Union Pacific Corporation: Building America's Railroad Empire

I. Introduction & Cold Open

The boardroom at Union Pacific's Omaha headquarters hummed with tension on July 29, 2025. CEO Jim Vena, the operational maestro who'd transformed the railroad's efficiency metrics over the past five years, was about to make the announcement that would reshape American transportation. At 9:30 AM Eastern, the press release hit the wires: Union Pacific would acquire Norfolk Southern Railway for $85 billion, creating the first truly transcontinental railroad network under single ownership in United States history.

The audacity of the move was breathtaking. Here was a company born from Civil War necessity, forged in scandal, bankrupted in financial panic, and rebuilt through sheer force of will, now positioning itself to control freight movement from Los Angeles to Atlanta, from Seattle to Charleston. The merger would unite 50,000 miles of track across 43 states—a steel web spanning the continent that Abraham Lincoln could only have dreamed of when he signed the Pacific Railway Act on July 1, 1862.

But how did we get here? How did a railroad chartered during America's darkest hour, when the Union itself hung in the balance, evolve into a $150 billion colossus that moves 40% of the nation's freight? The story of Union Pacific isn't just about laying track and hauling cargo. It's a saga of empire building, featuring robber barons and visionaries, government subsidies and private greed, technological revolution and regulatory capture. It's the story of how transportation infrastructure became the backbone of American capitalism.

This is that story—from Lincoln's wartime gamble to create a transcontinental railroad, through bankruptcy and rebirth, consolidation and innovation, to today's bold bid for continental dominance. Along the way, we'll meet the titans who built this empire: Thomas "Doc" Durant, the medical doctor turned railroad schemer who orchestrated one of history's great financial frauds; Edward Henry Harriman, the Wall Street operator who rescued Union Pacific from the ashes and created the template for modern railroad management; and Jim Vena, the current CEO whose operational excellence philosophy has positioned the company for its most ambitious acquisition yet.

The journey ahead takes us through Gilded Age excess, Progressive Era reform, wartime mobilization, deregulation revolution, and digital transformation. We'll examine how a 19th-century technology remains indispensable in the 21st century, why Warren Buffett calls railroads "the circulatory system of the American economy," and what Union Pacific's continental ambitions mean for investors, shippers, and the future of American infrastructure.

II. Origins: Lincoln's Vision & The Pacific Railroad Act

Picture Washington D.C. on the sweltering afternoon of July 1, 1862. Confederate forces under Robert E. Lee had just repulsed General George McClellan's Army of the Potomac in the Seven Days Battles, ending the Union's Peninsula Campaign in humiliating failure. The capital itself seemed vulnerable—panic gripped the city as wounded soldiers streamed back from Virginia. In this atmosphere of crisis, Abraham Lincoln sat at his desk in the White House, pen in hand, about to sign legislation that would prove as consequential as any military victory.

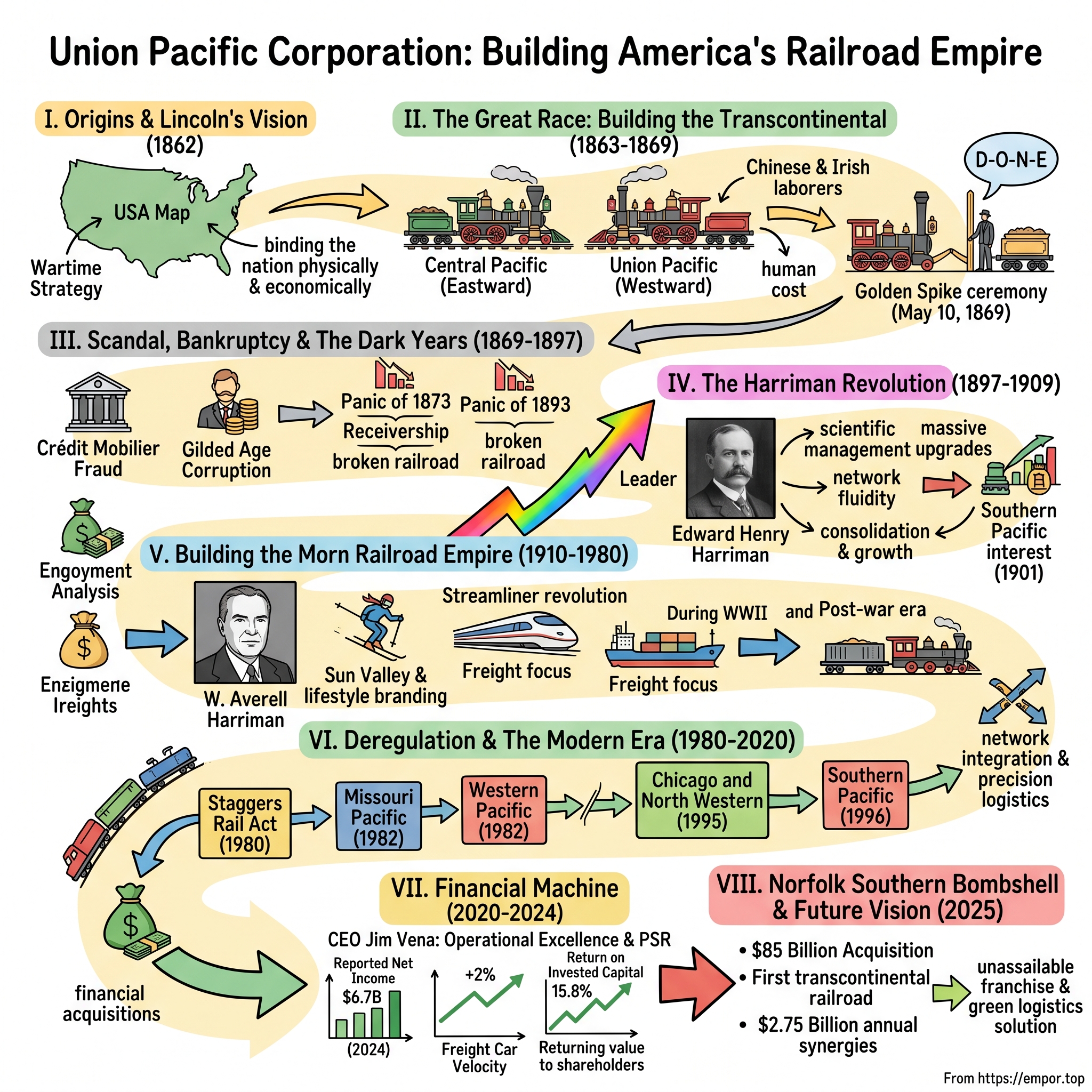

The Pacific Railway Act, signed into law by President Abraham Lincoln on July 1, 1862, provided Federal subsidies in land and loans for the construction of a transcontinental railroad across the United States. This wasn't merely infrastructure legislation—it was wartime strategy dressed as economic development. Lincoln understood what his generals sometimes failed to grasp: the Civil War wasn't just about preserving the Union politically, but binding it together physically, economically, and psychologically.

The dream of a transcontinental railroad had tantalized Americans for decades. Visionaries first began talking about a route to the Pacific in the 1830s, and by the time Lincoln took office in 1861, many Americans believed that expanding the railroad was absolutely necessary, though Congress had tried to make it happen and failed. The debate had always foundered on sectional politics—would the route favor the North or South? Would slave states or free states benefit? Jefferson Davis himself, as Secretary of War in the 1850s, had authorized surveys of five potential routes, but no consensus could be reached.

No route or bill could be agreed upon and passed authorizing the Government's financial support and land grants until the secession of the southern states in 1861 removed their opposition to a central route. The Confederate exodus from Congress created an unexpected opportunity. Without Southern Democrats to object, Republicans could finally push through their vision of a northern transcontinental route—one that would cement the economic and political dominance of the free states forever.

In Lincoln's mind, the railroad was part of the Civil War effort—the new line would support communities and military outposts on the frontier. But the president's vision extended beyond military logistics. He saw the railroad as the sinews that would hold together a continental empire, preventing California's gold and Nevada's silver from drifting toward independence or foreign influence. The railroad would make the theoretical union of states into a practical reality.

The Act itself was a marvel of government intervention in the economy, unprecedented in American history. The 1862 Act authorized extensive land grants in the Western United States and the issuance of 30-year government bonds at 6 percent to the Union Pacific Railroad and Central Pacific Railroad companies to construct a continuous transcontinental railroad. The method of apportioning these additional land grants provided the companies with a total of 6,400 acres for each mile of their railroad.

The Pacific Railway Act of 1862 gave the work of building the railroad to two companies: Central Pacific, an existing California railroad, and a new railroad chartered by the Act itself—Union Pacific, with Central Pacific starting at the Pacific and heading east, and Union Pacific starting in the middle of the country and heading west. This created a race—whoever built more track would receive more government subsidies.

But the Act also created something darker: an opportunity for corruption on a scale America had never seen. Enter Thomas Clark Durant, a character who seemed lifted from a morality play about greed. Durant was an American physician who graduated cum laude from Albany Medical College in 1840, but after retiring from medicine, he became involved in the railroad industry and served as vice-president of the Union Pacific Railroad.

Durant understood something fundamental about the railroad that would define its early years: Durant was convinced building a railroad would be more profitable than running one, so he had to get into the construction business. Why operate a risky transcontinental railroad through empty territory when you could profit from constructing it with guaranteed government money?

George Francis Train and Thomas C. Durant formed Crédit Mobilier of America in March 1864, a company that was one of the first to take advantage of the new limited liability financial structures. The scheme was breathtakingly audacious. Durant paid crony Herbert M. Hoxie to submit a construction bid to the Union Pacific—no one else got the call to bid, and Hoxie's offer was unanimously approved. Hoxie signed the contract over to Durant, who transferred it to Crédit Mobilier. In essence, Durant hired himself to construct the railroad, paying Crédit Mobilier with government bonds and investor money while using inflated estimates to ensure significant profit. Because there was no liability, it didn't matter whether the railroad actually got built.

The numbers tell the story of one of American history's greatest frauds. The U.S. Congress paid $94,650,287 to the Union Pacific, but though the railroad cost only $50 million to build, Crédit Mobilier billed $94 million and Union Pacific executives pocketed the excess $44 million. Durant had managed to accumulate some $23 million by defrauding the railroad's investors with his Crédit Mobilier scheme.

Durant didn't just steal money—he corrupted the entire political system. Part of the excess cash and $9 million in discounted stock was used to bribe several Washington politicians for laws, funding, and regulatory rulings favorable to the Union Pacific. Future President James Garfield, Vice President Schuyler Colfax, and Speaker of the House James G. Blaine all found themselves entangled in the web of corruption that Durant had spun.

Yet here's the extraordinary paradox: this corrupt enterprise, born from Lincoln's wartime desperation and Durant's greed, would succeed in building exactly what America needed. The very corruption that enriched Durant and his cronies also ensured that the railroad would be built with unprecedented speed. The race between Union Pacific and Central Pacific, fueled by government subsidies tied to track miles, would complete in seven years what many thought would take decades.

As we'll see in the next section, the actual construction of the railroad would prove even more dramatic than its financial engineering—a story of Irish and Chinese laborers battling mountains and deserts, of engineering miracles and human tragedies, all racing toward a meeting point that would unite a continent and transform a nation.

III. The Great Race: Building the Transcontinental (1863–1869)

The morning of May 10, 1869, dawned clear and cold at Promontory Summit, Utah Territory. The desolate spot, 5,900 feet above sea level and surrounded by sagebrush, seemed an unlikely location for one of the defining moments in American history. Yet here, where the tracks of the Union Pacific and Central Pacific railroads would finally meet, a drama six years in the making was about to reach its climax.

The completion of the first transcontinental railroad lines at Promontory Summit, Utah, on May 10, 1869, when Leland Stanford, co-founder of the Central Pacific Railroad, connected the eastern and western sections of the railroad with a golden spike, represented far more than an engineering triumph. It was the culmination of a race that had consumed fortunes, destroyed bodies, and transformed a continent.

The race had begun in earnest in 1863, with the Central Pacific beginning to lay track eastward from Sacramento, California, and the Union Pacific starting to lay track westward from Omaha, Nebraska, in July of 1865. But what made this a race was the compensation structure Congress had devised: companies received a total of 6,400 acres for each mile of their railroad, plus those lucrative government bonds. Every mile of track meant money—lots of it.

The two companies could not have been more different in their challenges and solutions. The Central Pacific, attacking the granite walls of the Sierra Nevada, faced a labor crisis from the start. In early 1865 the Central Pacific had work enough for 4,000 men. Yet contractor Charles Crocker barely managed to hold onto 800 laborers at any given time. Most of the early workers were Irish immigrants. But these workers often abandoned the dangerous railroad work for the lure of Nevada's silver mines.

Charles Crocker's solution would transform not just the railroad but American demographics. Despite initial resistance—Leland Stanford, president of the railroad, had been elected governor on a program opposing Chinese immigration, calling the Chinese "the dregs" of Asia—the Central Pacific turned to Chinese workers. Foreman James Harvey Strobridge grudgingly agreed to hire 50 Chinese men as wagon-fillers. Their work ethic impressed him, and he hired more Chinese workers for more difficult tasks.

The numbers tell the story of this transformation: At the height of the construction, 80-90% of the railroad workforce was Chinese. Different sources estimate that from 1865 to the railroad's completion in 1869, anywhere from 10,000 to 20,000 Chinese workers were employed by the Central Pacific Railroad. These men, mostly from Guangdong Province, would accomplish what seemed impossible—blasting fifteen tunnels through the Sierra Nevada.

To meet its manpower needs, the Central Pacific hired 15,000 laborers, of whom more than 13,000 were Chinese immigrants. These immigrants were paid less than white workers, and, unlike whites, had to provide their own lodging. The discrimination was systematic: Chinese workers, though compensated for their work, were still paid about $10-15 less than their White counterparts.

Meanwhile, the Union Pacific faced different demons. The end of the Civil War brought a change of fortune for the Union Pacific. Thousands of demobilized soldiers were eager for work. Additionally, by 1866 the railroad had managed to import Irishmen from the teeming cities of the eastern seaboard. The workers, many of them Irish immigrants or veterans of the Civil War, were paid the average of a dollar a day. These were the pick and shovel men, the teamsters, blacksmiths, masons, carpenters, mechanics and track layers.

The Union Pacific's chief engineer, Grenville Dodge, and construction boss Jack Casement ran their operation with military precision—literally. Former Brigadier General Jack ran his men with a military precision that hinged upon the efficient division of labor. Teamsters piloted small horse-drawn carts along freshly-laid track. Men on either side of those carts unloaded rails and moved forward to place them parallel to one another on embedded ties. Gaugers stepped in to ensure the rails were the correct distance apart.

But the Union Pacific workers faced a threat the Central Pacific largely avoided: fears of the Native Americans across whose land the laborers built their road. There were Native American snipers, raids, livestock rustlings, scalpings, and burnings all along the railroad right of way. Indian sightings sufficed to spook men, and line surveyors did not always return from their routes.

The human cost of this race was staggering. They toiled through back-breaking labor during both frigid winters and blazing summers. Hundreds died from explosions, landslides, accidents and disease. The most dangerous work fell to the Chinese workers boring through the Sierra Nevada. They were lowered in baskets down sheer cliff faces to drill holes for explosives, then hauled up before the blast—if they were lucky. Many weren't.

As 1868 turned to 1869, the race intensified to absurd proportions. The two companies' grading crews actually passed each other in Utah, each company refusing to stop building because every mile meant more money. The situation grew violent: From this cause several Chinamen were severely hurt... One day the Chinamen, appreciating the situation, put in what is called a "grave" on their work, and when the Irishmen right under them were all at work let go their blast and buried several of our men. This brought about a truce at once. From that time the Irish laborers showed due respect for the Chinamen, and there was no further trouble.

Finally, Congress had to intervene, setting Promontory Summit as the meeting point. The ceremony itself, originally scheduled for May 8, had to be postponed when over 400 laid-off unpaid graders and tie cutters chained U.P.R.R. Vice-President Thomas Durant's dignitary railcar to a siding in Piedmont, Wyoming, until he wired for money to pay them—a fitting reminder of whose sweat had actually built the railroad.

When the day finally arrived, the ceremony was both grand and farcical. The golden spike is the ceremonial 17.6-karat gold final spike driven by Leland Stanford to join the rails of the first transcontinental railroad, though the truth was more prosaic. Stanford missed the Spike, hitting the wooden tie instead; however, the telegraph operator hit his key as though Stanford had hit the spike. Durant missed the spike and the tie entirely; but likewise, the operator hit his key so the Nation would not know the difference.

Fittingly, it was a railway worker who drove in the final spike, and with that the Western Union telegrapher present tapped D-O-N-E to the nation at 12:47 p.m. Monday, May 10th, 1869. The message flashed across the continent, setting off celebrations from San Francisco to New York. Church bells rang, cannons fired, and the nation rejoiced.

But in the famous photograph taken that day—the one showing the two locomotives nose to nose with officials shaking hands—something was conspicuously absent. In this photograph the Chinese workers are excluded, though they had done the majority of the work on the Central Pacific side. The Irish workers who had built much of the Union Pacific were likewise absent from the frame. The men who had actually built the railroad were already being written out of its history.

The numbers were staggering: in just over six years, the companies had laid 1,776 miles of track, moved millions of tons of earth and rock, and created an iron road where none had existed before. They had done it ahead of schedule and, remarkably, under budget. But the human cost—the Chinese workers buried in Sierra avalanches, the Irish workers killed in Indian raids, the lives ground down by exhaustion and disease—would never be fully tallied.

As Stanford's private car headed back to California carrying the golden spike (now marked with dents from Union Army officers who had struck it with their sword pommels in celebration), the construction crews were already being disbanded. The Chinese workers would face decades of discrimination, culminating in the Chinese Exclusion Act of 1882. The Irish workers would melt into the growing cities of the West. Their achievement would stand, but their stories would fade.

The race to build the transcontinental railroad was over. The race to control it—and the wealth it would generate—was just beginning. As we'll see, the triumph at Promontory Summit would soon give way to financial scandal, bankruptcy, and a bitter struggle for the soul of the Union Pacific.

IV. Scandal, Bankruptcy & The Dark Years (1869–1897)

The champagne had barely dried from the Golden Spike celebration when the bills came due. By late 1869, the Union Pacific's financial house of cards, so carefully constructed by Thomas Durant through the Crédit Mobilier scheme, began to collapse. The railroad that had united a continent now threatened to tear apart the republic's faith in its institutions.

The unraveling began with a falling out among thieves. George Francis Train and Thomas C. Durant formed Crédit Mobilier of America in 1864 as a deliberate façade to present the appearance that an independent corporate enterprise had been impartially chosen as the principal contractor, when in fact it was created to shield the company's shareholders from the charge that they were using the construction phase to generate profit.

The scheme had worked beautifully—for a while. The U.S. Congress paid $94,650,287 to the Union Pacific and $50,720,959 to Crédit Mobilier. The arrangement thus generated $43,929,328 in profits for Crédit Mobilier (equivalent to over $1.1 billion in 2025). But by 1872, the greed that built the railroad would destroy its architects.

The scandal broke during the heated presidential campaign of 1872. The story was broken by The New York Sun during the 1872 campaign of Ulysses S. Grant. Part of the excess cash and $9 million in discounted stock was then used to bribe several Washington politicians for laws, funding, and regulatory rulings favorable to the Union Pacific. The newspaper's exposé revealed a web of corruption that reached into the highest levels of government.

The roll call of the disgraced read like a who's who of American politics. Vice President Schuyler Colfax, Speaker of the House James G. Blaine, and future President James A. Garfield all found themselves implicated. Representative Oakes Ames of Massachusetts, who had distributed Crédit Mobilier stock to his colleagues like party favors, was censured by Congress. The scandal destroyed political careers and shattered public trust in both government and big business.

Durant himself had already been forced out. President Grant, disgusted by the corruption, had fired him from Union Pacific. Like many others, Durant lost a great deal of his wealth in the Panic of 1873. The man who had orchestrated one of history's great frauds died in 1885, largely forgotten and financially diminished.

But Durant's departure didn't save the Union Pacific. The railroad he had built on financial manipulation rather than operational excellence was fundamentally unsound. The problems were manifold: the track, hastily laid to maximize government subsidies, required constant expensive repairs. The route, chosen for political rather than commercial reasons, often bypassed population centers. The debt load from construction was crushing.

Then came the Panic of 1873, triggered partly by railroad overexpansion. Jay Gould, the notorious robber baron, had taken control of Union Pacific in 1874, but even his financial manipulations couldn't save the company. Gould had purchased the old company on January 24, 1880, already owning the Kansas Pacific and sought to merge it with UP.

The death blow came with the Panic of 1893, one of the worst economic depressions in American history. The Union Pacific Railway declared bankruptcy during the Panic of 1893. The railroad that Lincoln had envisioned as binding the nation together was itself broken.

For four years, the Union Pacific languished in receivership. Its tracks deteriorated, its rolling stock fell apart, and its reputation sank even lower. Creditors circled like vultures. The U.S. government, still owed millions in construction loans, faced the prospect of losing its entire investment. Wall Street consensus was that the Union Pacific was finished—a cautionary tale of ambition exceeding grasp.

An internal report suggested the railroad could be rebuilt for $44 million. Most observers thought even that was too much for what appeared to be 1,800 miles of rust and regret stretching across an empty continent. The idea that someone would pay nearly double that amount seemed preposterous.

Yet as 1897 dawned, a diminutive figure with piercing eyes and an outsized ambition was examining Union Pacific's books with intense interest. Edward Henry Harriman saw something in those numbers that others missed—not just a failed railroad, but the foundation of an empire. What happened next would transform not just the Union Pacific, but the entire concept of what a railroad could be. The age of true railroad titans was about to begin.

V. The Harriman Revolution (1897–1909)

The scene at the Windsor Hotel in New York on a November morning in 1897 was electric with tension. The foreclosure auction for the bankrupt Union Pacific Railroad was about to begin, and most of Wall Street's titans had already walked away from what they considered a hopeless wreck. J.P. Morgan himself had examined the books and declined to participate. But seated quietly in the corner was a slight man with intense eyes and a banker's bearing who saw something everyone else had missed.

Edward Henry Harriman was nearly 50 years old when he decided to make the gamble that would define American capitalism. Edward Harriman purchased the Union Pacific out of receivership in 1897 for over $84 million. This was an astounding sum to pay, considering that just a few years earlier an internal report estimated that the Union Pacific railroad could be rebuilt and re-equipped in its entirety for $44 million.

The audacity of the bid stunned even Harriman's partners. In 1898 his career as a great railway organizer began with his formation, by the aid of the bankers Kuhn, Loeb & Co., of a syndicate to acquire the Union Pacific Railroad Company, which was then in receivership. Through a syndicate of backers — the Vanderbilts, Rockefellers, Goulds, Ameses, and Kuhn, Loeb & Co. — Harriman took control of the road. In total, they paid $75 million for 1,800 miles of railroad and got every penny back in profits within three years.

But Harriman saw what the doubters didn't: the land grants alone were worth more than the purchase price. The timber rights in Oregon, the mineral deposits along the route, the prime urban real estate in growing Western cities—these were assets that didn't show up properly on a balance sheet drawn up by Eastern bankers who'd never been west of Chicago.

Harriman was an unlikely railroad titan. He quit school at age 14 to take a job as an errand boy on Wall Street in New York City. His uncle Oliver Harriman had earlier established a career there. By age 22, he was a member of the New York Stock Exchange. Unlike the flamboyant Durant or the ruthless Gould, Harriman was methodical, scientific, almost monastic in his devotion to operational excellence.

Harriman was nearly 50 years old when in 1897 he became a director of the Union Pacific Railroad. By May 1898, he was chairman of the executive committee, and from that time until his death, his word was the law on the Union Pacific system. In 1903, he assumed the office of president of the company.

What Harriman did next revolutionized not just the Union Pacific but the entire concept of railroad management. Harriman quickly set to changing the culture at UP, restructuring its heavy debt, and pouring millions of dollars into upgrading the railroad's property. Under Harriman, Union Pacific saw its main line between Omaha, Nebraska and Granger, Wyoming entirely double-tracked, a more efficient route scaling Sherman Hill (located in Wyoming), significant line relocations to improve grades and curves, and an updated, automatic signaling system.

But physical improvements were only part of Harriman's revolution. He introduced something radical for the era: scientific management based on data and efficiency metrics. Every aspect of operations was measured, analyzed, optimized. Train speeds increased. Accident rates plummeted. On-time performance became an obsession.

It was reorganized in 1897 under the leadership of Edward H. Harriman, who was responsible for major improvements and standardization and who led the railroad to participate in the economic development of the West. Harriman standardized equipment across the system, allowing for interchangeable parts and reduced maintenance costs. He invested in heavier rails that could handle bigger loads. He straightened curves and reduced grades, allowing trains to move faster with less fuel.

The transformation was immediate and dramatic. Harriman first set about retrieving the various pieces of UP lost during the receivership and soon reassembled the company's three basic networks: those running between Omaha and Ogden, Ogden and the Pacific Northwest, and Ogden and Los Angeles. Between 1898 and Harriman's death in 1909, the UP increased its track miles from 2,000 to 6,000.

But Harriman's ambitions extended far beyond simply fixing the Union Pacific. Harriman recognized that expansion through acquisition was the most efficient way to lower costs and ensure profitability for Union Pacific. He quickly bought up competing railroads until Union Pacific dominated the U.S. west of Omaha.

The crown jewel of Harriman's empire-building came in 1901. From 1901 to 1909, Harriman was also the president of the Southern Pacific Railroad. The vision of a unified UP/SP railroad was planted with Harriman. In 1901, the company acquired a 46% interest in Southern Pacific Railroad; however, the government forced the company to sell the stake in 1913 due to antitrust concerns.

This acquisition of Southern Pacific was transformative. SP was UP's chief rival and equal, the owner of three main routes between San Francisco and Portland, Oregon; San Francisco and Ogden; and San Francisco and the entire Southwest to New Orleans. SP also owned a series of steamship lines extending from California to Japan and Panama, and from New Orleans to New York.

Harriman had created something unprecedented: a transportation network that spanned from the Atlantic to the Pacific, with steamship connections to Asia. Harriman used the railroad as a holding company for the securities of other transportation companies in his empire. This wasn't just a railroad—it was an integrated logistics system decades ahead of its time.

But Harriman's methods also attracted powerful enemies. At the peak of his power, Harriman controlled about 60,000 miles of railroads in the U.S., earning him the scrutiny of President Theodore Roosevelt. This resulted in regulation changes that restricted monopoly power in the railroad industry.

The confrontation with Roosevelt represented a turning point in American capitalism. The era of unfettered railroad consolidation was ending. The Progressive Era, with its trust-busting fervor, would challenge the very foundations of Harriman's empire.

Yet Harriman's legacy transcended the regulatory battles. Harriman explained that the Union Pacific and Southern Pacific together needed 4.5 million ties annually for maintenance of the system, and called ties "the foundation of the transportation line." He understood that railroads weren't just about moving freight—they were about long-term stewardship of vast resources.

Harriman died on September 9, 1909, at his home, Arden, at 1:30 p.m. at age 61. Naturalist John Muir, who had joined him on the 1899 Alaska expedition, wrote in his eulogy of Harriman, "In almost every way, he was a man to admire."

When Harriman died, he left behind a Union Pacific that bore no resemblance to the bankrupt wreck he had purchased twelve years earlier. The railroad was profitable, efficient, and positioned for a century of growth. But more importantly, he had established the template for modern corporate management: data-driven decision making, operational excellence, strategic consolidation, and long-term thinking.

The Harriman revolution had saved Union Pacific from the dustbin of history. Now his successors would have to navigate a new century of challenges: world wars, economic depressions, technological disruption, and regulatory upheaval. The foundation Harriman built would be tested as never before.

VI. Building the Modern Railroad Empire (1910–1980)

The grand ballroom of New York's Waldorf-Astoria hummed with anticipation on January 9, 1920. The board of Union Pacific was about to announce Edward H. Harriman's successor—not as president, but as the spiritual guardian of the railroad empire he had built. The choice surprised no one and everyone: William Averell Harriman, the founder's 28-year-old son, would assume the chairmanship. What followed would be seven decades of transformation that would see Union Pacific evolve from a steam-powered anachronism into a modern transportation colossus.

During his chairmanship of Union Pacific (1920-1946), Harriman promoted the development of Sun Valley and the Utah Parks system, contributed to the design of the first Streamliner, and invented the "roomette" in sleeping cars. The younger Harriman inherited not just his father's railroad but his vision of what a railroad could be: not merely tracks and trains, but a complete transportation and hospitality empire.

W. Averell Harriman was an unlikely railroad baron. William Averell Harriman (November 15, 1891 – July 26, 1986) was an American politician, businessman, and diplomat. He was a founder of Harriman & Co. which merged with the older Brown Brothers to form the Brown Brothers Harriman & Co. investment bank. Unlike his father, who lived and breathed railroads, Averell saw the Union Pacific as one piece of a larger portfolio that would eventually include diplomacy, politics, and international finance.

President of Union Pacific from 1920-1937. During World War I, he was Director of the Division of Transportation Operations for the United States Railroad Administration, a role which placed under his supervision the direction of the operations of all the country's railroads, as a wartime measure. This experience during the war years taught Harriman a crucial lesson: railroads were not just businesses but national infrastructure, essential to American power.

The 1920s brought unprecedented challenges. The automobile was no longer a curiosity but a threat. Commercial aviation was in its infancy but growing. The interstate highway system was still decades away, but roads were improving rapidly. Passenger revenues, once the lifeblood of railroads, began their long decline.

Harriman's response was characteristically bold: if people wouldn't ride trains for transportation, make them ride for experience. In 1936, Averell Harriman, then chairman of the board of the Union Pacific Railroad, built the first streamlined U.S. passenger trains. Looking to attract passenger traffic to his railroad business, he hit upon the idea of building a ski resort.

The creation of Sun Valley represented something unprecedented in American business: a railroad company becoming a lifestyle brand. Sun Valley Resort was the brainchild of Union Pacific Railroad Chairman, Averell Harriman, who thought that creating a ski resort that rivaled those in Europe—St. Moritz, Chamonix—might help reinvigorate passenger service for the railroad. An Austrian count was hired to find the perfect mountain and, once discovered in the midst of remote central Idaho, Harriman immediately began work on creating a destination ski resort worthy of his vision.

The numbers were staggering. Architect Gilbert Stanley Underwood designed the $1.5 million Sun Valley Lodge, incorporating a mix of "Art Deco designs and anything reminiscent of the Union Pacific's streamliners." When Harriman approved construction of the Challenger Inn in 1937, he asked Underwood to design "something like a Tyrolean village."

But Sun Valley wasn't just about skiing. Harriman said Sun Valley operated with a deficit from the beginning, but "we didn't run it to make money; we ran it to be a perfect place. And the deficit was relatively small compared to Union Pacific's income, and the publicity I thought was worth very much more than the deficit." This was a new kind of corporate thinking—the loss leader as brand builder.

Parallel to the resort development came the streamliner revolution. "Tomorrow's Train Today" sped out of the gate on February 12, 1934, beating rival Ralph Budd's Burlington Zephyr into the public eye by two months. Though the now-legendary Burlington Zephyr was in production, it was Averell Harrimann and the Union Pacific that gave America its first taste of streamline design.

The M-10000 was more than a train—it was a cultural phenomenon. Newsweek described the M-10,000 as "a great bulbous-headed caterpillar," but, according to one writer, the train looked more like a snake as it sped along the track. With its novel bubble top, tapered rear car, and waterfall grille, it embodied smooth forward motion even when it stood still. The three-car aluminum-clad train had an exterior color scheme that accentuated its horizontal flow: high-gloss brown on top with a wide yellow band on each side.

By the end of the tour, the M-10,000 had covered 13,000 miles on the tracks of 14 railroads in 22 states, making dozens of stops to allow breathless fans to climb aboard. It is estimated that 15 million people lined up to glimpse the M-10,000 and its rival, the Zephyr, as they sped across the country that summer. In the depths of the Depression, the streamliners offered hope—sleek, modern, fast, they embodied the future America wanted to believe in.

But the real transformation was operational. January 1, 1936: Union Pacific formally leased subsidiaries including Oregon Short Line, Oregon-Washington Railroad & Navigation, Los Angeles & Salt Lake Railroad. This corporate simplification, seemingly mundane, revolutionized how the railroad operated, creating unified command and standardized operations across the system.

World War II changed everything again. As tourist numbers declined, Harriman decided to close the resort in 1942, offering the facilities for government use. In 1943, the Sun Valley Lodge was commissioned as a Naval Convalescent Hospital. "I offered to do it….it was the right thing to do," Harriman recalled. The Navy spent two and a half years at Sun Valley, providing treatment to almost 7,000 men, veterans from the war in the Pacific.

The war years demonstrated Union Pacific's strategic importance. The railroad moved troops, materiel, and raw materials on a scale that dwarfed even the Civil War mobilization. The government effectively controlled operations, but unlike after World War I, there would be no nationalization threat. The railroads had proven themselves too valuable to American capitalism.

The post-war era brought new challenges. The interstate highway system, authorized in 1956, represented an existential threat. Trucking companies could now compete directly with railroads for long-haul freight. Airlines captured the passenger market almost entirely. By 1970, most major railroads had abandoned passenger service entirely, leaving it to the government-created Amtrak.

But Union Pacific adapted. The focus shifted entirely to freight—coal from Wyoming, grain from Nebraska, containers from California ports. The railroad that had been built to carry passengers and mail transformed into a bulk commodity hauler. It was less glamorous than streamliners and Sun Valley, but far more profitable.

The transformation required massive capital investment. Old steam locomotives gave way to diesels. Manual switching yielded to computerized dispatch. Small branch lines were abandoned while main lines were double and triple-tracked. The romantic age of railroading was ending, but a new era of efficiency was beginning.

By 1980, after decades of regulation that had stifled innovation and consolidation, Union Pacific stood at another crossroads. The Staggers Act was about to unleash forces that would transform American railroading as dramatically as the Pacific Railway Act had in 1862. The stage was set for the final act in Union Pacific's evolution: from regulated utility to deregulated profit machine.

VII. Deregulation & The Modern Era (1980–2020)

The conference room at the Interstate Commerce Commission headquarters in Washington D.C. was packed to capacity on October 13, 1980. Railroad executives, lawyers, and journalists had gathered to witness what many thought impossible: the signing of the Staggers Rail Act by President Jimmy Carter. With a stroke of his pen, Carter dismantled nearly a century of suffocating federal regulation. American railroads, including Union Pacific, were finally free to compete.

The timing couldn't have been more critical. By 1980, the railroad industry was dying. Penn Central's spectacular 1970 bankruptcy—the largest corporate failure in American history at the time—had shocked the nation. The Rock Island Line, immortalized in folk songs, had ceased operations earlier that year. Even mighty Union Pacific, despite its storied history, was struggling with antiquated regulations that prevented it from abandoning unprofitable routes, setting competitive rates, or merging with other carriers without years of bureaucratic approval.

The Staggers Act changed everything. Railroads could now negotiate rates directly with shippers, abandon unprofitable branch lines, and most importantly, merge with competitors to achieve economies of scale. Union Pacific wasted no time.

Union Pacific Corporation, the parent company of the Union Pacific Railroad, agreed to buy the Missouri Pacific Railroad on January 8, 1980. Lawsuits filed by competing railroads delayed approval of the merger until September 13, 1982. After the Supreme Court denied a trial to the Southern Pacific, the merger took effect on December 22, 1982.

The Missouri Pacific acquisition was transformative. By the 1980s, the system owned 11,469 miles (18,458 km) of rail line over 11 states bounded by Chicago to the east, Pueblo, Colorado, in the west, north to Omaha, south to the U.S.-Mexico border in Laredo, Texas, and southeast along the Gulf seaports of Louisiana and Texas. At the time of its mega-merger in 1982, the MoPac owned more and newer locomotives and operated more track than partner Union Pacific Railroad.

On December 22, 1982, the Missouri Pacific was purchased by the Union Pacific Corporation and combined with the Western Pacific Railroad and Union Pacific Railroad to form one large railroad system. The merger created a railroad system that could compete with the trucking industry that had been eating away at rail's market share since the interstate highway system's completion.

The integration wasn't without its quirks. During the merger time period, some locomotives were even painted Armour Yellow with "Missouri Pacific" or "Western Pacific" on the hoods. This visual confusion reflected the deeper challenge of melding three distinct corporate cultures into one.

But Union Pacific's appetite for growth was just beginning. As the 20th century waned, Union Pacific recognized—like most railroads—that remaining a regional railroad would only lead to bankruptcy. On December 31, 1925, UP and its subsidiaries operated 9,834 miles (15,826 km) routes and 15,265 miles (24,567 km) tracks; in 1980, these numbers had remained roughly constant (9,266 route-miles and 15,647 track-miles). But in 1982, UP acquired the Missouri Pacific and Western Pacific railroads, and 1988, the Missouri–Kansas–Texas. By 1993, Union Pacific had doubled its system to 17,385 miles (27,978 km) routes.

The consolidation wave accelerated in the mid-1990s. By then, few large (class I) railroads remained. The same year that Union Pacific merged with the Chicago and North Western (1995), Burlington Northern and ATSF announced merger plans. The impending BNSF amalgamation would leave one mega-railroad in control of the west. To compete, UP merged with Southern Pacific, thereby incorporating D&RGW and Cotton Belt, and forming a duopoly in the West.

The Southern Pacific acquisition in 1996 was the crown jewel—and nearly a catastrophe. With its acquisition of the Southern Pacific Rail Corporation in 1996, Union Pacific became the largest domestic railroad in the United States, controlling almost all of the rail-based shipping in the western two-thirds of the country. Union Pacific acquired control of SP on Sept. 11, 1996.

But the merger created operational chaos. The 1996 merger of Union Pacific and Southern Pacific had temporarily led to severe congestion and delays across the Southwest. Trains sat idle for days. Shipments of everything from grain to chemicals backed up. The Surface Transportation Board, successor to the ICC, had to intervene, forcing Union Pacific to grant trackage rights to competitors and implement emergency measures to clear the congestion.

The crisis taught Union Pacific a crucial lesson: size without operational excellence was a recipe for disaster. The company spent the late 1990s and early 2000s focusing on what it called "network fluidity"—making sure trains actually moved rather than just acquiring more track.

Technology became the differentiator. Union Pacific invested billions in Positive Train Control, automated dispatching systems, and predictive maintenance. The railroad that had been built with picks and shovels was now run by algorithms and satellites.

From the second half of 2005 to the summer of 2006, UP unveiled a new set of six EMD SD70ACe locomotives in "Heritage Colors", painted in schemes reminiscent of railroads acquired by the Union Pacific Corporation since the 1980s. The engine numbers match the year that the predecessor railroad became part of the Union Pacific system. The locomotives commemorate the Missouri Pacific with UP 1982, the Western Pacific with UP 1983, the Missouri–Kansas–Texas with UP 1988, the Chicago and North Western with UP 1995, the Southern Pacific with UP 1996, and the Denver and Rio Grande Western with UP 1989.

These heritage units were more than nostalgia—they were a statement that Union Pacific had successfully integrated a half-dozen major railroads into one cohesive system. By 2020, the consolidation era appeared complete. Only seven Class I railroads remained in North America, down from over 100 a century earlier. Union Pacific and BNSF controlled the West, Norfolk Southern and CSX the East, with Canadian National, Canadian Pacific, and Kansas City Southern filling the gaps.

The modern Union Pacific bore little resemblance to the railroad Durant had schemed into existence or Harriman had rescued from bankruptcy. It was a precision logistics machine, moving 40% of the nation's freight with an efficiency that would have seemed impossible to previous generations. Coal from Wyoming's Powder River Basin, containers from Long Beach, automobiles from Mexico, grain from Nebraska—all moved on a network optimized by decades of consolidation and billions in technology investment.

By 2020, as the world entered a new decade, Union Pacific seemed to have reached its final form—a Western giant in comfortable duopoly with BNSF, generating steady profits for shareholders while efficiently moving America's freight. The era of massive mergers appeared over.

But in corporate boardrooms in Omaha and Atlanta, executives were having quiet conversations about something that hadn't been attempted since the Gilded Age: creating a truly transcontinental railroad under single ownership. The stage was being set for Union Pacific's boldest move yet.

VIII. The Financial Machine: 2020–2024 Performance

The fluorescent lights in Union Pacific's Omaha headquarters war room glowed 24/7 in August 2023. Maps covered every wall, displaying real-time train movements across 32,000 miles of track. Into this nerve center walked Jim Vena, the new CEO who'd been hired to transform America's largest railroad from a good operator into a great one. His mandate was simple but daunting: make Union Pacific the industry's operational gold standard while delivering superior returns to increasingly impatient shareholders.

"One of the most vital characteristics we considered as we conducted the search to identify the next CEO was extensive railroad operating experience," said McCarthy. "Jim has that and more. After a comprehensive search process, the Board unanimously determined that his track record of operating excellence was unparalleled, and he is the right candidate for the job." The board had recruited Vena from retirement after activist investor Soroban Capital Management pushed for change, arguing Union Pacific was underperforming its potential.

Vena brought a different philosophy to Union Pacific—one forged over 40 years at Canadian National Railway where he'd helped pioneer Precision Scheduled Railroading (PSR). But Vena's version wasn't just about running longer trains with fewer locomotives. It was about creating a culture of continuous improvement where every employee thought like an owner.

"The team has fully embraced our strategy to lead the industry in safety, service, and operational excellence. That commitment has produced industry leading financial results in 2024, punctuated by our strong finish to the year." By the end of 2024, Vena's transformation was delivering results that exceeded even optimistic projections.

The numbers told a story of operational metamorphosis. Reported net income for full year 2024 was $6.7 billion, or $11.09 per diluted share. These full year results compare to full year 2023 net income of $6.4 billion, or $10.45 per diluted share. A 6% improvement in earnings per share might seem modest, but in the capital-intensive railroad business, it represented billions in value creation.

What drove these results wasn't revenue growth—Operating revenue of $6.1 billion was down 1% driven by lower fuel surcharge revenue, unfavorable business mix, and lower other revenue, partially offset by increased volume and core pricing gains. Instead, Vena focused relentlessly on efficiency, turning Union Pacific into a lean operating machine.

The operational metrics revealed the transformation's depth. Freight car velocity improved 2% to 208 daily miles per car. That might sound incremental, but it meant freight moved faster, reducing the need for expensive rolling stock. Locomotive productivity improved 5% to 135 GTMs per horsepower day. Each locomotive was pulling more tonnage more miles—the railroad equivalent of getting more miles per gallon.

Most impressively, Workforce productivity improved 6% to 1,062 car miles per employee. Union Pacific was moving more freight with fewer people, not through layoffs but through smarter operations. Trains ran on schedule. Switching yards operated like clockwork. The chaos that had plagued the 1996 Southern Pacific merger was ancient history.

The financial engineering matched the operational excellence. The company generated $9.3 billion in cash from operations, with free cash flow surging from $1.5 billion to $2.8 billion. Union Pacific returned $4.7 billion to shareholders through dividends and buybacks—a staggering amount that reflected confidence in sustainable cash generation.

But Vena's true innovation was cultural. "I said from day one I would ask a lot of you, and demand even more from myself," Vena said. He pushed decision-making down to the field level, empowering local managers to solve problems without waiting for Omaha's approval. "Driving decision-making down to the front level so that they make the decisions locally because they're better off making them locally -- the decisions -- than somebody in Omaha."

The safety improvements were perhaps most remarkable. Union Pacific's reportable personal injury and reportable derailment rates both improved. In an industry where one derailment could cost hundreds of millions and destroy public trust, safety wasn't just morally imperative—it was financially essential.

Vena also understood that Union Pacific's future depended on winning market share from trucking. With Fuel consumption rate improved 1% to 1.082, measured in gallons of fuel per thousand GTMs, railroads could move a ton of freight 470 miles on a single gallon of fuel—four times more efficient than trucks. As environmental regulations tightened and carbon pricing loomed, this advantage would only grow.

The technology investments were less visible but equally transformative. Artificial intelligence optimized train consists. Predictive analytics anticipated equipment failures before they happened. Automated track inspection eliminated human error. Union Pacific was becoming a technology company that happened to run trains.

By year-end 2024, Union Pacific's operating ratio—operating expenses as a percentage of revenue—had improved 240 basis points to 59.9%. In railroad terms, this was approaching best-in-class performance. The company's return on invested capital reached 15.8%, well above its cost of capital and among the best in the industry.

The market responded enthusiastically. Union Pacific's stock price surged, reaching all-time highs. The company's market capitalization exceeded $150 billion, making it one of America's most valuable transportation companies. Institutional investors who'd been skeptical of railroads' future were converts.

But Vena wasn't satisfied with incremental improvement. In private strategy sessions, he pushed his team to think bigger. What if Union Pacific didn't just compete with other railroads but redefined what a railroad could be? What if they could offer truck-like service with rail economics? What if they could guarantee delivery times like FedEx while moving trainloads of freight?

These weren't idle questions. Vena knew that to justify Union Pacific's premium valuation, the company needed to do more than optimize existing operations. It needed to grow. And in the consolidated world of North American railroading, organic growth had limits.

As 2024 drew to a close, rumors began circulating in railroad circles. Union Pacific executives were spotted in Atlanta. Investment bankers were working overtime. Something big was brewing. The operational excellence Vena had delivered wasn't the end goal—it was preparation for Union Pacific's boldest move yet. The company that had united East and West in 1869 was about to attempt something even more audacious: creating America's first truly transcontinental railroad system.

IX. The Norfolk Southern Bombshell & Future Vision

The morning of July 29, 2025, began like any other in the financial district of lower Manhattan. But by 7:00 AM Eastern, when the joint press release hit the wires, the railroad industry—and American business—would never be the same. Under the terms of the agreement, Union Pacific will acquire Norfolk Southern in a stock and cash transaction, implying a value for Norfolk Southern of $320 per share based on Union Pacific's unaffected closing stock price on July 16, 2025, and representing a 25% premium to Norfolk Southern's 30-trading day volume weighted average price on July 16, 2025. The value per share implies an enterprise value of $85 billion for Norfolk Southern, resulting in the creation of a combined enterprise of over $250 billion.

The announcement represented the culmination of months of secret negotiations that had begun in January 2025. The slow drip of merger news started weeks before the announcement, when on July 16, online news site Semafor reported that UP had hired Morgan Stanley to explore acquiring one of the other five Class I railroads. Later that day, it was reported that UP had been in talks with NS about a possible merger since the beginning of the year.

Jim Vena had orchestrated the deal with the precision he brought to railroad operations. "Railroads have been an integral part of building America since the Industrial Revolution, and this transaction is the next step in advancing the industry," said Jim Vena, Union Pacific Chief Executive Officer. "Imagine seamlessly hauling steel from Pittsburgh, Pennsylvania to Colton, California and moving tomato paste from Huron, California to Fremont, Ohio.

The strategic logic was compelling. Union Pacific and Norfolk Southern announced an $85 billion merger to create the first U.S. transcontinental railroad, resulting in a combined enterprise value exceeding $250 billion. The merger aims to improve the U.S. supply chain by creating $2.75 billion in annual synergies (revenue growth and cost savings) and offering faster, more comprehensive freight service. The combined company will stretch across 52,215 route miles, serving 43 states and approximately 100 ports, shifting freight to rail to reduce highway congestion.

For the first time in American history, a single railroad would span coast to coast. The inefficiencies of interchange—where cargo had to be transferred between railroads, adding days to transit times and billions in costs—would disappear for transcontinental shipments. A container from Shanghai could land in Long Beach and travel all the way to Norfolk, Virginia, on a single railroad's network.

The financial engineering was as sophisticated as the operational strategy. Norfolk Southern shareholders will receive 1.0 Union Pacific common share and $88.82 in cash for each share of Norfolk Southern. The implied value of $320 per share represents an implied total enterprise value for Norfolk Southern of $85 billion based on Union Pacific's unaffected closing stock price on July 16, 2025. Union Pacific will issue a total of approximately 225 million shares to Norfolk Southern shareholders, representing 27% ownership in the combined company on a fully diluted basis, and providing the ability of Norfolk Southern shareholders to participate in the upside of the combined company's growth opportunities and synergies.

But the announcement immediately triggered a cascade of reactions across the industry. Then, on July 21, Semafor reported that BNSF Railway had enlisted Goldman Sachs for its own merger bid. Reuters later reported that CSX was its target. BNSF has not given a statement regarding the proposed UP-NS merger. However, if it doesn't make an offer for CSX — or even a competing offer for NS — it's likely that the Class I railroad (currently the largest in North America) will vigorously oppose the UP-NS merger.

The regulatory challenge loomed large. The deal will face lengthy regulatory scrutiny amid union concerns over potential rate increases, service disruptions and job losses. The 1996 merger of Union Pacific and Southern Pacific had temporarily led to severe congestion and delays across the Southwest. The ghosts of that operational meltdown still haunted the Surface Transportation Board.

Yet the political environment had shifted dramatically. The deal reflects a shift in antitrust enforcement under U.S. President Donald Trump's administration. Executive orders aimed at removing barriers to consolidation have opened the door to mergers that were previously considered unlikely. Surface Transportation Board (STB) Chairman Patrick Fuchs, appointed by Trump in January to head the agency that oversees competition and other areas of economic importance in the rail industry, has advocated for faster preliminary reviews and a more flexible approach to merger conditions.

Union Pacific and Norfolk Southern pitched the merger as essential to American competitiveness. Clearly framed as a message to the current Presidential Administration and its "America First" mantra, Union Pacific and Norfolk Southern noted that, combined, they "invest approximately $5.6 billion annually in infrastructure, innovation, and network expansion. U.S. freight railroads move approximately 1.5 billion tons of material and goods every year. The transcontinental railroad will compete more effectively with Canadian railroads to win back U.S. freight volume and American jobs."

The labor angle was carefully managed. Both railroads envision every union employee who wants a job in the combined company will have one. The deal is subject to Surface Transportation Board (STB) approval and is expected to close by early 2027, with all union jobs preserved. This promise—remarkable in an industry known for workforce reductions after mergers—reflected both the tight labor market and the political necessity of union support.

Jim Vena would lead the combined company, having "committed his intent to remain at Union Pacific for at least the next five years." Norfolk Southern CEO Mark George would have a senior role in the transition, with three Norfolk Southern Directors, including Mark George and Richard Anderson, expected to join the Union Pacific Board of Directors after completing the corporate governance process.

The integration plan was ambitious but methodical. The transaction, expected to be filed with the Surface Transportation Board within six months, undergo a 15-month review process and close by early 2027. The companies expect to file their application with the STB within six months, in which the companies will describe how the combined rail network will provide safer, faster, and more reliable service and increased competition. A pre-filing notification of intent to file an application could come as soon as Wednesday, and is the first official step in the merger evaluation timeline.

The financial markets' initial reaction was mixed. Union Pacific stock fell on dilution concerns while Norfolk Southern soared on the premium. But longer-term investors saw the strategic logic: Union Pacific and Norfolk Southern shareholders are expected to realize significant value from the transaction, including more than $30 billion of potential value creation through the expected achievement of approximately $2.75 billion in annualized synergy opportunity.

The operational benefits extended beyond simple cost savings. Single-line service from Los Angeles to Atlanta would cut transit times by 24-48 hours. Automotive plants in the Southeast could receive parts from Mexico without interchange delays. Coal from Wyoming could reach Eastern power plants more efficiently. The network effects were multiplicative, not additive.

Technology would be crucial to integration success. Unlike the 1996 Southern Pacific debacle, Union Pacific now had sophisticated network modeling tools, AI-driven dispatch systems, and real-time visibility across its entire network. The company had learned from past mistakes and invested billions in the infrastructure needed to handle increased traffic flows.

Environmental considerations also factored prominently. A transcontinental railroad could shift millions of truck-miles to rail, reducing carbon emissions and highway congestion. With the Biden administration's infrastructure focus and climate goals, this environmental angle provided political cover for a deal that might otherwise face opposition.

But challenges remained formidable. "The Union Pacific merger would create a railroad with the largest market share across most commodities," according to Jason Miller, interim chair of the department of supply chain management at Michigan State University's business college. "I can't help but think this would create pressure for BNSF Railway and CSX to explore a merger possibility."

The competitive response was already forming. BNSF and CSX, facing the prospect of competing against a transcontinental giant, would likely pursue their own merger or mount fierce opposition to the UP-NS combination. Shippers worried about reduced competition and higher rates were organizing opposition. The Brotherhood of Railway Carmen and other unions, despite job guarantees, remained skeptical.

As Jim Vena and Mark George signed the merger agreement in Union Pacific's Omaha headquarters, they were acutely aware of the historical moment. Union Pacific CEO Jim Vena and Norfolk Southern President and CEO Mark George sign the agreement between the two companies. Union Pacific signed an agreement to merge with Norfolk Southern and become America's first transcontinental railroad, creating a coast-to-coast network that will span more than 50,000 miles, serve 43 states from the East Coast to the West Coast, link approximately 100 ports and reach nearly every corner of North America.

The dream that had begun with Lincoln's signature in 1862—a truly unified transcontinental railroad—was finally within reach. But whether this bold vision would survive regulatory scrutiny, operational integration, and competitive challenges remained the great unknown. The next 18 months would determine whether Union Pacific's continental ambitions would reshape American transportation or join the graveyard of failed mega-mergers.

X. Playbook: Lessons in Empire Building

The conference room on the 19th floor of Union Pacific's headquarters overlooks the Missouri River, the same waterway that served as the railroad's eastern terminus when construction began in 1863. It's here that senior executives gather each morning to review operational metrics that would have seemed like sorcery to Thomas Durant or even Edward Harriman. But the fundamental questions they grapple with remain unchanged: How do you build and sustain a continental empire?

The Union Pacific story offers a masterclass in empire building, with lessons that transcend the railroad industry. From Lincoln's wartime gamble to Vena's transcontinental vision, certain patterns emerge—strategies that enabled survival through panics, depressions, wars, and technological disruption.

The Power of Government Partnership (When It Works)

The Pacific Railway Act of 1862 created Union Pacific through unprecedented government intervention—land grants, loans, and monopoly rights that would be unthinkable today. Yet this partnership nearly destroyed the company through the Crédit Mobilier scandal. The lesson isn't that government partnership is good or bad, but that it must be carefully structured with aligned incentives.

Modern Union Pacific still benefits from government partnership, but in different forms. Tax incentives for infrastructure investment, public-private partnerships for grade separations, and environmental credits for fuel efficiency all echo the original government support, albeit with better oversight. The key is ensuring public benefit aligns with private profit—when that balance tips too far either way, disaster follows.

Surviving Existential Crises: From Bankruptcy to Dominance

Union Pacific has faced existential threats roughly every generation: the Panic of 1873, the receivership of 1893, the Great Depression, the interstate highway system, deregulation chaos, and now the promise and peril of autonomous vehicles. Each crisis followed a pattern: overleveraging during boom times, near-death in the bust, then resurrection through operational excellence and consolidation.

The Harriman rescue of 1897 provides the template. When others saw a failed railroad worth only scrap value, Harriman recognized undervalued assets and operational potential. He didn't just recapitalize the company; he transformed its culture, operations, and strategic position. This pattern—crisis, transformation, dominance—has repeated throughout Union Pacific's history.

The Harriman Doctrine: Consolidation as Competitive Advantage

Known for possessing a vision of the new order toward which railroads were evolving, Harriman embraced gigantic undertakings and served as a catalyst in changing how railroads were run, specifically promoting consolidation and acquiring rival companies. One scholar writes of Harriman, "If they would not sell the colt, Harriman would buy the mare."

Harriman understood that in capital-intensive industries with high fixed costs and network effects, scale is destiny. Every merger—Missouri Pacific, Western Pacific, Southern Pacific, and now Norfolk Southern—follows this logic. The combined network is worth more than the sum of its parts because eliminating interchange points, combining parallel routes, and spreading fixed costs over more volume creates value that organic growth cannot match.

But consolidation without integration is destruction, as the 1996 Southern Pacific merger nearly proved. The playbook requires not just financial engineering but operational excellence, cultural integration, and customer focus. Size alone doesn't guarantee success—execution does.

Network Effects in Physical Infrastructure

Unlike digital networks where adding users is virtually costless, physical networks require massive capital investment. Yet the principle remains: each additional connection makes the entire network more valuable. A railroad that reaches both coasts is exponentially more valuable than two railroads that meet in the middle.

Union Pacific has systematically built these network effects through strategic acquisitions and partnerships. Intermodal terminals that connect rail to truck, agreements with steamship lines, and even the old Harriman idea of integrated transportation systems all leverage network effects. The Norfolk Southern merger represents the ultimate expression of this strategy—a network so comprehensive that shippers can't avoid using it.

Capital Intensity as a Moat

Warren Buffett famously said railroads have the widest moats in American business because nobody can replicate their infrastructure. Union Pacific has turned this capital intensity from burden to advantage. The billions required to maintain and upgrade 32,000 miles of track, thousands of locomotives, and hundreds of yards creates an insurmountable barrier to entry.

But capital intensity only becomes a moat if coupled with operational excellence. Poorly run railroads eat capital without generating returns. Well-run railroads like Union Pacific generate returns on invested capital that exceed their cost of capital, creating a virtuous cycle of investment and returns that competitors can't match.

Operational Excellence as the Ultimate Differentiator

The Vena era has proven that operational excellence, not financial engineering, drives sustainable value creation. Improving velocity by 2%, productivity by 5%, and safety metrics by double digits translates to billions in value. These improvements compound—faster trains need fewer locomotives and crews, which reduces costs, which allows for better pricing, which wins more volume, which improves density, which enables faster trains.

This operational flywheel, once spinning, is hard for competitors to stop. Union Pacific's current operational metrics lead the industry not through radical innovation but through thousands of incremental improvements. It's the aggregation of marginal gains that creates insurmountable advantage.

Why Railroads Still Matter in the Digital Age

In an economy increasingly dominated by bits rather than atoms, railroads seem anachronistic. Yet they've never been more essential. E-commerce requires physical delivery. Electric vehicles need raw materials. Solar panels and wind turbines must be transported. The digital economy runs on physical infrastructure, and railroads remain the most efficient way to move heavy things long distances.

Moreover, environmental pressures make rail transport increasingly attractive. Moving freight by rail produces 75% fewer greenhouse gas emissions than truck transport. As carbon pricing becomes reality and environmental regulations tighten, this advantage will only grow. The 19th-century technology may be the 21st century's environmental solution.

The Integration Imperative

Union Pacific's history teaches that successful integration requires more than combining operations. It demands cultural alignment, systems integration, and customer communication. The failures—like the Southern Pacific merger chaos—occurred when financial timelines overrode operational readiness. The successes—like the Missouri Pacific integration—happened when operations drove the timeline.

The Norfolk Southern integration will test these lessons. Success requires maintaining service levels while capturing synergies, preserving both cultures while creating one company, and delivering shareholder value while serving customers. It's a three-dimensional puzzle that requires strategic thinking, operational excellence, and flawless execution.

The Long Game

Perhaps the most important lesson from Union Pacific's history is the value of long-term thinking. The transcontinental railroad took seven years to build and didn't become profitable for decades. The Harriman improvements required massive upfront investment that took years to pay off. Today's technology investments won't show full returns for years.

This long-term orientation conflicts with quarterly earnings pressure, but Union Pacific has learned to balance both. The company delivers consistent quarterly results while investing for decades ahead. It's this ability to operate in multiple time horizons simultaneously that separates empire builders from mere operators.

The Innovation Paradox

Railroads are simultaneously ancient and cutting-edge. The basic technology—steel wheels on steel rails—hasn't changed since the 1820s. Yet Union Pacific employs artificial intelligence, automated systems, and precision scheduling that would seem like magic to previous generations. The lesson: innovation doesn't always mean disruption. Sometimes it means perfecting existing technology.

Union Pacific has learned to be a fast follower rather than a first mover. Let others test new technologies; Union Pacific implements proven solutions at scale. This approach lacks Silicon Valley glamour but generates superior returns with lower risk.

As Union Pacific stands on the verge of its transcontinental transformation, these lessons become more relevant than ever. The company that began as Lincoln's wartime necessity has evolved into a logistics platform essential to American commerce. The playbook written over 160 years—through bankruptcy and boom, scandal and success—provides the roadmap for continued dominance. The rails may be steel, but the strategy is timeless.

XI. Analysis: Bull vs. Bear Case

The investment committee at a major pension fund sits around a polished table, Union Pacific's latest investor presentation glowing on the screen. The fund already owns $2 billion worth of UP stock. The question before them: with the Norfolk Southern merger pending and the stock near all-time highs, should they add, hold, or trim their position? The debate that follows encapsulates the bull and bear cases that investors worldwide are weighing.

Bull Case: The Irreplaceable Infrastructure Thesis

The bull case begins with Union Pacific's irreplaceable asset base. Over the next century, UP absorbed the Missouri Pacific Railroad, the Western Pacific Railroad, the Missouri–Kansas–Texas Railroad and the Chicago, Rock Island and Pacific Railroad. This consolidation created a network that would cost hundreds of billions to replicate today—if it were even possible given environmental and property rights constraints.

The Norfolk Southern acquisition amplifies this advantage exponentially. Union Pacific and Norfolk Southern announced an $85 billion merger to create the first U.S. transcontinental railroad, resulting in a combined enterprise value exceeding $250 billion. The combined company will stretch across 52,215 route miles, serving 43 states and approximately 100 ports. No competitor could match this reach without their own transformative merger.

The operational leverage story is compelling. With operating ratio improving 240 basis points to 59.9% and return on invested capital at 15.8%, Union Pacific has proven it can convert revenue growth directly to the bottom line. The company's ability to move more freight with fewer resources—productivity up 6% with existing assets—suggests significant untapped potential.

The synergy opportunity from Norfolk Southern is massive. Union Pacific and Norfolk Southern shareholders are expected to realize significant value from the transaction, including more than $30 billion of potential value creation through the expected achievement of approximately $2.75 billion in annualized synergy opportunity. These aren't speculative revenue synergies but hard cost savings from eliminating interchange, combining back-office functions, and optimizing network flows.

Environmental tailwinds provide long-term support. Rail transport's 75% lower emissions than trucking becomes increasingly valuable as carbon pricing spreads. The Biden infrastructure bill's emphasis on rail, combined with corporate ESG commitments, positions Union Pacific as the green logistics solution. The company moving a ton of freight 470 miles on a gallon of fuel isn't just efficient—it's essential to meeting climate goals.

Pricing power remains robust despite competition. Union Pacific has consistently achieved core pricing gains above inflation, even during economic softness. The elimination of truck competition for long-haul freight—trucks can't match rail economics over 500 miles—provides a pricing floor. With the Norfolk Southern merger, pricing power for transcontinental shipments increases dramatically.

The technology transformation story is underappreciated. While markets obsess over autonomous vehicles threatening railroads, Union Pacific is deploying AI and automation that dramatically improves returns. Predictive maintenance reduces derailments. Automated dispatching optimizes network flows. Precision Scheduled Railroading drives efficiency. The company is becoming a technology platform that happens to own rails.

Management quality under Jim Vena represents a step change. His track record of operational improvement at Canadian National, replicated at Union Pacific, suggests sustainable margin expansion. The cultural transformation—pushing decision-making to the field, emphasizing safety and service—creates a virtuous cycle of improvement that compounds over time.

Capital allocation remains shareholder-friendly. The company repurchased 6.3 million shares in 2024 at an aggregate cost of $1.5 billion. With free cash flow surging to $2.8 billion, Union Pacific can fund growth, maintain the network, pay rising dividends, and buy back stock. This balanced approach satisfies both income and growth investors.

Bear Case: The Disruption and Regulatory Risk Thesis

The bear case starts with regulatory risk on the Norfolk Southern deal. The Surface Transportation Board has become increasingly skeptical of railroad consolidation. The 1996 Southern Pacific merger's operational meltdown remains fresh in regulators' minds. Even with a friendly administration, approval isn't guaranteed, and conditions could gut projected synergies.

The integration risk is enormous. The 1996 merger of Union Pacific and Southern Pacific had temporarily led to severe congestion and delays across the Southwest. Combining two massive railroads with different systems, cultures, and operations could trigger another service crisis. Customer defections during integration chaos could permanently impair the franchise.

Coal's structural decline accelerates. Coal shipments fell 22% in just one quarter, and this trend will only worsen as utilities shift to renewables. Coal has been Union Pacific's highest-margin business; its loss can't be fully offset by other commodities. The energy transition that helps rail versus trucking hurts Union Pacific's most profitable franchise.

Autonomous trucking poses an existential threat. While bulls dismiss self-driving trucks, the technology is advancing rapidly. Autonomous trucks could eliminate drivers—trucking's largest cost—making them competitive with rail for long-haul freight. If trucks can match rail economics, Union Pacific's moat evaporates.

Economic sensitivity remains high despite diversification. Recessions hit railroads hard as volumes collapse faster than costs can be cut. With recession risks rising from Federal Reserve tightening, Union Pacific could face sharp earnings declines. The operational leverage that drives profits in good times amplifies losses in downturns.

The capital intensity limits returns. While bulls tout capital requirements as a moat, bears see them as a ball and chain. Union Pacific must spend $3.5 billion annually just to maintain its network. Growth requires billions more. This capital intensity caps returns on equity and limits financial flexibility during downturns.