Unum Group: America's Disability Insurance Giant

The 175-Year Transformation of a Fortune 500 Insurance Colossus

I. Introduction: The Resilience Paradox

Picture a company that has survived the Civil War, two World Wars, the Great Depression, a devastating regulatory scandal that forced it to reopen 200,000 denied claims, and a "ticking time bomb" of legacy long-term care liabilities that has spooked investors for over a decade. Now picture that same company trading near all-time highs, generating a return on equity approaching 20%, and commanding the dominant position in America's disability insurance market.

Welcome to Unum Group.

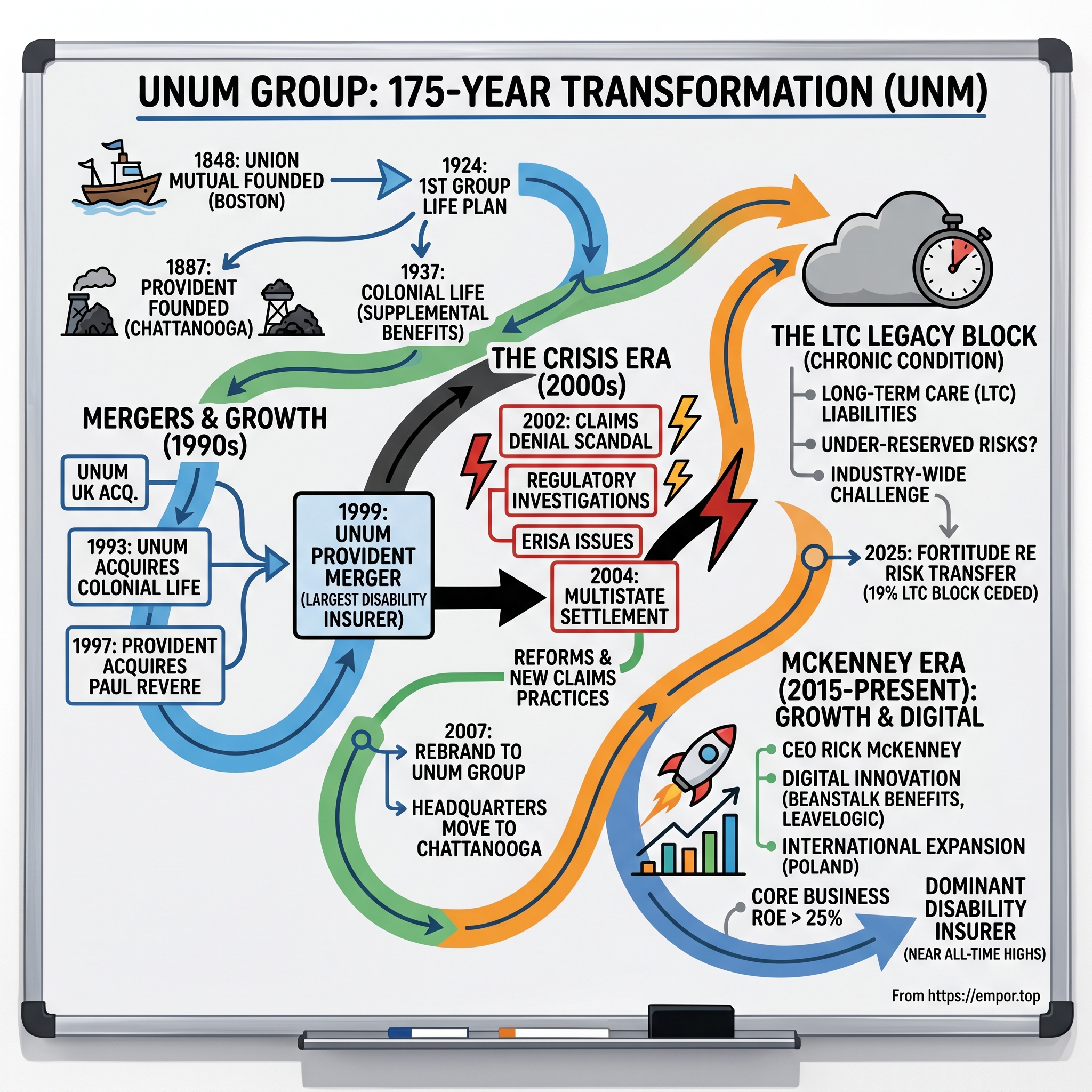

Unum Group is an American insurance company headquartered in Chattanooga, Tennessee. Founded as Union Mutual in 1848 and known as UnumProvident from 1999–2007, the company is part of the Fortune 500. In 2022, Unum insured about 45 million individuals through group policies and reported revenue of $11.991 billion.

The company's journey is one of the most improbable survival stories in American corporate history—a tale of strategic pivots, regulatory crises, leadership transitions, and the slow, grinding work of managing legacy liabilities while building a modern employee benefits franchise. Founded in Chattanooga, Tennessee, Unum is the largest disability insurance provider in the United States. Its legacy dates to its founding as Union Mutual in 1848, and it became a pioneer in offering disability insurance products.

The core question animating this deep dive: How did a 175-year-old mutual insurance company survive scandal, regulatory crisis, and a massive legacy liability time bomb to become a market leader? And what does Unum's future look like as it attempts to shed the weight of its troubled past?

II. The Origins: Three Companies That Became One

The Birth of Union Mutual (1848-1986)

The story begins not in Tennessee, but in the parlor of a Boston home in 1848. Elisha B. Pratt had been one of the founders of Connecticut Mutual Life Insurance Company that same year, but after a falling out with management—the kind of corporate discord that has launched countless entrepreneurial ventures—Pratt obtained a charter in Maine to form Union Mutual. In 1849, our first policy for $5,000 in life insurance was issued by Union Mutual.

Despite the Maine charter, Pratt ran the company out of Boston, a geographic quirk that would persist for decades. The company was slow to grow, but it proved remarkably durable. By 1864, Union Mutual had become a pioneer in an obscure but consequential corner of insurance: the company helped birth the American reinsurance market by reinsuring Chicago Mutual Life—a risk-sharing mechanism that would become essential to the modern insurance industry.

The company's real breakthrough came in 1924, when Union Mutual offered the industry's first group life insurance plan. This innovation—selling life insurance to companies rather than individuals, with employees as beneficiaries—would prove transformative. The group insurance model aligned the interests of employers (who wanted to attract and retain workers), employees (who gained coverage they couldn't afford individually), and insurers (who achieved scale and administrative efficiency). It was a business model insight that would eventually define Unum's entire identity.

The Provident Story: From Coal Mines to Corporate Benefits (1887-1999)

Seven hundred miles south of Portland, Maine, a very different insurance company was taking shape. Provident's forerunner, the Mutual Medical Aid and Accident Insurance Company, was founded in Chattanooga, Tennessee, in May 1887. Established in 1887 during the southern industrial boom, Provident has weathered two world wars, the Great Depression and, more recently, health-care-cost inflation and increasing industry regulation. The company was a pioneer in first covering "uninsurable" workers, such as those at coal mines, blast furnaces, coke ovens, and certain railroad occupations.

The founders—a group that included lawyers, an architect, and a real estate salesman, none of whom had any real knowledge of insurance—learned hard lessons fast. The founders were forced to reverse their medical-aid policies almost immediately, after realizing that a single yellow fever epidemic—like the one in 1878—could wipe out the company. They bought back some 100 medical policies and resolved to sell only accident insurance.

The early years were brutal. When local iron ores proved unsuitable for steelmaking, Chattanooga's development stalled. Companies withdrew, businesses defaulted, and seven banks collapsed. In five years of business, Provident had moved five times. It had 850 accident policies and no life policies. By 1892 Provident had also moved through 15 directors, and two Scotsmen offered to pay $1,000 for a one-half interest in the directionless company.

Those Scotsmen—Thomas Maclellan and John McMaster—would transform the company. The Maclellan family would guide Provident for generations, building it into a regional powerhouse. Provident became the first insurer to offer disability benefits in 1939—a product innovation that would ultimately define the merged company's identity.

Despite its name, Provident did not sell its first life insurance policy until 1917—three decades after its founding. The company's DNA was accident and disability insurance, coverage for America's industrial workforce in dangerous occupations. This specialized focus would prove prescient.

Colonial Life: The Voluntary Benefits Pioneer (1937-1993)

Mutual Accident Company was founded in Columbia, South Carolina. It was renamed Colonial Life and Accident Insurance Company two years later. Colonial carved out its own niche: voluntary benefits sold directly to employees through the worksite, often through payroll deduction. These products—accident, cancer, life insurance—were supplemental to employer-provided coverage, giving workers the option to purchase additional protection.

The voluntary model created a different distribution and underwriting dynamic than group insurance. Employees made individual purchasing decisions, and Colonial's sales force developed deep relationships with both employers and workers. This ground-level presence would eventually prove invaluable to Unum.

In 1993, UNUM acquired Colonial, recognizing that the voluntary benefits platform complemented its group insurance franchise. The acquisition brought both distribution capabilities and a product line that addressed gaps in employer-provided coverage.

What investors should take from this origin story: The three companies that eventually merged into Unum each pioneered distinct approaches to employee benefits—Union Mutual in group life, Provident in disability, and Colonial in voluntary products. This diversified heritage created a franchise that could address the full spectrum of workplace protection needs, from employer-paid core benefits to employee-purchased supplemental coverage. The foundation was laid for what would become America's dominant disability insurer.

III. The Demutualization & Strategic Pivot (1982-1990)

The Bold Gamble on Focus

By the early 1980s, Union Mutual faced an existential question that confronts many mature companies: compete broadly against larger rivals, or find a niche and dominate it?

In recognition of the encroaching threat to the company, executives in 1982 took measures to shift Union Mutual's focus away from market segments that were becoming dominated by the major national insurers. They also decided to take the company public (Union Mutual Life Insurance Company was a mutual company, meaning that it was owned by its policyholders).

The decision to demutualize was revolutionary. "The company was in a very, very exciting period of transition—demutualization. It was the first, if not only, major demutualization in insurance that's ever taken place," recalled James Orr later. Mutual insurance companies—owned by policyholders rather than shareholders—were the traditional structure for life insurers. Going public meant introducing an entirely new stakeholder group with different expectations: quarterly earnings, return on equity, share price performance.

In 1986 Union Mutual changed its name to UNUM, the Latin word for the numeral one. UNUM's directors hired James F. Orr III to help Chief Executive Colin Hampton oversee its transition from a mutual to a public company. Hampton, who had served as UNUM's leader for 15 years, believed that going public would bring much-needed expansion capital into the company. He also felt that Union Mutual would benefit from the accountability imposed by a corporate structure. The 43-year-old Orr was an executive at Connecticut Bank & Trust before joining UNUM.

The Capital Transformation

In November 1986 UNUM distributed its entire net worth of $700 million to its policyholders. The company simultaneously sold new shares to new shareholders, a move that brought $700 million into the corporation's coffers.

This financial engineering was elegant: policyholders received the value they had accumulated over decades, while new shareholders provided fresh capital for growth. But the cultural transition was wrenching.

Policyholders and employees were not accustomed to having the company's business scrutinized by the general public. As a result, Orr was deluged with complaints at times. "Looking back on it, I think we all underestimated how difficult it would be to get the people in the company oriented to having a new stakeholder group out there, namely, our shareholders," Orr noted.

The Orr Transformation

James Orr proved to be the right leader for a company in transition. Orr, who had been a track star at Villanova University in the 1960s, was recognized as an intelligent, frank, even-tempered achiever. He brought banking and financial services experience—crucially, he understood capital markets and shareholder expectations in ways that lifetime insurance executives might not.

Within a year of his arrival—Orr officially assumed the chief executive slot in 1987—he slashed $25 million from UNUM's annual expenses by trimming back the workforce and dumping some of the organization's slumping divisions.

But Orr's most consequential decision wasn't about cost-cutting—it was about strategic focus. Union Mutual had been trying to exit various nonperforming businesses since the early 1980s. Orr intensified that effort in 1986, and UNUM eventually bailed out of several of its core businesses, including life insurance, general investment contracts, and individual annuities and pensions. Most important, Orr and fellow executives decided to eliminate the company's involvement in the medical insurance business. Orr poured the resources saved from that business segment into sales and marketing programs for its remaining products.

From 1982 to 1990, Unum abandoned many insurance products, including medical insurance, individual life insurance, general investment contracts, and individual annuities and pensions. Under the leadership of then-CEO James Orr, the company turned its focus to long-term group disability insurance.

The Disability Bet

Why disability insurance? Orr's decision to concentrate on the long-term disability market was influenced in part by UNUM's established leadership position in the relatively small industry. In addition, the long-term disability market was growing quickly in comparison with most other types of insurance.

Between 1962 and 1986, in fact, the number of Americans prevented from working because of a disability more than doubled to 9.3 million, a rate of growth that outstripped population growth more than fourfold. Some industry observers noted that, although sales of disability policies were increasing at a rapid rate of about 15 percent annually, the potential U.S. market of 117 million (by one estimate) was only 36 percent saturated by the late 1980s.

Between 1985 and 1988 UNUM significantly bolstered its lead in the U.S. disability insurance market. By early 1989, UNUM's portfolio held a heady 30 percent of all U.S. group disability premiums.

The strategic logic was compelling: disability insurance required specialized actuarial expertise, deep claims management capabilities, and return-to-work programs that generalist insurers couldn't easily replicate. By concentrating resources in this niche, UNUM could build competitive moats that larger rivals would struggle to breach.

The investor insight: Orr's transformation established the playbook that defines Unum to this day: focus relentlessly on workplace benefits where you have distinctive capabilities, avoid commodity insurance products where scale alone determines winners, and build expertise in claims management and return-to-work that creates ongoing value for customers. The 1986 demutualization wasn't just a capital event—it was a strategic inflection point that positioned the company for three decades of dominance.

IV. Building the Disability Empire: The Acquisition Years (1990-1999)

Going Global

Armed with public capital and strategic clarity, UNUM embarked on an acquisition spree that would transform it from a regional specialist into a global disability insurance leader.

In March 1990, Unum acquired National Employers Life Assurance Holdings, which at the time was the United Kingdom's largest disability insurer. The UK acquisition accomplished two objectives: it gave UNUM a beachhead in Europe's largest market for income protection insurance, and it provided diversification away from American regulatory and economic cycles.

The company later acquired Duncanson & Holt, a reinsurer and insurance underwriter for the accident and health insurance sectors—adding expertise in risk management and reinsurance that complemented its core underwriting capabilities.

The Colonial Merger

In 1993, UNUM completed what would prove to be one of its most strategically important acquisitions: the Colonial Companies, parent of Colonial Life & Accident Insurance Company. Colonial's voluntary benefits platform—accident, cancer, and life insurance products sold through worksite marketing—gave UNUM a new distribution channel and product set that complemented its group disability franchise.

The Colonial acquisition reflected a crucial insight: employer-paid group benefits and employee-paid voluntary benefits were complementary, not competing. Employers increasingly wanted to offer workers a full menu of protection options, and Colonial's direct-to-employee distribution model captured demand that the group sales force couldn't reach.

Provident's Parallel Path

Meanwhile, in Chattanooga, Provident Companies was executing a similar strategic transformation. Although Provident's earnings in the early 1990s represented improvement over the late 1980s, the company was still struggling with underperforming operations. In November 1993, J. Harold Chandler, a senior executive with NationsBank Corporation, was brought on board as president and chief executive.

Chandler initiated a company-wide restructuring that included the 1995 sale of Provident's health-related business to Healthsource for $231 million—mirroring UNUM's exit from medical insurance years earlier. Both companies had independently concluded that health insurance was a commodity business where scale determined profitability, while disability remained a specialty product where expertise mattered.

Provident also increased its focus on individual disability and life policies with the 1997 acquisition of the Paul Revere Corporation, a Worcester, Massachusetts-based provider of individual disability insurance, from Textron for $1.2 billion. The purchase of Paul Revere made Provident the nation's largest provider of individual disability policies.

The Paul Revere deal was transformative. Paul Revere had pioneered "own-occupation" disability coverage for professionals—policies that paid benefits if a doctor, lawyer, or executive couldn't perform their specific job, even if they could work in another occupation. These "Cadillac" policies commanded premium prices and attracted high-income customers, but they also created substantial long-duration liabilities that would haunt the company for decades.

The Mega-Merger

By 1998, the industry logic was inescapable: UNUM dominated group disability, Provident dominated individual disability, and together they could create an unassailable position in America's workplace protection market.

Unum and Provident of Chattanooga, Tennessee announced their intention to merge in November 1998. When the merger was completed in 1999, the new company, named UnumProvident, was the United States' largest disability insurance provider. Then-Unum chairman and chief executive James Orr was retained as chairman and CEO of UnumProvident, which was headquartered in Portland, Maine.

The merger, which was completed on June 30, 1999, and which was valued at about $5 billion, involved Provident shareholders receiving 0.73 shares of the new entity's stock for each of their shares, while UNUM shareholders exchanged their shares on a one-for-one basis. Technically, Provident was the surviving entity and adopted the new name UnumProvident Corporation. Headquarters for the company remained in Chattanooga, but significant operations were kept in Portland, Maine.

Company Chief Operating Officer J. Harold Chandler, who had served as Provident's chief executive prior to the merger, succeeded Orr as UnumProvident CEO in November 1999.

What investors should understand: The 1990s consolidation wave created the company that exists today. UNUM had group disability expertise; Provident had individual disability and the Paul Revere book; Colonial had voluntary benefits and worksite distribution. Together, they formed a vertically integrated employee benefits platform that could serve the full spectrum of workplace protection needs. But the Paul Revere acquisition also brought substantial long-duration liabilities in individual disability policies that would become problematic when claims experience deviated from projections.

V. INFLECTION POINT #1: The Claims Denial Scandal & Regulatory Crisis (2002-2007)

The Scandal Unfolds

Every great turnaround story requires a crisis. Unum's came in spectacular fashion in the early 2000s, when evidence emerged that the company had systematically denied legitimate disability claims to boost short-term profits.

Unum received negative attention in 2002, when California regulators fined Unum, and alleged that the company inappropriately denied long-term disability insurance claims.

