Targa Resources: The Pipeline to Prosperity

I. Introduction & Opening Thesis

Picture this: It's 2003, and in a Warburg Pincus conference room overlooking Park Avenue, a group of private equity partners are staring at a map of Texas dotted with aging pipelines, processing plants, and storage facilities. The assets look unremarkable—rusted steel and concrete scattered across scrubland. But they see something else entirely: the skeletal structure of what would become America's energy superhighway.

Twenty years later, Targa Resources stands as a Fortune 500 colossus, commanding a $40+ billion enterprise value and moving enough natural gas liquids to fuel entire economies. The company processes nearly 5 billion cubic feet of natural gas daily—enough to heat 50 million homes—and operates the crown jewel of American energy infrastructure: the Grand Prix pipeline system that connects the Permian Basin's bounty to global markets. The central question driving this story isn't just how a company grows—plenty do that. It's how a private equity rollup, birthed in the boom years of energy financialization, transformed into the critical infrastructure backbone connecting America's shale revolution to global markets. This is the story of perfect timing meeting relentless execution, of boring pipes becoming profit machines, and of how Warburg Pincus and a team of energy veterans built what competitors now call "the uncopyable asset."

Targa Resources today commands a market cap exceeding $40 billion, but its true moat lies not in size but in strategic positioning. While tech unicorns grab headlines, Targa quietly became the tollbooth operator for American energy independence, processing and transporting the natural gas liquids that fuel everything from plastics manufacturing to winter heating across continents.

The midstream sector—that unglamorous middle child between upstream drilling and downstream refining—rarely captures imaginations. Yet it's precisely this invisibility that makes it so powerful. Producers need to move their product. Refiners need reliable supply. Targa sits in between, collecting fees regardless of whether oil trades at $40 or $140. It's the picks-and-shovels play of the modern energy economy, except the picks are billion-dollar pipelines and the shovels are fractionation towers that turn mixed hydrocarbons into money.

What follows is a deep dive into how strategic location, patient capital, and impeccable timing created one of energy's great success stories—a company that went from PowerPoint slides to the S&P 500 in under two decades.

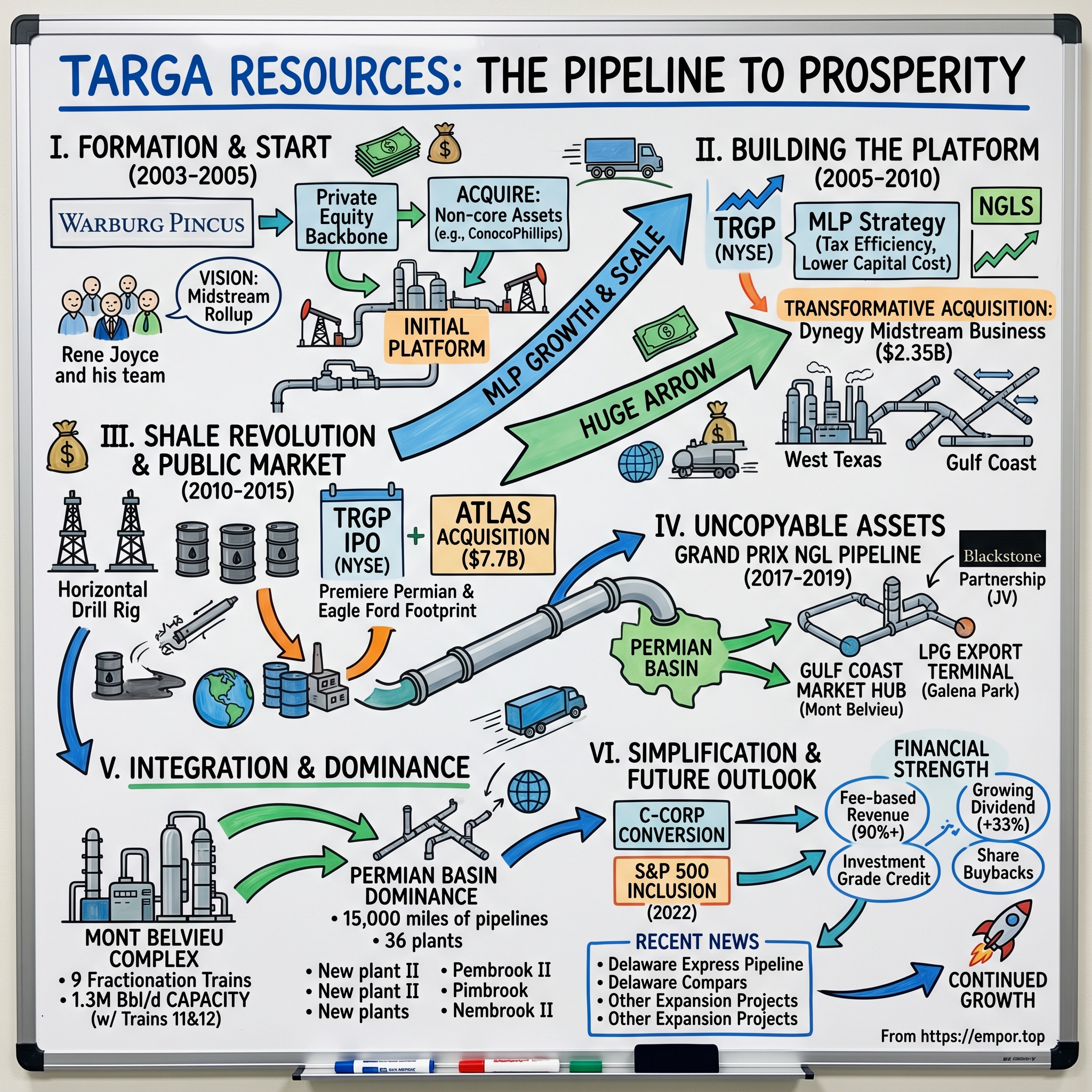

II. The Warburg Pincus Formation Story (2003–2005)

The year 2003 marked a peculiar moment in American energy. Natural gas prices were volatile, swinging from $2 to $10 per thousand cubic feet within months. The shale revolution was still a decade away from mainstream recognition. And in the gleaming offices of Warburg Pincus, the private equity firm's energy team was hunting for their next big play. In 2003, Targa Resources was formed by Warburg Pincus and an experienced management team in order to build a leading midstream energy company through acquisitions and reinvestment in oil and gas gathering, processing, storage, and transmission assets. The architect of this vision was Rene Joyce, a Houston energy veteran who'd spent the 1990s building Tejas Gas Corporation from a regional player into a $2.4 billion enterprise before Shell acquired it.

Joyce wasn't your typical CEO. Rene R. Joyce, CEO of Targa Resources, formed the Company last year with a veteran management team with over 140 years of collective experience in acquiring and managing midstream assets. He'd seen the boom-bust cycles, understood the importance of fee-based revenue, and most crucially, recognized that the midstream sector was ripe for consolidation. The fragmented ownership of gathering systems, processing plants, and pipelines across Texas created inefficiencies that smart capital could exploit.

The investment thesis was elegantly simple: acquire underperforming or non-core midstream assets from major oil companies, stabilize operations through better management, then reinvest cash flows into high-return expansion projects. It was the classic private equity playbook—buy, improve, expand—but applied to an industry where location and scale created natural monopolies.

Targa Resources, Inc., an independent company formed in 2003 by management and Warburg Pincus to pursue gas gathering, processing, and pipeline asset acquisition opportunities, announced today that it has signed a definitive agreement to acquire major midstream assets owned by ConocoPhillips in Texas and Louisiana. Targa and ConocoPhillips have already received all necessary regulatory and other approvals, and the Company expects to close the transaction in April of 2004.

This wasn't Warburg's first rodeo in energy. Warburg Pincus has invested approximately $1.1 billion in energy companies since the late 1980s, predominantly in exploration and production, power, oilfield and other services. But Targa represented something different: a platform investment designed to roll up an entire sector.

The ConocoPhillips acquisition was transformative. The Texas assets consist of an integrated gathering and processing system with approximately 1,200 miles of low and high-pressure lines, gathering from approximately 2,800 wells and 750 wellhead and central delivery locations in the Permian Basin, covering parts of eight counties from San Angelo to Big Springs. The Louisiana assets also consist of an integrated gathering and processing system, covering approximately 2,000 square miles from Lake Charles to Lafayette, with approximately 700 miles of pipeline and processing capacity of about 260 MMcfd and 14 MBD of NGL raw mix production.

For context, these weren't trophy assets. ConocoPhillips was divesting non-core infrastructure to focus on exploration and production. But Joyce and his team saw opportunity where others saw aging steel. These systems connected thousands of wells to processing facilities and ultimately to markets. Once you controlled the gathering lines, producers had little choice but to flow their gas through your system. It was the ultimate toll road.

The management team consists of Rene Joyce, CEO; Roy Johnson, EVP; Joe Bob Perkins, President; Mike Heim, COO, and Jeff McParland, CFO. This wasn't just a collection of executives—it was a reunion of the Tejas Gas brain trust, reassembled to execute a familiar playbook in a new era.

The private equity model brought discipline to an industry often driven by boom-time exuberance. Every acquisition had to meet strict return thresholds. Every expansion project needed contracted volumes. And unlike the public companies they'd eventually compete with, Targa could move fast, closing deals while competitors were still scheduling board meetings.

By late 2004, the foundation was set. But acquiring assets was just the beginning. The real challenge—and opportunity—lay in transforming these scattered pieces into an integrated, efficient midstream machine. That transformation would require a different kind of financial engineering: the master limited partnership.

III. Building the Platform: Early Acquisitions & MLP Strategy (2005–2010)

October 27, 2005, marked Targa's official founding as an operating company, with headquarters established in Houston's energy corridor. But the real financial innovation came sixteen months later. In February 2007, Targa Resource Partners was established as an MLP and completed an IPO on NASDAQ under the symbol "NGLS". Targa retained a 39% ownership interest in NGLS, as well as incentive distribution rights.

The MLP structure was financial engineering at its finest. Master Limited Partnerships don't pay corporate taxes; instead, they pass through income directly to unitholders. For capital-intensive businesses like pipelines and processing plants, this tax efficiency translated into a lower cost of capital—a crucial advantage when competing for acquisitions. The real game-changer came in August 2005 when Targa announced it had entered into a definitive agreement with Dynegy Inc. to purchase Dynegy's Midstream natural gas business for $2.35 billion along with return of Dynegy's cash collateral and letters of credit. The acquisition closed in November, instantly catapulting Targa from a regional player to a major force. Dynegy's midstream assets were located in West Texas, southeast New Mexico, North Texas, and along the Texas and Louisiana Gulf Coast, including about 9,300 miles of natural gas gathering pipeline systems and 11 operated gas plants, stakes in six nonoperated gas plants and in three stand-alone fractionation facilities and strategic storage, transportation and terminalling facilities, as well as NGL transportation and logistics assets throughout the United States.

The Dynegy acquisition was transformative not just for its scale but for its timing. Natural gas prices were surging toward historic highs, making midstream assets increasingly valuable. More importantly, Dynegy's existing 800-member workforce joined Targa, bringing institutional knowledge and operational expertise that would prove invaluable.

Joyce and his team now controlled an integrated midstream platform spanning the value chain from wellhead to waterway. But they needed more capital to fund growth. Enter the MLP.

The February 2007 IPO of Targa Resources Partners was a masterclass in financial structuring. By dropping assets down to the MLP while retaining control through the general partner and incentive distribution rights (IDRs), Targa created a virtuous cycle. The MLP would acquire assets from the parent, fund expansions through public markets, and kick increasing cash distributions back up to Targa Resources Inc. through the IDR waterfall.

This wasn't just financial engineering—it was strategic positioning for the coming shale boom. While nobody was using the term "shale revolution" yet, savvy operators could see the writing on the wall. Horizontal drilling and hydraulic fracturing were unlocking previously uneconomic reserves across Texas. These new wells needed gathering lines, processing plants, and takeaway capacity. Targa was building the infrastructure before the boom fully materialized.

The company continued its acquisition spree through the late 2000s, picking up additional assets from ConocoPhillips and expanding its footprint across key basins. Each deal followed the same playbook: acquire undervalued or non-core assets, improve operations, expand capacity, and drop down to the MLP at attractive multiples.

Warburg Pincus worked closely with management on the development of the business plan and on screening and evaluating the initial acquisitions. This wasn't passive private equity ownership—it was active partnership. The firm's networks opened doors to financing, its expertise guided strategy, and its patient capital allowed management to think long-term.

By 2010, the stage was set for the next phase: taking the parent company public and beginning the gradual exit of Warburg Pincus. The private equity firm had built a midstream giant from scratch. Now it was time to monetize that creation in the public markets, just as the shale revolution was about to explode.

IV. The IPO and Public Market Evolution (2010–2015)

December 2010 should have been a disaster for an energy IPO. Oil prices were volatile, natural gas was stuck below $5/MMBtu, and investors were still nursing wounds from the financial crisis. Yet when Targa executed an IPO on the New York Stock Exchange under the symbol "TRGP", the offering was oversubscribed. Wall Street saw what Warburg Pincus had been building: a toll road for the coming American energy renaissance.

The timing, in retrospect, was nearly perfect. The Haynesville Shale in Louisiana had proven that shale gas wasn't a one-basin phenomenon. The Eagle Ford in South Texas was beginning to show promise. And in West Texas, pioneers like EOG Resources were quietly proving that horizontal drilling could unlock oil—not just gas—from tight rock formations.

Warburg Pincus exited its investment between 2010 and 2013, a gradual withdrawal that avoided flooding the market while allowing new institutional investors to build positions. The private equity firm's returns were never publicly disclosed, but industry insiders estimate they made 3-5x their invested capital—a home run in the infrastructure space. But the real watershed moment came in October 2014 when Targa announced agreements to acquire Atlas Pipeline Partners, L.P. and Atlas Energy, L.P. The acquisitions were contingent on one another, and the transactions closed concurrently in February 2015. Atlas Pipeline Partners will be acquired by Targa Resources Partners L.P. in a transaction valuing Atlas Pipeline at $7.7 billion, including debt and general partner interests. The deal added gathering and processing positions in the Eagle Ford Shale, Anadarko Basin and Arkoma Basin, and created a premier combined Permian Basin footprint.

The Atlas acquisition wasn't just about scale—it was about strategic positioning. The combination created a midstream franchise with increased scale, geographic diversity and best in class capabilities in key producing basins in the U.S., and created one of the largest diversified MLPs on an enterprise value basis. The combined position across the Permian Basin enhanced service capabilities in one of the most active producing basins in North America, with a combined 1,439 MMcf/d of processing capacity and 10,250 miles of pipelines.

Joe Bob Perkins, who'd been president since the company's founding and would later become CEO, captured the strategic importance: "We have a leadership position in almost every basin, play, and market hub in which we participate. Where we participate is in the best basins and the best market hubs. It just doesn't get any better than that."

The timing was exquisite. Oil prices had begun their dramatic collapse in late 2014, falling from over $100/barrel to under $50 within months. While this devastated many energy companies, it created opportunities for well-capitalized midstream players. Distressed producers needed to maximize cash flow from existing wells. Processing and transportation became even more critical as margins compressed.

Moreover, the Atlas deal brought something invaluable: a massive footprint in the Eagle Ford Shale of South Texas, one of the most prolific liquids-rich plays in North America. This complemented Targa's existing Permian position perfectly, creating a corridor of infrastructure across Texas's most productive basins.

The financing of the deal showcased Targa's evolution as a public company. The company was able to secure $670 million when the merger was first announced (above its initial expectation of $350 million) as part of $1.1 billion of total committed financing. Capital markets had fully embraced the Targa story.

By 2015, Targa had transformed from a private equity portfolio company into a diversified midstream giant with assets spanning from the Bakken in North Dakota to the Gulf Coast of Louisiana. The company controlled critical infrastructure in every major shale play. But the next phase of growth would require something even more ambitious: building, not buying, the infrastructure for America's energy dominance.

V. The Grand Prix Pipeline: Targa's Crown Jewel (2017–2019)

In the summer of 2017, as West Texas crude production surged past 2.5 million barrels per day, Targa's executive team stood before a wall-sized map in their Houston war room. Red pins marked existing processing plants. Blue lines traced current pipelines. But it was the dotted yellow line—still just a proposal—that would define the company's future: the Grand Prix NGL Pipeline. The announcement came in May 2017: Targa would construct a new common carrier natural gas liquids pipeline from the Permian Basin. The capacity of the pipeline from the Permian Basin would be approximately 300 thousand barrels per day, expandable to 550 thousand barrels per day. Grand Prix would transport volumes from the Permian Basin, and also from Targa's North Texas system, to Targa's fractionation and storage complex in the NGL market hub at Mont Belvieu, Texas.

The strategic brilliance of Grand Prix wasn't just its scale—it was its integration. Unlike competitors who moved products piecemeal through multiple systems, Grand Prix created a superhighway directly connecting America's most prolific oil basin to the world's largest NGL trading hub. It was the energy equivalent of building a private autobahn between Silicon Valley and Wall Street.

Total growth capital for Grand Prix was expected to be $1.3 billion, with $250 million of spending in 2017. For context, this single project represented more capital investment than many midstream companies' entire asset base. But Targa's management saw what others missed: the Permian was just getting started.

"We are excited to be moving forward with Grand Prix, which will enhance our ability to move our customers' volumes from the wellhead in the Permian Basin and North Texas to key petrochemical and export markets," said Joe Bob Perkins, Chief Executive Officer of the Company. "Our ability to offer a highly competitive, fully integrated model, from gathering and processing through transportation and fractionation, to current and future customers should drive continued growth for Targa in both our Gathering and Processing and Downstream segments."

The project attracted heavyweight partners. In October 2017, Targa agreed to sell a 25% stake to Blackstone Energy Partners for an undisclosed amount. Blackstone's EagleClaw Midstream Ventures LLC also executed a long-term raw product purchase agreement for transportation and fractionation services, with EagleClaw agreeing to dedicate and commit liquids associated with its gas volumes produced or processed in the Permian Delaware sub-basin.

Construction proceeded at breakneck speed. By August 2019, Houston-based Targa Resources commenced full operations of its $1.4 billion Grand Prix NGL pipeline from Permian Basin to Mont Belvieu. Initial flows of 150,000 to 170,000 barrels per day quickly ramped up, with expectations for volumes to increase to approximately 200,000 barrels per day in September, then further increase over the balance of 2019.

The performance exceeded all projections. "The performance of our Grand Prix NGL Pipeline has exceeded expectations since it began full operations in the third quarter of 2019," management would later note. What started as a 300,000 barrel per day system expandable to 550,000 had grown even larger. Grand Prix has capacity to transport up to 1 million barrels per day of natural gas liquids to the NGL market hub at Mont Belvieu, Texas.

But Targa wasn't done. In January 2023, the company announced it would acquire Blackstone Energy Partners' 25% interest in Targa's Grand Prix NGL Pipeline for $1.05 billion. The acquisition price represented about 8.75 times Grand Prix's estimated 2023 adjusted EBITDA multiple—a testament to the pipeline's extraordinary cash generation.

Grand Prix had become what industry insiders called "the uncopyable asset." Building a similar pipeline today would cost multiples of Targa's investment, assuming you could even get the permits. Environmental opposition, landowner resistance, and regulatory hurdles had made new long-haul pipelines nearly impossible. Targa had built its moat just before the drawbridge went up.

The pipeline didn't just move molecules—it transformed Targa's entire business model. With Grand Prix operational, Targa could guarantee producers in the Permian a direct path to global markets while ensuring its Mont Belvieu fractionation complex had steady supply. It was vertical integration at its finest, creating value at every link in the chain from wellhead to waterway.

VI. Mont Belvieu & Downstream Integration

Mont Belvieu, Texas, sits 30 miles east of Houston, a cluster of industrial facilities surrounded by cattle ranches and rice fields. To the casual observer, it's unremarkable. To the energy industry, it's the beating heart of America's petrochemical complex—and Targa controls one of its largest fractionation operations.

At Targa's Mont Belvieu operated facility, the company has nine wholly-owned fractionation trains, representing an aggregate capacity of 963.0 MBbl/d and Train 7, a 120 MBbl/d fractionation train, which is a joint venture between Targa and The Williams Companies, Inc., where Targa owns an 80% equity interest. The scale is staggering: over one million barrels per day of fractionation capacity, enough to supply feedstock for plastics manufacturing across the continent.

Fractionation is the alchemy of the midstream business. Mixed NGLs arrive as an undifferentiated soup of hydrocarbons. Through precise heating and cooling in towering fractionation columns, this mixture separates into distinct products: ethane for plastics, propane for heating, butane for gasoline blending, and natural gasoline for fuel production. Each product trades at different prices, serves different markets, and requires different logistics. Master this complexity, and you print money.

The expansion never stops. Targa is constructing Trains 11 and 12, both of which are wholly-owned 150 MBbl/d fractionation trains, at its Mont Belvieu operated facility, which are expected to begin operations in the third quarter of 2026 and the first quarter of 2027, respectively. When complete, Targa's Mont Belvieu complex will process nearly 1.3 million barrels per day—more volume than many oil refineries.

But fractionation is just one piece of the downstream puzzle. Targa's fractionation trains are fully integrated with existing Gulf Coast NGL storage, terminaling and delivery infrastructure, which includes an extensive network of connections to key petrochemical and industrial customers as well as the LPG export terminal at Galena Park on the Houston Ship Channel.

The Galena Park terminal represents another strategic masterstroke. As America transformed from energy importer to exporter, international demand for U.S. propane and butane exploded. Asian petrochemical plants, Mexican households, and European autogas stations all wanted American NGLs. Targa's export terminal, with its deep-water dock access and massive storage capacity, became a crucial link to these global markets.

Storage itself is a hidden profit center. In general, Targa's NGL storage assets provide warehousing of mixed NGLs, NGL products and petrochemical products in underground wells, which allows for the injection and withdrawal of such products at various times in order to meet supply and demand cycles. When winter heating demand spikes, Targa can withdraw stored propane at premium prices. When summer driving season boosts gasoline demand, butane commands top dollar. It's commodity trading with a physical edge.

The integration creates powerful network effects. A barrel of mixed NGLs entering Grand Prix from the Permian can be fractionated at Mont Belvieu, stored in underground caverns, and exported from Galena Park—all without leaving Targa's system. Each step generates fees, and controlling the entire chain means capturing value that competitors leave on the table.

The expansion plans tell the story of expected growth. Beyond Trains 11 and 12, Targa continues evaluating additional fractionation capacity, storage expansion, and export infrastructure. The company's Downstream facilities are located predominantly in Mont Belvieu and Galena Park, Texas, positioning them perfectly to serve both domestic petrochemical demand and international export markets.

This downstream complex isn't just infrastructure—it's irreplaceable infrastructure. Environmental permits for new fractionation facilities take years. Underground storage caverns require specific geological formations that don't exist everywhere. Export terminals need deep-water access and extensive permitting. Targa built or acquired these assets when it was still possible. Today, the barriers to entry are nearly insurmountable.

The financial performance reflects this moat. The Logistics and Transportation segment, which includes Mont Belvieu operations, generates stable, fee-based cash flows with minimal commodity exposure. Fractionation spreads might fluctuate, but the tolls for moving and processing NGLs remain steady. It's the definition of a wide-moat business: essential service, high barriers to entry, and growing demand.

As petrochemical companies expand along the Gulf Coast, as LNG plants proliferate, as global demand for plastics feedstock grows, Mont Belvieu becomes ever more critical. And Targa, with its massive fractionation complex at the center of it all, collects its toll on America's energy abundance.

VII. The Permian Dominance Strategy

The Permian Basin sprawls across 86,000 square miles of West Texas and southeastern New Mexico, a seemingly endless expanse of mesquite, pump jacks, and desert. But beneath this austere landscape lies the most prolific oil and gas field in American history. And above ground, Targa has methodically built the largest gathering and processing position in the basin. The numbers tell the story of dominance. The Permian Midland system consists of approximately 7,600 miles of natural gas gathering pipelines and 19 processing plants with an aggregate processing capacity of 3,844 MMcf/d, all located within the Permian Basin in West Texas. The Permian Delaware system consists of approximately 7,400 miles of natural gas gathering pipelines and 17 processing plants with an aggregate capacity of 3,285 MMcf/d, within the Delaware Basin and Central Basin in West Texas and Southeastern New Mexico.

Combined, Targa operates over 15,000 miles of gathering pipelines and 36 processing plants with over 7 billion cubic feet per day of capacity across the Permian—infrastructure that would cost tens of billions to replicate today, if it could be built at all.

The growth trajectory has been relentless. In a separate Nov. 5 presentation to investors, Targa said its 43 Permian gas processing plants have an overall processing capacity of 8.8 bcfd, including 4.7 bcfd in Midland basin and 4.1 bcfd in Delaware basin. Every quarter brings announcements of new plants: Greenwood, Pembrook, Bull Moose, Falcon, East Driver—names that mean nothing to outsiders but represent hundreds of millions in capital investment and decades of cash flow generation.

The strategy goes beyond just building capacity. Targa has positioned its plants at strategic locations where multiple producers converge, creating natural aggregation points. Producers face a simple choice: connect to Targa's existing system or spend millions building their own gathering lines to distant competitors. Geography becomes destiny.

Recent bolt-on acquisitions have consolidated this dominance. In 2017, Targa acquired Outrigger Delaware Operating, LLC, Outrigger Southern Delaware Operating, LLC and Outrigger Midland Operating, LLC, adding critical acreage dedications in the core of the Delaware Basin. In 2022, Targa acquired Southcross Energy Operating LLC for $200 million.

But the real genius lies in the integration with Grand Prix and Mont Belvieu. Unlike competitors who might gather and process gas in the Permian but then hand it off to third parties for transportation and fractionation, Targa controls the entire value chain. A molecule of natural gas entering a Targa gathering line in Reeves County can travel all the way to Asian markets without ever leaving Targa's system.

The producer relationships tell the story. Eleven of these plants and approximately 5,300 miles of gathering pipelines belong to a joint venture ("WestTX"), in which we have an approximate 72.8% ownership. Exxon Mobil Corporation owns the remaining interest in the WestTX system. When Exxon, one of the world's most sophisticated energy companies, chooses to partner rather than compete, it validates the strategy.

The expansion continues at a breathtaking pace. In response to increasing production and to meet the infrastructure needs of producers, we are constructing the Pembrook II plant, East Pembrook plant and East Driver plant, each a 275 MMcf/d cryogenic natural gas processing plant, which are expected to begin operations in the third quarter of 2025, the second quarter of 2026 and the third quarter of 2026, respectively.

Each new plant costs $200-300 million, but the returns are compelling. With 10-20 year contracts from investment-grade producers, minimal commodity exposure, and strategic locations that become more valuable as surrounding production grows, these investments generate returns well above Targa's cost of capital.

The Daytona Pipeline expansion adds another layer to the dominance strategy. In other operational updates, Targa said it began operations ahead of schedule and under budget on its 400,000-b/d Daytona NGL pipeline in third-quarter 2024. This new pipeline creates additional takeaway capacity from the Permian to Grand Prix, ensuring Targa can handle the expected surge in NGL production through the decade.

The moat around this Permian empire grows wider each year. Environmental opposition makes new gathering systems nearly impossible to permit. Existing rights-of-way become more valuable. First-mover advantage compounds. What started as a collection of acquired assets has evolved into an integrated machine that would take competitors decades and tens of billions to replicate—assuming they could get the permits, which they likely couldn't.

VIII. Capital Structure Evolution & Simplification

The path from complex MLP structure to simple C-corporation reads like a masterclass in financial engineering. What began as a necessary evil—the MLP dropdown model that funded growth but created conflicts—evolved into today's streamlined structure that institutional investors can actually understand. The journey to simplification began with recognition of a fundamental problem: the MLP structure that had funded Targa's growth was now constraining it. Institutional investors, particularly index funds and international buyers, couldn't or wouldn't own MLPs due to tax complications. The K-1 tax forms scared off retail investors. The IDR waterfall created misalignment between the general partner and limited partners.

The solution came through a series of strategic moves that would take years to execute. First, Targa began buying back the public units of Targa Resources Partners, slowly increasing its ownership stake. The complex incentive distribution rights were restructured, then eliminated. Debt was refinanced at the parent level rather than the MLP.

The crowning achievement came in October 2022: Targa Resources Corp joined the S&P 500 prior to the opening of trading on Wednesday. The Houston, TX-headquartered midstream energy infrastructure corporation moved up from the S&P MidCap 400. With the addition of Targa, there are four midstream companies included in the S&P 500 as of October 12: Kinder Morgan Inc, ONEOK, Williams Companies, and Targa.

This wasn't just a symbolic victory. S&P 500 inclusion triggers automatic buying from index funds managing trillions in assets. It signals institutional legitimacy. It opens doors to investment mandates that explicitly require S&P 500 membership. The stock's liquidity improves, borrowing costs decline, and the multiple expands.

The transformation reflects a broader industry trend. Many MLPs have converted to traditional C-corporations to attract a broader range of investors and simplify tax reporting. But Targa executed the transition while maintaining growth, increasing distributions, and expanding operations—a threading of the needle that many peers failed to achieve.

Today's capital structure is elegantly simple: a single class of common stock, traditional corporate debt, and straightforward financial statements. No IDRs, no complex waterfall calculations, no K-1s. Just a C-corporation generating substantial free cash flow and returning it to shareholders through dividends and buybacks.

The dividend story illustrates the transformation. From volatile MLP distributions dependent on commodity prices and growth capital needs, Targa evolved to steady, growing dividends backed by fee-based cash flows. The company now targets returning 35-50% of free cash flow to shareholders through dividends, with the remainder available for opportunistic buybacks.

Capital allocation has become more disciplined. Gone are the days of growth at any cost, replaced by strict return thresholds and strategic focus. Recent acquisitions like the $1.05 billion purchase of Blackstone's 25% stake in Grand Prix show the new approach: buy assets you already know, at reasonable multiples, that immediately enhance cash flow.

The balance sheet tells the story of financial strength. Investment-grade credit ratings, access to commercial paper markets, and a $3.5 billion revolving credit facility provide ample liquidity. Debt maturities are well-laddered, interest coverage is robust, and leverage ratios remain within the targeted 3.0-4.0x range.

Tax efficiency hasn't been abandoned—just restructured. While Targa now pays corporate taxes, the company's massive depreciation from its infrastructure investments provides significant shields. The 2023 estimated effective cash tax rate was just 10-15%, far below the statutory rate.

The investor base transformation is remarkable. Where once retail investors and MLP-focused funds dominated, today's shareholder register includes Vanguard, BlackRock, State Street, and other institutional giants. These stable, long-term owners provide a foundation for continued growth without the volatility of hot money flows.

Simplification has created optionality. Targa can now pursue larger acquisitions using stock as currency. International investors can buy without tax complications. The company can tap global debt markets efficiently. What started as necessary financial engineering has become a competitive advantage, allowing Targa to access capital on terms that MLP-structured competitors cannot match.

IX. Business Model Deep Dive & Unit Economics

Strip away the complexity of fractionation towers and pipeline networks, and Targa's business model reduces to elegant simplicity: charge tolls for essential services that connect energy supply with demand. But the unit economics underlying this toll road reveal why some midstream companies print money while others struggle to cover their distributions. The two-segment structure creates clarity. Gathering and Processing handles the upstream work—connecting wells to plants, removing impurities, extracting NGLs. Logistics and Transportation manages the downstream—moving, fractionating, storing, and exporting products. Each segment has distinct economics, risk profiles, and growth trajectories.

The Company reported adjusted earnings before interest, income taxes, depreciation and amortization, and other non-cash items ("adjusted EBITDA") of $966.2 million for the first quarter of 2024. For the full year, the Company estimates full year adjusted EBITDA to be above the top end of its $4.05 billion range. These aren't just big numbers—they represent EBITDA margins approaching 40%, extraordinary for an industrial business.

The fee-based model provides the foundation. Approximately 90% of Targa's gross margin comes from fee-based activities—gathering fees per thousand cubic feet, processing fees per gallon of NGLs extracted, transportation tariffs per barrel-mile, fractionation fees per barrel processed. These fees typically include annual escalators and minimum volume commitments, creating predictable cash flows even when commodity prices gyrate.

But the real magic happens in the contract structures. Take a typical Permian gathering agreement: a producer dedicates all production from specified acreage for 10-20 years, guarantees minimum volumes that ratchet up over time, and pays fees that escalate with inflation. If volumes exceed projections, Targa wins. If they fall short but stay above minimums, Targa still wins. Only in catastrophic scenarios does Targa lose.

The commodity exposure that remains is carefully managed. While pure fee-based businesses might seem ideal, some commodity sensitivity actually enhances returns when managed properly. Targa retains certain volumes as payment for services, sells at optimal times, and benefits from location and quality differentials. When Permian gas trades at a discount to Henry Hub, Targa's transportation assets capture that spread. When propane demand spikes in winter, storage positions pay off.

Return on invested capital tells the story of value creation. A new processing plant might cost $250 million but generate $40-50 million in annual EBITDA once ramped—a 20% unlevered return. A pipeline expansion might cost $500 million but produce $75 million in EBITDA—a 15% return. These returns, sustained over 20-30 year asset lives, create enormous value.

The network effects amplify unit economics. Each new gathering line makes the processing plant more valuable. Each processing plant makes the Grand Prix pipeline more valuable. The pipeline makes Mont Belvieu fractionation more valuable. Fractionation makes export facilities more valuable. It's a virtuous cycle where 1+1 equals 3.

Operating leverage is substantial. In the G&P segment, higher sequential adjusted operating margin was attributable to record Permian natural gas inlet volumes and higher fees. Once a plant is built, incremental volumes flow through at 70-80% margins. Fixed costs are largely covered by minimum volume commitments, so growth volumes are extraordinarily profitable.

The maintenance capital requirements are surprisingly modest—typically 2-3% of gross PP&E annually. These aren't manufacturing plants requiring constant retooling. Pipelines and processing facilities, properly maintained, last decades. This translates into substantial free cash flow generation once the growth spending moderates.

Working capital dynamics favor Targa. The company typically gets paid monthly for services while paying suppliers on longer cycles. In growth periods, this creates a natural funding source. In steady state, it's a permanent source of free capital.

The transportation and logistics segment showcases pricing power. Pipeline transportation and fractionation volumes benefited from higher supply volumes primarily from the Company's Permian Gathering and Processing systems. When you control the only pipeline from A to B, you set the tolls. When you own one of the few fractionation complexes at the market hub, you have pricing leverage.

Marketing and optimization add alpha. Marketing margin increased due to greater optimization opportunities. This isn't speculation—it's using physical assets and market knowledge to capture inefficiencies. Store propane in summer when it's cheap, sell in winter when it's dear. Buy distressed volumes from producers, blend and sell to premium markets. These opportunities exist because Targa has the infrastructure to execute them.

The capital efficiency has improved dramatically over time. Early plants might have cost $150,000 per MMcf/d of capacity. Today, through standardization and scale, new plants are built for under $100,000 per MMcf/d. This improving capital efficiency drops straight to returns.

X. Competitive Landscape & Industry Dynamics

The midstream sector resembles a medieval battlefield where position matters more than size. Enterprise Products Partners, with its $160 billion enterprise value, may be the giant, but Targa's strategic positioning in the Permian and vertical integration through Grand Prix creates competitive advantages that pure scale cannot replicate. The competitive dynamics in midstream resemble trench warfare more than blitzkrieg. According to Bloomberg, energy stocks comprise 5.2% of the S&P 500 Index, with four midstream companies included in the S&P 500: Kinder Morgan Inc, ONEOK, Williams Companies, and Targa. Each has carved out distinct territories and strategies.

Enterprise Products Partners remains the 800-pound gorilla, with over 50,000 miles of pipelines and a fully integrated value chain from wellhead to waterway. But size alone doesn't guarantee victory. Enterprise's commodity price exposure—13% of gross margin—exceeds Targa's more fee-based model. In the midstream game, predictability trumps scale.

ONEOK's recent acquisition of Magellan Midstream Partners for $18.8 billion represents the consolidation wave sweeping the sector. ONEOK is a leading midstream service provider focused on natural gas and NGLs, with gathering, processing, storage, and transportation assets primarily located in key production basins. The deal creates overlap with Targa in the Permian but also highlights different strategic priorities—ONEOK focuses on refined products while Targa dominates NGLs.

Kinder Morgan owns an interest in or operates approximately 83,000 miles of pipelines and 143 terminals, making it the pipeline colossus. But Kinder's broad exposure across multiple commodities and basins dilutes its Permian focus. Where Targa built Grand Prix as a dedicated NGL superhighway, Kinder's Gulf Coast Express Pipeline moves natural gas—a different product, different economics, different customers.

Williams Companies operates a vertically integrated business model that encompasses the entire natural gas value chain, with its crown jewel being the Transco pipeline system. Williams' main competitors include Kinder Morgan, Enbridge, TC Energy, Enterprise Products Partners, and ONEOK. But Williams' focus on interstate natural gas transmission creates limited overlap with Targa's NGL-centric model.

The competitive moats vary by geography and product. In the Permian, physical proximity to production matters most. Targa's 15,000 miles of gathering lines create density that competitors can't economically replicate. A producer would need to lay miles of expensive pipe to reach a competing plant—economics that rarely pencil out.

In NGL transportation, the barriers are even higher. Building a new pipeline from the Permian to Mont Belvieu would cost $3-5 billion today, assuming you could get permits—which you probably couldn't. Environmental opposition has made new long-haul pipelines nearly impossible, transforming existing systems like Grand Prix into irreplaceable assets.

At Mont Belvieu, the competition is more direct but still limited. Enterprise, Targa, and a handful of others control the fractionation capacity. But even here, Targa's integration with Grand Prix creates advantages—guaranteed supply, optimized logistics, and the ability to capture value across the chain.

The ESG (Environmental, Social, Governance) pressures reshape competition in unexpected ways. While all midstream companies face scrutiny, those with newer, more efficient assets gain advantages. Targa's relatively modern processing plants emit fewer pollutants per unit processed than older facilities. Its focus on NGLs—which enable plastics and petrochemicals—positions it better than coal or heavy oil infrastructure.

International competition is minimal but growing. LPG exports to Asia and Latin America create new dynamics, where Targa competes not with domestic pipelines but with Middle Eastern and Australian suppliers. Here, the U.S. shale advantage—low-cost, abundant NGLs—combined with Targa's export infrastructure creates sustainable competitive advantages.

The consolidation wave continues. Smaller players lack the scale to compete for major projects. Environmental opposition makes greenfield development nearly impossible. The result: a slow-motion roll-up where the strong get stronger and the weak get acquired.

Technology matters less than you'd think. While competitors tout digital initiatives and AI optimization, the midstream business remains stubbornly physical. The company that owns the pipe in the ground, the plant in the field, and the dock at the port wins—regardless of their software stack.

Customer relationships create switching costs. When Exxon partners with Targa on the WestTX joint venture, it's not just about today's volumes—it's about decades of interdependence. These relationships, built over years of reliable service, become competitive moats that new entrants can't quickly replicate.

Regulatory capture—though nobody calls it that—advantages incumbents. The permits, easements, and approvals required for midstream infrastructure take years to obtain. Existing players know the process, have the relationships, and can navigate the bureaucracy. New entrants face a maze of federal, state, and local regulations that effectively protect incumbent positions.

The capital markets dimension adds another layer. Targa's S&P 500 inclusion, investment-grade rating, and simplified structure provide access to capital that smaller competitors can't match. In a capital-intensive industry, the cost of capital becomes a competitive weapon.

XI. Playbook: Lessons for Builders & Investors

The Targa story offers a masterclass in value creation through strategic positioning, patient capital deployment, and relentless execution. The lessons extend far beyond energy infrastructure to any capital-intensive industry where location, scale, and integration create competitive advantages.

Lesson 1: Timing Matters More Than Vision Warburg Pincus didn't predict the shale revolution when forming Targa in 2003. But they positioned for optionality—acquiring assets in multiple basins, building flexible infrastructure, maintaining financial capacity for growth. When the Permian exploded, Targa was ready. The lesson: position for multiple futures rather than betting on one.

Lesson 2: The Power of Strategic Incrementalism Targa didn't build Grand Prix on day one. They started with scattered gathering systems, added processing plants, expanded coverage, then connected everything with a mega-pipeline. Each step made sense standalone but created exponentially more value combined. Build in modules that work independently but shine together.

Lesson 3: Boring Businesses Can Generate Exciting Returns Pipeline tolls and fractionation fees won't make magazine covers. But Targa's 15-20% annual returns over two decades crushed most tech stocks. The lesson: sustainable competitive advantages in mundane industries often outperform disruption plays in sexy sectors.

Lesson 4: Vertical Integration in Commodity Industries When your product is undifferentiated (molecules are molecules), controlling the value chain matters. Targa's integration from wellhead to waterway captures margins that pure-play gatherers or processors leave on the table. Own the toll roads, not the trucks.

Lesson 5: Financial Engineering as Competitive Advantage The MLP-to-C-corp transition wasn't just financial reshuffling—it was strategic repositioning. By simplifying structure and broadening the investor base, Targa lowered its cost of capital and increased strategic flexibility. Sometimes the best investment is in your own capital structure.

Lesson 6: Managing Through Commodity Cycles Targa survived $26 oil in 2016 and $140 oil in 2008. The key: fee-based revenue with commodity optionality. When prices crash, fees provide stability. When prices soar, retained volumes generate windfalls. Structure for survival in the trough and participation in the peak.

Lesson 7: The Acquisition Integration Playbook Targa has completed dozens of acquisitions, from small bolt-ons to transformative deals like Atlas. The pattern: buy distressed or non-core assets, improve operations, expand capacity, integrate with existing systems. Value creation comes not from the purchase but from post-merger optimization.

Lesson 8: Building Uncopyable Assets Grand Prix can't be replicated—not because of technology or patents, but because of permits, rights-of-way, and environmental opposition. The best moats aren't built; they emerge from regulatory, environmental, and social constraints that protect incumbents.

Lesson 9: Customer Concentration as Strength Conventional wisdom warns against customer concentration. But when your customers are Exxon, Chevron, and ConocoPhillips, concentration creates stability. These investment-grade counterparties won't disappear overnight and value reliable infrastructure partners.

Lesson 10: The Power of Patient Capital Warburg Pincus held Targa for seven years, allowing management to build for the long term rather than optimize for quarterly earnings. Patient capital enables strategic investments that public market myopia would punish. Find investors who measure success in decades, not quarters.

Lesson 11: Location, Location, Location In midstream, geography is destiny. Targa's Permian focus wasn't luck—it was strategic concentration in America's lowest-cost, highest-growth basin. Better to dominate one great market than participate in many good ones.

Lesson 12: Operational Excellence as Differentiator In commodity industries where products are identical, execution separates winners from losers. Targa's 98%+ plant uptime, minimal safety incidents, and consistent project delivery create trust that translates into new business. Excellence in execution beats brilliance in strategy.

Lesson 13: The Platform Value Creation Model Private equity's platform playbook—buy a foundation asset, add bolt-ons, improve operations, exit at multiple expansion—works when executed properly. Targa shows how: start with quality assets, add strategic acquisitions, create synergies, and build something worth more than the sum of parts.

Lesson 14: Simplicity Scales As Targa grew, it simplified—from complex MLP structure to C-corp, from scattered assets to integrated systems, from commodity exposure to fee-based revenue. Complexity might generate short-term gains, but simplicity creates long-term value.

Lesson 15: The Exit is the Strategy Warburg Pincus's gradual exit—through IPO, secondary offerings, and market sales—maximized value while ensuring continuity. The best exits aren't events but processes that balance value realization with business stability.

For builders, the Targa playbook offers a template: identify a fragmented industry with stable cash flows, consolidate strategically, integrate operations, simplify structure, and create a platform that others can't replicate.

For investors, the lessons are equally clear: look for businesses with strategic assets, fee-based revenue, integration opportunities, and management teams that think in decades. Value emerges not from disruption but from patient construction of competitive advantages in essential industries.

The ultimate lesson might be the most counterintuitive: in an era obsessed with disruption, the biggest opportunities might lie in industries that can't be disrupted—where physical assets, regulatory barriers, and customer relationships create moats that software can't cross.

XII. Bear vs. Bull Case Analysis

Bull Case: The Infrastructure Aristocrat

The bullish thesis on Targa rests on irreplaceability. In a world where new pipeline construction faces insurmountable opposition, existing infrastructure becomes priceless. Targa owns the toll roads of American energy, and the tolls only go up.

Start with the Permian position. Despite talks of peak oil, the basin continues setting production records. Targa's infrastructure touches nearly every molecule produced, creating a natural monopoly in gathering and processing. Competitors would need to spend tens of billions and secure thousands of permits to replicate Targa's footprint—both impossible in today's environment.

Grand Prix represents the ultimate moat. Building a competing NGL pipeline from the Permian to Mont Belvieu would cost $5+ billion and take 5-7 years, assuming permits could be obtained—which they couldn't. Environmental groups have effectively closed the window on new long-haul pipelines. Targa owns one of the last pipes built before the door slammed shut.

NGL demand growth remains robust despite energy transition concerns. Petrochemicals drive modern life—from medical devices to electric vehicle components. Even aggressive renewable scenarios show NGL demand growing 2-3% annually through 2040. Asia's rising middle class demands plastics, fertilizers, and consumer goods—all NGL derivatives.

The free cash flow generation is undeniable. With major growth projects completing, capital expenditure drops from $3 billion to $1.5 billion annually while EBITDA approaches $5 billion. That's $2+ billion in annual free cash flow—enough to fund 5-10% dividend growth and substantial buybacks indefinitely.

Energy security has become paramount. The Ukraine conflict reminded the world that energy independence matters. U.S. NGL exports to Europe have surged as the continent weans itself off Russian supply. Targa's export infrastructure becomes strategically vital, potentially warranting government support if needed.

The inflation hedge is built-in. Most contracts include annual escalators tied to inflation indices. As replacement costs soar, existing infrastructure becomes more valuable. A pipeline that cost $1 billion to build might cost $3 billion to replace—but generates fees based on replacement value.

Management's track record speaks volumes. From the 2003 formation through today, they've delivered 15%+ annual returns through multiple cycles. They've proven ability to allocate capital, integrate acquisitions, and navigate commodity volatility.

The shareholder returns framework is clear: 35-50% of free cash flow to dividends, growing 5-10% annually; the remainder for opportunistic buybacks. At current valuations, buybacks are massively accretive. The company could retire 5% of shares annually while growing the dividend high-single digits.

Consolidation opportunities abound. Smaller operators struggle with environmental compliance costs and capital access. Targa can acquire assets at 6-8x EBITDA and integrate them into systems where they're worth 10-12x. It's multiple arbitrage with operational synergies.

The S&P 500 inclusion creates permanent buyers. Index funds must own Targa regardless of price. This technical support provides downside protection and multiple expansion over time.

Bear Case: Stranded in Transition

The bearish perspective sees Targa as a melting ice cube—profitable today but facing inexorable decline as the world transitions beyond hydrocarbons.

Peak oil demand isn't a theory—it's emerging reality. Electric vehicles are destroying gasoline demand. Renewable power is displacing natural gas. Even petrochemicals face pressure from recycling and bio-based alternatives. Targa's infrastructure could become stranded as demand evaporates.

Permian production must eventually plateau. No basin produces forever. The best acreage is drilled first. Decline rates accelerate. What happens to gathering systems when there's nothing left to gather? History is littered with abandoned energy infrastructure.

Capital intensity remains problematic. Even in "maintenance mode," Targa spends $500+ million annually just to maintain existing capacity. Growth requires billions more. This isn't a capital-light compounder—it's a capital-eating industrial complex.

ESG pressures intensify regardless of returns. European investors divest from fossil fuels. American institutions face pressure from stakeholders. Banks restrict lending to hydrocarbon infrastructure. The cost of capital rises even as cash flows remain strong.

Commodity exposure, while reduced, still exists. A sustained collapse in NGL prices—from recession, demand destruction, or alternatives—would impact margins. Fee-based doesn't mean risk-free when your customers are commodity producers.

Stranded asset risk is real and growing. California bans gas stoves. Europe phases out petrochemicals. What's a fractionation tower worth when nobody wants the fractions? Infrastructure built for 30-year lives might be obsolete in 15.

Regulatory risks multiply. Pipeline safety regulations tighten. Environmental standards escalate. Carbon taxes loom. Each new rule increases costs and reduces returns. The regulatory ratchet only turns one direction: tighter.

Customer concentration creates vulnerability. If Exxon or Chevron divests Permian assets to focus on lower-carbon investments, Targa loses anchor volumes. The investment-grade counterparties that provide stability could become the source of disruption.

Technology disruption, while slow, is coming. Direct air capture of CO2, hydrogen production, synthetic fuels—all threaten traditional hydrocarbon infrastructure. Targa's pipes might be worthless when molecules can be manufactured anywhere.

Debt levels, while manageable, limit flexibility. With $15+ billion in debt, Targa can't pivot quickly. Rising rates increase interest expense. Refinancing risk grows if capital markets lose faith in fossil fuel infrastructure.

The Mexico risk deserves consideration. Mexican energy policy remains volatile. Export infrastructure depends on stable cross-border relations. A populist turn could strand Gulf Coast assets.

Competition from renewable alternatives accelerates. Green hydrogen, renewable diesel, sustainable aviation fuel—all compete with NGL-derived products. As costs decline and mandates expand, traditional products lose market share.

The Verdict

Both cases have merit, but the timeline matters most. The bull case dominates the next 5-10 years—cash flows will grow, dividends will increase, and buybacks will enhance returns. The bear case might dominate beyond 2035, but that's too distant for accurate prediction.

The key question: Will Targa generate enough cash in its remaining prime years to justify today's valuation? With $2+ billion in annual free cash flow against a $40 billion enterprise value, the math suggests yes.

XIII. Recent News

The latest developments paint a picture of a company firing on all cylinders while positioning for continued growth through the decade.

Financial Performance Momentum The Company reported adjusted earnings before interest, income taxes, depreciation and amortization, and other non-cash items ("adjusted EBITDA") of $1,178.5 million for the first quarter of 2025, representing continued sequential growth. For the full year 2024, the Company reported adjusted EBITDA exceeding $4 billion, validating management's aggressive targets.

Dividend Growth Acceleration Targa's board of directors has declared an increase to its quarterly cash dividend to $4.00 per common share on an annualized basis, for the first quarter of 2025. This dividend represents a 33 percent increase over the common dividend declared with respect to the first quarter of 2024. This aggressive dividend growth reflects management's confidence in sustainable cash flow generation.

Capital Structure Optimization Targa announced today a definitive agreement to repurchase all of the outstanding preferred equity in Targa Badlands LLC from funds managed for $1.8 billion in cash. The Repurchase represents a refinancing of higher cost preferred equity with Targa's lower cost of debt capital, resulting in meaningful cash savings. This transaction eliminates dilutive preferred equity while reducing the overall cost of capital.

Infrastructure Expansion Continues Targa announced: Delaware Express, a 100-mile, 30-inch diameter pipeline expansion of its Grand Prix NGL Pipeline in the Permian Delaware. Delaware Express is expected to commence operations in the third quarter of 2026, Train 12 is expected to commence operations in the first quarter of 2027, and Targa's GPMT LPG Export Expansion is expected to commence operations in the third quarter of 2027.

Operational Excellence Completed its new 275 million cubic feet per day ("MMcf/d") Greenwood II plant in Permian Midland and its new 120 thousand barrels per day ("MBbl/d") Train 10 fractionator, demonstrating continued execution of growth projects on time and on budget.

Share Buyback Activity During the second quarter of 2025, Targa repurchased 1.96 million shares of its common stock. In August 2025, the Company's Board of Directors approved a new share repurchase program for the repurchase of up to $1.0 billion of the Company's outstanding common stock. The amount authorized under the new share repurchase program is in addition to the amount remaining under the existing share repurchase program.

Credit Facility Enhancement In February 2025, Targa entered into a new five-year revolving facility with aggregate capacity of $3.5 billion. The New TRGP Revolver replaces Targa's $2.75 billion credit facility, scheduled to mature in February 2027. The additional capacity aligns with the Company's increased scale and continued growth opportunities.

Robust Growth Outlook $4.85 billion supported by forecasted growth across its Permian G&P footprint, which is expected to drive record Permian, NGL pipeline transportation, fractionation, and LPG export volumes in 2025 relative to records set in 2024. While the growth is weighted to the second half of 2025, current and expected producer activity levels continue to support an outlook of meaningfully increasing volumes across the rest of 2025 and 2026.

These developments confirm Targa's position as a best-in-class midstream operator executing a clear strategy: expand infrastructure in core positions, optimize capital structure, and return increasing capital to shareholders. The company continues to benefit from its strategic positioning in the Permian Basin and integrated value chain from wellhead to water.

XIV. Links & Resources

Company Resources - Targa Resources Investor Relations: https://www.targaresources.com/investors - SEC Filings: https://www.sec.gov/edgar/browse/?CIK=1389170 - Quarterly Earnings Presentations: https://www.targaresources.com/investors/financial-information/quarterly-earnings - Annual Reports: https://www.targaresources.com/investors/financial-information/annual-reports

Industry Analysis & Reports - Energy Information Administration - Natural Gas Liquids: https://www.eia.gov/naturalgas/ - Permian Basin Production Statistics: https://www.eia.gov/petroleum/drilling/ - Mont Belvieu NGL Pricing: https://www.opis.com/price/natural-gas-liquids - Pipeline & Gas Journal: https://www.pgjonline.com/

Historical Context & Private Equity - Warburg Pincus Portfolio: https://www.warburgpincus.com/portfolio/ - Master Limited Partnership Association: https://www.mlpassociation.org/ - Private Equity in Energy Infrastructure Studies: Various academic journals

Regulatory & Environmental - Pipeline and Hazardous Materials Safety Administration: https://www.phmsa.dot.gov/ - Texas Railroad Commission: https://www.rrc.texas.gov/ - Federal Energy Regulatory Commission: https://www.ferc.gov/ - Environmental Impact Assessments: Available through FERC dockets

Market Analysis - Alerian MLP Index: https://www.alerian.com/ - S&P Energy Select Sector Index: https://www.spglobal.com/spdji/ - Natural Gas Intelligence: https://www.naturalgasintel.com/ - Oil & Gas Journal: https://www.ogj.com/

Conference Presentations & Management Interviews - J.P. Morgan Energy Conference Archives - Goldman Sachs Energy Conference Presentations - Barclays CEO Energy Conference Materials - Wells Fargo Midstream Symposium Presentations

Competitor Analysis - Enterprise Products Partners: https://www.enterpriseproducts.com/ - ONEOK Inc.: https://www.oneok.com/ - Williams Companies: https://www.williams.com/ - Kinder Morgan: https://www.kindermorgan.com/

Technical Resources - Natural Gas Processing Principles: Society of Petroleum Engineers - Pipeline Construction & Engineering: American Society of Civil Engineers - Fractionation Technology Overview: American Institute of Chemical Engineers - NGL Market Fundamentals: Various industry white papers

Energy Transition & Future Outlook - International Energy Agency Reports: https://www.iea.org/ - Wood Mackenzie Energy Transition Studies - BloombergNEF Energy Outlook - McKinsey Energy Insights

Financial Analysis Tools - TIKR Terminal for historical financials - CapitalIQ for detailed segment analysis - FactSet for consensus estimates - Bloomberg Terminal for real-time pricing

Note: This analysis represents an independent assessment based on publicly available information. It does not constitute investment advice. Prospective investors should conduct their own due diligence and consult with qualified financial advisors before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube