The Trade Desk: Building the Future of Digital Advertising

I. Introduction & Episode Roadmap

Picture this: It's September 21, 2016, and the NASDAQ opening bell rings for a company most people have never heard of. The Trade Desk, a seven-year-old advertising technology firm from Ventura, California, prices its IPO at $18 per share. By day's end, it's trading at $30.10—a 67% pop that signals something extraordinary is happening. Fast forward to today, and that $18 share is worth over $1,390. The company that started with two ex-Microsoft employees and a vision to democratize digital advertising has become the world's largest independent demand-side platform, with revenues approaching $2.4 billion in 2024.

But here's what's truly remarkable: The Trade Desk achieved this while competing directly against Google, Facebook, and Amazon—the titans who control over 70% of digital advertising. How did a second-time founder build what many call "the anti-Google" in adtech? How did they create one of the best-performing tech IPOs of the 2010s while remaining profitable from day one?

The answer lies in a contrarian bet: while everyone else was building walled gardens, Jeff Green was building bridges. While competitors hoarded data, The Trade Desk championed transparency. While Silicon Valley burned cash for growth, this Ventura-based company quietly printed profits. This is the story of how The Trade Desk became the Switzerland of digital advertising—neutral, trusted, and indispensable. We're building toward a comprehensive exploration of this enigmatic company—one that most consumers have never heard of, yet touches billions of advertising decisions daily. Q3 2024 revenues hit $628 million, up 27% year-over-year, accelerating from previous quarters and defying the broader adtech slowdown. This isn't just another tech growth story; it's a masterclass in building mission-critical infrastructure that even competitors depend upon.

Our journey will trace The Trade Desk from Jeff Green's formative experiences at Microsoft through the company's audacious bet on the open internet, its prescient pivot to Connected TV, and its emergence as the Switzerland of digital advertising. We'll explore how a company with just over 1% market share of the trillion-dollar advertising ecosystem became indispensable to brands spending billions, all while maintaining customer retention rates above 95%.

II. Origins: Jeff Green's Journey & AdECN

The salt-crusted highways of Utah shaped Jeff Green long before Silicon Valley knew his name. Born March 15, 1977 in Salt Lake City, Green's childhood was nomadic—his father's business of buying and selling companies meant the family moved constantly through Utah, Colorado, Kansas, Minnesota, and Rhode Island. While other kids played video games, young Green taught himself to code and build computers—an early sign of the builder's instinct that would define his career.

The paradox of Jeff Green begins with his education: a bachelor's degree from Brigham Young University in 2001, with a major in English literature and a minor in marketing and accounting, followed by a degree in marketing communications from the University of Southern California. Not your typical Silicon Valley engineering pedigree. After college, Green even got his securities broker license and spent a year working for an insurance company in investments—experiences that would later inform his understanding of marketplaces and financial systems.

Microsoft came calling when Green was working as a technical account manager, but it was his entrepreneurial leap in 2003 that changed everything. Green co-founded AdECN in 2003, pioneering programmatic trading in digital advertising. The company wasn't just another ad network—it was revolutionary. AdECN's technology served as a hub where advertising networks could come together in a neutral, real-time auction marketplace for buying and selling display advertising—a true ad exchange that was neutral, transparent, and automated.

The timing was prescient. Digital advertising in 2003 was still the Wild West—banner ads, pop-ups, and crude targeting dominated. Green saw what others missed: the future would be programmatic, automated, and data-driven. Bill Urschel, AdECN's CEO and co-founder, hired Green as the company's third sales hire after Green impressed him while buying media at a small L.A.-based agency called 411 Interactive. Green quickly became what colleagues called a "product driver," visionary, and nexus of energy in AdECN's halls.

On July 26, 2007, Microsoft announced it would acquire AdECN—a deal that would prove transformative for both Green and the industry. The acquisition price was rumored at $50-75 million, though it was overshadowed by Microsoft's simultaneous $6 billion acquisition of aQuantive. For Green, the Microsoft years from 2007 to 2009 became a masterclass in what not to do.

At Microsoft, Green became COO of AdECN Exchange. But his role expanded far beyond managing the exchange. He advised on strategy for the Online Services Division and oversaw all of Microsoft's reseller and channel partner business, which included the monetization of Facebook ads, Fox Sports, MSNBC, Hotmail and several other large Internet sites. This was heady stuff—Green was suddenly at the center of one of the world's largest digital advertising operations.

Yet frustration mounted daily. Microsoft's advertising division was a classic case of corporate dysfunction—multiple competing teams, unclear strategy, and most critically, an inherent conflict of interest. Microsoft wanted to be both a publisher (through MSN and other properties) and an infrastructure provider. They wanted to compete with Google while also partnering with the industry. The walled garden mentality was suffocating innovation.

Green watched as Microsoft struggled to integrate AdECN, saw brilliant ideas die in committee, and witnessed firsthand how the giants of tech were building moats rather than bridges. The contrast with AdECN's original vision—neutral, transparent, supportive of the entire ecosystem—couldn't have been starker. By 2009, Green had seen enough and left Microsoft to found a new company.

The lessons from AdECN and Microsoft crystallized into a clear vision: the advertising industry needed a truly independent platform, one that would never compete with its customers, never hoard data, and always prioritize transparency. The stage was set for The Trade Desk's founding—but first, Green needed to find the right partner and the right moment to strike.

III. Founding The Trade Desk (2009)

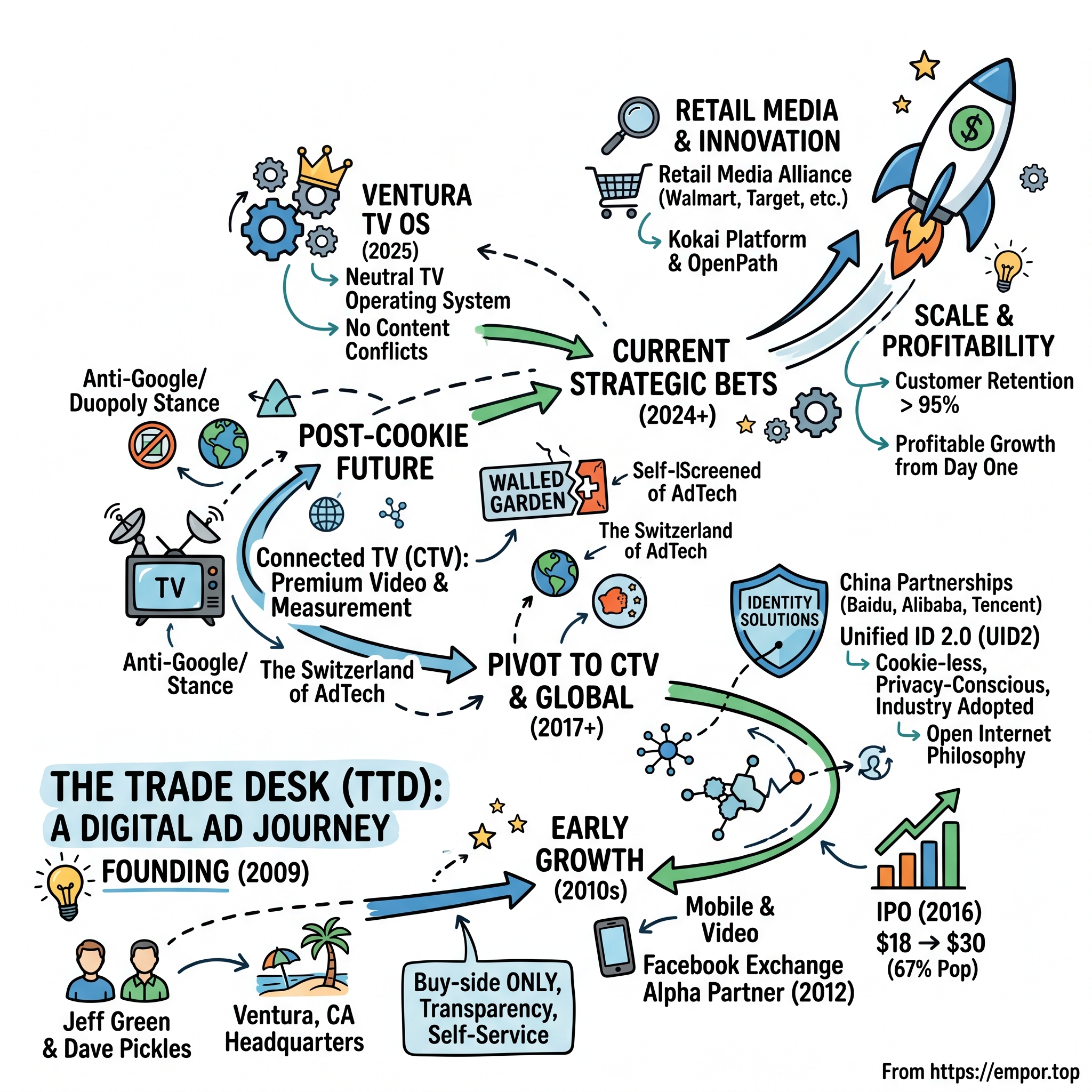

The Ventura sun was setting over the Pacific on a late summer evening in 2009 when Jeff Green and Dave Pickles sat in a small office space, mapping out what would become The Trade Desk. They'd both left Microsoft with something to prove: that advertising technology didn't have to be a zero-sum game where platforms extracted maximum value from both buyers and sellers. The Trade Desk was co-founded in 2009 by Jeff Green and David Pickles. They met at Microsoft after it had acquired Green's real-time digital advertising auction firm, AdECN, in 2007.

The location itself was symbolic. The Trade Desk is headquartered in Ventura, California. The company began operations in Ventura, California. Not San Francisco. Not Mountain View. Not Seattle. Ventura—a surf town an hour north of Los Angeles, known more for its beaches than its bytes. Green chose it deliberately. He wanted to build a different kind of company, one where engineers could afford houses, where work-life balance wasn't an oxymoron, and where the company culture wouldn't be infected by Silicon Valley groupthink.

Dave Pickles brought the technical gravitas that would transform Green's vision into reality. With a B.S. in Computer Science from UC Santa Barbara, Pickles had spent his entire career building real-time internet delivery systems. At Microsoft, after the AdECN acquisition, he'd led the development team that handled performance testing of 30 billion daily impressions—the kind of scale that would be crucial for what they were about to build. In his role as CTO, Pickles has overseen all aspects of the company's industry-leading demand-side platform, including engineering, product innovation and data science.

The founding vision crystallized around three core principles that would differentiate The Trade Desk from every other player in adtech. First, they would be purely buy-side—no conflicts of interest, no competing with their customers. Second, they would be radically transparent—every fee, every margin, every data point visible to clients. Third, they would be self-service—empowering advertisers and agencies with tools, not managing campaigns for them.

"When Jeff and I founded The Trade Desk 14 years ago, we shared a vision of a better way to price and buy digital advertising. Our amazing progress since then is testament to the incredible work of our product, engineering and data science teams," said Pickles. This wasn't just rhetoric. The programmatic advertising market in 2009 was ripe for disruption. Google had just acquired DoubleClick for $3.1 billion. Yahoo had bought Right Media. The giants were consolidating, creating walled gardens that trapped both advertisers and publishers.

But starting a company in late 2009 meant launching into the teeth of the Great Recession. Advertising budgets were slashed. Venture capital had dried up. Most rational people would have waited. Green and Pickles saw opportunity where others saw disaster. Advertisers desperately needed efficiency, transparency, and measurable ROI—exactly what programmatic promised.

The early days were brutal. Working from a modest office in Ventura, the founding team built the platform from scratch. No acquired technology, no shortcuts. Every line of code was purpose-built for their vision of what a demand-side platform should be. Green handled the business side—pitching agencies, building relationships, evangelizing the vision. Pickles led the technical charge—architecting a system that could evaluate millions of ad impressions per second while maintaining sub-100 millisecond response times.

The Trade Desk raised $2.5 million of venture capital in March, 2010. Investors included venture capital firms Founder Collective and IA Ventures, and angel investors Jerry Neumann and Josh Stylman. This seed funding was modest by Silicon Valley standards but transformative for The Trade Desk. It allowed them to hire their first engineers, expand the platform's capabilities, and most importantly, prove that their contrarian approach could work.

The decision to focus exclusively on the buy-side was revolutionary and risky. A crucial decision early on was committing exclusively to the buy-side of the advertising ecosystem. Unlike competitors who tried to serve both buyers and sellers, TTD focused solely on representing advertisers and agencies. This built trust and eliminated conflicts of interest, becoming a core differentiator. Every major competitor—Google, Yahoo, even Facebook—operated on both sides of the market. They sold inventory and provided buying tools. The conflicts were obvious to everyone but rarely discussed.

Green's pitch to early clients was simple but powerful: "We will never compete with you. We will never own media. We will never mark up media. We make money only when we help you buy better." This message resonated particularly with agencies who were tired of black-box platforms that obscured fees and margins. The Trade Desk's take rate would be transparent—a clear percentage of media spend, nothing hidden, nothing bundled.

The self-service philosophy was equally radical. Most DSPs in 2009 operated as managed services—agencies would hand over campaigns and budgets to platform operators who would optimize on their behalf. The Trade Desk flipped this model. They built tools that put control directly in the hands of media buyers. Yes, it meant more work for agencies initially, but it also meant unprecedented control and transparency.

By the end of 2009, The Trade Desk had its first clients, its core platform, and most importantly, proof that there was hunger in the market for an independent alternative. The programmatic revolution was just beginning, and The Trade Desk had positioned itself perfectly to ride the wave. The foundation was set for what would become one of the most remarkable growth stories in enterprise software.

IV. Early Growth & Product Evolution (2010–2015)

The cramped conference room in Ventura felt electric in early 2012. Jeff Green was on a call with Facebook's advertising team, and what he heard would change everything. Facebook was launching Facebook Exchange (FBX), their real-time bidding platform, and they wanted The Trade Desk as an alpha partner. By 2012, the company was included as an alpha partner in Facebook's launch of the real-time bidding (RTB) advertising platform, Facebook Exchange.

This was validation of the highest order. Facebook, the social media giant that everyone assumed would build everything in-house, was acknowledging they needed partners. More importantly, they chose The Trade Desk—a three-year-old startup—over established players with deeper pockets. "We think the early results from Facebook Exchange are very positive," said The Trade Desk CEO Jeff Green. "Our advertisers are excited to measure the impact of Facebook advertising on sales and ROI offline. The results to date have been impressive – one retailer is sourcing conversions at half the CPA they find on other inventory sources."

The early years from 2010 to 2015 were defined by relentless product iteration and trust-building with agencies. The initial focus on display advertising was pragmatic—it was where the money was. But Green and Pickles knew that display was just the beginning. Every quarter brought new channels, new formats, new capabilities. The platform evolved from handling simple banner ads to sophisticated multi-channel campaigns spanning display, mobile, video, and social.

Building trust with agencies required a radical departure from industry norms. Where competitors obscured their operations behind proprietary algorithms and black-box pricing, The Trade Desk opened the kimono. Agencies could see exactly what they were paying for media, what fees The Trade Desk charged, and how their campaigns performed at granular levels. This transparency wasn't just philosophical—it was architectural, built into every line of code.

The Facebook Exchange partnership exemplified The Trade Desk's strategic positioning. "In terms of RTB inventory, the Facebook Exchange is the most in demand right now," said Brian Stempeck, VP of Business Development at The Trade Desk. "It represents a huge amount of scale for any buyer running a retargeting or audience targeted campaign." While other DSPs scrambled to get access, The Trade Desk was already optimizing campaigns, building custom solutions, and demonstrating the power of programmatic on social inventory.

The pivot to mobile came faster than anyone expected. In 2010, mobile advertising was an afterthought—tiny screens, terrible targeting, minimal budgets. By 2013, it was existential. Smartphones were everywhere, and advertisers desperately needed to reach consumers across devices. The Trade Desk's engineering team worked around the clock to rebuild their bidding algorithms for mobile's unique constraints: limited bandwidth, different user contexts, and new ad formats.

Video advertising presented an even bigger opportunity. YouTube had proven that people would watch ads online, but the broader video advertising ecosystem was fragmented and inefficient. The Trade Desk built integrations with emerging video exchanges, developed new optimization algorithms for completion rates rather than clicks, and educated agencies on the nuances of programmatic video buying. By 2014, video was one of their fastest-growing channels.

The numbers told a story of explosive growth. Revenue grew from essentially zero in 2010 to $113.8 million by 2015—a compound annual growth rate that made venture capitalists salivate. But what was more impressive was that this growth came while maintaining positive EBITDA. In an industry where companies routinely burned millions to buy market share, The Trade Desk was printing cash.

In 2015, The Trade Desk was named among the top 10 of America's Most Promising Companies by Forbes. Founders Green and Pickles were also named as Ernst & Young Entrepreneurs of The Year 2015 in the Greater Los Angeles region. These accolades weren't just vanity metrics—they signaled to the market that The Trade Desk had graduated from promising startup to established player.

The customer list read like a who's who of global advertising. Omnicom, Publicis, WPP—the holding companies that controlled billions in ad spend—were all running campaigns through The Trade Desk. But equally important were the smaller, nimble agencies that saw The Trade Desk as their secret weapon against larger competitors. The platform democratized access to programmatic technology, allowing a five-person agency to access the same inventory and tools as a thousand-person firm.

Product evolution during this period was relentless. The team shipped new features weekly: algorithmic optimization models, cross-device tracking, attribution modeling, brand safety controls. Each feature was designed with a singular focus: give buyers more control and transparency. The philosophy was simple but revolutionary in adtech: treat advertisers like adults who could make their own decisions if given the right tools and data.

The talent density in Ventura was becoming legendary. Engineers who could work anywhere—Google, Facebook, Amazon—chose The Trade Desk. The culture Green and Pickles cultivated was unique: technically rigorous but not elitist, ambitious but not cutthroat, transparent internally just as they were externally. The Ventura headquarters, with its ocean views and surf-break proximity, became a recruiting advantage. Who wouldn't want to build world-class technology while living in paradise?

By the end of 2015, The Trade Desk had reached an inflection point. They had proven the model worked, built a world-class platform, and assembled a team that could compete with anyone. The question was no longer whether they could survive against the giants, but how big they could become. The stage was set for their next act: going public and proving to Wall Street that there was a different way to build an adtech company.

V. The IPO Story & Wall Street Validation (2016)

September 21, 2016. The morning fog had barely lifted from Ventura harbor when Jeff Green stood on the floor of the NASDAQ, watching the opening bell ceremony that would change everything. The Trade Desk became a public company with an $18 offering price. Within seconds of trading, the stock jumped to $28.75 per share—a nearly 60% surge that defied the conventional wisdom about adtech IPOs.

The decision to go public in 2016 was strategic brilliance wrapped in contrarian timing. The adtech sector was radioactive on Wall Street. Rocket Fuel had cratered. Tremor Video was struggling. YuMe was bleeding value. The narrative was clear: Google and Facebook had won, everyone else was roadkill. Investment bankers advised Green to wait, to let the market forget the adtech disasters. Green saw opportunity where others saw danger.

"This is a $640 billion industry that is in the very early stages of transforming," Chief Client Officer Brian Stempeck told investors. The pitch was simple but powerful: The Trade Desk wasn't just another adtech company. They were profitable—a rarity in Silicon Valley. Revenue had more than doubled year-over-year to $113.8 million in 2015. Customer retention was above 95%. This wasn't a growth-at-all-costs story; it was sustainable, profitable expansion.

The Trade Desk debuted on NASDAQ today at a price of $28.75 per share, up nearly 60 percent from its IPO price of $18. And while there wasn't a dramatic pop, it continued to climb and closed the day at $30.10 per share. The company's opening day was reported as a "vote of confidence for the demand-side platform, whose S1 filing revealed healthy financials: Triple digit revenue growth and profitability — rare in a sector that is seeing much of its growth chomped away by the duopoly Google and Facebook."

The S-1 filing had revealed something remarkable: The Trade Desk had cracked the code on unit economics in adtech. While competitors burned cash acquiring customers, The Trade Desk's platform approach meant that once an agency was onboarded, they stayed and grew their spending. The company had average days sales outstanding (DSO) of 88 days and average days payable outstanding (DPO) of 64 days—managing working capital efficiently despite the industry's notorious payment delays.

Being profitable at IPO was more than a financial achievement—it was a philosophical statement. In an era when Silicon Valley celebrated losses as investments in growth, The Trade Desk proved you could grow fast and make money. They'd achieved this through disciplined execution: keeping the team lean, focusing on product over marketing, and maintaining their Ventura headquarters instead of expensive San Francisco real estate.

The roadshow had been a masterclass in expectation management. Green didn't promise to kill Google or revolutionize advertising overnight. Instead, he laid out a methodical vision: capture more share of programmatic spending, expand internationally, move into new channels like Connected TV, and maintain the independence that made them valuable to agencies. It was boring by Silicon Valley standards—and that's exactly what Wall Street wanted to hear.

The investor base they attracted was telling. This wasn't a collection of momentum traders looking for a quick flip. The Trade Desk's early institutional investors included T. Rowe Price, Wellington Management, and Sands Capital—long-term, fundamental investors who understood the business model and believed in the secular shift to programmatic advertising. They saw what the market would eventually recognize: The Trade Desk wasn't competing with Google and Facebook; they were enabling everyone else to compete.

The dual-class structure was controversial but necessary. Green and the founding team maintained control through Class B shares with 10 votes per share, ensuring they could execute their long-term vision without quarterly pressure. Critics called it undemocratic. Green called it insurance against short-term thinking. Given what would come next—massive investments in Connected TV, identity solutions, and international expansion—that control would prove invaluable.

For the employees in Ventura watching the stock price tick higher throughout the day, it was validation of years of sacrifice. Many had taken below-market salaries in exchange for equity. The opening day performance meant those paper gains were real. But Green's message to the team was clear: this was the beginning, not the end. Going public meant more scrutiny, more pressure, and higher expectations.

The financial media's reaction was fascinatingly bifurcated. Tech publications focused on the competitive dynamics with Google and Facebook, questioning whether any independent player could survive. Financial publications saw something different: a rare profitable tech IPO with tremendous operating leverage. The Trade Desk had achieved what seemed impossible—they'd made adtech investable again.

The IPO raised $84 million for the company (before underwriter fees), providing capital for expansion without diluting the team's ownership significantly. But more importantly, it provided currency—public stock that could be used for acquisitions, employee retention, and strategic partnerships. The public market validation also strengthened their position with customers. Agencies could now point to The Trade Desk's market cap and financial stability when justifying platform decisions to clients.

By the end of that first trading day, The Trade Desk had a market cap of approximately $1.4 billion. An $18 investment in the IPO would eventually be worth over $1,390—a staggering 77-fold return that would make it one of the best-performing tech IPOs of the decade. But on September 21, 2016, no one knew what lay ahead. All they knew was that an adtech company from Ventura had just proved the doubters wrong. The question now was: what would they do with this newfound platform and credibility?

VI. Connected TV & The Future of Television (2017–Present)

The boardroom at Disney's Burbank headquarters was silent as Jeff Green finished his presentation in early 2017. The executives around the table—veterans who'd seen every pitch imaginable—were processing something unprecedented. Green wasn't just proposing to buy ads on their streaming inventory. He was suggesting they rebuild the entire economics of television advertising from the ground up. In 2017, The Trade Desk integrated connected TV buying and measurement directly into its platform.

This moment marked the beginning of The Trade Desk's most audacious bet: that streaming would completely replace linear television, and that programmatic advertising would be the engine that powered it. Seven years later, with CTV representing nearly 50% of The Trade Desk's business and the November 2024 announcement of Ventura—their own TV operating system—that bet looks prescient.

The Connected TV opportunity in 2017 was massive but messy. Netflix was still ad-free. Hulu was experimenting. Roku was primarily a hardware company. The inventory was fragmented, measurement was broken, and most advertisers still thought of streaming as a nice-to-have, not a must-buy. Green saw what others missed: this wasn't just another channel. It was the future of the $70 billion TV advertising market.

The Trade Desk's approach to CTV was characteristically contrarian. While competitors tried to force-fit display advertising tactics onto television, The Trade Desk rebuilt their platform from the ground up for the unique demands of premium video. They understood that a 30-second spot during Thursday Night Football wasn't the same as a banner ad—it required different targeting, different measurement, different optimization.

Building relationships with content owners became Green's personal mission. He flew to meetings with Disney, NBCUniversal, Paramount, and Warner Bros Discovery, making the same pitch: programmatic wasn't about commoditizing their content, it was about maximizing its value. By letting advertisers target specific audiences rather than broad demographics, publishers could charge premium CPMs while advertisers got better ROI. It was the holy grail of advertising—everyone wins.

In May 2024, Netflix announced its first expansion of its advertising partnerships to include The Trade Desk, Magnite and Google DV360. This partnership was seismic. Netflix, the company that had sworn off advertising for over a decade, was acknowledging that The Trade Desk had become too important to ignore. For Green, it validated years of patient relationship-building and platform investment.

But the real bombshell dropped in November 2024. The Trade Desk announced it has developed Ventura, an innovative new streaming TV operating system. Ventura, a nod to the company's headquarters in Ventura, California, will be rolled out to the market in the second half of 2025. The company has been working to build the system quietly for three years.

The Ventura announcement sent shockwaves through the industry. An adtech company building a TV operating system? It seemed insane. But Green's logic was impeccable: "Existing OS providers, like Roku, Amazon's Fire TV and Google's Android TV, have a conflict of interest because they own content," Green said. "We're looking at a concentration around a handful of players that lack objectivity. We think we're in a unique position to make the ecosystem better."

Ventura represents The Trade Desk's most ambitious project yet. Ventura solves key issues with prevailing market systems today, including frustrating user experiences, inefficient advertising supply chains, and content conflicts-of-interest. The major benefits include a more intuitive, engaging user experience, including cross-platform content discovery, personalization, subscription management, and ultimately fewer (more relevant) ads. A much cleaner supply chain for streaming TV advertising, minimizing supply chain hops and costs – ensuring maximum ROI for every advertising dollar and optimized yield for publishers.

The industry support for Ventura is telling. Jamie Power, SVP Addressable Advertising Sales at Disney Advertising said "As the streaming TV landscape rapidly evolves, we are entering a new paradigm for TV advertising. These trends are driven not only by consumer adoption but also by the innovation in the marketplace. We look forward to seeing The Trade Desk continue to drive innovation." John Halley, President of Paramount Advertising added "The Trade Desk has been a great partner and real innovator in the programmatic space, and we are excited to see them bring their approach to the OS marketplace. Both broadcasters and consumers will undoubtedly benefit."

Even hardware manufacturers are interested. Patrick Spence, CEO of Sonos said, "At Sonos, we are committed to providing our customers with the very best home entertainment experience. We are excited to explore the integration of premium audio and video with The Trade Desk and the Ventura OS."

The strategic brilliance of Ventura lies in its positioning. The Trade Desk has "no intention of getting into the hardware business." Rather, it will partner with other hardware companies, such as smart TV manufacturers, as well as various television distributors, such as airlines, hotel chains, and gaming companies, to bring its OS to their devices. This isn't about competing with Roku or Amazon—it's about providing an alternative for the long tail of devices that need a TV OS but don't want to hand control to a competitor.

The integration with Unified ID 2.0 is crucial. The Trade Desk's privacy framework, called Unified ID 2.0, will be part of Ventura. The Trade Desk incubated Unified ID 2.0, a cookie-less ad-targeting framework, several years ago as an alternative to internet tracking cookies. It's since been adopted by hundreds of publishers. By building identity into the OS layer, The Trade Desk can deliver the targeting precision advertisers demand while respecting consumer privacy.

The economics are compelling. CTV is the fastest-growing advertising channel in the U.S. It's projected to total $38.3 billion in 2024, per GroupM's latest forecast. By 2029, CTV is expected to overtake linear television in ad sales. CTV and video advertising represent nearly 50% of The Trade Desk's business. With Ventura, The Trade Desk isn't just riding the CTV wave—they're positioning themselves to control the infrastructure that powers it.

The risks are real. Building an OS is expensive, complex, and requires partnerships across the entire value chain. Roku, Amazon, and Google won't cede ground easily. But The Trade Desk has advantages: independence from content conflicts, deep advertiser relationships, and a reputation for innovation. Most importantly, they have patience. Like everything else at The Trade Desk, Ventura is a long-term bet on where the market is heading, not where it is today.

VII. The Open Internet Philosophy & Identity Solutions

The conference room at Google's Mountain View headquarters was tense in early 2020. Chrome's leadership team had just announced they would kill third-party cookies by 2022, and the advertising industry was in panic. Jeff Green sat across from a room full of anxious agency executives and made a bold declaration: "This isn't the end of the open internet. It's the beginning of something better." With initial development led by The Trade Desk, Unified ID 2.0 is a new industry-wide approach to internet identity that preserves the value of relevant advertising, while putting user control and privacy at the forefront.

The open internet philosophy wasn't just marketing—it was The Trade Desk's raison d'être. While Google, Facebook, and Amazon built higher walls around their gardens, The Trade Desk positioned itself as the Switzerland of digital advertising: neutral, trusted, and essential for everyone else. The company's unwavering bet on programmatic advertising and the open internet, rather than walled gardens like Google or Facebook, proved transformative.

The cookie apocalypse presented an existential threat to this vision. More and more internet usage now occurs in mobile apps and connected TV devices, where cookies are largely irrelevant and new identifying technologies have been developed. At the same time, major tech platforms such as Apple, Firefox and Google have all started to limit the use of third-party cookies on their web browsers. Without cookies, how would the open internet compete with the walled gardens' logged-in user bases?

Green's answer was audacious: build a better identity solution that the entire industry could adopt. Designed with the needs of modern marketers in mind, Unified ID 2.0 (UID2) provides holistic targeting and measurement for an internet that's becoming more privacy-conscious. By converting email and phone number data into hashed, salted identifiers, UID2s can serve as a superior signal to cookies in myriad ways.

The technical elegance of UID2 was matched by its philosophical clarity. UID 2.0 aims to fix that problem in several ways: Pseudonymization. A person's UID 2.0 contains zero information about who they are in the real world. Rather, a person's UID 2.0 is a string of numbers and letters that cannot be reverse engineered to an email address or any other form of identification. This wasn't about tracking users without consent—it was about creating a value exchange where consumers understood and controlled how their data was used.

Building industry consensus was the real challenge. Google had Chrome. Facebook had billions of users. The Trade Desk had... persuasion. Green personally met with every major publisher, advertiser, and technology platform, making the case that an independent identity solution was in everyone's interest. "Nielsen represents the gold standard in media data and measurement. Their support of Unified ID 2.0 is a significant step in advancing the value of the open internet," said Jeff Green, CEO of The Trade Desk. "As consumers embrace connected devices more than ever and TV becomes fully digitized, advertisers are looking for a new approach to identity that helps them measure across platforms in a way that puts the consumer in control. With industry-wide collaboration, Unified ID 2.0 accomplishes these objectives while preserving the value exchange of relevant advertising."

The coalition building was methodical. Publishers such as MediaVine and FuboTV are now part of the UID community, along with The Washington Post and their Zeus technology platform that powers over 100 other media publishers including some of the leading daily newspapers in the US. Nielsen, the gold standard in media measurement, is making Unified ID 2.0 a core element of their upgraded measurement portfolio.

The master stroke came in 2021 when The Trade Desk handed control of UID2 to Prebid.org, an industry nonprofit. Unified ID 2.0 named Prebid.org as operator, according to a press release, marking an important step as the solution races to become an alternative to the third-party cookie. As operator, Prebid will manage the technical backbone on which Unified ID runs, including hardware and software. The Trade Desk, which first created Unified ID, relinquishes oversight of the solution to Prebid as part of the move. This wasn't abandoning their creation—it was ensuring its independence and widespread adoption.

The technical implementation of UID2 was elegant in its simplicity. Unlike cookies, Unified ID 2.0 will require users to directly provide consent to a publisher by providing their email address before a publisher can create a UID2 identifier. Publishers will need to explain to the user the value-exchange of the open Internet and why creating a universal identifier for the ad tech ecosystem is crucial in providing the free content users have come to love.

The cross-channel capabilities of UID2 addressed the fragmentation problem that had plagued digital advertising. Unlike cookies, Unified ID 2.0 will operate across advertising channels. Advertisers will now be able to understand campaign performance across streaming TV, browsers, mobile, audio, TV apps and devices with a single ID, creating a stronger environment for precision and measurement. This is critical as marketers and publishers look to understand their audience across platforms in a simple way.

Competition from Google's Privacy Sandbox was fierce. In January, Google said that its Federated Learning of Cohorts (FLoC) technology — part of the company's Privacy Sandbox initiative — could drive at least 95% of the conversions marketers currently see with cookies. The claim has been met with some skepticism. But The Trade Desk had advantages: independence, industry trust, and a solution that worked across all browsers and devices, not just Chrome.

The philosophical battle lines were clear. Google argued for cohort-based targeting that kept data within Chrome. The Trade Desk championed individual-level targeting with explicit consent and user control. The industry's choice would determine the future of the open internet.

Fighting the walled gardens required more than technology—it demanded a narrative. The Trade Desk positioned itself as David against multiple Goliaths, the champion of agencies and publishers against the tech monopolies. Every product announcement, every partnership, every industry initiative reinforced this positioning.

The open internet philosophy extended beyond identity. It influenced every strategic decision: remaining independent rather than selling to a larger company, maintaining transparency in all operations, never competing with customers by owning media. These weren't just business decisions—they were statements of principle that resonated with an industry tired of conflicts of interest.

Pioneering Unified ID 2.0 represents another pivotal moment. Anticipating the deprecation of third-party cookies, TTD proactively developed and championed an alternative identity framework. This leadership solidified its role not just as a technology provider, but as a standard-setter shaping the future of digital advertising infrastructure, particularly critical as regulatory and browser changes unfolded through 2024.

By 2024, UID2 had achieved critical mass, with adoption across major publishers, measurement providers, and advertisers. The open internet had its identity solution. More importantly, The Trade Desk had proven that an independent player could lead industry-wide change. The cookie apocalypse that threatened to strengthen the walled gardens had instead created an opportunity for The Trade Desk to cement its position as the essential infrastructure of open web advertising.

VIII. International Expansion & Scale (2018–Present)

The Shanghai skyline glittered outside the conference room windows as Jeff Green prepared to make his pitch in late 2018. Across the table sat executives from Baidu, Tencent, and Alibaba—China's internet triumvirate. What Green was proposing seemed impossible: a foreign adtech company partnering with all three rivals simultaneously. Yet by the meeting's end, history was made. In 2018, the firm began investing heavily into the Asia Pacific region with the launch of its programmatic ad buying platform in China, giving access to Chinese media companies, such as Alibaba, Tencent and Baidu Exchange Services.

The China strategy was counterintuitive brilliance. While other Western tech companies tried to compete with local players or build their own operations, The Trade Desk positioned itself as a conduit—bringing foreign advertising dollars into China. The Trade Desk has been welcomed into China because they are not bringing a competing product into the country. Instead, through partnerships with global advertisers like Mazda, they are bringing ad-dollars into the country. This dynamic has led to recent partnerships with some of China's largest platforms, including Alibaba, Tencent Holdings, and Baidu.

The partnerships were unprecedented. The adtech firm has partnered with Baidu Exchange Services, Baidu-owned video platform iQIYI, Tencent Social Ads and Alibaba-owned video platform Youku. The new partnerships create access to inventory across display, mobile, video, and native advertising. For some partners, it was a historic moment. "Our partnership with The Trade Desk is our first partnership with an international demand-side platform. We value The Trade Desk's independence and objectivity and see this partnership as an important step in providing leading global brands access to millions of engaged consumers in China," explained Andy Sun, general manager of the programmatic business at iQIYI.

Building a global footprint required more than just market entry—it demanded localization without fragmentation. The Trade Desk now operates across 24 markets worldwide, but maintains a single, unified platform. This wasn't multiple regional products cobbled together; it was one global platform that could adapt to local requirements while maintaining consistency for multinational advertisers.

The approach to each market was surgical. Rather than blanket expansion, The Trade Desk identified markets where programmatic adoption was accelerating and regulatory environments were favorable. Japan came early, with its sophisticated digital advertising ecosystem. Southeast Asia followed, capitalizing on rapid smartphone adoption. Europe required careful navigation of GDPR and local privacy regulations. Each market brought unique challenges, but the core value proposition remained constant: independence, transparency, and performance.

Localizing for different markets while maintaining platform unity was a technical and operational feat. Currency support, language localization, local payment terms, regional data partnerships—each market required dozens of adaptations. But the genius was in what didn't change: the core platform, the user interface, the data models. A trader in Singapore could seamlessly manage campaigns in Germany, while a planner in London could optimize inventory in Tokyo.

Competition with Google internationally took on different dimensions. In some markets, Google's dominance was even more pronounced than in the U.S. In others, local players had carved out significant positions. The Trade Desk's strategy was consistent: partner rather than compete with local players, provide value that Google couldn't or wouldn't, and leverage their independence as a differentiator.

The Asia-Pacific expansion showcased this approach perfectly. Rather than trying to build direct relationships with thousands of local publishers, The Trade Desk partnered with regional exchanges and SSPs. They didn't try to replace local infrastructure; they enhanced it. Benson Ho, chief data strategy officer at Tencent Social Ads, noted: "Our high audience coverage and unique data insights are crucial for marketers wanting to understand consumers in China throughout their entire journey. Through our PMP integration with The Trade Desk, innovative global brands can more effectively reach and engage with this valuable audience."

The China opportunity was particularly tantalizing. Jeff Green believes China, which is currently the company's smallest market, will rapidly become its largest as the country becomes the largest advertising market in the world. The market's scale was staggering—over 900 million internet users, a rapidly growing middle class, and digital advertising spend growing at double-digit rates. But success required patience and cultural sensitivity.

The technical challenges of operating in China were immense. The Great Firewall meant data couldn't flow freely between China and other markets. Local regulations required data localization. The advertising formats, user behaviors, and campaign objectives were fundamentally different from Western markets. The Trade Desk built dedicated infrastructure, hired local teams, and created China-specific features while maintaining platform consistency.

The partnerships strategy in China was masterful. As an objective partner that doesn't own any media itself, The Trade Desk should continue to find success leveraging partnerships with large platforms to expand internationally. By working with all three major platforms—Baidu, Alibaba, and Tencent—The Trade Desk became the only DSP that could offer truly comprehensive reach in China for international advertisers.

Latin America presented different opportunities. Digital transformation was accelerating, programmatic adoption was in early stages, and there was hunger for sophisticated advertising technology. The Trade Desk entered markets like Brazil and Mexico with a playbook refined through years of international expansion: partner with local agencies, integrate with regional exchanges, provide extensive training and support.

The Middle East and Africa represented frontier markets with massive potential. Young populations, increasing smartphone penetration, and growing digital ad spend created opportunities for early movers. The Trade Desk's approach was measured—establishing presence in key hubs like Dubai and Tel Aviv, then expanding based on client demand and market maturity.

Cultural adaptation went beyond language and currency. In Japan, the emphasis on relationship-building meant months of meetings before deals closed. In Germany, privacy concerns required extensive documentation and compliance frameworks. In Brazil, payment terms and credit management required completely different approaches. Each market taught lessons that made the next expansion smoother.

The international expansion wasn't just about revenue diversification—it was strategic positioning for the future. As digital advertising becomes truly global, advertisers need partners who can execute seamlessly across markets. The Trade Desk's presence in 24 markets makes them indispensable for global campaigns. When a brand wants to launch simultaneously in New York, Tokyo, London, and São Paulo, The Trade Desk is one of the few platforms that can deliver.

By 2024, international markets represent a significant and growing portion of The Trade Desk's revenue. More importantly, the global footprint creates network effects—the more markets they're in, the more valuable they become to multinational advertisers, which attracts more inventory, which attracts more advertisers. It's a virtuous cycle that's extremely difficult for competitors to replicate.

IX. Culture, Leadership & Management Philosophy

The Ventura headquarters tells you everything about Jeff Green's leadership philosophy before you even walk through the door. No gleaming Silicon Valley campus. No Seattle skyscraper. Just a modest building blocks from the beach, where engineers can surf at lunch and still ship world-class code by dinner. The location choice wasn't accidental—it was a declaration of independence from tech orthodoxy.

Green's leadership style defies categorization. Part missionary, part mercenary, all intensity. Employees describe him as someone who can debate advertising philosophy for hours, then dive into database architecture details, then negotiate with Fortune 500 CMOs—all before lunch. His background—English literature major turned programmer turned CEO—created a leader who thinks in narratives but executes in code.

In April 2022, Green attracted note in the press for a $834 million pay package, much of which was in stock options. The headline number was shocking—the biggest CEO compensation package disclosed in 2021 across the S&P 500. But the structure revealed Green's philosophy: these weren't guaranteed payouts. For those stock options to become exercisable, The Trade Desk's stock would need to hit successively higher price targets, ranging from $90 a share to $340 a share, as well as other goals, such as beating most other companies on the Nasdaq 100.

The compensation controversy illuminated a crucial aspect of Green's leadership: he bets on himself and expects others to do the same. The Trade Desk noted in its SEC filing that Green and other executives "may never realize any value from their equity rewards," and the dollar amounts attached to them are "theoretical" number to this point. This wasn't extraction—it was alignment. Green would only get paid if shareholders won massively.

Building an engineering-first culture in adtech was revolutionary. Most competitors were sales-driven organizations that happened to have technology. The Trade Desk inverted this: they were a technology company that happened to sell advertising solutions. Engineers weren't support staff; they were the stars. Product managers weren't translators between business and tech; they were technical themselves. Even salespeople needed to understand the platform deeply enough to debug client issues.

The Ventura headquarters became a powerful recruiting tool. While competitors fought over talent in expensive tech hubs, The Trade Desk offered something different: meaningful work, competitive compensation, and a life outside the office. Engineers could buy houses, start families, pursue hobbies. The retention rates proved the strategy worked—The Trade Desk's employee turnover was a fraction of Silicon Valley norms.

Green's communication style is distinctive—dense, philosophical, uncompromising. His quarterly earnings calls became legendary for their length and depth. Where other CEOs delivered scripted platitudes, Green gave masterclasses on advertising economics, technology trends, and competitive dynamics. Analysts complained about the information overload. Serious investors loved it.

Green signed The Giving Pledge, committing to give away more than 90 percent of his wealth in his lifetime. This wasn't just philanthropy—it was philosophy. He founded the Jeff T. Green Family Foundation in June 2020, which has donated to a number of educational programs. With the motto "Dismantling Disparity Through Data," in 2019 and 2020, the foundation made donations to California State University Channel Islands (CSUCI) to support mentorship programs. The data-driven approach to giving mirrored his approach to business: measure everything, optimize relentlessly, scale what works.

The compensation philosophy extended throughout the organization. Every employee received equity. Not token amounts—meaningful stakes that could change lives if the company succeeded. This created a culture of ownership rare in public companies. Support staff thought like executives. Engineers considered business impact. Sales teams understood unit economics.

Board composition reflected Green's approach to governance. This wasn't a collection of celebrity directors or retired executives. The Trade Desk's board included operational experts, industry veterans, and independent thinkers who could challenge Green while supporting the long-term vision. The dual-class structure gave Green control, but the board culture encouraged debate.

The management team Green assembled was notably stable for a high-growth tech company. Blake Grayson, the CFO, had been with the company since before the IPO. David Pickles, co-founder and CTO until 2023, provided technical continuity. This stability allowed The Trade Desk to execute complex, multi-year strategies while competitors cycled through leadership.

Decision-making at The Trade Desk balanced speed with deliberation. Quick decisions on tactical issues, deep analysis on strategic choices. Green's framework was consistent: Will this increase transparency? Does it benefit the open internet? Can we execute it better than anyone else? If yes to all three, move fast. If not, keep thinking.

The culture of transparency extended internally. Financial metrics, strategic plans, competitive intelligence—information that most companies guard jealously was widely shared at The Trade Desk. This created alignment but also accountability. Everyone knew the numbers. Everyone understood the strategy. There was nowhere to hide poor performance.

Managing through COVID revealed the culture's strength. While competitors laid off thousands, The Trade Desk protected its people. Remote work was implemented smoothly because the culture of trust and accountability was already established. When offices reopened, the company maintained flexibility—another contrast with tech giants demanding return-to-office.

The "anti-Silicon Valley" positioning wasn't just marketing—it permeated every decision. No free gourmet meals (people could afford their own lunch). No lavish perks (the work was the perk). No campus infantilization (treat adults like adults). The money saved went into salaries, equity, and R&D. Employees appreciated the respect more than the perks.

Green's personal evolution paralleled the company's growth. The entrepreneur who started in a small Ventura office became a billionaire CEO managing thousands of employees and billions in market cap. Yet the core philosophy remained unchanged: transparency, independence, and relentless focus on adding value. The $834 million compensation package might have changed his net worth, but by all accounts, it didn't change his approach.

By 2024, The Trade Desk's culture had become its own recruiting tool. The company regularly appeared on "best places to work" lists—not because of perks, but because of purpose. Employees believed they were building something important: preserving the open internet, democratizing advertising technology, fighting the monopolies. In tech, where cynicism often rules, The Trade Desk maintained something rare: genuine mission alignment from CEO to newest hire.

X. Business Model & Financial Analysis

The genius of The Trade Desk's business model lies in its simplicity: they take a transparent percentage of ad spend flowing through their platform. No hidden fees, no markup games, no inventory risk. This take-rate model—typically around 20% of what advertisers spend—scales beautifully. As clients grow spend, The Trade Desk grows revenue without proportional cost increases.

Understanding the gross spend versus net revenue distinction is crucial for investors. When an advertiser spends $100 through The Trade Desk, roughly $80 goes to publishers for the media, while The Trade Desk keeps $20 as revenue. This isn't a margin—it's the entire revenue. The company then pays its operating expenses from this $20. The beauty is that processing $100 or $100 million requires roughly the same platform infrastructure.

The platform fees versus managed services decision was foundational. Competitors offered managed services—running campaigns for clients, optimizing manually, providing consulting. Higher margins, more control, but also more people, more complexity, less scalability. The Trade Desk chose the harder path: build tools so good that clients would pay to use them directly. Lower take rates, but infinite scalability.

Revenue in Q3 was $628 million, representing growth of 27% year over year, accelerating from the prior quarter and year over year. The acceleration in 2024 despite a challenging macro environment demonstrates the model's resilience. Adjusted EBITDA: $257 million, approximately 41% of revenue—margins that would make most software companies envious.

The operating leverage in the model is stunning. Operating Expenses (Excluding Stock-Based Compensation): $391 million, up 24% year over year while revenue grew 27%. This widening gap between revenue and expense growth drops straight to the bottom line. Every incremental dollar of revenue costs less to generate than the last.

The working capital dynamics are complex but manageable. The Trade Desk typically pays publishers before collecting from advertisers—a cash flow challenge that destroyed many adtech companies. But disciplined credit management and scale advantages have turned this into a competitive moat. Smaller competitors simply can't finance the float required to compete for large accounts.

Cash and Liquidity Position: $1.7 billion in cash, cash equivalents, and short-term investments; no debt. This fortress balance sheet provides strategic flexibility—they can invest in R&D, make acquisitions, or weather downturns without external financing. In an industry where many competitors are leveraged or unprofitable, this financial strength is a massive advantage.

Capital efficiency at The Trade Desk borders on miraculous. Besides Sincera, The Trade Desk's only other acquisition to date was its 2017 acquisition of Adbrain. Two acquisitions in 15 years. Compare this to competitors rolling up companies desperately seeking scale. The Trade Desk built rather than bought, invested in R&D rather than M&A, and created more value with less capital than perhaps any company in adtech history.

The margin structure reveals the model's elegance. Gross margins are essentially 100%—they're a software company, not a media company. They don't buy and resell inventory; they charge for platform access. From there, the biggest expenses are people (engineering and support) and infrastructure (data centers and connectivity). Both scale sub-linearly with revenue.

Customer economics are the model's foundation. Geographical Revenue Distribution: North America 88%, International 12%. Customer retention above 95% for seven consecutive years. Net revenue retention consistently above 100%, meaning existing customers increase spend faster than churn reduces it. These metrics create compounding growth—each cohort of customers becomes more valuable over time.

The M&A philosophy reflects financial discipline. Rather than acquiring for revenue or market share, The Trade Desk acquires for technology or talent, and only when building internally doesn't make sense. The Adbrain acquisition in 2017 brought device-graph technology that would have taken years to build. But most capabilities—from Connected TV to identity solutions—were built internally.

Seasonality in the business follows advertising patterns. Q4 is traditionally strongest (holiday shopping), Q1 weakest (post-holiday hangover). But The Trade Desk has progressively smoothed these cycles by diversifying across verticals, geographies, and channels. Political advertising creates even-year bumps, but the core business growth overwhelms these fluctuations.

The investment cycle is counter-cyclical to profits. When growth slows, The Trade Desk invests more in R&D and infrastructure, emerging from downturns with better products and more capacity. When growth accelerates, they harvest profits while maintaining investment levels. This approach requires confidence and long-term thinking rare in public markets.

Q4 Revenue Outlook: At least $756 million, representing about 25% year-over-year growth. Q4 Adjusted EBITDA Outlook: Approximately $363 million. The guidance philosophy is conservative—underpromise and overdeliver. This builds credibility with investors and reduces volatility.

The unit economics tell the real story. Customer acquisition costs are minimal—The Trade Desk doesn't advertise, relying on word-of-mouth and industry reputation. The platform's self-service nature means support costs scale logarithmically with customer count. Infrastructure costs benefit from cloud economics and Moore's Law. Every unit economic metric improves with scale.

Free cash flow generation is remarkable. Free Cash Flow: $222 million in just one quarter. This cash generation funds everything: R&D, international expansion, Ventura OS development, share buybacks. No dilution, no debt, no financial engineering—just a business model that prints cash.

The Trade Desk in 2024 isn't just financially successful—it's financially antifragile. Economic uncertainty makes advertisers focus on ROI, benefiting The Trade Desk's transparent, measurable platform. Technology disruption creates opportunities for an agile, innovative player. Regulatory pressure on Big Tech opens doors for an independent alternative. The business model doesn't just survive challenges—it thrives on them.

XI. Competitive Landscape & Market Position

The Trade Desk is headquartered in Ventura, California. It is the largest independent demand-side platform in the world, competing against DoubleClick by Google, Facebook Ads, and others. But calling The Trade Desk the "largest independent DSP" understates their strategic position. They're not just competing—they're redefining the battlefield.

Google's conflicts of interest are The Trade Desk's greatest marketing asset. The Trade Desk's main competitor is Google, which operates a DSP, an SSP, and has its own content. Green has been an outspoken critic of Google, citing conflicts of interest, even before the Justice Department sued the tech giant for antitrust around its ad dominance. Google owns YouTube (content), runs DV360 (demand-side platform), operates AdX (supply-side platform), and controls Chrome (the browser). They're player, referee, and league commissioner simultaneously.

The "independent" positioning resonates because it's real. Agencies using The Trade Desk know they're not funding a future competitor. Publishers integrating with The Trade Desk know their data won't be used against them. This trust premium—impossible to quantify but impossible to ignore—drives customer acquisition and retention.

Amazon's advertising ambitions represent the fastest-growing competitive threat. With first-party purchase data, massive reach through Prime Video, and unlimited capital, Amazon DSP is formidable. But Amazon faces the same conflict problem as Google—they're both buyer and seller, platform and participant. The Trade Desk's response has been strategic partnership where possible, superior technology where necessary.

Facebook (Meta) operates in a parallel universe. Their walled garden is so complete that they barely compete with The Trade Desk directly. Advertisers need both—Facebook for its massive logged-in user base, The Trade Desk for everything else. The relationship is more symbiotic than competitive, though this could change as Meta pushes into Connected TV.

Other independent DSPs struggle to achieve scale. Amazon DSP benefits from corporate subsidies. DV360 leverages Google's ecosystem. Yahoo DSP has decent technology but lacks investment. MediaMath's bankruptcy in 2023 demonstrated the difficulty of competing without scale or differentiation. The Trade Desk stands alone as the only independent DSP with the scale, technology, and financial strength to compete globally.

Supply-side platforms are partners and frenemies. Magnite, PubMatic, and others need The Trade Desk's demand, but they also work with competitors. The Trade Desk's approach—be the best source of demand, maintain fair relationships, never squeeze partners—has made them the preferred DSP for most SSPs. When publishers have to choose who gets priority access, The Trade Desk usually wins.

The competitive moat has multiple layers. Network effects: more advertisers attract more publishers, which attract more advertisers. Jeff Green, CEO, noted that The Trade Desk represents just over 1% of the $1 trillion advertising ecosystem, indicating significant growth potential. He emphasized the importance of adding more value than extracted and creating an efficient supply chain to continue capturing market share without cannibalizing the market.

Switching costs are substantial but not insurmountable. Agencies invest years learning The Trade Desk's platform, building custom algorithms, integrating data sources. Moving to another DSP means retraining staff, rebuilding campaigns, losing historical optimization data. Not impossible, but painful enough that 95% retention makes sense.

Scale economies manifest everywhere. R&D costs spread across more revenue. Infrastructure investments amortize over more impressions. Data processing benefits from larger sample sizes. Partnership negotiations leverage greater volume. Every aspect of the business gets more efficient with scale, and The Trade Desk has reached escape velocity.

Counter-positioning versus Google is genius strategy. Every Google scandal—privacy violations, antitrust investigations, publisher complaints—benefits The Trade Desk. They don't have to attack Google directly; they just have to exist as the obvious alternative when advertisers and publishers get frustrated. As one agency executive put it: "Google is the devil we know. The Trade Desk is the angel we're learning to trust."

Process power comes from years of refinement. The Trade Desk's bidding algorithms evaluate 15 million queries per second, each requiring hundreds of calculations in under 100 milliseconds. This isn't just software—it's orchestration of thousands of design decisions, optimizations, and trade-offs that competitors can't easily replicate.

The retail media explosion creates new competitive dynamics. Walmart, Target, Kroger—every retailer wants to monetize their data and customer relationships. They need DSP capabilities but don't want to build them. The Trade Desk's retail data alliance positions them as the Switzerland of retail media—trusted by all because they compete with none.

International competition varies by market. In China, local players dominate but need international demand—hence The Trade Desk's partnerships. In Europe, GDPR created opportunities for privacy-compliant players. In emerging markets, The Trade Desk often arrives before Google gets serious, establishing relationships that become difficult to displace.

The Connected TV battlefield showcases The Trade Desk's competitive strengths. CTV and video advertising represent nearly 50% of The Trade Desk's business. While Google struggles with YouTube TV conflicts, Amazon pushes Prime Video, and Roku builds its own ad business, The Trade Desk remains neutral—the arms dealer in the streaming wars, selling to all sides.

Competitive responses have been telling. Google rarely mentions The Trade Desk publicly but has copied numerous features. Amazon accelerated DSP investment after The Trade Desk's CTV success. Facebook opened up more inventory to external DSPs. When giants change strategy in response to your moves, you're no longer a startup—you're a force.

The venture capital exodus from adtech benefits The Trade Desk. With few new entrants and existing competitors struggling for funding, The Trade Desk can hire the best talent, partner with the best companies, and invest for the long term without worrying about venture-backed disruption. The last mover advantage is real.

Platform commoditization is the existential risk. If DSPs become interchangeable—similar features, similar inventory, similar performance—then price becomes the only differentiator. The Trade Desk's response: continuous innovation, deeper moats, and relationships that transcend technology. Unified ID 2.0, Ventura OS, retail media partnerships—each initiative makes commoditization less likely.

By 2024, The Trade Desk's competitive position is paradoxical: dominant yet vulnerable, essential yet replaceable, powerful yet dependent on ecosystem partners. But this tension drives innovation. Complacency would be fatal. Paranoia keeps them sharp. As Green often says: "We're only as good as our next product release." In the fast-evolving world of adtech, that's exactly the right attitude.

XII. Playbook: Business & Investing Lessons

Building in the shadow of giants requires a different playbook. The Trade Desk couldn't outspend Google, out-engineer Facebook, or out-scale Amazon. Instead, they found the one thing the giants couldn't do: be neutral. This wasn't just positioning—it was strategy. Every product decision, every partnership, every public statement reinforced their independence. When you can't win the game, change the rules.

The power of transparency in opaque markets cannot be overstated. AdTech in 2009 was a black box inside a black box. Publishers didn't know what advertisers paid. Advertisers didn't know where ads ran. Agencies didn't know their true costs. The Trade Desk made transparency their weapon. Show every fee. Expose every margin. Document every impression. What seemed like giving away leverage became their greatest source of power.

Platform versus services remains one of the most important strategic decisions any company makes. Services businesses scale linearly—more revenue requires more people. Platform businesses scale exponentially—the millionth customer costs less than the first. The Trade Desk chose the harder path: build tools so good that clients would rather use them directly than have someone else do it for them. The first years were brutal. The long-term rewards were extraordinary.

Timing markets is usually impossible, but occasionally the stars align. Programmatic advertising in 2009 was like e-commerce in 1995 or cloud computing in 2006—obviously the future, but early enough that dominant players hadn't emerged. The Trade Desk didn't create the programmatic wave, but they positioned themselves perfectly to ride it. Being early is often indistinguishable from being wrong—until suddenly you're right.

Being profitable while growing fast seems like a paradox in Silicon Valley, where losses are worn as badges of honor. The Trade Desk proved you could do both. The discipline required was immense—saying no to expansion opportunities, keeping teams lean, focusing relentlessly on unit economics. But profitability provided freedom: no dilutive fundraising, no demanding VCs, no pressure to exit. They could build for the long term because they controlled their destiny.

The benefits of founder-led companies extend beyond vision and passion. Jeff Green, CEO, highlighted that The Trade Desk is performing strongly, particularly in CTV, which is both the largest and fastest-growing channel. He noted that CMOs are under pressure to grow amidst uncertainty, which benefits The Trade Desk as brands seek data-driven solutions. Despite market tensions, the company is well-positioned with strong partnerships and innovations like Kokai and UID2. Founders can make decade-long bets that hired CEOs can't. They can sacrifice short-term profits for long-term position. They can maintain culture through hypergrowth.

Building standards and ecosystems is the ultimate power move. Microsoft didn't win by building the best computer—they won by making DOS and Windows the standard. The Trade Desk understood this playbook. Unified ID 2.0 wasn't just a product—it was an attempt to define the future of identity online. Ventura OS isn't just software—it's infrastructure for the next generation of television. When you control standards, you control markets.

The anti-disruption strategy deserves its own business school case. Clay Christensen taught that incumbents fail because they can't disrupt themselves. The Trade Desk inverted this: they positioned themselves so that every disruption in adtech—privacy regulations, cookie deprecation, streaming growth—made them stronger. They weren't disrupting; they were enabling everyone else to disrupt.

Capital allocation at The Trade Desk should be taught in finance courses. No massive acquisitions. No financial engineering. No dividends or buybacks (until absolutely necessary). Just relentless reinvestment in the business. Every dollar stayed in the company, compounding. The patience required—especially as a public company—was extraordinary.

The ecosystem approach multiplied their impact. Rather than trying to do everything, The Trade Desk became the center of a network. Publishers, data providers, measurement companies, attribution vendors—all integrated with The Trade Desk because it was the nexus of demand. This created powerful network effects without the capital requirements of building everything internally.

Customer selection matters more than customer acquisition. The Trade Desk could have grown faster by working with lower-quality agencies or accepting lower-margin business. Instead, they focused on sophisticated buyers who valued the platform's capabilities. These customers had lower churn, higher growth rates, and became evangelists. Quality compounds; quantity doesn't.

The regulatory arbitrage opportunity was subtle but powerful. While Google and Facebook fought regulators, The Trade Desk positioned itself as the solution. Privacy-compliant. Transparent. Pro-publisher. Pro-consumer. When GDPR hit, they were ready. When CCPA arrived, they were prepared. Every regulation that hurt the giants helped The Trade Desk.

Organizational design followed strategy. No separate business units competing for resources. No regional fiefdoms. One platform, one team, one P&L. This created alignment and eliminated politics. When everyone wins or loses together, collaboration isn't a nice-to-have—it's survival.

The VC avoidance strategy paid massive dividends. After the initial $2.5 million seed round, The Trade Desk never raised primary capital again. No Series B, C, or D. No private equity. This meant no board seats given away, no liquidation preferences, no forced exit timeline. The founders maintained control and could build for permanence, not exit.

Technical debt management was masterful. Rather than constant rewrites, The Trade Desk evolved their platform incrementally. Old code was refactored, not replaced. New capabilities were added modularly. This allowed them to maintain velocity while avoiding the paralysis that kills many scaling companies.

The lesson for founders is clear: find a massive market with powerful incumbents, identify their structural disadvantages, position yourself as the solution to those disadvantages, then execute relentlessly for a decade. Simple to describe, nearly impossible to execute. The Trade Desk shows it can be done.

For investors, The Trade Desk demonstrates the power of business model innovation. They didn't invent programmatic advertising. They didn't create new ad formats. They simply restructured how the industry worked—transparency instead of opacity, platform instead of services, independence instead of conflicts. Sometimes the biggest opportunities come not from new technology but from new business models applied to existing markets.

XIII. Bear vs. Bull Case Analysis

Bull Case: The Secular Growth Story

Connected TV is still in the early innings of a massive transformation. CTV is the fastest-growing advertising channel in the U.S. It's projected to total $38.3 billion in 2024, per GroupM's latest forecast. By 2029, CTV is expected to overtake linear television in ad sales. The Trade Desk's dominant position in CTV, combined with their Ventura OS initiative, positions them to capture an outsized share of the $70 billion that will shift from linear to streaming.

The retail media explosion is just beginning. Every retailer with first-party data wants to monetize it. Every CPG brand needs to access that data. The Trade Desk sits in the middle, neutral and trusted by all. As retail media grows from $40 billion to potentially $150 billion by 2028, The Trade Desk's platform becomes increasingly essential.

International expansion opportunities remain massive. Geographical Revenue Distribution: North America 88%, International 12%. This means 88% of revenue comes from markets representing less than 30% of global advertising spend. As programmatic adoption accelerates internationally, The Trade Desk's growth could accelerate even from current levels.

Identity solution leadership post-cookies positions them perfectly for the privacy-first future. Unified ID 2.0 has achieved critical mass adoption. When cookies finally die, The Trade Desk will be one of the few platforms that can still deliver targeted advertising at scale. This isn't just maintaining position—it's potential market share gain as competitors struggle.

Operating leverage at scale is breathtaking. Adjusted EBITDA: $257 million, approximately 41% of revenue. As revenue scales from $2 billion to $5 billion to $10 billion, margins could expand to 50% or higher. The incremental economics get better with size, not worse.

Bear Case: The Risks Are Real

Competition from Amazon is intensifying rapidly. Amazon's advertising business is growing 20%+ annually and approaching $50 billion in revenue. They have first-party purchase data The Trade Desk can never access. Prime Video's ad tier gives them premium inventory. AWS gives them infrastructure advantages. If Amazon decides to seriously compete in the independent DSP market, The Trade Desk faces its most formidable challenger yet.

Google's dominance might be unbreakable despite antitrust pressure. Chrome still commands 65% browser market share. YouTube remains the largest video platform. Google's DSP benefits from integration advantages that regulation might limit but won't eliminate. The Trade Desk is fighting a guerrilla war against an empire—inspiring but possibly futile.

Economic sensitivity to ad spending is unavoidable. Advertising is the first budget cut in recessions. While The Trade Desk's platform provides ROI advantages during downturns, they're not immune. A serious recession could halt growth or even shrink revenue, testing investor patience and the valuation multiple.

Valuation concerns at 30x revenue are legitimate. Even assuming continued 25% growth and margin expansion, the current valuation requires perfect execution for years. Any stumble—a quarter of deceleration, a failed product launch, a key customer loss—could trigger multiple compression and significant stock price decline.

Regulatory risks around data and privacy keep escalating. Each new privacy law adds complexity and cost. Browser changes limit targeting capabilities. Consumer privacy expectations keep rising. The Trade Desk has navigated well so far, but one misstep could undermine their entire value proposition.

The Nuanced Reality

The truth encompasses both narratives. The Trade Desk operates in genuinely massive markets with powerful secular tailwinds. Their execution has been near-flawless. The competitive moats are real and deepening. But the valuation assumes continued perfection. The competitors aren't standing still. The regulatory environment keeps tightening.