In the Unum class action lawsuit that's been called "The Unum/Provident Scandal," Unum (known then as Unum/Provident) was alleged to have denied or terminated thousands of legitimate disability claims starting in the 1990s and continuing until 2002. The Unum class action lawsuit came about after an investigation by the Department of Labor that put the long history of Unum claim denial under the microscope. The investigation also looked into Unum's subsidiary companies, which at the time were Unum Life Insurance Company, Paul Revere Life Insurance Company, and Provident Life and Accident Insurance Company.

The Department of Labor found the company was acting "unfair and unjust" by deliberately resorting to fraudulent tactics of claim denial as a cost control measure. The claims involved employee group disability policies.

The evidence was damning. The California Settlement Agreement particularly noted Unum's practice of "Targeting certain types of claims for 'resolution' (i.e., denial or termination of benefits) in the interest of improving 'net termination ratios.'" The paper trail documenting Unum's efforts to pressure claims adjusters to meet financial projections on the amount of claims that would be denied on a monthly and quarterly basis was clear. Indeed, in one particular e-mail from 2002, a Unum claim manager advised his team of adjusters, "We are projected to have 1,800,000.00 in recoveries this month but are coming up short at 1,772,000.00…Are there any other claims that are possible recoveries this week???"

In 2002, 60 Minutes reported that claims representatives who denied high-value claims often received cash incentives for their efforts. Today, those whiteboards are long gone, and the incentive structure is more subtle.

Internal emails, whistleblower testimony, and court filings painted a picture of a claims operation that had become a profit center rather than a service function. Evidence showed that the bonuses and performance of Unum's employees were based on several factors, including overall corporate success. The court stated that "encouraging claim handling employees to evaluate their performance based on their contribution to corporate stock price further supports the conclusion that [the Unum companies] were turning their claims handling operation into a profit center. This, despite the undisputed evidence, that it would be inappropriate to use the claims operation in such a manner."

The Multistate Settlement (2004)

The regulatory response was unprecedented in scale. The chief insurance regulators of Maine, Massachusetts, and Tennessee released their examination of the claim handling practices of three disability insurers owned by UnumProvident Corp., along with settlement agreements requiring the companies to change their claims practices and to re-assess certain claims going back as far as 1997. Forty-seven other states and the District of Columbia joined the three "lead states" in this multistate market conduct examination. The U.S. Department of Labor, which conducted a related investigation of UnumProvident's practices involving employee benefit plans covered by the Employee Retirement Income Security Act, was also a party to the settlement agreements.

"This action is one of the most significant multistate insurance regulatory actions in history, providing a uniform, verifiable and effective state-based settlement for the benefit of UnumProvident policyholders nationwide," said Maine Superintendent Iuppa.

Under court order, Unum was directed to reopen more than 200,000 denied claims, and to reevaluate the claims based on their merit. To ensure fair and just review and handling of all further policyholders' claims, Unum was charged with overhauling the methods by which they evaluate and process claims. Unum was also ordered to pay a fine of $15 million to several states.

The settlement cost it in excess of $120 million to comply, required it to reassess claims it has denied dating back to 1997, and called for an additional $15 million in fines.

The Regulatory Findings

The multistate examination identified specific claims handling practices that regulators found problematic:

"The examination team identified numerous instances in which the Companies relied heavily upon the analysis of their in-house medical professionals, and refrained from securing an IME. In many such instances, the Companies discounted or disputed the opinions of claimants' attending physicians, but chose not to invoke the requirement that the claimant attend an IME. Where there is conflicting medical evidence or conflicting medical opinions with respect to a claimant's eligibility for benefits, the Companies have the ability to invoke the policy provision and obtain an IME, and should do so."

The Multistate regulators identified a "significant number of instances" where Unum denied benefits for lack of "objective evidence" of disability in spite of the fact that its policies contained no such requirement.

California's Department of Insurance found that UnumProvident targeted claims for termination or denial based on company economics aimed at improving "net-termination ratios" instead of the claim's merits; selectively used portions of a claim file to the company's own advantage; misapplied policy provisions in order to limit or deny benefits; and failed to document claim files regarding in-person meetings at which substantive claims decisions were made.

Leadership Changes

Thomas Watjen replaced Orr as UnumProvident's chief executive later that year. The leadership transition marked a clear break from the scandal era. Watjen, who would lead the company for over a decade, focused on rebuilding trust with regulators, policyholders, and investors.

In 2002, UnumProvident relocated its headquarters from Portland, Maine to Chattanooga, Tennessee. The move consolidated operations and symbolically distanced the company from the Portland headquarters where the scandal-era practices had been developed.

In 2007, UnumProvident Corporation changed its name to Unum Group, with three primary divisions: Unum US, Unum UK and Colonial Life. The name change—ostensibly to simplify the corporate identity—also helped distance the company from the "UnumProvident" brand that had become synonymous with claims abuse.

The Long Tail of Reputational Damage

The scandal created lasting reputational damage that persists to this day. Plaintiff's attorneys continue to cite the 2004 settlement in litigation, and the company remains a frequent target of bad-faith claims lawsuits. A decade after the settlement, Unum had suffered trial losses of over $136 million, had to pay an additional $23 million in penalties to government regulators, and agreed to transform its claims handling practices. Based on the manner in which Unum continues to evaluate claims, critics argue that Unum has simply paid lip service to the promises it made.

The investor takeaway: The claims scandal represents both a cautionary tale and a turnaround opportunity. The company's short-term profit focus in the 1990s created massive long-term liabilities—legal, regulatory, and reputational—that took years to work through. But the scandal also forced fundamental reforms in claims handling, corporate governance, and risk management that arguably made the company stronger. Understanding this history is essential for assessing current management credibility and claims practices.

VI. INFLECTION POINT #2: The Long-Term Care Time Bomb (2009-Present)

The Legacy That Won't Die

If the claims scandal was an acute crisis, Unum's long-term care (LTC) insurance block represents a chronic condition—a slowly-building liability that has cast a shadow over the company's valuation for more than a decade.

UNM discontinued offering individual long-term care in 2009 and group long-term care in 2012. But unlike an operating business that can simply be shut down, insurance liabilities persist for decades. Policyholders who purchased LTC coverage years or decades ago continue to age, file claims, and draw benefits—often for far longer than original actuarial assumptions projected.

Premium rate increases, persistency, investment returns, mortality and other claims experience, and the level of administrative expenses adversely affected the profitability. In 2024, the Closed Block segment's adjusted operating income decreased 16.4% year over year, primarily due to unfavorable benefits experience in long-term care.

The Industry-Wide Problem

Unum is hardly alone in facing LTC challenges. The entire industry mispriced these products in the 1980s and 1990s, underestimating how long policyholders would live, how many would file claims, and how long those claims would last. The result has been an industry-wide reckoning.

Long term care insurance has been a millstone around the necks of many insurers as the assumptions about claim expenses, claim rates, lapse rates, and other factors on which liability reserves were based have often proven too optimistic. The result has been a series of reserve charges from various insurers, most notoriously that of General Electric (GE), but also on the part of Unum.

GE's $6.2 billion after-tax charge in 2018 highlighted the scale of the problem. If a company the size of General Electric could be blindsided by LTC liabilities, smaller insurers were even more vulnerable.

The Reserve Question

Market skepticism about Unum's LTC reserves has persisted for years. Clearly, there is skepticism in the market that Unum's current long term care reserves are adequate to cover the underlying liabilities which will eventually arise. Andrew Kligerman, an analyst with Credit Suisse, has stated his belief that the company is underreserved by around $5.7 billion (on an after tax basis), a rather charitable perspective given his initial projection without including information provided by the company ran as high as $14.3 billion. In addition, Fitch believes that Unum, along with several other long term care insurers, are underreserved for future long term care liabilities.

In 2020, the Maine Bureau of Insurance examined Unum America's LTC reserves and reached a concerning conclusion. MBOI concluded that Unum America's long-term care statutory reserves were deficient by $2.1 billion as of December 31, 2018. As permitted by MBOI, Unum America will phase in the additional statutory reserves over seven years beginning with year-end 2020 and ending with year-end 2026. The 2020 phase-in amount was estimated to be between $200 million and $250 million.

The Fortitude Re Solution (2025)

After years of managing the LTC block through rate increases and operational improvements, Unum in 2025 executed a significant risk-transfer transaction that marked a strategic turning point.

Unum Group announced that its Unum Life Insurance Company of America subsidiary (Unum America) has agreed to cede to Fortitude Reinsurance Company Ltd. (Fortitude Re), on a coinsurance basis, individual LTC insurance policies representing 19% of Unum's total LTC block and a quota share of IDI policies reinsured from an affiliate representing 20% of Unum's total in-force IDI premium, effective January 1, 2025. At the closing of the transaction, Unum America will cede $3.4 billion of individual LTC reserves and approximately $120 million of IDI in-force premium to Fortitude Re.

Overall, the transaction is expected to generate an estimated $100 million capital benefit, comprised of a $200 million capital impact related to the reinsured LTC block and a $300 million capital benefit related to the reinsured IDI block.

The transaction closed on July 1, 2025. "With the close of this transaction, we have achieved a significant milestone in reducing the company's exposure to the legacy long-term care business," said Richard P. McKenney, president and chief executive officer.

"The transaction announced today with Fortitude Re is consistent with our strategy of growing a leading employee benefits business while reducing our exposure to the legacy long-term care business. Through this action we further improve our risk profile, decrease the footprint of the closed block, and shift focus towards our more capital efficient, higher-returning core businesses," said McKenney. "The transaction also validates our assumptions for the LTC block, and the actions we have taken over the last several years."

The Fortitude Re deal is significant for several reasons. First, it demonstrates that third-party capital is willing to take on Unum's LTC liabilities at prices that generate capital benefit for Unum—suggesting the market's most pessimistic reserve estimates may be overstated. Second, it provides a template for additional risk transfers that could further shrink the closed block. Third, it signals management's commitment to repositioning the company away from legacy liabilities and toward growth businesses.

What investors need to monitor: The LTC block remains Unum's largest tail risk. While the Fortitude Re transaction reduced exposure by 19%, approximately 81% of LTC reserves remain on Unum's balance sheet. Key variables to watch include: (1) pace of additional risk-transfer transactions, (2) approval rates for premium increases by state regulators, (3) claims experience trends (particularly cognitive impairment claims, which tend to have longer duration), and (4) investment returns on assets backing LTC reserves. The company has consistently maintained that its reserves are adequate, but outside analysts remain skeptical, and the uncertainty will likely persist for years.

VII. INFLECTION POINT #3: The McKenney Turnaround Era (2015-Present)

A New Leader for a New Phase

Unum Group's CEO is Rick McKenney, appointed in April 2015, with a tenure now exceeding 10 years. McKenney's ascension marked the transition from crisis management to growth and transformation.

He previously served as Executive Vice President and Chief Financial Officer from August 2009 until April 2015. Before joining Unum in July 2009, Mr. McKenney served as Executive Vice President and Chief Financial Officer of Sun Life Financial, Inc., an international financial services company, from February 2007 until July 2009. Mr. McKenney has significant executive management, financial, and insurance industry experience through his prior service as chief financial officer of their company and other publicly traded insurance companies.

Mr. McKenney began his career at General Electric Company, transitioning his roles from manufacturing to financial leadership. The GE pedigree matters: McKenney learned financial discipline and operational excellence at a company famous for both, and he brought those sensibilities to Unum during a period when the company needed to rebuild credibility with investors.

McKenney's tenure as CFO from 2009-2015 coincided with Unum's most challenging post-crisis years, as the company absorbed the impact of the financial crisis, implemented reforms mandated by the regulatory settlement, and began managing its LTC exposure more aggressively. By the time he became CEO, McKenney understood Unum's complexities intimately.

The Strategic Playbook

McKenney's strategy has focused on three pillars: growing the core employee benefits business, managing and shrinking the closed block, and returning capital to shareholders.

Core Business Growth: The company has systematically expanded its product capabilities through targeted acquisitions:

In 2015, Unum completed the U.K. acquisition of National Dental Plan, expanding Unum UK into the dental market. In 2016, Unum acquired Starmount Life, expanding Unum US (2017) and Colonial Life (2018) into the dental market.

In 2018, Unum acquired technology company LeaveLogic to enhance the leave management process for businesses and their employees.

Unum Group's most recent deal was a Merger/Acquisition with Beanstalk Benefits. The deal was made on 24-Jul-2025. Unum acquired Beanstalk Benefits, Inc., a benefits platform that gives employees the ability to choose and manage their own health, wealth, and well-being benefits.

These acquisitions reflect a coherent strategy: expand the product suite (dental, vision), enhance distribution capabilities (voluntary benefits platforms), invest in technology (leave management, benefits administration), and strengthen the value proposition for both employers and employees.

Digital Transformation: During recent earnings calls, executives highlighted the company's digital innovation efforts, including the HR Connect platform and the strategic acquisition of Beanstalk Benefits to enhance digital capabilities. The company has invested heavily in benefits administration technology, recognizing that employers increasingly expect integrated platforms rather than standalone insurance products.

International Expansion: In 2018, Unum acquired Pramerica Žycie TUiR SA, a leading financial protection provider in Poland, and rebranded as Unum Poland. The Polish operation provides geographic diversification and exposure to an emerging market with growing demand for supplemental insurance.

Financial Performance Under McKenney

The results have been strong. In 2024, Unum Group's revenue was $12.89 billion, an increase of 4.05% compared to the previous year's $12.39 billion. Earnings were $1.78 billion, an increase of 38.58%.

Positive business trends are expected to continue into 2025 with outlook for core operations premium growth of 4 percent to 7 percent and after-tax adjusted operating earnings per share growth of 8 percent to 12 percent.

Return on Equity stood at 20.9% in Q2 2025—a level that demonstrates the core business quality despite the drag from closed block liabilities. Despite the slightly higher benefit ratio in the second quarter, returns on the disability business line remain robust, as shown by its ROE in excess of 25%.

Shares in Unum last closed at $80.47 and the price had moved by +52.78% over the past 365 days. In terms of relative price strength the Unum share price has outperformed the S&P500 Index by +40.98% over the past year.

Capital Allocation

McKenney has emphasized returning capital to shareholders while maintaining financial flexibility. During Q2 2025, Unum repurchased 3.8 million shares at a cost of $303.3 million and paid dividends of $151.5 million, highlighting its focus on returning capital to shareholders. The company maintained a leverage ratio of 23.0% and holding company liquidity of $1,956 million, indicating a solid financial foundation. The weighted average risk-based capital ratio for Unum's traditional U.S. life insurance companies stood at approximately 485%, well above regulatory requirements.

The investor perspective: McKenney's tenure represents a successful transformation from crisis management to growth execution. The company has delivered consistent premium growth, maintained strong returns in core operations, and demonstrated disciplined capital allocation. The LTC overhang remains, but the Fortitude Re transaction suggests management is actively working to shrink this exposure. Key questions going forward include: Can premium growth accelerate? Will additional LTC risk transfers follow? And can digital investments drive market share gains in an increasingly competitive employee benefits landscape?

VIII. Business Model Deep Dive: How Disability Insurance Works

The Mechanics of Income Protection

Understanding Unum requires understanding how disability insurance actually functions—because the business model dynamics explain both the company's competitive advantages and its historical challenges.

The company offers group long-term and short-term disability, group life, and accidental death and dismemberment products; supplemental and voluntary products, such as voluntary benefits, individual disability, and dental and vision products; and accident, sickness, disability, life, and cancer and critical illness products. It also provides group pension, individual life and corporate-owned life insurance, reinsurance pools and management operations, and other miscellaneous products. The company sells its products to employers for the benefit of employees. It sells its products through field sales personnel, independent brokers, consultants, and independent contractor agent sales force and brokers.

Group Disability Insurance is the company's core product. Employers purchase coverage for their workforce; when an employee becomes unable to work due to illness or injury, the insurance pays a percentage of their salary (typically 60-70%) until they can return to work, reach a maximum benefit period, or become eligible for other benefits like Social Security Disability Insurance.

Short-term disability typically covers 13-26 weeks; long-term disability kicks in afterward and can extend for years—sometimes until retirement age for severe disabilities. The combination of short-term and long-term coverage creates a seamless income protection system that bridges the gap between sick days and permanent disability.

The Economics of Underwriting: Disability underwriting requires actuarial analysis of incidence rates (how often disabilities occur), claim duration (how long claimants stay disabled), recovery rates (how many return to work), and mortality (how many die while disabled). These variables differ dramatically by industry, occupation, age, and geography. A desk-bound professional has very different disability risk than a construction worker; a 30-year-old has different claim patterns than a 55-year-old.

This complexity creates barriers to entry. Underwriting disability effectively requires decades of claims data, sophisticated actuarial models, and deep understanding of how specific occupations and medical conditions affect work capacity. Generalist insurers can't easily replicate this expertise.

Claims Management as Competitive Advantage: Unlike life insurance (where claims are binary—death triggers payment), disability claims require ongoing management. Is the claimant truly disabled? From what occupation? Can they return to work in a modified capacity? What medical treatments might restore function? Effective claims management can dramatically reduce claim duration and cost.

Unum's scale allows investment in return-to-work programs, vocational rehabilitation, and clinical expertise that smaller competitors can't match. When the claims operation works as intended (unlike the scandal-era practices), it creates value for all stakeholders: claimants get support returning to productive lives, employers retain experienced workers, and the insurer reduces claim costs.

The ERISA Factor: The Employee Retirement Income Security Act shapes the competitive landscape for group benefits. ERISA establishes federal standards for employee benefit plans and preempts many state laws. This creates a more predictable regulatory environment for group insurance compared to individual products, which face state-by-state regulation.

ERISA provides policyholders with the right to appeal a denial of disability benefits, but insurance companies often use its complex rules and regulations to navigate the claims process. The ERISA framework has been criticized for providing too much deference to insurer claim decisions, but it also creates operational efficiency and legal predictability that benefits scale players like Unum.

The Segment Structure

Unum operates through four principal segments:

Unum US: The largest segment, comprising group disability, group life and AD&D, and supplemental/voluntary lines. The Unum US segment contributes a total revenue of approximately 60% of total company revenue.

Colonial Life: Voluntary benefits sold through worksite marketing—accident, cancer, critical illness, and life insurance. Colonial's direct-to-employee distribution model reaches workers who want coverage beyond what their employers provide.

Unum International: UK and Poland operations. The UK business primarily offers group income protection (their term for disability), while Poland provides individual and group life with accident and health riders.

Closed Block: Legacy products no longer actively marketed, including the troublesome long-term care book as well as individual disability and other runoff products.

IX. Porter's Five Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces: The Competitive Landscape

1. Threat of New Entrants: LOW-MODERATE

The disability insurance market presents substantial barriers to entry. Regulatory requirements demand significant capital (insurers must maintain risk-based capital ratios), actuarial expertise (underwriting disability requires decades of claims experience), and distribution relationships (broker networks take years to build).

Unum's legacy dates to its founding as Union Mutual in 1848, and it became a pioneer in offering disability insurance products. Its merger with Provident Insurance in 1999 solidified its position among the country's leading disability insurance companies. A new entrant would face the daunting task of competing against 175 years of accumulated expertise.

However, InsurTech companies are beginning to chip at certain segments, particularly in voluntary benefits and benefits administration technology. These digital-first competitors may not directly challenge core disability underwriting but could disrupt distribution and customer experience.

2. Bargaining Power of Buyers: MODERATE

Large employers have significant leverage in group policy negotiations—they can demand competitive pricing, customized coverage, and high service standards. Benefits consultants and brokers concentrate buying power, often representing multiple large clients and having sophisticated knowledge of market pricing.

Individual policyholders have limited power; they generally accept the coverage their employer offers. However, the growth of voluntary benefits gives employees more choice, potentially shifting some power toward workers.

3. Bargaining Power of Suppliers: LOW

Key suppliers to disability insurers are reinsurers and capital markets. Multiple sources of reinsurance capital are available, and the Fortitude Re transaction demonstrates that sophisticated third-party capital is willing to assume disability and LTC risk at reasonable prices. Investment management can be done in-house (as Unum does) or outsourced to numerous asset managers.

4. Threat of Substitutes: MODERATE

Government programs represent the primary substitute for private disability insurance. Social Security Disability Insurance (SSDI) provides income replacement for severely disabled workers, but coverage is limited, qualification is difficult, and benefits are modest relative to most workers' incomes.

Self-insurance by large employers is an option, but most companies prefer to transfer disability risk to insurers with specialized claims management capabilities. The complexity of managing long-term disability claims makes pure self-insurance impractical for most employers.

Notably, the market remains underpenetrated. According to Bureau of Labor Statistics data, two-thirds of American workers do not carry disability insurance policies. This coverage gap represents both a market opportunity and a structural limit on the substitute threat—workers without coverage have no substitute, good or bad.

5. Industry Rivalry: HIGH

American Financial Group, Reinsurance Group of America, Lincoln Financial Group, American International Group, and Aflac are some of the 35 competitors of Unum Group. Competition is intense among established players for large employer accounts, where pricing pressure is substantial.

MetLife is a leader in the development of new products and services. The Hartford is a leading provider of insurance, annuities, and employee benefits, offering a wide range of disability insurance products including individual disability insurance, group disability insurance, and long-term disability insurance. The Hartford has a strong distribution network and a large customer base.

However, Unum is the largest disability insurance provider in the United States. Unum remains the top provider in North America, serving millions of workers and their families via group and individual policies. Market leadership provides scale advantages in claims management, actuarial analysis, and technology investment.

Hamilton's 7 Powers Framework

1. Scale Economies: Unum benefits from significant scale advantages in claims management, actuarial analysis, and technology investment. The cost of maintaining sophisticated return-to-work programs, clinical expertise, and benefits administration platforms can be spread across millions of covered lives. Smaller competitors face higher per-policy costs for equivalent capabilities.

2. Network Effects: Limited direct network effects, though Unum's relationships with brokers and HR technology platforms create some distribution advantages. The more employers and brokers that use Unum's benefits administration tools, the more valuable those platforms become.

3. Counter-Positioning: Unum's focus on workplace benefits represents counter-positioning versus diversified insurers. Life/health insurance giants like MetLife and Prudential must balance disability against other priorities; Unum can concentrate resources and attention on its core franchise.

4. Switching Costs: Moderate switching costs for employers. Changing disability providers requires employee communication, benefits reenrollment, and potential claims transition complexities. However, these costs aren't prohibitive, and competitive pressure at renewal remains substantial.

5. Branding: Unum's brand is a double-edged sword. The company is well-known among benefits professionals and employers, but brand perception is complicated by the claims scandal legacy. The 2007 name change from UnumProvident was partly an attempt to refresh brand associations.

6. Cornered Resource: Unum possesses proprietary claims data spanning decades and millions of disability claims. This actuarial dataset represents a genuine cornered resource—competitors cannot replicate historical claims experience, and Unum's underwriting and pricing models benefit from this information advantage.

7. Process Power: Unum's claims management processes—developed over 175 years and refined through both positive innovation and scandal-driven reform—represent substantial process power. The company's return-to-work programs, vocational rehabilitation capabilities, and clinical expertise are difficult to replicate.

Competitive Position Summary

Unum's competitive position rests primarily on scale economies, cornered actuarial resources, and process power in claims management. The company's market leadership provides durable advantages, though intense rivalry among established competitors prevents monopoly pricing power. The closed block overhang distinguishes Unum from cleaner competitors like Aflac, creating both risk and potential opportunity as the company executes risk-transfer transactions.

X. Bull and Bear Cases

The Bull Case: Core Franchise Compounding

Premium Growth Momentum: Unum's financial highlights for Q2 2025 show premium income of $2,748.0 million, representing a 4.6% increase from $2,627.2 million in the same quarter of 2024. Core operations continue to grow through a combination of new sales, renewals, and natural growth from wage inflation and employment gains at existing clients.

Return on Equity Excellence: Despite slightly higher benefit ratios, returns on the disability business line remain robust, with ROE in excess of 25%. The core franchise generates attractive returns even in a competitive market—a testament to market position and operational execution.

LTC Risk Transfer Playbook: The Fortitude Re transaction demonstrates that third-party capital will absorb LTC risk at prices that benefit Unum shareholders. "The transaction also validates our assumptions for the LTC block." Additional risk transfers could systematically shrink the closed block, releasing capital and reducing tail risk.

Digital Transformation Optionality: Investments in HR Connect, Beanstalk Benefits, and benefits administration technology position Unum for a more integrated role in employer HR ecosystems. If these investments generate market share gains, premium growth could accelerate beyond current expectations.

Shareholder Returns: During Q2 2025, Unum repurchased 3.8 million shares at a cost of $303.3 million and paid dividends of $151.5 million. Consistent capital return at attractive valuations (P/E around 8-9x) represents material shareholder value creation.

The Bear Case: Legacy Risks and Competitive Threats

LTC Reserve Uncertainty: Despite management's confidence, analysts have expressed beliefs that the company is underreserved by billions on an after-tax basis. Fitch believes that Unum, along with several other long term care insurers, are underreserved for future long term care liabilities. If actual claims experience proves worse than reserves assume, substantial charges could materialize.

Competitive Pressure: The employee benefits market is increasingly competitive, with aggressive pricing from established rivals and technology-enabled disruption from InsurTech entrants. Sales in the first half of 2025 have started slower than annual growth expectations and are lower year-over-year. The back half of the year is critical, with the fourth quarter accounting for more than half of annual group sales.

Interest Rate Sensitivity: Insurance company investment portfolios benefit from higher rates (better yields on fixed income), but rate sensitivity works both ways. Significant rate declines could pressure investment income and require reserve strengthening.

Reputational Overhang: The claims scandal legacy persists in public perception and plaintiff's bar narratives. While current claims practices appear reformed, the company remains a frequent target for bad-faith litigation, creating ongoing legal costs and reputational risk.

Regulatory Risk: State insurance regulation creates ongoing uncertainty around premium rate increases (particularly for LTC), reserve requirements, and market conduct expectations. Adverse regulatory developments could constrain profitability or capital flexibility.

XI. Key Performance Indicators for Investors

For long-term fundamental investors monitoring Unum, three KPIs stand out as most important:

1. Core Operations Premium Growth Rate

Why it matters: Premium growth is the top-line driver of the core business franchise. Unlike the closed block (which will decline over time), core operations should grow through new sales, renewals, and natural growth. Consistent premium growth in the 3-6% range demonstrates competitive positioning and market health.

What to watch: Quarterly premium income for Unum US, Colonial Life, and Unum International segments. Compare year-over-year growth rates to management guidance and peer performance. Watch for signs of pricing pressure (discounting to win business) or competitive share loss.

2. Group Disability Benefit Ratio

Why it matters: The benefit ratio (claims paid as a percentage of premiums) directly measures underwriting profitability in the largest product line. A stable or improving benefit ratio indicates good risk selection, effective claims management, and appropriate pricing. Rising benefit ratios suggest claims experience deterioration or competitive pricing pressure.

What to watch: Quarterly group disability benefit ratio reported in earnings. Group disability adjusted operating earnings in Q2 2025 reflected a benefit ratio of 62.2% compared to 59.1% in the year-ago period. Management guidance targets "low 60s" for full-year 2025. Sustained benefit ratio above 65% would signal concern.

3. Closed Block Adjusted Operating Income

Why it matters: The closed block (primarily LTC) represents Unum's primary tail risk. While this segment will decline over time, quarter-to-quarter volatility reflects claims experience, reserve adjustments, and investment performance. Large negative swings indicate LTC problems; stable-to-positive results suggest reserves are adequate.

What to watch: Quarterly closed block adjusted operating income and commentary on LTC claims experience. Track progress on risk-transfer transactions (like Fortitude Re) that reduce closed block exposure. Watch for reserve charges or adverse assumption changes that could signal emerging problems.

XII. The Myth vs. Reality Box

| Myth | Reality |

|---|---|

| "Unum is just a disability insurer" | Unum offers a comprehensive suite of employee benefits including disability, life, accident, critical illness, dental, vision, and leave management. Colonial Life provides voluntary products; Unum UK and Poland extend the franchise internationally. |

| "The claims scandal means Unum still denies legitimate claims" | While the 2004 settlement required substantial claims practice reforms, and plaintiff attorneys continue to pursue cases, current claims operations have been restructured with regulatory oversight. Management emphasizes "continued discipline in pricing and risk selection" rather than claims denial as a profitability lever. |

| "LTC will bankrupt the company" | While LTC represents meaningful tail risk, the Fortitude Re transaction suggests third-party capital values the block at prices that benefit Unum. The company maintains substantial capital buffers (485% RBC ratio) and has multiple levers including rate increases, reserve releases, and additional risk transfers. |

| "Disability insurance is a commodity" | Unlike many insurance products, disability requires specialized actuarial expertise, sophisticated claims management, and return-to-work programs. Scale players like Unum have significant competitive advantages over generalist insurers. |

XIII. Conclusion: The Long Game

Unum Group's 175-year journey—from a Boston parlor to a Fortune 500 disability giant—illustrates both the power of strategic focus and the long tail of past mistakes. The company that emerged from the 2004 scandal and the LTC crisis is leaner, more focused, and better positioned than the sprawling UnumProvident of two decades ago.

Unum Group is a leading international provider of workplace benefits and services, helping workers and their families thrive for more than 175 years. Through its Unum and Colonial Life brands, the company offers disability, life, accident, critical illness, dental, and vision insurance; leave and absence management support; and behavioral health services.

Under Rick McKenney's decade-long leadership, Unum has demonstrated that a 175-year-old insurance company can adapt to changing markets, invest in technology, and deliver competitive returns while managing substantial legacy liabilities. As McKenney stated: "We have the capabilities and capital to deliver for our customers, expand our reach, and create increasing value for our shareholders."

The LTC overhang will persist for years, requiring ongoing management attention and creating valuation uncertainty. But the core employee benefits franchise—built over decades through acquisition, innovation, and operational excellence—generates attractive returns and steady growth. For patient investors comfortable with legacy insurance complexity, Unum offers a case study in turnaround execution and the enduring value of market leadership in specialized products.

The company that survived a Civil War, a Depression, a scandal, and a liability crisis is unlikely to succumb to today's challenges. The question is whether it can translate survival into value creation—and on that measure, the McKenney era evidence is encouraging.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube