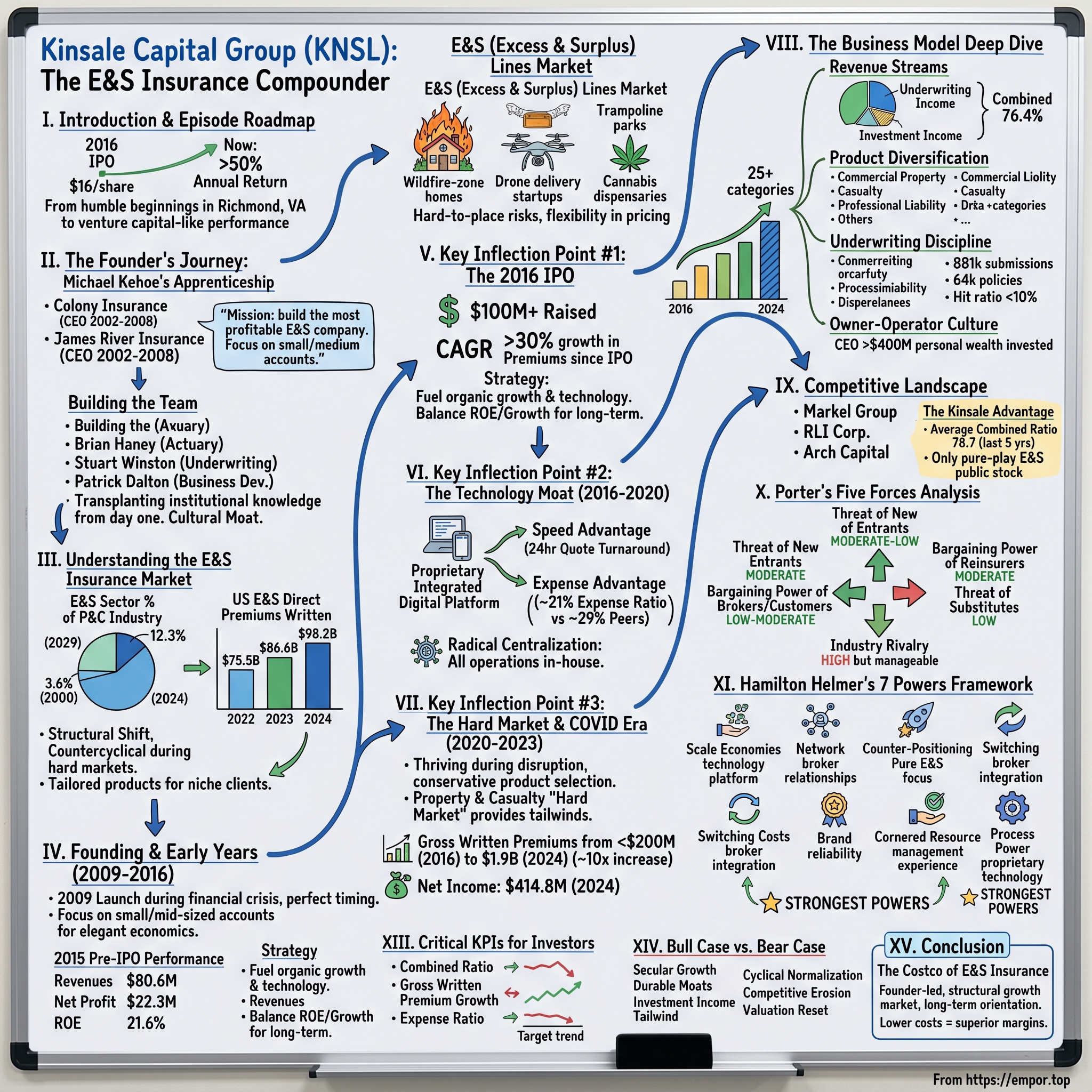

Kinsale Capital Group: The E&S Insurance Compounder

I. Introduction & Episode Roadmap

Picture this: It's July 28, 2016. A specialty insurance company from Richmond, Virginia—one that most investors have never heard of—makes its debut on the New York Stock Exchange at $16 per share. The IPO raises just over $100 million. In a year when Renaissance Capital declared it the worst for IPOs since 2003, this quietly confident insurer named Kinsale Capital Group stands out, delivering a 14.7% first-day return.

Fast forward to today. Since its IPO, Kinsale has returned more than 50% annually, or enough to turn $10,000 into $263,690 during the past eight years. That's not a typo. In an industry known for generating reliable but modest returns, Kinsale has delivered venture capital-like performance from an insurance company.

How did a company founded in 2009—during the wreckage of the financial crisis—become one of the most remarkable wealth-creation stories in American insurance history? That's the question that draws us into the Kinsale story.

Founded in 2009, Kinsale Capital Group is an established and expanding specialty insurance company focused on the excess and surplus lines market in the U.S. But that clinical description barely scratches the surface. What makes Kinsale extraordinary isn't just what they do—it's how they do it.

The company operates in a corner of the insurance world that most people don't know exists: the excess and surplus (E&S) lines market. It underwrites policies outside of traditional insurance, like automotive and homeowners insurance, and instead focuses on hard-to-place risks that regular insurers decline to cover. Think wildfire-zone homes, drone delivery startups, trampoline parks, and cannabis dispensaries—risks that make traditional insurers run for the exits.

The investment thesis for Kinsale rests on a deceptively simple question: Can a specialty insurance company with industry-leading profitability, technology-driven cost advantages, and a founder-led culture continue compounding at exceptional rates? In the E&S market, Kinsale Capital is the only publicly traded pure-play. That exclusivity matters.

In this deep dive, we'll trace Michael Kehoe's remarkable journey from insurance apprentice to company founder, unpack the E&S market opportunity that powers Kinsale's growth, examine the technology moat that competitors struggle to replicate, and ultimately address the central investment question: Is this the "Berkshire Hathaway of specialty insurance" or a cyclical player riding a favorable wave?

II. The Founder's Journey: Michael Kehoe's Insurance Apprenticeship

The Colony and James River Years

The origin story of exceptional companies often traces back to founders who served an apprenticeship, learning the craft before striking out on their own. For Michael Kehoe, that education came through two distinct but connected chapters: Colony Insurance Company and James River Insurance.

Michael Kehoe has served as our Chief Executive Officer since June 2009, when he founded Kinsale, and Chairman of the Board since 2024. Mike's previous roles include President and Chief Executive Officer at James River Insurance Company and various senior positions at Colony Insurance Company, finishing as Vice President of Brokerage Underwriting.

What's remarkable about this background is its specificity. Kehoe didn't just work in insurance—he worked in the precise segment of insurance that he would later transform. Colony Insurance, based in Richmond, Virginia, was a specialty E&S carrier where Kehoe rose through the underwriting ranks. This wasn't corporate ladder climbing; it was education by immersion.

The James River chapter proved even more formative. "Like most companies, our overall mission is to deliver consistently high returns on equity to our investor shareholders by building the most profitable E&S company in the business," Kehoe said in a 2005 interview. "Operationally, we want to provide fast, efficient, creative solutions to small to medium account business that requires a true underwriter's touch, often in tough and higher hazard classes of business."

Read those words again. They could have been spoken yesterday about Kinsale. Two decades before Kinsale became a $10 billion market cap company, Kehoe had already articulated the exact strategy he would deploy.

In 2002, a group of experienced insurance executives with a history of starting and operating profitable specialty insurance operations created James River Group, Inc. James River Group was listed on the NASDAQ Stock Market in 2005 and consistently produced attractive underwriting results.

Kehoe served as President and CEO of James River Insurance from its founding as a development stage company in November 2002 until March 2008. The critical insight here: Kehoe learned to build E&S insurers from scratch twice before founding Kinsale. When he launched Kinsale in 2009, he wasn't experimenting. He was executing a refined playbook.

Mr. Kehoe earned a B.A. in Economics from Hampden-Sydney College and a J.D. from the University of Richmond School of Law. The legal training matters more than it might appear. E&S insurance involves complex coverage language, exclusions, and policy structures that require precise drafting. Having a CEO who can parse legal language at expert level isn't decorative—it's foundational.

Building the Team

The difference between a good company and a great one often lies in the quality of the founding team. Kehoe didn't build Kinsale alone—he reassembled his band.

Brian Haney served as Kinsale's Chief Actuary from 2009 to 2015. Prior to joining the Company, Mr. Haney was the Chief Actuary of James River Insurance Company from 2002 to 2009, where he was responsible for the actuarial functions, as well as catastrophe modeling and ceded reinsurance.

This is the actuarial equivalent of the band getting back together. Haney knew how Kehoe thought about risk, understood his philosophy on reserving, and had already proven they could build profitable books together. "Brian has been a tremendous influence on the Company's success since its founding back in 2009 through the variety of senior executive roles that he has held along the way."

Stuart Winston joined the Company in 2010 and has over 20 years of industry underwriting experience. During his tenure at the Company, Mr. Winston has served in positions of increasing responsibility in the leadership team. Winston, too, came from James River Insurance, bringing underwriting expertise shaped by the same disciplined culture.

Patrick Dalton has served as our Senior Vice President and Chief Business Development Officer since 2024, leading business development and marketing. Pat joined Kinsale in 2010 and has managed both Kinsale's professional lines underwriting and casualty underwriting. Prior to joining Kinsale, he held various underwriting positions at James River Insurance Company and USLI.

See the pattern? Kinsale wasn't just recruiting talent—it was transplanting institutional knowledge from day one. When you start a company with people who already share mental models, vocabulary, and expectations, you skip years of organizational friction.

The average manager has over 30 years of relevant experience. What's also positive is that Michael Kehoe and Brian Haney worked together for over 20 years (since 2002). As you can see, many employees of Kinsale worked together for decades at other E&S insurance companies.

This cohesion creates what investment analysts sometimes call "cultural moat"—the intangible competitive advantage that comes from a team that's been winning together for so long that success becomes habitual. Culture, as they say, eats strategy for breakfast. At Kinsale, culture and strategy are the same meal.

For investors, the founder's journey reveals something essential: Kinsale wasn't a leap of faith. It was an iteration on proven concepts, executed by people who had already demonstrated they could succeed together. The risk profile of the founding was dramatically lower than the typical startup—even if no one realized it at the time.

III. Understanding the E&S Insurance Market

What is E&S Insurance?

Before we can appreciate Kinsale's competitive advantages, we need to understand the unusual market it operates in. Most investors' mental model of insurance involves familiar categories: auto insurance, homeowners insurance, life insurance. The excess and surplus lines market exists in the shadows of this mainstream landscape.

Kinsale is a unique insurance company because it covers an area of the market called excess and surplus (E&S) insurance. It underwrites policies outside of traditional insurance, like automotive and homeowners insurance, and instead focuses on hard-to-place risks that regular insurers decline to cover. Its coverage includes small business casualty, construction, professional liability, and product recalls, to name a few.

Here's how it works: Standard insurance companies—the "admitted" carriers you've heard of—operate under state regulatory frameworks that constrain what they can charge and what policy forms they can use. When a risk is too unusual, too volatile, or too hard to price, these standard insurers decline to write coverage. That's when the E&S market steps in.

What makes the E&S market appealing is that these companies don't face the same stringent regulations like traditional insurers. For example, regulations specify what standard insurers must cover and how much they can charge. These rigorous restrictions can make it harder for an insurer to squeeze out attractive margins. On the other hand, Kinsale has more flexibility about what risks it is willing to cover and how much it will charge.

This flexibility is both the opportunity and the challenge. E&S insurers have freedom of rate and form—they can design custom policies and charge risk-appropriate premiums. But they also bear the responsibility of getting the pricing right. There's no regulatory safety net requiring neighbors to subsidize your risk.

Why E&S Matters

The E&S market's value proposition becomes clearer when you consider the alternative: no coverage at all. A trampoline park, a drone delivery company, or a cannabis dispensary needs liability insurance to operate. If no standard insurer will write the policy, the business faces an existential threat. E&S carriers like Kinsale step into this void.

The insurance industry is cyclical and goes through periods of growth or contraction. When many insurers compete on price and coverage, this is known as a "soft" market. During times like this, insurers' margins face pressure because of the increased competition. However, when insurers face higher claims due to increased catastrophes or higher regulations, it creates conditions for a hard market where insurers are more selective about what they will cover.

A "hard market" is E&S territory. When standard carriers retreat from certain risk categories—whether due to rising wildfire losses in California, nuclear verdicts in liability cases, or pandemic-era uncertainties—the E&S market expands to fill the gap. This countercyclical dynamic is one of Kinsale's structural advantages.

Kinsale focuses on smaller insurable risks, a segment with far less competition. While larger industry players compete intensely for high-value deals, driving margins lower, Kinsale capitalizes on overlooked smaller opportunities that offer higher profitability. A key differentiator is Kinsale's ability to create bespoke insurance products tailored to the specific needs of niche clients, setting it apart from competitors that predominantly offer generalized solutions. This advantage is amplified by the less sophisticated competition in this segment.

Market Growth Dynamics

The numbers tell a compelling story about E&S market expansion.

For full-year 2024, the U.S. E&S direct premiums written reached nearly $100 billion—coming in at $98.2 billion across all lines, up from $86.6 billion in 2023 and $75.5 billion in 2022.

2024 marked the 7th straight year of double-digit growth for the U.S. excess and surplus lines market. "The 2018 to 2024 period of double-digit growth in the surplus lines market has yielded conditions that attracted new capital to the market and incentivized established surplus lines companies to pursue additional avenues to grow their books of business."

An industry executive recalled that "Fifteen years ago, the E&S sector was just 10% of the industry. Right now, it's about 20% to 25%." According to AM Best's Annual Surplus Lines Report, in 2000 the E&S sector accounted for just 3.6% of total property/casualty premium; today that market share stands at 12.3% in 2024.

Think about that trajectory. The E&S market has more than tripled its share of total P&C premiums in 24 years. This isn't a cyclical blip—it's a structural shift driven by increasing complexity in the risk landscape.

After years of breakneck acceleration, the excess and surplus (E&S) insurance market shows signs of a new era: sustainable, stable, and still highly relevant. As reported in a recent Insurance Insider US article, the E&S market reached $135 billion in insurance premium growth in 2024—a 12.5% increase over 2023. That's a notable climb, but it also marks a slight deceleration from the previous year's 14.4% growth. Compare that to the massive 32.3% jump in 2021, and a clear pattern emerges: the E&S insurance market is settling into a more measured rhythm.

For investors, this market context matters. Kinsale isn't merely executing well within a static market—it's riding a secular growth wave. The question is whether this wave represents durable tailwinds or temporary conditions that will eventually normalize.

IV. Founding & Early Years (2009-2016)

The 2009 Launch

The timing of Kinsale's founding looks almost too perfect in hindsight. June 2009: the U.S. economy was crawling out of the worst financial crisis since the Great Depression. Credit markets had seized, insurers had taken massive losses on investments, and the survivors were licking their wounds.

Kinsale Capital Group was established in 2009. Michael P. Kehoe is identified as a founder and the current CEO. The company went public on July 28, 2016, with an IPO price of $16.00 per share.

Kinsale's journey began in the aftermath of the 2008 financial crisis, perhaps by luck or maybe by strategic design, in a more constrained market environment. During a deep recession, when the competition has battened-down its hatches, it becomes far easier for new entrants to gain traction and win business.

This wasn't Kehoe's first time launching into chaos. James River Insurance was founded in the aftermath of the September 11 attacks and the corporate scandals of 2001-2002, when insurance markets were hardening dramatically. Kehoe understood that crisis conditions often create the best entry points for disciplined new entrants.

The company established headquarters in Richmond, Virginia—the same city where Kehoe had built his career at Colony Insurance and James River. Richmond might seem like an unusual insurance hub compared to Hartford or New York, but the choice was strategic. Lower operating costs, a stable workforce, and proximity to the regulatory environment of the mid-Atlantic all factored into the decision.

The Strategic Vision

From day one, Kinsale's strategy was defined by what it wouldn't do as much as what it would.

Kinsale Capital Group is a U.S.-based specialty insurer focusing on the Excess and Surplus (E&S) lines market, targeting small to mid-sized businesses with hard-to-place risks. Founded in 2009 by Michael Kehoe, Kinsale has grown steadily, leveraging its underwriting expertise to carve out a niche in a high-growth segment of the insurance industry. The company operates as an owner-operator stock, with its headquarters in Richmond, Virginia.

The focus on small and mid-sized accounts was particularly deliberate. While larger competitors chased headline-grabbing accounts with millions in premium, Kinsale built its book one modest policy at a time. The strategy had elegant economics: smaller accounts meant less concentrated risk, more pricing power, and less competitive intensity.

"Second, we focus on small to medium-sized accounts, typically in the $10,000 to $100,000 premium range. Third, and somewhat atypical in the E&S market, we get called on for solutions at the last minute in a placement search, and we're able to deliver fast. We are striving to build a culture where smart underwriters work with brokers to find solutions for business the standard markets cannot do or cannot do well."

These words from Kehoe's James River days became the blueprint for Kinsale. Fast quotes, specialized solutions, smaller accounts. It sounds unglamorous—and that's precisely the point.

Building the Foundation

The pre-IPO years saw steady, disciplined growth as Kinsale proved its model worked.

In 2015, KNSL increased its revenues to $80.596 million from its 2014 revenue of $63.676 million. Net profit increased from $12.97 million to $22.27 million, and gross written premiums increased from $158.58 million to $177.00 million. Return on equity increased from 14.01% in 2014 to a healthy 21.62% in 2015.

Those early returns matter because they demonstrate that Kinsale's exceptional performance isn't a recent phenomenon or a side effect of hard market conditions. The company was generating above-industry returns from the beginning, validating its strategic positioning and operational execution before public market scrutiny.

By 2016, Kinsale had established proof of concept across multiple dimensions: profitable underwriting, geographic expansion to all 50 states, and technology infrastructure that would become a defining competitive advantage. The foundation was set for the next phase.

V. Key Inflection Point #1: The 2016 IPO

Going Public

The decision to go public often marks a turning point in a company's trajectory—for better or worse. For Kinsale, the 2016 IPO proved to be an accelerant.

At the time of its IPO in July 2016, KNSL was priced at $16—the high end of its expected range of $14 to $16. On its first day of trading, the stock opened at $18.30. In sum, Kinsale delivered a first day return of 14.7%.

According to Renaissance Capital, 2016 may go down in history as the worst year for IPOs since 2003. Against that backdrop, Kinsale's successful debut was notable. Investors were hungry for quality, and Kinsale's track record of profitable growth stood out in a sea of unprofitable startups.

The IPO raised approximately $105.6 million, providing essential capital for expansion initiatives while significantly enhancing Kinsale's public profile and market visibility. For a specialty insurer, credibility matters: brokers, reinsurers, and regulators all pay attention to a company's capitalization and financial strength ratings.

The Capital Deployment Strategy

What Kinsale did with its IPO capital reveals management's priorities.

Kehoe's decision to raise capital through stock issuances (e.g., $76M in 2016, $142M in 2022) has fueled Kinsale's growth, with gross written premiums growing at a CAGR of over 30% since its IPO. This capital has supported expansion into new E&S segments and technology investments, maintaining a low expense ratio (around 20.7% in 2024).

The pattern here is instructive. Kinsale didn't use its capital to acquire competitors or diversify into adjacent businesses. It plowed resources into organic growth and technology—the two areas where disciplined execution compounds over time.

His preference for balancing a 15% ROE with 15% growth over a higher ROE with slower growth (as noted in the 2024 meeting) reflects a long-term perspective, aligning with Kinsale's 8x book value growth since 2014.

This trade-off illuminates Kehoe's philosophy. Many insurers chase higher near-term ROE by constraining growth or taking outsized risks. Kehoe explicitly chose the compounding path: moderate but sustainable returns, reinvested to build durable competitive advantages.

Technology Investment Inflection

The IPO also marked an inflection point in Kinsale's technology investments. With public market capital and increased scale, the company accelerated its build-out of proprietary systems.

The goal was to create an integrated digital platform that could handle the complexity of E&S underwriting while maintaining industry-leading efficiency. Most specialty insurers rely on patchwork systems—legacy platforms acquired through M&A, third-party software, and manual processes. Kinsale built its stack from scratch, optimized for its specific business model.

Kinsale stood out from the IPO crowd in 2016. In a weak IPO climate, Kinsale delivered a first day return of 14.7% and 78.9% in the after-market. While being slightly more expensive than peers at present, KNSL faces a favorable macro climate. ROE has shown healthy growth.

The market was already recognizing what would become apparent: Kinsale warranted a premium valuation relative to traditional insurance peers. That premium has only grown as the technology advantage became more pronounced.

VI. Key Inflection Point #2: The Technology Moat (2016-2020)

The Proprietary Platform

Insurance has historically been a technology laggard. Walk into most insurance company offices and you'll find green-screen terminals, paper files, and processes that haven't fundamentally changed since the 1990s. Kinsale chose a different path.

The combination of deep underwriting expertise in a specialized market, coupled with a technology-driven, low-cost operating model, creates a strong competitive moat for Kinsale. The company's management has explicitly stated that its operating model is designed to create a cost advantage, a specialization advantage, and a technology advantage. This is not merely a collection of good business practices but an integrated and intentional design. By controlling its underwriting and claims processes in-house, and by aggressively using technology to manage expenses and select risks, Kinsale has built an operational structure that is difficult for competitors to replicate.

Over the years, Kinsale Capital has built a proprietary technology platform that reflects the best practices of its management team and has learned from its extensive prior experience. Kinsale operates on an integrated digital platform with a data warehouse that collects statistical data. The platform provides high efficiency, accuracy, and speed across all processes. Management believes its technology platform will provide them with an enduring competitive advantage. It allows them to respond to market opportunities quickly and will continue to scale as the business grows.

The platform enables something competitors struggle to match: 24-hour quote turnaround. When a broker submits a risk that their standard markets have declined, speed matters. The policy might be expiring in days. The business owner is anxious. The broker wants an answer. Kinsale's systems allow underwriters to evaluate complex submissions and return quotes faster than the industry norm.

The Expense Advantage

The technology investment translates directly to bottom-line advantage through the expense ratio—the percentage of premiums consumed by operating costs.

This digital platform provides the company with a significant competitive edge, enabling more informed underwriting decisions and contributing to an approximately 8-point expense ratio advantage over peers. This technological superiority translates into an estimated 5-point benefit in Return on Equity (ROE).

Kinsale's advanced technology platform and strict expense discipline yield an industry-low expense ratio (approximately 20.7%). This positions the company to preserve and expand net margins as automation and data analytics further scale underwriting, quoting, and policy servicing over time.

An 8-point expense ratio advantage sounds abstract, so let's make it concrete. If Kinsale writes $100 in premium, it spends about $21 on operating expenses. A typical competitor spends $29. That $8 difference falls directly to underwriting income—every year, on every dollar of premium. As the premium base grows, the absolute advantage compounds.

The company maintains one of the lowest expense ratios in the industry, which provides a significant competitive advantage. According to industry data, Kinsale's expense ratio has consistently been 10-15 percentage points lower than the industry average, allowing the company to offer competitive pricing while maintaining strong underwriting profitability.

Centralized Operations

The technology platform enables another strategic choice that differentiates Kinsale: radical centralization.

By controlling its underwriting and claims processes in-house, and by aggressively using technology to manage expenses and select risks, Kinsale has built an operational structure that is difficult for competitors to replicate.

Most other insurers outsource one or both functions, leading to higher costs, slower processes, and misaligned incentives. Kinsale's integrated approach allows it to issue quotes quickly and operate with exceptional cost efficiency.

All underwriting and claims handling for all 50 states is done in-house, centrally, at headquarters. No delegated underwriting authority to MGAs. No outsourced claims adjusting. This approach creates consistency, allows rapid knowledge sharing, and prevents the quality drift that often accompanies distributed operations.

Thanks to the team's deep expertise and knowledge, they are able to successfully balance their broad risk appetite by maintaining a diversified book of smaller accounts with strong pricing and well-defined coverages. Unlike many of their competitors, they do not extend their underwriting authority to third parties, which further demonstrates the company's dedication to the quality of their underwriting team.

For investors, the technology moat represents a sustainable competitive advantage that grows stronger over time. Each year of data collection improves Kinsale's underwriting models. Each iteration of the platform increases efficiency. And the cost of replicating what Kinsale has built—both in dollars and time—creates a meaningful barrier to entry.

VII. Key Inflection Point #3: The Hard Market & COVID Era (2020-2023)

Thriving During Disruption

When COVID-19 disrupted global business in early 2020, the insurance industry faced unprecedented uncertainty. Would claims explode? Would businesses cancel policies? Would the investments that insurers rely on for returns collapse?

Kinsale's response demonstrated the strength of its model.

Gross written premium was up 41% for the quarter, notwithstanding the disruption of the COVID virus. The company posted an 83.8% combined ratio and a 16.9% annualized operating return on equity for the six months ending June 30, 2020.

Given what we know at this point, we do not believe the coronavirus will have a material impact on Kinsale's profitability or growth. Specifically, Kinsale does not write any of the following lines of business that may have a heightened exposure to virus-related losses.

Kehoe's conservative approach to product selection—avoiding lines like event cancellation, workers' compensation, and trade credit that were heavily impacted by the pandemic—paid dividends. While competitors scrambled to assess their exposure, Kinsale continued writing business.

At the end of the first quarter 2020, we noted that we did not expect the COVID-19 virus to have a material impact on Kinsale's profitability or growth. Three months later, we have the exact same position. The temporary drop-off in March and the growth of new business submissions reversed within a couple of weeks, and we have experienced a V-shaped recovery in submission activity and premium.

Hard Market Tailwinds

Beyond the pandemic, 2020-2023 represented a period of exceptional opportunity for disciplined E&S insurers. The property & casualty industry experienced what's called a "hard market"—a period when insurers can be selective about coverage and charge higher premiums.

The combination of disciplined and highly controlled underwriting, combined with technology-driven low costs and a focus on the E&S market is propelling our profitability and growth, and we believe will continue to do so over the long term. Kinsale's growth rate at the moment is being enhanced by continued dislocation within the P&C market. Some competitors are reacting to substandard results by restructuring books of business, canceling programs and withdrawing capacity.

Multiple factors converged to harden the market: increasing natural catastrophe losses from wildfires and hurricanes, rising litigation costs from "social inflation" (larger jury verdicts), and persistent economic inflation increasing loss costs. Standard insurers, burned by inadequate pricing, withdrew from riskier segments—pushing business toward E&S carriers.

As more aggressive competitors have had to reduce their risk, they've found themselves unable to provide certain coverage. This ultimately works to Kinsale's benefit, as it has stepped up to fill the gap, helping grow its share of the specialty insurance market while increasing premiums, which is driving bottom-line growth. Property and casualty insurers have faced challenges resulting from what's called a hardening of the market.

Premium Growth Acceleration

The combination of favorable market conditions and Kinsale's competitive advantages produced remarkable growth.

Gross written premiums were $443.3 million for the fourth quarter of 2024 compared to $395.2 million for the fourth quarter of 2023, an increase of 12.2%. Gross written premiums were $1.9 billion for the year ended December 31, 2024 compared to $1.6 billion for the year ended December 31, 2023, an increase of 19.2%.

To put this in perspective, Kinsale's gross written premiums grew from under $200 million at its 2016 IPO to $1.9 billion in 2024—nearly a 10x increase in eight years. This wasn't acquisition-driven roll-up; it was organic growth powered by underwriting excellence and market share gains.

Net income was $414.8 million, $17.78 per diluted share, for the year ended December 31, 2024 compared to $308.1 million, $13.22 per diluted share, for the year ended December 31, 2023.

Profitability kept pace with growth. Net income expanded 35% year-over-year in 2024, demonstrating that Kinsale wasn't chasing volume at the expense of margins. This discipline—growing fast while staying profitable—is the hallmark of great compounders.

VIII. The Business Model Deep Dive

Revenue Streams

Kinsale's business model combines two primary revenue engines: underwriting income and investment income. Understanding how each contributes illuminates the company's economic engine.

In 2024, Kinsale reported strong financial results, with net income of $414.8 million, up 34.6% from $308.1 million in 2023. This increase was primarily due to continued profitable growth in the business and strong investment performance, including higher investment income and higher unrealized gains on equity investments. Underwriting income, which excludes investment income and other non-underwriting items, was $325.9 million in 2024, up 20.5% from $270.4 million in 2023. The corresponding combined ratio, which is the sum of the loss ratio and expense ratio, was 76.4% in 2024 compared to 75.4% in 2023.

The combined ratio deserves explanation. In insurance, a combined ratio below 100% means the company earns an underwriting profit—it collects more in premiums than it pays in claims and expenses. Kinsale's 76.4% combined ratio means it keeps roughly $24 of every $100 in premium as underwriting profit, before investment income.

Net investment income was $41.9 million in the fourth quarter of 2024 compared to $30.4 million in the fourth quarter of 2023, an increase of 37.8%. Net investment income was $150.3 million for the full year of 2024 compared to $102.3 million for the full year of 2023, an increase of 46.9%.

Investment income represents the "float" strategy that made Warren Buffett famous. Insurance companies collect premiums upfront but don't pay claims until later. That gap creates investable assets—float—that generates returns. Cash and invested assets totaled $4.1 billion at December 31, 2024 compared to $3.1 billion at December 31, 2023.

Kinsale invests its float conservatively. Funds are generally invested conservatively in high-quality securities, including government agency, asset- and mortgage-backed securities, and municipal and corporate bonds with an average credit quality of "AA-." The weighted average duration of the fixed-maturity investment portfolio, including cash equivalents, was 3.0 years.

This conservative approach reflects management's philosophy: insurance should be profitable from underwriting, with investment income as gravy rather than necessity. Companies that rely on investment income to offset underwriting losses are one bad market away from crisis.

Product Diversification

Kinsale's product breadth provides both diversification and multiple avenues for growth.

The company's commercial lines offerings include commercial property, excess casualty, small business casualty, general casualty, construction, allied health, small business property, products liability, entertainment, energy, life sciences, commercial auto, professional liability, excess professional, environmental, inland marine, health care, management liability, public entity, aviation, ocean marine, agribusiness, product recall, and railroad insurance.

That's 25+ distinct coverage categories, each with its own underwriting dynamics, risk characteristics, and competitive landscape. This diversification protects against concentration risk—a problem in one line doesn't sink the ship.

The company's commercial lines offerings include commercial property, excess casualty, small business casualty, general casualty, construction, allied health, small business property, products liability, entertainment, energy, life sciences, commercial auto, professional liability, excess professional, environmental, inland marine, health care, management liability, public entity, aviation, ocean marine, agribusiness, product recall, and railroad insurance. Its personal lines offerings also include high value homeowners and personal insurance products. The company sells its insurance products in all 50 states, the District of Columbia, the Commonwealth of Puerto Rico, and the U.S. Virgin Islands primarily through a network of independent insurance brokers.

Underwriting Discipline

The heart of Kinsale's business model is underwriting discipline—the willingness to say no to business that doesn't meet profitability standards.

This strategic focus has allowed Kinsale to achieve a net loss and LAE ratio consistently below 60% (e.g., 54.6% in 2023), far outperforming the P&C industry (76.1%) and surplus lines sector (64.4%).

The selectivity metrics illustrate this discipline. Kinsale receives hundreds of thousands of submissions annually. Of those, only a small fraction become policies.

Last year, Kinsale received 881,000 new business submissions and accepted 64,000 new policies, with less than 660 FTEs. That's just an incredible efficiency.

The hit ratio—policies written divided by submissions received—runs in the single digits. This pickiness isn't random; it reflects a granular understanding of which risks are profitable at which prices. The technology platform enables this analysis at scale.

Owner-Operator Culture

The company fosters an 'owner-operator' culture, encouraging leadership and employees to invest personal capital. This approach encourages a significant personal investment from employees, particularly within the leadership team, into the business. This strategy is designed to create a strong alignment between the incentives of employees and the interests of the company's shareholders.

The "Value of At-Risk Investment" for Kehoe cited by Board was $446,036,770 (based on 3/27/2025 close).

When a CEO has over $400 million of personal wealth tied to the company's stock price, incentive alignment isn't theoretical—it's visceral. Kehoe isn't managing for quarterly earnings calls; he's building a legacy company that will compound his family's wealth for generations.

IX. Competitive Landscape & Strategic Positioning

Key Competitors

Kinsale operates in a competitive market with several formidable players.

Markel Group Inc. is another major direct competitor. As a diversified financial holding company, Markel has a substantial E&S insurance segment. Markel offers a broad range of coverages, competing directly with Kinsale Capital Group in various specialty lines.

RLI Corp. is a significant direct competitor. It's known for its focus on specialty insurance lines and consistent underwriting profitability. RLI's financial performance and market position make it a key player to watch. In 2024, RLI Corp. reported gross premiums written of approximately $1.4 billion in its specialty insurance segment.

Markel's insurance segment generated approximately $8.5 billion in gross written premiums in 2024.

Primary competitors in the E&S sector include Arch Capital Group, Argo Group, James River Group, Lloyds of London, Markel Corporation, RLI Corp., and W. R. Berkley Corporation.

The Kinsale Advantage

Despite facing larger, well-resourced competitors, Kinsale maintains meaningful advantages.

[Markel's CEO] Wilson referenced combined ratios of competitors—Kinsale, averaging 78.7 over the last five years, and RLI, averaging 87.2.

"We've almost taken it for granted that we will just continue to win in that area. We've gone after other bits of the market saying, 'Oh, there's lots of premium over here, there's lots of premium over there. And meanwhile, Kinsale has gone right into that wholesaling specialty E&S market and started making money at a 70-something combined ratio."

That's a direct quote from Markel's insurance CEO, essentially acknowledging that Kinsale has outmaneuvered them in the core E&S market. When your largest competitor is publicly lamenting your success, that's evidence of durable competitive advantage.

Kinsale Capital has a moat based on 4 main factors: 1️⃣Leveraging its technology to generate superior data, insights, and services 2️⃣Exclusive focus on the E&S market (a more profitable segment within insurance) 3️⃣Vigilantly controlling expenses (resulting in a lower expense ratio versus competitors) 4️⃣Focus on small accounts (Kinsale is a market leader in this underserved niche). It's great seeing that Kinsale Capital's combined ratio is one of the lowest amongst their specialty insurer peers. Over the past 10 years, Kinsale Capital's combined ratio averaged 78% and the combined ratio has never been higher than 86% over the past decade.

In the E&S market, Kinsale Capital is the only publicly traded pure-play.

This pure-play status matters for two reasons. First, it provides investors clean exposure to the E&S market without the conglomerate complexity of competitors. Second, it means management attention isn't divided across disparate businesses—they wake up every day thinking only about E&S insurance.

X. Porter's Five Forces Analysis

1. Threat of New Entrants: MODERATE-LOW

The E&S market's attractiveness has drawn interest from new entrants, but several barriers limit their impact.

Building the underwriting expertise Kinsale possesses takes years. The company's actuarial models reflect decades of loss experience; new entrants start with blank slates. Similarly, Kinsale's IT system took seven years to build. Replicating that infrastructure requires substantial investment and patience that venture-backed startups may lack.

Capital requirements present another hurdle. Insurance companies need regulatory approval, appropriate capitalization, and ratings from agencies like AM Best. A startup can't simply launch without this infrastructure.

However, the threat isn't negligible. Technology investments in AI and automation drive cost advantages, while management retains centralized underwriting control amid rising MGA competition. Managing General Agents (MGAs) backed by private equity have entered segments of the E&S market, creating pockets of intense competition.

2. Bargaining Power of Suppliers (Reinsurers): MODERATE

To manage risk and protect capital, Kinsale utilizes reinsurance. They purchase reinsurance coverage from highly rated reinsurers to reduce their exposure to large losses.

The company's strategic reinsurance programs are designed to mitigate risk and protect financial stability. By employing property quota share and catastrophe reinsurance, KNSL effectively limits its exposure to large losses.

Kinsale maintains relationships with multiple A-rated reinsurance companies to manage concentration risk. However, reinsurance markets are cyclical, and capacity can tighten following major catastrophe years. The 2024-2025 environment saw some moderation in reinsurance pricing, benefiting primary carriers like Kinsale.

3. Bargaining Power of Buyers (Brokers/Customers): LOW-MODERATE

E&S insurance serves hard-to-place risks where customers have limited alternatives. A cannabis dispensary or wildfire-exposed homeowner can't simply shop for coverage on a consumer comparison site—they need specialized brokers and specialized carriers.

Kinsale's technology advantage creates broker stickiness. This technology enables "scalable growth, enhanced customer interactions, and improved cost control." It facilitates quicker adjustments to market conditions, helping Kinsale capture market share from slower competitors.

When Kinsale can quote a complex risk in 24 hours while competitors take days, brokers gravitate toward the faster option. This speed advantage, enabled by technology, creates switching costs.

4. Threat of Substitutes: LOW

Standard admitted insurers cannot easily substitute for E&S coverage due to regulatory constraints. The E&S market exists precisely because standard markets won't write these risks. It typically expands when the standard market tightens or becomes overly cautious, filling coverage gaps. The company's exclusive focus on the E&S market means it operates in a segment designed for specialized, often complex risks that traditional insurers avoid. This dynamic gives Kinsale a clear structural advantage.

Alternative risk transfer mechanisms like captives or self-insurance exist, but they're typically viable only for large enterprises with dedicated risk management functions—not the small and mid-sized businesses that comprise Kinsale's core market.

5. Industry Rivalry: HIGH (but manageable for disciplined players)

Gross written premium growth has decelerated for 7 straight quarters, with this quarter coming in at just mid-single digits. This reflects a more competitive market, moderating rate increases, and a shift away from the hard market conditions that powered Kinsale's earlier growth.

The E&S market is experiencing intensifying competition as the hard market conditions that characterized 2020-2023 begin to normalize. Standard carriers are re-entering segments they previously abandoned, and E&S carriers are competing more aggressively on price.

However, Kinsale's cost advantage provides resilience. The company's technology-driven efficiency, evidenced by its low expense ratio, allows Kinsale to offer competitive pricing while maintaining strong profitability. This cost advantage could enable the company to capture market share from less efficient competitors, particularly in a market where pricing is becoming more competitive.

XI. Hamilton Helmer's 7 Powers Framework

For investors seeking to understand Kinsale's durability, Hamilton Helmer's 7 Powers framework provides useful structure.

Scale Economies

Kinsale benefits from meaningful scale advantages in its technology platform. Fixed development costs spread across a growing premium base, reducing unit costs over time. However, insurance is less scale-dependent than manufacturing—a smaller, well-managed carrier can compete effectively.

Network Effects

Limited direct network effects, though broker relationships create a form of ecosystem value. Brokers who become proficient with Kinsale's systems prefer continuing that relationship.

Counter-Positioning

This is Kinsale's strongest power. Large competitors like Markel and W.R. Berkley have diversified business models, including admitted insurance, ventures, and international operations. "We've almost taken it for granted that we will just continue to win in that area... And meanwhile, Kinsale has gone right into that wholesaling specialty E&S market and started making money at a 70-something combined ratio."

To match Kinsale's pure E&S focus, competitors would need to divest or de-emphasize other businesses—an unappealing choice given their existing commitments. Kinsale's narrow focus allows optimization that diversified players can't replicate.

Switching Costs

Moderate switching costs exist for brokers who have integrated with Kinsale's quoting systems and developed relationship-specific knowledge. However, insurance products themselves are not locked-in; customers can switch at renewal.

Brand

In B2B specialty insurance, brand manifests as reputation for reliability, fair claims handling, and underwriting expertise. Kinsale has built strong broker relationships, but this isn't consumer brand in the traditional sense.

Cornered Resource

Kinsale's management team represents a form of cornered resource. The average manager has over 30 years of relevant experience. Michael Kehoe and Brian Haney worked together for over 20 years. This institutional knowledge is difficult to replicate or poach.

Process Power

This is Kinsale's second-strongest power. The combination of proprietary technology, centralized operations, and disciplined underwriting culture creates operational excellence that's embedded in organizational routines rather than individual heroics. This is not merely a collection of good business practices but an integrated and intentional design. By controlling its underwriting and claims processes in-house, and by aggressively using technology to manage expenses and select risks, Kinsale has built an operational structure that is difficult for competitors to replicate.

For investors, the 7 Powers analysis suggests Kinsale's advantages are durable but not impenetrable. Counter-positioning and process power provide meaningful protection, but the company must continue executing to maintain its edge.

XII. Key Risks and Considerations

Cyclical Market Dynamics

Gross written premium growth has decelerated for 7 straight quarters, with this quarter coming in at just mid-single digits. This reflects a more competitive market, moderating rate increases, and a shift away from the hard market conditions that powered Kinsale's earlier growth. What we may be seeing is the beginning of a new cycle, where Kinsale's growth remains solid but no longer exceptional. (It's worth noting that some of the growth slowdown reflects management's deliberate strategy: profit comes first, growth second.)

Insurance is inherently cyclical. The extraordinary growth rates of 2020-2023 reflected hard market conditions that won't persist indefinitely. As the market softens, Kinsale faces a choice between maintaining margins (accepting slower growth) or chasing volume (risking underwriting quality). Management has consistently chosen the former, but this means near-term growth rates may disappoint investors expecting perpetual acceleration.

Catastrophe Exposure

Another persistent risk is Kinsale's exposure to unpredictable loss events. The company operates in the excess and surplus lines segment, insuring hard-to-place risks that traditional insurers avoid. Although this niche is typically more profitable, it can also be more volatile. Q1 2025 offered a clear reminder when catastrophe losses from the Palisades Fire pushed Kinsale's combined ratio above 82%. While the company uses reinsurance to limit exposure, large events can still hit earnings and introduce significant volatility.

In January 2025, the company estimates approximately $25 million in pre-tax catastrophe losses from Southern California wildfires.

E&S insurance inherently involves writing risks that standard carriers consider too volatile. Kinsale mitigates this through reinsurance, diversification, and concentration limits, but catastrophe losses remain an earnings volatility factor.

Valuation Premium

At 27x forward earnings and over 6x book, the risk/reward skews more neutral at current levels.

The company trades at 18.2x [earnings], which is higher than both the industry average of 12.7x and the peer average of 17.2x. This sits notably above the fair ratio of 10.8x, suggesting less room for upside and possible valuation risk.

Kinsale has warranted a premium multiple throughout its public life, reflecting superior execution and growth prospects. However, premium valuations compress when growth slows or competitive advantages erode. Investors must assess whether current multiples appropriately reflect both opportunities and risks.

Key Person Risk

Brian D. Haney, President and Chief Operating Officer, has been elected to the Company's Board of Directors, effective October 23, 2025. In addition, Mr. Haney has informed the Company of his plans to retire on March 2, 2026. Michael P. Kehoe, who currently serves as Chairman of the Board and Chief Executive Officer, will assume the additional title as President of the Company upon Mr. Haney's retirement.

The upcoming retirement of Brian Haney, who has been with the company since founding and represents half of the Kehoe-Haney leadership partnership, deserves attention. While Stuart Winston's promotion to Chief Underwriting Officer provides continuity, succession planning at founder-led companies always introduces uncertainty.

XIII. Critical KPIs for Investors

For long-term fundamental investors tracking Kinsale, three metrics deserve particular attention:

1. Combined Ratio

The combined ratio remains the single most important indicator of underwriting quality. Kinsale's historical average around 78% represents best-in-class performance. Investors should watch for: - Trend direction: Sustained increases could signal competitive pressure or declining underwriting quality - Catastrophe-adjusted figures: Large cat events can distort quarterly results - Comparison to peers: Maintaining the ~8-point advantage over competitors indicates enduring competitive strength

2. Gross Written Premium Growth

Premium growth reflects Kinsale's ability to expand market share while maintaining discipline. Historical growth rates above 30% CAGR since IPO reflected exceptional conditions; management guidance of 10-20% normalized growth provides a reasonable baseline.

Long-term growth target of roughly 10%–20% annualized over the cycle.

Investors should focus on the trade-off between growth and profitability. Growth acceleration at the expense of combined ratio would be concerning; growth moderation while maintaining underwriting excellence suggests management discipline.

3. Expense Ratio

Expense ratio expected to gradually decline over time via technology/productivity gains.

The expense ratio measures operational efficiency and the sustainability of Kinsale's cost advantage. Continued improvement validates technology investments; deterioration would suggest competitive catch-up or scale diseconomies.

XIV. Bull Case vs. Bear Case

The Bull Case

Secular E&S Market Growth: The structural shift of risks from admitted to E&S markets shows no signs of reversing. Climate volatility, emerging technologies, and litigation trends continue pushing complex risks into E&S territory. Kinsale rides this wave as the only pure-play public company.

Durable Competitive Advantages: Counter-positioning versus diversified competitors, process power embedded in technology and culture, and a management team with 20+ years of collaborative history create moats that take years to replicate.

Operating Leverage: As premium scales, Kinsale's fixed technology costs spread across a larger base, enabling continued expense ratio improvement. Higher premiums with stable expenses means widening margins.

Investment Income Tailwind: A $4+ billion investment portfolio generating consistent returns adds earnings stability independent of underwriting cycles.

Reinvestment Runway: The E&S market remains fragmented, with Kinsale currently holds less than 2% of the market. Market share gains can continue for years before competitive saturation.

The Bear Case

Cyclical Normalization: The hard market conditions of 2020-2023 represented extraordinary tailwinds. As pricing softens and standard carriers re-enter segments, Kinsale's growth rates may compress toward industry averages.

Competitive Erosion: Technology advantages can be replicated over time. If competitors invest in modern platforms and improve efficiency, Kinsale's expense ratio advantage could narrow.

Catastrophe Concentration: Despite reinsurance and diversification, a sufficiently large catastrophe event could produce material losses and call into question underwriting discipline.

Valuation Reset: Trading at premium multiples means any disappointment—slower growth, margin compression, competitive pressures—could produce outsized stock price declines as the multiple de-rates.

Management Transition: The departure of Brian Haney and eventual succession from founder Michael Kehoe introduce uncertainty about whether exceptional culture and execution persist.

XV. Conclusion: The E&S Insurance Compounder

Kinsale Capital Group represents something increasingly rare in public markets: a founder-led company with demonstrable competitive advantages, operating in a structural growth market, and managed with long-term orientation.

Our goal is to provide long-term value to our stockholders by generating exceptional profit and growth. Kinsale seeks to accomplish our goal by producing consistent underwriting profits, steady investment returns along with sound capital management. Kinsale Capital Group, Inc. is designed to be highly entrepreneurial and efficient. We differentiate ourselves from our competitors by effectively leveraging technology, vigorous expense management and by maintaining control over our claims and underwriting processes.

The comparison to Berkshire Hathaway—frequently invoked by analysts—is both apt and misleading. Like Berkshire, Kinsale generates underwriting profits while investing its float. Like Berkshire, it benefits from long-tenured management with significant equity stakes. Unlike Berkshire, Kinsale is focused exclusively on specialty insurance rather than diversified into railroads, utilities, and consumer brands.

Perhaps a better mental model is Kinsale as "the Costco of E&S insurance"—a company that uses operational excellence to achieve structurally lower costs, passing some savings to customers (faster quotes, competitive pricing) while retaining superior margins. Like Costco, Kinsale's advantages compound over time: better data leads to better underwriting, which attracts more submissions, which generates more data.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube