first frost in October, but by that time, 20,000 people in the Southeast had died and another 80,000 had survived infection. The economic toll was staggering: The $15 million in losses caused by the epidemic bankrupted the city of Memphis. The federal government convened a commission to investigate the outbreak and established the National Board of Health in 1879.

The loss of over 30,000 people led financial crisis for the city, and in 1879, the state legislature revoked Memphis' city charter.

But First National Bank never closed its doors. As thousands of Memphians died in the yellow fever epidemic and many more fled the city, bookkeeper Charles Q. Harris kept the bank open, serving clients and distributing relief funds from across the country.

This moment became foundational to First Horizon's corporate identity. When the company talks about resilience, about staying with clients through crisis, this is the origin story they point to—a lone bookkeeper in a dying city who refused to close the bank.

Building the Regional Franchise (1895-1980)

From Recovery to Dominance

Yellow fever epidemics checked the bank's growth in 1867, 1873, and 1878. The end of the epidemics, combined with the end of Reconstruction in Memphis, allowed the bank to focus on core business and expand.

The modernization of Memphis's sanitation systems following the epidemic eventually eliminated the mosquito breeding grounds, and the city slowly rebuilt. First National Bank grew with it.

The bank acquired German Bank in 1895. This was followed by steady expansion as Memphis transformed from a regional cotton market into a diversified commercial hub.

In 1897 First National purchased the German Bank, which increased the bank's deposits from $700,000 to approximately $1.15 million. First National would later complete its first merger by uniting with Central-State National Bank, another Memphis bank, in July 1926.

The early 20th century brought First National into the emerging national financial infrastructure. The bank was one of five banks in the twelve Federal Reserve districts to help implement the Federal Reserve Act of 1913, participating in the organization of the Federal Reserve Bank of St. Louis.

Post-War Transformation

In 1942, the bank opened its first suburban branch and by 1952, First National had seven offices. As of 1967, First National was the largest bank in the Mid-South.

The post-war years represented a golden age of steady growth. Memphis was benefiting from the broader Sunbelt migration, and First National Bank was positioned at the center of the region's commercial activity.

A holding company, First National Holding Corporation, was created in 1969. Two years later, because leadership intended to acquire other banks, this became First Tennessee National Corporation. The corporation acquired five banks in 1972 and changed their names to First Tennessee Bank. In 1977, First National also became First Tennessee Bank.

The transformation to a holding company structure was crucial. It allowed the bank to pursue an aggressive acquisition strategy while maintaining the trust and relationships built under the First Tennessee name. First Tennessee, with its principal subsidiary, First National Bank of Memphis, began acquiring Tennessee-based banks at a rapid pace. Five banks were purchased in 1972, with more to follow throughout the decade, as First Tennessee extended its presence outside of Memphis and into other regions within the state.

By the end of the 1970s, First Tennessee had established itself as the dominant banking franchise in the Volunteer State—a position it maintains to this day.

Diversification & National Ambitions (1980s-2006)

The Siren Song of National Mortgage Lending

The 1980s brought deregulation, and with it, the temptation to expand beyond traditional commercial banking. During the 1980s, the company expanded into mortgage brokerage, mortgage loan origination, and insurance. In 1981 First Express became the first national check-clearing service, and First Tennessee offered brokerage services starting the next year.

In 1993, the bank acquired MNC Mortgage, marking its serious entry into national mortgage origination. In 1999, to reflect its diversification, the bank adopted the slogan, "All Things Financial."

The strategy seemed sound at the time. Mortgage origination offered fee income that wasn't dependent on interest rate spreads. It allowed the bank to serve customers nationally without building an expensive branch network. And in the boom years of the early 2000s, the profits were spectacular.

In 2004, the company changed its name to First Horizon National Corporation to reflect its interstate growth. In May 2007, the company acquired Republic Mortgage, based in Las Vegas.

The timing of that Las Vegas mortgage acquisition could not have been worse. By May 2007, the cracks in the housing market were already visible to those paying attention. Subprime delinquencies were rising. The ABX index—which tracked the value of mortgage-backed securities—had been declining since January.

First Horizon, like many regional banks seduced by the mortgage boom, was about to learn a brutal lesson about the dangers of chasing growth without fully understanding risk.

The 2008 Financial Crisis: Near-Death Experience

The Crash Arrives

The American subprime mortgage crisis was a multinational financial crisis that occurred between 2007 and 2010, contributing to the 2008 financial crisis. It led to a severe economic recession, with millions becoming unemployed and many businesses going bankrupt.

For First Horizon, the crisis hit with devastating speed. The national mortgage operation that had seemed so promising was suddenly hemorrhaging losses.

In September 2007, the company sold 34 branches outside of Tennessee, including 13 branches to M&T Bank, 10 branches to Sterling Bank, 9 branches to Fifth Third, and 2 branches to FMCB Holdings.

This wasn't expansion in reverse—it was triage. The company was selling assets to raise capital and retreating to its Tennessee core.

In June 2008, the company sold its residential-mortgage origination and servicing business to Metlife.

The Metlife sale was the definitive end of First Horizon's national mortgage ambitions. But by this point, the damage was done. The bank's balance sheet was laden with troubled assets, and the broader financial system was seizing up.

TARP and Survival

In September 2008 our nation was on the edge of falling into a second Great Depression. Confidence in the financial system was vanishing and panic was spreading. Every major financial institution was vulnerable. The credit markets that provide financing for credit cards, student loans, mortgage loans, auto loans, small business loans and other types of financing stopped functioning.

In November 2008, the United States Department of the Treasury invested $866 million in the company as part of the Troubled Asset Relief Program and in December 2010, the company repurchased the investment from the Treasury.

After reporting heavy losses in mid- and late-2008 and receiving a $866,540,000 injection from the TARP as a transaction under the Capital Purchase Program on Nov. 14, 2008, the company's balance sheet appears to be stabilizing somewhat.

The arrival of Bryan Jordan as CEO in 2008 marked a turning point. Bryan Jordan is chairman, president and chief executive officer of First Horizon Corporation. Before joining First Horizon in 2007, Jordan was Chief Financial Officer at Regions Financial Corporation. His career also includes positions at First Union Corporation and KPMG.

Jordan joined First Horizon as Chief Financial Officer in 2007 and was named president and CEO a year later. He inherited a company in crisis and immediately began the painful work of restructuring.

"Our early decisions to raise capital, sell assets and exit our lending businesses outside our banking region put us in a stronger position by the end of one of the worst years the financial services industry has faced," said CEO Bryan Jordan. "We're leveraging the money we received from the government's TARP program to facilitate lending to our consumer, small business and commercial customers. The TARP funds contributed to our ability to originate more than $900 million in new loans in the fourth quarter."

The company repaid its TARP investment in December 2010—faster than many expected. But the scars from the mortgage crisis would take years to fully heal.

The Key Lesson: The mortgage expansion nearly destroyed a 144-year-old institution. It was a classic case of "crossing the Rubicon"—venturing into businesses that looked adjacent but required fundamentally different risk management capabilities. The episode would shape the company's approach to growth for the next decade: organic expansion in core markets, disciplined underwriting, and a deep skepticism of businesses that promised high returns without commensurate relationship depth.

The Rebuilding Years (2010-2017)

Back to Basics

The 2010s began as a period of healing and strategic refocusing. Across the 2010s, First Horizon acquired three regional banks, starting in 2013, when it acquired the failing Mountain National Bank.

These were small, in-footprint acquisitions designed to strengthen the Tennessee franchise rather than chase national ambitions. The company was rebuilding its capital base, restoring trust with regulators, and recommitting to relationship banking.

The Capital Bank Transformation (2017)

The first major sign that First Horizon was ready to think big again came in May 2017.

First Horizon and Capital Bank Financial Corp. have entered into a definitive agreement that will create the fourth largest regional bank in the Southeast. Under the agreement First Horizon, which has $30 billion in assets, will acquire Capital Bank, which has $10 billion in assets.

First Horizon National Corporation today announced the final merger consideration election and allocation results for its acquisition of Capital Bank Financial Corp., which was completed effective November 30, 2017.

Effective November 30, 2017, Capital Bank Financial merged into First Horizon, and its subsidiary, Capital Bank Corporation, merged into First Tennessee Bank National Association. The merger brings together two respected financial institutions under the First Horizon family of companies and creates the fourth largest regional bank in the Southeast with approximately $40 billion in assets, $32 billion in deposits, $27 billion in loans and 350 branches in Tennessee, North Carolina, South Carolina, Florida, Mississippi, Georgia, Texas and Virginia.

The Capital Bank deal was strategic in multiple dimensions. It gave First Horizon a meaningful presence in North Carolina—one of the fastest-growing banking markets in the Southeast. It added scale that would reduce unit costs. And it positioned the company for the next wave of consolidation in regional banking.

The total transaction value, at yesterday's First Horizon closing stock price, is $2.2 billion. "This is an exciting time for First Horizon," said Bryan Jordan, chairman and CEO of First Horizon. "Together with the accomplished team at Capital Bank we will be able to leverage the strengths of both banks and capitalize on growth opportunities in attractive, high-growth Southeast markets."

Brand Unification & IberiaBank Merger (2019-2020)

Creating a Pan-Southern Franchise

By 2019, First Horizon had emerged from the crisis years as a stronger, more focused institution. But the management team recognized that scale was increasingly critical in regional banking. The largest banks were investing billions in technology. Regulators were imposing ever-more-complex compliance requirements. Customer expectations were rising.

During Memphis' bicentennial year, we announced our entire company would operate under the unified First Horizon brand name, marking a new era in our rich history. Concurrently, First Tennessee filed an application to convert from a national bank into a Tennessee state-chartered bank to better align with the bank's strategic priorities, streamline oversight processes and provide better client service under the bank's new First Horizon brand.

Then came the transformational deal.

In November 2019, First Horizon Corporation and IberiaBank Corporation agreed to merge, closing in July 2020. The combined bank is based in Memphis, Tennessee, and uses the First Horizon name.

IBERIABANK is headquartered in Lafayette, Louisiana and has $32 billion in assets and 3,400 associates across its footprint. Our combined organization will have $75 billion in assets, $57 billion in deposits and $55 billion in loans across 11 states.

The merger was structured as a merger of equals—though First Horizon shareholders ended up with 56% of the combined company. The combined company, with $79 billion in assets, $60 billion in deposits and $58 billion in loans as of March 31, 2020, will be headquartered in Memphis, Tennessee and operate under the First Horizon name.

Closing During a Pandemic

The IberiaBank merger closed on July 2, 2020—in the midst of the COVID-19 pandemic. "We are pleased to receive regulatory approval to merge our two companies," said Bryan Jordan, Chairman and CEO of First Horizon. "First Horizon and IBERIABANK together will be well positioned to navigate a changing financial services landscape, deliver superior client solutions, strengthen the communities we serve and create strong returns."

"The completion of this merger marks a significant milestone for our clients, associates, shareholders and communities," said Bryan Jordan. "The combined company's enhanced scale, diversified business model and expertise in financial services uniquely positions us to better serve our clients and communities, accelerate our growth and create long-term shareholder value."

The pandemic timing created integration challenges—blending cultures and systems while much of the workforce was working remotely—but the combined company emerged from 2020 with substantial scale and a pan-Southern footprint.

First Horizon plans to cut $170 million in annual noninterest expenses, representing a quarter of Iberiabank's annual operating expenses, by reducing redundant overhead, branches, operations and computer services. The combined company should have an efficiency ratio of 51%.

At the end of 2020, our parent company dropped "National" from its name, becoming First Horizon Corporation, to more closely align with our First Horizon brand.

The TD Bank Saga: The $13.4 Billion Deal That Wasn't (2022-2023)

The Announcement

By early 2022, First Horizon was riding high. The IberiaBank integration was proceeding smoothly. The Southeast was experiencing robust economic growth. The company was generating strong returns.

Then came an announcement that would fundamentally alter the company's trajectory.

On February 28, 2022, TD Bank, a major Canadian multinational bank, announced that it had entered into an agreement to purchase First Horizon, a Memphis-based bank, for $13.4 billion in cash.

As part of the deal, TD pledged to pay $25 per share for First Horizon, a 37% premium as of February 2022.

The deal represented a massive strategic bet by TD Bank, Canada's second-largest lender. The now-scrapped acquisition of First Horizon would have boosted TD from the eighth-largest bank in the U.S. to the sixth and given it a presence in several new markets, especially in the Southeast.

For First Horizon shareholders, the $25 per share offer seemed like a generous exit. For TD, First Horizon offered everything the Canadian bank wanted: a presence in the fastest-growing region of the country, a strong commercial banking franchise, and a respected management team.

The Unraveling

But something was wrong at TD Bank—something that would ultimately torpedo the largest pending bank deal in America.

TD executives knew as early as November 2022—six months before the bank's $13.4 billion proposed acquisition of First Horizon was terminated—that multiple U.S. agencies, including the Justice Department, had found anti-money laundering deficiencies serious enough to put the deal at risk of rejection, the Capitol Forum reported.

TD and Memphis, Tennessee-based First Horizon called off their proposed deal last week, blaming "uncertainty" as to when the transaction might gain regulatory approval. The Office of the Comptroller of the Currency and the Federal Reserve's reluctance to sign off on the deal, in light of TD's handling of suspicious customer transactions, contributed to the tie-up's demise.

The delay coincided with the 2023 regional banking crisis. First Horizon is a regional lender in the southeast United States and would have helped Canada's TD expand south of the border. But regional banks have been losing the confidence of investors and customers since the March collapse of Silicon Valley Bank and Signature Bank. On Monday, a third regional bank, First Republic, failed and JPMorgan purchased most of its assets.

First Horizon declined as much as 33% Monday morning and was briefly halted due to volatility. The stock pared losses but still ended the day down 20% at $16.04. That's about 36% below TD's takeover offer.

The Collapse

On May 4, 2023, the companies announced that the acquisition would not proceed citing regulatory uncertainties, with TD owing First Horizon a total of $225 million in break-up fees as part of the termination agreement. The merger's call off happened within the same week as the collapse and buyout of First Republic Bank by JPMorgan Chase.

Caught up in the worst banking crisis since 2008, First Horizon's share price has plunged about 40% over the past couple months, falling well below the $25 per share that TD offered when the takeover was announced in February 2022.

On a call following the termination announcement, First Horizon Chairman, President and CEO D. Bryan Jordan said TD "could not provide assurance of regulatory approval in 2023 or 2024."

The full extent of TD's problems emerged later. Following these disclosures, on October 10, 2024, the DOJ and regulators from the OCC, FinCEN, and the Federal Reserve announced that TD Bank had pleaded guilty to criminal violations of the Bank Secrecy Act ("BSA") and conspiracy to commit money laundering, resulting in over $3 billion in fines and penalty. This guilty plea was unprecedented, as TD became the largest bank in U.S. history to plead guilty to BSA program failures and the first U.S. bank in history to plead guilty to conspiracy to commit money laundering.

The Office of the Comptroller of the Currency imposed a $434 billion asset cap on TD's U.S. retail banking operations. The growth restriction comes in addition to $3.09 billion in penalties stemming from investigations into TD's safeguards against money laundering.

First Horizon, through no fault of its own, had been caught up in one of the most significant compliance failures in modern banking history.

The Recovery: Standing Alone (2023-Present)

The Immediate Response

The day the TD deal collapsed, First Horizon's stock fell precipitously. Average deposits at First Horizon fell 4% to $62.2 billion in the first quarter, compared to the end of last year. The company was now a standalone regional bank in the middle of a banking crisis, with no acquirer to provide a floor for its stock price.

Management responded with decisive action. The company launched an aggressive deposit campaign, offering competitive rates on certificates of deposit to stem outflows and attract new customers. First Horizon saw deposit growth after the termination, with total deposits sitting at $65.43 billion at June 30 compared to $61.44 billion at March 31, largely thanks to an aggressive deposit campaign. The company held an investor day June 6 where it reintroduced guidance and outlined its independent priorities, which center around focusing inward on initiatives such as building capital and retaining employees and customers.

The company also implemented a substantial retention program. With the TD deal dead, there was real risk that key employees—who had expected to become part of a much larger organization—would depart. Management invested heavily in retaining talent and stabilizing the organization.

Financial Performance

The company navigated the post-crisis period with remarkable stability. First Horizon Corporation today reported full year 2024 net income available to common shareholders ("NIAC") of $738 million or earnings per share of $1.36, compared with full year 2023 NIAC of $865 million or earnings per share of $1.54.

While earnings declined from 2023, the results demonstrated that First Horizon could operate effectively as a standalone entity. In 2024, First Horizon's revenue was $3.04 billion, an increase of 1.95% compared to the previous year's $2.98 billion. Earnings were $738.00 million, a decrease of -14.68%.

Most importantly, credit quality remained strong. "We successfully grew the business in 2024, driven by a strong net interest margin, improved counter-cyclical revenues, and declining net charge-offs. In the fourth quarter 2024, we delivered solid results with a two basis point expansion of net interest margin, a 6% increase in fixed income revenue, and 8 basis points of net charge-offs, starting 2025 with positive momentum."

First Horizon Corporation today reported first quarter net income available to common shareholders ("NIAC") of $213 million or earnings per share of $0.41, compared with fourth quarter 2024 NIAC of $158 million or earnings per share of $0.29.

The Q1 2025 results showed the company building momentum as a standalone franchise.

Technology and Operational Investments

Post-TD, First Horizon has invested significantly in technology and operational capabilities. When asked about the company's approach to managing capital and regulatory thresholds, particularly regarding the $100 billion asset threshold, Bryan Jordan stated that the company is preparing for crossing the $100 billion threshold by making necessary investments and building infrastructure.

FHN Financial is an important part of First Horizon's business model, as it provides unique countercyclical benefits and complements our approach to managing our company for soundness and profitability throughout shifts in the economy. With an average daily trading volume of $5+ billion, FHN Financial has transacted business in recent years with approximately 50% of all US banks with portfolios more than $100 million.

Business Model Deep Dive

Segment Structure

First Horizon operates through three principal segments, each serving distinct customer needs while creating cross-selling opportunities.

First Horizon Corporation operates as the bank holding company for First Horizon Bank that provides various financial services. It operates through Regional Banking, Specialty Banking, and Corporate segments. The company offers commercial banking, business banking, consumer banking, and private client and wealth management business such as deposit, commercial, consumer & wealth investment, wealth management, financial planning, trust and asset management services.

The Specialty Banking segment provides wholes banking services like fixed income/capital markets, professional commercial real estate, mortgage warehouse lending, asset-based lending, franchise finance, equipment finance, energy finance, healthcare finance, and trucking and transportation finance.

Fixed Income/Capital Markets: The Hidden Gem

One of the most distinctive aspects of First Horizon's business model is its fixed income and capital markets division, FHN Financial.

FHN Financial is an industry leader in fixed income sales, trading, and strategies for institutional customers in the United States and abroad. The company also provides investment services and balance sheet management solutions.

FHN Financial is an industry leader in fixed income sales, trading, and strategies for institutional customers in the US and abroad. With an average daily trading volume of over $4.2bn, FHN Financial transacts business with ~45% of all domestic depository institutions with portfolios larger than $100 million. Complementing its unique distribution capabilities are a range of additional products and services, including investment banking, institutional investment advisory, interest rate derivatives, loan trading and consulting, asset liability management, and portfolio accounting.

This business provides crucial countercyclical benefits. When interest rates are volatile—exactly when traditional banking margins can be squeezed—the fixed income trading business tends to perform well as institutional clients reposition portfolios.

Wealth Management

With 30 trust officers, 86 financial advisors, 10 financial planning professionals, and $32 billion in assets under administration, First Horizon Advisors' mission is to provide you with access to a range of resources that can help you build the financial future you deserve.

Competitive Position and Strategic Analysis

The Southeast Banking Battlefield

First Horizon competes in one of the most dynamic banking markets in America. The Southeast has experienced tremendous population and economic growth, attracting investment from both super-regional banks and the national giants.

"Banks like Fifth Third, PNC and Truist are building out their presence in the Sun Belt and Southeast, where population growth, new business formation and household wealth are all rising fastest in the U.S.," says Max Friar, founder and managing partner of Calder Capital. "Even with digital banking on the rise, physical branches still play an important role in establishing and maintaining commercial relationships."

Key traditional competitors in many of our markets include Wells Fargo Bank N.A., Bank of America N.A., SunTrust Bank, and Regions Bank, among many others including many community banks and credit unions. An additional key competitor in Tennessee is Pinnacle National Bank.

The Core Competitive Advantage: Tennessee Dominance

First Horizon's most defensible competitive position is its Tennessee franchise. Our First Tennessee and Capital Bank brands have the largest deposit market share in Tennessee and one of the highest customer retention rates of any bank in the country. We have been ranked by American Banker as No. 5 among the Top 10 Most Reputable U.S. Banks.

In its core Tennessee markets, the bank holds significant deposit market share, including 33.35% in the Memphis metropolitan area with $14.01 billion in local deposits as of June 2025, and remains the leading deposit holder in Chattanooga.

First Tennessee Bank has one of the highest customer retention rates of any bank in the country and the number one combined market share in its Tennessee markets.

This market dominance creates a virtuous cycle: strong market share leads to better economics, which funds superior service, which reinforces customer loyalty. It's exactly the kind of local competitive advantage that's difficult for national players to replicate.

Porter's Five Forces Analysis

1. Threat of New Entrants: MODERATE-HIGH

The traditional barriers to banking—capital requirements, regulatory approval, branch networks—remain formidable. But digital-only banks and fintech players are attacking specific product categories without the overhead of physical infrastructure.

Companies like Chime, SoFi, and Marcus by Goldman Sachs can offer deposit products nationally with minimal physical presence. They target younger, digitally-native customers who may never develop the branch-based banking habits of prior generations.

For First Horizon, the threat is most acute in commoditized products like savings accounts and payments. The defense lies in relationship complexity—the commercial treasury management, wealth advisory, and lending relationships that require human judgment and local knowledge.

2. Bargaining Power of Suppliers: LOW

Capital is commoditized. First Horizon can source deposits from retail customers, wholesale funding markets, or Federal Home Loan Bank advances. Technology vendors are numerous, and while switching costs exist, no single supplier has meaningful pricing power.

The talent market represents perhaps the most significant "supplier" challenge, as competition for experienced bankers, technologists, and compliance professionals intensifies.

3. Bargaining Power of Buyers: MODERATE-HIGH

Large commercial clients have significant leverage—they can shop treasury management services, lending relationships, and capital markets execution across multiple banks. The largest corporates often maintain relationships with multiple banks simultaneously.

Retail consumers are increasingly rate-sensitive thanks to online comparison tools, though the switching costs of moving primary banking relationships remain material.

First Horizon's defense here is relationship depth. "Strong client relationships and our attractive business mix positioned us to deliver earnings through a complex interest rate cycle."

4. Threat of Substitutes: HIGH

This is perhaps the most significant long-term structural threat. Private credit funds are taking market share in middle-market lending. Payment apps are disintermediating transactions. Robo-advisors are competing for wealth management assets. Money market funds compete for deposits when rates rise.

The traditional regional bank model—gathering deposits and making loans—faces substitution pressure from multiple directions.

5. Industry Rivalry: HIGH

Regional banking is intensely competitive. More than ever, according to Bill Demchak, chairman, president and CEO at PNC Financial Services Group. According to Demchak, the Goliaths of the industry have been winning on organic deposit share growth, particularly from businesses. "That trend line has accelerated as a function of the mini-crisis in March [2023], where corporations bluntly didn't trust the regulatory environment to ensure that their deposits at a bank [were] safe. So we've seen those deposits flow uphill."

Hamilton's Seven Powers Analysis

1. Scale Economies: MODERATE

First Horizon has regional scale that provides cost advantages over smaller community banks. Technology investments, compliance infrastructure, and marketing expenses can be spread across a larger base.

But the company lacks the scale of national giants like JPMorgan Chase or Bank of America, which can invest billions annually in technology and still achieve superior cost ratios.

2. Network Effects: LIMITED

Banking generally lacks strong network effects—your deposit at First Horizon doesn't become more valuable because your neighbor also banks there.

The fixed income business may benefit from counterparty relationships and market-making positions, but these are modest compared to true network effect businesses.

3. Counter-Positioning: WEAK

First Horizon is not pursuing a differentiated strategy that incumbents cannot copy. "Regional relationship bank" is a well-understood model employed by Regions, Synovus, Pinnacle, and dozens of others.

4. Switching Costs: MODERATE

Commercial banking relationships are sticky. Treasury management, credit facilities, and commercial card programs are complex to switch. Once a CFO has integrated their ERP system with a bank's treasury management platform, there's meaningful friction to change.

Retail banking switching costs have declined with digital tools, though the hassle of changing direct deposits and automatic payments still creates meaningful retention.

5. Branding: MODERATE

Founded in 1864, First Horizon's banking subsidiary has been ranked by American Banker as No. 5 among the Top 10 Most Reputable U.S. Banks.

In Tennessee, the First Horizon brand carries real equity built over 160 years. Outside Tennessee, brand awareness is more limited. The yellow fever story, the TARP repayment, the TD Bank saga—these elements create a narrative of resilience that can be compelling for relationship-focused commercial clients.

6. Cornered Resource: WEAK

First Horizon does not control any unique resource that competitors cannot access.

7. Process Power: MODERATE

The company's underwriting processes, relationship management discipline, and credit culture have been refined over decades. The avoidance of major credit losses during recent stress periods suggests institutional competence in risk management.

Overall Assessment: First Horizon's competitive position rests primarily on its Tennessee market dominance, relationship depth with commercial clients, and the countercyclical benefits of its fixed income business. These are meaningful but not transformative advantages. The company operates in a competitive industry without dominant competitive moats.

Key Risks and Considerations

Credit Risk

Regional banks are inherently exposed to local economic conditions. First Horizon's concentration in the Southeast means that a regional economic downturn—whether from natural disasters, industry disruptions, or other factors—could disproportionately impact the loan portfolio.

However, the company's credit performance through recent cycles has been strong. First Horizon's net interest margin expanded by 2 basis points in Q4 2024. First Horizon's Q4 shows resilience with 2% adjusted earnings growth and improved credit metrics.

Interest Rate Sensitivity

Like all banks, First Horizon's net interest margin is sensitive to the shape of the yield curve and the pace of rate changes. Management has been working to reduce asset sensitivity and maintain flexibility across rate scenarios.

Regulatory and Compliance Risk

The TD Bank episode is a stark reminder that AML and BSA compliance failures can have profound consequences. While First Horizon was the victim rather than the perpetrator in that saga, the experience underscores the importance of robust compliance infrastructure.

M&A Execution Risk

As a mid-sized regional bank, First Horizon is both a potential acquirer and acquisition target. Any future M&A—whether buying or selling—carries integration risk, cultural challenges, and regulatory uncertainty.

Technology Disruption

The shift to digital banking continues to accelerate. While First Horizon has invested in technology, the company will need to continue significant investment to maintain competitive digital capabilities.

Key Performance Indicators for Monitoring

For long-term fundamental investors, three KPIs are particularly important to track:

1. Net Interest Margin (NIM)

NIM is the fundamental driver of banking profitability—the spread between what a bank earns on its assets and pays for its liabilities. First Horizon's NIM provides insight into competitive dynamics, balance sheet management, and the impact of interest rate changes on profitability.

2. Non-Interest Income as Percentage of Revenue

This ratio captures the diversification value of FHN Financial's fixed income business and wealth management fees. Higher non-interest income provides countercyclical benefits and reduces dependence on rate spreads.

3. Tennessee Deposit Market Share

First Horizon's dominant position in Tennessee is its most defensible competitive advantage. Tracking deposit market share in the Memphis metropolitan area and statewide provides insight into whether this core franchise is strengthening or eroding.

Bull Case and Bear Case

Bull Case

Scale benefits in growing markets: The Southeast continues to experience above-average population and economic growth. First Horizon is well-positioned to benefit from this secular tailwind.

Defensive Tennessee franchise: The company's dominant market share in Tennessee provides a stable earnings base that competitors will struggle to disrupt.

Countercyclical fixed income business: FHN Financial provides diversification benefits that are underappreciated, generating strong returns during periods of interest rate volatility.

Management credibility: Bryan Jordan has navigated the company through the 2008 financial crisis, the IberiaBank integration, and the TD Bank collapse. The management team has demonstrated resilience and strategic discipline.

Potential acquisition target: First Horizon remains an attractive franchise in a consolidating industry. A future acquirer may pay a meaningful premium for access to Tennessee markets and the Southeast footprint.

Bear Case

Scale disadvantage vs. mega-banks: JPMorgan Chase, Bank of America, and Wells Fargo can invest more in technology, offer more competitive rates, and absorb more regulatory burden. This scale advantage will likely widen over time.

Commodity deposit pricing: Rising rates and digital competition have made deposit pricing more competitive. The days of "sticky" low-cost deposits may be over, pressuring margins.

CRE exposure risk: Like many regional banks, First Horizon has commercial real estate exposure that could face stress if office and retail markets deteriorate further.

Limited growth optionality: Without M&A (which carries regulatory uncertainty), First Horizon's organic growth opportunities are constrained to its existing footprint.

Technology disruption: Fintech players and digital banks continue to erode traditional banking relationships, particularly with younger customers who may never develop branch-based banking habits.

Conclusion: A Survivor's DNA

The story of First Horizon is ultimately a story about institutional resilience. From Frank Davis opening a bank under martial law in 1864, to Charles Q. Harris keeping the doors open during yellow fever, to Bryan Jordan steering through the mortgage crisis and the TD Bank collapse—this is a company that has repeatedly demonstrated the ability to survive and adapt.

But survival is not the same as thriving. The regional banking model faces profound structural challenges: scale economics favor the giants, technology disruption threatens traditional relationships, and private capital competes for the best lending opportunities.

First Horizon's competitive position rests on three pillars: Tennessee market dominance, relationship depth with commercial clients, and the countercyclical benefits of its fixed income business. These advantages are real but not transformative.

For investors, the key question is whether relationship-based regional banking remains a viable long-term business model—or whether scale advantages will ultimately consolidate the industry into a handful of national players and a constellation of purely local community banks.

First Horizon has survived for 160 years by adapting to change. The next decade will test whether the company can do more than survive—whether it can thrive in an industry being reshaped by technology, regulation, and competitive dynamics that would have been unimaginable to Frank Davis as he drafted his charter application in occupied Memphis.

The bank that kept its doors open during yellow fever has proven it knows how to weather a crisis. The question now is whether it can navigate a transformation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube