RenaissanceRe Holdings: The Story of the World's Premier Catastrophe Reinsurer

I. Introduction & Episode Roadmap

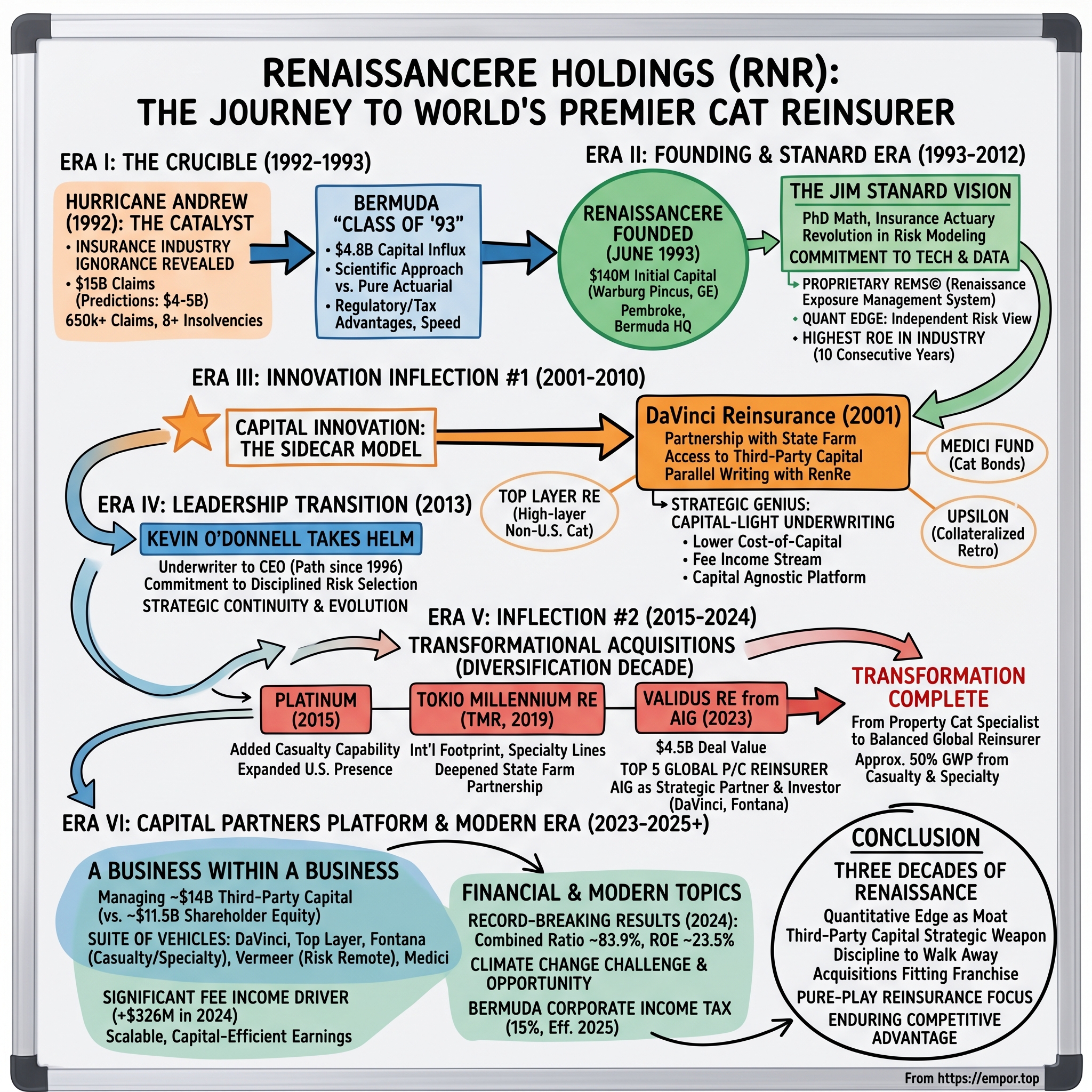

The morning of August 24, 1992, began with an almost eerie stillness across South Florida. Then Hurricane Andrew arrived—a Category 5 monster that would fundamentally reshape how the world thinks about, prices, and finances catastrophic risk. In 1992, Hurricane Andrew virtually recreated the catastrophe reinsurance business in Bermuda's image, blowing what was at the time unprecedented capital offshore to form much needed programmes to improve the financing of catastrophe risks. In so doing, it created the genesis of the broader reinsurance market that exists today on the island.

Less than a year later, a small team led by a PhD mathematician and insurance actuary named Jim Stanard would raise $140 million to launch a company with a revolutionary premise: that hurricanes, earthquakes, and other catastrophic events could be quantified, modeled, and priced with scientific precision. RenaissanceRe was founded in June 1993 in Bermuda with the goal of embracing the emerging science of catastrophe modeling to bring a renaissance to the underwriting of property catastrophe reinsurance.

Founded in Bermuda in 1993, RenaissanceRe is now one of the world's largest and most successful reinsurers of natural and man-made catastrophes. The company that began with a handful of underwriters and an idea has grown into a global reinsurance powerhouse. As of June 2025, RenaissanceRe has trailing twelve-month revenue of $12.9 billion, with a current market cap of $11.3 billion and 47.1 million shares outstanding.

The central question animating this story: How did a company founded with $140 million in the aftermath of a devastating hurricane become the gold standard for sophisticated catastrophe risk management?

The answer lies in understanding four interconnected threads. First, the birth of modern catastrophe reinsurance in Bermuda and the revolution in quantitative risk modeling that accompanied it. Second, the vision and analytical edge that Jim Stanard embedded in RenaissanceRe's DNA from day one. Third, the pioneering innovation in third-party capital that transformed how institutional investors access insurance risk. And fourth, the acquisition-driven transformation of the 2010s and 2020s that elevated RenaissanceRe from a niche property catastrophe specialist into a diversified global reinsurance leader.

What emerges is a story about the power of intellectual discipline, the value of walking away from bad business, and how the right kind of capital—deployed with surgical precision—can build enduring competitive advantage.

II. The Crucible: Hurricane Andrew and the Birth of Modern Bermuda

The 1992 Catalyst

Before diving into RenaissanceRe's founding, one must understand the catastrophic moment that created the opportunity. Hurricane Andrew didn't just devastate South Florida—it revealed the insurance industry's profound ignorance about the risks it had been underwriting for decades.

Industry predictions at the time were that it would cost insurers around $4 billion to $5 billion, but Andrew ended up costing the insurance industry $15 billion (in 1992 values) for Florida claims. That's not a minor miss—it's being off by 300%. The models, such as they existed, had catastrophically failed.

Following Hurricane Andrew, more than 650,000 claims were filed, leaving eight insurers becoming insolvent and a further three driven into insolvency the following year. The storm didn't just test balance sheets; it broke them. The Insurance Information Institute estimates Andrew caused $30 billion in insured losses in 2021 dollars, fundamentally changing the face of the global reinsurance market.

The human toll was staggering—65 lives lost, 44 in Florida alone—but for the insurance industry, Andrew represented an existential reckoning. The comfortable assumption that historical loss data could adequately capture tail risk was proven violently wrong.

The Bermuda Class of '93

Nature abhors a vacuum, and capital even more so. Within months of Andrew's landfall, the foundations of modern Bermuda reinsurance were being laid.

Mid Ocean Re was the first reinsurer to be set up in Bermuda in November 1992, barely three months after the storm had left a trail of destruction in southern Florida. In the ensuing months, nine more reinsurers followed.

Following Mid Ocean Re's blueprint came a wave of new reinsurers, including two still operating today, RenaissanceRe and PartnerRe. Centre Cat, LaSalle Re, International Property Catastrophe Re, Tempest Reinsurance, Global Capital Re, Compass Re and Starr Excess Liability also drew investments from insurance brokers and insurers, investment banks and private equity. In total, Bermuda's Class of 1993 raised $4.8 billion. The Bermudian newcomers brought to market not only capital to restore underwriting capacity, but also a more measured, scientific approach using complex models.

This location offered regulatory and tax advantages crucial for the reinsurance industry. But Bermuda's advantages went far beyond taxes. As one industry veteran noted: "Every dollar of capital for newly formed reinsurers in the immediate aftermath of Hurricane Andrew ended up in Bermuda. Every company that I was associated with chose Bermuda for what at the time was a robust regulatory environment. To some degree its location—90 minutes outside of New York—was helpful, but so also the speed with which the capital was able to form and get into the market, which remains an advantage in Bermuda today."

The speed mattered enormously. Primary insurers needed reinsurance capacity desperately, and Bermuda's efficient company formation process allowed new reinsurers to begin underwriting within months rather than years.

The Revolution in Risk Modeling

Perhaps the most profound change Andrew catalyzed wasn't in regulation or capital formation—it was in how catastrophe risk itself was understood and quantified.

Andrew coincided to a large extent with the emergence of the computer model. It was the Bermuda underwriters who took an analytical approach to underwriting property cat exposures and "were at the forefront of providing a quantitative analysis of exposure to pricing and to the capacity that they offered in the marketplace."

Using catastrophe models enabled reinsurers to differentiate between insurers with similar property premium levels. "Of course, there is qualitative stuff that goes into underwriting, and there's no substitute for that, but there has to be an underlying foundation of analytics that drives the pricing, the risk selection and the whole portfolio composition."

This wasn't just incremental improvement—it was a paradigm shift. Before Andrew, catastrophe underwriting was largely actuarial, based on historical loss frequencies adjusted for exposure growth. After Andrew, it became increasingly probabilistic and simulation-based, using computer models to generate thousands of possible loss scenarios based on physical understanding of hazard, exposure, and vulnerability.

In time, catastrophe models would enable the creation of insurance-linked securities such as catastrophe bonds, to tap into capital markets for alternatives to reinsurance. Without Hurricane Andrew, it might have taken much longer for this revolution to happen.

The Bermuda Class of '93 companies would be the primary beneficiaries and drivers of this revolution, and none more so than RenaissanceRe.

III. Founding & The Jim Stanard Era (1993–2012)

The Visionary Founder

RenaissanceRe Holdings Ltd. was established in 1993. It emerged in the wake of Hurricane Andrew, a period when significant capital dislocation created opportunities in the property catastrophe reinsurance market. The company was founded and remains headquartered in Pembroke, Bermuda.

The key figure behind the founding was James (Jim) N. Stanard, who served as the initial Chairman, President, and CEO.

James Stanard wasn't a typical insurance executive. He holds a BA in Mathematics from Lehigh University, a PhD in Finance from New York University, is a fellow of the Casualty Actuarial Society, and has authored award-winning actuarial papers. This combination—academic rigor in quantitative finance married to actuarial credentialing—proved uniquely suited for what RenaissanceRe would attempt.

From 1990 to 1993, Stanard was Executive Vice President of USF&G. As a member of a successful turnaround team, he was responsible for underwriting and claims. From 1983 to 1990, he was co-founder and Executive Vice President of F&G Re, one of the most successful reinsurers in the world during that period. During his 35 years in the insurance industry, he has also held underwriting and actuarial positions at Prudential, Chubb and INA.

Stanard saw what others in the industry were slow to grasp: that the emerging science of catastrophe modeling, combined with the computing power that was becoming available in the early 1990s, offered an opportunity to fundamentally reimagine how catastrophe risk was assessed and priced.

The Capital Formation

RenaissanceRe was launched with significant initial capital, approximately $140 million, primarily raised through a private placement led by Warburg Pincus Ventures L.P. and GE Investment Private Placement Partners I-A, L.P., among others.

This was the PE-backed reinsurer model in its earliest form—private equity spotting an arbitrage opportunity in catastrophe pricing following Andrew. Post-storm, catastrophe reinsurance rates had spiked dramatically, creating exceptional return potential for well-capitalized, well-managed new entrants.

But what differentiated RenaissanceRe from many Class of '93 peers was the intensity of its commitment to technological differentiation from day one.

The Analytical Edge

From its inception, the company focused intensely on sophisticated modeling and underwriting of property catastrophe risk. This data-driven approach allowed it to price complex risks effectively, often leading the market.

The company stated: "We have been a pioneer in the use of sophisticated computer modeling for risk analysis and management. Using proprietary technology, our seasoned team of underwriters seeks to construct a superior risk portfolio, while cultivating long-term relationships with clients who appreciate our problem-solving capabilities."

The key technological asset was REMS—the Renaissance Exposure Management System. With respect to Reinsurance operations, since 1993 the company developed a proprietary, computer-based pricing and exposure management system, Renaissance Exposure Management System (REMS©). The company believed that REMS© was a more robust underwriting and risk management system than was currently commercially available elsewhere in the reinsurance industry and offered a significant competitive advantage amongst its competitors. REMS© was developed to analyze catastrophe risks.

The company's value creation hinges on disciplined underwriting powered by proprietary risk modeling technology (REMS©). This allows for precise risk selection and pricing, particularly in complex catastrophe markets.

What made REMS© different? Most competitors purchased catastrophe models from vendors like AIR Worldwide or RMS and used them more or less out of the box. RenaissanceRe invested heavily in developing proprietary views of risk that could supplement, challenge, or supersede vendor models. This gave underwriters an independent basis for assessing whether a risk was attractively priced—a crucial advantage in a market where all competitors had access to the same commercial models.

Building the Foundation

RenaissanceRe was formed in 1993 to address an identified market need, with differentiated capabilities in underwriting, service, responsiveness, and a unique ability to match capital to risk. We started with a handful of underwriters in one office and an idea to transform the property catastrophe market.

The company went public, listing on the NYSE, and the Stanard era produced extraordinary results. As the Founder and former Chairman and CEO of RenaissanceRe, Jim grew the company's market value from $141 million in 1993 to over $3 billion when he left in 2005. As a worldwide leader in property catastrophe reinsurance, RenaissanceRe achieved the highest ROE in the insurance industry in each of ten consecutive years.

That last statistic bears repeating: highest ROE in the insurance industry for ten consecutive years. This wasn't a company riding market conditions—it was systematic outperformance driven by superior risk selection.

Stanard's tenure ended under a cloud in 2005, amid SEC investigations into finite reinsurance transactions that were roiling the industry. RenaissanceRe Holdings Ltd.'s longtime chairman and chief executive officer, James N. Stanard, stepped down amid investigations into the reinsurer's use of finite risk coverage and concerns over charges he and the company may face from U.S. securities regulators.

Neill A. Currie was named CEO and W. James MacGinnitie, non-executive chairman. Currie had co-founded RenaissanceRe in 1993 and served as a senior vice president through 1997.

The succession was smooth in a practical sense—Currie knew the company's DNA intimately—but Stanard's departure marked the end of the founding era.

IV. Innovation Inflection #1: The DaVinci Revolution and Third-Party Capital (2001–2010)

The Birth of the Sidecar Model

If REMS represented RenaissanceRe's intellectual moat, DaVinci Reinsurance represented its capital innovation moat—and arguably, it was even more consequential for the company's long-term competitive position.

DaVinci Reinsurance Ltd. (DaVinci Re) was established by Bermuda-based reinsurer RenaissanceRe (RenRe) in October 2001, making it one of the oldest reinsurance sidecar vehicles with available data.

DaVinci Re was founded in October 2001 as a sidecar by RenaissanceRe and State Farm for property catastrophe risk. Shortly thereafter, additional investors joined.

The timing was telling—October 2001, just weeks after 9/11, when catastrophe reinsurance capacity was once again in high demand. But the structure was what mattered most.

A "sidecar" in reinsurance parlance is a vehicle that writes risk in parallel with its sponsor, allowing third-party investors to participate in the sponsor's underwriting without owning equity in the sponsor itself. The investors get access to the sponsor's deal flow and underwriting expertise; the sponsor gets access to capital that can be deployed alongside its own, earning fee income in the process.

The early creation of DaVinci Re (2001) and subsequent ventures like Upsilon RFO and Medici Fund marked RNR as an innovator in managing third-party capital alongside its own balance sheet.

The Strategic Genius: Capital-Light Underwriting

The genius of the DaVinci structure wasn't immediately obvious to outside observers, but it would become RenaissanceRe's secret weapon.

The sidecar, or joint-venture, is a key component of RenaissanceRe's capital agnostic underwriting platform, giving it an edge by lowering its cost-of-capital, which in the currently challenging reinsurance market is a key contributor to underwriting strength.

Think about what this means practically. In traditional reinsurance, a company's capacity is constrained by its own capital base. If shareholders want a 15% return and you have $1 billion in equity, you can write perhaps $2-3 billion in premium while maintaining appropriate risk levels. If you want to write more, you need more capital—which means diluting existing shareholders or taking on leverage.

DaVinci offered an elegant alternative. DaVinci Re, the joint-venture largely third-party capitalised reinsurance sidecar, is both "core and strategic" to Bermudian reinsurer RenaissanceRe's business and future, according to rating agency Moody's.

Moody's notes that the investors in DaVinci Re typically expect a lower return than would shareholders of traditional reinsurance companies, which the rating agency says bodes well for "maintaining and attracting capital despite a very challenging reinsurance market."

The lower return expectation of DaVinci investors isn't a bug—it's a feature. These investors are typically large institutions (pension funds, sovereign wealth funds) seeking diversifying exposure to insurance risk. They're not seeking equity-like returns; they're seeking an asset class uncorrelated with their equity and fixed income portfolios. RenaissanceRe provided access to that asset class with top-tier risk selection and earned fees for doing so.

Post-9/11 and Katrina Era Expansion

Established in 1993 in the wake of Hurricane Andrew, RenaissanceRe's birth, evolution and success have been intricately linked to its response to calls for capacity. From the shortage of catastrophe coverage following Hurricane Andrew in 1992, to events such as September 11, 2001 and the year of Katrina-Rita-Wilma (2005), "every major event has resulted in something of a rebirth, with RenaissanceRe able to commit additional capital to the market whenever there has been a scarcity." Following each of these events the company identified customers' need for protection and been in a position to access and deliver that additional capital.

Top Layer Re was a joint venture formed to provide capacity following 9/11 with additional capacity in 2005 following Hurricanes Katrina, Rita and Wilma. The joint venture with State Farm targets high layers of non-U.S. catastrophe reinsurance business.

This pattern—major catastrophe creates capacity crunch, RenaissanceRe deploys capital at attractive terms—repeated across the 2000s and would continue in subsequent decades.

Expanding the Third-Party Capital Arsenal

It is through its exploration of alternative structures such as DaVinci Re and Top Layer Re that RenaissanceRe has led the field in the delivery of capacity in the convergence space. As O'Donnell outlined, these structures have been "critically important to the company's success", helping to create "permanent vehicles with long-standing and trusted partners." For its partners these vehicles have in turn enabled RenaissanceRe to deliver "greater security across the spectrum of rated balance sheets and third party capital."

Beyond DaVinci and Top Layer, RenaissanceRe launched additional structures to access different investor segments:

- Medici Fund (2009): A catastrophe bond fund that enabled investors to access the ILS market through RenaissanceRe's expertise in bond selection

- Upsilon: Collateralized vehicles focused on retrocessional business

- Purpose-built sidecars: Short-term vehicles deployed opportunistically after major events

Each structure served a different purpose, but all shared a common thread: using RenaissanceRe's underwriting expertise to connect institutional capital with catastrophe risk, earning fees for the platform.

V. The Leadership Transition: Kevin O'Donnell Takes the Helm (2013)

The Next Generation Leader

Kevin O'Donnell holds a BA in Economics from Hamilton College and an MBA from Stern School of Business, New York University. His former positions include Vice-President at Centre Financial Products and Underwriter at SCOR. In 1996, he joined RenaissanceRe to lead the International Underwriting and Ceded Reinsurance businesses; has served as Chief Underwriting Officer for key joint ventures, Top Layer Re and DaVinci Re; 2005, President, Renaissance Reinsurance, overseeing the company's reinsurance lines, including property catastrophe and specialty reinsurance, as well as its joint ventures; 2009, directed the launch of RenaissanceRe Syndicate 1458 at Lloyd's; 2010, Executive Vice-President and Global Chief Underwriter; 2012, President; July 2013, Chief Executive Officer.

O'Donnell's path to the top was classic RenaissanceRe—he was an underwriter who rose through the ranks, not a finance person or an outsider. His technical background shaped his approach to leadership and strategy.

Kevin J. O'Donnell is the President and Chief Executive Officer of RenaissanceRe, a leading global property and casualty reinsurer. He joined RenaissanceRe in 1996, with roles over that time including Executive Vice President and Global Chief Underwriter.

The promotion of an underwriter to CEO sent a message: RenaissanceRe's identity remained rooted in disciplined risk selection, not financial engineering.

Strategic Continuity and Evolution

As O'Donnell explained, "we have seen considerable change in the form and structure of capital entering the market" with the company evolving as a result. In its early days RenaissanceRe deployed a rated balance sheet to underwrite risk, but has since blazed a trail in the deployment of third party capital.

O'Donnell articulated this philosophy clearly: "At a high level, our job as underwriters is to go out into the market, find desirable risk and match it with efficient capital. If that capital is coming into the market in new ways we need to anticipate that."

This "capital agnostic" approach—being indifferent to whether risk is underwritten on RenaissanceRe's balance sheet or through third-party structures—became the organizing principle for how the company thought about growth.

The O'Donnell era would be defined by a willingness to make bold acquisitions that transformed RenaissanceRe's scale and scope while maintaining the analytical discipline that defined the company from its founding.

VI. Inflection #2: The Diversification Decade—Transformational Acquisitions (2015–2024)

The Platinum Acquisition (2015): The First Major Bet

Kevin J. O'Donnell, President and Chief Executive Officer of RenaissanceRe, commented at the time: "The combination of RenaissanceRe and Platinum marks an important milestone for our company, benefiting our expanded client base by providing additional products and underwriting expertise, two strong underwriting platforms in the United States, and increased scope and market presence. We expect the transaction to be accretive to book value per share and earnings per share, as well as increase the long-term value of our business for shareholders. With the acquisition successfully completed, we are a stronger, broader-reaching RenaissanceRe, offering more underwriting, product and capital solutions to both existing clients and new clients."

The acquisition was originally announced on November 24, 2014. The completion of the acquisition followed the receipt of all necessary regulatory approvals and approval of the transaction by Platinum shareholders, which was obtained at a special general meeting of Platinum shareholders held on February 27, 2015.

The Platinum acquisition accomplished two things. First, it added meaningful casualty reinsurance capability—an area where RenaissanceRe had been a relatively minor player. Second, it expanded U.S. presence and client relationships.

While rooted in property cat, the acquisitions of Platinum (2015), TMR (2019), and Validus Re (2023) represented deliberate moves to build a more balanced portfolio.

The Tokio Millennium Re (TMR) Acquisition (2019)

Kevin O'Donnell, President and CEO of RenaissanceRe commented: "We are very pleased to have entered into a definitive agreement to acquire Tokio Millennium Re from Tokio Marine. This transaction will increase our scale, broaden our reach and extend our ability to apply our core strengths to a deeper customer base. Our unique ability to capitalize on large, one-of-a-kind opportunities underscores our global reinsurance leadership, including in Casualty and Specialty lines, and our ability to execute on our successful, highly differentiated strategy." Mr. O'Donnell added: "We are also honored that State Farm has agreed to broaden its relationship with RenaissanceRe by investing in our common shares and extending a long-standing partnership between our two firms."

Bermuda-based RenaissanceRe Holdings agreed to acquire its competitor Tokio Millennium Re (TMR) for approximately $1.5 billion from its parent company Tokio Marine Holdings. The purchase consisted of approximately $1.22 billion of cash and $250 million of RenaissanceRe common shares.

Integration execution took center stage following Bermudian reinsurer RenaissanceRe's (RenRe) $1.5 billion takeover of Tokio Millennium Re (TMR), which completed on March 22nd, 2019.

TMR brought additional international footprint and specialty lines capability, continuing the diversification theme from Platinum. Importantly, the deal also deepened RenaissanceRe's relationship with Tokio Marine, one of Asia's largest insurers, and brought State Farm in as a direct shareholder—complementing its existing role as partner in Top Layer Re.

The Game-Changer: Validus Acquisition from AIG (2023)

If Platinum and TMR were meaningful acquisitions, Validus was transformational.

RenaissanceRe Holdings Ltd. announced it concluded its acquisition of Validus Re, the treaty reinsurance business of American International Group. AIG received total consideration of $3.3 billion in cash, including a pre-closing dividend, and approximately $275 million in RenaissanceRe common shares. The deal, which was announced on May 22, 2023, includes Validus Reinsurance Ltd. and its consolidated subsidiaries, AlphaCat Managers Ltd., and all renewal rights to the Assumed Reinsurance Treaty Unit of Talbot.

At the time of the May 2023 announcement, RenRe said the acquisition creates a top five global P/C reinsurer. The deal "further simplifies our business model and reduces volatility in our portfolio, while generating significant cash liquidity and capital efficiencies that enable us to accelerate our capital management strategy," said AIG's Chairman and CEO Peter Zaffino.

RenaissanceRe, a prominent figure in the reinsurance market, acquired the reinsurer Validus Re, along with AlphaCat and the Talbot Treaty reinsurance business, for a total deal value of $4.5 billion. The sale, pegged at $2.985 billion in cash and common shares of RenaissanceRe, provided AIG with considerable liquidity and capital efficiencies. With the inclusion of future capital synergies of about $400 million and excess capital over shareholders' equity of Validus Re, the total transaction value anticipated to exceed $4.5 billion.

The Validus deal did more than add premium—it fundamentally repositioned RenaissanceRe in the global reinsurance hierarchy.

AIG as Strategic Partner

Global insurance giant AIG is set to invest up to $500 million into third-party capital and joint-venture vehicles run by RenaissanceRe's Capital Partners unit, as part of the arrangement that sees the company selling the Validus reinsurance and AlphaCat ILS arms to RenaissanceRe. RenaissanceRe is intending to leverage its third-party reinsurance capital and insurance-linked securities (ILS) operations to extract greater efficiencies out of the Validus Re reinsurance book, as it assumes it after the acquisition.

The structure of the AIG deal was particularly elegant. Rather than simply selling Validus and walking away, AIG became a strategic partner—investing in RenaissanceRe's common shares and committing significant capital to DaVinci and Fontana. This created ongoing alignment between the two companies and brought one of the world's largest insurers into RenaissanceRe's third-party capital ecosystem.

The Transformation Complete

While rooted in property cat, the acquisitions of Platinum (2015), TMR (2019), and Validus Re (2023) represented deliberate moves to build a more balanced portfolio. These deals added substantial casualty and specialty lines, reducing volatility and broadening client relationships, transforming RNR from a niche player into a diversified global reinsurer by the end of 2024.

Although a recognized leader in property catastrophe since our founding, we have moved successfully into casualty and specialty, with approximately 50% of our gross premiums written now coming from this business.

The transformation was remarkable. A company that for its first two decades was almost synonymous with property catastrophe reinsurance had become a balanced, diversified global reinsurer—while maintaining the analytical discipline and capital efficiency that defined its competitive advantage.

RenaissanceRe stands out among traditional listed Bermudian peers in that it is the only one that has not attempted to build an insurance franchise or sold out. Its 2023 takeover of Validus, which catapulted it to fifth place among global reinsurers ranked by P&C premium, demonstrates a doubling down in reinsurance. RenRe restrains its primary exposure to a small segment of its property business.

VII. The Capital Partners Platform: A Business Within a Business

The Third-Party Capital Machine

What began with DaVinci in 2001 has evolved into a significant standalone business generating hundreds of millions in annual fee income.

At September 30, 2025, RenaissanceRe Capital Partners managed approximately $8.54 billion of third-party capital in various structures including DaVinci Reinsurance Ltd., RenaissanceRe Medici Fund Ltd., RenaissanceRe Medici UCITS Fund, RenaissanceRe Upsilon Fund, Vermeer Reinsurance Ltd., and Fontana Holdings. RenaissanceRe has total shareholder's equity of $11.5 billion.

Over the last twelve months, RenRe's third-party capital AUM has risen by $820 million, or 11%. The new highs underscore the important role third-party capital plays for RenaissanceRe, as the reinsurance joint ventures, catastrophe bond and insurance-linked security (ILS) funds continue to cement their role as a key income driver for the reinsurer. This third-party capitalised firepower also augments RenRe's stature in the global reinsurance market, and the now more than $14 billion of capital deployed by Capital Partners strategies continues to be a meaningful addition to RenRe's own $11.5 billion of shareholders' equity.

Think about those numbers. RenaissanceRe's shareholders have contributed approximately $11.5 billion in equity. But the company deploys over $14 billion of additional capital through its third-party vehicles—more than its own equity base. That capital generates fee income for RenaissanceRe while sharing in underwriting results, creating an earnings stream that doesn't require RenaissanceRe's own capital.

The Vehicles Explained

The various vehicles serve different purposes and investor needs:

The Medici UCITS Fund was established to provide European and other global investors with access to RenaissanceRe's property catastrophe bond investment strategy through a dedicated European-regulated UCITS structure. Fontana is RenaissanceRe's first joint venture 100% dedicated to writing casualty and specialty risks, including long-tail lines. Vermeer focuses on risk remote layers in the U.S. property catastrophe market. Upsilon was formed to provide collateralized capacity to RenaissanceRe via private placement of participating notes.

DaVinci: The original and still the largest third-party vehicle. DaVinciRe expanded its third-party capital base by an impressive $600 million over the year to June 30th 2025, ending the period at $3.51 billion. DaVinci functions like a sidecar—it writes property catastrophe reinsurance in parallel with Renaissance Reinsurance, giving investors equity-like exposure to RenaissanceRe's underwriting.

Top Layer Re: The joint venture with State Farm, targeting high-layer (meaning high attachment point, low probability) non-U.S. catastrophe risk. Add Top Layer Re, the joint venture backed by State Farm, and Capital Partners deploys $14.2 billion. That's RenRe's biggest end of quarter deployment on record.

Fontana: The Fontana joint-venture structure, which enables investors to allocate to casualty and specialty lines of reinsurance alongside RenaissanceRe, grew to $600 million of third-party capital assets by March 31st 2025. Fontana represented an important expansion—it was the first vehicle to allow institutional investors to access RenaissanceRe's casualty underwriting expertise, not just property catastrophe.

Medici Fund: A catastrophe bond fund that invests in the secondary and primary ILS markets, using RenaissanceRe's credit and modeling expertise to select bonds.

Vermeer: Bermuda-based RenaissanceRe Holdings and Dutch pension fund manager PGGM launched a new property catastrophe reinsurer called Vermeer Reinsurance to provide capacity focused on risk remote layers in the US property catastrophe market.

The Business Model Advantage

Strong performance across Three Drivers of Profit: underwriting income of $1.6 billion, net investment income of $1.7 billion, and fee income of $326.8 million in 2024.

For full-year 2024, fee income for the RenaissanceRe Capital Partners third-party capital and ILS business reached $326.8 million, which was up by an impressive 38% year-on-year.

The fee income stream is remarkable for several reasons. First, it's relatively stable—management fees accrue regardless of underwriting results, providing a base level of earnings even in catastrophe-heavy years. Second, it's capital-efficient—fees are earned on third-party capital, not RenaissanceRe's own equity. Third, it scales beautifully—as AUM grows, fee income grows proportionally without requiring additional capital from shareholders.

Q3 2025 fee income from the third-party capital business of RenRe Capital Partners reached $101.8 million, which is an increase of 24.1% from Q3 2024's $82.1 million (which was itself up 27.1% from Q3 2023).

The quarterly run-rate of fee income has more than doubled since early 2023, reflecting both AUM growth and the addition of AlphaCat through the Validus acquisition.

VIII. Financial Performance & The Modern Era (2023–2025)

Record-Breaking Results

The Validus acquisition positioned RenaissanceRe for a strong 2024, and the company delivered.

Return on average common equity of 19.3% and operating return on average common equity of 23.5% in 2024. 18.5% growth in book value per share and 26.0% growth in tangible book value per share plus change in accumulated dividends.

Combined ratio of 83.9% and adjusted combined ratio of 81.5%. Repurchased $677.6 million of common shares in 2024. Raised $857.4 million of third-party capital in the Capital Partners unit, with a further $237.8 million raised from third-party investors effective January 1, 2025.

A combined ratio of 83.9% is exceptional in reinsurance—it means RenaissanceRe made $16.10 in underwriting profit for every $100 of premium earned. The share repurchases demonstrate management's confidence in intrinsic value, while the continued growth in third-party capital validates the Capital Partners platform.

RenaissanceRe reported net income available to common shareholders of $1.8 billion for the 2024 fiscal year, despite recording a fourth quarter net loss. The company reported $2.2 billion of operating income available to common shareholders.

Climate Change and the Protection Gap

Kevin J. O'Donnell, President and Chief Executive Officer of RenaissanceRe, stated: "Climate change is one of the most complex challenges faced by the world and our business. As a reinsurer, we believe that we play an important role in managing climate risk while helping facilitate the transition to a lower carbon economy."

RenaissanceRe announced key appointments that advance its Environmental, Social, and Governance (ESG) strategy and further the Company's industry-leading understanding of climate risk. RenaissanceRe's purpose is to protect communities and enable prosperity, which is reflected in an ESG strategy centered on promoting climate resilience, closing the protection gap, and inducing positive societal change.

Climate change presents an interesting paradox for catastrophe reinsurers. On one hand, increasing frequency and severity of weather events create challenges for modeling and pricing. On the other hand, these same trends increase demand for reinsurance protection and may drive primary insurers to purchase more coverage at higher attachment points—potentially benefiting sophisticated reinsurers who can price climate risk accurately.

Bermuda Corporate Tax Change

A significant development affecting RenaissanceRe and its Bermuda peers was the introduction of corporate income tax in Bermuda.

With the assent of the governor on December 27, the Bermuda Corporate Income Tax Act of 2023 became law. Consistent with three prior public consultations, a 15% corporate income tax (CIT) will be applicable to Bermuda businesses that are part of multinational enterprise (MNE) groups with annual revenue of €750M or more. The tax is effective beginning in 2025.

Income tax expense of $32.6 million in 2024 compared to an income tax benefit of $510.1 million in 2023. The income tax expense in 2024 was primarily driven by operating income in the Company's taxable jurisdictions. The income tax benefit in 2023 was primarily driven by a net deferred tax benefit of $593.8 million recorded in connection with the enactment of the 15% Bermuda corporate income tax on December 27, 2023.

The Bermuda tax represents a structural change for the industry, but its impact is somewhat mitigated by transition provisions and the reality that many Bermuda reinsurers already faced meaningful U.S. tax exposure through BEAT (Base Erosion and Anti-Abuse Tax) provisions.

Bermuda's new 15% corporate income tax rate, set to take effect in January 2025, is unlikely to diminish the island's status as a global hub for insurance and reinsurance, according to insights from S&P Global Ratings.

"Bermuda is going to remain a sophisticated regulatory regime with a good amount of talent on the island in the insurance space. And that coupled with the fact that it's a reciprocal jurisdiction to the US as well," analysts noted.

IX. Playbook: Business & Investing Lessons

The RenaissanceRe Playbook

1. Quantitative Edge as Moat

RenaissanceRe is widely recognized as a premier player in the global reinsurance market, particularly esteemed for its deep expertise in property catastrophe risk, a segment it helped pioneer. Its reputation is built on rigorous underwriting discipline, sophisticated proprietary risk modeling technology (like REMS©), and a strong capital position, enabling it to provide significant capacity for complex risks. The company consistently generates strong returns on equity over the cycle, reflecting its underwriting focus. While smaller than some diversified competitors based on total premiums, its specialization and analytical prowess grant it significant influence.

From its founding, RenaissanceRe invested heavily in proprietary analytics that gave underwriters an independent view of risk. This wasn't about having better marketing or larger balance sheets—it was about being right more often than competitors about which risks to write and how to price them.

2. Third-Party Capital as Strategic Weapon

The DaVinci innovation—now expanded into a suite of vehicles managing over $8 billion in third-party capital—created multiple strategic advantages:

- Lower blended cost of capital than competitors relying solely on shareholder equity

- Fee income stream that's partially insulated from underwriting cycles

- Ability to deploy capital opportunistically after major events without diluting shareholders

- Long-term relationships with sophisticated institutional investors who become advocates for the platform

3. Discipline to Walk Away

The company decided not to renew its Timicuan Re sidecar, citing ample supply and an inability to deliver adequate returns to investors. The decision reflects another of RenaissanceRe's convictions, "that not only are our clients partners, but so too is the capital we deploy." O'Donnell said that the company had learned to return capital to investors when it could not be appropriately deployed, encouraging a close and mutually beneficial partnership with third party participants. "We have been diligent with our own equity, but equally so with that of our third party partners—an approach on which we are consistently complimented by investors."

This willingness to return capital—to third-party investors and shareholders alike—when opportunities don't meet hurdle rates is perhaps the most underrated aspect of RenaissanceRe's culture. Many reinsurers grow for growth's sake; RenaissanceRe grows only when returns justify it.

4. Acquisitions That Fit the Franchise

Each major acquisition—Platinum, TMR, Validus—expanded capabilities without compromising underwriting discipline. The company avoided the temptation to diversify into primary insurance (unlike Arch, Everest, and many peers) and instead deepened its reinsurance franchise across more product lines and geographies.

Porter's Five Forces Analysis

Threat of New Entrants: MODERATE

The Bermuda reinsurance market has meaningful barriers—regulatory capital requirements, rating agency scrutiny, the need for established client relationships—but post-catastrophe capital formation remains a recurring feature. New entrants have traditionally been well-capitalized and focused, but few survive long enough to build the relationships and analytical capabilities of established players.

Bargaining Power of Buyers: MODERATE TO HIGH

Primary insurers (the "buyers" of reinsurance) are sophisticated purchasers who can evaluate competing offerings. However, after major catastrophes, supply constraints can shift power toward reinsurers. RenaissanceRe's relationships with major cedents and brokers provide some insulation.

Bargaining Power of Suppliers: LOW

Reinsurers don't have traditional suppliers. Their key inputs are capital (sourced from shareholders and third-party investors) and talent (underwriters, modelers, actuaries). Capital is increasingly commoditized, while talent is scarce—making human capital the key supplier relationship to manage.

Threat of Substitutes: MODERATE

Insurance-linked securities, parametric insurance, and other capital markets products can substitute for traditional reinsurance. However, RenaissanceRe has embraced these alternatives through its Capital Partners platform rather than fighting them.

Competitive Rivalry: HIGH

RenaissanceRe, Everest Re, Arch Capital and PartnerRe all made the top tier in the 2025 AM Best rankings, with RenRe leading the local pack at number five globally. The Pembroke-based reinsurer increased gross premiums written to $12.3 billion, thanks in part to its acquisition of Validus Re. Everest Re and Arch Capital followed closely behind, posting $11.5 billion and $9.1 billion in gross premiums respectively.

Competition among major reinsurers is intense. However, RenaissanceRe's pure-play reinsurance focus, analytical capabilities, and capital efficiency provide durable differentiation.

Hamilton Helmer's 7 Powers Framework

Counter-Positioning: RenaissanceRe's third-party capital model represents meaningful counter-positioning. Competitors see the model working but face difficulty replicating it—building trusted relationships with institutional investors takes years, and pivoting capital structures creates near-term earnings dilution.

Scale Economies: Moderate. While larger balance sheets provide some advantage in taking large lines on major programs, RenaissanceRe has shown that superior risk selection can substitute for raw scale.

Network Effects: The third-party capital platform creates modest network effects—a larger platform attracts more institutional investors and provides access to more risk, making the platform more attractive to both sides.

Switching Costs: Meaningful in the reinsurance business. Cedents value long-term relationships, prompt claims payment, and capacity reliability—advantages established players like RenaissanceRe possess.

Branding: RenaissanceRe's brand carries weight with brokers and cedents as a sophisticated, well-capitalized, prompt-paying counterparty. This brand took decades to build.

Cornered Resource: The company's analytical talent and proprietary REMS technology represent scarce resources. The RenaissanceRe Risk Sciences unit's research capabilities in tropical cyclone, wildfire, flood, and seismic risk provide differentiated views of hazard.

Process Power: The underwriting process—how risks are evaluated, priced, and portfolio-managed—represents embedded institutional knowledge that's difficult for competitors to replicate.

Key Performance Indicators to Track

For investors following RenaissanceRe, three KPIs matter most:

1. Combined Ratio (and Adjusted Combined Ratio)

This is the fundamental measure of underwriting profitability. A combined ratio below 100% means the company makes money underwriting before investment income. RenaissanceRe's 83.9% combined ratio in 2024 was exceptional; sustainable performance in the low-to-mid 90s would still represent excellent underwriting.

2. Operating Return on Average Common Equity

This captures how efficiently management deploys shareholder capital to generate returns. RenaissanceRe's stated long-term target is 15%+ annual growth in tangible book value per share plus dividends. The 23.5% operating ROAE in 2024 significantly exceeded that target, though investors should expect more normalized results in average years.

3. Third-Party Capital Under Management and Fee Income

Growth in third-party AUM (now over $8 billion) and fee income (running above $100 million quarterly) validates the Capital Partners platform and provides earnings diversification. This metric captures a key differentiator versus competitors.

Myth vs. Reality

Myth: RenaissanceRe is a high-risk catastrophe bet that will eventually blow up.

Reality: The company has navigated Hurricane Andrew's aftermath, 9/11, Katrina-Rita-Wilma, and numerous other catastrophe years while delivering superior long-term returns. The third-party capital structure actually reduces balance sheet volatility by sharing catastrophe risk with institutional investors.

Myth: Bermuda reinsurers are tax arbitrage plays that will suffer from the new 15% corporate tax.

Reality: While the tax is a headwind, RenaissanceRe's competitive advantages stem from analytical capabilities and capital efficiency, not tax rates. The company was already paying meaningful taxes through U.S. BEAT provisions.

Myth: AI and alternative data will commoditize catastrophe modeling, eliminating RenaissanceRe's edge.

Reality: Proprietary modeling requires not just technology but decades of loss experience, relationships that provide granular exposure data, and organizational culture that integrates analytics into underwriting decisions. These are not easily replicated.

Risks and Regulatory Overhangs

Climate Change: Increasing frequency and severity of weather events challenges historical modeling assumptions. RenaissanceRe invests heavily in climate research, but model uncertainty is real.

Reserve Adequacy: Casualty reserves are inherently uncertain, and RenaissanceRe's growing casualty book following acquisitions introduces reserve risk that wasn't present in the property-focused historical business.

Key Person Risk: Kevin O'Donnell has been CEO since 2013 and with the company since 1996. Succession planning for the next generation of leadership will be important.

Tax and Regulatory Evolution: Beyond Bermuda's corporate tax, ongoing evolution in OECD Pillar Two minimum tax rules and potential U.S. tax changes could affect the competitive landscape.

Catastrophe Tail Risk: While third-party capital sharing mitigates this, an extraordinarily severe catastrophe year could still materially impact results and capital.

X. Conclusion: Three Decades of Renaissance

From a $140 million startup born in Hurricane Andrew's wake to a $12 billion revenue global reinsurer, RenaissanceRe's journey illustrates what's possible when analytical discipline, capital innovation, and strategic patience come together.

RenaissanceRe was formed in 1993 to address an identified market need, with differentiated capabilities in underwriting, service, responsiveness, and a unique ability to match capital to risk. We started with a handful of underwriters in one office and an idea to transform the property catastrophe market. Fast forward, we have grown and changed in many ways. We now write business from offices over three continents. Although a recognized leader in property catastrophe since our founding, we have moved successfully into casualty and specialty.

The company that Jim Stanard founded with a vision of bringing quantitative rigor to catastrophe underwriting has evolved under Kevin O'Donnell into a diversified reinsurance powerhouse—yet it remains true to its founding principles of analytical excellence and capital efficiency.

For investors, RenaissanceRe represents a differentiated way to access the reinsurance sector. The company has demonstrated an ability to compound book value at attractive rates through cycles, while the Capital Partners platform provides earnings diversification and capital efficiency that peers struggle to match.

The test going forward will be whether RenaissanceRe can maintain its analytical edge as technology evolves, integrate its acquisition-driven growth while preserving underwriting culture, and navigate an increasingly complex climate-risk landscape.

If history is any guide, the company that pioneered catastrophe modeling, invented the reinsurance sidecar, and transformed itself from a niche specialist to a global leader has earned the benefit of the doubt. In an industry where capital alone isn't enough, RenaissanceRe has proven that intellectual capital—the ability to assess risk better than competitors—creates durable competitive advantage.

The renaissance in catastrophe reinsurance that Jim Stanard envisioned in 1993 continues, thirty-two years later, in the company that bears its vision in its name.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube