ULTA Beauty: The American Beauty Democracy

I. Introduction & Episode Roadmap

Picture this: A strip mall in suburban Chicago, sandwiched between a Subway and a dry cleaner. Inside, a woman in scrubs on her lunch break tests a $50 Urban Decay eyeshadow palette while her teenage daughter grabs a $7 mascara from the drugstore section. In the back, someone's getting a blowout for tonight's date. This isn't Sephora. It's not CVS. It's not Nordstrom. It's ULTA Beauty—and this mundane scene represents one of the most successful retail stories in American history.

Here's the staggering fact that should make every investor pay attention: Since the depths of the 2009 financial crisis, ULTA has delivered a 7,000% return, making it the best-performing S&P 500 stock of that era. Today, this "strip mall beauty retailer" commands a market capitalization that exceeds Macy's, Kohl's, and Nordstrom—combined. Let that sink in. A company that started as five stores in Chicago suburbs now dwarfs the department store titans that once ruled American retail. The big question isn't just how ULTA got here—it's why a company selling lipstick and eyeshadow in strip malls could build a market capitalization of $23.14 billion, while department store icons languish with Macy's at $3.58 billion, Kohl's at $1.54 billion, and Nordstrom at $4.12 billion. Combined, these three retail legends command less than half of ULTA's valuation—a stunning reversal of retail's traditional hierarchy.

What follows is the unlikely story of how a former drugstore executive saw beauty differently: not as a luxury to be guarded behind glass counters, but as a democracy to be celebrated in the open aisles of suburban America. It's a story about timing, technology, and most importantly, the radical idea that prestige and mass could coexist under one roof. This is how ULTA Beauty rewrote the rules of American retail, one strip mall at a time.

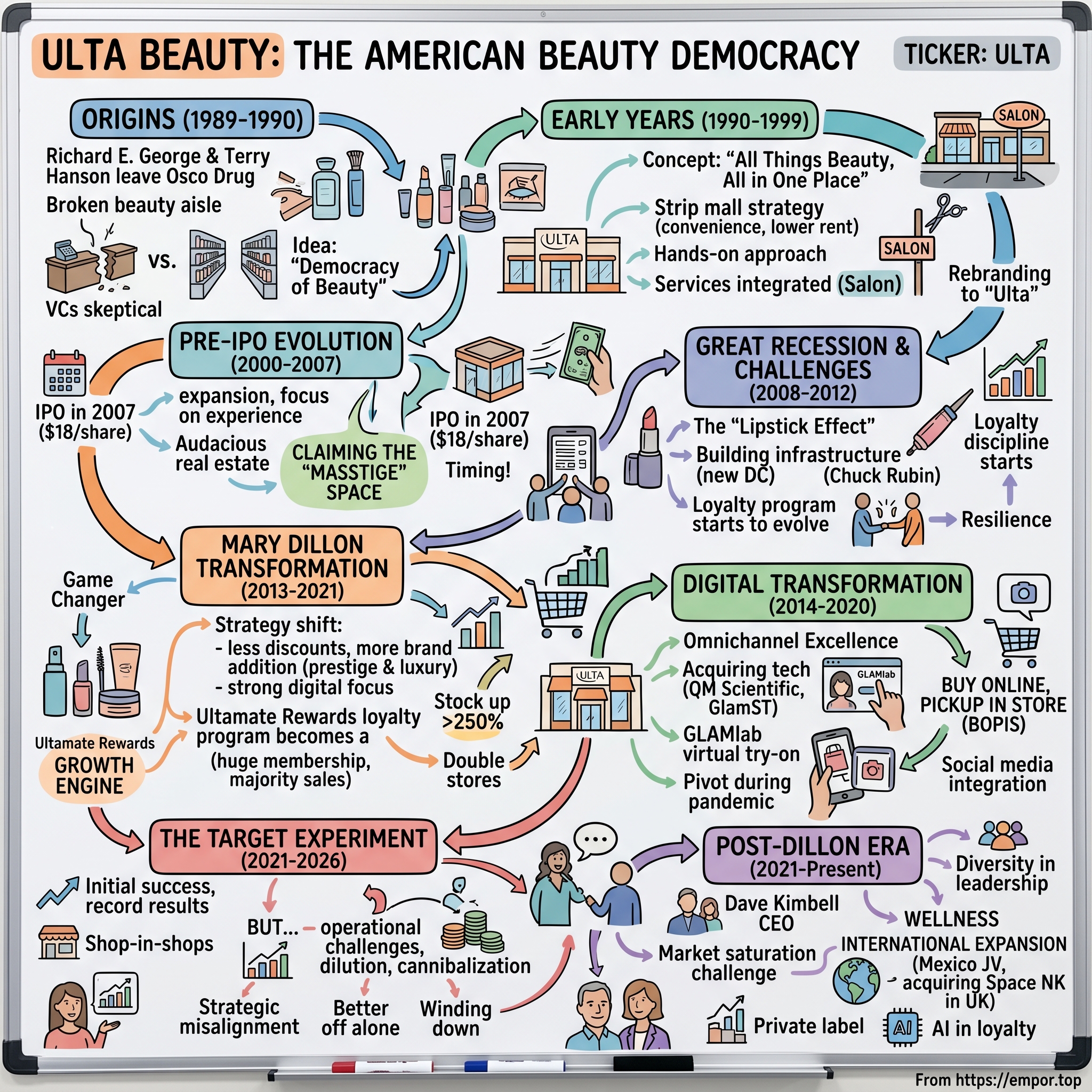

II. Origins & The Osco Drug Connection (1989–1990)

The year was 1989. The Berlin Wall was coming down, George H.W. Bush had just entered the White House, and in the fluorescent-lit offices of Osco Drug in Illinois, Richard E. George was having his Jerry Maguire moment—minus the goldfish. After years of running one of America's largest drugstore chains, George saw something his colleagues couldn't: the beauty aisle was broken.

Picture the landscape: If you wanted Clinique, you dressed up and went to Marshall Field's, where an intimidating woman in a lab coat would judge your pores. If you wanted Maybelline, you grabbed it at Walgreens next to the toilet paper. There was no middle ground. No place where a teenager could buy drugstore mascara and then splurge on Urban Decay eyeshadow with her birthday money. The industry had built a Berlin Wall of its own—prestige on one side, mass on the other—and George was about to tear it down.

George didn't leave Osco alone. He brought Terry Hanson, and together they embarked on what must have seemed like a quixotic quest: convincing venture capitalists that America needed a new kind of beauty store. Not a department store. Not a drugstore. Something entirely different—a beauty democracy where Chanel could sit three aisles away from CoverGirl, where you could touch and try everything without a salesperson hovering, where getting your hair done wasn't a separate trip to a separate place.

The pitch meetings must have been fascinating. "We're going to put $50 lipsticks next to $5 ones," they likely explained to skeptical VCs. "We're going to let customers touch everything. No counters. No territories. No commission-hungry salespeople pushing this month's quota." In an era when Estée Lauder wouldn't dare let their products sit near Wet n Wild, this was heresy. But George and Hanson weren't just challenging retail conventions—they were betting on a fundamental shift in how Americans thought about beauty, class, and consumption.

By early 1990, they had done the impossible: raised $11.5 million in venture capital for a concept that violated every rule of beauty retail. The money came from investors who saw what George saw—that American women were tired of the beauty caste system, tired of being judged at department store counters, tired of choosing between prestige and price. The company they created was called Ulta3—a name that sounds more like a failed startup than a future retail giant. The company, initially called Ulta3, was launched in 1990, with five stores in Chicago suburbs. The first of these opened at High Point Centre in Lombard, Illinois in early October 1990.

That first store in Lombard was sacred ground for the founding team. John Kromer, director of store operations and human resources, slept overnight in the Lombard store to protect it just before the grand opening. The alarm system had not yet been installed, and Kromer felt the building and stock were vulnerable, especially after a minor fire was lit in a dumpster the night before. This wasn't just a store opening—it was a revolution requiring bodyguards.

The revolutionary concept was deceptively simple yet profoundly disruptive: "All Things Beauty, All in One Place." But it wasn't just about product assortment. Each location has a beauty salon available to the public. This was the genius move that department stores missed—integrating services with retail, making beauty a destination rather than a transaction. While Macy's kept their salon separate from cosmetics, and drugstores wouldn't dream of cutting hair, Ulta3 said: why not both?

The timing was perfect. America in 1990 was experiencing a democratization of luxury across categories. This was the era of outlet malls, of Michael Kors bringing designer sensibility to the masses, of Starbucks teaching Americans to pay $4 for coffee. The old rules about what belonged where were crumbling. George and Hanson weren't just opening stores—they were surfing a cultural wave that would reshape American consumption patterns for the next three decades.

III. Early Years & Building the Model (1990–1999)

Ulta3 employees sell a variety of products and services and do not work on commission. Hanson participated in the design of the stores, down to the placement of light fixtures, shelves and displays. He and other managers would arrange the products on the shelves for attractive displays, usually before a grand opening. This hands-on approach—executives literally stocking shelves before grand openings—would become part of Ulta's DNA.

The strip mall strategy was counterintuitive but brilliant. While competitors fought for prime real estate in malls and downtown districts, Ulta3 deliberately chose locations next to grocery stores and dry cleaners. Why? Because that's where their customers already were—running errands, not making special trips. Beauty became part of the weekly routine, not a special occasion. Lower rents meant better margins. Ample parking meant easier access. The suburbs weren't a compromise; they were the point.

By 1995, the company had reached an inflection point. George left Ulta3, and Hanson became the company's Chief Executive Officer. George left Ulta3's top spot to became president and chief executive officer of Handy Andy, a home improvement discount chain. "I had a difference of opinion between the outlook and the direction (with) the board and the investors," George said. "I just felt it was better for them to have someone on line who would provide that direction. Terry (Hanson) is a natural."

This wasn't just a leadership change—it was a philosophical evolution. George, the visionary who broke down the walls, was replaced by Hanson, the operator who would build the infrastructure. The company began to shed its drugstore DNA, eliminating some of the typical drugstore items from their shelves, including vitamins and oral health products, such as toothpaste. The lines of cosmetics and fragrances increased. They also went for a more upscale look and added more space to the salon and areas to test the products. In December 1999, Lyn Kirby became the President and Chief Executive Officer and Charles "Rick" Weber became Senior Executive Vice President, Chief Operating Officer and Chief Financial Officer. This marked the beginning of what would become known as the Ulta transformation—though few could have predicted the magnitude of change that was coming.

Kirby brought a new vision for what Ulta could become. When Lyn Kirby, the company's current President and Chief Executive Officer, joined in December 1999, Ulta embarked on a multi-year strategy to transform from a discount beauty retailer into something entirely different. The company had reached about 70 stores by then, but Kirby saw potential for something much bigger. She created what she called the "four E's": providing an experience for women by providing them with entertainment, education, escape, and aesthetics.

The company also underwent a critical rebranding at the end of 1999—dropping the "3" to become simply "Ulta." It was more than cosmetic. The new name signaled a new ambition. This wasn't a third option anymore—it was becoming its own category. As the millennium turned, Ulta stood at the precipice of transformation, with new leadership, new vision, and a strategy that would either revolutionize beauty retail or become another footnote in retail history.

IV. The Pre-IPO Evolution (2000–2007)

The early 2000s were Ulta's chrysalis years—a period of intense metamorphosis that would determine whether the company could transcend its discount roots to become something unprecedented in American retail. Under Kirby's leadership, the company embarked on an ambitious expansion beyond its Chicago stronghold, opening stores across Minnesota, Georgia, Texas, Arizona, and Colorado. But this wasn't just geographic growth—it was a complete reimagining of what a beauty store could be.

The transformation from Ulta3 to "Ulta Salon, Cosmetics & Fragrance Inc." wasn't merely nomenclature—it was a statement of intent. Kirby understood that the future of beauty retail wasn't just about products on shelves; it was about creating a destination. The salon component, which had been part of the concept from day one, became increasingly central to the value proposition. While Sephora was teaching customers about products, Ulta was actually doing their hair, nails, and makeup. It was experiential retail before anyone called it that.

The competitive landscape during this period was treacherous. Department stores still dominated prestige beauty, controlling distribution through exclusive deals and territorial agreements. Sephora, owned by luxury conglomerate LVMH since 1997, was aggressively expanding its U.S. footprint with a focus on the mall-based prestige consumer. CVS and Walgreens owned the mass market. Ulta was trying to claim territory that didn't technically exist—the space between mass and class.

What made Ulta's strategy particularly audacious was its real estate approach. While Sephora pursued prime mall locations and department stores clung to their anchors, Ulta deliberately chose power centers and strip malls. These weren't glamorous locations, but they were convenient—situated where women already shopped for groceries, picked up dry cleaning, and ran errands. Beauty became part of the routine, not a special trip.

By 2007, the company had grown to approximately 200 stores and was generating enough revenue to attract serious attention from public markets. The timing for an IPO seemed perfect: the economy was booming, consumer spending was strong, and the beauty industry was showing remarkable resilience. But the company faced a critical question: could a beauty retailer that had built its reputation on accessibility and value command respect from Wall Street? On October 25, 2007, the company became publicly traded on the NASDAQ. The initial public offering was priced at $18.00 per share. The company raised the estimated price for its IPO of about 8.5 million shares to a range of $17 to $18 a share from $14 to $16 a share—strong demand pushed the pricing higher than initially anticipated. Ulta said it expects net proceeds from the IPO to be about $121.2 million.

The timing couldn't have been worse—or, in retrospect, better. Ulta went public just as storm clouds were gathering over the American economy. Within months, Bear Stearns would collapse, Lehman Brothers would fail, and the global financial system would teeter on the brink. But this crisis would prove to be Ulta's crucible—the test that would either destroy the company or forge it into something stronger.

V. The Great Recession & Post-IPO Challenges (2008–2012)

If going public in October 2007 seemed like perfect timing, by March 2008 it looked like corporate suicide. The stock that opened at $32.63 would soon plummet as the financial crisis devastated retail. Department stores hemorrhaged sales. Specialty retailers shuttered locations. Yet something curious happened at Ulta: women kept buying beauty products. They might skip the new outfit, but they still bought mascara. This was the "lipstick effect" in action—the phenomenon where consumers maintain small luxuries during economic downturns.

In 2008, Ulta also opened a second distribution center in Phoenix, Arizona. While competitors were retrenching, Ulta was quietly building infrastructure for future growth. This Phoenix facility wasn't just about logistics—it was a statement of intent. The company was betting that the West Coast represented massive untapped potential, and they needed the operational capacity to serve it.

In 2010, Carl "Chuck" Rubin was appointed as chief operating officer, president, and as a member of the board of directors. Rubin brought operational discipline at a critical moment. While Kirby had transformed Ulta from discount retailer to beauty destination, Rubin would focus on execution—improving same-store sales, optimizing inventory management, and preparing the company for its next phase of growth.

The numbers tell a remarkable story of resilience. While department stores saw beauty sales decline during the recession, Ulta actually grew. The company opened stores at a measured pace, focusing on profitable locations rather than aggressive expansion. The strip mall strategy that once seemed downmarket now looked prescient—lower rents meant better unit economics during tough times.

But the most important development during this period was the evolution of Ulta's loyalty program. While the program had existed since the early 2000s, the recession years saw it transform from a simple points system into a sophisticated data-gathering and customer retention machine. As customers became more value-conscious, the ability to offer targeted promotions and rewards became a critical competitive advantage.

By 2012, Ulta had emerged from the recession not just intact but strengthened. The company has created 22,000+ jobs created across the country. The company had proven that its model could withstand economic turbulence. More importantly, it had demonstrated that beauty retail wasn't just about selling products—it was about creating an experience that customers valued even in tough times. The stage was set for transformation, but it would take new leadership to fully realize Ulta's potential.

VI. The Mary Dillon Transformation (2013–2021)

On June 24, 2013, it was announced that Mary Dillon would be appointed as Chief Executive Officer and a member of the Board of Directors, effective July 1, 2013. The announcement sent shockwaves through the retail world. Here was a CEO with zero beauty industry experience since working at an Osco cosmetics counter at age 16. Dillon was global chief marketing officer and executive vice president of McDonald's from 2005 to 2010. She was CEO and president of U.S. Cellular from 2010 to 2013. A telecom executive running a beauty retailer? Wall Street was skeptical.

But the board saw something others missed. "Mary brings strategic vision, a rich consumer marketing background, strong operational experience, and a passion for the customer," said Dennis Eck, Interim Chief Executive Officer. "Her experience with developing national brands, her expertise in the digital world, and her track record in building strong teams will all be important assets."

Dillon herself was initially hesitant. "Ulta was not even on my radar" when she was approached about the gig in 2013, she later told Fortune. But when CEO Mary Dillon joined Ulta in 2013, she saw a company that was already growing well. It had solid product assortment, services and real estate—it was simply underinvested for the future. It needed to strengthen its digital components.

The transformation began immediately. Six months into her tenure, on Christmas Eve 2013, Dillon worked a six-hour shift at an Ulta store near Salt Lake City during a family ski holiday. She found herself overwhelmed by questions about the 20,000 different products Ulta sells. "The only thing I was qualified for was handing out shopping bags," she recalls. But that experience taught her something crucial: customers were drowning in complexity, particularly around coupons and promotions. Dillon repositioned the brand, putting new stores closer to urban centers and investing in technology to deliver online orders more efficiently. Before Dillon's arrival, Ulta was known for its abundance of discounts and coupons. She has edged away from that blunt-force strategy, instead incentivizing customers to join the loyalty program. The program's 21.7 million active members now generate more than 90% of Ulta's overall sales.

The transformation under Dillon was comprehensive. Dave Kimbell and Dillon have introduced 200 new brands, including luxury lines like Estée Lauder, Clarins, and Jessica Alba's Honest Beauty. This wasn't just about adding brands—it was about changing perception. Prestige brands that once wouldn't dream of being sold next to drugstore makeup now saw Ulta as essential to reaching younger consumers.

The loyalty program became the engine of growth. Membership in the company's Ultamate Rewards loyalty program has grown by 64.8% over three years, from 18.2 million members in 2015 to 30 million members as of November 2018. By 2024, the program would reach 44.4 million active members, with 95% of every dollar that comes through the company coming from members. Ulta's stock is up more than 250% since Dillon became CEO, and its market capitalization now exceeds $15 billion, towering over retailers like Macy's, Kohl's, and Nordstrom. During Dillon's tenure as CEO, Ulta's stock more than tripled. The company doubled its number of stores to upwards of 1,200, and it joined both the S&P and Fortune 500 listings.

The digital transformation was equally dramatic. Ulta invested in marketing across channels, such as television and social media. This was a particularly important move for Ulta, since beauty is the second most popular type of tutorial on YouTube. E-commerce sales grew 72.3 percent in the second quarter of 2017 alone. The company fortified its e-commerce sector, and it has since then kept growing from a 2014 sales goal of five percent to almost 50 percent each year.

But perhaps Dillon's greatest achievement was cultural. She transformed Ulta from a discount beauty retailer into a beauty democracy—a place where a teenager could buy drugstore mascara alongside her mother purchasing La Mer moisturizer, where beauty wasn't about judgment but discovery. Under her leadership, net sales growth would continue, maintaining a 20% or higher growth rate from 2013 to 2017.

By 2021, as Dillon prepared to step down, she had built something remarkable: a company that had proven beauty retail wasn't just recession-resistant but could thrive through technological disruption, changing consumer preferences, and even a global pandemic. The foundation was set for the next chapter, but first, Ulta would have to navigate the digital revolution that was reshaping all of retail.

VII. Digital Transformation & Omnichannel Excellence (2014–2020)

The beauty industry in 2014 was having its Kodak moment. Instagram had just crossed 200 million users, YouTube beauty tutorials were exploding, and a new generation of digitally-native brands like Glossier were being born in Brooklyn lofts rather than corporate labs. Traditional retailers were scrambling to understand this new world. Ulta, under Dillon's leadership, decided not just to adapt but to lead.

The first major move came through acquisition. Ulta acquired QM Scientific and GlamST—two technology companies that most Wall Street analysts had never heard of. These weren't flashy deals, but they were strategic masterstrokes. QM Scientific brought personalization capabilities, while GlamST offered virtual try-on technology. While competitors were outsourcing their digital transformation, Ulta was building tech capabilities in-house.

The investment in digital wasn't just about e-commerce—it was about reimagining the entire customer journey. The company launched GLAMlab, a virtual try-on experience that let customers test products digitally before buying. They introduced "Buy Online, Pickup in Store" when many retailers were still debating whether online and offline should compete or collaborate. Each store became a mini-fulfillment center, with employees picking online orders between helping in-store customers.

Social media became Ulta's secret weapon. Beauty is the second most popular type of tutorial on YouTube, and Ulta didn't just advertise on these platforms—they became part of the conversation. They partnered with influencers before "influencer marketing" was a budget line item. They turned their loyalty members into content creators, encouraging them to share looks and reviews. The traditional beauty counter conversation moved online, scaled infinitely.

The numbers told the story: e-commerce sales grew from representing less than 5% of revenue in 2014 to nearly 20% by 2019. But more importantly, digital wasn't cannibalizing stores—it was enhancing them. Customers who engaged with Ulta online and in-store spent 2.5 times more than single-channel shoppers. The company had cracked the omnichannel code that eluded so many retailers.

Then came 2020. The COVID-19 pandemic should have been catastrophic for a retailer dependent on customers trying products in-store. In 2020 before the COVID-19 pandemic there were 44,000 employees. Stores shuttered. Makeup sales plummeted as Zoom calls made lipstick irrelevant. As of 2021, Ulta employs approximately 37,000 people. The company had to furlough thousands.

But the digital infrastructure Dillon had built over six years became Ulta's lifeline. Curbside pickup, which would have taken months to implement in normal times, rolled out in weeks. Virtual consultations replaced in-store makeovers. The app became a beauty advisor in everyone's pocket. While department stores struggled with outdated systems, Ulta pivoted with the agility of a startup. The pandemic didn't break Ulta's model—it accelerated its digital transformation by years. By the time stores reopened, Ulta had proven it could serve customers anywhere, anytime, through any channel.

VIII. The Target Partnership Experiment (2021–2026)

In August 2021, two titans of American retail made an announcement that sent shockwaves through the industry: Ulta Beauty would open shop-in-shops inside Target stores. For Ulta, it was a chance to reach millions of new customers without the capital expense of new stores. For Target, it was an opportunity to elevate its beauty offering and drive traffic. On paper, it was brilliant. In reality, it would become one of the most fascinating experiments—and cautionary tales—in modern retail.

The partnership, launched in 2021, allowed Ulta to place its mini-beauty shops in over 600 Target locations, alongside online integration. These weren't just beauty aisles—they were 1,000-square-foot Ulta experiences, complete with trained beauty advisors and prestige brands that had never before appeared in a Target. The initial results were spectacular. Ulta Beauty shows record-breaking results for 2021, with sales up 40% and profits up 461%. The company saw a net profit of $985.8 million over the previous year's $178 million. William Blair estimates that by the end of 2024 financial year, revenue from Target shop-in-shops reached $465 million, a 16 percent increase on the previous year, representing around 4 percent of Ulta Beauty's total revenue. The numbers looked good on paper, but beneath the surface, cracks were forming.

The fundamental problem was overlap. Despite initial success, Ulta Beauty's shop-in-shop partnership with Target never reached its goal of 800 stores, and top-line revenue decreased as store openings slowed. The collaboration struggled as the two retailers overlapped in customer profile and geography. While Sephora's partnership with Kohl's worked because they served different markets—Sephora in urban malls, Kohl's in smaller markets—Ulta and Target were often competing for the same suburban customer, sometimes just minutes apart.

Operational challenges compounded the strategic misalignment. Employee feedback highlighted issues such as understaffing, shoplifting, and cannibalization of foot traffic between Ulta's standalone stores and the Target locations. What started as sharp execution descended into operational chaos—haphazard merchandising, out-of-stock products, and anti-theft measures that made the shopping experience feel more like a prison commissary than a beauty destination.

The company disclosed that the wind-down is not expected to affect its 2025 results or long-term targets, with royalty revenue from the partnership accounting for less than 1% of its total revenue. This revelation was telling—what had been positioned as a transformative partnership was actually a rounding error on Ulta's financials. Why the partnership ended: Operational challenges, brand dilution, and strategic misalignment all played roles, but ultimately, both companies realized they were better off alone.

The Target partnership experiment taught valuable lessons about the limits of retail collaboration. Not every partnership creates value, even when both brands are successful independently. Sometimes, maintaining focus on core strengths trumps the allure of new distribution channels. For Ulta, the future lay not in piggybacking on another retailer's footprint but in international expansion and digital innovation.

IX. Post-Dillon Era & Current Strategy (2021–Present)

When Dave Kimbell, president, succeeded Mary Dillon as chief executive officer in June 2021, Wall Street was skeptical. The stock dropped 8.5% on the announcement, with analysts fretting about timing—would Kimbell be able to maintain the explosive growth Dillon had delivered? The concern was understandable. Kimbell had worked alongside Dillon since their days together at U.S. Cellular a decade ago, where he was chief marketing officer and executive vice president. He joined Ulta Beauty in 2014, a year after Dillon, as chief marketing officer, and with Dillon, has helped the retailer more than double sales and store count over the last eight years.

Kecia Steelman, the retailers' current chief store operations officer, assumed the role of chief operating officer where she would oversee store and services operations, supply chain, Ulta Beauty at Target and other key initiatives. The new leadership team was notably diverse—60% women and 20% people of color—reflecting Ulta's commitment to representation both in leadership and on shelves.

The post-Dillon era began with ambitious plans but soon faced reality checks. With 1,325 stores across the country, Ulta has nearly exhausted its geographic growth opportunities. New store openings have dropped from 100 annually under Dillon to a goal of 50 for Kimbell. The challenge was clear: how to grow when you're running out of America?

As of January 28, 2023, Ulta had some 1,355 stores across all 50 states with about 250 of those stores located inside Target stores. By 2024, the company was generating over $11 billion in annual revenue, but growth was moderating. The beauty industry's post-pandemic surge was normalizing, competition from Sephora was intensifying, and the Target partnership was proving more problematic than profitable.

The answer came in 2024: international expansion. In 2025, Ulta Beauty announced its expansion into the Mexican market through a joint venture with the retail group Axo, marking its first international operation outside the United States. This wasn't Ulta's first attempt at going global—plans to enter Canada had been announced in 2019 but were abandoned during the pandemic. This time, however, the approach was different.

Dave Kimbell explained: "International expansion represents an incremental, long-term opportunity for Ulta Beauty to extend our reach and leverage our differentiated value proposition. We have evaluated various operating models and partners, and geographies, and we are excited to announce the formation of a joint venture with Axo, a highly experienced operator of global brands, to launch and operate Ulta Beauty in Mexico in 2025".

The Mexico strategy represented a new playbook for Ulta. Mexico has a very young population with nearly 50% of the population being under the age of 29 years old. Secondly, the middle class continues to show strong growth as Mexico develops as a nation. This is advantageous for Ulta not only because they boast an assortment that spans the full range of price points (from mass to prestige) but also because there are not as many strong beauty competitors catering to the masstige price points in MX.

But Mexico was just the beginning. In 2024, Ulta made an unexpected move that shocked the industry: Ulta acquired Space NK in early July for an undisclosed sum. As part of the deal, Space NK, which has 83 stores in the U.K. and Ireland and turnover of 196.5 million pounds in 2024, will operate as a stand-alone subsidiary of Ulta and will continue to be led by its existing management team. The acquisition gave Ulta instant access to the British market with an established premium beauty retailer.

The wellness pivot represents another frontier for growth. Beauty is increasingly blurring with wellness—from adaptogenic skincare to CBD-infused products to beauty supplements. Ulta has been quietly expanding these categories, recognizing that the future consumer doesn't distinguish between looking good and feeling good. The company has introduced meditation apps, stress-relief tools, and holistic beauty brands that would have seemed out of place in a cosmetics store a decade ago.

Digital innovation continues under Kimbell, though perhaps without the revolutionary fervor of the Dillon years. The company launched UB Media, its retail media network, allowing brands to advertise directly to Ulta's massive customer base. The loyalty program, now called Ulta Beauty Rewards, continues to evolve with personalized offers powered by AI and machine learning. The company aims to grow its loyalty program to 50 million members by 2028, up from 43.9 million in its most recent quarter. In 2021, Ulta's definition of "beauty enthusiasts" included women aged 18+, which amounted to some 70 million possible loyalty members. Now, men are also a part of the definition, as are younger generations, opening up a possible 140 million "beauty enthusiasts" that Ulta could attract.

Yet the post-Dillon era has also been marked by strategic retreats. The Target partnership wind-down, while positioned as mutual, represents an acknowledgment that not all growth strategies work. The competitive environment has intensified, with Sephora aggressively expanding (now with over 2,700 locations globally compared to Ulta's 1,400+), Amazon becoming a major force in beauty, and countless DTC brands bypassing traditional retail entirely.

Looking ahead, Ulta faces a complex landscape. Kimbell acknowledged the challenges: "While beauty has continued to expand and evolve, we remain true to our core purpose—we champion beauty for everyone, helping every guest discover their own possibilities through the power of beauty". The company has set ambitious targets: 200 net new stores over the next three years, targeting 1,800+ stores over the long-term, and 4% to 6% net sales growth and "low double-digit" diluted earnings-per-share growth for 2026 "and beyond".

X. Business Model Deep Dive

Understanding Ulta's business model requires dissecting an economic engine that turns lipstick into liquidity with remarkable efficiency. At its core, Ulta operates on a deceptively simple premise: aggregate demand across price points, minimize inventory risk through vendor partnerships, and maximize customer lifetime value through data-driven loyalty programs. But the execution is anything but simple.

Start with the economics of beauty retail. The beauty industry enjoys gross margins that would make most retailers weep with envy—typically 35-40% for Ulta compared to 25-30% for general merchandise retailers. These margins are possible because beauty products combine high perceived value with relatively low manufacturing costs. A $50 face cream might cost $5 to produce, creating margin structures that can absorb promotional activity while still delivering profitability.

Merchandise inventories at the end of fiscal 2023 increased 8.6% to $1.7 billion. The increase was primarily due to inventory to support new brand launches, 30 net new stores, increase in distribution center inventory primarily due to the opening of the new market fulfillment center in Greer, SC, and product cost increases. This inventory management is crucial—beauty products have expiration dates, trend cycles are increasingly compressed, and the wrong shade of foundation is worthless inventory.

The company offers more than 20,000 products from over 500 well-established and emerging beauty brands across all categories and price points, including Ulta Beauty's own private label. This massive SKU count would be a nightmare for most retailers, but Ulta has turned it into an advantage through sophisticated inventory management systems and vendor partnerships that often operate on consignment or scan-based trading models.

The real genius of Ulta's model lies in its loyalty program economics. With 43.9 million members generating 95% of sales, Ulta has essentially created a subscription business without charging a subscription fee. The data generated from these members—purchase history, browsing behavior, response to promotions—creates a feedback loop that improves everything from inventory planning to store locations.

Consider the customer acquisition cost (CAC) versus lifetime value (LTV) equation. While Ulta doesn't publicly disclose these metrics, industry analysis suggests CAC in the $25-40 range with LTV exceeding $500 for active loyalty members. This 12-15x LTV/CAC ratio is exceptional in retail, rivaling software companies. The loyalty program acts as both a retention mechanism and a margin protector—members are less price-sensitive because they're accumulating points toward future purchases.

The real estate strategy deserves special attention. The average investment in a new location is $2.1 million, with first-year sales typically $4.1 million. The payback period for those new sites is three to four years. These economics are possible because of Ulta's strip mall strategy—lower rents, easier access, ample parking. While Sephora pays premium rents in malls, Ulta's average rent is estimated at $20-25 per square foot compared to $50-100 for prime mall locations.

The service integration—salons in every store—transforms the business model in subtle but important ways. Services drive traffic (customers visit every 6-8 weeks for hair services versus every 2-3 months for product purchases), increase dwell time (a haircut takes an hour, creating browsing opportunities), and build emotional connection (your stylist becomes your beauty advisor). Services typically generate 5-10% of store revenue but contribute disproportionately to customer retention and basket size.

Private label represents the holy grail of retail—complete control over pricing, promotion, and profit margins. The Ulta Beauty Collection, launched in 2016, now encompasses over 1,000 SKUs across makeup, skincare, and tools. With margins estimated at 60-70% compared to 35-40% for third-party brands, private label products are margin accelerators. More importantly, they're exclusive—you can't buy them anywhere else, creating a competitive moat.

The omnichannel integration has transformed unit economics. Buy Online, Pickup In Store (BOPIS) orders have higher margins than pure e-commerce (no shipping costs) while driving incremental in-store purchases (60% of BOPIS customers buy additional items when picking up). Each store effectively becomes a micro-fulfillment center, with ship-from-store capabilities that reduce delivery times and costs.

The promotional strategy has evolved from heavy discounting to targeted personalization. The old model—20% off everything coupons sent to everyone—has given way to AI-driven offers tailored to individual purchase patterns. A customer who buys prestige skincare might get a free deluxe sample of a new serum, while a teen buying drugstore makeup receives points multipliers on trending TikTok brands. This precision reduces promotional waste while increasing relevance.

Working capital management in beauty retail is particularly complex. Payment terms with vendors typically range from 30-90 days, while inventory turns 4-5 times annually. This creates a cash conversion cycle that, when optimized, generates float—selling products before paying for them. Ulta's scale allows it to negotiate favorable terms that smaller retailers can't match, creating another competitive advantage.

Since 2014, Ulta Beauty has returned $5.8 billion to shareholders through its share repurchase program, while continuing to make strategic growth investments. On March 12, 2024, the Company's board of directors approved a new share repurchase authorization of $2.0 billion. This capital allocation strategy reflects the cash-generative nature of the business model—even while investing in growth, Ulta generates enough free cash flow to return billions to shareholders.

The model's resilience was tested during COVID and proved remarkably robust. While mall-based retailers struggled with extended closures, Ulta's strip mall locations could reopen faster. The diversified product mix—from $5 masks to $500 hair tools—allowed customers to trade up or down based on economic conditions. The integrated digital platform enabled pivoting to e-commerce when stores were closed.

XI. Playbook: Key Business Lessons

If Ulta's journey were distilled into a business school case study, it would challenge fundamental assumptions about retail, disruption, and competitive advantage. The lessons extend far beyond beauty, offering a masterclass in category creation, customer psychology, and strategic patience.

Democratization as Disruption: Ulta's core insight wasn't technological—it was sociological. The company recognized that the beauty industry's caste system (prestige in department stores, mass in drugstores) was an artificial construct that no longer reflected how consumers actually thought about beauty. By putting $5 mascara next to $50 mascara, Ulta didn't just change where products were sold—they changed what those products meant. The lesson: sometimes the most powerful disruption comes from challenging social conventions, not technical limitations.

The Power of Location: Ulta's strip mall strategy seemed like settling for second-best. Couldn't afford mall rents? Stick to strip malls. But this apparent weakness became a strength. Strip malls meant convenience, parking, and proximity to routine errands. Ulta made beauty part of the weekly grocery run, not a special trip to the mall. The lesson: in retail, being where your customers already are beats making them come to you.

Loyalty Program Excellence: Ulta's loyalty program isn't just a retention tool—it's a data engine, margin protector, and competitive moat rolled into one. With 95% of sales from members, Ulta knows what sells, to whom, and why. This data advantage compounds over time, improving everything from inventory management to site selection. The lesson: in the age of Amazon, data is the only sustainable competitive advantage in retail.

Leadership Transitions: The handoff from Dillon to Kimbell offers a textbook example of succession planning. Kimbell wasn't an outside savior brought in to transform the company—he was a longtime lieutenant who understood the culture and strategy. The transition was planned years in advance, with Kimbell gradually taking on more responsibilities. The lesson: the best succession plans are boring—gradual, planned, and preserving what works while evolving what doesn't.

Omnichannel Integration: While competitors treated online and offline as separate channels, Ulta recognized they were the same customer journey. A customer might discover a product on Instagram, research it on Ulta's app, try it in store, and buy it online for home delivery. Each touchpoint reinforces the others. The lesson: omnichannel isn't about technology—it's about recognizing that customers don't think in channels.

Brand Portfolio Management: Ulta's ability to merchandise across price points—from mass to prestige—requires sophisticated portfolio management. It's not just about having different price points but understanding the consumer journey. A teenager buying $7 drugstore mascara today might buy $30 prestige mascara in five years and $100 anti-aging serums in twenty. Ulta captures this entire lifecycle. The lesson: think about customer lifetime value not just in monetary terms but in evolving needs and aspirations.

The strategic patience Ulta has demonstrated is perhaps most instructive. The company spent 17 years as a private company before going public. It took 30 years to reach 1,000 stores. This wasn't sluggishness—it was discipline. Each phase built capabilities for the next. The lesson: in an era obsessed with blitzscaling, there's value in patient capital and measured growth.

The company's approach to innovation offers another lesson. Ulta has never been first—they weren't the first beauty retailer, the first to offer services, the first online, or the first with a loyalty program. But they've consistently been the best integrator, taking proven concepts and combining them in new ways. The lesson: innovation isn't always about invention—sometimes it's about integration.

The cultural component cannot be overlooked. From executives stocking shelves before grand openings to the CEO working store shifts, Ulta has maintained a connection to frontline operations that many retailers lose as they scale. This isn't just symbolic—it ensures leadership understands the reality of retail operations. The lesson: culture doesn't scale automatically—it requires deliberate reinforcement.

Risk management has been another strength. Ulta's expansion has been methodical, testing concepts in small batches before rolling out widely. The international expansion through partnerships rather than owned operations reflects this conservatism. Even the Target partnership, while ultimately unsuccessful, was structured to limit downside. The lesson: in retail, where margins are thin and mistakes costly, risk management is as important as growth strategy.

XII. Bear vs. Bull Case

Bull Case:

The bulls see Ulta as a uniquely positioned beneficiary of long-term beauty trends with multiple growth vectors and a proven execution track record. Start with the market itself—beauty has proven remarkably resilient across economic cycles, growing steadily even during recessions. The "lipstick effect" isn't just an anecdote; it's a documented phenomenon where consumers maintain small luxuries even when cutting back elsewhere.

Ulta's market position is formidable. As the largest specialty beauty retailer in the U.S., the company has achieved scale advantages that compound over time. Vendor relationships, real estate negotiations, technology investments, and marketing efficiency all benefit from scale in ways smaller competitors cannot match. The 43+ million loyalty members represent a moat that would take competitors decades and billions of dollars to replicate.

International expansion opens a multi-decade growth runway. The Mexico joint venture, UK acquisition through Space NK, and potential Middle East franchise represent just the beginning. The global beauty market exceeds $500 billion, and Ulta has barely scratched the surface outside the U.S. If the company can successfully export its model—even capturing a small share of international markets—it could double or triple its addressable market.

The wellness category expansion represents another massive opportunity. As beauty and wellness converge, Ulta is well-positioned to capture this $1.5 trillion global market. From CBD skincare to adaptogenic supplements to meditation apps, the definition of beauty is expanding, and Ulta's broad platform can accommodate this evolution better than narrow specialists.

Digital transformation continues to unlock value. The retail media network (UB Media) could become a high-margin revenue stream as brands pay for access to Ulta's customer data and marketing channels. With $11+ billion in sales running through its platform, Ulta could capture advertising revenues similar to Amazon's model, potentially adding hundreds of millions in high-margin revenue.

The demographic tailwinds are powerful. Gen Z and Alpha are more engaged with beauty than any previous generation, starting younger and experimenting more. Men's beauty is exploding, potentially doubling the addressable market. The aging population is spending more on skincare and anti-aging treatments. Every demographic trend points toward increased beauty consumption.

Bear Case:

The bears see a mature retailer facing structural headwinds in an increasingly fragmented market. Start with competition—it's never been fiercer. Sephora has LVMH's deep pockets and continues aggressive expansion. Amazon has become a major force in beauty, offering convenience and selection Ulta cannot match. Countless DTC brands are building direct relationships with consumers, bypassing traditional retail entirely.

Market saturation is a real concern. With 1,400+ stores in the U.S., Ulta is running out of prime locations. New store productivity has been declining, and comparable store sales growth is moderating. The law of large numbers suggests maintaining growth rates becomes increasingly difficult as the base grows.

The Target partnership failure raises questions about execution. If Ulta couldn't make a partnership work with one of America's most successful retailers, what does that say about international partnerships? The complexity of managing joint ventures and franchises across different markets and cultures could prove overwhelming for a company that has operated in one market for 35 years.

Margin pressure looms from multiple directions. Promotional intensity is increasing as competitors fight for market share. Labor costs are rising, particularly for the skilled aestheticians and stylists Ulta employs. Technology investments are necessary but expensive. Private label penetration has limits. The path to margin expansion is narrow.

Consumer behavior is evolving in potentially adverse ways. Younger consumers are increasingly buying directly from brands via social commerce. The influencer economy allows brands to bypass retailers entirely. Virtual try-on technology could make physical stores less relevant. If beauty follows fashion's trajectory, traditional multi-brand retailers could see their role diminished.

Execution risk in international expansion is significant. Retail history is littered with successful domestic retailers who failed internationally—from Walmart in Germany to Best Buy in Europe. Beauty preferences vary significantly by market. Operational complexity multiplies. Management attention gets divided. The risks are real and substantial.

The DTC threat deserves special attention. Brands like Glossier, Kylie Cosmetics, and Fenty Beauty have shown that powerful brands can build massive businesses without traditional retail. As more brands develop direct relationships with consumers, multi-brand retailers risk becoming showrooms where customers try products before buying directly from brands.

XIII. Epilogue & Looking Forward

Standing at the entrance of an Ulta store today—perhaps in a strip mall in suburban Dallas, sandwiched between a Chipotle and a nail salon—it's worth reflecting on the audacity of what Richard George imagined in 1989. He saw beauty not as a luxury to be guarded but as a democracy to be celebrated. That vision, refined and executed over 35 years, has created one of the most successful retail stories in American history.

The future of beauty retail will be shaped by forces Ulta cannot control but must navigate. Technology will continue its inexorable advance—AR try-on, AI personalization, social commerce, and innovations we cannot yet imagine. Demographics will shift—Gen Alpha will develop their own beauty values, different from Millennials or Gen Z. Cultural attitudes toward beauty, gender, and self-expression will continue evolving. Climate change will drive demand for sustainable beauty. Geopolitics will affect global expansion.

Yet Ulta's fundamental value proposition—"All Things Beauty, All in One Place"—remains remarkably relevant. The human desire to look and feel beautiful is timeless. The joy of discovery, the pleasure of transformation, the confidence that comes from finding the perfect shade—these experiences transcend technology and time.

The international expansion represents the next chapter in Ulta's story. Success is far from guaranteed. Mexico's beauty market differs from America's in countless ways. The UK acquisition of Space NK introduces complexity. The Middle East franchise will test Ulta's model in a vastly different cultural context. But the opportunity is immense—if Ulta can successfully internationalize, it could become the world's first truly global beauty democracy.

The wellness pivot could prove transformative. As the boundaries between beauty, health, and wellness blur, Ulta's broad platform positions it to capture this convergence. Imagine Ulta stores offering meditation classes, nutrition consultations, and hormone testing alongside traditional beauty services. The company that democratized beauty could democratize wellness.

Gen Z and Alpha represent both opportunity and challenge. These digital natives have different relationships with beauty—more experimental, less brand loyal, more values-driven. They discover products on TikTok, not in stores. They care about ingredients, sustainability, and social impact. Ulta must evolve to remain relevant while not alienating its core customer base.

The technology integration will accelerate. Virtual consultations, AI-powered skin analysis, personalized product formulation, same-day delivery—these aren't futuristic concepts but near-term realities. Ulta's ability to integrate technology while maintaining human connection will determine its relevance in the digital age.

The competitive landscape will continue intensifying. Amazon will get better at beauty. Sephora will expand more aggressively. New competitors will emerge from unexpected directions—perhaps a social media platform that vertically integrates into commerce, or a healthcare company that expands into beauty. Ulta's moat is strong but not impregnable.

Climate change and sustainability will reshape the industry. Consumers increasingly demand sustainable packaging, clean ingredients, and ethical sourcing. Refillable products, waterless formulations, and circular economy models will move from niche to mainstream. Ulta must navigate this transition while maintaining its value proposition and margins.

The lessons from Ulta's journey extend beyond beauty or even retail. It's a story about recognizing artificial barriers and having the courage to tear them down. About meeting customers where they are, not where you wish they were. About building a business model that aligns company success with customer success. About patient capital and measured growth in an era of growth-at-all-costs.

As we look forward, the question isn't whether Ulta will face challenges—it will. The question is whether the company can maintain the adaptability that has characterized its history. Can it evolve from an American beauty retailer to a global beauty platform? Can it navigate the digital transformation while maintaining its physical presence? Can it remain relevant to new generations while serving existing customers?

The beauty industry will continue growing and evolving. New categories will emerge—perhaps beauty supplements, genetic customization, or holographic makeup. New channels will develop—maybe shopping in virtual worlds or AI stylists that know you better than you know yourself. New values will shape consumption—sustainability, inclusivity, and authenticity will only grow in importance.

Through all these changes, one thing remains constant: the human desire for beauty, self-expression, and transformation. Ulta has spent 35 years serving this desire, democratizing access to beauty products and services that were once reserved for the privileged few. Whether the next 35 years will be as successful depends on Ulta's ability to continue evolving while staying true to its democratic ideals.

The strip mall in Lombard, Illinois, where Ulta opened its first store in 1990, has been redeveloped multiple times. The original store is long gone. But the idea born there—that beauty belongs to everyone—has proven more durable than bricks and mortar. It has survived recessions, technology disruptions, and global pandemics. It has created billions in shareholder value while serving millions of customers.

That first store may be gone, but its spirit lives on in 1,400+ locations across America and, soon, around the world. Each one a temple to the radical idea that you shouldn't have to choose between prestige and price, between service and self-service, between luxury and accessibility. Each one proof that in retail, as in life, the most powerful innovations often come not from technology or capital, but from recognizing a simple truth: beauty isn't a luxury—it's a democracy.

The Ulta story is far from over. New chapters are being written in Mexico City boardrooms, London beauty halls, and Silicon Valley tech labs. The company that revolutionized American beauty retail now seeks to transform global beauty retail. Success is not guaranteed—retail history is littered with companies that couldn't scale beyond their home markets. But if any company can democratize beauty globally, it might just be the one that started in a strip mall, selling drugstore mascara next to designer perfume, and called it a revolution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube