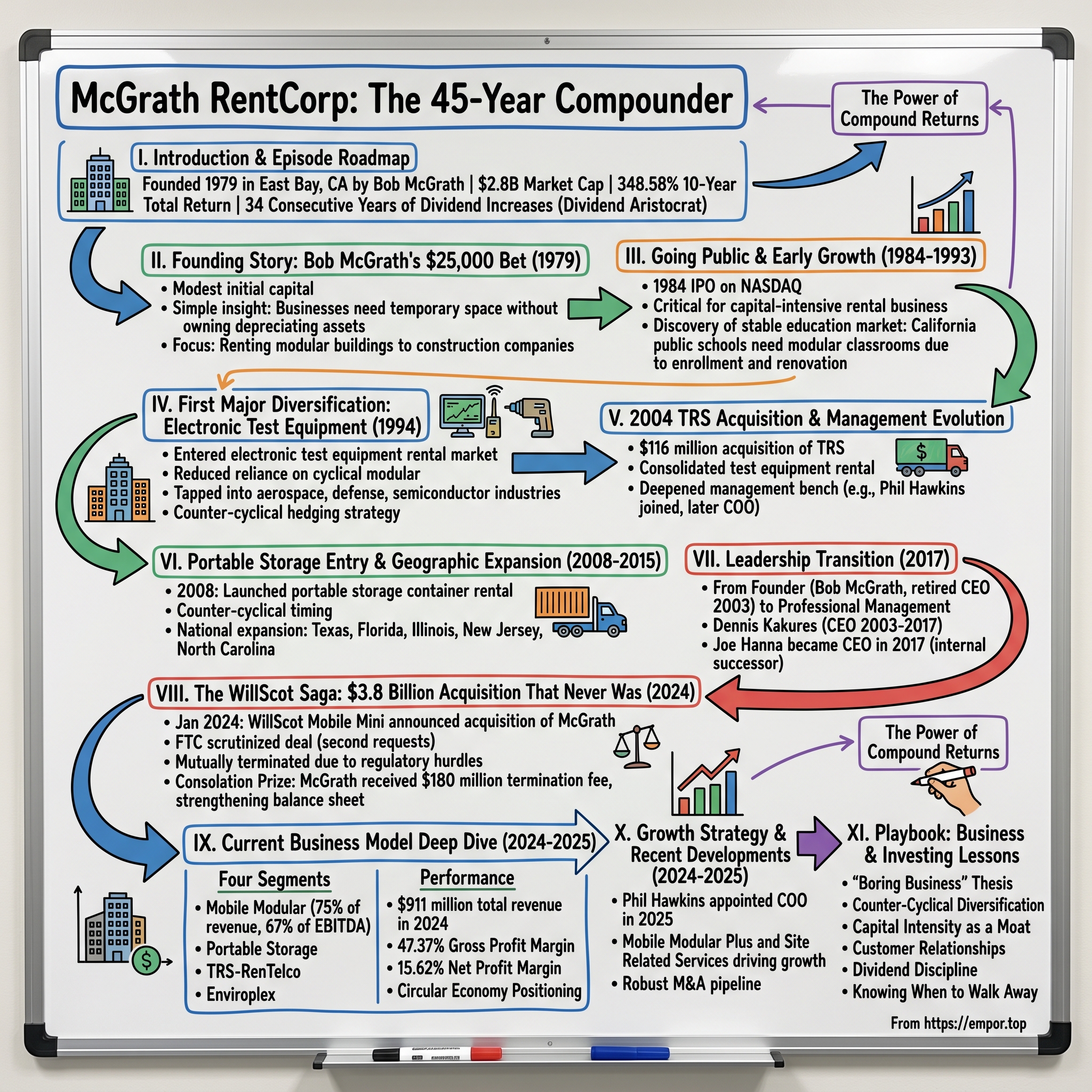

McGrath RentCorp: The 45-Year Compounder You've Never Heard Of

I. Introduction & Episode Roadmap

Picture this: It's 1979, and somewhere in the East Bay of California, a man with an electrical engineering degree from Notre Dame is betting $25,000 of his friends' and family's money on a seemingly mundane proposition—renting out mobile offices to construction companies. No revolutionary technology. No venture capital. No grand vision of disrupting an industry. Just a simple insight: businesses need temporary space, but they don't want to own depreciating boxes.

McGrath was founded by Bob McGrath on a small two-acre inventory center in San Leandro, California. Forty-five years later, that modest bet has compounded into something remarkable. The market cap of McGrath RentCorp (MGRC) is approximately $2.8 billion.

The 10-year total return for MGRC stock is 348.58%. That's not a typo. A business that rents modular buildings and electronic test equipment has delivered nearly 4.5x returns over a decade—all while flying under the radar of most investors who chase the latest tech unicorns.

But here's what makes the McGrath story truly extraordinary: The year 2025 marks 34 consecutive years that McGrath RentCorp has raised its dividend to shareholders. In an era when companies routinely slash dividends at the first sign of trouble, McGrath has increased its payout every single year since 1992—through the dot-com bust, the Great Financial Crisis, COVID-19, and everything in between. Few firms exemplify this better than McGrath RentCorp (MGRC), which has now extended its dividend growth streak to 34 consecutive years, positioning it as a rare "dividend aristocrat" in the rental industry.

The company that started on two acres now operates as a business-to-business rental company in the United States and internationally that rents and sells relocatable modular buildings, portable storage containers, and electronic test equipment. The company operates through four segments: Mobile Modular, Portable Storage, TRS-RenTelco, and Enviroplex.

This is the story of how boring can be beautiful—how a customer-obsessed culture, disciplined capital allocation, and counter-cyclical diversification created one of the most consistent compounders in American small-cap history. It's also the story of a $3.8 billion acquisition that never happened, an FTC intervention that handed McGrath $180 million in cash, and why the company that almost got swallowed by its larger competitor may emerge stronger than ever.

II. Founding Story: Bob McGrath's $25,000 Bet (1979)

The Origin of a Compounder

The late 1970s were an era of stagflation, energy crises, and economic uncertainty. Yet in California, something else was happening: a construction boom was transforming the Golden State's landscape. Office parks sprouted across Silicon Valley. Schools struggled to accommodate baby boomers' children. And everywhere you looked, construction crews needed temporary space.

The company was founded by Robert P. McGrath. The initial capital was raised with $25,000 from friends and family. Founded as Mobile Modular Management Corporation, focused on renting and selling mobile offices in California.

Bob McGrath wasn't a typical entrepreneur. He graduated from the University of Notre Dame in 1955 with a bachelor's degree in electrical engineering. But it wasn't engineering that shaped his business philosophy—it was a deep understanding of customer economics and asset utilization.

The business model insight was elegant in its simplicity: construction companies, schools, and corporations need temporary space, but they don't want to own depreciating assets. Why would a contractor buy a mobile office for $50,000 when the project would be done in eighteen months? Why would a school district purchase portable classrooms when enrollment fluctuations meant they might not need them in five years?

McGrath saw the opportunity to be the bridge—owning the assets that customers needed but didn't want to hold on their balance sheets. It was a classic rental economics play: high upfront capital investment creates barriers to entry, while long rental durations create predictable revenue streams.

Building the Foundation

The early days weren't glamorous. Mobile Modular Management Corporation, founded in 1979 by Bob McGrath, is the original business that led to the creation of McGrath RentCorp in 1984. Headquartered in Livermore, California, it began on two acres in the East Bay and expanded across Southern California and Texas.

What distinguished McGrath from day one was an almost obsessive focus on customer service. "For more than 40 years, we have pursued a relentless customer-centric approach." This wasn't just marketing copy—it was the foundation of a culture that would persist for decades.

Joan, a former nun and native San Franciscan, earned a master's in theology at USF and later became a high school teacher. She was principal of the Sacred Heart School in Atherton, California when she met and married Bob. She then joined the McGrath Corporation as executive vice president, developing the sales team and helping to lead the company until its successful public offering.

The McGrath family partnership wasn't just a marriage—it was a business alliance that combined Bob's operational acumen with Joan's talent for building and motivating sales teams. Together, they created something rare: a rental company that treated every customer interaction as an opportunity to build a relationship, not just close a transaction.

By the early 1980s, the company had proven its model worked. The California construction boom provided the perfect launching pad, and McGrath's reputation for reliability and service created organic growth. But Bob McGrath understood that staying private would limit the company's potential. To truly scale a capital-intensive rental business, you need access to capital markets.

III. Going Public & Early Growth (1984-1993)

The IPO Decision

In 1984, just five years after founding, Bob McGrath made a bold decision that would shape the company's trajectory for decades: going public.

As an investment banker, Mr. Dawson assisted in three public equity offerings for McGrath RentCorp, beginning with its initial public offering in 1984. William Dawson, who would later join McGrath's board of directors, helped orchestrate the company's transition from a small private operation to a publicly traded entity on the NASDAQ.

Why go public so early? The answer lies in the fundamental economics of the rental business. Unlike software companies that can scale with minimal capital investment, rental businesses are inherently asset-heavy. Every new customer requires additional inventory. Every geographic expansion demands warehouse space and fleet purchases. Without access to public equity markets and the credibility they provide for debt financing, growth would be constrained by retained earnings alone.

Based on 1984 IPO through 12/31/22 assuming reinvestment of dividends. The company's sustainability report highlights this long track record, demonstrating how early access to capital markets enabled decades of compound growth.

The Education Market Discovery

The period between the IPO and the mid-1990s represented a critical phase of market discovery. While commercial construction remained cyclical—booming in good times, collapsing during recessions—McGrath identified a more stable customer segment: education.

The Mobile Modular segment rents and sells modular buildings designed for use as classrooms, temporary offices adjacent to existing facilities, sales offices, construction field offices, restroom buildings, health care clinics, child care facilities, office spaces, and various other purposes.

California's public schools faced a chronic problem: enrollment fluctuations that made permanent construction risky, combined with aging infrastructure that required temporary solutions during renovations. Modular classrooms offered the perfect answer—rapid deployment, lower cost than permanent construction, and the flexibility to remove or relocate units as needs changed.

This wasn't just diversification—it was counter-cyclical hedging. When commercial construction slowed during recessions, school districts often maintained or increased their modular needs. Budget constraints actually favored rentals over new construction, and temporary facilities became essential during renovation projects funded by bond measures.

During his tenure as CEO, McGrath built one of the most successful publicly traded rental businesses on Wall Street. Under Mr. McGrath's leadership as CEO, the Company was recognized five times as one of the "Top 200 Best Small Public Companies" by Forbes Magazine.

The combination of commercial and educational customers created a revenue base that was more resilient than pure-play construction rentals. This insight—that customer mix matters as much as market share—would become a recurring theme in McGrath's strategic evolution.

IV. The First Major Diversification: Electronic Test Equipment (1994)

Strategic Expansion into Tech Rentals

By the mid-1990s, McGrath had established itself as California's leading modular building rental company. But Bob McGrath and his leadership team recognized a limitation: geographic expansion in the modular business was capital-intensive and slow. They needed another growth vector.

In 1994, the company strategically expanded into the electronic test equipment rental market. This move reduced reliance on the cyclical modular building sector and tapped into industries with steady demand, providing a more stable revenue stream.

On the surface, renting oscilloscopes and spectrum analyzers seems utterly unrelated to renting portable classrooms. But the underlying business logic was identical: customers need expensive equipment temporarily, they don't want to own depreciating assets, and they value service and reliability over the lowest price.

The TRS-RenTelco segment rents and sells general purpose electronic test equipment, such as oscilloscopes, amplifiers, analyzers, signal source, and power source test equipment primarily to aerospace, defense, electronics, industrial, research, and semiconductor industries. This segment also provides communications test equipment, including network and transmission test equipment for various fiber, copper, and wireless networks.

The Genius of Counter-Cyclical Diversification

Here's where McGrath's strategic thinking becomes truly impressive. The electronic test equipment business serves aerospace, defense, semiconductor, and telecommunications industries. These sectors have their own cycles—but they're often inversely correlated with construction.

When the economy slows and commercial construction collapses, companies don't stop investing in research and development. If anything, competitive pressures during downturns accelerate R&D spending as companies seek the next breakthrough product. Semiconductor companies still need to test chips. Defense contractors still need to validate equipment. Telecom providers still need to install and test networks.

The rental model arbitrage is particularly powerful in test equipment. A cutting-edge spectrum analyzer might cost $100,000 and become obsolete within five years as technology advances. Why would a company buy such equipment for a six-month project when they can rent it for a fraction of the cost? McGrath absorbed the depreciation risk and earned returns by maximizing utilization across multiple customers.

This diversification also provided operational synergies that aren't immediately obvious. Both modular buildings and test equipment require calibration, maintenance, refurbishment, and logistics expertise. McGrath's infrastructure for managing and tracking rental assets could be leveraged across product categories.

V. The 2004 TRS Acquisition & Management Evolution

Consolidation in Electronic Test Equipment

By 2004, McGrath had operated its electronic test equipment rental business for a decade. But the real transformation came through acquisition.

"The transaction is for approximately $116 million in cash and is expected to close by May 31, 2004. Based in Dallas, Texas, TRS is a leading rental provider of general purpose and communications test equipment in North America." The CEO at the time declared: "The TRS acquisition has great strategic importance for our core test equipment rental business."

This was McGrath's largest acquisition to date—a bet that consolidation could create a dominant player in the fragmented test equipment rental market. "Over the past 30 years TRS has built a very successful rental business serving large and middle market companies with both general purpose and communications test equipment. Comparatively, RenTelco has created its success by serving the test equipment rental needs of smaller companies, especially communications contractors, installers and integrators."

Building Management Depth Through Acquisitions

What's often overlooked in M&A analysis is the talent dimension. Acquisitions don't just bring assets and customers—they bring people. And McGrath used the TRS acquisition to deepen its management bench.

Mr. Hawkins joined the Company in 2004 with the acquisition of TRS, an electronics equipment rental division of CIT Technologies Corporation, where he held the position of Senior Business Analyst for Technology Rentals and Services (TRS).

Philip Hawkins would spend the next two decades rising through McGrath's ranks, eventually becoming Chief Operating Officer in 2025. His trajectory illustrates McGrath's "promote from within" culture—the company didn't just acquire TRS's equipment and customers; it acquired the people who knew how to run the business and gave them room to grow.

John P. Skenesky currently serves as Vice President and Division Manager of TRS-RenTelco, a position he has held since November 2011. He previously served as the division's Director of Sales and Product Management from June 2007 to November 2011 and Director of Operations and Product Management from June 2004 to June 2007. Mr. Skenesky joined the Company in 1995 and has held various leadership roles within the RenTelco division, including branch management and sales.

This pattern—identifying talented operators, giving them increasing responsibility, and promoting them into leadership—would become a hallmark of McGrath's management philosophy. It created institutional knowledge that competitors couldn't easily replicate and alignment between management incentives and long-term shareholder value.

VI. Portable Storage Entry & Geographic Expansion (2008-2015)

Launching Through the Great Recession

The timing seems almost reckless in hindsight. In 2008, as the global financial system teetered on collapse and construction activity plummeted, McGrath launched a new business line.

In 2008, the Company entered the portable storage container rental business under the trade name Mobile Modular Portable Storage.

Bold or reckless? The answer reveals something fundamental about McGrath's strategic thinking. Launching during a recession meant acquiring storage containers at distressed prices, hiring talent from competitors cutting headcount, and building market presence when others were retrenching.

The Portable Storage segment offers steel containers, such as storage and office containers to provide a temporary storage solution to construction, retail, commercial and industrial, energy and petrochemical, manufacturing, education, and healthcare markets.

The portable storage business shares the same economic logic as modular buildings and test equipment: customers need temporary solutions but don't want to own depreciating assets. Storage containers serve construction sites, retail overflow during seasonal peaks, industrial facilities requiring temporary warehousing, and countless other applications.

Geographic Footprint Expansion

The 2008-2015 period also marked McGrath's push beyond California. Today, the business is located in the key markets of California, Texas, Florida, Northern Illinois, New Jersey and most recently entered the North Carolina region.

Geographic expansion in rental businesses follows a specific logic. Each new market requires significant upfront investment—warehouse facilities, delivery vehicles, inventory, and local sales teams. But once established, a regional presence creates barriers to competition. Customers value local availability, rapid response times, and relationships with sales representatives who understand their needs.

The company also expanded its product offerings through acquisitions. The Company's Adler Tank Rentals subsidiary rents and sells containment solutions for hazardous and nonhazardous liquids and solids with operations today serving key markets throughout the United States.

By the mid-2010s, McGrath had transformed from a California-focused modular building company into a diversified national rental platform serving multiple end markets with distinct product categories. The foundation for the next phase of growth was in place.

VII. Leadership Transition: From Founder to Professional Management (2017)

The Succession Challenge

For any founder-led company, leadership transition represents an existential risk. Too many businesses falter when the charismatic founder departs, leaving behind a culture that was sustained by personal presence rather than institutional systems.

Bob McGrath had been planning for this moment for years. Mr. McGrath started the Company in 1979 and served as its Chairman & Chief Executive Officer until April 2003 when he stepped down as CEO. He continued to serve as Chairman of the Board of Directors until June 2009 when he transitioned to his current board member role as Chairman Emeritus.

The transition was deliberately gradual. Bob stepped down as CEO in 2003 but remained Chairman for another six years. This allowed his successors to establish their authority while maintaining continuity with the founding culture.

"Bob was also very focused on management succession planning and building a quality team of high-integrity and deeply committed leaders to the Company. Today, that management team is led by Dennis Kakures, the current CEO, a 31-year Company veteran, who continues to build this culture."

Dennis Kakures led the company from 2003 to 2017, presiding over the major diversification initiatives and geographic expansion. But by 2017, it was time for another transition.

Joe Hanna Takes the Helm

Joseph F. Hanna currently serves as President, Chief Executive Officer, and Director of the Company, a position he has held since February 2017, following a distinguished 14-year career with the Company in roles of increasing responsibility. Mr. Hanna served as Chief Operating Officer from 2007 to 2017, overseeing the company's operational strategy and driving significant growth.

"It is a testimony to the leadership of Dennis C. Kakures, recently retired as President and Chief Executive Officer, that our management bench has such depth that this transition to new leadership is seamless. The continuity that Joe brings to the transition will preserve the McGrath RentCorp culture that has so contributed to our reputation in the marketplace and with shareholders."

Joe Hanna represented the ideal internal successor. "He joined the Company in 2003 as Vice President of Operations. Throughout his tenure, Mr. Hanna has played a pivotal role in developing and executing the company's strategic product and geographic expansion across its diverse rental businesses. His deep understanding of the company, its products, services, strategies, and customers uniquely positions him for success as Chief Executive Officer."

What's remarkable about Hanna's background is how it reflects the McGrath culture of operational excellence. Prior to joining the Company, Mr. Hanna held various sales and operational leadership positions at SMC Corporation of America, a subsidiary of SMC Corporation, Tokyo, Japan. He also served as an officer in the United States Army. Mr. Hanna holds a B.S. in Electrical Engineering from the United States Military Academy, West Point, New York.

A West Point graduate with a background in sales and operations management—someone who understood both the discipline required to execute consistently and the customer relationships that drive rental businesses.

VIII. The WillScot Saga: $3.8 Billion Acquisition That Never Was (2024)

The Announcement

On January 29, 2024, the modular building rental industry received news that could have reshaped its competitive landscape entirely.

WillScot Mobile Mini announced a "60% Cash and 40% Stock Transaction Provides McGrath RentCorp Shareholders with $123 Per Share and Upside through Approximately 12.6% Stake in Combined Company."

McGrath shareholders would receive either $123.00 in cash or 2.8211 shares of WillScot Mobile Mini common stock. The transaction values McGrath at an enterprise value of $3.8 billion, including approximately $800 million of net debt, and the per-share consideration represents a premium of 10.1% to McGrath's closing stock price on January 26, 2024.

The strategic logic seemed compelling. WillScot Mobile Mini's broad North American footprint and 80-year history as an innovative space solutions provider would combine with McGrath's strengths. The combined company would serve more than 85,000 customers.

For WillScot, the deal would eliminate its most credible competitor in key markets and add McGrath's electronic test equipment business as a diversification play. The combined entity would have combined 2023 revenues of $3.2 billion and adjusted EBITDA of $1.4 billion.

The FTC Steps In

What followed was a masterclass in regulatory intervention and corporate discipline.

On February 22, 2024, McGrath announced that both it and WillScot had received second requests for additional information from the FTC in connection with the agency's review of the proposed acquisition.

Second requests are the FTC's signal that a deal faces serious scrutiny. They require companies to produce vast amounts of documentation and effectively pause the transaction timeline while regulators conduct deep-dive investigations.

Although both companies continue to believe in the merits and procompetitive benefits of the combination, WillScot and McGrath mutually agreed to terminate the transaction based on a joint determination that there was no commercially reasonable path to clear the necessary regulatory requirements for the transaction. Despite extensive and exhaustive engagement with the U.S. Federal Trade Commission ("FTC") over several months, in recent weeks, it became evident that the path to regulatory clearance would be excessively onerous.

The FTC's statement was blunt: "Strong competition in the markets for modular and portable storage solutions is essential to ensuring low prices and high levels of product quality and customer service for businesses and school districts nationwide. The FTC is pleased that WillScot has announced that it is terminating its proposed deal to acquire McGrath RentCorp in the face of a potential Commission challenge. FTC staff worked tirelessly to investigate the potential impacts of the proposed acquisition and found that customers in the construction, retail, education, and many other industries will benefit from continued competition between these two companies."

The $180 Million Consolation Prize

Here's where the story takes an unexpected turn. Under the terms of the merger agreement, WillScot owed McGrath a termination fee if the deal fell through due to regulatory failure.

McGrath received a $180.0 million merger termination payment from WillScot Mobile Mini and incurred $63.2 million in transaction costs during the year.

The net effect: McGrath walked away with approximately $117 million in cash—money for doing nothing except agreeing to be acquired by a company that couldn't close the deal.

The company's recent cash inflow from the termination of a merger agreement resulted in net proceeds of $116.8 million during the year ended December 31, 2024. The mutual termination of the company's prior merger agreement resulted in net proceeds of $116.8 million during the year ended December 31, 2024, which strengthened the balance sheet and kept leverage below 1.6 times adjusted EBITDA as of Q1 2025.

"The proposed transaction was a recognition of the enormous value created by our talented employees. Now, our team is energized and ready to execute our standalone strategy, and I am proud of the focus and tenacity the McGrath team demonstrated throughout this process."

The failed acquisition validated McGrath's value while leaving it independent, flush with cash, and positioned to pursue organic growth and tuck-in acquisitions on its own terms.

IX. Current Business Model Deep Dive (2024-2025)

Four Segments Explained

Today's McGrath operates through four segments: Mobile Modular, Portable Storage, TRS-RenTelco, and Enviroplex.

The segment breakdown reveals where McGrath makes its money:

Mobile Modular – which represents 75% of total revenues and 67% of adjusted EBITDA. This is the core business that Bob McGrath started in 1979, now scaled across multiple geographies and serving commercial, educational, and governmental customers.

McGrath's business mix remains heavily weighted toward Mobile Modular, which accounted for 75% of total revenues ($911 million) and 67% of total adjusted EBITDA ($352 million) in 2024. Portable Storage contributed 15% of revenues and 21% of adjusted EBITDA, while TRS-RenTelco represented 10% of revenues and 12% of adjusted EBITDA.

The Enviroplex segment manufactures and sells portable classrooms directly to public school districts and other educational institutions in California.

Financial Performance

Total revenues from continuing operations for the full year ended December 31, 2024 increased to $910.9 million, an increase of 10%, from $831.8 million in 2023, with adjusted EBITDA increasing $33.4 million, or 10%, to $351.7 million.

Net income from continuing operations for the year was $231.7 million, or $9.43 per diluted share, compared to $111.9 million, or $4.56 per diluted share, in 2023.

The net income figure requires context—it includes the $180 million termination fee from WillScot. Adjusting for that one-time item, the underlying business still demonstrated solid growth.

Gross profit margin of 47.37% is in the top 25% of its industry. Net profit margin of 15.62% is in the top 25% of its industry.

The Circular Economy Positioning

McGrath has increasingly emphasized its sustainability positioning: The Company's rental product offerings and services are part of the circular supply economy, helping customers work more efficiently, and sustainably manage their environmental footprint.

This isn't just marketing. Modular buildings and storage containers that are rented, refurbished, and re-rented multiple times represent a fundamentally more sustainable approach than constructing and demolishing temporary structures. As ESG considerations become more important to corporate customers and school districts, McGrath's rental model has genuine environmental advantages.

X. Growth Strategy & Recent Developments (2024-2025)

Leadership Evolution Continues

In January 2025, McGrath announced another step in its leadership evolution: "McGrath RentCorp today announced the appointment of Philip B. Hawkins to Chief Operating Officer (COO). Joe Hanna, CEO stated, 'I am very pleased to announce the promotion of Phil Hawkins to the position of Chief Operating Officer (COO).'"

"In this role, Phil will continue to oversee our Mobile Modular businesses while expanding his attention to increased operational leadership responsibilities across McGrath. Phil has taken on increased responsibilities and continuously delivered results for over 20 years with McGrath and especially over the last 15 years in leading our Mobile Modular division, which has been our strategic focus."

Hawkins represents the third generation of "promote from within" leadership—having joined through the 2004 TRS acquisition and risen through the ranks over two decades.

Strategic Initiatives

The company has outlined clear growth priorities: The company highlighted several initiatives driving revenue growth, including Mobile Modular Plus and Site Related Services, which have achieved compound annual growth rates of 26% and 33%, respectively, since 2022.

"Over the course of this year, we have taken steps to enter new regions, grow our Mobile Modular Plus and site-related services initiatives, and increase our coverage through tuck-in acquisitions. All of these items support our efforts to become a true national modular solutions provider capable of serving our customers with storage units, single-wide units, large multi-floor and multi-story facilities, and services to meet all their space needs."

Financial Guidance

Updated 2025 outlook: revenue $935–955M, Adjusted EBITDA $350–357M, and gross rental equipment capex $120–125M.

Management has highlighted a "robust M&A pipeline," suggesting opportunities to expand geographically or vertically.

XI. Playbook: Business & Investing Lessons

The "Boring Business" Thesis

There's a recurring theme in the best investment returns: they often come from businesses that most people overlook. Renting modular buildings and test equipment won't land you on magazine covers or get you invited to tech conferences. But recurring revenue from essential business infrastructure compounds silently and relentlessly.

McGrath embodies this principle. With over 40 years of experience, McGrath's success is driven by a focus on exceptional customer experiences. This focus has underpinned the Company's long-term financial success and supported over 30 consecutive years of annual dividend increases to shareholders, a rare distinction among publicly listed companies.

Counter-Cyclical Diversification

McGrath's strategic evolution demonstrates the power of thoughtful diversification. Each business segment hedges against the others: - When commercial construction slows, educational facility needs often persist - When the broader economy weakens, R&D spending on test equipment may actually increase - Geographic diversification reduces exposure to regional economic cycles

Capital Intensity as a Moat

High upfront capital requirements create natural barriers to entry. A new competitor can't simply launch a modular building rental business—they need millions in fleet investment, warehouse facilities, and delivery capabilities before serving a single customer. McGrath's established infrastructure and customer relationships make it difficult for newcomers to compete.

Customer Relationships Over Transactions

McGrath RentCorp has always placed a strong emphasis on providing excellent customer service. This commitment has helped the company build strong relationships with its customers and differentiate itself from its competitors.

In rental businesses, the customer relationship extends far beyond the initial sale. Installation, maintenance, modification, and eventual removal all require ongoing interaction. Companies that excel at these touchpoints create switching costs and generate repeat business.

Founder-Led Culture Preservation

The most impressive aspect of McGrath's story may be how effectively the founding culture survived multiple leadership transitions. "Bob was also very focused on management succession planning and building a quality team of high-integrity and deeply committed leaders to the Company."

Dividend Discipline

The company has not only consistently paid dividends but has also increased its dividend annually, earning it the prestigious title of a dividend aristocrat—a recognition awarded to companies with at least 34 consecutive years of dividend increases.

This discipline signals management confidence in future cash flows and creates accountability. Once a company has established a dividend increase streak, breaking it carries significant reputational consequences.

Knowing When to Walk Away

The WillScot saga illustrates an underappreciated form of discipline: recognizing when a deal's value proposition has deteriorated. Both companies concluded that the regulatory hurdles weren't worth the cost, and they walked away—leaving McGrath better positioned than before.

XII. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces Assessment

Threat of New Entrants: LOW-MODERATE

High capital requirements for fleet acquisition create substantial barriers. Established customer relationships in education and commercial sectors take years to develop. Regulatory knowledge for modular building permitting and installation adds complexity that favors incumbents.

Bargaining Power of Suppliers: MODERATE

Multiple modular building manufacturers exist, limiting any single supplier's leverage. Test equipment comes from major OEMs like Keysight Technologies. However, during supply chain disruptions, manufacturers can prioritize customers, giving some suppliers periodic advantage.

Bargaining Power of Buyers: MODERATE

Large customers like school districts and major corporations can negotiate pricing due to volume. However, switching costs are meaningful—once a modular building is installed and configured, changing suppliers involves significant disruption. Long rental durations (often multi-year) create relationship stickiness.

Threat of Substitutes: LOW

Alternatives to modular buildings—permanent construction—are far more expensive and time-consuming. The value proposition of temporary, flexible space solutions has no close substitute at comparable economics. Test equipment ownership is the alternative, but depreciation and utilization economics favor rental for most use cases.

Industry Rivalry: MODERATE-HIGH

Major players such as WillScot Mobile Mini, ATCO, and McGrath RentCorp are poised to play pivotal roles in shaping the market's trajectory in the coming years. Other market players include Black Diamond Group, United Rentals, Modular Space Corporation, Triumph Modular, Satellite Shelters, Inc., Vanguard Modular Building Systems, LLC, and Redi-Bilt.

WillScot is significantly larger than McGrath, creating competitive pressure. Regional competition exists in many markets. Price competition in portable storage can be intense during construction downturns.

Hamilton's 7 Powers Analysis

Scale Economies: MODERATE

Fleet size enables better utilization economics. National presence provides service advantages for customers with multi-location needs. However, modular building rental is somewhat localized—you can't easily ship a portable classroom from California to Florida.

Network Effects: LOW

Limited network effects in equipment rental. Unlike technology platforms, McGrath's value doesn't increase as more customers use the service.

Counter-Positioning: HIGH

The rental model disrupts traditional purchase/construction economics. Companies that sell modular buildings face a dilemma—aggressively promoting rentals would cannibalize their sales business. McGrath has no such conflict; its entire model is built around asset utilization through rental.

Switching Costs: MODERATE-HIGH

Long rental durations (often multi-year for education) create stickiness. Setup and teardown costs make switching disruptive. Customer relationships with local sales teams and service personnel add human switching costs.

Branding: MODERATE

Strong reputation in California education market. "McGrath might be the best company you may never have heard of. While we started out small, 44 years later we deliver over $734 million dollars in annual revenue, employ more than 1,200 associates." B2B reputation is relationship-based rather than brand-driven.

Cornered Resource: LOW

No unique resources. Expertise and culture are differentiators, but not legally protected. Competitors can theoretically hire away talent and replicate processes.

Process Power: HIGH

45+ years of operational excellence. Efficient logistics and refurbishment capabilities. Deep knowledge of modular building permits and regulations in key markets. Customer service culture that's difficult to replicate.

Key Insight

McGrath's primary competitive advantages stem from Process Power (operational excellence developed over 45 years) and Counter-Positioning (the rental model that asset-heavy incumbents won't copy because it would cannibalize their sales). The company is not the biggest (WillScot is larger), but competes effectively through superior customer service and regional strength.

XIII. Bear vs. Bull Case

Bull Case

Dividend Reliability and Growth

McGrath RentCorp stands out as a rare combination of dividend reliability, operational diversification, and circular economy alignment. With a track record of thriving through economic cycles, a payout ratio that leaves room for growth, and a business model inherently aligned with sustainability.

The payout ratio of McGrath RentCorp in relation to the last financial year is 20.15%. A low payout ratio means substantial room for continued dividend growth.

Profitability Metrics

Gross profit margin of 47.37% is in the top 25% of its industry. Net profit margin of 15.62% is in the top 25% of its industry.

Balance Sheet Strength Post-Termination Fee

The mutual termination of the company's prior merger agreement resulted in net proceeds of $116.8 million during the year ended December 31, 2024, which strengthened the balance sheet and kept leverage below 1.6 times adjusted EBITDA.

Education Market Stability

America's aging school infrastructure creates ongoing demand for modular classroom solutions. California, Texas, and Florida—McGrath's core markets—face chronic facility needs driven by enrollment fluctuations and renovation cycles.

Data Center and Infrastructure Tailwinds

The AI boom is driving unprecedented demand for data center construction, which requires temporary office and workspace solutions during multi-year build-outs.

Bear Case

Utilization Challenges

Mobile Modular, McGrath's largest segment, faced utilization challenges with average utilization declining from 77.1% in Q3 2024 to 72.6% in Q3 2025.

Lower utilization directly impacts profitability. Fixed costs (depreciation, storage, maintenance) don't decline when utilization falls, creating operating leverage that works against the company during demand softness.

Portable Storage Weakness

Portable Storage faced a 13% rental revenue decline to $16.1 million due to weaker construction activity.

The portable storage segment is highly sensitive to construction activity, which remains challenged by elevated interest rates.

Stock Performance

The total return for McGrath RentCorp (MGRC) stock is -13.97% over the past 12 months vs. 14.80% for the S&P 500.

Recent underperformance raises questions about near-term momentum.

Competitive Pressure from WillScot

WillScot faces competition from firms like McGrath RentCorp (MGRC) and ATCO, but its capital efficiency and operational metrics set it apart. McGrath RentCorp, for example, reported a 3.9% revenue decline in Q3 2025.

WillScot's scale advantages could intensify competitive pressure, particularly if the larger competitor becomes more aggressive on pricing to gain market share.

Construction Cycle Sensitivity

Interest rates remain elevated, depressing commercial real estate activity. A prolonged downturn in construction would pressure both the modular building and portable storage segments.

XIV. KPIs to Track

For long-term investors evaluating McGrath RentCorp, two metrics deserve particular attention:

1. Mobile Modular Utilization Rate

This is the single most important operating metric for McGrath's core business. Mobile Modular's average utilization declined from 77.1% in Q3 2024 to 72.6% in Q3 2025.

Utilization directly drives profitability. The company incurs significant fixed costs regardless of how many units are rented—depreciation, storage, maintenance, and insurance. Higher utilization spreads these costs across more rental revenue, expanding margins. Lower utilization does the opposite.

Historical utilization around 77-78% represented healthy demand. "If you go back 18 months, two years ago, utilization was higher. It was more common that when a new order came in, we were already highly utilized, and we would look to invest capital to meet the order."

A sustained return to historical utilization levels would be the clearest signal that demand has normalized and margin expansion is likely.

2. Revenue Per Unit on Rent (Pricing Power)

Revenue per unit on rent increased by 6%, while revenue per new unit shipped rose by 3% on a last-twelve-months basis.

This metric reveals whether McGrath can maintain or expand pricing even during periods of softer demand. If utilization declines but revenue per unit rises, it suggests the company has pricing power with customers who value its service quality. If both metrics decline simultaneously, it signals competitive pressure and margin compression.

XV. Epilogue & Future Outlook

The Road Ahead

Updated 2025 outlook: revenue $935–955M, Adjusted EBITDA $350–357M.

Management has narrowed guidance ranges, suggesting greater confidence in near-term visibility despite macro uncertainty.

Management has highlighted a "robust M&A pipeline," suggesting opportunities to expand geographically or vertically. The rental industry's consolidation trend remains intact, driven by demand for modular solutions in education, healthcare, and industrial sectors. McGrath's modular divisions—particularly Mobile Modular Plus and Site Related Services—are positioned to capitalize on this.

Infrastructure and ESG Tailwinds

Federal infrastructure spending creates multi-year tailwinds for construction activity, which drives demand for temporary workspace solutions. School facility funding at state and federal levels supports the education market that has been McGrath's foundation since the 1980s.

The Company's rental product offerings and services are part of the circular supply economy, helping customers work more efficiently, and sustainably manage their environmental footprint. With over 40 years of experience, McGrath's success is driven by a focus on exceptional customer experiences.

The Power of Compound Returns

"McGrath might be the best company you may never have heard of. While we started out small, 44 years later we deliver over $734 million dollars in annual revenue, employ more than 1,200 associates, and operate as a publicly traded company."

What started as a $25,000 bet on a two-acre lot in the East Bay has become a nearly $3 billion enterprise. The magic wasn't a revolutionary product or brilliant timing—it was consistent execution, thoughtful diversification, and a relentless focus on customer service compounded over 45 years.

The 10-year total return for MGRC stock is 348.58%.

That's the power of boring done brilliantly.

XVI. Resources for Further Reading

Top Resources for Investors:

-

McGrath RentCorp Annual Reports & Investor Presentations – investors.mgrc.com – The primary source for financial data, segment breakdowns, and management commentary.

-

"The Outsiders" by William Thorndike – Capital allocation lessons highly relevant to understanding McGrath's disciplined approach to dividends and reinvestment.

-

"7 Powers" by Hamilton Helmer – Framework for understanding McGrath's competitive position, particularly its Process Power and Counter-Positioning advantages.

-

WillScot Mobile Mini Investor Materials – Understanding the competitive landscape and the industry leader's strategy provides context for McGrath's positioning.

-

Modular Building Institute Resources – Industry context on trends, growth drivers, and regulatory environment affecting modular construction.

-

SEMI (Semiconductor Equipment and Materials International) – For TRS-RenTelco market context and understanding the semiconductor cycle's impact on test equipment demand.

-

California Department of Education School Facilities Reports – Understanding the education market that remains central to McGrath's modular building business.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube