Trinity Industries: How a Mule Barn Tank Shop Became North America's Railcar King

I. Introduction & Episode Roadmap

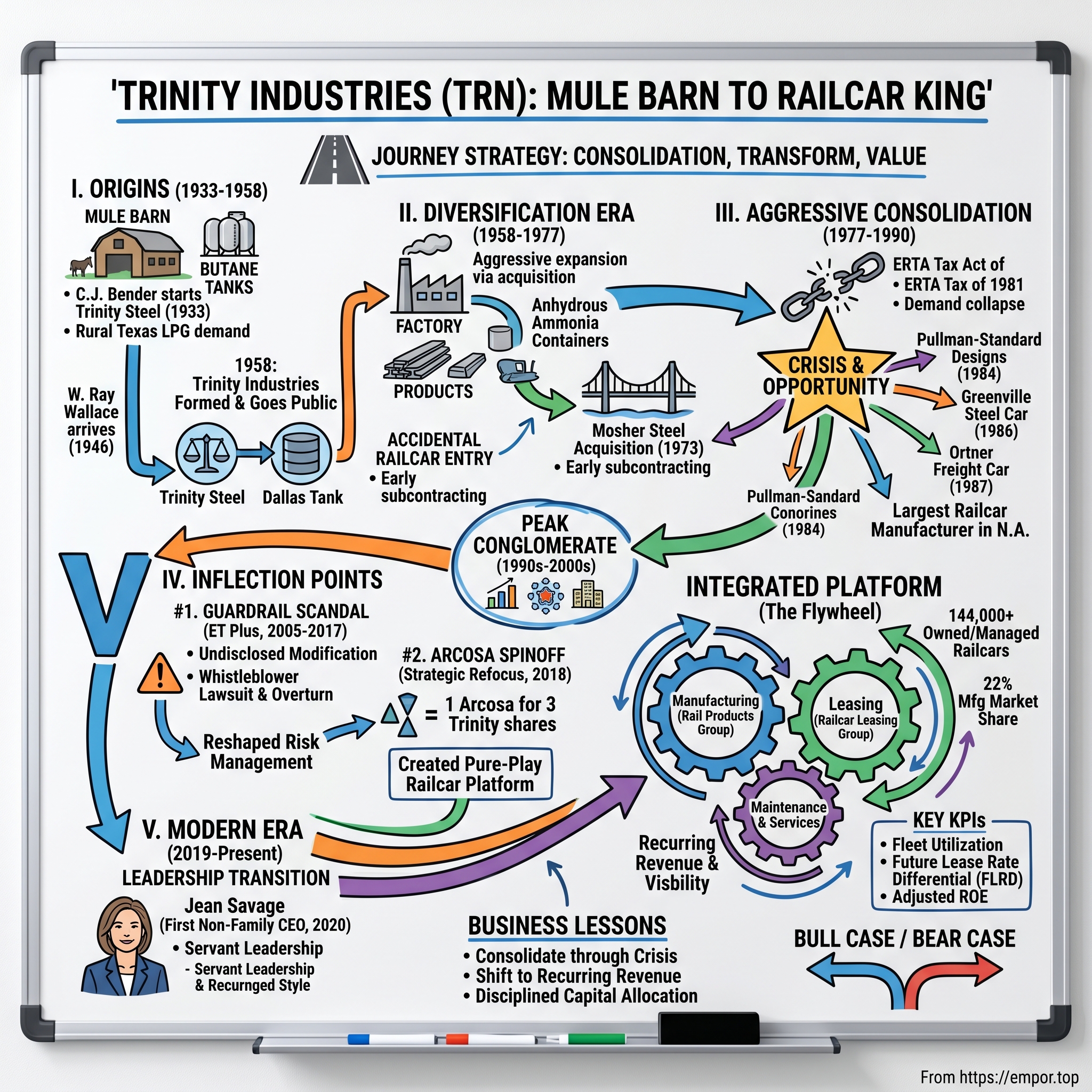

Picture Dallas, Texas, in the depths of the Great Depression. While breadlines stretched around city blocks and dust storms ravaged the Southwest, a small operation hummed away in an unlikely setting: a converted mule barn in Dallas County. Here, workers welded butane tanks—utilitarian vessels for the liquefied petroleum gas that rural Texans were just beginning to embrace for home heating and cooking. The year was 1933, and no one could have imagined that this modest enterprise would one day become the largest freight railcar manufacturer on the North American continent.

Trinity Industries Inc. is an American industrial corporation that owns a variety of businesses which provide products and services to the industrial, energy, transportation and construction sectors. Today, the company commands roughly 22% market share in North American railcar manufacturing and operates one of the continent's largest railcar leasing fleets. With over 140,000 leased and managed railcars in our portfolio, we are a leading provider of comprehensive rail transportation products and solutions, including digitally enabled logistics services, manufacturing resources, railcar management, parts and maintenance.

But Trinity's story isn't merely one of growth—it's a case study in strategic transformation, crisis survival, and disciplined capital allocation. The central question that animates this deep dive: How did a butane tank maker in a Dallas mule barn become the largest railcar manufacturer in North America—and then strategically shrink to become even more valuable?

The company achieved full year reported EPS of $1.81 and adjusted EPS of $1.82, representing a 32% increase over 2023, driven by higher lease rates, significantly improved margin performance. This performance comes from a business that has deliberately narrowed its focus, spinning off billions in revenue to concentrate on what it does best.

The themes that emerge from Trinity's 90-year journey read like a masterclass in industrial strategy: consolidation through crisis, the transformation from pure manufacturing to integrated leasing platform, surviving scandal that nearly destroyed the company, and disciplined capital allocation that has kept the enterprise relevant across generations. Let's dive in.

II. The Origins: Butane Tanks and the Texas Industrial Frontier (1933–1958)

The Texas of 1933 was a land of paradoxes. The oil boom that had transformed the state into an energy powerhouse was temporarily stalled by Depression-era demand collapse, yet the infrastructure needs of an industrializing Southwest continued to grow. Rural electrification hadn't reached most of Texas, and families depended on bottled gas—butane and propane—for cooking and heating. Someone had to make the tanks.

The company, first known as Trinity Steel, was founded by C. J. Bender in Dallas in 1933. Bender saw opportunity where others saw hardship. The manufacture of pressure vessels for liquefied petroleum gas required specialized welding skills and metallurgical knowledge, but the barriers to entry were relatively low. A converted agricultural building would suffice.

The pivotal figure in Trinity's story arrived thirteen years later. W. Ray Wallace, an engineering graduate of Louisiana Tech, worked for Dallas's Austin Bridge Company in 1944 before joining the company in 1946 as its seventeenth employee. At the time Trinity Steel manufactured butane tanks in a Dallas County mule barn.

Wallace was young, technically trained, and ambitious. His engineering background from Louisiana Tech gave him the analytical tools to understand both the production process and the financial engineering that would later define Trinity's growth strategy. He joined a small company, but his timing was impeccable.

Post-WWII Texas was transforming rapidly. The oil boom returned with vengeance, and with it came insatiable demand for petroleum infrastructure—storage tanks, refinery vessels, and pipeline components. For a time the company profited by producing larger tanks that enabled it to enter the petroleum business and do steel fabrication for refineries.

At the time Trinity had revenues reaching $2.5 million and employed 200 workers. For a company that had started in a mule barn, this represented remarkable progress. But the petroleum tank business was becoming crowded, and Ray Wallace could see the competitive pressures mounting.

Nonetheless, by 1957 Trinity faced competition and declines in the petroleum industry. The solution was consolidation. Dallas Tank, Trinity Steel, and Bender-Wallace Development Company merged in 1958 to form Trinity Industries, Incorporated, and went public.

In 1958 Trinity Steel merged with Dallas Tank Company, which was also founded in 1933, and Ray Wallace became the new firm's president and first chief executive officer. At just thirty-two years old, Wallace took the helm of a newly public company. He would run it for the next four decades.

The 1958 merger set a pattern that would define Trinity for generations: when facing competitive pressure, don't retreat—consolidate. Buy your competitors, integrate their operations, and emerge stronger. Wallace learned this lesson early, and he never forgot it.

III. The Diversification Era: Steel, Barges & Structural Products (1958–1977)

The newly public Trinity Industries operated in a business school case study of related diversification. Ray Wallace understood that pressure vessels, tanks, and steel fabrication shared common production capabilities: welding expertise, metallurgical knowledge, large-scale manufacturing facilities, and relationships with steel suppliers. The question was which adjacent markets offered the best growth opportunities.

The 1960s saw Trinity pursue a strategy of disciplined expansion through acquisition. Trinity's tank manufacturing expertise was also applied to containers for anhydrous ammonia fertilizer, which was another burgeoning industry in the 1960s. Pressure and non-pressure storage containers made up about 75 percent of Trinity's business. The company also manufactured custom metal products for the chemical and petroleum industries, and enjoyed phenomenal growth in the 1960s.

In 1967, the company's name was changed to Trinity Industries to reflect its growing diversified product lines—a symbolic acknowledgment that the company had outgrown its steel-tank origins.

The early 1970s brought even more aggressive expansion. In 1970 Trinity diversified with the acquisition of 153 acres of land adjacent to the Dallas-Fort Worth International Airport and in 1971 established its first real estate subsidiary. In 1972, Trinity's stock began trading on the New York Stock Exchange under the symbol TRN. Acquisition of Mosher Steel in 1973, after initially contracting work out to them, enhanced the company's structural business.

The Mosher Steel acquisition deserves particular attention. In 1973 the company bought the Equitable Equipment Company, with shipyards in New Orleans and Madisonville, Louisiana, and the Mosher Steel Company of Houston, a large manufacturer of steel beams and framing. Trinity had been contracting work out to Mosher; now they owned them. This pattern—first become a customer, then acquire your supplier—would repeat throughout Trinity's history.

The structural steel business produced some remarkable projects. Among projects completed by the firm's structural steel division were the Texas Stadium, New York's World Trade Center, the Balboa Bridge in Panama, the Pennzoil Building, and two buildings in Moscow. When workers assembled the iconic World Trade Center towers in lower Manhattan, they were handling Trinity steel.

By 1977, the transformation was complete. Bridge girders and other structural products generated 37 percent of Trinity's sales, and the company had become a true industrial conglomerate spanning tanks, marine vessels, structural steel, and construction products.

But buried in Trinity's portfolio was a small, almost accidental business that would eventually dwarf everything else—railcar manufacturing.

IV. The Accidental Railcar Entry & Aggressive Consolidation (1977–1990)

The Accidental Beginning

The railcar business came to Trinity not through strategic planning, but through opportunistic capacity utilization. Although Trinity began fabricating railway tank car bodies as a subcontractor to Richmond Tank Car and Union Tank Car as early as 1966, in 1978 Trinity began producing complete tank and covered hopper rail cars in association with Quick Car of Fort Worth, Texas, which Trinity later absorbed.

The 1966 opportunity came when Union Tank Car fell behind on production and needed a subcontractor to build tank portions for 1,500 railcars designed to transport LPG and anhydrous ammonia. Trinity had already been supplying tank components to Richmond Tank Car for years. Building the tank portion of a tank car wasn't terribly different from building industrial pressure vessels—it was welded steel fabrication at scale. Trinity completed the order, but then stepped back. It wasn't until 1977-1978 that the company made its permanent jump into complete railcar manufacturing.

The 1981 Crisis and Opportunity

The early 1980s presented Trinity with its defining moment. By 1980, the company had become one of the top five railcar builders in the United States. Then the market collapsed.

The Economic Recovery Tax Act of 1981 (ERTA)—Reagan's signature legislation—fundamentally altered the economics of railcar ownership. The Economic Recovery Tax Act of 1981 (ERTA) was a federal tax law passed on August 13, 1981 by the 97th U.S. Congress as a big move to encourage economic growth by providing crucial tax cuts. The legislation was also known as the "Kemp-Roth Tax Cut." It was signed into law by then-President Ronald Reagan.

ERTA aimed to simplify the tax code by eliminating many tax shelters that were seen as loopholes. This had the effect of broadening the tax base, meaning that while rates were lower, more income was subject to taxation.

The impact on railcar demand was catastrophic. Prior to ERTA, railcars had served as popular tax shelters for wealthy individuals—doctors, dentists, and other professionals could buy railcars, lease them to railroads, and claim accelerated depreciation benefits that often exceeded their actual economic value. When ERTA eliminated these benefits, orders for new cars plummeted from 96,000 to just 5,300 in four years—a 94% collapse.

Most railcar manufacturers viewed this as an existential crisis. Ray Wallace saw opportunity.

The Consolidation Spree (1984–1987)

What happened next remains one of the most remarkable consolidation campaigns in American industrial history. Trinity systematically acquired its weakened competitors, buying not just manufacturing capacity but—crucially—intellectual property in the form of railcar designs and engineering expertise.

In 1984 Trinity absorbed Quick Car and acquired the railcar designs and production facilities of the Pullman-Standard Car Manufacturing Company, once the largest railcar manufacturer in North America. That same year Trinity also acquired the railcar designs of General American Transportation Corporation.

The Pullman-Standard acquisition deserves particular emphasis. This was the company that had built the sleeping cars that carried generations of Americans across the continent—George Pullman's creation, a name synonymous with railroad travel itself. In mid-1981, Pullman, Inc., spun off its freight car manufacturing interests as Pullman Transportation Company. Several plants were closed and in 1984, the remaining railcar manufacturing plants and the Pullman-Standard freight car designs and patents were sold to Trinity Industries.

The acquisition price was reportedly $15 million—a pittance for the industry's largest player, but Pullman was desperate to exit a business that had become a drag on its diversified corporation.

In 1986 the rail car designs and production facilities of Greenville Steel Car Company were purchased, including the auto rack designs of Portec-Paragon. Also acquired in 1986 were the railcar designs of North American Car Corporation, and in 1987 Ortner Freight Car was acquired. These combined acquisitions made Trinity the largest rail car manufacturer in North America.

Making the best of these soft market conditions, Trinity acquired several of its weakened competitors, including Pullman Standard, once the largest freight car manufacturer in the United States. In late 1986 the Greenville Steel Car Company, the Ortner Freight Car Company, and the Standard Forgings Corporation (a locomotive and rail car axle maker) were acquired.

Trinity emerged from the 1980s owning the design libraries and manufacturing know-how of nearly every major American railcar builder. Our comprehensive library includes drawings from TrinityRail as well as former car builders like Thrall, Ortner Freight Car, Greenville Steel Car, Pullman Standard, and Whitehead & Kales. This intellectual property portfolio would prove invaluable for decades, allowing Trinity to manufacture virtually any type of railcar design and provide replacement parts for aging fleets.

During the mid- to late 1980s more rail cars were being taken out of service than were purchased, creating pent-up demand, and Trinity anticipated a massive rail car replacement program on the part of the nation's railroad operators. The bet was straightforward: when the industry recovered, Trinity would be the dominant supplier.

Although Trinity's core businesses showed disappointing growth in the 1980s, the company was able to absorb some of its stronger competitors as they went out of business without overextending itself. The company entered the 1990s financially strong and ready to benefit from the long-anticipated modernization of the American transportation infrastructure.

V. The Conglomerate Peak & Industry Evolution (1990s–2000s)

The 1990s represented Trinity's heyday as a diversified industrial conglomerate. In the 1990s expansion continued with the acquisition of the Transit Mix Concrete and Materials Company of Beaumont, Texas, Beiard Industries, Syro Steel and Stearns Airport Equipment of Fort Worth, Texas.

By 1993 revenues exceeded $1.5 billion, and the firm employed 13,000 people. Trinity had become a genuine industrial powerhouse spanning railcars, barges, highway products, construction materials, and energy equipment.

The company continued acquiring railcar competitors. In 1998 Trinity acquired the Differential Steel Car Company (DIFCO), which designed and built specialty rail cars. That same year Trinity also opened a rail car production plant in Monclova, Mexico.

The crown jewel acquisition came in 2001. In 2001 Trinity Industries acquired the designs and production facilities of Thrall Car Manufacturing Company, then North America's second largest producer of railroad freight cars. With Thrall, Trinity had now acquired the design libraries of the two largest railcar manufacturers in North American history—Pullman-Standard and Thrall.

In 2002-2003, Trinity consolidated its rail car building operations under the name Trinity Rail Group (TRG), and then shortened the name to TrinityRail. The TrinityRail brand would become the company's public face for its railcar operations.

The mid-2000s brought strategic pruning. In June 2006, the company completed the sale of its weld pipe fittings business. In August the same year, the company sold its European Rail business to International Railway Systems S.A. Trinity was beginning to think more carefully about where it had competitive advantages.

Perhaps most importantly, the 1990s and 2000s saw Trinity build its leasing business alongside manufacturing. As Trinity increasingly builds and then leases its railcars, within the past 25 years its fleet has grown significantly, expanding from 8,000 railcars and $4-500 million of invested capital, to 130,000 railcars and roughly $8 billion in invested capital.

This transition—from pure manufacturer to integrated lessor-manufacturer—would prove to be the most important strategic decision in Trinity's modern history. By owning railcars rather than simply building them, Trinity gained recurring revenue, customer relationships throughout the railcar lifecycle, and insulation from manufacturing cyclicality.

VI. INFLECTION POINT #1: The ET Plus Guardrail Scandal (2005–2017)

The Undisclosed Modification

Every great company faces a moment that tests its character, governance, and ultimately its survival. For Trinity Industries, that moment came in the form of a highway guardrail end terminal called the ET Plus.

According to a class action lawsuit against Trinity Industries, the manufacturer made changes to the ET-Plus guardrails' design in 2005 without announcing the redesign or seeking approval. However, these changes allegedly caused the Trinity Industries ET-Plus guardrails to be unsafe. The new design allegedly causes the ET-Plus devices to lock up during a crash. As a result, the guardrail doesn't ribbon away from the vehicle and instead can puncture the vehicle, the class action lawsuit contends.

The change in question seemed minor: Trinity reduced the width of a steel channel in the ET Plus system from five inches to four inches. The change in 2005 involved trimming the width of a metal piece of the end terminal down from five inches to four, a modification that a company employee estimated at the time would save the company $50,000 per year. But Trinity failed to tell state or federal safety inspectors about the change until 2012.

Fifty thousand dollars per year. That was the estimated annual savings from a modification that would expose the company to hundreds of millions in potential liability.

The Whistleblower Lawsuit

The company faced very few product-related lawsuits – and almost none against its guardrails – until March 2012, when Joshua Harman, a competitor-turned-whistle-blower, sued under the FCA.

In 2012, Joshua H., a Trinity competitor, filed a whistleblower lawsuit against the company under the False Claims Act, a federal law that allows private citizens or entities to bring legal claims on behalf of the government.

The False Claims Act is a powerful statute dating to the Civil War era, designed to allow private citizens to sue on behalf of the federal government when they discover fraud. If successful, the whistleblower receives a portion of any recovery.

Two years ago today, an East Texas jury ruled that the Dallas industrial supply company violated the False Claims Act – a 153-year-old law that allows whistleblowers to sue companies that defraud the U.S. government. The jury found that Trinity failed to inform federal officials that it modified its highway guardrail systems but kept promoting the product as approved by the Federal Highway Administration. The verdict resulted in a $663 million judgment against Trinity – the largest in the history of the FCA.

The verdict stunned corporate America. The jury said that those violations caused the U.S. Government to incur $175 million in damages, as the federal government helps state transportation departments purchase approved products, including Trinity guardrail products, for use on highways across the country. Under the federal False Claims Act, the verdict amount would be tripled to $525 million.

The Broader Impact

The fallout extended far beyond the courtroom. After revelations in 2013 that Trinity concealed from federal and state regulators that it had shortened the width of the ET Plus device's guide channels (a critical design feature) from five inches to four inches, the ET Plus was removed from the MoDOT's approved products list—eventually 30 other states followed suit.

The massive federal verdict rippled through state departments of transportation and dozens of states halted sales of the guardrails, with Virginia DOT announcing it would begin replacing the controversial guardrail.

The Legal Reversal

Most corporations facing such catastrophic liability would have raced to settle. Trinity chose to fight.

"Trinity is taking a different approach. It is fighting back and fierce. 'We do not believe that we did anything wrong,' Trinity Chief Legal Officer Theis Rice said in an exclusive interview."

The legal question at the heart of the case was genuinely novel: Can a whistleblower recover hundreds of millions of dollars when the government itself denies it was defrauded, denies the guardrails are unsafe, and denies it lost any money?

Although this judgement was a win for Joshua, the 5th Circuit Court of Appeals overturned the judgement in 2017. The 5th Circuit found that, because the Federal Highway Administration continued to reimburse Trinity for the ET-Plus after hearing Joshua's claims, he couldn't claim that Trinity's misstatements had a notable effect on the government's decisions. More recently in January 2019, the U.S. Supreme Court rejected Joshua's attempt to revive the verdict.

Trinity won on appeal, but the victory came at enormous cost—years of legal fees, reputational damage, and distraction from core operations. The ET Plus guardrail is no longer produced or sold.

The guardrail scandal offers a sobering lesson for investors: even seemingly minor engineering decisions can create existential risks when regulatory compliance and transparency are compromised. Trinity survived, but the experience reshaped how the company thought about risk management.

VII. INFLECTION POINT #2: The Arcosa Spinoff—Strategic Refocus (2018)

The Rationale for Separation

As Trinity navigated the final stages of the guardrail litigation, management was simultaneously planning a more fundamental transformation: spinning off the company's non-rail businesses into an independent entity.

"Today's filing marks an important step in the process toward establishing two independent, publicly-traded companies with high-performing businesses and long-term growth potential," said Timothy R. Wallace, Trinity's Chairman, Chief Executive Officer, and President. "We believe that this strategic separation will enable both companies to enhance their competitive positions, advance distinct investment theses, and optimize their balance sheets and capital allocation priorities to achieve the best returns for their respective stockholders."

Timothy Wallace was Ray Wallace's son, and he had led Trinity since 1999. The Dallas-based company was founded by his great uncle in the 1930s and later run by his father, Ray. Trinity provides rail transportation products and services throughout North America. The family had guided Trinity for three generations, but Tim Wallace recognized that the conglomerate structure was no longer optimal.

With $1.5 billion in 2017 revenues and $132 million in 2017 operating profit, Arcosa plans to leverage its strong platform of businesses to capitalize on North American economic expansion and infrastructure spending.

The Mechanics

Arcosa became an independent, publicly-traded company listed on the New York Stock Exchange on November 1, 2018 in connection with the separation (the "Separation") of Arcosa from Trinity Industries, Inc. (NYSE: TRN, "Trinity"). At the time of the Separation, Arcosa consisted of certain of Trinity's construction products, energy equipment, and transportation products businesses.

The Arcosa stock dividend occurred effective at 12:01 a.m. local New York City time on November 1, 2018. Trinity stockholders of record as of 5:00 p.m. local New York City time on October 17, 2018 received one share of Arcosa common stock for every three shares of Trinity common stock held as of the record date.

The New Trinity

As a result of the spin-off, Trinity's focus will center on its integrated rail manufacturing, leasing, and services businesses while continuing to operate its highway products and logistics businesses.

"Today marks an exciting day for the future of Trinity Industries and our history of evolutionary growth," Timothy R. Wallace, Trinity's chairman, CEO and president, said. "I look forward to focusing our attention and resources on growth initiatives in the North American railcar industry while optimizing our capital structure to support our operational and financial objectives."

Trinity subsequently sold Trinity Highway Products in November 2021 to private equity firm Monomoy Capital in a $375 million cash deal, further concentrating the company on its rail platform.

The Arcosa spinoff represents a classic case of conglomerate simplification creating shareholder value. Both companies could now pursue distinct strategies with optimized capital structures, and investors could choose their preferred exposure rather than accepting a blended portfolio.

VIII. The Modern Era: Pure-Play Railcar Platform (2019–Present)

Leadership Transition

Wallace started with Trinity in 1975. He has been CEO and president of the company since 1999. Additionally, Wallace was chairman of the board at Trinity for 20 years, from 1999 to March 2019.

In September 2019, Tim Wallace announced his retirement after 45 years with the company. As Trinity's first female CEO following Tim Wallace's retirement after 45 years of service, Savage has also witnessed the welcome diversification of the people behind the industry.

Savage (55) has served as a member of Trinity's Board since November 2018 and brings significant executive experience in the industrial, engineering and rail transportation sectors. Ms. Savage most recently spent 17 years at Caterpillar Inc. in a variety of senior leadership positions.

Jean Savage brought a distinctive background to the CEO role. Ms. Savage began her career spending nine years as an Intelligence Officer in the U.S. Army Reserves. She has a bachelor's degree in electrical and computer engineering from the University of Cincinnati and a master's degree in engineering management from the University of Dayton.

Savage became the first non-family member—and the first woman—to take the helm when she became CEO and president in early 2020.

Her timing was challenging—she started the job just weeks before COVID-19 lockdowns began. But Savage brought exactly the skills Trinity needed: deep experience in cyclical industrial businesses, a track record of operational improvement, and fresh eyes on a company that had been family-led for three generations.

Savage adheres to a style of leadership honed during her military service and peppered with the experience that she has gained during previous tenures at both heavy industrial firm Parker Hannifin, and Progress Rail. "The values for someone in the military really match well with those at Trinity. What I learned from the military was the servant leadership style – you are there to take the roadblocks away that let people do their job and unleash their talents."

Strategic Positioning

Under Savage, Trinity has articulated a clear identity: the company views itself primarily as a leasing company that is enabled by manufacturing and services capabilities. This represents a philosophical shift from historical positioning as a manufacturer that also leases.

"We are introducing our full year 2025 EPS guidance of $1.50 to $1.80. This guidance range reflects continued leasing revenue improvement, consistent operating margins, lower deliveries, and a higher proportion of deliveries to our lease fleet with slightly lower gains on lease portfolio sales in support of our net fleet investment targets."

Recent Performance

Full year reported EPS of $1.81 and adjusted EPS of $1.82; $0.44 improvement in adjusted EPS year over year · Full year cash flow from continuing operations of $588 million and net gains on lease portfolio sales of $57 million · Full year Return on Equity ("ROE") of 13.3% and Adjusted ROE of 14.6%.

Trinity delivered 17,570 railcars in 2024 with a year-end backlog of $2.1 billion.

The company has maintained disciplined capital allocation, targeting 12-15% return on equity. Trinity Industries (NYSE:TRN) has announced a quarterly dividend of $0.30 per share on its common stock. This marks the company's 246th consecutive dividend payment, demonstrating a strong history of returning value to shareholders.

IX. Business Model Deep Dive: The Integrated Platform

Two-Segment Structure

Beginning January 1, 2024, Trinity reports its financial results in two reportable business segments: (1) Railcar Leasing and Services Group, formerly the Railcar Leasing and Management Services Group, and (2) Rail Products Group.

The Railcar Leasing and Services Group represents Trinity's recurring revenue engine. The segment leases freight and tank railcars, originates and manages railcar leases for third-party investors, and provides fleet management, maintenance, modification, and logistics services. As of recent reports, Trinity owns or manages approximately 144,000 railcars.

The Rail Products Group manufactures freight and tank railcars for transporting various liquids, gases, and dry cargo. This segment serves railroads, leasing companies, and industrial shippers across agriculture, construction, metals, consumer products, energy, and chemicals markets.

The "Flywheel" Effect

Trinity's integrated model creates powerful feedback loops. Manufacturing provides a source of new railcars for the lease fleet at cost, while the leasing relationship gives Trinity visibility into customer needs that inform product development. Maintenance operations extend asset life and keep customers engaged through the railcar lifecycle.

"In our Railcar Leasing and Services segment, our fleet of 144,000 owned and managed railcars have robust demand reflected in strong renewal rates."

The key metric that demonstrates pricing power is the Future Lease Rate Differential (FLRD). "In our Railcar Leasing and Services segment, our revenue is up 22% year over year, and we expect to continue to see growth as we re-price the lease fleet upward. Furthermore, our FLRD in the first quarter was 34.7%, representing a significant lift in market rates over expiring rates."

FLRD measures the differential between expiring lease rates and the rates on new or renewed leases. A positive FLRD means Trinity can re-price its fleet higher, driving organic revenue growth without fleet expansion. The metric has remained consistently positive, though it has moderated from peak levels.

Trinity's Q3 2025 results showed lease fleet utilization of 96.8% and Future Lease Rate Differential of positive 8.7% at quarter-end. While FLRD has compressed from the 30%+ levels seen in 2023-2024, it remains positive, indicating continued pricing momentum.

X. Playbook: Business & Investing Lessons

Consolidation Through Crisis

Trinity's most important strategic decisions came during industry downturns. The 1980s railcar collapse that devastated competitors became Trinity's consolidation opportunity. Making the best of these soft market conditions, Trinity acquired several of its weakened competitors, including Pullman Standard, once the largest freight car manufacturer in the United States.

The lesson: companies with strong balance sheets and long-term orientation can use industry distress to acquire assets at attractive prices. Trinity didn't just buy manufacturing capacity—it acquired intellectual property (railcar designs) that remains valuable decades later.

Business Model Evolution

Trinity's transformation from pure manufacturer to integrated leasing platform represents a classic shift from transactional to recurring revenue. Manufacturing is inherently cyclical—railcar orders can swing dramatically with economic conditions. Leasing provides a stable cash flow stream that persists through cycles.

2009 Trinity's lease fleet reaches 50,000 railcars and generates steady revenue, making it North America's fastest-growing railcar leasing company. The lease fleet has nearly tripled since then, and the strategic emphasis has shifted accordingly.

Spinoff as Value Creation

The Arcosa separation allowed both entities to optimize capital structures, pursue distinct strategies, and present clearer investment theses. "We believe that this strategic separation will enable both companies to enhance their competitive positions, advance distinct investment theses, and optimize their balance sheets and capital allocation priorities to achieve the best returns for their respective stockholders."

Disciplined Capital Allocation

Management has consistently emphasized returns over growth. Rather than chasing volume in manufacturing, Trinity targets 12-15% ROE and manages the manufacturing business within a tighter band than historical industry practice of dramatic ramping up and down.

Family Business Succession

Trinity successfully transitioned from family leadership to professional management. Led for 40 years by W. Ray Wallace, Trinity grew from two struggling propane tank companies into a $3 billion a year diversified manufacturer. Tim Wallace continued his father's legacy, and the transition to Jean Savage has maintained strategic continuity while bringing fresh perspective.

XI. Competitive Landscape & Porter's Five Forces Analysis

Major Competitors

The Greenbrier Companies competitors include Freightcar America, Trinity Industries, American Railcar Industries, and Wabtec Corporation.

The primary competitive landscape includes:

-

The Greenbrier Companies (GBX): In fiscal 2025, lease fleet growth of nearly 10%, to 17,000 units, with robust utilization of 98%. In Q4, new railcar orders for 2,400 units valued at more than $300 million and deliveries of 4,900 units, resulting in a new railcar backlog of 16,600 units with an estimated value of $2.2 billion.

-

GATX Corporation: The company is a leader in leasing transportation assets and controls one of the largest railcar fleets in the world.

-

Union Tank Car: Owned by Marmon Group (Berkshire Hathaway subsidiary), a significant tank car manufacturer and lessor.

Porter's Five Forces

1. Threat of New Entrants: LOW

The railcar industry presents formidable barriers to entry: - Capital intensity for manufacturing facilities runs into hundreds of millions - Decades of accumulated intellectual property in railcar designs - Regulatory expertise required for AAR and DOT compliance - Customer relationships built over generations - Scale economies in manufacturing and parts procurement

2. Bargaining Power of Suppliers: MODERATE

Steel is Trinity's primary input, and it's a commodity—multiple suppliers compete for business. However, specialized components (wheels, couplers, brakes) require specific suppliers. Trinity's scale provides leverage, and the company has pursued vertical integration in some components.

3. Bargaining Power of Buyers: MODERATE

Trinity serves diverse customers including Class I railroads, leasing companies, and industrial shippers. Large customers have negotiating leverage, but specialized railcar designs create switching costs. "Market dynamics are favorable, with a fleet utilization of 96.8% and an FLRD of 17.9%." High utilization rates indicate pricing power.

4. Threat of Substitutes: MODERATE-LOW

Rail remains the most cost-effective mode for bulk commodities over long distances. Trucking competes on shorter hauls but faces driver shortages, fuel costs, and capacity constraints. "In 2006 in the U.S., rail had 33 percent of modal share, and by 2019 we had 27 percent. Since the Great Recession while all other modes of transportation went up by 20 percent, rail volumes remained nearly constant."

Environmental regulations increasingly favor rail given its superior fuel efficiency—trains move a ton of freight an average of nearly 500 miles per gallon of fuel, three to four times more efficient than trucks.

5. Industry Rivalry: HIGH

Competition among surviving players is intense. "Fiscal 2025 was a record year for Greenbrier, demonstrating the continued success of our strategy to deliver consistent, high-quality performance," said Lorie L. Tekorius, CEO and President. "As we enter fiscal 2026, we are navigating the current North American and European freight rail markets with a resilient business model, growing lease fleet, and continued productivity gains."

Industry consolidation has reduced the number of competitors but intensified competition among survivors who compete on price, product innovation, and service capabilities.

XII. Hamilton's Seven Powers Analysis

1. Scale Economies: STRONG

Trinity holds roughly 22% market share in North American railcar manufacturing, creating significant purchasing leverage with steel suppliers and component manufacturers. Manufacturing facilities operate with fixed costs that decline on a per-unit basis as volumes increase. The 140,000+ railcar lease fleet generates administrative efficiencies impossible for smaller lessors.

2. Network Economies: MODERATE

Trinity's platform benefits from network effects in its maintenance and logistics businesses. More railcars under management creates denser geographic coverage for maintenance facilities, reducing transit time for repairs. Customer data from 700+ customers improves demand forecasting and product development.

3. Counter-Positioning: MODERATE

Trinity's integrated model—combining manufacturing, leasing, and services—represents counter-positioning against pure-play competitors. Pure lessors like GATX must purchase railcars from manufacturers; pure manufacturers like Freightcar America miss recurring lease revenue. Adopting Trinity's model would require competitors to cannibalize existing business or make massive capital investments.

4. Switching Costs: MODERATE-HIGH

Customers face meaningful switching costs: - Long-term lease agreements (typically 5-10 years) - Specialized railcar configurations customized to commodity needs - Maintenance relationships and parts availability - Fleet management systems integration

5. Branding: LOW

Railcars are industrial products purchased by sophisticated buyers on performance specifications and economics. Brand premium is minimal; procurement decisions are analytical rather than emotional.

6. Cornered Resource: MODERATE

Trinity's intellectual property portfolio—comprising railcar designs acquired over decades from Pullman-Standard, Thrall, GATC, and others—represents a cornered resource. Our comprehensive library includes drawings from TrinityRail as well as former car builders like Thrall, Ortner Freight Car, Greenville Steel Car, Pullman Standard, and Whitehead & Kales. This enables manufacturing of virtually any railcar type and parts for legacy fleets.

7. Process Power: MODERATE

Decades of manufacturing experience have created operational knowledge embedded in workforce skills, production processes, and quality systems. The Mexico manufacturing facility provides cost advantages through labor arbitrage while maintaining quality standards.

XIII. Key Performance Indicators for Investors

For long-term investors tracking Trinity Industries, three KPIs deserve particular attention:

1. Lease Fleet Utilization Rate

This measures the percentage of Trinity's owned lease fleet that is under active lease agreements. Current levels around 96-97% indicate robust demand and limited excess capacity in the market. Utilization below 90% would signal overcapacity and pricing pressure; sustained levels above 95% indicate pricing power.

2. Future Lease Rate Differential (FLRD)

FLRD measures the percentage difference between expiring lease rates and rates on new or renewed leases. A positive FLRD indicates Trinity can re-price its fleet higher, driving organic revenue growth. FLRD peaked above 30% in early 2024 and has moderated to single digits in late 2025, reflecting a normalizing rate environment. Sustained negative FLRD would signal competitive pressure and declining pricing power.

3. Adjusted Return on Equity (ROE)

Management targets 12-15% Adjusted ROE, and this metric captures the efficiency of capital deployment across the integrated platform. Full year Return on Equity ("ROE") of 13.3% and Adjusted ROE of 14.6%. Sustained performance within this target range validates the strategic focus on returns over growth.

XIV. Bull Case and Bear Case

Bull Case

Rail's Structural Advantages Are Durable: Rail remains three to four times more fuel-efficient than trucking, and environmental regulations increasingly favor lower-carbon transportation modes. As ESG considerations influence logistics decisions, rail should capture modal share.

Integrated Platform Creates Competitive Moat: Trinity's combination of manufacturing, leasing, and services creates customer relationships that persist through the railcar lifecycle. Pure-play competitors cannot easily replicate this model.

Cyclical Positioning Is Favorable: The North American railcar fleet is aging, with significant portions approaching replacement age. The current North American railcar fleet is aging and in need of updating. The fleet currently consists of more than 1.6 million railcars, with over 200,000 in the U.S. being more than 40 years old. Estimates indicate that nearly 250,000 freight railcars will become obsolete and require replacement within the next 15 years.

Recurring Revenue Provides Stability: The shift toward leasing means Trinity's revenue stream is less cyclical than historical manufacturing-centric business models.

Bear Case

Rail Modal Share Continues Declining: "In 2006 in the U.S., rail had 33 percent of modal share, and by 2019 we had 27 percent." If this secular decline continues, demand for railcars will remain structurally pressured regardless of fleet age.

Manufacturing Cyclicality Creates Earnings Volatility: Despite the leasing cushion, Trinity remains exposed to railcar manufacturing cycles. For 2025, Trinity projects industry deliveries of approximately 35,000 railcars, a 20% decrease from 2024.

Competitive Pressure from Greenbrier: For the full fiscal year 2025, Greenbrier achieved record earnings of $6.35 per diluted share. Strong competitor performance indicates a rational competitive environment, but also suggests limited market power for any single player.

Interest Rate Sensitivity: As a capital-intensive leasing business, Trinity's economics are sensitive to financing costs. Higher interest rates increase funding costs for fleet investments.

Regulatory Risk: The guardrail scandal demonstrated that regulatory compliance failures can create existential risks. While Trinity has addressed the specific guardrail issues, the broader lesson about regulatory exposure remains relevant.

XV. Conclusion: The Mule Barn to the Modern Railroad

Trinity Industries' ninety-year journey from a Dallas mule barn to North America's railcar leader offers lessons that transcend the specifics of steel fabrication and rail transport.

First, industry crises create consolidation opportunities for companies with strong balance sheets and long-term orientation. Trinity's systematic acquisition of distressed competitors during the 1980s railcar collapse built competitive advantages that endure decades later.

Second, business model evolution matters as much as operational excellence. Trinity's transformation from pure manufacturer to integrated leasing platform fundamentally changed the company's risk profile and value proposition.

Third, family businesses can successfully transition to professional management while maintaining strategic continuity. Ray Wallace built the foundation, Tim Wallace scaled the empire, and Jean Savage is optimizing the platform—each generation contributing distinctive capabilities.

Fourth, regulatory and ethical failures can threaten even dominant market positions. The ET Plus guardrail scandal demonstrated that $50,000 in annual savings could create hundreds of millions in potential liability.

Finally, strategic focus creates value. The Arcosa spinoff allowed Trinity to present a clearer investment thesis, optimize capital allocation, and pursue a distinctive strategy.

Now, under the leadership of President and CEO, Jean Savage, Trinity performs as a wholly rail-focused entity. "The company has a long history in diversified industrial products," she explains. "Now, Trinity is one of the top five railcar lessors in North America, and we also specialize in new railcar manufacturing and maintenance."

From butane tanks in a converted barn to over 140,000 railcars crossing the continent, Trinity Industries demonstrates that industrial success isn't about avoiding cycles—it's about building capabilities that compound through them.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube