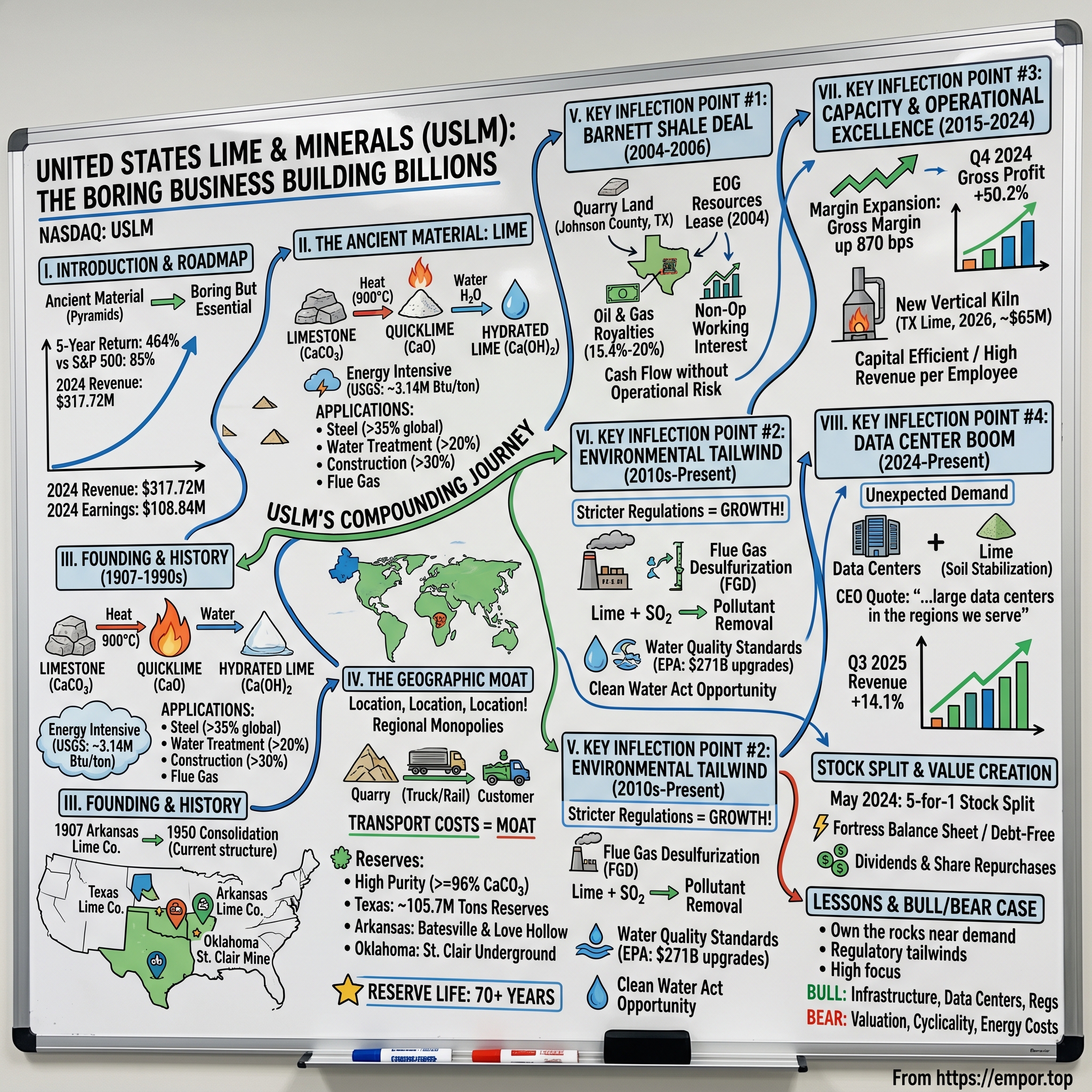

United States Lime & Minerals: The Boring Business Building Billions

I. Introduction & Episode Roadmap

Picture a material so fundamental to human civilization that the ancient Egyptians used it to build the pyramids. A substance so ubiquitous that it underpins everything from the steel in skyscrapers to the water flowing from municipal taps. Now imagine telling an investor in 2020 that a company extracting this exact material—unchanged in chemical composition for millennia—would deliver one of the most spectacular stock performances of the decade.

United States Lime & Minerals (NASDAQ: USLM) has generated a five-year return of 464%, crushing the S&P 500's 85% gain over the same period. The stock reached an all-time high in November 2024, capping a journey that transformed this sleepy industrial supplier into a wealth-compounding machine that would make even the most growth-obsessed Silicon Valley investor pause.

The company's story defies the narrative we've been conditioned to expect. There are no disruptive technologies here, no network effects, no viral growth loops. United States Lime & Minerals manufactures and supplies lime and limestone products in the United States. It extracts limestone from open-pit quarries and an underground mine, and processes it as pulverized limestone, quicklime, hydrated lime, and lime slurry.

The financial results speak for themselves. In 2024, USLM's revenue was $317.72 million, an increase of 12.94% compared to the previous year's $281.33 million. Earnings were $108.84 million, an increase of 46.00%. These aren't Silicon Valley growth rates, but they represent something arguably more valuable: consistent, profitable expansion backed by irreplaceable assets.

Gross profit saw substantial improvements, with Q4 2024 profit up 50.2% to $35.4 million and full-year profit increasing 40% to $144.0 million. Net income for Q4 reached $27.0 million ($0.94 per share), up 58.8%, while full-year net income grew 46% to $108.8 million ($3.79 per share).

What makes USLM fascinating isn't just the numbers—it's the strategic positioning that makes those numbers possible. This is a company that has built an almost impregnable competitive position through geographic proximity to customers, multi-decade mineral reserves, and operational excellence honed over more than a century.

This deep dive will trace USLM's evolution from its 1907 roots as the Arkansas Lime Company through its 1950 consolidation into the current corporate structure, examining the key inflection points that transformed a regional lime producer into a wealth-creating machine. Along the way, we'll explore the fascinating economics of bulk commodities, the unexpected synergy between lime production and natural gas royalties, and why environmental regulations—typically a headwind for industrial companies—have become one of USLM's most powerful tailwinds.

II. The Ancient Material: What Is Lime & Why Does It Matter?

Before understanding why USLM has been such a remarkable investment, one must first appreciate the peculiar economics and essential nature of lime itself. This is not merely an industrial commodity—it's a chemical transformation as old as human civilization.

The journey begins with limestone, a sedite sedimentary rock composed primarily of calcium carbonate (CaCO₃). When heated to temperatures exceeding 900°C in a process called calcination, the limestone releases carbon dioxide and transforms into calcium oxide—commonly known as quicklime or "burnt lime." The production of lime is highly energy-intensive, primarily due to the calcination process, which requires temperatures exceeding 900°C. According to the U.S. Geological Survey (USGS), producing one ton of lime consumes approximately 3.14 million British thermal units (Btu) of energy, making it one of the most energy-demanding industrial processes.

The chemistry continues when quicklime meets water. This highly exothermic reaction produces calcium hydroxide—hydrated lime or "slaked lime"—releasing enough heat to boil water on contact. This reactivity is precisely what makes lime so valuable across dozens of industrial applications.

The Lime and Limestone Operations manufactures lime and limestone products, supplying primarily the construction (including highway, road and parking lot contractors), metals (including steel producers), environmental (including municipal sanitation and water treatment facilities and flue gas treatment), oil and gas services, industrial (including paper and glass manufacturers), roof shingle and agriculture (including poultry and cattle feed producers) industries.

Consider the breadth of applications: Hydrated lime is used primarily in municipal sanitation and water treatment, in soil stabilization for highway, road and building construction, in flue gas treatment, in asphalt as an anti-stripping agent, as a conditioning agent for oil and gas drilling mud, in the production of chemicals and in the production of construction materials such as stucco, plaster and mortar. Lime slurry is used primarily in soil stabilization for highway, road and building construction.

The market dynamics are instructive. Lime is a critical chemical for key end-use industrial applications such as construction, metallurgy, chemicals, and environmental. The construction sector alone contributes more than 30% to national lime consumption, while water treatment accounts for over 20%.

The steel industry's dependence on lime deserves special attention. According to the European Lime Association, the steel industry is the largest consumer of calcium hydroxide and currently utilizes more than 35% of the products produced worldwide. In steelmaking, quicklime serves as a fluxing agent in blast furnaces and electric arc furnaces, purifying molten steel by forming slag that absorbs unwanted impurities like silica, phosphorus, and sulfur.

What makes lime particularly interesting from an investment perspective is its "boring but essential" quality. Unlike many commodities that face potential disruption from technological substitutes, lime's applications often have no practical alternatives. The product utilization to treat wastewater and flue gases is increasing as it can capture impurities such as lead and SOx gases. The stringent pollution control regulations in the U.S., China, and India are expected to raise the application of these products during the forecast period.

The global market provides context for USLM's positioning. The global lime market size reached USD 47.8 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 64.8 Billion by 2033, exhibiting a growth rate (CAGR) of 3.43% during 2025-2033. In the United States specifically, The U.S. lime market is projected to expand steadily due to rising water treatment infrastructure and growing demand from the construction and chemical sectors. Around 17 million tons of lime were produced in 2023, supported by 28 domestic companies.

The real insight here isn't that lime is growing explosively—it isn't. The insight is that lime demand is structurally embedded in civilization's basic functions. Water treatment, steel production, construction, environmental compliance—these aren't going away. And within this stable demand environment, companies that control the right quarries near the right customers can generate exceptional returns for shareholders.

III. Founding & Early History (1907–1990s)

The corporate entity known today as United States Lime & Minerals, Inc. carries within it the accumulated history of multiple lime businesses, their quarries, and their customer relationships stretching back more than a century.

The current entity, United States Lime & Minerals, Inc., was effectively formed in 1950 through the consolidation of several lime businesses. However, its roots go deeper, with predecessor companies operating much earlier, such as Arkansas Lime Company, founded in 1907. Operations were initially centered in the south-central United States, particularly Texas, Arkansas, and Oklahoma, leveraging the rich limestone deposits in these regions.

The choice of geography was no accident. The south-central United States sits atop some of North America's richest calcium limestone deposits, formed during the Cretaceous period when shallow seas covered much of what is now Texas and the surrounding states. The Edwards Limestone formation, in particular, contains exceptionally pure calcium carbonate—the raw material essential for high-quality lime production.

Rather than a single founding team, USLM emerged from the strategic combination of existing lime producers. Leadership evolved through the management of these consolidated entities. Specific details on the initial capitalization surrounding the 1950 consolidation are not readily public. The formation relied on the combined assets and operations of the merging companies.

The company was incorporated in 1950 and is headquartered in Dallas, Texas. What's notable about this corporate structure is its longevity and stability. United States Lime & Minerals, Inc. is a subsidiary of Inberdon Enterprises Ltd.

The Texas Lime Company operation near Cleburne, Texas, represents the crown jewel of this consolidated enterprise. The TLC mine began operations in the 1940s. USLM (formerly known as Rangaire Corporation) purchased TLC in the 1960s, which owned 458 acres in Johnson County, Texas, at the time. In the years that followed, TLC acquired additional acres of land resulting in the current ownership of approximately 5,200 acres of land in Johnson County, and built three rotary kilns, two of which have preheaters and are still in operation, as well as other operational and office facilities.

The Arkansas Lime Company, founded in 1907, brought the Batesville operation—a quarry situated on approximately 1,260 acres containing high-quality limestone resources in a bed averaging 60 feet in thickness. This exceptional bed thickness provides significant mining efficiency advantages over thinner deposits.

Colorado Lime acquired the Monarch Pass Quarry in November 1995 and has not carried out any mining on the property. The Monarch Pass Quarry, which had been operated for many years until the early 1990s, contains a mixture of limestone types, including high-quality calcium limestone and dolomite.

Throughout the latter decades of the twentieth century, USLM pursued a consistent strategy: accumulate high-quality reserves, maintain operational efficiency, and build lasting customer relationships in industries with steady lime demand. This wasn't a growth-at-all-costs approach. It was patient capital allocation focused on long-term competitive positioning.

USLM built a reputation for consistent profitability and returning value to shareholders through regular dividends and share repurchases, reflecting disciplined operational management and financial strength.

The foundation laid during these decades—the quarry positions, the customer relationships, the operational expertise—would prove remarkably durable. When new growth opportunities emerged in the 2000s and beyond, USLM possessed both the assets and the financial strength to capitalize on them.

IV. The Geographic Moat: Quarry Assets & Reserve Quality

In the lime industry, three words matter above all else: location, location, location. The economics of bulk commodity transportation create natural regional monopolies that are almost impossible to replicate.

Transportation costs can significantly impact the overall cost of lime, especially for long distances. Freight rates, fuel prices, and the mode of transportation (truck, rail, or barge) all contribute to the final price. Choosing a supplier closer to your location can reduce transportation expenses.

This insight is fundamental to understanding USLM's competitive position. United States Lime & Minerals, Inc., ("US Lime") is a public company traded on the NASDAQ Global Market under the symbol USLM and conducts its business through two segments: Lime and Limestone Operations, consisting of plants and facilities in Arkansas, Colorado, Louisiana, Oklahoma and Texas, serving markets in the Central United States; and Natural Gas Interests, consisting of natural gas wells on US Lime's Johnson County, TX, property in the Barnett Shale Formation.

The company's mineral reserves are nothing short of extraordinary. The Company's limestone mineral resources and reserves contain at least 96% calcium carbonate (CaCO₃). This exceptional purity translates directly into product quality and customer value.

Consider the Texas Lime Quarry, the company's flagship operation:

Texas Lime owns the Texas Lime Quarry and has crushed limestone, PLS, quicklime, and hydrated lime production facilities, located on approximately 5,200 acres of land in Johnson County, Texas that contains known high-quality limestone mineral resources in a bed averaging 25 to 35 feet in thickness. As of December 31, 2024, the total net book value of the Texas Lime Quarry was $14.2 million. As of December 31, 2024, the Texas Lime Quarry had 58.2 million tons of proven limestone mineral reserves and 47.5 million tons of probable limestone mineral reserves.

The Arkansas operations add additional depth to the reserve base. Arkansas Lime owns the Batesville Quarry and has crushed limestone, PLS, quicklime, and hydrated lime production facilities, located on approximately 1,260 acres of land located in Independence County, Arkansas that contains known high-quality limestone mineral resources in a bed averaging 60 feet in thickness. As of December 31, 2024, the Batesville Quarry had a net book value of $3.9 million. As of December 31, 2024, the Batesville Quarry had 8.2 million tons of indicated limestone mineral resources, 6.9 million tons of proven limestone mineral reserves, and 3.5 million tons of probable limestone mineral reserves. Based on forecasted production levels and recovery rates, the Company estimates that these reserves are sufficient to sustain its limestone operations for approximately 18 years.

The Love Hollow Quarry, acquired in 2005, represents strategic foresight:

In 2005, the Company acquired the Love Hollow Quarry, which is owned by ACT and associated with Arkansas Lime, located on approximately 2,500 acres of land in Izard County, Arkansas. In 2022, the Company improved and developed the transportation infrastructure between the Love Hollow Quarry and Arkansas Lime's production facilities, incurred other development costs to prepare the Love Hollow Quarry for mining, and began sourcing a portion of the Arkansas Lime plant's limestone requirements from the Love Hollow Quarry. As of December 31, 2024, the Love Hollow Quarry had a net book value of $5.4 million. As of December 31, 2024, the Love Hollow Quarry had 10.4 million tons of measured limestone mineral resources, 67.8 million tons of proven limestone mineral reserves, and 21.0 million tons of probable limestone mineral reserves.

The St. Clair Mine in Oklahoma adds underground mining capabilities to the portfolio:

St. Clair operates the St. Clair Mine and has crushed limestone, PLS, quicklime, and hydrated lime production facilities located on approximately 1,400 acres that it owns in Sequoyah County, Oklahoma containing high-quality limestone resources and also has long-term mineral leases that provide the right to mine high-quality limestone resources contained in approximately 1,340 adjacent acres. As of December 31, 2024, the St. Clair Mine had a net book value of $7.7 million. As of December 31, 2024, the St. Clair Mine had 7.8 million tons of measured limestone mineral resources, 129.7 million tons of indicated limestone mineral resources, and 22.0 million tons of proven limestone mineral reserves.

Why does reserve life matter so much? Because new quarry development faces increasing obstacles. The European Lime Association notes that quarrying operations face increasing opposition due to land-use conflicts, noise pollution, and dust emissions. For instance, stricter permitting processes under the EU's Environmental Impact Assessment Directive have delayed new projects.

This regulatory trend creates a widening moat around existing operations. USLM's competitors cannot simply buy land and start quarrying—they must navigate multi-year permitting processes, community opposition, and environmental reviews. Meanwhile, USLM continues extracting from quarries that have operated for decades, with reserves stretching 70+ years into the future.

The production infrastructure reflects decades of capital investment and operational refinement. The Texas Lime plant has an annual capacity of approximately 470 thousand tons of quicklime from two preheater rotary kilns. The plant also has PLS equipment, which, depending on the product mix, has the capacity to produce approximately 800 thousand tons of PLS annually. The Arkansas Lime plant is situated at the Batesville Quarry. Utilizing three preheater rotary kilns, this plant has an annual capacity of approximately 630 thousand tons of quicklime.

V. Key Inflection Point #1: The Barnett Shale Deal (2004–2006)

Sometimes the most valuable assets lie beneath those you already own. The story of USLM's natural gas interests illustrates how shrewd asset monetization can generate returns from resources a company never intended to develop.

In May 2004, the shale gas revolution was just beginning to transform American energy production. George Mitchell's decades of persistence with hydraulic fracturing techniques in the Fort Worth Basin had finally cracked the code, and major oil companies were scrambling to secure drilling rights in the Barnett Shale formation.

The Barnett Shale is known as an unconventional "tight" gas reservoir, indicating that the gas is not easily extracted. The shale is very impermeable, and it was virtually impossible to produce gas in commercial quantities from this formation until oil and gas companies learned how to effectively use massive hydraulic fracturing in the formation. The use of horizontal drilling further improved the economics, and made it easier to extract gas from under developed areas.

USLM found itself sitting on a strategic asset: approximately 3,800 acres in Johnson County, Texas—prime Barnett Shale territory—acquired decades earlier purely for limestone quarrying.

The Company, through its wholly owned subsidiary, U.S. Lime Company — O & G, LLC ("U.S. Lime O & G"), has royalty interests ranging from 15.4% to 20% and a 20% non-operating working interest with respect to oil and gas rights on the Company's approximately 3,800 acres of land located in Johnson County, Texas, in the Barnett Shale Formation. These interests are derived from the Company's May 2004 oil and gas lease agreement (the "O & G Lease") with EOG Resources, Inc.

EOG Resources, formerly Enron Oil & Gas Company before its 1999 spin-off, was emerging as one of the most aggressive and technically capable operators in the Barnett. During 2008, EOG continued to experience successful drilling in Johnson, Hill, and the western extension counties of the Barnett Shale gas play. Additionally, EOG saw successful drilling in the Barnett Combo play located in the northern portion of the Fort Worth Basin.

The genius of USLM's approach was structural: rather than attempting to become an oil and gas operator—a business it knew nothing about—the company secured royalty and non-operating working interests. This structure delivered cash flow without operational risk or capital expenditure requirements.

Through its wholly owned subsidiary, the company has royalty interests and working interests resulting in an overall average revenue interest of 34.8%, with respect to oil and gas rights in wells drilled on approximately 3,800 acres of land located in Johnson County, Texas, in the Barnett Shale Formation.

Consider what this deal accomplished: USLM monetized subsurface rights to land it already owned, securing decades of cash flow without disrupting its core lime quarrying operations. The limestone lies near the surface; the natural gas formations sit thousands of feet deeper. One asset has nothing to do with the other, except that USLM owns both.

From 2002 to 2010 the Barnett was the most productive source of shale gas in the US; it is now third, behind the Marcellus Formation and the Haynesville Shale. In January 2013, the Barnett produced 4.56 billion cubic feet per day, which made up 6.8% of all the natural gas produced in the US.

While natural gas production from the Barnett has declined from its peak, the royalty stream continues to contribute to USLM's cash flows. More importantly, the deal demonstrated management's ability to identify and capture value from non-core assets—a discipline that serves shareholders well across economic cycles.

VI. Key Inflection Point #2: Environmental Regulations Tailwind (2010s–Present)

The conventional wisdom suggests that environmental regulations burden industrial companies with compliance costs, hamper expansion, and squeeze margins. For USLM, the reality has been precisely the opposite: stricter environmental standards have become a secular growth driver.

Flue-gas desulfurization (FGD) is a set of technologies used to remove sulfur dioxide (SO₂) from exhaust flue gases of fossil-fuel power plants, and from the emissions of other sulfur oxide emitting processes such as waste incineration, petroleum refineries, cement and lime kilns. Since stringent environmental regulations limiting SO₂ emissions have been enacted in many countries, SO₂ is being removed from flue gases by a variety of methods.

The chemistry is elegant in its simplicity. Lime-based scrubbing systems work because quicklime and hydrated lime are alkaline—they neutralize acidic pollutants like sulfur dioxide. Common methods used: Wet scrubbing using a slurry of alkaline sorbent, usually limestone or lime, or seawater to scrub gases; Spray-dry scrubbing using similar sorbent slurries; Dry sorbent injection systems that introduce powdered hydrated lime.

The effectiveness is remarkable: For a typical coal-fired power plant, FGD systems will remove ~95% of the SO₂ in the flue gases.

This creates a structural demand driver that grows with environmental stringency. In 2023, the U.S. wastewater treatment sector used over 3 million metric tons of lime, as reported by the U.S. Environmental Protection Agency (EPA). This figure is expected to rise as cities upgrade their water treatment facilities to comply with stricter water quality standards. The Clean Water Act's requirements for improved water treatment processes present a growing market opportunity for lime suppliers.

The water treatment opportunity is particularly significant given the scale of infrastructure investment required. The U.S. Environmental Protection Agency (EPA) highlights that lime-based treatments are cost-effective and environmentally sustainable, making them a preferred choice for municipalities and industries. In the United States, the EPA estimates that $271 billion will be required over the next two decades to upgrade aging wastewater infrastructure, creating a substantial market for lime.

The irony is rich: a company extracting minerals from the earth has benefited enormously from regulations designed to protect the environment. This isn't because lime production is particularly clean—the calcination process itself generates significant CO₂ emissions. Rather, lime serves as an essential input for the pollution control systems that other industries must install.

Coal-fired boiler has been a major emission source of atmospheric pollutants like smoke and nitrogen oxide, especially sulfur dioxide (SO₂), affecting the environment seriously. Approximately 85% of the flue gas desulfurization units installed in the US are wet scrubbers, 12% are spray dry systems, and 3% are dry injection systems.

USLM's customer base reflects this environmental demand. The company supplies its products primarily to the construction customers, including highway, road, and building contractors; industrial customers, such as paper and glass manufacturers; environmental customers comprising municipal sanitation and water treatment facilities, and flue gas treatment processes; oil and gas services companies; roof shingle manufacturers; and poultry producers.

The regulatory tailwind extends beyond pollution control. Lime is essential for soil stabilization in construction, helping projects meet increasingly stringent foundation requirements. It's used in mining operations to meet water discharge standards. It's applied in agricultural settings to improve soil pH under sustainable farming practices.

Each regulatory tightening—whether targeting air quality, water quality, or construction standards—tends to increase, not decrease, lime demand. This creates a fundamentally different risk profile than most industrial businesses face.

VII. Key Inflection Point #3: Capacity Expansion & Operational Excellence (2015–2024)

The decade from 2015 to 2024 witnessed USLM's transformation from a quietly profitable regional player into a margin-expanding powerhouse. This wasn't achieved through dramatic strategic pivots or transformative acquisitions—it emerged from relentless operational improvement and disciplined capital allocation.

The Company operates lime and limestone plants and distribution facilities in Arkansas, Colorado, Louisiana, Missouri, Oklahoma and Texas through its subsidiaries, Arkansas Lime Company, ART Quarry TRS LLC, Colorado Lime Company, Mill Creek Dolomite, LLC, Texas Lime Co.

The margin expansion story is remarkable. Gross profit saw substantial improvements, with Q4 2024 profit up 50.2% to $35.4 million and full-year profit increasing 40% to $144.0 million. This 870 basis point improvement in annual gross margins reflects successful price optimization and operational efficiency.

The net profit margin of United States Lime & Minerals (USLM) is 34.26%. The operating profit margin of United States Lime & Minerals (USLM) is 39.32%.

These are exceptional numbers for a bulk commodity business. Most materials companies would celebrate operating margins in the low teens; USLM operates closer to software industry margins.

The workforce reflects the capital-efficient nature of the business. As of Aug 27, 2025, the company has 345 employees. Generating over $300 million in revenue with fewer than 350 employees translates to revenue per employee exceeding $900,000—a testament to the capital-intensive but labor-efficient nature of modern lime production.

A key strategic investment currently underway demonstrates management's commitment to capacity expansion. Construction began in 2024 on a new vertical kiln at the Texas Lime Company plant, with estimated costs of $65 million and completion expected in 2026.

This kiln investment represents the largest capacity expansion in recent company history and positions USLM to capture growing demand from construction and environmental customers.

Management's commentary on operational performance has consistently emphasized the interplay between pricing discipline and cost management. USLM's lime and limestone gross profit in the first quarter was $30.7 million. That total is up 27.5 percent from the first quarter of 2023, with a decrease in operating expenses – including lower natural gas costs – playing a role.

The energy intensity of lime production means that natural gas prices significantly impact operating costs. Management has demonstrated skill in optimizing fuel blends and hedging strategies to mitigate this exposure.

VIII. Key Inflection Point #4: Data Center & Infrastructure Boom (2024–Present)

In 2024, an unexpected demand driver emerged that highlighted USLM's positioning at the intersection of old-economy materials and new-economy infrastructure: the data center construction boom.

"We are pleased with the Company's continued strong financial performance in the third quarter 2025. Demand from our construction customers remained solid, supported by the construction of large data centers in the regions that we serve," said Timothy W. Byrne, President and Chief Executive Officer.

The connection between lime and data centers may not be immediately obvious. Data centers require massive foundations to support the weight of servers, power equipment, and cooling systems. Soil stabilization—one of lime's core applications—is essential for these projects.

Revenues increased in the first nine months 2025, compared to the first nine months 2024, primarily due to a 13.3% increase in sales volumes of our lime and limestone products, which was principally due to increased demand from our construction, including for the construction of large data centers, environmental, and steel customers, partially offset by decreased demand from our oil and gas services customer, and a 6.6% increase in the average selling prices for our lime and limestone products. Looking ahead, we anticipate ongoing data center construction demand being partially offset by softer demand from some of the other industries that we serve.

The Q3 2025 results demonstrate the strength of this demand driver:

United States Lime & Minerals (NASDAQ: USLM) reported Q3 2025 revenue of $102.0 million, up 14.1% from Q3 2024, and nine-month 2025 revenue of $284.8 million, up 19.8% year-over-year. Gross profit for Q3 was $52.2 million (+21.1% YoY) and nine-month gross profit was $140.2 million (+29.2% YoY). Net income was $38.8 million ($1.35 diluted) for Q3 and $103.7 million ($3.61 diluted) for the first nine months.

As of September 30, 2025, United States Lime & Minerals Inc (USLM, Financial) reported total assets of $652.8 million, up from $543.2 million at the end of 2024. The company's stockholders' equity increased to $602.3 million from $497.7 million, reflecting its strong financial position.

The broader construction industry context supports continued strength. Data centers and infrastructure builds dominated public contractors' Q3 earnings calls.

What makes the data center opportunity particularly attractive for USLM is its geographic concentration. A general view of the Google Midlothian Data Center on Nov. 14, 2025, in Midlothian, Texas. Texas—where USLM's flagship Texas Lime operation is located—has emerged as a major hub for data center construction, driven by favorable energy costs, tax incentives, and land availability.

The diversity of USLM's customer base provides stability even as individual end markets fluctuate. The company cited higher sales volumes and average selling prices, driven by construction, environmental and steel customers, partly offset by weaker oil and gas services demand.

IX. The Stock Split & Shareholder Value Creation

In May 2024, USLM's Board of Directors made a decision that reflected both the company's success and its commitment to shareholder accessibility: a 5-for-1 stock split.

DALLAS, May 06, 2024 (GLOBE NEWSWIRE) -- United States Lime & Minerals, Inc. (NASDAQ: USLM) (the "Company") today announced that it will conduct a split of its outstanding shares of common stock at a ratio of 5:1, effected in the form of a stock dividend of four additional shares of common stock for each share outstanding. The Company's Board of Directors determined that, with the significant growth of the trading price for the Company's common stock over the past several years, the stock split is appropriate to make the Company's common stock more affordable on a per-share basis to certain investors and employees and to narrow the bid and ask prices of the common stock.

The dividend of shares to be issued in the stock split will be payable after the market close on Friday, July 12, 2024 to shareholders of record at the close of business on June 21, 2024. Shareholders will receive a dividend of four additional shares of common stock for each share held. The Company's common stock will begin trading on a post-split basis at the market open on Monday, July 15, 2024, under the Company's existing trading symbol "USLM."

The split will issue four additional shares for each outstanding share, increasing the total outstanding shares from 5.7 million to 28.5 million.

The stock split itself doesn't create value—it simply divides the same pie into more pieces. But it signals management's recognition that the stock price appreciation had potentially limited accessibility for retail investors and employee stock programs.

The dividend policy reflects the company's shareholder-friendly orientation. The company completed a 5-for-1 stock split in July 2024 and declared an increased quarterly dividend of $0.06 per share, payable March 14, 2025.

The balance sheet position is particularly noteworthy for an industrial company. USLM boasts a dominant regional position, a debt-free balance sheet, and robust free cash flow, making it a compelling, low-risk industrial investment.

This fortress balance sheet provides strategic flexibility. Management can pursue acquisitions opportunistically, invest in capacity expansion during downturns, or simply weather cyclical weakness without distress. For shareholders, it means the equity isn't leveraged against commodity price volatility or economic cycles.

X. Porter's Five Forces Analysis

Understanding USLM's competitive position requires systematic analysis of the industry forces shaping profitability.

1. Threat of New Entrants: LOW

Barriers to entry in the lime industry are substantial and rising. The European Lime Association notes that quarrying operations face increasing opposition due to land-use conflicts, noise pollution, and dust emissions. For instance, stricter permitting processes under the EU's Environmental Impact Assessment Directive have delayed new projects.

The capital requirements are substantial. Developing a new quarry requires land acquisition, environmental permitting (often taking years), mining equipment, processing facilities, and transportation infrastructure. A new entrant would need to compete against established players with multi-decade reserve lives and depreciated capital bases.

USLM's reserve position creates an almost insurmountable barrier. With reserves sufficient for 70+ years at current production rates, the company can amortize its capital investments over extraordinarily long timeframes.

2. Bargaining Power of Suppliers: LOW

USLM's vertical integration from limestone extraction through processing to distribution minimizes supplier power. The company owns its quarries—it doesn't purchase limestone from third parties. The primary input cost is energy (natural gas for the calcination process), which is a commodity purchased in competitive markets.

3. Bargaining Power of Buyers: MODERATE

USLM serves a diversified customer base with no excessive concentration. The company supplies approximately 600 customers across construction, environmental, industrial, steel, and agricultural applications. This diversification prevents any single customer from exercising undue pricing leverage.

However, buyers do have some power in bulk commodity markets. Lime competes with other materials for certain applications, and customers can sometimes substitute or source from alternative suppliers in adjacent regions.

4. Threat of Substitutes: LOW-MODERATE

Effectiveness: Both lime and limestone are highly effective at neutralising the acidic SO₂, converting it into harmless compounds. Availability and Cost: Limestone, in particular, is widely available, cheap, and easy to access, making it a preferred choice for many operations.

For many applications, lime has no practical substitutes. Water treatment processes, flue gas desulfurization, and steel production have used lime for decades because no alternative provides comparable effectiveness at reasonable cost. However, for some construction applications, competing materials exist.

5. Competitive Rivalry: MODERATE (but regionally LOW)

The lime industry is relatively consolidated, with a handful of large players (Lhoist, Carmeuse, Graymont, Mississippi Lime) alongside regional specialists like USLM. Transportation costs can significantly impact the overall cost of lime, especially for long distances. Freight rates, fuel prices, and the mode of transportation (truck, rail, or barge) all contribute to the final price.

This transportation economics creates regional competition dynamics. Within its Central United States footprint, USLM faces limited competition from distant producers. The cost of shipping lime hundreds of miles makes local suppliers strongly preferred.

XI. Hamilton's 7 Powers Framework Analysis

Hamilton Helmer's 7 Powers framework provides a complementary lens for understanding USLM's sustainable competitive advantages.

1. Scale Economies: PRESENT

USLM operates through its dedicated Lime and Limestone Operations segment, ensuring that every stage of the production process—from extraction to distribution—is conducted with a focus on efficiency and sustainability. The company's network of wholly owned subsidiaries enhances its operating footprint across several key states including Arkansas, Colorado, Louisiana, Missouri, Oklahoma, and Texas.

The company's production scale allows fixed costs to be spread across larger volumes, reducing per-unit costs. Larger kilns operate more efficiently than smaller ones, and larger quarries benefit from lower extraction costs per ton.

2. Network Effects: ABSENT

Lime is a bulk commodity without network effects. Each customer's purchase doesn't make the product more valuable to other customers. This power is simply not applicable to the business model.

3. Counter-Positioning: WEAK

USLM's focus on lime and limestone, while larger competitors diversify into cement and aggregates, represents mild counter-positioning. The company has chosen to remain a specialist rather than becoming a diversified materials conglomerate. However, larger competitors could plausibly replicate this focus if they chose.

4. Switching Costs: MODERATE

For industrial customers like steel producers and water treatment facilities, switching lime suppliers involves qualification testing, logistics reconfiguration, and relationship disruption. These aren't insurmountable barriers, but they create customer stickiness that favors incumbents.

5. Branding: WEAK

As a B2B commodity supplier, USLM doesn't benefit from consumer brand recognition. What matters is reliability, product quality, and delivery consistency—not brand equity.

6. Cornered Resource: STRONG ⭐

This is USLM's most powerful competitive advantage. Texas Lime owns the Texas Lime Quarry and has crushed limestone, PLS, quicklime, and hydrated lime production facilities, located on approximately 5,200 acres of land in Johnson County, Texas that contains known high-quality limestone mineral resources in a bed averaging 25 to 35 feet in thickness.

The Company's limestone mineral resources and reserves contain at least 96% calcium carbonate (CaCO₃).

High-quality limestone reserves in favorable geographic locations are finite resources that cannot be replicated. USLM's quarry positions represent decades of accumulated land acquisition that new entrants cannot easily duplicate.

7. Process Power: STRONG ⭐

Decades of operational experience have created embedded organizational knowledge in kiln operations, mining techniques, and logistics management. This institutional knowledge compounds over time and is difficult for competitors to observe and replicate.

XII. The Playbook: Business & Investing Lessons

USLM's success offers several lessons that extend well beyond the lime industry.

Lesson 1: Geographic Moats in Bulk Commodities

Transportation economics create natural regional advantages that can persist indefinitely. "Own the rocks near the demand" isn't glamorous advice, but it's proven remarkably lucrative.

Lesson 2: The Power of Focus

USLM has resisted the temptation to diversify into adjacent businesses like cement or aggregates. This focus has allowed the company to develop deep expertise in lime production while avoiding the integration challenges that often plague diversifying acquisitions.

Lesson 3: Regulatory Tailwinds as Secular Growth

Environmental regulations transformed what could have been a cyclical commodity into a growth story. Investors should look for industries where regulation increases rather than decreases demand.

Lesson 4: Accidental Diversification Can Be Golden

The Barnett Shale natural gas royalties came from land USLM already owned for limestone quarrying. The lesson: understand what assets sit beneath your primary business.

Lesson 5: Fortress Balance Sheets Enable Opportunism

USLM's net cash position provides strategic flexibility that leveraged competitors lack. The company can invest through cycles, pursue acquisitions without financing risk, and weather downturns without distress.

XIII. Bull vs. Bear Case

Bull Case:

The secular trends supporting USLM's business are compelling and durable. The U.S. lime market is projected to expand steadily due to rising water treatment infrastructure and growing demand from the construction and chemical sectors.

The Hydrated Lime market is projected to grow at a CAGR of 5.2% between 2024 and 2034, reaching a value of USD 29.77 billion by 2034. The Hydrated Lime Market is projected to grow at a 5.2% CAGR from 2024 to 2035, driven by increasing demand in construction, environmental regulations, and industrial applications.

The data center construction boom provides multi-year demand visibility, particularly in Texas where USLM's largest operations are located. The $65 million vertical kiln investment positions the company to capture this growing demand.

Environmental regulations continue tightening, driving structural demand for lime in flue gas treatment and water purification. The $271 billion EPA estimate for wastewater infrastructure upgrades represents decades of potential demand.

USLM's reserve position ensures supply security for 70+ years, while competitors face increasing permitting obstacles for new quarry development. The geographic moat around existing operations widens over time.

Bear Case:

The stock's valuation has expanded significantly, potentially pricing in much of the growth opportunity. At current multiples, any demand weakness could trigger meaningful multiple compression.

The implementation of stringent environmental regulations in some countries regulating the production of lime, the escalating levels of competition between industry players, and the depletion of high-quality limestone, which is reducing the prevalence of raw material sources, are among the major market challenges. Moreover, the fluctuating product demand, on account of macroeconomic factors affecting end-use sectors, such as steel, iron, construction, etc., is also of growing concern.

Construction demand is cyclical, and any economic slowdown would impact volumes. The steel industry—a major lime consumer—faces structural challenges from decarbonization initiatives that could reduce domestic production.

Energy costs (particularly natural gas) remain a key input, and price volatility can pressure margins. The calcination process itself generates CO₂ emissions, potentially exposing the company to future carbon regulations.

XIV. Key Performance Indicators

For investors monitoring USLM's ongoing performance, three KPIs merit particular attention:

1. Gross Margin % — This is the single most important metric for understanding pricing power and operational efficiency. USLM's gross margin expansion from the low 30s to over 50% has driven the stock's outperformance. Any deterioration would signal competitive pressure or cost inflation that management cannot pass through.

2. Lime & Limestone Revenue Growth — Tracking the core lime segment (excluding natural gas interests) provides visibility into underlying demand trends. Watch for volume growth versus price increases—sustainable growth requires both.

3. Capital Expenditure as % of Revenue — USLM operates a capital-intensive business requiring ongoing investment in quarry development and processing equipment. Capex levels indicate management's confidence in demand visibility and return expectations.

The USLM story isn't about disruption or reinvention. It's about the compounding power of owning scarce, essential resources positioned near growing demand. For more than a century, this company has extracted limestone, processed it into lime, and delivered it to customers who cannot function without it. The fundamental business model hasn't changed. What has changed is the recognition—reflected in the stock price—that some "boring" businesses are anything but.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube